EC Economic Outlook Book

150

A DEDEA & Treasury Publication e Eastern Cape ECONOMIC PROFILE AND OUTLOOK

-

Upload

maagathalephoto -

Category

Documents

-

view

73 -

download

5

Transcript of EC Economic Outlook Book

A DEDEA & Treasury Publication

The Eastern CapeE C O N O M I C P R O F I L E

A N D O U T L O O K

The Eastern Cape Economic Profile and Outlook, 2010, is compiled

using the available information from different sources.

Some of the information is subject to revision.

FOREWORDThe Eastern Cape Economic Profile and Outlook – 2010, is the first of a series of

publications that will be released by the Department of Economic Development &

Environmental Affairs (DEDEA) in partnership with the Provincial Treasury on an annual

basis. This initiative seeks to provide reliable, accurate and up to date information on the

economic sector within the Eastern Cape Province. This document is intended to serve

as a point of reference to the public and the private sector for decision making. It is our

hope that this work will be of great value to those involved in the investment space,

economic planning, research, budgeting processes, to name but a few.

Through this publication, our intention is to provide a single point of reference for the

economic profile of the Eastern Cape, including District Municipalities and the Metro, as

well as key economic sectors. The publication is also forward looking in that it provides a

forecast and an outlook of key variables in the economy over a three- year period. This is

very important to us, as the global economy begins to show signs of recovery from the

economic crisis.

As the Department of Economic Development & Environmental Affairs we have a

mandate to provide leadership and guidance in economic development and planning

discourse. With this in mind I invite all our stakeholders to receive, study, and make use

of this publication. As the first of many to come, our stakeholders can look forward to this

being an annual release and can also look forward to other publications in other areas of

economic thought. I must also commend the team that has worked tirelessly to put this

together, under the leadership of the Head of Department.

Hon Mcebisi Jonas, Mr (MPL)

MEC for Finance, Economic Development & Environmental Affairs

ABBREVIATIONS ........................................................................................................................................ II

TABLES ....................................................................................................................................................... IV

FIGURES ..................................................................................................................................................... V

ACKNOWLEDGEMENTS ............................................................................................................................ VI

EXECUTIVE SUMMARY ............................................................................................................................. VII

FORECASTS ............................................................................................................................................... IX

National ..................................................................................................................................................... IX

Eastern Cape .............................................................................................................................................. X

1 GLOBAL ECONOMIC OUTLOOK AND FORECAST METHODOLOGY ............................................. 1

1.1 Global Economic Outlook ................................................................................................................. 1

1.1.1 USA .................................................................................................................................................... 1

1.1.2 JAPAN ............................................................................................................................................... 2

1.1.3 CHINA ............................................................................................................................................... 3

1.1.4 INDIA ................................................................................................................................................. 3

1.1.5 MAJOR EUROPEAN UNION MEMBER STATES ................................................................................ 4

1.1.6 BRAZIL ............................................................................................................................................... 4

1.2 The Theoretical Framework of the South African Macro-model .............................................. 5

1.3 Eastern Cape Model Conceptualisation ........................................................................................ 5

2 NATIONAL ECONOMIC PERFORMANCE AND OUTLOOK .............................................................. 9

2.1 Overview of current situation .......................................................................................................... 9

2.2 Consumer spending .......................................................................................................................... 10

2.3 Public Fixed Investment ................................................................................................................... 11

2.4 Private Fixed Investment ................................................................................................................. 11

2.5 Labour-Market Condition ................................................................................................................. 12

2.6 Inflation ............................................................................................................................................... 13

2.7 Monetary Policy and Interest Rates .............................................................................................. 13

2.8 Fiscal Policy ....................................................................................................................................... 14

3 THE ECONOMY OF THE EASTERN CAPE ......................................................................................... 17

3.1 Profile of the Eastern Cape ............................................................................................................. 17

3.1.1 Overview ........................................................................................................................................... 17

3.1.2 Population size and age distribution ................................................................................................ 18

3.1.3 HIV and AIDS .................................................................................................................................... 19

3.1.4 Migration .......................................................................................................................................... 20

3.2 Economic Outlook of the Eastern Cape ........................................................................................ 20

3.2.1 Economic performance and projections ........................................................................................... 20

3.2.2 Total Investment in the Eastern Cape .............................................................................................. 21

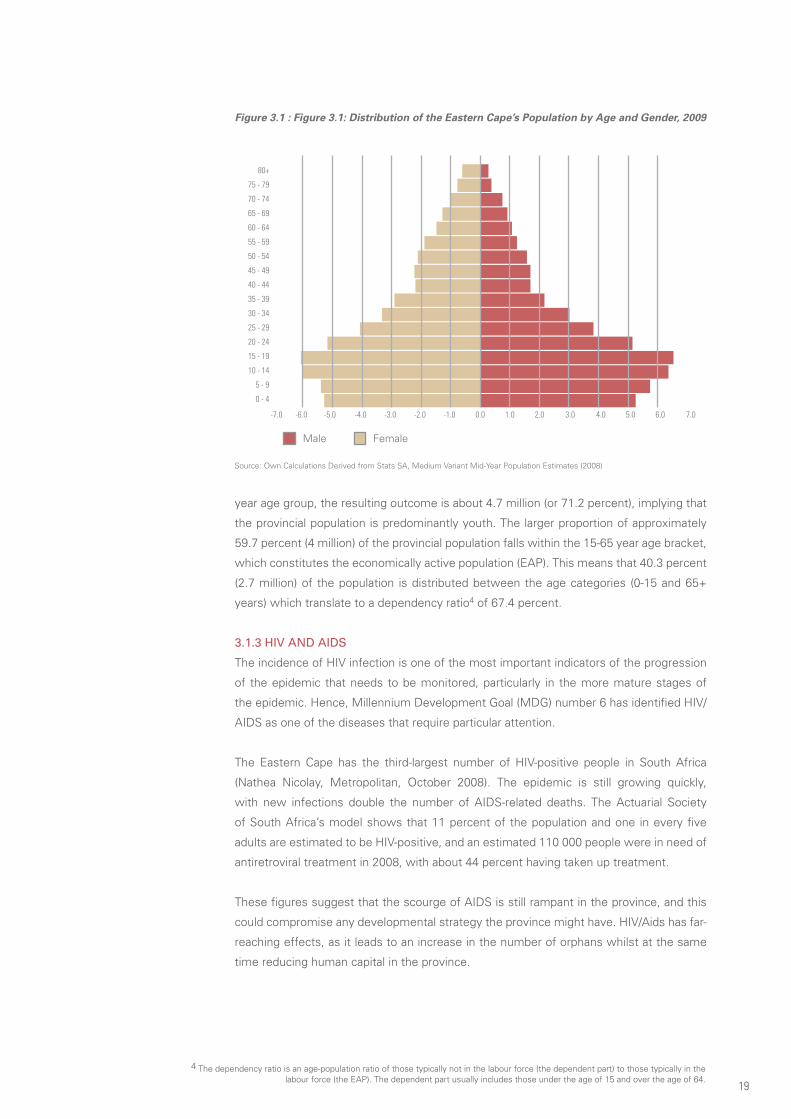

3.2.2.1 Machinery and other equipment ................................................................................................... 22

3.2.2.2 Building and construction .............................................................................................................. 23

3.2.2.3 Transport equipment ..................................................................................................................... 24

3.2.3 Final Consumption Expenditure in the Eastern Cape ....................................................................... 24

3.2.3.1 Consumption of durable goods in Eastern Cape ........................................................................... 26

3.2.3.2 Consumption of non-durable goods in Eastern Cape .................................................................... 27

3.2.3.3 Consumption of semi-durable goods in Eastern Cape .................................................................. 28

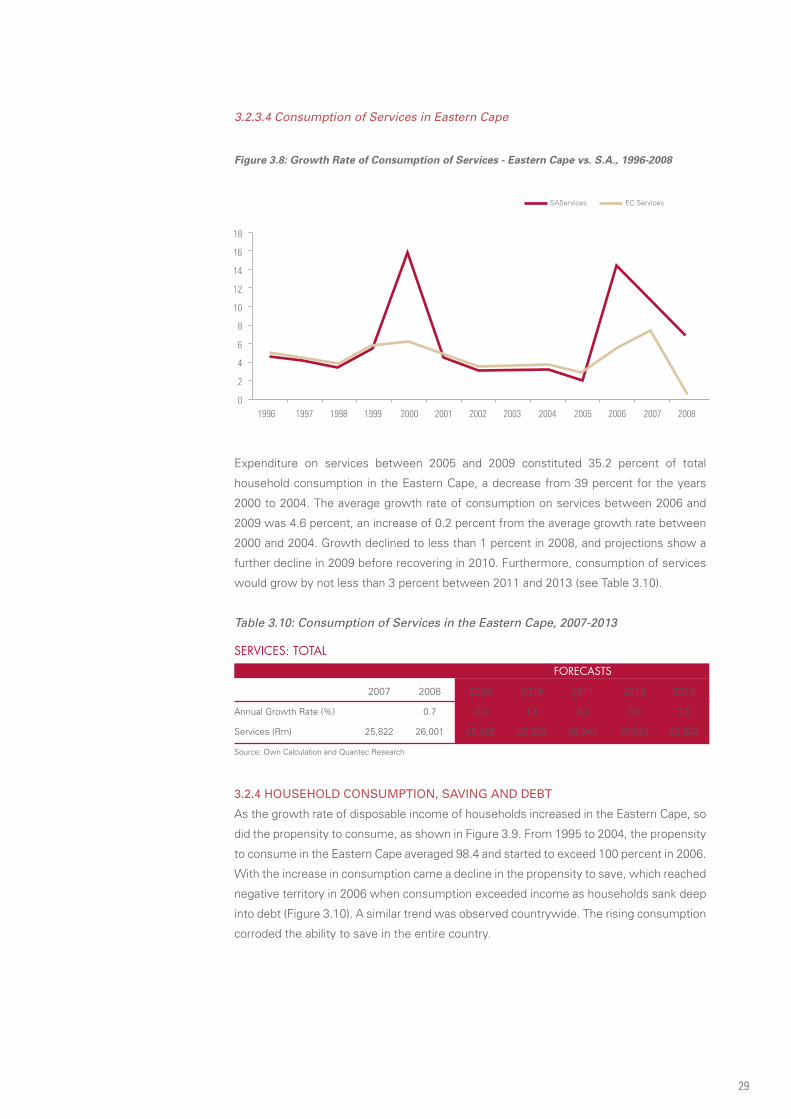

3.2.3.4 Consumption of Services in Eastern Cape .................................................................................... 29

3.2.4 Household Consumption, Saving and Debt ..................................................................................... 29

Tabl

E O

F C

On

TEn

Ts

3.2.5 Trade Position .................................................................................................................................... 30

3.2.5.1 Exports of Goods ............................................................................................................................ 30

3.2.5.2 Imports of Goods ............................................................................................................................ 31

3.2.5.3 Balance of Trade ............................................................................................................................. 32

3.3 Sectoral Analysis of the Eastern Cape .......................................................................................... 33

3.3.1 Sectoral Contribution Analysis in Eastern Cape ............................................................................... 33

3.3.1.1 Primary Sector ................................................................................................................................ 33

3.3.1.2 Secondary Sector ........................................................................................................................... 34

3.3.1.3 Tertiary Sector ................................................................................................................................ 34

3.3.2 Sectoral Growth Analysis in the Eastern Cape ................................................................................. 34

3.3.2.1 Primary Sector ................................................................................................................................ 34

3.3.2.2 Secondary Sector ........................................................................................................................... 35

3.3.2.3 Tertiary Sector ................................................................................................................................ 35

3.4 Labour-Market Analysis in Eastern Cape ..................................................................................... 36

3.4.1 Employment ....................................................................................................................................... 38

3.4.1.1 Employment by province ................................................................................................................ 38

3.4.1.2 Employment Sectoral Analysis ....................................................................................................... 39

3.4.1.2.1 Employment Industry’s Contribution to Total Employment ......................................................... 39

3.4.1.2.2 Formal Employment by Industry .................................................................................................. 39

3.4.1.2.3 Informal Employment by Industry ............................................................................................... 41

3.4.1.3 Employment by Occupation and by Skills ...................................................................................... 42

3.4.1.3.1 Employment by Occupation ......................................................................................................... 42

3.4.1.3.2 Employment by Skills .................................................................................................................. 43

3.4.2 Unemployment Rate in Eastern Cape ............................................................................................... 43

3.4.3 Labour Remuneration ........................................................................................................................ 44

3.4.3.1 Remuneration by Gender ............................................................................................................... 45

3.4.3.2 Remuneration by Age Group .......................................................................................................... 46

3.4.3.3 Remuneration by sector ................................................................................................................. 46

4 ECONOMIC PERFORMANCE OF DISTRICT MUNICIPALITIES ...................................................... 49

4.1 Amatole District Municipality ......................................................................................................... 49

4.1.1 Total Population by Age Group ......................................................................................................... 49

4.1.2 Total Population Affected by HIV ...................................................................................................... 50

4.1.3 Household Income and Expenditure ................................................................................................. 50

4.1.4 Sectoral Contribution Analysis ......................................................................................................... 51

4.1.5 Sectoral Growth Analysis ................................................................................................................. 52

4.1.6 Access to Services ............................................................................................................................ 53

4.1.6.1 Access to Water ............................................................................................................................. 53

4.1.6.2 Access to Energy ............................................................................................................................ 54

4.1.6.3 Access to Sanitation ...................................................................................................................... 54

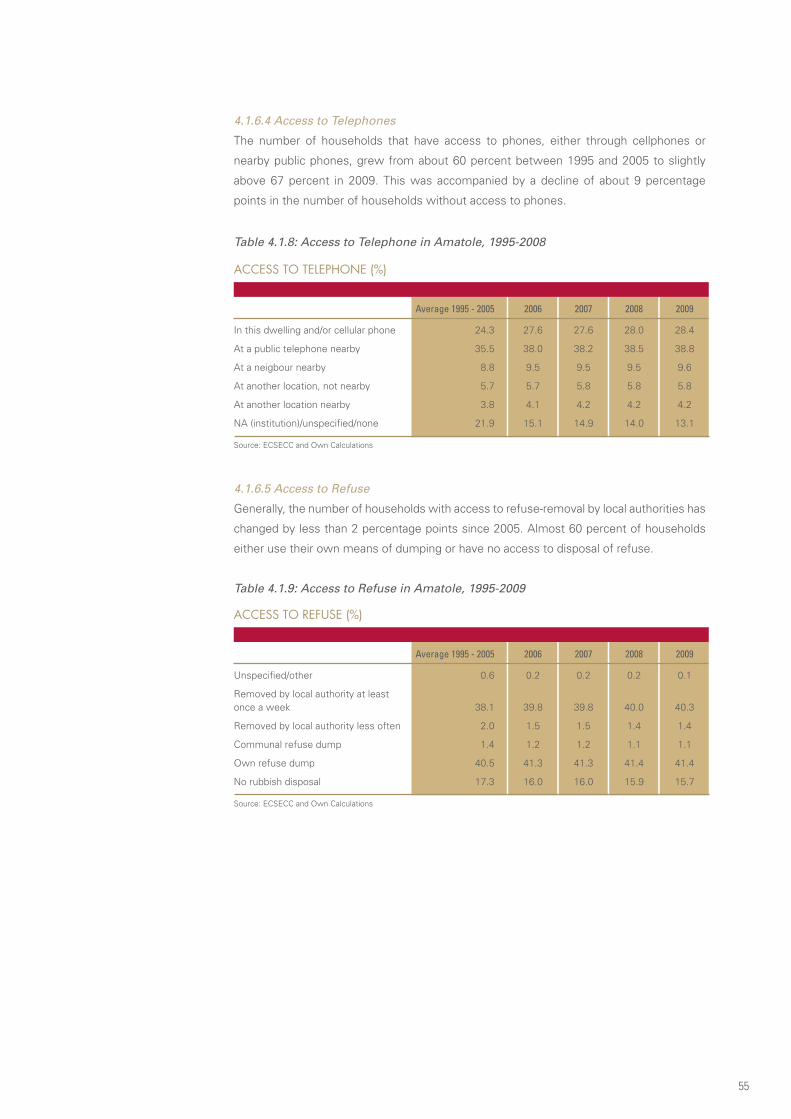

4.1.6.4 Access to Telephones .................................................................................................................... 55

4.1.6.5 Access to Refuse ........................................................................................................................... 55

4.1.7 Types of Dwelling ............................................................................................................................. 56

4.1.8 Formal Employment by Sector .......................................................................................................... 56

4.1.9 Informal and Formal Employment by Skill ........................................................................................ 57

4.1.10 Dependency Ratio ........................................................................................................................... 57

4.1.11 Level of Education ........................................................................................................................... 57

Tabl

E O

F C

On

TEn

Ts

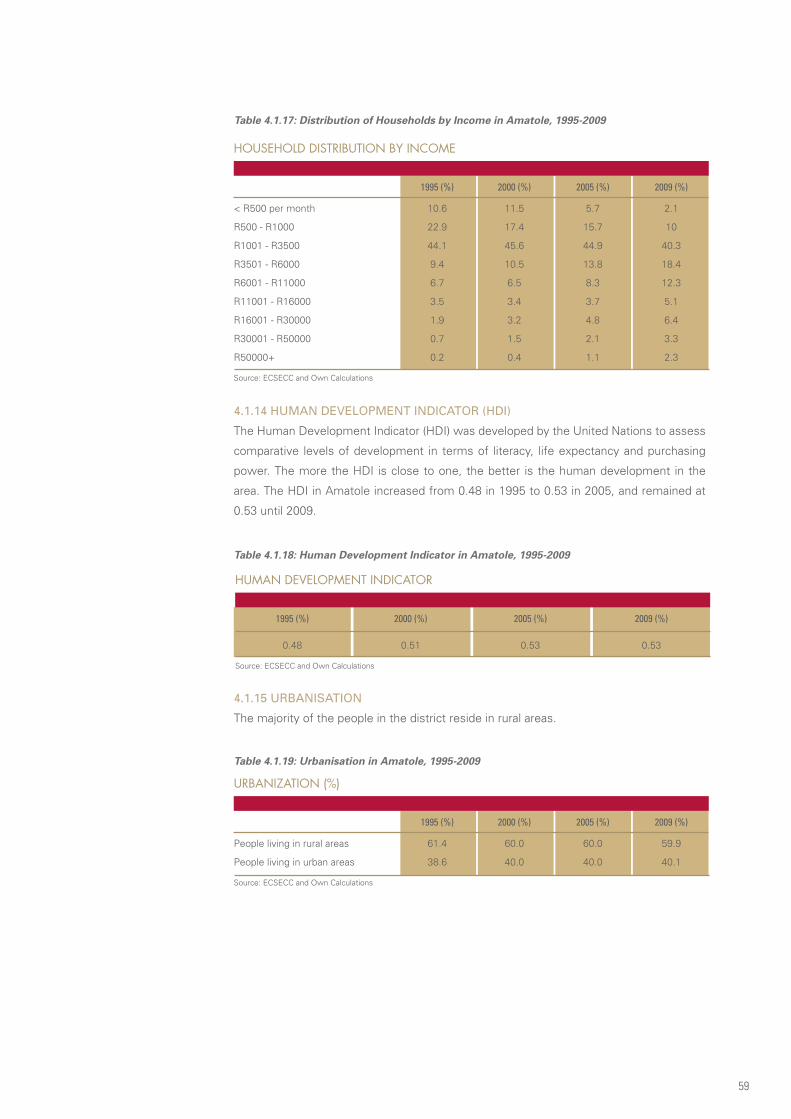

4.1.12 Number of People in Poverty .......................................................................................................... 58

4.1.13 Distribution of Households by Income ........................................................................................... 58

4.1.14 Human Development Indicator (HDI) .............................................................................................. 59

4.1.15 Urbanisation ................................................................................................................................... 59

4.2 Alfred Nzo District Municipality ..................................................................................................... 60

4.2.1 Total Population by Age Group ......................................................................................................... 60

4.2.2 Total Population Affected by HIV ..................................................................................................... 60

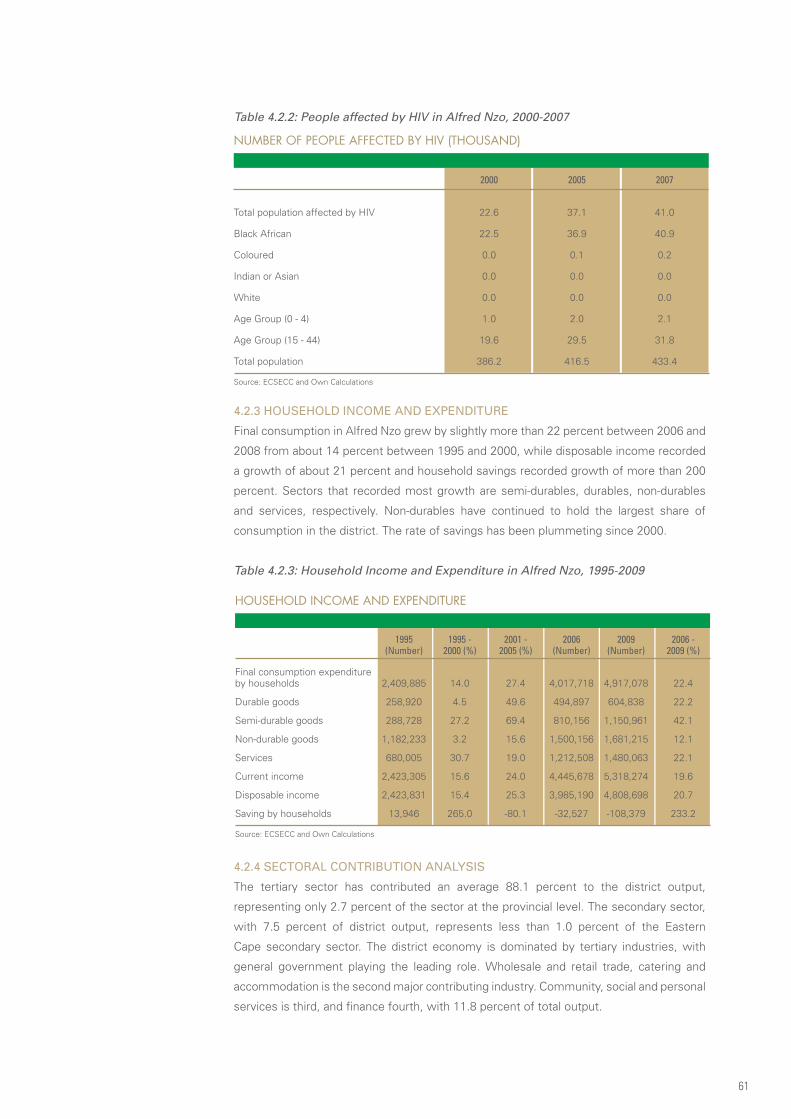

4.2.3 Household Income and Expenditure ................................................................................................. 61

4.2.4 Sectoral Contribution Analysis ......................................................................................................... 61

4.2.5 Sectoral Growth Analysis ................................................................................................................. 62

4.2.6 Access to Services ........................................................................................................................... 63

4.2.6.1 Access to Water ............................................................................................................................ 63

4.2.6.2 Access to Energy ........................................................................................................................... 63

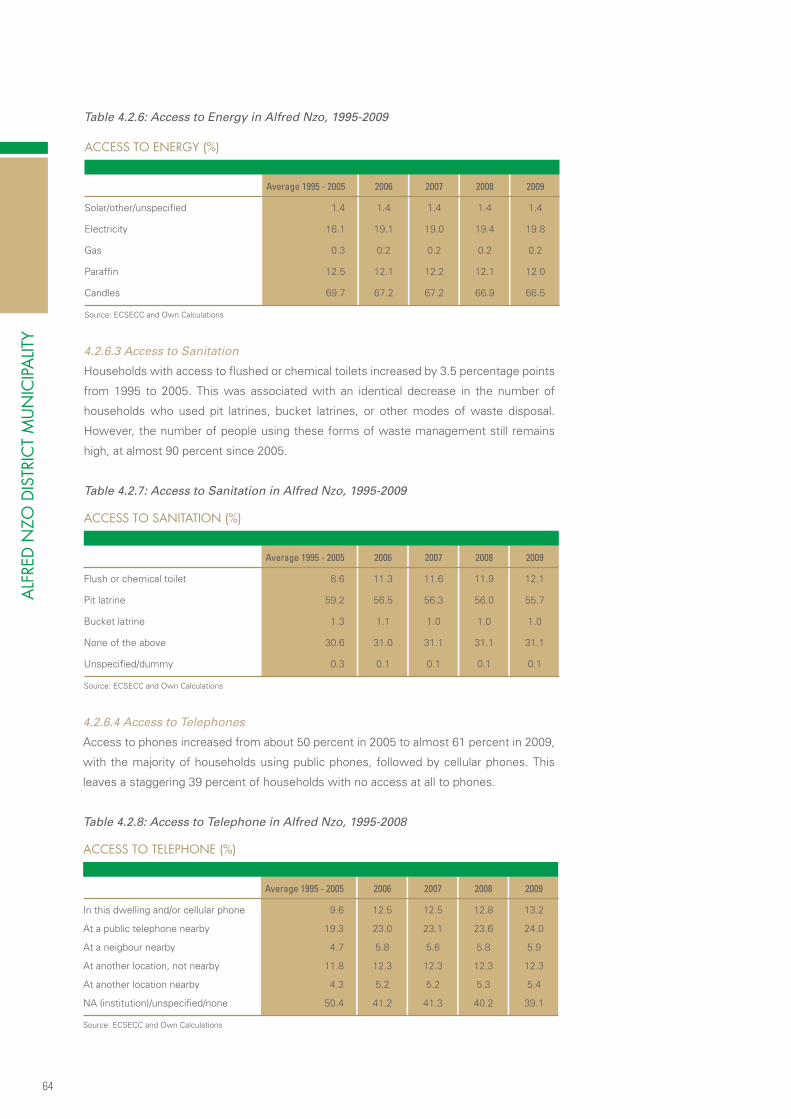

4.2.6.3 Access to Sanitation ..................................................................................................................... 64

4.2.6.4 Access to Telephones .................................................................................................................... 64

4.2.6.5 Access to Refuse ........................................................................................................................... 65

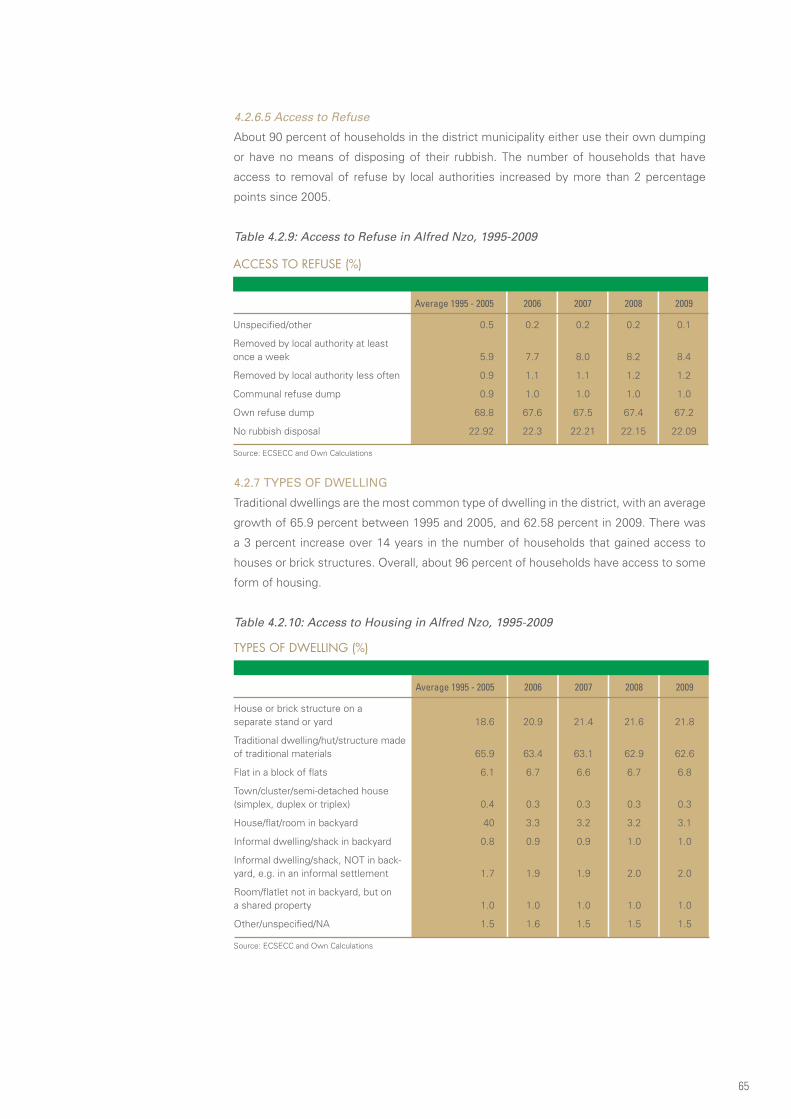

4.2.7 Types of Dwelling ............................................................................................................................. 65

4.2.8 Formal Employment by Sector .......................................................................................................... 66

4.2.9 Informal and Formal Employment by Skill ........................................................................................ 66

4.2.10 Dependency Ratio .......................................................................................................................... 67

4.2.11 Level of Education .......................................................................................................................... 67

4.2.12 Number of people in poverty .......................................................................................................... 68

4.2.13 Distribution of Households by Income ........................................................................................... 68

4.2.14 Human Development Indicator (HDI) .............................................................................................. 68

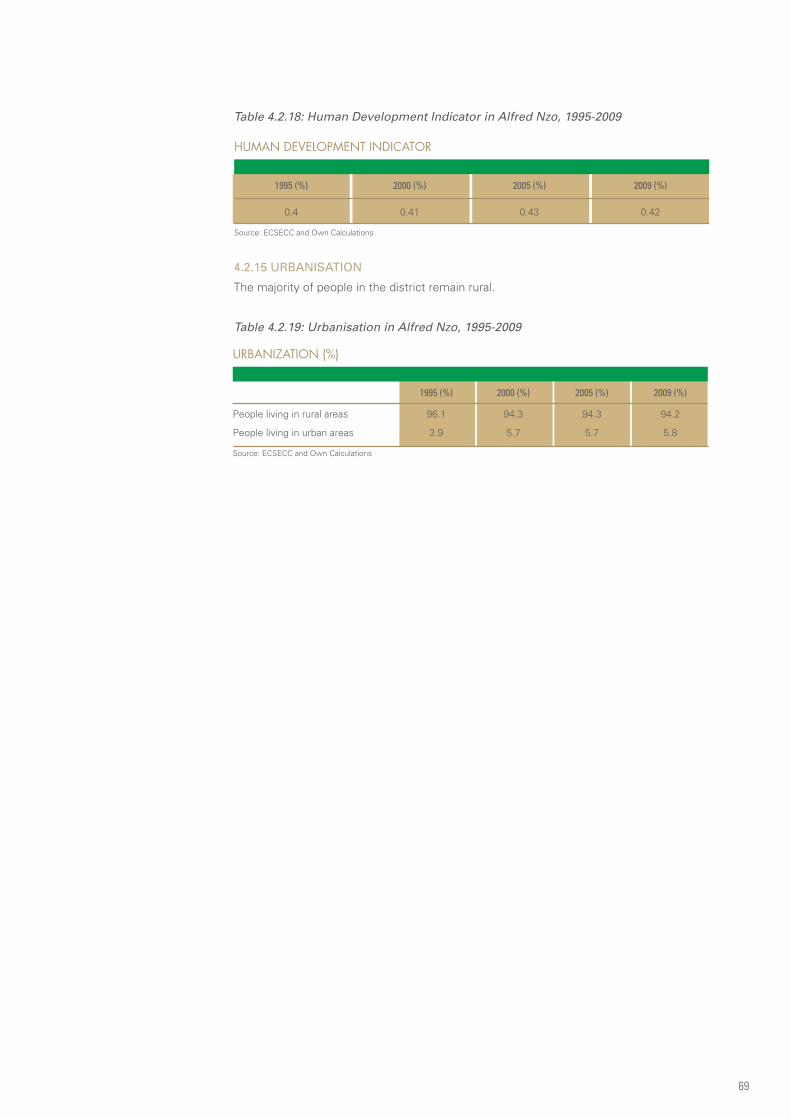

4.2.15 Urbanisation ................................................................................................................................... 69

4.3 Cacadu District Municipality .......................................................................................................... 70

4.3.1 Total Population by Age Group ......................................................................................................... 70

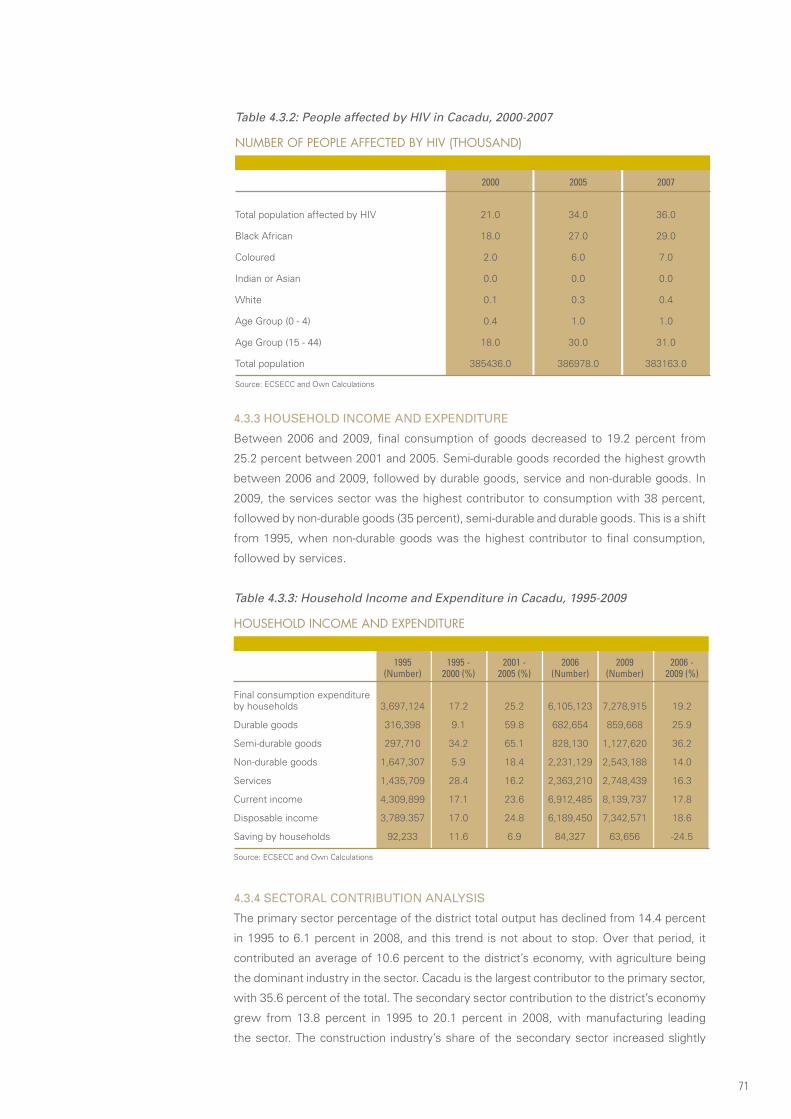

4.3.2 Total Population by Affected HIV ..................................................................................................... 70

4.3.3 Household income and expenditure ................................................................................................ 71

4.3.4 Sectoral Contribution Analysis ......................................................................................................... 71

4.3.5 Sectoral Growth Analysis ................................................................................................................. 72

4.3.6 Access to Services ........................................................................................................................... 73

4.3.6.1 Access to Water ............................................................................................................................ 73

4.3.6.2 Access to Energy ........................................................................................................................... 74

4.3.6.3 Access to Sanitation ..................................................................................................................... 74

4.3.6.4 Access to Telephones .................................................................................................................... 74

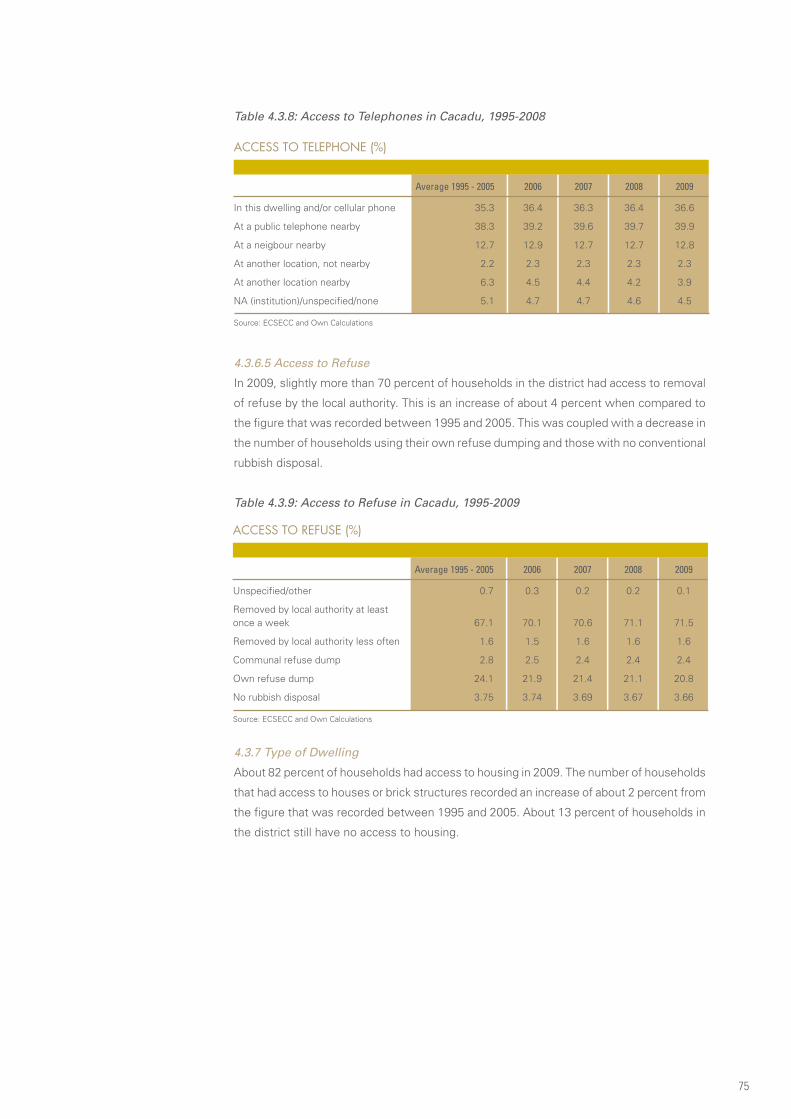

4.3.6.5 Access to Refuse ........................................................................................................................... 75

4.3.7 Type of Dwelling ............................................................................................................................... 75

4.3.8 Formal Employment by Sector .......................................................................................................... 76

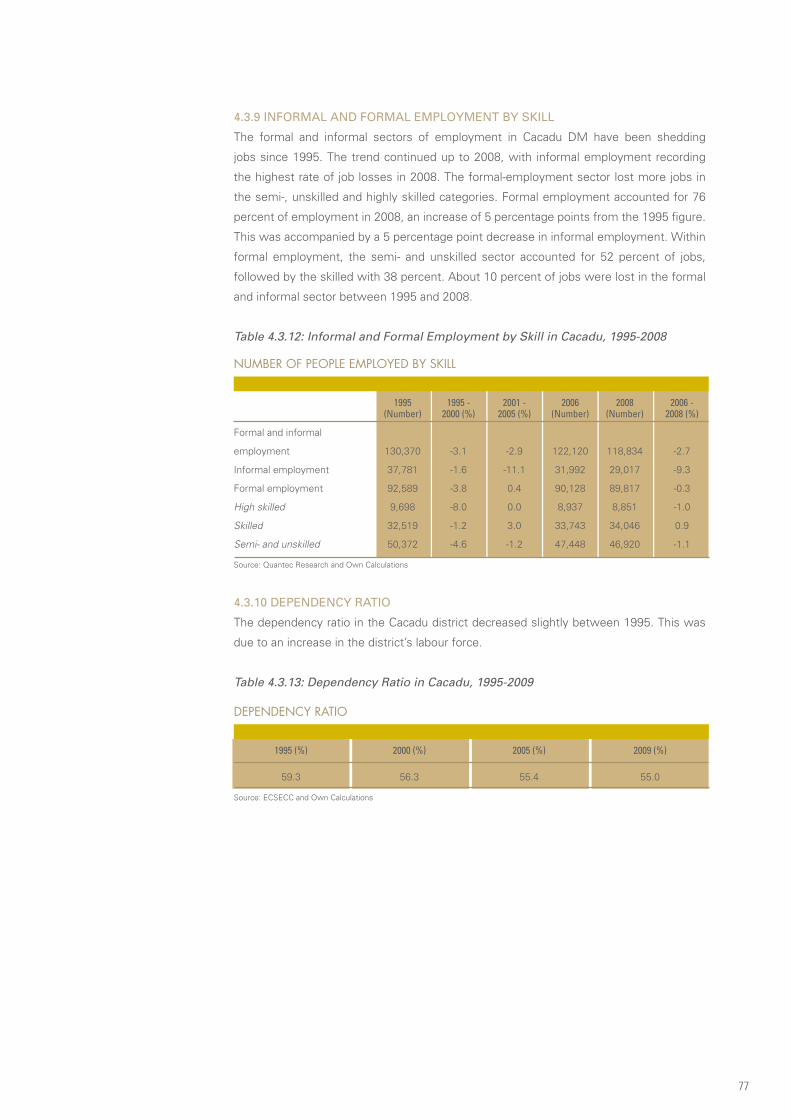

4.3.9 Informal and Formal Employment by Skill ........................................................................................ 77

4.3.10 Dependency Ratio .......................................................................................................................... 77

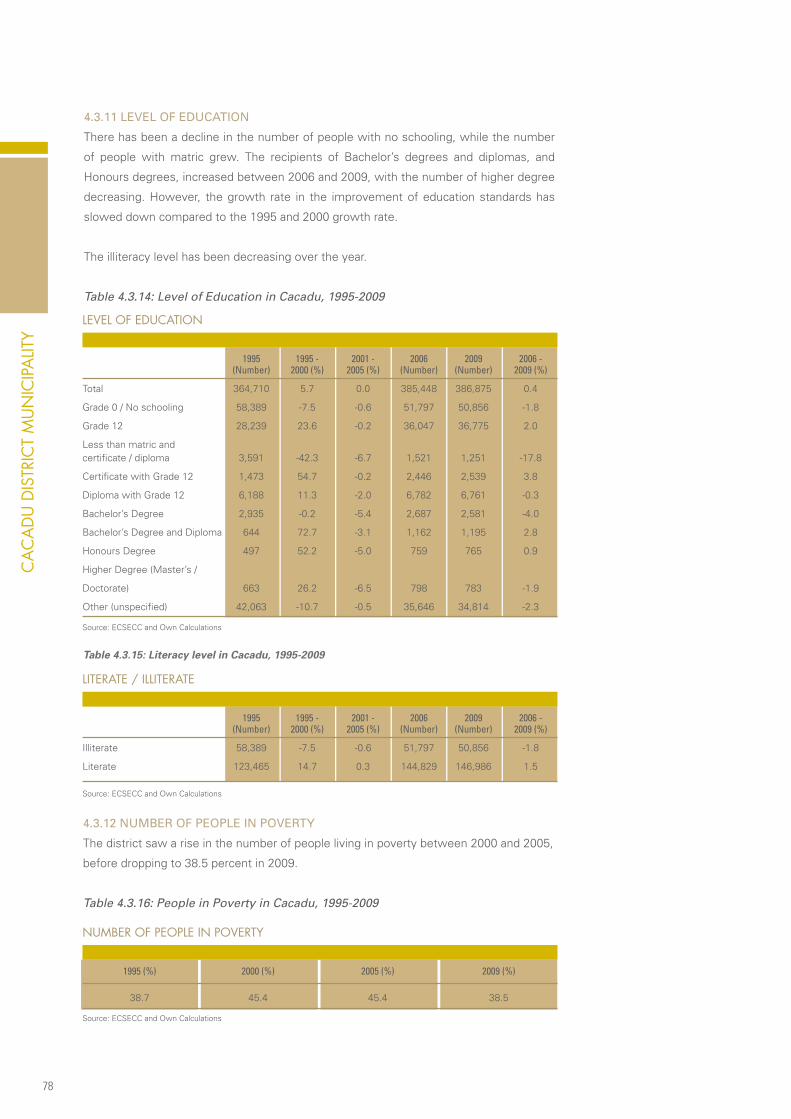

4.3.11 Level of Education .......................................................................................................................... 78

4.3.12 Number of People in Poverty ......................................................................................................... 78

4.3.13 Distribution of Households by Income ........................................................................................... 79

4.3.14 Human Development Indicator (HDI) .............................................................................................. 79

4.3.15 Urbanisation ................................................................................................................................... 79

4.4 Chris Hani District Municipality ..................................................................................................... 80

4.4.1 Total Population by Age Group ......................................................................................................... 80

4.4.2 Total Population Affected by HIV ..................................................................................................... 80

4.4.3 Household Income and Expenditure ................................................................................................. 81

4.4.4 Sectoral Contribution Analysis ......................................................................................................... 82

4.4.5 Sectoral Growth Analysis ................................................................................................................ 82

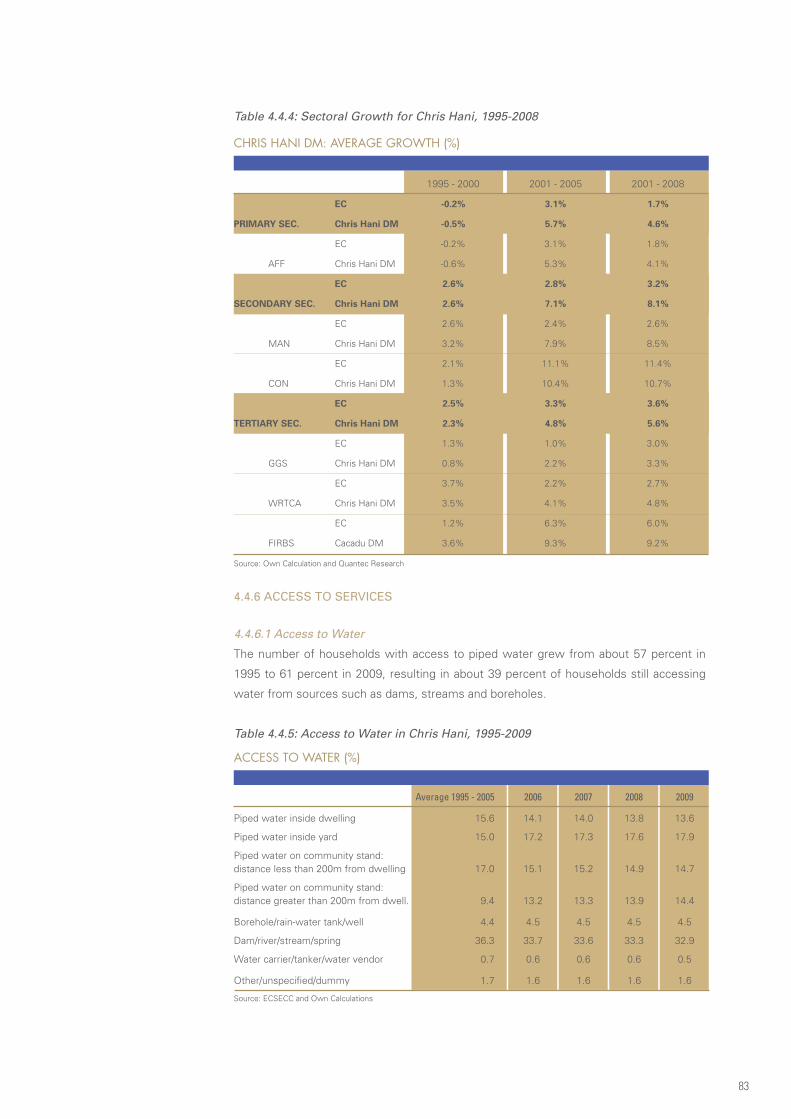

4.4.6 Access to Services ............................................................................................................................ 83

4.4.6.1 Access to Water ............................................................................................................................ 83

4.4.6.2 Access to Energy ........................................................................................................................... 84

4.4.6.3 Access to Sanitation ..................................................................................................................... 84

4.4.6.4 Access to Telephones .................................................................................................................... 84

4.4.6.5 Access to Refuse ........................................................................................................................... 85

4.4.7 Types of Dwelling ............................................................................................................................. 85

4.4.8 Formal Employment by Sector .......................................................................................................... 85

4.4.9 Informal and Formal Employment by Skill ........................................................................................ 86

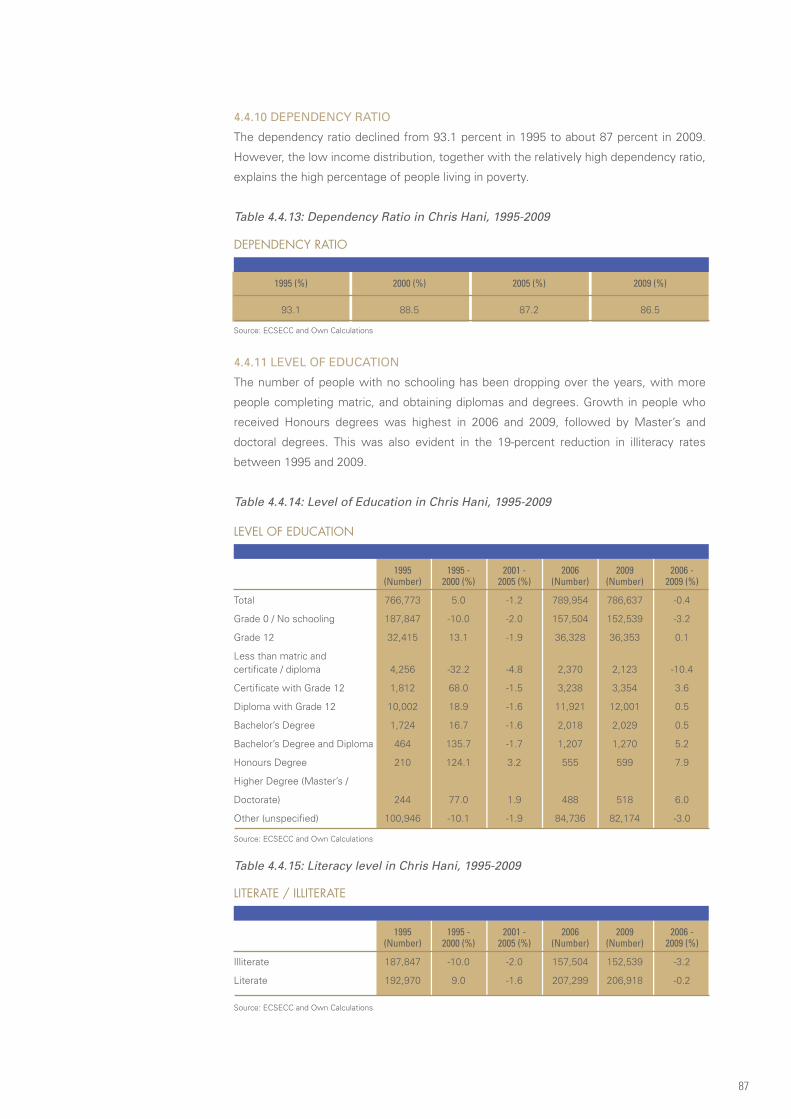

4.4.10 Dependency Ratio ........................................................................................................................... 87

4.4.11 Level of Education .......................................................................................................................... 87

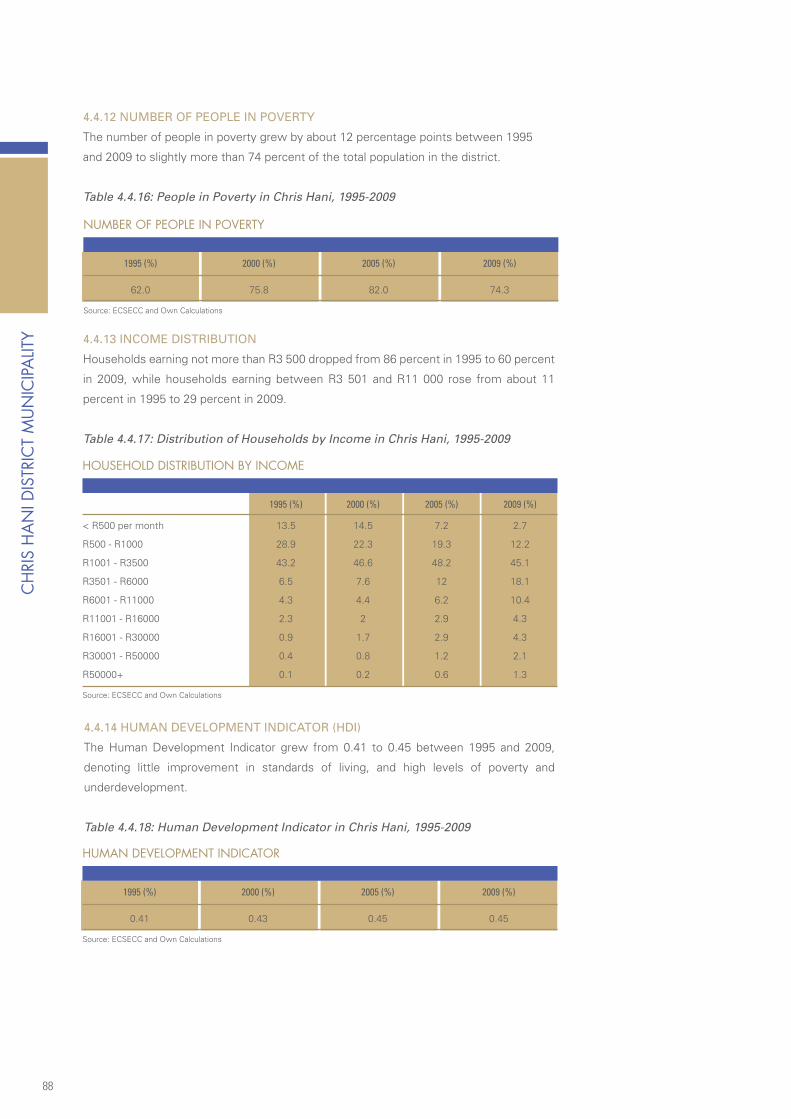

4.4.12 Number of People in Poverty .......................................................................................................... 88

4.4.13 Income Distribution ........................................................................................................................ 88

4.4.14 Human Development Indicator (HDI) .............................................................................................. 88

4.4.15 Urbanisation ................................................................................................................................... 89

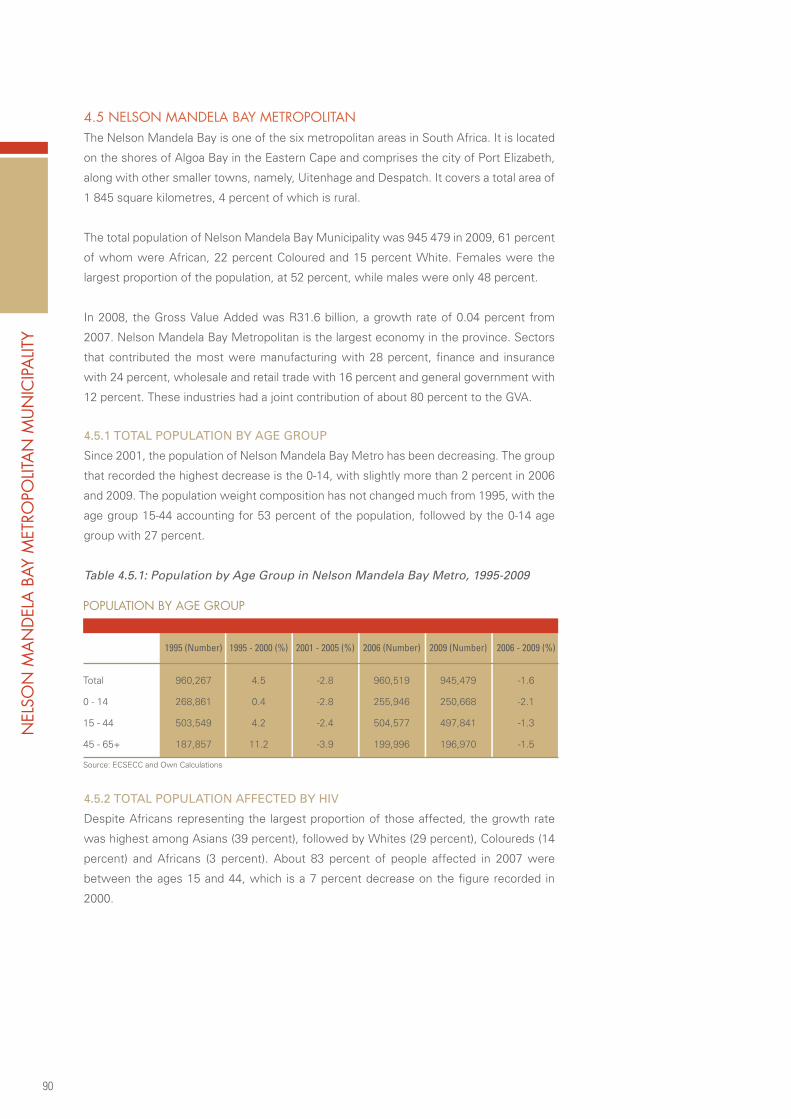

4.5 Nelson Mandela Bay Metropolitan ............................................................................................... 90

4.5.1 Total Population by Age Group ......................................................................................................... 90

4.5.2 Total Population Affected by HIV ..................................................................................................... 90

4.5.3 Household Income and Expenditure ................................................................................................. 91

4.5.4 Sectoral Contribution Analysis ......................................................................................................... 92

4.5.5 Sectoral Growth Analysis ................................................................................................................. 92

4.5.6 Access to services ............................................................................................................................ 94

4.5.6.1 Access to water ............................................................................................................................. 94

4.5.6.2 Access to Energy ........................................................................................................................... 94

4.5.6.3 Access to Sanitation...................................................................................................................... 94

4.5.6.4 Access to telephones .................................................................................................................... 95

4.5.6.5 Access to Refuse ........................................................................................................................... 95

4.5.7 Type of dwelling ............................................................................................................................... 96

4.5.8 Formal Employment by sector .......................................................................................................... 96

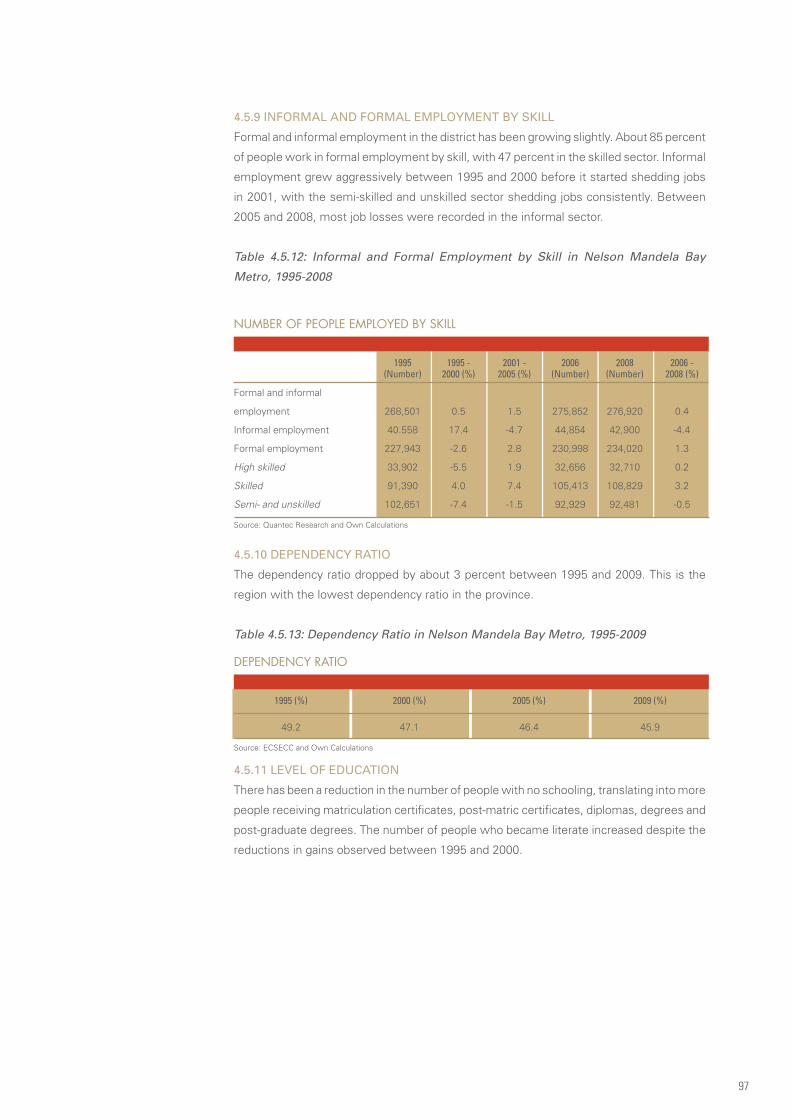

4.5.9 Informal and Formal Employment by skill ........................................................................................ 97

4.5.10 Dependency Ratio .......................................................................................................................... 97

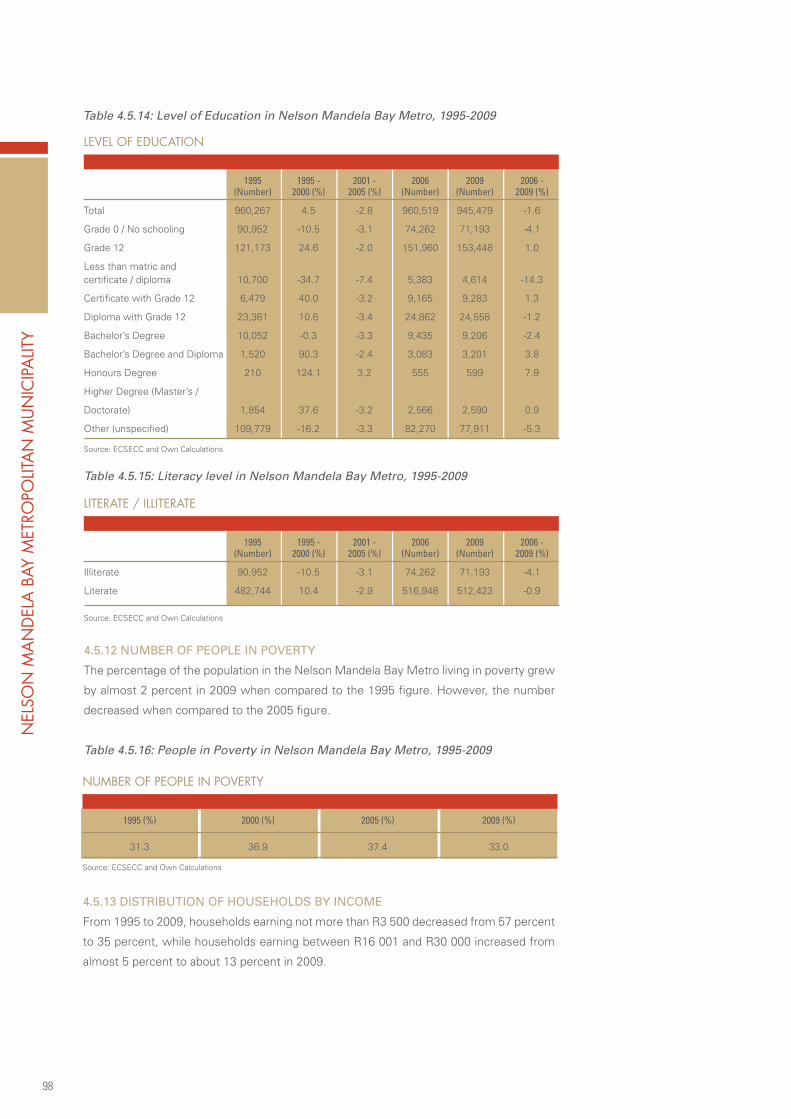

4.5.11 Level of Education .......................................................................................................................... 97

4.5.12 Number of People in Poverty .......................................................................................................... 98

4.5.13 Distribution of Households by Income ........................................................................................... 98

4.5.14 Human Development Indicator (HDI) ............................................................................................. 99

4.5.15 Urbanisation ................................................................................................................................... 99

4.6 O.R. Tambo District Municipality ................................................................................................... 100

4.6.1 Total Population by Age Group ........................................................................................................ 100

4.6.2 Total Population Affected by HIV ..................................................................................................... 100

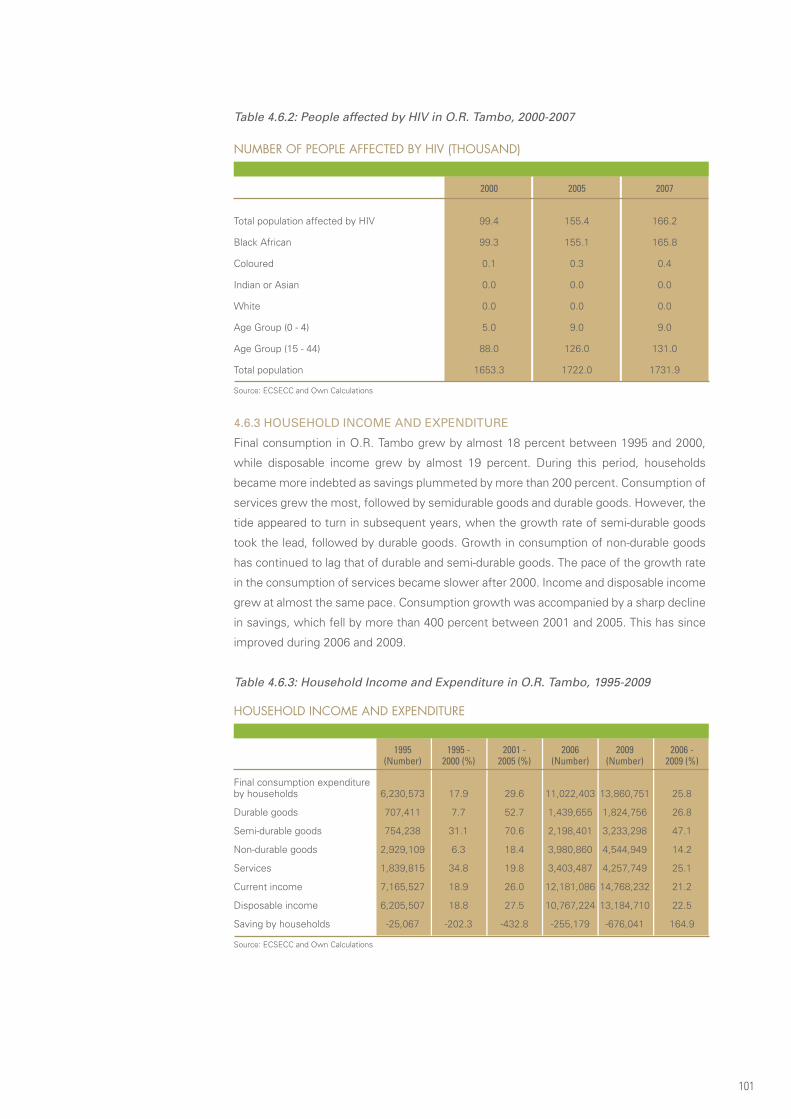

4.6.3 Household income and expenditure ................................................................................................ 101

4.6.4 Sectoral Contribution Analysis ........................................................................................................ 102

4.6.5 Sectoral Growth Analysis ................................................................................................................. 102

Tabl

E O

F C

On

TEn

Ts

4.6.6 Access to Services ............................................................................................................................ 103

4.6.6.1 Access to Water ............................................................................................................................. 103

4.6.6.2 Access to Energy ............................................................................................................................ 104

4.6.6.3 Access to Sanitation ...................................................................................................................... 104

4.6.6.4 Access to Telephones .................................................................................................................... 105

4.6.6.5 Access to Refuse ........................................................................................................................... 105

4.6.7 Types of dwelling .............................................................................................................................. 105

4.6.8 Formal Employment by sector .......................................................................................................... 106

4.6.9 Informal and Formal employment by skill ........................................................................................ 107

4.6.10 Dependency Ratio ........................................................................................................................... 107

4.6.11 Level of Education .......................................................................................................................... 108

4.6.12 Number of people in poverty .......................................................................................................... 109

4.6.13 Distribution of households by income ............................................................................................ 109

4.6.14 Human Development Indicator (HDI) .............................................................................................. 109

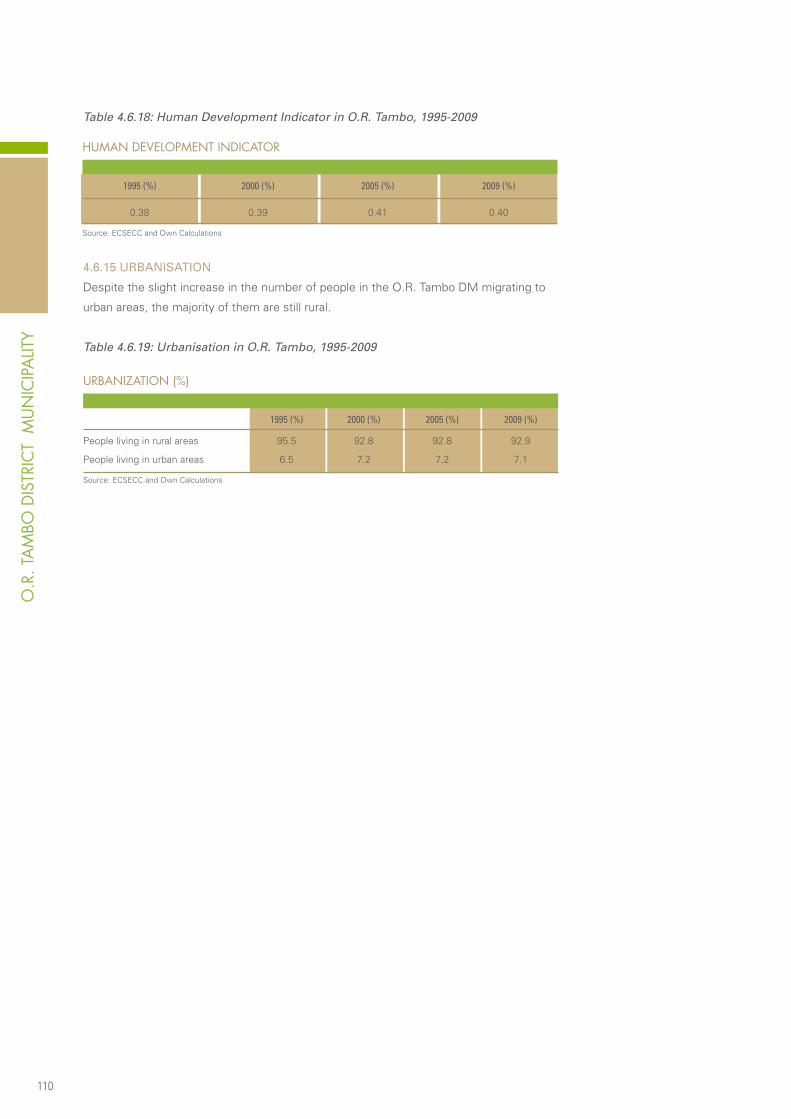

4.6.15 Urbanisation .................................................................................................................................... 110

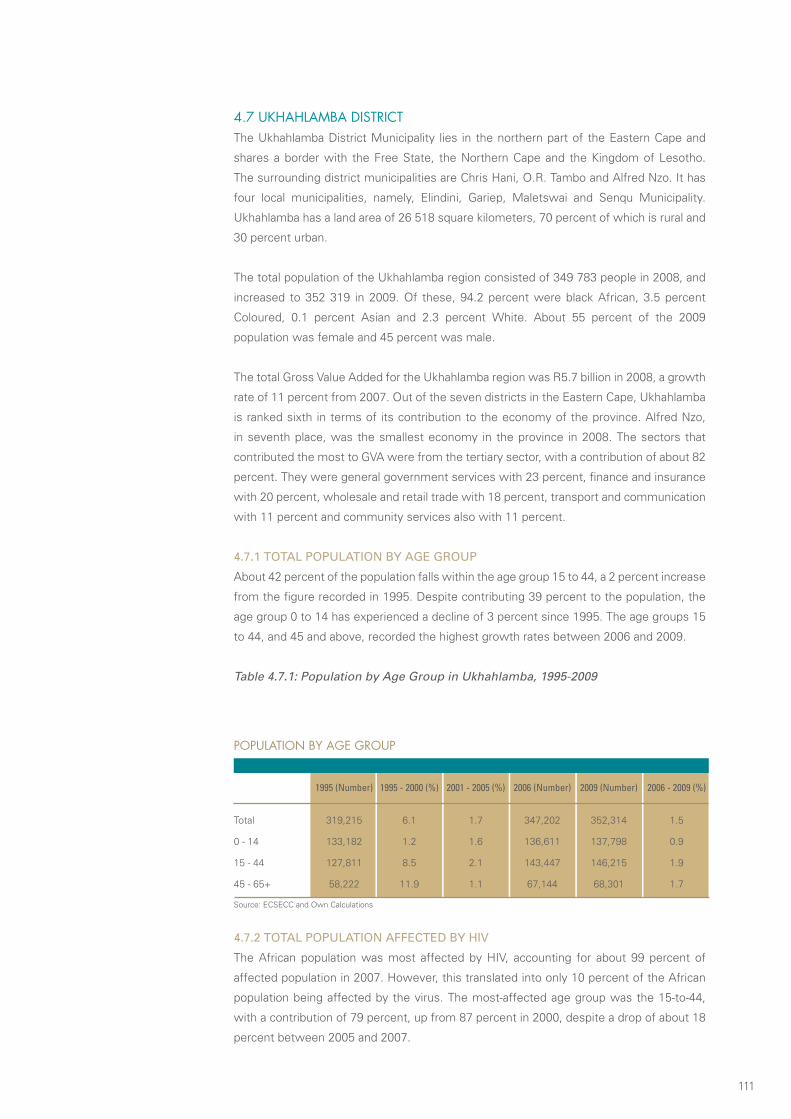

4.7 UKhahlamba District ........................................................................................................................ 111

4.7.1 Total Population by Age Group ......................................................................................................... 111

4.7.2 Total Population Affected by HIV ...................................................................................................... 111

4.7.3 Household Income and Expenditure ................................................................................................. 112

4.7.4 Sectoral Contribution Analysis ......................................................................................................... 112

4.7.5 Sectoral Growth Analysis ................................................................................................................. 113

4.7.6 Access to Services ............................................................................................................................ 114

4.7.6.1 Access to Water ............................................................................................................................ 114

4.7.6.2 Access to Energy ............................................................................................................................ 115

4.7.6.3 Access to Sanitation ...................................................................................................................... 115

4.7.6.4 Access to Telephones .................................................................................................................... 115

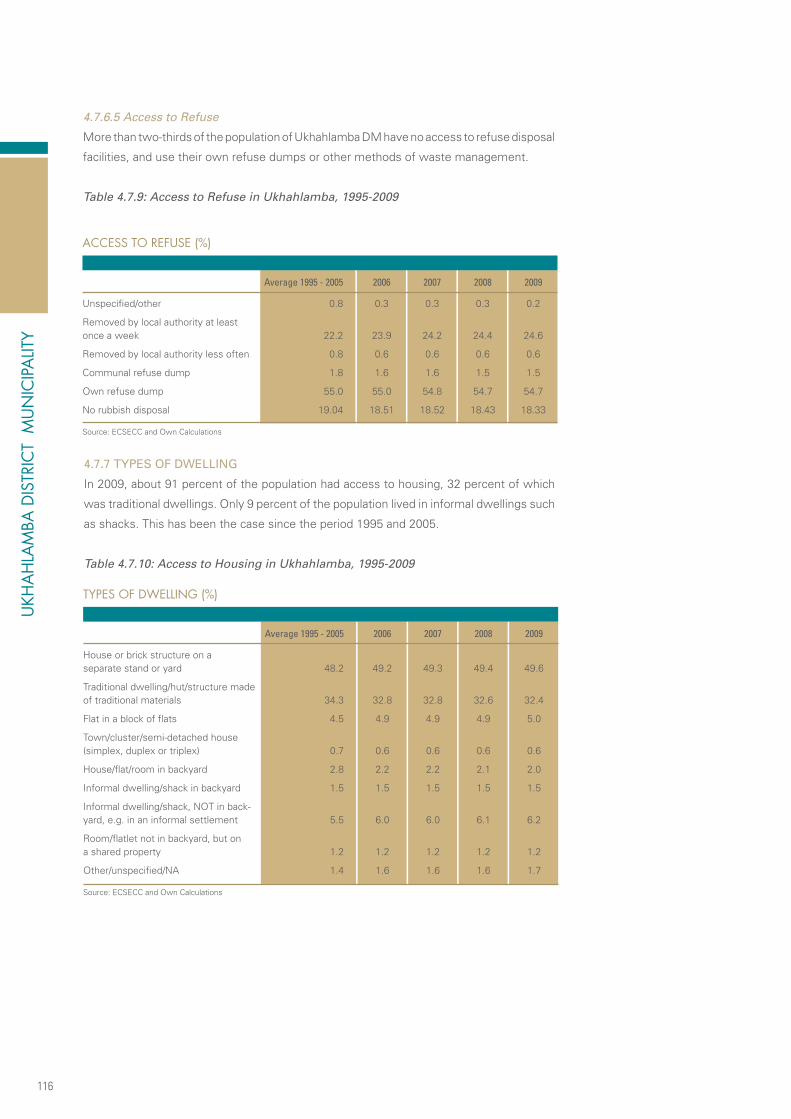

4.7.6.5 Access to Refuse ............................................................................................................................ 116

4.7.7 Types of Dwelling ............................................................................................................................. 116

4.7.8 Formal Employment by Sector .......................................................................................................... 117

4.7.9 Informal and Formal Employment by Skill ........................................................................................ 117

4.7.10 Dependency Ratio ........................................................................................................................... 118

4.7.11 Level of Education ........................................................................................................................... 118

4.7.12 Number of People in Poverty .......................................................................................................... 119

4.7.13 Distribution of Household by Income ............................................................................................. 119

4.7.14 Human Development Indicator ....................................................................................................... 119

4.7.15 Urbanisation .................................................................................................................................... 120

5 STRATEGIC IMPLICATIONS ................................................................................................................ 123

APPENDIX .................................................................................................................................................. 126

II

AFF Agriculture, Forestry and Fishing

AIDS Acquired Immune Deficiency Syndrome

COICOP Classification of Individual Consumption by Purpose

CON Construction

Cons. Consumption

CPI Consumer Price Index

CPIX Consumer Price Index Excluding Mortgage

CSPS Community, Social and Other Personal Services

DM District Municipality

Dur. Goods Durable Goods

EAP Economically Active Population

EC Eastern Cape

EGW Electricity, Gas and Water

EMEs Emerging Market Economies

Equip. Equipment

FCEH Final Consumption Expenditure by Household

FET Further Education and Training

FIBS Finance, Insurance and Business Services

GDP Gross Domestic Product

GDP_R Gross Domestic Product by Region

GGS General Government Services

GVA Gross Value Added

HDI Human Development Indicator

HIV Human Immune Virus

ILO International Labour Office

IMF International Monetary Fund

Inv. Investment

ITC International Trade Classification

MAN Manufacturing

MDG Millennium Development Goal

MPC Monetary Policy Committee

MQ Mining and Quarrying

NCA National Credit Act

Non-Dur. Goods Non-Durable Goods

OGSS Other General Government Services

PPI Producer Price Index

ABB

REVI

ATIO

NS

III

PPP Public-Private Partnerships

Priv. Private

Prop. Cons. Propensity to Consume

Prop. Sav. Propensity to Save

PSBR Public Sector Borrowing (Budget) Requirement

Pub. Public

Q-Q/Q-on-Q Quarter to Quarter / Quarter on Quarter

SA South Africa

SARB South African Reserve Bank

SEC Sector

Semi- Dur. Goods Semi-Durable Goods

Serv. Services

STATSSA Statistics South Africa

TSC Transport Storage and Communication

US United States

VCI Visual Condition Index

WRTCA Wholesale & Retail Trade, Catering and Accommodation

IV

TABl

ES

SEcTION 2Table 2.1: South African Gross Domestic Product, 2007-2013

Table 2.2: Final Consumption Expenditure by Household, 2008-2013

Table 2.3: Public Fixed Investment, 2008-2013

Table 2.4: Private Fixed Investment, 2008-2013

Table 2.5: Labour Market, 2007-2013

Table 2.6: Price Inflation, 2007-2013

Table 2.7: Monetary Sector and Exchange Rate, 2007-2013

Table 2.8: Public Finance, 2006/07-2011/12

SEcTION 3Table 3.1: Gross Domestic Product of the Eastern Cape, 2007-2013

Table 3.2: Total Gross Domestic Fixed Investment of the Eastern Cape, 2007-2013

Table 3.3: Machinery and Other Equipment Investment in the Eastern Cape, 2007-2013

Table 3.4: Building and Construction Investment in the Eastern Cape, 2007-2013

Table 3.5: Transport Equipment Investment in the Eastern Cape, 2007-2013

Table 3.6: Final Consumption Expenditure by Households in the Eastern Cape, 2007-2013

Table 3.7: Consumption of Durable Goods in the Eastern Cape, 2007-2013

Table 3.8: Consumption of Non-durable Goods in the Eastern Cape, 2007-2013

Table 3.9: Consumption of Semi-durable Goods in the Eastern Cape, 2007-2013

Table 3.10: Consumption of Services in the Eastern Cape, 2007-2013

Table 3.11: Consistent Major Export Contributors in the Eastern Cape, 1995-2008

Table 3.12: Consistent Major Import Contributors in the Eastern Cape, 1995-2009

Table 3.13: Eastern Cape Primary Sector Average Growth, 1995-2008

Table 3.14: Eastern Cape Secondary Sector Average Growth, 1995-2008

Table 3.15: Eastern Cape Tertiary Sector Average Growth, 1995-2008

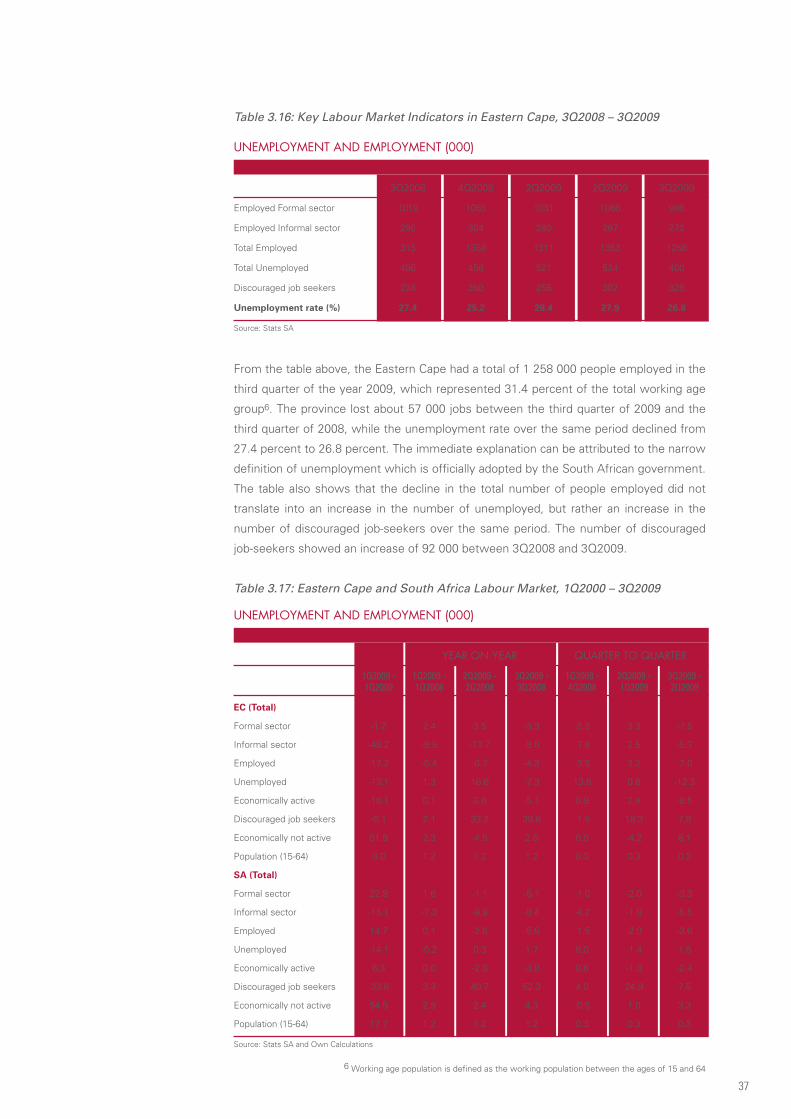

Table 3.16: Key Labour Market Indicators in Eastern Cape, 3Q2008 – 3Q2009

Table 3.17: Eastern Cape and South Africa Labour Market, 1Q2000 – 2Q2009

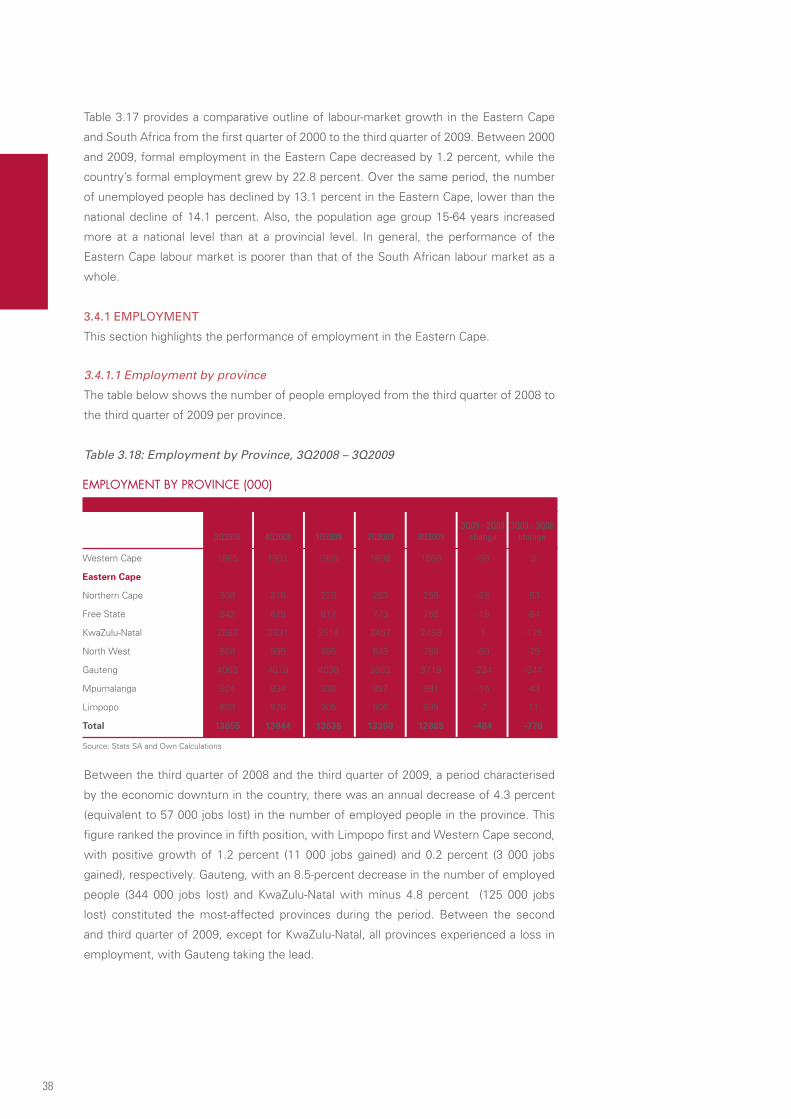

Table 3.18: Employment by Province, 3Q2008 – 3Q2009

Table 3.19: Formal Employment by Industry in Eastern Cape, 1Q2000 – 2Q2009

Table 3.20: Informal Employment by Industry in Eastern Cape, 1Q2000 – 2Q2009

Table 3.21: Employment by Occupation in the Eastern Cape, 2004-2008

Table 3.22: Unemployment Rate and Number by province, 3Q2008 – 3Q2009

Table 3.23: Labour Remuneration by Gender in Eastern Cape, 2008

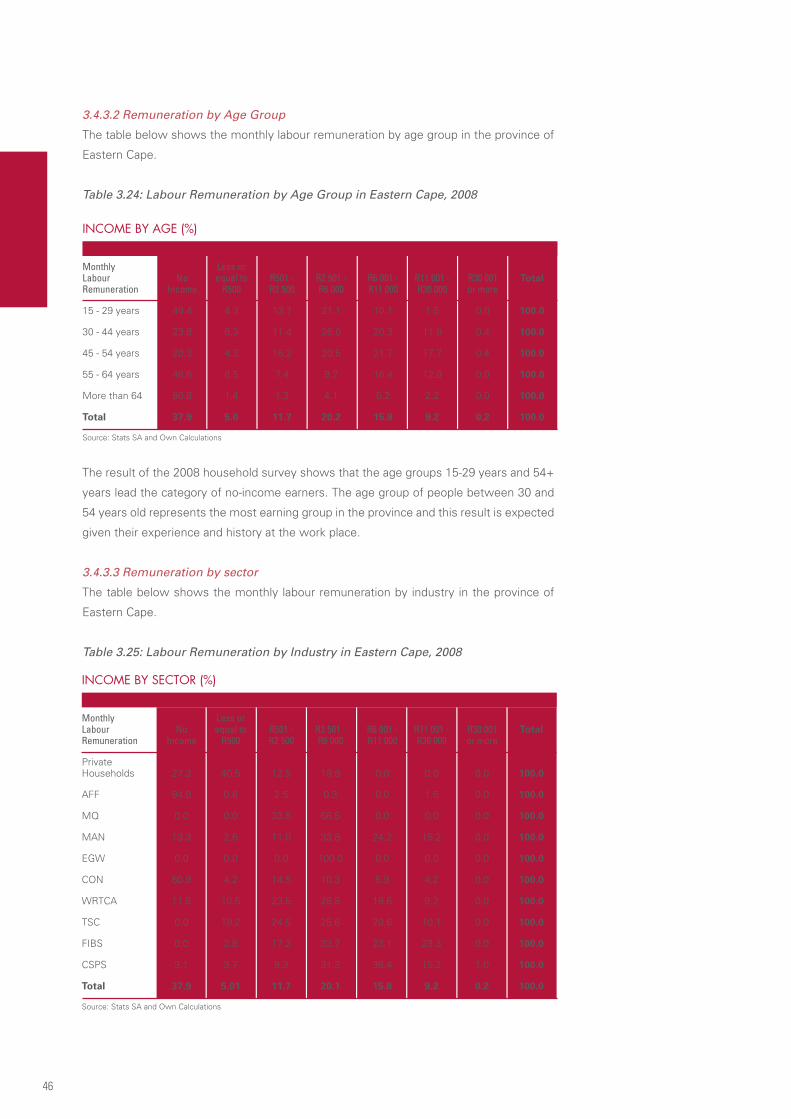

Table 3.24: Labour Remuneration by Age Group in Eastern Cape, 2008

Table 3.25: Labour Remuneration by Industry in Eastern Cape, 2008

SEcTION 4NB. The following tables are applicable to all district municipalities and the metropolitan.

Table: Population by Age Group, 1995-2009

Table: People affected by HIV, 2000-2007

Table: Household Income and Expenditure, 1995-2009

Table: Sectoral Growth, 1995-2008

Table: Access to Water, 1995-2009

Table: Access to Energy, 1995-2009

Table: Access to Sanitation, 1995-2009

Table: Access to Telephones, 1995-2008

V

Table: Access to Refuse, 1995-2009

Table: Access to Housing, 1995-2009

Table: Formal employment by sector, 1995-2008

Table: Informal and Formal Employment by Skill, 1995-2008

Table: Dependency Ratio, 1995-2009

Table: Level of Education, 1995-2009

Table: Literacy level, 1995-2009

Table: People in Poverty, 1995-2009

Table: Distribution of Households by Income, 1995-2009

Table: Human Development Indicator, 1995-2009

Table: Urbanisation, 1995-2009

SEcTION 1Figure 1: Conceptual Model of the Eastern Cape Economy

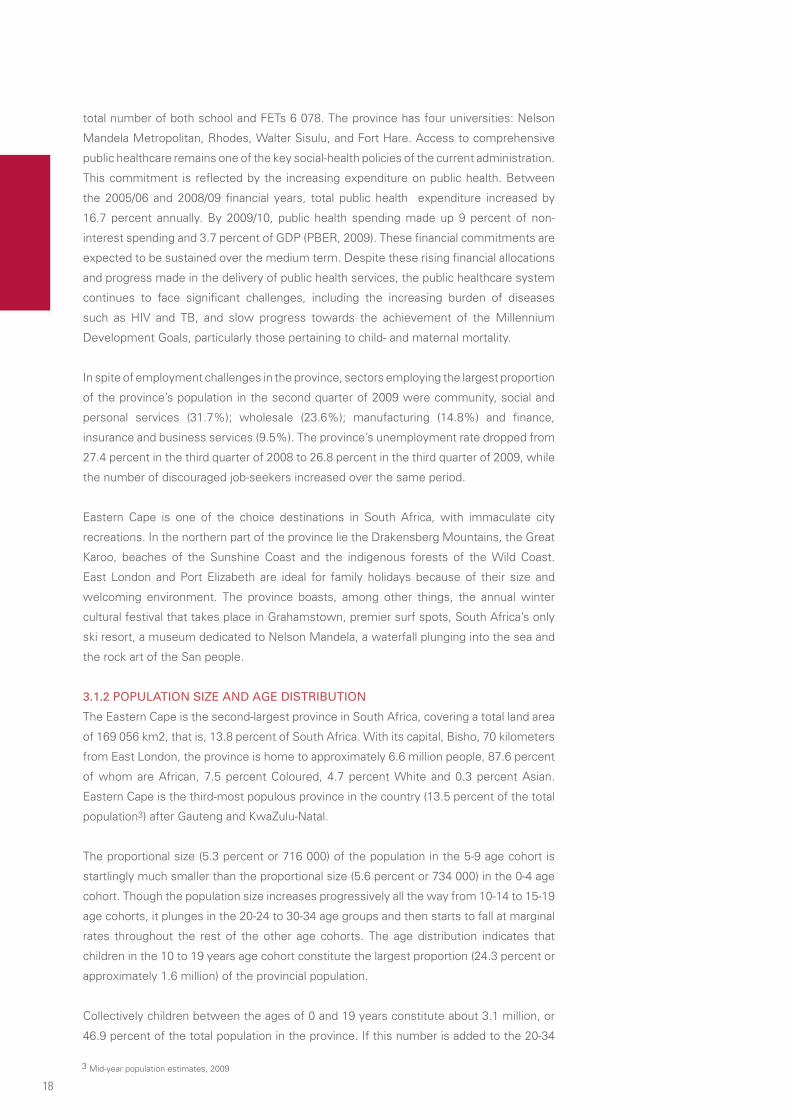

SEcTION 3Figure 3.1: Distribution of the Eastern Cape’s Population by Age and Gender, 2009

Figure 3.2: Gross Domestic Product of Eastern Cape

Figure 3.3: Growth Rate of Investment in the Eastern, 1996-2013

Figure 3.4: Household Consumption in the Eastern Cape, 1996-2013

Figure 3.5: Growth Rate of Consumption of Durable Goods -

Eastern Cape vs. S.A., 1996-2008

Figure 3.6: Growth Rate of Consumption of Non-durable Goods -

Eastern Cape vs. S.A., 1996-2008

Figure 3.7: Growth Rate of Consumption of Semi-durable Goods -

Eastern Cape vs. S.A., 1996-2008

Figure 3.8: Growth Rate of Consumption of Services - Eastern Cape vs. S.A.,

1996-2008

Figure 3.9: Propensity to Consume, Eastern Cape vs. S.A., 1995-2009

Figure 3.10: Propensity to Save Eastern Cape vs. S.A., 1995-2009

Figure 3.11: Balance of Trade of the Eastern Cape, 1995-2008

Figure 3.12: Industry Share of the Eastern Cape Output, 1995-2008

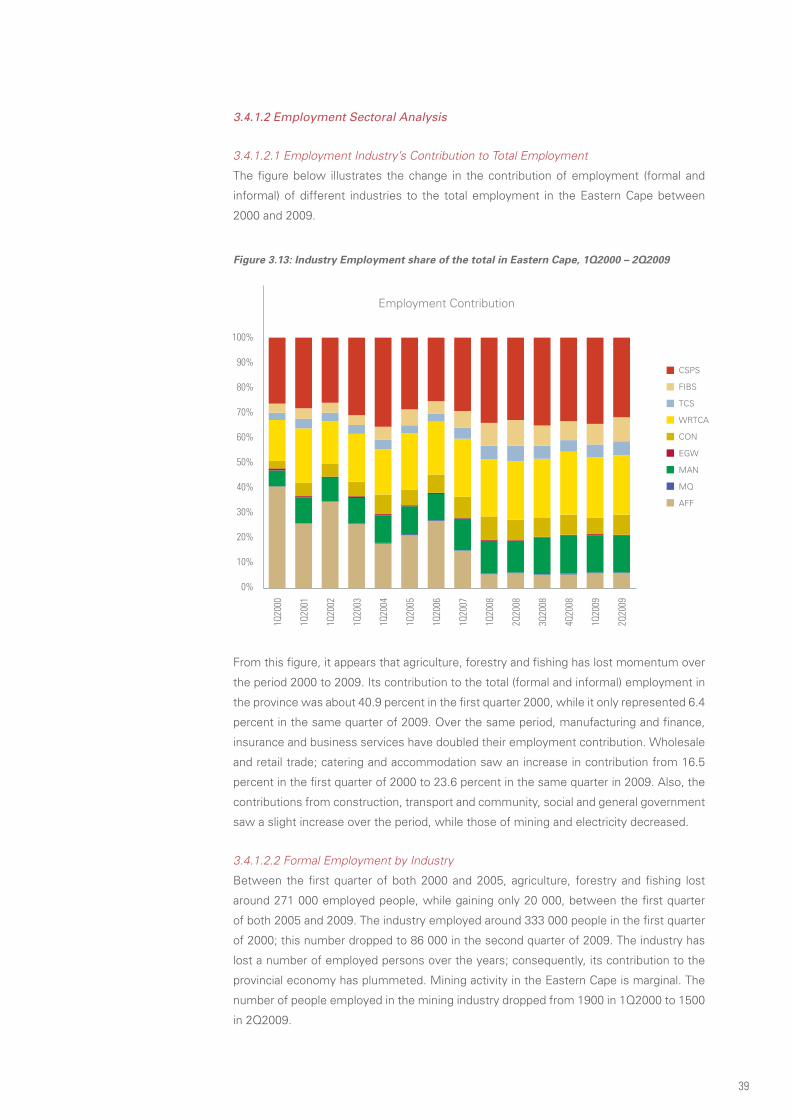

Figure 3.13: Industry Employment share of the total in Eastern Cape, 1Q2000 – 2Q2009

Figure 3.14: Composition of Employment by Skills

Figure 3.15: Labour Remuneration per Income Category in the Eastern Cape

1995 – 2009

SEcTION 4Figure 4.1: GVA Contribution for Amatole, 1995-2008

Figure 4.2: GVA Contribution for Alfred Nzo, 1995-2008

Figure 4.3: GVA Contribution for Cacadu, 1995-2008

Figure 4.4: GVA Contribution for Chris Hani, 1995-2008

Figure 4.5: GVA Contribution for Nelson Mandela, 1995-2008

Figure 4.6: GVA Contribution for O.R. Tambo, 1995-2008

Figure 4.7: GVA Contribution for Ukhahlamba, 1995-2008

FIG

URE

S

VI

Ac

KNO

WlE

DG

EMEN

TS

This publication was commissioned by the Honorable MEC Mcebisi Jonas, and

prepared by the CDC Research Unit under the overall guidance of Njabulo Sithebe.

Invaluable comments were received from Sybert Liebenberg, Ronney Ncwadi,

Phumla Ndaba, Pepi Silinga, Khwezi Tiya and Idriss Mouchili.

TEAMNjabulo Sithebe (Head: CDC Research Unit)

Senzeni Mtetwa (Senior Economist / Study Leader)

Semiyou Rafiou (Senior Economist / Study Leader)

Nonesi Golotile (Research Assistant)

Mawande Jiyana (Research Assistant)

Nomzamo Kolo (Research Assistant)

Unathi Lutshaba (Research Assistant)

Vukani Nkasa (Research Assistant)

Vuyokazi Tyida (Research Assistant)

VII

THE GlOBAl EcONOMYIn 2008, the growth of the world economy fell from 3.8 percent in 2007 to 2.2 percent.

At the beginning of the year 2009, the common expectation was that global growth

would slow further to reach the lowest rate since World War II. Global output and trade

plummeted in the last months of 2008 as the contagion set off by the United States (US)

financial crisis spread from the developed world to emerging economies.

The world economy has started to enter recovery due to high-frequency indicators

pointing to stronger growth in the second half of the year and global activity rising by

3 percent during the second quarter of 2009, from a 6.5 percent contraction in the first

quarter. However, employment continues to drop, household wealth continues to decline

and consumer demand continues to go down owing to the high rate of bankruptcies

in companies. Worldwide, disruption in the provision of credit has curtailed household

spending and business investment.

THE SOUTH AFRIcAN EcONOMYIn the mid 2000s, South Africa experienced unprecedented levels of growth which were

underpinned by favorable external conditions coupled with strong domestic demand and

rapid credit extension. These conducive conditions raised growth to 5 percent on average

in 2004 to 2007 and lowered the rate of unemployment by approximately 5 percentage

points, while strengthening public finances and maintaining single-digit inflation, and

improving external reserves.

Despite these positive results yielded by prudent economic policies, South Africa still

faces a number of medium-term challenges. The country’s output growth has remained

lower than in many Emerging Market Economies (EMEs), even during the economic

expansion. Strong employment growth over the same period failed to bring down a very

high unemployment rate of over 23 percent despite the lower labor-force participation

compared to other emerging economies. Another challenge that plagued South Africa

was increasing income inequality, which is still among the highest in the world.

Output and demand remain weak in spite of the slow recovery in the economy. In the

fourth quarter of 2008, output contracted by 1.8 percent quarter-on-quarter (Q-on-Q)

and by more than 6.7 percent in the first quarter of 2009. The annual output for 2009 is

expected to contract further by about 2 percent, with a slow recovery towards the end of

the year. It would not be until 2011 before output starts to show strong signs of recovery,

when it is expected to tread at about 3.8 percent before climbing to about 4.2 percent in

2012 and 4.5 percent in 2013. While the projected growth may be disappointing in light of

the experience of the mid-2000s, it is still encouraging given the severity of the external

shocks.

THE EASTERN cAPE EcONOMYThe Eastern Cape output is expected to remain fragile in spite of the slow recovery in the

economy. The outlook shows that by 2010, the Eastern Cape Province would again start

seeing positive growth as global recovery and consumption levels improve to those last

seen before the financial crisis. The province’s output would start showing relative strong

signs of recovery by 2011, when it is expected to tread at about 3.5 percent before rising

ExEc

UTI

VE S

UM

MA

RY

VIII

ExEc

UTI

VE S

UM

MA

RY

to about 3.9 percent in 2012 and 4.2 percent in 2013.

Growth in fixed investment spending contracted in 2009, registering an annual growth

rate of 2.04 percent from 12.44 percent in 2007. Nevertheless, while the growth rates

in investment in assets remain relatively strong, the trend is clearly declining. While

total fixed investment spending for 2009 is likely to disappoint, forecasts pronounce a

rebound in 2011, 2012 and 2013 due to government’s investment plan. In line with the

total investment in the Eastern Cape, machinery and other equipment would contract in

2009 and bounce back from 2010 onwards due to the global economic recovery and rising

investment confidence.

Building and construction was the second-largest contributor to the total gross domestic

fixed investment in the Eastern Cape for the past 14 years. In 2009/10, a decline is

expected as most construction projects would be completed for the 2010 World Cup.

Given the rural development priorities of national government, investment in building and

construction is expected to start showing signs of improvement from 2011 and pick up

further in 2012 before declining slightly in 2013.

The average annual contribution of transport equipment to the total gross domestic fixed

investment was about 14 percent between 1995 and 2008. In 1996, this sector of fixed

investment observed negative growth of about minus 2 percent associated with the first

South African currency crisis, before an all-time low of approximately minus 27 percent

in 1999 from 11 percent growth the previous year. This sector proves susceptible to both

domestic and international macroeconomic shocks. Projections show that investment in

transport equipment would improve from 2009 onwards, with robust growth rates from

2010 to 2013.

The Eastern Cape is ranked fourth in terms of consumption expenditure after KwaZulu-

Natal. The total spending growth in the province declined from 8.9 percent in 2006 to 8.6

percent in 2007, before plummeting to 0.9 percent in 2008 and is expected to contract by

0.7 percent in 2009. Final consumption is expected to start improving from 2010, given

the easing in monetary policy and the improving economic climate.

STRATEGIc INITIATIVESThe Eastern Cape Province faces a number of challenges such as underdevelopment,

high unemployment, high dependency ratios, high poverty levels, and a skewed economic

structure. This is a province which is more than 60 percent rural and yet is driven by

the tertiary sector, with a total contribution of more than 70 percent to the economy

– a serious anomaly. There is a dire need to reconfigure the structure of the provincial

economy. The starting point in this undertaking is to consider the natural comparative

advantage of the province such as land endowment and favourable climatic conditions.

The province needs to revive its primary sector and invest in market-oriented agricultural

infrastructure. This includes infrastructure that supports on-farm production (irrigation,

energy, transportation, pre- and post-harvest storage), ensures efficient trading and

exchange (telecommunications, covered markets), adds value to the domestic economy

(agro-processing and packaging facilities), and enables produce to move rapidly and

efficiently from farmgate to processing facilities, and on to wholesalers (transportation

and bulk storage).

IX

NB. All figures are at constant 2000 prices

NATIONAl

SOUTH AFRIcAN GROSS DOMESTIc PRODUcT FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) 5.1 3.1 -2.0 2.0 3.8 4.2 4.5

GDP* (Rm) 1,233,930 1,271,717 1,246,111 1,270,787 1,319,577 1,375,619 1,437,222

FINAl cONSUMPTION ExPENDITURE BY HOUSEHOlD FOREcASTS

2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) -2.2 2.3 3.8 4.2 4.5

FCEH* (Rm) 864,346 845,330 864,773 897,633 935,335 977,426

PUBlIc FIxED INVESTMENT FOREcASTS

2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) 7.1 5.7 7.5 7.8 -0.1

Gross Fixed Pub. Inv.* (Rm) 95,379 102,182 108,017 116,123 125,181 125,038

PRIVATE FIxED INVESTMENT FOREcASTS

2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) 1.3 1.3 3.8 5.6 5.2

Gross Fixed Priv. Inv.* (Rm) 189,416 191,902 194,430 201,896 213,221 224,206

PRIcE (ANNUAl PERcENTAGE cHANGE)

FOREcASTS

2007 2008 2009 2010 2011 2012 2013

CPI inflation (annual average) 7.1 11.5 7.1 5.9 5.1 4.4 4.5

GDP deflator 9 10.8 7.5 8.6 7.1 6 5.9

PPI (annual average) 10.9 14.3 1.4 5.3 5.8 5.6 5.5

MONETARY SEcTOR AND ExcHANGE RATE FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Repo Rate (year-end %) 11 11.5 7 8.5 7 7 7

USD / ZAR (annual average) 7.06 8.25 8.62 8.26 8.58 9 9.44

EUR / ZAR (annual average) 9.66 12.13 11.7 11.5 12.15 13.12 13.5

lABOUR MARKET (ANNUAl PERcENTAGE cHANGE)

FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Population Growth Rate 1.1 1.1 1.07 1.04 1.04 1.05 1.05

Unemployment Growth Rate 22.7 21.9 24.9 24.3 23.4 22.1 20.7

Employment Growth Rate 0 10.2 1.1 0.4 1.4 1.8 1.8

Nominal Unit Labour Cost 4.2 11.5 9.2 8.6 5.3 5.2 5.1(excluding agriculture sectors)

Labour Productivity 2.4 1.1 0.6 0.9 2.3 2.3 2.5 (excluding agriculture sectors)

FORE

cA

STS

X

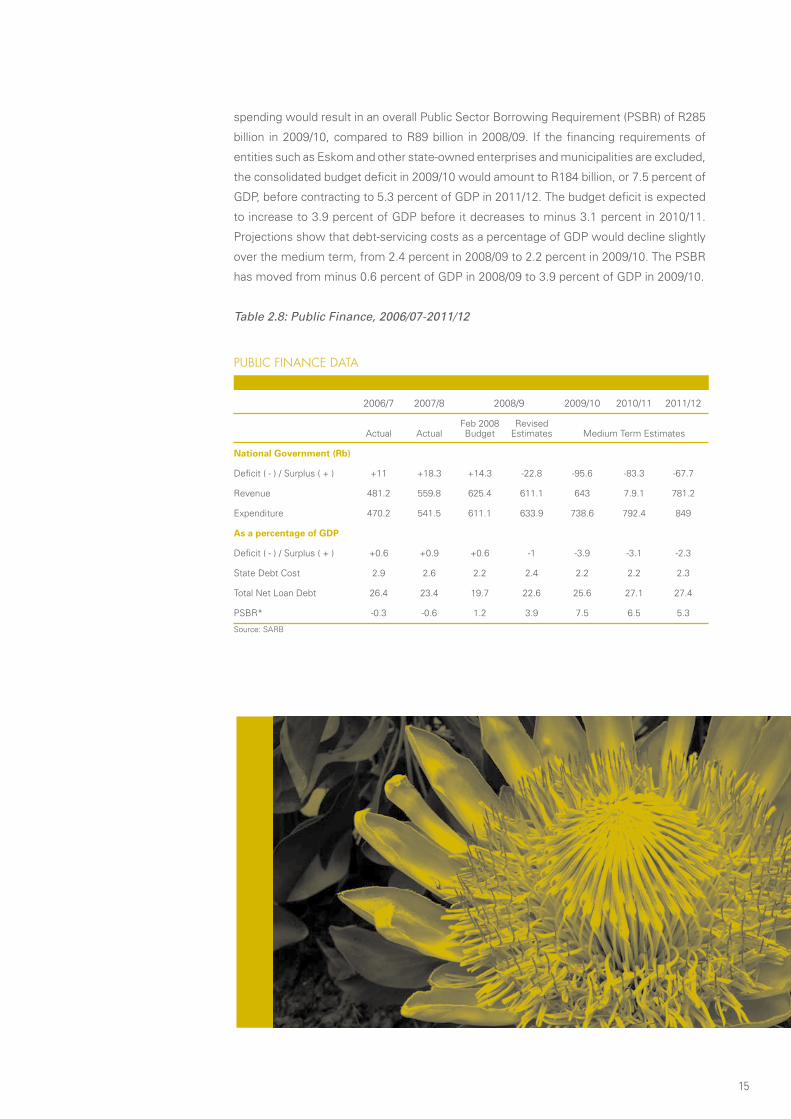

PUBlIc FINANcE DATA FOREcASTS

2006/7 2007/8 2008/9 2009/10 2010/11 2011/12

Feb 2008 Revised Actual Actual Budget Estimates Medium Term Estimates

National Government (Rb)

Deficit ( - ) / Surplus ( + ) 11 18.3 14.3 -22.8 -95.6 -83.3 -67.7

Revenue 481.2 559.8 625.4 611.1 643 7.9.1 781.2

Expenditure 470.2 541.5 611.1 633.9 738.6 792.4 849

As a percentage of GDP

Deficit ( - ) / Surplus ( + ) 0.6 0.9 0.6 -1 -3.9 -3.1 -2.3

State Debt Cost 2.9 2.6 2.2 2.4 2.2 2.2 2.3

Total Net Loan Debt 26.4 23.4 19.7 22.6 25.6 27.1 27.4

PSBR* -0.3 -0.6 1.2 3.9 7.5 6.5 5.3

FORE

cA

STS

EASTERN cAPE

GDP_R FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) 2.7 -2.4 1.6 3.5 3.9 4.2

GDP_R* (Rm) 96,704 99,269 96,922 98,499 101,954 105,973 110,424

GROSS DOMESTIc FIxED INVESTMENT (GDFI) FOREcASTS

2007 2008 2009 2010 2011 2012 2013

GDFI Growth Rate (%) 7.3 2.7 2 8.1 9.4 7.3

GDFI share of GDP (%) 19.2 20 21.1 21.1 22.1 23.3 24

GDFI (Rm) 18,521 19,879 20,408 20,825 22,521 24,646 26,453

GROSS DOMESTIc FIxED INVESTMENT: MAcHINERY AND OTHER EqUIPMENT FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) 10 -0.2 7.6 10.8 9.7 10

Machinery and Other Equipment (Rm) 7,418 8,157 8,137 8,852 9,696 10,637 11,696

GROSS DOMESTIc FIxED INVESTMENT: BUIlDING AND cONSTRUcTION FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) 11.4 3 -0.9 0.6 8.3 7.6

Buildings and Construction Works (Rm) 7,670 8,545 8,797 8,721 8,774 9,505 10,231

GROSS DOMESTIc FIxED INVESTMENT: TRANSPORT EqUIPMENT FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) -3.9 1.8 3.8 10.3 11.3 9.2

Transport Equipment (Rm) 2,910 2,796 2,847 2,955 3,260 3,629 3,962

XI

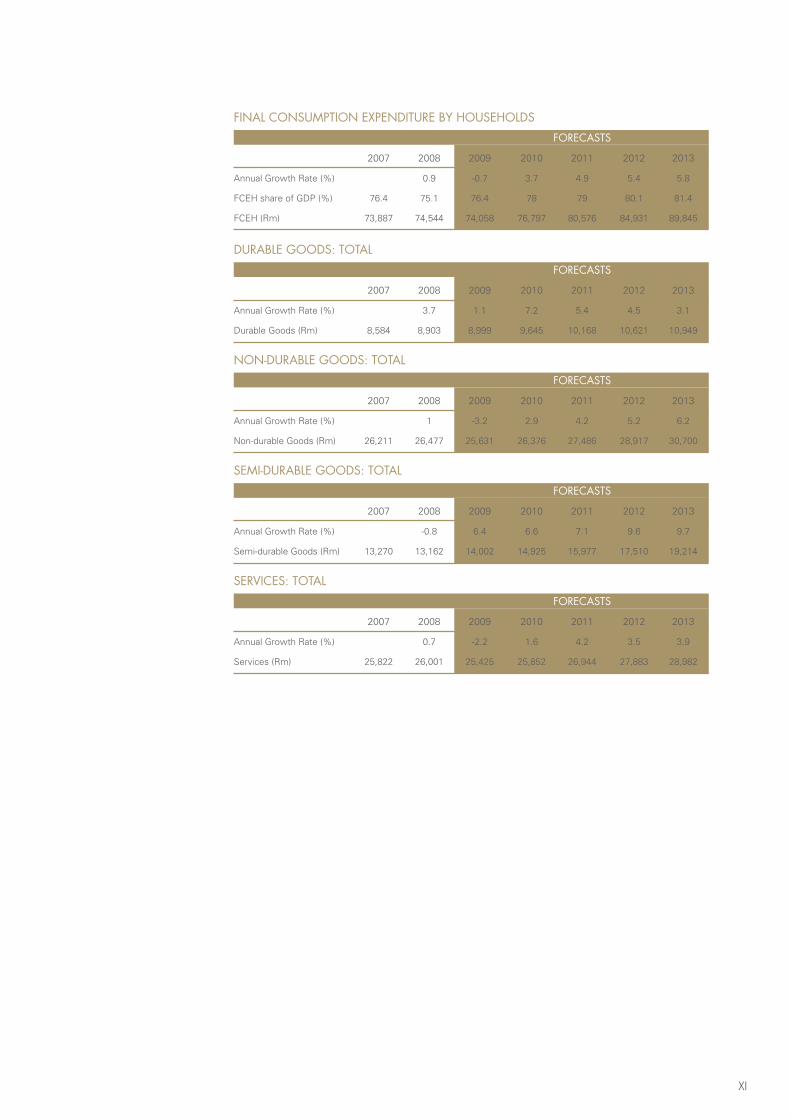

FINAl cONSUMPTION ExPENDITURE BY HOUSEHOlDS FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) 0.9 -0.7 3.7 4.9 5.4 5.8

FCEH share of GDP (%) 76.4 75.1 76.4 78 79 80.1 81.4

FCEH (Rm) 73,887 74,544 74,058 76,797 80,576 84,931 89,845

DURABlE GOODS: TOTAl FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) 3.7 1.1 7.2 5.4 4.5 3.1

Durable Goods (Rm) 8,584 8,903 8,999 9,645 10,168 10,621 10,949

NON-DURABlE GOODS: TOTAl FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) 1 -3.2 2.9 4.2 5.2 6.2

Non-durable Goods (Rm) 26,211 26,477 25,631 26,376 27,486 28,917 30,700

SEMI-DURABlE GOODS: TOTAl FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) -0.8 6.4 6.6 7.1 9.6 9.7

Semi-durable Goods (Rm) 13,270 13,162 14,002 14,925 15,977 17,510 19,214

SERVIcES: TOTAl FOREcASTS

2007 2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) 0.7 -2.2 1.6 4.2 3.5 3.9

Services (Rm) 25,822 26,001 25,425 25,852 26,944 27,883 28,982

1

1 GLOBAL ECONOMIC OUTLOOK AND FORECAST METHODOLOGY

1.1 GLOBAL ECONOMIC OUTLOOKThe economic data showed that in 2008, the growth of the world economy fell from 3.8

percent in 2007 to 2.2 percent. At the beginning of the year 2009, the common expectation

was that global growth would slow further this year to reach the lowest rate since World

War II. Global output and trade plummeted in the last months of 2008 as the contagion set

off by the United States (US) financial crisis spread from the developed world to emerging

economies.

According to the October 2009 World Economic Outlook, the world economy has started

to enter recovery due to high-frequency indicators pointing to stronger growth in the

second half of the year and global activity rising by 3 percent during the second quarter of

2009 from a 6.5 percent contraction in the first quarter. However, employment continues

to drop, household wealth continues to decline and consumer demand continues to go

down owing to the high rate of bankruptcy in companies. Worldwide, disruption in the

provision of credit has curtailed household spending and business investment.

1.1.1 USA

The US economy is forecast to contract by 2.75 percent in 2009 due to the sharp

contraction during the first half of the year. As 2009 progressed, output data confirms that

the U.S. economy is stabilising owing to the result of the monetary, financial and fiscal

policy interventions which helped stabilise consumer spending, the housing default rate

and financial markets. Despite these positive upshots, business investment continues to

sink, the savings rate is still climbing and the markets remain stressed.

These events will collectively depress investment and consumption. Intertwining these

occurrences with the impact of rising unemployment, it is apparent that growth will remain

lethargic, reaching 1.5 percent for the entire year of 2010. The short-lived nature of the

fiscal stimulus and subdued growth in tradingpartnereconomies also play a considerable

role in depressing growth further. A number of developments, including the rise of more

than 10 percent in the level of unemployment in the second half of 2010 and a core

inflation of below 1 percent through the greater part of the year, are expected.

2

There is great uncertainty around the near-term outlook for the economy, which

is underpinned by the scale of shocks and the hazy outlook for the rest of the world.

However, the strong policy response and a rapid recovery in emerging markets could

reverse the uncertainty that has plagued the U.S. economy, leading to a healthy rise

in confidence, improving financial conditions and promoting strong aggregate demand

growth. Although the economic turmoil is easing, downside risks still remain a concern.

In particular, continued cutting down on household debt, also known as deleveraging,

and rising unemployment, may have serious ramifications on consumption than initially

forecast. Also, accelerating corporate and commercial property defaults could delay the

improvement in financial conditions.

The medium-term outlook sees potential growth likely to fall below 2 percent for a

considerable time. History tells that previous financial crises are followed by large

permanent output losses relative to precrisis trends due to the nature of impaired financial

systems, which generally take time to heal. In return, this slows down investment and

innovation. High cyclical unemployment could also raise structural unemployment. On the

demand side, although the personal saving rate has already climbed to about 5 percent, it

may have to rise further given the need to rebuild the balance sheets of households.

The fiscal legacy of the crisis is a high and rising debt trajectory that could become

unsustainable without significant medium-term measures. Such financial crises give birth

to high and rising debt trails that also pose the risk of being unsustainable if no adequate

medium-term measures are put in place.

Forecasts show that deficits will be around 10 percent of gross domestic product

(GDP) for the period 2009/10 and 2010/11. However, it’s not all gloom and doom; the

economic climate shows that these deficits will gradually decline to levels below 10

percent afterwards, while the level of gross government debt will continue rising swiftly,

reaching 108.2 percent of GDP by 2014 from 84.8 percent of GDP in 20091. In light of

the impending healthcare and pension pressures brought about by aging population,

this is bad news for the US economy. These pressures are made more transparent by

the current budget proposal, which augments medium-term forecasts by using growth

assumptions that tend to be optimistic. Adjustments may become a necessity to ensure

long-term fiscal sustainability, particularly on the revenue side, considering that non-

defence optional spending is approaching historical lows. The critical state of the U.S.

healthcare system cannot be ignored. It is plagued by inefficiencies, as proven by the fact

that similar healthcare results are achieved at different costs across the U.S. states. This

necessitates that coverage be expanded in a budget-neutral manner, and that measures

to curb the rate of cost growth be put in place to help preserve debt sustainability.

1.1.2 JAPAN

Japan’s ongoing dependence on exports is the primary cause of the abrupt impact of the

global downturn on its economy. As the worldwide credit crunch pinched off external

demand, export of goods and services plunged by 35 percent in December 2008 from

the previous year. Industrial output fell by 9.4 percent in December following a decrease

of 8.5 percent in November. Industries which were particularly hit are transport (including

automotive), machinery and electrical-equipment manufacturing.

1 IMF World Economic Outlook, October 2009

3

Firmly entrenched in recession territory last year, Japan’s economy returned to growth

(2.3 percent) in the second quarter of 2009 after a range of fiscal stimulus measures by

the government. On average, Japan’s economy is expected to shrink by 5.4 percent in real

terms in 2009, with sluggish growth of 1.7 percent in 2010. Inflation will remain negative

until 2012, given the significant slack in the economy.

1.1.3 CHINA

China’s economic growth rate would slow in 2009. GDP growth fell to 6.8 percent in the

fourth quarter of 2008, down from 9 percent in the third quarter. Growth is forecast to

chug along at 8.5 percent in 2009 and 9.0 percent in 2010. While this appears positively

robust compared to the rest of the world, it is less than the strong 13-percent rate the

country achieved in 2007. Exports to the West have slowed, but a number of other factors

have contributed to China’s economic deceleration. The housing construction industry has

come to a virtual standstill as a result of the government’s efforts to deflate a potential

real-estate bubble. The government has introduced a number of fiscal stimulus measures,

such as transportation investment (which is expected to be expanded by 70 percent in

2009), public housing spending, rebates on purchases of consumer goods and additional

healthcare. The inflation rate is expected to be around an annual average of minus 0.1 in

2009 and 0.6 percent in 2010. The current-account surplus would remain substantial, but

is likely to fall to 7.8 percent of GDP in 2009 and rise to 8.6 percent in 2010.

1.1.4 INDIA

India’s economy is expected to slow in 2009. After dropping from a growth rate of 9.4

percent in 2007 to 7.3 percent in 2008, 2009 is expected to post gains of only 5.4 percent,

while the growth rate for the coming year is expected to be about 6.4 percent. India

continues to face inflationary pressures from high resource utilisation and strong credit

growth. The inflation rate jumped from 6.4 percent in 2007 to 8.3 percent in 2008, and is

expected to reach 8.7 percent in 2009 before decreasing slightly to around 8.4 percent in

2010. The country’s current-account balance stood at minus 2.2 percent of GDP in 2008. It

is expected to be flat in 2009 and drop to minus 2.5 percent of GDP in 2010. In an attempt

to boost liquidity, the government has eased restrictions on lending in the property sector

and increased the availability of export credit finance.

In summary, the risks associated with growth are steadily becoming domesticated. Most

of the improvement in activity is still owed to measures that could turn out to be short-

lived, such as the rebounding capital markets, adjustment in inventory, and expansionary

fiscal and monetary policy. The risk that these factors bring is a recovery that will not be

self-sustaining unless activity spreads to other regions. On the positive side, the policy

stimulus in China could shore up recoveries in other parts of Asia.

The greatest challenge that still lies ahead is the timing of the withdrawal of policy support.

Two questions that would need careful consideration are when and how to withdraw

policy support while ensuring a successful transition to more balanced, medium-term

growth. The dependence of Asia on export demand has resulted in the global imbalances

that have made the region susceptible to developments in demand. This in turn would

force the growth composition to be driven by internal demand as global demand proves

unlikely to pick up in the short-term.

4

1.1.5 MAJOR EUROPEAN UNION MEMBER STATES

The economies of the European Union (EU) were in deep recession at the beginning of the

year, and are currently showing signs of slow recovery. In 2007, when the financial crisis

was surging through the United States and Britain, the EU was enjoying comparatively

faster growth and lower unemployment. All of this changed in late 2008, when the credit

crunch stormed Europe’s shores just when businesses and consumers needed access

to credit to tide them over the tough times. Also, the economy was hit by high energy

prices, an overvalued currency and a sharp fall in domestic demand from the EU’s trading

partners. The EU GDP contracted less than expected in the second quarter of 2009.

Countries like France and Germany showed positive growth, while GDP in the United

Kingdom contracted less than expected.

After expanding by an estimated 1.2 percent in 2008, the German economy is forecast to

decline by 5.3 percent in 2009 before rebounding to 0.3 percent in 2010. During the crisis,

the German government introduced a series of fiscal stimulus packages to boost growth

and stimulate consumption. Consumer price inflation is expected to fall from its 2008 level

of 2.8 percent to 0.1 percent in 2009 and 0.2 percent in 2010. Also, the unemployment

rate is expected to rise from 8 percent in 2009 to 10.7 percent in 2010.

The economy of the United Kingdom, after stalling in 2008 with a growth rate of 0.7

percent, is expected to contract by 4.4 percent in 2009 before rebounding to 1.7 percent in

2010. Squeezed by the credit crunch and falling consumer demand, businesses have shed

inventories, halted investment and shed staff. Consumer spending has been bolstered

by falling energy prices and declining mortgage rates. However, rising unemployment

and an increase in precautionary saving would exert downward pressure on household

expenditure. Inflation stood at 3.6 percent in 2008 but would fall to an average of 1.9

percent in 2009 and 1.5 percent in 2010. The unemployment rate is estimated to rise from

7.6 percent in 2009 to 9.3 percent in 2010.

The economy of France is expected to decline to minus 2.4 percent in 2009, from a

growth rate of 0.3 percent in 2008. A gradual recovery is expected to take root in 2010

with 0.9 percent positive growth, but it would depend on the stabilisation of financial

markets and a resurgence of global activity. The recent growth observed is the fruit of

the French government’s plans to alleviate the impact of the slowdown through stimulus

measures in the form of higher public investment, the shoring-up of corporate liquidity and

support for unemployed and low-paid workers. France’s unemployment rate is expected

to rise from 9.5 percent in 2009 to 10.3 percent in 2010. Consumer-price inflation is also

expected to increase from 0.3 percent in 2009 to 1.1 percent in 2010.

1.1.6 BRAZIL

Brazil’s economy is forecast to decline significantly in 2009, compared with the 5.1 percent

growth pace of 2008. It is expected to be around minus 0.7 percent before entering positive

territory once again, with an expected growth rate of around 3.5 percent in 2010. The

Brazilian economy is expected to pick up faster than the rest of South America because

of its large domestic market, high degree of integration into the world and diversification

of its export market. Also, inflation is expected to slow down from 4.8 percent in 2009 to

4.1 on average in 2010. However, the current-account deficit is expected to increase from

minus 1.3 in 2009 to minus 1.9 in 2010.

5

1.2 THE THEORETICAL FRAMEWORK OF THE SOUTH AFRICAN MACRO-MODELThe model used is a Keynesian demand-side model, and was built to provide a theoretical

structure for understanding the linkages between key macro-economic variables. The

following four sectors of the South African economy are modelled:

The real sector, including the external sector, estimates private consumption and •

investment, total government expenditure, and exports and imports to determine an

aggregate demand function for the economy;

The monetary sector deals with the estimation of the main monetary variables, •

namely the broad monetary aggregate;

The price-sector estimates equations, which try to capture the influencing factors on •

the domestic price level; and

The labour sector could not be estimated because of the poor quality of available •

data.

The starting point for specifying the real sector of a comprehensive macro-econometric

model for any economy is the national identity from the national accounts. The national

identity, or aggregate demand for domestic consumption, is the sum of consumption,

investment, government expenditure and the trade balance:

Y = C + I + G + (X - M)

where,

Y is the real GDP; C is the final consumption expenditure by household; I is the real

private investment expenditure and G is the real government expenditure. X denotes real

exports and M real imports. Additional equations provide links between these demand-

side equations. These linking equations would include the consumer-price index and the

producer-price index; the GDP deflator (measuring the general price level in the economy);

various Rand exchange rates; interest rates; and employment and the associated wages.

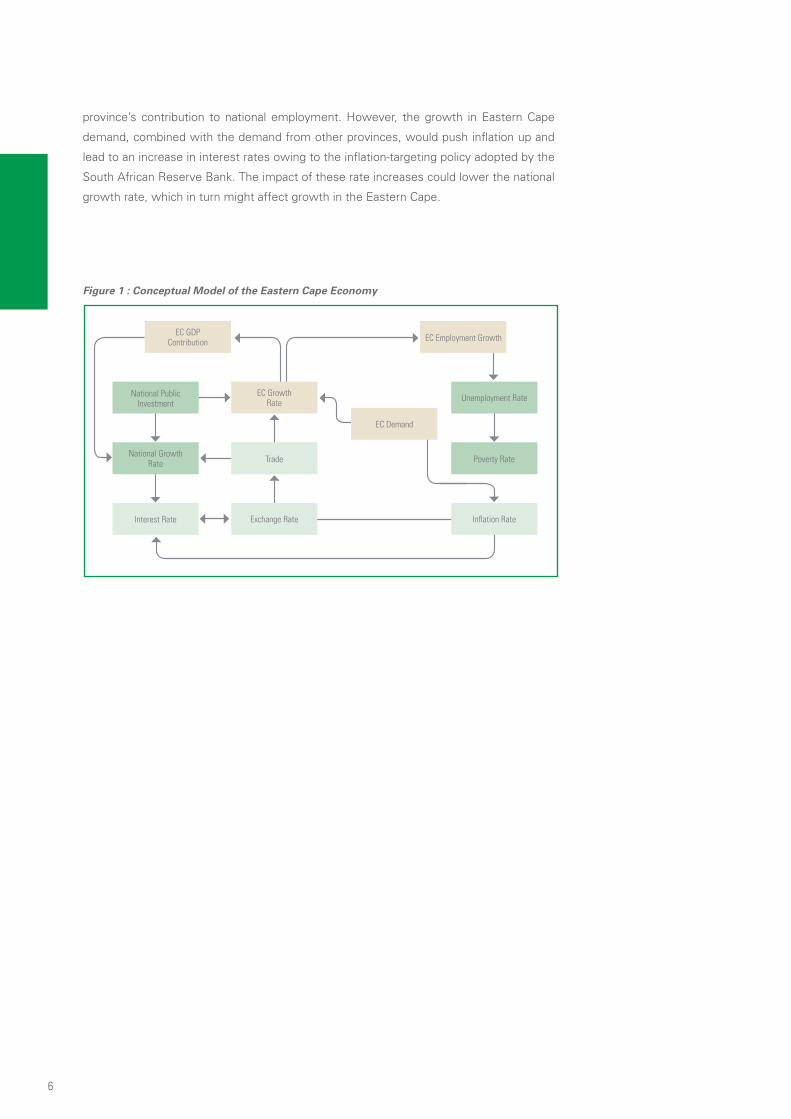

1.3 EASTERN CAPE MODEL CONCEPTUALISATIONThe Eastern Cape economy is not modelled explicitly due to data constraints, but is

inferred from the core target variables generated by the national macro-economic model.

The signs between the variables specify the nature of the expected relationship between

those variables, with the direction of the arrow representing the direction of causality

among variables.

The simple conceptualised model is structured taking into account that the province is part

of the national economy. For this reason, any national developments regarding interest

rates, exchange rates, imports and exports, and the growth rates of other provinces,

would have an impact on the Eastern Cape economy. The increase in the growth rate

and employment would lead to an increase in workers’ incomes, which would stimulate

provincial demand, investment and hence national economic growth. The continued rise

in employment, if sustainable, would reduce the unemployment rate, which in turn would

cumulatively reduce the poverty rate. The growth rate of the province’s output, if it was

more than the national average, would lead to an increase in the province’s contribution

to national output. The rise in Eastern Cape employment would lead to an increase in the

6

province’s contribution to national employment. However, the growth in Eastern Cape

demand, combined with the demand from other provinces, would push inflation up and

lead to an increase in interest rates owing to the inflation-targeting policy adopted by the

South African Reserve Bank. The impact of these rate increases could lower the national

growth rate, which in turn might affect growth in the Eastern Cape.

Figure 1 : Conceptual Model of the Eastern Cape Economy

EC GDPContribution

National PublicInvestment

National GrowthRate

Interest Rate Exchange Rate

Trade

EC GrowthRate

EC Demand

EC Employment Growth

Unemployment Rate

Poverty Rate

Inflation Rate

7

8

9

2 NATIONAL ECONOMIC PERFORMANCE AND OUTLOOK

2.1 OVERVIEW OF CURRENT SITUATIONIn the mid 2000s, South Africa experienced unprecedented levels of growth which were

buoyed by favorable external conditions, coupled with strong domestic demand and rapid

credit extension. These conducive conditions raised growth to 5 percent on average in

2004 to 2007 and lowered the rate of unemployment by approximately 5 percentage

points, while strengthening public finances, maintaining single-digit inflation and improving

the level of external reserves. The favorable economic climate is attributed to sound

macroeconomic policies, which were firmly supported by a consistent and transparent

policy framework.

Despite these positive results, South Africa still faces a number of medium-term

challenges. The country’s output growth has remained lower than in many Emerging

Market Economies (EMEs), even during the 2004 to 2007 economic expansion. Strong

employment growth over the same period failed to bring down a very high unemployment

rate of over 23 percent, even though labour-force participation remains lower than in

other emerging economies. Another challenge that plagued South Africa was increasing

income inequality, which, despite modest improvement, remains among the highest in

the world.

Output and demand remain weak in spite of the slow recovery in the economy. In the

fourth quarter of 2008, output contracted by 1.8 percent quarter-on-quarter (Q-on-Q) and

by more than 6.7 percent in the first quarter of 2009. The contraction in output can be

traced to the dramatic slump in manufacturing and mining output. Residential property

prices continued trending downwards. Consumer spending has fallen, and the short-

term outlook for South Africa remains constricted. Annual output for 2009 is expected to

contract further by about 2 percent, with a slow recovery towards the end of the year as

shown in Table 2.1. The recovery is supported by policy measures that government has

put in place aimed at countering the cycle of the crisis, which have also been dampened

by the weak recovery of demand in trading-partner countries. Projections show that by

2010, the country would again start seeing positive growth as global recovery improves

and commodity prices recede to levels last seen before the crisis. It would not be until

2011 before output starts to show strong signs of recovery, when it is expected to tread

10

SOUTH AFRICAN GROSS DOMESTIC PRODUCT FORECASTS

2007 2008 2009 2010 2011 2012 2013

Annual Growth Rate (%) 5.1 3.1 -2.0 2.0 3.8 4.2 4.5

GDP* (Rm) 1,233,930 1,271,717 1,246,111 1,270,787 1,319,577 1,375,619 1,437,222

Source: Own Calculation and Quantec Research *Constant 2000 prices

at about 3.8 percent before climbing to about 4.2 percent in 2012 and 4.5 percent in 2013.

The potential output growth of about 4 percent is underpinned by private investment

(which is not expected to continue to grow at the rates seen from 2007 to 2008), weak

demand from trading-partner countries, commodity prices and diminished capital flows

for EMEs. While the projected growth may be disappointing in light of the experience of

the mid-2000s, it is still encouraging given the severity of external shocks. Medium-term

growth is sustained by large public infrastructure investment programs aimed at reducing

bottlenecks in transport infrastructure, electricity and ports, which are all likely to impede

growth as the economy recovers.

Table 2.1: South African Gross Domestic Product, 2007 - 2013

2.2 CONSUMER SPENDINGAgainst the backdrop of a sharply weakening economy, together with weak business-

and consumer-confidence indices, final household consumption expenditure has fallen

substantially in South Africa. The economy lost more than 200 000 jobs in early 2009,

leading to an increase in the unemployment rate of 23.5 percent in the first quarter of

2009, from a low of 21.9 percent in the fourth quarter of 2008. These job losses have

throttled household consumption expenditure.

Household expenditure also declined due to stringent extension of credit in light of the

National Credit Act (NCA) implemented in mid-2007, the global credit crisis, the high debt

burden, increased interest rates aimed at curtailing extreme spending, rising prices which

also corroded the disposable income of consumers and the national economic downturn.

Collectively, these events have dampened appetite for new debt, as shown in the growth

rate for credit, which declined from 23.1 percent in July 2007 to 4 percent in July 2009.

Spending decreased from 4 percent in 2008:Q1 to minus 1.7 percent in 2009:Q1, and

again from 3.4 percent in 2008:Q2 to minus 3.5 percent in 2009:Q2 as the impact of the

crisis began to be felt. Projections indicate that the figure would drop to about minus 3.9

percent in 2009:Q4 compared to about 0.5 percent in the 2008:Q4. Household expenditure