Economic outlook and mortgage market implications

20

Economic outlook and mortgage market implications Little recovery in sight Martin Gahbauer Senior Economist

description

Economic outlook and mortgage market implications. Little recovery in sight Martin Gahbauer Senior Economist. Outline. 3 negative shocks to mortgage transactions “Credit crunch” Economic downturn House price expectations Future prospects for activity. Shock #1: Credit Crunch. - PowerPoint PPT Presentation

Transcript of Economic outlook and mortgage market implications

Economic outlook and mortgage market

implications

Little recovery in sight

Martin Gahbauer

Senior Economist

Outline

• 3 negative shocks to mortgage transactions

1. “Credit crunch”

2. Economic downturn

3. House price expectations

• Future prospects for activity

Shock #1: Credit Crunch

2007 Flow of funds (£bn)

0

20

40

60

80

100

120

140 Net mortgage and consumer creditChange in deposit balances

RMBS, covered bonds, etc.

Shock #1: Credit Crunch

Likely Flow of Funds in 2008

-40

-20

0

20

4060

80

100

120

140

Retail depositgrowth

Maturing RMBS Funds availablefor lending

2007 lending tohouseholds

Source: Nationwide calculations

Credit crunch impact on lending criteria

Expected change in credit scoring criteria (net balance)

-50

-40

-30

-20

-10

0

10

Dec-07 Mar-08 Jun-08Source: BoE Credit Conditions Survey.

Shock #2: Economic downturn

• Economic output likely to fall over next year

• Domestic demand to be hit hardest

• Noticeable recovery not likely before 2010

GDP Fan Chart - Aug Inflation Report

ONS Data

-2

-1

0

1

2

3

4

5

6

2003q1 2004q3 2006q1 2007q3 2009q1 2010q3Source: Bank of England

-2

-1

0

1

2

3

4

5

6

Shock #2: Economic downturn

Sterling Oil Price

£40

£45

£50

£55

£60

£65

£70

£75

1/ 1/ 08 2/ 12/ 08 3/ 25/ 08 5/ 6/ 08 6/ 17/ 08 7/ 29/ 08 9/ 9/ 08

Source: Reuters

Shock #2: Economic downturn

Real post-tax income per household

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Mar-00 Mar-01 Mar-02 Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08

Source: ONS, DCLG

Mortgage Affordability

Initial Affordability of Mortgages

10%

20%

30%

40%

50%

60%

1984 Q1 1987 Q1 1990 Q1 1993 Q1 1996 Q1 1999 Q1 2002 Q1 2005 Q1 2008 Q1Source: Nationwide

FTB mortgage cost as % oftake-home pay

Long-run average

• Falling real incomes are a problem …

• … especially since affordability metrics were stretched to begin with

Labour market beginning to buckle

Claimant count monthly change

-20

-10

0

10

20

30

40

Aug-03 Aug-04 Aug-05 Aug-06 Aug-07 Aug-08Source: ONS

• Unemployment rate likely to rise appreciably

• Most job losses so far in construction, manufacturing and hotel/restaurant sectors

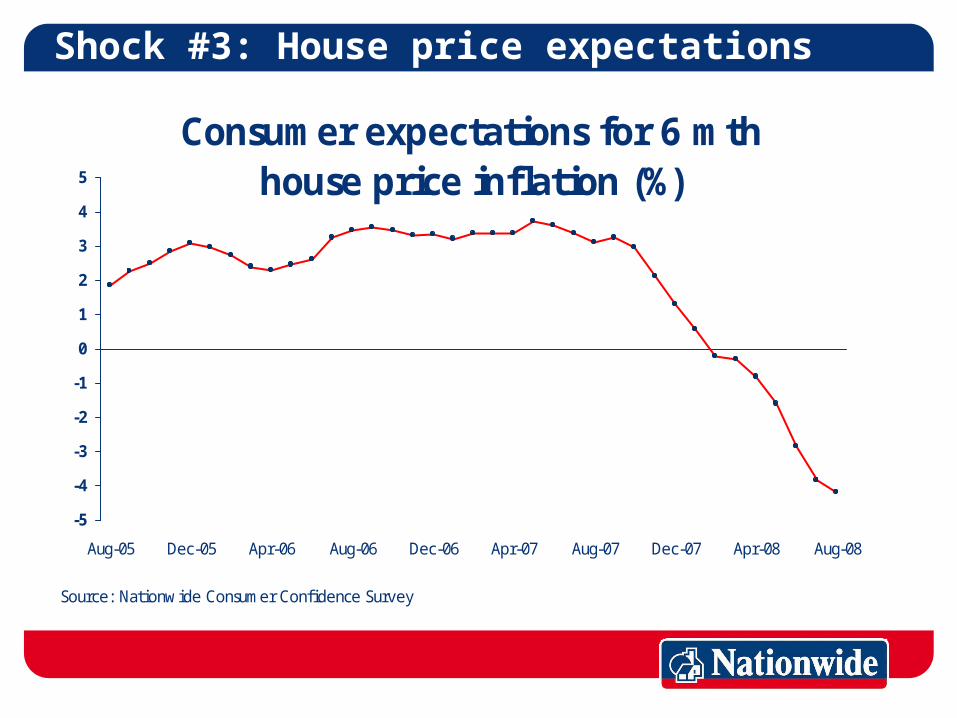

Shock #3: House price expectations

House price inflation (% yoy)

-15

-10

-5

0

5

10

15

20

25

30

35

Aug

-91

Aug

-92

Aug

-93

Aug

-94

Aug

-95

Aug

-96

Aug

-97

Aug

-98

Aug

-99

Aug

-00

Aug

-01

Aug

-02

Aug

-03

Aug

-04

Aug

-05

Aug

-06

Aug

-07

Aug

-08

Source: Nationwide, Halifax

Nationwide Halifax

Shock #3: House price expectations

Consumer expectations for 6 mth house price inflation (%)

-5

-4

-3

-2

-1

0

1

2

3

4

5

Aug-05 Dec-05 Apr-06 Aug-06 Dec-06 Apr-07 Aug-07 Dec-07 Apr-08 Aug-08

Source: Nationwide Consumer Confidence Survey

Big impact of shocks on lending volumes

Mortgage approvals for house purchase ('000s)

0

20

40

60

80

100

120

140

Apr-93 Apr-96 Apr-99 Apr-02 Apr-05 Apr-08

Source: Bank of England

0

5

10

15

20

25

30

35Total Specialist

Impact of shocks on lending volumes II

Remortgage Approvals ('000s)

60

70

80

90

100

110

120

J ul-05 J an-06 J ul-06 J an-07 J ul-07 J an-08 J ul-08Source: Bank of England

Reasons to be cheerful: Inflation now peaking …

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Aug-99 Aug-00 Aug-01 Aug-02 Aug-03 Aug-04 Aug-05 Aug-06 Aug-07 Aug-08 Aug-09 Aug-10

Headline inflation Core Inflation

… and base rate likely to fall sharply

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

Oct-06 Apr-07 Oct-07 Apr-08 Oct-08 Apr-09 Oct-09

Base rate 2-yr Swap

Market will eventually recover

• Valuations will adjust to more affordable level

• Rental yields likely to rise well above “risk-free” rate of return

• US rescue plan may boost investor confidence

• Economy and employment outlook should improve by 2010

• Low activity has been leading to build-up of pent-up demand

Demographic projections still favourable

Demographic Projections

-400

-300

-200

-100

0

100

200

300

1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012

Source: Government Actuary's Department

15-24 yrs old 25-34 yrs old Total FTB cohorts

Specific market dynamics

• House purchase:

Activity should already be in a bottoming out process, albeit at extremely low levels

Expect FTB activity to recover somewhat in 2009

• Re-mortgage:

Deal maturity pipeline to slow in 2009

Some borrowers may not meet criteria

But rate cuts should lead to more attractive deals

Conclusions

• Near-term outlook for transaction volumes remains very difficult

• Adjustment takes time to work through system …

• … but a cyclical recovery will eventually arrive