Drewry marine terminal finance investment summit 2015

17

www.drewry.co.uk Global dynamics changing the landscape of cargo flows Dinesh Sharma, Senior Manager Marine Terminal Finance and Investment Summit 2015

-

Upload

drewrymarketing -

Category

Business

-

view

388 -

download

4

Transcript of Drewry marine terminal finance investment summit 2015

www.drewry.co.uk

Global dynamics changing the

landscape of cargo flows

Dinesh Sharma, Senior Manager

Marine Terminal Finance and

Investment Summit 2015

www.drewry.co.uk 2 Overview of global container port and shipping trends | © Drewry 2015

Two dynamic aspects of demand…

…both affect capacity needs and investment decisions

Demand

growth

1. Growth rate %

2. Size of market

Changes in

the nature of

demand

1. Ship size growth

2. Carrier alliances and partnerships

TERMINAL

CAPACITY

requirements

www.drewry.co.uk 3 Overview of global container port and shipping trends | © Drewry 2015

Global container port traffic 2000-2014

Market is growing but at a much slower pace

249 279

315

363

399

443

497 525

478

548

596 625

645 678

713 749

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 (f) 2016 (f)

Source Drewry Maritime Research

Million teu

CAGR 11.3% CAGR 5.3%

www.drewry.co.uk 4 Overview of global container port and shipping trends | © Drewry 2015

Global container port traffic growth

Increased volatility: 5% seems to be the floor

-15%

-10%

-5%

0%

5%

10%

15%

20%

Source Drewry Maritime Research

www.drewry.co.uk 5 Overview of global container port and shipping trends | © Drewry 2015

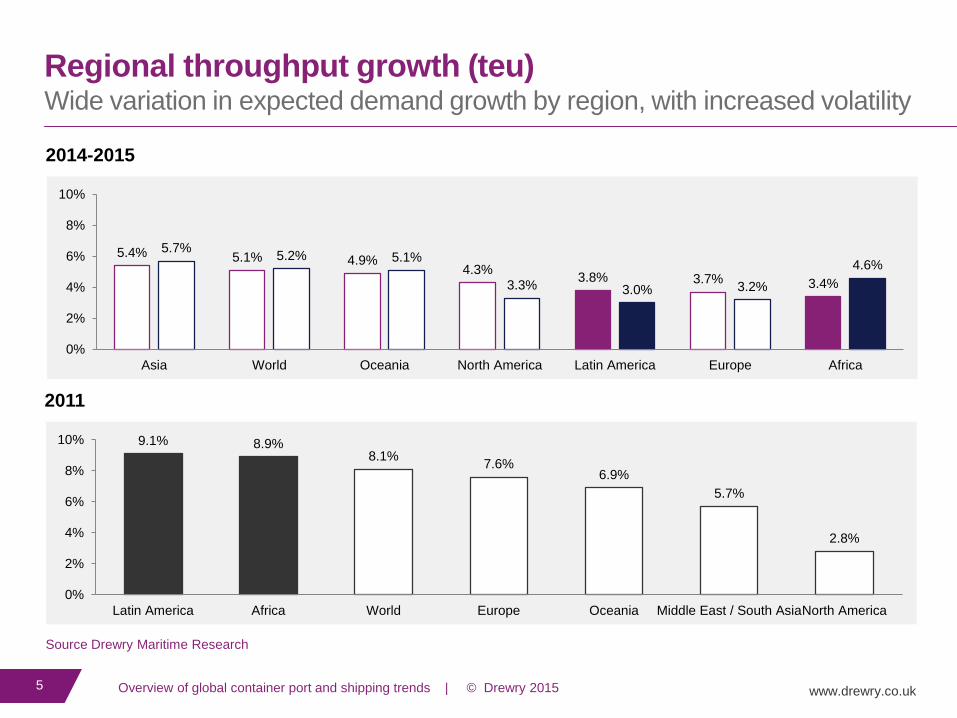

Regional throughput growth (teu) Wide variation in expected demand growth by region, with increased volatility

5.4% 5.1% 4.9% 4.3%

3.8% 3.7% 3.4%

5.7% 5.2% 5.1%

3.3% 3.0% 3.2%

4.6%

0%

2%

4%

6%

8%

10%

Asia World Oceania North America Latin America Europe Africa

Source Drewry Maritime Research

2014-2015

9.1% 8.9% 8.1%

7.6% 6.9%

5.7%

2.8%

0%

2%

4%

6%

8%

10%

Latin America Africa World Europe Oceania Middle East / South AsiaNorth America

2011

www.drewry.co.uk 6 Overview of global container port and shipping trends | © Drewry 2015

Global containership size development Rapid move towards bigger ships; 2015 - scheduled delivery of 1.9 million teu and 60 ULCVs

-5%

0%

5%

10%

15%

20%

25%

30%

35%

<4000 4,000-4,999 5,000-5,999 6,000-6,999 7,000-7,999 8,000-9,999 10,000 +

1Q 2014 1Q 2015 Change

• Ships of 10,000 teu or above comprise 18% of the global fleet by capacity (14% a year ago)

• Ships of 8,000 teu or above comprise 37% of the global fleet by capacity (33% a year ago)

• Ships of less than 5,000 comprise 46% of the global fleet by capacity (43% a year ago)

www.drewry.co.uk 7 Overview of global container port and shipping trends | © Drewry 2015

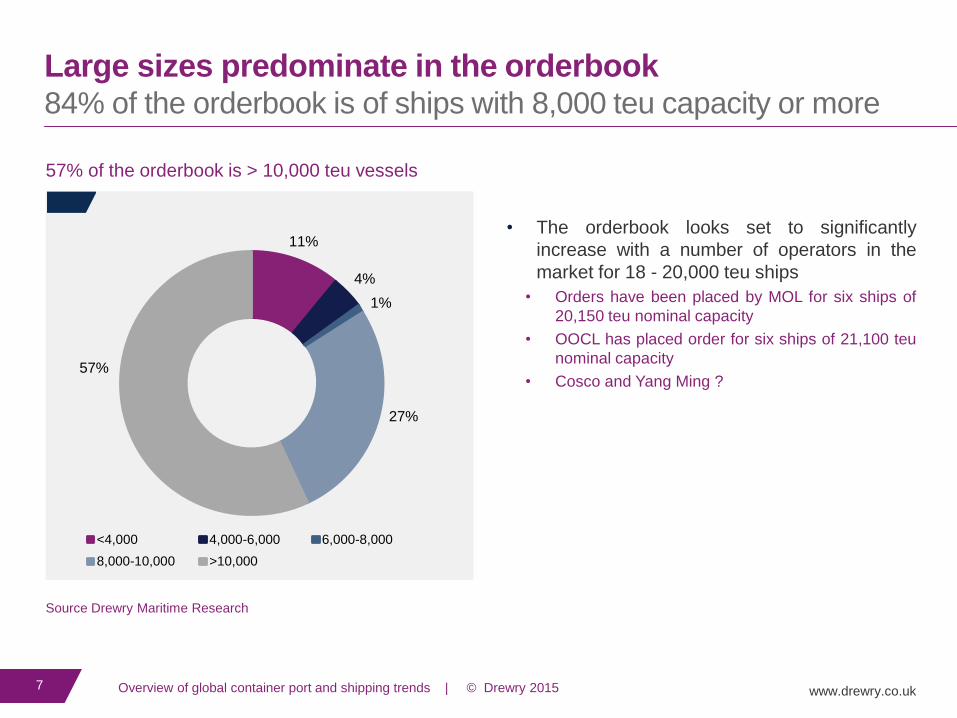

Large sizes predominate in the orderbook 84% of the orderbook is of ships with 8,000 teu capacity or more

11%

4%

1%

27%

57%

<4,000 4,000-6,000 6,000-8,000

8,000-10,000 >10,000

• The orderbook looks set to significantly

increase with a number of operators in the

market for 18 - 20,000 teu ships

• Orders have been placed by MOL for six ships of

20,150 teu nominal capacity

• OOCL has placed order for six ships of 21,100 teu

nominal capacity

• Cosco and Yang Ming ?

Source Drewry Maritime Research

57% of the orderbook is > 10,000 teu vessels

www.drewry.co.uk 8 Overview of global container port and shipping trends | © Drewry 2015

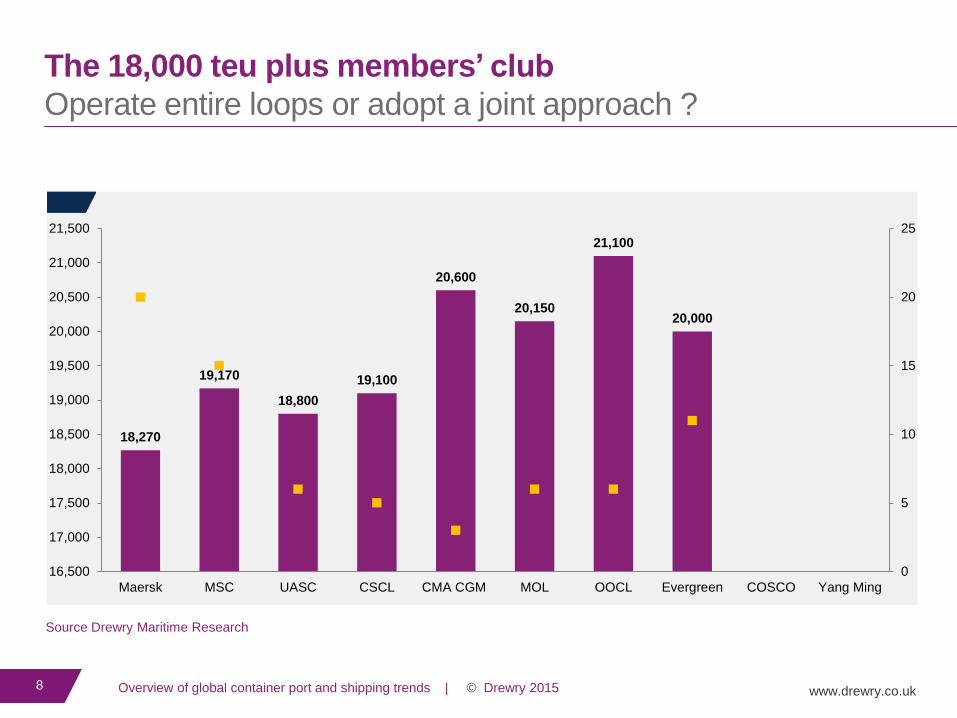

The 18,000 teu plus members’ club

Operate entire loops or adopt a joint approach ?

18,270

19,170

18,800

19,100

20,600

20,150

21,100

20,000

0

5

10

15

20

25

16,500

17,000

17,500

18,000

18,500

19,000

19,500

20,000

20,500

21,000

21,500

Maersk MSC UASC CSCL CMA CGM MOL OOCL Evergreen COSCO Yang Ming

Source Drewry Maritime Research

www.drewry.co.uk 9 Overview of global container port and shipping trends | © Drewry 2015

Increase in average container ship size, 1Q2013 - 1Q2015 Increase in ship size on all trade lanes…significant upsizing on certain trades

80%

37%

34%

32%

21%

19%

15%

15%

14%

10%

9%

9%

8%

8%

6%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Europe-S Africa

Asia-ECSA

Asia-W Africa

Europe- W Africa

Europe-ECSA

Asia-N Europe

Asia-USEC (Suez)

Asia-USWC

N Europe-Gulf/Mex

Asia-S Africa

SE Asia-Aus

N Europe- N Atlantic

Asia-WCSA

Asia-Med

N Asia-Aus

Source Drewry Maritime Research

www.drewry.co.uk 10 Overview of global container port and shipping trends | © Drewry 2015

Average ship size

More than 6,000 teu on most trade lanes

8,625

7,444

7,390

7,386

7,375

7,188

6,861

6,569

4,702

4,606

4,467

4,393

4,066

3,828

3,613

3,556

2,470

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000

Asia-Med

Europe-ECSA

Asia-USWC

Asia-ECSA

Asia-USEC (Suez)

Europe-S Africa

Asia-WCSA

Asia-S Africa

N Europe- N Atlantic

Asia-USEC (Panama)

N Asia-Aus

N Europe-Gulf/Mex

Asia-W Africa

SE Asia-Aus

Europe-WCSA

N Europe-Montreal

Europe- W Africa

Source Drewry Maritime Research

www.drewry.co.uk 11 Overview of global container port and shipping trends | © Drewry 2015

Alliances

Fragmented terminal capacity is a challenge at many ports

Lines

Terminal Operators

www.drewry.co.uk 12 Overview of global container port and shipping trends | © Drewry 2015

Changing nature of cargo flows Bigger ships resulting in changing day to day flow of cargo and peaking of volumes

7,109

7,528

8,144

122

114

109

1Q 2013 1Q 2014 1Q 2015

Average ship size and number of weekly loops on main East West trades

Typically the same number of ports called at per loop, but less frequently

Greater peaks and troughs at terminals (shipside and landside)

www.drewry.co.uk 13 Overview of global container port and shipping trends | © Drewry 2015

Changing nature of cargo flows

Transhipment; bigger ships and alliances increase the need

www.drewry.co.uk 14 Overview of global container port and shipping trends | © Drewry 2015

Changing nature of cargo flows Terminal performance is critical to achieving benefits of largest ships; who pays?

Lines Expect:

• Reliability

‒ Departure on schedule

‒ Connectivity with feeders/relay services at

hubs

‒ All containers loaded (including empties)

‒ No constraints/congestion on landside

service

• Productivity

‒ Speed of vessel turnaround is important.

As vessel size increases, port time is

maintained, in spite of increased container

exchange

• Efficiency

‒ Largest vessels for the trade/route to be

handled without physical constraints

‒ Unit handling costs are maintained –

requires a competitive environment

www.drewry.co.uk 15 Overview of global container port and shipping trends | © Drewry 2015

Key Takeaways

A. Global container port demand growth at its lowest (excluding 2009), wide

variation and increased volatility in demand growth by region

B. Influx of Ultra large container vessels on key trade routes is resulting in cascading

of bigger ships on all trade lanes with significant upsizing on certain trades

C. This is resulting in changing nature of cargo flows at container terminals and

posing key challenges terminal operators. Cascading is passing these

challenges throughout the global port network and throughout the supply

chain

Header

Sub header

www.drewry.co.uk

Panel Discussion

Demand outlook - Global implications on the relative attractiveness of

container terminal investments in selected geographies

Very Large Container Ships - The implications on container terminal

operators’ existing and future investments

Where is the value for terminal operators in making investment in infrastructure

to handle large container ships and global consortia

www.drewry.co.uk

UK

15-17 Christopher Street

London

EC2A 2BS

United Kingdom

India

209 Vipul Square

Sushant Lok - 1

Gurgaon 122002

India

Singapore

#13-02 Tower Fifteen

15 Hoe Chiang Road

Singapore 089316

China

Office 555, 4th floor

Standard Chartered Tower

201 Shi Ji Avenue

Pudong District, Shanghai

China, 200120

T +44 20 7538 0191 T +91 124 497 4979 T +65 6220 9890 T +86 (0) 21 6182 6759

From our origins in 1970 London to a 21st

century maritime and shipping consultancy,

Drewry has established itself as one of the most

widely used and respected sources of impartial

market insight and industry analysis. This in-

depth understanding and objectivity provides our

clients with the actionable advice and

recommendations they need to achieve their

ambitions and stay ahead of the market.

Our advisors have been involved in 400 port

assignments in 50 countries over the past 10 years

Since 2010, we have provided commercial and due

diligence advice in port M&A and financing projects

with a value of approximately $20bn

In the last 5 years we have provided advice on

vessel valuations with combined asset value of

more than $180bn

We have advised on container shipping industry

investments totalling $6bn in the last 5 years