Enron Scandal from Auditor's Perspective (F-310)

28

-

Upload

pantho-sarker -

Category

Business

-

view

53 -

download

4

Transcript of Enron Scandal from Auditor's Perspective (F-310)

“ACCOUNTING FRAUD: A STUDY ON ENRON SCANDAL”

A Presentation on

WE ARE….

Names IDPantho Sarker 20-033

Md. Gulam Kibria 20-075Md. Touhidul Islam 20-77 Khaleda Easmin 20-087 Sheikh Sajid Hasan 20-181

Now Presenting …..Md.

Gulam Kibria

ID: 20-

075

COMPANY OVERVIEW OF THE ENRON

Former type

Public

Industry

Energy

Fate BankruptcyPredecessor

InterNorth (Northern Natural Gas Company)

Houston Natural Gasmerged in 1985

Successor DynegyPrisma Energy International

Founded 1985 in Omaha, Nebraska, United States

Founder Kenneth LayDefunct 2007Headquarters 1400 Smith Street

Houston, Texas, United StatesNumber of employees

20,600 during 2001

Website www.enron.com

PRODUCTS AND SERVICE OF THE ENRON

Products

Online marketplace services

Broadband services

Energy and commodities services

Capital and risk management services

Commercial and industrial outsourcing

services

Project development and management

services

TIMELINE OF ENRON’S COLLAPSE

Date Event20 February, 2001 Fortune Magazine story calls Enron a highly impenetrable company and stock was overpriced.

14 August, 2001 Jeff skilling resigned as CFO, citing personal reasons. Kenneth Lay became CEO once again.

12 October, 2001 Arthur Anderson legal counsel instructs workers who audit Enron’s books to destroy all but the most basic documents.

16 October, 2001 Enron reports a third quarter loss of $618 million.24 October, 2001 CFO Andrew Fastow who ran some of the controversial SPE’s was replaced

8 November, 2001 The company took the highly unusual move of restating its profits for the past four years. It admitted accounting errors, inflating income by $586 million since 1997. It effectively admitted that it had inflated its profits by concealing debts in the complicated partnership arrangements.

2 December, 2001 Enron filed for chapter 11-bankruptcy protection on the same day hit Dynegy corporation with a $10 billion breach of contract lawsuit.

12 December, 2001 Anderson CEO Jo Berardino testifies that his firm discovered possible illegal acts committed by Enron.

9 January, 2002 US justice department launches criminal investigations.

Now Presenting …..Khaleda Yeasmin

ID: 20-087

Managements' role in the fraud

INHERENT RISKS OF ENRON BUSINESS

The unique-ness of

business.Diversified business

Inherent Risks

Complex accounting system.

Complex business model.

Extremely volatility

MANAGERS IN THE PROCESS OF FRAUD

Unethical corporate

culture

The managers were just concerned about their personal benefits; they didn't have the ethical sense to be reasonable and accountable to their actions.

Managerial dishonest activities

1. Complex accounting system adaption.2. Overstatements of Revenues and assets.3. Understatement of debt and liabilities.4. Increase market share price with false information and financial statements.5. Collecting funds through selling of share and mis-distribution of funds.6. Selling of their shares before the collapse.

MANAGERS IN THE PROCESS OF FRAUD ( CONTINUED)

Embezzlement of Funds

The managerial executives collected funds through share capital but they didn't invest it rater the embezzled the whole money.

The ultimate results The Largest bankruptcy in history.

Now Presenting …..Md.

Touhidul Islam

ID: 20-77

Auditor‘s role in the fraud

AURTHER ANDERSEN: ENRON’S AUDITOR

Aurther Andersen

Operated with fewer offices

It had "High flying" companies as client, Enron, Worldcom etc.

Enron was Andersen's 2nd

largest client

One of the 5 biggest accounting

firm

During 2000, it earned $25 & $27 million as audit and consulting

fee from Enron

How they did this….The Ways They Did It

The auditors have searched for new ways including loopholes in GAAP to save the company money

One Enron accountant revealed, "We tried to aggressively use GAAP, use it in our advantage and exploited the weaknesses

Andersen's auditors were pressured by Enron's management to defer recognizing the charges from the special purpose entities.

They pressured Andersen into meeting Enron's earnings expectations

Enron occasionally brought Ernst & Young or PricewaterhouseCoopers to complete accounting tasks to create the illusion of hiring a new company to replace Andersen

Though Andersen has a strong control over conflict of interest, it failed in case of enron.

IMPACT ON ANDERSEN AND CONVICTION

Finally, Andersen covicted and

ceased to conduct business

in June 2002

CEO conceded email deletion and document

shredding was an error

They delete nearly 30,000

emails and computer files

Chief auditor ordered the shredding of thousand of documents

The scandal Broke out

Now Presenting …..Pantho Sarker

ID: 20-033

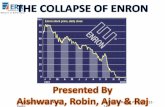

STOCK PRICE OF ENRON$ 90.56

$0.26

• Enron’s value at it’s peak was about $ 70 billion.

• After filing for bankruptcy Enron’s stocks were delisted from the New York stock exchange.

• It was traded in pink sheets or OTC markets before the whole liquidation process completed.

IMPACT ON MAJOR STOCK INDICES

Enron Scand

al Broke

• Stock prices had been falling for a full 18 months prior to the event.• A social mood downtrend caused the stock market to decline rather than the Enron Scandal.• When the Enron scandal broke out the stock market was on its way to a probable recovery.• The Scandal played a part in the latter year to affect investor sentiment and the stock market

reaching a new low.

EFFECT ON US ECONOMY

Inflation (Source: world bank) Real interest rate (Source: world bank)

• Both inflation and interest rate dropped substantially from the period 2000 to 2002.

• The economy was already going through a recessionary phrase.

• The Enron scandal just added to the misery as Investors were reluctant to invest, resulting in an increase in oil and electricity prices in the subsequent years.

Now Presenting …..Sheikh Sajid Hasan

ID: 20-181

Wiser Oil Co.

Dominion Resources Inc. Dynegy Inc.

Loss: 6 millionReason: Oil and gas hedges that it had placed with Enron

Loss: special after-tax charge of $97 million

Reason: Estimated Enron exposure

Loss: $67 million after-tax charge

Reason: Exposure to Enron's bankruptcy and costs related to

the terminated merger agreement.

EFFECT ON THE ENERGY INDUSTRY• Electricity and natural gas companies were facing higher costs of capital.

• Projects to build power plants, pipelines and transmission lines were being put on hold.

• More than $12 billion of investment in new power plants were postponed.

ULTIMATE RESULT OF FRAUD ON EMPLOYEES

5000 employees got fired Lost all health and medical insurance

Lost all money of pension fund

ULTIMATE RESULT OF FRAUD ON DIRECTORS AND TOP EXECUTIVES

Lou L. Paichairman and CEO of

Enron XceleratorCashed in

$33,629,380Disappeared after the

fraud

Kenneth L. Laychairman and CEO

Cashed in $16,103,181

Sentence: 45 years

Jeffrey K. Skillingformer president and

CEOCashed in

$15,554,700Sentence: 24 years,

4 months.

AUDITOR’S CONSEQUENCES

In June 2002, Arthur Andersen was convicted in a US federal court of the crime of obstructing justice by shredding working papers related to Enron audits.

SEC disallowed all audits from convicted felons

The company surrendered its CPA license on August 31, 2002

85,000 employees lost their jobs

June 2005, the US Supreme Court overturned Andersen’s conviction on a legal technicality, but did not absolve Andersen from guilt

LAWS AND REGULATIONS In response to Enron Scandal, The “Sarbanes-Oxley Act” was passed by U.S

congress in 2002 with the objectives of-

Closing loopholes in recent accounting

practices and strengthening corporate

governance rules

Increasing accountability and

disclosure requirements of corporations and

corporate transparency in reporting

Increasing penalties for corporate and executive

malfeasanceStrengthening whistle-

blower protections

Sarbanes-Oxley Act

Thank you for being with

us….