EQ03 CORPORATE STRATEGIC ANALYTICS I - … EQ03 Dr Chng utar 080411.pdf · EQ03 CORPORATE STRATEGIC...

50

EQ03 CORPORATE STRATEGIC ANALYTICS I: Essentials of Corporate Proposal Analysis Dr Ch’ng Huck Khoon UTAR, Kampar 8 April 2011

Transcript of EQ03 CORPORATE STRATEGIC ANALYTICS I - … EQ03 Dr Chng utar 080411.pdf · EQ03 CORPORATE STRATEGIC...

EQ03CORPORATE STRATEGIC ANALYTICS I:Essentials of Corporate Proposal Analysis

Dr Ch’ng Huck Khoon

UTAR, Kampar

8 April 2011

Session One

Essentials Of Understanding The IPO And Restructure Exercise

3

Financial Objectives

• Maximize the wealth of the ordinary shareholder

• Shareholder’s return• Capital gain

• Dividends

4

Reasons for Seeking a Stock Market Listing (IPO) ?

5

Reasons for Seeking a Stock Market Listing (IPO)

• Access to wider pool of finance

• Improved marketability of shares

• Transfer of capital to other uses

• Enhancement of the company image

• Facilitation of growth by acquisition

6

IPO

7

TASCO – IPO price RM 1.10

8

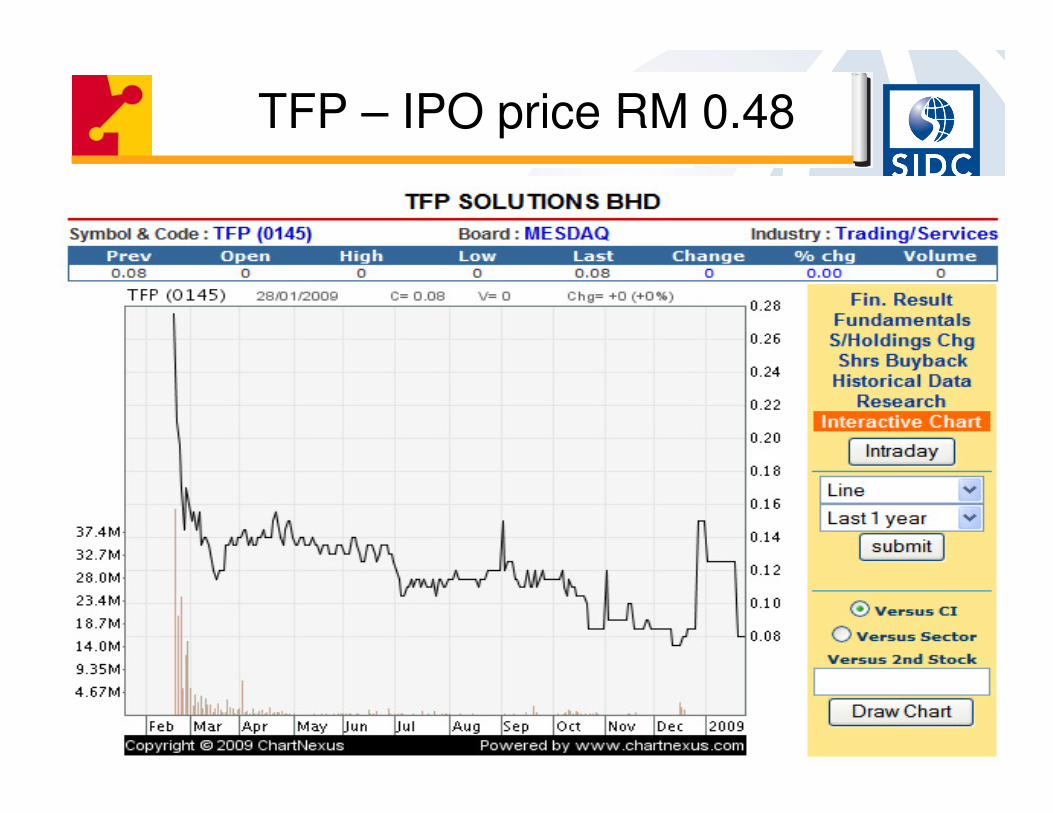

TFP – IPO price RM 0.48

9

10

3rd August 2009

SponsorProfit

ACE

Last year > RM 4 mil

3 to 5 years > RM 12 milProfit

Second Board

Last year > RM 8 mil

3 to 5 years > RM 30 milProfit

Main Board

NOW

last year > RM 6mil

3 to 5 years > RM20 milprofit

MAIN MARKET

11

IPO : Prospectus

• What to look out for in a prospectus ?

12

IPO : Prospectus

• What to look out for in a prospectus ?

– About the company

– Competitive strengths

– Financial highlights

– Industry prospects

– Future plans

– Particulars of listing

13

Type of Proposal and Rationale

• Public issue

• Offer for sale

• Tender

• Private placement

• SC introduces “green shoe” option and price stabilization mechanism for IPOs on 11 January 2008

14

“Green Shoe”

• The “green shoe” mechanism allows the issuer to over-allot securities in excess of the number of shares constituting the original offer size to ensure that the demand for shares in an IPO can be met in an efficient manner and that price volatility during the period immediately after listing can be minimised.

15

• The mechanism can be used for any IPO where the total value of shares offered is not less than RM150 million. It can commence on the date of listing of the issuer and continue to be carried out during the first 30 days of trading from the IPO date.

“Green Shoe”

16

Resorts – Share Buybacks

9,284,944.204,700,000Total

1.97 to 1.992,387,050.701,200,00010/3/2009

1.92 to 1.942,904,753.501,500,00012/3/2009

1.993,993,140.002,000,00024/3/2009

Range

Total amount paid for

Share Purchased (RM)

No of share

buyback

17

Resorts – Share Buybacks

18

Share Buybacks

• Why share buybacks ?

• Motivation ?

• Disadvantages ?

• Impact on share valuation ?

19

Share Buybacks

• Share buybacks or share repurchases can be a method of capital reduction

• A share buyback occurs when the listed company uses its own funds to go into the open market and acquire its own shares.

• The shares may or may not be retained by the company.

• The company can choose to keep them as treasury shares, or choose to cancel them.

20

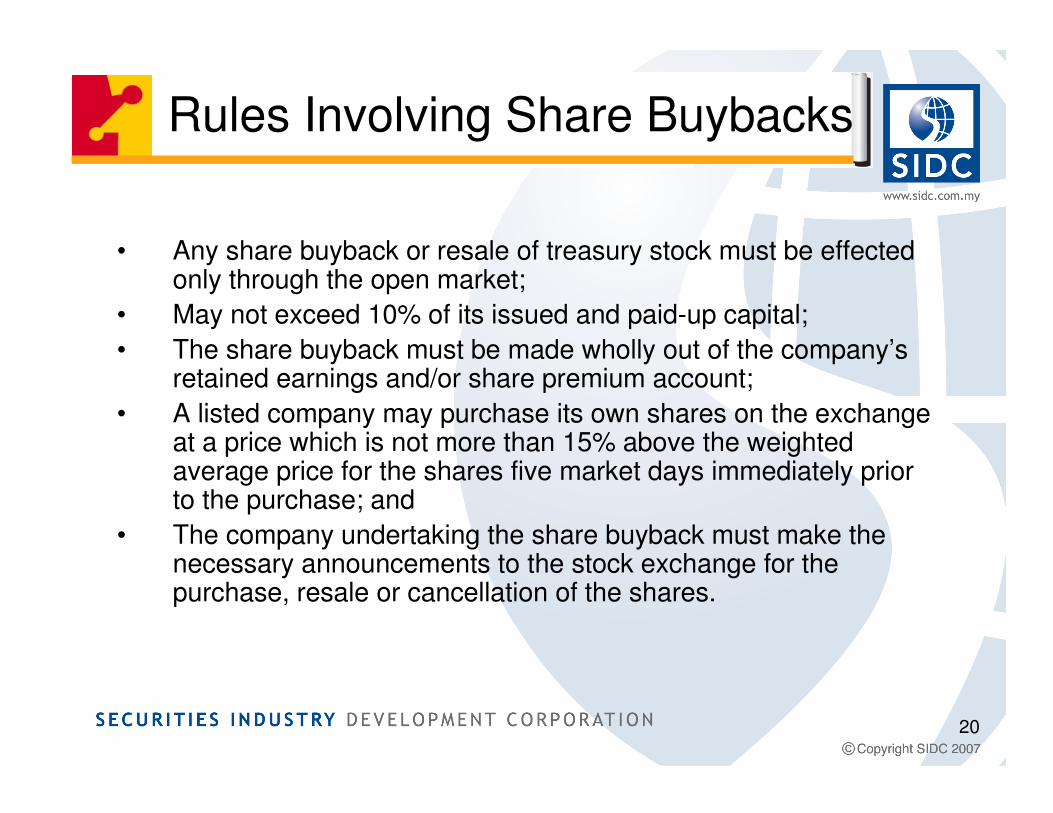

Rules Involving Share Buybacks

• Any share buyback or resale of treasury stock must be effected only through the open market;

• May not exceed 10% of its issued and paid-up capital;

• The share buyback must be made wholly out of the company’s retained earnings and/or share premium account;

• A listed company may purchase its own shares on the exchange at a price which is not more than 15% above the weighted average price for the shares five market days immediately prior to the purchase; and

• The company undertaking the share buyback must make the necessary announcements to the stock exchange for the purchase, resale or cancellation of the shares.

21

Motivation Behind Share Buybacks

• Underlying belief that their shares are undervalued.

• Company is able to control, to some extent, the trading of the shares in the open market, and ensure that the price of the share is stabilized and supports the fundamentals of the company.

• Available dividend payment is spread between fewer shares, so the dividend per share is higher for the remaining shareholders.This also means that the net profit is spread over fewer shares,thereby raising net EPS and increasing value for existing shareholders.

• If shares are kept as treasury shares, they may be paid out as stock dividends to existing shareholders. Can choose to sell shares which are purchased and kept in treasury at a higher price in the future resulting in capital gains to the company.

22

Disadvantage

• Reflects that the management can think of

nothing better to do with company money than

buy its own shares

• This could result in a reduction in the financial

resources of the company

• May increase the risk of the company having to

forego profitable investment opportunities in the

future.

23

Impact on Share Valuation

• Hence, a share buyback is usually welcomed by existing shareholders as a positive corporate action to

enhance shareholder valuation

• A tax efficient vehicle to minimize tax liabilities of

investors.

• Usually when companies announce intentions to buy back own shares, investors perceive that the

company’s share price will be well supported, hence resulting in a subsequent rise in share prices.

24

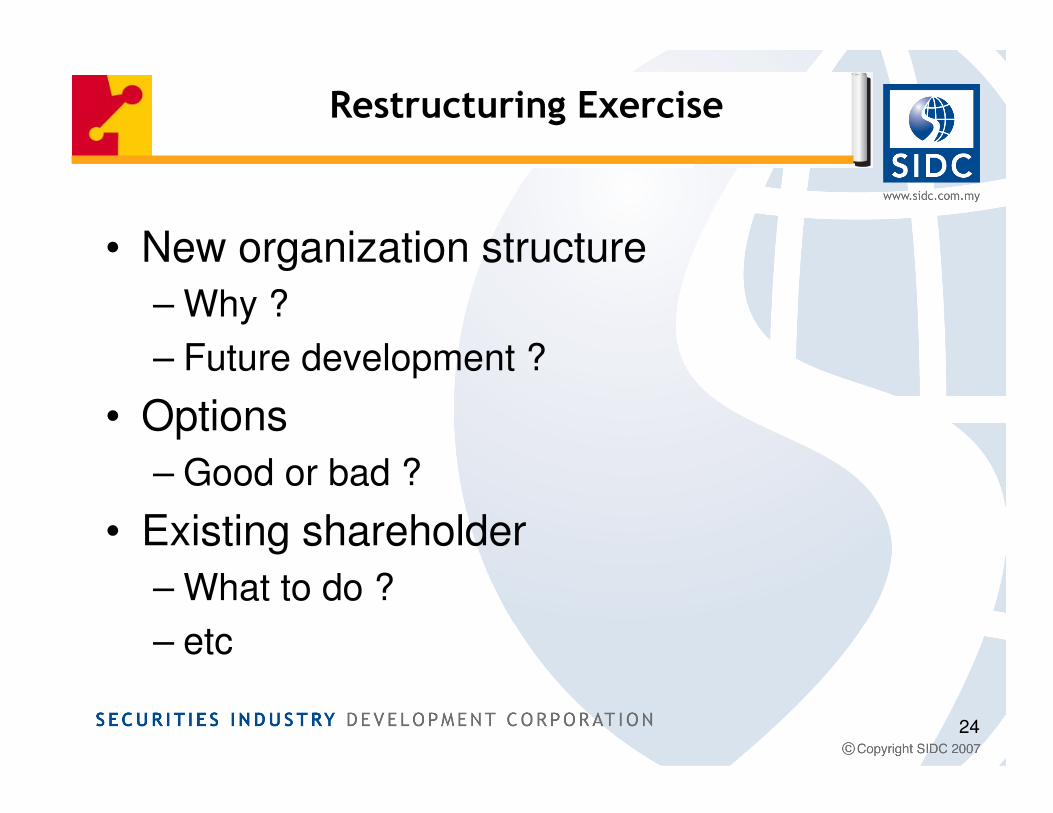

Restructuring Exercise

• New organization structure

– Why ?

– Future development ?

• Options

– Good or bad ?

• Existing shareholder

– What to do ?

– etc

25

Case Study 1 – UEM World

• You are required to comment on the UEMWORLD restructure exercise. < News Release on 15 February

2008 >

• Discuss the importance of listing of UEM Land.

26

Session Two

Understanding The Nature Of Business Activities Related To Company

Valuation

27

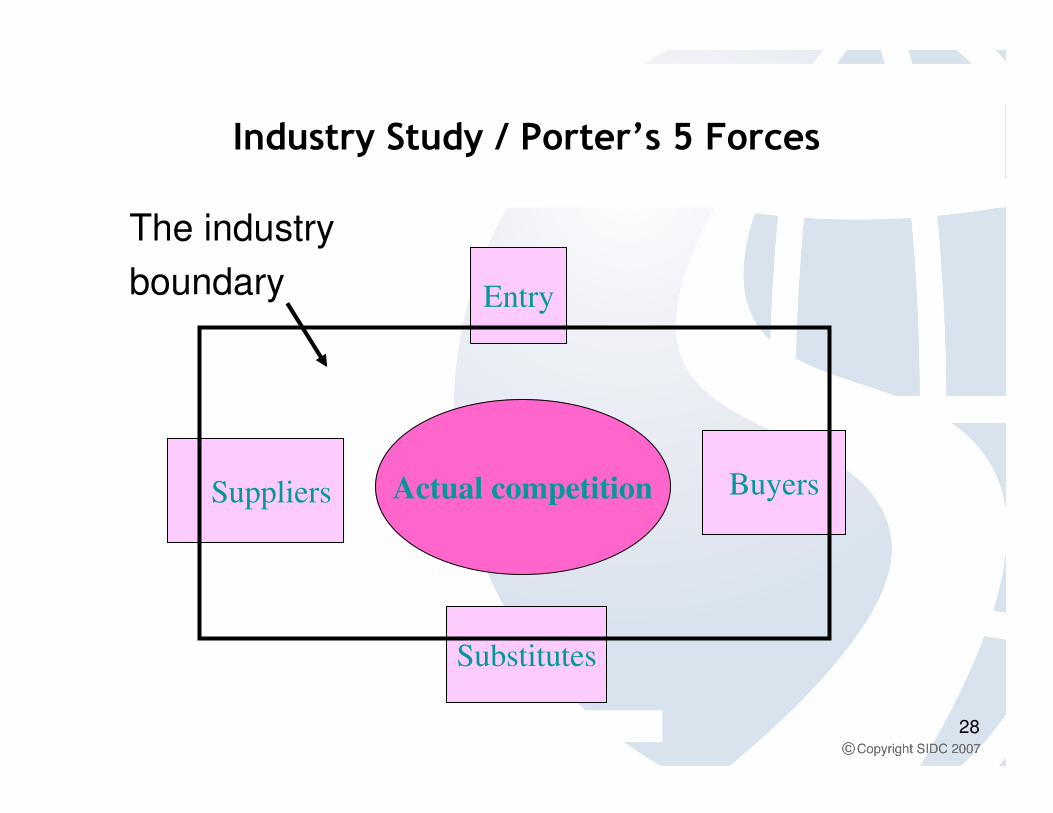

Nature of Business Activities

– Who are their competitors

– Industry study

– Risk associated with the business, its merits

and demerits – systematic risk, beta, barrier

to entry & exit

– Track record

28

Industry Study / Porter’s 5 Forces

The industry

boundary

Buyers

Substitutes

Suppliers

Entry

Actual competition

29

Nature of Business Activities

30

31

Financial Analysis

• Ratio analysis

• Trend analysis

• Segmental analysis

• Cash flow analysis

• Notes to the account

32

Company Valuation

– Comparative analysis

– Target price (fair value)

– Quality of sector PE

– Market PE

– Discount/premium etc.

33

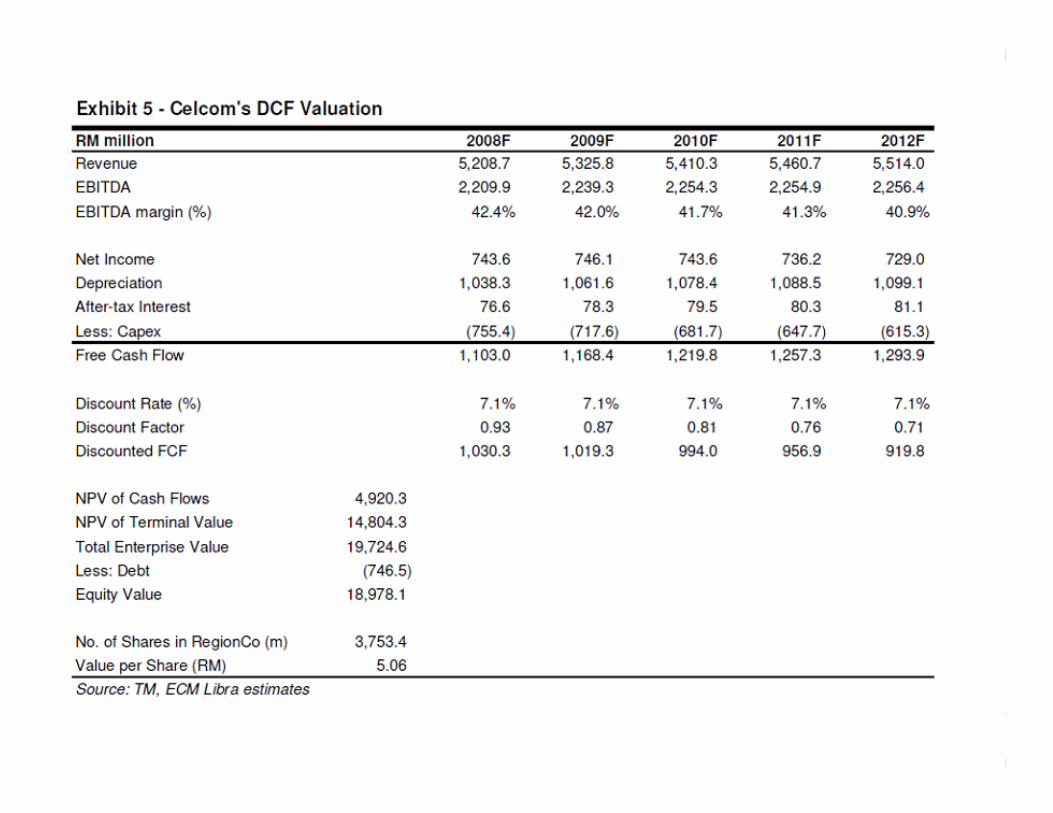

Company Valuation

• DCF

– refer to research report - TM by ecmlibra - 13

March 2008

34

35

Case Study 2 – Synergy Drive (SIME)

• Refer to Synergy Drive articles in The Star dated 7 May 2007, comment on the restructure exercise.

36

• Key questions

• Why merge?– What benefit?

• Centralization of management– Good or bad?

• Impact– % in KLCI?

– Influence on Bursa

– Possible of take over smaller company?

Case Study 2 – Synergy Drive (SIME)

37

Session Three

Reasons and Factors in M&A Decision

38

Reasons for M&A

• Operating economies

• Management acquisition

• Diversification

• Asset backing

• The quality of earning

39

Reasons for M&A

• Finance and liquidity

• Growth

• Tax factors

• Defensive merger

40

Reasons for M&A

• The aims of a M&A should be to

make profit in the long term as

well as the short term.

41

Rules and Regulations

• Malaysian code on Take-Overs and Mergers 1998

• Capital Market Services Act 2007

• Company Act 1965

• Securities Commission Act 1993

42

– What would the cost of acquisition be

– Would the acquisition be worth the price (what

is the highest price that it would be worth

paying to acquire the business?)

• Value of a business could be assessed in term of:

– Its earning

– Its assets

– Its prospects for sale and earning growth

– How it would contribute to the strategy of the “predator company”

Factors in a Takeover Decision

43

• Other factors

– Would the takeover be regarded as desirable

by the predator company’s shareholders and

the stock market in general?

– Are the owners of the target company

amenable to a takeover bid? Or would they be

likely to adopt defensive tactics to resist a

bid?

Factors in a Takeover Decision

44

• Other factors

– What form would the purchase consideration

take ?

– How would the takeover be reflected in the

published accounts of the predator company?

– Would there be any other potential problems

arising from the proposed takeover, such as

future dividend policy and service contracts

for the key personnel?

Factors in a Takeover Decision

45

Session Four

Equity Financing

46

Case Study 4

• you are required to comment on Hap SengConsolidated Berhad proposals from the point of the management and retail shareholder.

47

• On behalf of the Board of Directors of HSCB, CIMB Investment Bank Berhad wishes to announce that the Company proposes to undertake the following:

(i) a private placement of up to 124,532,000 new ordinary shares of RM1.00 each in HSCB (“HSCB Shares”) (“Proposed Placement”);

(ii) a bonus issue of up to 1,494,384,000 new HSCB Shares (“Bonus Shares”) on the basis of two (2) Bonus Shares for every one (1) existing HSCB Share held after the Proposed Placement (“Proposed Bonus Issue”);

48

• (iii) a renounceable rights issue of up to 448,315,200 new HSCB Shares (“Rights Shares”) together with up to 448,315,200 new free detachable warrants (“Warrants”) on the basis of one (1) Rights Share together with one (1) Warrant for every five (5) HSCB Shares held after the Proposed Bonus Issue (“Proposed Rights Issue with Warrants”);

(iv) an increase in the authorised share capital of HSCB from RM1,000,000,000 comprising 1,000,000,000 HSCB Shares to RM5,000,000,000 comprising 5,000,000,000 HSCB Shares (“Proposed Increase in Authorised Share Capital”); and

49

• (v) amendments to the Memorandum and Articles of Association of HSCB (“Proposed M&A Amendments”).

(collectively, (i) to (v) above are referred to as the “Proposals”)

Please refer to the attachment for the details of the Proposals.

This announcement is dated 7 January 2011.

50