Essentials of Fund 73 WASBO Accounting Seminar March, 2009 Presented by: Kathy Guralski, School...

35

Essentials of Fund 73 WASBO Accounting Seminar March, 2009 Presented by: Kathy Guralski, School Finance Auditor Wisconsin Department of Public Instruction

-

Upload

jaylyn-chatt -

Category

Documents

-

view

214 -

download

0

Transcript of Essentials of Fund 73 WASBO Accounting Seminar March, 2009 Presented by: Kathy Guralski, School...

Essentials of Fund 73WASBO Accounting Seminar

March, 2009

Presented by:

Kathy Guralski, School Finance AuditorWisconsin Department of Public Instruction

How does establishing aFund 73 affect State Aid?

Equalization aid Pay as you go

Retiree payments are an expenditure for shared cost

TrustShared cost does not include the retiree payments RATHER

Shared cost includes the total amount of the contribution to the trust less the implicit rate subsidy on current benefits paid retirees

How does establishing aFund 73 affect State Aid?

Equalization aid (cont.) Trust Example:

Contribution of $500,000 Expenditure for shared cost

Retiree benefits of $300,000 No impact on shared cost – paid from trust

Implicit rate subsidy of $100,000 Paid from trust to District because it has already

been funded by the active employees Reduces expenditure for shared cost

Amount that impacts shared cost is $400,000

How does establishing aFund 73 affect State Aid?

State Categorical Aid Pay as you go

No impact Trust

Contribution amount less implicit rate subsidy may be allocated to individual functions as a fringe benefit IF:

Intent to fund the trust is shown DPI measures that intent with 3 criteria

State categorical aid eligibility requirements

One of three criteria must be metContribution must equal ARC amount

Contribution in current year must be 105% of the expenditures paid from the trust in the current year

Combined contributions for the current year plus the previous 2 years must equal 115% of the combined expenditures paid from the trust in the current year plus the previous 2 years.

State categorical aid eligibility requirements

Example: Current year contribution $500,000 ARC $600,000 Does not meet the 1st criteria

State categorical aid eligibility requirements

Example: Current year contribution $500,000 Retiree benefits including implicit rate

subsidy $300,000 $300,000 X 105% = $315000 Contribution does meet the 2nd criteria

State categorical aid eligibility requirements

Example: Current year contribution $500,000 Previous two year contributions $300,000 total Current year retiree benefits including implicit rate

subsidy $300,000 Previous two year retiree benefits including

implicit rate subsidy $590,000 total$300,000 X 105% = $315,000

$290,000 X 105% = $304,500

$300,000 X 105% = $315,000

Total = $934,500

Total Contributions = $800,000 Contribution does not meet the 3rd criteria

State categorical aid eligibility requirements

If none of the three are met, no allocation of the contribution is made and there is no impact on state categorical aid

In this example, criteria 2 has been met so the entire $500,000 of contribution is allocated (object 218) and reduced by the implicit rate subsidy of $100,000 (object 240)

State categorical aid eligibility requirements

CONTRIBUTION IN EXCESS OF ARC

How should a contribution that exceeds the ARC be accounted for? Treat the amount up to the ARC the same

as meeting the ARC Excess must be accounted for as function

290000, object 218

CONTRIBUTION IN EXCESS OF ARC

How should the implicit rate subsidy when the contribution exceeds the ARC be accounted for? Example:

ARC - $500,000

Contribution $600,000

Implicit Rate Subsidy - $200,000. 100% of implicit rate subsidy is allocated to

individuals Implicit rate subsidy has no connection to the

amount of the contribution

Should our District establish a FUND 73 Trust?

Can our District afford the minimum 5% required each year to receive additional categorical aid?

How is our district aided for general aid? Negative territiary? Run the numbers

How much categorical aid will I received? Example: Contribution is $200,000 of which

15% is special education salaries and benefits If this is aided at 28.5% Additional categorical aid of approximately

$8,550

Should our District establish a FUND 73 Trust?

How will the District pay for these benefits in the future?

How will not funding impact bond rating?

What is the legal cost of establishing a trust?

What are the yearly administrative costs associated with a trust?

If you do not plan to fund the trust with more than the current year pay as you go, these are additional cost with possibly little to no benefit

SEGREGATED FUNDS

Physical segregation of trust assets must be made. Assets are titled in the trust name

Never pooled cash

Never part of investment pool in districts name

Must be available to pay benefits Contributions are physical movement of funds

from the District assets to the trust assets Payments of benefits are physical payment

from the trust assets

ACCOUNTING FOR FUND 73 ACTIVITY

What do you need to have in front of you to properly account for district contribution and the trust activity? Actuary study Total insurance cost of current year retirees Portion of insurance cost paid by retirees

versus district Group of employees to which benefit is offered FTE or salaries by individual for the group of

employees

Determining how to Account for fund 73 activity

Follow the steps! Collect general information

Exhibit A Calculate implicit rate subsidy on retirees

Exhibit B Determine whether the contribution is eligible

for state categorical aidExhibit C

Allocation of contributionExhibit D

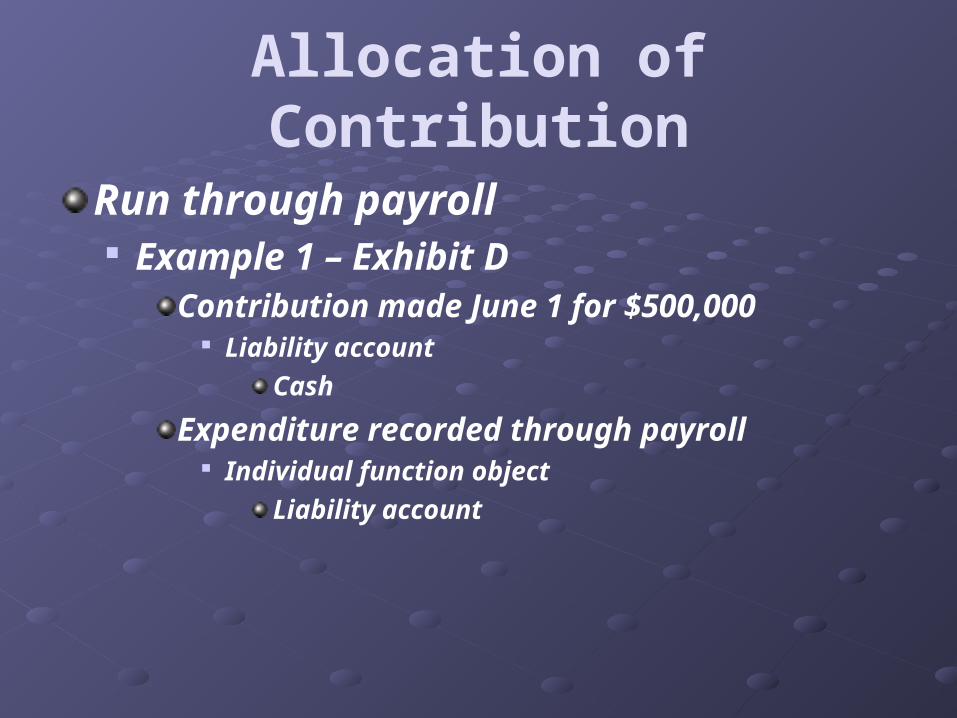

Allocation of Contribution

Run through payroll Example 1 – Exhibit D

The budgeted amount of $5724.12 would be divided by number of pay periods

Included as a fringe benefit

Credited to a liability account until time contribution is made to trust

Credited to a prepaid account if contribution made prior to the payroll

Allocation of Contribution

Run through payroll Example 1 – Exhibit D

Contribution made July 1 for $500,000 Prepaid Expense

Cash

Expenditure recorded through payroll Individual function object

Prepaid Expense

Allocation of Contribution

Run through payroll Example 1 – Exhibit D

Contribution made June 1 for $500,000 Liability account

Cash

Expenditure recorded through payroll Individual function object

Liability account

Allocation of ContributionRun through payroll Year end should reflect actual

contribution. If the contribution is different at year end than budgeted, a year end adjustment needs to be made. That can be done either with the last payroll or as a year end journal entry.

Journal entry Can do the allocation as a journal entry

versus run through the payroll

Accounting for fund 73Follow the steps! Account for contribution to trust

Exhibit E Account for retiree contribution towards

insuranceExhibit F

Retiree benefits paid from trustExhibit G

Summary of transactions per accountExhibit H

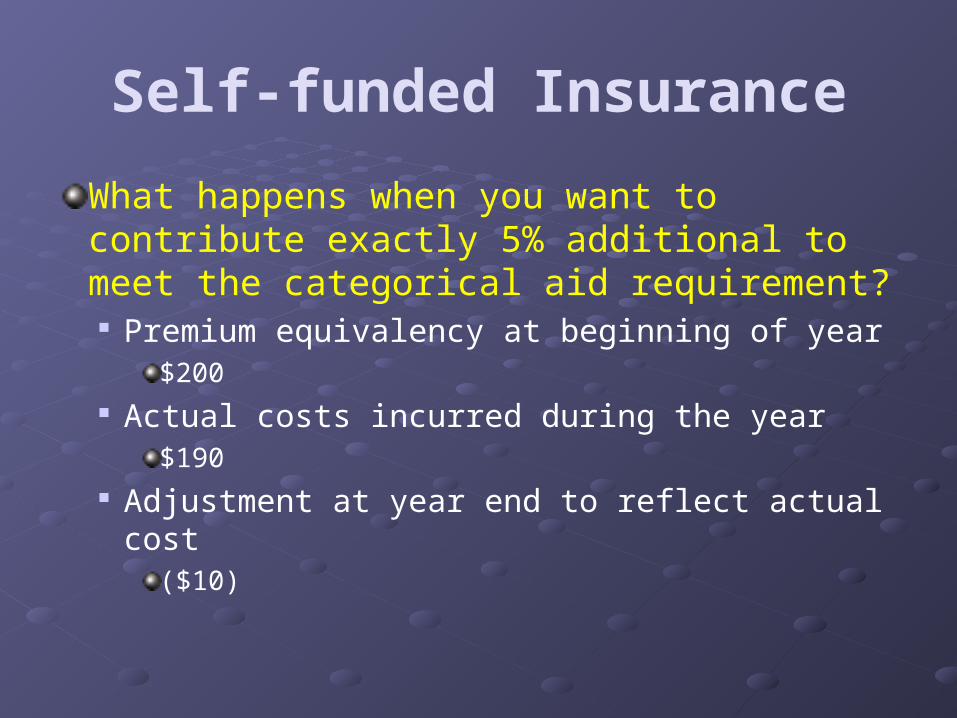

Self-funded Insurance

Contribution Based on premium equivalency plus implicit

rate subsidy

Retiree Benefits Generally the actual costs are paid from the

trust (no need to account for implicit rate subsidy because the actual costs are being paid)

Self-funded Insurance

What happens when you want to contribute exactly 5% additional to meet the categorical aid requirement? Premium equivalency at beginning of year

$200 Actual costs incurred during the year

$190 Adjustment at year end to reflect actual cost

($10)

Self-funded Insurance

What happens when you want to contribute exactly 5% additional to meet the categorical aid requirement?

It may be hard to determine the actual costs by June 30th

Contribution to the trust is due June 30th

The 5% is a minimum requirement to show intent

What happens when you want to contribute exactly 5% additional to meet the

categorical aid requirement?

Example:

Year 1: Premium equivalency - $500, Actual cost - $490

Year 2: Premium equivalency - $500, Actual cost - $550

Year 3: Premium equivalency - $550, Actual cost – $525

What happens when you want to contribute exactly 5% additional to meet the

categorical aid requirement?

Example:

Year 1 ARC $800,000 Contribution $525,000 ($500,000 x 105%) Actual retiree payments $490,000 Meets the 2nd criteria of additional 5%

What happens when you want to contribute exactly 5% additional to meet the

categorical aid requirement? Example:

Year 2 ARC $800,000 Contribution $525,000 ($500,000 x 105%) Actual retiree payments $550,000 Does not meet any of the 3 criteria

What happens when you want to contribute exactly 5% additional to meet the

categorical aid requirement?

Example:

Year 3 ARC $800,000 Contribution $577,500 ($550,000 x 105%) Actual retiree payments $525,000 Meets the 2nd criteria of 5% Premium was increased

??

Could you increase the contribution every 3 years to have a cushion? Example:

Year 1: Premium equivalency - $500, Actual cost - $490

Year 2: Premium equivalency - $500, Actual cost - $550

Year 3: Premium equivalency - $550, Actual cost – $525

Could you increase the contribution every 3 years to have a cushion?

Example:

Year 1 ARC $800,000 Contribution $595,000 ($500,000 x 105%

plus a cushion of $70,000) Actual retiree payments $490,000 @105% = $514,500 Now it’s 21% additional but still below

ARC Meets the 2nd criteria of additional 5%

Could you increase the contribution every 3 years to have a cushion?

Example:

Year 2 ARC $800,000 Contribution $595,000 ($500,000 x 105%) Since there is not 3 years yet, will add

another $70,000 cushion Actual retiree payments $550,000 @ 105% = 577,500 Now it’s 8% additional but still below ARC Meets the 2nd criteria of additional 5%

Could you increase the contribution every 3 years to have a cushion?

Example:

Year 3 ARC $800,000 Contribution $577,500 ($550,000 x 105%) Now there is 3 years and there is $98,000

cushion from the 2 prior years Actual retiree payments $525,000 Three year contributions $1,767,500 Three year retiree payments @ 105%

$1,617,000 Now meets the 2nd and 3rd criteria

Criteria does not change for self-funded it just becomes harder to determine

CONTRIBUTION MUST BE MADE BY JUNE 30TH TO BE AN ELIGIBLE COST