Dr. René Lochtman BASF in excellent Deputy Head of IR ... · Feasibility studies to be completed...

52

BASF in excellent shape, optimistic for 2011 Dr. René Lochtman Deputy Head of IR Juliane Schöningh IR Manager Bankhaus Lampe Kapitalmarktkonferenz Baden-Baden, Germany April 1, 2011

Transcript of Dr. René Lochtman BASF in excellent Deputy Head of IR ... · Feasibility studies to be completed...

BASF in excellent shape, optimistic for 2011

Dr. René

LochtmanDeputy

Head

of IR

Juliane

SchöninghIR Manager

Bankhaus

Lampe

KapitalmarktkonferenzBaden-Baden, Germany

April 1, 2011

2BASF Capital Market Story March 2011

1 | Record year 2010

2 | Focus on operational excellence

3 | Well positioned for profitable growth

4 | Outlook

3BASF Capital Market Story March 2011

Sales €63.9 billion +26%EBITDA €11.1 billion +51%EBITDA margin 17.4% 14.6%EBIT before special items €8.1 billion +68%EBIT €7.8 billion +111%Net income €4.6 billion +223%Adjusted EPS €5.73 +90%

Business performance

2010

vs. 2009

Record year 2010

Record sales and record EBIT before special itemsChemical businesses take advantage of strong economic recoveryConsistent long term value generation

4BASF Capital Market Story March 2011

Excellent segment performance 2010

Segment€

million

Sales Δvs. 2009

EBITDA EBITDA margin

EBIT before SI

Δvs. 2009

Chemicals 11,377 +51% 3,000 26.4% 2,302 +126%

Plastics 9,830 +38% 1,721 17.5% 1,284 +123%

Performance Products 12,288 +31% 2,162 17.6% 1,554 +123%

Functional Solutions 9,703 +36% 861 8.9% 467 +123%

Agricultural Solutions 4,033 +11% 938 23.3% 749 (4%)

Oil & Gas 10,791 (5%) 2,977 27.6%* 2,430 +6%

* Excluding non-compensable oil taxes: 18.5%

5BASF Capital Market Story March 2011

*

Cash provided by operating activities less capex

(in 2005 before CTA)** 2009 adjusted for re-classification of settlement payments for currency

derivatives

Continuous strong cash flow

Cash Flow (billion €)

Cash provided by operating activitiesFree cash flow*

-1

0

1

2

3

4

5

6

7

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

6.5

3.9

**

6BASF Capital Market Story March 2011

Average annual dividend increase of 14.5%(2001-2010)

Dividend yield above 3% in any given year since 2001

Attractive dividend yield of 3.7% in 2010*

3.9%

Key factsDividend per share (€)

2.20

0.65 0.70 0.700.85

1.00

1.50

1.95 1.951.70

0.0

0.5

1.0

1.5

2.0

2.5

2001 2004 2007 2010

0.50

1.00

1.50

2.00

3.1%

* Dividend yield based on share price at year-end

3.2% 3.1% 4.1% 3.8% 7.0%Yield*

Proposal:

3.7%

2.50

3.1% 3.9%

Attractive shareholder returns Record dividend

7BASF Capital Market Story March 2011

Delivering consistent, long-term value

Long-term performance January 2001 –

December 2010 (average annual performance with dividends reinvested)

+13.9%

-2.7%

+7.1%

-3 0 3 6 9 12 15

BASF

Euro Stoxx

50

DAX 30

MSCI World Chemicals

+0.7%

8BASF Capital Market Story March 2011

1 | Record year 2010

2 | Focus on operational excellence

3 | Well positioned for profitable growth

4 | Outlook

9BASF Capital Market Story March 2011

Vertical and horizontal integration of production plants, energy and waste flows, logistics and site infrastructure

Know-how Verbund

Energy Verbund and combined heat and power plants lead to-

Savings of ∼2.6 million tons oil equivalent p.a.

-

Reduction of CO2

-emissions of ~6 million tons p.a.

9

Unique ‘Verbund’

concept Cost savings of >€500 million p.a. in Ludwigshafen alone

BASF site Ludwigshafen, Germany Verbund Concept

10BASF Capital Market Story March 2011

Fixed costs represent around 30% of total costs

Only slightly higher fixed costs, despite major acquisitions(Engelhard, Degussa Construction Chemicals, Ciba and Cognis)

Ciba and Cognis synergies as well as NEXT program will drive fixed costs down–

Cost synergies Ciba:>€450 million by 2012

–

Cost synergies Cognis:

€140 million by 2013

Stringent fixed cost management

Key facts

Fixed costs indexed EBITDA indexedSales indexed

BASF Group development 2001-2010

Index

~270%

~200%

~20%

Δ

50

100

150

200

250

300

2001 2004 2007 2010

11BASF Capital Market Story March 2011

> 500 individual projects to simplify processes, structures and production sites in all regions

Project timeline:2008-2011

Annual earnings contribution of €600 million in 2010 achieved

Targeted earnings contribution by 2012: ≥€1 billion

Completed restructuring programs

New efficiency program NEXT

Sustainable improvement of cost base Efficiency program NEXT on track

New

EXcellence

Targets

(NEXT)Annual earnings contribution (million €)

20120

500

1,000

1,500

2,000

2,500

2003 2005 2007 2009

12BASF Capital Market Story March 2011

1 | Record year 2010

2 | Focus on operational excellence

3 | Well positioned for profitable growth

4 | Outlook

13BASF Capital Market Story March 2011

Leading positions in growth industries

and emerging markets

Ongoing portfolio

optimization

Excellent innovation platform

We strive to outperform global chemical production growth by at least 2 percentage points p.a.

Well positioned for profitable growth

Continue expansion in emerging markets, especially AsiaTranslate megatrends into business growth

Continue with active portfolio managementDrive portfolio closer to end customer

Product and system innovation as growth driversMegatrend innovations for long-term growth

Growth target:

14BASF Capital Market Story March 2011

Leading positions in growth industries and

emerging markets

14

15BASF Capital Market Story March 2011

FunctionalSolutions

6%

Other12%

By region

Oil & Gas* 35%

Chemicals15%

Alternative sitesunder review

2%South America, Africa, Middle East4%

North America14%

Europe**63%

By segment

AgriculturalSolutions4%

Plastics14%

Asia Pacific17%

€12.6 billion

€12.6 billionPerformance

Products14%

Planned capital expenditures 2011-2015

** Thereof ~€4.4 billion for Oil & Gas* Excluding investments in Nord Stream

16BASF Capital Market Story March 2011

0

10

20

30

40

50

60

Emerging markets Significant sales growth in emerging markets

Sales 2010 in emerging markets: €14.5 billion (27%)

Investments in emerging markets 2005-2010:€3 billion

Ongoing increase of - sales force- regional R&D

Emerging markets definition, according to Dow Jones:35 countries *

* Bahrain, Brazil, Bulgaria, Chile, China, Colombia, Czech Republic, Egypt, Estonia, Hungary, India, Indonesia, Jordan, Latvia, Kuwait, Lithuania, Malaysia, Mauritius, Mexico, Morocco, Oman, Pakistan, Peru, Philippines, Poland, Qatar, Romania, Russia, Slovakia, Sri Lanka, South Africa, South Korea, Taiwan, Thailand, Turkey, United Arab Emirates

Emerging MarketsNet sales in billion €BASF Group (w/o Oil & Gas)

2005 2010

CAGR 7%22%

27%CAGR 13%

Emerging Markets (Dow Jones definition)

Developed Markets

17BASF Capital Market Story March 2011

Emerging markets Recently announced major investment projects

Location Product group Start up

Chongqing, China

MDI plant with world-scale capacity of 400,000 metric tons –

investment of €860 millionCommercial operation expected in 2014

Nanjing, China

MoU

signed with SINOPEC to explore expansion of the Verbund site –

potential investment of approx. $1 billion

Feasibility studies to be completed by 2012

Malaysia MoU

signed with Petronas

to build world-scale specialty chemical facility –

potential investment of approx. €1 billion

Feasibility studies to be completed in 2011

Brazil World-scale acrylic acid, butyle

acrylate

and superabsorbant

polymers (SAP) plantFeasibility study to be completed in 2011

Russia MoU

signed with Gazprom

to further develop Achimov

deposits in SiberiaNegotiation to be conducted in 2011

18BASF Capital Market Story March 2011

6.5

12.5

20

0

5

10

15

20

2005 2010* 2020

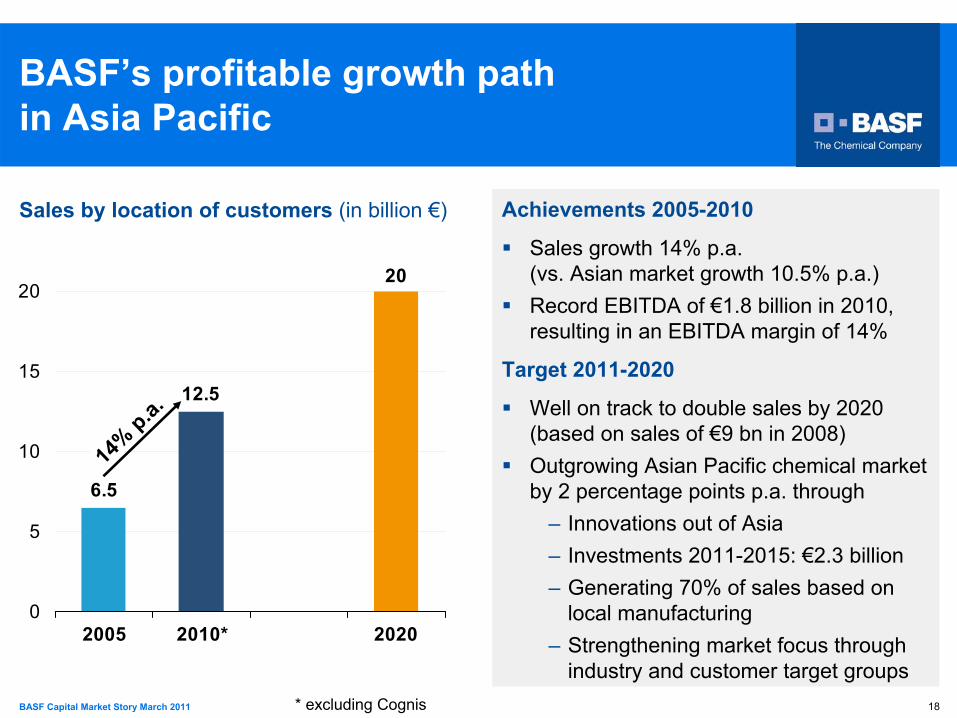

BASF’s profitable growth path in Asia Pacific

Sales by location of customers (in billion €)

* excluding Cognis

14% p.a.

Achievements 2005-2010

Sales growth 14% p.a.(vs. Asian market growth 10.5% p.a.)Record EBITDA of €1.8 billion in 2010, resulting in an EBITDA margin of 14%

Target 2011-2020

Well on track to double sales by 2020(based on sales of €9 bn in 2008)Outgrowing Asian Pacific chemical market by 2 percentage points p.a. through

–

Innovations out of Asia–

Investments 2011-2015: €2.3 billion–

Generating 70% of sales based on local manufacturing

–

Strengthening market focus through industry and customer target groups

19BASF Capital Market Story March 2011

Ongoing portfolio optimization

19

20BASF Capital Market Story March 2011

BASFcore

businesses

Powerful partnerships

Major acquisitions Major divestitures

Pharmaceuticals

Fibers

Printing systems

Polyolefins (Basell)

Polystyrene North America

Agchem generics

Premix

Crop protectionOil & Gas (Revus)Engineering Plastics Electronic ChemicalsCustom synthesisCatalysts (Engelhard)Construction Chem.Water-based resinsPigments (Ciba)Plastic additives (Ciba)Care Chem. (Cognis)Nutrition & Health (Cognis)

15 billion Euro(Sales)

9 billion Euro*

(Sales)

GazpromMonsantoPetronasShellSinopecTotal

* Not including Styrenics business

Selected transactions 2001

to date

Styrenics (Styrolution)(LoI for JV announced)

Pro-active portfolio management

Sale of shares in K+S(Proceeds for BASF ~€1 billion)

21BASF Capital Market Story March 2011

Cognis –

integrating a global leader in value-added products

Pro forma business performance FY’2010Sales: ~€3 billionEBITDA: ~€550 millionEBITDA margin: ~18%Closing on December 9, 2010

Integration objectivesAchieve 20% EBITDA margin in the Performance Products segment by 2012Acquisition accretive as of 2012 Integration costs of €290 million until end of 2012Inventory step-up of €120 million in 2010/2011In 2010, total integration costs of €80 million incurred –thereof 75% inventory step-up.Synergies to generate €275 million of additional EBIT

-

Cost synergies: €140 million by 2013-

Growth synergies: €135 million by 2015

22BASF Capital Market Story March 2011

BASF + Cognis Improved market positions

PreviousBASF position

FutureBASF position

Personal care ingredients 3 1Home care ingredients 1 1

Functional nutritioningredients 6 3

Coating additives 7 3Heavy-duty driveline lubricants >

10 3

Mining chemicals 3 2

23BASF Capital Market Story March 2011

Styrolution Planning a 50/50 joint venture with INEOS

ScopeGlobal No.1 in styrenicsSales of about €5 billion*, thereof

–

48% Europe, 32% Americas, 20% Asia Pacific–

34% SM, 34% PS, 21% ABS, 11% Copolymer Specialties

Customers in more than 110 countries29 production facilities across 11 countriesMore than 3,000 employees

MilestonesNov 29, 2010: LoI signed by BASF and INEOSJan 1, 2011: Carve-out of BASF‘s Styrenics activities into separate legal entitiesSecond half of 2011: Start of planned JV Styrolution

* Pro-forma figures, based on BASF‘s and INEOS‘

sales in 2009

Styrolux

T/S shrink filmValue creating divestiture process

24BASF Capital Market Story March 2011

Active portfolio management pays off

Chemical activities

Agricultural Solutions

Oil & Gas, including non-deductible oil taxes

EBITDA by activity (in billion €, excluding Other)

Recent acquisitions reshaped portfolio–

Closer to end customers–

Innovation-driven–

Profitable growth above industry average

BASF’s EBITDA in 2010 (excluding Other) amounted to €11.7 billion

* Based on German GAAP**

As of 2007 according to new segment structure (excl. Styrenics and corporate costs)

Our diversified portfolio is a key strength

0

2

4

6

8

10

12

2001* 2004 2007** 2010

25BASF Capital Market Story March 2011

Excellent innovation platform

25

26BASF Capital Market Story March 2011

NaphthaMax®

III

Xemium®Kaurit®

Light

CypoSol®

Elastopave®

Ecovio®

Natugrain®

TS X-SEED® PCI Geofug®

27BASF Capital Market Story March 2011

Xemium® BASF’s next-generation fungicide for broad use

Key facts

Xemium® complements BASF‘s outstanding fungicide portfolio

Our 1st carboxamide fungicide for all market segments

BASF is carboxamide pioneer,Xemium®

strengthens lead

Launch planned in >50 countries and >100 crops

World-wide data submissionprocess underway

Market launch from 2012 onwards

* Source: Philips McDougall, own estimation

Untreated

Xemium®

global peak sales potential: >€200 million

28BASF Capital Market Story March 2011

0,0 0,00

5

10

15

20

4.53.5

Innovation pipeline worth €21 billion

* New or improved products or new applications, max. 5 years on market, including Growth Clusters

The pipeline NPV of €21 billion is a bottom-up aggregation of all R&D projects

High success rate due to stringent R&D controlling via Phasegate process

Expected Commercial Value:~50% of NPV (probability-weighted)

In 2010, sales of new products (5 years or younger) exceeded the target of €6 billion

Target 2015: up to €8 billion sales with new products

R&D contributes significantly to earnings growth

14% Performance Products7% Plastics3% Chemicals

8% Functional Solutions

46% Agricultural Solutions

2% Oil & Gas20% Corporate Research

2009 2010

€19 bn€21 bn

Net present value by segments (billion €)

29BASF Capital Market Story March 2011

Further increase in R&D spending planned for 2011

Innovation will spur further growth

Total R&D expenditures 2010 (billion €)

€1.5 bn R&D expenditures in 2010 (vs. €1.4 bn in 2009)

~ 9,600 employees in R&D

~ 3,000 projects and topics

Research Verbund: About 1,900 partnerships with universities, start-ups and industry partners

Strong commitment to R&D

24%

1%

Corporate Research22%

Agricultural Solutions

26%

Functional

Solutions12%

Performance

Products19%

Chemicals9%

Plastics10%

€1.5 billion

Other2%

30BASF Capital Market Story March 2011

1 | Record year 2010

2 | Focus on operational excellence

3 | Well positioned for profitable growth

4 | Outlook

31BASF Capital Market Story March 2011

Outlook BASF Group 2011 Expectations for global economy

2010

GDP 3.9%

Chemical production (excl. Pharma)

9.3%

Industrial production 8.9%

US$ / Euro 1.33

Oil price (US$ / bbl) 79.50

Forecast

2011

3.3%

5.2%

5.0%

1.35

90

32BASF Capital Market Story March 2011

Outlook 2011 by regionChemical production

(excl. Pharma)

EU-27

USA

Asia (excl. Japan)

Japan

South America

Industrial production

5.2%

2.9%

3.3%

9.6%

1.9%

5.0%

3.0%

3.9%

10.0%

2.3%

4.3%4.6%

World 9.3%

10.1%

5.0%

13.0%

8.8%

6.4%

8.9%

6.0%

5.7%

14.5%

15.8%

6.2%

2010 2011 2010 2011

33BASF Capital Market Story March 2011

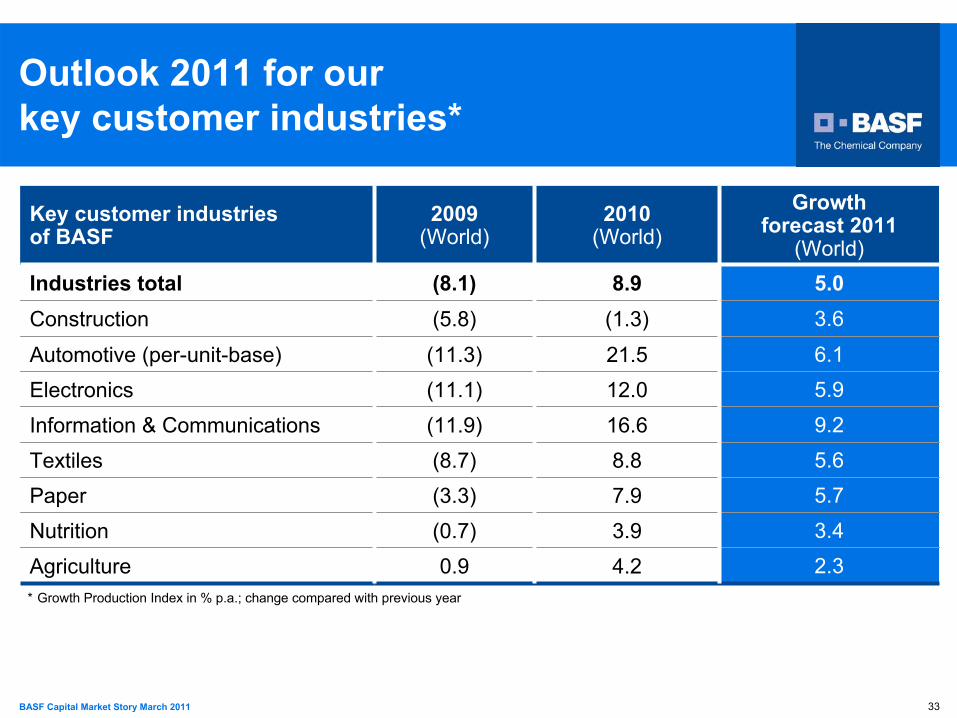

Outlook 2011 for our key customer industries*

Key customer industries of BASF

2009 (World)

2010 (World)

Growth forecast 2011

(World)Industries total (8.1) 8.9 5.0Construction (5.8) (1.3) 3.6

Automotive (per-unit-base) (11.3) 21.5 6.1Electronics (11.1) 12.0 5.9

Information & Communications (11.9) 16.6 9.2

Textiles (8.7) 8.8 5.6Paper (3.3) 7.9 5.7

Nutrition (0.7) 3.9 3.4

Agriculture 0.9 4.2 2.3*

Growth Production Index in % p.a.; change compared with previous

year

34BASF Capital Market Story March 2011

Outlook 2011 by segments

Segments EBIT before special items 2011

Chemicals

Plastics

Performance Products

Functional Solutions

Agricultural Solutions

Oil & Gas

BASF Group

(incl. Other)

35BASF Capital Market Story March 2011

We aim to grow sales on average by two percentage points per year faster than chemical production growth.We strive to grow our earnings further year by year, and to achieve an EBITDA margin of 18% by 2012.

We expect to achieve in 2011:-

Significant increase in sales and EBIT before special items.-

A high premium on our cost of capital. -

Significantly higher sales and earnings in the 1st

quarter 2011 vs. previous year’s quarter.

Targets 2011

Medium-term targets

Outlook 2011

We aim to continuously increase the annual dividend, or at least maintain it at the level of the previous year.

Dividend policy

36BASF Capital Market Story March 2011

This presentation includes forward-looking statements that are subject to risks and uncertainties, including those pertaining to the anticipated benefits to be realized from the proposals described herein. This presentation contains a number of forward-looking statements including, in particular, statements about future events, future financial performance, plans, strategies, expectations, prospects, competitive environment, regulation and supply and demand. BASF has based these forward-looking statements on its views with respect to future events and financial performance. Actual financial performance of the entities described herein could differ materially from that projected in the forward-looking statements due to the inherent uncertainty of estimates, forecasts and projections, and financial performance may be better or worse than anticipated. Given these uncertainties, readers should not put undue reliance on any forward-looking statements.

Forward-looking statements represent estimates and assumptions only as of the date that they were made. The information contained in this presentation is subject to change without notice and BASF does not undertake any duty to update the forward-looking statements, and the estimates and assumptions associated with them, except to the extent required by applicable laws and regulations.

Forward-looking statements

37BASF Capital Market Story March 2011

38BASF Capital Market Story March 2011

Sales developmentPeriod Volumes Prices Portfolio Currencies

Q4’10 vs. Q4’09 4%* 13% 2% 6%

FY’10 vs. FY’09 11% 8% 2% 5%

* Volumes +8% (without Oil & Gas)

1.5

2.02.2 2.2

1.8

0.0

0.5

1.0

1.5

2.0

2.5

Q4 Q1 Q2 Q3 Q4

EBIT before special items (billion €)

13.215.5 16.2 15.8 16.4

0

4

8

12

16

20

Q4 Q1 Q2 Q3 Q4

Sales (billion €)

20102009 20102009

BASF Group Q4 2010 Record sales and strong earnings increase vs. PYQ

39BASF Capital Market Story March 2011

Chemicals Strong earnings improvement vs. PYQ due to higher demand

Intermediates655+32%

Inorganics326

+24%

Petrochemicals1,964+41%

€2,945 +37%

315

461

687617

537

0

200

400

600

Q4 Q1 Q2 Q3 Q4

Sales developmentPeriod Volumes Prices Portfolio Currencies

Q4’10 vs. Q4’09 9% 20% 0% 8%

FY’10 vs. FY’09 18% 28% 0% 5%

Q4’10 segment sales

(million €) vs. Q4’09 EBIT before special items (million €)

20102009

40BASF Capital Market Story March 2011

Plastics High demand and price increases lifted sales significantly

Polyurethanes1,363+20%

Performance

Polymers

1,088+34%

€2,451 +26%

251279

349 371

285

0

200

400

Q4 Q1 Q2 Q3 Q4

Sales development Period Volumes Prices Portfolio Currencies

Q4’10 vs. Q4’09 10% 9% 0% 7%

FY’10 vs. FY’09 22% 10% 0% 6%

Q4’10 segment sales

(million €) vs. Q4’09 EBIT before special items (million €)

20102009

41BASF Capital Market Story March 2011

Sales developmentPeriod Volumes Prices Portfolio Currencies

Q4’10 vs. Q4’09 3% 4% 6% 5%

FY’10 vs. FY’09 12% 4% 11% 4%

Performance Products Earnings significantly up vs. previous year despite one-off costs

209

419471

370294

0

100

200

300

400

500

Q4 Q1 Q2 Q3 Q4

PerformanceChemicals

778+15%

Care Chemicals763+42%

€3,060 +18%

Paper Chemicals405+2%

Q4’10 segment sales

(million €) vs. Q4’09 EBIT before special items (million €)

Nutrition & Health384+10%

20102009

Dispersions

& Pigments

730

+17%

42BASF Capital Market Story March 2011

Sales developmentPeriod Volumes Prices Portfolio Currencies

Q4’10 vs. Q4’09 15% 10% 1% 9%

FY’10 vs. FY’09 17% 10% 1% 8%

Functional Solutions Earnings declined considerably due to one-time operating costs

Catalysts1,369+62%

Construction Chemicals514

+11%

Coatings686

+15%

€2,569 +35%

101 111

165 158

33

0

50

100

150

Q4 Q1 Q2 Q3 Q4

Q4’10 segment sales

(million €) vs. Q4’09 EBIT before special items (million €)

20102009

43BASF Capital Market Story March 2011

Agricultural Solutions South America drove strong sales growth

44 42

0

10

20

30

40

50

Q4 Q4

Q4’10 segment sales

(million €) vs. Q4’09 EBIT before special items (million €)

20102009

0

200

400

600

800

1,000

Q4 Q420102009

+20% (5)%

Sales developmentPeriod Volumes Prices Portfolio Currencies

Q4’10 vs. Q4’09 18% (4)% 0% 6%

FY’10 vs. FY’09 9% (3)% 0% 5%

703845

44BASF Capital Market Story March 2011

132230

0

200

400

600

800

Q4 Q4

Oil & Gas Earnings grew substantially y-o-y

as a result of higher oil prices

Exploration &

Production1,059+9%

Natural Gas

Trading

1,905+16%

€2,964 +13%

Sales developmentPeriod Volumes Prices/Currencies Portfolio

Q4’10 vs. Q4’09 (15)% 28% 0%

FY’10 vs. FY’09 (2)% (3)% 0%

106

EBIT bSI

Natural Gas TradingEBIT bSI

Exploration & ProductionNet income

Q4’10 segment sales

(million €) vs. Q4’09 EBIT before

special

items

/ Net income

(million

€)

20102009

374607

508

713

134

45BASF Capital Market Story March 2011

Review of “Other”

Million € Q4 2010 Q4 2009 2010 2009Sales 1,590 1,263 5,851 4,577thereof Styrenics 857 685 3,401 2,502

EBIT before special items (139) 51 (648) (717)thereof Corporate research

Group corporate costs Currency results, hedges and other valuation effects Styrenics, fertilizers, other businesses

(96) (66)

(229)

142

(79) (45)

9

80

(323) (226) (460)

387

(319) (209) (512)

339

Special items 149 293 (59) 90

EBIT 10 344 (707) (627)

46BASF Capital Market Story March 2011

0

1

2

3

4

5

6

7

8

9

1.8

(0.6)

(2.5)

(1.8)

6.5

(1.9)

1.5

* Payments related to intangible assets and property, plant and equipment

Cash

12/31/09

Operating

CF

Capex* Acquisitions Dividends Other cash

inflows

Cash

12/31/10

Excellent operating cash flow in 2010

thereof €1.6 bn

dividends to BASF SE shareholders

Net cash-out for purchase of Cognis: €0.6 bn

Excellent operating cash flow despite €1.7 bn

increase in net working capital

Capex* on last year´s level

Full Year 2010 (billion €)

Debt

repayment

(2.3)0.5

47BASF Capital Market Story March 2011

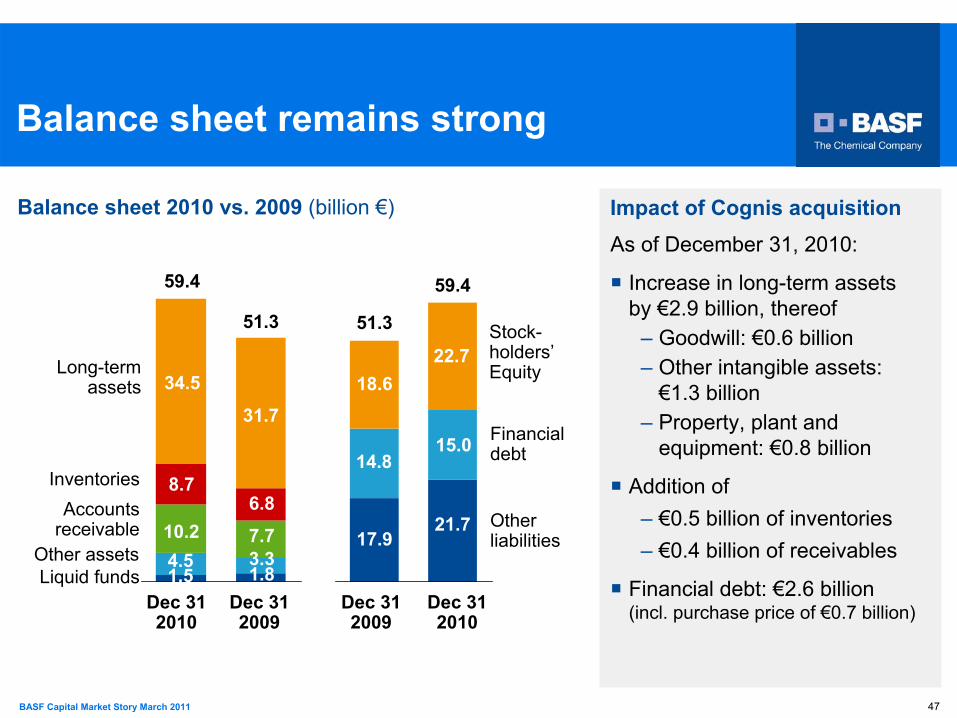

Balance sheet remains strong

Balance sheet 2010 vs. 2009 (billion €)

Liquid funds

Accounts

receivable

Long-term

assets

22.7

15.0

21.7

31.7

7.7

1.8

Other

liabilities

Financial

debt

Stock-

holders’

Equity

Dec 31

2010

Dec 31

2009

Dec 31

2009

Dec 31

2010

59.4

34.5

10.2

1.5

51.3

18.6

14.8

17.9

Inventories

Other assets

8.7

4.5

6.8

3.3

59.4

51.3

Impact of Cognis acquisitionAs of December

31, 2010:

Increase in long-term assets by €2.9 billion, thereof

–

Goodwill: €0.6 billion–

Other intangible assets:

€1.3 billion–

Property, plant and equipment: €0.8

billion

Addition of–

€0.5 billion of inventories–

€0.4 billion of receivables

Financial debt: €2.6 billion(incl. purchase price of €0.7 billion)

48BASF Capital Market Story March 2011

BackupFinancial Highlights Agricultural Solutions

48

49BASF Capital Market Story March 2011

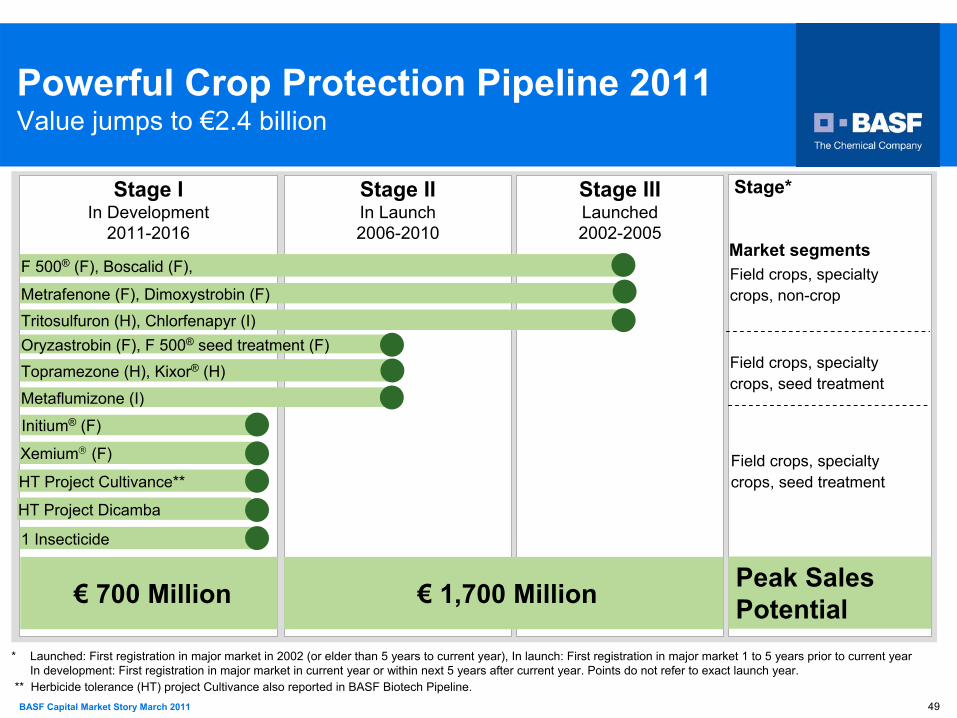

Powerful Crop Protection Pipeline 2011 Value jumps to €2.4 billion

* Launched: First registration in major market in 2002 (or elder than 5 years to current year), In launch: First registration in major market 1 to 5 years prior to current year

In development: First registration in major market in current year or within next 5 years after current year. Points do not refer to exact launch year.** Herbicide tolerance (HT) project Cultivance also reported in BASF Biotech Pipeline.

Stage IIILaunched

2002-2005

Stage IIIn Launch

2006-2010

Stage I

In Development

2011-2016

F 500®

(F), Boscalid (F),

Oryzastrobin (F), F 500®

seed treatment (F)

HT Project Cultivance**

Tritosulfuron (H), Chlorfenapyr (I)

Metaflumizone (I)

1 Insecticide

Topramezone (H), Kixor®

(H)

€

700 Million €

1,700 Million

Stage*

Market segments

Peak Sales Potential

Initium®

(F)

Xemium®

(F)

HT Project Dicamba

Field crops, specialty

crops, seed treatment

Metrafenone (F), Dimoxystrobin (F)

Field crops, specialty

crops, seed treatment

Field crops, specialty

crops, non-crop

50BASF Capital Market Story March 2011

Million € Q4 2010 Q4 2009 Δ% FY 2010 FY 2009 Δ%

Sales* 845 703 20 4,033 3,646 11

EBITDA** 88 100 (12) 938 980 (4)

EBITDA** margin 10.4% 14.2% - 23.3% 26.9% -

EBIT** 42 44 (5) 749 776 (4)

EBIT** margin 5.0% 6.3% - 18.6% 21.3% -

Assets (as of Dec. 31) - - - 5,063 4,681 8

*

Sales increase at constant exchange rates in Q4: +15% (FY: +6%)**

before special items

Agricultural Solutions Performance Q4 and FY 2010

51BASF Capital Market Story March 2011

Million € FY 2010 FY 2009 Δ% Δ% (CER)*

Europe 1,566 1,520 +3 +1

North America 999 932** +7 +2

South America 1,030 816** +26 +20

Asia / Pacific 438 378 +16 +7

Total 4,033 3,646 +11 +6

* constant exchange rates

** restated figures due to new definition of regions

Agricultural Solutions Sales by region

52BASF Capital Market Story March 2011

Million € FY 2010 FY 2009 Δ% Δ% (CER)*

Fungicides 1,739 1,708 +2 -2

Herbicides 1,410 1,165 +21 +16

Insecticides / Others 884 773 +14 +9

Total 4,033 3,646 +11 +6

* constant exchange rates

Agricultural Solutions Sales by indication