Economic Forum of Chad - Ashta Arvind

25

Microfinance Arvind Ashta Titulaire du Chaire de Microfinance ESC Dijon-Bourgogne Financé par Banque Populaire de Bourgogne Franche Compté Muhammad Yunus Prix Nobel du Paix 2006, Fondateur/ Pt du Grameen Bank

-

Upload

emrc -

Category

Investor Relations

-

view

988 -

download

5

Transcript of Economic Forum of Chad - Ashta Arvind

MicrofinanceArvind Ashta

Titulaire du Chaire de Microfinance

ESC Dijon-Bourgogne

Financé par Banque Populaire de Bourgogne Franche Compté

Muhammad Yunus

Prix Nobel du Paix 2006,

Fondateur/ Pt du Grameen Bank

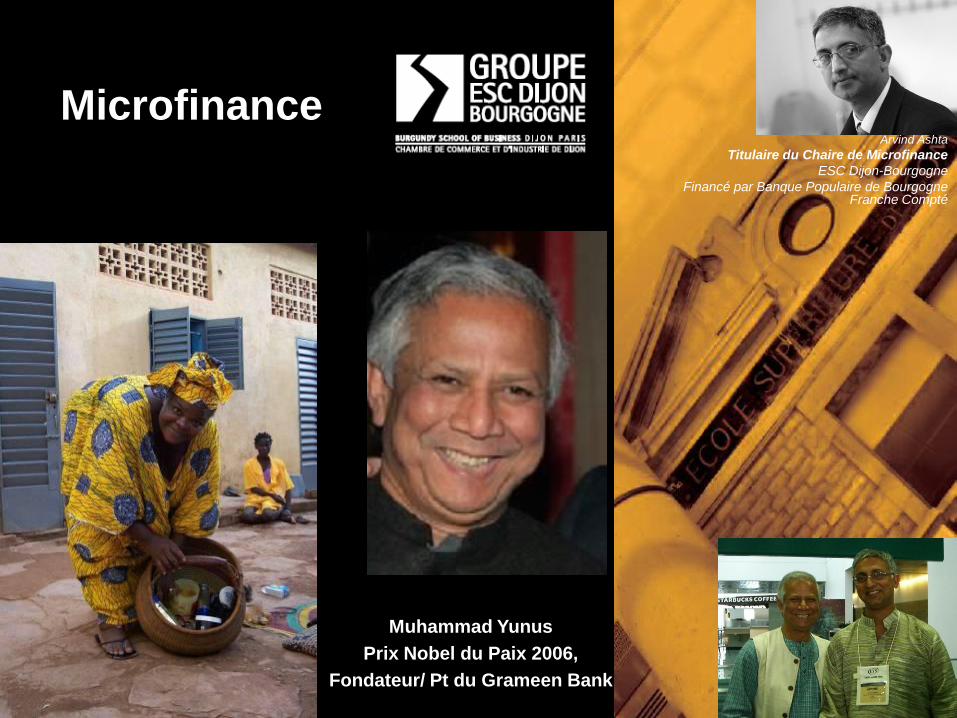

Pourquoi les pauvres ne recevaient pas des prêts?

MR poor

MR rich

Supply

of credit

Loans

Intérêts

The MR of capital curve is discontinuous at a point owing to effect of human capital available only to not-

so poor borrowers. The supply curve is U shaped owing to asymmetric information and transaction costs.

As a result, poor people do not receive loans but wealthier people do, at a fairly low interest rate, ro if

there is competition and rm if there is not.

ro

ARpoor

AR richrm

A BO C

Ashta, 2009

Qu'avez fait Yunus?

1. Prêt aux groupes

2. Incitations

• Menace de ne plus prêter

• Crédits différés (aux emprunteur

différents)

• Prêts progressifs

• Remboursement publics

• Médailles

3. Remboursement fréquents

4. Collatéral

• Flexible (bétail, bijoux)

• La capacité d'épargne démontré

5. Femmes

6. Les informations des voisins

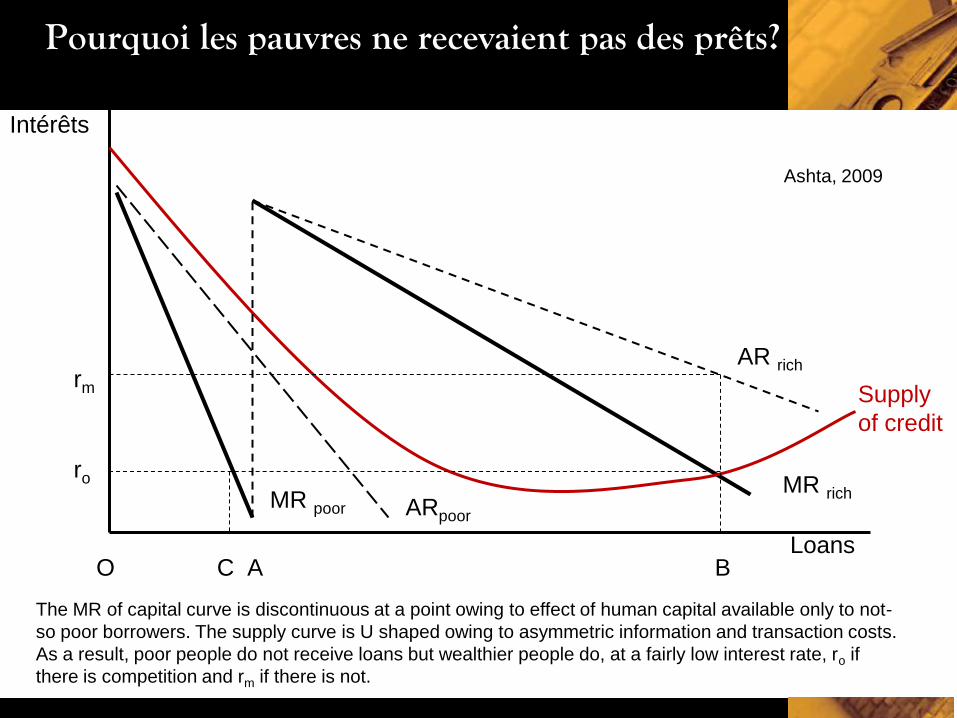

Formes des IMFs

4

Sociétés de

Finance

Banques

Usuriers

Rural

Development

Banks

Specialized IMFsCredit and Savings

Associations

and Village Banks

Mutuelles

Cooperatives

Au sein des

ONGs

Tontines

Self-Help groups

Famille

et

Amis

Emprenteurs

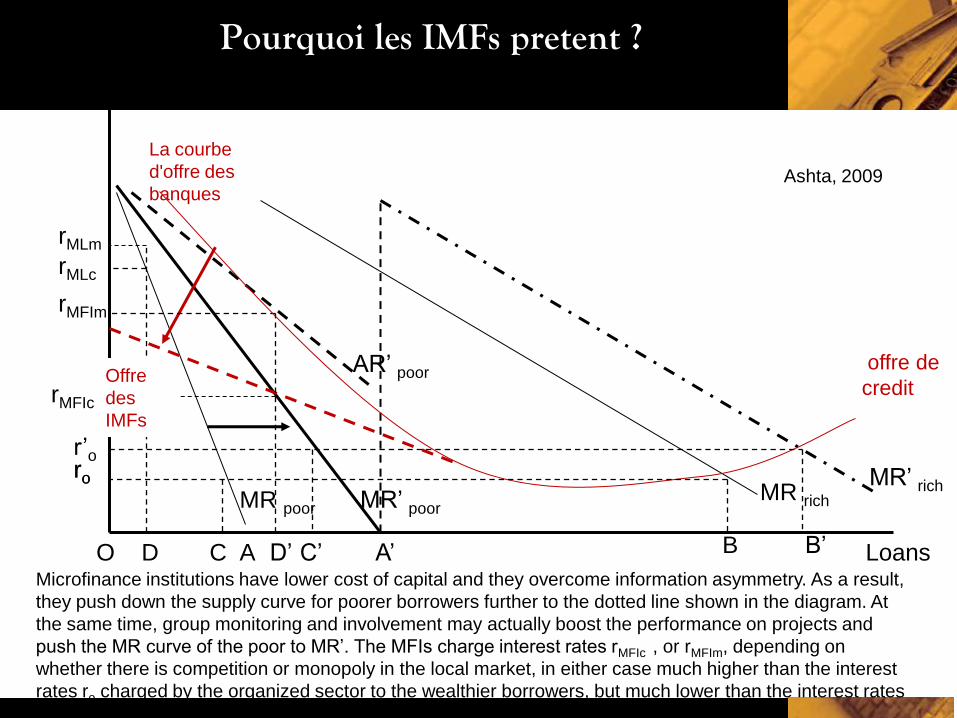

Pourquoi les IMFs pretent ?

MR poorMR rich

Intérêt

Microfinance institutions have lower cost of capital and they overcome information asymmetry. As a result,

they push down the supply curve for poorer borrowers further to the dotted line shown in the diagram. At

the same time, group monitoring and involvement may actually boost the performance on projects and

push the MR curve of the poor to MR’. The MFIs charge interest rates rMFIc , or rMFIm, depending on

whether there is competition or monopoly in the local market, in either case much higher than the interest

rates ro charged by the organized sector to the wealthier borrowers, but much lower than the interest rates

rML charged by money-lender.

ro

MR’ poor

rMFIc

AR’ poor

rMFIm

AO A’CD

rMLm

rMLc

MR’ richro

r’o

C’ LoansB B’D’

Ashta, 2009

offre de

creditOffre

des

IMFs

La courbe

d'offre des

banques

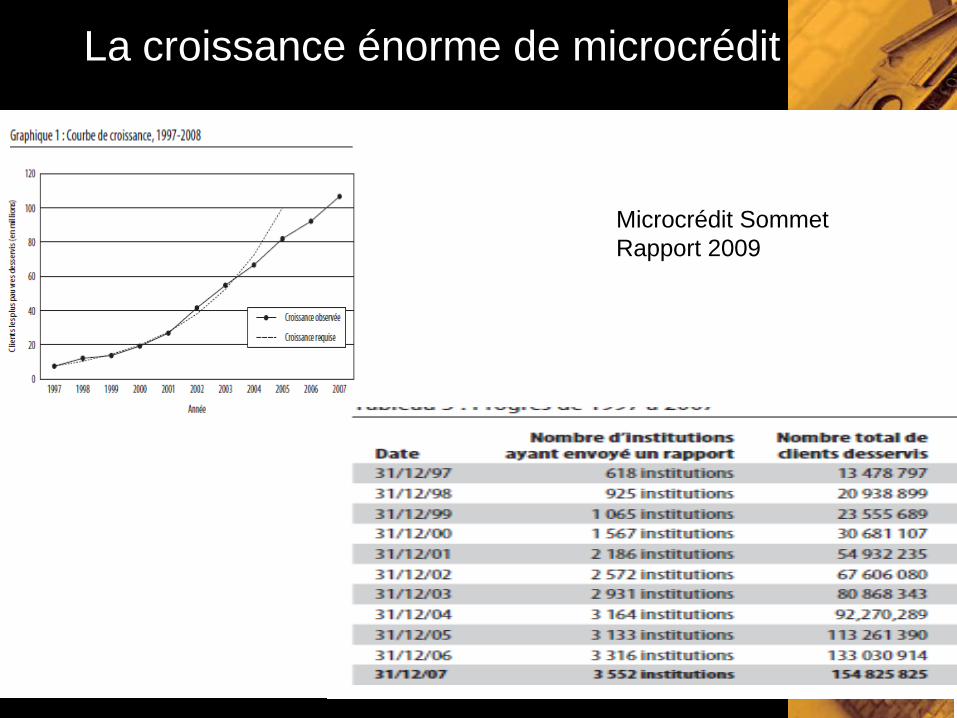

La croissance énorme de microcrédit

Microcrédit Sommet

Rapport 2009

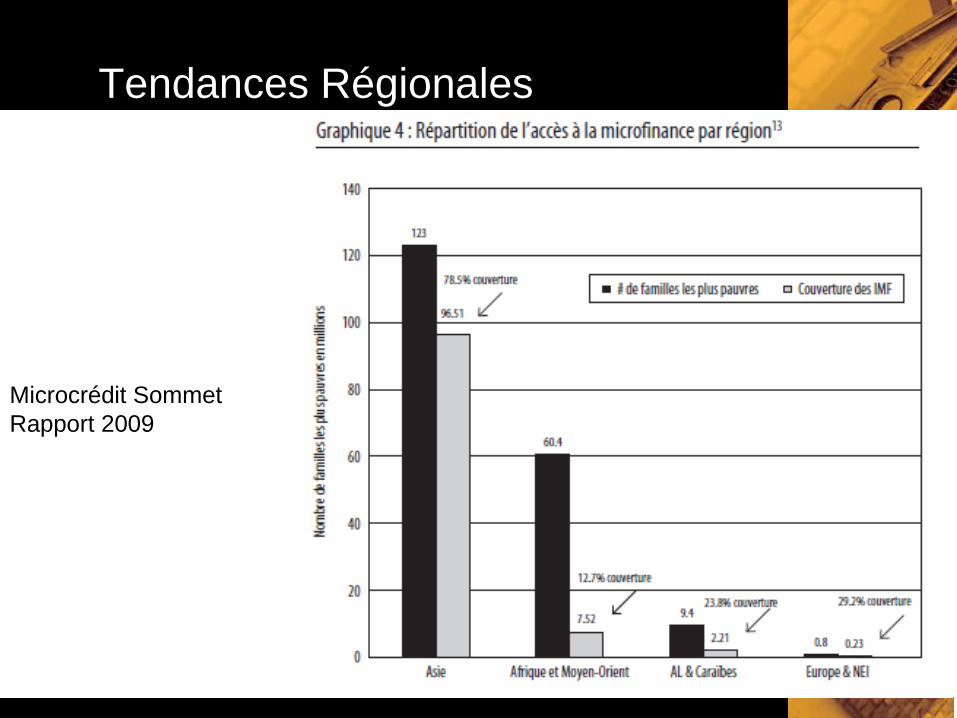

Tendances Régionales

Microcrédit Sommet

Rapport 2009

La croissance étonnante de

Microcrédit

Il est consideré que globalement

Plus de 175 million d'emprunteurs

Plus de10,000 IMFs

Taux de remboursement 97 percent.

Croissance 30 % p.a.

8

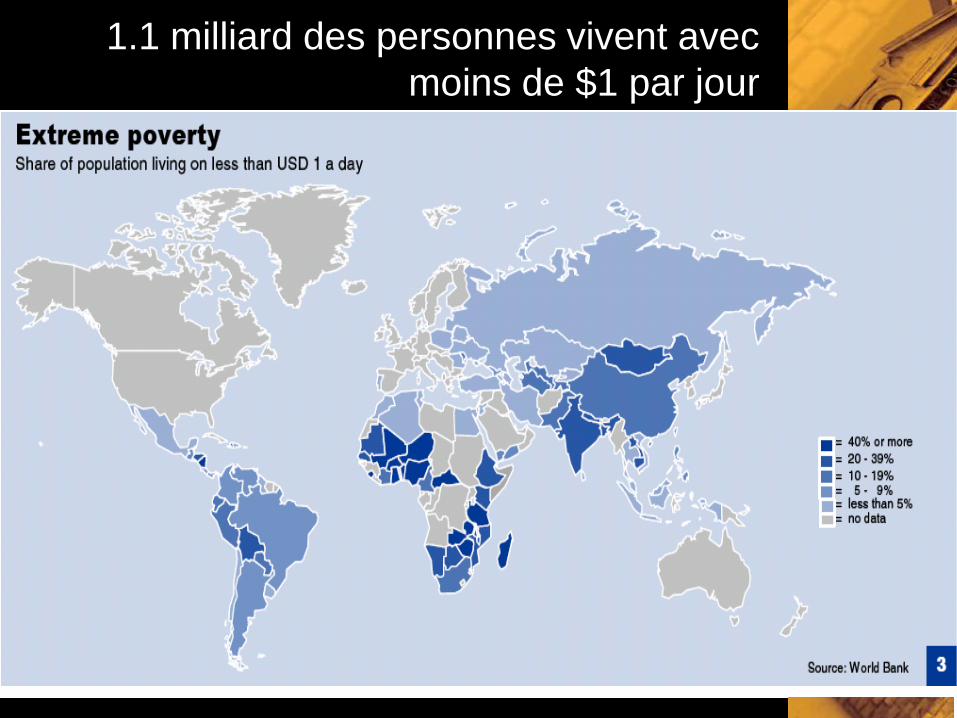

1.1 milliard des personnes vivent avec

moins de $1 par jour

Microfinance touche le gris, mais pas les

plus pauvres

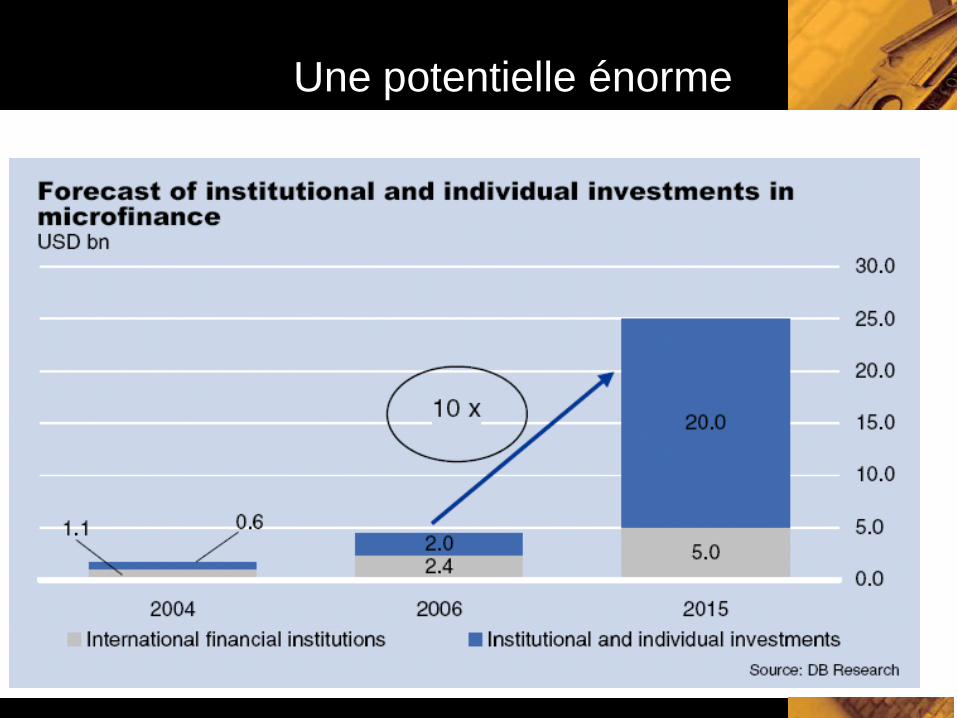

Une potentielle énorme

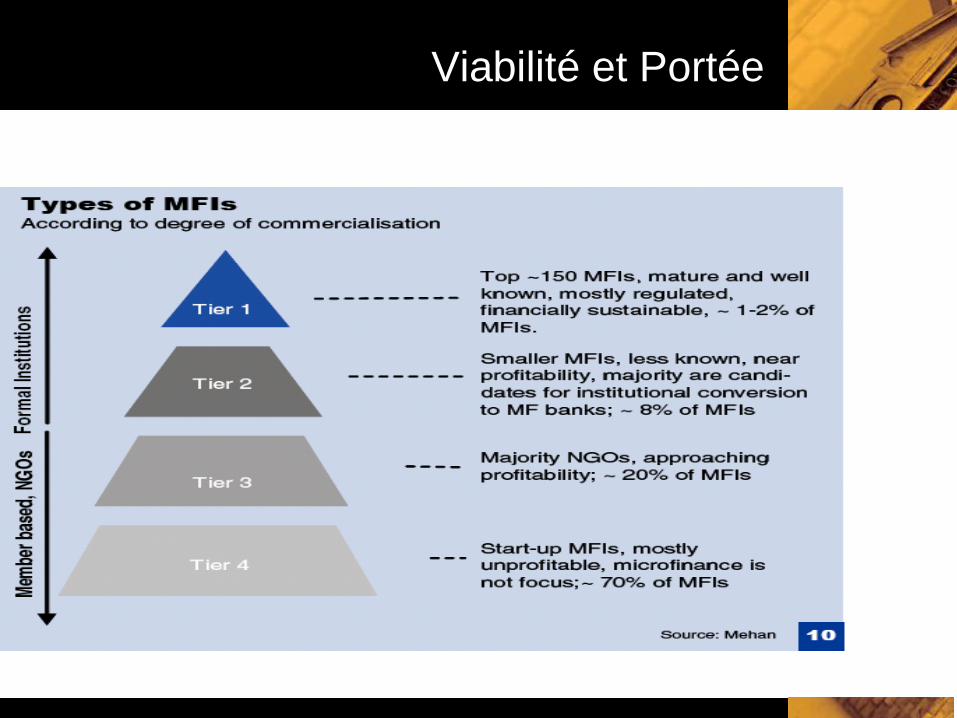

Viabilité et Portée

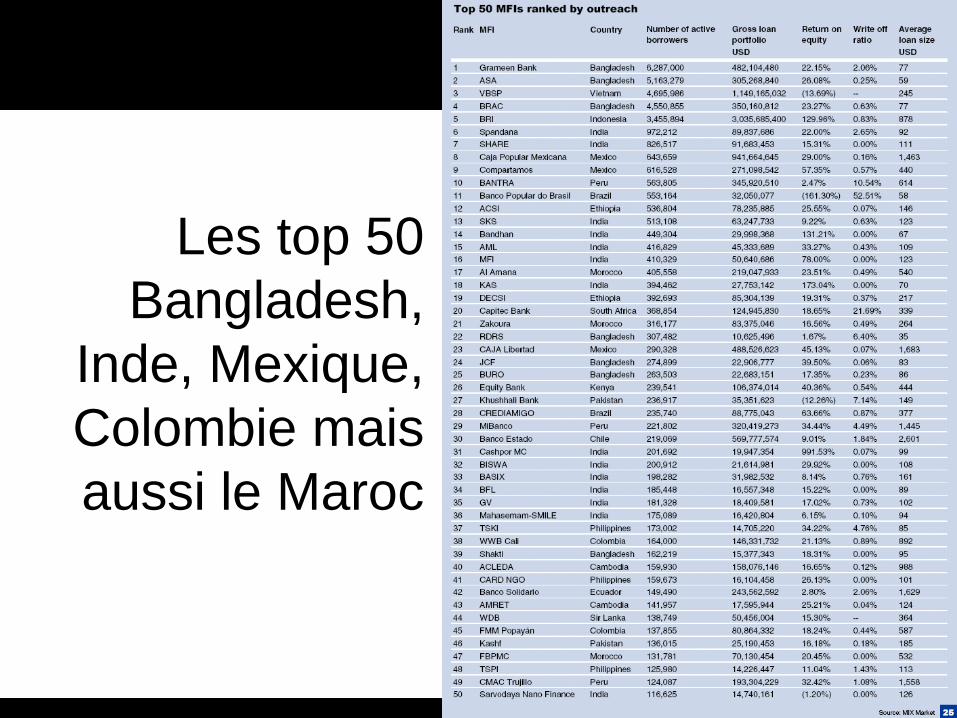

Les top 50

Bangladesh,

Inde, Mexique,

Colombie mais

aussi le Maroc

Pourquoi certains pays réussissent?

Etude sur l'Afrique du Nord (Allaire et al, 2008)

… pourquoi le Maroc

• More postal accounts mean less MFIs,

but Post is offering MF

• High male adult literacy means less

MFIs

• Le pauvreté

• Donations matter

• Geography matters (area and density)

× Fermeture au monde n'aide pas (Libye

, Algérie)

× L'exportation de pétrole n'aide pas

• La chômage: oui

• Les lois spécifique aide, mais ne

doivent pas être contraignant

• Adult literacy

Etude sur l'Afrique d'Ouest (Ashta & Fall,

2009)… pourquoi le Sénégal?

Revenu par habitant

Remittances des expatriés

• Dans un moindre mesure• Croissance Du PIB

• Esperance de vie à naissance

Public Governance

• Government effectiveness

• Rule of law

• Legislative quality

• Control of corrumtion

× But not

× Political stabiility

× Voice and accountablility

• Une ministère independent

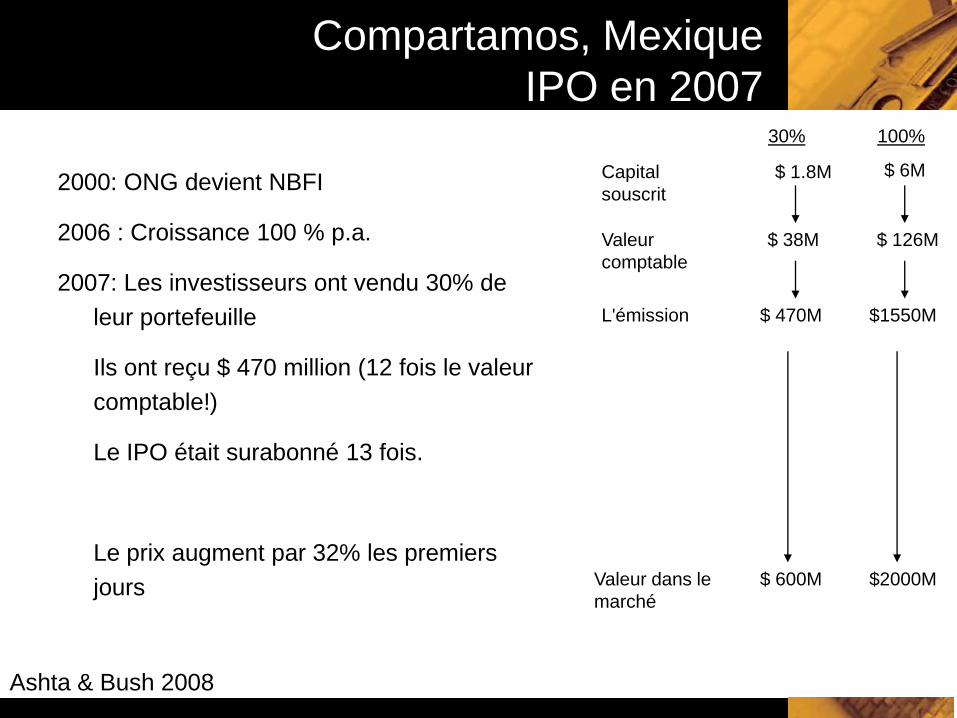

Compartamos, Mexique

IPO en 2007

2000: ONG devient NBFI

2006 : Croissance 100 % p.a.

2007: Les investisseurs ont vendu 30% de

leur portefeuille

Ils ont reçu $ 470 million (12 fois le valeur

comptable!)

Le IPO était surabonné 13 fois.

Le prix augment par 32% les premiers

jours

$ 1.8M

$ 38M

$ 470M

$ 600M

30%

$ 6M

$ 126M

$1550M

$2000M

100%

Capital

souscrit

Valeur

comptable

L'émission

Valeur dans le

marché

Ashta & Bush 2008

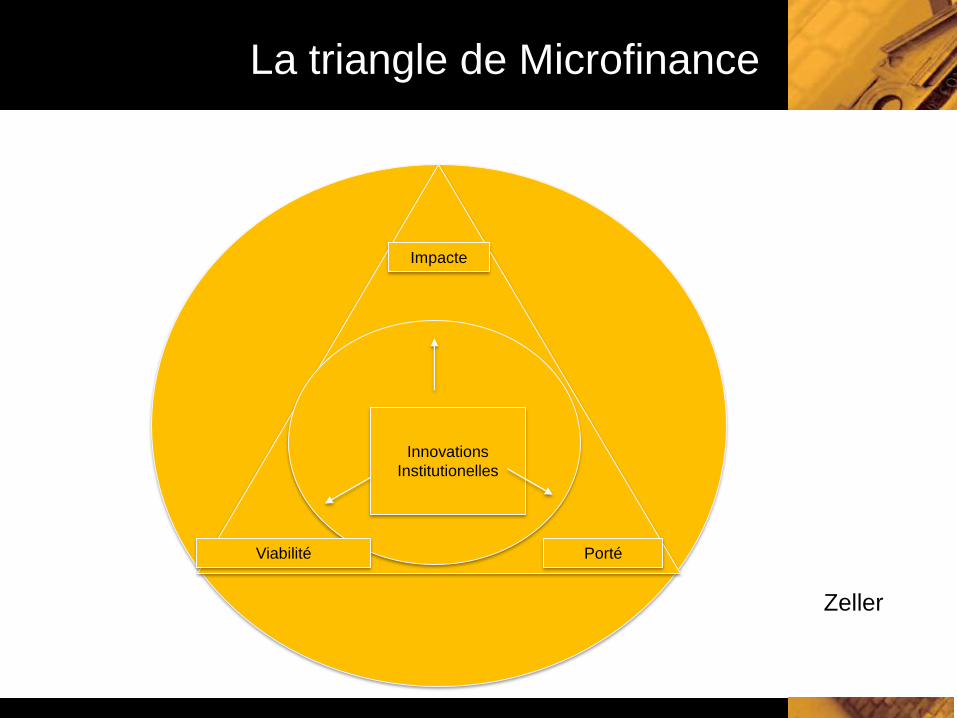

La triangle de Microfinance

Impacte

Viabilité Porté

Innovations

Institutionelles

Zeller

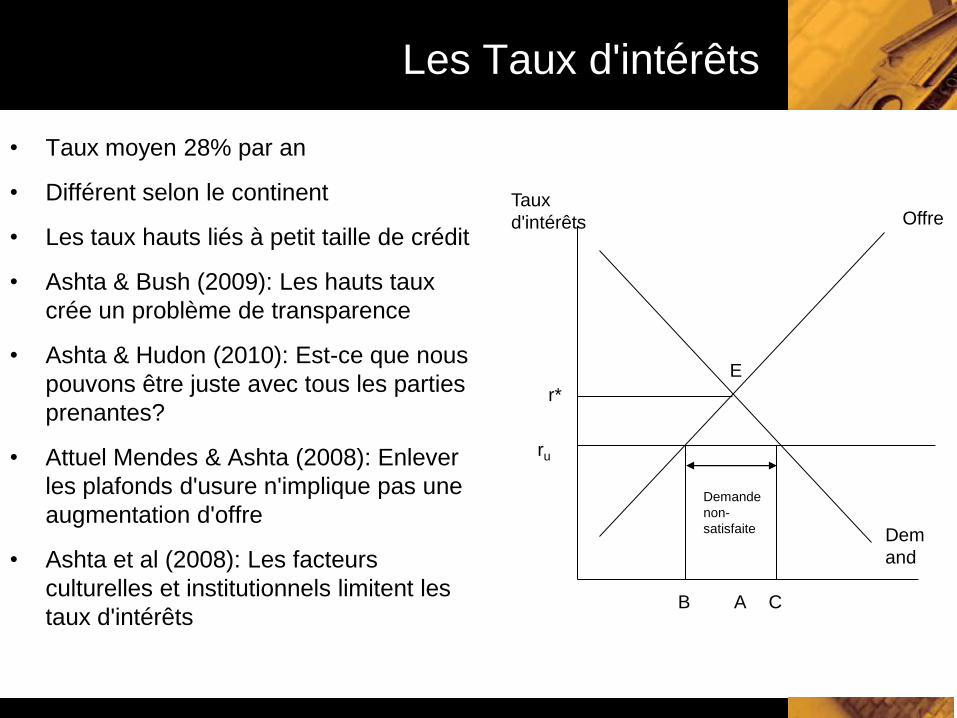

Les Taux d'intérêts

• Taux moyen 28% par an

• Différent selon le continent

• Les taux hauts liés à petit taille de crédit

• Ashta & Bush (2009): Les hauts taux

crée un problème de transparence

• Ashta & Hudon (2010): Est-ce que nous

pouvons être juste avec tous les parties

prenantes?

• Attuel Mendes & Ashta (2008): Enlever

les plafonds d'usure n'implique pas une

augmentation d'offre

• Ashta et al (2008): Les facteurs

culturelles et institutionnels limitent les

taux d'intérêts

Taux

d'intérêts

r*

ru

AB C

Demande

non-

satisfaite

E

Offre

Dem

and

Est-ce que la technologie pourrait

contribuer?

POS

ATM

SIG

PDA

Téléphone

Biométriques

Internet

On monte le cocotier

Quelques Web 2.0 opérateurs:

Intermédiares ou facilitateurs?

KIVA, Wokii: Movement of funds

KivaField Partner

MFILenders

The MFI distributes funds to

individual borrowers or to

groups of borrowers

The Lender chooses

who to lend to, but

routes the funds

through KIVA

Entrepreneur

Prosper, Zopa and Lending club:

Movement of funds

Commercial

IntermediaryLenders Entrepreneur

The intermediary distributes

funds to individual borrowers

The Lender chooses who

to lend to, but routes the

funds through the

intermediary

Virgin Money: Movement of funds

Virgin Money

LendersEntrepreneur

Lenders and borrowers

know each others

Virgin money facilitates

Microplace: Movement of funds

SecurityIssuers

Field PartnerIMF

Lenders Entrepreneur

The security issuers distribute funds to the identified IMFs

The Lender (investor) buys bonds of security issuers but indicates which IMF these should be directed to.

Microplace

(Ashta & Assadi, 2008)

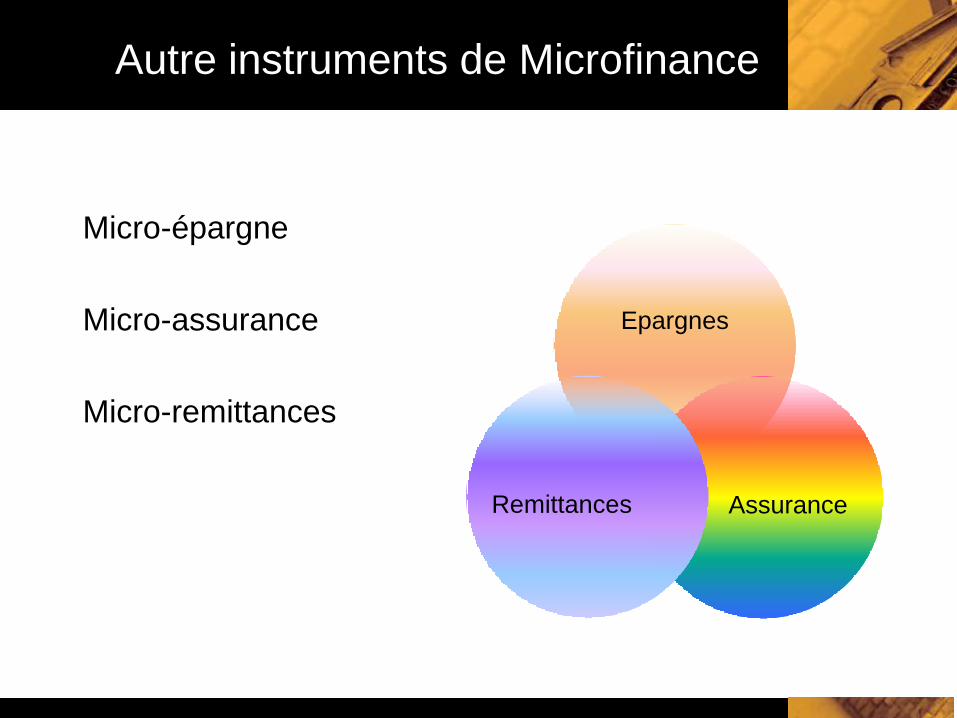

Autre instruments de Microfinance

Micro-épargne

Micro-assurance

Micro-remittances

Epargnes

AssuranceRemittances

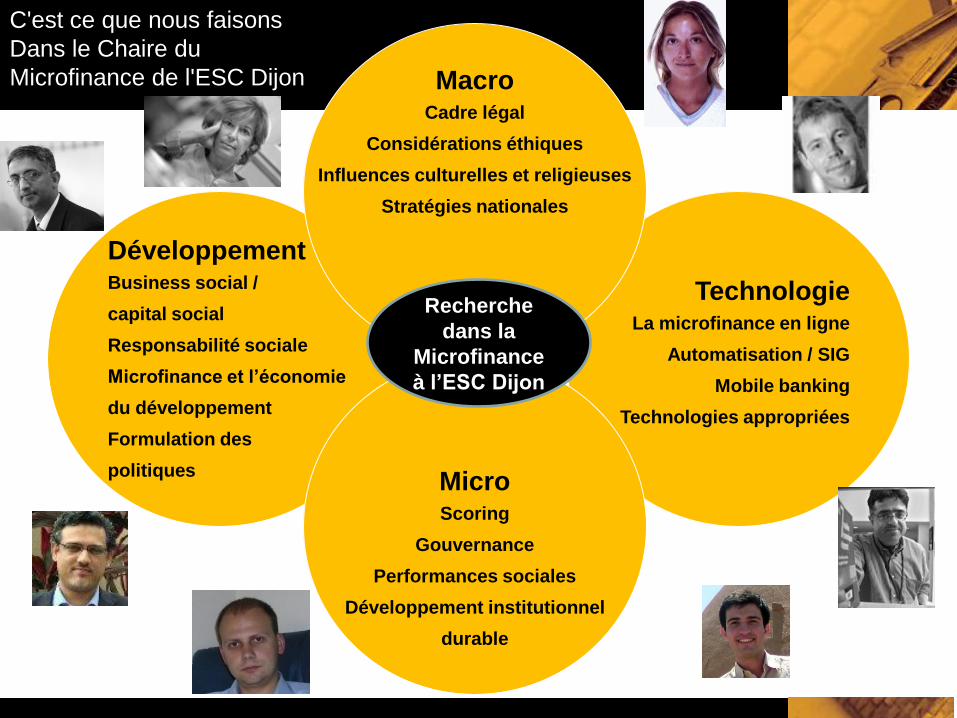

Où va-t-on?

Peut Microfinance devenir l'infrastructure

Grameen ladies deviennent

opératrices de téléphone

Grameen ladies distribuent

yaourt de Danone

Peut-on s'amuser?

TechnologieLa microfinance en ligne

Automatisation / SIG

Mobile banking

Technologies appropriées

DéveloppementBusiness social /

capital social

Responsabilité sociale

Microfinance et l’économie

du développement

Formulation des

politiquesMicroScoring

Gouvernance

Performances sociales

Développement institutionnel

durable

MacroCadre légal

Considérations éthiques

Influences culturelles et religieuses

Stratégies nationales

Recherche

dans la

Microfinance

à l’ESC Dijon

C'est ce que nous faisons

Dans le Chaire du

Microfinance de l'ESC Dijon

Contact

Arvind ASHTA

Professor - Finance, Control and Law

Holder of the Microfinance Chair of the Burgundy School of Business

Groupe ESC Dijon Bourgogne

29, rue Sambin - BP 50608 - 21006 DIJON

Tél. +33 (0) 380 725 966

Fax. +33 (0) 380 725 999

Web : http://www.escdijon.eu