Energy Subsidy Reform - International Monetary Fund · Energy Subsidy Reform: Lessons and...

29

Energy Subsidy Reform: Lessons and Implications for India Thomas Richardson IMF Senior Resident Representative—India Indian Council for Research on International Economic Relations (ICRIER) May 6, 2013

Transcript of Energy Subsidy Reform - International Monetary Fund · Energy Subsidy Reform: Lessons and...

Energy Subsidy Reform: Lessons and Implications for India

Thomas Richardson IMF Senior Resident Representative—India

Indian Council for Research on International

Economic Relations (ICRIER) May 6, 2013

Outline

1. Global Experience with Subsidy Reform

o Consequences of Energy Subsidies

o Magnitude – by Product and Region

o International Lessons for Subsidy Reform

• 22 case studies (www.imf.org/subsidies)

2. Subsidy Reform in India (draft IMF WP)

o Emphasis on Equity Considerations

3

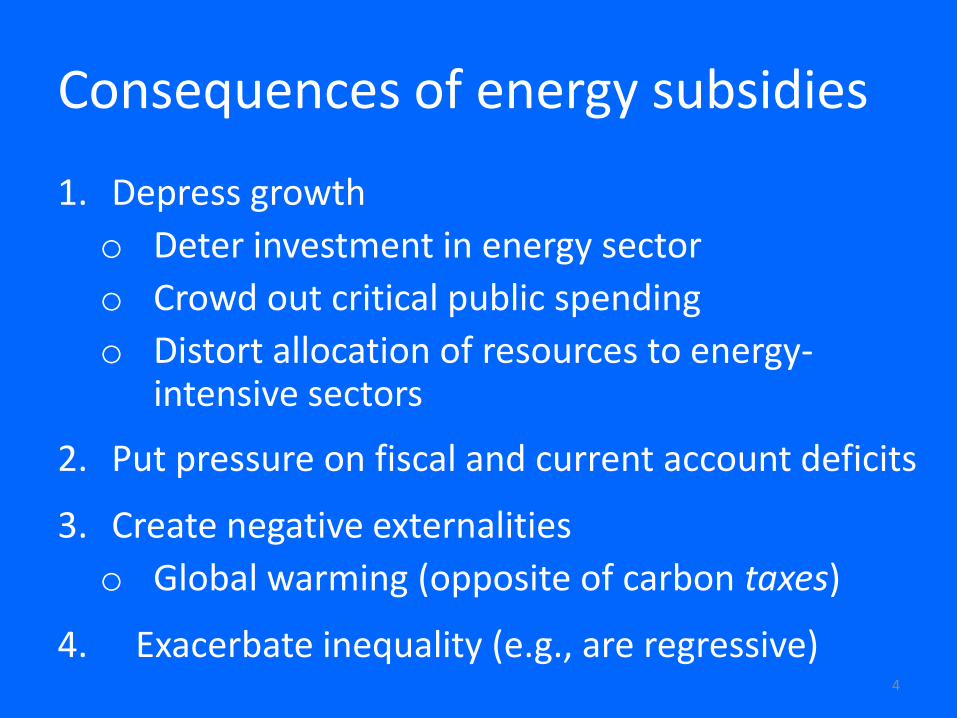

Consequences of energy subsidies

1. Depress growth

o Deter investment in energy sector

o Crowd out critical public spending

o Distort allocation of resources to energy-intensive sectors

2. Put pressure on fiscal and current account deficits

3. Create negative externalities

o Global warming (opposite of carbon taxes)

4. Exacerbate inequality (e.g., are regressive) 4

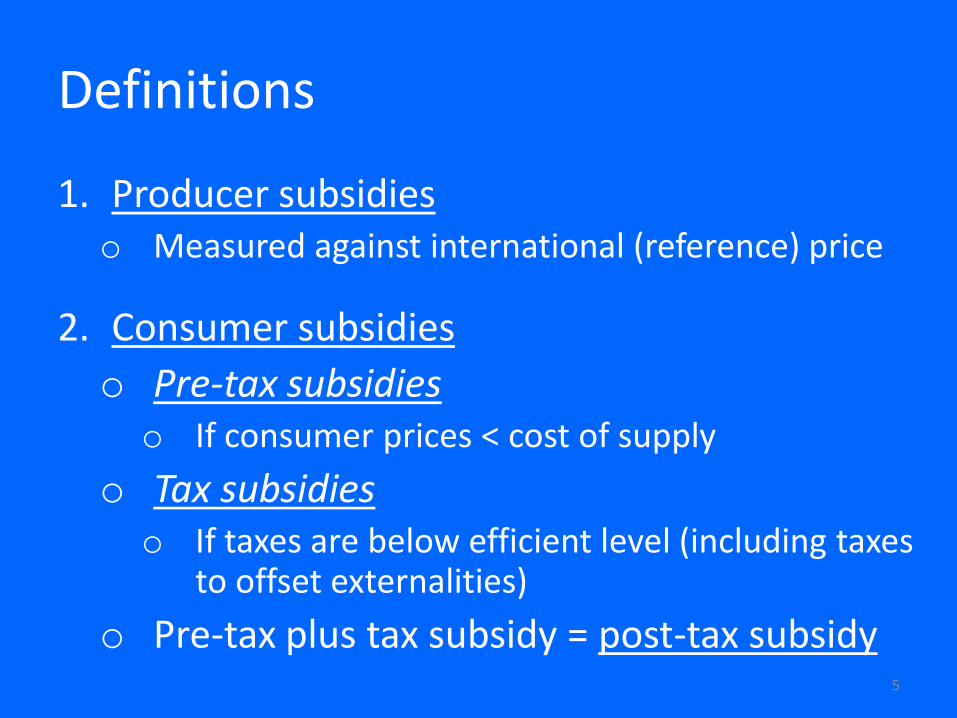

Definitions

1. Producer subsidies o Measured against international (reference) price

2. Consumer subsidies

o Pre-tax subsidies o If consumer prices < cost of supply

o Tax subsidies o If taxes are below efficient level (including taxes

to offset externalities)

o Pre-tax plus tax subsidy = post-tax subsidy 5

Magnitude of energy subsidies: Petroleum and electricity dominate pre-tax subsidies

Pre – tax: $480 billion (0.7% GDP, 2.1% revenues)

Petroleum

products

Natural

gas

Electricity

Coal

6

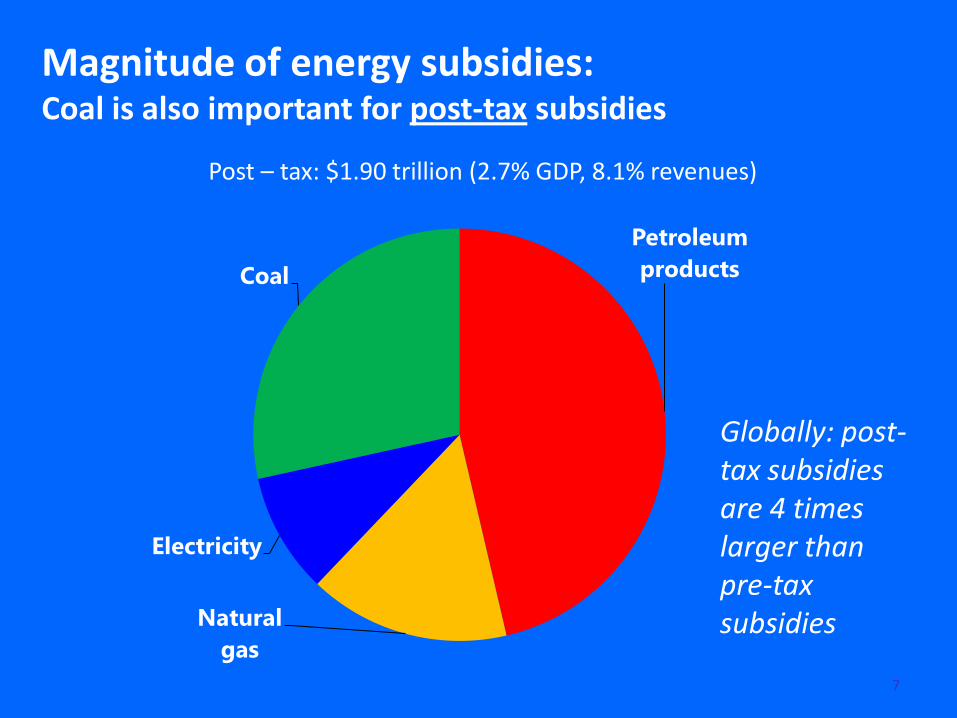

Magnitude of energy subsidies: Coal is also important for post-tax subsidies

Post – tax: $1.90 trillion (2.7% GDP, 8.1% revenues)

7

Petroleum

products

Natural

gas

Electricity

Coal

Globally: post-tax subsidies are 4 times larger than pre-tax subsidies

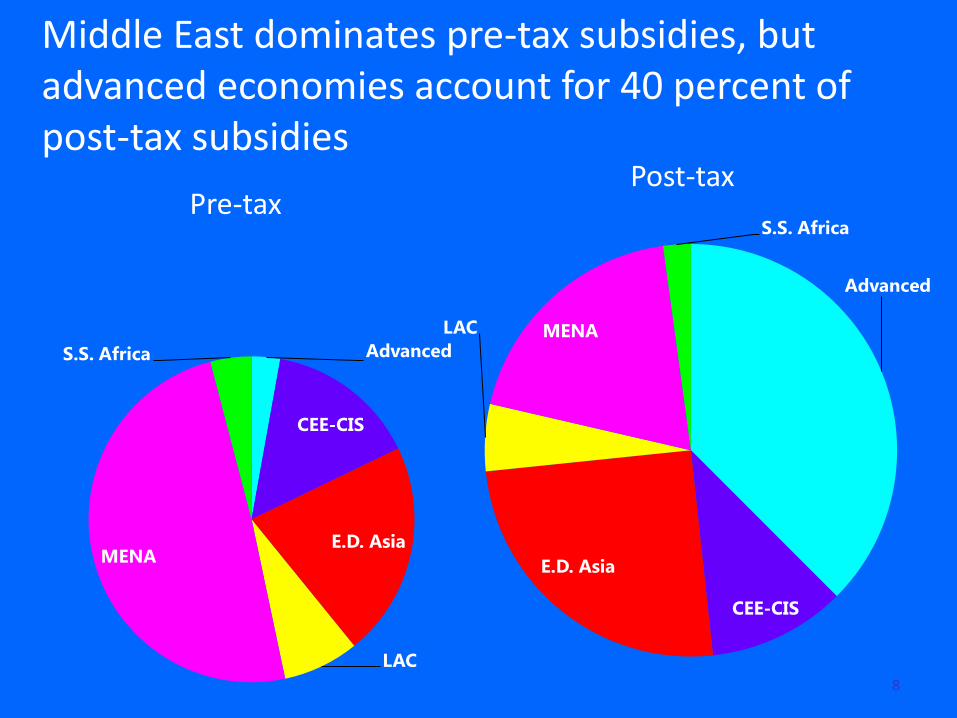

Middle East dominates pre-tax subsidies, but advanced economies account for 40 percent of post-tax subsidies

Advanced

CEE-CIS

E.D. Asia

LAC MENA

S.S. Africa

Advanced

CEE-CIS

E.D. Asia

LAC

MENA

S.S. Africa

Pre-tax Post-tax

8

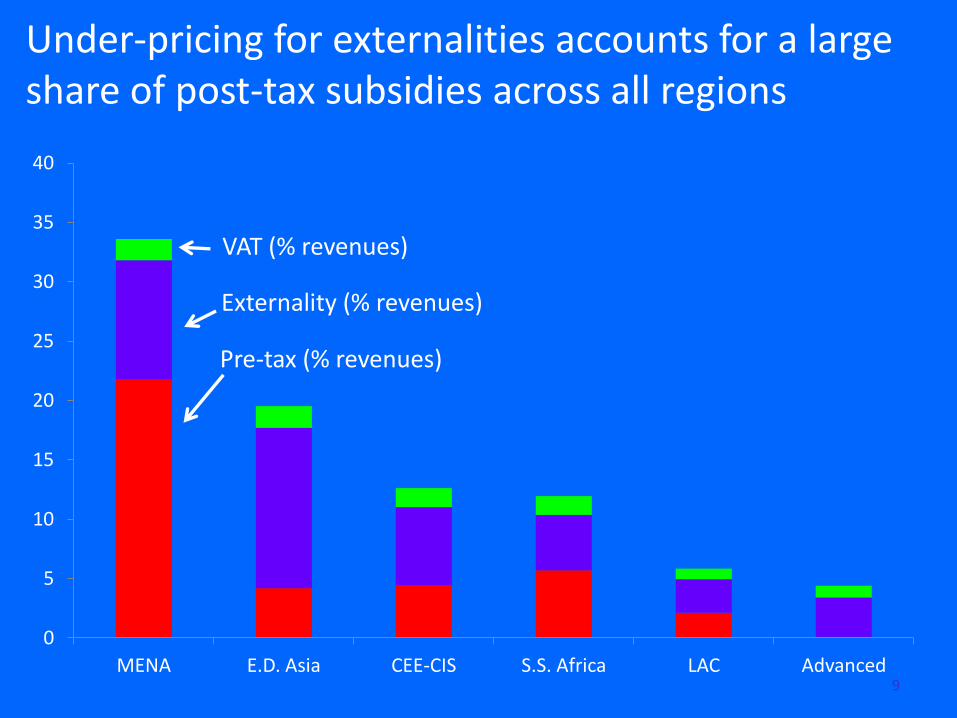

0

5

10

15

20

25

30

35

40

MENA E.D. Asia CEE-CIS S.S. Africa LAC Advanced

Under-pricing for externalities accounts for a large share of post-tax subsidies across all regions

VAT (% revenues)

Externality (% revenues)

Pre-tax (% revenues)

9

International Lessons for Subsidy Reform

o Based on 22 case studies

o All 5 regions of the world

o 28 reform episodes:

• 12 successes, 11 partial successes, 5 failures

• Uganda is one (success)

Six key reform ingredients

10

Six Key Reform Ingredients

1. Comprehensive reform plan o Clear long-term objectives

o Assess impact of reforms (who wins, loses)

2. Extensive communication strategy o Transparency about size of subsidies

o Consult w/ stakeholders about benefits of reform

3. Appropriately phased, sequenced price hikes o Allow time to adjust, build safety net

o Sequence increases differently across products Petrol & diesel, then LPG, then kerosene

11

Six Key Reform Ingredients

4. Improve efficiency of state-owned firms

o Depoliticize, set performance targets, introduce competition if appropriate

5. Target mitigating measures to protect the poor

o Targeted cash transfers are preferred

o Expand other programs if cash transfers impossible

6. Depoliticize price (tariff) setting

o Automatic, rules-based price mechanism

May involve price smoothing

o Autonomous body to oversee price setting 12

Case Study: Ugandan Electricity Sector

Background: Power sector reformed in late 1990s

Problem (as of 2011-12): Politicization: “Independent” regulator left tariffs unchanged for 10 years

-- Subsidy (mainly on-budget) > 1% GDP

-- Little investment in sector (load shedding)

Solution: Broad discussion of incidence of benefits

(only better-off families had power)

One-off tariff hike & independent tariff setting mechanism

13

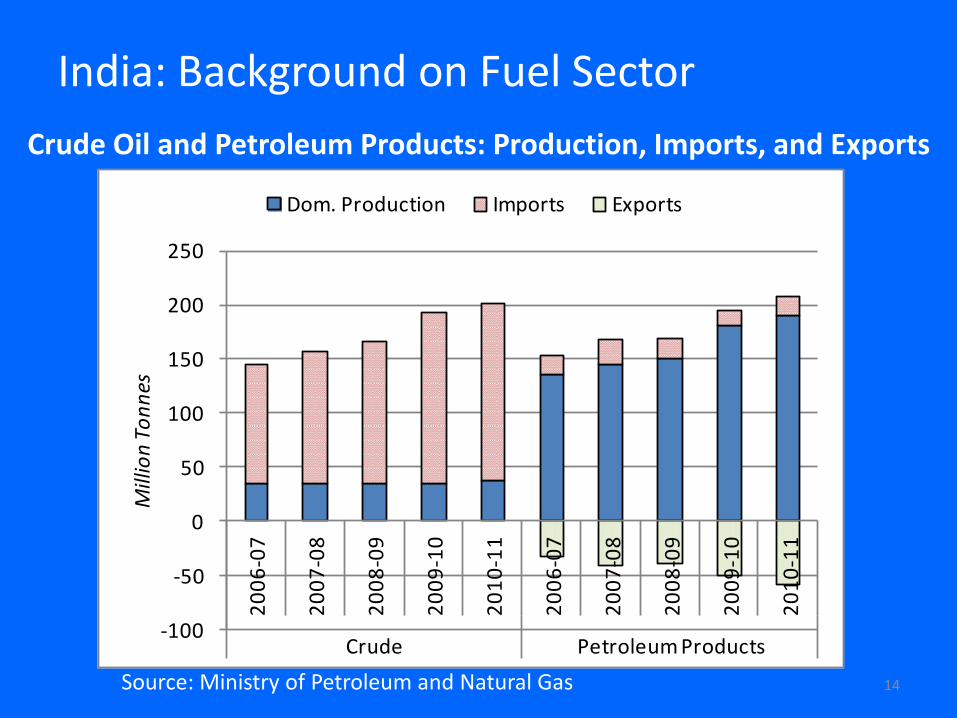

India: Background on Fuel Sector

14

-100

-50

0

50

100

150

200

2502

00

6-0

7

20

07

-08

20

08

-09

20

09

-10

20

10

-11

20

06

-07

20

07

-08

20

08

-09

20

09

-10

20

10

-11

Crude Petroleum Products

Mill

ion

Ton

nes

Dom. Production Imports Exports

Source: Ministry of Petroleum and Natural Gas

Crude Oil and Petroleum Products: Production, Imports, and Exports

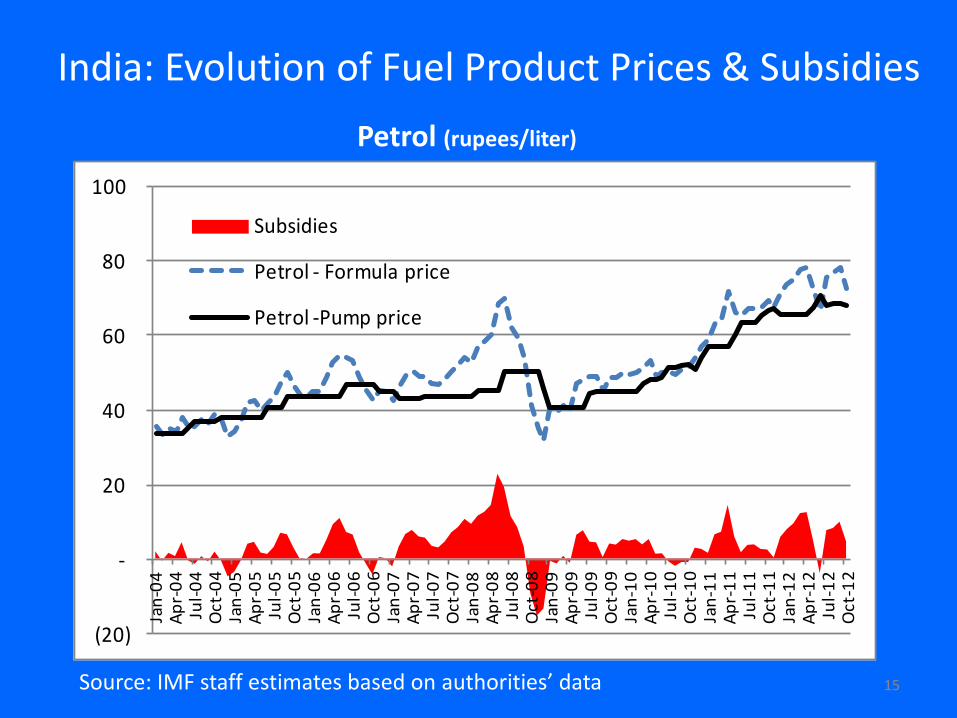

India: Evolution of Fuel Product Prices & Subsidies

15 Source: IMF staff estimates based on authorities’ data

Petrol (rupees/liter)

(20)

-

20

40

60

80

100

Jan

-04

Ap

r-0

4Ju

l-0

4O

ct-0

4Ja

n-0

5A

pr-

05

Jul-

05

Oct

-05

Jan

-06

Ap

r-0

6Ju

l-0

6O

ct-0

6Ja

n-0

7A

pr-

07

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8Ju

l-0

8O

ct-0

8Ja

n-0

9A

pr-

09

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0Ju

l-1

0O

ct-1

0Ja

n-1

1A

pr-

11

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2Ju

l-1

2O

ct-1

2

Subsidies

Petrol - Formula price

Petrol -Pump price

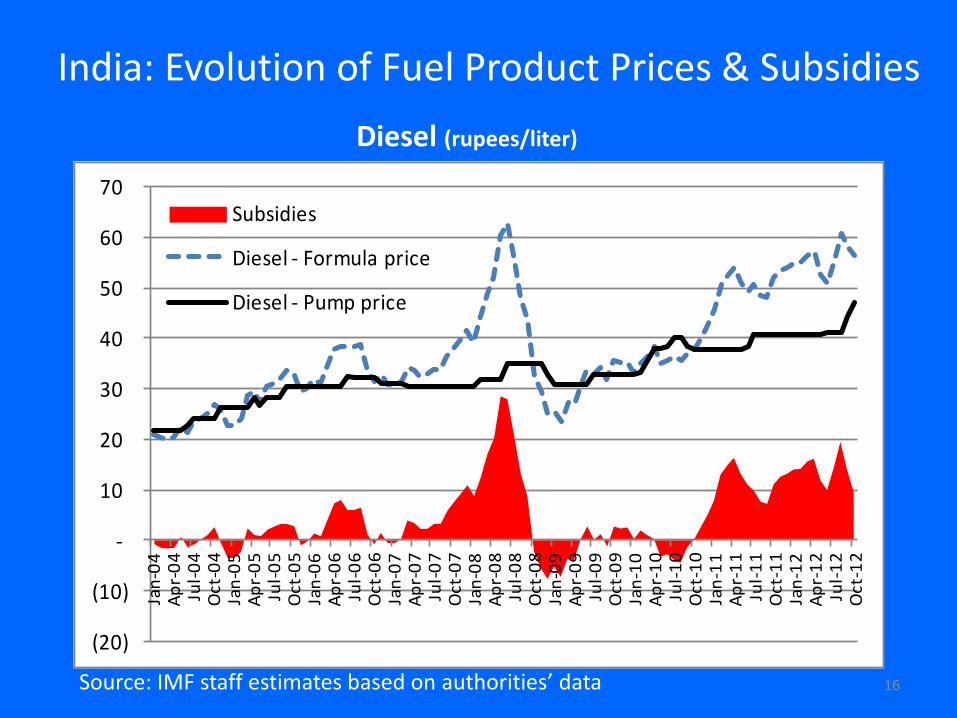

India: Evolution of Fuel Product Prices & Subsidies

16 Source: IMF staff estimates based on authorities’ data

Diesel (rupees/liter)

(20)

(10)

-

10

20

30

40

50

60

70

Jan

-04

Ap

r-0

4Ju

l-0

4O

ct-0

4Ja

n-0

5A

pr-

05

Jul-

05

Oct

-05

Jan

-06

Ap

r-0

6Ju

l-0

6O

ct-0

6Ja

n-0

7A

pr-

07

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8Ju

l-0

8O

ct-0

8Ja

n-0

9A

pr-

09

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0Ju

l-1

0O

ct-1

0Ja

n-1

1A

pr-

11

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2Ju

l-1

2O

ct-1

2

Subsidies

Diesel - Formula price

Diesel - Pump price

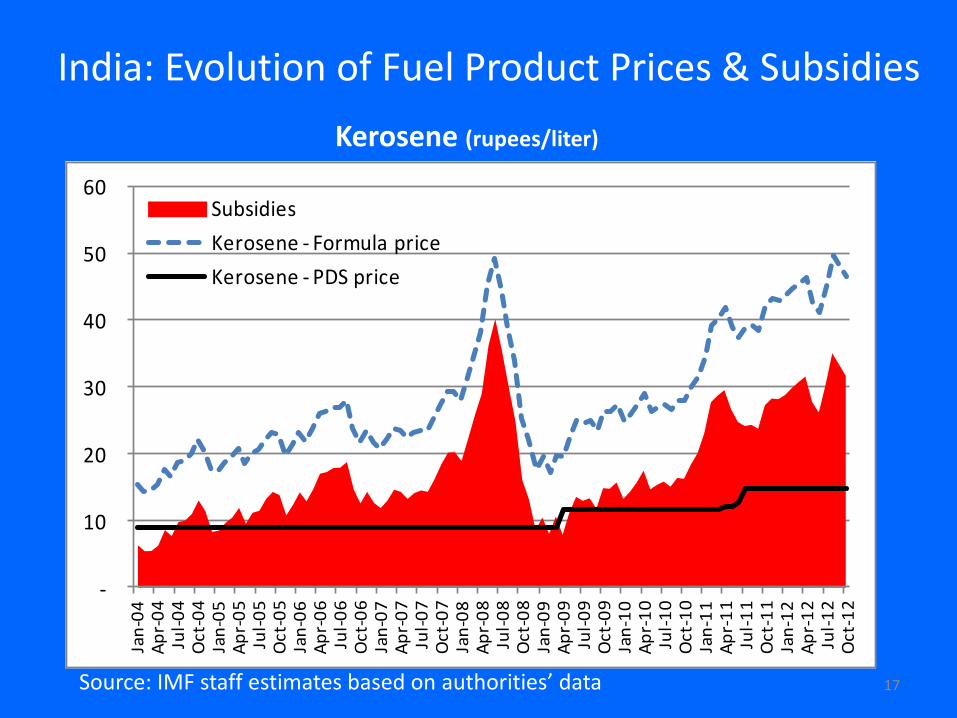

India: Evolution of Fuel Product Prices & Subsidies

17 Source: IMF staff estimates based on authorities’ data

Kerosene (rupees/liter)

-

10

20

30

40

50

60

Jan

-04

Ap

r-0

4Ju

l-0

4O

ct-0

4Ja

n-0

5A

pr-

05

Jul-

05

Oct

-05

Jan

-06

Ap

r-0

6Ju

l-0

6O

ct-0

6Ja

n-0

7A

pr-

07

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8Ju

l-0

8O

ct-0

8Ja

n-0

9A

pr-

09

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0Ju

l-1

0O

ct-1

0Ja

n-1

1A

pr-

11

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2Ju

l-1

2O

ct-1

2

Subsidies

Kerosene - Formula price

Kerosene - PDS price

India: Evolution of Fuel Product Prices & Subsidies

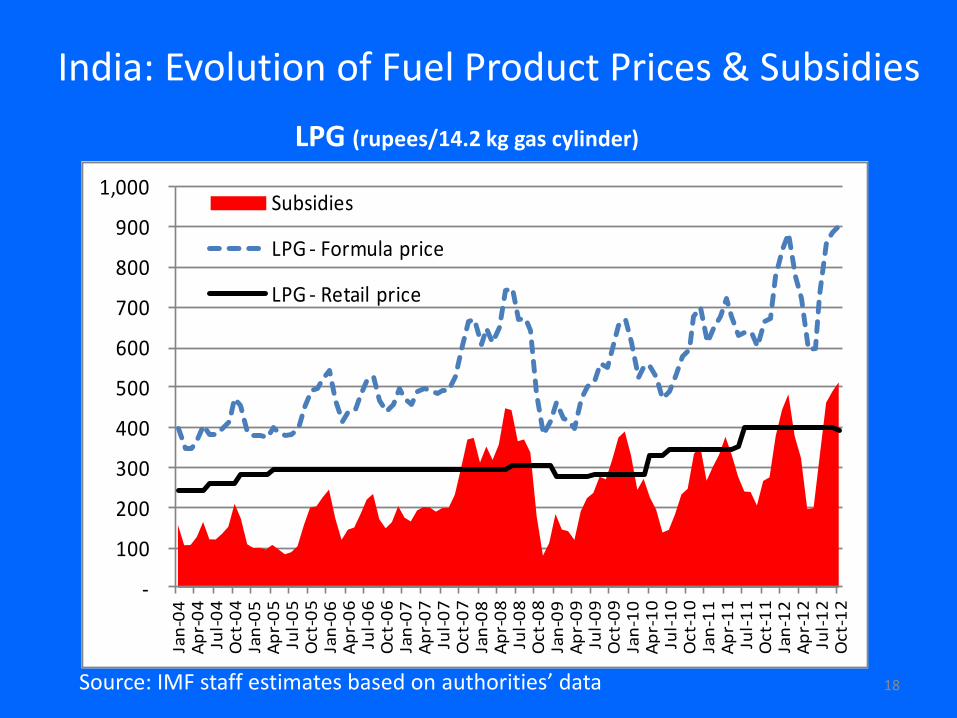

18 Source: IMF staff estimates based on authorities’ data

LPG (rupees/14.2 kg gas cylinder)

-

100

200

300

400

500

600

700

800

900

1,000 Ja

n-0

4A

pr-

04

Jul-

04

Oct

-04

Jan

-05

Ap

r-0

5Ju

l-0

5O

ct-0

5Ja

n-0

6A

pr-

06

Jul-

06

Oct

-06

Jan

-07

Ap

r-0

7Ju

l-0

7O

ct-0

7Ja

n-0

8A

pr-

08

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9Ju

l-0

9O

ct-0

9Ja

n-1

0A

pr-

10

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1Ju

l-1

1O

ct-1

1Ja

n-1

2A

pr-

12

Jul-

12

Oct

-12

Subsidies

LPG - Formula price

LPG - Retail price

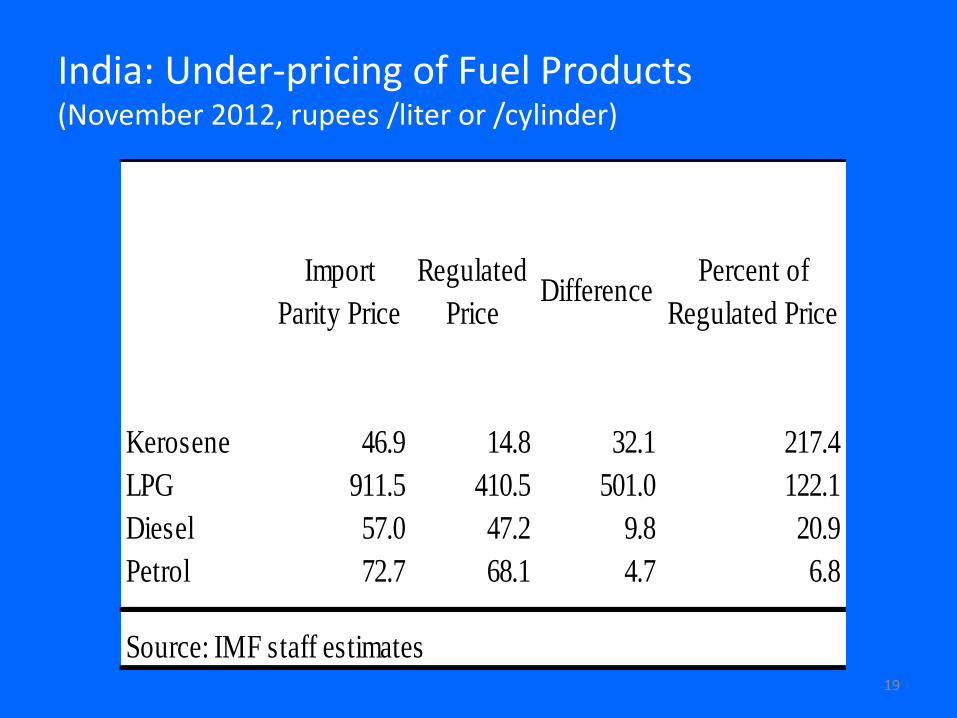

India: Under-pricing of Fuel Products (November 2012, rupees /liter or /cylinder)

19

Import

Parity Price

Regulated

PriceDifference

Percent of

Regulated Price

Kerosene 46.9 14.8 32.1 217.4

LPG 911.5 410.5 501.0 122.1

Diesel 57.0 47.2 9.8 20.9

Petrol 72.7 68.1 4.7 6.8

Source: IMF staff estimates

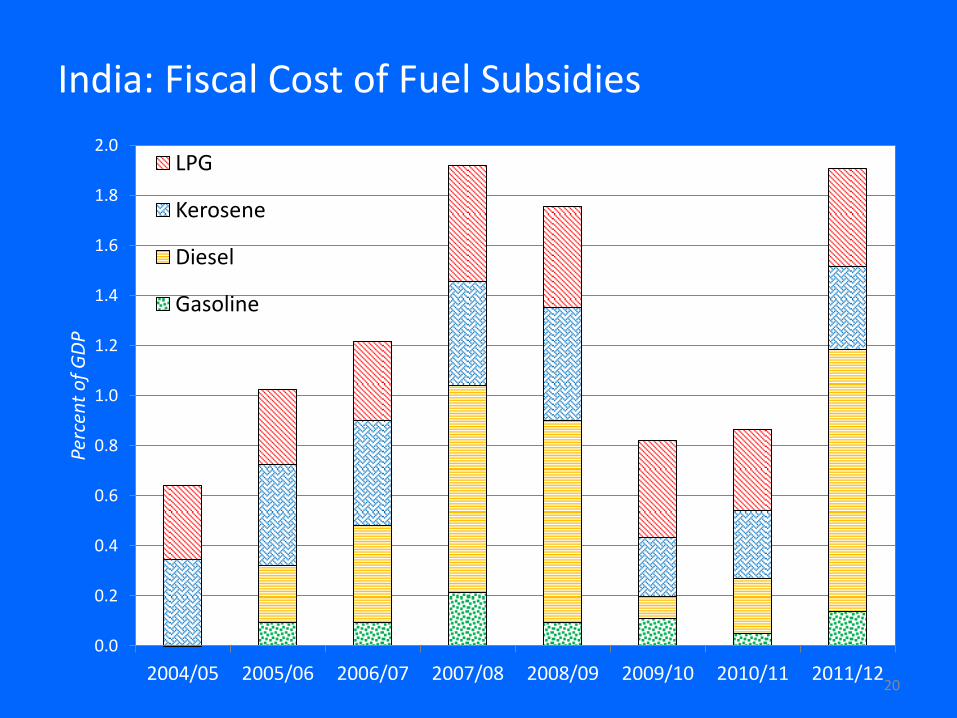

India: Fiscal Cost of Fuel Subsidies

20

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12

Perc

ent

of

GD

P

LPG

Kerosene

Diesel

Gasoline

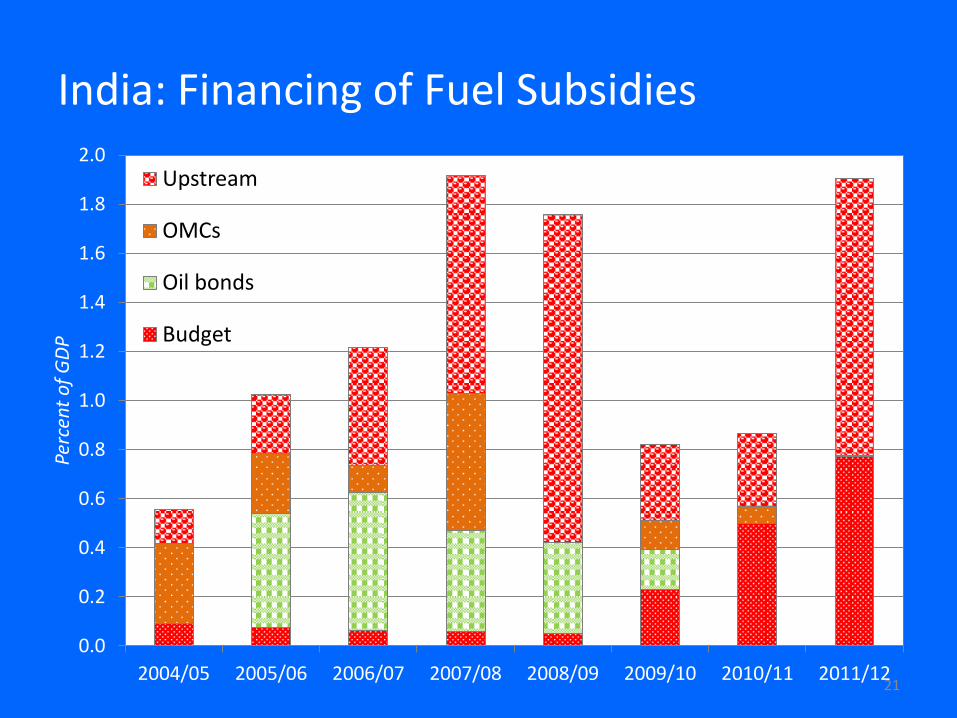

India: Financing of Fuel Subsidies

21

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12

Perc

ent

of

GD

P

Upstream

OMCs

Oil bonds

Budget

India: Who spends what on fuel?

22 Source: IMF staff estimates based on 2009-10 HH Socio-Economic Survey

Composition of HH Fuel Spending by Income Group, 2009-10 (Rupees per capita/month)

0

2

4

6

8

10

0

50

100

150

200

250

Dec

ile 1

Dec

ile 2

Dec

ile 3

Dec

ile 4

Dec

ile 5

Dec

ile 6

Dec

ile 7

Dec

ile 8

Dec

ile 9

Dec

ile 1

0

Kerosene

LPG

Petrol

Diesel

Share in total monthly expenditure (%, right scale)

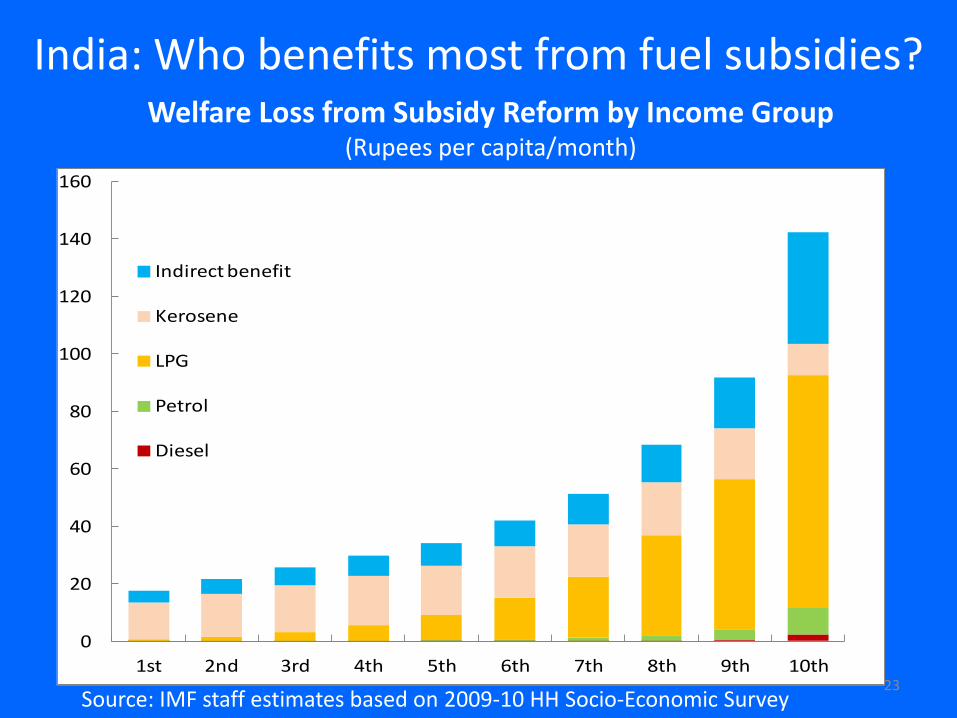

India: Who benefits most from fuel subsidies?

23 Source: IMF staff estimates based on 2009-10 HH Socio-Economic Survey

Welfare Loss from Subsidy Reform by Income Group (Rupees per capita/month)

0

20

40

60

80

100

120

140

160

1st 2nd 3rd 4th 5th 6th 7th 8th 9th 10th

Indirect benefit

Kerosene

LPG

Petrol

Diesel

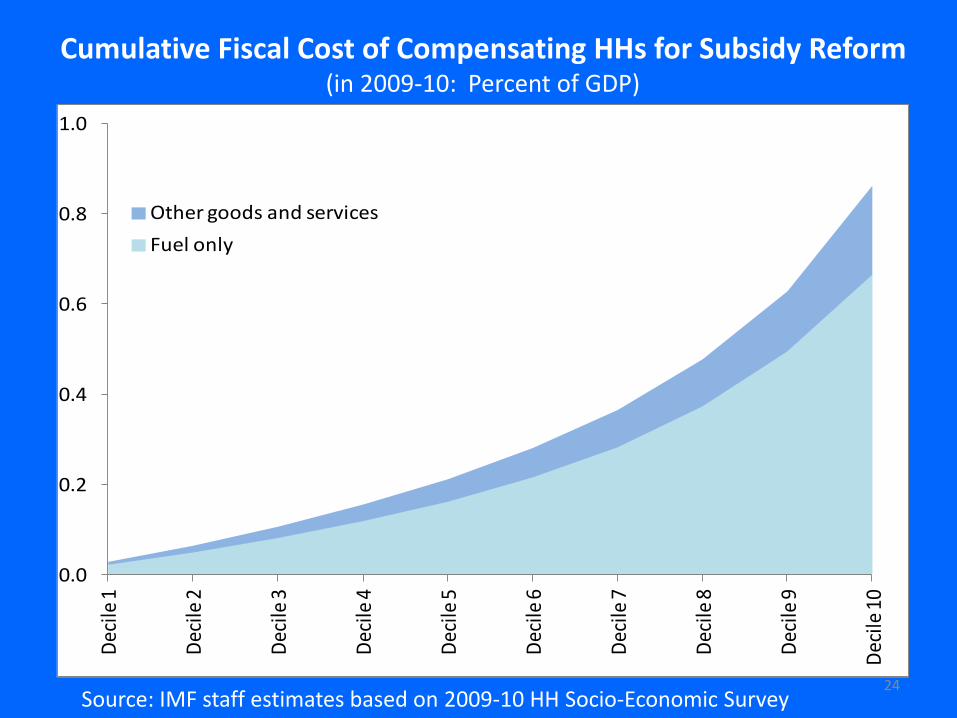

24 Source: IMF staff estimates based on 2009-10 HH Socio-Economic Survey

Cumulative Fiscal Cost of Compensating HHs for Subsidy Reform (in 2009-10: Percent of GDP)

0.0

0.2

0.4

0.6

0.8

1.0D

ecile

1

Dec

ile 2

Dec

ile 3

Dec

ile 4

Dec

ile 5

Dec

ile 6

Dec

ile 7

Dec

ile 8

Dec

ile 9

Dec

ile 1

0

Other goods and services

Fuel only

India: Progress is being made

• Kelkar Commission recommendations aligned with most of 6 key reform ingredients

• Petrol already mostly unsubsidized; diesel price increased significantly – monthly path

• LPG cylinders limited per household, pilot

• Roll out of Aadhaar-based direct cash transfers is in pilot phase, to be rolled out across India

• Kerosene subsidy seen as delicate – poverty impact could be significant

25

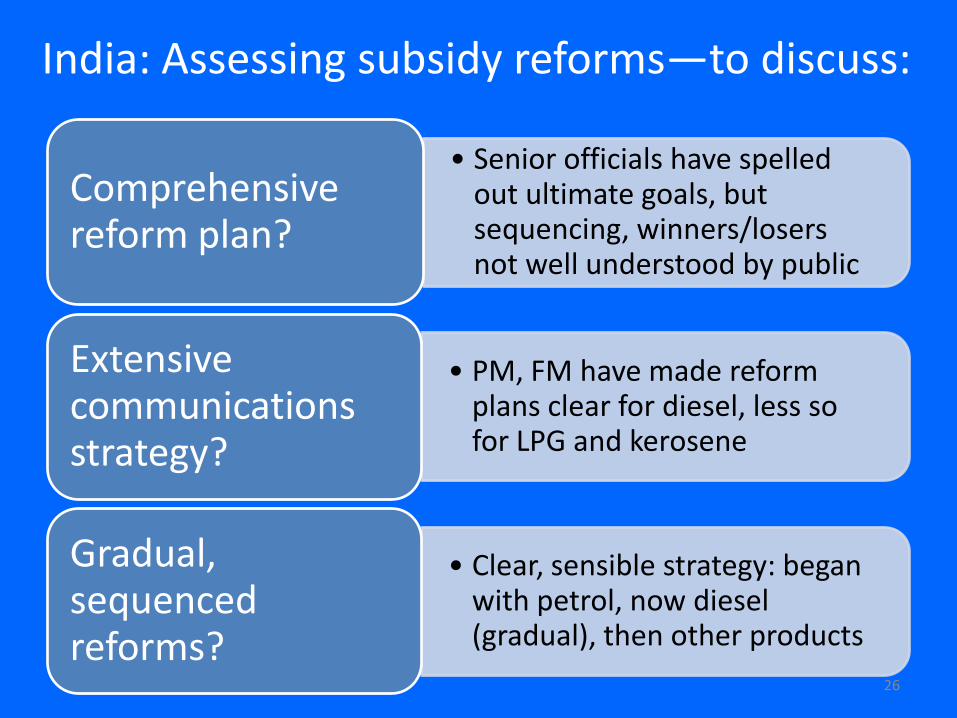

• Senior officials have spelled out ultimate goals, but sequencing, winners/losers not well understood by public

Comprehensive reform plan?

• PM, FM have made reform plans clear for diesel, less so for LPG and kerosene

Extensive communications strategy?

• Clear, sensible strategy: began with petrol, now diesel (gradual), then other products

Gradual, sequenced reforms?

26

India: Assessing subsidy reforms—to discuss:

• SEBs are raising power tariffs, but more work is needed

Improvements in SOE efficiency?

• Impressive effort to introduce direct cash transfers based on UID

Targeted social safety net?

• Mostly done at state level, so picture is mixed across India

Depoliticize price setting?

27

India: Assessing subsidy reforms—to discuss:

Thank you

“Both goals of expanding new investment and achieving energy efficiency require a more rational pricing policy, aligning India’s energy prices with global prices. This cannot be done immediately, but we need to outline a phased programme for such adjustment and then work to develop support for making the transition.”

Prime Minister's Address to the Nation

December 31, 2011 28

29

Want to know more? www.imf.org/subsidies: on energy subsidy reforms www.imf.org/asia: on our work in Asia Pacific www.imf.org/india: on IMF analysis of India

References & materials

IMF Fiscal Affairs Dept project, with IMF African and Middle East and Central Asian Depts

Includes case studies of 22 countries

Available at: www.imf.org/subsidies

30

Draft IMF working paper: “The Fiscal and Welfare Impacts of Reforming Fuel Subsidies in India,” by R. Anand, D. Coady, A. Mohommad, V. Thakoor, & J. P. Walsh

Comments welcome!