Douja Promotion Groupe Addoha‰SENTATION AUX... · §Sister company “Ciments de l’Afrique”...

28

Douja Promotion Groupe Addoha An African leader of Real Estate Development

-

Upload

nguyenthien -

Category

Documents

-

view

213 -

download

1

Transcript of Douja Promotion Groupe Addoha‰SENTATION AUX... · §Sister company “Ciments de l’Afrique”...

Douja Promotion Groupe AddohaAn African leader of Real Estate Development

IV

I

II

Summary

Addoha Group: Strong fundamentals & a clear focus

Development in Morocco

III Development in Africa

V Appendix

Key highlights & H1 2017 Results

Addoha Group: Strong fundamentals & a clear focus

§ Leading African real estate development Group

§ Four strong brands giving multi segment market exposure

§ Robust long term growth fundamentals

§ The most attractive dividend yield in the real estate sector in Morocco

§ Full benefits now largely harvested from Cash Generation Plan

§ Strong competitive advantages that ensure the continuity of its leadership in Morocco

and will allow it to conquer new geographical markets

Strong fundamentals

Clear focus

A robust Group possessing all the resources to move forward with confidence

§ Cash generation is N°1 priority

§ Disciplined operational management to maintain margin growth momentum

§ A focused and prudent development strategy in Morocco

§ Ramp up in African development projects

§ Well-known multi-market brands allow to focus on segments showing positive trends

§ Operating strengths and financial discipline support future growth & give flexibility

§ Robust financial structure maintains land investment momentum

§ Operating expertise underrights success potential of African development

§ A track record of commitment delivery

§ A new strategic plan set to be announced before the end of 2017

Robust foundations to build our future

Development in Morocco

§ Growth potential of the real estate sector in Morocco

§ Unique business model

§ Strong brands across all market segments

§ Robust consented land reserves

§ Proven real estate project development know-how

§ A successful client focused commercial know-how

key player in the real estate sector in Morocco

Growth potential of the real estate sector in Morocco

§ Growing urbanization rate to reach 63% by 2020Morocco’s young population:

§ 68% < 34 years

§ 25% between 20 and 34 years

§ Cultural desire to become home owner

§ Fight against insalubrious housing is a national priority:583 000 households

§ Government goal: achieve a domestic production of190 000 units / year

§ Government incentives for affordable housing loans(2010 Finance Act)

§ Mobilization of private promoters (ie Addoha Fogarim,Fogalef)

§ Well positioned to leverage sector growth drivers

§ Significant deficit of 583 000 units expected to reach760 000 in 2020

§ Current average housing production 120 000 units toincrease to 150 000 units

Shortage of affordable& social housing

Demographicdynamics

Government priorities

Mortgages access

Unique business model

Customer confidence to

commit to property

acquisition from

development plans and

show homes

11 Market reputation and trust

22

33

44

Price transparency

Commercial know-how

Innovative one stop shop forcustomers

Strong brands across all market segments

§ Leader in providing access to affordable housing for low-income households

§ Several programs of social housingwithin the framework of Moroccanstate objectives

§ Pioneer in the field ofintermediate housing

§ Several housing programs mid-range for the middle classes with more demanding residential criteria.

§ Prestigia Luxury Home positionedto meet strong demand for luxuryproperties in the most popularcities in Morocco.

§ Top of the range standards ofdesign, equipment and finish

Robust consented land reserves

§ 4 000 ha fully authorized

§ Mainly composed of urban land

§ Focused acquisitions for affordable & social housing in the Casablanca-Rabat axis

§ Momentum of search for high potential opportunities

Proven real estate project development know-how

§ The optimization of the project development essential to drive margins

Prospectingstage Development stage Commercialization stage Implementation stage

§ Identification and acquisition of land reserves required for the implementation of Real Estateprojects

§ Obtaining authorizations

§ Implementation of the communication and marketing strategy;

§ Sales management.

§ Architectural conception and dimensioning of the Project;

§ Financial arrangements of the Project;

§ Negociations of contracts with the suppliers;

§Management and coordination of the various external teams involved in the project.

§ Launch of on-site construction ;

§Monitoring and guidance of the buyers.

A successful client focused commercial know-how

“Guichet Unique” One-stop shop: an innovative concept

Authenticationof signaturesNotary

Land registry

Public services

Registration

Banks

1 single point of entry for the customer

Duplicated in all the cities in which the Group is present

Advantageous pricing conditions (banks, notaries) for the customers

§ The innovative concept of the one-stop shop

Commercial chain value

A clear and monitored approach

Receptionthe of customers

Viewingof the show house

Loansimulation

Registration and bookings

Elaboration of the loanprocess

Preparationof notarial deeds

Release of loans and settlement of the full price

Key handover

Development in Africa

An ambitious development strategy in Sub-Saharan Africa

§ An extensive presence on the African continent§ Addoha continues its exploration in sub-Saharan Africa to position itself as a leader in the real estate sector in the African

continent

§ Objective : 3 000 units§ 2 lands acquired

Guinea

§ Objective : 30 000 units§ 2 lands acquired

Ivory Cost

§ Objective :10 000 units§ 1 land allocated

Congo

§ Objective :10 000 units§ 1 land allocated

Cameroun

§ Objective : 10 000 units§ 2 500 housing under the

agreement

Senegal

§ Objective : 15 000 units§ 1 land allocated

Tchad

Countries to develop in a second phase

Countries in development - Priority (tax agreements and first purchased or allocated land)

An ambitious development strategy in Sub-Saharan Africa

Challenges in the real estate sector across Africa

Addoha Group has the know-how

§ Ongoing housing shortage vs continuous demand

§ Multiple segment housing needs (affordable, social, intermediate)

§ Financing & funding a major barrier to property acquisition

§ Poor availability of construction materials

§ Absence of coherent real estate planning & development

§ Complex operating environment and conditions

§ Core strategy to develop real estate projects based on provenexperience (Cote d’Ivoire, Senegal, Guinea Conakry)

§ Expertise of covering all market segments and adapting projects to local needs

§ Leverage banking partnerships to facilitate & support credit access

§ Sister company “Ciments de l’Afrique” expansion plans to ensure cement supply in Sub-Saharan Africa

§ Replicate successful Moroccan “one stop shop” customer model

§ Expertise in developing affordable housing programs with agreements signed in several countries

§ Disciplined land acquisition policy focused on growth locations

Key highlights & H1 2017 Results

Key highlights of H1 2017

§ Ongoing improvement in operational performancedespite mixed market conditions

§ Operating margin climbs 3 points to 29.4%

§ 10% increase in sales reservations to 6,000 units

§ Further reinforcement in the financial structure

§ Reduction in Working Capital Requirement to 669 m Dh

§ Continues debt reduction to 5.9 bn Dh

§ Debt ratio decreased to 32%

Operating margin

29,4%

+3 pts

Net debt

5,9 bn Dh

-3,2%

Debt ratio*

32%

-0,4 pts

Financingcost

204 m Dh

-16%

(*) Debt ratio : Net debts/(Net debts + Equity)

Consolidated accounts – H1 2017 P&L figures

In m Dh H1 2016 H1 2017

Turnover 3 546 3 024

Operating profit 933 890

Operating margin 26.3% 29.4%

Net margin 19.5% 21.4%

Net profit, Group share 568 561

§ Turnover in the 1st Half 2017 totaled 3 bn Dh representing 7 210 units delivered.

§ Addoha postponed part of its building programme to the 2nd half so as to maximise cash generation and continue to improve

margins.

§ The operating margin stood at 29.4%.

§ The Net Profit Group Share stood at 561 m Dh, despite the postponement of production to the second half.

§ Financing costs were reduced by 16% compared to the first half of 2016 following renegotiation of terms coupled with the ongoing

debt reduction.

Consolidated accounts – H1 2017 Balance sheet figures

In m Dh 31.12.2016 30.6.2017

Total shareholder’s equity 12 723 12 543

Long term debt 4 869 4 654

Working Capital Requirement 17 661 16 992

§ The success of the Cash Generation Plan has delivered 3.4 bn Dh of net debt reduction as at the end of June. The Group’sfinancial structure now places it in a position of strength with the property sector:

§ Gearing 32%

§ Continuous WCR reduction totaling more than 3 bn Dh since 2015

§ Operating cashflow of close to 1.4 bn Dh

§ Consolidated shareholder equity of 12.5 bn Dh

Operational performance as at June 30, 2017

Cumulative operational performanceSocial & intermediate housing BU at June 30, 2017

High end BU at June 30, 2017

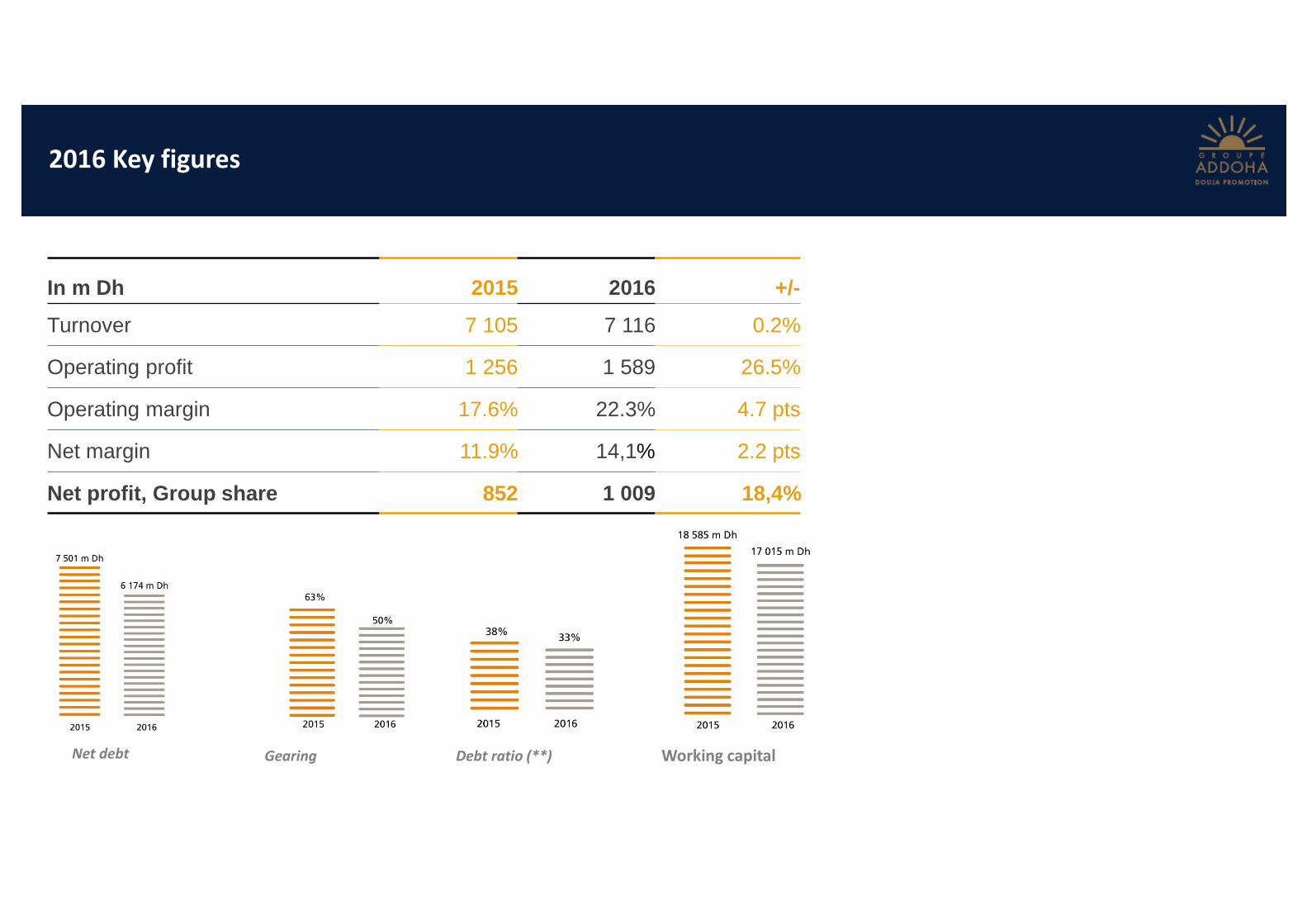

2016 Key figures

In m Dh 2015 2016 +/-

Turnover 7 105 7 116 0.2%

Operating profit 1 256 1 589 26.5%

Operating margin 17.6% 22.3% 4.7 pts

Net margin 11.9% 14,1% 2.2 pts

Net profit, Group share 852 1 009 18,4%

Working capitalNet debt Gearing Debt ratio (**)

Addoha Group leading the way in the region

Appendix

P&L performance

Key figures as at December 31, 2016

§ The consolidated revenue of 2016 amounted to 7.12 bn Dh, corresponding to 15 587 units, registering a slight.

§ The gross margin was 29%.

§ The net margin was 15.8%.

Consolidated turnover

Income and margin

Gross margin Net margin

§ Net debt at December 31, 2016 was 6.2 bn Dh, with a gearing (*) of 50% versus 63% in 2015.

§ The Group aims to bring gearing down to 33% by end-2017

(*) Gearing: Net debt/Equity(**) Debt ratio: Net debts/(Net debts + Equity)

Key Balance sheet items as at December 31, 2016

§ The Group’s working capital decrease allowed a significant improvement in the Group’s financial situation. This decrease was achieved mainly through.

§ Reduction of finished product inventories

- 771 m Dh vs 2015 & 1805 m Dh vs 2014

- Cumulative reduction of 31% since launch of CGP

§ The disbursements related to land acquisition

- 160 m Dh in 2016 (mainly the Casablanca-Rabat axis)

§ The reduction in account receivables:

- Account receivables decreased by 1 25 m Dh since December 2014

Working capital

Net debt

Gearing Debt ratio (**)

Stock Performance