ESG’s Distribution Strategy for Managed ETF Solutions

14

Distribution Strategy for Managed ETF Solutions A Guide to Developing Effective Growth Strategies in a Competitive Market Randy Bullard CEO ETF Strategy Group www.ETFStrategyGroup.com October 2012 www.RandyBullard.com

-

Upload

randy-bullard -

Category

Documents

-

view

219 -

download

1

description

This guide was developed as a resource to help ETF Strategist investment managers better understand the distribution landscape, aid them in making product development decisions necessary to support broad market distribution, and provide guidance about how to organize and implement a productive distribution strategy.

Transcript of ESG’s Distribution Strategy for Managed ETF Solutions

Distribution Strategy for Managed ETF Solutions

A Guide to Developing Effective Growth Strategies in a Competitive Market

Randy Bullard

CEO

ETF Strategy Group

www.ETFStrategyGroup.com

October 2012

www.RandyBullard.com

Page | 2

The Managed ETF Solutions industry has experienced significant growth over the last several years. According to

Morningstar’s ETF Managed Portfolios Landscape Report, the entire industry is growing at approximately 50%

annualized as of September 2012. With this growth has also come a proliferation of new products, as well as a

growing number of maturing products with competitive 3+ year track records. Recent conferences hosted by the

major ETF issuers for ETF Strategist asset management firms have highlighted the increasingly competitive

nature of the industry.

Morningstar currently reports on almost $50 billion in AUM/AUA from 130 ETF Strategist firms. But only a dozen

of those firms are managing or administering over $1 billion in AUM, and only one (Windhaven) is over $10

billion in AUM/AUA. Relative to the broader asset management industry, even the larger ETF Strategists are very

small firms, and most struggle with growth on a variety of dimensions. The vast majority of ETF Strategist asset

management firms are operating well below the critical scale necessary to run efficient and profitable

businesses. Compounding this problem, the most recent Morningstar report indicates that the big are getting

bigger, with flows of new assets predominantly going to the handful of largest providers. Smaller firms are

struggling to stand out in an increasingly crowded market, even with annual industry-level growth of 50%.

Growth Through Effective Distribution

It will not come as a surprise to any veteran of the asset management industry that distribution is the key to

building a long-term successful asset management firm. Even firms with great stories, performance track

records, and management teams will fail to succeed in growing their businesses without a well-developed and

executed distribution strategy. ETF Strategy Group has developed this overview and guide to aid ETF Strategist

investment management firms in understanding obstacles and opportunities for distribution in the wealth

management industry, and to aid them in formulating productive distribution strategies that will help th em be

more competitive in the market, raise awareness of their products and services with financial advisors, and grow

assets under management/advisement. The guide is broken into the following main topics:

Evolution of the Managed ETF Solutions Market

Wealth Management Program Types & Product Packaging

Distribution Channel Overview & Opportunities

Implementing a Productive Distribution Strategy

o A Content-Centric PR & Marketing Strategy

o The Changing Face of Advisor Sales & Wholesaling

Page | 3

Evolution of the Managed ETF Solutions Market

The market collapse of 2008 was a watershed event for the asset management industry. A number of industry

trends already in process have accelerated in the subsequent market recovery. One of those trends is the

considerable growth in all categories of managed solutions.

Managed Solutions (including traditional

separately managed accounts, mutual fund

wrap/advisory, Rep-as-Advisor, Rep-as-

Portfolio Manager, Unified Managed Account,

and ETF Advisory) have all seen a steady

recovery since 2008. Due to expanded

regulatory requirements for delivering a

fiduciary standard of care, and pressure to

increase margins and recurring revenue,

advisory firms in all channels have

aggressively pushed their advisors away from

traditional transaction-based investment

products, and towards fee-based managed

solutions.

Exchange Traded Funds (ETFs) had a small footprint within the realm of managed solutions prior to 2008, and

were largely relegated to brokerage accounts and the self-directed market. Since 2008 though, and particularly

since 2010, ETFs have had the fastest growth rates within the Managed Solutions marketplace. In their 2012

report “Growth in a Time of Uncertainty, The Asset Management Industry in 2015”, McKinsey Consulting predicts

that the “second act” is about to begin in ETF industry growth. Currently at $1.5T in total assets (at the time of

the report), they predict that by 2015 more than $1.6T in new money will enter ETFs with a globa l market in

excess of $3.1T.

Managed ETF solutions (as defined by the Money Management Institute and reported by participating MMI

survey respondents) have seen the most dramatic growth of all of the different program types within managed

solutions (28.1% in 2011). This growth in managed ETF solutions is likely understated though, as the MMI survey

data focuses on the wirehouse and national/regional broker dealer markets, and a large portion of the g rowth in

managed ETF solutions has been in the independent RIA and independent broker-dealer markets.

Assets in Total Managed Solutions

($Billions) – 2007 to 2011

Source: Money Management Institute & Dover Financial Research

Page | 4

The utilization of non-correlated asset

classes and diversification through style-

box constrained investment products (e.g.

growth / value, large / small cap, equity /

fixed income) according to modern

portfolio theory failed to protect many

clients in 2008 when supposedly non-

correlated products became highly

correlated in a collapsing market.

At the same time, the ability to add alpha

through individual security selection has

come under renewed attack. Managers

and products that focus on individual

security selection (e.g. long-only equity

separately managed accounts and mutual

funds, as well as traditional transactional brokerage business) are declining in favor with advisors. The most

dramatic growth in recent years has been in lower cost indexed or passive investment strategies through ETFs

and mutual funds. An increasing portion of the returns that investment products produce are explainable in

various forms of beta. As a result, there has been a proliferation of product development and innovation from a

growing universe of ETF issuers that package that beta in very low cost ETFs. As demonstrated by the graphs,

the growth and adoption of ETFs is now challenging the traditional security selection-centric asset management

industry, leading advisors to change the types of solutions and products they offer their clients.

Building on these market dynamics and others, a new category of asset managers has emerged in the last

decade – ETF Strategists. Rather than seeking alpha through individual security selection, ETF Strategists

generally seek to minimize risk, improve diversification, and seek alpha by selecting and managing exposures

using ETFs rather than through stock or other security selection. By using ETFs, strategists are able to avoid

stock/security specific risk, while addressing many of the shortcomings in the failed traditional style-boxed based

investment approach.

The development of the ETF Strategist segment of the asset management industry began around 2000 with the

growth and adoption of ETFs, but has seen its most explosive growth since the 2008 market reset. Starting

around 2000, a large number of independent RIAs and emerging quantitative asset managers began

constructing solutions for their clients using ETFs rather than the individual equities and bonds that had

traditionally been used. The products developed by many of these firms have now matured, resulting in top-

performing portfolios with one, three, five, and even ten year track records, making them suitable for broad

market distribution into the fast growing managed ETF solutions market. The next phase of evolution for this

segment of the industry is now upon us – broad market distribution and adoption.

2011 AUM, Market Share & Growth by Program Type

Source: Money Management Institute & Dover Financial Research

Page | 5

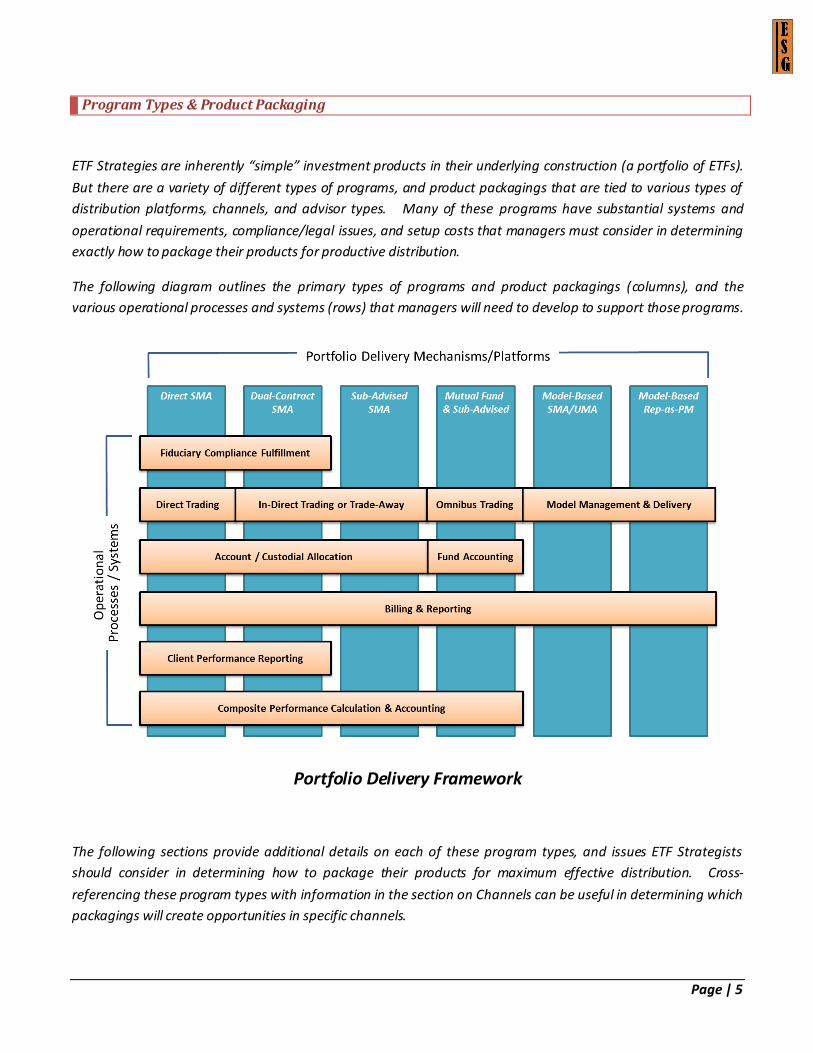

Program Types & Product Packaging

ETF Strategies are inherently “simple” investment products in their underlying construction (a portfolio of ETFs).

But there are a variety of different types of programs, and product packagings that are tied to various types of

distribution platforms, channels, and advisor types. Many of these programs have substantial systems and

operational requirements, compliance/legal issues, and setup costs that managers must consider in determining

exactly how to package their products for productive distribution.

The following diagram outlines the primary types of programs and product packagings (columns), and the

various operational processes and systems (rows) that managers will need to develop to support those programs.

Portfolio Delivery Framework

The following sections provide additional details on each of these program types, and issues ETF Strategists

should consider in determining how to package their products for maximum effective distribution. Cross-

referencing these program types with information in the section on Channels can be useful in determining which

packagings will create opportunities in specific channels.

Page | 6

Direct Separately Managed Accounts (SMA) – In this type of program, the ETF Strategist is directly soliciting a

client, operating as a primary fiduciary RIA, and typically working on one of the major RIA custodial platforms for

custody, trading, and other services. The key distinction between direct SMA business and other business is the

strategist firm is acting both as a fiduciary advisor to the client and as the asset manager. There is no other

advisor sitting between the manager and the client. For this reason, asset managers offering their products

directly to clients via Direct SMAs must have robust client service teams, and compliance procedures to ensure

adherence to fiduciary standards. Because the strategist is operating as a full advisor to the client, Direct SMA

business tends to be the highest margin (and highest cost) business, with a typical advisory fee of 50-125bps

depending on the nature of the firm and client relationship.

Dual-Contract SMA – Many firms (wirehouse, regional/national BD, RIA custodians) operate dual-contract SMA

programs in which the manager has a direct contract with the client and is serving in the same

discretionary/fiduciary role as with Direct SMA business. The primary differences with Direct SMA are that the

manager is working in concert with the client’s primary advisor (who has their own contract with the client,

hence the term “dual contract”), and the manager typically must trade and manage the assets on the advisor’s

custodial platform. Dual-contract SMA programs are a bit of the “worst of both worlds” in that they have all of

the operational costs and complexities of managing accounts on a 3rd party platform, but are generally not

promoted or otherwise heavily supported by the home office organization. Managers available in dual-contract

SMA programs are explicitly not covered by home office research, and are not “endorsed” or recommended to

advisors, thereby limiting growth and distribution opportunities. On the positive side, managers can typically

charge higher fees (individually negotiated directly with the advisor and/or client). To operate on a dual-contract

SMA platform, managers will either need to utilize an in-house multi-custody shadow portfolio accounting and

order management systems, or access and trade the accounts directly via tools provided by the custodian o r

platform provider. Some ETF Strategists have had great success building high-margin books of business via dual-

contract SMA programs, particularly in the wirehouse channel.

Sub-Advised SMA – Sometimes called SMA “wrap” accounts, or just separately managed accounts, Sub-advised

SMAs were historically the largest type of program accessible to ETF Strategists, prior to the development of

model-based UMA/SMA programs (more on that shortly). Managers/products available to advisors through

Sub-Advised SMA programs must be approved by the sponsor’s research organization, typically requiring

managers to have a minimum of $500mm in total AUM/AUA, $100mm in specific strategies to be supported on

their platform, and a 3+ year GIPS compliant track record. Sponsors typically negotiate lower fees in sub-advised

programs, often with volume breaks (e.g. 40bps for the first $100mm, 35bps for assets over $100mm). In Sub-

Advised SMA programs, the manager is discretionary and responsible for all trading. As with dual-contract SMA

programs, managers typically need to have a robust portfolio accounting and trading infrastructure that

supports trading through the underlying brokerage’s desk, or trading away with settlement to the custodian.

Sub-Advised SMA programs are generally superior distribution opportunities (as compared to dual-contract

programs) since they have smaller product rosters and are promoted to advisors and better supported by th e

sponsoring institution.

Page | 7

Mutual Fund & Sub-Advised – An increasing number of managers are having success packaging their strategies

as 40-act mutual funds, or even as an “ETF of ETFs” (e.g. AdvisorShares). Mutual funds are more accessible to

advisors and clients, are simpler to administer than SMAs, and are more cost-effective for smaller account sizes

(e.g. < $50k). There’s also a significant portion of the advisor marketplace that are more comfortable using

mutual funds than various forms of SMA and UMA programs. Managers wanting to launch mutual funds of their

portfolios should budget $125,000 in total startup costs, and will need to get AUM up to approximately $20mm

before the administrative costs of the fund are being covered by fees. Managers can typically charge a much

higher asset management fee in mutual funds and have greater control of the economics as compared to

SMA/UMA programs. There are several quality outsourced providers that can turnkey the development and

operations of a mutual fund for ETF Strategists. In addition to launching a mutual fund directly, there are

numerous fund families that actively research and hire sub-advisors for their own funds. The details and business

case considerations regarding mutual fund development and sub-advisory distribution opportunities are beyond

the scope of this paper, but launching mutual funds for high performing and high potential products can be a

cost effective means to generate assets in many channels that are inaccessible via SMA/UMA programs.

Model-Based SMA/UMA (Unified Managed Accounts) – The most accessible (requiring the least infrastructure)

and fastest growing form of distribution for ETF Strategists is via Model-Based SMA/UMA programs. In UMA

programs, managers transmit changes to their model portfolios to the sponsor or overlay manager who is

responsible for trading and other operations. The manager is operating solely as a “research provider” or non-

discretionary sub-advisor in the provision of their model. Because of this reduced role, managers typically receive

a reduced fee (20-35bps) in model-based programs. Most UMA programs have research-constrained product

rosters, as well as pre-configured asset allocations administered by the sponsor’s research organization. These

pre-configured asset allocations are often particularly productive distribution opportunities for asset managers

as they are promoted heavily by the home office and are the easiest solution for advisors to access for their

clients. Some sponsors have begun to convert their existing sub-advised SMA programs to model-based

SMA/UMA programs as a means to capture additional revenue and reduce manager fees. Some sponsors have

also begun to set up separate and distinct model-based ETF Strategist programs that have become the most

productive distribution channel for a number of the leading ETF Strategist asset managers.

Model-Based Rep-as-Portfolio Manager – Rep-as-Portfolio Manager programs are generally utilized by more

sophisticated advisors that select securities directly and act as their own portfolio manager, rather than selecting

ETF Strategists or other 3rd party asset managers to manage their clients’ assets. There are though a growing

number of programs that allow advisors to select securities (e.g. individual stocks, bonds, ETFs) for a portion of a

client portfolio, and comingle those selections with models managed by 3rd party strategists. Some of these

programs are configured as Unified Managed Accounts, whereas others are configured more like discretionary

brokerage accounts where the advisor is given trading tools and direct access to manager mo dels for

implementation. Presently there are limited distribution opportunities for ETF Strategists in these types of

programs, but as the fee-based platforms within the industry continue to evolve in the coming years, it is likely

that the lines between rep-as-PM and UMA programs will continue to blur, and ETF Strategists will have

increasing opportunities to distribute their portfolios to the sophisticated advisors that utilize those programs.

Page | 8

Distribution Channel Overview & Opportunities

ETF Strategist asset managers have multiple opportunities for distributing their portfolios, from directly soliciting

and serving retail investors as a discretionary RIA (typically via directly managed SMAs), to sub-advising in the

institutional market. The following framework outlines the major distribution channels available to ETF

Strategist asset managers with sample firms (certainly not exhaustive lists) within each channel. The following

pages provide details for each channel, some perspective on the distribution opportunity for the channel, and

costs, considerations and strategies for pursuing opportunities in the channel.

Distribution Channel Framework

Page | 9

Wirehouse – While the term “wire house” has a much broader definition in some circles, general usage refers to

the (now) four major historic broker dealer advisory firms – Morgan Stanley Smith Barney, Wells Fargo Advisors,

Merrill Lynch (owned by Bank of America) and UBS. The wirehouses led the development of fee-based wealth

management solutions and have the largest and most mature platforms, accessible to thousands of advisors.

Wirehouse advisors are generally constrained to the solutions/programs supported by their home office

organizations. Some ETF Strategists have raised significant assets in the dual-contract programs of wirehouses

without research coverage or endorsement from the home office, but as of this publication, the wirehouses are

not broadly distributing 3rd party ETF Strategist solutions in their more productive sub-advised (SMA and UMA)

programs. This is typically because they have developed proprietary asset allocation products that they would

prefer to promote over 3rd party offerings. As ETF Strategists gain traction in the broader market and the

wirehouses are forced to compete for advisors that use those portfolios, and as the wirehouses’ in-house

solutions are forced to compete (on a performance basis) against 3rd party managed ETF solutions, the channel is

likely to become more productive for ETF Strategists.

Regional/National Broker Dealer – The “regional” broker dealer market has shrunk considerably in the last

decade as firms have been acquired and merged into the wirehouses (e.g. UBS acquiring Piper Jaffray and

McDonald Investments), and as former regionals have merged to become larger nationals (e.g. Stifel Nicolaus

acquiring Ryan Beck and others). Nevertheless, the regional broker dealers are a strong channel and represent a

good distribution opportunity for ETF Strategists. Some regional/national broker dealers have been leaders in

the promotion of 3rd party ETF Strategists to their advisors, even constructing dedicated programs (e.g. RBC

Wealth Management Consulting Solutions). Most of the regional/national BDs have mature fee-based platforms

analogous to the wirehouse offerings, but are typically easier to work with and provide sales coverage for.

Independent Broker Dealer (IBD) – Unlike advisors in the wirehouses and regional/national broker dealer firms,

independent broker dealer firms don’t typically have strong proprietary fee-based platforms that would support

ETF Strategist distribution. Advisors at IBDs vary considerably in the nature of their practice and utilization of

investment solutions (e.g. insurance affiliated brokers focusing in insurance products, or transactional brokers

focusing on traditional stock brokerage business). IBD advisors will often operate in a hybrid model, being

affiliated with a broker dealer for their brokerage business, and one or more of the RIA custodians or turnkey

platforms for their fee-based advisory business. IBD advisors that provide any substantial investment advisory

services typically use one of the turnkey platforms (see below). ETF Strategists that seek opportunities in the IBD

market should focus on specific firms where they can develop a preferential home-office sales relationship, or

pursue firms in partnership with the TAMPs that are better positioned to service IBD advisors.

Registered Investment Advisors & Hybrid BD/RIA – Independent RIAs are the fastest growing channel of the

financial advisory market. Independent RIAs generally partner with one of the major RIA custodians (Fidelity,

Schwab, TD Ameritrade or Pershing) for custody and trading services, and often for other platform and product

services. The TAMPs (see below) also generally target advisors in the RIA market, and also partner with the

major RIA custodians. We have also included LPL and Raymond James in this category as “hybrid” firms that

straddle the line between national broker dealers and independent RIA platforms, in that they have programs

that allow advisors to operate independently and utilize their platforms as independent RIAs, competing with the

Page | 10

other RIA custodians (e.g. Schwab). While the entire independent RIA market is growing, it is also one of the

most complex channels to target for distribution. Independent RIAs are very different in how they practice, the

products they use, and the vendors they partner with. Many ETF Strategists also operate as RIAs in servicing

their direct retail clients, and many are actively partnered with one or more of the major RIA custodians for

marketing and promotion of their solutions to other RIAs. The Independent RIA channel probably represents the

highest potential, but also complex to address market for ETF Strategists.

Turnkey Platforms (TAMPs) – The TAMPs are typically used by advisors in the independent broker dealer and

independent RIA channels. Some turnkey platforms target other niche markets such as small banks. Turnkey

programs are extremely varied in their product rosters and philosophies. Some firms (e.g. Placemark) have a

broad super-market approach and provide very easy access for ETF Strategists, where other firms (e.g.

Genworth) offer their advisors very constrained product rosters based on their internal research and investment

philosophy. Some TAMPs have also created their own managed ETF solutions (e.g. Envestnet PMC) that compete

with 3rd party ETF Strategist portfolios. The TAMPs as a category have been early adopters and promoters of ETF

Strategists and represent good distribution opportunities/partners and efficient access points for ETF Strategists.

Multi-Family Office (MFO) & Small Institutions – The smaller institutional (< $100mm) and multi-family office

markets have traditional used more sophisticated products (e.g. hedge funds, private equity, limited

partnerships, real assets), often selected in partnership with institutional consultants. Recently though, some

institutions (particularly $10-50mm portfolios) have begun working with established ETF Strategists in lieu of

institutional consultants in something of an outsourced CIO model. Like the independent RIA channel, the MFO

and small institutions market is very heterogeneous and difficult to penetrate without a highly experienced sales

force. The larger traditional institutional market is not covered in this guide, as those firms generally would not

consider ETF Strategists for their portfolios.

U.S. Banks – The U.S. banks could rightly be sub-segmented by size (smaller regionals vs. the larger nationals) as

well as advisor types (retail bank brokers and wealth advisors vs. HNW private client and trust groups). In

general, banks are late adopters of wealth management solutions, and the bank channel is not a particularly

lucrative market at this time for ETF Strategists. In addition, many bank research groups are averse to tactical

management and other characteristics of many managed ETF solutions, and typically control asset allocation

choices and limit product selection to traditional products (e.g. long only equity and fixed income). There are

exceptions though, and some ETF Strategists have had considerable success partnering with banks (particularly

regional banks) in utilizing their managed ETF solutions as the “house” solution for their advisors.

Canada – While not truly a “channel” per se, the Canadian market represents a unique opportunity for U.S.

based asset managers. The market is dominated by approximately six bank-affiliate financial institutions, plus a

handful of independent RIA equivalents and a few large insurance affiliated advisory firms. Two of the top -3

firms have well developed model-based programs that provide efficient distribution opportunities for managers,

and the rest have well developed sub-advised SMA programs. The Canadian market is typically several years

behind the U.S. market in product development/adoption, but the major Canadian platforms are likely to develop

Page | 11

ETF Strategist rosters for their advisors in the next few years, following in the footsteps of the major U.S. based

platforms.

Direct Retail – Many ETF Strategists started as wealth managers, directly soliciting and servicing individual

investors and operating as independent RIAs. Managed ETF solutions are particularly well suited to direct retail

distribution given their relatively simple operations, holistic nature (as compared to style-box constrained

products), transparency, and low cost. For ETF Strategists with established direct retail advisory practices,

invested in digital and local market marketing efforts can be highly productive. Some ETF Strategists have

developed very innovative and productive direct retail strategies, such as hosting a local radio program. For ETF

Strategists that do not presently directly solicit or service retail investors, developing a full advisory offering can

be a cost-effective way to diversify the business.

International – Like Canada, “International” isn’t truly a channel, but it does represent a very large potential

future distribution opportunity for ETF Strategist asset managers. The non-U.S. markets are extremely varied in

their regulatory requirements, and in their use of investment products. The European markets are increasingly

accessible to U.S. based asset managers, and some ETF Strategists have had success packaging UCITs for EU-

wide distribution, typically in partnership with the major European banks. The European private banks, as well

as major private/trust banks in Asia (Singapore, Shanghai, Tokyo), the UAE and Latin America are all potential

distribution partners for ETF Strategists. Effectively selling into any of these markets requires considerable

investment in understanding the market, legal/regulatory expenses, and the establish of partnerships with

foreign banks/institutions with dedicated and knowledgeable sales resources.

Insurance / Annuities – The U.S. insurance industry has primarily utilized proprietary (and expensive) mutual

fund families for annuity products. Recently some insurance companies have begun using (or at least

considering) ETFs, and managed ETF portfolios within variable and fixed annuity wrappers. Success in the

insurance channel generally requires sales, legal and operations resources familiar with the operating

requirements for running portfolios within insurance packages, and an active partnership sales model with a

leading insurance provider.

401K / Retirement – Perhaps one of the largest (largely untapped) distribution opportunities for ETF Strategists

is the 401k (and other retirement accounts) market. 401k programs tend to be dominated by proprietary (and

often expensive) mutual fund offerings, but in recent years several providers such as Mid Atlantic Capital Group

have begun offering programs and technology for implementing managed ETF solutions efficiently within 401K

programs. As with other channels, opportunities in the 401k market are best developed by experienced sales

staff that are familiar with the variety of 401k program providers and plan administrators.

Page | 12

Implementing a Productive Distribution Strategy

Distribution is more than “sales”. Implementing a productive distribution strategy for an ETF Strategist asset

manager requires planning and execution across six primary disciplines and functional areas.

PR & Centers of Influence Awareness – An effective press strategy can provide enormous leverage in support of

sales. A PR strategy requires the cultivation of relationships with key writers for the on -line and print

publications most frequently read by a strategist’s primary target channels. Creating regular newsworthy

“events” or stories, as well as writing by-lined articles can provide significant inbound interest in your portfolios,

as well as provide content (reprints) that can be used in support of your direct sales and marketing efforts.

Event Planning, Marketing & Materials – A productive marketing program is organized around key industry

events and activities, with a deliberate plan and calendar to drive preparations of necessary materials, event

planning, follow-up communications and sales dialogs, etc. Collateral that highlights product metrics and

attributes are necessary but insufficient to support mailings, digital distribution and conference participation.

Value-adding content in the firm of meaningful research and ideas that advisors can use to support their

utilization of your product are critical.

Digital Marketing – Not surprisingly, today advisors often first turn to an asset manager’s web-site to learn more

about the firm and products. A high quality, professional, and regularly updated web site is a basic “cost of

entry” requirement for ETF Strategists operating in a competitive asset management market. A well-organized

direct email marketing infrastructure, managed social media presence, webinars, and other on-line interactions

can build awareness and loyalty with advisors.

Page | 13

Key Account / Home Office Sales – Generally responsible for getting your portfolios “on the shelf” and keeping

them there, key account management and home office sales is particularly important for ETF Strategists looking

to compete in the wirehouse, regional/national BD, and independent BD/hybrid channels. Key account staff need

to be highly skilled (e.g. CFA holders) and able to represent the firm well both in research dialogs, and business

exchanges (i.e. financial arrangements) required to get preferential positioning on major fee-based platforms.

Outside Advisor Sales – Historically referred to as “wholesaling”, the role of outside advisor sales has changed

significantly in the past decade. Due to the cost of providing branch-level support, most ETF Strategists have

adopted a hybrid sales model in which representatives participate in major events/conferences and pursue

referrals generated from digital marketing and inside sales campaigns. The section below on “The Changing

Face of Advisor Sales & Wholesaling” provides additional content on this topic.

Inside Sales & Support – Most asset managers (including ETF Strategists) typically maintain a ratio of at least

one inside agent to one field wholesaler, with that ratio being much higher in some instances. Some ETF

Strategists have been very successful in staffing a larger inside sales function to drive sales through targeted call

and email campaigns, and in digital marketing campaigns tied to major industry events. Inside sales is much

more cost-effective and flexible than outside wholesalers. See the section below on “The Changing Face of

Advisor Sales & Wholesaling” for additional thoughts on the role of inside vs. outside sales.

A Content-Centric PR & Marketing Strategy

Core to a productive public relations and digital marketing strategy is regularly developing content that is

compelling and value-adding to advisors. Beyond information specific to your strategies and investment

philosophy, what is your firm going to be known for? Developing compelling content is hard work and requires

deliberate planning and resource allocation. While some firms work with outside agents/consultants on the

development of content, a content strategy must ultimately be driven by the CIO and other thought leaders

within the ETF Strategist’s organization. Content can take the form of white papers, “how to” guides, trade

rationales, economic views and opinions, and other topical content that advisors can use to become informed,

and also aid them in their own efforts at raising assets and utilizing your products in the development of

solutions for their clients.

The Changing Face of Advisor Sales & Wholesaling

The advisor sales model has changed significantly in the past decade. In the 1990s and before, branch-level

wholesaling (often buying lunch for the branch and handing out sleeves of golf balls while giving a rote product

pitch via PowerPoint) was key to driving product awareness and adoption. Increasingly, large sponsors do not

allow wholesalers in their branches, and advisors don’t want to invest the time. There are multiple models that

ETF Strategists have developed in lieu of putting ‘feet on the street’, primarily digital marketing, event marketing,

and outbound campaigns via inside sales organizations. Partnership selling with ETF issuers, TAMPs and other

industry Centers of Influence are also increasingly providing sales leverage for ETF Strategist asset managers.

Page | 14

About Randy Bullard & ETF Strategy Group

ETF Strategy Group (ESG) was founded in July 2012 to help ETF Strategist investment management firms develop

and grow their businesses. ESG provides a variety of services including the following:

Strategic business consulting, and distribution strategy development and implementation services for

ETF Strategist asset management firms.

Third-party marketing services designed to help ETF Strategist asset managers execute effective

distribution strategies and grow assets under management in key markets.

Investment banking services designed to help ETF Strategist asset managers gain access to growth

capital, and implement productive growth and business transformation strategies.

Consulting and business development services to ETF issuers, private equity firms, and product/service

providers targeting the growing ETF Strategist asset management market.

ETF Strategy Group is led by Randy Bullard. Randy has over 20 years of industry experience in strategy consulting

and asset management services, most recently as co-founder in 1999 of Placemark Investments. While at

Placemark, Randy led the firm’s PR, Marketing and Business Development efforts, as well as many aspects of the

firm’s product and service development and evolution. Randy led the establishment of custom wealth

management programs for ~20 leading providers including Smith Barney Consulting Group, UBS, RBC Wealth

Management, TD Ameritrade, BMO Nesbitt Burns and many others resulting in $8B+ in assets under

management and relationships with thousands of financial advisors. Prior to founding Placemark Investments,

Randy was a Principal Consultant with A.T. Kearney, leading strategy and systems implementation projects for

firms in the financial services industry including Goldman Sachs and Citigroup. Randy has published numerous

articles and papers on wealth management industry topics, and is a frequent speaker and cited industry leader

on a variety of topics including Unified Managed Accounts, Overlay Management, Wealth Management

Platforms, and Managed ETF Solutions.

For additional information, please contact Randy at [email protected]

Copyright © 2012 Randy Bullard, ETF Strategy Group. Distribution in whole permitted without notification. Distribution in

part or other usage granted upon request. www.RandyBullard.com