Everest Group PEAK MatrixTM for Life and Pensions ... Assessment for Accenture, Capita, CSC, and...

15

Everest Group PEAK Matrix TM for Life and Pensions Insurance BPO Service Providers Focus on TCS November 2015 Copyright © 2015 Everest Global, Inc. This document has been licensed for exclusive use and distribution by TCS EGR-2015-11-E-1602

Transcript of Everest Group PEAK MatrixTM for Life and Pensions ... Assessment for Accenture, Capita, CSC, and...

Everest Group PEAK MatrixTM for Life and Pensions

Insurance BPO Service Providers

Focus on TCS

November 2015

Copyright © 2015 Everest Global, Inc.

This document has been licensed for exclusive use and distribution by TCS

EGR-2015-11-E-1602

2Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

Everest Group recently released its report titled “Life and Pensions Insurance BPO – Service Provider

Landscape with PEAK MatrixTM Assessment 2015”. This report analyzes the changing dynamics of the Life

and Pensions (L&P) insurance BPO landscape and assesses service providers across several key

dimensions.

As a part of this report, Everest Group updated its classification of 19 service providers on the Everest Group

Performance | Experience | Ability | Knowledge (PEAK) Matrix for L&P insurance BPO into Leaders, Major

Contenders, and Aspirants. The PEAK Matrix is a framework that provides an objective, data-driven, and

comparative assessment of L&P insurance BPO service providers based on their absolute market success

and delivery capability.

Based on the analysis, TCS emerged as a Leader. This document focuses on L&P insurance BPO

experience and capabilities of TCS. It includes:

Position of TCS on the Everest Group L&P insurance BPO PEAK Matrix

Detailed L&P insurance BPO profile of TCS

Buyers can use the PEAK Matrix to identify and evaluate different service providers. It helps them understand

the service providers’ relative strengths and gaps. However, it is also important to note that while the PEAK

Matrix is a useful starting point, the results from the assessment may not be directly prescriptive for each

buyer. Buyers will have to consider their unique situation and requirements, and match them against service

provider capability for an ideal fit.

Introduction and scope

3Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

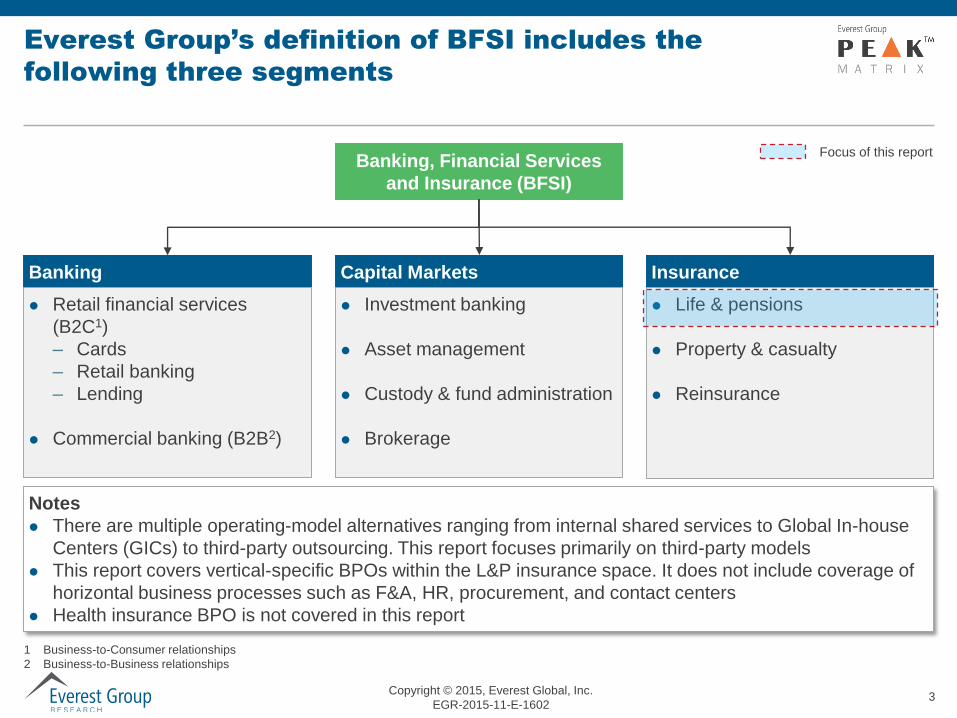

Banking, Financial Services

and Insurance (BFSI)

Everest Group’s definition of BFSI includes the

following three segments

1 Business-to-Consumer relationships

2 Business-to-Business relationships

Focus of this report

Banking

Retail financial services

(B2C1)

– Cards

– Retail banking

– Lending

Commercial banking (B2B2)

Capital Markets

Investment banking

Asset management

Custody & fund administration

Brokerage

Notes

There are multiple operating-model alternatives ranging from internal shared services to Global In-house

Centers (GICs) to third-party outsourcing. This report focuses primarily on third-party models

This report covers vertical-specific BPOs within the L&P insurance space. It does not include coverage of

horizontal business processes such as F&A, HR, procurement, and contact centers

Health insurance BPO is not covered in this report

Insurance

Life & pensions

Property & casualty

Reinsurance

4Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

Everest Group PEAK Matrix – 2015 L&P insurance

BPO market positions

Performance | Experience | Ability | Knowledge

Everest Group Performance | Experience | Ability | Knowledge (PEAK) Matrix for L&P insurance BPO1 Leaders

Major Contenders

Aspirants

1 Service providers scored using Everest Group’s proprietary scoring methodology

Notes: Assessment for Accenture, Capita, CSC, and Tech Mahindra excludes service provider inputs on this particular study and is based on Everest Group’s

estimates that leverage its proprietary Transaction Intelligence (TI) database, ongoing coverage of these service providers, their public disclosures, and

interaction with buyers.

Since L&P insurance BPO PEAK Matrix assessment has been done for the first time in 2015, Star Performer assessment will be done from 2016 onwards

Source: Everest Group (2015)

25

thp

erc

en

tile

High

Low

25th percentile

75th percentile

Low High

75

thp

erc

en

tile

Mark

et

su

ccess

(Revenue, num

ber

of clie

nts

, and

revenue g

row

th)

L&P insurance BPO delivery capability

(Scale, scope, technology solutions & innovation, delivery footprint, and buyer satisfaction)

Major Contenders

Leaders

Aspirants

TCSCapita

CSCEXL

Cognizant

Accenture

Sutherland Global Services

Dell

Infosys

WNS

GenpactHCL

IGATE

Xerox

Serco

SyntelNIIT Technologies

Tech Mahindra

MphasiS

5Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

12%

28%

41

330

TCS (page 1 of 5)

Everest Group assessment

Delivery capability assessment

Dimension Rating Remarks

Scale Best-in-class scale and stability, owing to high overall

company revenue and greater contribution of L&P

insurance BPO than industry benchmarks

Scope An exhaustive coverage of buyer segments and processes

within L&P insurance BPO; significant capabilities in

judgment-intensive processes

Technology

solutions &

innovation

Best-in-class capabilities powered by strong technology-led

offerings in core BPO processes and value-added services

such as automation, analytics, and risk management

Delivery

footprint

Good delivery mix in terms of FTEs at onshore and offshore

locations; high number of centers

Buyer

satisfaction

Best-in-class overall score, with key strengths being domain

expertise and relationship management

Market success assessment

Best-in-class Very high High Medium high Medium Medium low Low Not mature

TCS

Peer set median1

TCS

Peer set median

With the second largest market share by revenue and a large client base, TCS has achieved very

high market success. This, in conjunction with best-in-class BPO delivery capabilities, has

ensured an uncontested position among Leaders for it on the L&P insurance BPO PEAK Matrix

It has best-in-class revenue-spread across buyer segments and processes within L&P insurance

BPO, reflecting its low exposure to market risk and capability to serve diverse demands

It is strong on technology and is capable of delivering holistic suites, end-to-end platforms, and

augmentation solutions

It has developed very good BPSDA capabilities, primarily because of focused efforts in building

in-house RPA solutions

It enjoys best-in-class buyer satisfaction ratings

Key strengths

Revenue distribution for TCS is very much concentrated, with

United Kingdom accounting for almost all of its revenue in L&P

insurance BPO which raises market risk. It needs to cover other

geographies in terms of revenue share

It needs to strengthen its offerings around analytics and

regulatory reporting, along with increasing deployment rate of

RPA solutions

Its delivery footprint is limited to India and United Kingdom.

Further, there is relatively higher onshore component. It needs

to explore nearshore locations to enhance cost effectiveness

Areas of improvement

YOY Growth

% revenue

YOY Growth

% clients

7

22

~3x

6%

38%

~8x

L&P insurance BPO revenue

US$ million

L&P insurance BPO clients

Number of clients

1 Median based on 15 L&P insurance BPO service providers who participated in this particular research

Source: Everest Group (2015)

6Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

TCS (page 2 of 5)

L&P insurance BPO – overview

Recent acquisitions and partnerships

2014: Partnered with CII, to drive completion of UK

Insurance certifications

2012: Formed a joint venture with Mitsubishi to establish an

IT, BPO, and infrastructure services delivery center in Japan

2012: TCS BaNCS signed an agreement with Savvis, a

Century Link company in cloud infrastructure, to offer

services on a cloud-enabled hosted environment

Recent developments

2014: Developed customer life time value and built churn

models, cross sell / up-sell, win-back, and market basket

analysis

2012: Invested in developing platform model for L&A closed

books for North America

2012: Invested in enhancing its existing competencies in

actuarial and business process management (BPM) services

2012: FORETM provides customers with operational agility

and regulatory compliance

2012: Signed a 15-year contract with Friends Life UK for

US$2.2 billion

Suite of services

New business and underwriting support

Policy servicing and claims transformation

Insurance CRM solutions – customer interaction management

Robotic Process Automation

Analytics and insights

Actuarial services

Company overview

Tata Consultancy Services (TCS) is an IT services, consulting, and

business process services organization. TCS’ extensive experience with

diverse insurance organizations has helped it develop in-depth domain

expertise. Within insurance, TCS deploys its BaNCS platform, analytics

and automation to deliver on value based business outcomes for its

customers and provides an enhanced customer experience to enable

increased competitiveness and retention. Deploying its Robotic Process

Automation (RPA) solution with its modular approach, TCS can address

any business scenario of insurers.

Key leaders

Dinanath Kholkar, Vice President and Global Head, Business Process

Services (BPS)

Arun Batra, Global Head, BFSI, BPS

VR Krishnan, Head, Insurance BPO Services

Headquarters: Mumbai, India

Website: www.tcs.com

2012 2013 2014

Revenue (US$ million) 400* 375* 330

Number of FTEs 5,100* 5,150* 5,100

Number of clients 14 16 22

1 Includes horizontal services such as F&A, SCM, and HR

Source: Everest Group (2015)

7Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

TCS (page 3 of 5)

L&P insurance BPO – key delivery locations

Kolkata

BangaloreMumbai

Peterborough

Pune

Liverpool

GurgaonCincinnati

Nagpur

Bristol

Source: Everest Group (2015)

8Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

TCS (page 4 of 5)

L&P insurance BPO – capabilities and key clients

L&P insurance BPO FTE mix by

processes covered

FTEs in numbers

Insurance BPO revenue mix by

geography

Revenue in US$ million

Split of FTEs by location

FTEs in numbers

Insurance BPO number of

contracts by buyer size

Number of active contracts

100% = 5,100

48%

32%

12%

7%

New

business

management

Policy

servicing

and

reporting

100% = 330

90%

7%3%

Europe

North

America

100% = 5,100

47%53%

Onshore

APAC

Offshore

100% = 22

61%

38%

1%

Large

Small

Medium

Key L&P insurance BPO engagements

Client name Region Client since year

Top five superannuation player in Australia APAC 2013

Friends Life Europe 2012

NEST Europe 2010

Fortune 100 annuity and retirals provider US 2010

Fortune 500 financial services and annuity provider US 2008

Phoenix Group Europe 2006

India operations of a US top five life insurer APAC 2008

Claims

processing

Others

1 Buyer size is defined as large (>US$10 billion in revenue), medium (US$5-10 billion in revenue), and small (<US$5 billion in revenue)

Notes: Based on contractual and operational information as on December 2014

Source: Everest Group (2015)

9Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

Tools RPA

TCS Digital Insurance

Agent Solution TRAPEZE

TCS BaNCS – insurance

platform (BPaaS)

Solution

description

TCS’ Robotic Process

Automation (RPA) helps to

enhance process efficiencies,

with greater business agility. It

requires no change in underlying

systems and processes.

Repetitive processes are

executed by features such as

optical character recognition &

intelligent character recognition,

document & image parsers,

macros & scripts, and record.

A tablet-based

application that

operationalizes all the

day-to-day activities of

insurance agents on a

mobile tablet.

TCS delivery

ecosystem

consists of

governance,

reporting,

workflow,

document

management,

and process

management

applications,

along with

domain-specific

accelerators.

TCS offers the best-in-class

web-based insurance product

suite. It ensures efficient

service delivery across all lines

of business (property &

casualty, individual & group life,

and reinsurance).

Year launched 2014 2012 2011 2009

Number of

clients

4 5 9 8

TCS (page 5 of 5)

L&P insurance BPO – technology solutions

10Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

Appendix

11Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

Everest Group classifies the L&P insurance BPO

service provider landscape into Leaders, Major

Contenders, and Aspirants on the Everest Group PEAK Matrix

Everest Group Performance | Experience | Ability | Knowledge (PEAK) Matrix1 for L&P insurance BPO

Top Quartile performance

across market success and

delivery capability2nd or 3rd quartile performance

across market success and

delivery capability

4th quartile performance

across market success and

delivery capability

High

Low

25

thp

erc

en

tile

75

thp

erc

en

tile

75th percentile

Aspirants

Leaders

Major Contenders

Low High25th percentile

L&P insurance BPO delivery capability

(Scale, scope, technology solutions & innovation, delivery footprint, and buyer satisfaction)

Ma

rke

t s

uc

ce

ss

(Re

ve

nu

e, n

um

ber

of clie

nts

, a

nd

reve

nu

e g

row

th)

1 Service providers scored using Everest Group’s proprietary scoring methodology on page 12

Source: Everest Group (2015)

12Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

Service providers are positioned on PEAK Matrix

based on evaluation across two key dimensions

Measures success achieved in

the market. Captured through

L&P insurance BPO revenue,

number of clients, and y-o-y

revenue growth

Ma

rke

t s

uc

ce

ss

Measures the scope of

services provided

across processes,

geographies, and buyer

size

Measures the capability

and investment in

technology solutions

and ability to deliver

value-added services

(innovation) with high

technology leverage

Measures the delivery

footprint across regions

and the global sourcing

mix

Measures ability to deliver services successfully

Captured through five subdimensions

Measures the scale of

operations (overall

company revenue and

relative focus on the

vertical)

Scale ScopeTechnology solutions

and innovationDelivery footprint

Delivery capability

Measures the

satisfaction levels1 of

buyers across:

Business driver

Implementation

Process expertise

Relationship

management

Buyer satisfaction

Aspirants

Leaders

Major Contenders

1 Measured through responses from referenced buyers for each service provider

Source: Everest Group (2015)

13Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

Does the PEAK Matrix assessment incorporate any subjective criteria?

The Everest Group’s PEAK Matrix assessment adopts an objective and fact-based approach (leveraging service

provider RFIs and the Everest Group’s proprietary databases containing providers’ deals and operational capability

information). In addition, these results are validated / fine-tuned based on our market experience, buyer interaction,

and provider briefings

Is being a “Major Contender” or “Aspirant” on the PEAK Matrix an unfavorable outcome?

No. PEAK Matrix highlights and positions only the best-in-class service providers in a particular functional/vertical.

There are a number of providers from the broader universe that are assessed and do not make it to the PEAK

Matrix at all. Therefore, being represented on the PEAK Matrix is in itself a favorable recognition

What other aspects of the PEAK Matrix assessment are relevant to buyers and providers besides the “PEAK

Matrix position”?

The PEAK Matrix position is only one aspect of the Everest Group’s overall assessment. In addition to assigning a

“Leader”, “Major Contender” or “Aspirant” title, Everest Group highlights the distinctive capabilities and unique

attributes of all the PEAK Matrix providers assessed in its report. The detailed metric level assessment and

associated commentary is helpful to the buyers in selecting particular providers for their specific requirements. It

also helps providers showcase their strengths in specific areas

What are the incentives for buyers and providers to participate / provide input to the PEAK Matrix research?

Participation incentives for buyers include a summary of key findings from the PEAK Matrix assessment

Participation incentives for providers include adequate representation and recognition of their capabilities/success in

the market place, and a copy of their own “profile” that is published by Everest Group as part of the “compendium of

PEAK Matrix providers” profiles

FAQs (page 1 of 2)

14Copyright © 2015, Everest Global, Inc.

EGR-2015-11-E-1602

What is the process for a service provider to leverage their PEAK Matrix positioning status ?

Providers can use their PEAK Matrix positioning in multiple ways including:

– Issue a press release declaring their positioning/rating

– Customized PEAK Matrix profile for circulation (with clients, prospects, etc.)

– Quotes from the Everest Group’s analysts could be disseminated to the media

– Leverage the PEAK Matrix branding across communications (e-mail signatures, marketing brochures, credential

packs, client presentations, etc.)

The provider must obtain the requisite licensing and distribution rights for the above activities through an

agreement with the designated PoC at Everest Group

FAQs (page 2 of 2)

Blog

www.sherpasinblueshirts.com

@EverestGroup

Stay connected

Websites

www.everestgrp.com

research.everestgrp.com

Dallas (Headquarters)

+1-214-451-3000

New York

+1-646-805-4000

Toronto

+1-647-557-3475

London

+44-207-129-1318

Delhi

+91-124-284-1000

About Everest Group

Everest Group is a consulting and research firm focused on strategic IT, business

services, and sourcing. We are trusted advisors to senior executives of leading

enterprises, providers, and investors. Our firm helps clients improve operational

and financial performance through a hands-on process that supports them in

making well-informed decisions that deliver high-impact results and achieve

sustained value. Our insight and guidance empowers clients to improve

organizational efficiency, effectiveness, agility, and responsiveness. What sets

Everest Group apart is the integration of deep sourcing knowledge, problem-

solving skills and original research. Details and in-depth content are available at

www.everestgrp.com and research.everestgrp.com.

![EVEREST Ultimate Edition ]------------------------------------------------------------------------------------ Version EVEREST v5.50.2100/fr Module de ...](https://static.fdocuments.in/doc/165x107/5aa972ce7f8b9a90188cd90e/everest-ultimate-edition-.jpg)