Download Webinar Slides - SiliconExpert

120

Supply Chain Planning in the Global Electronics Industry Supply Chain Webinar

Transcript of Download Webinar Slides - SiliconExpert

Supply Chain Planning in the Global Electronics Industry

Supply Chain Webinar

Asking Questions

• Ask questions during the webinar by using the Questions window

• Questions will be addressed at the end of the webinar

• Any question we do not get to will be answered individually by email

• The presentation will be sent to you after the webinar

• Please respond to the survey questions at the end of the webinar

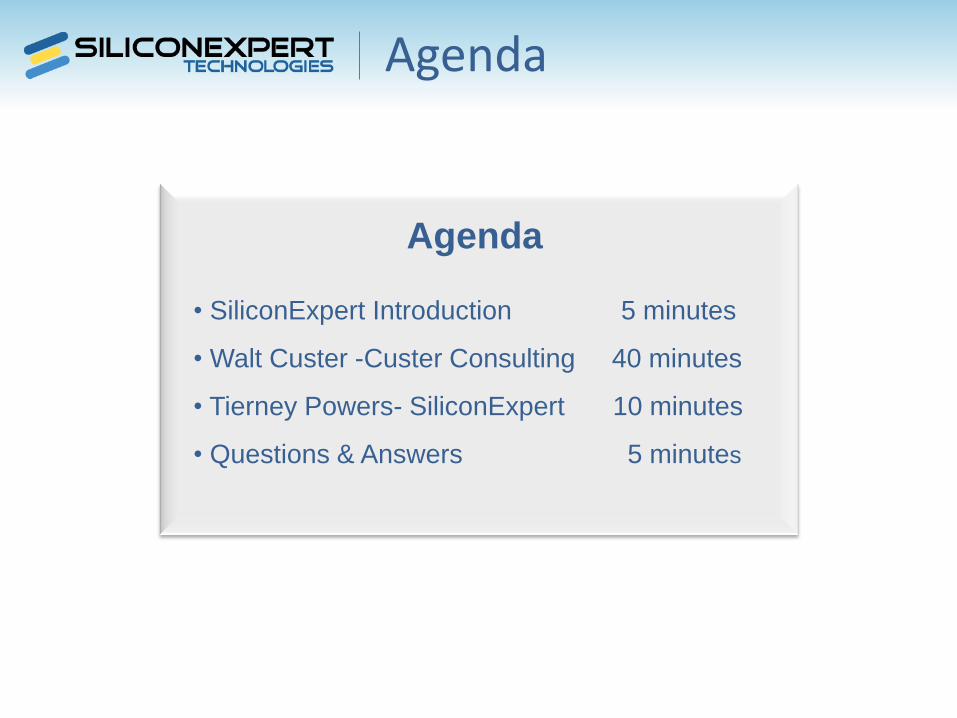

Agenda

Agenda

• SiliconExpert Introduction 5 minutes

• Walt Custer -Custer Consulting 40 minutes

• Tierney Powers- SiliconExpert 10 minutes

• Questions & Answers 5 minutes

Tierney Powers

Sales Associate

(415) 990-7256

SiliconExpert Panelist

• Serving Electronic OEMs, Distributors,

Manufacturers & Contract Manufacturers

• Our Electronic Component Database of

over 250 million components powers our:

o Comprehensive software tools

o Integrated solutions

o Professional services

About Us

Reactive vs. Proactive Approaches to Obsolescence Management

250 Million+ Orderable Part Numbers

Up to 42 Parametric values/product line

Risk Analysis & Obsolescence

Forecasting Algorithms developed

with CALCE

Environmental Data tracked: EU &

China RoHS, REACH, WEEE

compliance & Material Declarations

Parametrically-derived cross-references

for millions of parts

Our Database

Walt Custer President at Custer Consulting Group

707 785-1777

www.custerconsulting.com

Today’s Expert Panelist

Business Outlook

Global Electronics

Industry

Custer Consulting Group

www.custerconsulting.com

September 2013

20130919

Topics of this Presentation

• Business Cycles & Global Economy

• World & Regional Electronic Supply Chain Growth

- Electronic Equipment

- Active & Passive Components

- EMS/ODM Companies

- Materials and Process Equipment

• Summary & Forecasts

• Forecasting tools and how to use this information

to predict your companies sales

BUSINESS CYCLE

Electronic Equipment, EMS/ODM Companies,

Components, Materials & Capital Equipment

-6

-4

-2

0

2

4

6

0 30 60 90 120 150 180 210 240 270 300 330 360

Electronic Equipment

EMS/ODM

Components

Raw Materials

Capital Equip

Expansion ContractionTime ->

20130915

% Growth

+

-

0

Global Economy

Industrial Production – World% Change vs. One Year Earlier

Britain - 1.5 Jul

Czech Republic +2.0 Jul

France - 1.8 Jul

Germany - 2.3 Jul

Italy - 4.4 Jul

Netherlands - 0.4 Jul

Russia - 0.8 Jul

Spain +0.4 Jul

Euro Area - 2.2 Jul

Canada - 0.6 Jun

USA + 1.4 Jul

China +10.4 Aug

India - 2.2 Jun

Malaysia + 7.6 Jul

Singapore + 2.7 Jul

S Korea + 0.9 Jul

Taiwan + 2.1 Jul

Thailand - 4.5 Jul

Japan + 1.6 Jul

www.economist.com + Eurostat

20130913

52.2

50

47.5

50.1

51.4

55.7

51.7

50.7

48.6

47.2

47.7

50.3

55.4

50.8

45.0 47.0 49.0 51.0 53.0 55.0 57.0

Japan

Taiwan

S Korea

China

Europe

USA

World

PMI

July August

Purchasing Managers' Indices

July vs. August 2013

Markit Economics, JPMorgan and ISM

Above 50 = Growth

Below 50 = Contraction

20130905

Global "Purchasing Managers" IndexDiffusion Index, >50 = Growth

Markit Economics

30

35

40

45

50

55

60

Ja

nA

pr

Ju

lO

ct

Ja

nA

pr

Ju

lO

ct

Ja

nA

pr

Ju

lO

ct

Ja

nA

pr

Ju

l

Oc

tJ

an

Ap

rJ

ul

Oc

tJ

an

Ap

r

Ju

lO

ct

Ja

nA

pr

Ju

lO

ct

Ja

nA

pr

Ju

lO

ct

Ja

nA

pr

Ju

lO

ct

Ja

n

Ap

rJ

ul

Oc

tJ

an

Ap

rJ

ul

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

PM

I20130905

World Purchasing Managers Index3/12 Rate of Change

ISM, JPMorgan, Markit Economics

20130905

0.6

0.8

1.0

1.2

1.4

1.6

Ja

n

May

Se

p

Ja

n

May

Se

p

Ja

n

May

Se

p

Ja

n

May

Se

p

Ja

n

May

Se

p

Ja

n

May

Se

p

Ja

n

May

Se

p

Ja

n

May

Se

p

Ja

n

May

Se

p

Ja

n

May

Se

p

Ja

n

May

Se

p

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

3/1

2 R

ate

of

Ch

an

ge

China

USA

Europe

World

0 Growth

Electronic

Equipment

World Electronic Equipment Production

by Type

Electronic Outlook 11/2012

2012 TOTAL: $2.15 Trillion

1.6%

27.7%

13.1%

6.9%

25.2%

8.7%

8.6%

8.2%

Business

Communication

Consumer

Auto

Computer

Gov/Military

Industrial

Instrument

Methods to Measure Growth

Sector composites based upon financial reports of similar

companies

- Typically quarterly, semiannually or monthly

Government and trade organization statistics

- Typically monthly

- TIMELY DATA REPORTED ON A CONSISTENT BASIS IS

KEY

Sector Analyses based

on Company Financial

Reports

Electronic Equipment Suppliers

Composite of 115 Public CompaniesRevenue, Net Income & Inventory

Computer 13, Internet 9, Storage 10, Communication 20, SEMI 20, Medical 23, Instruments 11,

Military 6, Business & Office 3

20130824

-50

0

50

100

150

200

250

300

350

400

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Mil

lio

ns

Revenue

Income

Inventory

+0.3%

Electronic Equipment Suppliers

Composite of 115 Public Companies

Quarterly Revenue Growth

Computer 13, Internet 9, Storage 10, Communication 20, SEMI 20, Medical 23, Instruments 11, Military 6, Business & Office 3

+ Media tablets from all vendors

20130824

-15

-10

-5

0

5

10

15

20

25

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

% G

row

th

Media

tablets

included

Inventory/Sales Ratios Large Component Distributors, Semiconductor, EMS & OEM Companies

Custer Consulting Group based upon company financials

20130810

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Semiconductor

EMS

OEM

Component Distrib

Ratio: Inventories/Sales

Global Electronic Supply Chain Growth

2Q'13 vs. 2Q'12

0-5

-30

-14

6-1

-78

21

-84

-2-2

7-1

-4

-10 -5 0 5 10

Electronic Equipment

Military

Business & Office

Instruments & Controls

Medical

Communication

Internet

Computer

Data Storage

SEMI Equip

Semiconductors (SIA)

Passive components

PCBs

Component Distrib

EMS (excl Foxconn)

ODM

PCB Process Equipment

PCB Laminate

Materials

% Change

20130824

US$ equivalent at fluctuating exchange; based upon industry composites including acquisitions

Regional Data from Government,

Industry & Trade Organization

Statistics

Europe

Japan

Taiwan/China

USA

Eurostat Data (NACE Rev 2)

Electronic Equipment Production by Country

•C26 computer, electronic & optical products

•C261 electronic components & boards

•C2611 electronic components

•C2612 loaded electronic boards

•C264 consumer electronics

•C2651 instruments & appliances for measuring, testing and navigation

•C266 irradiation, electromedical & electrotherapeutic equipment

•C2733 wiring devices

•C2751 electric domestic appliances

•C2823 office machinery & equipment (except computers & peripherals)

•C291 motor vehicles

•C303 air & spacecraft and related machinery

Monthly indices where average month in CY2005=100

European Computer, Electronic & Optical Products

Production

Eurostat, C26 category, EU 27 countries

20130913

80

85

90

95

100

105

110

115

120

1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Index (2010=100), Seasonally Adjusted

Japan Electronic Equipment Production

by Month 2000 to Present

0

200

400

600

800

1000

1200

1400

1600

1800

2000

1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Elec Application Equip

Electronic Measuring Instrumentation

Communications Equipment

Computers & Related Equipment

Electronic Business Machines

Consumer Electronic Equipment

JEITA www.jeita.or.jp/

20130823

Yen Billion

Taiwan/China Electronic Equipment Producers

Composite of 101 Manufacturers

Consolidated Revenue

Taiwan listed companies, often with significant manufacturing in China

20130911

0

100

200

300

400

500

600

700

800

900

1000

1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10 1 4 7 10

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Aug 2013 down 2.1% compared to

Aug 2012

NT$ Billions

U.S. Electronic Equipment Orders & ShipmentsComputer, Communications, Measurement & Control and Military

www.census.gov/indicator/www/m3/

20130905

14

16

18

20

22

24

26

28

30

32

34

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

Ja

n

Ju

n

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Th

ou

sa

nd

s

Orders

Shipments

$ Billions (monthly, seasonally adjusted)

U.S. Electronic Equipment OrdersMonthly Data

www.census.gov/indicator/www/m3/

20130905

0

2

4

6

8

10

12

14

16

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Th

ou

sa

nd

s Search & Navigation

Electromedical, Instr & Control

Communication

Computer

Defense

$ Billions (monthly, seasonally adjusted)

U.S. Electronic Equipment OrdersMonthly Data

www.census.gov/indicator/www/m3/

20130905

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ja

nM

ay

Se

pJ

an

May

Se

pJ

an

May

Se

pJ

an

May

Se

pJ

an

May

Se

pJ

an

May

Se

pJ

an

May

Se

pJ

an

May

Se

pJ

an

May

Se

pJ

an

May

Se

pJ

an

May

Se

pJ

an

May

Se

pJ

an

May

Se

pJ

an

May

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Medical, Measuring & Control

Search & Navigation - non Military

Communication- non Military

Computer & Related

Military-Search & Navigation

Military-Communications

$ Billions (monthly, seasonally adjusted)

Global Electronic Equipment

Europe

Japan

Taiwan/China

USA

World Electronic Equipment Production

by Region (Final Assembly)

Electronic Outlook 11/2012

2012 TOTAL: $2.15 Trillion

19.0%

15.0%

6.0%

52.0%

8.0%

N America

W Europe

Japan

Rest of Asia

Rest of World

Global Electronic Equipment Shipment

Growth3/12 Rate of Change

IU.S. Dept of Commerce, Eurostat, JEITA, Taiwan/China Composite

20130913

0.6

0.8

1.0

1.2

1.4

1.6

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

3/1

2 R

ate

of

Ch

an

ge

Taiwan/China

Europe

Japan

USA

0 Growth

World Electronic Equipment Monthly

ShipmentsConverted @ Constant 2010 Exchange Rates

Source: Custer Consulting Group

2013

0

10

20

30

40

50

60

70

80

90

100

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Th

ou

sa

nd

s

N America

W Europe

Japan

SE Asia

ROW

US$ B

World Electronic Equipment Monthly

ShipmentsConverted @ Constant 2010 Exchange Rates

Source: Custer Consulting Group

20130913

80

90

100

110

120

130

140

150

160

170

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

Mar

Au

g

Ja

n

Ju

n

No

v

Ap

r

Se

p

Feb

Ju

l

De

c

May

Oc

t

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Th

ou

sa

nd

s

Aug 2013

3.6% below

Aug 2012

US$ B

Market Segments

Volume (Shifted to Low Cost Areas)

Computers & Mobile Communication Devices

Other Consumer Electronics

Datacom/Telecom

Automotive

"Protected"

Military

Medical

Instruments & Controls

High IP Content

Prototype, Quick Response, Short Run, Need for Local Support

Military Equipment

Composite of 6 Public CompaniesRevenue, Net Income & Inventory

General Dynamics, Harris, Lockheed, Northrop Grumman, Raytheon, Rockwell Collins

20130824

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Revenue

Income

Inventory

- 5.3%

U.S. Military Electronics Orders & ShipmentsDefense Communication & Search & Navigation Equipment

www.census.gov/indicator/www/m3/

20130906

0

1

2

3

4

5

6

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Th

ou

sa

nd

s

Orders

Shipments

$ Billions (monthly, seasonally adjusted)

U.S. Aircraft & Parts Shipments

0

2

4

6

8

10

12

14

16

18

20

1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Defense Non-Defense

www.census.gov/indicator/www/m3

US$ Billion

20130906

Instruments & Control Equipment

Composite of 12 Public CompaniesRevenue, Net Income & Inventory

Agilent, Ametek, Emerson, Itron, Keithly, LeCroy, PerkinElmer, Rockwell Automation, Teledyne,

ThermoFisher, Varian, Woodward Govenor

20130824

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Revenue

Income

Inventory

+0.2%

U.S. Electromedical, Measurement & Control Equipment

Orders & Shipments

www.census.gov/indicator/www/m3/

20130906

4

5

5

6

6

7

7

8

8

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Orders

Shipments

$ Billions (monthly, seasonally adjusted)

Medical Equipment

Composite of 23 Public CompaniesRevenue, Net Income & Inventory

Analogic, Bio-Rad Laboratories, Boston Scientific, Bruker, CareFusion, Covidien, Draeger, Guidant,

Hill-Rom, Intuitive Surgical, Invacare, Kinetic Concepts, Medtronic, ResMed, St Jude Medical, Smith &

Nephew, STERIS, Stryker, Varian Medical, Waters, Zimmer, Zoll

20110824

-5

0

5

10

15

20

25

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Mil

lio

ns

Revenue

Income

Inventory

-0.5%

Mobile Phone Unit ShipmentsWorld

Gartner Dataquest 8/13 & prior reports

0

50

100

150

200

250

300

350

400

450

500

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Th

ou

sa

nd

s

UnitsUnits (Millions)

20130818

World Mobile Phone Sales to End Users

2Q’13

Gartner 8/13TOTAL: 435.2 Million Units

24.7%

14.0%

7.3%

3.9%3.5%2.6%

2.5%2.3%

2.2%

1.8%

35.1%

Units

Samsung

Nokia

Apple

LG

ZTE

Huawei

Lenovo

TCL

Sony

Yulong

Others

Smartphone Unit Shipments to

EndusersWorld

Gartner Dataquest 8/13 & prior reports,

0

50

100

150

200

250

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2007 2008 2009 2010 2011 2012 2013

Th

ou

sa

nd

s

Units (Millions)

20130814

"Internet" Equipment Suppliers

Composite of 9 Public CompaniesRevenue, Net Income & Inventory

ADTRAN, Cisco Systems, Extreme Networks, Juniper Networks, Mattson Technology, Netgear,

Sierra Wireless, Sonus Networks, Sycamore

20130824

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Revenue

Income

Inventory

+5.5%

Cisco SystemsRevenue, Net Income & Inventory

CY

20130819

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Revenue

Income

Inventory

CSCO

+ 6%

$639 M due to Scientific

Atlanta acquisition

Juniper NetworksRevenue & Net Income

CY

20130726

-200

0

200

400

600

800

1000

1200

1400

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Millions

Revenue

Income

+ 7%

1140-1180

7/23/13

JNPR"Inventory" not listed on Balance Sheet

2Q/06 Net Loss: $1.2 Billion

+4%

Smart Connected Device Market by Type

IDC 9/13

20130914

2011 2012 2013 2014 2015 2016 2017

Smartphone 53.2 59.5 65.2 68.0 69.0 69.8 70.5

Tablet 7.7 11.8 14.6 15.3 15.9 16.3 16.5

Portable PC 22.4 16.5 11.6 9.7 8.9 8.4 8.0

Desktop 16.6 12.2 8.6 7.0 6.2 5.5 5.0

0

10

20

30

40

50

60

70

80

90

100Unit % of Total

Personal Computer Unit ShipmentsWorld

Gartner Dataquest 7/13 & prior reports

Server & Media Tablets not included

0

10

20

30

40

50

60

70

80

90

100

Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Th

ou

sa

nd

s

UnitsUnits (Millions)

World Personal Computer Market

2Q’13

Gartner 7/2013

TOTAL: 76.0 Million Units

16.7%

16.3%

11.8%

8.3%6.0%

40.8%

Lenovo

HP

Dell

Acer Group

Asus

Other

Includes desk-based PCs, mobile PCs, mini-notebooks but not Media Tablets

20130713

Taiwan/China Motherboard Vendor Sales

Composite of 22 Manufacturers

Taiwan listed companies, often with significant manufacturing in China

20130911

0

20

40

60

80

100

120

140

160

180

200

1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9 1 5 9

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

NT$ Billions

Data Storage Equipment Suppliers

Composite of 10 Public CompaniesRevenue, Net Income & Inventory

Brocade, EMC, Iomega, Maxtor, Network Appliance, Qlogic, Quantum, Seagate, Western Digital, SanDisk

(Iomega & Maxtor historical data retained as both were purchased by other members of this group)

20130824

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Revenue

Income

Inventory

-7.3%

SanDiskRevenue, Net Income & Inventory

CY

20130722

-400

-200

0

200

400

600

800

1000

1200

1400

1600

1800

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Millions

Revenue

Income

Inventory

+ 43%

SNDK

4Q08 net loss: -$1.76 billion

“We are excited about our pending acquisition of SMART Storage Systems, as

it accelerates our growth in enterprise storage. The growth drivers of our

business are vibrant and SanDisk is poised for further gains.” 7/17/13

Components

- Semiconductors

- Passive Components

- Solar/Photovoltaic Industry

- Component Distributors

7/12 7/13 % CH

Americas 4.13 5.02 +21.5%

Europe 2.82 2.85 +1.1%

Japan 3.61 2.93 -18.6%

Asia Pacific 13.74 14.73 +7.2%

Total 24.29 25.53 +5.1%

Monthly Semiconductor Shipments

$ Billions (3-month average)

SIA www.sia-online.org/

20130902

Global Semiconductor ShipmentsMonthly US$

SIA

20130902

0

5

10

15

20

25

30

Jan

Au

gM

ar

Oc

tM

ay

Dec

Ju

lF

eb

Sep

Ap

rN

ov

Ju

nJan

Au

gM

ar

Oc

tM

ay

Dec

Ju

lF

eb

Sep

Ap

rN

ov

Ju

nJan

Au

gM

ar

Oc

tM

ay

Dec

Ju

lF

eb

Sep

Ap

rN

ov

Ju

nJan

Au

gM

ar

Oc

tM

ay

Dec

Ju

lF

eb

Sep

Ap

rN

ov

Ju

nJan

Au

gM

ar

Oc

tM

ay

83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Th

ou

sa

nd

s

3-Month AvgUS$ Billions (3-month average)

2009 recession

much sharper

but shorter

than 2001

Record high

Global Semiconductor Shipments3-Month Growth Rates on $ Basis

Total $ Shipments from All Countries to an Area

SIA website: www.sia-online.org/

20130902

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

Jan

Sep

May

84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

3/12 rate of change

2

1

4

3 6

5

8

7

10

911

13

12

Total Semiconductor Shipments to an Area

Monthly Shipments - Reporting Firms

SIA website: www.sia-online.org/

20130902

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Jan

Ju

n

No

v

Ap

r

Sep

Fe

b

Ju

l

Dec

May

Oc

t

Mar

Au

g

Jan

Ju

n

No

v

Ap

r

Sep

Fe

b

Ju

l

Dec

May

Oc

t

Mar

Au

g

Jan

Ju

n

No

v

Ap

r

Sep

Fe

b

Ju

l

Dec

May

Oc

t

Mar

Au

g

Jan

Ju

n

No

v

Ap

r

Sep

Fe

b

Ju

l

Dec

May

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Japan

N America

Europe

Asia-Pac

$ Billions SE Asia

Total Semiconductor Shipments to an AreaMonthly Shipments - Reporting Firms

SIA website: www.sia-online.org/

20130902

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

Jan

Ju

l

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Japan

Europe

NAmericaAsia

Asia grows from 20%

to 56.1% market share

7/13

11.1%

12.1%

20.7%

56.1%

N American Semiconductor ShipmentsMonthly & 3-Month Average Shipments

SIA website: www.sia-online.org/

20130902

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Jan

Ju

n

No

v

Ap

r

Sep

Fe

b

Ju

l

Dec

May

Oc

t

Mar

Au

g

Jan

Ju

n

No

v

Ap

r

Sep

Fe

b

Ju

l

Dec

May

Oc

t

Mar

Au

g

Jan

Ju

n

No

v

Ap

r

Sep

Fe

b

Ju

l

Dec

May

Oc

t

Mar

Au

g

Jan

Ju

n

No

v

Ap

r

Sep

Fe

b

Ju

l

Dec

May

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Th

ou

sa

nd

s

Month

3-Month Avg

$ Billions

Semiconductor Shipments to N. America

vs. U.S Electronic Equipment Production

Total $ Semiconductor Shipments from All Countries to N. America www.sia-online.org/

U.S. Electronic Equipment Shipments www.census.gov/indicator/www/m3/

20130905

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Semiconductors

El Equip

3/12 Rate of Change(US$)

Semiconductor Fab, Assembly,

Packaging,Test & Measurement

Equipment

Semiconductor Fab, Test & Measurement

Composite of 20 Public CompaniesRevenue, Net Income & Inventory

Applied Materials, ASM Intl, ASML, Advantest, KLA Tencor, Novellus, Hitachi Hi Tech, Lam Research, BTU,

LTX-Credence, FEI, FSI, Intervac, Kulicke & Soffa, MKS Instruments, Rudolph, Teradyne, Ultratech Stepper,

Varian semiconductor, Veeco

20130824

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

US$ Billions @ fluctuating exchange

Chart TitleRevenue

Income

Inventory

+8.4%

Applied MaterialsRevenue, Net Income & Inventory

CY

20130819

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Mil

lio

ns

Revenue

Income

Inventory

AMAT

- 16%

+20%%

Semiconductor Capital Equipment Shipments

by Area

www.semi.org, www.seaj.or.jp/ 9/13

20130914

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

ROW

China

Taiwan

S Korea

N America

Japan

Europe

$ Billions

Global Semiconductor & Semiconductor Capital Equipment

3-Month Shipment Growth Rates on $ Basis

Sources: SIA; Semiconductor Equipment Association of Japan, www.semi.org, Custer

Consulting Group SEMI equipment sector composite 2012 growth

20130914

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan

Au

g

Mar

Oc

t

May

Dec

Ju

l

Fe

b

Sep

Ap

r

No

v

Ju

n

Jan

Au

g

Mar

Oc

t

May

Dec

Ju

l

Fe

b

Sep

Ap

r

No

v

Ju

n

Jan

Au

g

Mar

Oc

t

May

Dec

Ju

l

Fe

b

Sep

Ap

r

No

v

Ju

n

Jan

Au

g

Mar

Oc

t

May

Dec

Ju

l

Fe

b

Sep

Ap

r

No

v

Ju

n

Jan

Au

g

Mar

84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Semiconductors

SEMI Capital Equip

Zero Growth

3/12 Rate of Change

Passive Components

Passive Components

Composite of 10 CompaniesRevenue, Net Income & Inventory

AVX, Bel Fuse, Diodes, Littlefuse, Murata, RF Micro, Rohm, Vishay, TDK, Yageo;

Euros, Yen & NT$ converted to US$ at fluctuating exchange rates

20130807

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2 Q4 Q2

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Revenue

Income

Inventory

0%

U.S. Passive Components Shipments

vs. Semiconductor Shipments to N America

U.S. Dept of Commerce

SIA

20130906

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Passive

Semiconductor

Zero Growth

3/12 Rate of Change

Semiconductors lead passive components

by 1-3 months and are more volatile

Taiwan Solar/Photovoltaic Panel Companies

Composite of 17 Manufacturers

20130912

0

5

10

15

20

25

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

00 01 02 03 04 05 06 07 08 09 10 11 12 13

NT$ (Billions)

Big Sun Energy Technology, Daxon, DelSolar, e_TON Solar Tec, Eversol, Gintech, Green Energy Technology (GET),

Ligitek, Motech, Neo Solar Power, Phoenixtec Power Co (PPC), Precision Silicon, Sino-American Silicon Products,

Sonartech, Sysgration, Tyntek, Wafer Works

Calendar Year

Global "Purchasing Managers" Index vs.

Global Passive Component & Semiconductor Shipments

20130902

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

l

00 01 02 03 04 05 06 07 08 09 10 11 12 13

Global PMI 3/12

Global Passives

Global Semiconductors

Zero Growth

Global PMI=JPMorgan

Global Passive Components = Custer Consulting Group Industry Composite

Global semiconductors = SIA

Component

Distributors

Electronic Component Distributors

Composite of 4 US Public CompaniesRevenue, Net Income & Inventory

Arrow, Avnet, Nu Horizons, Richardson

20130807

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Revenue

Income

Inventory

+4%

Q3'13/Q3'12

Guidance

+6%

Arrow ElectronicsRevenue, Net Income & Inventory

CY

20130726

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Mil

lio

ns

Revenue

Income

Inventory

+ 3%

4.9-5.3

7/24/13

ARW

+3%

DMASS - European Semiconductor

Distribution Industry

http://dmass.com/ 8/13

20130814

0

500

1000

1500

2000

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Other France UK Italy Germany

$ Millions

DMASSEuropean Semiconductor Distribution Industry

20130814

478 462

139 155123 122108 117

153 154160 167

393

333

0

100

200

300

400

500

600

Q1'13 Q2'13

Euros (Millions)

Germany

Italy

UK

France

Nordic

E Europe

Other

DMASS 8/2013; http://dmass.com/

Georg Steinberger, chairman of DMASS, commented on the results: “As expected, the

improvement on the booking side since Q4/CY12 materializes now in the form of higher

revenues, so that the market has slightly turned towards a positive trend. However, we

should be careful to over-interpret the market conditions, as bookings are just slightly

higher than billings. With China as one key economy softening, the trend could turn easily.

Nevertheless, I am cautiously optimistic that 2013 will remain positive.“

EMS & ODM

Companies

Large EMS Providers

Composite of 9 Public CompaniesRevenue, Net Income & Inventory

Benchmark+Pemstar, Celestica, Flextronics+Solectron, Foxconn, Jabil, Plexus, Sanmina-SCI,

Sypris, Venture Mfg

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

US$ Billions @ fluctuating exchange

Revenue

Income

Inventory

-1%

20130810

-8%

Q3'13/Q3'12

Guidance

Large EMS Providers

Composite of 8 Public CompaniesQuarterly Revenue Growth

Benchmark+Pemstar, Celestica, Flextronics+Solectron, Jabil, Plexus, Sanmina-SCI, Sypris,Venture Mfg

20130810

-40

-30

-20

-10

0

10

20

30

40

50

60

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Excludes Foxconn

2012/2011

2011 2012 Growth %

Foxconn (Hon Hai) 93,837 108,937 16%

Quanta Computer 35,884 32,659 -9%

Compal Electronics 21,976 20,562 -6%

Wistron 19,827 20,260 2%

Chimei Innolux 16,424 15,955 -3%

Asustek Computer 10,749 12,693 18%

Inventec 11,451 10,843 -5%

Lite On Technology 3,201 2,597 -19%

Mitac International 1,138 962 -15%

Inventec Appliance 837 0 0%

Total 215,324 225,468 +5%

Large Taiwan ODM Providers20130211

Source: Company data, NT$ converted at constant avg 2012 exchange (29.554 NT$ = 1US$)

Unconsolidated company sales (to be updated soon to consolidated sales)

2012 vs. 2011 Sales ($M)

Taiwan ODM Companies

Composite Sales of 10 Large Manufacturers

20130912

0

100

200

300

400

500

600

700

800

900

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Aug 2013 was 1.5% below

Aug 2012 and 1%

sequentially below July 2013

NT$ (Billions)

Asustek Computer, Chei Mei, Compal Electronics, Foxconn, Chimei Innolux , Inventec, Inventec Appliance, Lite On

Technology, Mitac International, Quanta Computer, Wistron, Chei Mei Display replacing Chei Mei & Innolux Display

3/10 & later

Calendar YearCompany Financial Releases

Apple Inc.Revenue, Net Income & Inventory

CY

20130726

-10

0

10

20

30

40

50

60

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Billions

Th

ou

sa

nd

s

Revenue

Income

Inventory

+ 1%

34-37

7/23/13

AAPLFY ends September

Foxconn Electronics (Hon Hai), TaiwanRevenue, Net Income & Inventory

CY

20130808

0

200

400

600

800

1000

1200

1400

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

NT$ (Billions)

Revenue

Income

Inventory

2317

+ 1%

Large ODM Companies

Composite of 10 Public ManufacturersQuarterly Revenue Growth

Asustek Computer, Compal Electronics, Foxconn, Chimei Innolux, Inventec, Inventec Appliance, Lite

On Technology, Mitac International, Quanta Computer, Wistron

20130713

-40

-20

0

20

40

60

80

100

120

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

PCB

Fabrication

2012 World PCB Production by Region

IPC 8/13

5.0%

4.5%

14.7%

42.8%

12.6%

13.4%6.6%

0.4%

N America

Europe

Japan

China/HK

Taiwan

S Korea

Rest of Asia

ROW

20130831

Total: $60.0 Billion

(US$ M @ Average 2012 Exchange)

Japan PCB Shipments20130825

0

10

20

30

40

50

60

70

80

90

100

Jan

Au

gM

ar

Oc

tM

ay

Dec

Ju

lF

eb

Sep

Ap

rN

ov

Ju

nJan

Au

gM

ar

Oc

tM

ay

Dec

Ju

lF

eb

Sep

Ap

rN

ov

Ju

nJan

Au

gM

ar

Oc

tM

ay

Dec

Ju

lF

eb

Sep

Ap

rN

ov

Ju

nJan

Au

gM

ar

Oc

tM

ay

Dec

Ju

lF

eb

Sep

Ap

rN

ov

Ju

nJan

Au

gM

ar

Oc

tM

ay

Dec

Ju

l

82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Yen (Billions)

Calendar Year

www.jpca.org/kikaitoukei/kikai2012.xls

2012/2011

-6%

Taiwan Rigid & Flex PCB ShipmentsBroad Composite of 46 Taiwan-listed Manufacturers

20130912

0

5

10

15

20

25

30

35

40

45

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

Jan

Ap

r

Ju

l

Oc

t

01 02 03 04 05 06 07 08 09 10 11 12 13

Consoldated

sales of

TSE-listed

companies

NT$ (Billions)

Calendar YearCompany Financial Releases

Includes significant

production by

Taiwan-owned

Companies

In China

European PCB Production

M Gasch 8/13

20130831

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Other 840.9 825.7 581.1 569.2 569 513.2 483.3 436 390 292.6 348.9 327.2 295 328.2

UK 641.1 478 367.5 339.6 330 278 252 197 176.6 137.4 148.5 144.7 135 105

Scandanavia 350.5 308.6 260 201.3 199.9 197.7 169 136.9 103.3 59.5 63.9 64.3 50.3 45

Austria 321.4 325.8 304 286.1 268 260.2 272.3 255.2 208.7 128.5 162.3 170.9 167 174.6

Italy 619.4 530 444 338 323.5 281 284 248 212.2 155.6 180.5 185.7 173.6 165

France 541.2 464.6 287 243.6 266 239.7 233.9 231.3 206.3 165 170 165.9 147.2 135

Germany 1460.7 1299.9 1006 1026.5 1044.4 980.6 1053.9 1039 969.5 676 882.7 902.1 834.8 888

0.00

1.00

2.00

3.00

4.00

5.00

6.00

Th

ou

sa

nd

s

Euros (Billions)

Russia & FSR not included

+1%

N American Rigid & Flexible PCB

Shipments & Orders

20130904

0

50

100

150

200

250

1 3 5 7 9 11 1 3 5 7 9 11 1 3 5 7 9 11 1 3 5 7 9 11 1 3 5 7 9 11 1 3 5 7

2008 2009 2010 2011 2012 2013

Shipments

Orders

2012/2011 Rigid & Flex

PCB Shipment Growth:

-3.2%

Note: IPC survey captures "market" not domestic production. About 15% of the above

represents imported boards resold by N American PCB producers in survey.

$M (statistical sample of about 50% of producers)

IPC

Process Equipment Related Suppliers

Composite of 9 CompaniesRevenue

C-Sun,Tailing Technology, Camtek, ESI, GSI Group, Orbotech, Mentor Graphics, Nordson,

Coherent

20130910

0

200

400

600

800

1000

1200

1400

Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1 Q3 Q1

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$ Millions

+6%PCB

Flat Panel

Displays

Touch Screens

Photovoltaic

World PCB Model

Regional PCB Shipment Growth20130913

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

lO

ct

Jan

Ap

rJu

l

00 01 02 03 04 05 06 07 08 09 10 11 12 13

Taiwan/China

Japan

N America

Europe

Zero Growth

3/12 Rate of Growth (in local currency)

Sources: IPC, JPCA, Taiwan/China composite; Eurostat "wiring devices" for Europe

Calendar Year

World PCB Monthly ShipmentsConverted @ Constant 2011 Exchange Rates

20130913

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

N America

Europe

Japan

ROA

$ Billions

Source: Custer Consulting Group

Calendar Year

World PCB Monthly ShipmentsConverted @ Constant 2011 Exchange Rates

Source: Custer Consulting Group

20130823

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

Sep

Jan

Ma

y

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

ROW

ROA

Japan

Europe

N America

Calendar Year

World PCB Shipments (with forecast)

Converted @ Constant 2011 Exchange Rates

20130913

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

May

Sep

Jan

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

Actual

Forecast

+0.9%

-4.2%

Aug 2013

1.6% below

Aug 2012

$ Billions

Source: Custer Consulting Group - 2010 base year expanded by monthly growth of

N. American, European, Japanese & Taiwan/China monthly PCB shipments

Calendar Year

Growth calculations:

Europe = composite European SIA & local

PCB assoc data

Japan & N. America from JPCA & IPC data

Taiwan/China:46 rigid & flex company

composite

Rest of Asia growth = Taiwan/China 44

company composite

Forecasts

World 4.2 0.1 1.9 5.5 6.4

USA 1.5 -0.8 -3.0 3.1 5.4

EU 1.8 -2.7 -2.3 2.0 2.7

Japan -13.5 -8.8 -12.3 3.6 4.4

Four Tigers 5.9 0.8 3.6 5.4 6.2

China 10.8 1.7 4.3 6.9 7.5

Henderson Ventures 9/2013

www.hendersonventures.com

2011 2012 2013 2014 2015

Electronic Equipment Production Growth

Constant $ Growth Rates Converted @ Constant Exchange Rates

20130912

Global PMI, Electronic Equipment, PCB &

Semiconductor Shipments

20130913

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

Dec

Mar

Ju

nS

ep

00 01 02 03 04 05 06 07 08 09 10 11 12 13

PCB

SIA

El Equip

Global PMI

Zero Growth

3/12 Rate of Change

Source: Custer Consulting Group

Calendar Year

Worldwide Semiconductor Market by Geography

WSTS Forecast

WSTS 6/13

20130604

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Asia Pacific 37.2 51.3 39.8 51.2 62.8 88.8 103.5 116.5 123.5 124.0 119.6 160.0 164.0 163.0 172.2 182.7 191.4

Japan 32.8 46.7 33.1 30.5 38.9 45.8 44.1 46.4 48.8 48.5 38.3 46.6 42.9 41.1 35.4 36.8 37.6

Europe 31.9 42.3 30.2 27.8 32.3 39.4 39.1 39.9 41.0 38.2 29.9 38.1 37.4 33.2 34.9 36.3 37.4

Americas 47.5 64.1 35.8 31.3 32.3 39.1 40.7 44.9 42.3 37.9 38.5 53.7 55.2 54.4 55.2 57.1 58.5

0

50

100

150

200

250

300

350

Worldwide Semiconductor Capital Equipment Market by

Geography (with forecast)

SEMI 7/13 (and prior reports)

20121208

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

ROW 2.69 2.1 4.49 2.86 3.71 3.05 2.61 1.44 3.84 3.41 2.1 2.17 1.94

China 1.15 2.73 1.33 2.31 2.92 1.89 0.94 3.68 3.65 2.5 2.81 5.11

S Korea 1.66 3.18 4.61 5.83 7.01 7.35 4.89 2.6 8.63 8.66 8.67 6.69 8.74

Europe 2.11 2.56 3.44 3.26 3.59 2.94 2.45 0.97 2.33 4.22 2.55 2.35 4.21

Taiwan 3.49 2.92 7.76 5.72 7.31 10.65 5.01 4.35 11.25 8.52 9.53 10.43 10.62

Japan 3.89 5.55 8.27 8.18 9.21 9.31 7.04 2.23 4.44 5.81 3.42 3.8 4.61

N America 5.91 4.73 5.81 5.7 7.32 6.55 5.63 3.39 5.75 9.26 8.15 8.04 8.75

0

5

10

15

20

25

30

35

40

45

50$ Billions

Global Electronic Supply Chain Forecast

2013 vs. 2012

-4 -2 0 2 4 6

SEMI Equipment

Semiconductors

PCBs

Electronic Equipment

Combined GDP

SEMI

Custer Consulting Group

Henderson Ventures

Henderson Ventures

HV

% Change

20130912

Global Electronic Supply Chain Forecast

2014 vs. 2013

0 5 10 15 20 25

SEMI Equipment

Semiconductors

PCBs

ElectronicEquipment

Combined GDP

SEMI

Custer Consulting Group

Henderson Ventures

HV

Henderson Ventures

% Change

20130808

ConclusionsWeak global business conditions in 1H’13; signs of

improvement in 2H’13

SE Asia dominates world electronics production.

Some increased talk of “re-shoring” due to rising costs in

China

Company financial “guidance” is a helpful forecasting tool

August PMI leading indicator data says global manufacturing

growth has resumed .

Leading indicators are useful for tracking the recovery

regionally and can be applied to products throughout

electronic supply chain.

20130814

Using This

Information to

Forecast Your

Company’s Sales

Data Sources

• Trade Organizations

• SIA, SEMI, JEITA, IPC, JPCA, DMASS, ZVEI

• Government Statistics

• US DOC, Eurostat

• Published Market Research Studies

• Company Financial Reports & Consolidated Sector Data

• Leading Indicators

• Purchasing Managers Indices, Conference Board CLI

• Consumer Confidence, Chip Foundry sales, etc.

• Your Own Company’s Sales

Forecasting Your Company Sales

• Organize monthly or quarterly sales in spreadsheet

• Obtain related industry time series for same time period

• Compare industry data and/or leading indicators to your

sales using 3/12 growth rates

• Determine lead times vs. your data

• Forecast your sales based upon lead times

• Estimate your market share gains/losses by comparing

your company growth to a related industry sector

•Custer Consulting Group can assist by providing:

• Historical industry data

• Help with analysis

Custer Consulting Group Products

Daily News Services (6 days/week)

- Global electronics supply chain

- Solar/Photovoltaic supply chain

Business Outlook

- Market charts & data

Global market

OEMs

Components, EMS, ODM, materials & process equip

Solar/Photovoltaic

- Weekly Market Comments with latest charts

20111007

Much More Information Exists

(both charts and actual chart data)

Due to time constraints only a

Limited Sample was Provided

to receive a much more complete

set of charts

Tierney Powers

Sales Associate

(415) 990-7256

SiliconExpert Panelist

Supply Chain Risk ?

Supply Chain Risk

• Inventory & Pricing

• Counterfeit Risk • Lead Time

• Lifecycle- obsolescence, Y-to-EOL • Acquisitions

• Natural Disasters

• Environmental & Regulation Compliance

– RoHS, REACH, Conflict Minerals

Current Events- Natural Disasters

http://www.eetimes.com/document.asp?doc_id=1319418

Sept. 4, 2013 SK Hynix China Computer-Memory Chip Factory Fire

“A fire at a giant Chinese factory making almost one sixth of the world's supply of a key high-tech component shows how vulnerable global manufacturing chains can be to an unexpected event, analysts say.” - Channel News Asia

Counterfeit Trends

10 16 18 30

15 19

247

68

107

22

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013throughJune 1st

Based on GIDEP & SiliconExpert Technologies

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

Product Line Percentage for the Counterfeit Parts

Counterfeit Incidents per Year

Obsolescence

Data Provided by SiliconExpert Technologies

58% of parts were obsoleteted

with PCN’s

42% of parts were obsoleted without PCN’s

Products Obsoleted with PCNs in the past 2 Years

Not all parts are obsoleted with

PCNs !

Parts Search is a powerful search tool with proprietary

search technology that produces the fastest and most

accurate search in the industry.

Extensive Search

Parametrically

Partial part number

Product line

Description

Supplier

Access

Lifecycle, PCNs

Datasheets, Application Notes

RoHS, Environmental data

Inventory

Parametric Data

1. Scrub and Validate

2. Manage Lifecycle

3. Create Custom Reports

4. Set up PCN Alerts

New Module: Supply Chain Live Demo Portion

Q&A

Q&A Session

Contact Information:

If we do not get to your question in this 1 hour allotted time period,

we will respond personally via email following this broadcast