Enron - Corporate Governance - Scandal - Nesr

94

ENRON FAILURE IMPACT Ahmad El Nesr - Ameen Hannout - Farid Kandil Khaled El Tahawy - Shady Hindawi - Shady Hatem Group E - MBA Intake# 63 – March 2013

-

Upload

anesr -

Category

Economy & Finance

-

view

30 -

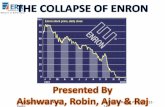

download

4

description

Transcript of Enron - Corporate Governance - Scandal - Nesr

- 1. Ahmad El Nesr - Ameen Hannout - Farid Kandil Khaled El Tahawy - Shady Hindawi - Shady Hatem Group E - MBA Intake# 63 March 2013Prof. Dr. Kami Rwegasira

2. Agenda Case Summary: History of Enron's rise and fall. What happened Theories: What is Corporate? Corporate Governance Analysis: CG institutions /mechanisms Fail of Board, Employees, Executive and Gatekeepers Lessons: Sarbox Domestic :Egypt CG standards OECD Principles of Corporate Governance. ROSC-WORLD BANK(June 2009) Conclusion Reference/Research 3. Questions Q1: What were the essence and causes ofthis corporate scandal inthe financial markets?Q2: Where did CGinstitutions /mechanisms ( including the corporate board ) fail in their duties?Q3: How did Sarbox (2002) Act try to amend the situation ? Q4: What are the home country CG standards /guidelines and how do they measure up to current USA and OECD CG standards?Q5: How couldthese home standards be ameliorated to competitively attract more international investment from abroad ? 4. Q1 Introduction about ENRON What were the essence and causes of this corporate scandal in the financial markets? 5. Enron's rise and fall Enron's life began as an interstate pipeline company through the merger of Houston Natural Gas and Omaha-based InterNorth. Kenneth Lay, the former chief executive officer of Houston Natural Gas, became CEO, and the next year won the post of chairman. 6. Enron's rise and fall The firm's business model evolved to focus on two related themes: the acquisition and operation of power plants and electric distribution companies, and trading operations in which Enron created markets for trading gas and electricity and financial securities based on those commodities. 7. Enron's rise and fall Enron hired Jeff Skilling who had helped Enron develop its Gas Bank idea calling for the firm to become an intermediary between suppliers and end-users in the natural gas market. Later, under Skilling's leadership as CEO, the company pioneered the use of risk management products and long-term contracting structures in the natural gas industry. 8. Enron's rise and fall Enron's principal innovation in energy markets was to combine financial contracts with contracts for physical delivery. This innovation was applied to the natural gas and electric power markets and was being extended to the markets for basic metals, broadband, and pulp and paper at the time of the firm's collapse. 9. Enron's rise and fall By the close of the nineties it was clear that trading operations had become Enron's primary focus and the firm began systematically shedding its physical assets following what it referred to as an asset light strategy. From this perspective, Enron's operations mimicked those of a trading or investment banking firm. 10. Enron's rise and fall During this period Enron made several significant advances including the launch of: EnronOnline (EOL), the firm's energy trading business that became the world's largest business-to-business web site. In Enron Broadband, Enron NetWorks (focusing on eCommerce), and Enron Energy Services (providing retail energy products and services to business customers) were created and appeared to be adding to the firm's bottom line. 11. Enron's rise and fall Growth for Enron was rapid. The company's annual revenue reached $100 billion US. It ranked as the seventh-largest company on the Fortune 500 and the sixth-largest energy company in the world. The company's stock price peaked at $90 US. Much of this increase was attributable to the creation of EOL and Enron's method of accounting for trading revenues 12. Enron's rise and fall On an annualized basis between 1995 and 2000: Enron's assets grew 38%, revenues grew more than 60%, and earnings grew 12%. 13. Enron's rise and fall Cracks began to appear In August of that year, Jeffrey Skilling, a driving force in Enron's revamp and the company's CEO of six months, announced his departure, and Lay resumed the post of CEO. In October 2001, Enron reported a loss of $618 million its first quarterly loss in four years. 14. Enron's rise and fall Chief financial officer Andrew Fastow was replaced, and the U.S. Securities and Exchange commission launched an investigation into investment partnerships led by Fastow. That investigation would later show that a complex web of partnerships was designed to hide Enron's debt. By late November, the company's stock was down to less than $1 US. Investors had lost billions of dollars. 15. Enron's rise and fall On Dec. 2, 2001, Enron filed for bankruptcy protection in the biggest case of bankruptcy in the United States up to that point. Roughly 5,600 Enron employees subsequently lost their jobs. The next month, the U.S. Justice Department opened its investigation of the company's dealings, and Ken Lay quit as chairman and CEO. 16. Enron's rise and fall On Feb 14, 2002, Sherron Watkins, the Enron whistleblower, testifies before a Congressional panel against Skilling and Lay. Sherron Watkins is an Enron vice president. She wrote to Lay in the past expressing concerns about Enron's accounting practices. 17. Enron's Timeline Stock Prices vs. Peer Index 18. Enron Operating Performance 1985 - 2000 19. So, what happened at ENRON? 20. What happened at ENRON? On October 16, 2001, Enron announced it was reducing its after-tax net income by $544 million and its shareholders equity by $1.2 billion. On November 8, 2001, Enron announced that, because of accounting errors, it was restating its previously reported net income for the years 19972000. 21. What happened at ENRON? These restatements reduced previously reported net income as follows: 1997, $28 million (27% of previously reported $105 million); 1998, $133 million (19% of previously reported $703 million); 1999, $248 million (28% of previously reported $893 million); 2000, $99 million (10% of previously reported $979 million). These changes reduced its stockholders equity by $508 million. Thus, within a month, Enrons stockholders equity was lower by $1.7 billion (18% of previously reported $9.6 billion at September 30, 2001). 22. What happened at ENRON? On December 2, 2001, Enron filed for bankruptcy under Chapter 11 of the United States Bankruptcy Code. With assets of $63.4 billion, it is the largest US corporate bankruptcy. The price of Enrons stock, which had increased spectacularly over the 1990s from a low of about $7 to a high of $90 a share in mid-2000, declined to under $1 by year-end 2001. Many Enron employees who had invested their tax deferred retirement plans in Enron stock saw their assets go from hundreds of thousands and even millions of dollars to almost nothing. 23. What happened at ENRON? The following four accounting and auditing issues are of primary importance, since they were used extensively by Enron to manipulate its reported figures: 1. The accounting policy of not consolidating SPEs that appear to have permitted Enron to hide losses and debt from investors. 2. The accounting treatment of sales of Enrons merchant investments to unconsolidated SPEs as if these were arms length transactions. 3. Enrons income recognition practice of recording as current income fees for services rendered in future periods and recording revenue from sales of forward contracts, which were, in effect, disguised loans. 4. Fair-value accounting resulting in restatements of merchant investments that were not based on trustworthy numbers. 24. What happened at ENRON? 1. Accounting for investments in subsidiaries and special-purpose entities (SPEs): A corporation can use Special-Purpose Entities (SPEs) to finance a large project without putting the entire firm at risk. Problem is, due to accounting loopholes, these entities became a way for CFOs to hide debt. Essentially, it looks like the company doesn't have a liability when they really do. Enron sponsored hundreds of SPEs with which it did business: Many of these were used to shelter foreign-derived income from US taxes. Some were sponsored to conduct business with Enron domestically. This is the source that Enron understated and hid its real debt from investors 25. What happened at ENRON? 1. Accounting for investments in subsidiaries and special-purpose entities (SPEs): Under GAAP rules at that time, Enron was not required to consolidate these SPEs with its financial statements As is usual with SPEs, Enron guaranteed their bank debt BUT the SPEs principal asset was restricted Enron stock. When the market price of Enrons stock declined, the SPEs assets were insufficient to cover its debt. As a result, Enron had to assume the debt. 26. What happened at ENRON? 1. Accounting for investments in subsidiaries and special-purpose entities (SPEs): Enrons not consolidating these SPEs increased its reported earnings as shown below ($millions). Thus, at a very considerable cost to shareholders, Enrons managers temporarily were able to hide substantial losses 27. What happened at ENRON? 2. Sales of merchant investments to unconsolidated SPEs: Enron had entered into forward contracts with an investment bank to purchase Enrons stock at a fixed price. In June 1999 the strike price was considerably below the market. Under GAAP, the increase in value cannot be recorded as income, because the gain was due to an increase in value of Enrons own stock. Enron used the gain on these contracts to fund its investment in several of the SPEs it sponsored. 28. What happened at ENRON? 3. Recording as current income fees for services rendered in future periods: Several of the SPEs paid Enron fees for guarantees on loans made by the SPEs. In accordance with the matching concept of income determination, the revenue should have been recognized over the period of the guarantees. Example: Enron recorded as income in December 1997 a $10 million up-front payment from Chewco (an SPE) for a guarantee that was outstanding for the next 12 months. 29. What happened at ENRON? 4. Fair value restatements of merchant investments that were not based on reliable numbers: Mark-to-market or fair value accounting refers to accounting for the "fair value" of an asset or liability based on the current market price, or for similar assets and liabilities, or based on another objectively assessed "fair" value. Mark-to-market accounting can change values on the balance sheet as market conditions change. In contrast, historical cost accounting, based on the past transactions, is simpler, more stable, and easier to perform, but does not represent current market value. 30. What happened at ENRON? 4. Fair value restatements of merchant investments that were not based on reliable numbers: In Jan. 30, 1992 - SEC approves mark-to-market accounting for Enron. Such procedures allow managers who want to manipulate net income the opportunity to make reasonable assumptions that would give them the gains they want to record. Such appears to have been what Enron did. 31. What happened at ENRON? To summarize: Enrons accounting for its nonconsolidated special-purpose entities (SPEs), sales of its own stock and other assets to the SPEs, and mark-ups of investments to fair value substantially inflated its reported revenue, net income, and stockholders equity, and possibly understated its liabilities. 32. What happened at ENRON? Enrons bankruptcy is of particular interest to accountants, because its longtime auditor, Arthur Andersen, was one of the Big 5 CPA firms. Arthur Andersen has been charged with gross dereliction of duty and even fraud by the press and members of the US Congress (amongst others), and is being sued in many lawsuits for very substantial damages. 33. What happened at ENRON? In 2000, Andersen was paid $25 million in audit fees and $27 million for non-audit consulting. This observation has given new impetus to demands that CPAs be prohibited from offering non-audit services (other than tax preparation and advice), on the assertion that these fees corrupt the independence of CPAs. In response to this criticism, all of the Big 5 CPA firms announced that they would no longer offer certain consulting services to their auditing clients. 34. What happened at ENRON? The Chairman of the Securities and Exchange Commission (SEC), Harvey Pitt, has called for the creation of a new oversight body to regulate and discipline CPAs. The SEC, the Financial Accounting Standards Board (FASB), and the American Institute of CPAs (AICPA) have been severely criticized for not having clarified the GAAP rules relating to special-purpose entities (SPEs), the vehicle associated with Enrons accounting restatements of its financial statements. 35. Q2 Theories: What is Corporate? Analysis: CG institutions /mechanisms: Fail of Board, Employees, Executive and Gatekeepers 36. What is a Corporate ? The most common form of business organization, and one which is chartered by a state and given many legal rights as an entity separate from its owners. This form of business is characterized by the limited liability of its owners, The process of becoming a corporation, call incorporation, gives the company separate legal standing from its owners and protects those owners from being personally liable in the event that the company is sued (a condition known as limited liability). 37. A Corporate:Environmental GroupsShareholders &Board Credit SupplierCustomersCorporationEmployeesLocal CommunityManagementGovernment 38. Corporate Governance: What is Corporate Governance? The corporate governance is a set of systems , structures ,processes and mechanisms by which a corporate entity is led, directed and controlled in the best interests of shareholders and other stakeholders. Corporate governance rules are primarily applied on listed joint stock companies and other financial institutions taking the form of joint stock companies. 39. The corporate governance framework should protect and facilitate the exercise of shareholders rights. Which are briefed as follows: the right to receive income The right to vote The right to appoint an authorized representative) on their behalf They possess legal rights to challenge the order of the company's management in the court of lawThe equitable treatment of shareholders.The corporate governance framework should promote transparent and efficient markets, be consistent with the rule of law and clearly articulate the division of responsibilities among different supervisory, regulatory and enforcement authorities.The rights of shareholders.Effective Corporate Governance Framework.Corporate governance principles 1/2The corporate governance framework should ensure the equitable treatment of all shareholders, including minority and foreign shareholders. All shareholders should have the opportunity to obtain effective redress for violation of their rights. 40. The corporate governance framework should ensure that timely and accurate disclosure is made on all material matters regarding the corporation, including the financial situation, performance, ownership, and governance of the company.The responsibilities of the boardThe corporate governance framework should recognize the rights of stakeholders established by law or through mutual agreements and encourage active between corporations and stakeholders in creating wealth ,jobs, and the cooperation sustainability of financially sound enterprises.Disclosure and transparencyThe role of stakeholders in corporate governanceCorporate governance principles 2/2The corporate governance framework should ensure the strategic guidance of the company, the effective monitoring of management by the board, and the boards accountability to the company and the shareholders 41. Corporate mechanisms and controls Corporate governance mechanisms and controls are designed to reduce the inefficiencies that arise from moral hazard and adverse selectionInternal corporate governance controlsExternal corporate governance controls 42. Corporate mechanisms and controls: 1. Internal corporate governance controls Internal corporate governance controls monitor activities and then take corrective action to accomplish organizational goals Monitoring by the board of directors The board of directors, with its legal authority to hire, fire and compensate top management, safeguards invested capital. Regular board meetings allow potential problems to be identified, discussed and avoidedInternal control procedures and internal auditors Internal control procedures are policies implemented by an entity's board of directors, audit committee, management, and other personnel to provide reasonable assurance of the entity achieving its objectives related to reliable financial reporting, operating efficiency, and compliance with laws and regulations 43. Corporate mechanisms and controls: 1. Internal corporate governance controls Balance of power The simplest balance of power is very common; require that the President be a different person from the Treasurer. This application of separation of power is further developed in companies where separate divisions check and balance each other's actions Remuneration Performance-based remuneration is designed to relate some proportion of salary to individual performance. It may be in the form of cash or non-cash payments, superannuation or other benefits Monitoring by large shareholders Given their large investment in the firm, these stakeholders have the incentives, combined with the right degree of control and power, to monitor the management 44. Corporate mechanisms and controls: 2. Internal corporate governance controls External corporate governance controls encompass the controls external stakeholders exercise over the organization Examples include: competition debt covenants demand for and assessment of performance information (especially financial statements) government regulations managerial labor market media pressure takeovers 45. Where did CG institutions /mechanisms( including the corporate board ) fail in their duties? Responsibility for recent corporate misconduct must be allocated to the failure of several components of business and governance system: 1. 2. 3. 4. 5.corporate managers; corporate boards; gatekeepers; shareholders, and especially institutional investors. 46. Where did CG institutions /mechanisms ( including the corporate board ) fail in their duties? Board of Directors (BOD) Audit Committee of the Board should have been more critical of the auditors and their work. Stock price and earnings rising, they were perhaps lulled into a false sense of security about ENRONs internal accounting The Board members enjoyed their status at ENRON 47. Corporate Governance Shareholders (or stakeholders?) -Too much trust, Incompetence - Lack awareness and/or understanding of role , -No control & reporting systems, - Lack of motivation, Conflicts of interestBOARD 48. Where did CG institutions /mechanisms ( including the corporate board ) fail in their duties? ENRON executives were further aided and supported by the Arthur Andersen auditors and scores of outside legal firms working for the company. A.A collected over $50 million in revenues in year 2000. Remaining in good standing with the executive team at ENRON Executives probably do not look favorably on outside firms who give contrary advice to that which the executives desire. 49. Corporate Governance Shareholders (or stakeholders?) -Too much trust, Incompetence - Lack awareness and/or understanding of role , -No control & reporting systems, - Lack of motivation, Conflicts of interestBOARDMajor players MANAGEMENTDishonest & Conflicts of Interest 50. Where did CG institutions /mechanisms ( including the corporate board ) fail in their duties? EMPLOYEES ENRON had an inside legal staff of over 100 lawyers, and an accounting staff of several hundred trained accountants All seemed to be operating in a way that supported the executive management team As employees were being paid good salaries Until Sherron Watkins finally tried to raise awareness of potential problems 51. Corporate Governance Shareholders (or stakeholders?) -Too much trust, Incompetence - Lack awareness and/or understanding of role , -No control & reporting systems, - Lack of motivation, Conflicts of interestBOARDMajor players MANAGEMENTProductivity & CompetitivenessCorporation DirectionDishonest & Conflicts of InterestEthics and social responsibility Viability and legitimacyFocus 52. Where did CG institutions /mechanisms ( including the corporate board ) fail in their duties? GATEKEEPERS External auditors, analysts, and credit rating agencies to detect and expose the questionable financial and accounting decisions that led to the collapse of Enron An argument can be made that during the 1990's the deterrent effect of legal liability for gatekeepers declined as well, further reducing market disciplineThus, to make gatekeepers more effective ways must be found both To reduce their conflicts of interest and To increase the threat of market discipline if they fail to adequately represent the interests of investors and creditors. 53. The Fraud Triangle Opportunities Weak Board of Directors Weak Internal Controls 54. Q3 Introduction to SOX How did Sarbox (2002) Act try to amend the situation ? 55. Introduction to SOX SarbOx stands for SarbanesOxley Paul Sarbanes is a United States Senator who represented the state of Maryland. Sarbanes Michael G. Oxley is an American politician of the Republican party who served as a U.S. representative from the 4th congressional district of Ohio. 56. Introduction to SOX (cont.) 1. Public Company Accounting Oversight Board (PCAOB) The PCAOB is a nonprofit corporation established by Congress to oversee the audits of public companies in order to protect the interests of investors2. Auditor Independence Establishes standards for external auditor independence, to limit conflicts of interest.3. Corporate Responsibility Senior executives take individual responsibility for the accuracy and completeness of corporate financial reports 57. Introduction to SOX (cont.) 4. Enhanced Financial Disclosures It describes enhanced reporting requirements for financial transactions, including off-balance-sheet transactions, pro-forma figures and stock transactions of corporate officers.5. Analyst Conflicts of Interest It defines the codes of conduct for securities analysts and requires disclosure of knowable conflicts of interest.6. Commission Resources and Authority It defines practices to restore investor confidence in securities analysts. 58. Introduction to SOX (cont.) 7. Studies and Reports It requires the Comptroller General and the SEC to perform various studies and report their findings. Studies and reports include the effects of consolidation of public accounting firms, the role of credit rating agencies in the operation of securities markets.8. Corporate and Criminal Fraud Accountability It describes specific criminal penalties for manipulation, destruction or alteration of financial records or other interference with investigations, while providing certain protections for whistle-blowers.9. White Collar Crime Penalty Enhancement This section increases the criminal penalties associated with white-collar crimes and conspiracies. 59. Introduction to SOX (cont.) 10. Corporate Tax Returns It states that the Chief Executive Officer should sign the company tax return.11. Corporate Fraud Accountability It identifies corporate fraud and records tampering as criminal offenses and joins those offenses to specific penalties. 60. How did Sarbox (2002) Act try to amend the situation ?The Enron scandal was certainly enough to show the American public and its representatives in Congress that new compliance standards for public accounting and auditing had to be put into place.Enron was one of the biggest and, it was thought, one of the most financially sound companies in the U.S. Enron was perhaps the catalyst for the Sarbanes-Oxley legislation. 61. How did Sarbox (2002) Act try to amend the situation ?Sarbanes-Oxley provides for increased corporate governance and corporate accountability. Therefore, SOX is in place to be sure that fraud on the scale of Enron never takes place again. If a publicly-traded company is not in compliance with the SOX law, the penalties are stiff. Multi-million dollar fines can result and imprisonment of the CEO or CFO. Penalties are based on the section of SOX that the company is not in compliance with. 62. How did Sarbox (2002) Act try to amend the situation ?In summary, the Sarbanes-Oxley Act of 2002 is probably the best piece of legislation to protect investors in modern times. It is a shame that it took debacles like Enron and others to shake up Congress into writing this legislation as many innocent people, investors and employees, literally lost their life savings. Perhaps SOX will make sure that doesn't happen again. 63. Q4 What are the home country CG standards /guidelines and how do they measure up to current USA and OECD CG standards? 64. What are the home country CG standards /guidelines and how do they measure up to current USA and OECD CG standards?Egypt Code of Corporate Governance Guidelines and Standards (October 2005) This guide was prepared by the Chairman of the General Authority of Investment and Free Zones, Dr. Zeyad Bahaa El Din, together with the Chairman of the Cairo and Alexandria Stock Exchange, Mr. Maged Shawqi. It is based on a questionnaire compiled by CIPE and consultations with a number of accounting and business experts in Egypt. The guide is prepared in accordance with the corporate governance principles issued by the OECD and a number of countries including South Africa, Malaysia and the Philippines. 65. What are the home country CG standards /guidelines and how do they measure up to current USA and OECD CG standards?Criteria of the code: 1. General Assembly 2. Board of Directors (BOD) 3. Internal Audit Department 4. External Auditor 5. Audit Committee 6. Disclosure of Social Policies 7. Avoiding Conflict of Interest 8. Corporate Governance Rules for Other Corporations 66. What are the home country CG standards /guidelines and how do they measure up to current USA and OECD CG standards? 1. General Assembly Shareholders should be encouraged to attend GAs. Agenda items should be explained clearly GA Should be managed to allow shareholders to express their opinions. Voting on general assembly motions should be recorded accurately.2. Board of Directors Should meet at least once every 3 months Non executive members may meet directors for consultation. Review internal regulations & procedures for their appropriateness & efficiency An internal audit committee formed from a number of non-executive members should be assigned to check internal controls & the company's working practices. Responsible for risk management in accordance with the company's activities, size, & market board should submit an annual report to shareholders including tasks assigned by law 67. What are the home country CG standards /guidelines and how do they measure up to current USA and OECD CG standards? 3. The Internal Audit Department Should maintain a tight internal control system established by the board members & directors Report directly to the CEO Direct consultation with the board director Submit a quarterly report to the board and the supervisory committee Design systems to evaluate risk management approaches, plans, procedures and the company's proper implementation of CG 4. External Auditor Independent from the company and the board Abides with Egyptian accounting principles and rules Should hold neutral opinions The auditors work is immunized against interference from the board 68. What are the home country CG standards /guidelines and how do they measure up to current USA and OECD CG standards? 6. The Audit Committee Comprises of a minimum of three non-executive members. One member should be a finance & accounting expert Assess the efficiency of the financial manager & other financial staff review the financial statements before being presented to the board and give opinions and recommendations review the internal/external auditors plan and make suggestions. The committee should meet periodically, at least once every three months, with a specified agenda 7. Disclosure of social policies At least once a year the company should disclose environmental, social, safety & health policies to shareholders, customers and employees. The policies disclosed should be clear & unambiguous, including the company's strategies for employee recruitment & training & social welfare programs within or outside the company. Relationships 69. What are the home country CG standards /guidelines and how do they measure up to current USA and OECD CG standards?8. Avoiding conflict of interests Each company should have clear and recognized regulations for the directors & staff regarding the prevention of conflict of interests Board members, directors and staff may not trade company stocks before the disclosure of the company's financial statements Draw up rules of professional code of conduct Impose an internal system for supervising the implementation of the code of conduct 70. What are the home country CG standards /guidelines and how do they measure up to current USA and OECD CG standards?9. Corporate Governance for other corporations These principles primarily target companies listed in the stock market and financial institutions and corporations financed by banks. Nevertheless, corporate governance may be implemented in all companies, achieving a balance of interests and a new management culture. Therefore, the greater the number of companies abiding by these principles, the higher is the probability of promoting the interests of society, shareholders and stakeholders. 71. OECD Principles of Corporate Governance. The Organization for Economic Cooperation and Development (OECD) issued its CG principles in 1999 that were later revised in 2003 after extensive and open consultations. The OECD CG Principles were further revised in 2004 by the 30-OECD member governments together with the WB, IMF, Bank for International Settlements (BIS), Financial Stability Forum (FSF), International Organization for Securities Commissioners (IOSCO), Basle Committee and many other parties in developing and emerging economies. Section I: The Rights of Shareholders ( 6 ) Section II: The Equitable Treatment of Shareholders (3 ) Section III: Role of Stakeholders in Corporate Governance ( 4 ) Section IV: Disclosure and Transparency ( 4 ) Section V: The Responsibility of the Board ( 6 ) 72. Q5 How could these home standards be ameliorated to competitively attract more international investment from abroad ? 73. Report on the Observance of Standards and Codes (ROSC)WORLD BANK(June 2009) The Ministry of Investment (MoI) founded the Egyptian Institute of Directors (EIoD), the region's first, and launched codes of corporate governance for private and state-owned companies. The Capital Markets Authority (CMA) created a special Corporate Governance Department and the Egyptian Stock Exchange (EGX) began to consistently enforce its listing rules, leading to an impressive wave of de-listings from a high of 1,148 in early 2002 to 333 by mid 2009. The Egyptian authorities have implemented many of the key recommendations of the 2001 and 2004 Corporate Governance ROSCs. 74. Report on the Observance of Standards and Codes (ROSC)WORLD BANK(June 2009) Actual corporate governance practices of EGX listed companies continue to lag behind the law on the books, in particular for companies outside the EGX-30. For example: A number of boards do not guide or supervise management by helping them develop and holding them accountable to a set of key performance indicators. Key policies on risk management, internal control and audit processes, and succession planning are often absent. Board nomination processes largely remain opaque and are frequently dominated by majority owners. 75. Report on the Observance of Standards and Codes (ROSC)WORLD BANK(June 2009) Financial reporting has improved in terms of the timeliness and quality of disclosure; however, non-financial disclosure remains underdeveloped. Few companies publicly disclose their ownership and governance structures or foreseeable risk factors online or in their annual reports. The laws and regulations that establish shareholder rights have improved markedly, though a few remaining weaknesses exist. Extraordinary transactions do not for example generally require shareholder approval, against good practice, unless the transaction constitutes a merger or an acquisition, or the transaction of a fixed asset, in which case EGM approval is required. In absence of an effective court system, shareholders are in practice unable to hold directors and officers accountable for a breach of their duties. 76. Report on the Observance of Standards and Codes (ROSC)WORLD BANK(June 2009) Egypt can take a major step forward in closing these gaps vis--vis the OECD Principles by: Requiring companies to implement the Egyptian Corporate Governance Code (ECGC) on a 'comply-or-explain' basis, and amending the ECGC to better meet good practice. Reinvigorating the company law reform process to combine the multitude of overlapping laws and regulations into one consistent framework that incorporates recent trends and developments in corporate governance. Further strengthening enforcement capacity and supporting the EIoD to roll-out its director training program, focusing on familyowned businesses outside the EGX-30. 77. Absence of engaged institutional investors leaves decision-making in the hands of majority owners & insiders, with underdeveloped market discipline. family ownership brings a unique set of governance issues. Overlapping provisions and inconsistencies causes some legal uncertainty. The institutional framework has been strengthened and enforcement capacity has improved markedly, yet important enforcement gaps in, for example, non-financial disclosure, continue. 78. Extraordinary transactions are not generally subject to GMS approval. Institutional investors do not typically vote or engage with their investee companies. 79. Egypt has broadly implemented Chapter III of the OECD Principles of Corporate Governance however, minority shareholders are not able to effectively hold the board accountable through a functioning court system. 80. Employees are allowed to participate in the management of the company through employee committees. Share reward and option programs for employees and managers are beginning to take root. Creditor rights are underdeveloped and specialized bankruptcy courts inefficient. CSR and stakeholder governance is not properly understood as a potential risk or opportunity by boards. 81. Egyptian companies must now follow EAS that are based on IFRS (with the previously mentioned four exceptions to IFRS); auditors must follow ESA, which similarly, are largely (but not exclusively) based on ISAs. Non-financial reporting has improved somewhat, however, overall remains underdeveloped; e.g., only 16 percent of EGX-30 companies disclosed their governance structures and three percent their internal control and audit policies. 82. The ability of boards to adhere to good corporate governance practices remains the main challenge in terms of implementing the OECD Principles. More specifically: The line between board oversight and day-to-day management is often blurred. The majority shareholder and not the board plays the lead role in selecting, monitoring, and replacing executives. Executive remuneration is not linked to long term company performance. Companies do not have robust risk, internal control, and audit policies in place. 83. After the Fall 84. Crime and Punishment Ken Lay, former Chairman of the board, convicted on six accounts (Dies at age 64) Jeffrey Skilling, former CFO convicted and sentenced for 24 years and 4 months in federal prison and has to pay back $26M from his own money. Paula Rieber, former managing director of investor relations pled guilty Richard Causey, former Chief Acccounting Office, pled guilty and testifies against Lay and Skiling Andrew Fastow, former Chief Financial Officer, accepted plea deal and will serve a 10 year sentence And many more went to jail. 85. Societal and Legal Impact New law was passed U.S Sarbanes Oxley Act on July 30, 2002 Reformed the stock market Deemed on the more important scandals of our lifetime Change the face of U.S business 86. Lawsuits Thousands of ENRON Employees and investors lost their savings, children college funds and pensions Shareholders filed lawsuit Employees filed lawsuit Creditors filed a lawsuit (Reuters) - A U.S. judge sentenced two former Enron energy traders involved in the scheme to manipulate California energy prices to two years' probation and a $10,000 (5,100 pounds) fine each on Wednesday after they co-operated with authorities in the case Etc 87. Conclusion 88. Conclusion The ENRON failure has not been the result of just questionable activities by ENRONs executive management team. The cast of contributors to the failure and bankruptcy are both inside and outside the company. Its the total system that resulted in failure that needs to be further understood and investigated. 89. Conclusion Multiple corporate governance mechanisms, both internal and external, failed to constrain the actions of Enron's management team: In particular, Enron's board failed to oversee management and apparently did not understand the risks inherent in the firm's business strategy. It also appears that several board members and the external auditor faced potential conflicts of interest that attenuated their role as monitors. Further, the board, analysts (credit and equity), external auditors, and federal agencies failed to identify problems at Enron or did not respond to obvious signs that there were problems at the firm. Finally, Enron's role as a dominant player in nascent and inefficient markets, afforded the firm's management the opportunity to manipulate prices, asset values, and thus the firm's financial position 90. Conclusion US GAAP, as structured and administered by the SEC, the FASB, and the AICPA, are also responsible for the Enron counting debacle. Enron and its outside counsel and auditor felt comfortable in following the specified accounting requirements for consolidation of SPEs. The SEC had the responsibility and opportunity to change these rules to reflect the known fact that corporations were using this vehicle to keep liabilities off their balance sheets, although the sponsoring corporations were substantially (often almost entirely) liable for the SPEs obligations 91. References http://bizfinance.about.com/od/smallbusinessfinancefaqs/a/sarbanes-oxley-act-and-enron-scandal.htm http://insanadfindingthepony.blogspot.com/2010/04/enron-scandal-and-people-of-wal-mart-by.html http://business.nmsu.edu/~dboje/enron/chronology.htm Chronological history of Enron http://usatoday30.usatoday.com/money/industries/energy/2006-01-23-enronchronology_x.htm http://en.wikipedia.org/wiki/Special_purpose_entity http://en.wikipedia.org/wiki/Timeline_of_the_Enron_scandal http://www.applet-magic.com/enron.htm http://blj.ucdavis.edu/archives/vol-6-no-2/Corporate-Governance-and-Sarbanes-Oxley-Post-Post-Enron.html http://www0.gsb.columbia.edu/faculty/fedwards/papers/U.S.%2520Corporate%2520Governance%25201005.pdf http://www.hawkama.net/files/toolkit/content/cgprogramspartners/Egyptian_Code_of_Corporate_Governance _Guidelines_and_Standards_October_2005__Egypt_English.pdf http://apps.chron.com/news/specials/enron/background.html http://online.wsj.com/article/SB113898435336064528.html http://www.hawkama.net/files/toolkit/content/cgprogramspartners/Egyptian_Code_of_Corporate_Governance _Guidelines_and_Standards_October_2005__Egypt_English.pdf 92. References http://www.cbc.ca/news/business/story/2006/05/25/enron-bkgd.html ELSEVIER - Journal of Accounting and Public Policy 21 (2002) 105127 - Enron: what happened and what we can learn from it - George J. Benston, Al L. Hartgraves Goizueta Business School, Emory University, 1300 Clifton Road, Atlanta, GA 303222710, USA ELSEVIER Journal of Corporate Finance 13 (2007) 929-958 - Corporate governance post-Enron: Effective reforms, or closing the stable door? Stuart L. Gillan a,John D. Martin b a Finance Department, Rawls College of Business, Box 42101, Texas Tech University, Lubbock, TX 79409-2101, United States b Department of Finance, Hankamer School of Business, Baylor University, Waco, TX 76798, United States 93. DO YOU HAVE ANY QUESTIONS