ENHANCING THE DEVELOPMENT OF THE ELECTRICITY FUTURES MARKET · PDF fileENHANCING THE...

16

ENHANCING THE DEVELOPMENT OF THE ELECTRICITY FUTURES MARKET CONSULTATION PAPER Closing date for submission of comments and feedback: 31 August 2017 1 August 2017 ENERGY MARKET AUTHORITY 991G ALEXANDRA ROAD #01-29 SINGAPORE 119975 www.ema.gov.sg

Transcript of ENHANCING THE DEVELOPMENT OF THE ELECTRICITY FUTURES MARKET · PDF fileENHANCING THE...

ENHANCING THE DEVELOPMENT OF THE

ELECTRICITY FUTURES MARKET

CONSULTATION PAPER

Closing date for submission of comments and feedback:

31 August 2017

1 August 2017 ENERGY MARKET AUTHORITY 991G ALEXANDRA ROAD #01-29 SINGAPORE 119975 www.ema.gov.sg

Disclaimer:

The information in this document is subject to change and shall not be treated as

constituting any advice to any person. It does not in any way bind the Energy Market

Authority to grant any approval or official permission for any matter, including but not limited

to the grant of any exemption or to the terms of any exemption. The Energy Market

Authority reserves the right to change its policies and/or to amend any information in this

document without prior notice. Persons who may be in doubt about how the information in

this document may affect them or their commercial activities are advised to seek

independent legal advice or any other professional advice as they may deem

appropriate. The Energy Market Authority shall not be responsible or liable for any

consequences (financial or otherwise) or any damage or loss suffered, directly or indirectly,

by any person resulting or arising from the use of or reliance on any information in this

document.

1

TABLE OF CONTENT

1. Background ............................................................................................. 2

2. Proposed Market Making Scheme beyond July 2018 ......................... 5

3. Enhancing Product Portfolio of the Electricity Futures Market ....... 12

4. Next Steps.............................................................................................. 13

2

ENHANCING THE DEVELOPMENT OF THE ELECTRICITY FUTURES MARKET

1. Background

1.1. The development of an electricity futures market complements both the existing

wholesale and retail electricity markets, by providing a platform for efficient trading to

manage volatility and mitigate risks. A liquid futures market also provides a robust price

discovery process for future supply of electricity, while enabling efficient transfer of risk

between participants. In addition, the electricity futures market enables the entry of

independent electricity retailers and facilitates new business models. This benefits

consumers by putting downward pressure on prices and facilitating the development of

new retail products.

1.2. The Energy Market Authority (EMA), in partnership with the Singapore Exchange (SGX)

and the electricity industry, therefore launched the electricity futures market in April

2015, starting with quarterly base load futures contracts. To better support industry

needs and increase the vibrancy of the electricity futures market, the Singapore

Exchange (SGX) also launched the monthly base load electricity futures contracts in

April 2017. The launch of the monthly contracts complements the existing quarterly

base load futures contracts launched in 2015, and caters to the needs of different

stakeholders. For example, electricity generators can use the monthly product to hedge

more precisely when on planned maintenance, while retailers will have more options to

structure their hedges (especially when their retail contracts may not start at the

beginning of the quarter).

1.3. Since the introduction of the electricity futures market, the number of electricity retailers

in Singapore have increased from 7 to 25, and electricity prices have become more

competitive. According to a study conducted by Professor Frank A. Wolak from Stanford

University, wholesale electricity prices had been lowered by at least 10%, and the prices

of new retail contracts lowered by about 10 to 20% on account of the electricity futures

market1.

1.4. In addition, the electricity futures market has enabled the development of innovative

business models, such as the offering of “green” power packages or green tariffs. Solar

providers are better able to hedge the price risk for providing power during non-sunny

hours, and blend the solar energy into the power package for customers. Another

example of a new business model is power packages linked to energy efficiency or

demand-side management. Energy service providers such as demand response

providers are now able to offer a complete energy package to consumers because they

can leverage on the electricity futures market to hedge their price risk, as the use of

base load electricity futures contracts can provide more price certainty compared to

purchasing solely on the wholesale electricity market.

1.5. As of 31 May 2017, there were 4,186 total lots traded for the quarterly base load

electricity futures contracts (about 4,600 GWh with a total value of approximately $376

1 Please refer to (https://web.stanford.edu/group/fwolak/cgi-bin/sites/default/files/benefits-forward-

contracting_posted.pdf) for the study conducted by Professor Wolak.

3

million). While transaction volumes and open interest2 for the quarterly contracts have

been generally increasing over time (refer to Fig 1), the volume was dominated by

market makers (MMs) (refer to Fig 2), indicating the importance of MMs at this stage of

market development. While MMs are required to put out quarterly contracts for 9

forward quarters at any one point in time, the open interest mix tends to be more heavily

weighted in the earlier quarters; in other words, futures market participants tend to trade

in quarterly contracts over shorter time horizons. Figure 3 lists the open interest mix for

quarterly contracts as of 31 May 2017, for reference.

Figure 1: Volume and Open Interest for Quarterly Contracts as of 31 May 2017 (Source: SGX)

2 Open interest figures refer to the number of contracts outstanding in futures trading, i.e. futures contracts

that have not been closed yet.

4

Figure 2: Volume Mix by Participant for Quarterly Contracts as of 31 May 2017 (Source: SGX)

Figure 3: Open Interest Mix for Quarterly Contracts as of 31 May 2017 (Source: SGX)

5

2. Proposed Market Making Scheme beyond July 2018

Rationale of Proposed Approach

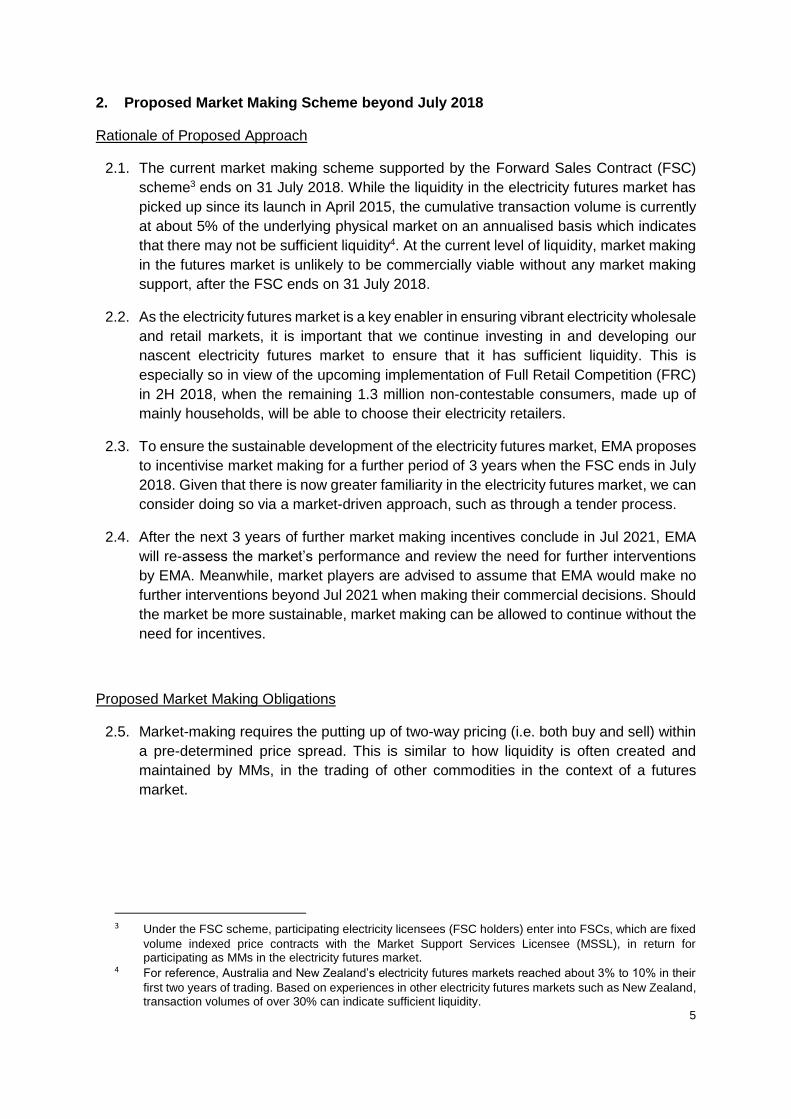

2.1. The current market making scheme supported by the Forward Sales Contract (FSC)

scheme3 ends on 31 July 2018. While the liquidity in the electricity futures market has

picked up since its launch in April 2015, the cumulative transaction volume is currently

at about 5% of the underlying physical market on an annualised basis which indicates

that there may not be sufficient liquidity4. At the current level of liquidity, market making

in the futures market is unlikely to be commercially viable without any market making

support, after the FSC ends on 31 July 2018.

2.2. As the electricity futures market is a key enabler in ensuring vibrant electricity wholesale

and retail markets, it is important that we continue investing in and developing our

nascent electricity futures market to ensure that it has sufficient liquidity. This is

especially so in view of the upcoming implementation of Full Retail Competition (FRC)

in 2H 2018, when the remaining 1.3 million non-contestable consumers, made up of

mainly households, will be able to choose their electricity retailers.

2.3. To ensure the sustainable development of the electricity futures market, EMA proposes

to incentivise market making for a further period of 3 years when the FSC ends in July

2018. Given that there is now greater familiarity in the electricity futures market, we can

consider doing so via a market-driven approach, such as through a tender process.

2.4. After the next 3 years of further market making incentives conclude in Jul 2021, EMA

will re-assess the market’s performance and review the need for further interventions

by EMA. Meanwhile, market players are advised to assume that EMA would make no

further interventions beyond Jul 2021 when making their commercial decisions. Should

the market be more sustainable, market making can be allowed to continue without the

need for incentives.

Proposed Market Making Obligations

2.5. Market-making requires the putting up of two-way pricing (i.e. both buy and sell) within

a pre-determined price spread. This is similar to how liquidity is often created and

maintained by MMs, in the trading of other commodities in the context of a futures

market.

3 Under the FSC scheme, participating electricity licensees (FSC holders) enter into FSCs, which are fixed

volume indexed price contracts with the Market Support Services Licensee (MSSL), in return for participating as MMs in the electricity futures market.

4 For reference, Australia and New Zealand’s electricity futures markets reached about 3% to 10% in their

first two years of trading. Based on experiences in other electricity futures markets such as New Zealand, transaction volumes of over 30% can indicate sufficient liquidity.

6

2.6. The proposed market making obligations, developed in consultation with SGX, are as follows:

Table 1: Proposed specifications for associated market making obligations

Parameters

Existing Obligations (Jan – Jul 2018) Proposed Obligations (Aug 2018 onwards) Rationale for Proposed

Changes Quarterly Base Load Electricity Futures

Monthly Base Load Electricity Futures

Quarterly Base Load Electricity Futures

Monthly Base Load Electricity Futures

Market Making Volume

MMs are required to put up 6 lots of

0.5MW contracts (totalling 3 MW) for

each side, for each of the 9 listed quarterly

contracts

MMs are required to put up 6 lots of

0.5MW contracts (totalling 3 MW) for

each side, for each of the 4 – 6

listed monthly contracts

MMs are required to put up

6 lots of 0.5MW

contracts (totalling 3 MW) for each side,

for each of the first 5 listed quarterly contracts; and

4 lots of 0.5MW

contracts (totalling 2 MW) for each side,

for each of the next 4 listed quarterly

contracts

MMs are required to put up 6 lots of

0.5MW contracts (totalling 3 MW) for

each side, for each of the 4 – 6

listed monthly contracts

For the 9 listed quarterly periods that MMs have to put up contracts at any one point in time, the liquidity in the last 4 listed quarterly periods tends to be lower than the first 5 (refer to Fig 3). As such, EMA is proposing to reduce the required market making volumes in the later four quarters, to reduce the associated burden on MMs. However, EMA is also proposing to institute continuous quoting requirements (reference refresh requirements below), to provide market participants the assurance that continuous prices would be available in the market, even at a lower market making volume.

7

Parameters

Existing Obligations (Jan – Jul 2018) Proposed Obligations (Aug 2018 onwards) Rationale for Proposed

Changes Quarterly Base Load Electricity Futures

Monthly Base Load Electricity Futures

Quarterly Base Load Electricity Futures

Monthly Base Load Electricity Futures

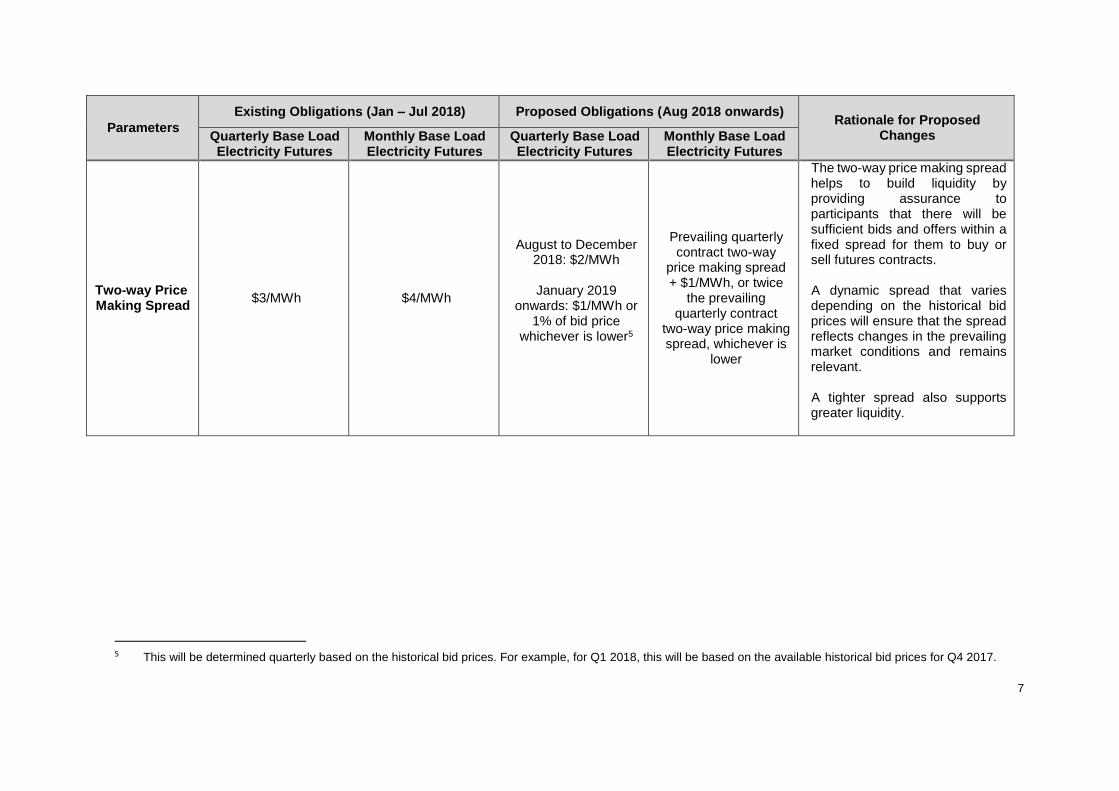

Two-way Price Making Spread

$3/MWh $4/MWh

August to December 2018: $2/MWh

January 2019

onwards: $1/MWh or 1% of bid price

whichever is lower5

Prevailing quarterly contract two-way

price making spread + $1/MWh, or twice

the prevailing quarterly contract

two-way price making spread, whichever is

lower

The two-way price making spread helps to build liquidity by providing assurance to participants that there will be sufficient bids and offers within a fixed spread for them to buy or sell futures contracts. A dynamic spread that varies depending on the historical bid prices will ensure that the spread reflects changes in the prevailing market conditions and remains relevant. A tighter spread also supports greater liquidity.

5 This will be determined quarterly based on the historical bid prices. For example, for Q1 2018, this will be based on the available historical bid prices for Q4 2017.

8

Parameters

Existing Obligations (Jan – Jul 2018) Proposed Obligations (Aug 2018 onwards) Rationale for Proposed

Changes Quarterly Base Load Electricity Futures

Monthly Base Load Electricity Futures

Quarterly Base Load Electricity Futures

Monthly Base Load Electricity Futures

Refresh requirements

Not less than one reload

Refresh of quotes needs to be as soon as

technically or operationally feasible and at most within a 60-second grace period

Continuous quoting

The refresh requirement is an important feature in a liquid electricity futures market to ensure continuous prices are available in the market for participants to enter and exit trading positions. The existing parameters oblige MMs to have no less than one reload of quotes after a trade has been made with respect to their bids. However, they do not require MMs to refresh their quotes the next time the new buy and sell prices are accepted by another participant. This may limit liquidity during periods of high trading. EMA is therefore proposing to institute continuous quoting requirements. These require MMs to reload their two-way pricing immediately after a trade has been made with respect to their bids (e.g. when another participant accepts the price offered by the MM, either on the buy or the sell side), throughout the market making period, which facilitates liquidity.

9

Parameters

Existing Obligations (Jan – Jul 2018) Proposed Obligations (Aug 2018 onwards) Rationale for Proposed

Changes Quarterly Base Load Electricity Futures

Monthly Base Load Electricity Futures

Quarterly Base Load Electricity Futures

Monthly Base Load Electricity Futures

Cumulative Contract Duration

Not less than 2 years (8 full quarters, plus the balance of the current quarter)

4 – 6 consecutive contract months starting with the current contract

month. A new quarter (3 months) will be

listed upon expiry of the nearest quarter6

No change N.A.

Market Making Coverage

The Market Making Coverage – the period within the Market Making Window where MMs meet all their market making obligations – will be (i) not less than 50% of the Market Making Window for each Singapore Business Day (for quarterly contracts only); and (ii) not less than

80% of the cumulative time of all Market Making Windows in a month (for quarterly and

monthly contracts).

The Market Making Window for each Singapore Business Day will be not less than ½

hour, as may be directed by the Exchange (currently set at 4.30pm-5.00pm).

The Market Making Coverage – the period within the Market Making Window where MMs meet all its market making obligations – will be not less than 80% of the cumulative time of all

Market Making Windows in a month (for quarterly and monthly contracts).

MMs will be required to respond to a Request-

for-Quote (RFQ) when they are not quoting during the Market Making Window, with a

Maximum Two-Way Price Making Spread of no more than 1.5 times the prevailing Maximum

Two-Way Price Making Spread.

The Market Making Window for each Singapore Business Day will be not less than ½

hour, as may be directed by the Exchange (currently set at 4.30pm-5.00pm).

The market making period facilitates the concentration of liquidity and trading at specific time periods of each trading day. The RFQ and coverage requirements provide assurance that prices are continuously available during the market making period.

6 The number of contracts varies depending on the month, based on quarters ending on the last day of March, June, September and December. For example, MMs are

required to put up 6 contracts in April 2017 (April to September 2017) but 5 contracts in May 2017 (May to September 2017).

10

Parameters

Existing Obligations (Jan – Jul 2018) Proposed Obligations (Aug 2018 onwards) Rationale for Proposed

Changes Quarterly Base Load Electricity Futures

Monthly Base Load Electricity Futures

Quarterly Base Load Electricity Futures

Monthly Base Load Electricity Futures

Contract Size

Not larger than 0.5 MW over ½ hour per day (i.e. for each of the 48 half-hourly periods in a day) at the Uniform Singapore Energy Price

(USEP) over the contract length

No change N.A.

Contract Length

No longer than quarterly contracts

with near term (prompt) quarter

contract7

No longer than monthly contracts

with near term (prompt) month

contract

No change N.A.

Safeguards

Safeguards to ensure orderly trading, e.g. position, daily, price, volume and concentration

limits

Phased net market making position limit shall be Clearing member’s position limit for each

MM.

No change N.A.

Compliance

Submission of compliance report to EMA, at a frequency of no longer than 6 months, and

whenever reasonably requested by the Authority.

No change N.A.

7 Trading of near term (prompt) quarter contract refers to the availability of the nearest quarter contract for trading within the quarter itself. For example, a trader should

be able to trade an electricity futures contract for Q1 2018 (with maturity date 31 March 2018) within that quarter (e.g. on 2 March 2018).

11

Proposed Tender Parameters

2.7. The proposed tender parameters for such a tender are as follows.

2.8. Uniform Price Auction

2.8.1. Tender for market making services for the quarterly and monthly base load

electricity futures contracts will be done via a uniform price auction where the

awarded price will be based on the highest marginal bid among the selected

Tenderer(s).

2.8.2. EMA reserves the right to determine the number of Tenderers to be selected

taking into account the bids by the respective Tenderers.

2.9. Contract Tenure

2.9.1. Each awarded Tenderer will provide market making services for the quarterly

and monthly base load electricity futures contracts for a duration of 3 years from

1 August 2018 to 31 July 2021.

2.10. Eligibility to Participate in the Tender

2.10.1. Each awarded Tenderer will be required to meet the criteria of the Tender

Exercise which includes, but is not limited to, the ability to meet SGX’s

requirements for participation in the futures market as MMs.

2.10.2. Tenderers are not required to be holders of electricity licences issued by the

EMA. This enables participation by a more diverse range of MMs, which may

be useful in improving liquidity.

2.11. Offers to be Submitted

2.11.1. Each Tenderer must submit an overall bid (in $ per month) to provide market

making services for the two products (i.e. quarterly and monthly base load

electricity futures contracts) over the contract tenure.

2.12. Contractual Arrangements

2.12.1. Based on the evaluation criteria that includes8, but is not limited to, the price

competitiveness of the Tenderers’ respective bids, EMA may select one or

more Tenderers to be awarded the contract to provide market making services.

The awarded Tenderers will be required to enter into a Market Making

Agreement (“MMA”) with SGX to show that they are compliant with the

associated market making obligations.

2.12.2. Any payment for the market making services will be based on fulfilment of the

market making obligations for each monthly period. Failure to fulfil any of the

8 For example, EMA may take into consideration past market making performance of Tenderers for

related products.

12

associated market making obligations within the period will result in non-

payment for that period.

3. Enhancing Product Portfolio of the Electricity Futures Market

3.1. Currently, participants are able to trade the quarterly and monthly base load electricity

futures contracts on SGX. Any introduction of new electricity products by SGX will seek

to benefit the industry by expanding the portfolio of electricity products to stakeholders,

and giving them more hedging options to meet their needs.

3.2. EMA would like to seek feedback on the relevance and viability of new electricity

products which provide useful information for SGX to enhance the product portfolio of

the electricity futures market, as well as the level of interest in market making for such

products. At this stage, EMA does not intend to incentivise market making for new

products. Examples include the following products as shown in Table 2.

Table 2: Indicative contract specifications for new electricity products

Product Indicative Contract Specifications

Monthly Peak Load Electricity Futures

Contract Size: 0.5 MW over each half an hour based on a peak load profile. Peak load profile is defined as the National Electricity Market of Singapore (NEMS) peak load period from 7.00am to 11.00pm Mondays to Fridays (excluding Public Holidays and any other non-trading days determined by SGX)

Contract Period: 4 – 6 consecutive contract months starting with the current contract month. A new quarter (3 months) will be listed upon expiry of the nearest quarter

Final Settlement Price: Arithmetic average of USEP peak load half - hourly prices over the expiring contract month

Average Rate Quarterly Base Load Electricity Options

Underlying Commodity: SGX USEP Quarterly Base Load Electricity Futures

Contract Size: 0.5 MW over each half an hour per day over the contract length

Contract Period: A specified number of consecutive contract quarters (Mar, Jun, Sep, Dec) starting with the current contract quarter

Option Exercise: European style: an option will be exercised automatically at expiry only if it is in-the-money

Final Settlement Price: Final settlement price of the underlying SGX USEP Quarterly Base Load Electricity Futures

13

4. Next Steps

4.1. The EMA seeks views on: (i) the proposed market making scheme outlined in Section

2 of the consultation paper; and (ii) enhancing the portfolio of electricity products

indicated in Section 3 of the consultation paper. EMA also welcomes any other

feedback on improvements to the electricity futures market, and alternatives to the

provision of incentives for market making in the electricity futures market. After

considering the feedback from key stakeholders, the EMA intends to issue a final

determination paper in 2H 2017 to provide details on its decision.

14

REQUEST FOR COMMENTS AND FEEDBACK

The EMA invites comments and feedback to the consultation paper. Please submit written feedback to [email protected] and by 31 August 2017. Alternatively, you may send the feedback by post/fax to:

Attn: Ms Ren Kejia

Energy Market Authority

991G Alexandra Road, #01-29

Singapore 119975

Fax: (65) 6835 8020

Anonymous submissions will not be considered.

The EMA will acknowledge receipt of all submissions electronically. Please contact Ms Ren Kejia at 6376 7759, Ms Michelle Fung at 6376 7523 or Ms Cheong Cui Wen at 6376 7868 if you have not received an acknowledgement of your submission within two business days. The EMA can facilitate meetings with stakeholders on an individual basis to discuss their feedback to this consultation paper. Please contact EMA via [email protected], [email protected] and [email protected] if you wish to arrange a meeting. The EMA reserves the right to make public all or parts of any written submissions made in response to this consultation paper and to disclose the identity of the source. Any part of the submission, which is considered by respondents to be confidential, should be clearly marked and placed as an annex which the EMA will take into account regarding the disclosure of the information submitted.

For clarifications, please contact us at [email protected]