Downloaded from Studyfromnotes.com - All FREE premium ...

463

CA FINAL INDIRECT TAX LAWSEC This Question Bank has been prepared by CA AMIT KHANDAL. He has more than 15 years of Practical & Teaching experience in Indirect Taxes. It contains More than 550 Questions. Part I contains 400+ GST Questions and Part B contains 150+ Custom Act Questions. The solutions of all the questions in this question bank are as per ICAI. For any queries regarding IDT, WhatsApp Amit Khandal Sir (TAX GURU) at 9829056469. Reach out to us at following:- • Telegram Channel – CA DR AMIT KHANDAL • Youtube – CA DR AMIT KHANDAL • Android App – AMIT KHANDAL CLASSES • Website – www.amitkhandal.in • Call/Whatsapp – 9829056469 • Email – [email protected] Question Bank with Solutions (Relevant for MAY/NOV 2021 examination) It covers: All ICAI SM Questions All RTP & MTP Questions upto Nov 20) All Past Exam Questions (upto Nov 19) All Additional Questions given by ICAI Downloaded from Studyfromnotes.com - All FREE premium notes

Transcript of Downloaded from Studyfromnotes.com - All FREE premium ...

CA FINAL

INDIRECT TAX LAWSECT TAX LAWS

This Question Bank has been prepared by CA AMIT KHANDAL. He has more than

15 years of Practical & Teaching experience in Indirect Taxes.

It contains More than 550 Questions. Part I contains 400+ GST Questions and

Part B contains 150+ Custom Act Questions. The solutions of all the questions in

this question bank are as per ICAI.

For any queries regarding IDT, WhatsApp Amit Khandal Sir (TAX GURU) at

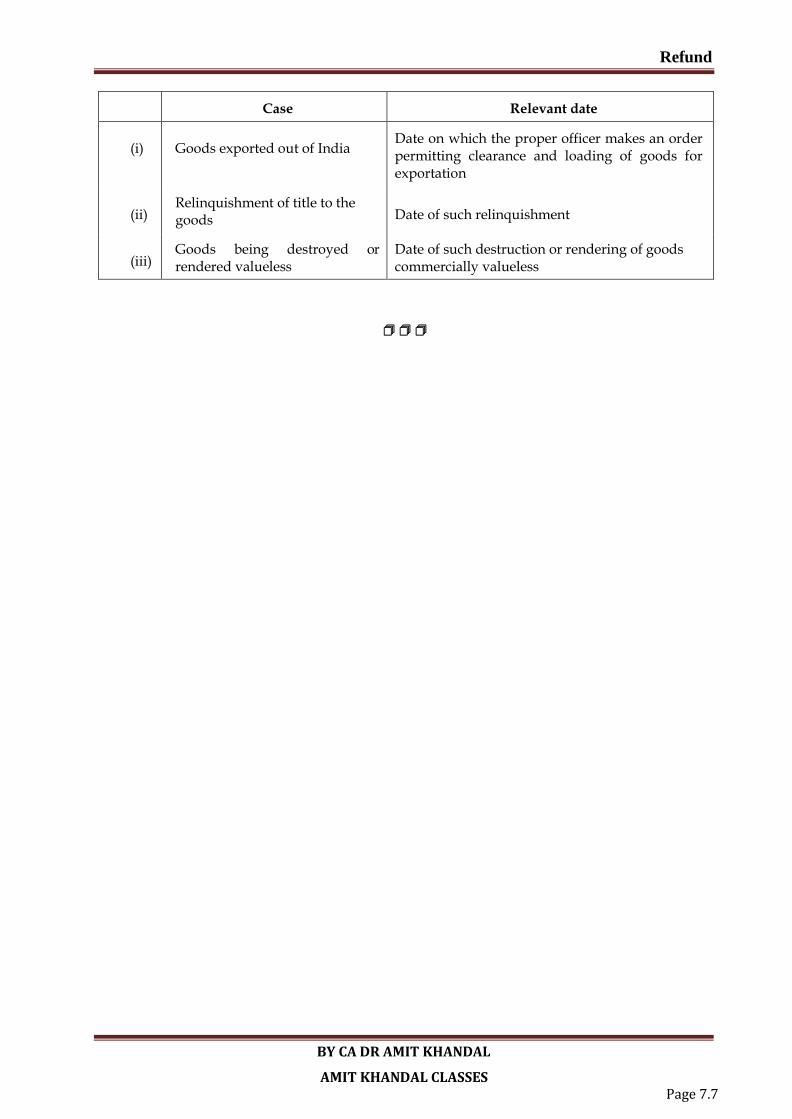

9829056469.

Reach out to us at following:-

• Telegram Channel – CA DR AMIT KHANDAL • Youtube – CA DR AMIT KHANDAL

• Android App – AMIT KHANDAL CLASSES • Website – www.amitkhandal.in

• Call/Whatsapp – 9829056469 • Email – [email protected]

Question Bank with Solutions

(Relevant for MAY/NOV 2021 examination)

It covers:

All ICAI SM Questions

All RTP & MTP Questions upto Nov 20)

All Past Exam Questions (upto Nov 19)

All Additional Questions given by ICAI

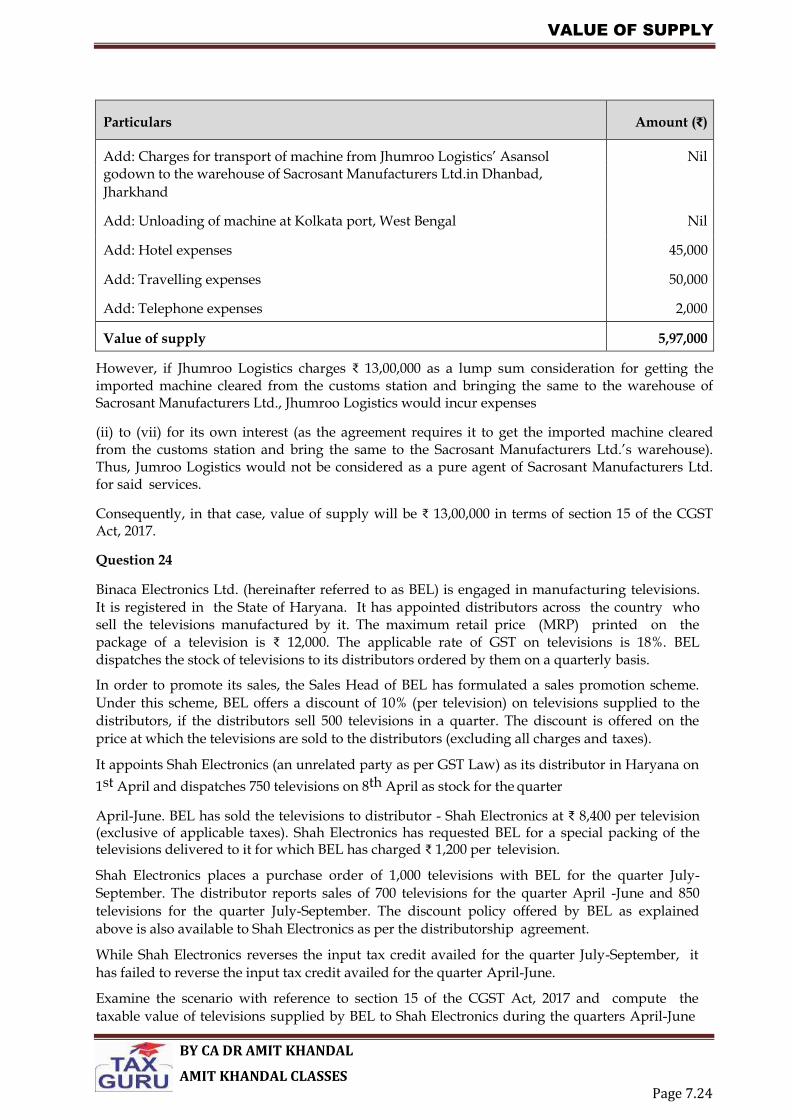

Downloaded from Studyfromnotes.com - All FREE premium notes

Contents

BY CA DR AMIT KHANDAL AMIT KHANDAL CLASSES

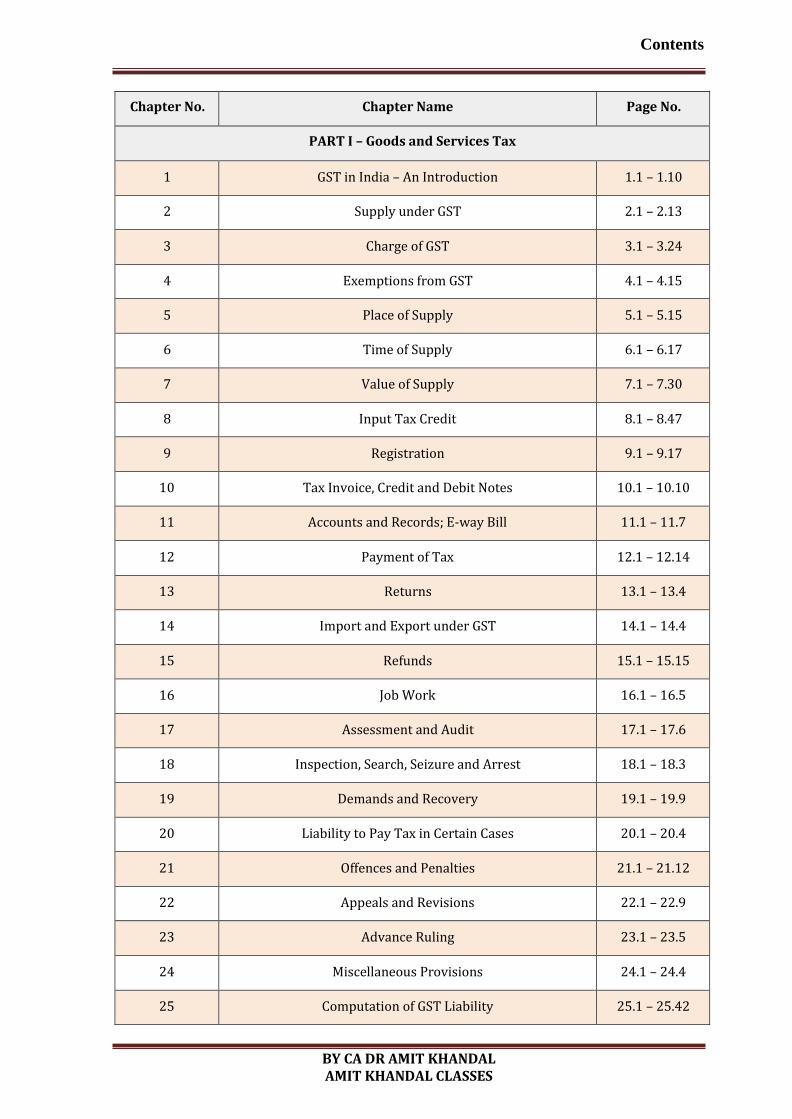

Chapter No. Chapter Name Page No.

PART I – Goods and Services Tax

1 GST in India – An Introduction 1.1 – 1.10

2 Supply under GST 2.1 – 2.13

3 Charge of GST 3.1 – 3.24

4 Exemptions from GST 4.1 – 4.15

5 Place of Supply 5.1 – 5.15

6 Time of Supply 6.1 – 6.17

7 Value of Supply 7.1 – 7.30

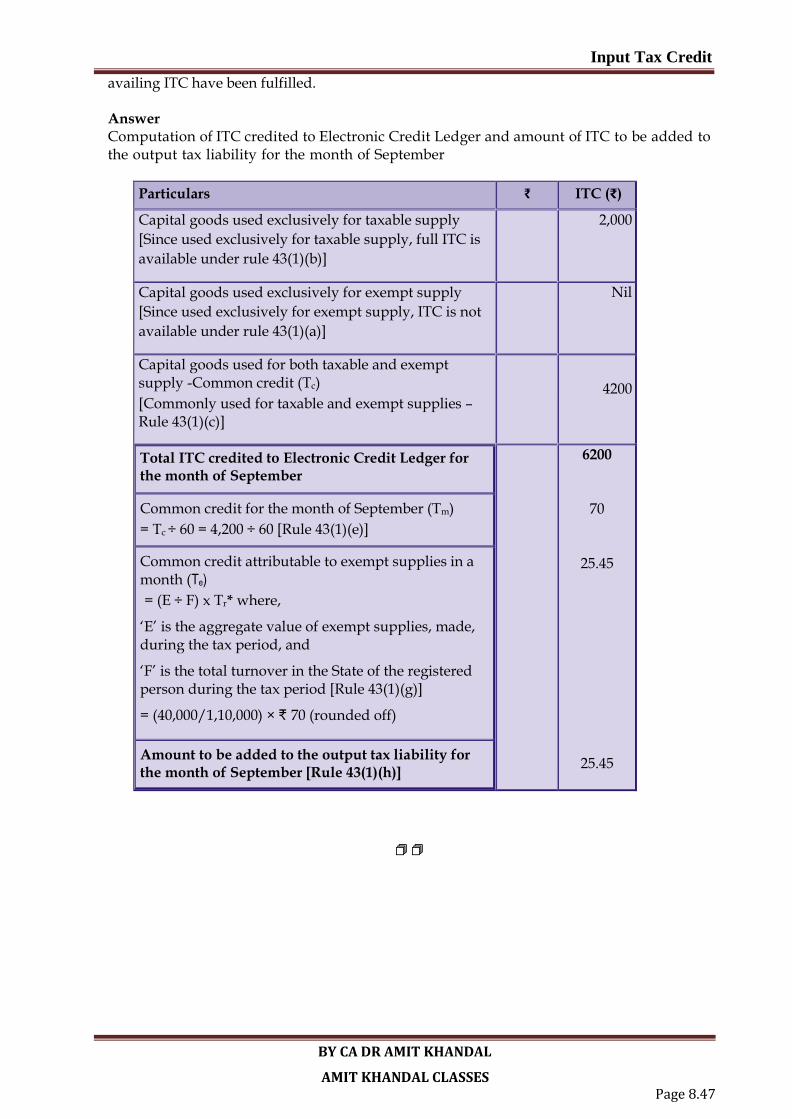

8 Input Tax Credit 8.1 – 8.47

9 Registration 9.1 – 9.17

10 Tax Invoice, Credit and Debit Notes 10.1 – 10.10

11 Accounts and Records; E-way Bill 11.1 – 11.7

12 Payment of Tax 12.1 – 12.14

13 Returns 13.1 – 13.4

14 Import and Export under GST 14.1 – 14.4

15 Refunds 15.1 – 15.15

16 Job Work 16.1 – 16.5

17 Assessment and Audit 17.1 – 17.6

18 Inspection, Search, Seizure and Arrest 18.1 – 18.3

19 Demands and Recovery 19.1 – 19.9

20 Liability to Pay Tax in Certain Cases 20.1 – 20.4

21 Offences and Penalties 21.1 – 21.12

22 Appeals and Revisions 22.1 – 22.9

23 Advance Ruling 23.1 – 23.5

24 Miscellaneous Provisions 24.1 – 24.4

25 Computation of GST Liability 25.1 – 25.42

Downloaded from Studyfromnotes.com - All FREE premium notes

Contents

BY CA DR AMIT KHANDAL AMIT KHANDAL CLASSES

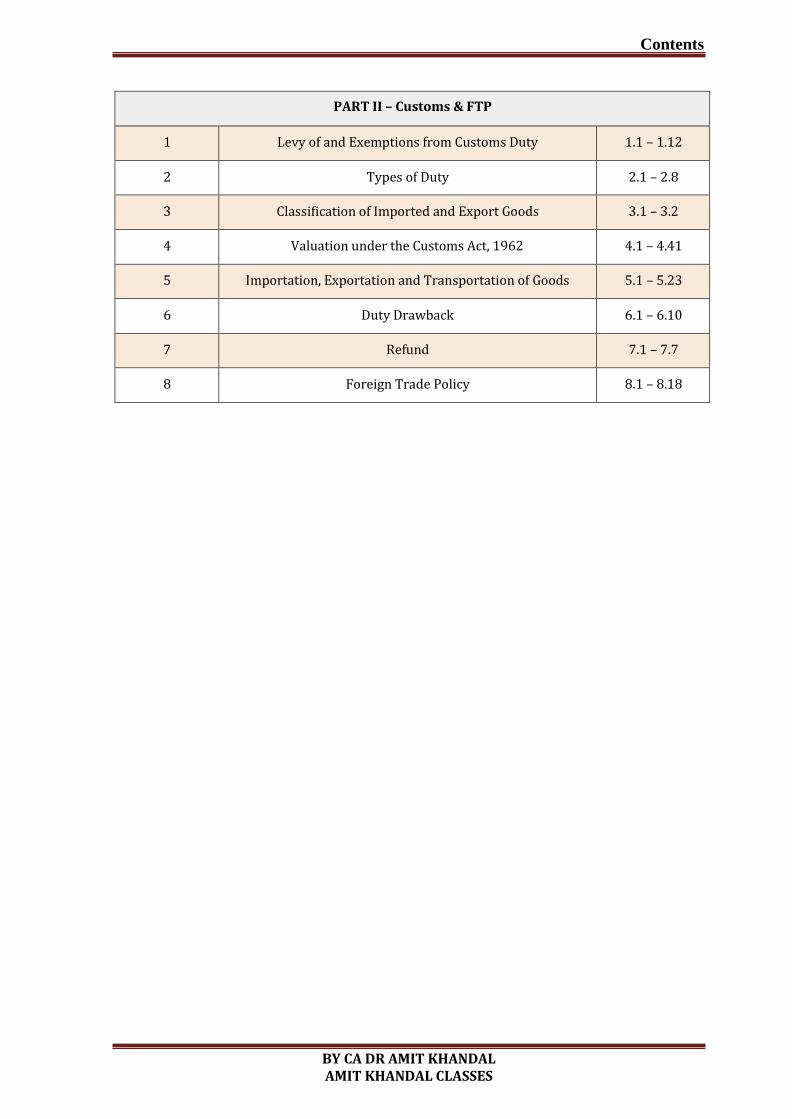

PART II – Customs & FTP

1 Levy of and Exemptions from Customs Duty 1.1 – 1.12

2 Types of Duty 2.1 – 2.8

3 Classification of Imported and Export Goods 3.1 – 3.2

4 Valuation under the Customs Act, 1962 4.1 – 4.41

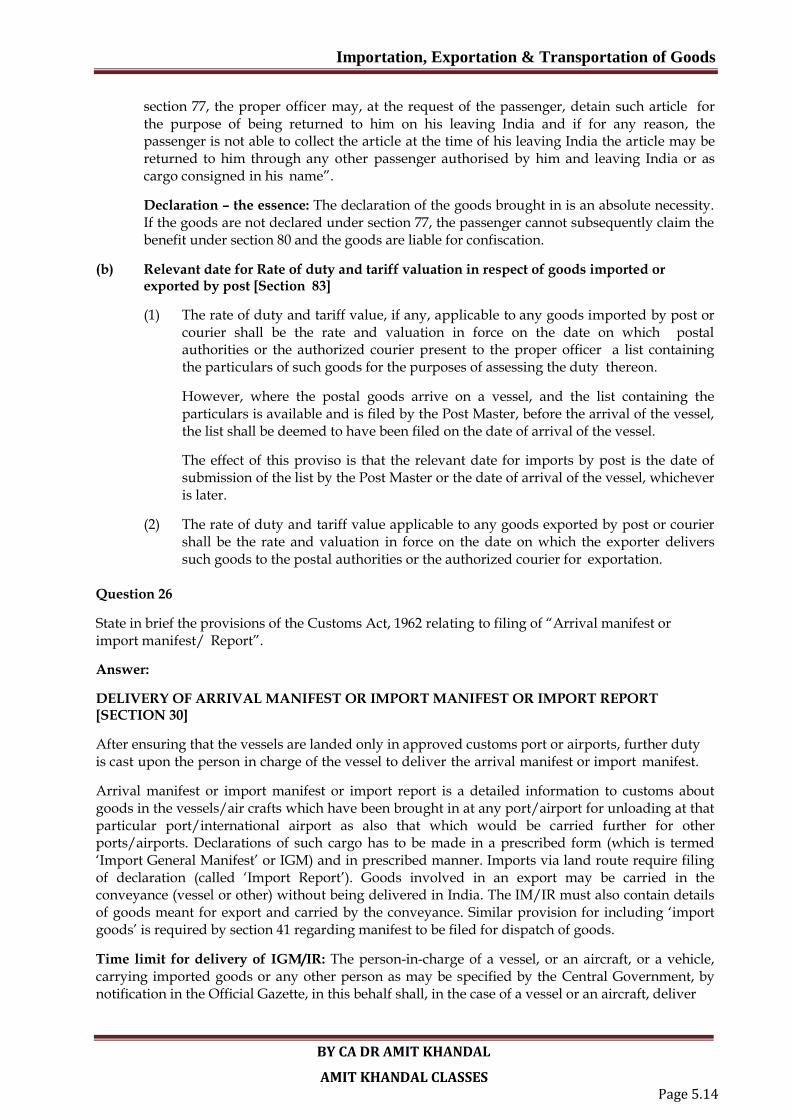

5 Importation, Exportation and Transportation of Goods 5.1 – 5.23

6 Duty Drawback 6.1 – 6.10

7 Refund 7.1 – 7.7

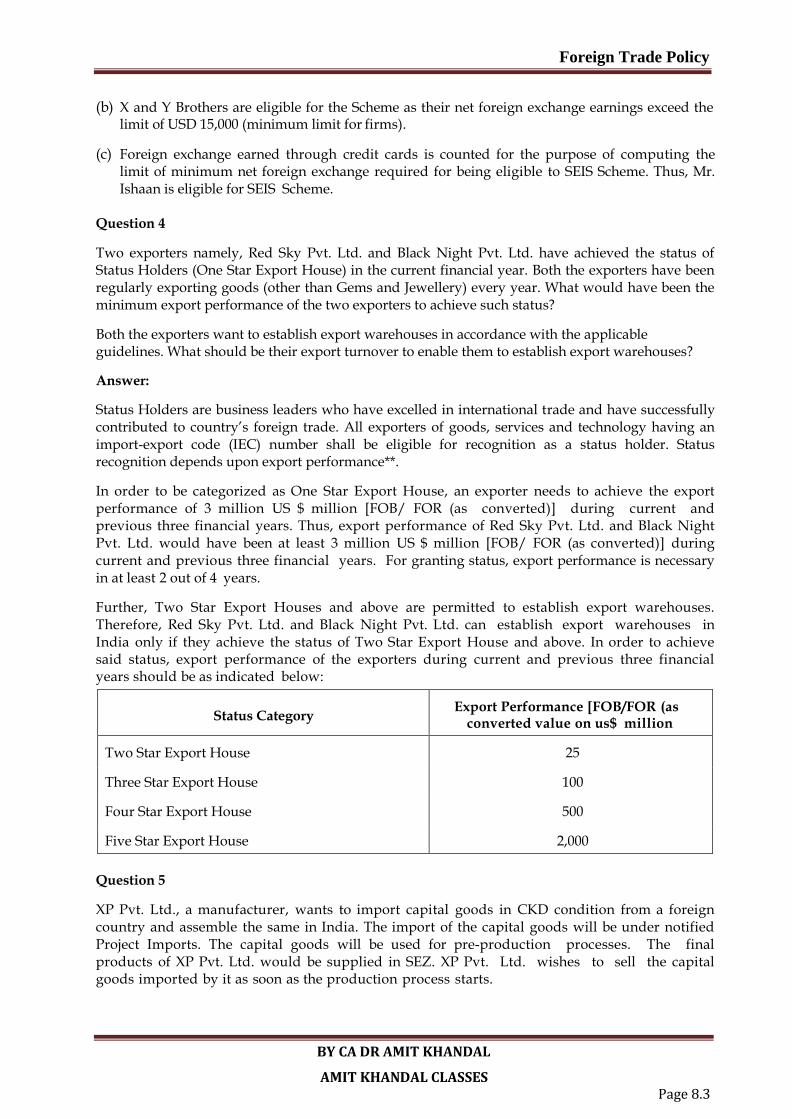

8 Foreign Trade Policy 8.1 – 8.18

Downloaded from Studyfromnotes.com - All FREE premium notes

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 1.1

CHAPTER – 1

GST IN INDIA – AN INTRODUCTION

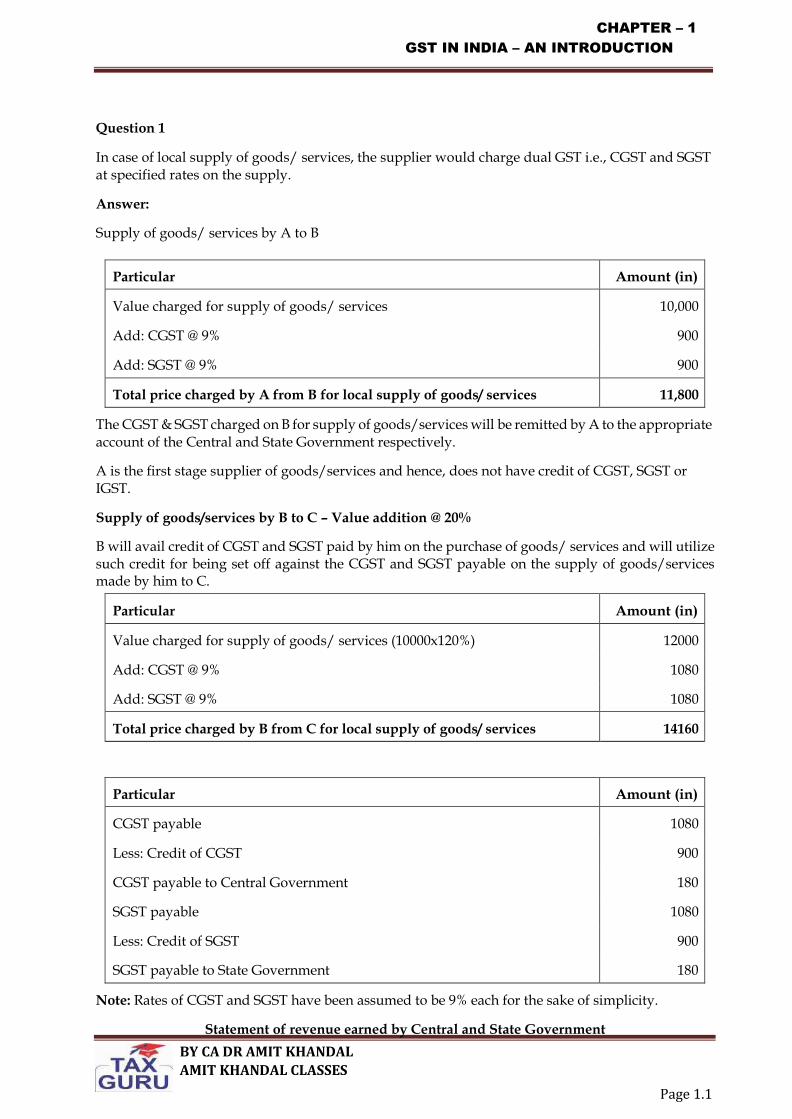

Question 1

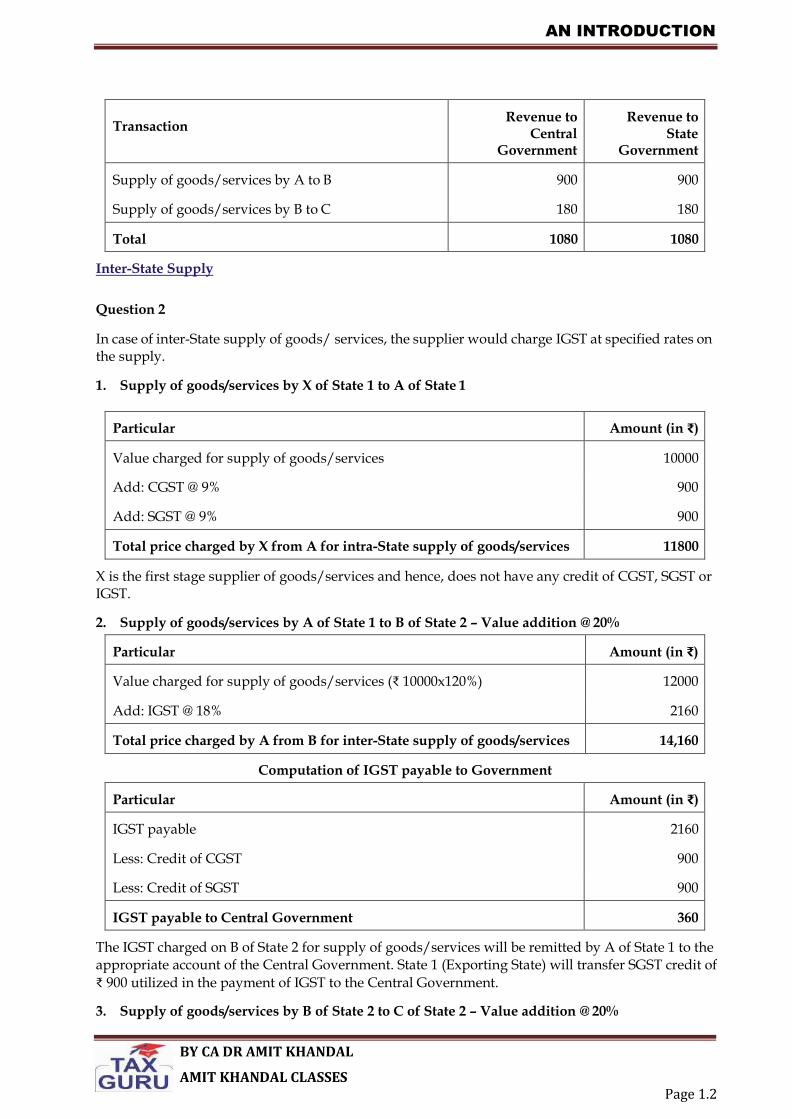

In case of local supply of goods/ services, the supplier would charge dual GST i.e., CGST and SGST at specified rates on the supply.

Answer:

Supply of goods/ services by A to B

Particular Amount (in)

Value charged for supply of goods/ services 10,000

Add: CGST @ 9% 900

Add: SGST @ 9% 900

Total price charged by A from B for local supply of goods/ services 11,800

The CGST & SGST charged on B for supply of goods/services will be remitted by A to the appropriate account of the Central and State Government respectively.

A is the first stage supplier of goods/services and hence, does not have credit of CGST, SGST or IGST.

Supply of goods/services by B to C – Value addition @ 20%

B will avail credit of CGST and SGST paid by him on the purchase of goods/ services and will utilize such credit for being set off against the CGST and SGST payable on the supply of goods/services made by him to C.

Particular Amount (in)

Value charged for supply of goods/ services (10000x120%) 12000

Add: CGST @ 9% 1080

Add: SGST @ 9% 1080

Total price charged by B from C for local supply of goods/ services 14160

Particular Amount (in)

CGST payable 1080

Less: Credit of CGST 900

CGST payable to Central Government 180

SGST payable 1080

Less: Credit of SGST 900

SGST payable to State Government 180

Note: Rates of CGST and SGST have been assumed to be 9% each for the sake of simplicity.

Statement of revenue earned by Central and State Government

Downloaded from Studyfromnotes.com - All FREE premium notes

AN INTRODUCTION

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES Page 1.2

Transaction

Revenue to Central

Government

Revenue to State

Government

Supply of goods/services by A to B

Supply of goods/services by B to C

900

180

900

180

Total 1080 1080

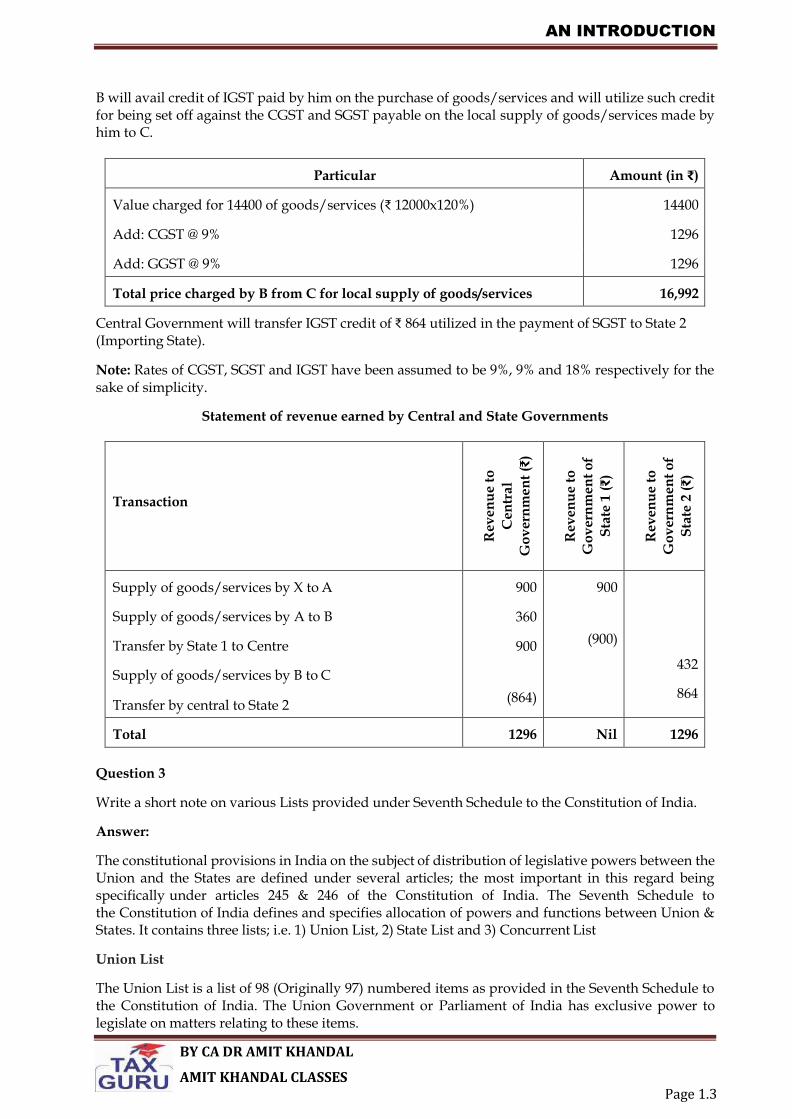

Inter-State Supply

Question 2

In case of inter-State supply of goods/ services, the supplier would charge IGST at specified rates on the supply.

1. Supply of goods/services by X of State 1 to A of State 1

Particular Amount (in ₹)

Value charged for supply of goods/services 10000

Add: CGST @ 9% 900

Add: SGST @ 9% 900

Total price charged by X from A for intra-State supply of goods/services 11800

X is the first stage supplier of goods/services and hence, does not have any credit of CGST, SGST or IGST.

2. Supply of goods/services by A of State 1 to B of State 2 – Value addition @ 20%

Particular Amount (in ₹)

Value charged for supply of goods/services (₹ 10000x120%) 12000

Add: IGST @ 18% 2160

Total price charged by A from B for inter-State supply of goods/services 14,160

Computation of IGST payable to Government

Particular Amount (in ₹)

IGST payable 2160

Less: Credit of CGST 900

Less: Credit of SGST 900

IGST payable to Central Government 360

The IGST charged on B of State 2 for supply of goods/services will be remitted by A of State 1 to the appropriate account of the Central Government. State 1 (Exporting State) will transfer SGST credit of

₹ 900 utilized in the payment of IGST to the Central Government.

3. Supply of goods/services by B of State 2 to C of State 2 – Value addition @ 20%

Downloaded from Studyfromnotes.com - All FREE premium notes

AN INTRODUCTION

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES Page 1.3

B will avail credit of IGST paid by him on the purchase of goods/services and will utilize such credit for being set off against the CGST and SGST payable on the local supply of goods/services made by him to C.

Particular Amount (in ₹)

Value charged for 14400 of goods/services (₹ 12000x120%) 14400

Add: CGST @ 9% 1296

Add: GGST @ 9% 1296

Total price charged by B from C for local supply of goods/services 16,992

Central Government will transfer IGST credit of ₹ 864 utilized in the payment of SGST to State 2 (Importing State).

Note: Rates of CGST, SGST and IGST have been assumed to be 9%, 9% and 18% respectively for the sake of simplicity.

Statement of revenue earned by Central and State Governments

Transaction

R

ev

en

ue t

o

Cen

tral

Go

vern

men

t (₹

)

R

ev

en

ue t

o

Go

vern

men

t o

f

Sta

te 1

(₹)

R

ev

en

ue t

o

Go

vern

men

t o

f

Sta

te 2

(₹)

Supply of goods/services by X to A

Supply of goods/services by A to B

Transfer by State 1 to Centre

Supply of goods/services by B to C

Transfer by central to State 2

900

360

900

(864)

900

(900)

432

864

Total 1296 Nil 1296

Question 3

Write a short note on various Lists provided under Seventh Schedule to the Constitution of India.

Answer:

The constitutional provisions in India on the subject of distribution of legislative powers between the Union and the States are defined under several articles; the most important in this regard being specifically under articles 245 & 246 of the Constitution of India. The Seventh Schedule to the Constitution of India defines and specifies allocation of powers and functions between Union & States. It contains three lists; i.e. 1) Union List, 2) State List and 3) Concurrent List

Union List

The Union List is a list of 98 (Originally 97) numbered items as provided in the Seventh Schedule to the Constitution of India. The Union Government or Parliament of India has exclusive power to legislate on matters relating to these items.

Downloaded from Studyfromnotes.com - All FREE premium notes

AN INTRODUCTION

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES Page 1.4

State List

The State List is a list of 61 (Originally 66) items in the Schedule Seven to the Constitution of India. The respective state governments have exclusive power to legislate on matters relating to these items.

Concurrent List

There are 52 (Originally 47) items currently in the list: This includes items which are under joint domain of the Union as well as the respective States.

Question 4

Discuss how GST resolved the double taxation dichotomy under previous indirect tax laws

Answer:

Before implementation of GST we have Excise Duty, Service Tax and Customs as Indirect Taxes in India at Central Level.

Coming to States every state had its own VAT Laws (Value Added Tax).

In pre-GST regime you will not get credit of Interstate purchases in any State because Inter State purchases will be dealt by CST (Central State Tax).

As there are many laws governing a single transaction and we could not get credit of Tax paid in One law in other law.

But after GST Implementation all these laws were subsumed in to GST Except Customs duty we will be getting credit of all the taxes paid from the stage of Purchase of Raw Material to Stage of Finished Goods.

Question 5

Enumerate the deficiencies of the existing indirect taxes which led to the need for ushering into GST regime.

Answer:

The GST is a welcome step in the Indirect Taxation. The GST is a tax regime which will subsume various tax which are levied currently in India by the Center & the State Authorities. GST will ensure transparency in the indirect tax system and avoid double Taxation. The major change is the avoidance of double taxation which will help in reducing the prices. In the current regime, VAT is charged on an amount inclusive of Excise which happens to be tax on tax, increasing the prices. In the proposed GST regime, dealer will be eligible for Credit on tax paid by his supplier. As states in the Model GST Law as released by the government

The GST would be following matching concept i.e. Statement of Outward Supply filed by the supplier should be in sync with the Statement of Inward Supply filed by the recipient. If the supplier did not file a Statement of Outward Supply or makes an error in his Statement, the recipient would not be eligible for Credit and his return would be deemed to be invalid. The council needs to make sure that suitable mechanism is in place to ensure the taxpayers complying with all the provisions are not denied the benefit.

The GST is the new regime in India which will revolutionize the Indian Taxation System which will be key to bringing India in sync with the world taxation regime which has mostly adopted GST & better understanding in the International markets

Downloaded from Studyfromnotes.com - All FREE premium notes

AN INTRODUCTION

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES Page 1.5

Question 6

Discuss the dual GST model as introduced in India

Dual GST: Many countries in the world have a single unified GST system i.e. a single tax applicable throughout the country. However, in federal countries like Brazil and Canada, a dual GST system is prevalent whereby GST is levied by both the federal and state or provincial governments. In India, a dual GST is proposed whereby a Central Goods and Services Tax (CGST) and a State Goods and Services Tax (SGST) will be levied on the taxable value of every transaction of supply of goods and services.

Impact on Prices of Goods and Services: The GST is expected to foster increased efficiencies in the economic system thereby lowering the cost of supply of goods and services. Further, in the Indian context, there is an expectation that the aggregate incidence of the dual GST will be lower than the present incidence of the multiple indirect taxes in force. Consequently, the implementation of the GST is expected to bring about, if not in the near term but in the medium to long term, a reduction in the prices of goods and services. The expectation is that the dealers would start passing on the benefit of the reduced tax incidence to the customers by way of reduced prices. As regards services, it could be that their short-term prices would go up given the expectation of an increase in the tax rate from the present 10% to approximately 14% to 16%.

Benefits of Dual GST: The Dual GST is expected to be a simple and transparent tax with one or two CGST and SGST rates. The dual GST is expected to result in:-

reduction in the number of taxes at the Central and State level

decrease in effective tax rate for many goods

removal of the current cascading effect of taxes

reduction of transaction costs of the taxpayers through simplified tax compliance

increased tax collections due to wider tax base and better compliance

Question 7

List the Central and State levies which have been subsumed in GST in India.

Answer:

Central Indirect Taxes:

Downloaded from Studyfromnotes.com - All FREE premium notes

AN INTRODUCTION

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES Page 1.6

Following Central Indirect Taxes and Levies would be subsumed in GST:

Central Excise Duty

Additional Excise Duties

Excise Duty levied under the Medicinal and Toilet Preparations (Excise Duties) Act, 1955

Service Tax

Additional Customs Duty commonly known as Countervailing Duty

Special Additional Duty of Customs

Central Surcharges and Cess, so far as they relate to the supply of goods and services.

State Indirect Taxes:

Following State Indirect Taxes and Levies would be subsumed in GST:

State Value Added Tax/Sales Tax

Entertainment Tax (other than the tax levied by the local bodies)

Central Sales Tax (levied by the Centre and collected by the States)

Octroi and Entry Tax

Purchase Tax

Luxury Tax

Taxes on lottery

Betting and gambling

State cess and surcharges insofar as they relate to supply of goods and services.

The above taxes are directly relatable to the supply of goods and services and fall in the supply chain from the point of procurement of the raw material to the consumption of the goods and services by the end customer.

Question 8

List some of the benefits that GST to accrues to the economy.

Answer :

GST accrues following benefits to the economy:

(a) Creation of unified national market: GST has made India a common market with

common tax rates and procedures. Further, it has removed the economic barriers

resulting in an integrated economy at the national level.

(b) Boost to ‘Make in India' initiative: GST has given a major boost to the ‘Make in India'

initiative of the Government of India by making goods and services produced in India

competitive in the national as well as international market. This will make India a

manufacturing hub.

(c) Enhanced investment and employment: The subsuming of major Central and State

taxes in GST, complete and comprehensive set-off of input tax on goods and services and

phasing out of Central Sales Tax (CST) has reduced the cost of locally manufactured

Downloaded from Studyfromnotes.com - All FREE premium notes

AN INTRODUCTION

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES Page 1.7

goods and services. Resultantly, the competitiveness of Indian goods and services in

the international market has increased which has given boost to investments and

Indian exports. With a boost in exports and manufacturing activity, more employment

is likely to be generated and GDP is likely to be increased.

Question 9

Explain with the help of examples how a particular transaction of goods and services is taxed simultaneously under Central GST (CGST) and State GST (SGST)?

Answer :

The Central GST and the State GST is levied simultaneously on every intra-State supply of goods or services or both made by registered persons except the exempted goods and services as well as goods and services which are outside the purview of GST. Further, both are levied on the same price or value. The same can be better understood with the help of following examples:

Example I: Suppose that the rate of CGST is 10% and that of SGST is 10%. When a wholesale dealer of steel in Uttar Pradesh supplies steel bars and rods to a construction company which is also located within the same State for, say ₹ 100, the dealer would charge CGST of ₹ 10 and SGST of ₹ 10 in addition to the basic price of the goods. He would be required to deposit the CGST component into a Central Government account while the SGST portion into the account of the concerned State Government (viz. U.P.). It is important to note that he might not actually pay ₹ 20 (₹ 10 + ₹ 10) in cash as he would be entitled to set-off this liability against the CGST or SGST paid on his eligible purchases (inputs, input services and capital goods) assuming that all his purchases are intra-State. However, for paying CGST, he would be allowed to use only the credit of CGST paid on his purchases while for U.P. GST he can utilize the credit of U.P. GST alone. In other words, CGST credit cannot, in general, be used for payment of SGST. Nor can SGST credit be used for payment of CGST.

Example II: Suppose, again the rate of CGST is 10% and that of SGST is 10%. When an advertising company located in Mumbai supplies advertising services to a company manufacturing soap also located within the State of Maharashtra for, let us say ₹ 100, the ad company would charge CGST of ₹ 10 as well as Maharashtra GST of ₹ 10 at the basic value of the service. He would be required to deposit the CGST component into a Central Government account while the Maharashtra GST portion into the account of the Maharashtra Government. He might not actually pay ₹ 20 (₹ 10+₹ 10) in cash as it would be entitled to set-off this liability against the CGST or SGST paid on his eligible purchases (say, of inputs such as stationery, office equipment, services of an artist etc.) assuming that all his purchases are intra-State. However, for paying CGST, he would be allowed to use only the credit of CGST paid on its purchase while for Maharashtra GST, he can utilise the credit of Maharashtra GST alone. In other words, CGST credit cannot, in general, be used for payment of SGST. Nor can SGST credit be used for payment of CGST.

Question 10

Why was the need to amend the Constitution of India before introducing the GST?

Answer :

Earlier, the fiscal powers between the Centre and the States were clearly demarcated in the Constitution with almost no overlap between the respective domains. The Centre had the powers to levy tax on the manufacture of goods (except alcoholic liquor for human consumption, opium, narcotics etc.) while the States had the powers to levy tax on the sale of goods. In the case of inter- State sales, the Centre had the power to levy the Central Sales Tax but the tax was collected and retained entirely by the States. As for services, it was the Centre alone that was empowered to levy service tax.

Introduction of the GST necessitated the amendments in the Constitution so as to simultaneously empower the Centre and the States to levy and collect this tax. The Constitution of India was amended by the Constitution (101st Amendment) Act, 2016 for this purpose. Article 246A of the

Downloaded from Studyfromnotes.com - All FREE premium notes

AN INTRODUCTION

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES Page 1.8

Constitution introduced thereby empowered the Centre and the States to simultaneously levy and collect the GST.

Question 11

GST is a destination-based tax on consumption of goods or services or both. Discuss the

validity of the statement

Answer :

The given statement is valid. GST is a destination-based tax on consumption of goods or services or both. GST is known as destination-based tax since the tax would accrue to the taxing authority which has jurisdiction over the place of consumption which is also termed as place of supply.

For example, if A in Delhi produces the goods and sells the goods to B in Haryana. In this case, the tax would accrue to the State of Haryana and not to the State of Delhi. On the other hand, under pre-GST regime, origin-based taxation was prevailing in such cases. Under origin-based taxation, the tax used to accrue to the State from where the transaction originated. In the given case, under origin-based taxation, the central sales tax would have been levied by Centre and collected by the State of Delhi and not by the State of Haryana.

Question 12

Discuss the leviability of GST or otherwise on the following:

(a) Alcoholic liquor for human consumption

(b) Petroleum crude, diesel, petrol, ATF and natural gas

(c) Tobacco

(d) Opium, Indian hemp and other narcotic drugs and narcotics

Answer :

(a) Alcoholic liquor for human consumption: is outside the realm of GST. The manufacture/production of alcoholic liquor continues to be subjected to State excise duty and inter-State/intra-State sale of the same is subject to CST/VAT respectively.

(b) Petroleum crude, diesel, petrol, ATF and natural gas: As regards petroleum crude, diesel, petrol, ATF and natural gas are concerned, they are not presently leviable to GST. GST will be levied on these products from a date to be notified on the recommendations of the GST Council.

Till such date, central excise duty continues to be levied on manufacture/production of petroleum crude, diesel, petrol, ATF and

natural gas and inter-State/intra-State sale of the same is subject to CST/ VAT respectively.

(c) Tobacco: Tobacco is within the purview of GST, i.e. GST is leviable on tobacco. However, Union Government has also retained the power to levy excise duties on tobacco and tobacco products manufactured in India. Resultantly, tobacco is subject to GST as well as central excise duty.

(d) Opium, Indian hemp and other narcotic drugs and narcotics: Opium, Indian hemp and other narcotic drugs and narcotics are within the purview of GST, i.e. GST is leviable on them. However, State Governments have also retained the power to levy excise duties on such products manufactured in India. Resultantly, Opium, Indian hemp and other narcotic drugs and narcotics are subject to GST as well as State excise duties.

natural gas and inter-State/intra-State sale of the same is subject to CST/ VAT

Downloaded from Studyfromnotes.com - All FREE premium notes

AN INTRODUCTION

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES Page 1.9

respectively.

(e) Tobacco: Tobacco is within the purview of GST, i.e. GST is leviable on tobacco. However, Union Government has also retained the power to levy excise duties on tobacco and tobacco products manufactured in India. Resultantly, tobacco is subject to GST as well as central excise duty.

(f) Opium, Indian hemp and other narcotic drugs and narcotics: Opium, Indian hemp and other narcotic drugs and narcotics are within the purview of GST, i.e. GST is leviable on them. However, State Governments have also retained the power to levy excise duties on such products manufactured in India. Resultantly, Opium, Indian hemp and other narcotic drugs and narcotics are subject to GST as well as State excise duties.

Question 13

Under Goods and Services Tax (GST), only value addition is taxed and burden of tax is to be borne by the final consumer. Examine the statement.

Answer :

The statement is correct. Goods and Services Tax is a destination-based tax on consumption of goods and services. It is levied at all stages right from manufacture up to final consumption with credit of taxes paid at previous stages available as setoff. Resultantly, only value addition is taxed and burden of tax is to be borne by the final consumer.

Question 14

Which are the commodities which have been kept outside the purview of GST? Examine the status of taxation of such commodities after introduction of GST?

Answer :

Article 366(12A) of the Constitution as amended by 101st Constitutional Amendment Act, 2016 defines the Goods and Services tax (GST) as a tax on supply of goods or services or both, except supply of alcoholic liquor for human consumption. Therefore, alcohol for human consumption is kept out of GST by way of definition of GST in the Constitution. Five petroleum products viz. petroleum crude, motor spirit (petrol), high speed diesel, natural gas and aviation turbine fuel have temporarily been kept out of the purview of GST; GST Council shall decide the date from which they shall be included in GST. The erstwhile taxation system (CST/VAT & central excise) still continues in respect of the said commodities.

Question 15

Discuss Article 269A pertaining to levy and collection of GST on inter-State supply. Answer :

Article 269A of the Constitution stipulates that Goods and Services Tax on supplies in the course of inter-State trade or commerce shall be levied and collected by the Government of India and such tax shall be apportioned between the Union and the States in the manner as may be provided by Parliament by law on the recommendations of the Goods and Services Tax Council.

Here, supply of goods, or of services, or both in the course of import into the territory of India shall be deemed to be supply of goods, or of services, or both in the course of inter-State trade or commerce.

The amount so apportioned to a State shall not form part of the Consolidated Fund of India. Where an amount collected as IGST has been used for payment of SGST or vice versa, such amount shall not form part of the Consolidated Fund of India/State respectively. This is to facilitate transfer of funds between the Centre and the States.

Parliament is empowered to formulate the principles for determining the place of supply, and when a supply of goods, or of services, or both takes place in the course of inter-State trade or commerce.

Downloaded from Studyfromnotes.com - All FREE premium notes

AN INTRODUCTION

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES Page 1.10

Discuss Article 246A which grants the power to make laws with respect to Goods and Services Tax.

Article 246A stipulates that Parliament, and, the Legislature of every State, have power to make laws with respect to goods and services tax imposed by the Union or by such State.

Parliament has exclusive power to make laws with respect to goods and services tax where the supply of goods, or of services, or both takes place in the course of inter-State trade or commerce.

However, in respect to petroleum crude, high speed diesel, motor spirit (commonly known as petrol), natural gas and aviation turbine fuel, the aforesaid provisions shall apply from the date to be notified by the Government on the recommendations by the GST Council.

Downloaded from Studyfromnotes.com - All FREE premium notes

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.1

CHAPTER - 2

SUPPLY UNDER GST

Question 1

What is the taxable event under GST?

Answer:

Taxable event under GST is supply of goods or services or both. CGST and SGST/ UTGST will be levied on intra-State supplies. IGST will be levied on inter-State supplies.

Question 2

What is the tax treatment of composite supply and mixed supply under GST?

Answer:

Composite supply shall be treated as supply of the principal supply. Mixed supply would be treated as supply of that particular goods or services which attracts the highest rate of tax.

Question 3

Whether transfer of title and/or possession is necessary for a transaction to constitute supply of goods?

Answer:

Title as well as possession both have to be transferred for a transaction to be considered as a supply of goods. In case title is not transferred, the transaction would be treated as supply of service in terms of Schedule II (1) (b) of the CGST Act. In some cases, possession may be transferred immediately but title may be transferred at a future date like in case of sale on approval basis or hire purchase arrangement. Such transactions will also be termed as supply of goods.

Question 4

Examine whether the following activities would amount to supply under section 7 read with Schedule I of the CGST Act:

a. Sulekha Manufacturers have a factory in Delhi and a depot in Mumbai. Both these establishments are registered in respective States. Finished goods are sent from factory in Delhi to the Mumbai depot without consideration so that the same can be sold.

Answer:

Title as well as possession both have to be transferred for a transaction to be considered as a supply of goods. In case title is not transferred, the transaction would be treated as supply of service in terms of Schedule II (1)(b) of the CGST Act. In some cases, possession may be transferred immediately but title may be transferred at a future date like in case of sale on approval basis or hire purchase arrangement. Such transactions will also be termed as supply of goods.

b. Raman is an architect in Chennai. His brother who is settled in London is a well-known lawyer. Raman has taken legal advice from him free of cost with regard to his family dispute.

Answer: Schedule I of CGST Act, inter alia, stipulates that import of services by a taxable person from a related person located outside India, without consideration is treated as supply if it is provided in the course or furtherance of business. Explanation to section 15, inter alia, provides that

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.2

persons shall be deemed to be “related persons” if they are members of the same family. Further, as per section 2(49) of the CGST Act, 2017, family means, —

i. the spouse and children of the person, and

ii. the parents, grand-parents, brothers and sisters of the person if they are wholly or mainly dependent on the said person.

In the given case, Raman has received free of cost legal services from his brother. However, in view of section 2(49)(ii) above, Raman and his brother cannot be considered to be related as Raman’s brother is a well-known lawyer and is not wholly/mainly dependent on Raman. Further, Raman has taken legal advice from him in personal matter and not in course or furtherance of business. Consequently, services provided by Raman’s brother to him would not be treated as supply under section 7 of the CGST Act read with Schedule.

c. Would your answer be different if in the above case, Raman has taken advice in respect of his business unit in Chennai?

Answer: In the above case, if Raman has taken advice with regard to his business unit, services provided by Raman’s brother to him would still not be treated as supply under section 7 of the CGST Act read with Schedule I as although the same are provided in course or furtherance of business, such services have not been received from a related person.

Question 5

State whether the following supplies would be treated as supply of goods or supply of services as per Schedule II of the CGST Act

a) Renting of immovable property

b) Goods forming part of business assets are transferred or disposed of by/under directions of person carrying on the business, whether or not for consideration.

c) Transfer of right in goods without transfer of title in goods.

d) Transfer of title in goods under an agreement which stipulates that property shall pass at a future date

Answer:

a) Supply of services

b) Supply of goods

c) Supply of services

d) Supply of goods

Question 6

Determine whether the following supplies amount to composite supplies

a. A hotel provides 4 days-3 night’s package wherein the facility of breakfast and dinner is provided

along with the room accommodation.

b. A toothpaste company has offered the scheme of free toothbrush along with the toothpaste.

Answer:

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.3

Under composite supply, two or more taxable supplies of goods or services or both, or any combination thereof, are naturally bundled and supplied in conjunction with each other, in the ordinary course of business, one of which is a principal supply [Section 2(30) of the CGST Act]. In view of the same,

(a) since, supply of breakfast and dinner with the accommodation in the hotel are naturally bundled, said supplies qualify as ‘composite supply’.

(b) since supply of toothbrush along with the toothpaste are not naturally bundled, said supplies do not qualify as ‘composite supply’

Question 7

Whether goods supplied on hire purchase basis will be treated as supply of goods or supply of services? Give reason.

Answer:

Supply of goods on hire purchase shall be treated as supply of goods as there is transfer of title, albeit at a future date

Question 8

Diligent Force, a professional training institute, gets its training material of ‘Aptitute Quotient’ printed from ‘Durga Printing House’ - a printing press. The content of the material is provided by the Diligent Force who owns the usage rights of the same while the physical inputs including paper used for printing belong to the Durga Printing House.

Ascertain whether supply of training material by the Durga Printing House constitutes supply of goods or supply of services

Answer:

Circular No. 11/11/2017 GST dated 20.10.2017 has clarified that supply of books printed with contents supplied by the recipient of such printed goods, is composite supply and the question, whether such supplies constitute supply of goods or services would be determined on the basis of what constitutes the principal supply.

Principal supply has been defined in section 2(90) of the CGST Act, 2017 as supply of goods or services which constitutes the predominant element of a composite supply and to which any other supply forming part of that composite supply is ancillary.

In the case of printing of books where content is supplied by the publisher or the person who owns the usage rights to the intangible inputs while the physical inputs including paper used for printing belong to the printer, supply of printing [of the content supplied by the recipient of supply] is the principal supply and therefore, such supplies would constitute supply of service.

Thus, in view of the above-mentioned provisions, the supply of training material by the Durga Printing House would constitute supply of services.

Question 9

Agrawal Carriers is a Goods Transport Agency (GTA) which is engaged in transportation of goods by road. As per the general business practice, Agrawal Carriers also provides intermediary and

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.4

ancillary services like loading/ unloading, packing/ unpacking, transhipment and temporary warehousing, in relation to transportation of goods by road. With reference to the provisions of GST law, analyze whether such services are to be treated as part of the GTA service, being a composite supply, or as separate supplies.

Answer:

Composite supply means a supply made by a taxable person to a recipient consisting of two or more taxable supplies of goods or services or both, or any combination thereof, which are naturally bundled and supplied in conjunction with each other in the ordinary course of business, one of which is a principal supply [Section 2(30) of the CGST Act, 2017].

Mixed supply means two or more individual supplies of goods or services, or any combination thereof, made in conjunction with each other by a taxable per son for a single price where such supply does not constitute a composite supply [Section 2(74) of the CGST Act, 2017].

The various intermediary and ancillary services provided by GTA are not provided as independent services, but as ancillary to the principal service, namely, transportation of goods by road. The invoice issued by the GTA for providing the said service includes the value of intermediary and ancillary services. In view of this, if any intermediary and ancillary service is provided in relation to transportation of goods by road, and charges, if any, for such services are included in the invoice issued by Aggarwal Carriers, such service would form part of the GTA service, and thus will be composite supply, and not a mixed supply even though a single price is charged for the supply.

Further, if such incidental services are provided as separate services and are billed separately, whether in the same invoice or separate invoices, they will be treated as separate supply and not composite supply and there being no single price, the supply will also not be treated as mixed supply.

Question 10

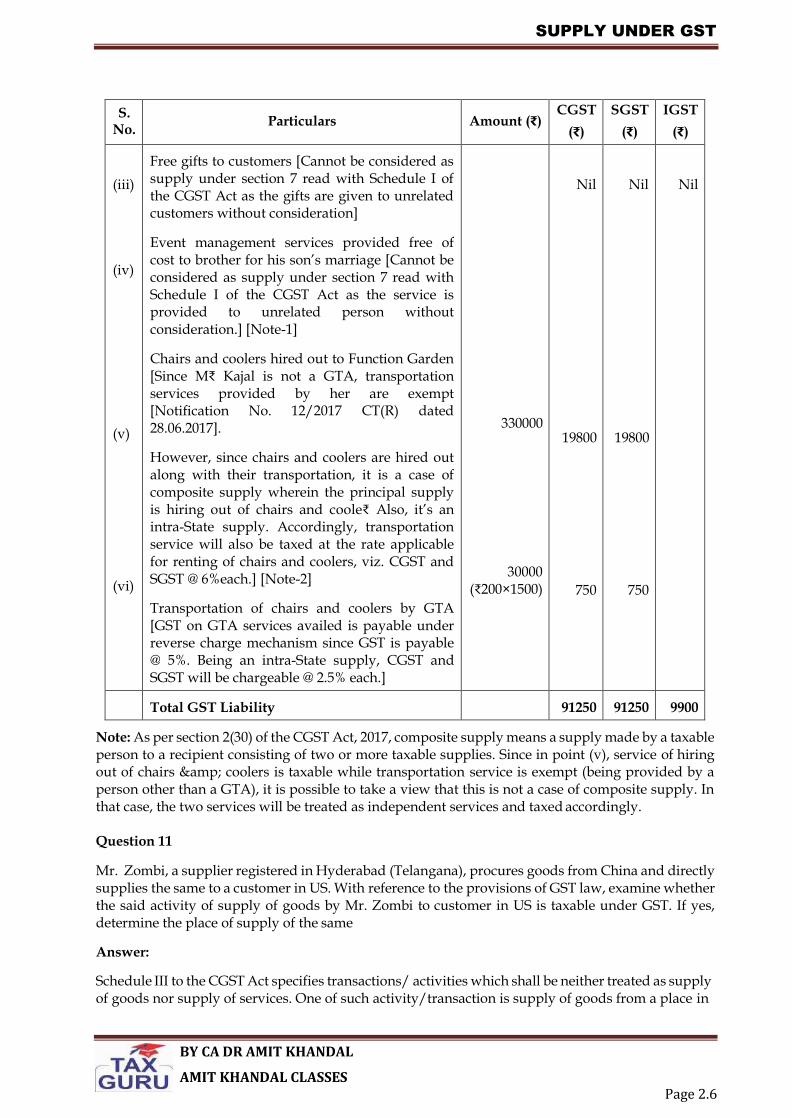

M₹ Kajal, a registered supplier of Jaipur (Rajasthan), has made the following supplies in the month of January, 20XX:

a. Supply of a laptop bag along with the laptop to a customer of Mumbai for ₹ 55,000 (exclusive of GST).

b. Supply of 10,000 kits (at ₹ 50 each) amounting to ₹ 5,00,000 (exclusive of GST) to Ram Fancy Store in Kota (Rajasthan). Each kit consists of 1 hair oil, 1 beauty soap and 1 hair comb.

c. 100 kits are given as free gift to Jaipur customers on the occasion of M₹ Kajal's birthday. Each kit consists of 1 hair oil and 1 beauty soap. Cost of each kit is ₹ 35, but the open market value of such kit of goods and of goods of like kind and quality is not available. Input tax credit has not been taken on the goods contained in the kit.

d. Event management services provided free of cost to her brother for his son’s marriage function in Indore (Madhya Pradesh). Cost of providing said services is ₹ 80,000, but the open market value of such services and of services of like kind and quality is not available.

e. 1,400 chairs and 100 coolers hired out to Function Garden, Ajmer (Rajasthan) for ₹ 3,30,000 (exclusive of GST) including cost of transporting the chairs and coolers from M₹ Kajal's godown at Jaipur to the Function Garden, Ajmer.

M₹ Kajal has paid the cost of transportation of chairs and coolers to an unregistered Goods Transport Agency (GTA) [located in the State of Rajasthan] @ ₹ 20 (exclusive of GST) for each chair and each cooler and in turn, has charged ₹ 20 only for each chair and each cooler from Function Garden for transportation of the same.

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.5

Interest of ₹ 6,400 (inclusive of GST) was collected by M₹ Kajal in January from Ram Fancy Store, Kota for the payment received with a delay of 30 days.

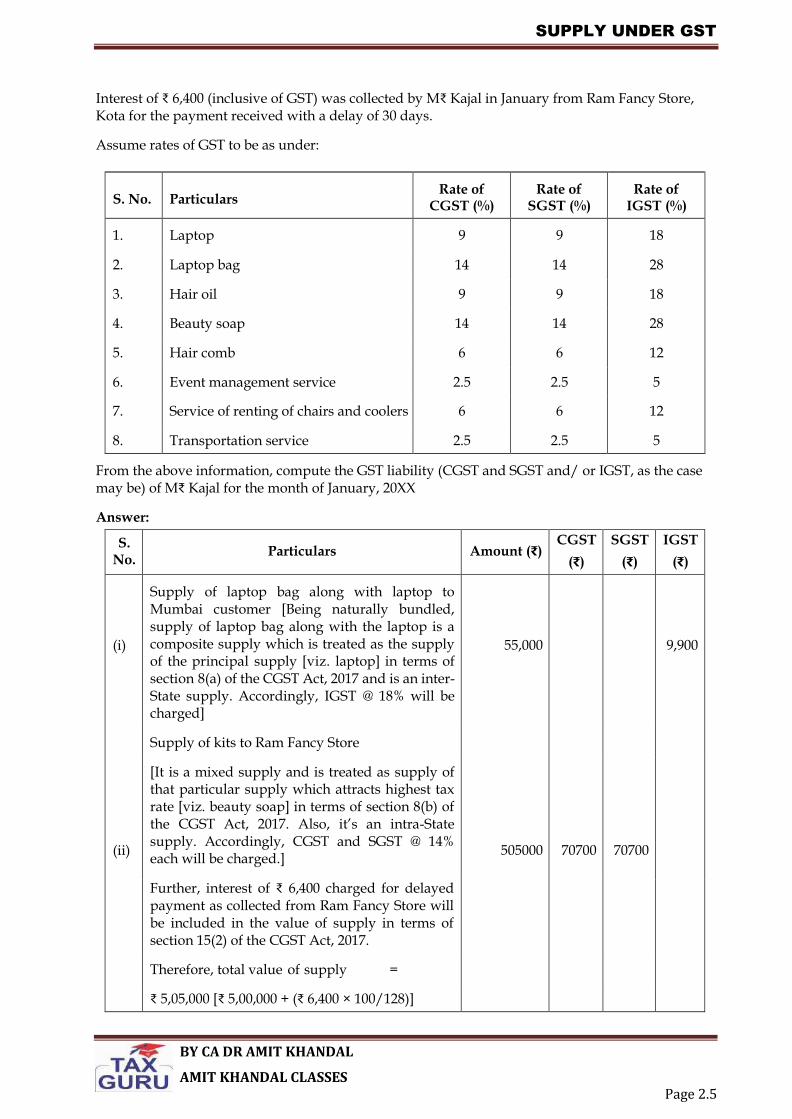

Assume rates of GST to be as under:

S. No.

Particulars

Rate of CGST (%)

Rate of SGST (%)

Rate of IGST (%)

1. Laptop 9 9 18

2. Laptop bag 14 14 28

3. Hair oil 9 9 18

4. Beauty soap 14 14 28

5. Hair comb 6 6 12

6. Event management service 2.5 2.5 5

7. Service of renting of chairs and coolers 6 6 12

8. Transportation service 2.5 2.5 5

From the above information, compute the GST liability (CGST and SGST and/ or IGST, as the case may be) of M₹ Kajal for the month of January, 20XX

Answer:

S. No.

Particulars Amount (₹) CGST

(₹)

SGST

(₹)

IGST

(₹)

(i)

Supply of laptop bag along with laptop to Mumbai customer [Being naturally bundled, supply of laptop bag along with the laptop is a composite supply which is treated as the supply of the principal supply [viz. laptop] in terms of section 8(a) of the CGST Act, 2017 and is an inter- State supply. Accordingly, IGST @ 18% will be charged]

55,000

9,900

Supply of kits to Ram Fancy Store

(ii)

[It is a mixed supply and is treated as supply of that particular supply which attracts highest tax rate [viz. beauty soap] in terms of section 8(b) of the CGST Act, 2017. Also, it’s an intra-State supply. Accordingly, CGST and SGST @ 14% each will be charged.]

505000

70700

70700

Further, interest of ₹ 6,400 charged for delayed payment as collected from Ram Fancy Store will be included in the value of supply in terms of section 15(2) of the CGST Act, 2017.

Therefore, total value of supply =

₹ 5,05,000 [₹ 5,00,000 + (₹ 6,400 × 100/128)]

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.6

S. No.

Particulars Amount (₹) CGST

(₹)

SGST

(₹)

IGST

(₹)

(iii)

(iv)

(v)

(vi)

Free gifts to customers [Cannot be considered as supply under section 7 read with Schedule I of the CGST Act as the gifts are given to unrelated customers without consideration]

Event management services provided free of cost to brother for his son’s marriage [Cannot be considered as supply under section 7 read with Schedule I of the CGST Act as the service is provided to unrelated person without consideration.] [Note-1]

Chairs and coolers hired out to Function Garden [Since M₹ Kajal is not a GTA, transportation services provided by her are exempt [Notification No. 12/2017 CT(R) dated 28.06.2017].

However, since chairs and coolers are hired out along with their transportation, it is a case of composite supply wherein the principal supply is hiring out of chairs and coole₹ Also, it’s an intra-State supply. Accordingly, transportation service will also be taxed at the rate applicable for renting of chairs and coolers, viz. CGST and SGST @ 6%each.] [Note-2]

Transportation of chairs and coolers by GTA [GST on GTA services availed is payable under reverse charge mechanism since GST is payable @ 5%. Being an intra-State supply, CGST and SGST will be chargeable @ 2.5% each.]

330000

30000 (₹200×1500)

Nil

19800

750

Nil

19800

750

Nil

Total GST Liability

91250 91250 9900

Note: As per section 2(30) of the CGST Act, 2017, composite supply means a supply made by a taxable person to a recipient consisting of two or more taxable supplies. Since in point (v), service of hiring out of chairs & coolers is taxable while transportation service is exempt (being provided by a person other than a GTA), it is possible to take a view that this is not a case of composite supply. In that case, the two services will be treated as independent services and taxed accordingly.

Question 11

Mr. Zombi, a supplier registered in Hyderabad (Telangana), procures goods from China and directly supplies the same to a customer in US. With reference to the provisions of GST law, examine whether the said activity of supply of goods by Mr. Zombi to customer in US is taxable under GST. If yes, determine the place of supply of the same

Answer:

Schedule III to the CGST Act specifies transactions/ activities which shall be neither treated as supply of goods nor supply of services. One of such activity/transaction is supply of goods from a place in

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.7

the non-taxable territory to another place in the non-taxable territory without such goods entering into India. Thus, it seeks to exclude from the tax net such transactions which involve movement of goods, caused by a registered person, from one non-taxable territory to another non-taxable territory.

Therefore, in view of the above-mentioned provisions, the said activity is not a supply. Hence, it is not leviable to GST since “supply” is the taxable event for chargeability of GST. Therefore, since the transaction is not leviable to GST, the question of place of supply does not arise in the given case.

Question 12

Satyamev Printers is a printing house registered under GST. It receives an order for printing 5000 copies of a book on yoga and meditation authored by a well-known yoga guru. The content of the book is to be provided by the yoga guru to Satyamev Printers. It is agreed that Satyamev Printers will use its own paper to print the said books.

You are required to determine the rate of GST applicable on supply of printed books by Satyamev Printers assuming that rate of GST applicable on printing services is 18% whereas the rate of GST applicable on supply of paper used in printing the books is 12%.

Answer:

Satyamev Printers is a printing house registered under GST. It receives an order for printing 5000 copies of a book on yoga and meditation authored by a well-known yoga guru. The content of the book is to be provided by the yoga guru to Satyamev Printers. It is agreed that Satyamev Printers will use its own paper to print the said books.

You are required to determine the rate of GST applicable on supply of printed books by Satyamev Printers assuming that rate of GST applicable on printing services is 18% whereas the rate of GST applicable on supply of paper used in printing the books is 12%.

Question 13

Answer the following questions:

(a) Sudama Associates, a registered supplier, disposes the computers owned by the business without consideration and it has not claimed input tax credit on such computers.

Examine whether the disposal of computers by Sudama Associates qualifies as deemed supply under Schedule I of the CGST Act.

(b) Prithvi Enterprises appoints Champak to procure certain goods from the market. Champak identifies various suppliers who can provide the goods as desired by Prithvi Enterprises, and asks a supplier – Satya Manufacturers to send the goods and issue the invoice directly to Prithvi Enterprises.

You are required to determine whether Champak can be considered as an agent of Prithvi Enterprises in terms of Schedule I of the CGST Act.

Answer :

(a) As per section 7(1)(c) read with Schedule I of the CGST Act, permanent transfer or disposal of business assets is treated as supply even though the same is made without consideration. However, this provision would apply only if input tax credit has been availed on such assets. Therefore, the disposal of computers by Sudama Associates is not a supply as the input tax credit has not been availed on the same.

(b) As per section 7(1)(c) read with Schedule I of the CGST Act, supply of goods by an agent to his principal where the agent undertakes to receive such goods on behalf of the principal qualifies as supply even if the same is made without consideration. Further, Circular No.

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.8

57/31/2018 GST dated 04.09.2018 clarifies that principal-agent relationship falls within the ambit of the Schedule I only where the goods being procured by the agent on behalf of the principal are invoiced in the name of the agent. In that case, further provision of the said goods by the agent to the principal without consideration, would be covered in Schedule I and thus would qualify as supply.

In the given case, Champak is only acting as the procurement agent, and has in no way involved himself in the supply or receipt of the goods. The invoice is being issued in the name of Prithvi Enterprises and not Champak. Hence, Champak is not an agent of Prithvi Enterprises for the supply of goods in terms of Schedule I of the CGST Act

Question 14

Ajatasatru Industries enters into a contract with an actor – Chandragupta - to act as a brand ambassador of products manufactured by Ajatasatru Industries. The duration of the contract is 5 years and the contract fee payable to Chandragupta for being a brand ambassador is ₹ 50 lakh per annum. As per the terms of the contract, in case the contract is terminated by Chandragupta before the end of the contract period, Chandragupta will have to repay to Ajatasatru Industries, 50% of the contract fee received by him till the time of termination of contract.

At the end of 3rd year, Chandragupta terminates the contract with Ajatasatru Industries. He has received the contract fee for 3 years at the time of termination of contract.

You are required to determine whether the given transaction(s) qualifies(y) as supply(ies).

Answer :

As per section 7(1)(a), supply includes all forms of supply of goods or services or both made or agreed to be made for a consideration by a person in the course or furtherance of business. In the given case, Chandragupta has agreed to provide his services as a brand ambassador of the products manufactured by Ajatasatru Industries at an agreed annual consideration. Thus, his services fall within the purview of the term “supply” under GST where the consideration charged for such supply is ₹ 50 lakh per annum.

Further, section 7(1A) provides that when certain activities or transactions constitute a supply in accordance with the provisions of section 7(1), they shall be treated either as a supply of goods or supply of services as referred to in Schedule II of the CGST Act. Tolerating non-performance of a contract is an activity or transaction which is treated as a supply of service as per Schedule II and the person is deemed to have received the consideration in the form of fines or penalty and is, accordingly, required to pay tax on such amount.

In the given case, since Ajatasatru Industries is tolerating the act of Chandragupta of terminating the contract before the expiry of its contract period, 50% of contract fee for 3 years amounting to ₹ 75 lakh is being received by it as a penalty for the same. The act of tolerating the non- performance of a contract by Chandragupta by Ajatasatru Industries is a supply of service where the consideration charged for such supply is ₹ 75 lakh [50% of (₹ 50 Lakh × 3 years)]

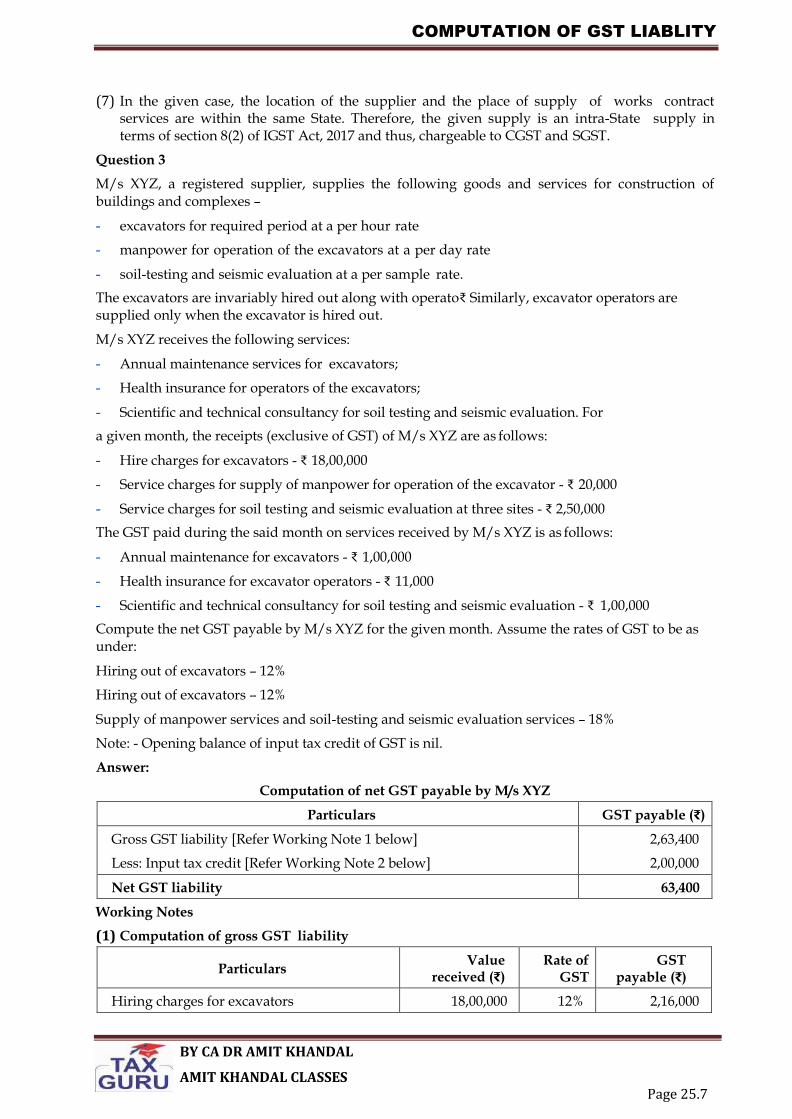

Question 15

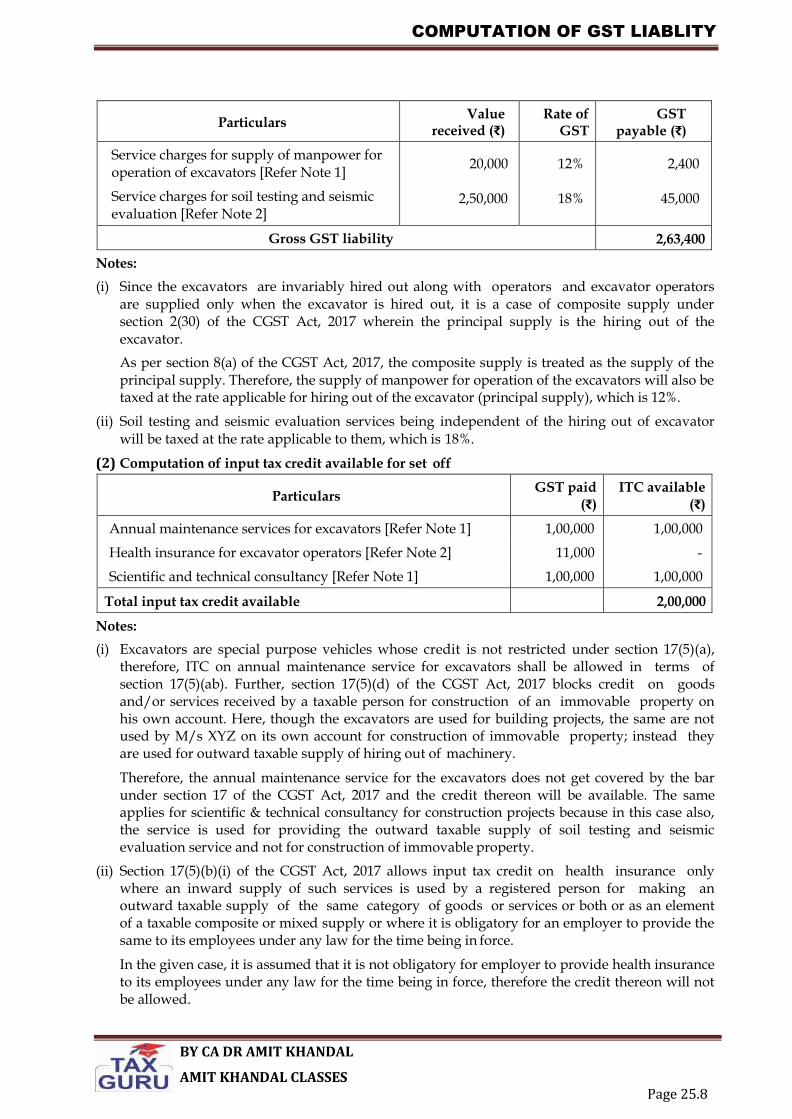

Shivaji Pvt. Ltd., a registered supplier, supplies the following goods and services for construction of buildings and complexes -

- excavators for required period at a per hour rate

- manpower for operation of the excavators at a per day rate

- soil-testing and seismic evaluation at a per sample rate.

The excavators are invariably hired out along with operators. Similarly, excavator operators are supplied only when the excavator is hired out For a given month, the receipts

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.9

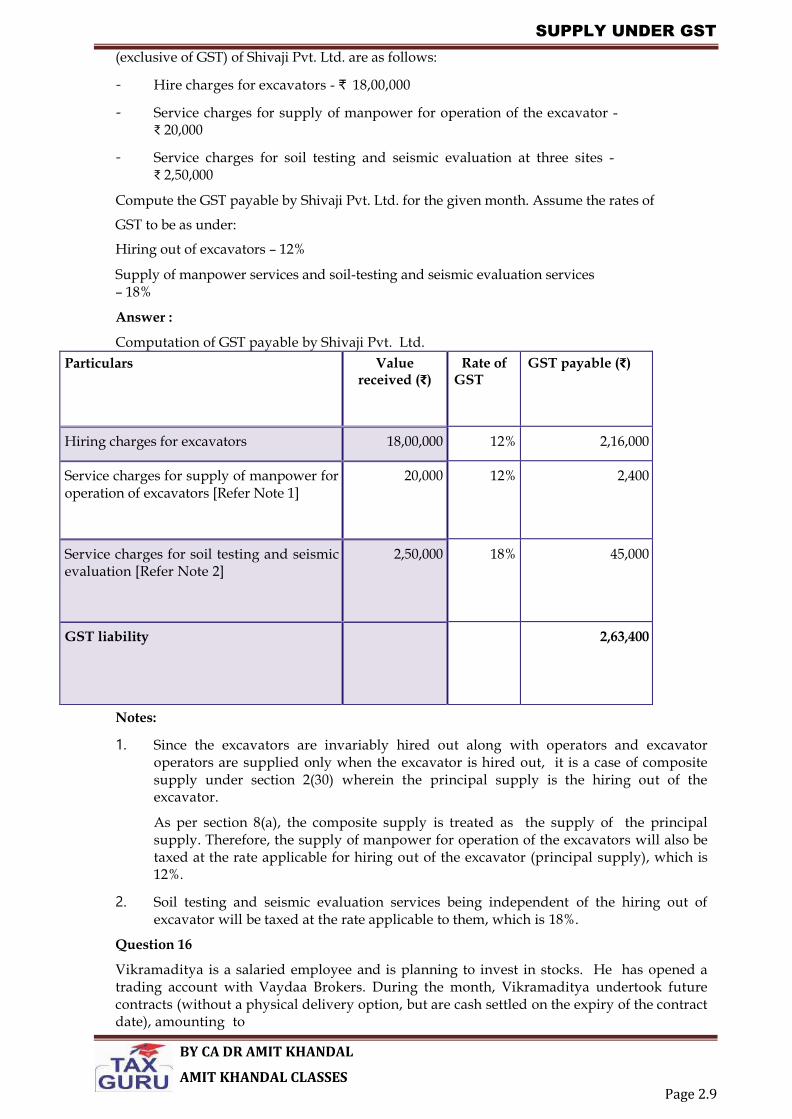

(exclusive of GST) of Shivaji Pvt. Ltd. are as follows:

- Hire charges for excavators - ₹ 18,00,000

- Service charges for supply of manpower for operation of the excavator - ₹ 20,000

- Service charges for soil testing and seismic evaluation at three sites - ₹ 2,50,000

Compute the GST payable by Shivaji Pvt. Ltd. for the given month. Assume the rates of

GST to be as under:

Hiring out of excavators – 12%

Supply of manpower services and soil-testing and seismic evaluation services – 18%

Answer :

Computation of GST payable by Shivaji Pvt. Ltd.

Particulars Value received (₹)

Rate of GST

GST payable (₹)

Hiring charges for excavators 18,00,000 12% 2,16,000

Service charges for supply of manpower for operation of excavators [Refer Note 1]

20,000 12% 2,400

Service charges for soil testing and seismic evaluation [Refer Note 2]

2,50,000 18% 45,000

GST liability 2,63,400

Notes:

1. Since the excavators are invariably hired out along with operators and excavator operators are supplied only when the excavator is hired out, it is a case of composite supply under section 2(30) wherein the principal supply is the hiring out of the excavator.

As per section 8(a), the composite supply is treated as the supply of the principal supply. Therefore, the supply of manpower for operation of the excavators will also be taxed at the rate applicable for hiring out of the excavator (principal supply), which is 12%.

2. Soil testing and seismic evaluation services being independent of the hiring out of excavator will be taxed at the rate applicable to them, which is 18%.

Question 16

Vikramaditya is a salaried employee and is planning to invest in stocks. He has opened a trading account with Vaydaa Brokers. During the month, Vikramaditya undertook future contracts (without a physical delivery option, but are cash settled on the expiry of the contract date), amounting to

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.10

₹ 35,00,000. Vikramaditya needs your advice whether such future contracts undertaken by him amount to supply and are liable to GST. Answer

For a transaction to fall within the purview of supply, it must be a supply of either goods or services or both. The definitions of the terms “goods” and “services” specifically exclude “securities” from their purview. Further, ‘derivatives’ are included in the definition of ‘securities’. As ‘derivatives’ fall in the definition of securities, they are neither goods nor services and hence, are not liable to GST.

Future contracts are in the nature of financial derivatives, the price of which is dependent on the value of underlying stocks or index of stocks or certain approved currencies and the settlement happens normally by way of net settlement with no actual delivery.

Since future contracts are in the nature of derivatives, these qualify as ‘securities’ and thus, are not subject to GST. In view of the above discussion, it can be inferred that since the future contracts undertaken by Vikramaditya are in the nature of derivatives, these qualify as ‘securities’ and do not qualify as supply and thus, are not subject to GST.

Question 17

Angad Private Ltd. is engaged in the business of distribution of construction material. As an incentive, Angad Private Ltd. pays an amount of ₹ 75,000 to its employees upon achieving a specified sales target. The incentive is part of the salary of the employees and applicable tax is deducted at source as per relevant income tax provisions. Angad Private Ltd. is of the view that GST is not leviable on such incentive paid to the employees. Whether the view taken by Angad Private Ltd. is correct?

Answer

Yes, Angad Private Ltd.’s view is correct. In terms of section 7(2) read with Schedule III of the CGST Act, services by an employee to employer in the course of or in relation to his employment shall not be treated as supply under GST. Further, the amount paid as incentive by Angad Private Ltd. is not in the nature of gift, and thus, is not covered under Schedule I of the CGST Act. In fact, in the given case, the incentive is part of the salary and is directly linked to the sales target. Therefore, the services provided by the employees in return of the incentive given to them shall not be treated as a “supply”.

In the light of above discussion, GST is not leviable on the incentive paid by Angad Private Ltd. to employees.

Question 18

Nandeeshwar Manufacturers sends certain category of yarn for processing to the job worker. The job worker undertakes the processing work on the yarn as per the requirement of Nandeeshwar Manufacturers. During the process, the job worker uses his own material also. The processed yarn is sold by Nandeeshwar Manufacturers directly from the job worker premises. Balance quantity of yarn and waste material is sent back by the job worker to Nandeeshwar Manufacturers. The job worker is of the opinion that he is using his own material also in the processing and hence the supply to Nandeeshwar Manufacturers is in the nature of supply of goods as well as services. Do you agree with the opinion of job worker?

Answer

No, the opinion of the job worker is not fully correct. Section 7(1A) provides that when certain activities or transactions constitute a supply in accordance with the provisions of section 7(1), they shall be treated either as a supply of goods or supply of services as referred to in Schedule II of the CGST Act. Any processing activity carried on any other person’s goods is treated as supply of service in terms of Schedule II. The job worker, in addition to the goods received from the principal, can use his own goods for providing the services of job work. These goods are not supply per se, but being used in the processing activity carried out by it.

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.11

Thus, the activity undertaken by the job worker, in the given case, squarely falls within the purview of Schedule II and shall be considered as supply of service by the job worker to Nandeeshwar Manufacturers.

Question 19

Mokshabhumi Industries has its manufacturing unit in the State of Maharashtra. It stores the finished goods manufactured by it at a depot located in the State of Gujarat. The depot is owned by Punyabhumi Ltd. – a related person of Mokshabhumi Industries. Punyabhumi Ltd. has not charged any consideration from Mokshabhumi Industries for usage of depot for storage purpose. Whether the storage of goods permitted by Punyabhumi Ltd. to Mokshabhumi Industries qualifies as supply under GST?

Answer

As per section 7(1)(c) read with Schedule I of the CGST Act, supply of goods or services or both between related persons without consideration when made in the course or furtherance of business qualifies as supply. Thus, the storage services provided by Punyabhumi Ltd. to Mokshabhumi Industries in course or furtherance of business qualifies as supply under GST even though no consideration has been charged for the same.

Question 20

Rob Shareholding Ltd., an approved intermediary, has entered into a transaction wherein certain securities were to be lent to Dhandhan Bank, under Securities Lending Scheme, 1997. Dhandhan Bank shall pay specified lending fee against such lending of securities to it. Explain the taxability of transactions involved in the Securities Lending Scheme, 1997.

Answer

Securities Lending Scheme, 1997 (hereafter referred to as SLS) facilitates the lending and borrowing of securities. Securities are neither covered in the definition of goods nor covered in the definition of services. Therefore, a transaction in securities which involves disposal of securities is not a supply in GST and hence not taxable.

However, SLS doesn’t treat lending of securities as disposal of securities and therefore is not excluded from the definition of services. The lending fee charged from the borrowers of securities has the character of consideration and is taxable under GST. Apart from above, the activities of the intermediaries facilitating lending and borrowing of securities for commission or fee are also taxable separately [Circular No. 119/38/2019 GST dated 11.10.2019].

Question 21

Krishnadev is a trader based in India. Ramakrishna, brother of Krishnadev, is located in China and is also engaged in business of trading of goods. Krishnadev places an order with Ramakrishna for procurement of certain goods from local market in China. Before the shipment of goods from China to India, Krishnadev sold such goods to Christiano, a trader located in Brazil. The goods were subsequently shipped from China to Brazil. Comment on the taxability of transaction between Krishnadev and Christiano under GST in India.

Answer

The transaction between Krishnadev and Christiano is in the nature of merchant trading. As per Schedule III of the CGST Act, transactions involving sale of goods from a place in non-taxable territory to another place in non- taxable territory, without such goods entering into India, shall not be treated as supply under GST. Therefore, the transaction between Krishnadev and Christiano shall not be treated as supply and is thus not leviable to GST.

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.12

Question 22

Mohandas International entered into a transaction for import of goods from a vendor located in Italy. Due to financial issues, Mohandas International was not in a situation to clear the goods upon payment of import duty. Mohandas International sold the goods to Radhakrishnan Export House by endorsement of title to the goods, while the goods were in high seas. The agreement further provided that Mohandas International shall purchase back the goods in future from Radhakrishnan Export House. Discuss the taxability of transaction(s) involved, under the GST law.

Answer

As per Schedule III of the CGST Act, high seas sale transactions i.e. supply of goods by the consignee to any other person, by endorsement of documents of title to the goods, after the goods have been dispatched from the port of origin located outside India but before clearance for home consumption shall not be considered as supply under GST. Thus, the sale of goods by Mohandas International to Radhakrishnan Export House in high seas shall not be liable to GST.

Further, the import duty including IGST shall be payable by Radhakrishnan Export House at the time of clearance of goods at port of import. In case the goods are sold back by Radhakrishnan Export House to Mohandas International at a subsequent point of time, the same shall be treated as normal domestic sale transaction and GST shall be applicable on the same subject to other conditions prescribed under GST Law.

Question 23

Mr. Happy has a huge residential property located at a prime location in Mumbai, Maharashtra. He has let out the 1st and 2nd floor to Mr. Peace for residential purposes in April. Mr. Peace surrenders his tenancy rights to Mr. Serene for a tenancy premium of ₹ 10,00,000 on 1st June. Mr. Serene has also paid the applicable stamp duty and registration charges on transfer of tenancy rights. Moreover, Mr. Serene has agreed to pay a monthly rent of ₹ 1,00,000 to Mr. Happy from June.

Determine the taxability of the transaction(s) involved in the given case, for the month of June.

Answer

Circular No. 44/2018 CT dated 02.05.2018 clarifies that the activity of transfer of tenancy right against consideration [i.e. tenancy premium] is squarely covered under supply of service liable to GST. It is a form of lease or renting of property and such activity is specifically declared to be a service in Schedule II i.e. any lease, tenancy, easement, licence to occupy land is a supply of services.

Although stamp duty and registration charges have been levied on such transfer of tenancy rights, it shall be still subject to GST. Merely because a transaction/supply involves execution of documents which may require registration and payment of registration fee and stamp duty, would not preclude them from the ‘scope of supply’ and from payment of GST.

The transfer of tenancy rights cannot be treated as sale of land/ building in Schedule III. Thus, it is not a non-supply under GST and consequently, a consideration for the said activity shall attract levy of GST. Services provided by outgoing tenant by way of surrendering the tenancy rights against consideration in the form of a portion of tenancy premium is liable to GST. Hence, in the given case, the tenancy premium of ₹ 10,00,000 received by Mr. Peace for surrendering his tenancy rights to Mr. Serene is liable to GST.

The circular further clarifies that since renting of residential dwelling for use as a residence is exempt [Entry 12 of Notification No. 12/2017 CT (R) dated 28.06.201732], grant of tenancy rights in a residential dwelling for use as residence dwelling against tenancy premium or periodic rent or both is exempt. Consequently, monthly rent ₹ 1,00,000 received by Mr. Happy

Downloaded from Studyfromnotes.com - All FREE premium notes

SUPPLY UNDER GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 2.13

from Mr. Serene is exempt.

Question 24

(a) Rudraksh Kapoor, owner of Rudraksh Publishing House, Ghaziabad, U.P., donated some money to a Divyaprakash Charitable Trust in the memory of his late father. The Divyaprakash Charitable Trust constructed a room in the school run by it from such donation and wrote “Donated by Rudraksh Kapoor in the memory of his father” on the door of the room so constructed. Examine whether the money donated by Rudraksh Kapoor is leviable to GST.

(b) In the above question, if the Divyaprakash Charitable Trust had written on the door of

the room constructed in the school run by it from the money donated by Rudraksh

Kapoor “Donated by Rudraksh Publishing House, Ghaziabad, U.P.”, would the given

transaction/activity qualifies as supply.

Answer

Circular No. 116/35/2019 GST dated 11.10.2019 has clarified that in case of donations

received by a charitable institution, when the name of the donor is displayed in

recipient institution’s premises, in such a manner, which can be said to be an

expression of gratitude and public recognition of donor’s act of philanthropy and is

not aimed at giving publicity to the donor in such manner that it would be an

advertising or promotion of his business, then it can be said that there is no supply of

service for a consideration (in the form of donation). Donations received by the

charitable organisations are treated as consideration only if there exists, quid pro quo,

i.e., there is an obligation on part of recipient of the donation or gift to do anything

(supply a service).

Thus, GST is not leviable where all the following three conditions are satisfied namely:

Gift or donation is made to a charitable organization

Payment has the character of gift or donation

Purpose is philanthropic (i.e., it leads to no commercial gain) and not advertisement.

(a) In the backdrop of the above discussion, since in the given case, the way the name of Rudraksh Kapoor is displayed on the door of the room constructed in the school run by Divyaprakash Charitable Trust, it is only an expression of gratitude and public recognition of Rudraksh’s act of philanthropy and is not aimed at advertising or promoting his business. There is no reference/mention of his publishing house which otherwise would have got advertised.

Thus, the money donated by Rudraksh Kapoor is not a leviable to GST.

(b) In the given case, since the name of Rudraksh Publishing House has been displayed on

the door of the room constructed in the school run by Divyaprakash Charitable Trust, it

might be aimed at advertising or promoting his business. There is a direct mention of

his publishing house which is being advertised. In such a case, it is a supply of service

by Divyaprakash Charitable Trust for a consideration received in the form of

donation.

Downloaded from Studyfromnotes.com - All FREE premium notes

CHAPTER - 3

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 3.1

CHARGE OF GST

Question 1

State person liable to pay GST in the following independent cases provided recipient is located in the taxable territory:

a) Services provided by an arbitral tribunal to any business entity.

b) Sponsorship services provided by a company to an individual.

c) Renting of immovable property service provided by the Central Government to a registered business entity.

Answer:

a) Since GST on services provided or agreed to be provided by an arbitral tribunal to any business entity located in the taxable territory is payable under reverse charge, in the given case, GST is payable by the recipient - business entity.

b) GST on sponsorship services provided by any person to anybody corporate or partnership firm located in the taxable territory is payable under reverse charge. Since in the given case, services have been provided to an individual, reverse charge provisions will not be attracted. GST is payable under forward charge by the supplier – company.

c) GST on services supplied by Central Government, State Government, Union territory/ local authority by way of renting of immovable property to a person registered under CGST Act, 2017 is payable under reverse charge. Therefore, in the given case, GST is payable under reverse charge by the recipient – registered business entity.

Question 2

A person availing composition scheme in Haryana during a financial year crosses the turnover of ₹ 1.5 crore during the course of the year i.e. he crosses the turnover of ₹ 1.5 crore in December? Will he be allowed to pay tax under composition scheme for the remainder of the year, i.e. till 31st March?

Answer:

No. The option to pay tax under composition scheme lapses from the day on which the aggregate turnover of the person availing composition scheme during the financial year exceeds the specified limit (₹ 1.5 crore). Once he crosses the threshold, he is required to file an intimation for withdrawal from the scheme in prescribed form within 7 days of the occurrence of such event.

Every person who has furnished such an intimation, may electronically furnish at the common portal, a statement in prescribed form containing details of the stock of inputs and inputs contained in semi-finished or finished goods held in stock by him on the date on which the option is withdrawn, within a period of 30 days from the date from which the option is withdrawn.

Question 3

Determine whether the supplier in the following cases are eligible for composition levy provided their turnover in preceding year does not exceed ₹ 1.5 Crore:

d) Mohan Enterprises is engaged in trading of pan masala in Rajasthan and is registered in the same State.

Downloaded from Studyfromnotes.com - All FREE premium notes

CHARGE OF GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 3.2

e) Sugam Manufacturers has registered offices in Punjab and Haryana and supplies goods in neighbouring States.

Answer:

i. A supplier engaged in the manufacture of goods as notified under section 10(2)(e), during the preceding FY is not eligible for composition scheme. Ice cream and other edible ice, whether or not containing cocoa, Pan masala and Tobacco and manufactured tobacco & Manufacturer of aerated water & supplier of aerated water cannot opt to pay tax under composition levy substitutes are hereby notified. However, in the given case, since Mohan Enterprises is engaged in trading of pan masala and not manufacture and his turnover does not exceed ₹ 1.5 crore, he is eligible for composition scheme subject to fulfilment of specified conditions.

ii. Since supplier of inter-State outward supplies of goods is not eligible for composition levy, Sugam Manufacturers is not eligible for composition levy.

Question 4

Subramanian Enterprises has two registered places of business in Delhi. Its aggregate turnover for the preceding year for both the places of business was ₹ 120 lakh. It wishes to pay tax under composition levy for one of the place of business in the current year while under normal levy for other. You are required to advice Subramanian Enterprises whether he can do so ?

Answer:

A registered person with an aggregate turnover in a preceding financial year up to ₹ 1.5 crore is eligible for composition levy in Delhi. Since the aggregate turnover of Subramanian Enterprises does not exceed ₹ 1.5 crore, it is eligible for composition levy in the current year. However, all registered persons having the same Permanent Account Number (PAN) have to opt for composition scheme. If one such registered person opts for normal scheme, others become ineligible for composition scheme. Thus, Subramanian Enterprises either have to opt for composition levy for both the places of business or under normal levy for both the places of business.

Question 5

Examine whether the suppliers are eligible for composition scheme in the following independent cases. Is there any other option available for concessional tax payment with any of these suppliers, wherever composition scheme cannot be availed?

a) M/s. Devlok, a registered dealer, is dealing in intra-State trading of electronic appliances in Jaipur (Rajasthan). It has turnover of ₹ 130 lakh in the preceding financial year. In the current financial year, it has also started providing repairing services of electronic appliances.

b) M/s. Narayan & Sons, a registered dealer, is running a “KhanaKhazana” Restaurant near City Palace in Jaipur. It has turnover of ₹ 140 lakh in the preceding financial year. In the current financial year, it has also started dealing in intra-State trading of beverages in Jaipur (Rajasthan).

c) M/s. Indra & Bro, a registered dealer, is providing restaurant services in Uttarakhand. It has turnover of ₹ 70 lakh in the preceding financial year. It has started providing intra-State interior designing services in the current financial year and discontinued rendering restaurant services.

Downloaded from Studyfromnotes.com - All FREE premium notes

CHARGE OF GST

BY CA DR AMIT KHANDAL

AMIT KHANDAL CLASSES

Page 3.3

d) M/s. Him Naresh, a registered dealer, is exclusively providing intra-State architect services in Uttarakhand. It has turnoverof ₹ 40 lakh in the preceding financial year.

Answer:

As per section 10 of the CGST Act, 2017, the following registered persons, whose aggregate turnover in the preceding financial year did not exceed 1.5 crore, may opt to pay tax under composition levy:

a) Manufacturer,

b) Persons engaged in making supplies referred to in clause (b) of paragraph 6 of Schedule II (restaurant services), and Any other supplier eligible for composition levy.

Thus, essentially, the composition scheme can be availed in respect of goods and only one service namely, restaurant service. However, the scheme permits supply of other marginal services for a specified value along with the supply of goods and restaurant service, as the case may be. Such marginal services can be supplied for a value up to 10% of the turnover in the preceding year or ₹

5 lakh, whichever is higher.

Further, the registered person should not be engaged in making any inter- State outward supplies of goods.

Furthermore, an option of availing benefit of concessional payment of tax has been provided to a registered person whose aggregate turnover in the preceding financial year is upto ₹ 50 lakh and who is not eligible to pay tax under composition scheme. Said person can pay tax @ 3% [Effective rate 6% (CGST+ SGST/UTGST)] on first supplies of goods and/or services up to an aggregate turnover of ₹ 50 lakh made on/after 1st April in any financial year (FY), subject to specified conditions vide Notification No. 2/2019 CT(R) dated 07.03.2019 as amended. One of such condition is that the registered person should not be engaged in making any inter-state outward taxable supplies.

In view of the above-mentioned provisions, the answer to the given independent cases is as under:-

a. The turnover limit for composition scheme in case of Jaipur (Rajasthan) is ₹ 1.5 crore. Thus, M/s. Devlok can opt for composition scheme as its aggregate turnover is less than ₹ 1.5 crore and he is making intra-State supplies. Further, since the registered person opting for composition scheme can also supply services (other than restaurant services) for a value up to 10% of the turnover in the preceding year or ₹ 5 lakh, whichever is higher. Thus, M/s. Devlok can supply repair services up to a value of ₹ 13 lakh [10% of ₹ 130 lakh] in the current financial year.

b. In the given case:-

i. the turnover in the preceding year is less than the eligible turnover limit, i.e. ₹ 1.5 crore.

ii. the supplier is engaged in providing restaurant service which is an eligible supply under composition scheme.

iii. the supplier wants to engage in trading of goods which is also an eligible supply under composition scheme.

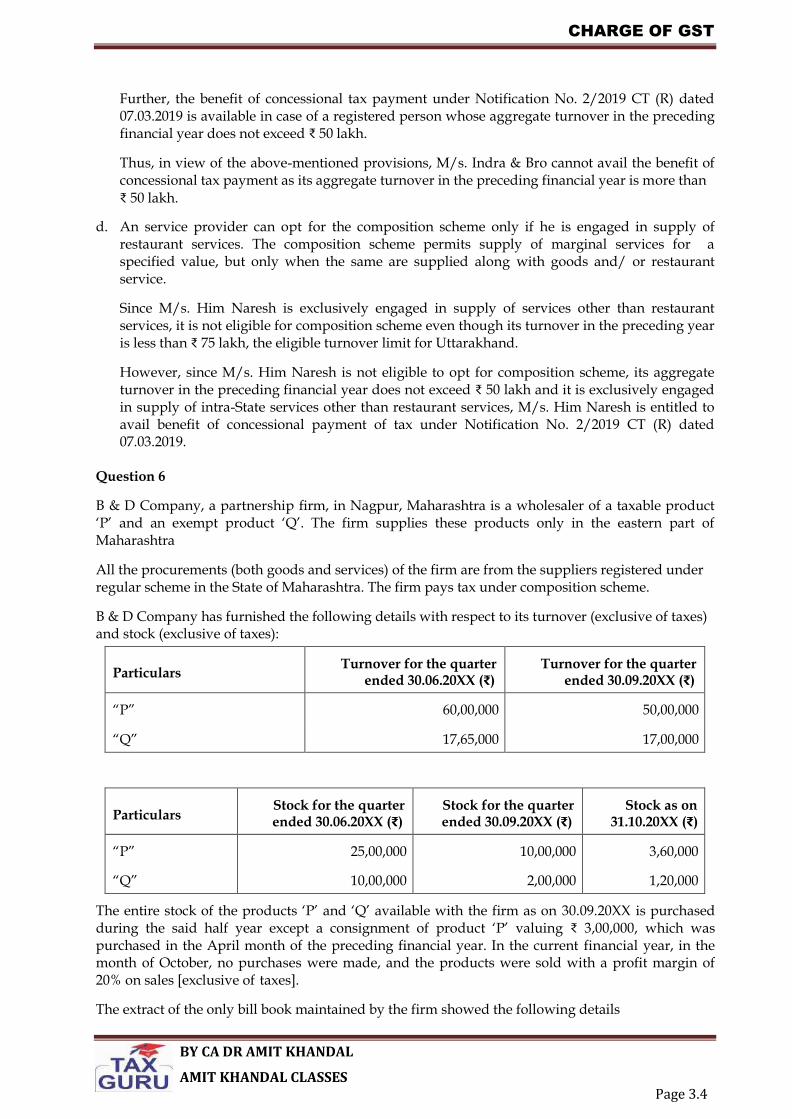

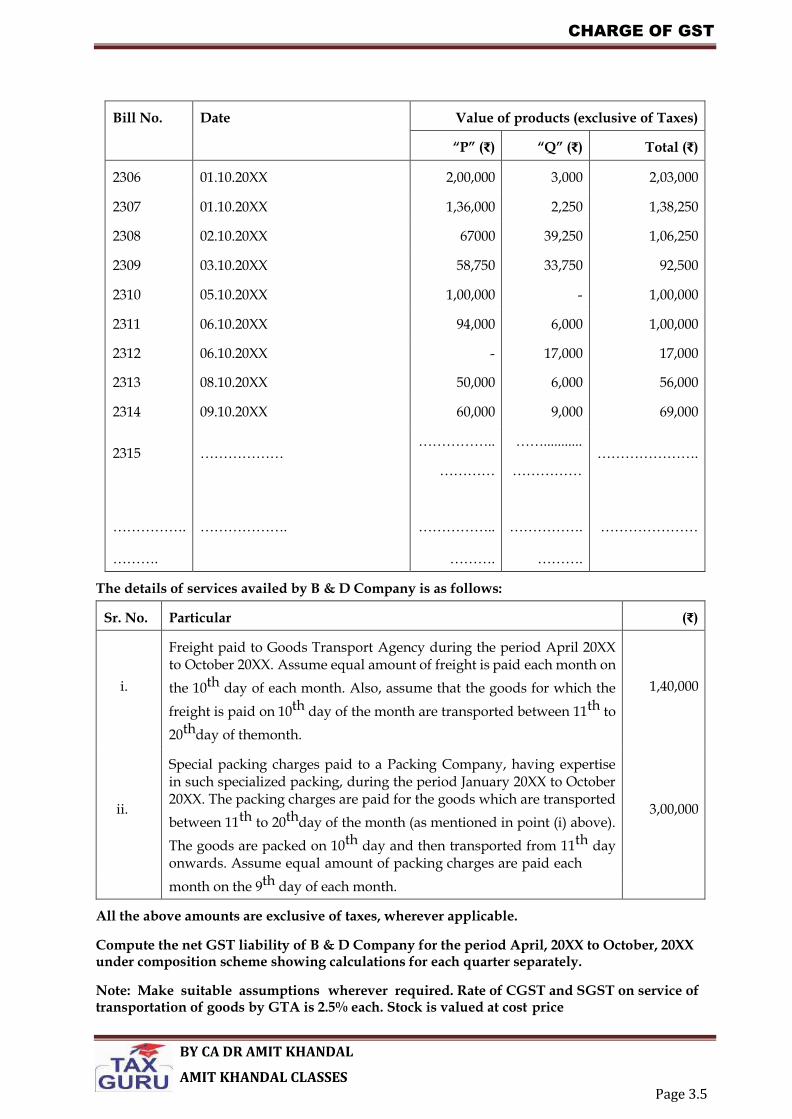

Thus, M/s. Narayan & Sons is eligible for composition scheme.