Employee Information Guide - Maxxiadoc.maxxia.com.au/Document/maxxia/MAXNBUEmployee... · Employee...

48

Employee Information Guide Salary Packaging – for Rio Tinto employees

Transcript of Employee Information Guide - Maxxiadoc.maxxia.com.au/Document/maxxia/MAXNBUEmployee... · Employee...

Employee Information Guide

Salary Packaging – for Rio Tinto employees

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 2 of 48

Contents Contents .............................................................................................................................................................. 2

1. Introduction ................................................................................................................................................ 4

2. Salary Packaging Options ......................................................................................................................... 5

2.1 What can you salary package? .......................................................................................................... 5

2.2 FBT Free Benefits ................................................................................................................................ 7

2.3 Concessionally Taxed Benefit Items ................................................................................................. 8

3. Taxation ..................................................................................................................................................... 10

3.1 Fringe Benefits Tax Exempt Items ................................................................................................... 10

3.2 Novated Motor Vehicle Leasing – FBT Method .............................................................................. 10

3.3 Novated Motor Vehicle Leasing – Employee Contribution Method (ECM) ................................ 11

3.4 Future Taxation .................................................................................................................................. 12

3.5 Payment Summary Reporting .......................................................................................................... 12

4. Administration .......................................................................................................................................... 13

4.1 Administration of Benefit Funds ...................................................................................................... 13

4.2 Terms and Conditions ....................................................................................................................... 13

4.3 Methods of Payment .......................................................................................................................... 14

4.4 Reconciliation .................................................................................................................................... 14

4.5 Changed Circumstances ................................................................................................................... 14

4.6 Leave ................................................................................................................................................... 14

4.7 Ceasing Packaging ............................................................................................................................ 15

4.8 Reports ............................................................................................................................................... 15

5. Administration Cost ................................................................................................................................. 16

6. Where To From Here? .............................................................................................................................. 17

7. Further Information .................................................................................................................................. 18

7.1 Access to Website ............................................................................................................................. 18

7.2 Privacy Policy ..................................................................................................................................... 18

7.3 Access to Your Personal Information.............................................................................................. 18

Appendix 1: ASSOCIATE MOTOR VEHICLE LEASE .................................................................................... 20 Appendix 2: NOVATED MOTOR VEHICLE LEASE ........................................................................................ 22 Appendix 3: REMOTE AREA HOUSING (EMPLOYER PROVIDED) ............................................................. 24 Appendix 4: REMOTE AREA RENTAL ASSISTANCE ................................................................................... 26 Appendix 5: REMOTE AREA REIMBURSEMENT OF INTEREST ................................................................. 28 Appendix 6: ....................................................................................................................................................... 30 REMOTE AREA REIMBURSEMENT ON PURCHASING OR BUILDING A PROPERTY ............................. 30 Appendix 7: REMOTE AREA – PROVISION OF GAS AND ELECTRICITY .................................................. 32 Appendix 8: REMOTE AREA – HOLIDAY TRAVEL ASSISTANCE ............................................................... 34 Appendix 9: IN HOUSE CHILDCARE EXPENSES ......................................................................................... 40 Appendix 10: IN HOUSE GYM ......................................................................................................................... 41 Appendix 11: AIRPORT LOUNGE MEMBERSHIP ......................................................................................... 42 Appendix 12: FINANCIAL COUNSELLING FEES .......................................................................................... 43 Appendix 13: ELIGIBLE WORK RELATED ITEM – TOOLS OF TRADE ....................................................... 44 Appendix 14: SELF FUNDED FLIGHTS - FLY IN FLY OUT (FIFO) ARRANGEMENTS ............................... 45 Appendix 15: FLY-IN FLY-OUT (FIFO) CAR PARKING ................................................................................. 46 Appendix 16: RELOCATION EXPENSES (DOMESTIC)…………………………………………………………..47

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 3 of 48

Disclaimer

This Employee Information Guide (the ‘Guide’) has been prepared without consideration of the particular

investment objectives, financial situation and needs of individual employees. In all cases, employees should

conduct their own investigation and analysis of the information contained in this Guide. No employee should

act on the basis of any matter contained in this Guide without taking appropriate legal, financial and other

professional advice regarding their own particular circumstances. Each employee who wishes to take

advantage of salary packaging is advised to seek independent financial advice particularly in relation to

complex motor vehicle fringe benefits tax and income tax issues.

Rio Tinto, Maxxia Pty Ltd (‘Maxxia’), each of their related bodies corporate, each of their employees, and

every person involved in the preparation of this Guide, expressly disclaim all liability for any loss or damage of

whatsoever kind (whether foreseeable or not) which may arise from any person acting or relying on any

statements contained in this Guide, or for any advice given by any salary consultant, and notwithstanding any

negligence, default or lack of due diligence and care.

The actions of your employer and Maxxia in relation to paying employment benefits from salary packages to a

third party does not in any way imply a transfer of responsibility or liability to the employer or Maxxia in relation

to any agreement, or understanding between the employee and that third party.

Maxxia provides administration and referral services on behalf of employers as an Authorised Representative

(No. 278683) of McMillan Shakespeare Ltd (AFSL No. 299054). It does not provide any form of financial,

taxation or financial product advice to employees on the relative merits of packaging programs or on any other

basis. Some information on taxation matters may be provided to illustrate possible advantages, but such

information is of a general nature only. You should seek your own independent professional advice on how

packaging programs may impact your particular financial, taxation and welfare benefit circumstances. Maxxia

may receive commissions or rebates in connection with some services it provides or arranges to be provided

by third parties. By appointing and utilising Maxxia’s services, you consent to its receipt of such commissions

and rebates. Tax laws regarding the treatment of salary benefits may change, which could adversely impact

your financial, taxation or welfare benefit decisions.

This disclaimer does not limit or alter those statutory rights that cannot be excluded.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 4 of 48

1. Introduction The purpose of this Guide is to provide an outline of the salary packaging arrangements that

employees who are eligible to participate may wish to take advantage of.

Salary packaging, also commonly referred to as salary sacrificing or total remuneration packaging, is

an arrangement between an employee and their employer, whereby the employee agrees to forgo

part of their future entitlement to salary or wages in return for the employer providing the employee

with benefits of a similar value.

Salary packaging provides a range of potential advantages to employees including:

the ability to allocate before tax dollars, not after tax dollars, towards eligible benefits, and

allocating salary and optional benefits to suit individual financial and personal situations.

The Income Tax Assessment Act 1936, the Income Tax Assessment Act 1997 and the Fringe

Benefits Tax Assessment Act 1986 together with your employer’s policy regulate and define the

type of benefits that can be included in a salary package, how the benefits are treated for taxation

purposes and the administrative arrangements that apply. This legislation or policy may change from

time to time. If changes do occur employees may be given the opportunity to adjust the structure of

their salary package to take account of any new requirements.

Fringe Benefits Tax (‘FBT’) was introduced in 1986 to tax the value of fringe benefits provided by an

employer to an employee or associate (related third party) in place of, or in addition to, the employee’s

salary or wages. FBT is payable by the employer on fringe benefits provided to employees.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 5 of 48

2. Salary Packaging Options In keeping with modern salary practices, employees will have the discretion to determine the mix of salary and benefits (within the approved list) that will

constitute their salary package.

Participation in salary packaging is voluntary.

2.1 What can you salary package?

The elements of the salary package are:

Salary;

Taxation;

Optional benefits; and

Administration fee(s).

All employees are eligible to salary package the following benefits:

Novated Lease (Car)

Financial Counselling Fees

Airport Lounge Memberships

Tools of Trade

Relocation Expenses (Domestic)

The following table on page 6 outlines additional benefits available by site.

At your discretion you may nominate an annual amount for each of these benefits, Fringe Benefits Tax and the Administration fee.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 6 of 48

All city based business unit em-ployees including corporate func-tions

Melbourne CBD Brisbane CBD Perth CBD Hunter Valley Opertions/Services Mount Thorley Warkworth

Self funded FIFO flights (contracted FIFO only) Airport car parking for FIFO (contracted FIFO only)

Aluminium Weipa Gove Yarwun

Remote area reimbursement of interest In house childcare (Weipa only) In house gymnasium fees (Weipa only) Remote area reimbursement of purchasing a prop-erty

Remote area housing (employer provided) Remote area rental assistance Remote area provision of gas and electricity (Gove only)

ERA Darwin Jabiru

Airport car parking for FIFO* Remote area reimbursement of interest (Jabiru on-ly)

Remote area housing (Jabiru only) Remote area provision of gas and electricity (Jabiru only) Self-funded FIFO flights*

Iron Ore Pilbara sites Remote area housing (employer provided) Remote area rental assistance Remote area reimbursement of interest

Remote area reimbursement of purchasing a property Self-funded FIFO flights* Airport car parking for FIFO*

Argyle Site/Kununurra Remote area housing Remote area provision of gas and electricity Remote area rental assistance Remote area reimbursement of interest

Remote area reimbursement of purchasing a property Remote area holiday travel assistance Self-funded FIFO flights* Airport car parking for FIFO*

Dampier Salt Non-Perth sites (Carnarvon, Dampier, Port Hedland)

Remote area housing Remote area provision of gas and electricity Remote area rental assistance Remote area reimbursement of interest

Remote area reimbursement of purchasing a property Self-funded FIFO flights* Airport car parking for FIFO*

* If employee is contracted to work FIFO

A detailed description of each of the benefits is provided in the Appendices to this Guide

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 7 of 48

2.2 FBT Free Benefits

AIRPORT LOUNGE MEMBERSHIP

An employee may salary package the cost of airport lounge membership.

Further information in relation to this benefit is provided in Appendix 11 or in the Rio Tinto Quick Ref-erence Card – Salary Packaging Airline Lounge Memberships

FINANCIAL COUNSELLING

An employee may salary package payments made for the provision of salary packaging advice from a

financial advisor or accountant.

Further information in relation to this benefit is provided in Appendix 12 or in the Rio Tinto Quick Ref-erence Card – Salary Packaging Airline Lounge Memberships

IN HOUSE CHILDCARE

An employee may salary package payments made in respect of childcare fees to Rio Tinto Alcan for

the provision of childcare at Cape Kids Childcare Centre.

Further information on this benefit is provided in Appendix 10. This benefit is ONLY available to em-ployees working at Weipa.

IN HOUSE GYMNASIUM

An employee may salary package payments made in respect of Gymnasium fees to Rio Tinto Alcan

at the onsite facility at the Weipa Fitness Centre.

Further information on this benefit is provided in Appendix 9. This benefit is ONLY available to em-ployees working at Weipa.

TOOL OF TRADE

An employee may salary package the cost of tools of trade. Tools of trade are those used by the

employee in the normal course of their employment and are eligible for an income tax deduction.

Further information on this benefit is provided in Appendix 13 or in the Rio Tinto Quick Reference Card – Salary Packaging Tools of Trade

REMOTE AREA HOUSING (EMPLOYER PROVIDED)

An employee may salary package rental payments to the employer for accommodation in nominated

remote area locations provided that the employee resides in accommodation leased or owned by the

Employer. The payments made in relation to this benefit are not subject to Fringe Benefits Tax (FBT).

Before undertaking remote area benefits, all Rio Tinto employees require an appointment with a local Customer Education Manager to assist them through the process. For details on how to contact your local representative, please click here.

Further information on this benefit is provided in Appendix 3 or in the Rio Tinto Quick Reference Guide – Salary Packaging Rent (company housing).

FLY IN FLY OUT (FIFO)

An employee may salary package payments the cost of airfares in relation to travel between their

usual place of employment and usual place of residence.

Further information on this benefit is provided in Appendix 14 or in the Rio Tinto Quick Reference Card – Salary Packaging Flights Policy (Australia)

FLY IN FLY OUT (FIFO) CAR PARKING

An employee may salary package the cost of parking their car at the airport when they are

undertaking travel under a fly-in fly-out arrangement .

Further information on this benefit is provided in Appendix 15 or in the Rio Tinto Quick Reference Card – Salary Packaging Airport Parking for FIFO Employees.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 8 of 48

RELOCATION EXPENSES (DOMESTIC)

An employee may salary package the cost of relocation expenses incurred in moving the employee and family members from one locality to another for employment purposes.

Before establishing relocation expenses, all Rio Tinto employees require an appointment with a local Customer Education Manager to assist them through the process. For details on how to contact your local representative, please click here.

Further information on this benefit is provided in Appendix 16 or in the Rio Tinto Quick Reference Guide – Salary Packaging Domestic Relocation Expenses

2.3 Concessionally Taxed Benefit Items

MOTOR VEHICLE LEASE

For some employees the inclusion of a motor vehicle in their salary package may be an attractive

option. This may be arranged through a novated vehicle lease.

The benefits of entering such an arrangement include:

Choice of vehicle, within employer guidelines

Tax-free running costs, and

Competitive finance rates.

Under a novated lease arrangement an employee leases a motor vehicle from a financier using the

standard finance lease. A Deed of Novation is then entered into between the employee, the employer

and the financier under which the employee’s obligation to pay the lease payments under the finance

lease is transferred to the employer for the term of the Deed of Novation.

If employment ceases with the employer then the employee is directly responsible for all

payments for the vehicle.

The novated lease arrangement is governed by both the fringe benefits tax and income tax legislation

and is also approved by the Australian Taxation Office.

In addition to the lease payments, all running costs (i.e. annual registration and comprehensive

insurance, fuel, servicing and repairs) in relation to the leased vehicle are also paid through the

employee’s salary package. A fuel card (three options to choose from) will also be made available

which provides the employee with a convenient way to purchase fuel.

Only the Deed of Novation approved by your employer and which is available from Maxxia may be

used.

Further information on the types of leasing available is provided in Appendices 1 and 2.

REMOTE AREA RENTAL ASSISTANCE

An employee may salary package rental payments in respect of non employer provided

accommodation in a remote area, provided the home is the employee’s usual place of residence, is in

a remote area, the employee is a current employee and the ATO requirements for a FBT concession

are met.

Further information on this benefit is provided in Appendix 4.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 9 of 48

REMOTE AREA REIMBURSEMENT OF INTEREST

An employee may salary package the interest payments accrued on a housing loan provided the

home is the employee’s usual place of residence, is in a remote area, the employee is a current

employee and the ATO requirements for a FBT concession are met.

Before undertaking remote area benefits, all Rio Tinto employees require an appointment with a local Customer Education Manager to assist them through the process. For details on how to contact your local representative, please click here. Further information on this benefit is provided in Appendix 5 or in the Rio Tinto Quick Reference Guide – Salary Packaging Remote Housing Purchase & Interest Costs

REMOTE AREA REIMBURSEMENT OF PURCHASING OR BUILDING A PROPERTY

An employee may salary package the costs incurred on the purchase of a property in a remote area,

or the purchase of land to build a home in a remote area provided the ATO requirements for a FBT

concession are met.

Further information on this benefit is provided in Appendix 6 or in the Rio Tinto Quick Reference Guide – Salary Packaging Remote Housing Purchase & Interest Costs

REMOTE AREA HOUSING PROVISION OF GAS AND ELECTRICITY

An employee may salary package the cost of gas or electricity provided that the employee resides

in accommodation leased or owned by the employer. The accommodation must be in a prescribed

remote area.

Before undertaking remote area benefits, all Rio Tinto employees require an appointment with a local Customer Education Manager to assist them through the process. For details on how to contact your local representative, please click here. Further information on this benefit is provided in Appendix 7.

REMOTE AREA HOLIDAY TRAVEL ASSISTANCE

An employee residing in a prescribed remote area may salary package certain expenses incurred in

relation to holiday travel (of more than 3 days annual or long service leave) from the remote area and

return for themselves, their partner and children.

Before undertaking remote area benefits, all Rio Tinto employees require an appointment with a local Customer Education Manager to assist them through the process. For details on how to contact your local representative, please click here. Further information on this benefit is provided in Appendix 8.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 10 of 48

3. Taxation The salary component of the salary package will continue to be subject to Pay As You Go (PAYG)

taxation

deductions in accordance with the Income Tax Assessment Act 1936 and the Income Tax

Assessment Act 1997.

Each benefit available under the employer’s salary packaging policy falls into one of the following two

(2)

FBT categories:

FBT exempt items; and

Concessionally taxed items.

Concessionally Taxed Benefit Items FBT Free Benefit Items

Novated Motor Vehicle Lease Financial Counselling Fees

Associate Motor Vehicle Lease In House Childcare (Weipa)

Remote Area – Provision of Gas & Electricity In House Gym (Weipa)

Remote Area Holiday Travel Assistance Remote Area Housing (Employer Provided)

Remote Area Rental Assistance*

Remote Area Reimbursement of Interest*

Remote Area Reimbursement of Purchasing

or Building a Property*

Self Funded Flights (FIFO)**

FIFO Airport Parking**

Relocation Expenses (Domestic)

Tools of Trade

Airport Lounge Membership

** If employee is contracted to work FIFO * Employees living and working in a remote area on a residential contract

3.1 Fringe Benefits Tax Exempt Items

Benefit items that are either specifically exempt or not subject to FBT because an employee could

usually claim a tax deduction for the expense as an “otherwise deductible item” does not incur FBT.

If “otherwise deductible” benefits are included in a salary package they cannot be claimed as a tax

deductible item in an income tax return.

3.2 Novated Motor Vehicle Leasing – FBT Method

Motor vehicles under a lease arrangement are concessionally taxed as a result of the calculation of their taxable value for the purpose of applying FBT. Assuming annual kilometres to be travelled by the vehicle, a percentage factor of 20% is applied to its cost price in order to calculate the taxable value. This is known as the “statutory formula method” of calculating “car fringe benefits tax”.

How the statutory formula method works

The taxable value of a motor vehicle provided to the employee by the employer is calculated by the

following formula:

Taxable value = [(A x B x C) / D – E] where:

A = the cost value of the car

B = Statutory rate of 20%

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 11 of 48

C = the number of days in the FBT year when the car was used or available for private

use of the employee

D = the number of days in the FBT year

E = the employee contribution (if any)

The FBT liability of a motor vehicle provided to the employee by the employer is calculated using the

following formula:

FBT = Taxable Value x Gross-up factor x FBT rate

For example, the FBT liability of a vehicle with a cost value of $25,000 would be $4,800, calculated as

follows:

Taxable Value = [($25,000 x 20% x 365) / 365] – $0 = $5,000

FBT = $5,000 x 2.0647 x 46.5% = $4,800

3.3 Novated Motor Vehicle Leasing – Employee Contribution Method (ECM)

The Employee Contribution Method (ECM) is a common method for salary packaging a motor vehicle

whereby the employee agrees to meet the running costs of the vehicle from a combination of pre and

post-tax salary, and/or an after-tax contribution to the employer in return for salary packaging the

vehicle. The combination of pre and post-tax salary is sent to Maxxia by the employer’s payroll

system. The result is a reduction in the taxable value of the vehicle when calculating fringe benefits

tax (FBT).

The preferred option is to contribute to the employer (as an after-tax payment) an amount equal to the

taxable value of the vehicle, the taxable value is reduced to nil, and hence the FBT is reduced to nil.

Example: For a motor vehicle of value $25,000:

Taxable value of vehicle = [(A x B x C) / D – E]

Taxable Value= [($25,000 x 20% x 365) / 365 – E]

Taxable Value= $5,000 – E

If E = $5,000, then the Taxable Value (TV) = $0

FBT= TV x 2.0647 x 46.5%

FBT= $0 x 2.0647 x 46.5% = $0

If the total running costs of the motor vehicle were $11,000 per annum, the employee using the ECM

would now pay $6,000 from pre-tax salary and $5,000 from after–tax salary. Where the employee

makes an after–tax contribution to the employer in respect of the novated lease, the employer will be

liable to Goods and Services Tax (GST). The GST is one-eleventh of the employee contribution.

In the example, the ECM is $5,000, and the GST payable will be $455. This GST amount is not

passed on to the employee, but is offset against the Input Tax Credits (ITCs) available to the

employer.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 12 of 48

3.4 Future Taxation

The employee must also meet the cost of any current or future taxes payable by Maxxia or the

Employer or the Employee under the Fringe Benefits Tax Assessment Act 1986, the Income

Assessment Act 1936 and Income Tax Assessment 1997, and A New Tax System (Goods and

Services Tax) Act 1999 and related legislation or similar Federal or State and Territory legislation.

3.5 Payment Summary Reporting

Employers are required to report the “grossed-up” value of fringe benefits on the employee’s

payment summary, where the total taxable value of the reportable benefits received in an FBT

year exceeds $2,000.

The grossed-up value is the sum of the value of the fringe benefit and FBT that would be payable on

the fringe benefit.

EXAMPLE: If the value of the benefit is $2,000 then the grossed-up value is calculated

as follows:

Value of Fringe Benefit = $2,000

Notional FBT ($2,000 x 0.8692) = $1,738

“Grossed-up” value ($2,000 + $1,738) = $3,738

Only fringe benefits that attract an FBT liability are reported on the payment summary. From 1 July

2009, additional superannuation contributions made under a salary sacrifice arrangement will be

included on an employee’s payment summary.

Fringe benefits included in a salary package for the FBT year (e.g. 1 April to 31 March of the next

calendar year) are reported on the payment summary for the financial year ending 30 June.

The grossed-up value of fringe benefits will be included for most government surcharges and income

tests including:

Child support obligations;

Higher Education Loan Program (HELP/HECS) repayment;

Medicare levy surcharge;

Personal superannuation contributions Rebate; and

Rebate for Spouse Superannuation Contributions.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 13 of 48

4. Administration The administration of salary packaging has been outsourced to Maxxia, a well-established provider of

salary packaging services throughout Australia.

The major functions to be performed by Maxxia in the administration of salary packaging are:

payment of the selected benefit item(s) in accordance with instructions provided by

the employee in the Salary Application Form

provision of reports to employees

undertaking full reconciliation of salary packages

obtaining and storing benefit payment substantiation for Australian Taxation Office

compliance and audit purposes

communicating directly with employees in relation to salary packaging, and

answering queries in relation to salary packaging.

The details concerning the administration of salary packaging are set out below and should be

carefully read prior to deciding to participate in salary packaging.

4.1 Administration of Benefit Funds

Upon commencement of salary packaging the following will be deducted on a pro-rata basis from the

employee’s salary:

the cost of the selected optional benefit(s)

any FBT applicable to these benefits, and

the administration cost.

The funds for the selected optional benefit(s) will be provided to Maxxia for disbursement.

Payments for benefit items will only be made where sufficient funds exist at the time the payment is

due or the employee submits a request for payment. Accordingly, when deciding to allocate money to

a particular benefit, employees may wish to provide an additional amount to meet any anticipated

increases in the cost of the payments.

4.2 Terms and Conditions

The following terms and conditions will apply:

benefit payments will only be made where Maxxia has received a salary package deduction

where insufficient package funds are available to cover a payment, no benefit payment will

be made

all benefit payments will cease immediately for those employees that terminate or are on leave

without pay where alternative arrangements have not been made

employees are only permitted to package benefits which form part of the employer’s approved

package menu, and

an employee may request for any unspent funds to be returned to the employee through the payroll

system when a change is made to the salary package.

These terms and conditions may be updated from time to time.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 14 of 48

4.3 Methods of Payment

REGULAR PAYMENTS

Benefit(s) that have a fixed instalment amount and occur on a regular basis (e.g. motor vehicle lease

payments) will be paid as a regular payment. The following details should be provided for these

payments:

name and address of where payments should be made

frequency of the payments

payment amount

commencement date for regular payments, and

BSB and account number for regular direct EFT and payments.

NON REGULAR PAYMENTS

These payments are for benefit(s) that do not have a fixed instalment amount, or do not occur on a

regular basis (e.g. motor vehicle registration). Payments will be made on receipt of a completed

Reimbursement Claim Form.

An employee who pays directly the cost of a benefit(s) will be reimbursed on receipt of a completed

Reimbursement Claim Form. Reimbursement will be by electronic funds transfer (EFT) to the

employee’s nominated bank or credit union account.

Non-regular payments and reimbursements will be made by Maxxia, subject to the employee having

sufficient package funds, within two business days of receiving an employee’s request. Please note

that the bank may take another few days to clear funds.

4.4 Reconciliation

A reconciliation of the salary package will occur when an employee alters their salary package.

Any balance remaining in an employee’s salary package on termination of employment will be paid as

salary and taxed accordingly.

Where Maxxia pays any expense that relates to the employee’s salary package, which is in excess of

the amount nominated, the employee will be required to repay such an expense.

4.5 Changed Circumstances

An employee may alter their salary package at no cost during the FBT year (i.e. 1 April to 31 March of

the next year).

4.6 Leave

An employee may be required to cease or suspend any salary packaging arrangements during any

period of leave. In most instances approval of any period of leave without pay will require the

employee to cease or suspend salary packaging.

The employee should notify Maxxia where an employee’s salary packaging arrangements will be

affected as a result of the approval of paid or unpaid leave. Where possible this notification should be

provided prior to the commencement of the leave period to enable the necessary administrative

arrangements to be made.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 15 of 48

4.7 Ceasing Packaging

An employee may elect at any time to cease salary packaging by giving at least twenty-eight (28)

days notice in writing to Maxxia.

In all circumstances where an employee’s salary packaging arrangements cease, it is necessary that

the employee notify Maxxia of their cessation date. This enables Maxxia to send final payments and

determine any action to be taken with account balances.

Any unspent funds will be returned to the employer who will arrange for these funds to be returned to

the employee via the payroll system. Note that these funds will be subject to PAYG taxation.

Any outstanding fees owing at the time of termination of an employee’s salary package arrangements

must be paid and will be deducted from the employee’s final termination payment (or as otherwise

agreed as per the Salary Packaging Agreement).

Any salary packaging arrangements will cease in the event that an employee is suspended without

pay or when employment is terminated.

4.8 Reports

Employees participating in salary packaging will receive quarterly reports in hard copy that provide

details on payments made for selected benefit items.

In addition the following online transaction reports are available:

Account Balance Report – shows the packaging account balance at the time of accessing the

report; and

Transactions in Last 90 days – lists the salary packaging contributions received and details of

payments made during the last 90 days.

The instructions for accessing online reports by the internet will be provided to the employee at the

commencement of salary packaging.

Employees can obtain an account balance by phone between the hours of 8.00am – 7.00pm

(EST/EDST) by calling Maxxia on 1300 123 123.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 16 of 48

5. Administration Cost Employees who choose to participate in salary packaging will be required to include within their salary

package the administration cost.

Administration Fee Description

Monthly Fee

(including

GST)

Salary packaging a Fully Maintained Novated lease or Associate Lease only $27.50

Salary packaging a combination of benefit items including a Motor Vehicle Lease. $42.41

Salary packaging a combination of benefit items excluding a Motor Vehicle Lease. $23.32

Employees wishing to salary package a motor vehicle under a novated lease must speak with a

Maxxia leasing consultant who will provide the employee with information and facts relevant to their

proposed lease.

During this consultation the employee will be required to complete a Novated Lease Checklist to

confirm their understanding of the information and facts provided.

Maxxia will forward a copy of the checklist to the employee together with their lease proposal.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 17 of 48

6. Where To From Here? If you wish to enquire about salary packaging a novated motor vehicle lease, call Maxxia My Car on 1300 123 123 or contact your local state office to arrange a consultation with a Customer Education Manager.

Maxxia’s Customer Education Managers travel the width and breadth of all states in Australia on a regular basis and are available for consultations when in your area. Alternatively, if access is difficult, our Customer Education Managers can arrange a person to person Webinex consultation where there is an available internet connection.

If you are considering packaging remote area benefits, or merely consult on your available benefits and wish to make an appointment with a Customer Education Manager at your local state office or when they are out on site, please see below:

WA State Office (WA/NT/SA) Phone: 08 9363 7000 Email: [email protected]

NSW Office (QLD/NSW/VIC) [email protected]

For simple salary packaging transactions (FIFO Parking/FIFO Flights/Tools of Trade/Airport Lounge Membership), please contact Maxxia’s Customer Care Centre on 1300 123 123 for assistance in the establishment of your package.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 18 of 48

7. Further Information A toll-free enquiry service has been established to provide information to employees in relation to

salary packaging. This service does not provide financial advice. However, the operators can assist

with general information regarding the salary packaging options that are available.

The enquiry service operates from 8.00 a.m. to 7.00 p.m. (EST/EDST) Monday to Friday.

Vehicle Lease Enquiries: 1300 123 123

General Enquiries: 1300 123 123

Website Address: maxxia.com.au

7.1 Access to Website

General information about salary packaging is available at maxxia.com.au

Specific employer policy information, Application Forms and Declarations are available by logging on

using your employer user id and password.

USER ID: RIOTINTO

PASSWORD: AUSTRALIA

All participating employees can also access their salary packaging reports online. The instructions

for accessing online reports using the internet will be provided when the employee commences

salary packaging.

7.2 Privacy Policy

Maxxia is bound by the National Privacy Principles contained in the Privacy Act 1988. Maxxia has

procedures in place to ensure the strict confidentiality of personal client information.

Maxxia’s Privacy Policy regulates the type of personal information we collect as well as the use of the

personal information. Your personal information is used by Maxxia to provide you with salary

packaging administration services, and in some cases to assist you in the acquisition of a motor

vehicle under a novated lease. Maxxia may also use this information to keep you informed of new

Maxxia products and services.

You can obtain a copy of the Maxxia’s Privacy Policy by contacting us. Alternatively you can obtain a

copy of the Privacy Policy from our website at maxxia.com.au

7.3 Access to Your Personal Information

Under the National Privacy Principles you are generally entitled to access the personal information

Maxxia holds about you. You can request access to your personal information by writing directly to

Maxxia at:

The Privacy Officer

Maxxia Pty Ltd

Locked Bag 18

Collins Street East

MELBOURNE VIC 8003

Or email Maxxia at [email protected]

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 19 of 48

Where you are entitled to obtain access to your personal information, the time we require to give you

access will depend on the type of information requested. In some circumstances we may charge you

a fee for providing access to your personal information. The fee will be based on our costs in locating

the information and the form of access you require. In all cases we will provide you with an estimate

of the fee so that you can confirm that you still require access to your personal information.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 20 of 48

Appendix 1: ASSOCIATE MOTOR VEHICLE LEASE

DESCRIPTION An associate lease involves the leasing of a vehicle owned or being purchased

by an associate of the employee (spouse, child over 18 year of age, family

member or family company). The associate leases the vehicle to the employer

who in turn provides it to the employee as part of their salary package.

What is allowable?

Direct lease payments.

Running costs (e.g. fuel, insurance, registration, servicing, maintenance and tyres).

Where capital improvements are made to the motor vehicle (e.g. sunroof, CD player) after the commencement of the lease, these items cannot be included in the salary package.

The cost of stamp duty and other costs related to the purchase of the motor vehicle can only be salary packaged as part of the lease cost, i.e. not as running costs.

Substantiation Copy of Associate Lease documentation.

Dealer’s invoice evidencing the purchase price of the motor vehicle if the vehicle is purchased at the commencement of the Associate Lease.

Independent valuation of the motor vehicle if the vehicle is already owned or being purchased by the “associate” prior to the commencement of the associate lease.

Original receipts must be submitted for reimbursement of running costs incurred by the employee where a fuel card is not used.

Original invoices must be submitted where an employee is seeking a direct payment for registration or insurance.

Taxation Issue Concessional FBT applies and is calculated by using the statutory formula method.

Goods and Services Tax does not apply to Motor Vehicle Registration, but does apply to the component relating to compulsory third party insurance.

Input Tax Credits are available.

The cost of a novated motor vehicle salary packaged are “grossed up” and may be included on the employee’s payment summary, as a fringe benefit.

Where the employee adopts the ECM and reduces the FBT on the motor vehicle to Nil, the benefit will not be included on the employee’s payment summary.

Maxxia will contact each employee with a motor vehicle lease in September and December of each year to obtain an interim motor vehicle odometer declaration.

The 2011-12 Federal Budget changes will see all leases, regardless of kilometres travelled, have a standard statutory percentage of 20% applied by 1 April 2014. Employees driving more than 25,000km will have a rate at the start of the lease, which will be revised each year until 1 April 2014 when a 20% standard rate is achieved. For these leases, Maxxia will contact the employees in writing if their annual kilometres are not on track.

The budget changes will not impact leases commenced prior to 10 May 2011 therefore Maxxia will continue to contact the employees in writing if their annual kilometres are not on track.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 21 of 48

Taxation Issue (continued)

Each employee will be required to lodge an end of FBT year odometer reading with Maxxia by 7 April of each year. Where the employee does not provide Maxxia with the odometer reading, Maxxia will calculate their FBT liability based on the highest statutory percentage.

The lodgement of the end of FBT year odometer reading is done via the Maxxia automated telephone odometer reading service and the Maxxia website.

Employee Declaration

Where the odometer reading declaration is not provided by the employee at the end of the FBT year, the FBT on the motor vehicle will be calculated using the highest statutory percentage (i.e.26% for pre – 10 May 2011 commitments and 20% for post – 10 May 2011), resulting in a higher than budgeted FBT liability.

A ‘Motor Vehicle-Fuel and Oil Expenses Declaration’ will be required where payments towards the running costs are being claimed to reduce the taxable value of the motor vehicle.

Repayment of any FBT incurred is the responsibility of the employee

Form of Payment

Lease payments – made directly to the associate.

Motor vehicle charge card – fuel and maintenance

Package Cost Lease payments, running costs plus any applicable FBT.

Additional Information

The associate party in an associate lease arrangement is strongly encouraged to take their own professional advice in relation to the financial, taxation and legal considerations for them in participating in the associate lease transaction.

Where input tax credits (i.e. a refund of GST) are available, a tax invoice must be submitted with the claim form.

If a complying tax invoice is not provided, input tax credits will not be processed by Maxxia.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 22 of 48

Appendix 2: NOVATED MOTOR VEHICLE LEASE

DESCRIPTION This is an arrangement whereby a motor vehicle is provided to an employee

by the employer through a novated lease, within the

employer’s guidelines.

You must use your employer’s Deed of Novation, which is available

from Maxxia.

What is Allowed? Direct Lease payments.

Running costs (fuel, insurance, registration, servicing and maintenance e.g. tyres).

Where capital improvements are made to the motor vehicle (e.g. sunroof, CD player) after the commencement of the lease, these items cannot be included in the salary package.

The cost of stamp duty and other costs related to the purchase of the motor vehicle can only be salary packaged as part of the lease cost, i.e. not as running costs.

Employee Contribution Method

The Employee Contribution Method (ECM) enables an employee to reduce the FBT of a novated motor vehicle to nil by making a post tax contribution to the operating costs of the vehicle.

The amount of employee’s contribution required must be equal to the taxable value of the motor vehicle.

Contributions made by an employee are subject to GST.

The GST on the employee contributions is calculated as 1/11th of the amount contributed by the employee.

Taxation Issues Goods and Services Tax does not apply to Motor Vehicle Registration, but does apply to the component relating to compulsory third party insurance.

The Type 1 gross-up factor of 2.0647 applies to a ‘Novated Motor Vehicle Lease’.

Input Tax Credits are available.

The cost of a novated motor vehicle salary packaged are “grossed up” and may be reported on the employee’s payment summary as a fringe benefit.

Where the employee adopts the ECM and reduces the FBT on the motor vehicle to Nil, the benefit will not be reported on the employee’s payment summary.

Maxxia will contact each employee with a motor vehicle lease in September and December of each year to obtain an interim motor vehicle odometer declaration.

The 2011-12 Federal Budget changes will see all leases, regardless of kilometres travelled, have a standard statutory percentage of 20% applied by 1 April 2014. Employees driving more than 25,000km will have a rate at the start of the lease, which will be revised each year until 1 April 2014 when a 20% standard rate is achieved. For these leases, Maxxia will contact the employees in writing if their annual kilometres are not on track.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 23 of 48

Taxation Issues (continued)

The budget changes will not impact leases commenced prior to 10 May 2011 therefore Maxxia will continue to contact the employees in writing if their annual kilometres are not on track. Each Employee will be required to lodge an end of FBT year odometer reading with Maxxia by 7 April of each year. Where the employee does not provide Maxxia with a completed declaration then Maxxia will calculate the FBT liability based on the highest statutory fraction.

The lodgement of the quarterly and end of FBT year odometer readings is done via the Maxxia automated telephone odometer reading service and the Maxxia website.

Leasing of Luxury Vehicles

When an employer novates a vehicle to an employee and the cost of the vehicle exceeds the luxury car tax limit of $57,466 (for accounting and taxation purposes), different taxation rules apply to the treatment of this vehicle from a company taxation perspective. In these circumstances the employer’s entitlement to claim an income tax deduction in respect of the luxury car lease is reduced. In order to compensate the employer for the partial loss of the tax deduction in respect of the luxury car lease, Maxxia calculates the loss of tax deduction (referred to be Maxxia as the Luxury Car Depreciation Allowance) and includes that amount in an employee’s novated lease proposal. The LCDA is retained by the employer to ensure that they are not disadvantaged from a taxation and financial aspect due to the employee entering into a novated luxury lease.

Substantiation Deed of Novation (signatory page and front page of lease, including the execution date, only required).

Copy of the finance schedule from the finance lease.

Dealer invoice for the purchase price of the motor vehicle.

Original invoices must be submitted where an employee is seeking a direct payment for registration or insurance.

At the end of each FBT year the employee is required to provide a declaration in relation to the opening and closing odometer readings for the number of kilometres travelled during the FBT year.

Employee Declaration

Where the odometer reading declaration is not provided by the employee at the end of the FBT year, the FBT on the motor vehicle will be calculated using the highest statutory percentage (i.e.26% for pre – 10 May 2011 commitments and 20% for post – 10 May 2011), resulting in a higher than budgeted FBT liability.

A ‘Motor Vehicle-Fuel and Oil Expenses Declaration’ will be required where payments towards the running costs are being claimed to reduce the taxable value of the motor vehicle.

Form of Payment Lease payments – made directly to financier.

Motor vehicle charge card – fuel and maintenance.

Additional Information

Where input tax credits (i.e. a refund of GST) are available, a tax invoice must be submitted with the claim form.

If a complying tax invoice is not provided, input tax credits will not be processed by Maxxia.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 24 of 48

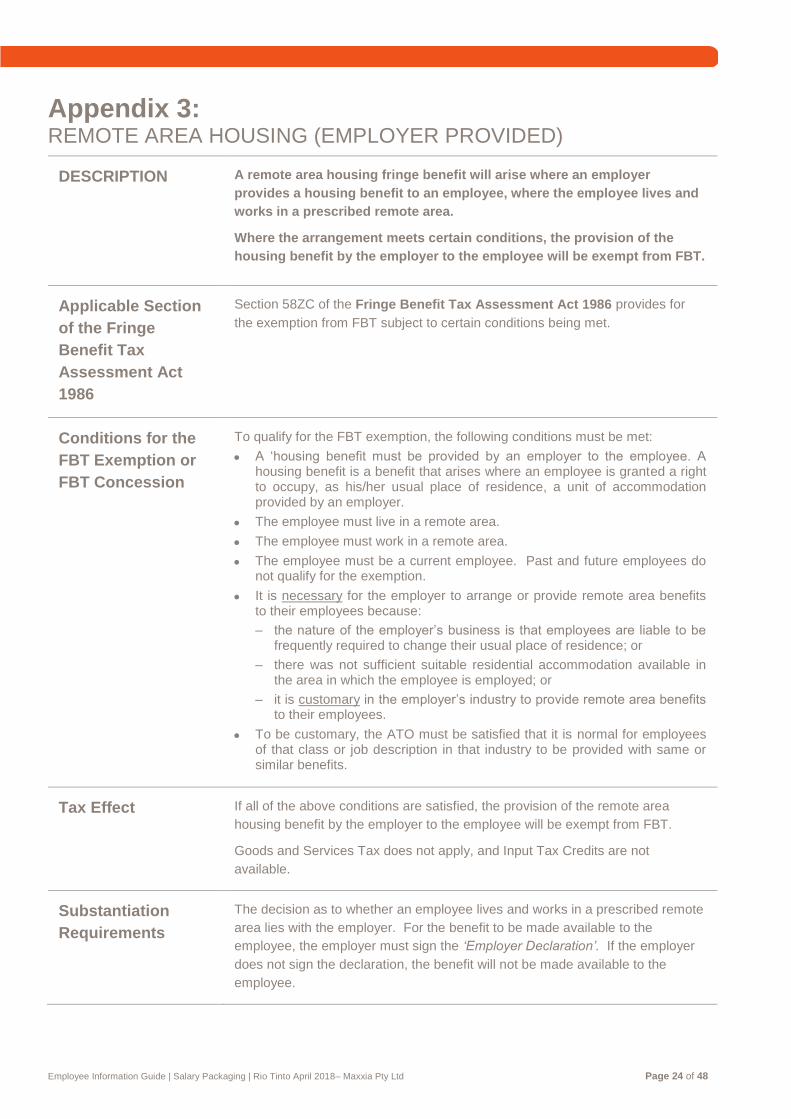

Appendix 3: REMOTE AREA HOUSING (EMPLOYER PROVIDED)

DESCRIPTION A remote area housing fringe benefit will arise where an employer

provides a housing benefit to an employee, where the employee lives and

works in a prescribed remote area.

Where the arrangement meets certain conditions, the provision of the

housing benefit by the employer to the employee will be exempt from FBT.

Applicable Section

of the Fringe

Benefit Tax

Assessment Act

1986

Section 58ZC of the Fringe Benefit Tax Assessment Act 1986 provides for

the exemption from FBT subject to certain conditions being met.

Conditions for the

FBT Exemption or

FBT Concession

To qualify for the FBT exemption, the following conditions must be met:

A ‘housing benefit must be provided by an employer to the employee. A housing benefit is a benefit that arises where an employee is granted a right to occupy, as his/her usual place of residence, a unit of accommodation provided by an employer.

The employee must live in a remote area.

The employee must work in a remote area.

The employee must be a current employee. Past and future employees do not qualify for the exemption.

It is necessary for the employer to arrange or provide remote area benefits to their employees because:

– the nature of the employer’s business is that employees are liable to be frequently required to change their usual place of residence; or

– there was not sufficient suitable residential accommodation available in the area in which the employee is employed; or

– it is customary in the employer’s industry to provide remote area benefits to their employees.

To be customary, the ATO must be satisfied that it is normal for employees of that class or job description in that industry to be provided with same or similar benefits.

Tax Effect If all of the above conditions are satisfied, the provision of the remote area

housing benefit by the employer to the employee will be exempt from FBT.

Goods and Services Tax does not apply, and Input Tax Credits are not

available.

Substantiation

Requirements

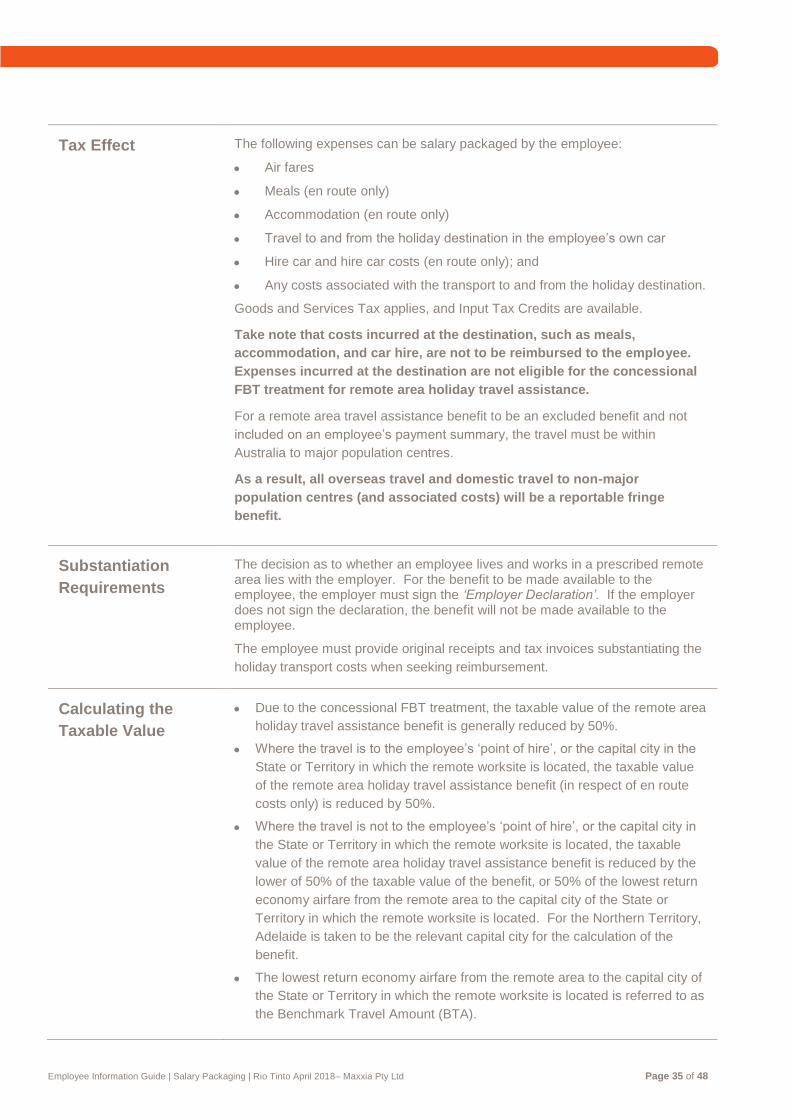

The decision as to whether an employee lives and works in a prescribed remote

area lies with the employer. For the benefit to be made available to the

employee, the employer must sign the ‘Employer Declaration’. If the employer

does not sign the declaration, the benefit will not be made available to the

employee.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 25 of 48

Calculating the

Taxable Value

Due to the exemption from FBT, the taxable value of this benefit is NIL.

Calculating the Cost

to the Employee’s

Package

The cost to the employee’s salary package will be the amount of rent paid by

the employee in respect of the housing benefit provided by the employer.

Calculating the Net

Benefit to the

Employee

Assumptions:

Annual salary $120,000

Rental payment $20,000

PAYG rates effective 1 July 2012. Input tax credits in relation to the Administration Fee are passed back to the employee.

Item No Packaging Packaging

Salary $120,000 $120,000

Rental payment $0 ($20,000)

FBT $0 $0

Average Administration

fee $0 ($280)

Input tax credits $0 $25

Net Salary $120,000 $99,745

Tax & Medicare ($34,147) ($26,349)

Net Salary $85,853 $73,396

Rental payment ($20,000) $0

Net Cash Salary $65,853 $73,396

Net Benefit n/a $7,543

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 26 of 48

Appendix 4: REMOTE AREA RENTAL ASSISTANCE

DESCRIPTION A remote area housing rental assistance fringe benefit will arise where the

employee lives and works in a prescribed remote area and enters into a

tenancy agreement with the owner of the property, or a real estate agent in

respect of a unit of accommodation.

The housing benefit (or unit of accommodation) is not provided by the

employer.

Where the arrangement meets certain conditions, the rental incurred by

the employee will be treated concessionally for FBT purposes.

The taxable value of the benefit is reduced by 50% of the amount paid by

the employee (that is, the recipient’s expenditure). This must not be

confused with the 50% reduction in the taxable value of other remote area

benefits.

Applicable Section

of the Fringe

Benefit Tax

Assessment Act

1986

Section 60(2A) of the Fringe Benefit Tax Assessment Act 1986 provides for

the concessional FBT treatment subject to certain conditions being met.

Conditions for the

FBT Exemption or

FBT Concession

To qualify for the FBT exemption, the following conditions must be met:

A ‘housing benefit must be provided by an employer to the employee. A housing benefit is a benefit that arises where an employee is granted a right to occupy, as his/her usual place of residence, a unit of accommodation provided by an employer.

The employee must live in a remote area.

The employee must work in a remote area.

The employee must be a current employee. Past and future employees do not qualify for the exemption.

It is necessary for the employer to arrange or provide remote area benefits to their employees because:

– the nature of the employer’s business is that employees are liable to be frequently required to change their usual place of residence; or

– there was not sufficient suitable residential accommodation available in the area in which the employee is employed; or

– it is customary in the employer’s industry to provide remote area benefits to their employees.

To be customary, the ATO must be satisfied that it is normal for employees of that class or job description in that industry to be provided with same or similar benefits.

Tax Effect If all of the above conditions are satisfied, the remote area housing rental assistance benefit will be treated concessionally for FBT purposes.

Goods and Services Tax does not apply, and Input Tax Credits are not

available.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 27 of 48

Substantiation

Requirements

The decision as to whether an employee lives and works in a prescribed remote

area lies with the employer. For the benefit to be made available to the

employee, the employer must sign the ‘Employer Declaration’. If the employer

does not sign the declaration, the benefit will not be made available to the

employee.

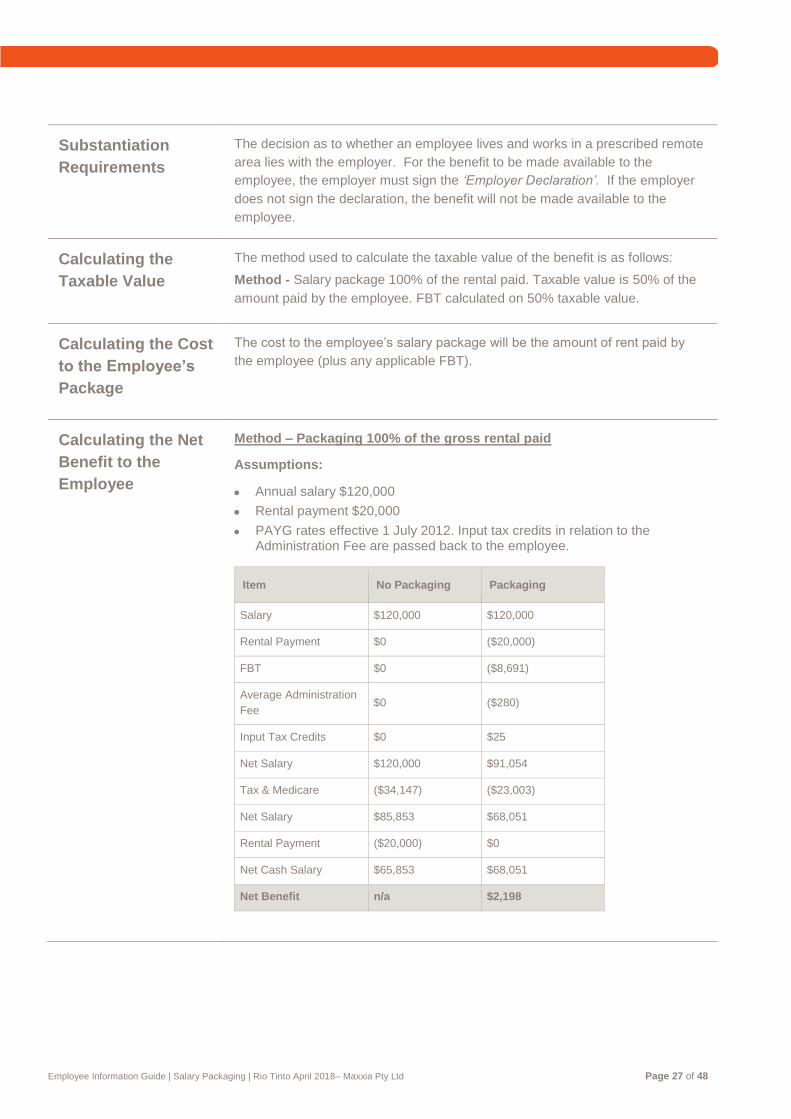

Calculating the

Taxable Value

The method used to calculate the taxable value of the benefit is as follows:

Method - Salary package 100% of the rental paid. Taxable value is 50% of the

amount paid by the employee. FBT calculated on 50% taxable value.

Calculating the Cost

to the Employee’s

Package

The cost to the employee’s salary package will be the amount of rent paid by

the employee (plus any applicable FBT).

Calculating the Net

Benefit to the

Employee

Method – Packaging 100% of the gross rental paid

Assumptions:

Annual salary $120,000

Rental payment $20,000

PAYG rates effective 1 July 2012. Input tax credits in relation to the Administration Fee are passed back to the employee.

Item No Packaging Packaging

Salary $120,000 $120,000

Rental Payment $0 ($20,000)

FBT $0 ($8,691)

Average Administration

Fee $0 ($280)

Input Tax Credits $0 $25

Net Salary $120,000 $91,054

Tax & Medicare ($34,147) ($23,003)

Net Salary $85,853 $68,051

Rental Payment ($20,000) $0

Net Cash Salary $65,853 $68,051

Net Benefit n/a $2,198

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 28 of 48

Appendix 5: REMOTE AREA REIMBURSEMENT OF INTEREST

DESCRIPTION A remote area reimbursement of interest benefit will arise where an

employee enters into a loan arrangement for the purpose of purchasing a

dwelling located in a remote that is to be used as the employee’s usual

place of residence.

Where there is a draw down facility on the mortgage account which is

accessed by the employee, the funds must be used solely for the

construction of an extension to the remote area dwelling. If the funds are

used for any other purpose, the FBT concession for this benefit is no

longer available.

Where the arrangement meets certain conditions, the interest on the loan

incurred by the employee will be treated concessionally for FBT purposes.

A 50% reduction in the taxable value of the reimbursement of interest benefit will apply.

Applicable Section

of the Fringe

Benefit Tax

Assessment Act

1986

Section 60(2) of the Fringe Benefit Tax Assessment Act 1986 provides for the

concessional FBT treatment subject to certain conditions being met.

Conditions for the

FBT Exemption or

FBT Concession

To qualify for the FBT exemption, the following conditions must be met:

A ‘housing benefit must be provided by an employer to the employee. A housing benefit is a benefit that arises where an employee is granted a right to occupy, as his/her usual place of residence, a unit of accommodation provided by an employer.

The employee must live in a remote area.

The employee must work in a remote area.

The employee must be a current employee. Past and future employees do not qualify for the exemption.

It is necessary for the employer to arrange or provide remote area benefits to their employees because:

– the nature of the employer’s business is that employees are liable to be frequently required to change their usual place of residence; or

– there was not sufficient suitable residential accommodation available in the area in which the employee is employed; or

– it is customary in the employer’s industry to provide remote area benefits to their employees.

To be customary, the ATO must be satisfied that it is normal for employees of that class or job description in that industry to be provided with same or similar benefits.

Tax Effect If all of the above conditions are satisfied, the remote area reimbursement of interest benefit will be treated concessionally for FBT purposes.

Goods and Services Tax does not apply, and Input Tax Credits are not available.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 29 of 48

Substantiation

Requirements

The decision as to whether an employee lives and works in a prescribed remote area lies with the employer. For the benefit to be made available to the employee, the employer must sign the ‘Employer Declaration’. If the employer does not sign the declaration, the benefit will not be made available to the employee.

Calculating the

Taxable Value

Due to the concessional FBT treatment, the taxable value of the reimbursement of interest benefit is reduced by 50% of the cost of the interest per annum plus the applicable FBT.

Calculating the Cost

to the Employee’s

Package

The cost to the employee’s salary package will be the amount of interest paid by

the employee in respect of the housing loan benefit plus the applicable FBT.

Calculating the Net

Benefit to the

Employee

Assumptions:

Annual salary $120,000

Interest reimbursed $20,000

PAYG rates effective 1 July 2012. Input tax credits in relation to the Administration Fee are passed back to the employee.

Item No Packaging Packaging

Salary $120,000 $120,000

Interest Payment $0 ($20,000)

FBT $0 ($8,691)

Average Administration

Fee $0 ($280)

Input Tax Credits $0 $25

Net Salary $120,000 $91,054

Tax & Medicare ($34,147) ($23,003)

Net Salary $85,853 $68,051

Interest Payment ($20,000) $0

Net Cash Salary $65,853 $68,051

Net Benefit n/a $2,198

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 30 of 48

Appendix 6:

REMOTE AREA REIMBURSEMENT ON PURCHASING OR BUILDING A PROPERTY

DESCRIPTION A remote area reimbursement on purchasing of building a property benefit

will arise where the employee incurs costs in connection with the

purchasing a property in a remote area, the purchase of land to build a

home in a remote area, or the loan deposit and principal.

Where the arrangement meets certain conditions, the costs incurred by

the employee will be treated concessionally for FBT purposes.

A 50% reduction in the taxable value of the reimbursement on purchasing

or building a property benefit will apply.

Applicable Section

of the Fringe

Benefit Tax

Assessment Act

1986

Section 60(4) of the Fringe Benefit Tax Assessment Act 1986 provides for the

concessional FBT treatment subject to certain conditions being met.

Conditions for the

FBT Exemption or

FBT Concession

To qualify for the FBT exemption, the following conditions must be met:

A ‘housing benefit must be provided by an employer to the employee. A housing benefit is a benefit that arises where an employee is granted a right to occupy, as his/her usual place of residence, a unit of accommodation provided by an employer.

The employee must live in a remote area.

The employee must work in a remote area.

The employee must be a current employee. Past and future employees do not qualify for the exemption.

It is necessary for the employer to arrange or provide remote area benefits to their employees because:

– the nature of the employer’s business is that employees are liable to be frequently required to change their usual place of residence; or

– there was not sufficient suitable residential accommodation available in the area in which the employee is employed; or

– it is customary in the employer’s industry to provide remote area benefits to their employees.

To be customary, the ATO must be satisfied that it is normal for employees of that class or job description in that industry to be provided with same or similar benefits.

Tax Effect If all of the above conditions are satisfied, the remote area reimbursement of purchasing or building a property benefit will be treated concessionally for FBT purposes.

Goods and Services Tax does not apply, and Input Tax Credits are not available.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 31 of 48

Substantiation

Requirements

The decision as to whether an employee lives and works in a prescribed remote area lies with the employer. For the benefit to be made available to the employee, the employer must sign the ‘Employer Declaration’. If the employer does not sign the declaration, the benefit will not be made available to the employee.

The employee must provide a ‘Copy of Offer and Acceptance’ and ‘Settlement Statement’ showing the purchase date and the expenses incurred.

The employee must also provide statements and invoices substantiating other

costs such as stamp duty.

Calculating the

Taxable Value

Due to the concessional FBT treatment, the taxable value of the reimbursement

of purchasing or building a property benefit is reduced by 50%.

Calculating the Cost

to the Employee’s

Package

The cost to the employee’s salary package will be the amount of the

reimbursement received by the employee in respect of the purchasing or

building a property benefit plus the applicable FBT.

Calculating the Net

Benefit to the

Employee

Assumptions:

Annual salary $120,000

Building or purchasing costs reimbursed $20,000

PAYG rates effective 1 July 2012. Input tax credits in relation to the Administration Fee are passed back to the employee.

Item No Packaging Packaging

Salary $120,000 $120,000

Purchasing or Building

Expenses $0 ($20,000)

FBT $0 ($8,691)

Average Administration

Fee $0 ($280)

Input Tax Credits $0 $25

Net Salary $120,000 $91,054

Tax & Medicare ($34,147) ($23,003)

Net Salary $85,853 $68,051

Purchasing or Building

Expenses ($20,000) $0

Net Cash Salary $65,853 $68,051

Net Benefit n/a $2,198

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 32 of 48

Appendix 7: REMOTE AREA – PROVISION OF GAS AND ELECTRICITY

DESCRIPTION A remote area residential fuel benefit will arise where the employee incurs

costs in connection with residential fuel to be used in connection with

their usual place of residence in a remote area.

Residential fuel is defined to mean any form of fuel (including electricity)

for use for domestic purposes.

Where the arrangement meets certain conditions, the costs incurred by

the employee will be treated concessionally for FBT purposes.

A 50% reduction in the taxable value of the remote area residential fuel

benefit will apply.

Applicable Section

of the Fringe

Benefit Tax

Assessment Act

1986

Section 59 of the Fringe Benefit Tax Assessment Act 1986 provides for the

concessional FBT treatment subject to certain conditions being met.

Conditions for the

FBT Exemption or

FBT Concession

To qualify for the FBT concession, the following conditions must be met:

The benefit is an expense payment fringe benefit, a property fringe benefit, or a residual fringe benefit in respect of remote area residential fuel.

The employee must be in receipt of a remote area housing benefit, a housing loan benefit, or a housing rent benefit.

Tax Effect If all of the above conditions are satisfied, the remote area residential fuel benefit will be treated concessionally for FBT purposes.

Goods and Services Tax applies, and Input Tax Credits are available.

Substantiation

Requirements

The decision as to whether an employee lives and works in a prescribed remote area lies with the employer. For the benefit to be made available to the employee, the employer must sign the ‘Employer Declaration’. If the employer does not sign the declaration, the benefit will not be made available to the employee.

The employee must provide original receipts and tax invoices substantiating the

residential fuel costs when seeking reimbursement.

Calculating the

Taxable Value

Due to the concessional FBT treatment, the taxable value of the remote area

residential fuel benefit is reduced by 50%.

Calculating the Cost

to the Employee’s

Package

The cost to the employee’s salary package will be the amount of the

reimbursement received by the employee in respect of the residential fuel

benefit plus the applicable FBT.

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 33 of 48

Calculating the Net

Benefit to the

Employee

Assumptions:

Annual salary $120,000

Residential fuel expense $5,000

PAYG rates effective 1 July 2012. Input tax credits in relation to the Administration Fee are passed back to the employee.

Item No Packaging Packaging

Salary $120,000 $120,000

Residential Fuel $0 ($5,000)

FBT $0 ($2,400)

Average Administration

Fee $0 ($280)

Input Tax Credits $0 $480

Net Salary $120,000 $112,800

Tax & Medicare ($34,147) ($31,375)

Net Salary $85,853 $81,425

Residential Fuel ($5,000) $0

Net Cash Salary $80,853 $81,425

Net Benefit n/a $572

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 34 of 48

Appendix 8: REMOTE AREA – HOLIDAY TRAVEL ASSISTANCE

DESCRIPTION A remote area holiday travel assistance benefit will arise where the

employee incurs costs in connection with holiday travel (of more than 3

days annual or long service leave) from the remote area and return.

The benefit includes the cost of the holiday travel for the employee, their

partner and child/children.

Where the arrangement meets certain conditions, the costs incurred by

the employee will be treated concessionally for FBT purposes.

The taxable value of the remote area holiday travel assistance benefit will

depend on the destination of the travel undertaken by the employee..

Applicable Section

of the Fringe

Benefit Tax

Assessment Act

1986

Sections 60A and 61 of the Fringe Benefit Tax Assessment Act 1986

provides for the concessional FBT treatment subject to certain conditions being met.

The concessional FBT treatment is dependent upon the employee’s ‘point of hire’ (as listed in their employment agreement) and the travel destination.

Conditions for the

FBT Exemption or

FBT Concession

To qualify for the FBT concession, the following conditions must be met:

The benefit is an expense payment fringe benefit, a property fringe benefit, or a residual fringe benefit in respect of transport, or accommodation, or meals en route.

The employee, apart from temporary absences, performs their duties of employment in a remote area.

The transport must be between the remote area employment location and

the relevant capital city in that state or territory, or

another place.

Transport provided to the employee must be during a period of recreation leave.

Spouse or Child Resides With the Employee

The transport must be between a place at or near the remote area employment location and another place (i.e. the holiday destination)

Spouse or Child Does Not Reside With the Employee

The transport must be between the place where they meet the employee and another place (i.e. the holiday destination)

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 35 of 48

Tax Effect The following expenses can be salary packaged by the employee:

Air fares

Meals (en route only)

Accommodation (en route only)

Travel to and from the holiday destination in the employee’s own car

Hire car and hire car costs (en route only); and

Any costs associated with the transport to and from the holiday destination.

Goods and Services Tax applies, and Input Tax Credits are available.

Take note that costs incurred at the destination, such as meals,

accommodation, and car hire, are not to be reimbursed to the employee.

Expenses incurred at the destination are not eligible for the concessional

FBT treatment for remote area holiday travel assistance.

For a remote area travel assistance benefit to be an excluded benefit and not

included on an employee’s payment summary, the travel must be within

Australia to major population centres.

As a result, all overseas travel and domestic travel to non-major

population centres (and associated costs) will be a reportable fringe

benefit.

Substantiation

Requirements

The decision as to whether an employee lives and works in a prescribed remote area lies with the employer. For the benefit to be made available to the employee, the employer must sign the ‘Employer Declaration’. If the employer does not sign the declaration, the benefit will not be made available to the employee.

The employee must provide original receipts and tax invoices substantiating the

holiday transport costs when seeking reimbursement.

Calculating the

Taxable Value

Due to the concessional FBT treatment, the taxable value of the remote area

holiday travel assistance benefit is generally reduced by 50%.

Where the travel is to the employee’s ‘point of hire’, or the capital city in the

State or Territory in which the remote worksite is located, the taxable value

of the remote area holiday travel assistance benefit (in respect of en route

costs only) is reduced by 50%.

Where the travel is not to the employee’s ‘point of hire’, or the capital city in

the State or Territory in which the remote worksite is located, the taxable

value of the remote area holiday travel assistance benefit is reduced by the

lower of 50% of the taxable value of the benefit, or 50% of the lowest return

economy airfare from the remote area to the capital city of the State or

Territory in which the remote worksite is located. For the Northern Territory,

Adelaide is taken to be the relevant capital city for the calculation of the

benefit.

The lowest return economy airfare from the remote area to the capital city of

the State or Territory in which the remote worksite is located is referred to as

the Benchmark Travel Amount (BTA).

Employee Information Guide | Salary Packaging | Rio Tinto April 2018– Maxxia Pty Ltd Page 36 of 48

When the remote area is the same as the point of hire, the taxable value of

the benefit is reduced by 50%.

The reduction of the taxable value of the benefit in each of the above

scenarios cannot exceed 50%.

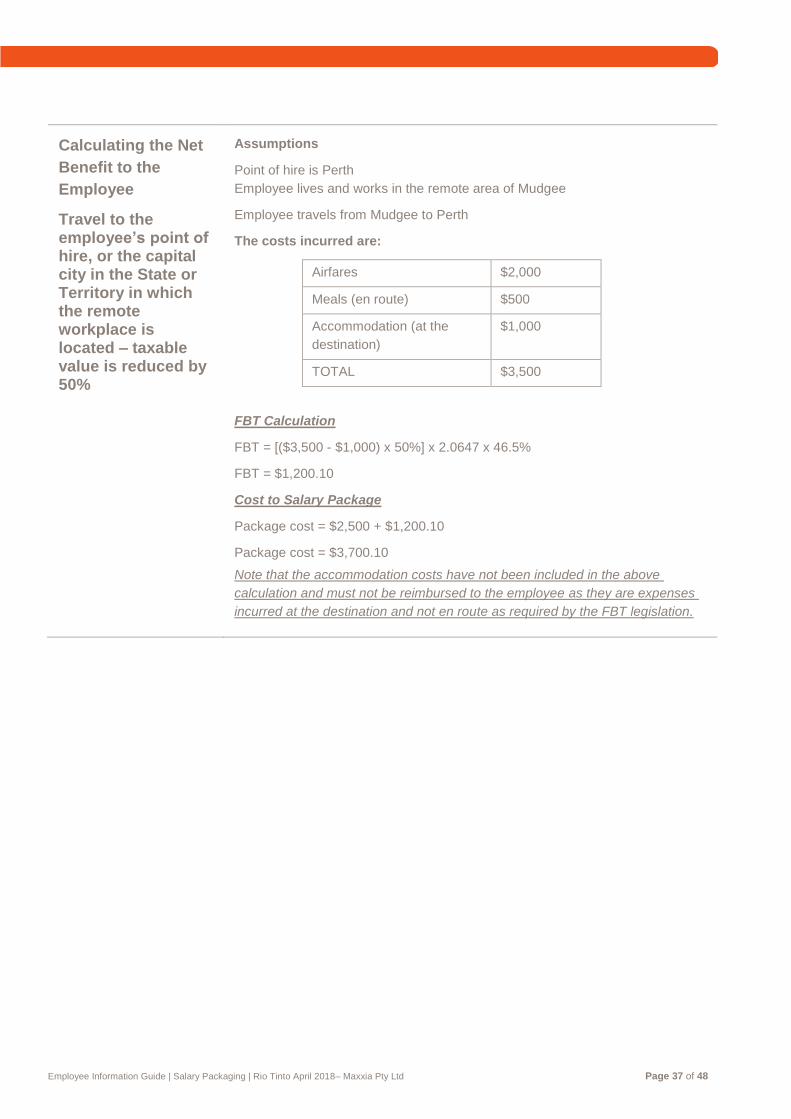

Calculating the Cost

to the Employee’s

Package

The cost to the employee’s salary package will be the amount of the

reimbursement received by the employee in respect of the remote area holiday

travel assistance benefit plus the applicable FBT.

The estimated amount of FBT will be calculated at the time of establishing the

employee’s salary package and deducted from the employee’s pre-tax salary in

addition to the cost of the benefit.