EPFL – leaving things right for your family is an Authorised Representative of RI Advice Group Pty...

48

EPFL – leaving things right for your family <Adviser’s Name> <Adviser name> is an Authorised Representative of RI Advice Group Pty Ltd

-

Upload

cathleen-skinner -

Category

Documents

-

view

218 -

download

0

Transcript of EPFL – leaving things right for your family is an Authorised Representative of RI Advice Group Pty...

EPFL – leaving things right for your family<Adviser’s Name>

<Adviser name> is an Authorised Representative of RI Advice Group Pty Ltd

2

Disclaimer

RI Advice Group Pty Ltd, ABN 23 001 774 125, holds Australian Financial Services Licence Number 238429 and is licensed to provide financial product advice and deal in financial products such as: deposit and payment products, derivatives, life products, managed investment schemes including investor directed portfolio services, securities, superannuation, Retirement Savings Accounts.

The information presented in this seminar is of a general nature only and neither represents nor is intended to be specific advice on any particular matter. RI Advice Group strongly suggests that no person should act specifically on the basis of the information contained herein but should obtain appropriate professional advice based on their own circumstances.

Important Notice

3

• Family succession planning – the overall picture

• The importance of a Will

• Superannuation

• Taxes

• The next generation

• The value of professional advice

Agenda

4

5

Family succession planning extends to…

• Superannuation

• Life insurance

• Joint assets

• Asset protection

• Tax issues

• Power of Attorney

• Recording key information so it is accessible

• Educating your dependants and more…

A standard Will may not be enough to protect assets and provide tax relief for beneficiaries.

6

Having the most appropriate net assets, placed in the hands of those you want to receive it, considering the where, who, when!

What is family succession planning?

7

Family succession planning

More than a plan to distribute certain assets

A Will

Instructions to distribute assets according to your wishes.

Asset ProtectionAssets jointly

ownedAvoidance, minimisation and

deferral of tax liabilities

Minimisation of taxPlanning for illness or

incapacityLife insurance

proceeds

Selection of guardians/ representatives/ other fiduciaries

Family succession planning overview

8

Preparing a Will is important

• Control

• Avoid family disputes

• To choose beneficiaries

• Appoint a guardian and name an executor

• Review

9

Is having a Will enough?

If you answer ‘yes’ to any of the following questions, you may have more complex issues to consider:

• Do you have superannuation or life insurance?

• Do you have shared assets?

• Do you owe money?

• Are you receiving a Government pension?

• Have you bought any assets since September 1985?

An effective family succession plan extends to asset protection and the ongoing minimisation of income tax for your beneficiaries

10

What are considered estate assets?

• All assets owned by the deceased at death

• Excludes:

- Joint assets

- Life insurance proceeds

- Assets of companies/trusts

- Superannuation (unless paid to the estate)

11

• What happens to the business on the death of one of the owners?

• Is there a buy/sell agreement in place?

• Is it properly drawn up?

• Is there an associated insurance policy which enables the remaining owners to pay the deceased’s beneficiaries without having to sell the business?

What about small business estate planning?

12

Don’t let your assets fall into the wrong hands!

Beneficiary’s creditors

Tax office

Former spouse

Child’s ex-spouse

Spouse

Children

Grandchildren

Trust

13

Two key issues

Who The recipient of your choice

Tax? Strategies for making as least an impact as possible

14

Structures to consider

• Discretionary family trusts – assets not owned by client

• Child support trusts

• Testamentary trusts

• Superannuation

15

Superannuation

• Restrictions

• Binding nominations

• Legislation

16

Tax effective distribution of assets?

SuperannuationSuper lump sum death benefits paid directly

Dependant

ALL Tax Free

Non-dependant

Tax free element = 0%

Taxed element =17%

Untaxed element 32%

Estate

Estate pays tax according to

distribution of assets

Dependant

ALL Tax Free

Non-dependantTax free element =

0%Taxed element = 17% Untaxed element =

32% Illustrates payment from accumulation phase of superannuation

17

How are estate assets distributed?

LPR

Other assetsEstate

assets

Super

Dependants

Will Intestacy

Family provision rules

18

Benefits of Life Insurance

• Cover CGT liability

• Maintain family’s lifestyle

• Pay off debts

• Pay cash legacies

19

Accidents happen, and no one is immune

1. Source: ABS, Causes of Death, Australia, 20122. Source: Road Deaths Australia 2014 Statistical Summary, Bureau of Infrastructure, Transport and Regional Economics3. Source: Safework Australia

20

Planning your estate

Financial Adviser

Solicitor

Accountant

... requires the advice of other professionals

You

21

Don’t delay the inevitable

• Family succession planning and working out intergenerational finances is not just for the very wealthy

• It’s important for all adults, especially if dependent children, debts, blended families or family businesses are involved

• What issues do the next generation face?

22

The next generation

• You might have your current finances in order but what if something were to happen to a loved one?

• Would the people and possessions that matter to you be well cared for?

• Where would all your hard-earned assets end up?

• And what about your loved ones?

– how are you children and grandchildren likely to manage the money gained through an inheritance?

23

Your beneficiaries – what’s their life stage?

Child

Marriage

Mortgage

Children

Lifestyle change

Retirement

24

What are their issues?

The average Australian family has a number of financial issues:

• Housing affordability is at an all-time low, debt is at all time high

• A lot of marriages end in divorce - in 2013, there were 47,638 divorces granted in Australia1

• The cost of raising two children from birth until when they leave home is about $812,0002

• Most people will spend over 20 years without employment income to sustain them in retirement, do they have enough super to last?

• Men and women aged 45 – 64 have the highest levels of underinsurance (74%-83% of their total level of adequate insurance)3

• Pension access and entitlements are undergoing review.

25

Case study

• Alex aged 36 years and his wife Helen aged 32 had three children under the age of 5 years when Alex was diagnosed with a brain tumour

• He was self-employed and was the sole source of income for the young family who had a mortgage of $250,000

• Unfortunately the couple’s happy-go-lucky attitude meant they never considered terminal illness would happen to them so they had no insurance

• Alex had $30,000 in superannuation but no death or disability insurance through super because he was self employed at the time and not contributing to super

26

Case study

• Alex received his $30,000 payout due to terminal illness but nine months later when he passed away, the family had no money to live on

• Helen received financial help from both sets of parents while she lived on a single parent pension for a while and cared for her young children

• Helen then had to decide whether to sell their home and move in with her parents or continue to live in the home and depend on assistance from both sets of parents

• She chose to stay in the home and rely on parents for financial support

• Helen returned to work part-time while the grandparents babysat

27

Case study

• If Alex and Helen had addressed their personal situation with a financial adviser they could have provided finance and peace of mind for themselves and their young family

• They would have also relieved their parents of this burden on their own finances, lifestyle and retirement

28

Overall deaths in Australia in 2013 of people aged between25 and 64 were 25,1241

1. Source: ABS, Deaths, Australia 2013

29

How can you help your loved ones?

• Your hopes of a secure financial future for your family depend on how well you and your loved ones plan now

• If you want the beneficiaries of your estate spend their inheritance wisely it is recommended they seek financial advice to help them realise their dreams

• For decades, RI Advice Group has been showing clients how to make sure their assets are distributed in the way they want, to whom they want, in the most tax effective manner

30

Value of professional advice

Your loved ones don’t have to be wealthy or thinking of retirement to

get financial advice

It’s about you and your family making the most of what you have and

securing financial peace of mind both now and in the future

Case Studies

32

Case study 1

Case study

Capital Gains Tax

33

Case study - CGT

Zoe’s inheritance investment unit

$

Sale Price 180,000

Less CGT 30,000

Net Proceeds 150,000

Chris’s inheritance principal residence

Sale Price 180,000

Less CGT Nil

Net Proceeds 180,000

$

John owns

home unit as principal residence

an investment home unit

His objective...?

... to pass on a home unit of equal value to each childJohn

Zoe Chris

34

Case study - CGT Executor Sale v Beneficiary Sale

• Estate holds: - share portfolio net capital gain $40,000 (after 50% discount)- $3,000 in other income

• Beneficiary on top marginal rate wants the cash

Executor sells

Tax on $40,000 gain*:

$3,000 income

= $5,522

Tax on $40,000 x 49% = $19,600

Result = $14,078 additional tax*

Beneficiary sells

* Ignores Medicare Levy

35

Case study 2

Case study

Superannuation

36

Case study - Superannuation

What are the tax implications of nominating Chris or Zoe as beneficiary of the policy?

Age 15 and dependant

Age 25 and non-dependant

John

ZoeChris

All Tax Free Up to 30%* lump sum tax

(depending upon elements )

*Plus Medicare Levy

37

Case study 3

Case study

Income Splitting

38

Case study - Income splitting

Peter’s Estate$

Family can receive tax free

TOTAL TAX FREE INCOME …….... $21,790

Rebecca invests

$416$416 $416Rebecca $20,542

39

Peter’s Estate$

Family can receive tax free

TOTAL TAX FREE INCOME $82,168 (about $42,000 MORE!)Includes effect of low income tax offset

Will incorporatestestamentary trustwhich invests funds

Case study - Income splitting

$20,542$20,542 $20,542Rebecca $20,542

40

Case study 4

Case study

Family Law Property Dispute

41

Case study - Family law property dispute

Janet is concerned David’s inheritance will be included in any divorce settlement

Margaret SusanDavid

Janet

Edward (deceased

)

42

Case study 5

Case study

Creditor Protection

43

Case study - Creditor protection

Both aged 72 and concerned for daughter & grandchildren

Business in trouble

Mounting debts

Daughter liable

Potential bankruptcy

Tom

Jean Phillip

Amy Sam

44

$

$

Case study - Creditor protection

PhillipJean

$Trust

Trustee

$Tom

Amy

45

Case study 6

Case study

Social Security

46

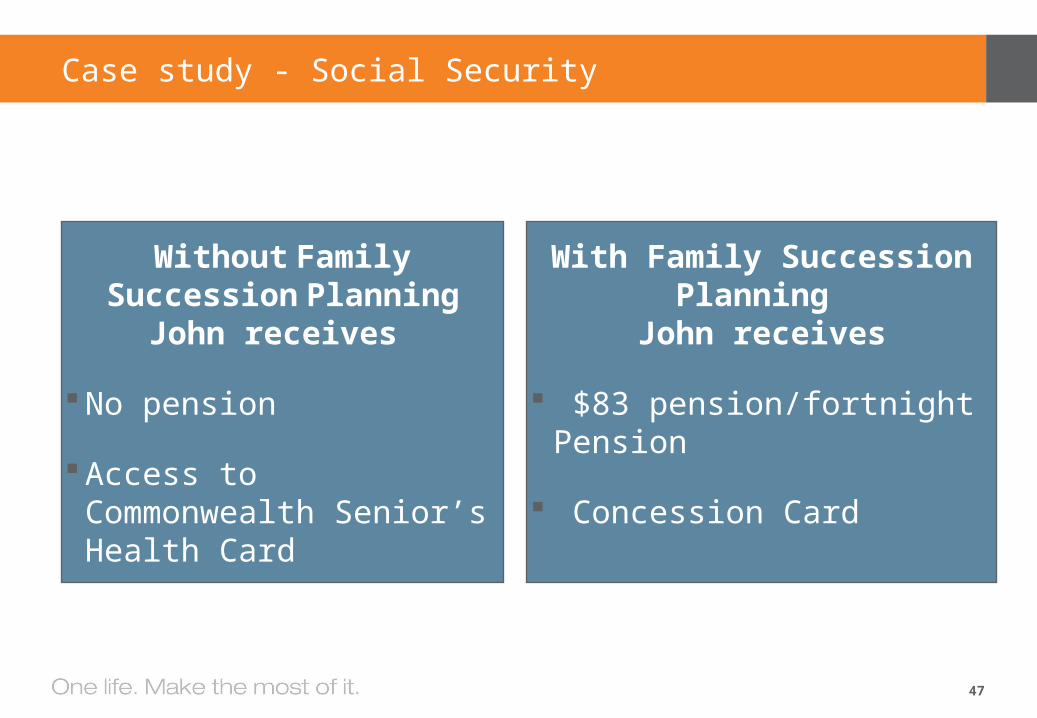

Case study - Social Security

Assets... Their home Other assets $800,000

including $80,000 in jewellery

Receive age pension of approx $263 per fortnight in pension (combined)

John Betty

Sue

47

Without Family Succession Planning

John receives

No pension

Access to Commonwealth Senior’s Health Card

With Family Succession Planning

John receives

$83 pension/fortnight Pension

Concession Card

Case study - Social Security

Thank you for attending.www.riadvice.com.au