ECOWORLD INTERNATIONALecoworldinternational.com/wp-content/themes/ecoworld-international/... · •...

22

ECOWORLD INTERNATIONAL Q2 FY2018 RESULTS & BRIEFING

Transcript of ECOWORLD INTERNATIONALecoworldinternational.com/wp-content/themes/ecoworld-international/... · •...

ECOWORLD INTERNATIONALQ2 FY2018 RESULTS & BRIEFING

FINANCIAL UPDATES

PROFIT & LOSS STATEMENTAS AT 30 APRIL 2018

HANDOVER IN LONDON CITY ISLAND & EMBASSY GARDENS WILL ENABLE PROFIT RECOGNITION IN H2 2018

RM’0001ST QUARTER ENDED

31 JAN 2018

2ND QUARTER ENDED

30 APR 2018

PERIOD ENDED

30 APR 2018

Revenue 18 0 18

Direct Expenses (1,668) (846) (2,514)

Gross Loss (1,650) (846) (2,496)

Other Operating Income 6,939 2,932 9,871

Selling & Marketing Expenses (3,099) (3,119) (6,218)

Administrative Expenses (17,192) (17,034) (34,226)

Unrealised gain/(loss) on foreign exchange 4,878 (6,883) (2,005)

Finance Costs - (98) (98)

Share of Results of Joint Ventures (8,631) (4,935) (13,566)

Loss before Taxation (18,755) (29,983) (48,738)

Taxation 2,337 1,108 3,445

Net Profit (16,418) (28,875) (45,293)

Basic Loss per Share (Sen) (0.7) (1.2) (1.9)

BALANCE SHEETAS AT 30 APRIL 2018

• Raised RM180 million via IMTN

Programme in Apr 2018

• Minimal equity contribution needed for

projects jointly-developed with Ballymore

after handovers in LCI and EG commence

in H2 2018

• Lower cash level year to date mainly due

to equity contribution for working capital

needs of existing projects and acquisition

of Stage 1 sites from Willmott Dixon

RM’000

PERIOD ENDED

30 APR 2018 31 OCT 2017

No. of Ordinary Shares 2,400,000 2,400,000

Share Capital 2,592,451 2,592,451

Shareholders’ Funds 2,425,144 2,544,876

NA per Share (RM) 1.01 1.06

Total Cash 460,840 992,388

Total Borrowings 253,510 128,597

Net Cash / (Debt) 207,330 863,791

Gross Debt – Equity Ratio (x) 0.10 0.05

Net Debt – Equity Ratio (x) (0.08 ) (0.35)

PROJECT UPDATES

PROJECT UPDATEEXISTING LONDON PROJECTS

LONDON CITY ISLAND WARDIAN EMBASSY GARDENS

• BLOCK A&M:

❑ 90% complete as at Apr 2018

❑ Target to commence handover in July

2018

• BLOCK B,C,D,E,F:

❑ Block B&C 61% complete and Block

D&E 54% complete as at Apr 2018

❑ Target handover in H2 2019

EAST & WEST TOWERS

❑ 45% complete as at Apr 2018

❑ Target handover in H2 2020

BLOCK A04:

❑ 91% complete as at Apr 2018

❑ Target to commence handover in Sept 2018

BLOCK A05:

❑ 54% complete as at Apr 2018

❑ Target handover in mid-2019

BLOCK A03:

❑ Yet to be launched

PROJECT UPDATEAUSTRALIAN PROJECTS

• Construction commenced in June 2018

• Target handover in H2 2020

• Basement levels being constructed

• Target handover in mid-2020

YARRA ONE, MELBOURNEWEST VILLAGE, SYDNEY

ECOWORLD LONDONREBRANDED FROM BE LIVING IN JUNE 2018

• EcoWorld International acquired DMco, six Stage 1 sites on 16 Mar 2018 + one stage 2 site on 30 May 2018

• This increased the number of active projects in London from 3 to 7. New sites are 1) Millbrook Park, 2) Kensal Rise & Maida Hill 3) Aberfeldy Village, and 4) Nantly House

• Be Living rebranded as EcoWorld London on 7 June 2018

THE MALAYSIAN-THEMED REBRANDING EVENT TOOK PLACE AT THE INSTITUTE OF DIRECTORS, PALL MALL

ACTIVE PROJECTS – ARTIST’S IMPRESSIONS

KENSAL RISE (M&J PHASE 1) MILLBROOK PARK PHASE 1

ABERFELDY VILLAGE NANTLY HOUSE

ECOWORLD LONDON

ACTIVE PROJECTMILLBROOK PARK PHASE 1

PROJECT OVERVIEW

• 92 townhouses and apartment units

• Average price* of c. £720 psf (upper

mainstream market)

• GDV: £45 million

• Target delivery: 2019

VALUE PROPOSITION

• 5-minute walk to Mill Hill East Station

• 20 minutes to Euston Station from Mill Hill

East Station (via Northern line)

• One of the few development schemes in

Millbrook Park that offers lifestyle

amenities such as gym, games room,

concierge and resident lounge

• Eligible for Help-to-buy

*Average price of private units

ACTIVE PROJECTKENSAL RISE (M&J PHASE 1)

PROJECT OVERVIEW

• 71 townhouses and apartment units

• Average price* of c. £800 psf (upper

mainstream market)

• GDV: £53 million

• Target delivery: 2018

VALUE PROPOSITION

• 7-minute walk to Kensal Rise Station

• 28 minutes to Charing Cross Station from

Kensal Rise Station (via Bakerloo)

• Position on Chamberlayne Road, a great

area for cafes, restaurants and boutiques.

Chamberlayne Road was named as the

“hippest street in Europe” by Vogue

*Average price of private units

ACTIVE PROJECTABERFELDY VILLAGE PHASE 3A

PROJECT OVERVIEW

• 50:50 joint venture with Poplar HARCA, a

housing association

• 121 apartment units

• Average price* of c. £610 psf (mid-

mainstream market)

• GDV: £47 million

• Target delivery: 2019

VALUE PROPOSITION

• 6-minute walk to East India DLR Station

• 12 minutes to Bank Station from East

India DLR Station (via DLR)

*Average price of private units

ACTIVE PROJECTNANTLY HOUSE

PROJECT OVERVIEW

• 50:50 joint venture project with Lampton

360 (London Borough of Hounslow)

• 75 apartment units

• GDV: £24 million

• Target delivery: 2019

VALUE PROPOSITION

• Sold affordable housing comprising 31

units to Octavia Housing, a housing

association

• Potential for en bloc sale of the remaining

OMS and BTR units

• 2-min walk to Hounslow Central Station

• 37 mins to Green Park St from Hounslow

Central St (via Piccadilly line)

UPCOMING PROJECTBARKING WHARF

PROJECT OVERVIEW

• 597 apartment units in Zone 4

• Net internal area (NIA): c. 360,000 sq ft

VALUE PROPOSITION

• 10-minute walk to Barking tube station, 30

minutes train ride to Liverpool St station

(via Hammersmith and City line)

• Situated immediately across an expansive

park (Barking Abbey Park)

• Designed for Build-to-Rent (BTR)

UPCOMING PROJECTKEW BRIDGE

PROJECT OVERVIEW

• 10 blocks of residential developments

surrounding a new football stadium for

Brentford FC in Zone 3

• Construction of football stadium by EW

London in exchange for development land

• GDV: c. £550 million

• Potential for 4 blocks of BTR component

with NIA of c. 310,000 sq ft

VALUE PROPOSITION

• <10-minute walk to Kew Bridge Station,

30 minutes train ride to Waterloo Station

(via South Western Rail)

• Close proximity to large offices such as

Dell, Worley Parsons, GSK & SkyTV

• Well served by road networks and public

transport links.

• Opportunity for cross-selling to tenants of

BTR units

MARKET UPDATE

UK PROPERTY MARKETENCOURAGING SIGNS

UNIT SALES OF RESIDENTIAL DEVELOPMENT SCHEME IN LONDON

TAKE-UP OF OFFICE SPACE IN CENTRAL LONDON

Source: Savills, Molior

SALES OF PRIVATE RESIDENTIAL UNITS IN LONDON IN Q1 2018 JUMPED 22% YEAR-ON-YEAR WHILE TAKE-UP FOR OFFICE SPACE IN CENTRAL LONDON ROSE 20% IN THE SAME PERIOD

-

5,000

10,000

15,000

20,000

25,000

30,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 Q12018

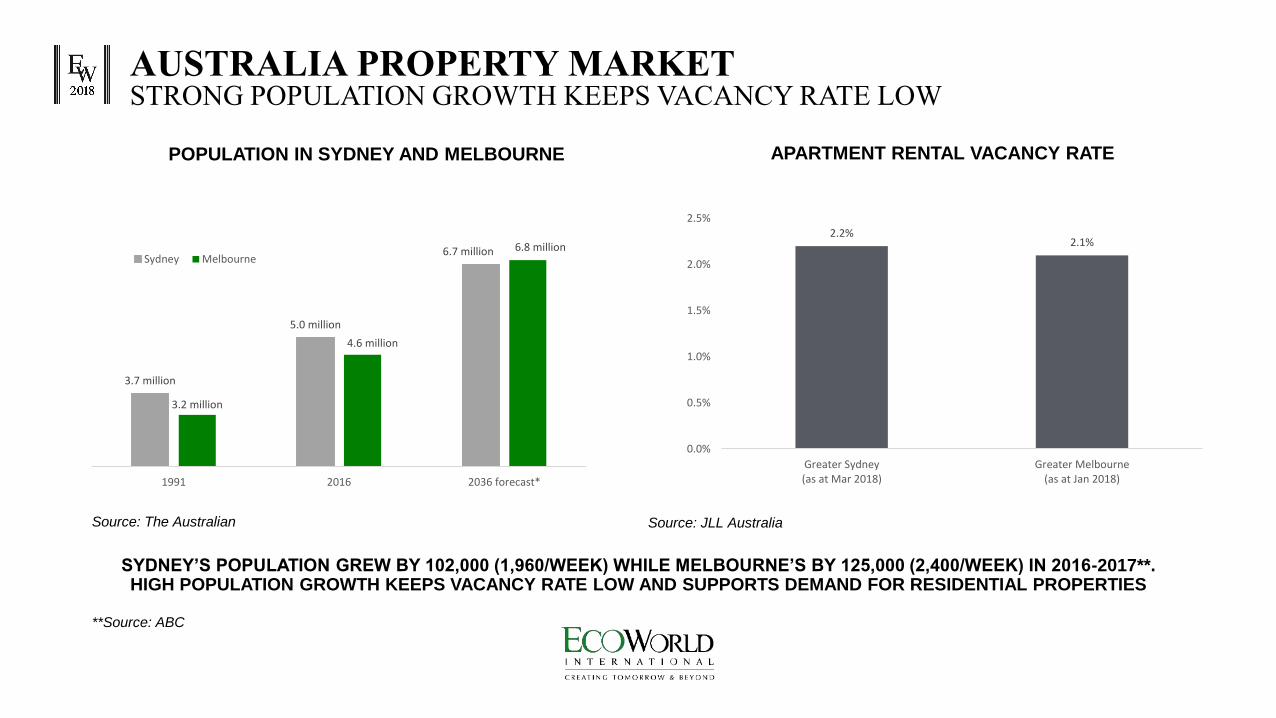

AUSTRALIA PROPERTY MARKETSTRONG POPULATION GROWTH KEEPS VACANCY RATE LOW

POPULATION IN SYDNEY AND MELBOURNE

Source: The Australian

2.2%2.1%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Greater Sydney(as at Mar 2018)

Greater Melbourne(as at Jan 2018)

APARTMENT RENTAL VACANCY RATE

Source: JLL Australia

SYDNEY’S POPULATION GREW BY 102,000 (1,960/WEEK) WHILE MELBOURNE’S BY 125,000 (2,400/WEEK) IN 2016-2017**. HIGH POPULATION GROWTH KEEPS VACANCY RATE LOW AND SUPPORTS DEMAND FOR RESIDENTIAL PROPERTIES

3.7 million

5.0 million

6.7 million

3.2 million

4.6 million

6.8 million

1991 2016 2036 forecast*

Sydney Melbourne

**Source: ABC

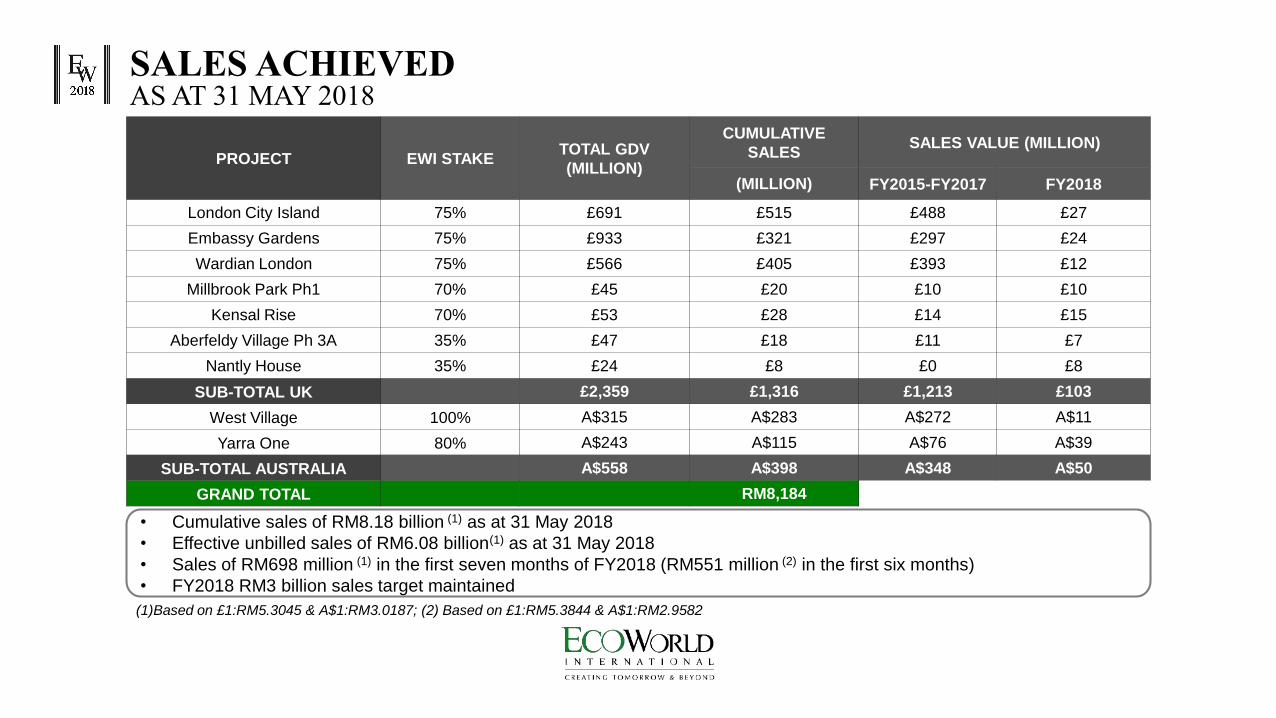

SALES ACHIEVEDAS AT 31 MAY 2018

PROJECT EWI STAKETOTAL GDV

(MILLION)

CUMULATIVE

SALESSALES VALUE (MILLION)

(MILLION) FY2015-FY2017 FY2018

London City Island 75% £691 £515 £488 £27

Embassy Gardens 75% £933 £321 £297 £24

Wardian London 75% £566 £405 £393 £12

Millbrook Park Ph1 70% £45 £20 £10 £10

Kensal Rise 70% £53 £28 £14 £15

Aberfeldy Village Ph 3A 35% £47 £18 £11 £7

Nantly House 35% £24 £8 £0 £8

SUB-TOTAL UK £2,359 £1,316 £1,213 £103

West Village 100% A$315 A$283 A$272 A$11

Yarra One 80% A$243 A$115 A$76 A$39

SUB-TOTAL AUSTRALIA A$558 A$398 A$348 A$50

GRAND TOTAL RM8,184

• Cumulative sales of RM8.18 billion (1) as at 31 May 2018

• Effective unbilled sales of RM6.08 billion(1) as at 31 May 2018

• Sales of RM698 million (1) in the first seven months of FY2018 (RM551 million (2) in the first six months)

• FY2018 RM3 billion sales target maintained

(1)Based on £1:RM5.3045 & A$1:RM3.0187; (2) Based on £1:RM5.3844 & A$1:RM2.9582

TARGET DELIVERYSUSTAINING EARNINGS VISIBILITY BEYOND 2021

2018 2019 2020 2021 POST - 2021

TARGET HANDOVER TIMELINE

A & M

A04

East &

West Tower

B, C, D, E, F

A05 A03

EcoWorld London

*Subject to change due to potential revision in development plan

EW LONDON PROJECTS

AND MACQUARIE PARK TO

SUSTAIN EARNINGS

BEYOND 2021

Phase 1 Phase 2*

Phase 1 Phase 2*

Phase 3A

Nantly House

CONCLUSIONECOWORLD INTERNATIONAL

➢ BUSINESS OUTLOOK

• London City Island and Embassy Gardens are on track to commence handovers in H2 FY2018

• Remaining units to be marketed to owner-occupiers, capitalising on the high occupancy in first

phases of LCI and EG

• EcoWorld London projects are being brought forward to accelerate sales and earnings recognition

• Target to close 1-2 BTR sales by end-FY2018

➢ FINANCIALS

• Profit recognition in H2 FY2018 on the back of 1st handovers

• Funding needs for development to be met by recycling of handover proceeds and bank borrowings

LAND BANK & PROJECT DETAILSECOWORLD INTERNATIONAL - AS AT 31 MAY 2018

OWNERSHIPLAND SIZE

( ACRES)GDV (MILLION) CUMULATIVE SALES (MILLION)

EFFECTIVE UNBILLED SALES

(MILLION)

United Kingdom

London City Island 75% 6.0 £691 £515 £383

Embassy Gardens 75% 5.4 £933 £321 £226

Wardian London 75% 1.4 £566 £405 £300

Millbrook Park Ph1 70% 2.7 £45* £20 £8

Kensal Rise & Maida Hill (M&J) 70% 1.9 £53* £28 £17

Aberfeldy Village 35% 7.0 £47* £18 £4

Nantly House 35% 1.1 £24 £8 £3

Barking Wharf 70% 3.9

Yet to launchedBarking site 70% 1.1

Woking 70% 3.4

TOTAL UK 33.8 £2,359 £1,316 £941

Australia

West Village 100% 1.2 A$315 A$283 A$281

Yarra One 80% 0.5 A$243 A$115 A$79

TOTAL AUSTRALIA 1.7 A$558 A$398 A$360

*GDV of M&J Ph 1, Millbrook Park Ph 1 and Aberfeldy Phase 3A

![Btr [PDF Library]](https://static.fdocuments.in/doc/165x107/577d28d21a28ab4e1ea54df8/btr-pdf-library.jpg)