MSME Conclave - Facilitating Financing & Enhancing Competitiveness

0

Enhancing Tourism Competitiveness through Improved Air ConnectivityPresented by:

ICF International

International Tourism FairMadrid, 20‐24 January, 2016

11

Agenda

1. Aviation Industry Overview

2. Improving Air Connectivity through Air Service Development (ASD)

3. Airline Route Planning Process

4. Conducting a Route Forecast

5. Example Business Case Slides

6. Tactics for Small Markets

22

Introduction to ICF

3

ICF is one of the most experienced global aviation and aerospace consultancies

Airports • Airlines • Aerospace & MRO • Asset AdvisoryAirports • Airlines • Aerospace & MRO • Asset Advisory

joined ICF in 2012

joined ICF in 2011

joined ICF in 2007

53 years in business (founded 1963)

100+ professional staff− Dedicated exclusively to aviation and aerospace

− Blend of consulting professionals and experienced aviation executives

Specialized, focused expertise and proprietary knowledge

Broad functional capabilities

More than 10,000 private sector and public sector assignments

Backed by parent company ICF International (2014 revenue: US$1.05 billion)

Global presence –– offices around the world with partner in Israel

New York • Boston • Ann Arbor • London • Singapore • Beijing • Hong Kong

44

Our client base spans the aviation industry, giving us a holistic view of the industry

International and regional passenger airlines

Major and regional airports

Tourism ministries and agencies

National, regional and local governments

Air cargo, express, and integrated logistics operators

IT, equipment, and service providers

Airframe, engine, and avionics suppliers

Aircraft leasing companies

Investors and financial institutions

Booking, distribution, and travel services

Maintenance, Repair, and Overhaul industry

Corporate and business aviation

55

ICF offers an unmatched global airline client list and network of airline contacts

66

We are especially strong in international air service experience and support

Boston

Baltimore

Miami

Dallas/Ft. Worth

Denver

LasVegas

LosAngeles

U.S./CanadaU.S./Canada

Tampa

SaltLake City Islip

SanFrancisco

Ft. Myers

Richmond

Edmonton

Indianapolis

Omaha

San Paulo

LiberiaBogota

Port ofSpain

Medellin

Lima

South / CentralAmerica, CaribbeanSouth / Central

America, Caribbean

*

* Mexico includes all airports managed by GAP, ASUR and OMA

San Jose

San Juan

Quito

Santiago

Rio De Janeiro

Natal

ManchesterNewcastle

Donetsk

Cairo

Nantes

Stockholm

Istanbul

Europe / Russia/ Middle EastEurope / Russia/ Middle East

*

Spain includes all airports managed by AENA

Birmingham

Oman

MedinahHeraklion

JeddahRiyadh

Morocco

MoscowHamburg

London

Cheongju

Krasnoyarsk

AsiaAsia

SiemReap

ShanghaiKunming

Beijing

Khabarovsk

Hong Kong

Singapore

SeoulICN

77

Introduction to the GAP Mexican Pacific Airports

88

Mexican Pacific Airport Group (GAP) maintains and operates 12 airports in Mexico, as well as Montego Bay Jamaica

Source: GAP

Airport Code

Guadalajara GDL

Tijuana TIJ

Puerto Vallarta PVR

Los Cabos SJD

Hermosillo HMO

Leon BJX

La Paz LAP

Mexicali MXL

Morelia MLM

Aguascalientes AGU

Los Mochis LMM

Manzanillo ZLO

Montego Bay MBJ

TIJ4.4-3%%

GAP airports served 29.2 million passengers in the 12 months ending June 2015, representing 4% growth over the previous year

MXL0.57%

HMO1.3-5%

LAP0.71%

SJD3.1-11% PVR

3.418%

GDL9.17%

LMM0.325%

ZLO0.2-1%

MLM0.54%

AGU0.619%

BJX1.323%

Passengers, MillionsYear-over-Year % Change

Investors include:

GAP listed on:

MBJ3.86.7%

99

Diversified Portfolio of Airports

Public Float85%

Aeropuertos Mexicanos del Pacífico15%

Controladora Mexicana de Aeropuertos (CMA)

66.6%

AENA Internacional

33.4%

GAP‐at‐a‐GlanceRelevant Information

Airport Geographic Presence in México

Shareholder Structure> Grupo Aeroportuario del Pacífico, S.A.B. de C.V. is a holding

company that operates 12 airports throughout Mexico’s Pacific region. The concession was granted for a 50-year period and will expire in 2049.

• In addition, in April 2015 GAP acquired “DCA” (Spanish company), which has a majority stake in MBJ Airports Limited.

• GAP’s shares are listed on the NYSE under ticker symbol “PAC” and on the Mexican Stock Exchange under ticker symbol “GAP”.

• S&P (mxAAA/stable/mxA-1+) and Moody’s (Aaa.mx/stable/Baa1)

2014 Profitability: • EBITDA of Ps. 3,690 mm (+13.3%), EBITDA Margin of 70.1%• 2014 dividends paid were Ps. 3,100 mm

Page 9

MexicaliTijuana

Hermosillo

Los Mochis

La PazLos CabosAguascalientesGuanajuatoPuerto VallartaGuadalajaraMoreliaManzanillo

Passenger share by Airport 2015

Jamaica

Desarrollo de Concesiones Aeroportuarias100%

MBJ Airports Limited74.5%

1010

Key events:• 2006 – 2007 – Low‐Cost Carrier Effect / Price Wars • 2008 – 2009 – Exit of 8 airlines, economic downturn and AH1N1 crisis • 2010 – 2011 – Mexicana Airlines ceases operations• 2012 – 2014 – Traffic Recovery, surpassing 2008 numbers• 2015 – Traffic reached highest numbers in Gap´s history

Page 10

GAP Passenger Traffic History

Traffic Composition 2015…

11.8%CAGR ' 06 vs 15:

4.42%

1111

A Company focused on profitability and development

Page 11

GAP continues generating constant growth, despite being in a mature industry, but with a great opportunity of growth in

future years.

CAGR ' 06 vs 14: 10.65%

*Figures include the recognition of a gain in the fair value of theacquisition of DCA and MBJ, which generated one‐time other incomeof Ps. 161.9 million.

2,023 2,337 2,239 2,134

2,441 2,597

2,939 3,256

3,690

4,517

‐

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015E*

Millions

EBITDA

CAGR ' 06 vs 15E: 9.34%

Billion

s of M

exican

Pesos

1212

What are the objectives of this session?

1. Understand the value of an Air Service Development Program

2. Learn the essential elements of an airline business case

3. Understand the network planning process of an airline

4. Learn how to conduct a route forecast (traffic and revenue)

5. Understand the key elements of a “Business Case” for airlines

6. Understand the need for Financial Incentives and a Stakeholder Committee

1313

Aviation Industry Overview

1414

World air traffic growth has outpaced GDP growth – a trend that is forecast to continue well into the future

0

500

1,000

1,500

2,000

2,500

3,000

3,500GDP History & Forecast

Traffic History

Airbus Traffic Forecast (4.7%)

Boeing Traffic Forecast (5.0%)

ICF Traffic Forecast (4.0%)

IATA Forecast (4.0%)

World GDP Growth and Air Transport World Traffic (RPKs)Indexed: 1970 = 100

Note: RPK (Revenue Passenger Kilometer): number of paying passengers x kilometers flownSource: Airline Monitor, February 2015; Oxford Economics; World Economic Outlook, Airbus/Boeing/Embraer Market Outlooks, ICF 2014

ICF’s traffic forecast allows for lumpy economic growth and a weakening of the low‐cost carrier cycle

ICF’s traffic forecast allows for lumpy economic growth and a weakening of the low‐cost carrier cycle

Forecast (2014‐2034)

World GDP

World Traffic

1515

8.0%

6.3%

5.3% 5.4%5.9%

6.7%

4.5%

6.6%

4.0%

5.0%5.6%

6.0%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2010 2011 2012 2013 2014 2015F

Traffic (RPK) Capacity (ASK)

Airlines appear to have found the art of “capacity discipline” in recent years, much to the delight of investors

Source: IATA Air Transport Market Analysis – Dec reports from 2010‐2014, September report for 2015

2015 YTD (September)

Passenger Traffic / Capacity GrowthYear‐Over‐Year Percent Change

As a result, average load factor has not dropped below 78% for over two yearsAs a result, average load factor has not dropped below 78% for over two years

1616

In the next 20 years, IATA forecasts a 4.0% annual average growth in global air passenger journeys – differing by region

Source: IATA

North America651m3.3%

Europe577m2.6%

Middle East250m5.1% Asia Pacific

1753m4.9%

Africa190m4.9%

2.2 times the number of air passenger journeys in 2034

compared with today

In order‐ China, USA, India, Indonesia, Brazil are expected to have the biggest increases

in passengers numbers

Latin America328m4.4%

Growth and change in passenger journeys by region (% and million, 2014‐2034)

1717

-$6 -$4

$5

$15

-$26

-$5

$17

$8$6

$11

$20

$25

-$30

-$20

-$10

$0

$10

$20

$30

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015F

Driven by capacity discipline, airline consolidation, and lower fuel costs, the industry has successfully returned to profitability

Global Airline Profitability (Net Profit)

Source: IATA Central Forecast Dec 2014

$ Billions

1818

Aviation fuel costs have dropped significantly during the past years to below $40/bbl (65% lower than summer 2014)

(USD)

If sustained, low fuel prices could bring dramatic changes to the industryIf sustained, low fuel prices could bring dramatic changes to the industry

Oil Price per Barrel (US$) – WTI Cushing, Oklahoma

Source: U.S. EIA data of January 18, 2016

$0

$20

$40

$60

$80

$100

$120

1919

ICF sees a number of potential impacts on aviation if low oil prices are sustained

income Increase of disposable income higher air travel demand

Lower airline operating costs can flow through to increased travel demand due to lower ticket prices

Higher profitsOlder airplanes kept in service longer

Capacity increases at a slightly greater rateMore new entrants/start‐up carriers(especially in emerging markets)

Higher air travel demand increased traffic at airports increased spending while at airports

Increased demand for airport access by airlinesDemand for more space to accommodate increased capacity

Air Travel Demand

Passenger Airlines

Airports

Sustained Low PricesNear Term

Source: ICF research

Industry consensus is it’s too early to tell if the reductions will be long‐termIndustry consensus is it’s too early to tell if the reductions will be long‐term

2020

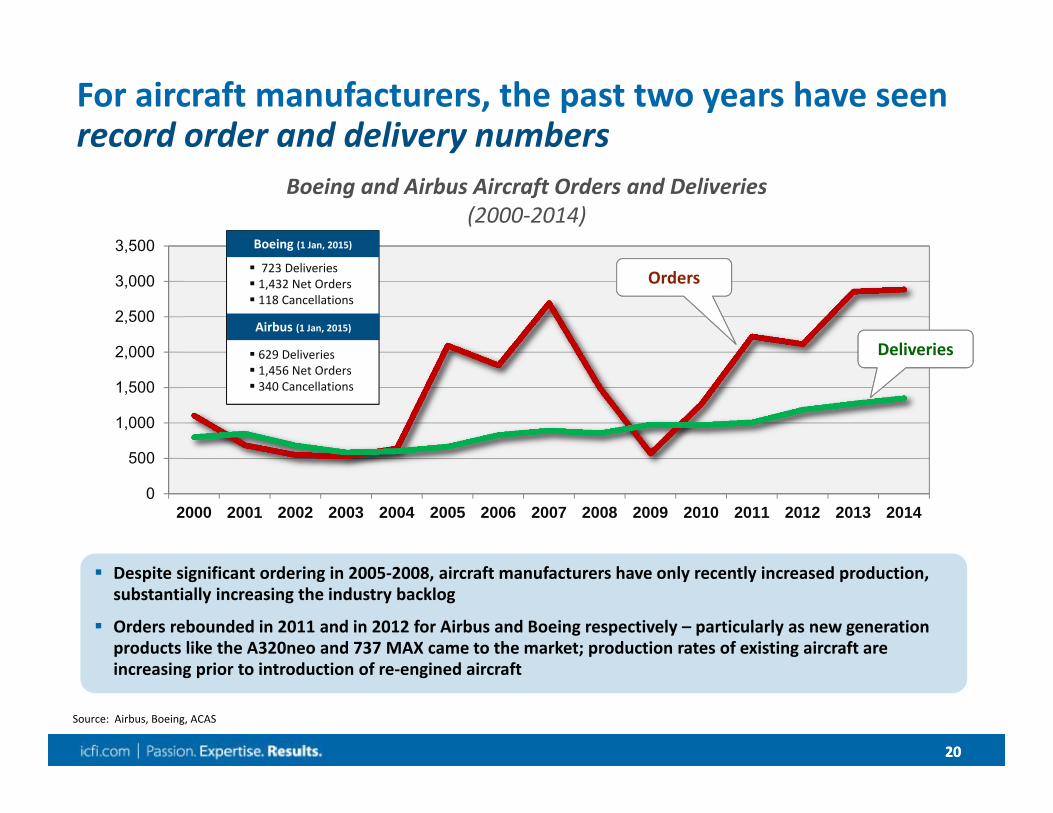

For aircraft manufacturers, the past two years have seen record order and delivery numbers

Despite significant ordering in 2005‐2008, aircraft manufacturers have only recently increased production, substantially increasing the industry backlog

Orders rebounded in 2011 and in 2012 for Airbus and Boeing respectively – particularly as new generation products like the A320neo and 737 MAX came to the market; production rates of existing aircraft are increasing prior to introduction of re‐engined aircraft

Source: Airbus, Boeing, ACAS

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Boeing and Airbus Aircraft Orders and Deliveries (2000‐2014)

Deliveries

Orders

Boeing (1 Jan, 2015)

Airbus (1 Jan, 2015)

629 Deliveries 1,456 Net Orders 340 Cancellations

723 Deliveries 1,432 Net Orders 118 Cancellations

2121

Airline strategy continues to evolve – a new long‐haul, low cost model has emerged

Note: Aircraft includes those place by operator and by lessors assigned to operator; Source: Innovata; CAPA

December 2013

December 2015 • 26 787‐9 Dreamliners on order• 9 long‐haul destinations added

2222

Airline strategy continues to evolve – hybrid low cost carriers are blurring the line between full service carriers and pure low‐cost carriers

Source: Innovata

New hybrid model: combination of cost savings methodology of pure LCCs with the services, flexibility, and routes structure of full service carriers

Low‐cost Carriers Full Service Carriers

Short haul, point‐to‐point

Same fare to all customers

No codesharing

Direct sales only

Single aircraft type/ one seating class

Short and long‐haul; connecting flights

Differentiated fares

Use of codesharing/alliances

Distributes through GDS

Mix of aircraft types / mix of seating classes

Network

Fares

Partnerships

Sales/Dist.

Operations

Examples:

2323

Airline strategy continues to evolve – New global network carriers have emerged to challenge existing players

Source: Innovata

December 2008 December 2015

+39 Destinations

‐8 Destinations

2424

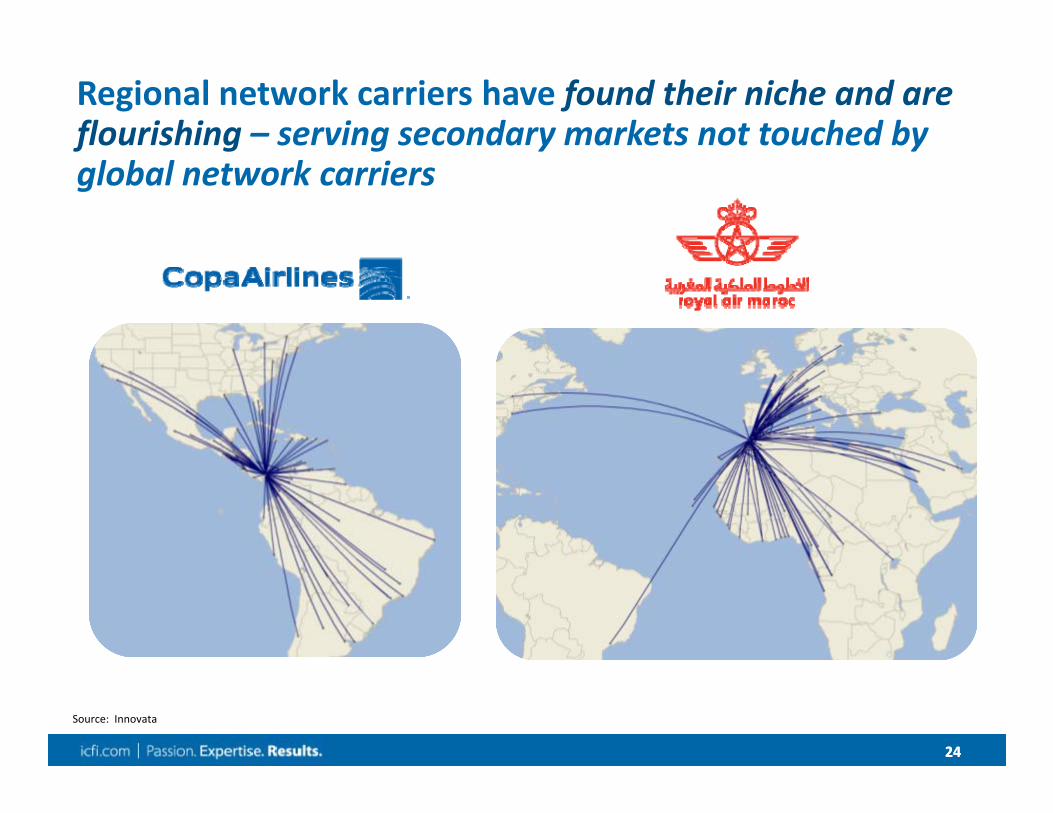

Regional network carriers have found their niche and are flourishing – serving secondary markets not touched by global network carriers

Source: Innovata

2525

What is the aviation outlook beyond 2015?

The air transport industry enjoys solid growth drivers, including:– Population growth

– Increasing air service liberalization

– Economic dynamism of emerging countries

Global economic expansion is expected to, which in turn will drive air travel demand, though performance will vary by region:– North America is leasing the economic global acceleration

– Eurozone is finally gaining momentum

– Despite concerns of economic slowdown in China, Asia remains a high growth region

– Latin American economies dependent on natural resources have slumped recently, though the long‐term trend is positive

Low cost carrier (LCCs) expansion is another aspect of the markets structure that will evolve. Low cost carriers are oised to take advantage of the growing middle classes in emerging markets that are flying for the first time

Source: Airbus

2626

Connecting your Destination through Air Service Development

27

What is Air Service Development (ASD) and what are its primary objectives?

Proactive strategy to influence airlines’ decision‐making process and increase air service by communicating the strengths of your destination – while talking to airlines in their own “language”

OBJECTIVES:

Create new first‐time flights– New markets; New airlines

Maintain existing flights– Monitor current performance

– Stay in contact with the airlines

Promote growth– More frequencies; Larger aircraft;

Better schedule

WHO:

ASD programs can be run by: – An airport, a destination, a region

or at the national level

– Should include multiple stakeholders so the destination talks with one‐voice

For all types of destinations:– Leisure, religious, cultural, etc.

28

Why does your airport/destination need an Air Service Development Program?

Your destination is competing with thousands of other destinations for air service – airlines have limited fleets and resources!

Airports Around the World – Traffic Density

2929

What does an ASD program consist of?

Ongoing Communication with Airlines and Operators – Not just one time!

Talk to airlines in their own language – with their own metrics and methodologies

Information about the

destinations (news ahead of time)

Quantitative business case with a specific proposal and

forecast

Team of stakeholders: one entity the

airline can speak with about service

Incentive program and support for the airline

A well‐coordinated effort that combines:

3030

Air Service Development strategy involves a diagnostic of the market, establishing a strategy and creating an implementation plan

1Diagnostic 2 DefineStrategy 3 Implement

Air Service Development Strategy

Benchmarking

Historical Evaluation

Airline Strategy

Identify Opportunities

Estimate Demand

Prioritize

Define Communication Plan

Conferences and Meetings

Support Channels

Business Cases

Introduction to the Market

Demand Statistics

Proposed Itinerary

Traffic/Revenue Projections

Incentives and Support

The Business Cases are the key tool for executing your Air Service Development Strategy

The Business Cases are the key tool for executing your Air Service Development Strategy

3131

The diagnostic of the airport environment is an essential step in identifying new opportunities for air service

Benchmarking– Compare the service offering (destinations, airlines, frequencies) of your airport vs.

competitors in the same region

Historical evaluation of traffic and service offering– Understand where the growth is, what hasn’t worked, where there is potential for growth,

etc.

Airline Strategy– Understand how airlines operate (Hub, point to point), evolution of alliances, aircraft

orders, etc.

3232

161100 100 82

52 48 28 22

93

206

92

369

5034

0

50

100

150

200

250

300

350

PTY LIM BOG SCL SJO CCS UIO GYE

Domestic

International

Example: Comparison of Quito’s international service vs. other airports in the region

Source: OAGSource: OAG

Weekly Seats by Airport (‘000s) June 2014

UIO has a lower international service offering than its competitorsUIO has a lower international service offering than its competitors

3333

The diagnostic allows you to define a strategy, focusing on and prioritizing objectives to increase air service

Identify potential routes and airlines– What existing routes merit additional service?

– What new routes do I want to promote?

– What airlines do I want to attract?

Estimating Origin‐Destination demand– This is the key element of air service development that allows you to:• Determine the volume of traffic in the local market and beyond‐hub• Understand the seasonality of traffic• Identify the point of sale

Establish priorities– Prioritize opportunities in the short, medium, and long‐term

– Understand the effort needed to achieve each objective

3434

Lastly, the best method of implementing the strategy should be determined – attending meetings and taking advantage of other support channels

Define how to contact the airlines of interest– Conferences and/or direct meetings with airlines

– Begin with the regional office or directly with headquarters?

– Contacting the right people saves time: Planners

Choose the conferences/frequency of attendance that best fit your strategy– Regional, global conferences• Routes, Jumpstart, Tourism conferences for vacation markets

– How many times per year?

Take advantage of external support channels– What other stakeholders can support the effort to develop air service?

35

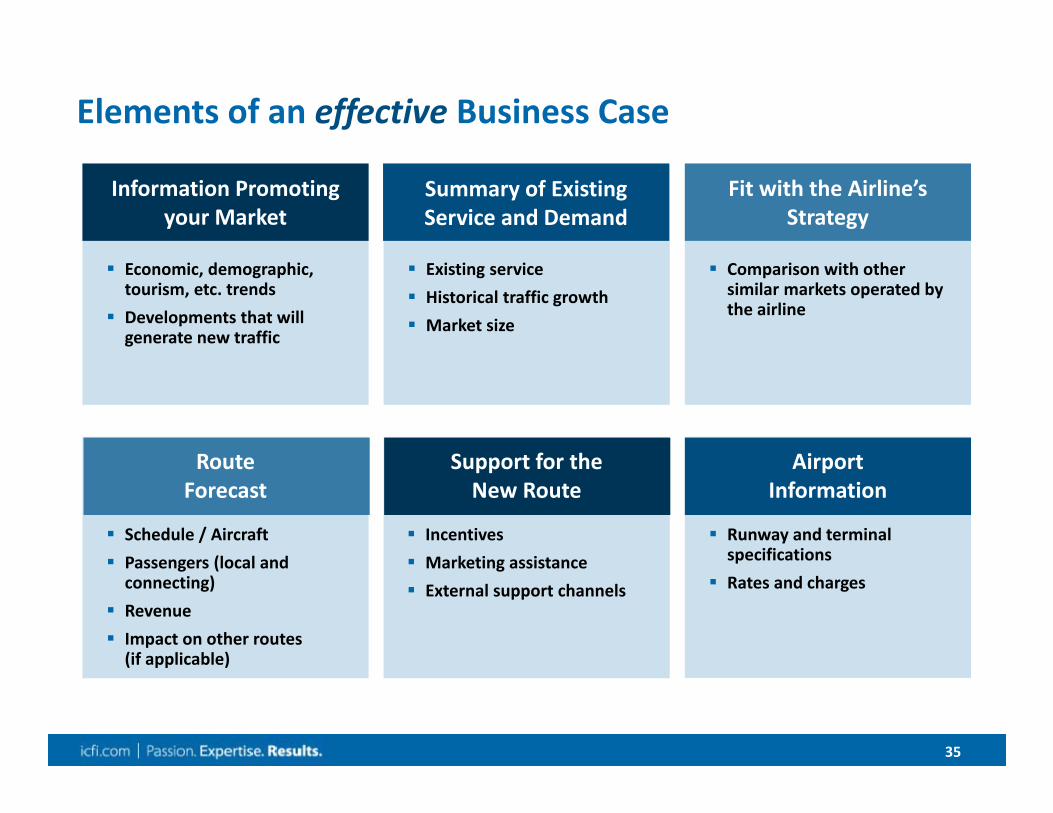

Elements of an effective Business Case

Economic, demographic, tourism, etc. trends

Developments that will generate new traffic

Existing service Historical traffic growth Market size

Comparison with other similar markets operated by the airline

Schedule / Aircraft Passengers (local and connecting)

Revenue Impact on other routes (if applicable)

Information Promoting your Market

Summary of Existing Service and Demand

Fit with the Airline’s Strategy

Route Forecast

Support for the New Route

Airport Information

Incentives Marketing assistance External support channels

Runway and terminal specifications

Rates and charges

36

Risk sharing and commitment are sought by many airlines, by way of financial incentives

Financial incentives from the airport can take many forms:– Discounts on traditional airport fees– Creative solutions (e.g. rebates, fuel savings) – Pre‐purchase of airline tickets by local businesses for

future use– Revenue and profitability guarantees– Funds for advertising and promotion

Other Stakeholders– Discounts on hotel, transportation and meals for

airline crew overnights– Preferential rates for airline vacation programs at

hotels and tourist attractions

Examples of airport discounts– Landing Fees– Security screening– Jet‐bridge

– Parking– Rental of check‐in counters

and office space

3737

Growing Air Service Usually Requires You…

Work with an Air Service Committee of stakeholders– If you don’t have one, start one!

Include Air Service planning – far in advance

Talk to airlines and operators regularly– Have an ongoing relationship with them– Tell them things they don’t know– Give them concrete proposals and financial incentives– The destination should speak with one voice and present unified proposals

– Attend “Routes” conferences, both global and regional– Attend relevant tourism conferences such as ITB, FITUR, World Travel Market

If you are not sure of how to do these things, ask for help!

3838

Golden Rules:

1 Do not assume that airlines and operators have enough staff or enough information to be evaluating your market regularly – they don’t!

2 Airports and destinations must be continually supplying information and making proposals in order to stay “top of mind”

3 Remember that you are competing with (many) other destinations and airports for limited airline capacity

3939

Airline Route Planning Process

40

Formal planning process

Centralized planning process with little input from regional offices

Various planning levels with different time horizons

Expansion plan guided by long‐term strategy

Focused on profitability

Less formal process

Value the input of their regional representatives

Few decision makers

Expect to share the risk (with the airport, tour operators, etc.)

Focused on growth

Focused on high volumes of traffic

In order to make logical and interesting route proposals to airlines, it’s important to understand how airlines think

Traditional Airlines “Niche” Airlines

4141

FINALIZE

The planning process for a traditional airline is long…

PLANNING

STRATEGY

FleetProductNetwork DesignFacilities

MarketsStaffItinerary StructurePreliminary Itinerary

5 Years 3 Years – 18 Months This YearHorizon

Final ItineraryAvailability of staff/gatesRates/Slots

4242

…While for “niche” airlines, the process is more streamlined

PLANNING

STRATEGY

FleetProduct

Prioritization of markets

1‐2 Year This YearHorizon

You will probably present to a

decision‐maker

You will probably present to a

decision‐maker

4343

What do airlines consider when evaluating a new route?

Network Strategy– Net new aircraft (orders minus retirements)

– Hub(s) structure– Strategy for short/long haul– Strategy for Latin America– Alliance strategy

Risks and Opportunities

Financial Position– Liquidity– Costs and revenue vs. competitors

4444

How does an airline decide to deploy its fleet?

If an airline doesn’t increase its active fleet, new service can only be added if an existing service is cancelled – It is difficult to create new international service by increasing the fleet’s utilization (i.e., the hours operated)

New (net) aircraft can be used for:– Increase frequencies on existing routes– No route development costs

– Increase the aircraft size on an existing route– No route development costs

– Open a new route/destination– Requires investment in staff, offices, marketing, etc.

4545

For the airport, the question is whether there is or is not demand– Can a high load factor and good fare be achieved?

For the airline, traffic and profitability are just the beginning– Do we have the right aircraft?– Does the route fit within our network strategy?• Independent• Our alliance

– Is the risk – reward trade‐off acceptable?– How does this opportunity compare with others?

For airlines, route planning is a question of finding the best use of limited resources

46

What chance does an airport have in influencing the decision‐making process of an airline?

Minimize risks associated with opening a new route

Make the best use of limited resources– Aircraft and staff– Planning analysts (important: airlines

cannot assess all opportunities)

Identify and analyze hundreds of new route opportunities– Participation in route development

conferences demonstrates that airlines seek help in this process

Reduce or share the risk– Reduce airport costs– Marketing assistance– Economic incentives for the route

Demonstrate a commitment to the client’s needs– Efficient operations– Modern and well‐maintained

infrastructure

Identify opportunities through a logical, quantitative, and convincing Business Case

The Goals of the airline… …are Opportunities for the airport

4747

Conducting a Route Forecast

4848

Overview of the route forecasting process

Identify potential markets

Choose the aircraft type for the airline/market

Collect data on existing demand and service offered

Define assumptions for the forecast– Suggested itinerary– Growth rate of traffic– Average fare– Market share

4949

Considerations when choosing the proposed aircraft

Aircraft range

Size corresponds to level of demand

Aircraft used by the airline in similar markets

Orders and delivery schedule

Operating restrictions– Runway length– Height above sea level, temperature– Noise restrictions

Key FactorsKey Factors

5050

Example of aircraft range analysis

Engine CF6-80C2B7F GE90-94B GEnx-1B70 CFM56-7B26 CFM56-7B27-B1 PW2040Capacity 218 PAX @ 210 lb 300 PAX @ 210 lb 242 PAX @ 210 lb 126 PAX @ 210 lb 162 PAX @ 210 lb 201 PAX @ 210 lb

Distance (nm) 767-300ER 777-200ER 787-800 737-700 737-800 757-200Europe

MAD 4,711 YES - 9,800 lb cargoAMS 5,148 NO NO NOCDG 5,043 YES - 520 lb cargo

LatinAmericaEZE 2,377 YES - 42,300 lb cargo YES - 6,900 lb cargo YES - 860 lb cargoSCL 2,058 YES - 10,400 lb cargo YES - 4,800 lb cargoGRU 2,341 YES - 7,400 lb cargo YES - 1,300 lb cargo

North AmericaEWR 2,446 YES - 6,200 lb cargo YES - 70 lb cargo YES - 12,260 lb cargoYYZ 2,610 YES - 4,482 lb cargoLAX 3,024 YES - 26,600 lb cargo

AsiaICN 8,143 NO NO NO

Preliminary Analysis of Aircraft Range

51

Local

Connecting Online

Interline

With Code Share partners

Possible PassengerFlows

Types of Connections

Identify local and connecting markets (on the same airline or multiple airlines) what will feed the proposed route

5252

PaxIS– Captures tickets purchased through all travel agencies that participate in IATA’s BSP and includes:• Origin and Destination airports, Connecting airports• Airline that markets and operates each segment, Point of sale• Month of trip, Fare class

– PaxIS supplier, IATA, estimates full market size

Market Information Data Tapes (“MIDT”) – Captures reservation data from the primary GDS systems (Amadeus, Sabre, Worldspan y Galileo). The level of detail is similar to what is provided by PaxIS

Estimate the size of the Origin – Destination market: the essential ingredient for making a successful Business Case

Sources of Origin – Destination Traffic Data

However, neither MIDT nor PaxIS capture direct sales…However, neither MIDT nor PaxIS capture direct sales…

53

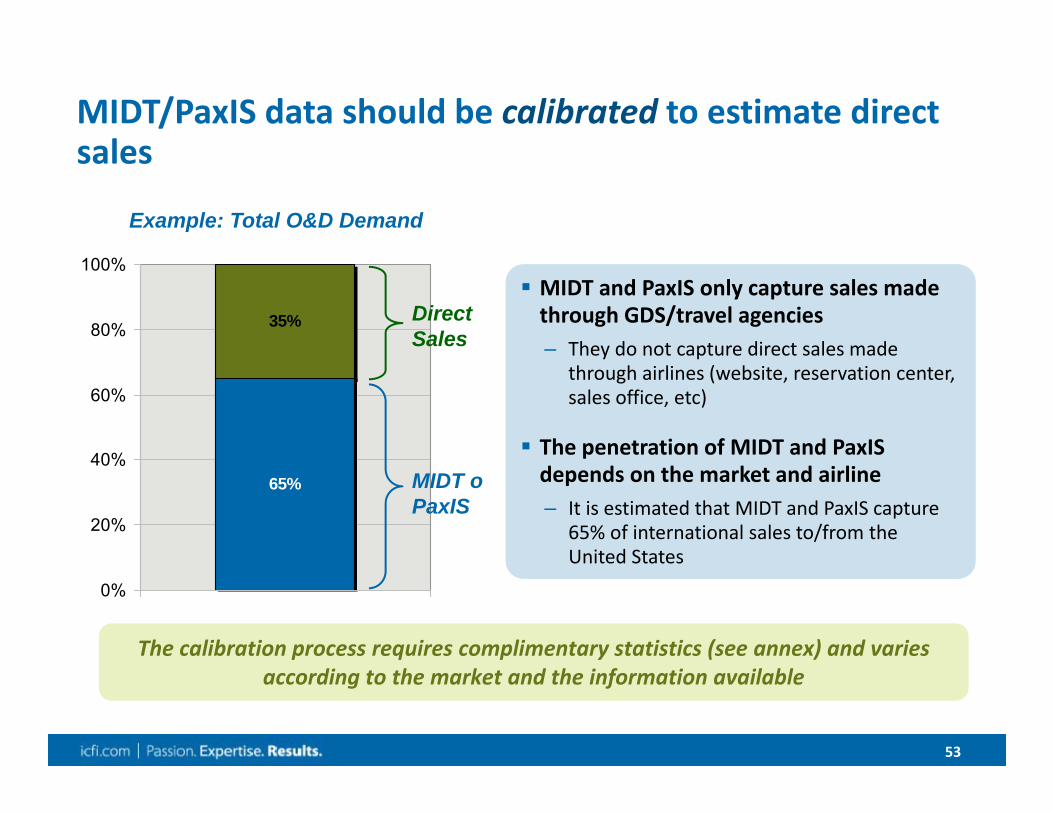

MIDT/PaxIS data should be calibrated to estimate direct sales

65%

35%

0%

20%

40%

60%

80%

100% MIDT and PaxIS only capture sales made through GDS/travel agencies– They do not capture direct sales made

through airlines (website, reservation center, sales office, etc)

The penetration of MIDT and PaxISdepends on the market and airline– It is estimated that MIDT and PaxIS capture

65% of international sales to/from the United States

MIDT and PaxIS only capture sales made through GDS/travel agencies– They do not capture direct sales made

through airlines (website, reservation center, sales office, etc)

The penetration of MIDT and PaxISdepends on the market and airline– It is estimated that MIDT and PaxIS capture

65% of international sales to/from the United States

Example: Total O&D Demand

MIDT o PaxIS

DirectSales

The calibration process requires complimentary statistics (see annex) and varies according to the market and the information available

5454

After calculating the actual Origin – Destination traffic, the demand stimulus generated by the new service must be estimated

New nonstop flights typically stimulate traffic demand– Stimulus is the result of easier market access and greater marketing of the destination (airlines, tour operators, etc.)

– New service attracts new passengers, just as it allows existing passengers to travel more frequently (above all in the business segment)

A market’s first nonstop flight can stimulate demand between 100% and 300%

In addition to demand in the local market, it is common to see lesser stimulation in connecting markets, especially when the airline serving the new route has a strong presence in the connecting markets

5555

For example, KLM’s entrance in the Amsterdam‐ Panama City market stimulated traffic

0

200

400

600

800

1,000

1,200

1,400 Other routingsAMS‐PTY nonstop6‐month average

1,030 Pax/Month(+161%)

395Pax/Month

1,150Pax/Month(+192%)

Amsterdam – Panama City TrafficApril 2007 – March 2010

Amsterdam – Panama City TrafficApril 2007 – March 2010

Source: MIDT, April 2007 – March 2010

MonthlyPassengers

5656

Estimating average fares by origin – destination market

Both PaxIS and MIDT have information on average fares by market– However, both sources tend to over estimate the fare as more price –sensitive passengers tend to to use direct sales channels

Average fares by airline and market can also be found on the internet– Travel agencies such as Expedia, Travelocity, Orbitz, etc.– Search engines such as Sidestep, Kayak, etc.– Airline websites

In order to estimate the average fare on the proposed route, it isrecommended to use the best information possible for markets with a similar profile as a point of reference

5757

Choosing the schedule – Key Factors

It is an airline that connects passengers through a hub?– If so, the schedule should fit into a connecting bank in order to maximize traffic

Does the airline have alliance partners at the airport?– If so, “online alliance” connections should be considered

What are the schedules in similar markets?– Overnight?– Morning arrival/departure? Evening? Etc.

How many weekly frequencies?– The maximum possible should be proposed according to demand, but also consistent with similar markets operated by the airline

Seasonal or year‐round service?– Depends on the seasonality of traffic and the type of market (business, leisure, VFR, etc)

5858

For example, in the case of a proposal for Copa, any new route should fit into a connecting bank

-10

-5

0

5

10

7:00

8:00

9:00

10:0

0

11:0

0

12:0

0

13:0

0

14:0

0

15:0

0

16:0

0

17:0

0

18:0

0

19:0

0

20:0

0

21:0

0

22:0

0

Operations by hour at PTYJune 2010

Operations by hour at PTYJune 2010

Arr

ival

sto

PTY

Dep

artu

res

from

PTY

Source: OAG Schedules

Bank1 Bank2 Bank3 Bank4

5959

All of this information is needed for the essential analysis of the Business Case: the forecast of market share, passenger traffic, and revenue on the proposed route

ICF SH&E uses NETWORKS, a proprietary tool that models route schedules to estimate the market share of each airline– Currently used by British Airways, Copa Airlines, Virgin Atlantic, Oneworld

NETWORKS is “QSI” (Quality of Service Index) model, an industry‐accepted methodology for calculating carrier share

NETWORKS quantifies the market share of each segment (the “QSI”), taking into account: – Type of service (Online, Interline, Etc.)

– Frequency

– Number of stops and connections

– Total travel time (between origin and destination)

– Type of aircraft (size, jet vs. turboprop)

– Etc.

6060

What is a “local” passenger?

“Local” passengers begin their journey at the flight’s departure airport and end their journey at the flight’s arrival airport (and vice versa)– Local passengers do not make connections or change planes

Example: Houston – Quito

IAH UIO

6161

What is a connecting passenger?

A connecting passenger begins their journey at a point before flight’s origin and/or ends their journey at a point beyond the flight’s destination– These passengers make one or more connections

Example: Houston – Quito

UIO

NRT

ORD

IAH

62

QSI example: SCL – NYC market

SCL

LIM

MIA

NYC

AA/LA

DL

AA

DL

LA

ATL

LALA

Source: SH&E NETWORKS based on OAG schedules June 2010

QSI Share SCL‐NYCJune 2010

Option Time Frequency Stops Cxns

LA nonstop 10:50 5x weekly 0 0

LA via LIM 12:30 Daily 1 0

AA via MIA 13:40 Daily 1 1

DL via ATL 13:55 Daily 1 1

LA41%

AA29%

CM6%

DL14%

Others10%

6363

The model quantifies each service in the market and allocates traffic and revenue according to its market share

Note: SICF uses thenomenclature “CSI” to refer to “QSI”

“QSI” is calculated based on several service perameters

Each carrier’s market share is based on its QSI score

6464

Traffic and Revenue Forecast for the Route FLL – UIO2010

Frequency: 2x WeeklyAircraft: A319Frequency: 2x WeeklyAircraft: A319

Revenue from passenger tickets is complemented by other sources (cargo, onboard sales, etc), which is estimated based on each airline’s experience

Revenue from passenger tickets is complemented by other sources (cargo, onboard sales, etc), which is estimated based on each airline’s experience

(Financials in USD) Per Flight Per Week (4 Flights)Passengers % Total Revenue Passengers Revenue

Local MarketMiami - Quito 54 56% $11,678 217 $46,712

Connecting MarketsNew York - Quito 29 30% $4,118 118 $16,473Chicago - Quito 4 4% $520 15 $2,082Quito - Washington 3 3% $483 13 $1,934Boston - Quito 3 3% $377 11 $1,508Orlando - Quito 2 2% $290 8 $1,161Other 2 2% $129 7 $517Total Connecting 43 44% $5,919 173 $23,675

Total Pax/Pax Revenue 98 $17,597 390 $70,386

Other Revenue ( @ 10% of pax) $1,760 $7,039Total Flight Revenue $19,356 $77,425

Load Factor 68%Average Fare (excl. surcharges) $180

The final result is a traffic and revenue forecast for the proposed route

Local PassengersLocal Passengers

Connecting Pass.Connecting Pass.

Other RevenueOther Revenue

Load Factor and FareLoad Factor and Fare

Frequency and AircraftFrequency and Aircraft

6565

For top tier airlines, network simulation tools have become an integral part of today’s management decision making process

Why? In an increasingly complex business environment with narrowing profit margins, simulation enables airlines to reduce financial exposure and risk

Who uses NetWorks?

Schedule and network planners Airline strategists Fleet and capacity managers Revenue Planners, and Regional Managers

… to help them better understand their network’s strengths and weaknesses – by itself and against its competitors

Network & Schedule Analysissystems and services

[ ][ ][ ][ ]

Created for Air France and fully developed for British Airways over ten years ago, NetWorks has been

continuously refined ever since

Created for Air France and fully developed for British Airways over ten years ago, NetWorks has been

continuously refined ever since

NetWorks traces its heritage to SH&E founder Nat Simat, who developed the original methodology while serving on the US CAB

6666

NetWorks is used to generate and model scenarios, before evaluating results

Service Generation:– Determines All Feasible Service Offerings in Each Relevant O&D

City‐Pair Market, for Your Airline and Your Competitors– Nonstop, Direct & Connect

– On‐Line, Interline, Code‐Share

– Takes Into Account Connecting Time & Circuity Limitations

Share Estimation:– NetWorks Estimates an “Entitlement Share” of Each O&D Market for each airline

– Based on a Comparison of Service Offerings in Each Market

Traffic Allocation:– Traffic is Allocated to Individual Flights Based on the “Entitlement Share”, Adjusting for

Spill– NetWorks Contains a Realistic Spill Model Which Iteratively Spills Traffic to Alternative Flights as

Capacity Limits are Approached

The key stages of a NetWorks simulation:

6767

Example Business Case

Guadalajara – Amsterdam, KLMGrupo Aeroportuario del Pacifico (GAP)

Prepared by

Mexican Pacific Airport Group (GAP) Route ProposalsMexican Pacific Airport Group (GAP) Route Proposals

Prepared forGAP by

Opportunity in Guadalajara (GDL)

Prepared for:

19 – 22 September 2015

69

Prepared forGAP by

Introduction

Route Forecast:

About the Destination:

Guadalajara is the 11th largest economy

in Latin America

Guadalajara is the second most

populous city in Mexico…

Guadalajara is one of the major

business destinations in

Mexico

Market Aircraft Season Passenger Segment

Weekly Freq.

Estimated Load Factor

AMS-GDL A330 Annual Business 3 84%

…with access to a population of more

than 16 million

#2

70

Prepared forGAP by

Mexican Pacific Airport Group (GAP) maintains and operates 12 airports in Mexico, as well as Montego Bay Jamaica

Source: GAP

Airport Code

Guadalajara GDL

Tijuana TIJ

Puerto Vallarta PVR

Los Cabos SJD

Hermosillo HMO

Leon BJX

La Paz LAP

Mexicali MXL

Morelia MLM

Aguascalientes AGU

Los Mochis LMM

Manzanillo ZLO

Montego Bay MBJ

TIJ4.4-3%%

GAP airports served 29.2 million passengers in the 12 months ending June 2015, representing 4% growth over the previous year

MXL0.57%

HMO1.3-5%

LAP0.71%

SJD3.1-11% PVR

3.418%

GDL9.17%

LMM0.325%

ZLO0.2-1%

MLM0.54%

AGU0.619%

BJX1.323%

Passengers, MillionsYear-over-Year % Change

Investors include:

GAP listed on:

MBJ3.86.7%

Prepared by

Mexican Pacific Airport Group (GAP) Route ProposalsMexican Pacific Airport Group (GAP) Route Proposals

Prepared forGAP by

Market Overview of Guadalajara

72

Prepared forGAP by

Mexico Highlights

Population of 121 million

Second most populous country in Latin America after Brazil

Member of the North American Free Trade Agreement (NAFTA) with the United States and Canada

In 2014, Mexico was the world’s 15th

largest economy*

Largest Latin American trading partner with Europe and second largest with Middle East/Asia

Average annual GDP growth of 3.5% projected between 2015 and 2018

*2014 Current prices

Sources: IMF World Economic Outlook April 2015; Inter-American Development Bank; European Commission

73

Prepared forGAP by

Passenger traffic and trade between Mexico and Europe have seen steady growth over the last five years

Source: IATA PaxIS, Instituto Nacional de Estadística, Geografía e Informática (INEGI)

The passenger air market between Mexico and Europe has grown by 9% annually in the last 5 years

O&D Passenger Traffic Trend

0

500

1,000

1,500

2,000

2,500

3,000

3,500

YE June2011

YE June2012

YE June2013

YE June2014

YE June2015

Passengers (‘000)

Mexico – Europe O&D TrafficYE June 2011 – YE June 2015

CAGR YE June ‘11 – YE June ‘15: +9%

% Growth Y-o-Y Change +22% 1% +8%+6%

USD Million

0

10

20

30

40

50

60

70

80

YE June2011

YE June2012

YE June2013

YE June2014

YE June2015

Imports from Europe

Exports to Europe

Trade Between Mexico and EuropeYE June 2011 – YE June 2015

+15% +5% +2%-1%Y-o-YChange

CAGR YE June ‘11 – YE June ‘15: +5%

74

Prepared forGAP by

Guadalajara will offer 858 weekly passenger departures to 52 destinations in October 2015

Source: Innovata October 2015

GAP Airports

27 destinations

22 destinations

Panama City

Guatemala City

San José

75

Prepared forGAP by

Guadalajara is the capital of the state of Jalisco, which combined with surrounding states has a population of more than 16 million

Guadalajara has the 2nd largest catchment area in Mexico

16.4m

Source: Consejo Nacional de Población, 2010 census

Rank Catchment Area Airport Population (millions)

1 Mexico City MEX 25.0

2 Guadalajara GDL 16.4

3 Monterrey MTY 11.5

Catchment Area Population = Drive time of 4 hours or less

Top 3 Catchment Areas in Mexico

25.0m

11.5m

GDL

MTY

MEX

76

Prepared forGAP by

Guadalajara is known as the “Silicon Valley” of Mexico, given the strong presence of technology and software companies

150Software and services

companies

20+ Universities that

graduate thousands of engineers and design students each year

600+ High‐technology

companies, more than any other city in Mexico

Guadalajara is home to…

Source: Plan Maestro para el Centro Creativo Digital

8Software/Technology

parks

77

Prepared forGAP by

Guadalajara is fast becoming a hub for start-up and creative/design companies

26 design centers and a multimedia park

35 business in the “Centro de Software”, a start-up incubator

IBM opened a “Smarter Cities Exploration Center” in Guadalajara dedicated to designing solutions for infrastructure challenges

Guadalajara is home to the Ciudad Creativa Digital (CCD), a cluster of digital, entertainment, and creative industries

78

Prepared forGAP by

Recent Business Developments:

The state of Jalisco received USD $1.2 billion in Foreign Direct Investment (FDI) in 2014

Source: El Financiero; El Economista

•After a recent outreach trip to Europe, the state of Jalisco received tentative commitments for investment of at least USD $200 million from 4 German auto manufacturers

•Nestle announced plans to invest USD $360 million in the construction and operation of a food plan that will open in 2016

•Several technology companies have announced investment for expansion projects in the region, including Cisco (USD $30m); Intel (USD $33.7m); y IBM (USD $4.5m)

•Hyatt will open a new hotel in Guadalajara in 2016 with 200 rooms

• A Starwood Luxury Collection Hotel will open in 2015

79

Prepared forGAP by

Source: Secretaría de Desarrollo Económico del Estado de Jalisco

European and Asian companies have offices in Jalisco

European Companies with Investment in Jalisco2007 – May 2015United Kingdom

Avntk S.C.

Worldmark De MéxicoXyratex

NetherlandsAD Optical Disc de México

Hitachi Global Storage Technologies

SpainCopreci de México S.A. De C.V.

Globa End´SHotel Riu Plaza Guadalajara

Inmobiliaria FadesamexMexikor

GermanyBader

Bdt MéxicoBoeringer Ingelheim Vetmedica

BoschContinental Automotive

DräxlmaierEpiq Mx

Fresenius Medical Care de MexicoGoTech

Petosa S.A.de C.V. Polymer Technik Elbe (PTE)

Siemens VDOVoit Automotive de México

VorwekWoco Tech de Mexico

Zf Sachs Suspension México

FranceAlmeria

Gamelofts de R.L. de C.VPromotora Automotriz (FIAT)

Sidel de MéxicoTechnicolor Mexicana

Total México S.A. de C.V.Virbac

Efi Automotive

SwitzerlandNestle México

Kuehne & Nagel

SwedenSandvik Mining and Construction

H&M

IndiaHCL Technologies Mexico

MGDC SC (Tata)

JapanDaido Metal

Miyazaki Seiko

Nippon Shokuhin

80

Prepared forGAP by

Foreign investment from Europe is distributed across a variety of sectors and totaled USD $500 million 2014

Source: Secretaría de Desarrollo Económico del Estado de Jalisco; Ciudad Creativa Digital

Investment Projects in the State of JaliscoBy Sector2011-2014

Automotive42%

Electronics17%

Renewable Energy9%

Trade8%

Food and Beverage8%

Aerospace8%

Construction4%

Information Technology

4%

The state of Jalisco has been the country’s leader in investment in the electronics sector for the past decade

In 2014, 15 companies have decided to invest in Jalisco, with a total investment of $500 million dollars and 2,600 potential employees

81

Prepared forGAP by

Due to a large number of both business and leisure travelers throughout the year, Guadalajara has a well-developed hotel infrastructure

Source: SECTUR. Cifras preliminares 2012

Guadalajara has many rich cultural attractions including, colonial architecture, museums,

shopping, various dining options, and exciting nightlife

Accommodation in GDL (2014)

Rooms (4 stars or more) 10,773

% Occupancy (4 stars or more) 58%

82

Prepared forGAP by

In 2017 a new highway will open between Guadalajara and Puerto Vallarta, reducing the drive time by 90 minutes

The new highway will connect Guadalajara with Puerto Vallarta in 3 hours (current drive time is 4.5 hours)

Puerto Vallarta is a popular leisure destination in Mexico, offering 40 km of beaches, world-class golf courses and sport fishing, among other activities

GDL

83

Prepared forGAP by

Guadalajara is a Gateway to other economically important regions in its catchment area

Sources: El Financiero; El Economista

Leon-Guanajuato

Aguascalientes

Michoacán

León-Guanajuato is one of Mexico’s most economically important cities

The state has a high presences of companies in the agro-industrial and automotive industries

Aguascalientes is another leading city in the country’s automotive industry

There are currently 75 automotive industry investment projects underway, with over 100 companies operating in the sector

These three regions are more accessible from Guadalajara

than Mexico City

Michoacán is an important logistics center with modern highway, rail, maritime, and air transportation infrastructure

The state’s geographic position gives it access to 60 million consumers, or 55% of national consumption

84

Prepared forGAP by

0 2 4 6 8

7. Nayarit

6. San Luis Potosi

5. Aguascalientes

4. Guanajuato

3. Querétaro

2. Michoacán

1. Colima

Guadalajara Mexico City

Most of the flights between Mexico and Europe go through Mexico City, and the majority of the passengers from the Guadalajara catchment areadrives to Mexico City to travel

Ground Travel TimeGuadalajara catchment area versus Mexico City

Ground Time

Places in states like Guanajuato, Aguascalientes, Michoacán, Colima and Nayarit have easier access to GDL, by distance and to avoid the

chaotic traffic at Mexico City

Source: México SCT

Time (Hours)

GDL

MEX1.

2.

3.4.

5.

6.

7.

85

Prepared forGAP by

The demand between Guadalajara and Europe, potential for KLM, consists of the local market from the city of Guadalajara and thedemand in the catchment area

GAP and ICF have used the following method to build market sizes:

1

2

3

4

Local demand from GDL

Passengers in the Guadalajara catchment areawho currently travel from/to Mexico City (using a point of sale analysis)

Market stimulation following new non-stop service

Size of the demand

=

+

+

86

Prepared forGAP by

KLM has the opportunity to be a leading airline between Mexico and Europe with a potential demand of more than 1,800 passengersweekly each way between Guadalajara and its catchment area

Potential demand between Guadalajara and EuropeActual air traffic + Traffic from the Guadalajara catchment area

Average weekly demand 2016, one-way

1/ Includes Jalisco, Guanajuato, Michoacán, Querétaro, Aguascalientes, Colima and Nayarit2/ Does not include the demand stimulation due to a new non-stop service

Source: MIDT – POS Analysis, PaxIS Market Sizes and ICF Analysis

The potential number of passengers who could fly from/to Guadalajara and who are currentlyflying from/to Mexico City was determined based on the analysis of the zip codes of passengers

flying from/to Mexico City

Local demand – one way Guadalajara –Amsterdam

Guadalajara – OtherEuropean destinations

Guadalajara – AllEurope

Actual Area 39 1,210 1,249

Diverted MEX1

(Guadalajara Area of Influence) 18 545 563

Total Potential withoutstimulation2 57 1,755 1,812

87

Prepared forGAP by

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Jul-06 Oct-06 Jan-07 Apr-07 Jul-07 Oct-07 Jan-08 Apr-08

CM launched PTY-GDL

Stimulation = 252%

Source: IATA PaxIS

A new non-stop flight, on a market without non-stop flights or only served by connecting flights, stimulates air demand

Panama City– Guadalajara Demand Stimulation due to Copa New ServicePassengers

0

500

1,000

1,500

2,000

2,500

Apr-07 Jul-07 Oct-07 Jan-08 Apr-08 Jul-08 Oct-08 Jan-09

KL launchedAMS-PTY

Stimulation = 186%

Amsterdam – Panama City Demand Stimulation due to KLM New ServicePassengers

0

500

1,000

1,500

2,000

2,500

Nov-10 Feb-11 May-11 Aug-11 Nov-11 Feb-12 May-12 Aug-12

KL launchedAMS-UIO

Stimulation = 152%

Amsterdam – Quito Demand Stimulation due to KLM New Service

Passengers

88

Prepared forGAP by

Note: Local TimeSource: ICF / GAP Analysis, OAG Schedules

KLM Schedule for Proposed Amsterdam – Guadalajara Nonstop Seasonal ServiceThree Weekly Flights on an 330-200

There is currently no non-stop service from Amsterdam to Guadalajara

New service from Europe to Guadalajara have historically resulted in traffic stimulation; the same is expected for Amsterdam – Guadalajara

GAP and ICF used a 90% conservative stimulation

KLM’s code-share agreements with its SkyTeam partners Air France and Aeromexico will enable KLM to reap the benefit of numerous connection opportunities

The proposed schedule is modeled after existing flights from Europe to Mexico and aims to maximize connecting traffic by leveraging synergies with Aeromexico, its SkyTeam partner

330-200 Aircraft 330-200135 Frequency 135

City10:00 Depart Amsterdam Arrive 11:52

14:52 Arrive Guadalajara Depart 17:00

Flight Distance: 9,365 kmAvg. Flight Time: 11:52

Paris, Madrid, Barcelona, London, Roma & Others

Connections via Amsterdam MCT: 90 min.

Mexico City, Culiacan, Mexicali, Tijuana, Veracruz & Others

Connections via GuadalajaraMCT: 90 min.

89

Prepared forGAP by

KLM could achieve a 84% average load factor in the Amsterdam –Guadalajara market

AMS GDL

Connection in AMS

Market Weekly Pax*

% of onboard

Paris 73 12%

Madrid 43 7%

Barcelona 31 5%

Zurich 29 5%

Rome 29 5%

Others 360 59%

Total Connecting 614 92%

AverageFare*:

US $582

QSI Share:

70%

Weekly Pax Each Way 2016:

60

Local MarketStimulation:

90%

Weekly Pax with Stimulation:

114

Loca

l Tra

ffic

*Average fare for all onboard passengers

Load Factor

84%A330-200

[3 Weekly Frequencies]

Local market share of onboard:

8%

Aircraft:

*Passengers each way

Tota

l

Notes: /1 GAP and ICF further adjust PaxIS Plus data to insure accuracy on market sizes/2 Based on IATA Traffic Forecast for the period YE May 2015 growth rate 2016 for Mexico-Europe market is 5.0%/3 Available Air fare data sources (PaxIS) do not include YQ's, taxes and commissions

90

Prepared forGAP by

Guadalajara has become a cargo center offering non-stop air services, not only in the Americas but in Asia and Europe

Source: WTC Confianza

Air France, Lufthansa, Cargolux y Panalpina offer direct air Service to

Paris, London-Stansted, Frankfurt and Luxemburg from Guadalajara

Destination Weekly Frequency

Aircraft Type

91

Prepared forGAP by

Multinational companies with offices in Jalisco move air cargo from and to Guadalajara

Source: WTC Confianza

Mexican and foreign

companies from different sectors

are part of the cargo ecosystem

of Jalisco

92

Prepared forGAP by

Europe is the second largest cargo destination to/from Guadalajara with 22% share of the cargo traffic

Share of Cargo Tonnage at Guadalajara by Origin/Destination Region

CY 2014

Source: WTC Confianza

Asia47%

Europe22%

North America

22%

South America6%

Others3%

Guadalajara is the perfect gateway to connect Mexico and Latin America with Europe

93

Prepared forGAP by

Guadalajara International Airport

Operates 24 hours a day, seven days a week

Two operating runways; the longest has a length of 3,999 meters

3rd busiest airport in Mexico in terms of annual passengers

Equipped with CUTE and CUSS systems

2nd busiest cargo airport in Mexico by volume

GAP will invest USD 35 million between 2015-2017 to expand

the passenger terminal

94

Prepared forGAP by

GAP is pleased to incentivize the new route by offering a discount on airport services for one year at GAP airports

The above package includes 100% discounts on Airport Services (Landing, parking, etc.), Passenger and Carry-on Screening Charges.

A discount of 100% in Airport Space Rental will also be included.

If KLM decides to open the route, GAP will also offer a 100% rebate in TUA at Guadalajara.

The above discounts do not include a rebate of the check-in luggage screening, buses and air bridges.

GAP is currently working to develop the incentives plan for Montego Bay.

Source: GAP, ICF Analysis

* These incentive amounts are representative, pending final schedules, passenger traffic and negotiations

The following discounts would be offered to KLM:

Market Season Weekly Freq.

Estimated Load Factor

Annual Incentive (USD)

AMS-GDL Annual 3 84% $XXX

95

Prepared forGAP by

GAP has the relationships and market knowledge to assist KLM in its evaluation of the proposed route

Market Analysis• GAP & ICF airport group are prepared to assist KLM with all due diligence required

to gain a thorough understanding of the proposed route

Market Analysis• GAP & ICF airport group are prepared to assist KLM with all due diligence required

to gain a thorough understanding of the proposed route

Visit to Guadalajara and Montego Bay • GAP would like to invite the KLM planners to visit GAP at the Guadalajara and

Montego Bay airport facilities and its touristic locations

Visit to Guadalajara and Montego Bay • GAP would like to invite the KLM planners to visit GAP at the Guadalajara and

Montego Bay airport facilities and its touristic locations

Visit to KLM’s offices• Alternatively, GAP would be pleased to meet with more KLM staff at corporate

headquarters

Visit to KLM’s offices• Alternatively, GAP would be pleased to meet with more KLM staff at corporate

headquarters

96

Prepared forGAP by

Mexican Pacific Airport Group Contact Information

Phone:+52 (33) 3880-1100

Dial 266 or 336 for Airline Marketing Services

Fax - Dial 339

Corporate Offices:Mariano Otero #1249 B

6th Floor (World Trade Center)Rinconada del Bosque

Guadalajara JaliscoMexico, 44530

Grupo Aeroportuario del Pacifico is the holder of the concessions to operate 12 international airports in Mexico, covering an influence area with a population of approximately 34.5 million.

Fernando Bosque [email protected]

Tomas RamirezChief Commercial [email protected]

Omar MirandaCommercial Airport Revenue [email protected]

Carlos CharpenelCommercial Activities and [email protected]

Florencia ZermeñoCommercial Activities and [email protected]

9797

Tactics for Small Markets

9898

What are some of the challenges small markets face in air service development?

Lack of reliable origin‐destination demand data for your marketLack of reliable origin‐destination demand data for your market11

22

33

44

55

Current demand does not reflect the full potential of your market

Convincing Airlines that flying to your destination will not negatively impact their other flights

Generating greater visibility with Airlines to differentiate yourself from competing markets

What can be done if demand is not sufficient enough to justify air service?

9999

Challenge #1 – Lack of reliable data for estimating current demand in your market

Common data sources for origin‐destination (O&D) demand are MIDT or IATA PaxIS…

In many cases, passengers in small markets do not arrive by plane but by bus, or have to buy two separate tickets (one international and one domestic)

Nevertheless, there are alternatives to measure and estimate demand:– MIDT / IATA PaxIS by Point of Sale

• Passengers that buy in your city by fly from another airport

– Estimate demand in proportion to total national demand• For example, based on the % of country GDP that your city/region represents

– Establish comparisons with other similar destinations• For example, based on the population’s purchasing power, number of 4‐star hotels, etc.

– Evaluate national or regional government statistics• For example, tourist arrivals to archeological sites, hotel nights, etc.

Typically data from different sources must be compared and combined for a complete view of current demand

100100

Challenge #1 – Lack of reliable data for estimating current demand in your market – Example

101101

Challenge #2 – Current demand does not reflect the full potential of your market

Various factors could make current demand lower than its true potential:– Limited air service offering– High airfares– Unattractive flight times

IT is well known by Airlines that limited air service reduced demand, and that an increase in the number of seats generates an increase in demand

In such cases, estimated demand must be stimulated in order to reflect the impact of the new flight– It is important to analyze examples of market stimulation generated by Airlines (using MIDT or IATA PaxIS)

102102

Challenge #2 – Current demand does not reflect the full potential of your market – Example

Roundtrip Airfares

$565

$415

$690

$560

MIA‐SMR MIA‐AUA MIA‐IQT MIA‐MAO

Nota: tarifas aéreas vigentes el 19 de mayo para salidas el 17 de junio y estadia de una semana. MIA‐SMR en Avianca; MIA‐AUA en InselAir; MIA‐IQT en Copa y MIA‐MAO en LATAM

Destinations with little air service tend to have higher fares than similar destination

with more air service

‐27%

‐19%

Santa Marta (SMR)

Iquitos (IQT)

103103

Challenge #3 – Convincing Airlines that flying to your destination will not negatively impact their other flights

When an airline already operates service to your country or airport, they may fear that adding an new flight will negatively impact their existing flights. For example:– United, which operates IAH‐Quito, might fear that EWR‐Quito will steal traffic from its flight to IAH

– Copa, which operates PTY‐Lima, might fear that PTY‐Chiclayo affect its Lima flight

Destinations must show Airlines that the new flight will complement the existing service, instead of cannibalizing it. But how?

Using a QSI analysis, combined with current flight load factor data– QSI (Quality of Service Index): allows modelling of how traffic that is “diverted” to the new flight is replaced by new demand

– Load factors: there is a relationship between load factor and the “spill” (demand that cannot be filled by the airlines)

104104

Challenge #3 – Convincing Airlines that flying to your destination will not negatively impact their other flights ‐ Example

105105

Challenge #4 – Generating greater visibility with airlines to differentiate yourself from competing markets

Competition for attracting new routes is intense: there are more routes and potential destination than what airlines are able to serve

In a context where demand exceeds supply, your destination must stand out among the rest – above all when it is a smaller and less well known market

There are various methods for achieving this objective:– Develop convincing analyses – without this, there is no working strategy

• Airlines seek relevant data that demonstrate the viability of the route

– Participate actively in route development conferences• The biggest is World Routes

• For tourism destinations, there are other events such as FITUR

– Visit with Airlines at their offices• Ideally after a making a first introduction

• The involvement of other stakeholders in highly recommended

– Offer a robust incentive program, including financial guarantees• These costs should be absorbed by the community, not just the airline

106106

Challenge #5 – What can be done if demand is not sufficient enough to justify air service – Example

There will be routes that simply do not have the demand needed to justify new service, but play an important, strategic role for your destination

There are alternatives that can generate more traffic for your destination

If you want to attract traffic from long‐haul markets where there is potential demand, you might suggest to a codeshare agreement to an airline to carry traffic to your airport– This generates additional traffic for the airline operating the flight, with low marginal costs – In some cases, it codesharing could lead to an increase in the size of the aircraft being used to

operate to your market to accommodated the increased demand– This is a low‐risk option for all parties

107

Thank You!