Epicurean Chocolates

208

EPICUREAN | 1

-

Upload

dexter-alonday -

Category

Education

-

view

141 -

download

1

Transcript of Epicurean Chocolates

EPICUREAN | 1

Epicurean Chocolates | 1

Ateneo de Davao University

A Project Feasibility Study in establishing a

Chocolate Patisserie in Davao City

“EPICUREAN CHOCOLATES”

In Partial Fulfilment of the requirements in

Accounting 12: Management Consultancy

Submitted to:

Ryan Morales, CPA

Submitted by:

Dexter Val Alonday

Jeanette Amabelle Ansing

Dawn Nicca Aryata

Joshua Rey Cosare

Jasper Nikko Estimada

Maricon Mamaclay

Sweetzel Dyne Morales

Shieldon Vic Pinoon

October 2016

EPICUREAN | i

Acknowledgement

We, the proponents of this feasibility study, would like to express our heartfelt gratitude to

the people who have contributed to the success and completion of this study:

To our Almighty Father, for without Him, everything will not be possible.

To our respective families, for the unfailing financial and moral support.

To Mr. Ryan Morales, CPA, subject professor, for the guidance and insights in our

revisions to make our study a good one.

To Mr. Charlon San Pedro, chef, for his insights regarding our proposed menu and sharing

his knowledge about the workings of a restaurant.

To Mr. Eric V. Mamaclay and Engr. Ely V. Mamaclay, for making the floor plan of our

proposed store.

To Rafski Pastry and Bakery Supplies, for accommodating us in our interviews regarding

the technical aspect of our study.

To Mr. Fernando Lagahit, Regional Head of DBP Davao, for sharing his knowledge

regarding the financial part of our study.

To Alonday Family, for their hospitality in offering their home and resources when we

needed it.

To the administrators of University of the Immaculate Conception, Holy Cross of Davao

College, and Mazda, for allowing us to enter their school and business premises in order to conduct

our survey.

To the respondents, who have willingly given their time to answer our survey questions.

To everyone, who have, in one way or another helped us in our journey.

EPICUREAN | ii

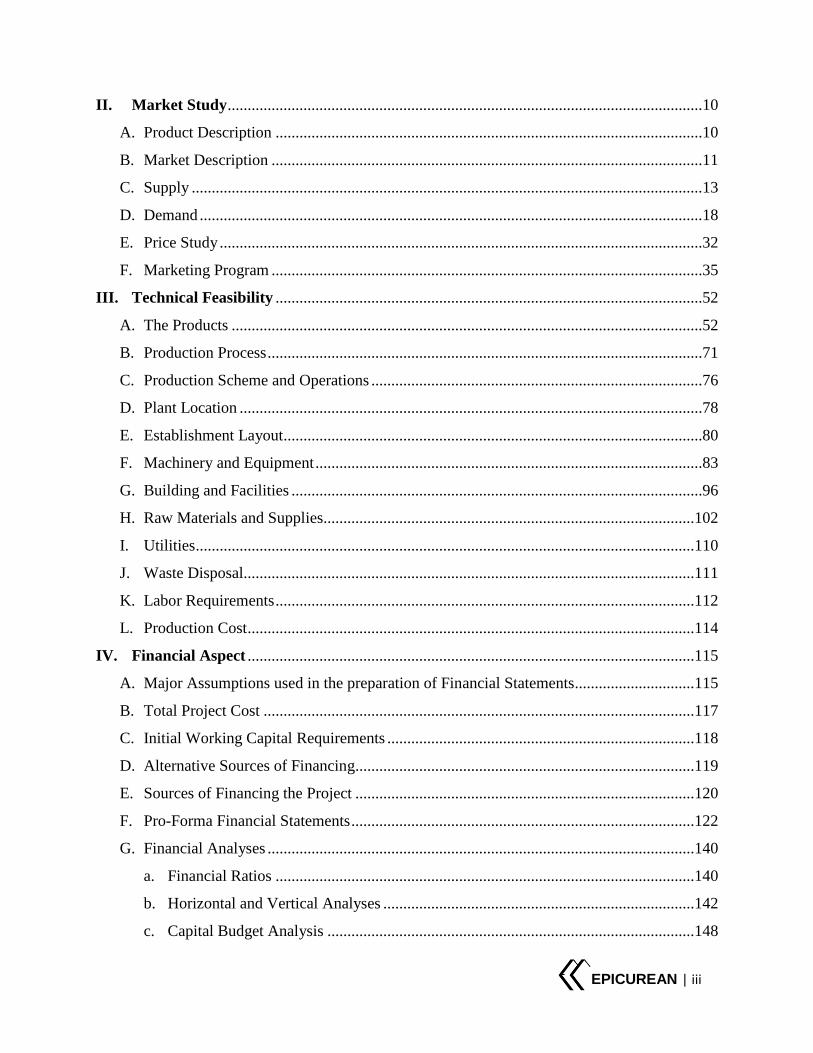

TABLE OF CONTENTS

Acknowledgment ............................................................................................................................ i

Table of Contents .......................................................................................................................... ii

List of Charts ................................................................................................................................ iv

List of Figures .................................................................................................................................v

List of Tables ..................................................................................................................................v

I. Summary of the Project ........................................................................................................1

A. Name of the Project .............................................................................................................1

B. Location ...............................................................................................................................2

C. Descriptive Definition of the Project ...................................................................................2

D. Long Range Objectives ........................................................................................................3

E. Feasibility Criteria ...............................................................................................................3

a. Market ............................................................................................................................3

b. Technical ........................................................................................................................3

c. Financial .........................................................................................................................3

d. Socio-economic..............................................................................................................4

e. Organization and Management ......................................................................................4

F. Highlights .............................................................................................................................4

a. History of the Project .....................................................................................................4

b. Nature of the Industry ....................................................................................................5

c. Problems faced by the industry ......................................................................................5

d. Mode of Financing .........................................................................................................5

e. Investment cost and initial working capital ...................................................................6

G. Major Assumptions and Summary of Findings and Conclusions .......................................6

a. Market ...........................................................................................................................6

b. Technical ........................................................................................................................7

c. Financial .........................................................................................................................7

d. Socio-economic..............................................................................................................8

e. Organization and Management ......................................................................................8

EPICUREAN | iii

II. Market Study .......................................................................................................................10

A. Product Description ...........................................................................................................10

B. Market Description ............................................................................................................11

C. Supply ................................................................................................................................13

D. Demand ..............................................................................................................................18

E. Price Study .........................................................................................................................32

F. Marketing Program ............................................................................................................35

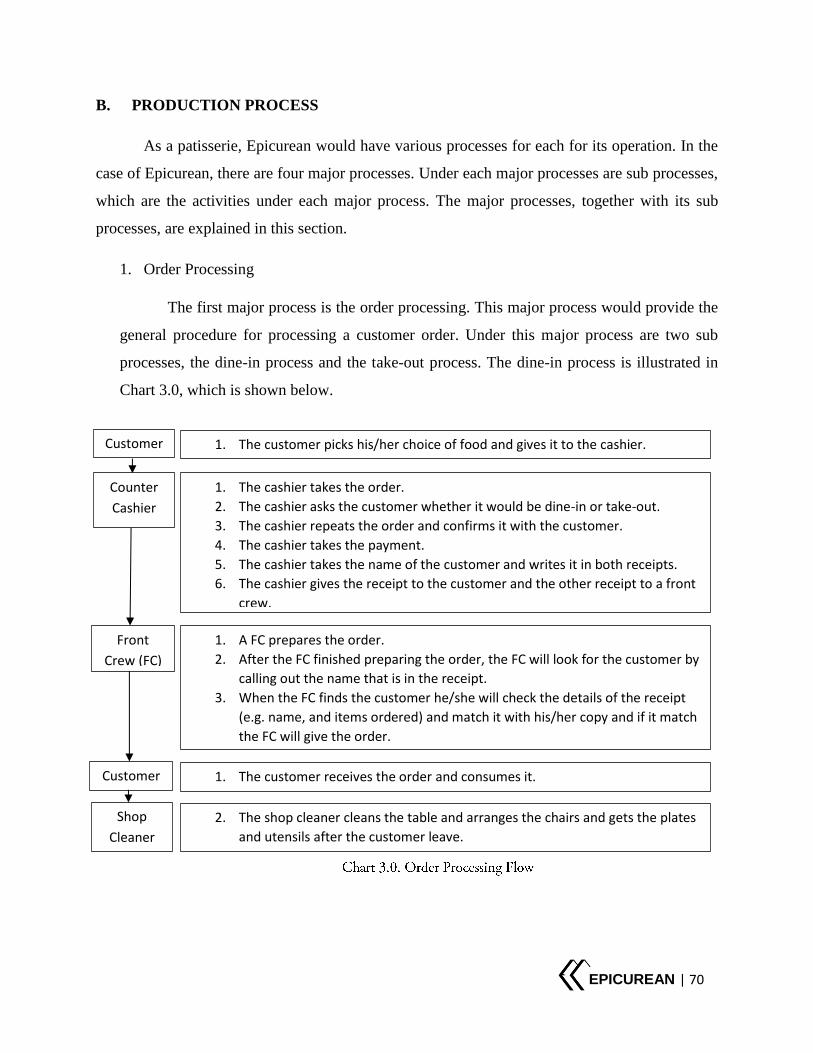

III. Technical Feasibility ...........................................................................................................52

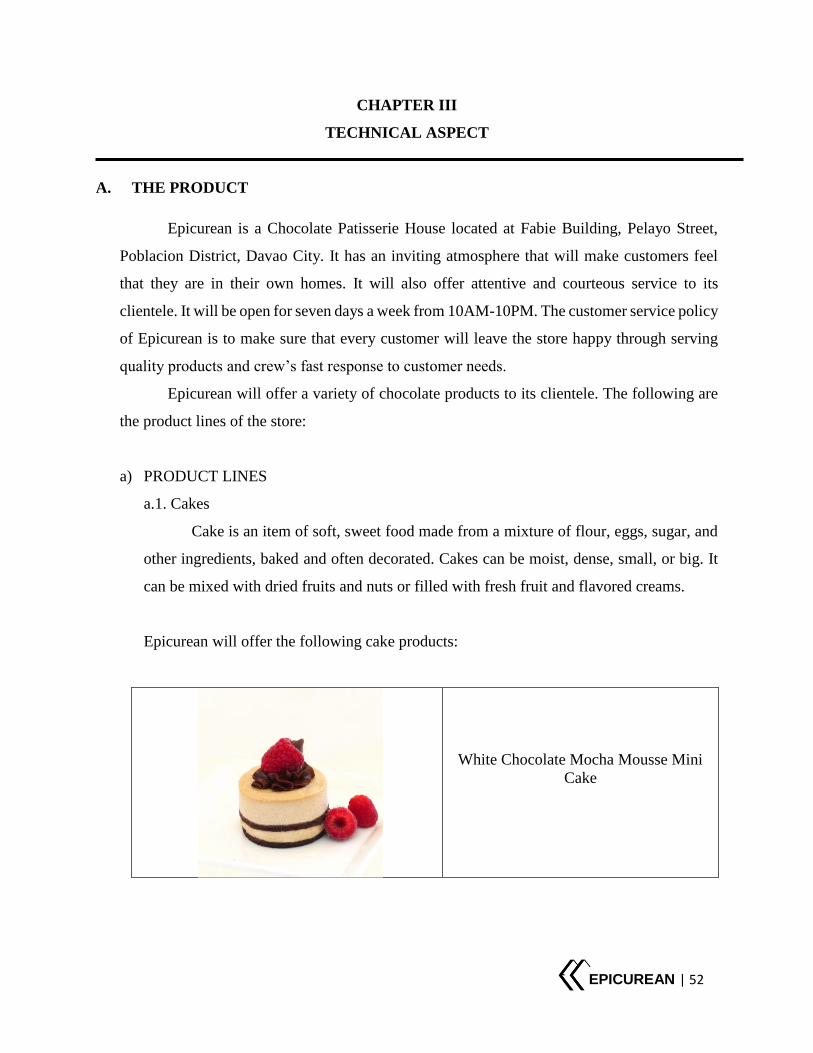

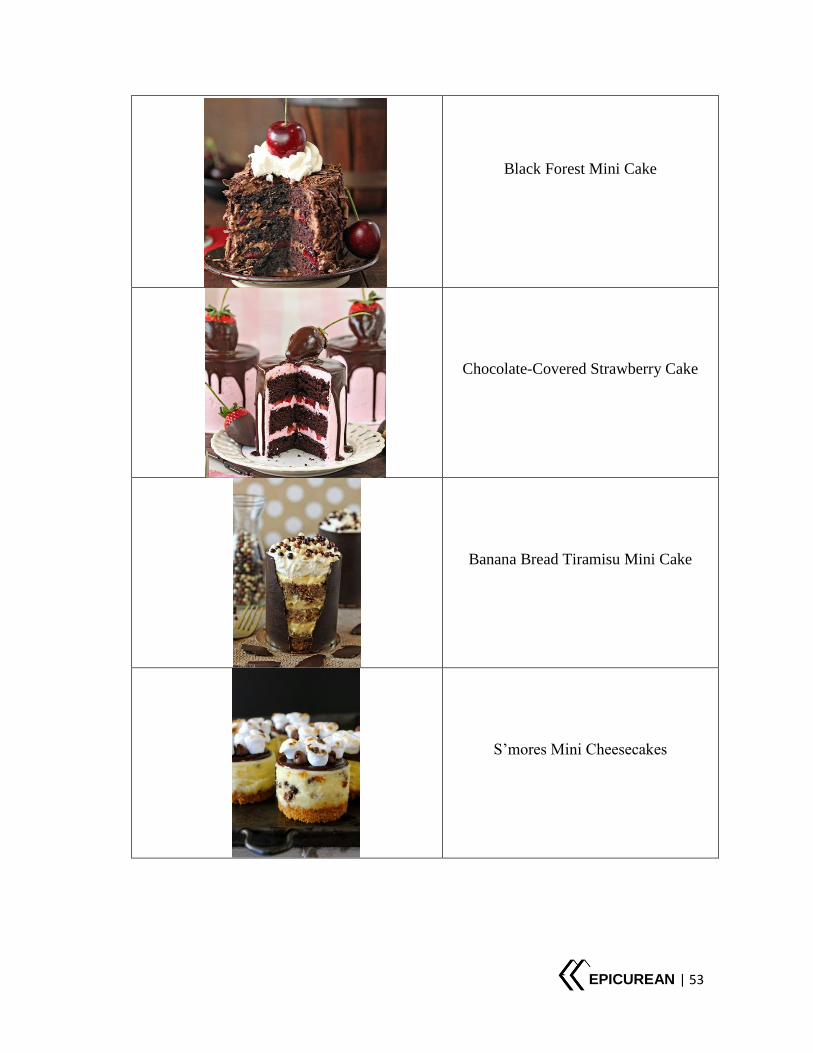

A. The Products ......................................................................................................................52

B. Production Process .............................................................................................................71

C. Production Scheme and Operations ...................................................................................76

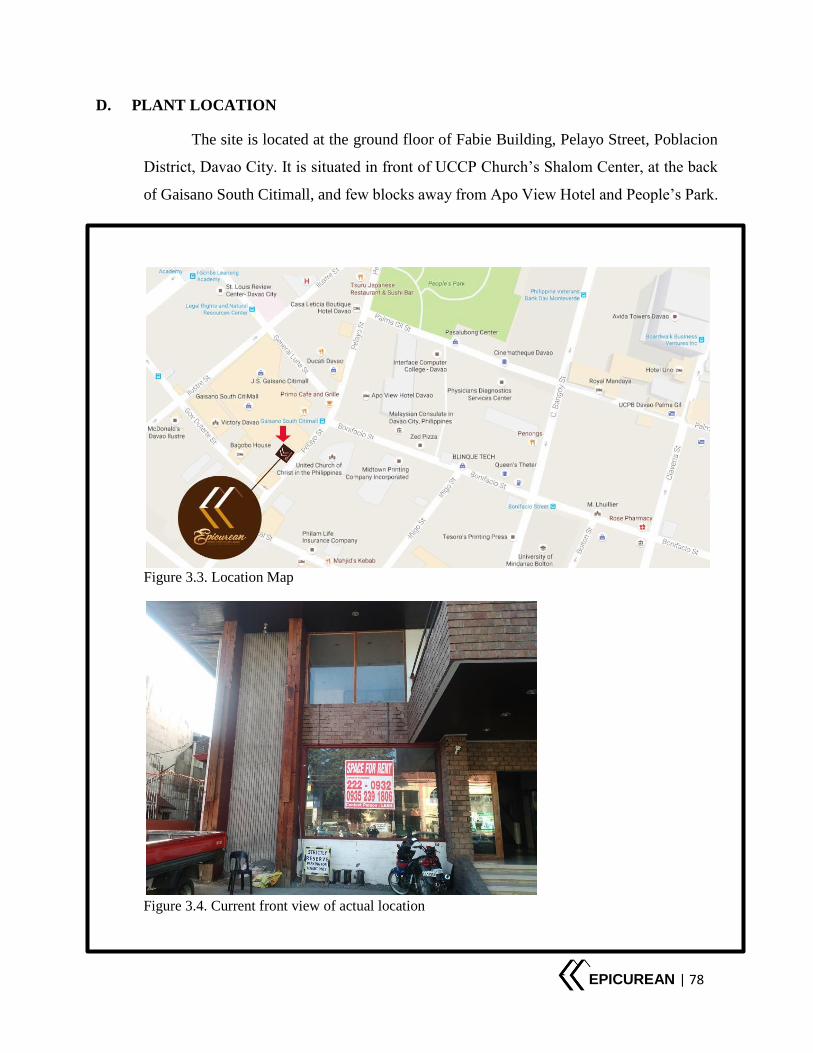

D. Plant Location ....................................................................................................................78

E. Establishment Layout.........................................................................................................80

F. Machinery and Equipment .................................................................................................83

G. Building and Facilities .......................................................................................................96

H. Raw Materials and Supplies.............................................................................................102

I. Utilities .............................................................................................................................110

J. Waste Disposal.................................................................................................................111

K. Labor Requirements .........................................................................................................112

L. Production Cost ................................................................................................................114

IV. Financial Aspect ................................................................................................................115

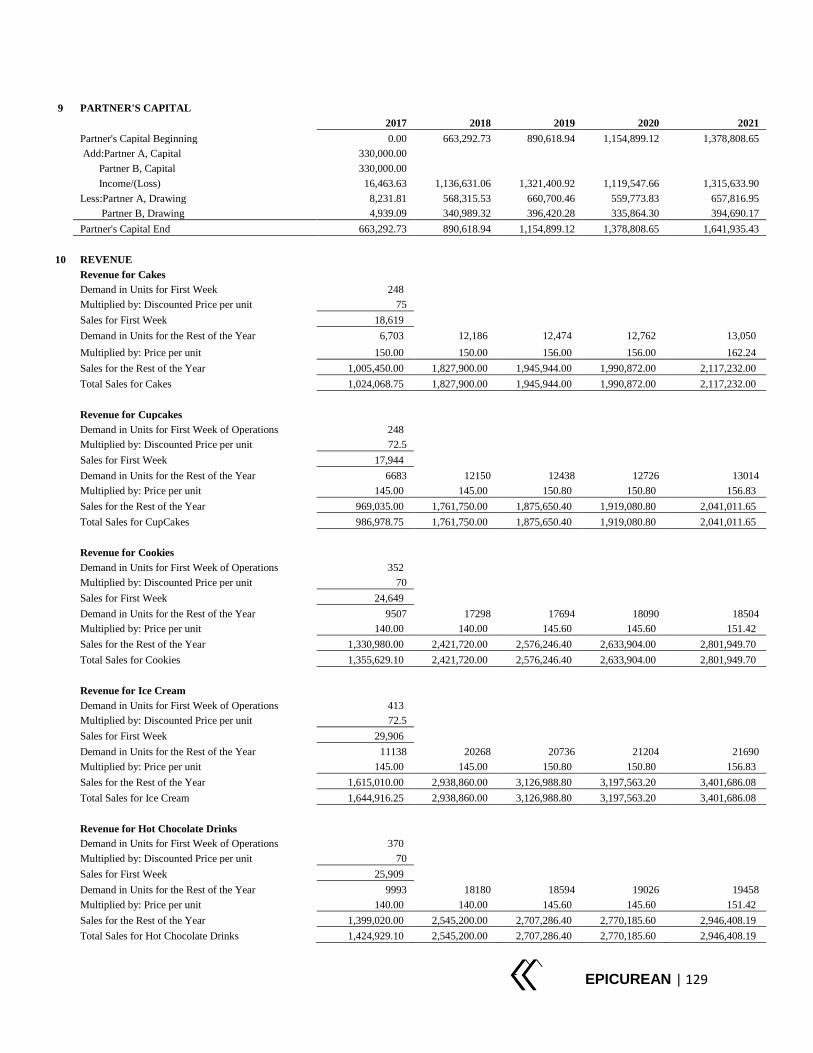

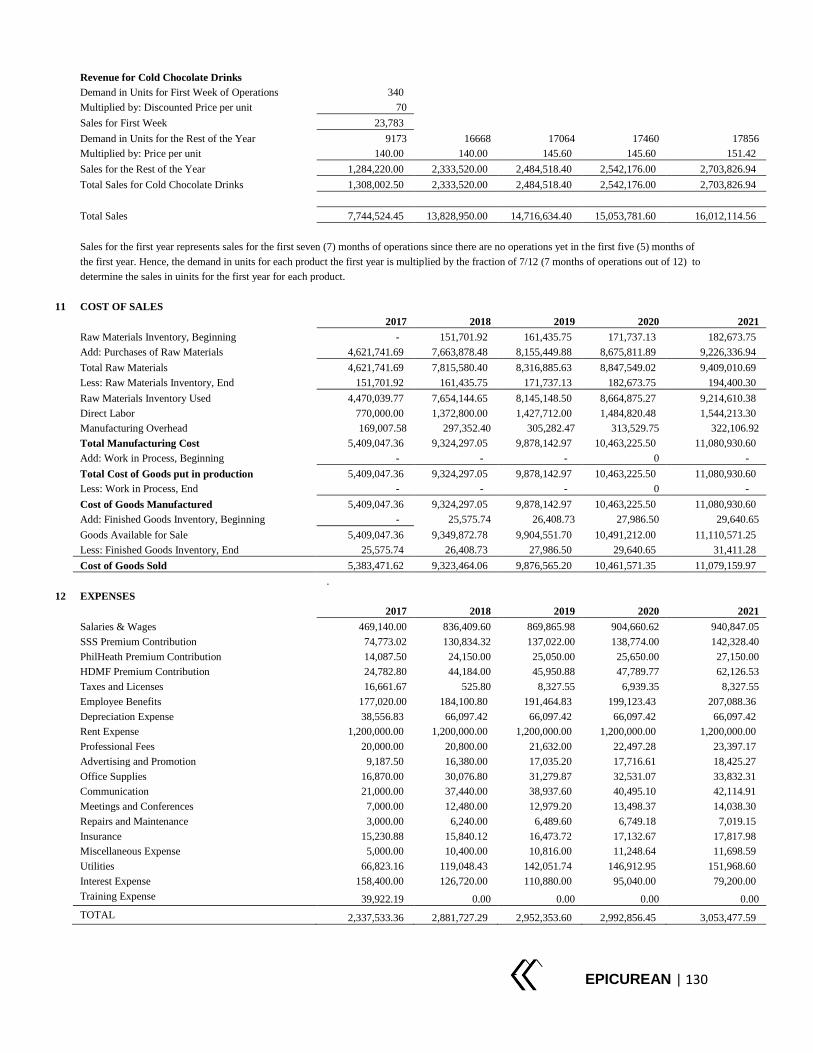

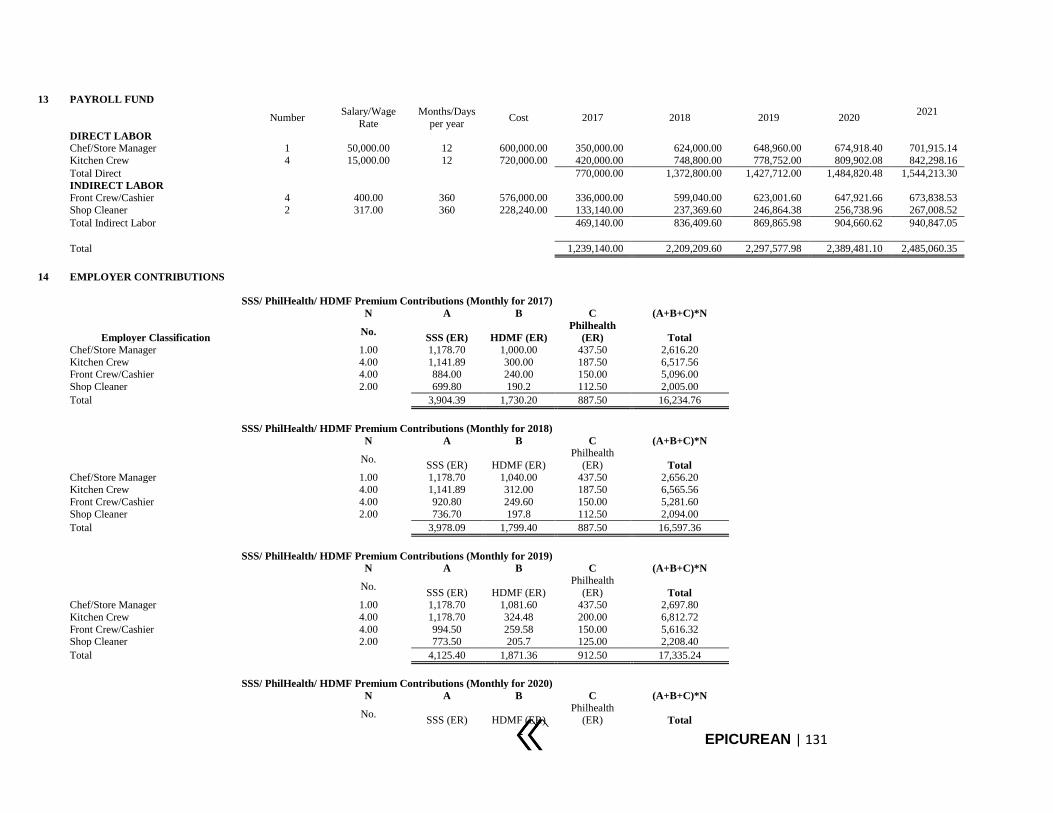

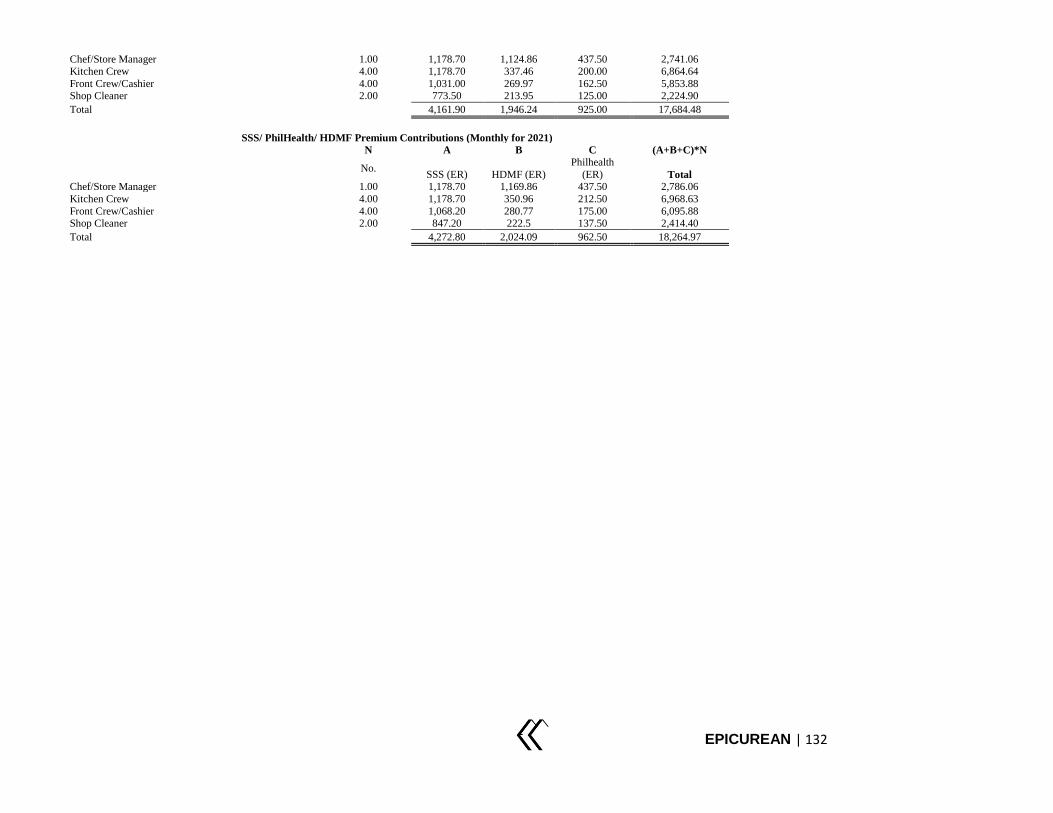

A. Major Assumptions used in the preparation of Financial Statements..............................115

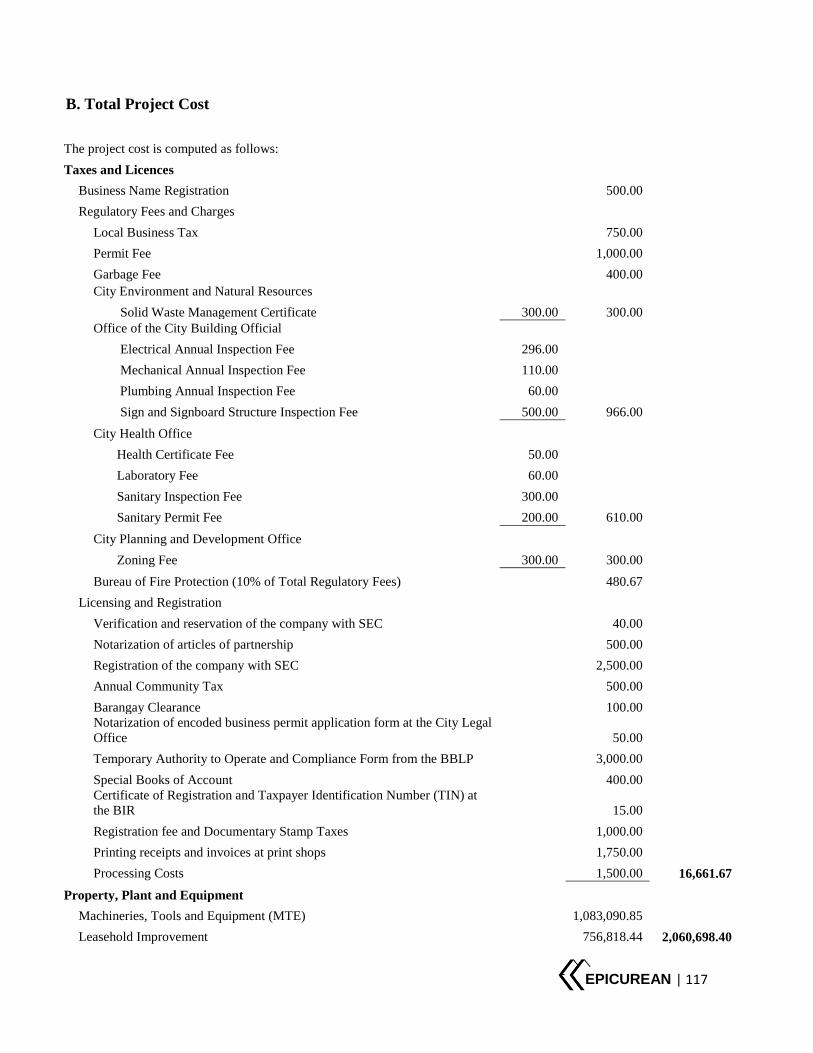

B. Total Project Cost ............................................................................................................117

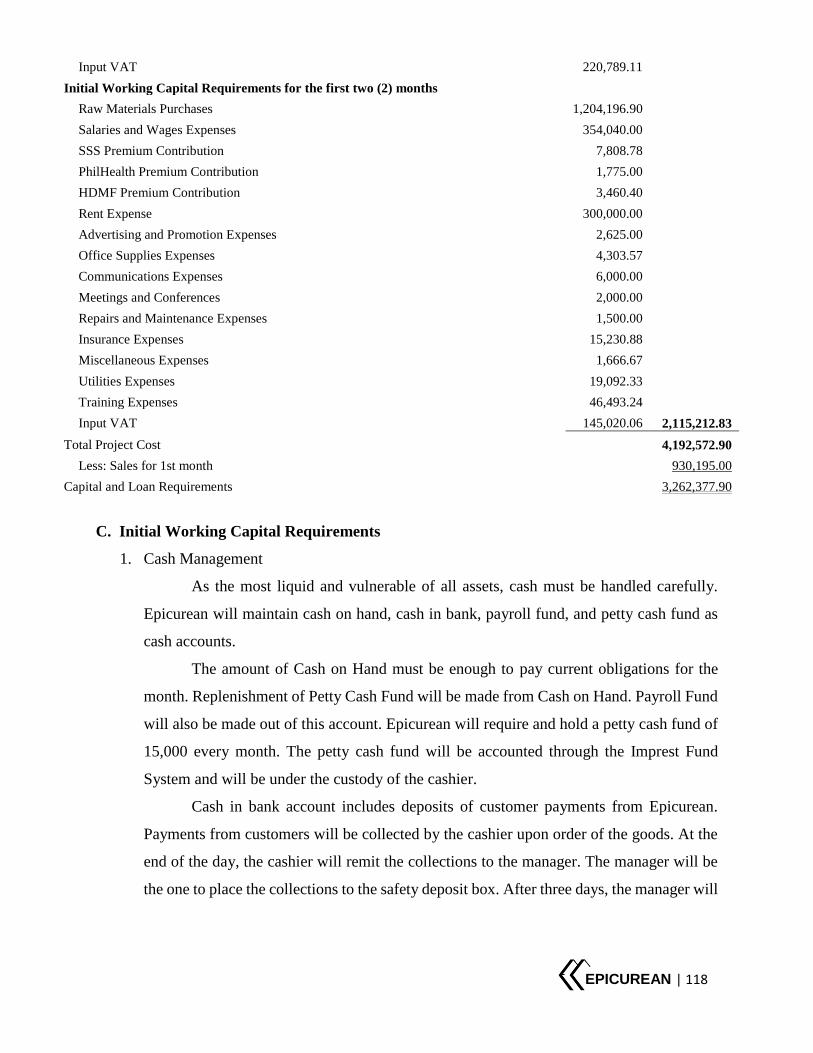

C. Initial Working Capital Requirements .............................................................................118

D. Alternative Sources of Financing.....................................................................................119

E. Sources of Financing the Project .....................................................................................120

F. Pro-Forma Financial Statements ......................................................................................122

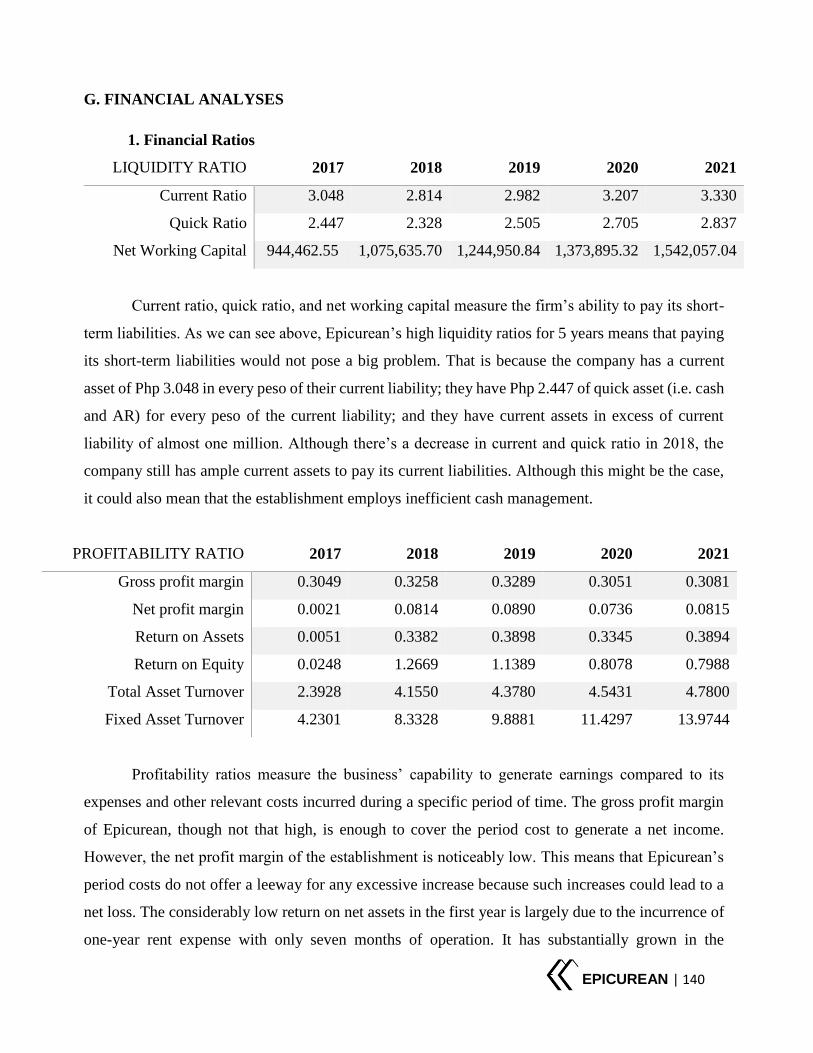

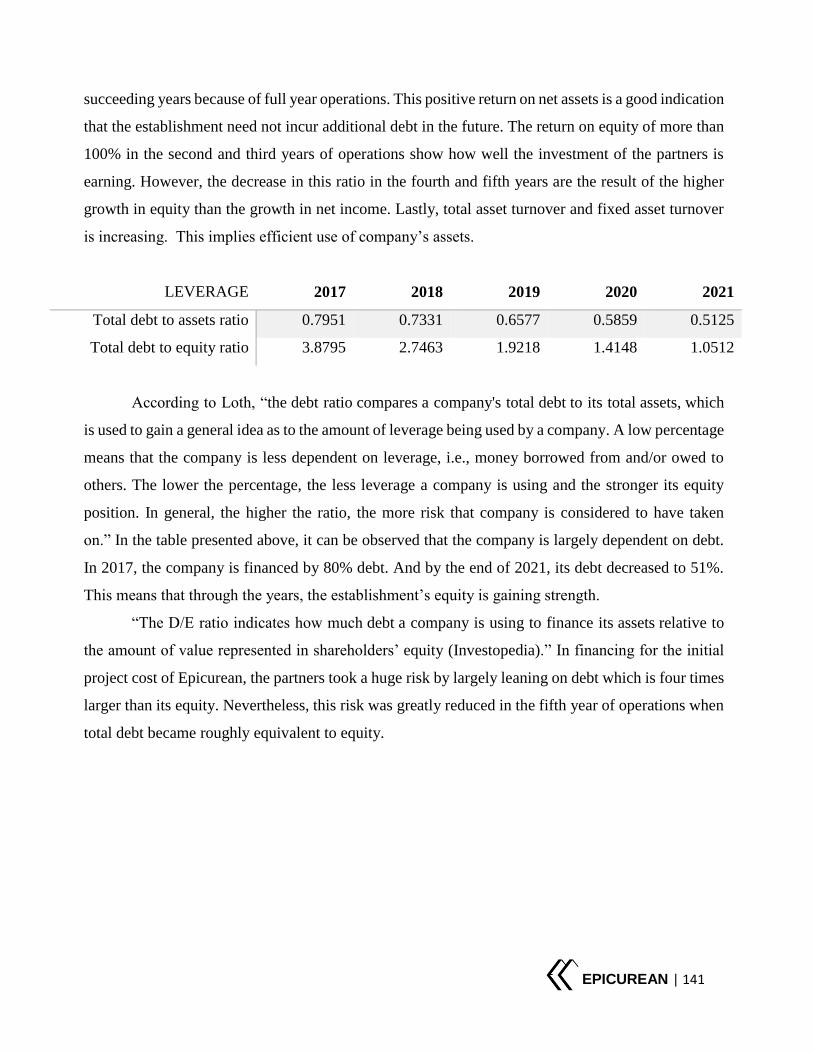

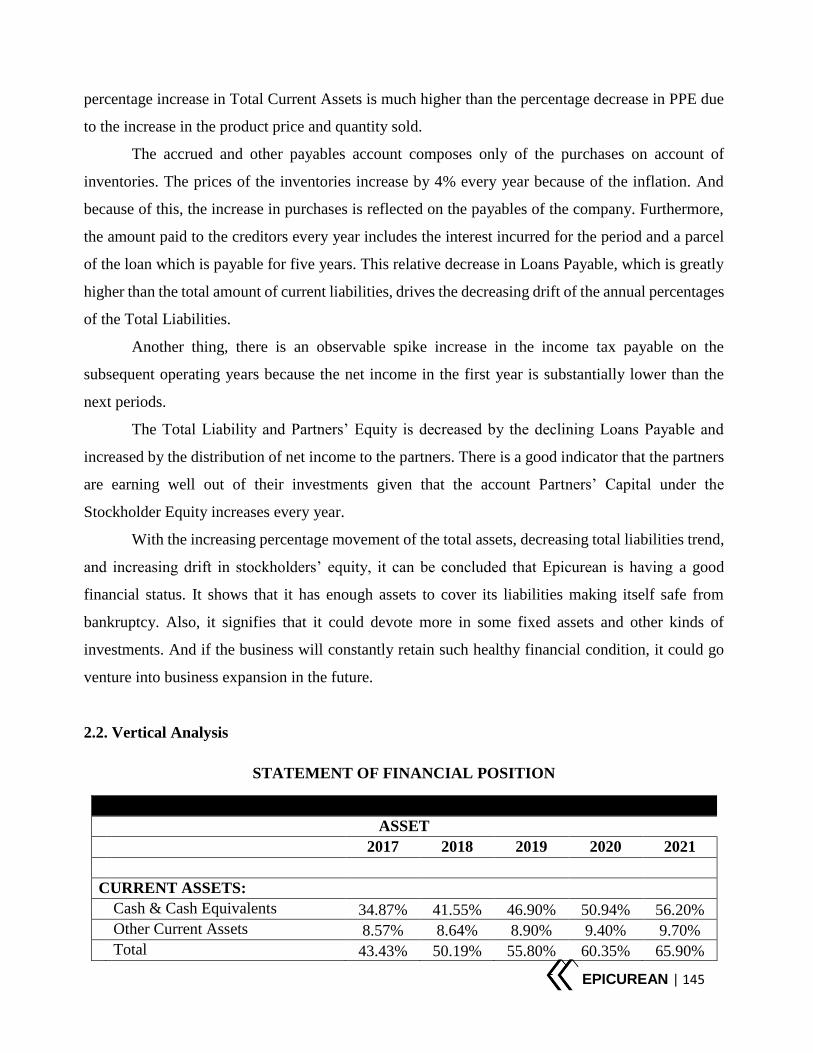

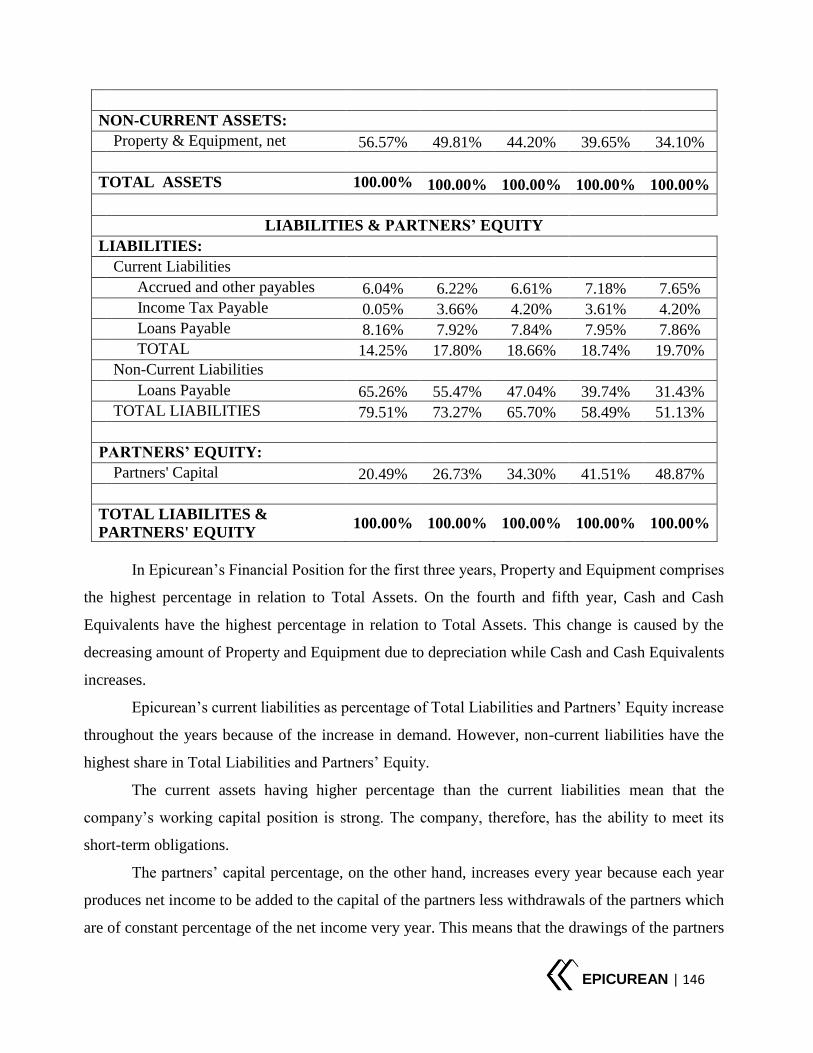

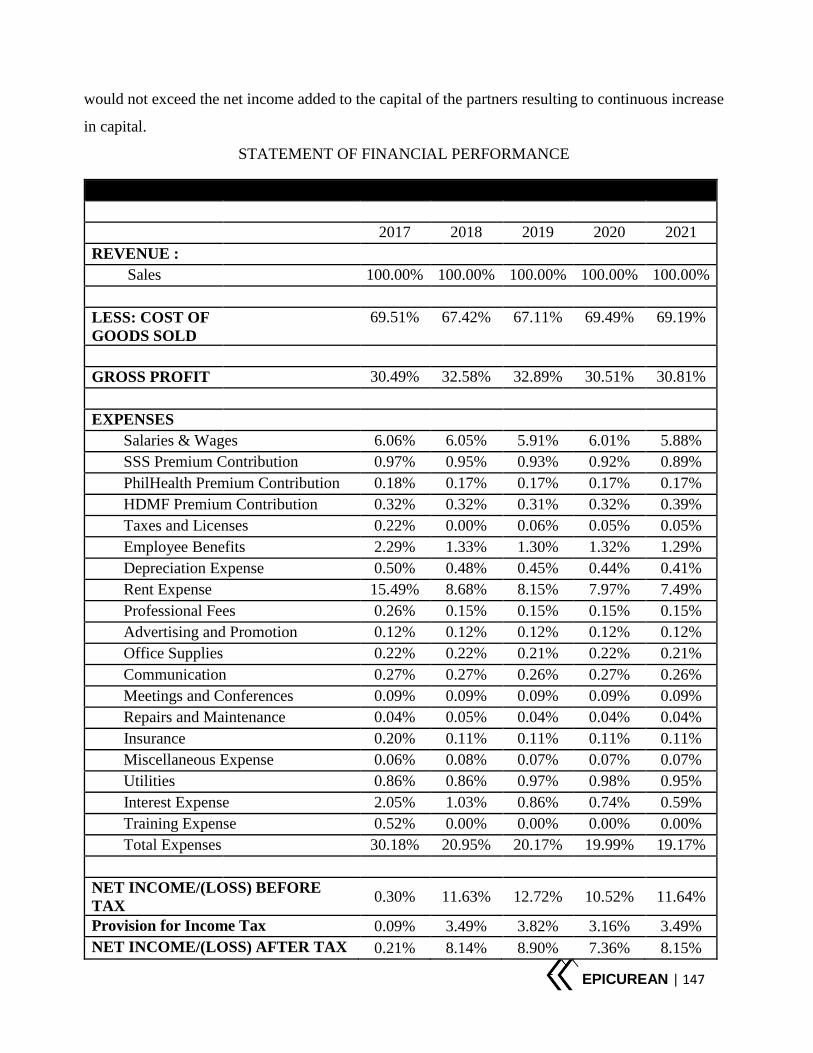

G. Financial Analyses ...........................................................................................................140

a. Financial Ratios .........................................................................................................140

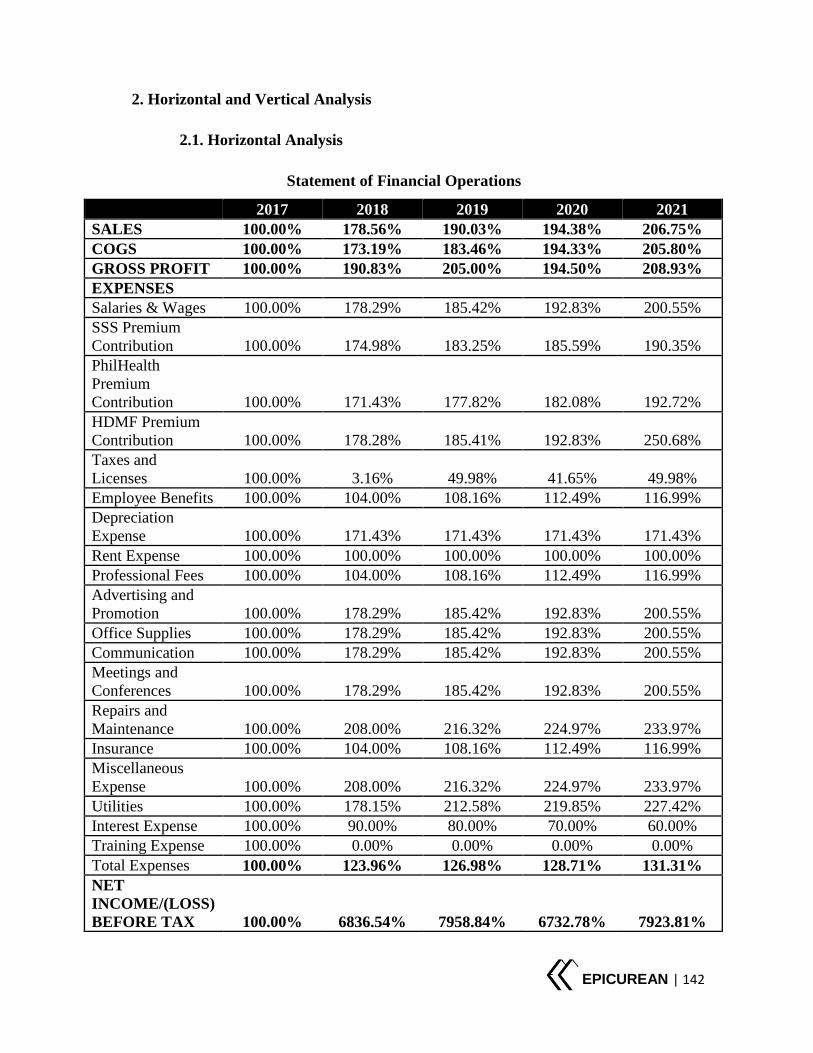

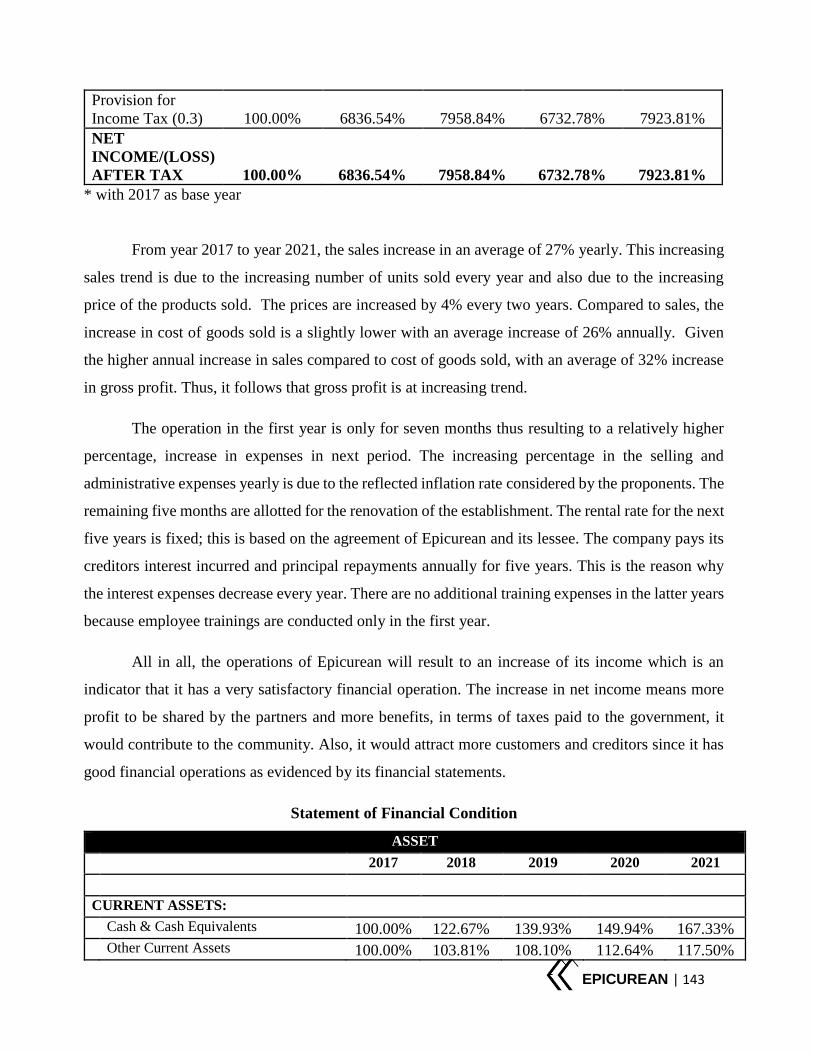

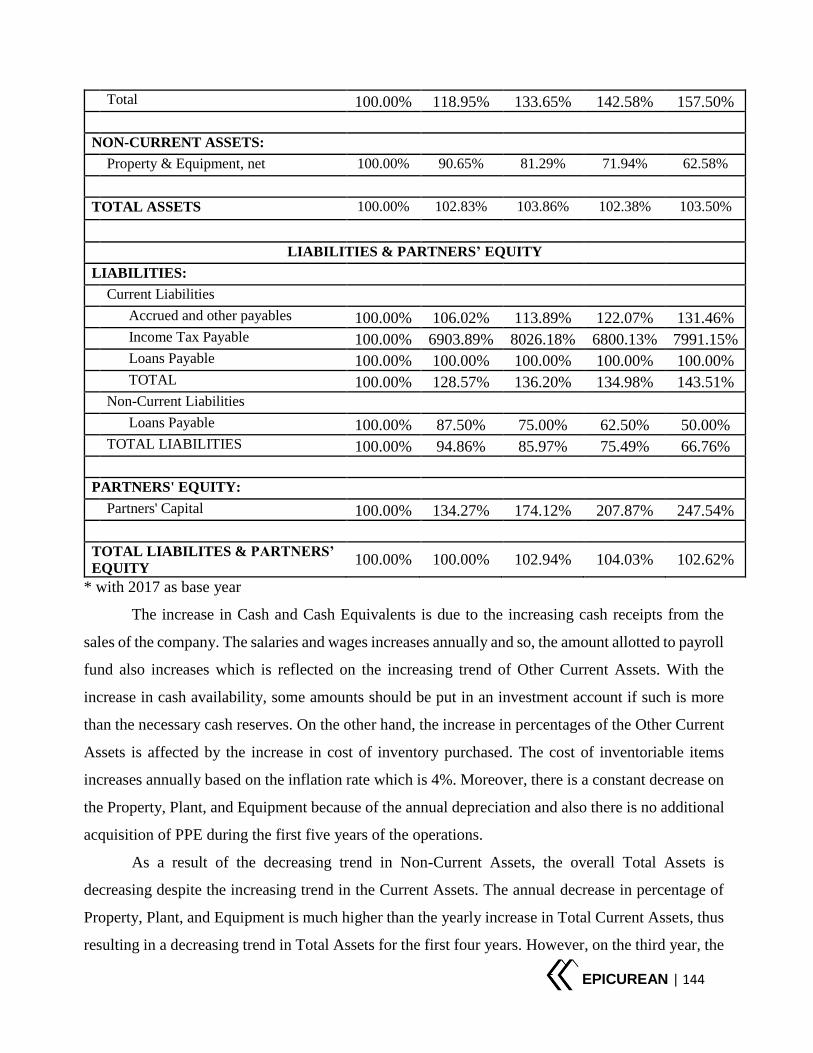

b. Horizontal and Vertical Analyses ..............................................................................142

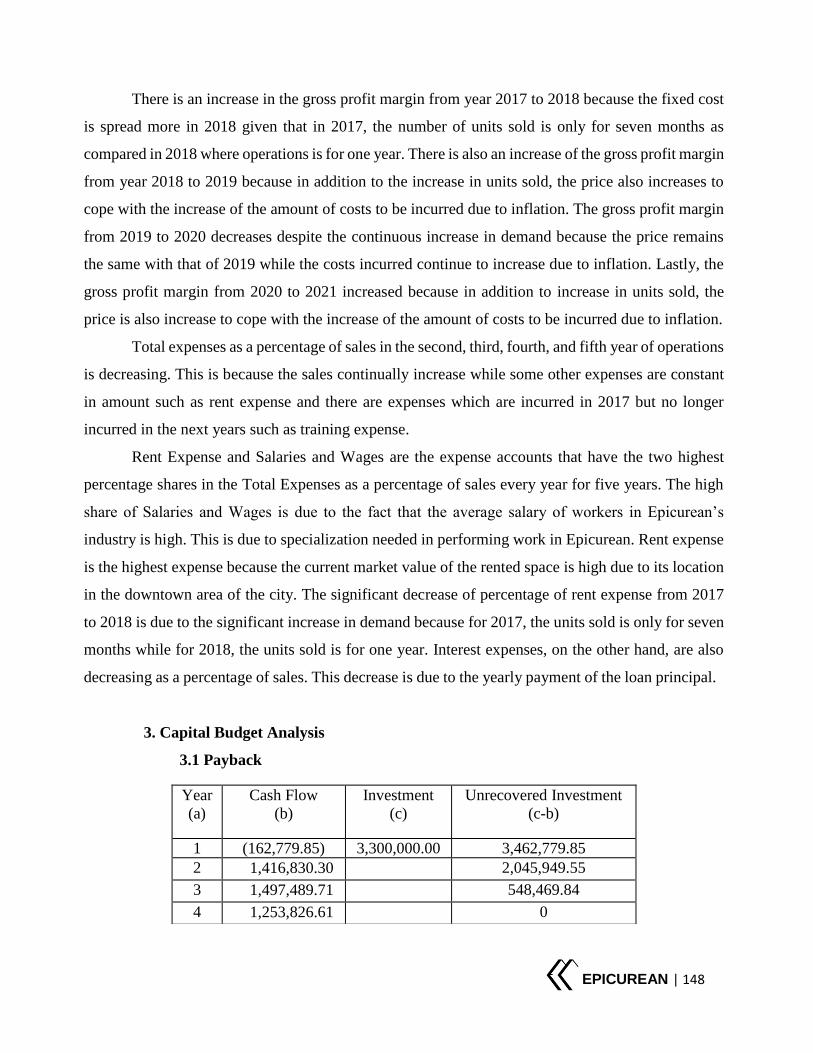

c. Capital Budget Analysis ............................................................................................148

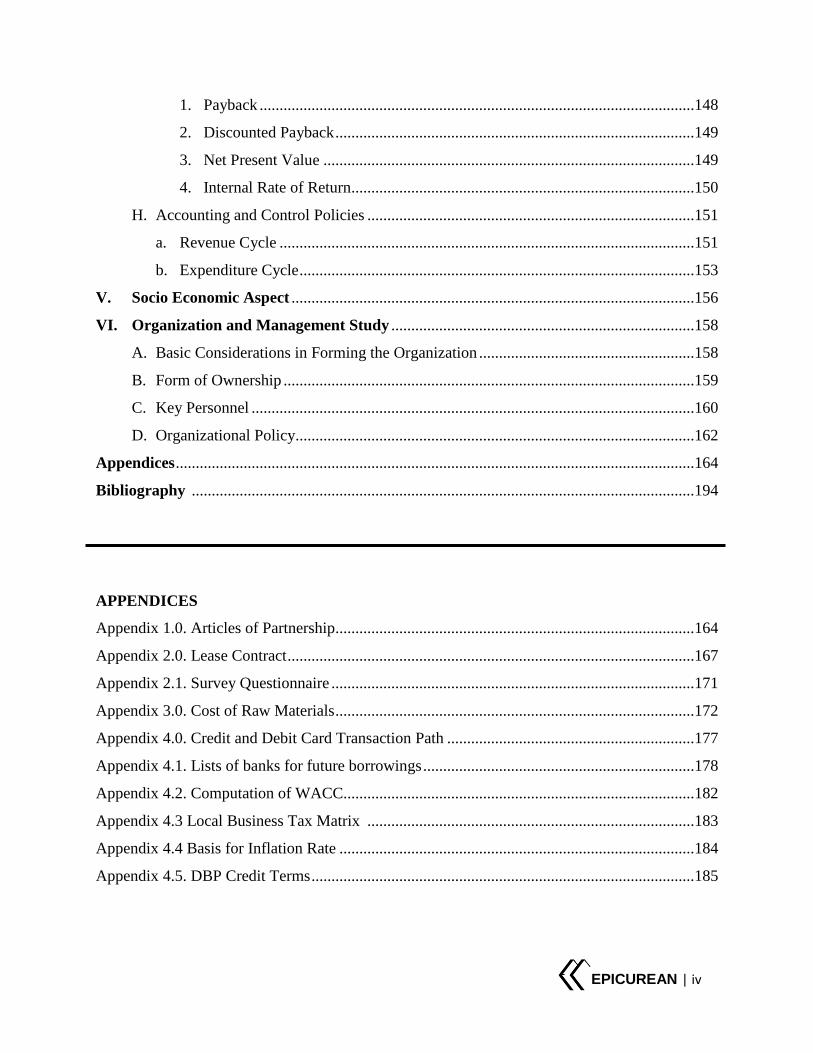

EPICUREAN | iv

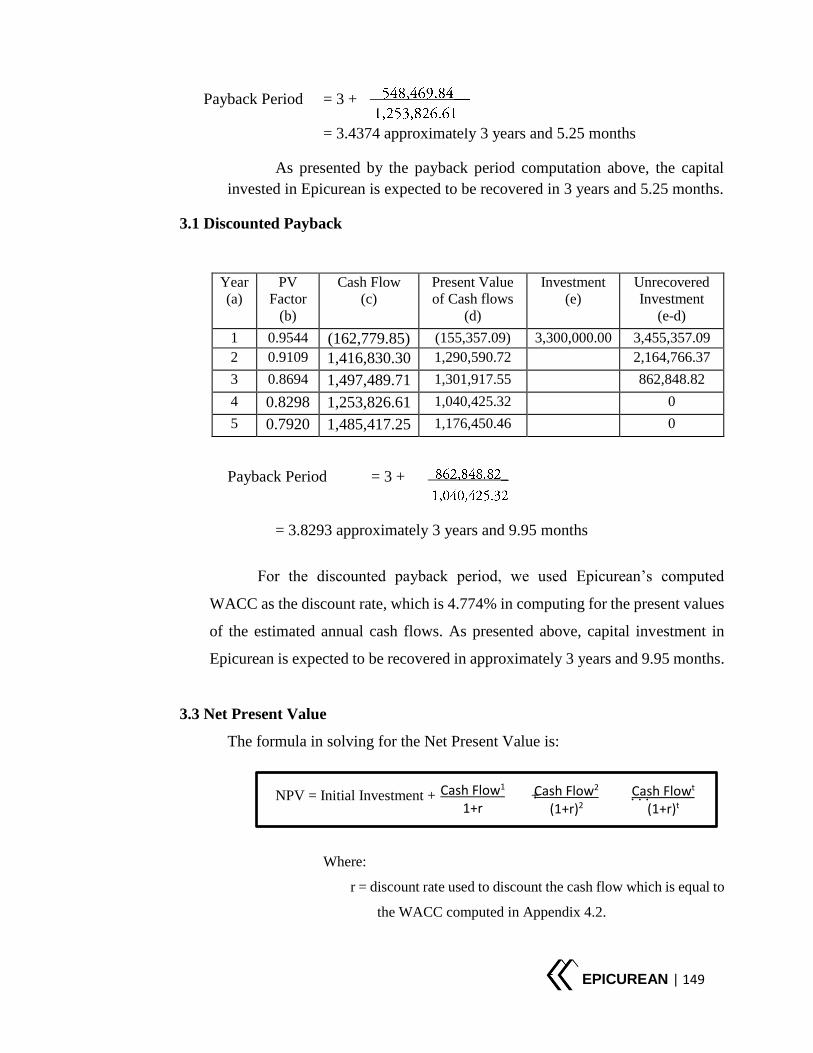

1. Payback .............................................................................................................148

2. Discounted Payback ..........................................................................................149

3. Net Present Value .............................................................................................149

4. Internal Rate of Return......................................................................................150

H. Accounting and Control Policies ..................................................................................151

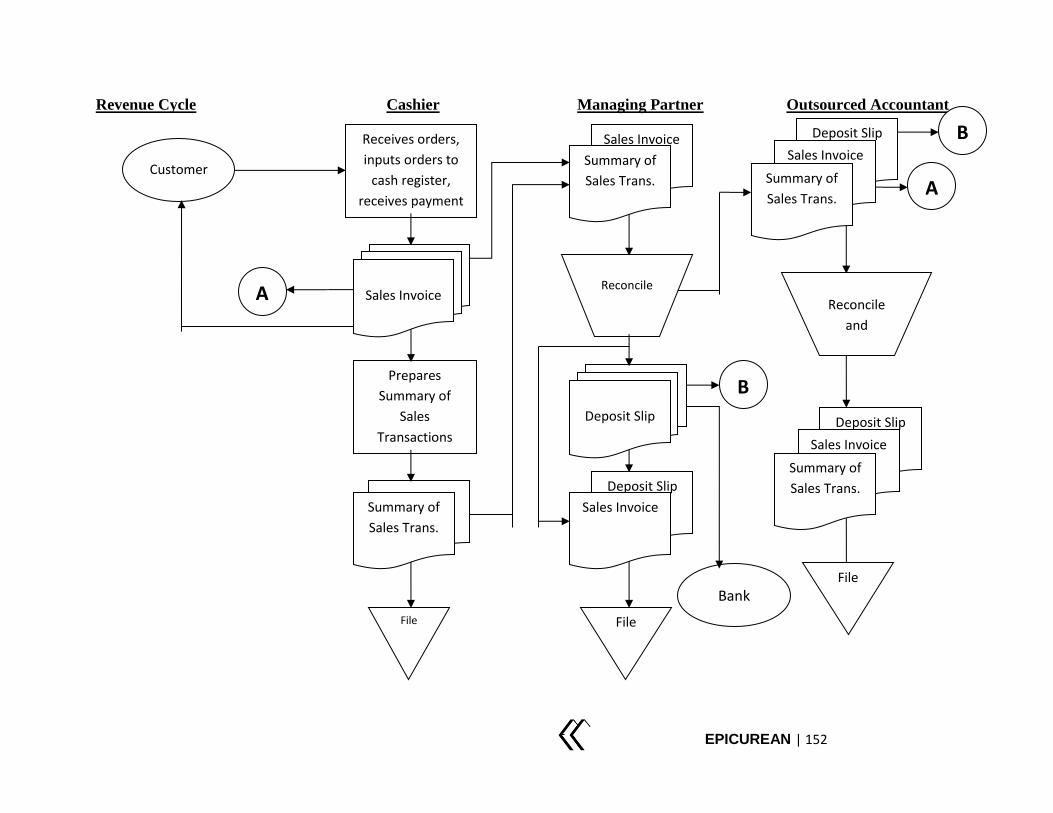

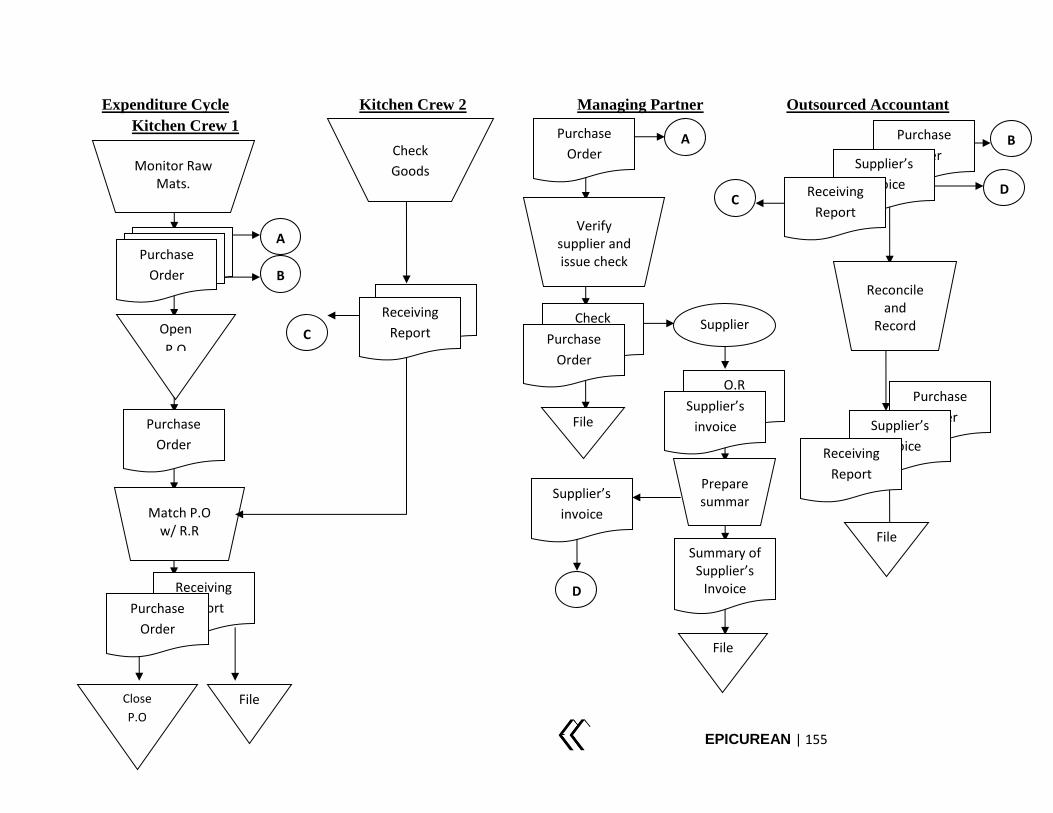

a. Revenue Cycle ........................................................................................................151

b. Expenditure Cycle ...................................................................................................153

V. Socio Economic Aspect .....................................................................................................156

VI. Organization and Management Study ............................................................................158

A. Basic Considerations in Forming the Organization ......................................................158

B. Form of Ownership .......................................................................................................159

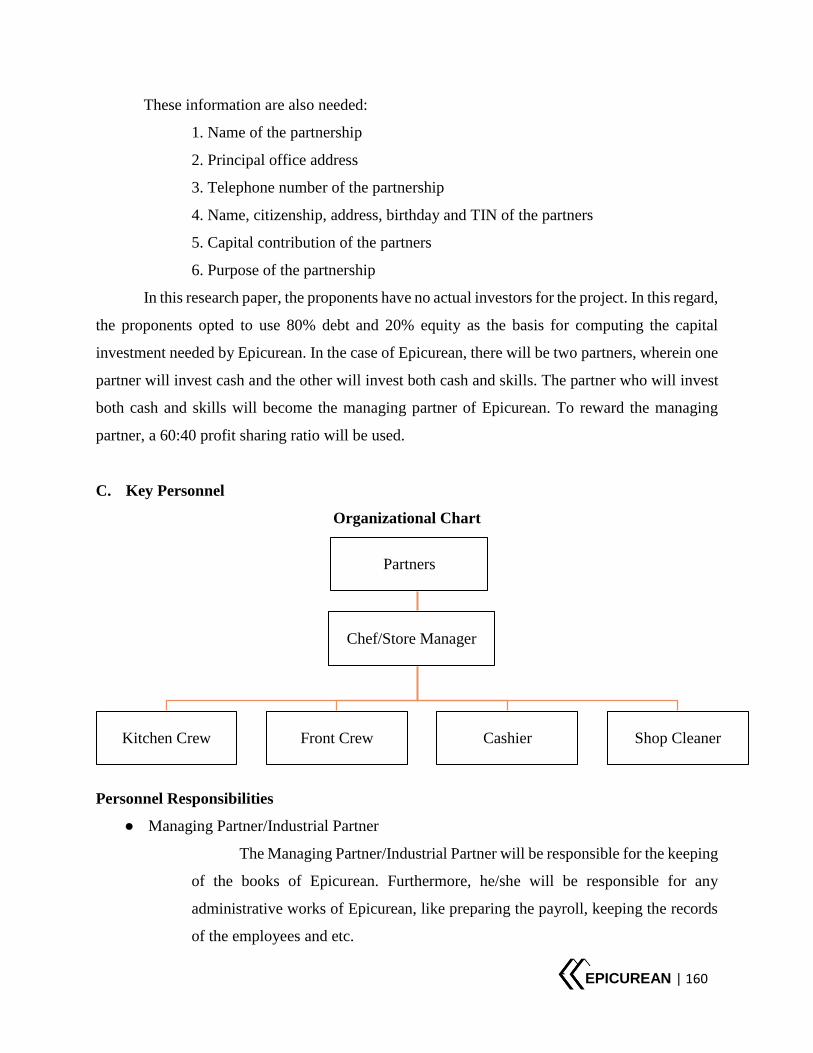

C. Key Personnel ...............................................................................................................160

D. Organizational Policy....................................................................................................162

Appendices ..................................................................................................................................164

Bibliography ..............................................................................................................................194

APPENDICES

Appendix 1.0. Articles of Partnership..........................................................................................164

Appendix 2.0. Lease Contract ......................................................................................................167

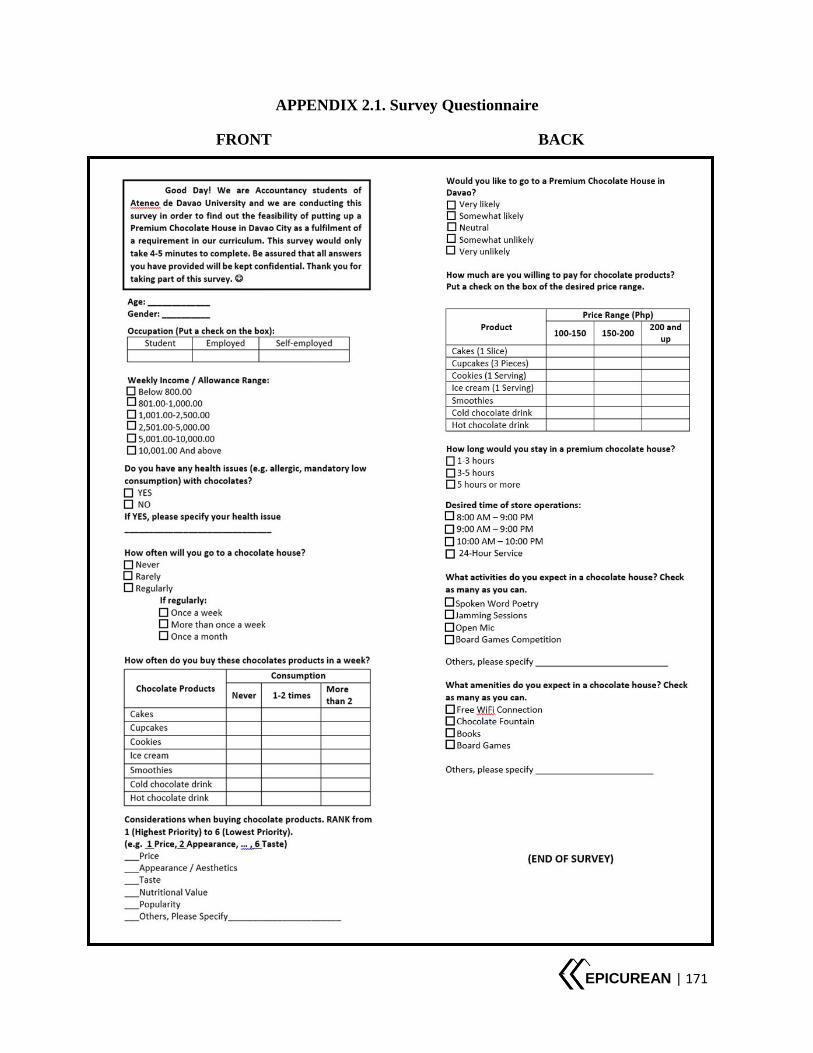

Appendix 2.1. Survey Questionnaire ...........................................................................................171

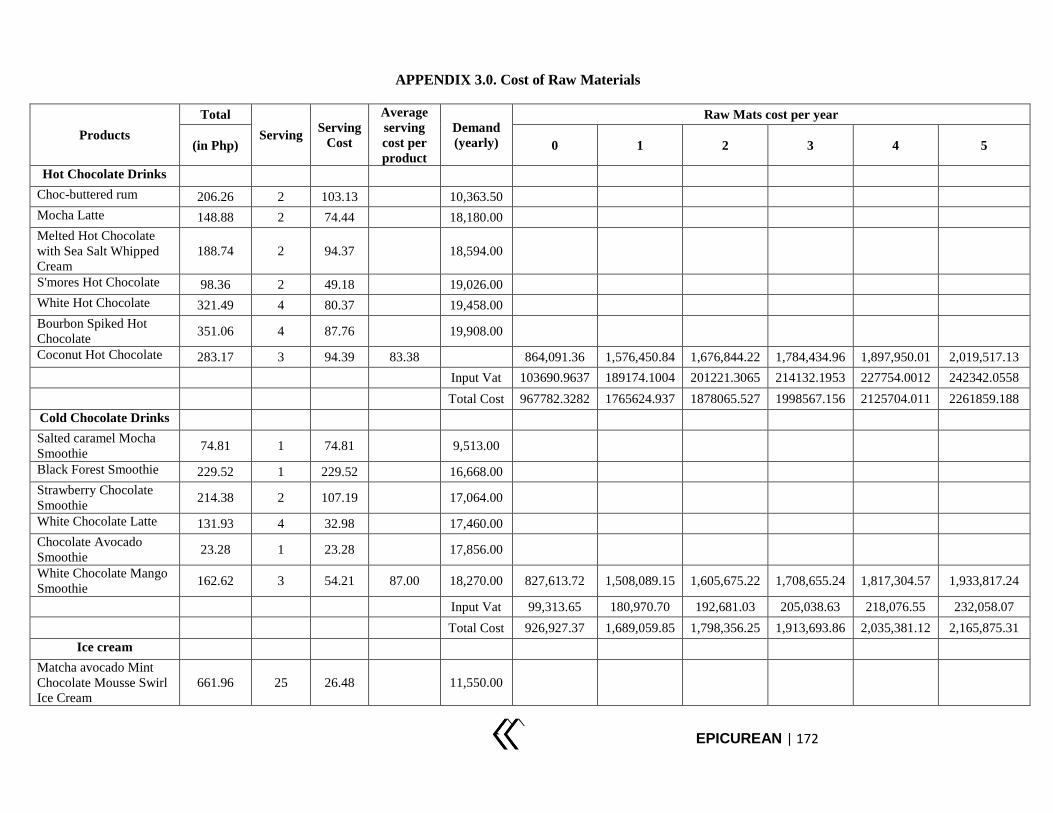

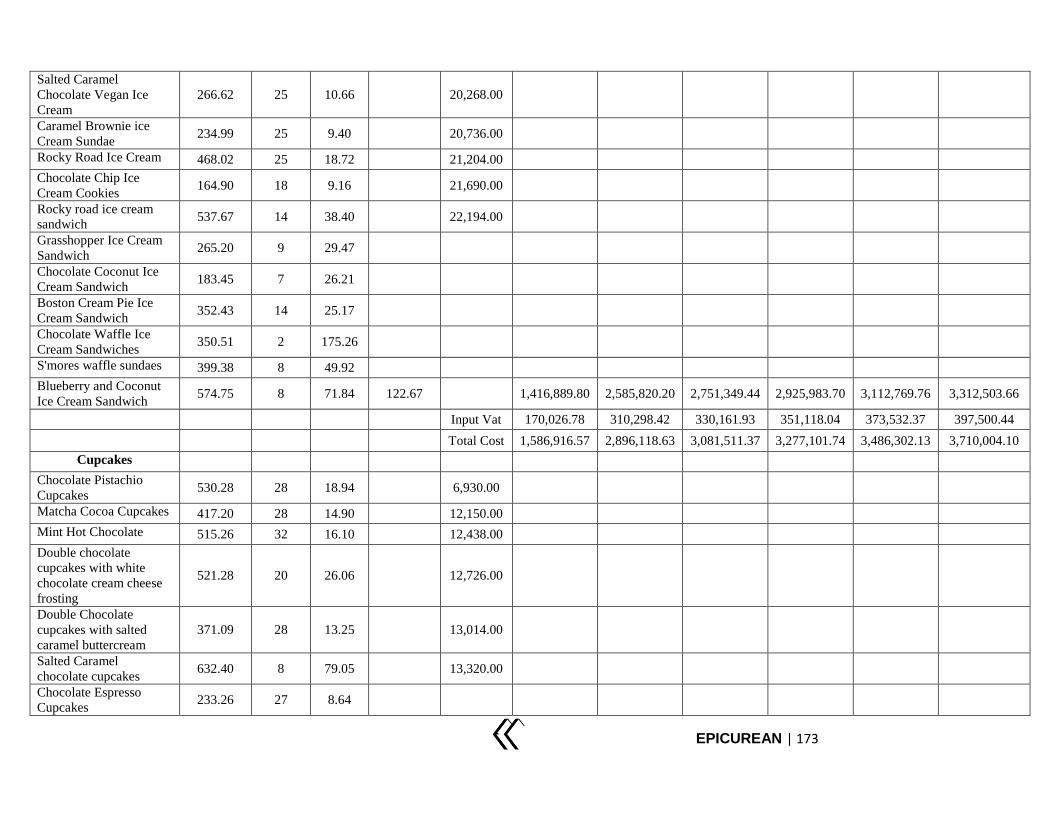

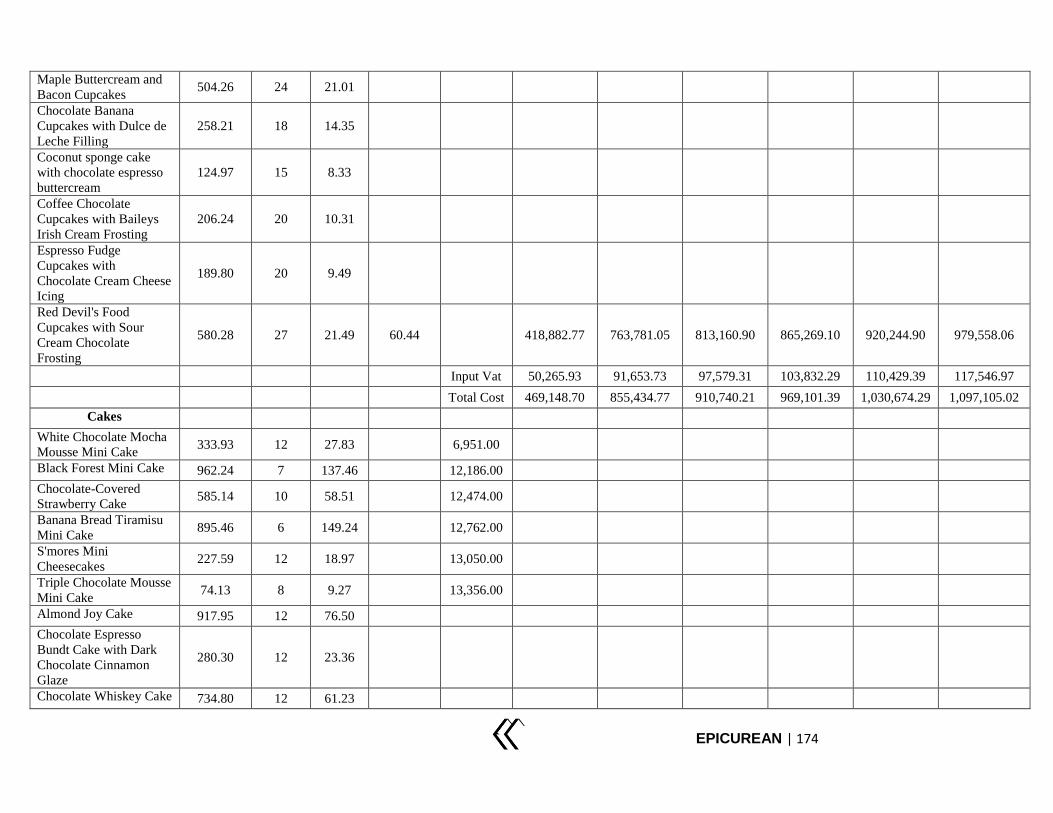

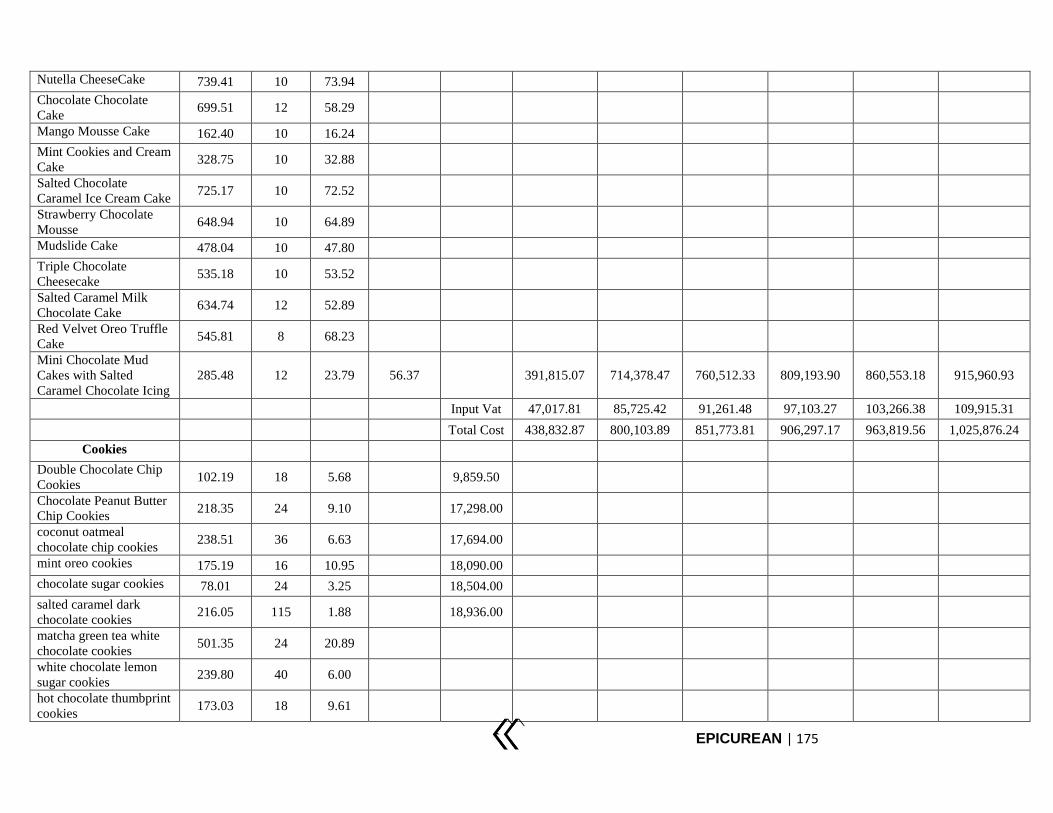

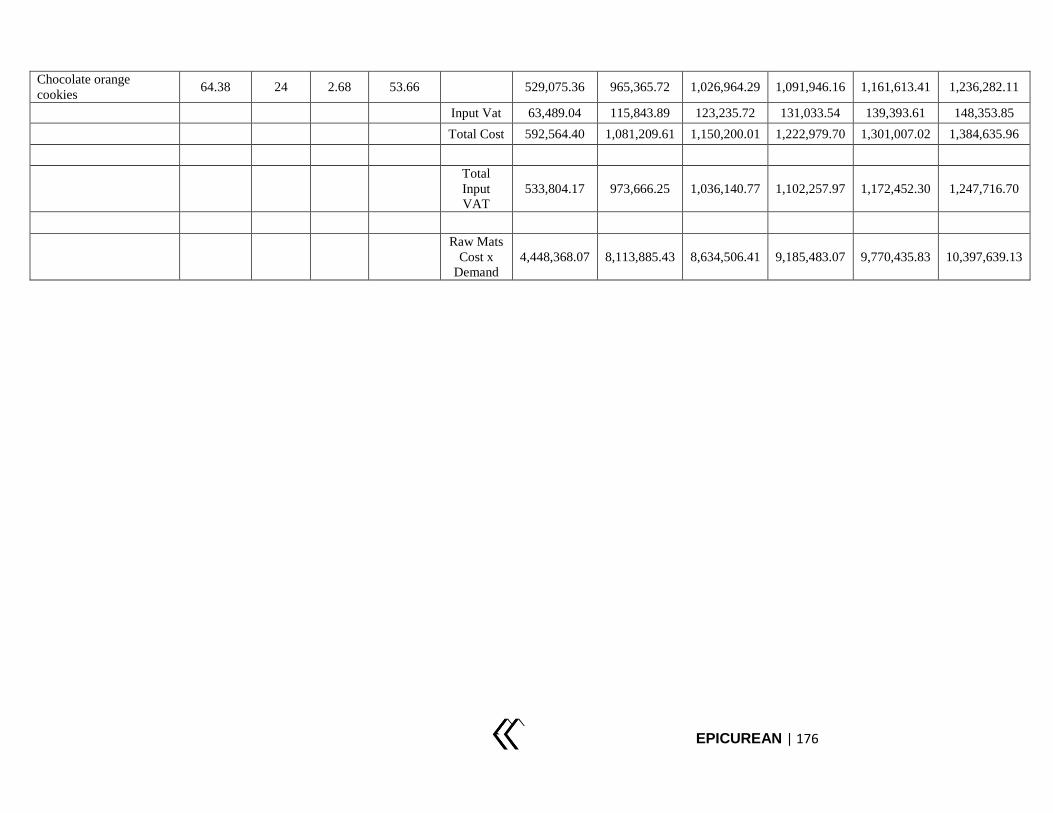

Appendix 3.0. Cost of Raw Materials ..........................................................................................172

Appendix 4.0. Credit and Debit Card Transaction Path ..............................................................177

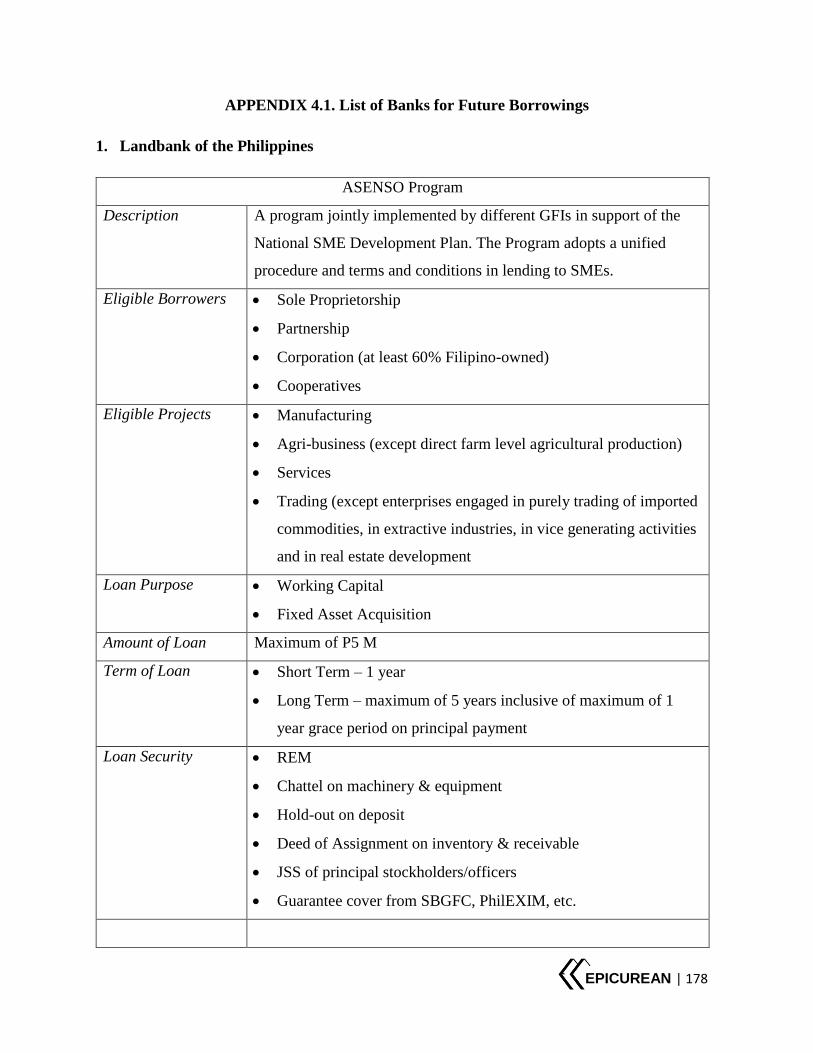

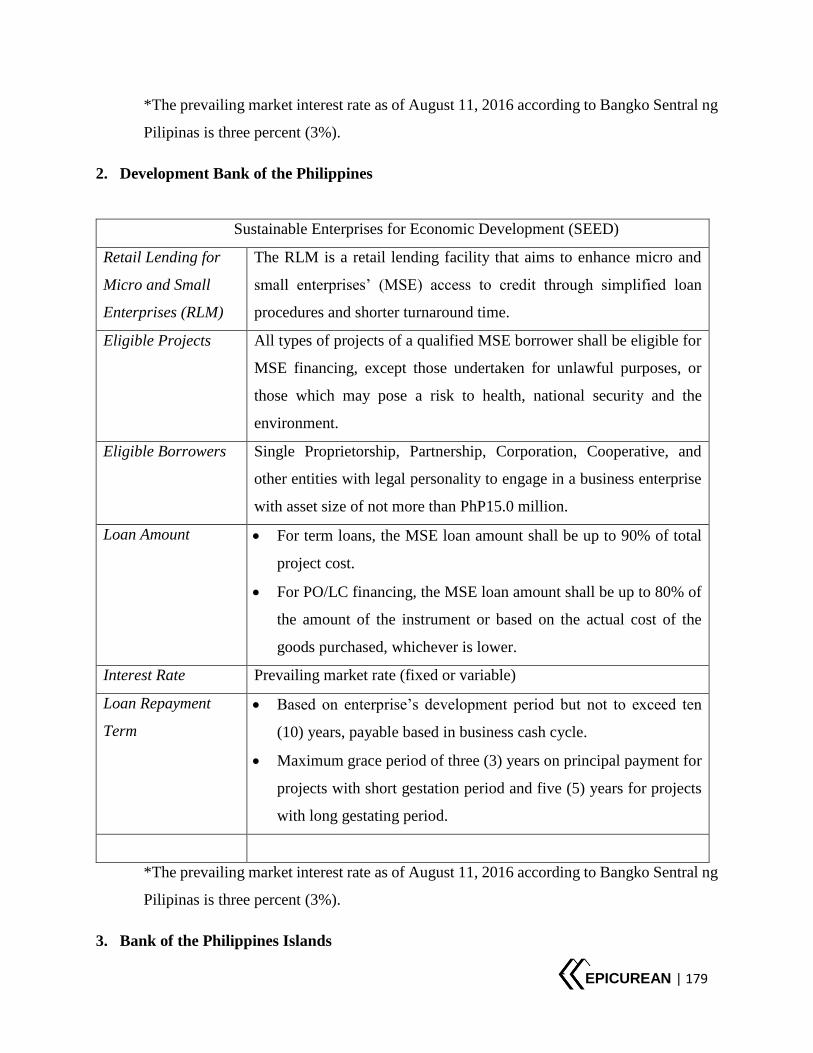

Appendix 4.1. Lists of banks for future borrowings ....................................................................178

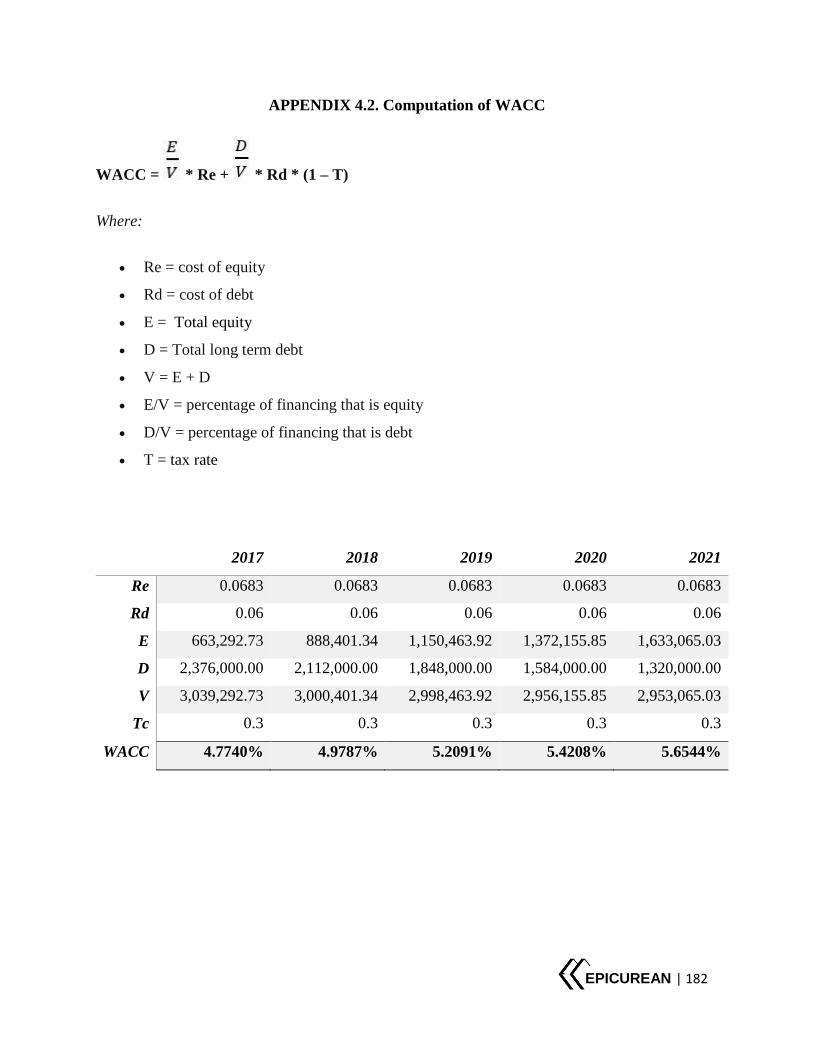

Appendix 4.2. Computation of WACC........................................................................................182

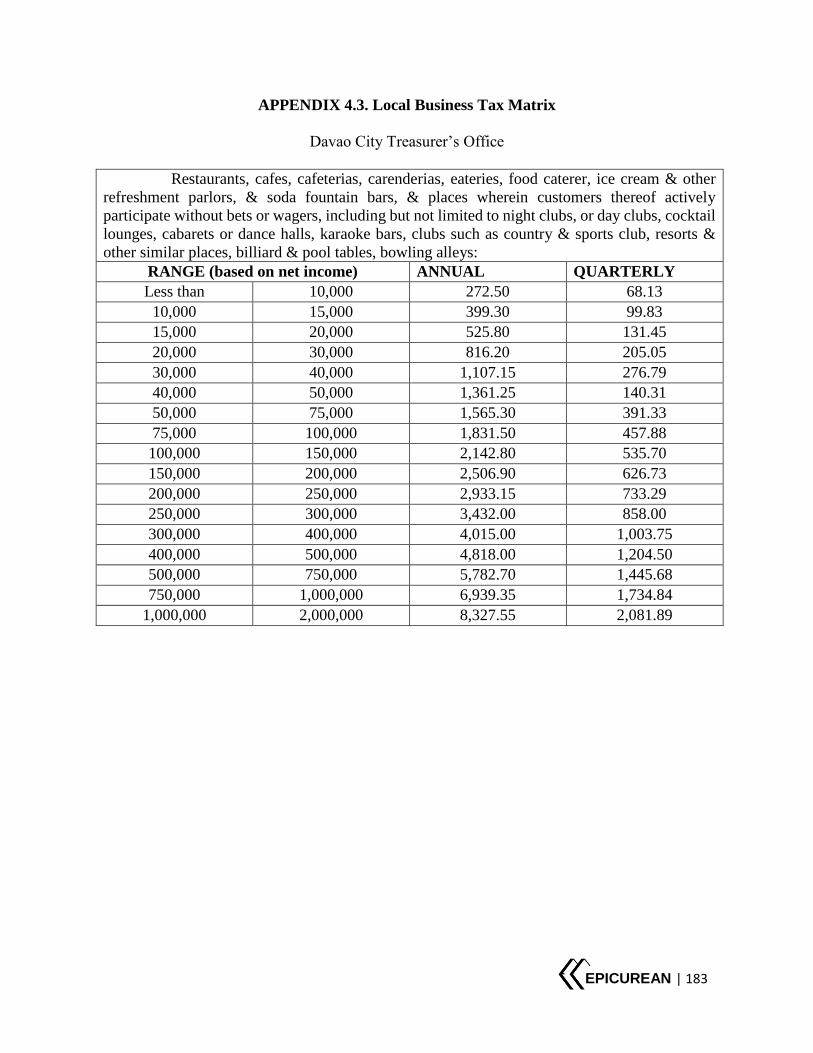

Appendix 4.3 Local Business Tax Matrix ..................................................................................183

Appendix 4.4 Basis for Inflation Rate .........................................................................................184

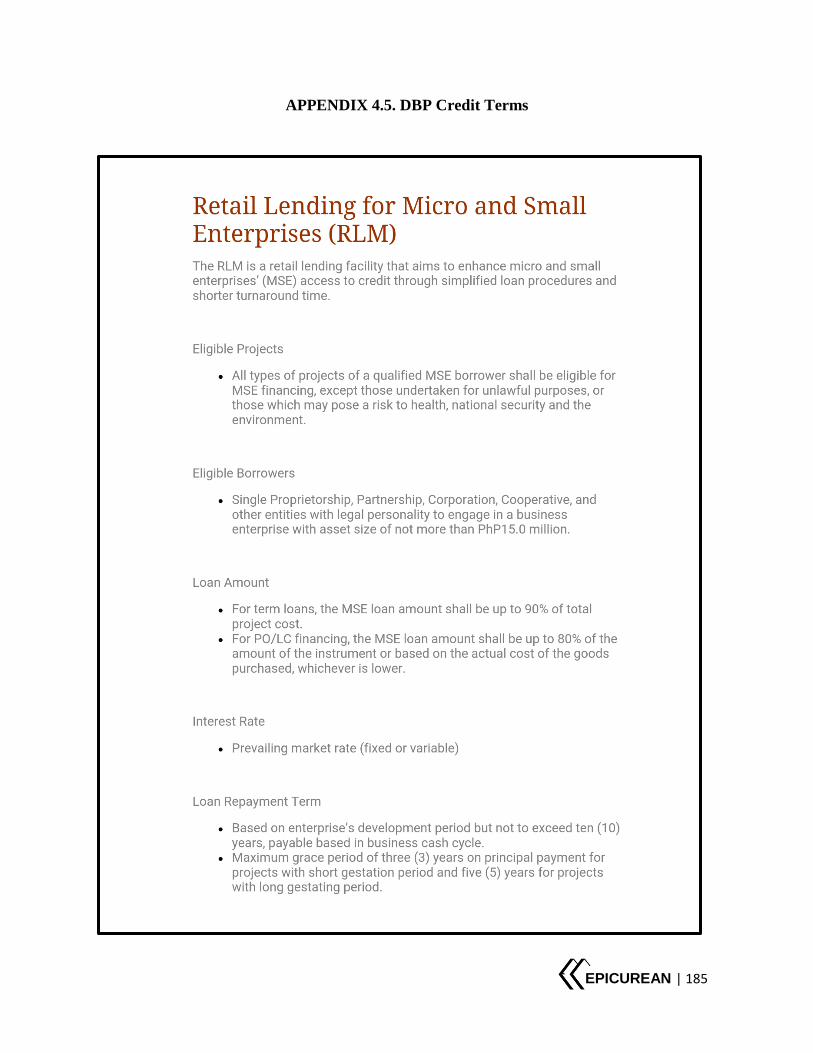

Appendix 4.5. DBP Credit Terms ................................................................................................185

EPICUREAN | v

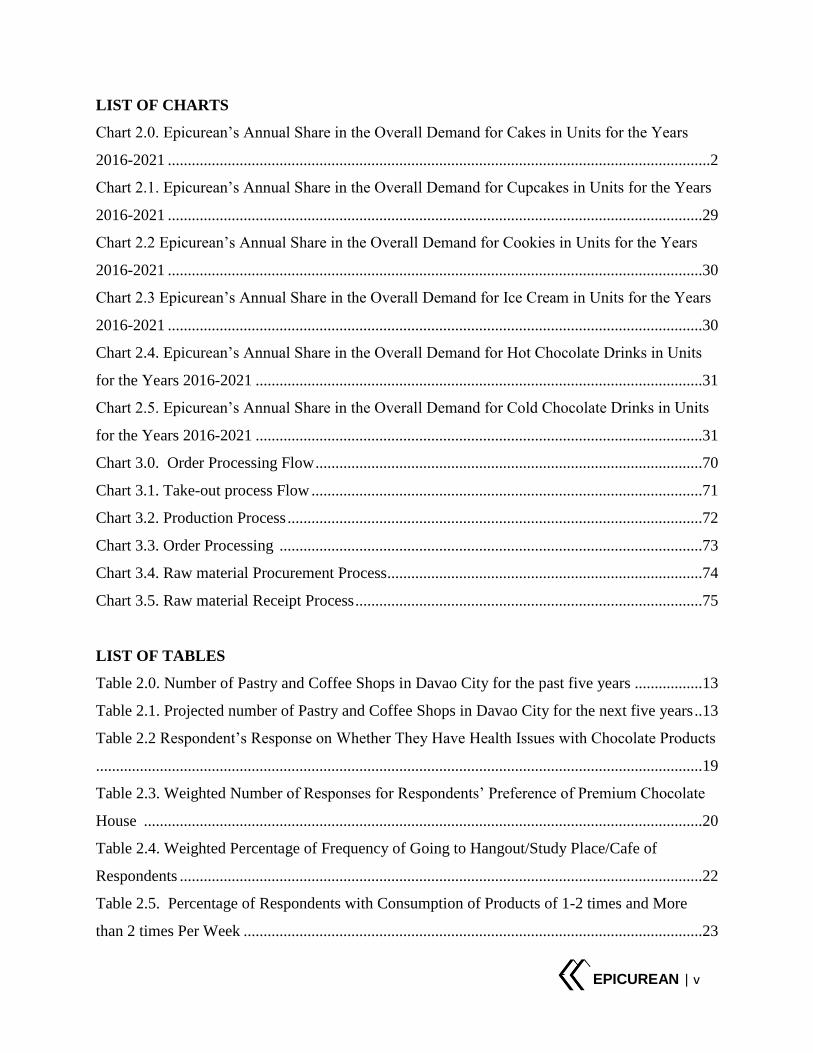

LIST OF CHARTS

Chart 2.0. Epicurean’s Annual Share in the Overall Demand for Cakes in Units for the Years

2016-2021 ........................................................................................................................................2

Chart 2.1. Epicurean’s Annual Share in the Overall Demand for Cupcakes in Units for the Years

2016-2021 ......................................................................................................................................29

Chart 2.2 Epicurean’s Annual Share in the Overall Demand for Cookies in Units for the Years

2016-2021 ......................................................................................................................................30

Chart 2.3 Epicurean’s Annual Share in the Overall Demand for Ice Cream in Units for the Years

2016-2021 ......................................................................................................................................30

Chart 2.4. Epicurean’s Annual Share in the Overall Demand for Hot Chocolate Drinks in Units

for the Years 2016-2021 ................................................................................................................31

Chart 2.5. Epicurean’s Annual Share in the Overall Demand for Cold Chocolate Drinks in Units

for the Years 2016-2021 ................................................................................................................31

Chart 3.0. Order Processing Flow .................................................................................................70

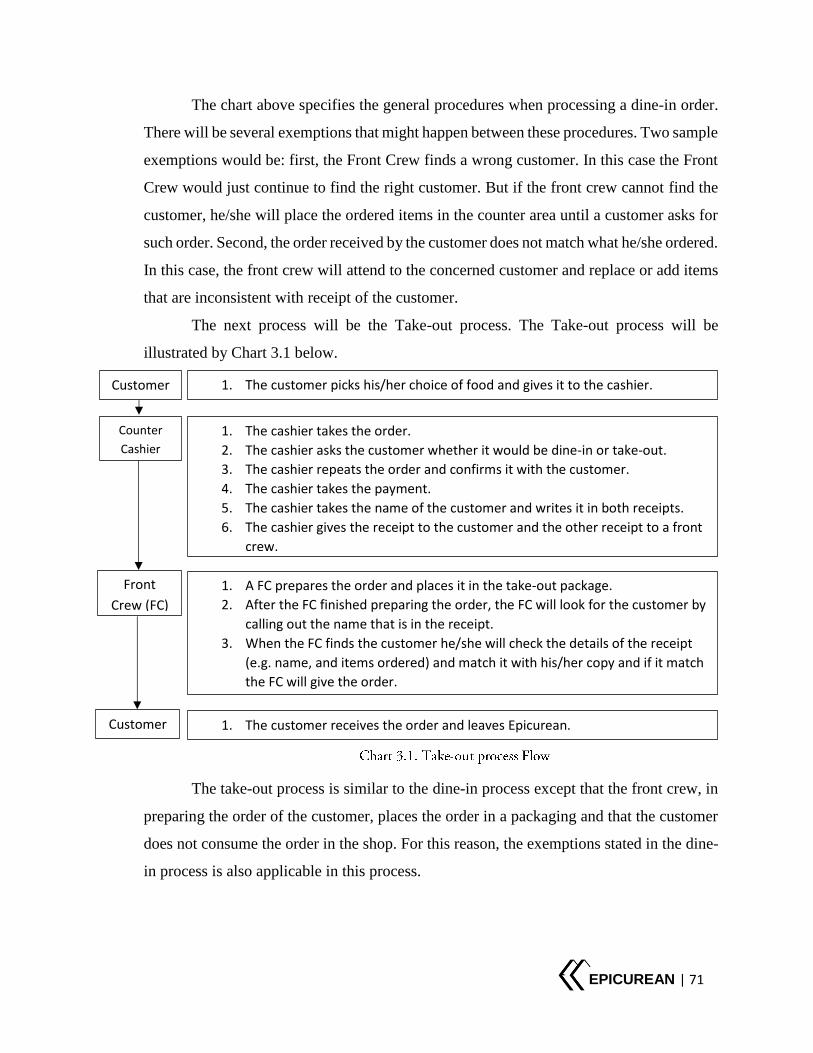

Chart 3.1. Take-out process Flow ..................................................................................................71

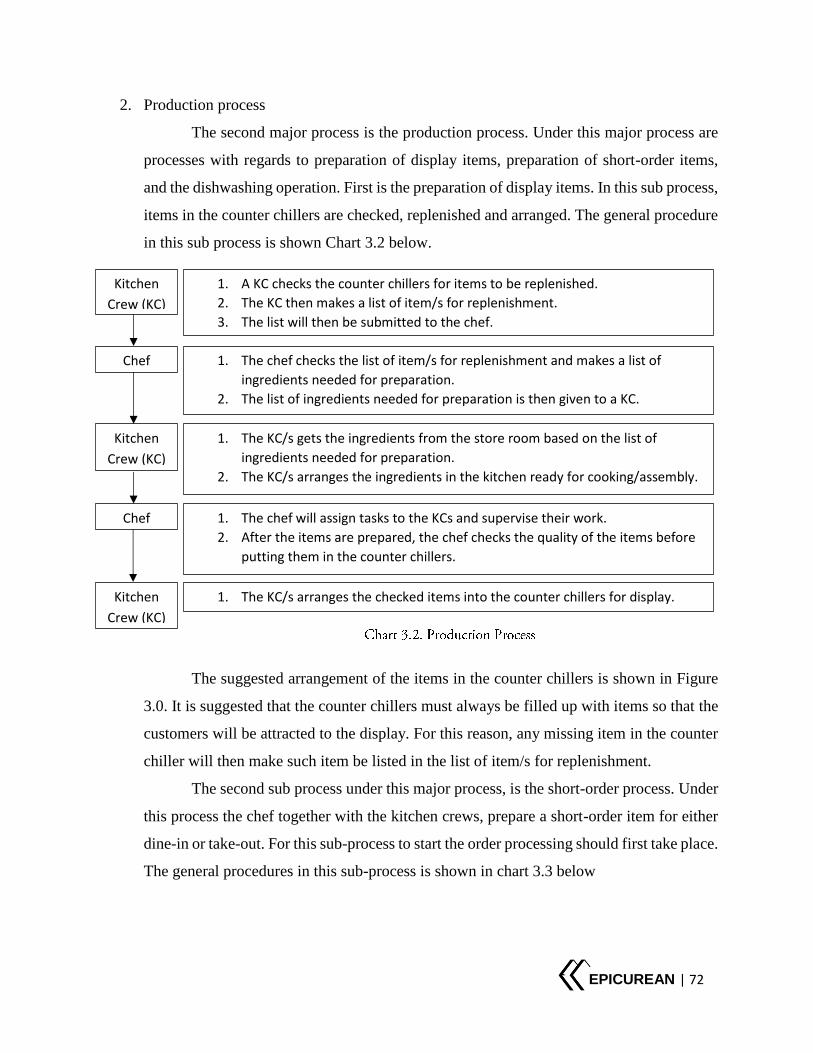

Chart 3.2. Production Process ........................................................................................................72

Chart 3.3. Order Processing ..........................................................................................................73

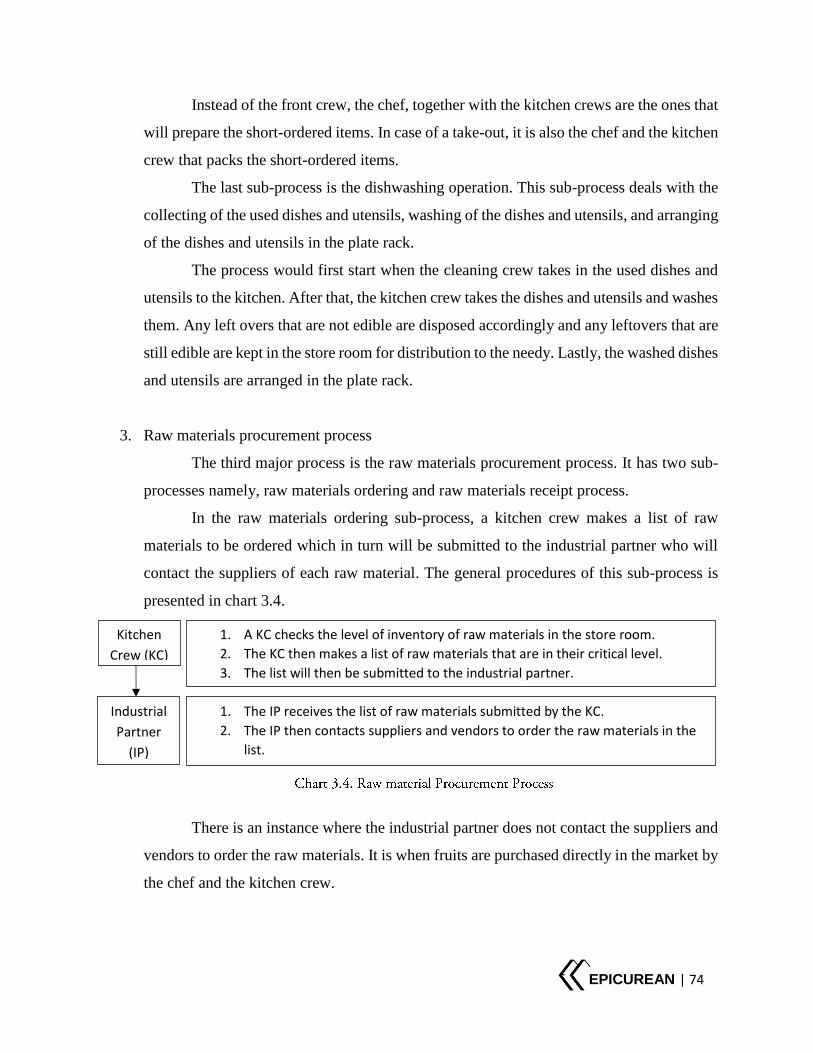

Chart 3.4. Raw material Procurement Process...............................................................................74

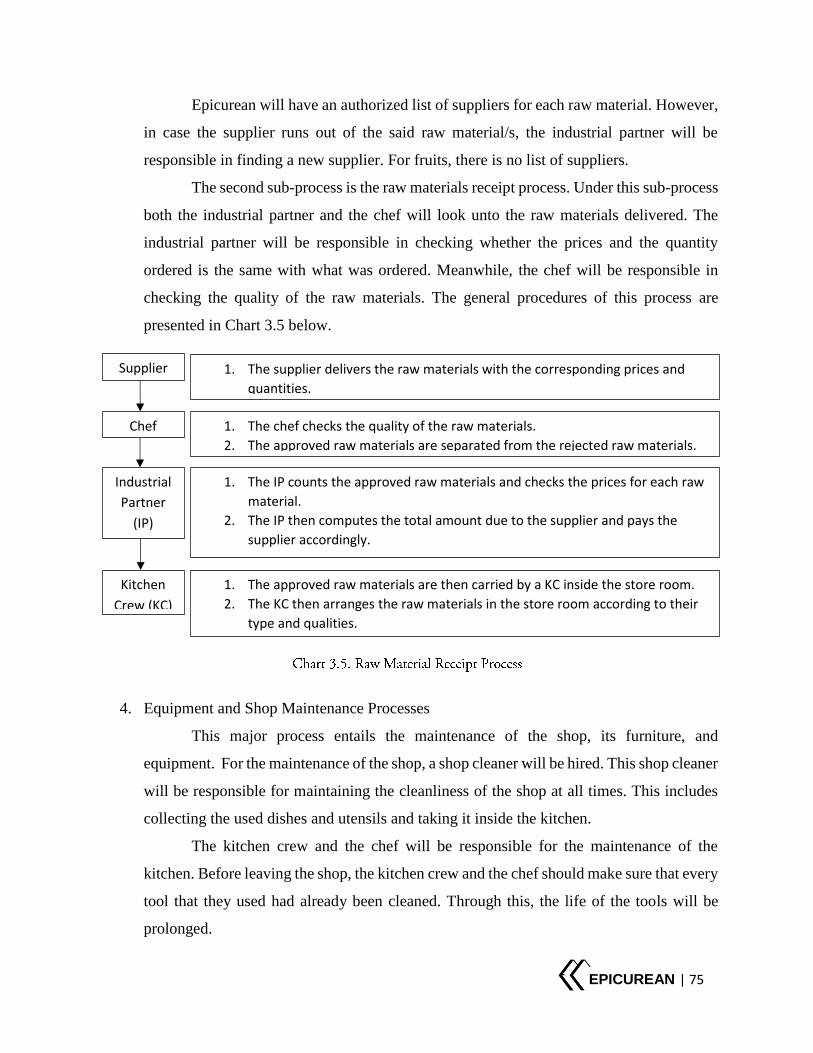

Chart 3.5. Raw material Receipt Process .......................................................................................75

LIST OF TABLES

Table 2.0. Number of Pastry and Coffee Shops in Davao City for the past five years .................13

Table 2.1. Projected number of Pastry and Coffee Shops in Davao City for the next five years ..13

Table 2.2 Respondent’s Response on Whether They Have Health Issues with Chocolate Products

........................................................................................................................................................19

Table 2.3. Weighted Number of Responses for Respondents’ Preference of Premium Chocolate

House ............................................................................................................................................20

Table 2.4. Weighted Percentage of Frequency of Going to Hangout/Study Place/Cafe of

Respondents ...................................................................................................................................22

Table 2.5. Percentage of Respondents with Consumption of Products of 1-2 times and More

than 2 times Per Week ...................................................................................................................23

EPICUREAN | vi

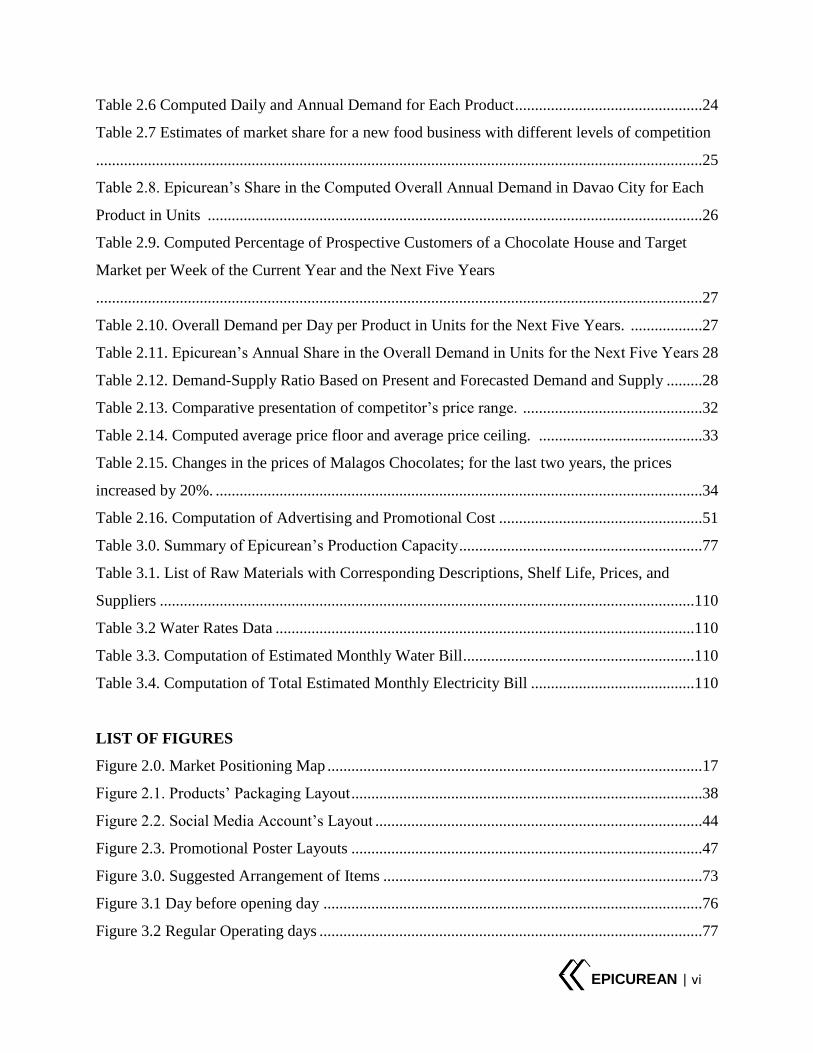

Table 2.6 Computed Daily and Annual Demand for Each Product ...............................................24

Table 2.7 Estimates of market share for a new food business with different levels of competition

........................................................................................................................................................25

Table 2.8. Epicurean’s Share in the Computed Overall Annual Demand in Davao City for Each

Product in Units ............................................................................................................................26

Table 2.9. Computed Percentage of Prospective Customers of a Chocolate House and Target

Market per Week of the Current Year and the Next Five Years

........................................................................................................................................................27

Table 2.10. Overall Demand per Day per Product in Units for the Next Five Years. ..................27

Table 2.11. Epicurean’s Annual Share in the Overall Demand in Units for the Next Five Years 28

Table 2.12. Demand-Supply Ratio Based on Present and Forecasted Demand and Supply .........28

Table 2.13. Comparative presentation of competitor’s price range. .............................................32

Table 2.14. Computed average price floor and average price ceiling. .........................................33

Table 2.15. Changes in the prices of Malagos Chocolates; for the last two years, the prices

increased by 20%. ..........................................................................................................................34

Table 2.16. Computation of Advertising and Promotional Cost ...................................................51

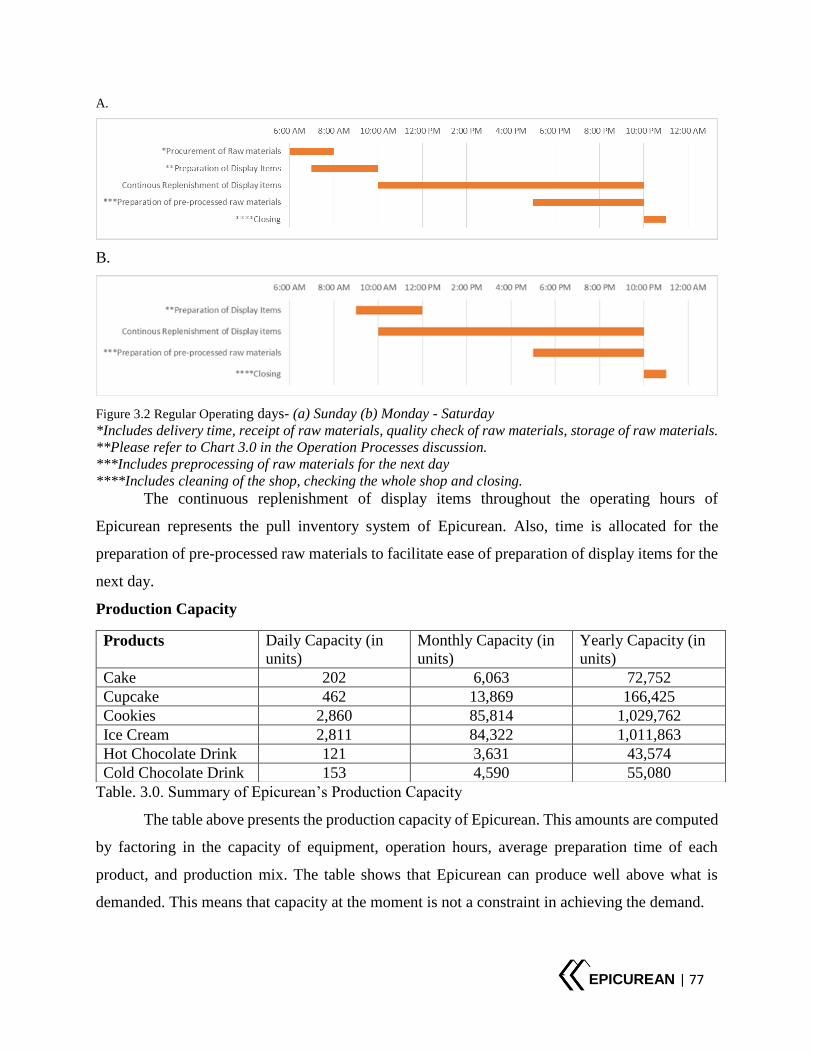

Table 3.0. Summary of Epicurean’s Production Capacity .............................................................77

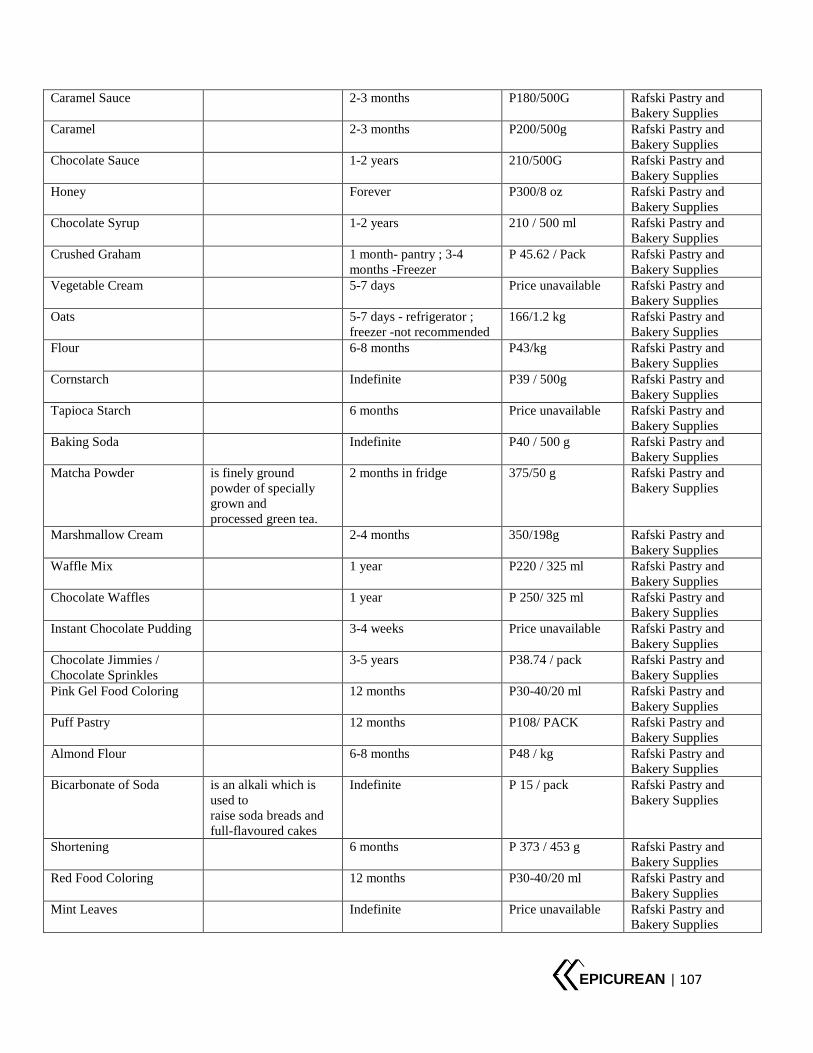

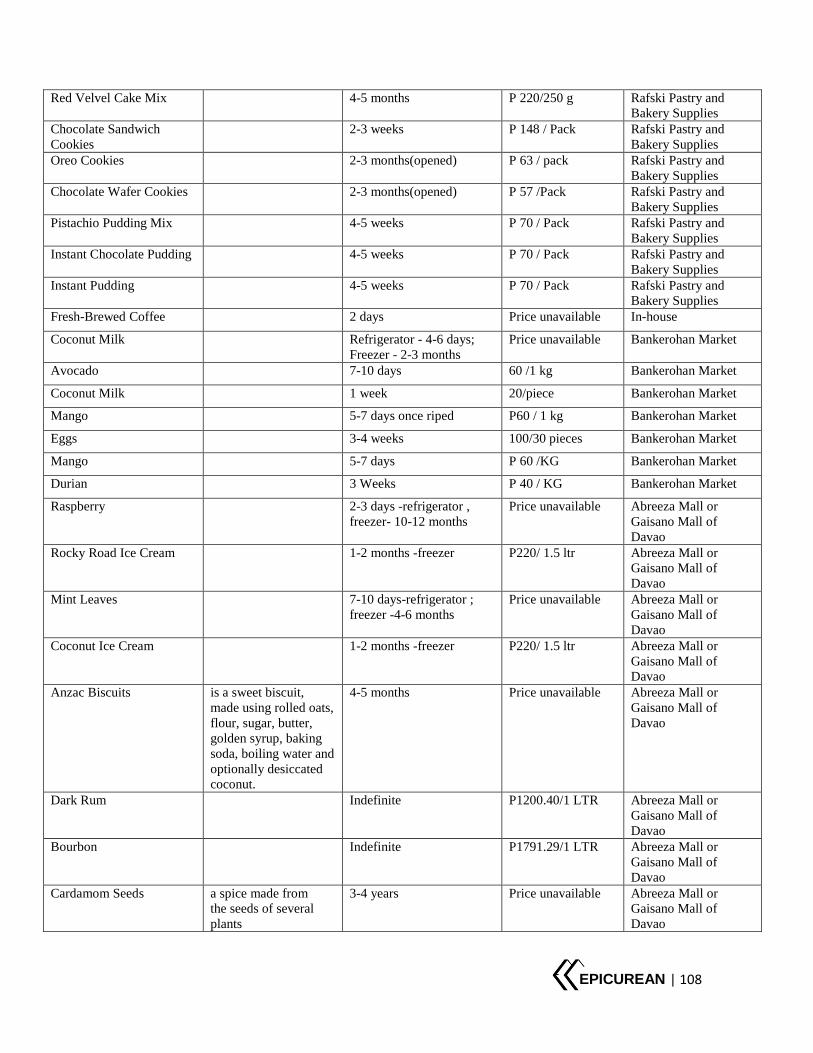

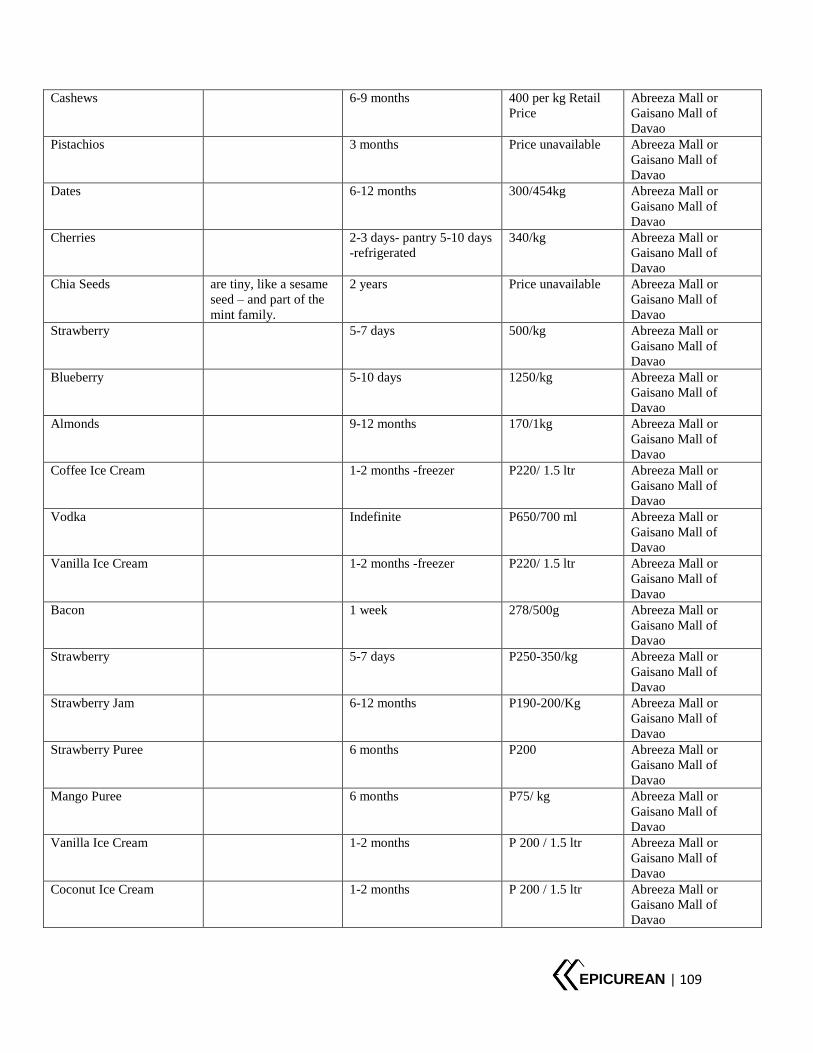

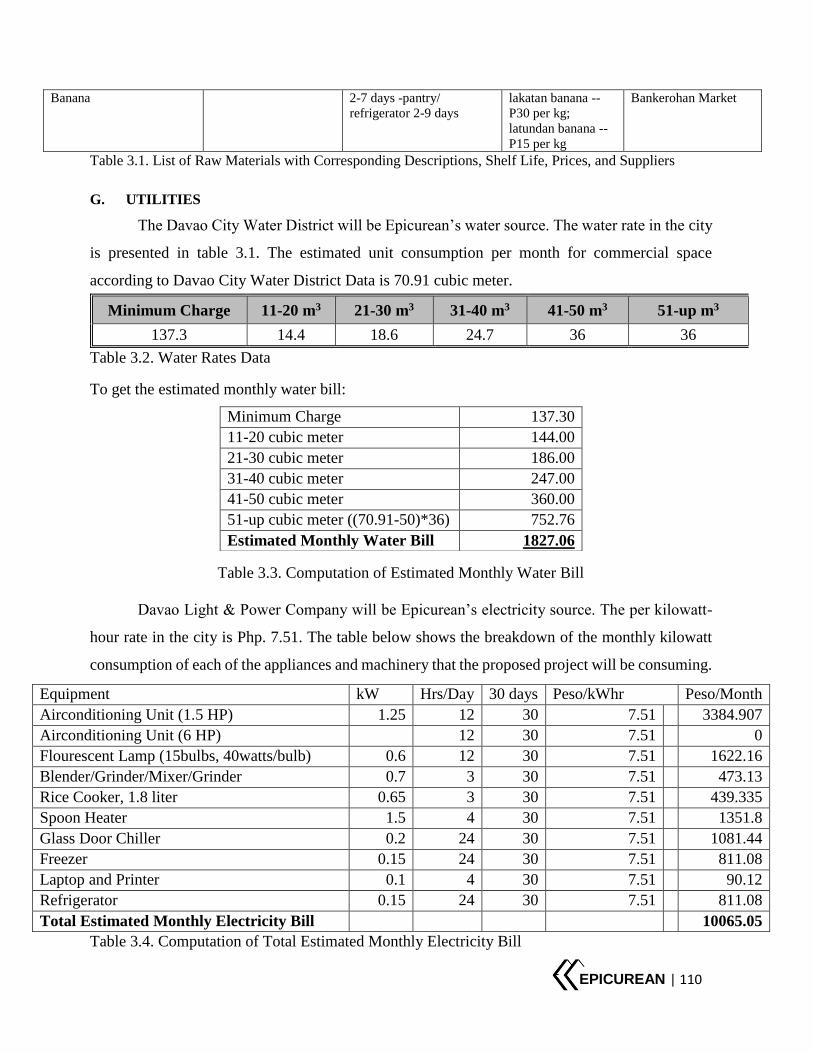

Table 3.1. List of Raw Materials with Corresponding Descriptions, Shelf Life, Prices, and

Suppliers ......................................................................................................................................110

Table 3.2 Water Rates Data .........................................................................................................110

Table 3.3. Computation of Estimated Monthly Water Bill ..........................................................110

Table 3.4. Computation of Total Estimated Monthly Electricity Bill .........................................110

LIST OF FIGURES

Figure 2.0. Market Positioning Map ..............................................................................................17

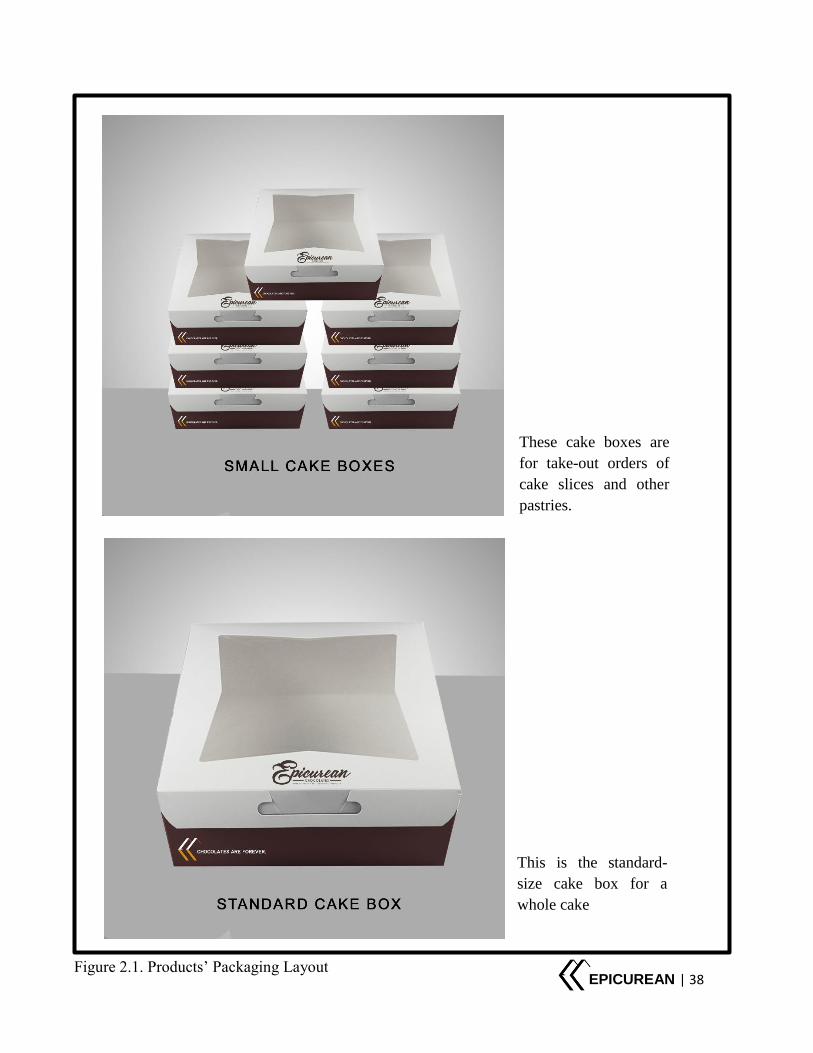

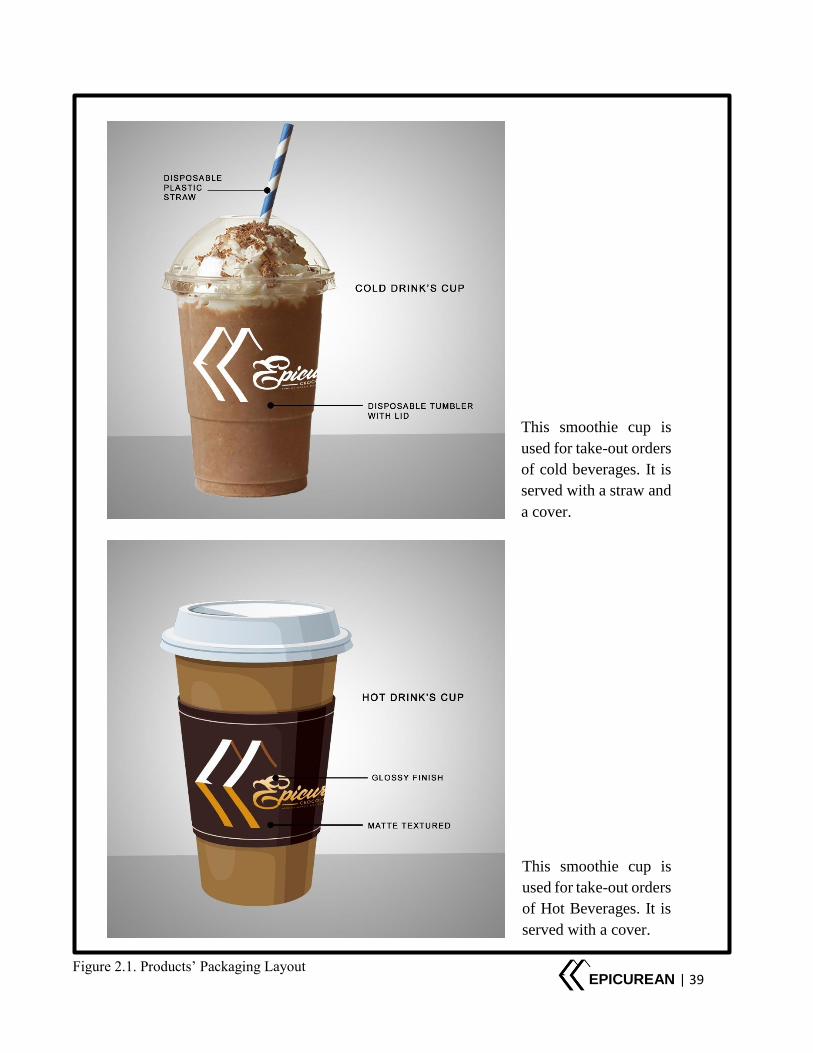

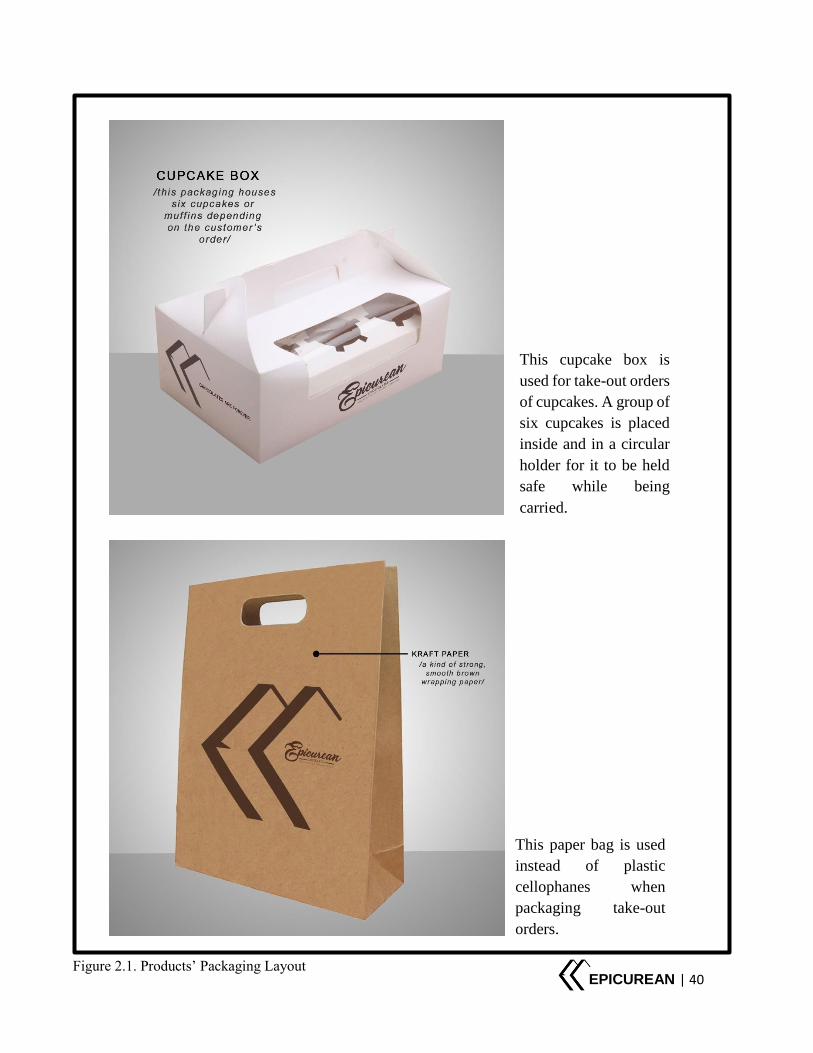

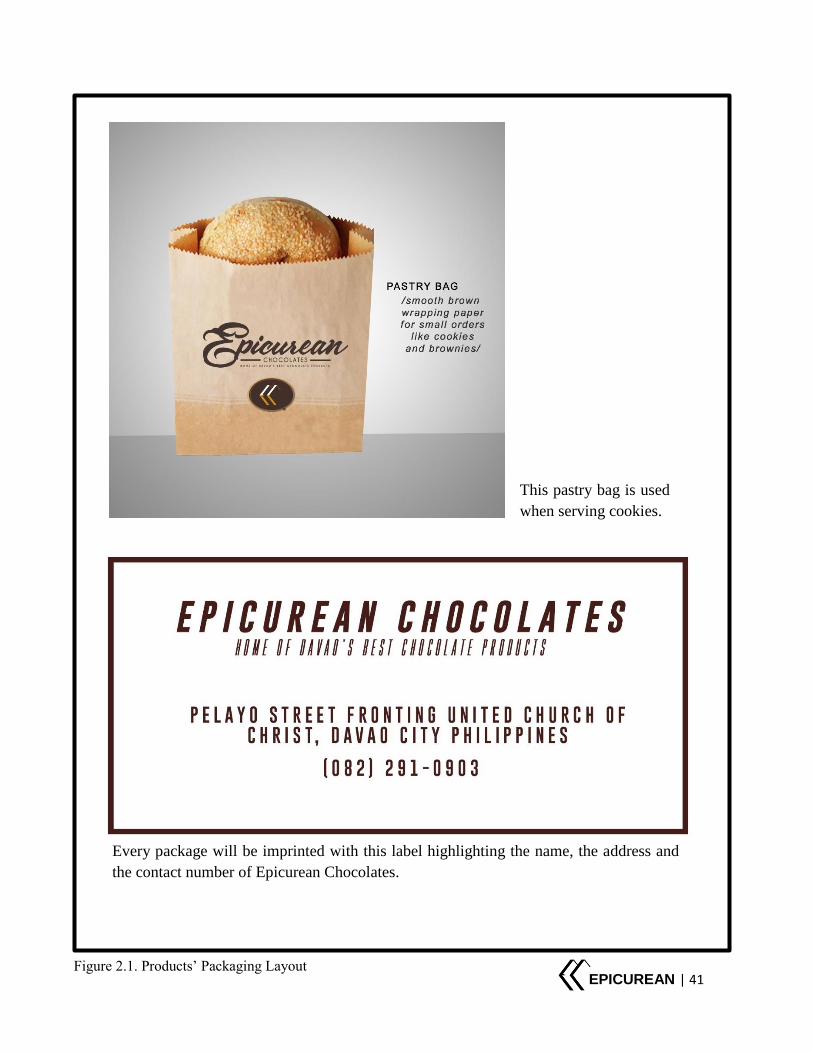

Figure 2.1. Products’ Packaging Layout ........................................................................................38

Figure 2.2. Social Media Account’s Layout ..................................................................................44

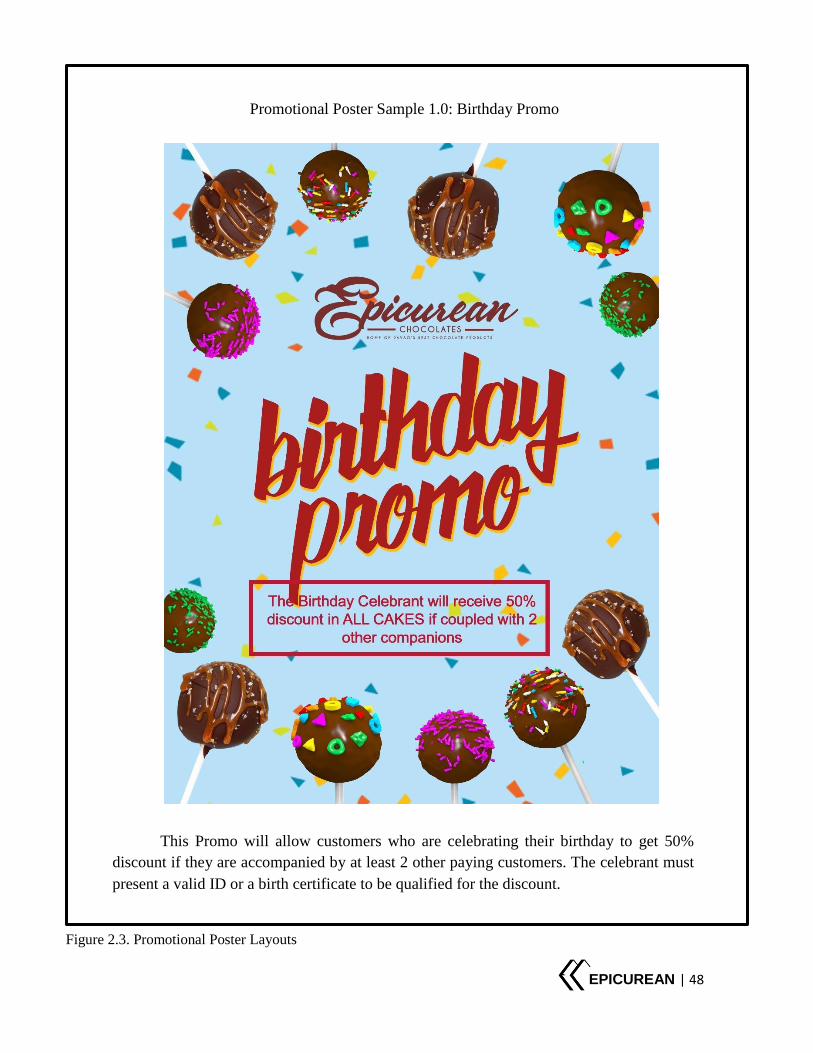

Figure 2.3. Promotional Poster Layouts ........................................................................................47

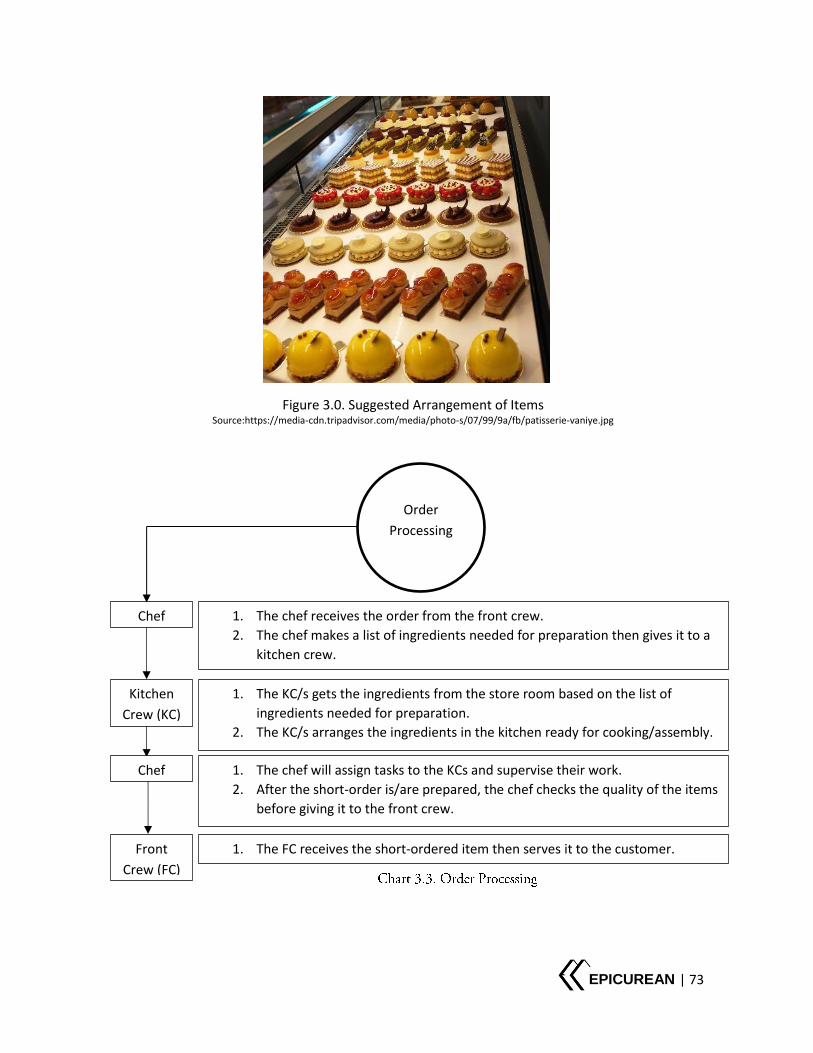

Figure 3.0. Suggested Arrangement of Items ................................................................................73

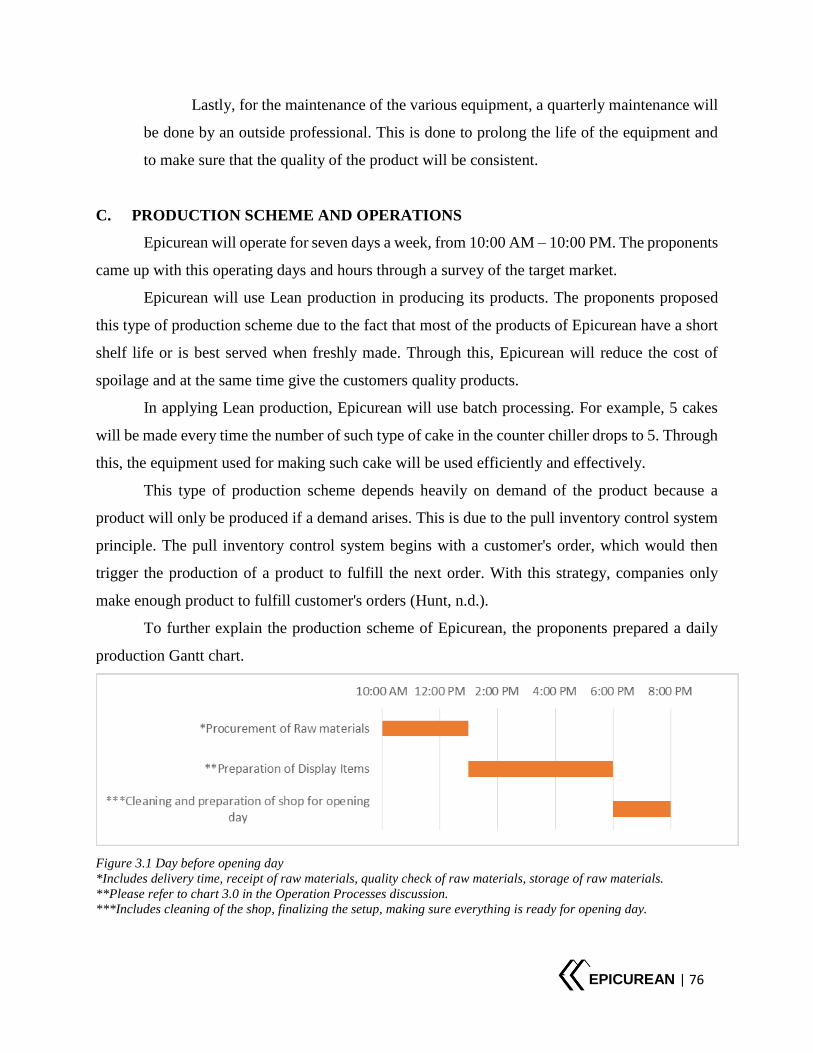

Figure 3.1 Day before opening day ...............................................................................................76

Figure 3.2 Regular Operating days ................................................................................................77

EPICUREAN | vii

Figure 3.3. Location Map...............................................................................................................78

Figure 3.4. Front View of Actual Location ....................................................................................78

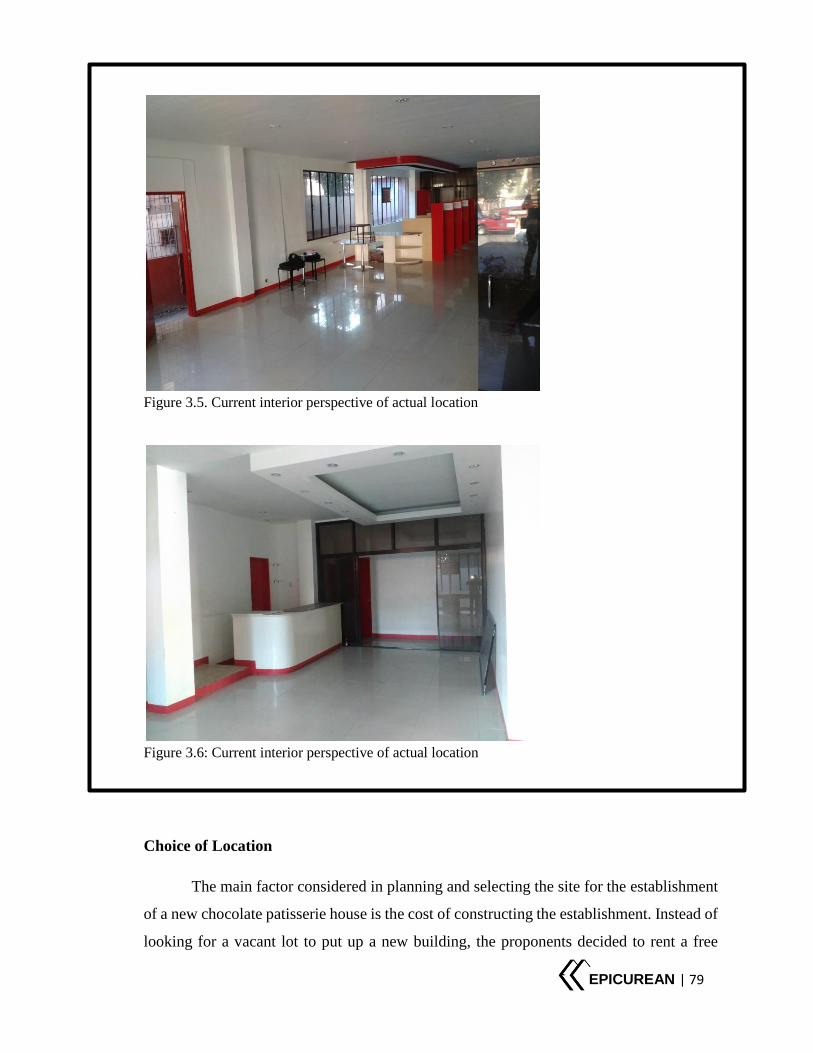

Figure 3.5. Interior perspective of Actual Location ......................................................................79

Figure 3.6. Interior perspective of Actual Location ......................................................................79

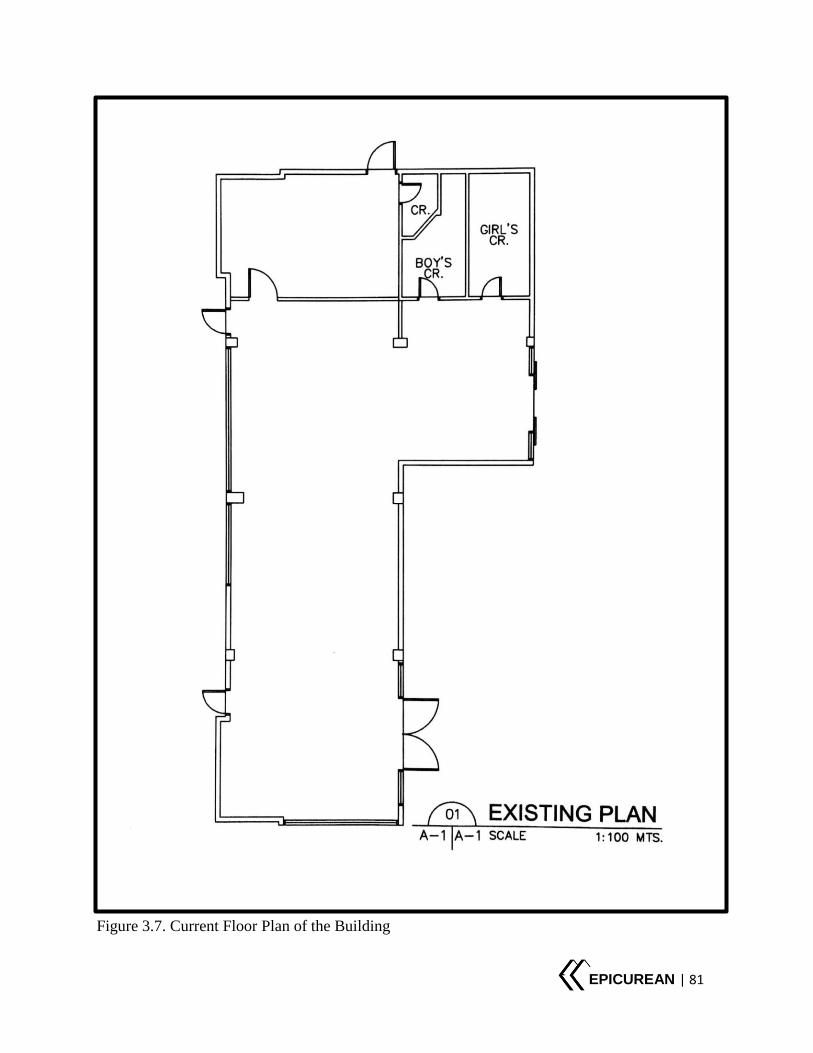

Figure 3.7. Current Floor Plan of the building...............................................................................81

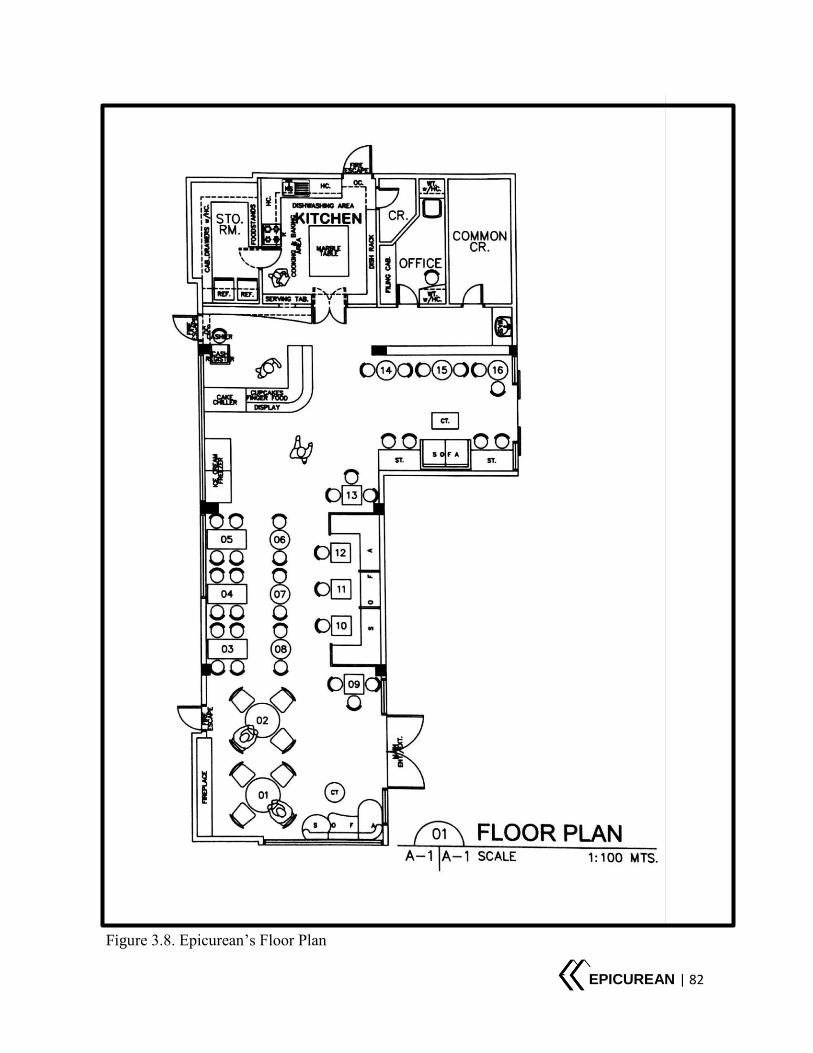

Figure 3.8. Epicurean’s Floor Plan ................................................................................................82

EPICUREAN | 1

CHAPTER I

SUMMARY OF THE PROJECT

A. Name of the Enterprise

The name of the enterprise will be Epicurean. Epicurean is rooted from the name of the ancient

philosopher, Epicurus. Epicurus advanced the philosophy Epicureanism, which teaches that the

greatest good is to seek modern pleasures in order to attain a state of tranquility, freedom from

fear, and absence from bodily pain. Epicurean as an adjective, means appreciation of good food

and drink. The proponents have chosen the name because Epicurean, as an enterprise, aims to serve

good food, drink, and service to its clientele.

Epicurean’s logo sports white chocolate bars which form the letters E and C. It symbolizes

Epicurean’s primary ingredient in all the food and drink that it will serve, which is chocolate. The

logo’s dominant color is brown which symbolizes the color of chocolates.

EPICUREAN | 2

B. Location

The proponents chose to establish Epicurean in a 150 sq.m. commercial space available

for lease situated at the ground floor of Fabie Building, Poblacion District, Davao City. It is located

in the downtown area – in front of UCCP Church’s Shalom Center, at the back of Gaisano South

Citimall, and few blocks away from Apo View Hotel and People’s Park.

The following are the factors considered in choosing the location. First, the initial capital

outlay in putting up the shop would be lesser. The cost of renovation and monthly rental fee would

be cheaper than the cost of buying a land and constructing a new building. Second, the shop would

be accessible to its customers since it would be situated in the downtown area where several

jeepneys pass. Lastly, the place would be conducive for study, business meetings, hang-out, and

the like because the location of the shop is not crowded nor busy.

C. Descriptive Definition of the Project

The project is proposed by a group of fifth year students of Ateneo de Davao University

enrolled in the course, Bachelor of Science in Accountancy. The proposition is due to the

proponent’s foreseen potential of establishing a chocolate house in Davao City i.e. the advantages

of entering an unsaturated industry.

Epicurean, the name of the business proposed, is a conceptual chocolate house in Davao

City that would be established through a contract of partnership. As a chocolate house, it will offer

products that have chocolate as the main ingredient such as chocolate cakes, cupcakes, cookies,

ice cream, and hot and cold chocolate drinks.

Epicurean would also adopt the concept of a patisserie which would have the products

displayed for easy selection. As a unique concept in Davao City, the business is expected to attract

college or senior high school students, young professionals, and other businessmen. Specifically,

the target market of Epicurean would be those with ages ranging between 15 and 34 and have an

income or allowance ranging between Php 1,001.00 and above.

In Davao City, there is only one known shop with the same concept with Epicurean i.e.

Chocolatier. However, the business would have many indirect competitors such as coffee shops

and pastry shops. The coffee shop industry, especially “homegrown” coffee shops, is continually

flourishing in Davao City (DavaoFoodTripper, 2014). Nonetheless, Epicurean, with something

EPICUREAN | 3

new to offer, is believed to have a huge potential of being a successful and profitable business

venture.

D. Long Range Objectives

Within ten years from its establishment, Epicurean aims to:

be widely known for its premium and quality product and service offering;

be a major player in the coffee and patisserie shop industry in Davao City;

create and maintain a loyal customer base;

be able to produce its chocolates (backward integration);

maintain if not increase a dominant market share despite potential entries of patisserie

shops in Davao City; and

have a considerable growth in Return on Assets of 20% per year.

E. Feasibility Criteria

Market

The main concern under this criterion is the capability of the business to introduce

itself to the market. This also concerns the determination of an existing demand for the

products offered by the business. This criterion determines the level of existing competition

in the same and related industries and the capacity of the business to compete.

Technical

Important considerations under technical feasibility are the availability of raw

materials needed for the production especially the seasonality of fruits to be used,

availability of technology relevant to Epicurean’s industry that are affordable and cost-

efficient, availability of spaces for Epicurean’s location, availability of manpower, and its

production capacity to meet demand.

Financial

The Internal Rate of Return (IRR), Net Present Value (NPV), and the Payback

Period are the measures that critically quantify the financial feasibility of the project. Ratios

such as liquidity, leverage and profitability are computed using the projected financial

statements prepared. These factors are affected by the (1) availability and mix of equity

EPICUREAN | 4

and debt sources of financing, (2) the computed Weighted Average Cost of Capital

(WACC) and (3) assumptions.

Socio-Economic

The primary considerations in this feasibility criteria are: how the project would be able

to help the people in the community, the government, and the economy of the country. In

line with this, specific activities are to be implemented to achieve the abovementioned

criterion.

Organization and Management

The primary considerations in choosing what type of organization and management

scheme to apply for Epicurean is the sufficiency of initial financing that it could provide to

the entity and how efficient and effective it will be in the implementation of the project. In

addition, the organizational chart used in the business, the policies and standards set are

also considered.

F. Highlights

History of the Project

The idea of a chocolate house emerged after the proponents read an online article

stating that in the present, one of the businesses with high potential for booming is a

chocolate house. The idea was then supported by the latest news about Malagos Chocolate

being awarded with Silver Awards in the 2015 International Chocolate Awards in

Germany. Given that Philippine chocolate is already internationally recognized as good

chocolate, the proponents were convinced of the great potential of establishing a chocolate

house.

The proponents then observed and researched on the popular chocolate houses in

Davao City and found only one which is Chocolatier. The said business is located at

Abreeza Mall, Davao City. The idea that the proponents had in mind for a chocolate house,

however, is in an independent location like most coffee shops and not attached to a mall

or any bigger entities. This made the idea unique and convinced the proponents to pursue

the project. Since there are no existing chocolate houses that positions itself the way the

proponents plan to position their conceptual chocolate house in terms of product

EPICUREAN | 5

presentation and offerings, the proponents pursued the project and named the conceptual

chocolate house, Epicurean.

Nature of the Industry

Description

A patisserie is a type of French or Belgian bakery that specializes in pastries

and sweets. Basically, a patisserie is a pastry shop with the distinction of its product

presentation.1 In Davao, the equivalent types of shop are coffee shops. The coffee and

pastry shop industries pose a tight competition in the market due to the many number

of shops littering the city.

Role in the economy

The Epicurean Chocolates belongs to the Hotel and Restaurant Industry. Based

on the census conducted by the Philippine Statistics Authority (PSA) on the year 2012,

the Restaurant and Mobile Food Service Activities, under the Hotel and Restaurant

Industry, garnered the highest number of establishments in the country which is

around 70% of the whole industry. With this, the Restaurant and Mobile Food Service

Activities give the highest percentage of employment and highest compensation to its

employees within its industry. It also ranked as the highest income earner and biggest

expenditure spender.

Products/product lines

A patisserie usually offers sweets such as cakes, cupcakes, cookies, pancakes,

ice cream, and hot and cold drinks. Epicurean will offer all of the mentioned products

with the exception of pancakes.

Problems Faced by the Industry

The chocolate house industry is not yet fully established in Davao City. Hence, it

faces the challenge of introduction to the market. There is no guarantee that businesses in

this industry would garner market acceptance. In addition, chocolate products are also

offered in most coffee and pastry shops which makes the industry prone to being

1 See Figure 3.0

EPICUREAN | 6

overmastered by the industry of coffee shops and pastry shops which are continually

thriving in Davao City.

Mode of Financing

Two modes of financing will be used. They are the following:

1. Long term borrowings from banks

2. Capital contributions from partners.

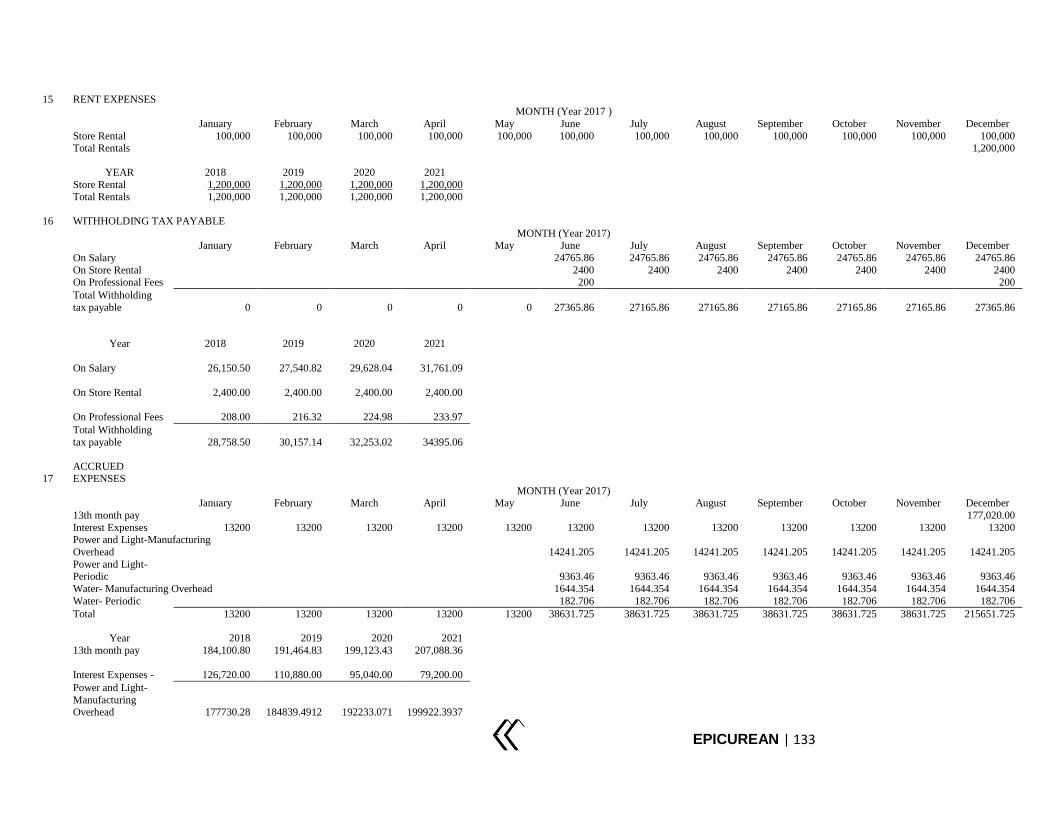

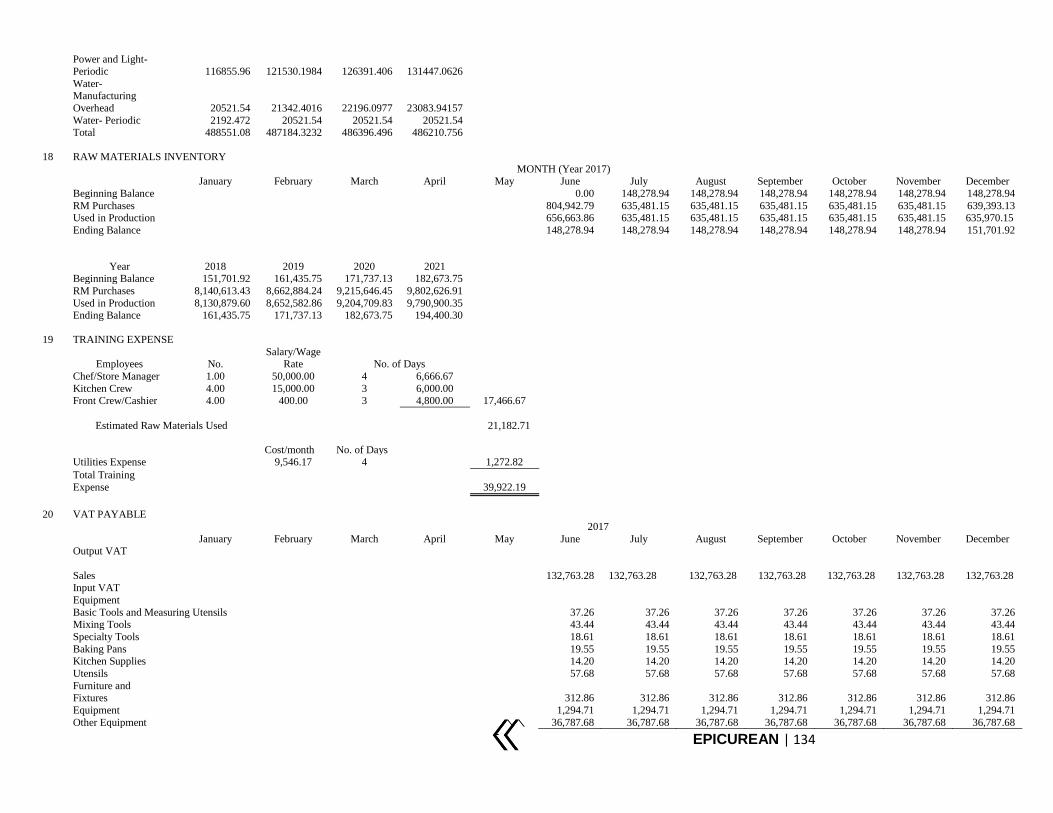

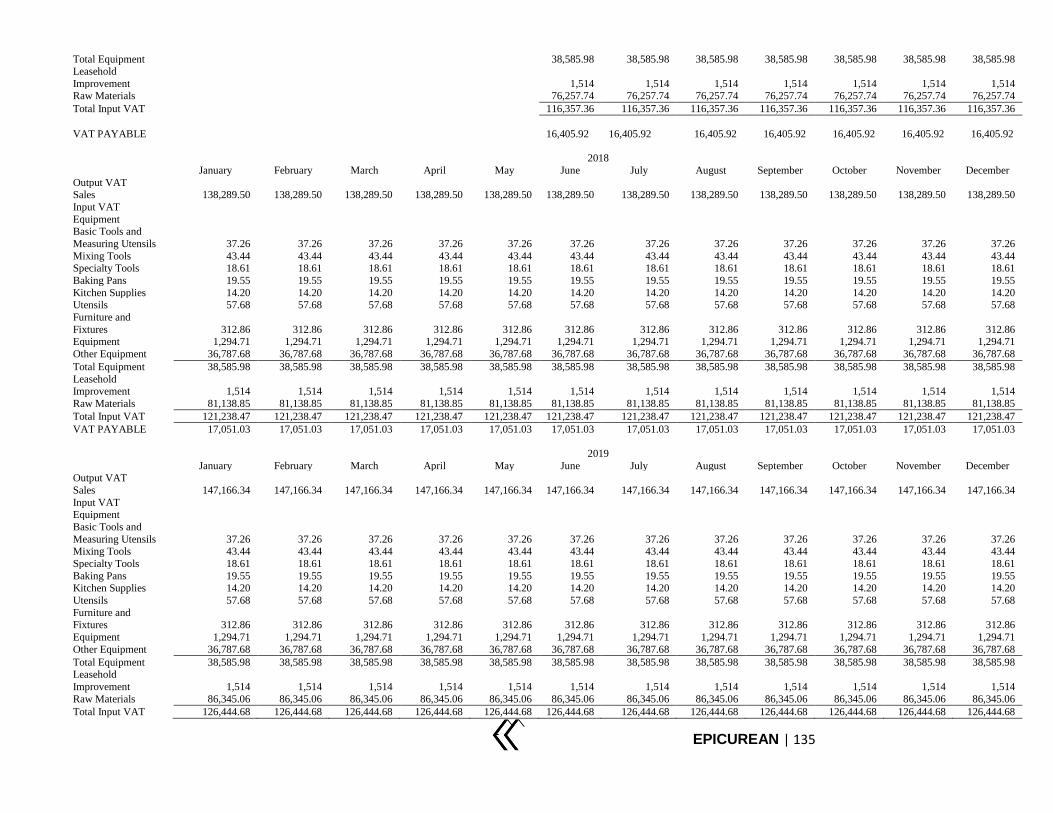

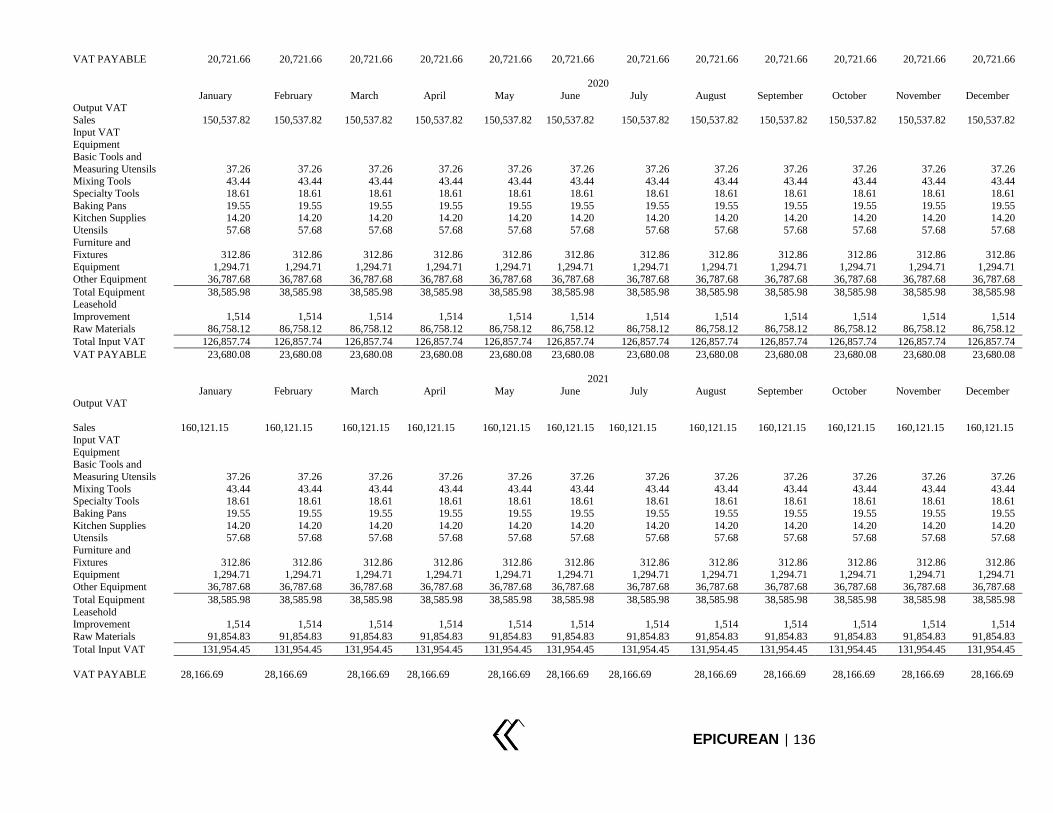

Specific capital structure is indicated in Chapter IV | Financial Aspect of this paper.

Investment Cost and Initial Working Capital

The project will be financed by the capital contributions of the partners and term

borrowings from local banks. The initial working capital will be used to pay for

Epicurean’s tax contributions and regulatory fees for partnership registration. These will

enable the business to operate and assure its customers that they are duly authorized to

open a patisserie.

Also, the initial investment will be used to fund the renovation of the store. It will

require a huge percentage of the initial investment. Moreover, in order for the store to

operate, it will require cash to fund its first two months of operation. These cash will come

from both the initial investment and the operation of the business for the first month.

G. Major Assumptions and Summary of Findings and Conclusion

Market

There is no data available about the historical demand level for Chocolate

Patisserie in Davao City. Hence, the current level of demand in Davao City for the

products offered by Epicurean is computed based on the survey conducted by the

proponents. There are 524 respondents of the survey with ages ranging from 15 to 34 years

old. The share of Epicurean in this overall demand is determined to be 5%. The projected

demand levels for all the products are at an increasing trend.

The projected data about the number of shops supplying similar products with

Epicurean shows no trend. This is made through moving average method.

EPICUREAN | 7

The target markets of the entity are senior high school and college students, and

young professionals with ages ranging from 15 to 34 years old having weekly allowance

or income of Php 1,001.00 or more. Chocolate, the main ingredient will be highlighted in

all of Epicureans products. The entity is a service-oriented establishment that provides

quality service to customers and offers chocolate products. The marketing strategy that

will be used to reach the market and secure a competitive position is mainly through the

use of Social Media namely Facebook, Twitter, and Instagram. Printed ads will also be

used by Epicurean for its advertising. The entity aims to attract customers and turn them

into patrons.

Technical

Raw materials of Epicurean needed for baking will come from Rafski Pastry and

Bakery Supplies. The chocolates that will be used as the main ingredient will also come

from the same supplier. Fruits that will be used as ingredients will come from the

Bankerohan wet market.

Orders for raw materials will be made every end of the week for the forecasted

demand of the next week. In cases where materials fall below critical level before the end

of the week, an order should be placed to replenish inventory levels enough for the

remaining days of the week. Shortages will be determined by checking the quantity of raw

materials in the storage room after every end of a work day. Product shelf life will also be

considered when buying raw materials.

Technology needed for Epicurean’s operation are primarily kitchen appliances and

tools such as ovens for baking, chillers for display of products, refrigerator for storage of

raw materials and other finished products not on display, freezer for ice cream display,

blenders for chocolate drinks, and other basic baking tools and equipment such as baking

pans, spatulas, and others.

Baked goods will undergo basic and specialized baking procedures. This process

will be done by the kitchen crews and the chef. Hot and cold chocolate drinks will undergo

heating, stirring, and blending by the front crews. Crews should always be courteous and

offer smiles to the clients.

EPICUREAN | 8

Epicurean’s staff will be composed of one chef, four kitchen crews, four front

crews/cashiers, and two shop cleaners. The chef will act as the store supervisor and in-

charge of the daily activities of the establishment as well as its employees.

Financial

Under financial feasibility, major assumptions include (1) all sales transactions are

made in cash, (2) purchases are made in cash and in credit, (3) sales are made evenly

throughout the year, (4) quantity of products sold increases by 2.3% per year based on

projected sales in the market study and (5) and an inflation rate of 4%.

Total capital requirements is P3,262,377.90. Paid-up capital of P660,000.00 will

be sourced from the partners on January 2017 which is 20% of the total capital

requirements. The remaining 80% amounting to P2,640,000.00 will be sourced out from

long-term debt.

For five years of operations, Epicurean has maintained a positive return. Payback

period is approximately 3 years and 5.25 months while return on equity for five years has

an average of 80.74%.

Socio-Economic

The main beneficiary of Epicurean will be the unemployed members of the

community. Epicurean targets to hire college students who are taking up Hotel and

Restaurant Management course and in need of financial help for their studies. Another

activity to help the community is distributing edible left-overs to beggars. Epicurean will

also provide additional revenue to the government through taxes. It will also promote the

locally produced chocolates.

Organization and Management

Epicurean’s form of business will be a partnership. Two partners will pool their

financial resources in order to realize the business. One partner will be a capitalist-

industrial partner and another will be a capitalist partner. They will share in the net profit

of the establishment in a 60:40 ratio with partner A receiving 60 and partner B receiving

40. They will hire a chef which will supervise the kitchen as well as other employees of

EPICUREAN | 9

the establishment such as the kitchen crews, front crews/cashier, and shop cleaner. The

Chef will then report to the partners. Also, policies will be established to manage the

business.

EPICUREAN | 10

CHAPTER II

MARKETING ASPECT

A. PRODUCT DESCRIPTION

Chocolate is one of the most famous desserts in the world. Every day, many people around

the world eat and crave for chocolate. The types of chocolate products made from cocoa bean

processing that will be used for our products are listed below.

Dark Chocolate: It is the type usually preferred when cooking because it has richer and

more intense flavor. The higher the cocoa solid content of a dark chocolate, the richer and more

intense the flavor you can get (Parragon, 2003). It has a minimum cocoa butter2 content of eighteen

percent (Notter, 2011).

Milk Chocolate: It is usually consumed as an ‘eating chocolate’ rather than used for

cooking. This is because of its creamy, mild, and sweet taste that the milk it contains produces. It

is used for decorations and when a recipe requires for a milder and creamier flavor (Parragon,

2003). Normally, it contains an estimate of 35% fat content. Its composition is 40% sugar, 30%

cocoa beans, 20% milk, and 10% extra cocoa butter (Notter, 2011).

White Chocolate: It is usually used to achieve color contrast when decorating cakes

(Parragon, 2003). It contains at least 20% cocoa butter and 14% milk solids. It also has 3.5% milk

fat and a maximum sugar content of 55% (Notter, 2011).

Chocolate Chips: They are usually used for baking and decorating. They are available in

dark, milk, and white variety (Parragon, 2003).

Cocoa Powder: It can be unsweetened and bitter in flavor or sweetened when mixed with

sugar. It is the powder residue after the cocoa butter has been pressed from the roasted and ground

cocoa beans. When cooking, unsweetened cocoa powder gives off a strong chocolate flavor

(Parragon, 2003).

Epicurean will make use of these types of chocolates to produce and serve a variety of

cakes, cupcakes, cookies, ice cream, hot and cold chocolate drinks.

As the leading producer of cacao in the world, the proponents will use Davao chocolates

in the store’s production. This is to increase Dabawenyo’s awareness about existing quality

chocolates in the region.

2 The natural fat present in cocoa beans. It is yielded by pressing the cocoa mass.

EPICUREAN | 11

The products offered will also be incorporated with fruits such as coconut, banana,

strawberry, durian, mango, and orange; nuts such as almond and pistachio; and other

complementary ingredients such as caramel, mocha, matcha, and whiskey.

As a service-oriented entity, Epicurean, will also offer quality customer service to its

customers. The staff will help the customers feel good about their day. From the moment a

customer enters the doors of the store to the time they will leave, Epicurean aims to give them a

comfortable dining experience. A heightened customer service is an important part in influencing

consumer decision whether to return or not.

B. MARKET DESCRIPTION

Epicurean’s general market will be the people of Davao and its tourists, since its location

will be in Pelayo Street, Poblacion District. As of 2010, Davao City has an estimated population

of 1.4 Million (Philippine Statistic Authority, 2013). It is ranked the 4th largest city in the

Philippines in terms of population (Worldatlas, n.d.). With regards to tourists, Davao City had

reached 680,000 visitors as counted by the Department of Tourism from accommodation

establishments in 2010 (Philippine Statistics Authority, 2012). This statistic shows that Davao City

can offer customers to current and potential establishments. Furthermore, the city has young

population. According to PSA, the median age of the population of the city is 24.0 years

(Philippine Statistic Authority, 2013). This suggests that the major customers of businesses in

Davao City will be in that age. Moreover, Davao City is a melting point of its neighboring cities

and municipalities. People from its neighboring cities and municipalities travel to Davao City to

work, to shop, and to do recreational activities.

Epicurean as a patisserie aims to attract college or senior high students, young professionals

and professionals. Due to this, the proponents decided to choose students, primarily senior high

and college students, young professionals and professionals with ages ranging between 15 – 34,

and have an income or allowance ranging between Php 1,001 and above as its target market. As to

the supply of student customers, Davao City provides a great number. Davao City has 20

College/Universities as per www.finduniversity.ph. The most popular colleges and universities in

Davao City are Ateneo de Davao University (AdDU), University of Southeastern Philippines

(USeP), Holy Cross of Davao College (HCDC), San Pedro College (SPC), University of Mindanao

(UM) and University of the Immaculate Conception (UIC). AdDU, SPC, and UIC are the schools

EPICUREAN | 12

which are in the high-tuition classification, with tuition ranging from Php 34,000 – 100,000 per

year. While HCDC, UM, and USeP are the schools which belongs to the low-tuition classification

with tuition ranging from Php 14,000 – 40,000 (Finduniversity.ph, n.d.). This data presents the

composition of students in Davao City in terms of allowance and buying power. Furthermore, the

result of the survey of the proponents shows that the usual student’s weekly allowance ranges from

Php 800 to Php 1000 and below Php 800. This represents 64.33% of the total students surveyed,

while the remaining 35.67% has an allowance of Php 1001 and above. This statistic shows that

most of the students have a low buying power. However, this statistic also shows that the 64.33%

is not the overwhelming majority thus allowing the proponents to implement a competitive pricing

strategy.

Davao City presents an impressive number of professional customers. According to the

article of Capon (2015), the employment rate of Davao Region remained stable at 94 percent in

April 2015 as per data from the Department of Labor and Employment (DOLE) 11. Furthermore,

based on the comparative employment status of the Davao Region for 2014 and 2015, employed

Dabawenyos reached 1,914 million of the 2,036 million total labor force. These employed

Dabawenyos are potential customers for every establishment and is a good indicator for businesses

like Epicurean.

As discussed earlier, Epicurean will serve pastries and sweets in Davao City. Consequently,

its major competitors would be pastry shops and coffee shops. In Davao City, pastry shops and

coffee shops are everywhere. Thus, the proponents decided that the point of comparison will be

Maitre Chocolatier, Starbucks, Green Coffee, Lachi’s Sans Rival Atbp. and Dulce Vida as these

are the shops that owns the bigger share of the market. First, Starbucks, a known international

coffee shop with international experience and popular name. Next, Green Coffee, a local coffee

shop which has a vast experience in the Davao City market due to its long years of existence in

the city. Another is Lachi’s San Rival Atbp, a known pastry shop in Davao City which offers cakes

at a low price. Finally, Dulce Vida, a sister shop of Tiny Kitchen, is a pastry shop which offers

premium cakes and delicacies. Despite of the advantages these shops have, the proponents believe

that Epicurean will have an edge against these competitors. According to Chef San Jose, in our

interview, a patisserie is a higher form of pastry of shop and currently there is no patisserie in

Davao City. This distinguishing feature would serve as a competitive advantage to Epicurean

because it would provide a first-mover advantage to the company.

EPICUREAN | 13

C. SUPPLY

Since Epicurean Chocolates (EC) is a type of business that is not yet common in Davao

City, we considered pastry shops and coffee shops as our competitors since these businesses offer

products similar in nature and could be substitutes to Epicurean’s products (e.g. cakes and other

pastries).

Presented below is the number of pastry and coffee shops (in total) which were able to

supply products (such as cakes, ice cream, chocolate drinks, etc.) to the Davao market for the past

five years.

Table 2.0. Number of Pastry and Coffee Shops in Davao City for the past five years

Using the average method of forecasting, we projected the probable number of pastry and

coffee shops in Davao for the next five years, presented below.

Pastry Shops Coffee Shops

2016 1 170

2017 1 171

2018 1 172

2019 1 171

2020 1 171 Table 2.1. Projected number of Pastry and Coffee Shops in Davao City for the next five years

As presented above, supply changes every year, with its number increasing and decreasing

from year to year. These fluctuations, however, do not follow a pattern; hence, the proponents

believe that the average method of forecasting is the most appropriate method in projecting the

supply for the next five years.

Among these establishments currently present in Davao City, the proponents identified five

businesses that they considered as major competitors of Epicurean. These are the following:

Maitre Chocolatier

Maitre Chocolatier is the first boutique cafe in the Philippines which offers a wide array of

High Quality, well known European Chocolate Brands. It has three branches – Manila, Cebu, and

Davao – and one of its branches is located in G/F, Abreeza Mall, J.P. Laurel Avenue, Bajada,

Davao City. The products the store serve to its clients include salads, sandwiches, soup, pasta, rice

Pastry Shops Coffee Shops

2011 2 164

2012 1 164

2013 1 169

2014 1 167

2015 1 175

EPICUREAN | 14

meals, desserts, cakes, drinks, and cocktails, all complemented with chocolates. Aside from

gourmet dishes and desserts, the store also offers chocolate gift baskets and bouquets to its

customers. The proponents considered this as a major competitor since Epicurean would offer

chocolates products, most likely similar to what Maitre Chocolatier offers.

Starbucks

Starbucks is an American coffeehouse chain. Its product offerings include pastries and

sandwiches, and coffee-based, tea, and juice drinks. Currently, it has three branches in Davao City

which have the following locations: (1) Abreeza Mall, J.P Laurel Avenue, (2) SM City, Ecoland,

Matina, Quimpo Boulevard, and (3) SM Lanang Premier, Lanang. The proponents considered

Starbucks as a major competitor since it offers products similar in nature to Epicurean’s products

(pastries, drinks), hence, could be substitutes to chocolate products.

Green Coffee

Green Coffee is a local coffee shop. Like Starbucks, its range of products include pastries

and pasta, and coffee-based, tea, and juice drinks. Currently, it has four branches: three of which

is in Davao City, located in the following areas: (1) F. Torres St., Poblacion District, (2) J.P. Laurel

Avenue, Bajada St., and (3) Ruby St., Marfori Heights; and one branch located along Apokon

Road, Tagum City. The proponents considered Green Coffee as one of the major competitors since

it offers products similar to Epicurean’s and could be considered substitutes to Epicurean’s

chocolate-based products.

Lachi’s Sans Rival Atbp.

Lachi’s Sans Rival Atbp. is a local dessert shop. Aside from the wide variety of pastries it

offers – particularly cakes – the store also offers sandwiches, rice meals, and pasta to its customers.

It has a single branch, located in Ruby St., Marfori Heights, Davao City. This store is considered

as a major competitor of Epicurean since it serves products similar to what Epicurean would be

offering (e.g. pastries and etc.)

Dulce Vida

Dulce Vida is a local dessert shop in Davao City. Aside from cakes and a variety of pastries,

the shop also offers pasta, rice meals, sandwiches, and coffee to its customers. This shop is located

at Tulip Drive Extension, Ecoland Subd., Matina, Davao City. The store also has a branch in Torres

St., Davao City under Tiny Kitchen’s management. The group considered Dulce Vida as a major

EPICUREAN | 15

competitor because of the products it offers, such as pastries, which would also be offered by

Epicurean.

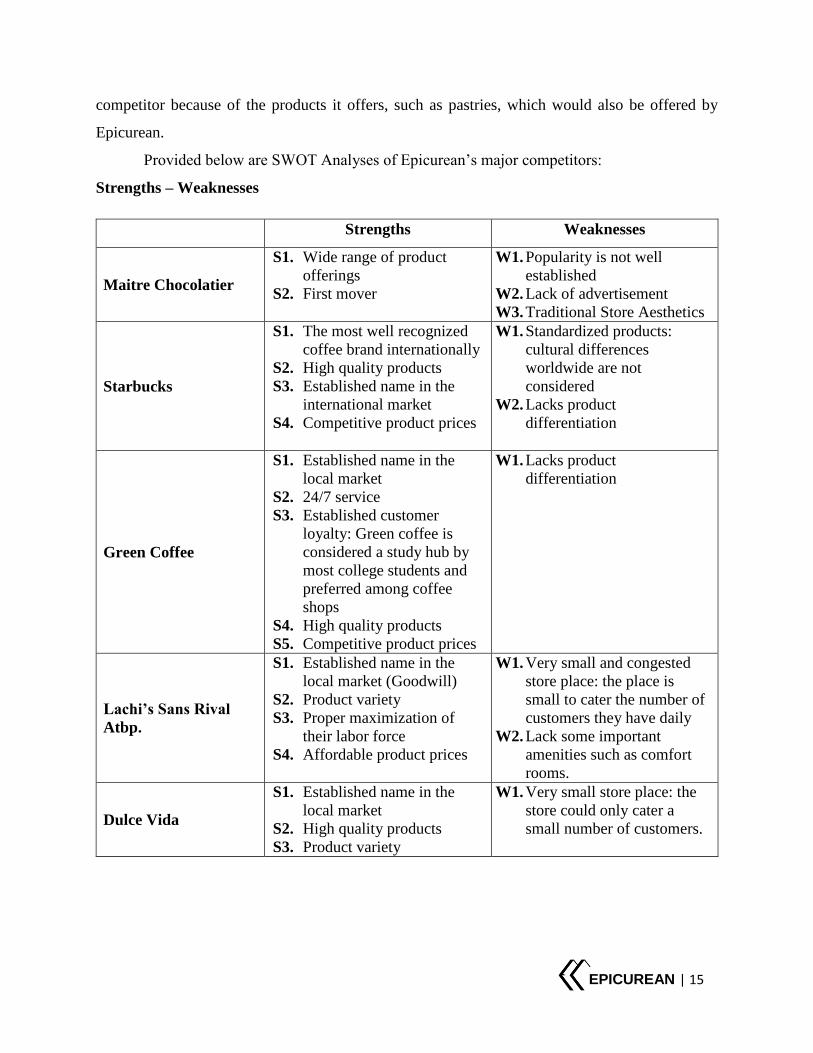

Provided below are SWOT Analyses of Epicurean’s major competitors:

Strengths – Weaknesses

Strengths Weaknesses

Maitre Chocolatier

S1. Wide range of product

offerings

S2. First mover

W1. Popularity is not well

established

W2. Lack of advertisement

W3. Traditional Store Aesthetics

Starbucks

S1. The most well recognized

coffee brand internationally

S2. High quality products

S3. Established name in the

international market

S4. Competitive product prices

W1. Standardized products:

cultural differences

worldwide are not

considered

W2. Lacks product

differentiation

Green Coffee

S1. Established name in the

local market

S2. 24/7 service

S3. Established customer

loyalty: Green coffee is

considered a study hub by

most college students and

preferred among coffee

shops

S4. High quality products

S5. Competitive product prices

W1. Lacks product

differentiation

Lachi’s Sans Rival

Atbp.

S1. Established name in the

local market (Goodwill)

S2. Product variety

S3. Proper maximization of

their labor force

S4. Affordable product prices

W1. Very small and congested

store place: the place is

small to cater the number of

customers they have daily

W2. Lack some important

amenities such as comfort

rooms.

Dulce Vida

S1. Established name in the

local market

S2. High quality products

S3. Product variety

W1. Very small store place: the

store could only cater a

small number of customers.

EPICUREAN | 16

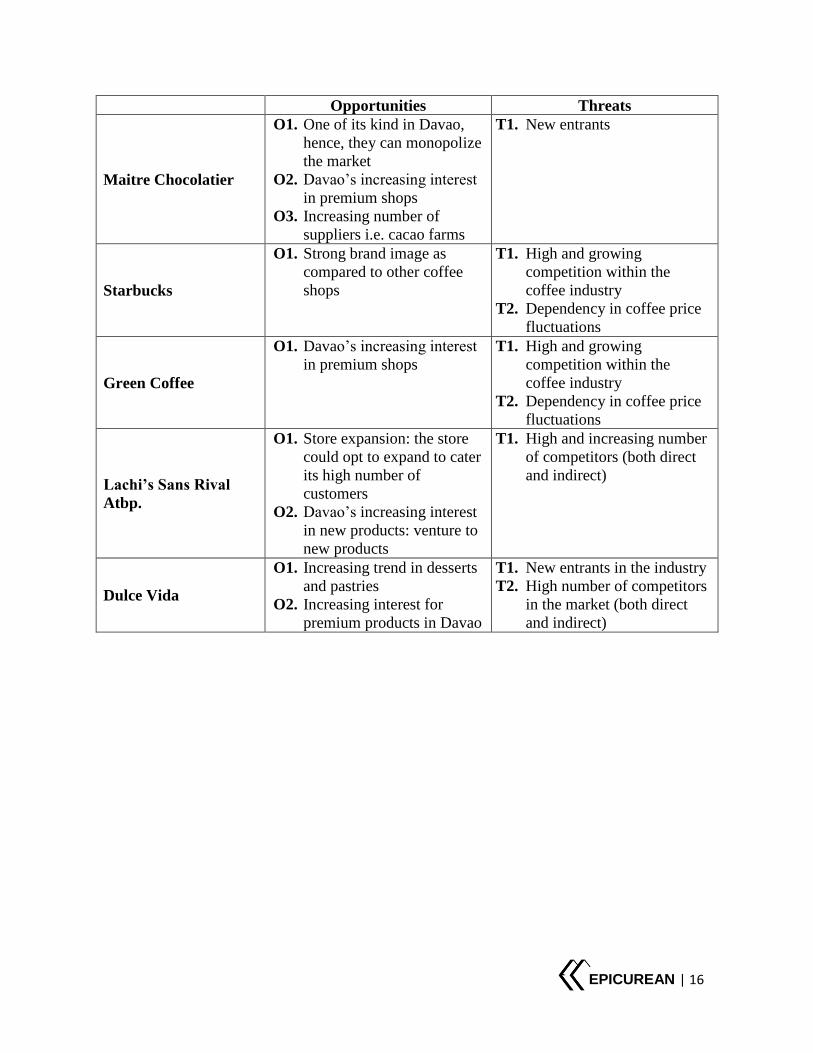

Opportunities Threats

Maitre Chocolatier

O1. One of its kind in Davao,

hence, they can monopolize

the market

O2. Davao’s increasing interest

in premium shops

O3. Increasing number of

suppliers i.e. cacao farms

T1. New entrants

Starbucks

O1. Strong brand image as

compared to other coffee

shops

T1. High and growing

competition within the

coffee industry

T2. Dependency in coffee price

fluctuations

Green Coffee

O1. Davao’s increasing interest

in premium shops

T1. High and growing

competition within the

coffee industry

T2. Dependency in coffee price

fluctuations

Lachi’s Sans Rival

Atbp.

O1. Store expansion: the store

could opt to expand to cater

its high number of

customers

O2. Davao’s increasing interest

in new products: venture to

new products

T1. High and increasing number

of competitors (both direct

and indirect)

Dulce Vida

O1. Increasing trend in desserts

and pastries

O2. Increasing interest for

premium products in Davao

T1. New entrants in the industry

T2. High number of competitors

in the market (both direct

and indirect)

EPICUREAN | 17

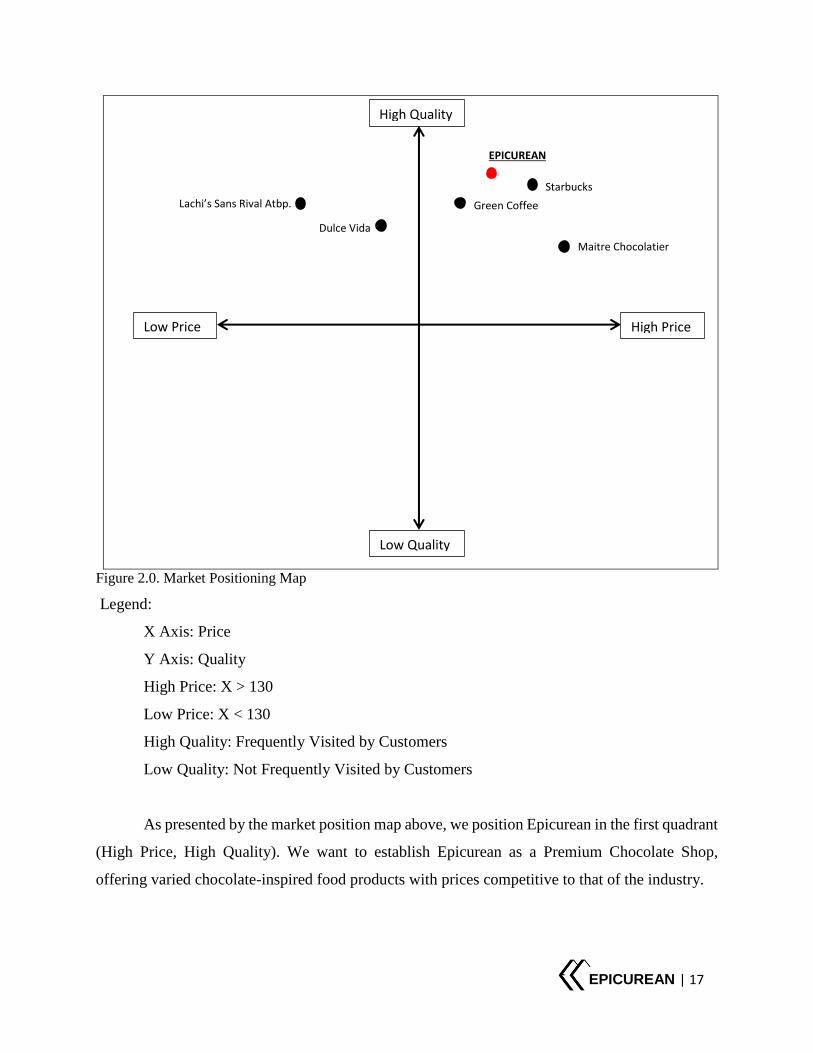

Figure 2.0. Market Positioning Map

Legend:

X Axis: Price

Y Axis: Quality

High Price: X > 130

Low Price: X < 130

High Quality: Frequently Visited by Customers

Low Quality: Not Frequently Visited by Customers

As presented by the market position map above, we position Epicurean in the first quadrant

(High Price, High Quality). We want to establish Epicurean as a Premium Chocolate Shop,

offering varied chocolate-inspired food products with prices competitive to that of the industry.

EPICUREAN

Dulce Vida

Lachi’s Sans Rival Atbp. Green Coffee

Starbucks

Maitre Chocolatier

Low Price High Price

High Quality

Low Quality

EPICUREAN | 18

DEMAND

I. Current Demand

Due to the lack of availability of historical data to determine the overall demand for

the products offered by Epicurean, a survey has been made to 524 respondents. The number

of respondents is 140 more than the recommended sample size by the Sample Size

Calculator. They are composed of randomly selected students and young professionals

aging from 15 to 34 years old in Davao City.

The following factors are taken into consideration in computing for the demand:

1. Health Issues Regarding Chocolate Products

There are people who cannot eat products with chocolates due to their health

implications. Some of these implications may be allergies and tonsillitis among

others. Those whose bodies react negatively to chocolates are those that are least

likely to buy the products involving chocolates.

2. Customer Preference

Varying human preferences challenge businesses to be able to increase

demand. The idea behind this is to find the group of people sharing the same

preferences that the business wants to cater. For a concept like a chocolate house,

only those who like the idea would possibly go in that place. If the chocolate house

offers chocolate cakes but not chocolate ice creams, only those preferring cakes

among those that like the idea of a chocolate house would determine the possible

customers of the chocolate house.

3. Frequency of Patronage and/or Consumption

The number of times a person consumes a product certainly affects the

product’s demand. The more a person consumes it in a day for example increases

the demand for that product in a day as well.

4. Income or Allowance

A person’s income and/or allowance would define that person’s capacity to

purchase the products available.

After taking into consideration the factors stated, a formula was derived to estimate

the overall demand of the products offered by Epicurean in Davao City. The procedure in

arriving at the estimated demand is as follows:

EPICUREAN | 19

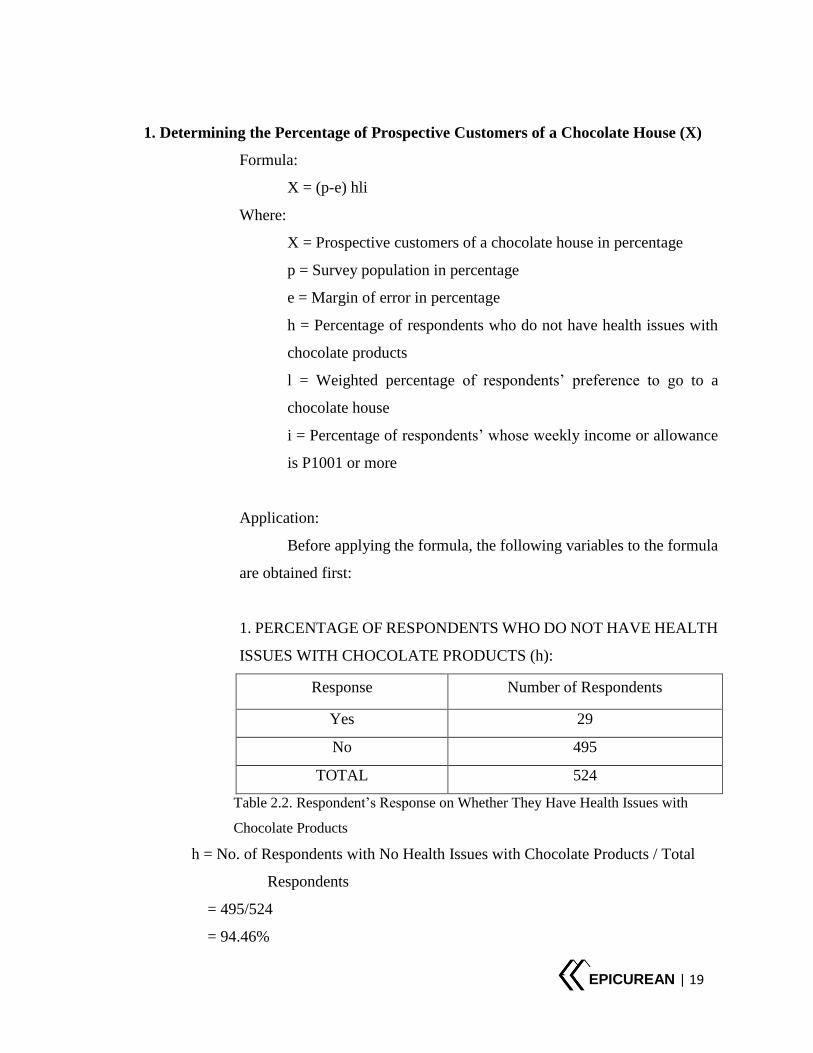

1. Determining the Percentage of Prospective Customers of a Chocolate House (X)

Formula:

X = (p-e) hli

Where:

X = Prospective customers of a chocolate house in percentage

p = Survey population in percentage

e = Margin of error in percentage

h = Percentage of respondents who do not have health issues with

chocolate products

l = Weighted percentage of respondents’ preference to go to a

chocolate house

i = Percentage of respondents’ whose weekly income or allowance

is P1001 or more

Application:

Before applying the formula, the following variables to the formula

are obtained first:

1. PERCENTAGE OF RESPONDENTS WHO DO NOT HAVE HEALTH

ISSUES WITH CHOCOLATE PRODUCTS (h):

Response Number of Respondents

Yes 29

No 495

TOTAL 524

Table 2.2. Respondent’s Response on Whether They Have Health Issues with

Chocolate Products

h = No. of Respondents with No Health Issues with Chocolate Products / Total

Respondents

= 495/524

= 94.46%

EPICUREAN | 20

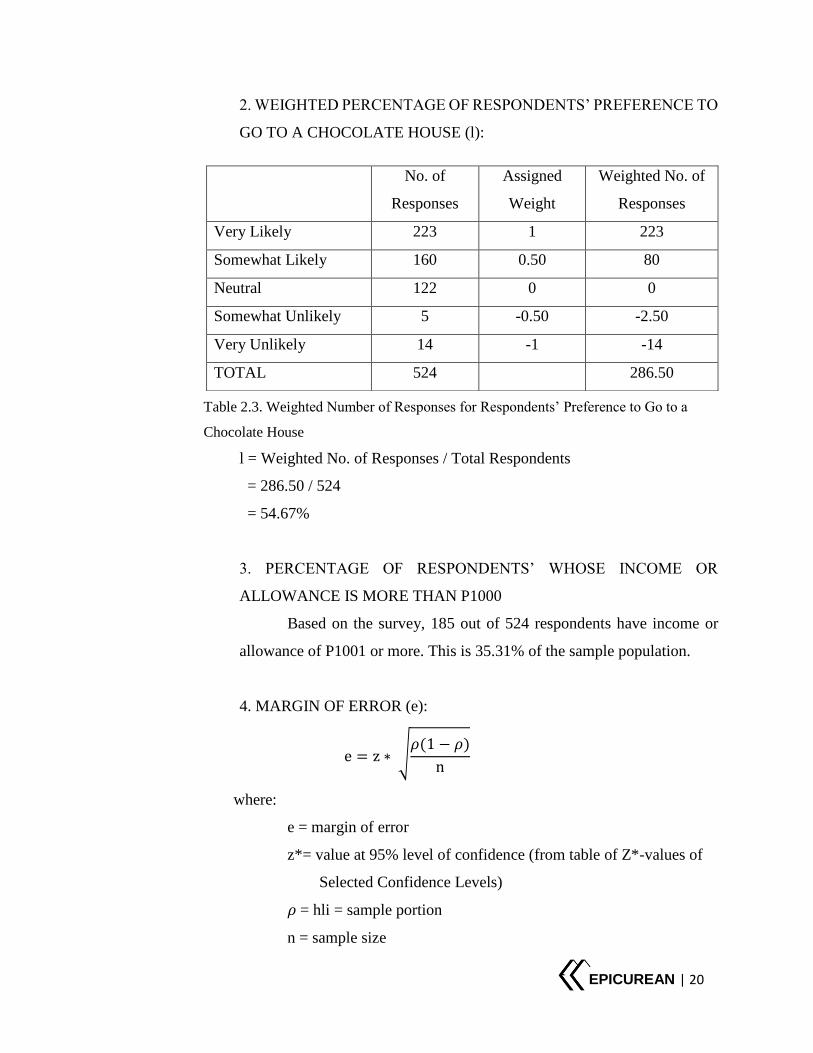

2. WEIGHTED PERCENTAGE OF RESPONDENTS’ PREFERENCE TO

GO TO A CHOCOLATE HOUSE (l):

Table 2.3. Weighted Number of Responses for Respondents’ Preference to Go to a

Chocolate House

l = Weighted No. of Responses / Total Respondents

= 286.50 / 524

= 54.67%

3. PERCENTAGE OF RESPONDENTS’ WHOSE INCOME OR

ALLOWANCE IS MORE THAN P1000

Based on the survey, 185 out of 524 respondents have income or

allowance of P1001 or more. This is 35.31% of the sample population.

4. MARGIN OF ERROR (e):

e = z ∗ √𝜌(1 − 𝜌)

n

where:

e = margin of error

z*= value at 95% level of confidence (from table of Z*-values of

Selected Confidence Levels)

𝜌 = hli = sample portion

n = sample size

No. of

Responses

Assigned

Weight

Weighted No. of

Responses

Very Likely 223 1 223

Somewhat Likely 160 0.50 80

Neutral 122 0 0

Somewhat Unlikely 5 -0.50 -2.50

Very Unlikely 14 -1 -14

TOTAL 524 286.50

EPICUREAN | 21

Computation:

e = 1.96 ∗ √[(0.9446 𝑋 0.5467 𝑋 0.3531)][1 − (0.9446 𝑋 0.5467 𝑋 0.3531)]

524

e = 0.0331 ≈ 3%

Hence,

X = (100% - 3%)(94.46%)(54.67%)(35.31%)

= 17.69%

The result shows that 17.69% of the sample constitutes the potential

customers of chocolate house.

2. Solving the Target Market (per Week) in the Population (n)

Target Market (n) represents the group that the business would be aimed.

The target market for Epicurean is obtained by applying the percentage of

prospective customers to the actual population and the product to be defined by the

frequency of going to a chocolate house.

Formula:

n = N x ( X ) x F

where

n = Target market

N = Actual population

X = Percentage of prospective customers of chocolate house

F = Frequency of going to a chocolate house

The following variables to the formula are obtained first:

1. ACTUAL POPULATION (N):

According to results of 2010 Census of Population and Housing,

Davao City has a total population of 1,449,296 with household population

EPICUREAN | 22

of 1,443,890. Out of that, the household population of people aging from 15

to 34 years old is 540,076.

Hence, N = 540,076.

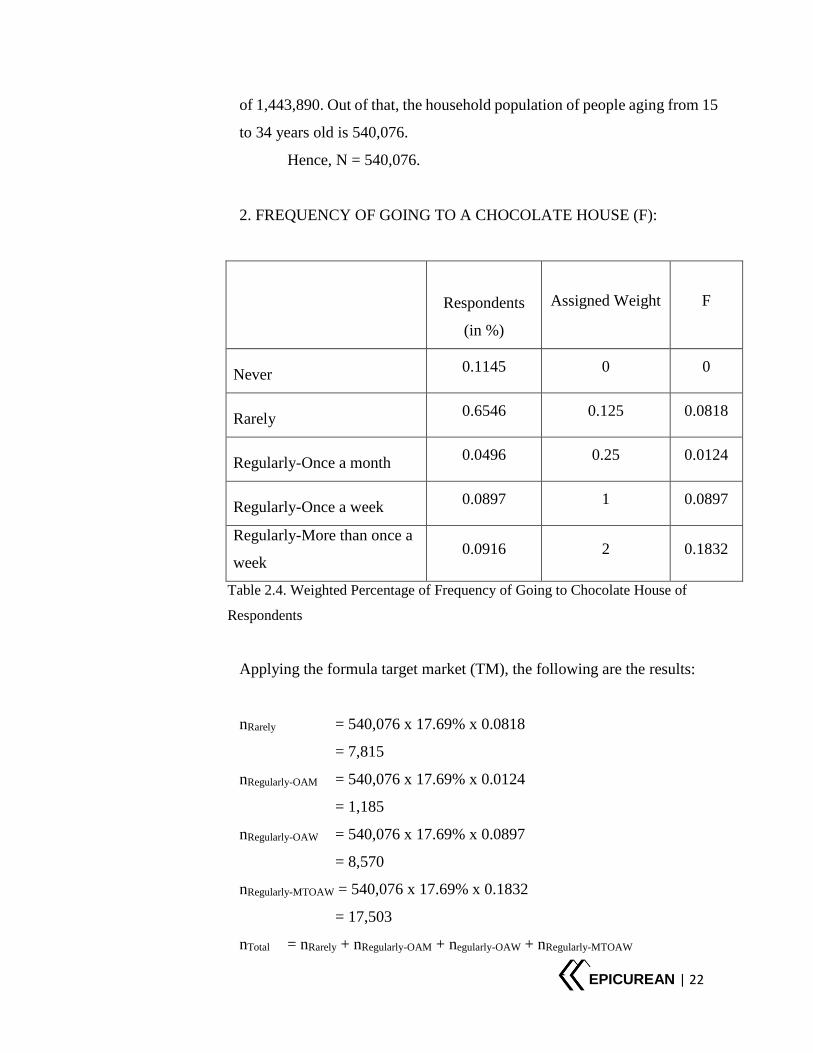

2. FREQUENCY OF GOING TO A CHOCOLATE HOUSE (F):

Respondents

(in %)

Assigned Weight

F

Never 0.1145 0 0

Rarely 0.6546 0.125 0.0818

Regularly-Once a month 0.0496 0.25 0.0124

Regularly-Once a week 0.0897 1 0.0897

Regularly-More than once a

week 0.0916 2 0.1832

Table 2.4. Weighted Percentage of Frequency of Going to Chocolate House of

Respondents

Applying the formula target market (TM), the following are the results:

nRarely = 540,076 x 17.69% x 0.0818

= 7,815

nRegularly-OAM = 540,076 x 17.69% x 0.0124

= 1,185

nRegularly-OAW = 540,076 x 17.69% x 0.0897

= 8,570

nRegularly-MTOAW = 540,076 x 17.69% x 0.1832

= 17,503

nTotal = nRarely + nRegularly-OAM + negularly-OAW + nRegularly-MTOAW

EPICUREAN | 23

= 7,815 + 1,185 + 8,570 + 17,503

= 35,073

The total target market (per week) is 35,073.

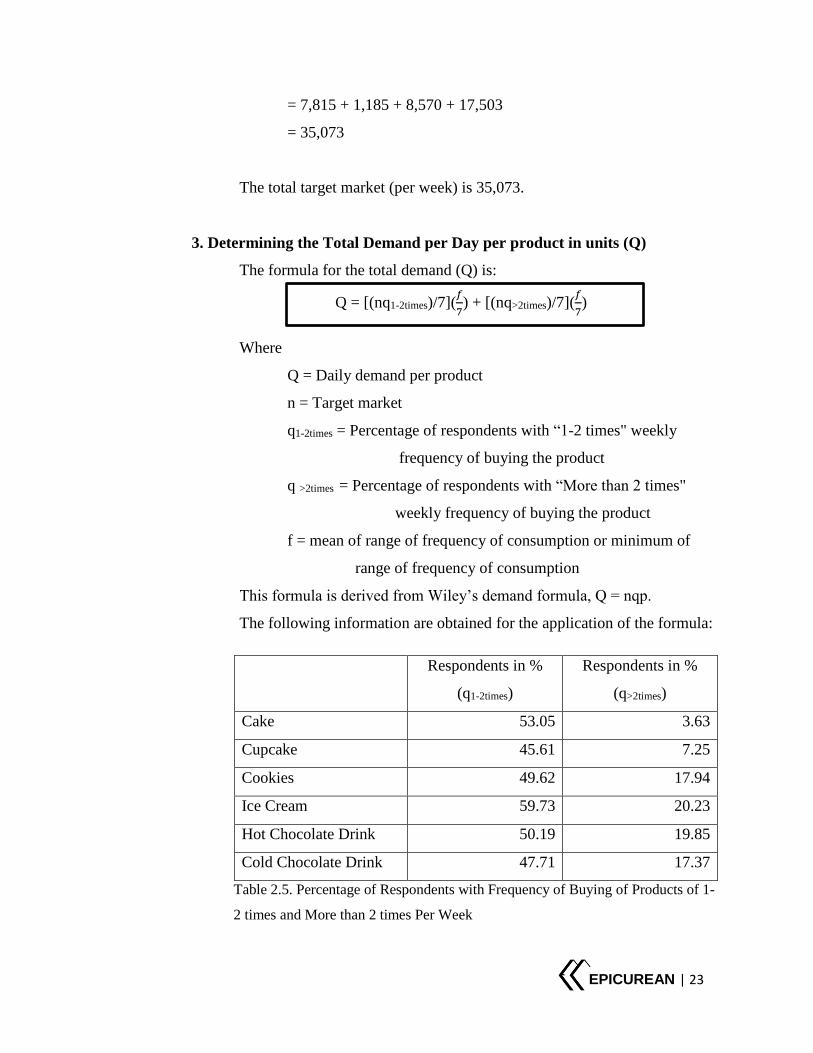

3. Determining the Total Demand per Day per product in units (Q)

The formula for the total demand (Q) is:

Q = [(nq1-2times)/7](𝑓

7) + [(nq>2times)/7](

𝑓

7)

Where

Q = Daily demand per product

n = Target market

q1-2times = Percentage of respondents with “1-2 times" weekly

frequency of buying the product

q >2times = Percentage of respondents with “More than 2 times"

weekly frequency of buying the product

f = mean of range of frequency of consumption or minimum of

range of frequency of consumption

This formula is derived from Wiley’s demand formula, Q = nqp.

The following information are obtained for the application of the formula:

Table 2.5. Percentage of Respondents with Frequency of Buying of Products of 1-

2 times and More than 2 times Per Week

Respondents in %

(q1-2times)

Respondents in %

(q>2times)

Cake 53.05 3.63

Cupcake 45.61 7.25

Cookies 49.62 17.94

Ice Cream 59.73 20.23

Hot Chocolate Drink 50.19 19.85

Cold Chocolate Drink 47.71 17.37

EPICUREAN | 24

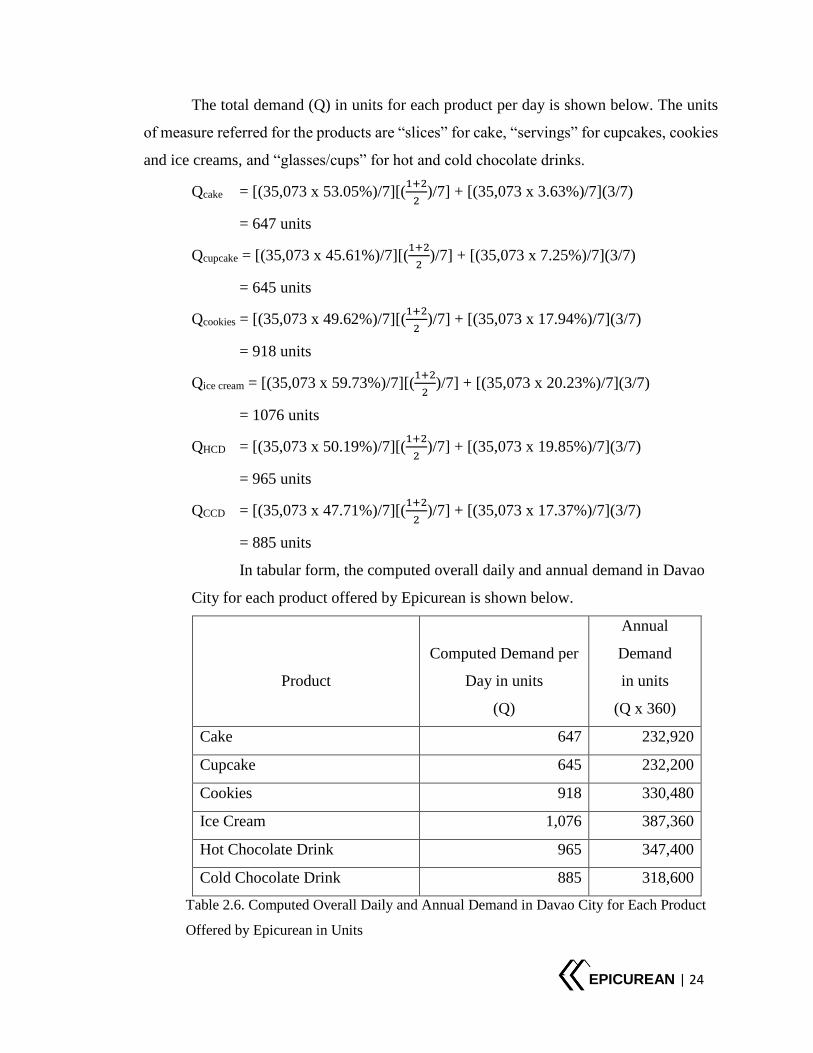

The total demand (Q) in units for each product per day is shown below. The units

of measure referred for the products are “slices” for cake, “servings” for cupcakes, cookies

and ice creams, and “glasses/cups” for hot and cold chocolate drinks.

Qcake = [(35,073 x 53.05%)/7][(1+2

2)/7] + [(35,073 x 3.63%)/7](3/7)

= 647 units

Qcupcake = [(35,073 x 45.61%)/7][(1+2

2)/7] + [(35,073 x 7.25%)/7](3/7)

= 645 units

Qcookies = [(35,073 x 49.62%)/7][(1+2

2)/7] + [(35,073 x 17.94%)/7](3/7)

= 918 units

Qice cream = [(35,073 x 59.73%)/7][(1+2

2)/7] + [(35,073 x 20.23%)/7](3/7)

= 1076 units

QHCD = [(35,073 x 50.19%)/7][(1+2

2)/7] + [(35,073 x 19.85%)/7](3/7)

= 965 units

QCCD = [(35,073 x 47.71%)/7][(1+2

2)/7] + [(35,073 x 17.37%)/7](3/7)

= 885 units

In tabular form, the computed overall daily and annual demand in Davao

City for each product offered by Epicurean is shown below.

Product

Computed Demand per

Day in units

(Q)

Annual

Demand

in units

(Q x 360)

Cake 647 232,920

Cupcake 645 232,200

Cookies 918 330,480

Ice Cream 1,076 387,360

Hot Chocolate Drink 965 347,400

Cold Chocolate Drink 885 318,600

Table 2.6. Computed Overall Daily and Annual Demand in Davao City for Each Product

Offered by Epicurean in Units

EPICUREAN | 25

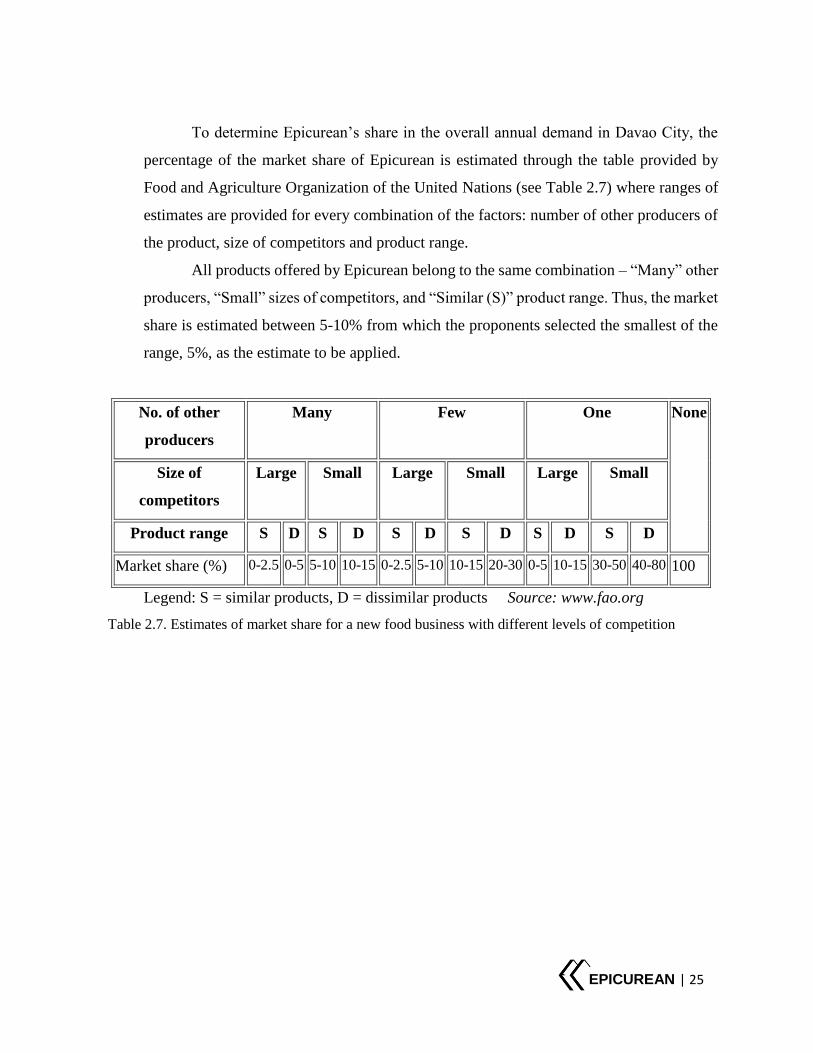

To determine Epicurean’s share in the overall annual demand in Davao City, the

percentage of the market share of Epicurean is estimated through the table provided by

Food and Agriculture Organization of the United Nations (see Table 2.7) where ranges of

estimates are provided for every combination of the factors: number of other producers of

the product, size of competitors and product range.

All products offered by Epicurean belong to the same combination – “Many” other

producers, “Small” sizes of competitors, and “Similar (S)” product range. Thus, the market

share is estimated between 5-10% from which the proponents selected the smallest of the

range, 5%, as the estimate to be applied.

No. of other

producers

Many Few One None

Size of

competitors

Large Small Large Small Large Small

Product range S D S D S D S D S D S D

Market share (%) 0-2.5 0-5 5-10 10-15 0-2.5 5-10 10-15 20-30 0-5 10-15 30-50 40-80 100

Legend: S = similar products, D = dissimilar products Source: www.fao.org

Table 2.7. Estimates of market share for a new food business with different levels of competition

EPICUREAN | 26

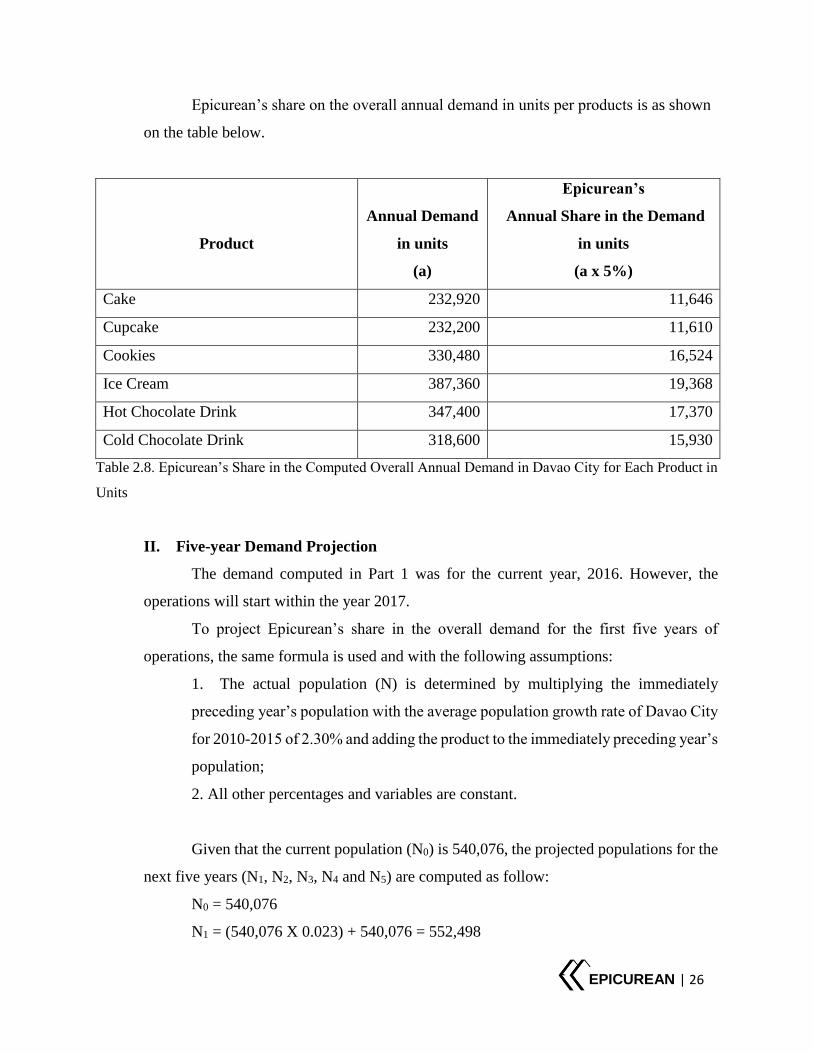

Epicurean’s share on the overall annual demand in units per products is as shown

on the table below.

Product

Annual Demand

in units

(a)

Epicurean’s

Annual Share in the Demand

in units

(a x 5%)

Cake 232,920 11,646

Cupcake 232,200 11,610

Cookies 330,480 16,524

Ice Cream 387,360 19,368

Hot Chocolate Drink 347,400 17,370

Cold Chocolate Drink 318,600 15,930

Table 2.8. Epicurean’s Share in the Computed Overall Annual Demand in Davao City for Each Product in

Units

II. Five-year Demand Projection

The demand computed in Part 1 was for the current year, 2016. However, the

operations will start within the year 2017.

To project Epicurean’s share in the overall demand for the first five years of

operations, the same formula is used and with the following assumptions:

1. The actual population (N) is determined by multiplying the immediately

preceding year’s population with the average population growth rate of Davao City

for 2010-2015 of 2.30% and adding the product to the immediately preceding year’s

population;

2. All other percentages and variables are constant.

Given that the current population (N0) is 540,076, the projected populations for the

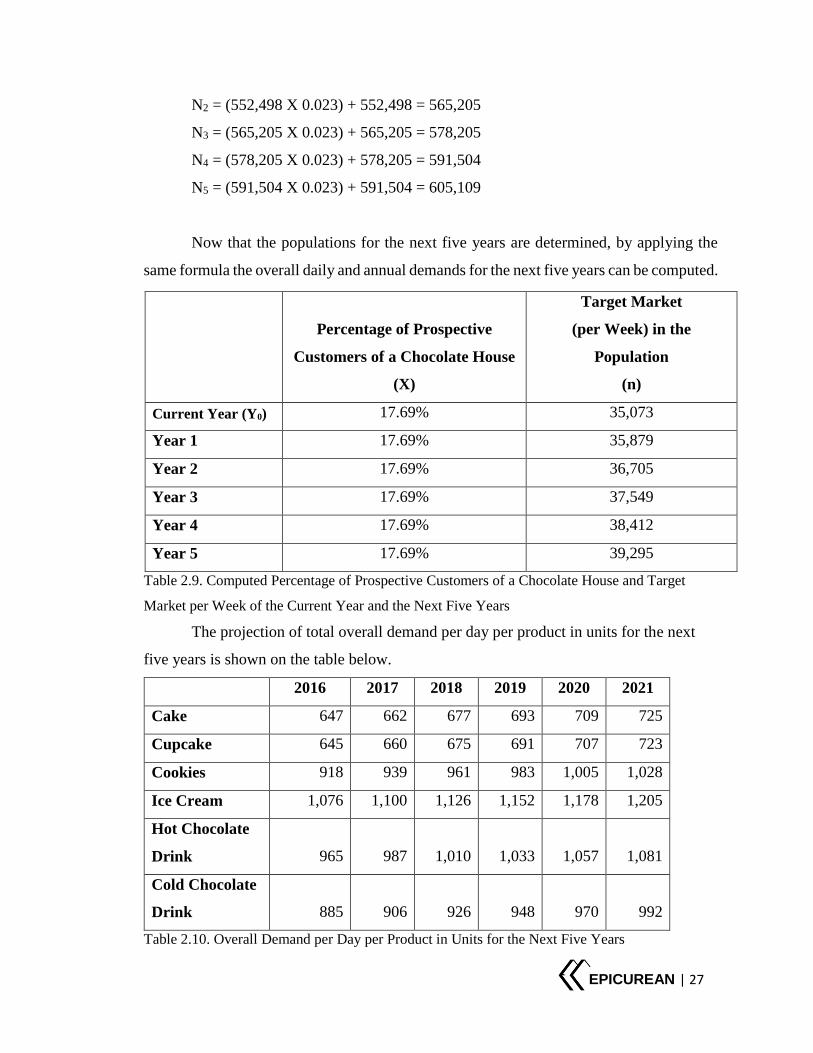

next five years (N1, N2, N3, N4 and N5) are computed as follow:

N0 = 540,076

N1 = (540,076 X 0.023) + 540,076 = 552,498

EPICUREAN | 27

N2 = (552,498 X 0.023) + 552,498 = 565,205

N3 = (565,205 X 0.023) + 565,205 = 578,205

N4 = (578,205 X 0.023) + 578,205 = 591,504

N5 = (591,504 X 0.023) + 591,504 = 605,109

Now that the populations for the next five years are determined, by applying the

same formula the overall daily and annual demands for the next five years can be computed.

Table 2.9. Computed Percentage of Prospective Customers of a Chocolate House and Target

Market per Week of the Current Year and the Next Five Years

The projection of total overall demand per day per product in units for the next

five years is shown on the table below.

2016 2017 2018 2019 2020 2021

Cake 647 662 677 693 709 725

Cupcake 645 660 675 691 707 723

Cookies 918 939 961 983 1,005 1,028

Ice Cream 1,076 1,100 1,126 1,152 1,178 1,205

Hot Chocolate

Drink 965 987 1,010 1,033 1,057 1,081

Cold Chocolate

Drink 885 906 926 948 970 992

Table 2.10. Overall Demand per Day per Product in Units for the Next Five Years

Percentage of Prospective

Customers of a Chocolate House

(X)

Target Market

(per Week) in the

Population

(n)

Current Year (Y0) 17.69% 35,073

Year 1 17.69% 35,879

Year 2 17.69% 36,705

Year 3 17.69% 37,549

Year 4 17.69% 38,412

Year 5 17.69% 39,295

EPICUREAN | 28

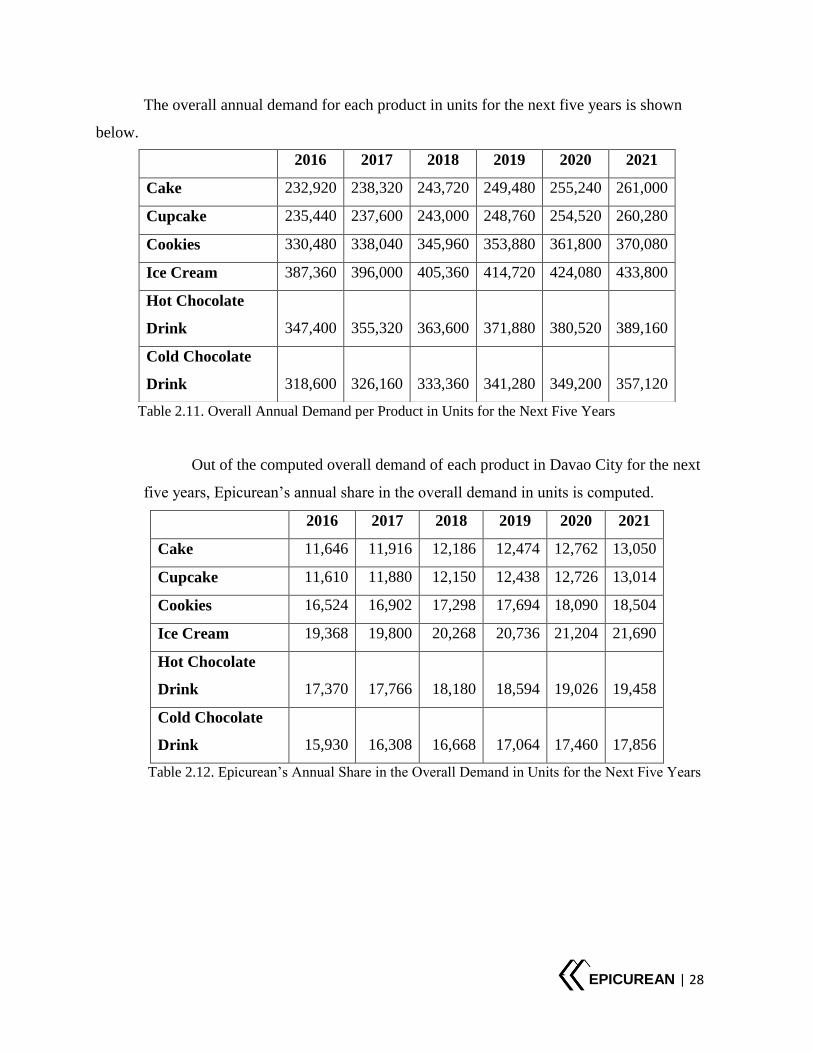

The overall annual demand for each product in units for the next five years is shown

below.

Table 2.11. Overall Annual Demand per Product in Units for the Next Five Years

Out of the computed overall demand of each product in Davao City for the next

five years, Epicurean’s annual share in the overall demand in units is computed.

2016 2017 2018 2019 2020 2021

Cake 11,646 11,916 12,186 12,474 12,762 13,050

Cupcake 11,610 11,880 12,150 12,438 12,726 13,014

Cookies 16,524 16,902 17,298 17,694 18,090 18,504

Ice Cream 19,368 19,800 20,268 20,736 21,204 21,690

Hot Chocolate

Drink 17,370 17,766 18,180 18,594 19,026 19,458

Cold Chocolate

Drink 15,930 16,308 16,668 17,064 17,460 17,856

Table 2.12. Epicurean’s Annual Share in the Overall Demand in Units for the Next Five Years

2016 2017 2018 2019 2020 2021

Cake 232,920 238,320 243,720 249,480 255,240 261,000

Cupcake 235,440 237,600 243,000 248,760 254,520 260,280

Cookies 330,480 338,040 345,960 353,880 361,800 370,080

Ice Cream 387,360 396,000 405,360 414,720 424,080 433,800

Hot Chocolate

Drink 347,400 355,320 363,600 371,880 380,520 389,160

Cold Chocolate

Drink 318,600 326,160 333,360 341,280 349,200 357,120

EPICUREAN | 29

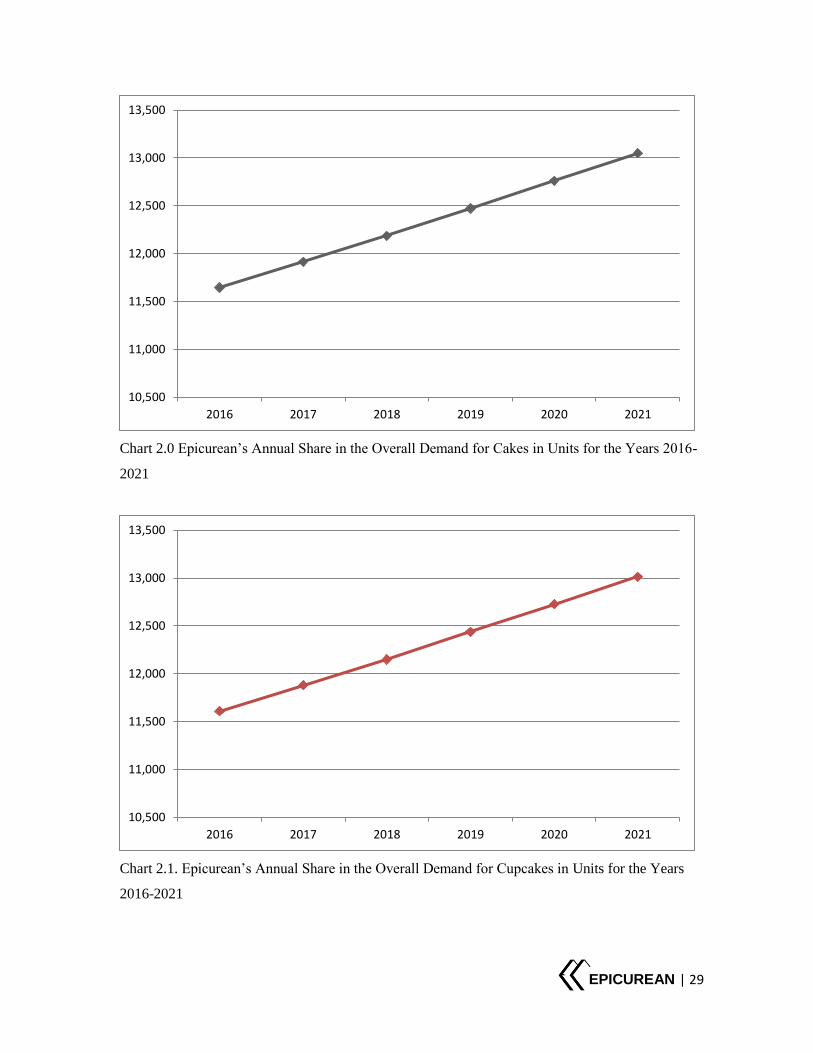

Chart 2.0 Epicurean’s Annual Share in the Overall Demand for Cakes in Units for the Years 2016-

2021

Chart 2.1. Epicurean’s Annual Share in the Overall Demand for Cupcakes in Units for the Years

2016-2021

10,500

11,000

11,500

12,000

12,500

13,000

13,500

2016 2017 2018 2019 2020 2021

10,500

11,000

11,500

12,000

12,500

13,000

13,500

2016 2017 2018 2019 2020 2021

EPICUREAN | 30

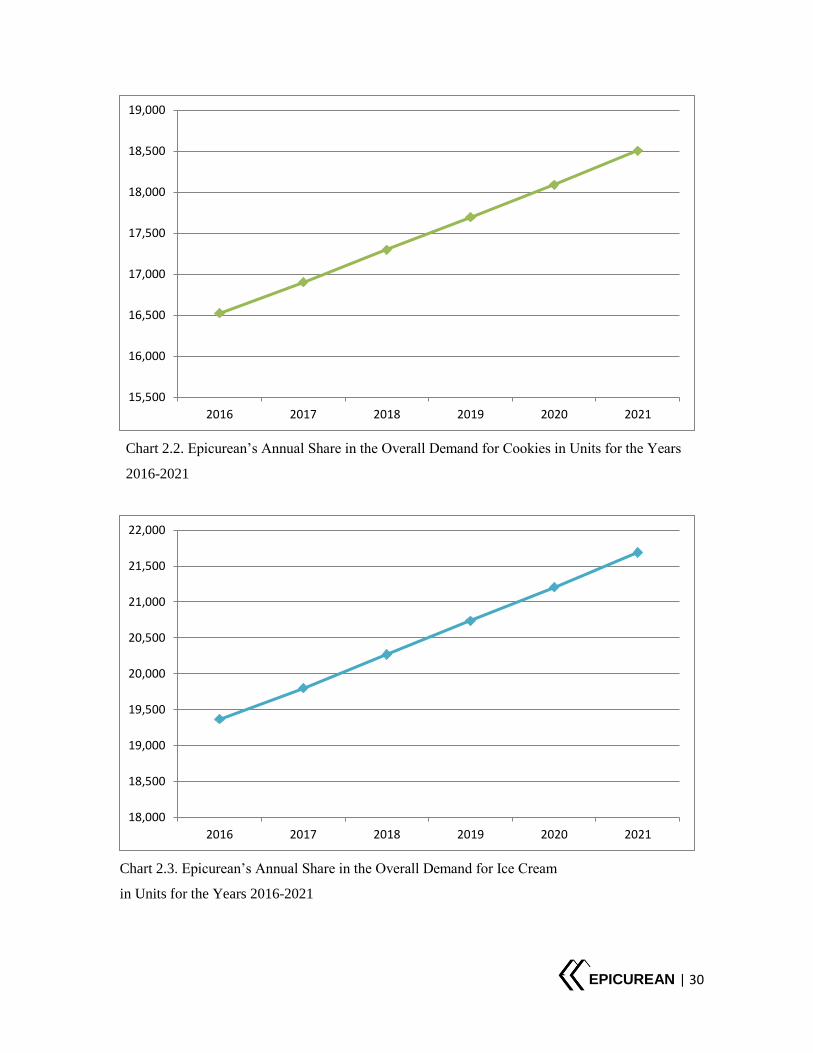

Chart 2.2. Epicurean’s Annual Share in the Overall Demand for Cookies in Units for the Years

2016-2021

Chart 2.3. Epicurean’s Annual Share in the Overall Demand for Ice Cream

in Units for the Years 2016-2021

15,500

16,000

16,500

17,000

17,500

18,000

18,500

19,000

2016 2017 2018 2019 2020 2021

18,000

18,500

19,000

19,500

20,000

20,500

21,000

21,500

22,000

2016 2017 2018 2019 2020 2021

EPICUREAN | 31

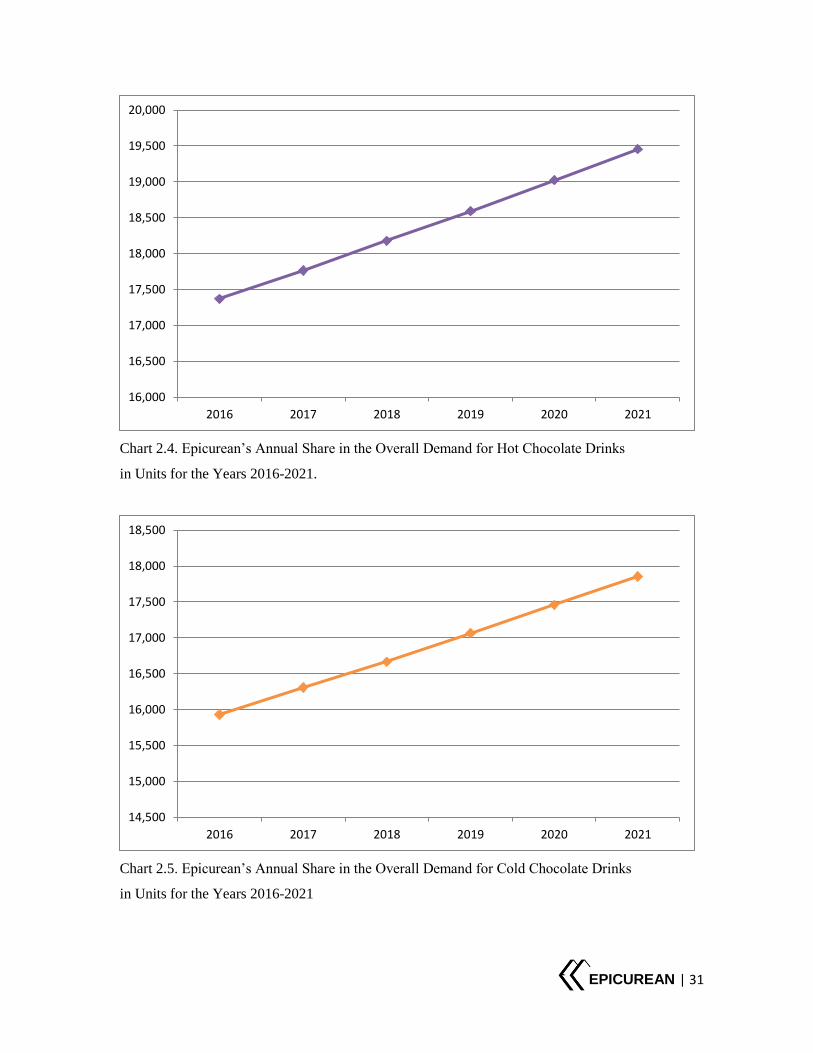

Chart 2.4. Epicurean’s Annual Share in the Overall Demand for Hot Chocolate Drinks

in Units for the Years 2016-2021.

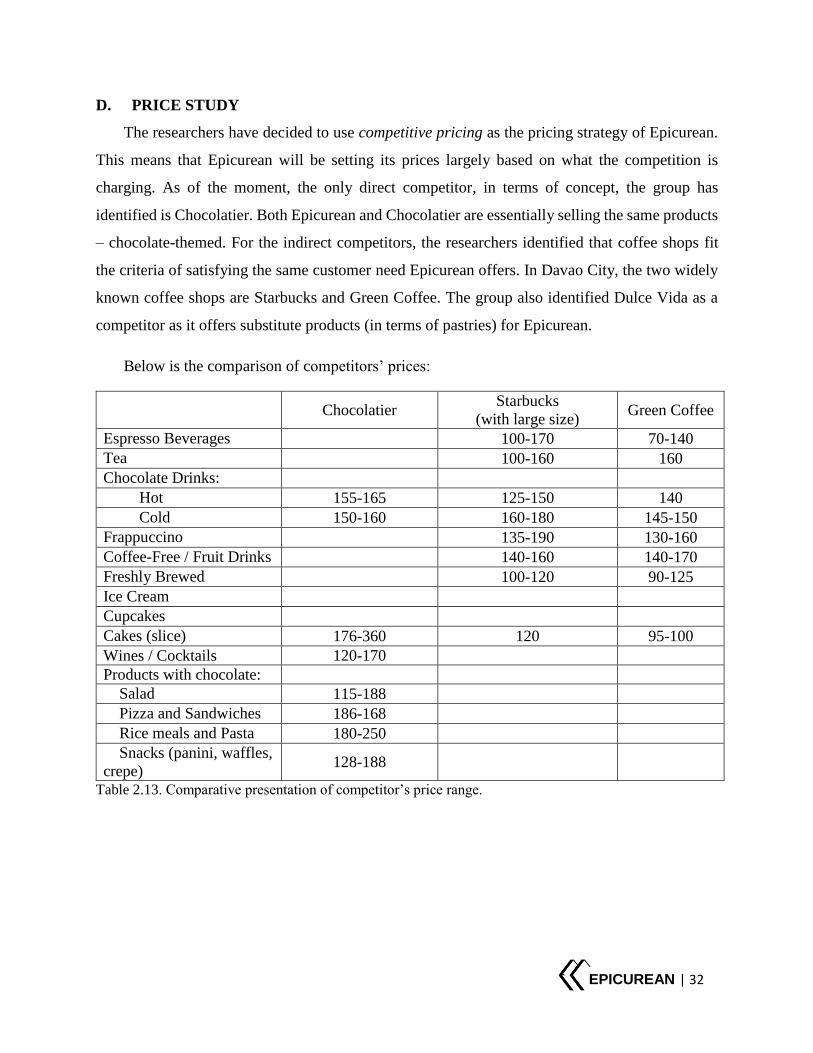

Chart 2.5. Epicurean’s Annual Share in the Overall Demand for Cold Chocolate Drinks

in Units for the Years 2016-2021

16,000

16,500

17,000

17,500

18,000

18,500

19,000

19,500

20,000

2016 2017 2018 2019 2020 2021

14,500

15,000

15,500

16,000

16,500

17,000

17,500

18,000

18,500

2016 2017 2018 2019 2020 2021

EPICUREAN | 32

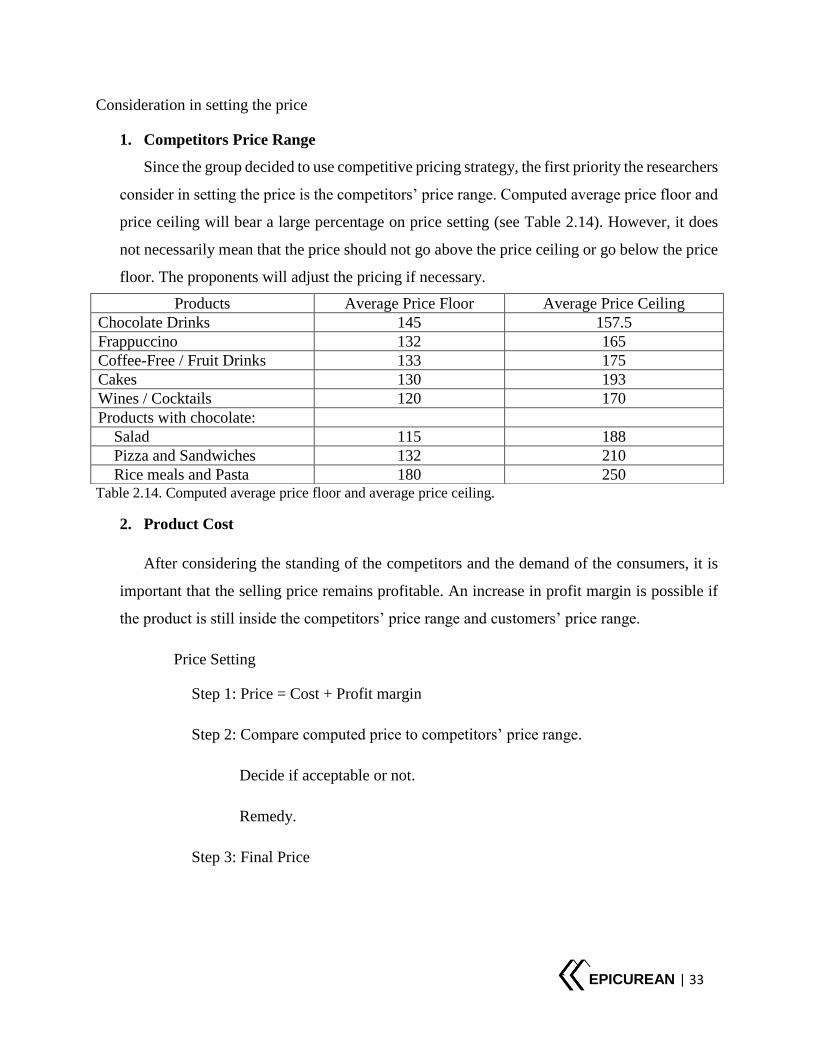

D. PRICE STUDY

The researchers have decided to use competitive pricing as the pricing strategy of Epicurean.

This means that Epicurean will be setting its prices largely based on what the competition is

charging. As of the moment, the only direct competitor, in terms of concept, the group has

identified is Chocolatier. Both Epicurean and Chocolatier are essentially selling the same products

– chocolate-themed. For the indirect competitors, the researchers identified that coffee shops fit

the criteria of satisfying the same customer need Epicurean offers. In Davao City, the two widely

known coffee shops are Starbucks and Green Coffee. The group also identified Dulce Vida as a

competitor as it offers substitute products (in terms of pastries) for Epicurean.

Below is the comparison of competitors’ prices:

Chocolatier Starbucks

(with large size) Green Coffee

Espresso Beverages 100-170 70-140

Tea 100-160 160

Chocolate Drinks:

Hot 155-165 125-150 140

Cold 150-160 160-180 145-150

Frappuccino 135-190 130-160

Coffee-Free / Fruit Drinks 140-160 140-170

Freshly Brewed 100-120 90-125

Ice Cream

Cupcakes

Cakes (slice) 176-360 120 95-100

Wines / Cocktails 120-170

Products with chocolate:

Salad 115-188

Pizza and Sandwiches 186-168

Rice meals and Pasta 180-250

Snacks (panini, waffles,

crepe) 128-188

Table 2.13. Comparative presentation of competitor’s price range.

EPICUREAN | 33

Consideration in setting the price

1. Competitors Price Range

Since the group decided to use competitive pricing strategy, the first priority the researchers

consider in setting the price is the competitors’ price range. Computed average price floor and

price ceiling will bear a large percentage on price setting (see Table 2.14). However, it does

not necessarily mean that the price should not go above the price ceiling or go below the price

floor. The proponents will adjust the pricing if necessary.

Table 2.14. Computed average price floor and average price ceiling.

2. Product Cost

After considering the standing of the competitors and the demand of the consumers, it is

important that the selling price remains profitable. An increase in profit margin is possible if

the product is still inside the competitors’ price range and customers’ price range.

Price Setting

Step 1: Price = Cost + Profit margin

Step 2: Compare computed price to competitors’ price range.

Decide if acceptable or not.

Remedy.

Step 3: Final Price

Products Average Price Floor Average Price Ceiling

Chocolate Drinks 145 157.5

Frappuccino 132 165

Coffee-Free / Fruit Drinks 133 175

Cakes 130 193

Wines / Cocktails 120 170

Products with chocolate:

Salad 115 188

Pizza and Sandwiches 132 210

Rice meals and Pasta 180 250

EPICUREAN | 34

Factors Affecting Change in Selling Price

1. Cost

In fixing the price, Epicurean should consider the cost involved in producing and

selling its products. This includes the product costs and period costs. The substantial

increase and decrease of these costs affects the profitability of the company and arises

the need for change in selling price. Presented below are the changes in the prices of

Epicurean’s main ingredient, chocolates. The price of chocolates increased roughly by

20%.

Chocolate

Weight

YEAR 2014 YEAR 2016

Price per Php Price per Kilo Price per Php Price per Kilo

100-gram bar 120.00 - 150.00 -

504 grams 264.00 - 330.00 -

1000 grams 440.00 440.00 550.00 550.00

2000 grams 840.00 420.00 1050.00 525.00

750-gram block 336.00 448.00 420.00 560.00

1600-gram block 640.00 400.00 800.00 500.00

Table 2.15. Changes in the prices of Malagos Chocolates; for the last two years, the prices increased by

20%.

2. Availability of substitute / similar products

Availability of substitute products increases competition in the market. New

entrants in the industry may offer more innovative products or there may be a product

development by the existing competitors. In order for the company to remain

competitive, it should also make product innovations which may directly affect the

product pricing.

3. Change in predetermined objectives

Epicurean should consider the objectives of the firm in fixing its prices. For

example, if the firm plans to have an increase to its return, then it may charge a higher

price and if the firm plans to capture a large market share, then it may charge a lower

price. (Chand, n.d.)

EPICUREAN | 35

4. Image of the firm

The change of price of the product may also be determined on the basis of the image

of the firm in the market. In the long run, if Epicurean will be able to establish its name,

it can demand to increase its price as it enjoys goodwill in the market. (Chand, n.d.)

5. Economic Conditions

In establishing the price, the prevailing economic conditions should also be

considered. For instance, during period of prosperity, people are much willing to buy

because they have more money and so, marketers can take advantage of the price setting.

While during recession, consumers have lesser money to spend, and so, prices are also

expected to go down.

E. MARKETING PROGRAM

Marketing is a form of communication between the entity and its customers. It includes

advertising, selling and distributing the products to the people. Moreover, it can be conducted in

various types and techniques.

i. Marketing Practices of Major Competitors

1. Maitre Chocolatier Boutique and Cafe (Davao Branch)

Maitre Chocolatier makes use of social media advertising in promoting their

store. They have a Facebook account which they update from time to time. They are

also featured in different food blogs in Davao. They created a website, www.m-

chocolatier.com, which highlights the products they are selling.

2. Lachi’s Sans Rival Atbp.

Lachi’s rely mostly on word-of-mouth advertising. This advertising scheme

involves the customers of Lachi’s and their sharing of their dining experience in the

store. It is an effective marketing tool because people put more credibility on the

comments of their friends and acquaintances. Lachi’s incurs zero cost with this

advertising. Lachi’s also have a Facebook page.

EPICUREAN | 36

Lachi’s is also featured in food blogs and food reviews. When you search

Google for the top pastries in Davao, Lachi’s is usually on the list. Tourists mostly rely

on this method when they are looking for an establishment to visit.

3. Green Coffee

Green Coffee employs social media advertising in promoting their store and

their products. They have a Facebook page that they update once in a while. Word-of-

mouth advertising is also utilized by Green Coffee.

4. Starbucks

Starbucks uses social media advertising in promoting their store and their

products. They have a Facebook page that they update every now and then.

They publicize promos such as “Buy 1, Take 1” schemes and other creatively

thought gimmicks to spice up their customer relations. They also make use of word-of-

mouth advertising.

5. Dulce Vida Bakery + Resto

Dulce Vida rely on word-of-mouth advertising. They have a Facebook page,

although unofficial, in which customers may rate and leave a comment. They received

a 4.8 out of 5-star rating in Facebook. They rely on their customers as they post pictures

of their cakes which attracts new customers to try their products.

They are also advertised in different blogs which highlight their menu like the

davaofoodtrips.com and libotero.com.

ii. Proposed Marketing Program

1. Marketing Mix

PRODUCT STRATEGY

Epicurean will offer a mixture of product and service to its clientele. It will

serve chocolate products highlighting Davao chocolates. At the same time, it will

also offer quality customer service.