DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO 17...

72

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO 17 March 2003 - NOT LEGALY BINDING - Page n°1 Model Contract (*) for the Sixth Framework Programme (*) except for actions to promote human resources and mobility

-

Upload

gavin-little -

Category

Documents

-

view

214 -

download

0

Transcript of DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO 17...

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°1

Model Contract(*) for the Sixth Framework

Programme

(*) except for actions to promote human resources and mobility

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°2

EC TREATY

FRAMEWORK PROGRAMME

SPECIFIC PROGRAMS

PARTICIPATION AND

DISSEMINATION RULES

CONTRACTS

Other relevant EC Regulations:

e.g. EC Financial Regulations

(Budgetary Law)

INTERNATIONAL AGREEMENTS

Introduction:0.1- Legal framework

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°3

Based on the rules for participation and dissemination of results and

collective approach

greater flexibility

greater autonomy of participants

reduction in the number of contracts

Introduction:0.2- General contractual principles

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°4

Introduction:0.3.1- Contract Structure

Core-contractStandard text completed with project data (+ special clauses)

Annex IThe “project” (technical tasks - work to be carried out)

Annex IIGeneral conditions (standard text applicable to every instrument, excepting actions to promote human resources and mobility)

Annex IIISpecific provisions for some instruments (standard text)

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°5

Introduction:0.3.2- Contract Structure

Annex IV - Form AConsent of contractors to accede to the contract (standard text completed with project data - To be filled in by each contractor identified in the core-contract (article 1.2) - To be signed by the contractor concerned and by the coordinator)

Annex V - Form BAccession of new legal entities to the contract (standard text completed with project data - To be filled in by each new participant willing to become contractor - To be signed by the new contractor concerned and by the coordinator)

Annex VI - Form CFinancial statement per activity (Specific to each instrument and/or type of action - To be filled periodically by each contractor)

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°6

Introduction:0.4- Guidelines

Different guidelines will provide supplementary information and guidance notes:

Financial guidelines (including cost models, audits, …) Negotiation guidelines (including technical annex, contract preparation, ...) Consortium agreement guidelines (including IPR, ...) Project management guidelines (including reporting, ...)

Plus guidelines explicitly required by the rules for participation and dissemination of results:

Guidelines on evaluation and selection procedures

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°7

Introduction:0.5- Consortium Agreement

Compulsory, unless exempted by the call for proposals

No model but non binding guidelines provided by the Commission

Regulates internal organisation and management of consortium (Commissionis not a party)

After or (preferably) before signing the contract.Some decisions must be made by the participants before signature of contract(e.g. exclusion of pre-existing know-how)By definition, contractors are supposed to have a consortium agreement.

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°8

1- Core-Contract1.1- Structure

The structure of the core-contract is the following:

Article 1 - Scope Article 2 - Constitution of the Consortium Article 3 - Evolution of the consortium Article 4 - Entry into Force of the Contract and Duration of Project Article 5 - Community financial contribution Article 6 - Reporting periods Article 7 - Reports Article 8 - Payment modalities Article 9 - Special clauses Article 10 - Amendments Article 11 - Communication Article 12 - Applicable law Article 13 - Jurisdiction Article 14 - Annexes forming an integral part of this contract

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°9

1- Core-Contract1.2.1- Main issues

Signature and entry into force of the contract

Contractual link of all contractors with the Commission (equal status)

Contract enters into force upon signature of coordinator and Commission

Coordinator must ensure other contractors sign within delays (established in contract) (Confere Form A)

Distribution of advance (pre-financing) to other contractors possible after minimum requirements met

Project begins on date established in the contract

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°10

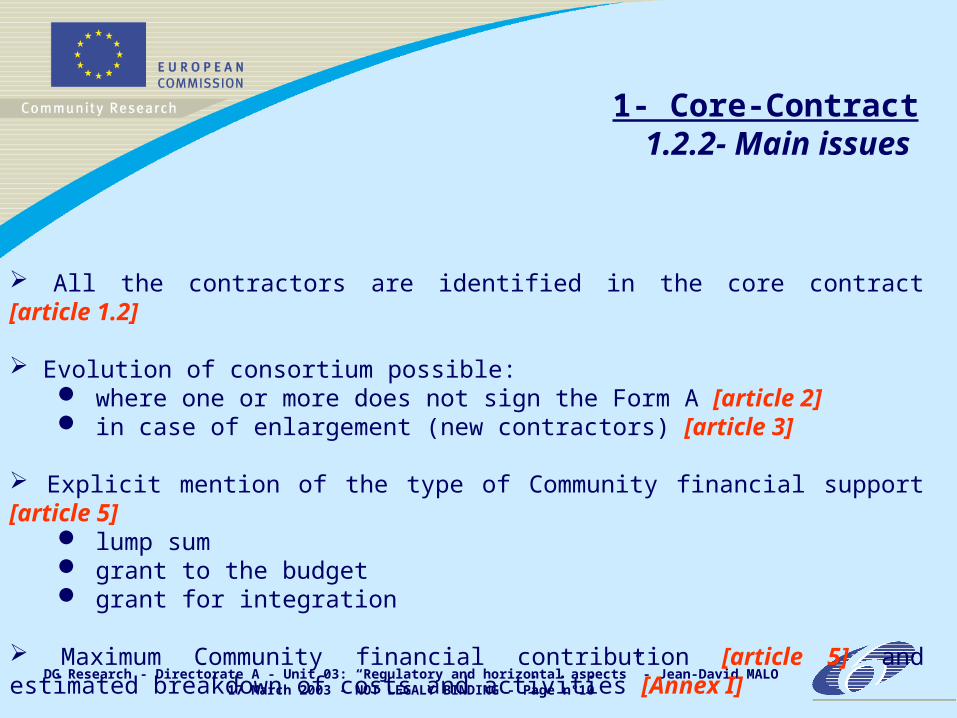

1- Core-Contract1.2.2- Main issues

All the contractors are identified in the core contract [article 1.2]

Evolution of consortium possible: where one or more does not sign the Form A [article 2] in case of enlargement (new contractors) [article 3]

Explicit mention of the type of Community financial support [article 5] lump sum grant to the budget grant for integration

Maximum Community financial contribution [article 5] and estimated breakdown of costs and activities [Annex I]

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°11

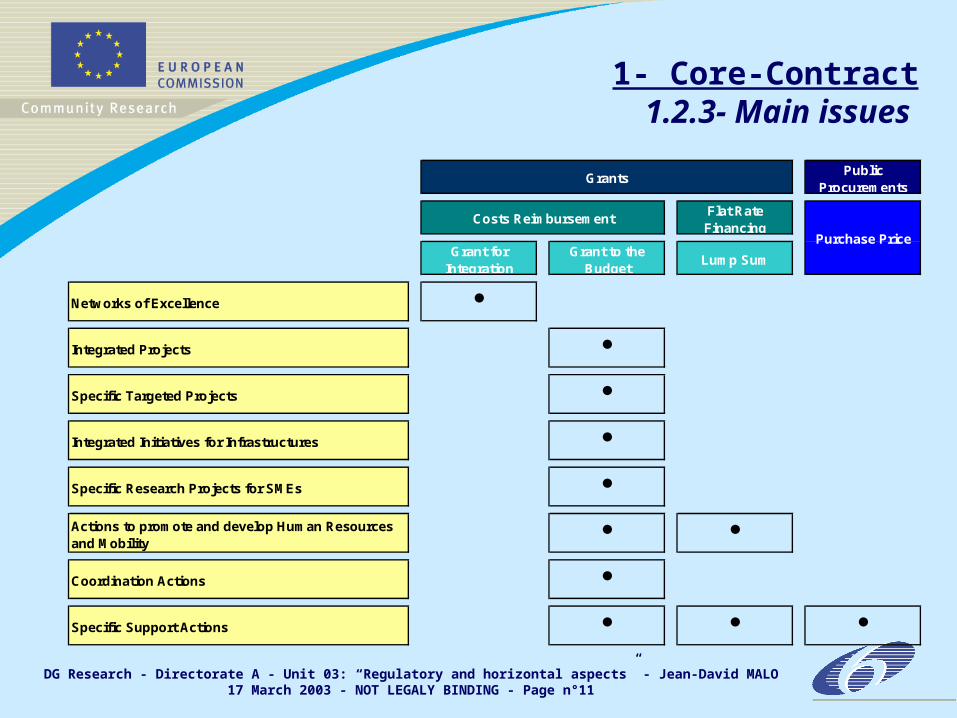

1- Core-Contract1.2.3- Main issues

Public Procurements

Flat Rate Financing

Grant for Integration

Grant to the Budget

Lump Sum

Networks of Excellence

Integrated Projects

Specific Targeted Projects

Integrated Initiatives for Infrastructures

Specific Research Projects for SMEs

Actions to promote and develop Human Resources and Mobility

Coordination Actions

Specific Support Actions

Grants

Costs Reimbursement

Purchase Price

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°12

1- Core-Contract1.2.4- Main issues

Reporting periods are clearly established in the core-contract [article 6]

The following reports must be submitted for each reporting period within 45 days after the end of the concerned reporting period [article 7.1 + Annex II.7.2]:

Periodic activity report (including plan for using and disseminating the knowledge) Periodic management report (including a justification of resources deployed + Forms C + summary financial report consolidating the claimed costs) Periodic report of the distribution between contractors of the Community financial contribution Any supplementary reports required by any Annex of the contract (Annexes I and III)

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°13

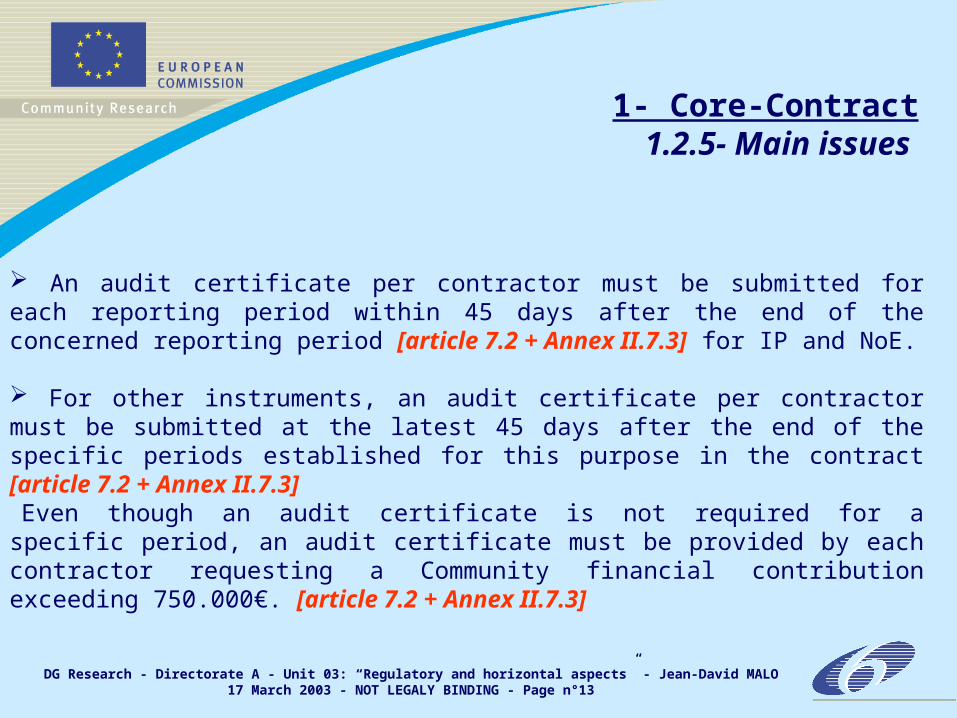

1- Core-Contract1.2.5- Main issues

An audit certificate per contractor must be submitted for each reporting period within 45 days after the end of the concerned reporting period [article 7.2 + Annex II.7.3] for IP and NoE.

For other instruments, an audit certificate per contractor must be submitted at the latest 45 days after the end of the specific periods established for this purpose in the contract [article 7.2 + Annex II.7.3] Even though an audit certificate is not required for a specific period, an audit certificate must be provided by each contractor requesting a Community financial contribution exceeding 750.000€. [article 7.2 + Annex II.7.3]

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°14

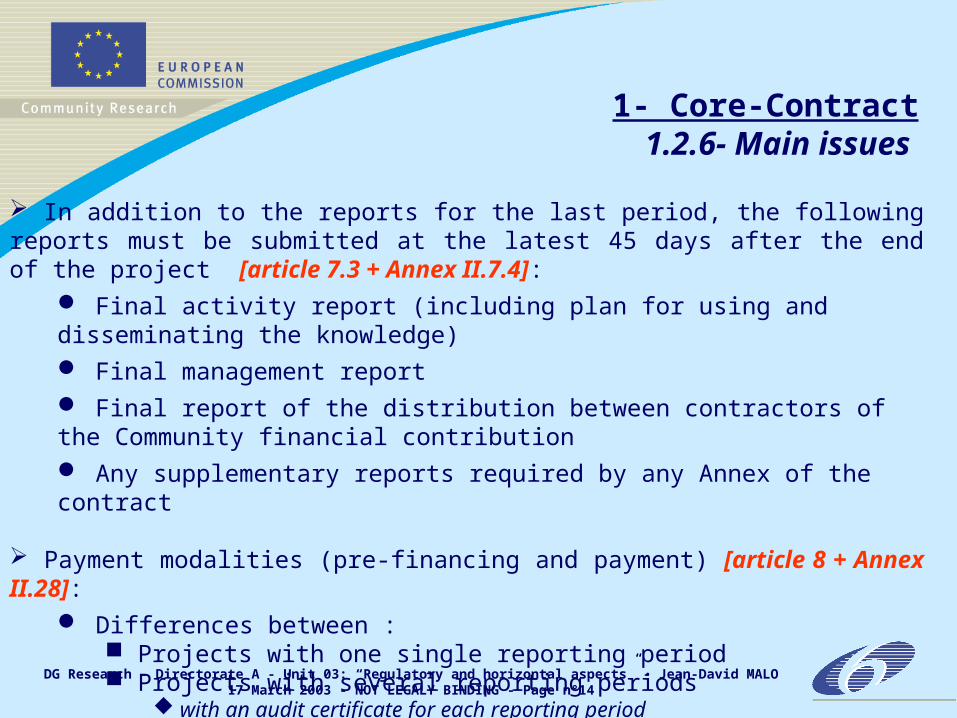

1- Core-Contract1.2.6- Main issues

In addition to the reports for the last period, the following reports must be submitted at the latest 45 days after the end of the project [article 7.3 + Annex II.7.4]:

Final activity report (including plan for using and disseminating the knowledge) Final management report Final report of the distribution between contractors of the Community financial contribution Any supplementary reports required by any Annex of the contract

Payment modalities (pre-financing and payment) [article 8 + Annex II.28]:

Differences between : Projects with one single reporting period Projects with several reporting periods

with an audit certificate for each reporting period without an audit certificate for each reporting period

Lump sum support

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°15

Payments and reporting Payments and reporting schedule for an IPschedule for an IP(example of a 4 year contract)(example of a 4 year contract)

Activity report

Reported costs

Activity report Detailed work plan

Reported costs Adjusted advance

Activity report Detailed work plan

Reported costs Adjusted advance

Activity report

Reported costs

Detailed work plan

Adjusted advance

Detailed work plan

Initial advance

0 6 12 18 24 30 36 42 48

Months

1- Core-Contract1.2.7- Main issues

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°16

1- Core-Contract1.2.8- Main issues Payments and reporting Payments and reporting

schedule for a STREP, CA or schedule for a STREP, CA or SSASSA(example of a 3 year contract)(example of a 3 year contract)

Final activity report

Reported costs + audit certificate (mandatory)

Final payment

Periodic activity report (mid-term review : optional)

Reported costs+ (audit certificate if required)

Intermediate payment/

settlement

Detailed work plan

Initial advance

0 6 12 14 18 20 24 26 30 36 38

Months

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°17

1- Core-Contract1.2.9- Main issues

The core-contract may content some special clauses [article 9]: Some of them may be imposed (e.g.: specific cost models rules for specific activities consisting in transnational access for an SSA - Infrastructures) Others, answering to specific situations will be at the disposal of the contractors

Amendments [article 10 + Annex II.8]:General rule: request in writingTacit amendments: only for modification and evolution of the consortium ; and for technical reports

The law of Belgian or Luxembourg govern the contract [article 12]

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°18

2- Annex II - General conditions2.1- General Structure

The structure of the Annex II is the following:

Article II.1 - Definitions

Part A: Implementation of the Project

Part B: Financial Provisions

Part C: Intellectual Property Rights

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°19

2- Annex II - General conditions2.2.1- Detailed structure

Part A: Implementation of the Project SECTION 1 - IMPLEMENTATION AND DELIVERABLES

Article II.2 - ACTIVITIES Article II.3 - PERFORMANCE OBLIGATIONS Article II.4 - FORCE MAJEURE Article II.5 - SUSPENSION AND PROLONGATION OF THE PROJECT Article II.6 - SUBCONTRACTING Article II.7 - REPORTS AND DELIVERABLES Article II.8 - EVALUATION AND APPROVAL OF REPORTS AND DELIVERABLES Article II.9 - CONFIDENTIALITY Article II.10 - COMMUNICATION OF DATA Article II.11 - INFORMATION TO MEMBER STATES AND ASSOCIATED STATES Article II.12 - PUBLICITY Article II.13 - LIABILITY Article II.14 - ASSIGNMENT

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°20

Part A: Implementation of the Project SECTION 2 - TERMINATION OF THE CONTRACT AND RESPONSIBILITY

Article II.15 - TERMINATION OF THE CONTRACT AND PARTICIPATION OF CONTRACTORS Article II.16 - TERMINATION FOR BREACH OF CONTRACT AND IRREGULARITY Article II.17 - TECHNICAL COLLECTIVE RESPONSIBILITY Article II.18 - FINANCIAL COLLECTIVE RESPONSIBILITY

2- Annex II - General conditions2.2.2- Detailed structure

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°21

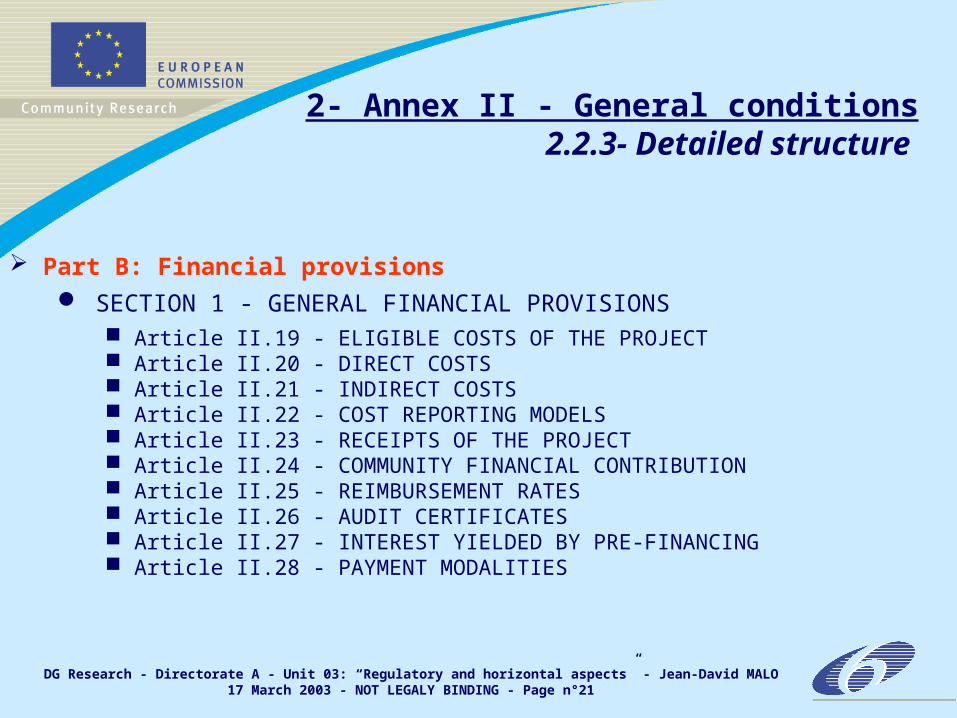

2- Annex II - General conditions2.2.3- Detailed structure

Part B: Financial provisions SECTION 1 - GENERAL FINANCIAL PROVISIONS

Article II.19 - ELIGIBLE COSTS OF THE PROJECT Article II.20 - DIRECT COSTS Article II.21 - INDIRECT COSTS Article II.22 - COST REPORTING MODELS Article II.23 - RECEIPTS OF THE PROJECT Article II.24 - COMMUNITY FINANCIAL CONTRIBUTION Article II.25 - REIMBURSEMENT RATES Article II.26 - AUDIT CERTIFICATES Article II.27 - INTEREST YIELDED BY PRE-FINANCING Article II.28 - PAYMENT MODALITIES

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°22

Part B: Financial provisions SECTION 2 - CONTROLS, RECOVERIES AND SANCTIONS

Article II.29 - CONTROLS AND AUDITS Article II.30 - LIQUIDATED DAMAGES Article II.31 - REIMBURSEMENT TO THE COMMISSION AND RECOVERY ORDERS

Part C: Intellectual Property Rights Article II.32 - OWNERSHIP OF KNOWLEDGE Article II.33 - PROTECTION OF KNOWLEDGE Article II.34 - USE AND DISSEMINATION Article II.35 - ACCESS RIGHTS Article II.36 - INCOMPATIBLE OR RESTRICTIVE COMMITMENTS

2- Annex II - General conditions2.2.4- Detailed structure

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°23

2- Annex II - General conditions2.3.1- Main issues

The main issues which must be highlighted are:

Performance obligations (consortium, contractors, coordinator, Commission) Force majeure Prolongation and suspension of the project (clear provisions for possibility to suspend and prolong project) Termination (simple without fault or breach and with breach) Nullification

and especially ...

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°24

2- Annex II - General conditions2.3.2.1- Main issues - Subcontracting

As far as subcontracts are concerned, the model contract of the 6th Framework Programme will mention the following:

Contractors shall ensure that the work to be performed, as identified in the technical annex of the contract (Annex I), can be carried out by them. However, where it is necessary to subcontract certain elements of the work to be carried out, this should be clearly identified in the technical annex of the contract (Annex I). During the implementation of the project, contractors may subcontract other minor services, which do not represent core elements of the project work, which cannot be directly assumed by them and where this proves necessary for the performance of their work under the project.

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°25

2- Annex II - General conditions2.3.2.2- Main issues - Subcontracting

Any subcontract, the costs of which are to be claimed as an eligible cost, must be awarded following competitive tender to the subcontractor offering best value for money (best price-quality ratio), under conditions of transparency and equal treatment. The following aspects must be taken into consideration in awarding subcontracts:

(a) they may only cover the execution of a limited part of the project;

(b) recourse to the award of subcontracts must be justified having regard to the nature of the action and what is necessary for its implementation;

(c) the tasks concerned must be set out in the technical annex of the contract (Annex I);

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°26

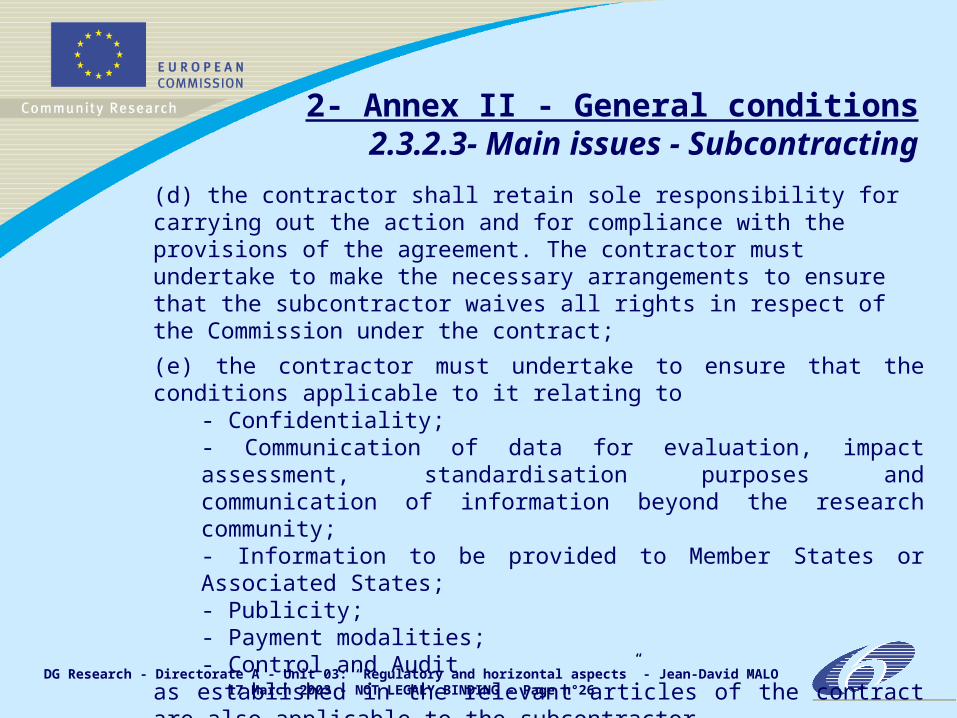

(d) the contractor shall retain sole responsibility for carrying out the action and for compliance with the provisions of the agreement. The contractor must undertake to make the necessary arrangements to ensure that the subcontractor waives all rights in respect of the Commission under the contract;

(e) the contractor must undertake to ensure that the conditions applicable to it relating to

- Confidentiality;- Communication of data for evaluation, impact assessment, standardisation purposes and communication of information beyond the research community;- Information to be provided to Member States or Associated States;- Publicity;- Payment modalities;- Control and Audit

as established in the relevant articles of the contract are also applicable to the subcontractor.

2- Annex II - General conditions2.3.2.3- Main issues - Subcontracting

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°27

2- Annex II - General conditions2.3.2.4- Main issues - Subcontracting

Where the contractors enter into subcontracts to carry out some parts of the tasks related to the project, they remain bound by their obligations to the Commission under the contract

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°28

2- Annex II - General conditions2.3.3- Main issues - Collective

Responsibility

Technical Responsibility (applicable to all instruments)

Financial Responsibility - New

Used as a last resort Limited in proportion to the participant’s share to the project, up to the total amount they are entitled to receive Exceptions:

International Organisations, public bodies or entities guaranteed by MS/AS: solely responsible for their own debts Specific research projects for SME’s [and actions to promote human resources and mobility] and, when duly justified, specific support actions

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°29

The cost models are applicable to all instruments in the Sixth Framework Programme where the Community contribution is a Grant for Integration (Networks of Excellence) or a Grant to the Budget (Integrated Projects, Specific Targeted Projects, Specific Research Projects for SMEs, Integrated Infrastructure Initiatives, Coordination Actions, and certain Specific Support Actions).

They do not apply to those instruments where the Community financial contribution is a Lump Sum Grant (certain Specific Support Actions and certain Actions promoting human resources and mobility).

For some Actions promoting human resources and mobility a specialised version of the cost model is applied.

Cost Models Applicability

2- Annex II - General conditions2.3.4.1- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°30

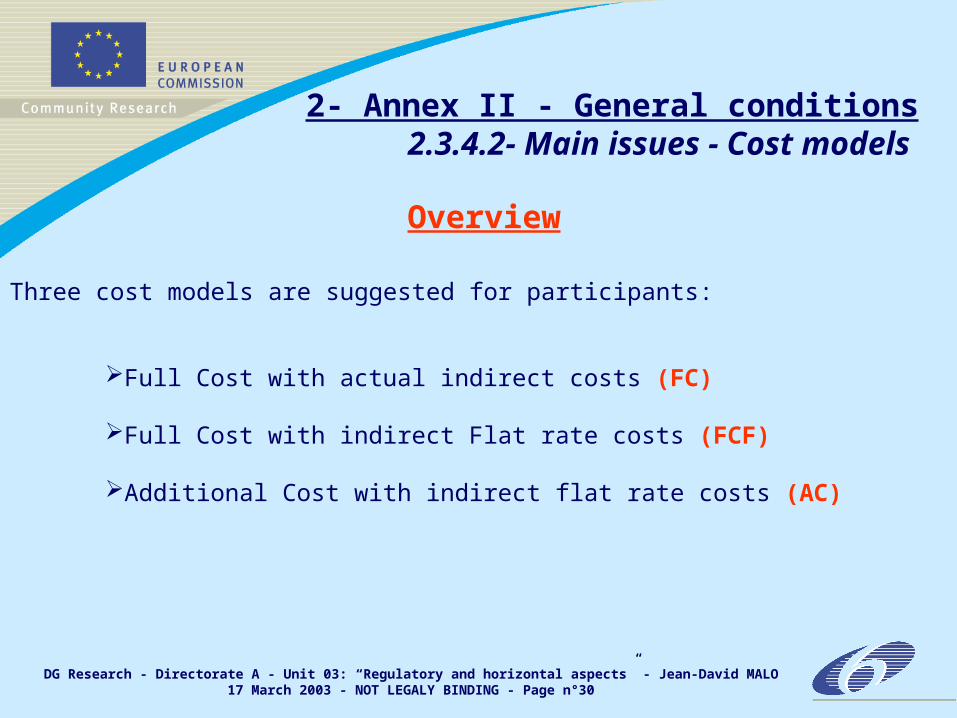

Three cost models are suggested for participants:

Full Cost with actual indirect costs (FC)

Full Cost with indirect Flat rate costs (FCF)

Additional Cost with indirect flat rate costs (AC)

Overview

2- Annex II - General conditions2.3.4.2- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°31

Full Cost with actual indirect costs (FC)In this model, eligible direct and indirect costs are charged by the contractors.

Full Cost with indirect Flat rate costs (FCF)In this model, eligible direct costs and a flat rate for indirect costs are charged by the contractors. This flat rate applied is 20% of all eligible direct costs minus the eligible direct costs of sub-contracts.

Additional Cost with indirect flat rate costs (AC)In this model, eligible direct additional costs and a flat rate for indirect costs are charged by the contractors. The flat rate is equal to 20% of all eligible direct additional costs minus the eligible direct additional costs of sub-contracts.

Definitions

2- Annex II - General conditions2.3.4.3- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°32

Direct costs are all costs that fall under the definition of eligible costs which can be charged directly to the project, and are determined by the contractor in accordance with its usual accounting practices. Direct additional costs are direct costs additional to the normal recurring costs of the contractor and not covered by any other sources of funding. For direct additional costs of personnel, there are three possibilities to charge these costs to the contract:

personnel with a temporary contract for working under the Community contract concerned ; personnel with a temporary contract with a view to completing a doctorate ; personnel whose employment contract depends wholly or in part on additional external financing. In this case, costs charged to the project must exclude all costs covered by normal recurring financing.

Definitions

2- Annex II - General conditions2.3.4.4- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°33

Indirect costs

For contractors working on the full cost model (FC), indirect costs are all eligible costs determined by the contractor, in accordance with its usual accounting practices, which are not directly attributable to the project but are incurred in direct relation to the direct costs of the project.

For those contractors using either of the flat rate models (FCF, AC) a flat rate is applied to the direct costs to cover the indirect costs.

Definitions

2- Annex II - General conditions2.3.4.5- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°34

Eligible costs incurred for the implementation of the project must fulfil all of the following conditions:

they must be actual, economic and necessary for the implementation of the project; and they must be determined in accordance with the usual accounting principles of the contractor andthey must be incurred during the duration of the project except for the costs incurred in drawing up the final reports which may be incurred during the period of up to 45 days after the end of the project or the date of termination whichever is earlier; and

Definitions

2- Annex II - General conditions2.3.4.6- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°35

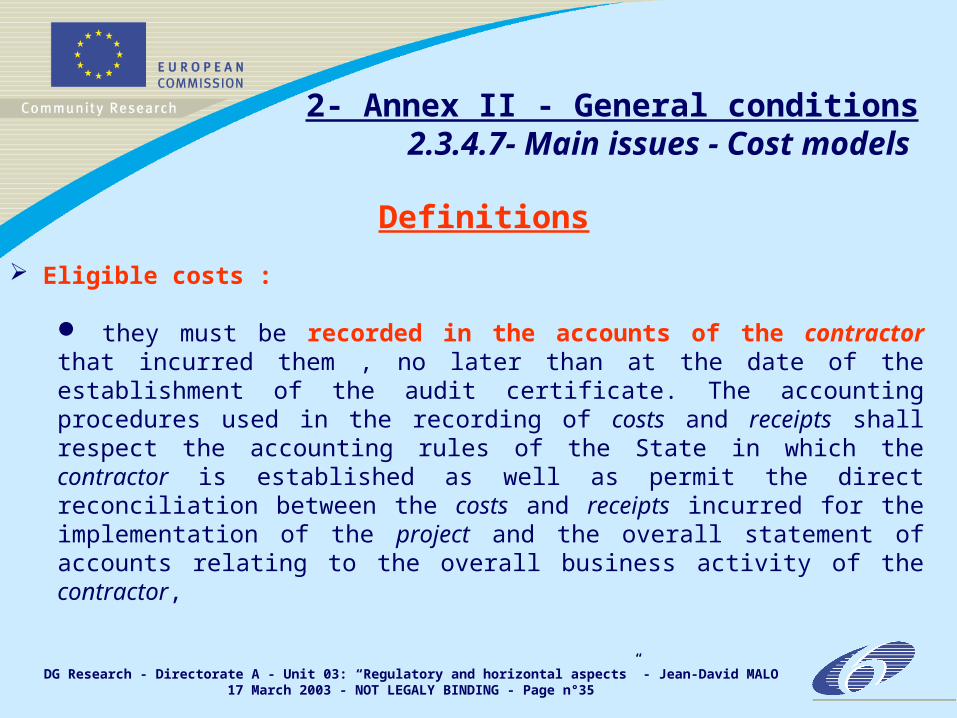

Eligible costs :

they must be recorded in the accounts of the contractor that incurred them , no later than at the date of the establishment of the audit certificate. The accounting procedures used in the recording of costs and receipts shall respect the accounting rules of the State in which the contractor is established as well as permit the direct reconciliation between the costs and receipts incurred for the implementation of the project and the overall statement of accounts relating to the overall business activity of the contractor,

2- Annex II - General conditions2.3.4.7- Main issues - Cost models

Definitions

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°36

Eligible costs :

In the case of contributions made by third parties established on the basis of an agreement between the contractor and the third party existing prior to the participation of the contractor in the contract, and for which the tasks and their execution by such a third party are clearly identified in the technical Annex (Annex I), the costs must be:

incurred in accordance with the usual accounting principles of such third parties and the principles set out for any contractor; meet the other provisions of the eligible costs definition and of Annex I.; and be recorded in the accounts of the third party no later than the date of the establishment of the audit certificate

2- Annex II - General conditions2.3.4.8- Main issues - Cost models

Definitions

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°37

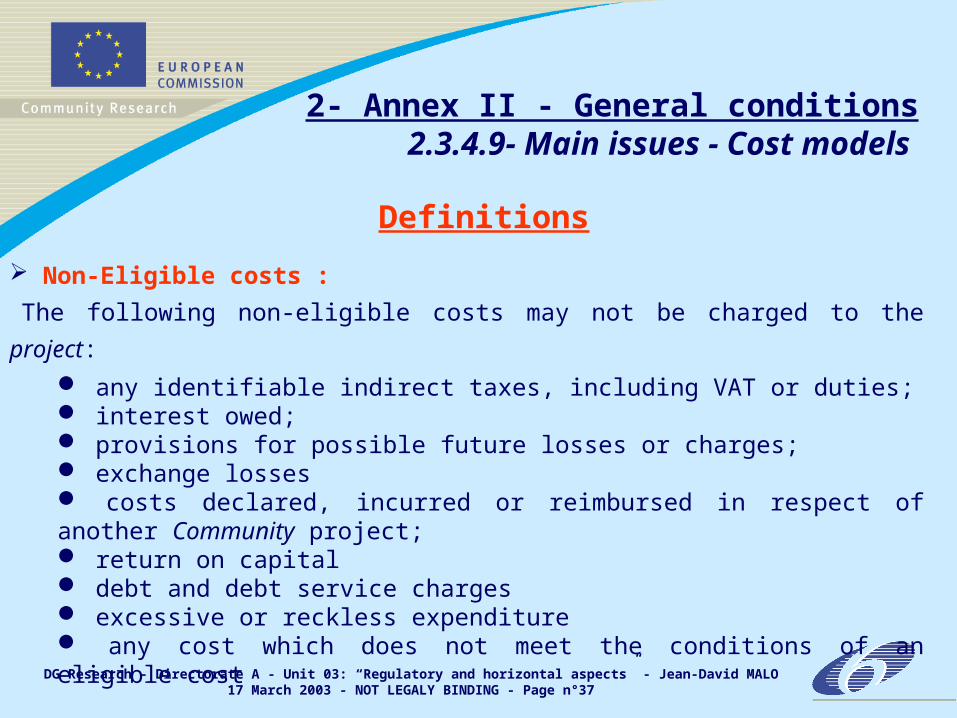

Non-Eligible costs :

The following non-eligible costs may not be charged to the project: any identifiable indirect taxes, including VAT or duties; interest owed; provisions for possible future losses or charges; exchange losses costs declared, incurred or reimbursed in respect of another Community project; return on capital debt and debt service charges excessive or reckless expenditure any cost which does not meet the conditions of an eligible cost

2- Annex II - General conditions2.3.4.9- Main issues - Cost models

Definitions

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°38

Access to a cost model depends on the type of legal entity concerned:

All legal entities can use the FC model with the exception of physical persons ;

Physical persons are obliged to use the AC model ;

Non-commercial or non-profit organisations established either under public law or private law and international organisations may choose one of the AC, FCF or FC models. However, only those non-commercial or non-profit organisations which do not have an accounting system that allows the share of their direct and indirect costs relating to the project to be distinguished may opt for the AC model.

Legal entities defined as SMEs have the choice between the FC and FCF model.

Access to the Cost Models

2- Annex II - General conditions2.3.4.10- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°39

Each contractor shall apply the same cost reporting model in all contracts established under the Sixth Framework Programme

As a derogation to this principle: any legal entity which is eligible to opt for the AC model in a first contract can change to the FCF or the FC model in a later contract. If it does so, it must then use the new cost reporting model in subsequent contracts;any legal entity which is eligible to opt for the FCF model in a first contract can change to the FC model in a later contract. If it does so, it must then use the new cost reporting model in subsequent contracts.

AC FCF FCFCF FCAC FC

Use of a Cost Model

2- Annex II - General conditions2.3.4.11- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°40

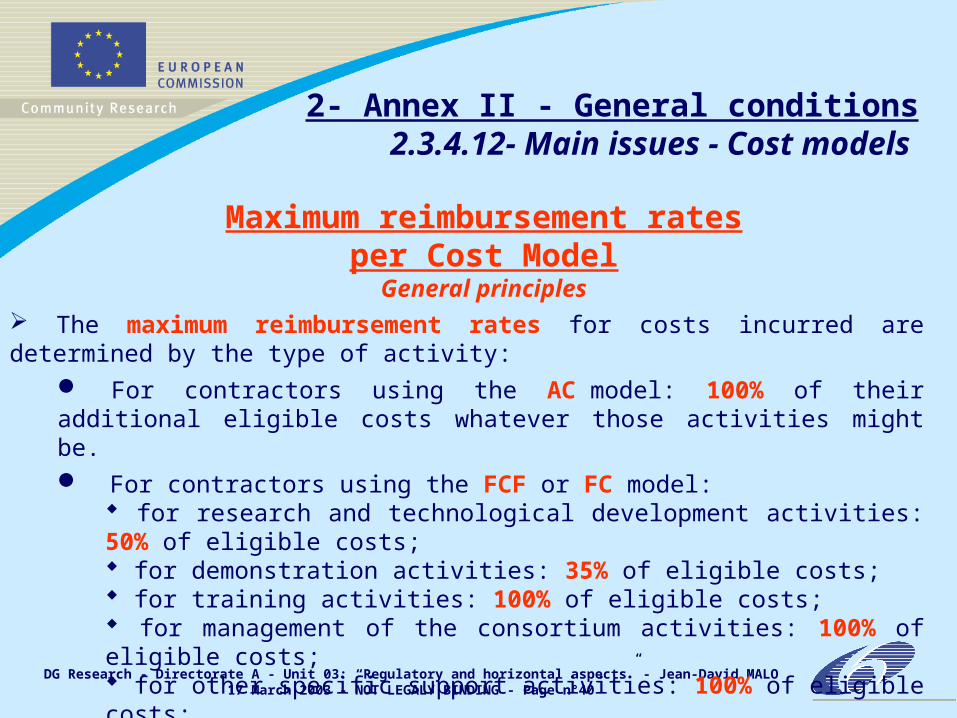

The maximum reimbursement rates for costs incurred are determined by the type of activity:

For contractors using the AC model: 100% of their additional eligible costs whatever those activities might be. For contractors using the FCF or FC model:

for research and technological development activities: 50% of eligible costs; for demonstration activities: 35% of eligible costs; for training activities: 100% of eligible costs; for management of the consortium activities: 100% of eligible costs; for other specific support activities: 100% of eligible costs;

Maximum reimbursement ratesper Cost ModelGeneral principles

2- Annex II - General conditions2.3.4.12- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°41

It should be noted that the Community financial contribution of 100% to the management of the consortium activities can not exceed 7% of the total Community financial contribution. This limitation does not apply to each individual participant but for the project as a whole.

One derogation to the definition of eligible costs, relates to the costs incurred for management of the consortium activities by contractors using the AC model. They may charge their eligible direct costs (especially of permanent personnel) to this activity, on condition that they can to identify and justify them precisely. The flat rate for indirect costs also applies to these eligible direct costs.

Maximum reimbursement ratesper Cost Model

Particularities

2- Annex II - General conditions2.3.4.13- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°42

For Coordination Actions and Specific Support Actions, contractors using the full cost model (FC) may not claim their actual indirect costs. A flat rate for indirect costs is applied in these instruments for all contractors, equal to 20% of the eligible direct costs minus the eligible direct costs of sub-contracts.

Finally, it should be noted that the reimbursement rate claimed represents a possible maximum rate since the receipts of the project must be taken into consideration in determining the total amount of the Commission financial contribution.

Maximum reimbursement ratesper Cost Model

Particularities

2- Annex II - General conditions2.3.4.14- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°43

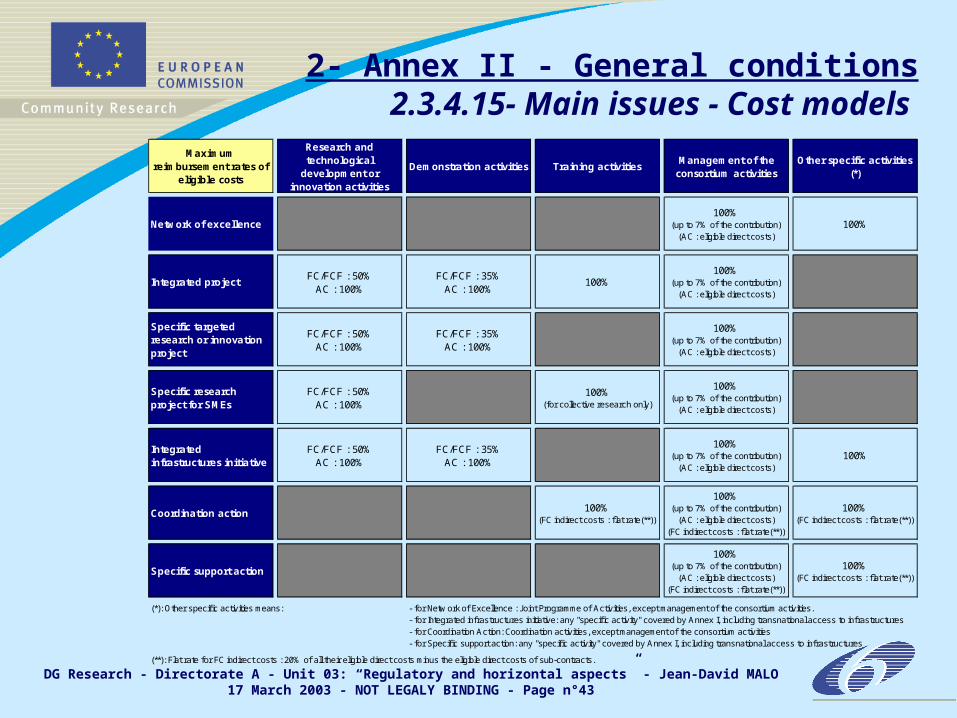

Maximum reimbursement rates of

eligible costs

Research and technological

development or innovation activities

Demonstration activities Training activitiesManagement of the

consortium activitiesOther specific activities

(*)

Network of excellence100%

(up to 7% of the contribution)(AC : eligible direct costs)

100%

Integrated projectFC/FCF : 50%

AC : 100%FC/FCF : 35%

AC : 100%100%

100%(up to 7% of the contribution)

(AC : eligible direct costs)

Specific targeted research or innovation project

FC/FCF : 50%AC : 100%

FC/FCF : 35%AC : 100%

100%(up to 7% of the contribution)

(AC : eligible direct costs)

Specific research project for SMEs

FC/FCF : 50%AC : 100%

100%(for collective research only)

100%(up to 7% of the contribution)

(AC : eligible direct costs)

Integrated infrastructures initiative

FC/FCF : 50%AC : 100%

FC/FCF : 35%AC : 100%

100%(up to 7% of the contribution)

(AC : eligible direct costs)100%

Coordination action 100%(FC indirect costs : f lat rate(**))

100%(up to 7% of the contribution)

(AC : eligible direct costs)(FC indirect costs : f lat rate(**))

100%(FC indirect costs : f lat rate(**))

Specific support action

100%(up to 7% of the contribution)

(AC : eligible direct costs)(FC indirect costs : f lat rate(**))

100%(FC indirect costs : f lat rate(**))

(*): Other specif ic activities means: - for Netw ork of Excellence : Joint Programme of Activities, except management of the consortium activities.- for Integrated infrastructures initiative: any "specif ic activity" covered by Annex I, including transnational access to infrastructures- for Coordination Action: Coordination activities, except management of the consortium activities- for Specif ic support action: any "specif ic activity" covered by Annex I, including transnational access to infrastructures

(**): Flat rate for FC indirect costs : 20% of all their eligible direct costs minus the eligible direct costs of sub-contracts.

2- Annex II - General conditions2.3.4.15- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°44

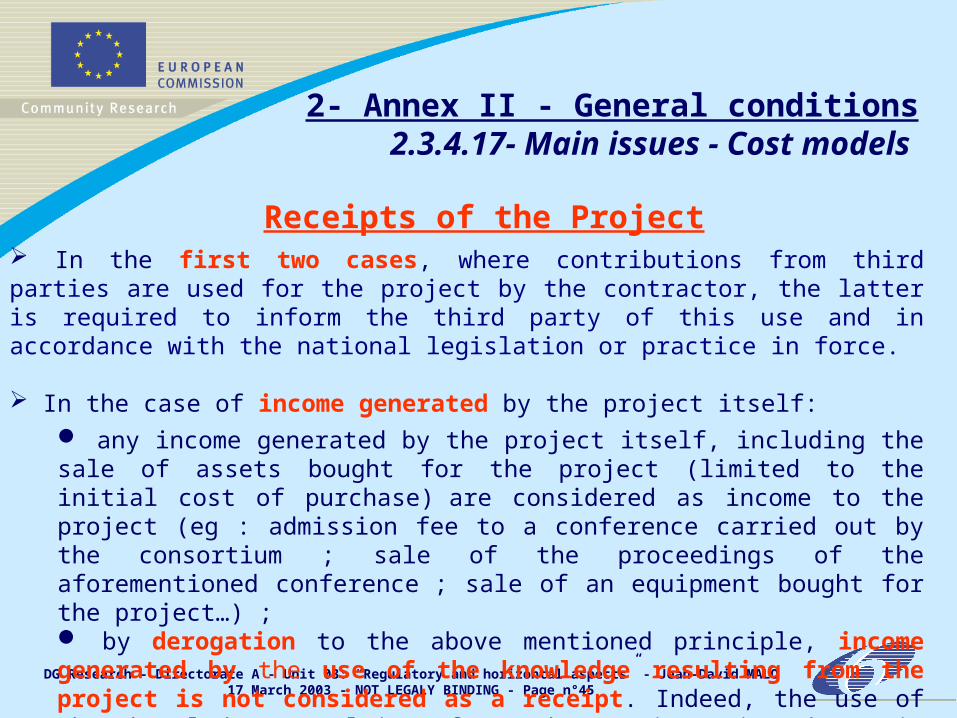

Three kinds of receipts must be taken into consideration: Financial transfers or their equivalent to the contractor from third parties ; Contributions in kind from third parties; Income generated by the project.

In the first two cases (financial transfers or contributions in kind), these endowments are considered as receipts of the project if the third party has provided them specifically to be use in the project.If, on the other hand, these endowments are at the discretion of the contractor they are not to be considered as receipts.

Receipts of the Project

2- Annex II - General conditions2.3.4.16- Main issues - Cost models

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°45

In the first two cases, where contributions from third parties are used for the project by the contractor, the latter is required to inform the third party of this use and in accordance with the national legislation or practice in force.

In the case of income generated by the project itself: any income generated by the project itself, including the sale of assets bought for the project (limited to the initial cost of purchase) are considered as income to the project (eg : admission fee to a conference carried out by the consortium ; sale of the proceedings of the aforementioned conference ; sale of an equipment bought for the project…) ; by derogation to the above mentioned principle, income generated by the use of the knowledge resulting from the project is not considered as a receipt. Indeed, the use of the knowledge resulting from the project is the main objective of any project supported by an FP6 Community financial contribution.

2- Annex II - General conditions2.3.4.17- Main issues - Cost models

Receipts of the Project

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°46

2- Annex II - General conditions2.3.5- Main issues - Audit

certificates

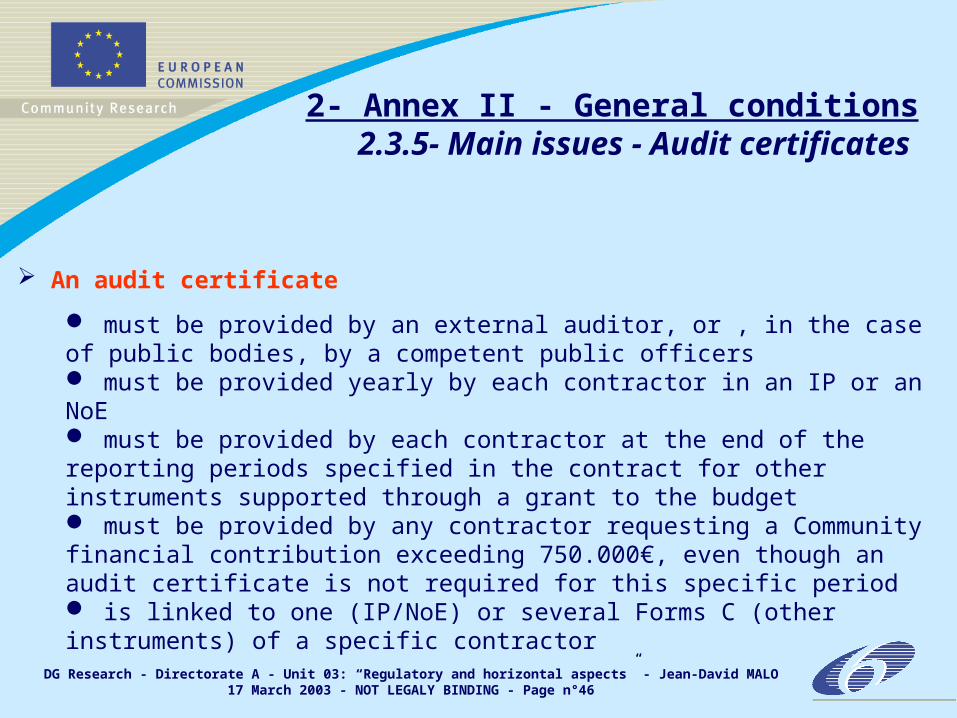

An audit certificate

must be provided by an external auditor, or , in the case of public bodies, by a competent public officers must be provided yearly by each contractor in an IP or an NoE must be provided by each contractor at the end of the reporting periods specified in the contract for other instruments supported through a grant to the budget must be provided by any contractor requesting a Community financial contribution exceeding 750.000€, even though an audit certificate is not required for this specific period is linked to one (IP/NoE) or several Forms C (other instruments) of a specific contractor

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°47

2- Annex II - General conditions2.3.6- Main issues - Payments

Periodic advances

yearly for IP and NoE (specified in the contract for other instruments) up to 85% (80% for instruments without collective liability)

Community financial contribution depends on:

Contractor’s cost model (AC, FC, FCF) Type of activity (research, demonstration, management, training, etc) Submission of audit certificates

Distribution depends on consortium’s decisions

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°48

2- Annex II - General conditions2.3.7- Main issues - Controls &

Audits Controls

Periodic activity report (including plan for using and disseminating the knowledge) Periodic management report (including a justification of resources deployed + Forms C + summary financial report consolidating the claimed costs) Periodic report of the distribution between contractors of the Community financial contribution Any supplementary reports required by any Annex of the contract (Annexes I and III)

Audits

Scientific, technological, and financial audits New - annual monitoring by Commission with external experts (particularly for IP and NoE) Ethical or other reviews Contractors right to refuse particular expert

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°49

2- Annex II - General conditions2.3.8- Main issues - Sanctions

Financial irregularity is grounds for exclusion from evaluation or selection procedure

Violation of fundamental ethical principles is grounds for exclusion from evaluation or selection procedure

Recovery decisions (article 256 EC Treaty)

Other sanctions in contract (liquidated damages for overclaims)

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°50

Pre-existing know-how

Background + Sideground

Knowledge

Foreground

Use

Commercial exploitation + Utilization in further research activities

Dissemination

Access rights

Licenses + User rights

Key words (definitions)

2- Annex II - General conditions2.3.9.1- Main issues - IPR

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°51

Pre-existing know-how

Always remains the property of the participant concerned

Knowledge

Principle: property of the participant who generates it Exceptions:

Joint property of several participant: where generated by several participants + impossibility to determine the exact contribution of the participants concerned Always the property of the SMEs for knowledge generated within specific actions for SMEs (Co-operative & Collective RTD projects) 100% EC-funded actions (direct actions, public procurements)

Ownership

2- Annex II - General conditions2.3.9.2- Main issues - IPR

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°52

Transfer of ownership of knowledge

The participant concerned shall inform the Commission and the other participants The participant concerned shall conclude agreement(s) to pass on its obligations (e.g. access rights) The Commission and other participants may object in exceptional cases:

case of transfer to entities established in non-Member States

or non-Associated States affecting to the rights of the other participants affecting to the “legitimate interest” of the Community

Ownership

2- Annex II - General conditions2.3.9.3- Main issues - IPR

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°53

Requirement

Principle: participant owning knowledge Exception: the Commission if the owner fails to do so

Knowledge concerned

“Knowledge that is capable of industrial and commercial application … having due regard to the legitimate interest on the participants concerned” (flexible requirement)

How?

By an adequate and effective protection In conformity with relevant provisions of the contract (and of the consortium agreement, the case being)

Protection of knowledge

2- Annex II - General conditions2.3.9.4- Main issues - IPR

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°54

Requirement

By who?

Participants owning (or having access rights to) knowledge Possibly third parties having access rights

How?

By commercial exploitation or utilization in further research activities If needed, by using pre-existing know-how as well In accordance with the interest of the participants concerned (flexible requirement) Terms to be set out by the participants in a detailed and verifiable manner

Use of knowledge

2- Annex II - General conditions2.3.9.5- Main issues - IPR

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°55

Knowledge concerned

Any data or information concerning the knowledge Requirement for dissemination

By who?

Publication: the participant owning the knowledge (in Cooperative & Collective research : all participants) Dissemination: all participants The Commission where the participant fails to do so

How?

Publications: required prior approval of the Commission and the other participants, which may object Provided that dissemination/publication does not adversely affect the protection or use of the knowledge

Dissemination/Publication of knowledge

2- Annex II - General conditions2.3.9.6- Main issues - IPR

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°56

General principles

Granted on written request

No sub-licensing (even for affiliate companies) unless explicitly agreed possible optional clause for software, allowing sub-licensing, ...

Obligatory access rights between participants are limited to what they really need …

… either for carrying out the project or for using their own knowledge ... … but broader access rights may be freely negotiated

Possible granting of access rights to third partiesThe Commission may object in exceptional cases (cf. transfer of ownership)

Access rights

2- Annex II - General conditions2.3.9.7- Main issues - IPR

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°57

New features

Obligatory access rights are limited to participants of a same project

Clear/simplified financial conditions royalty-free basis fair and non-discriminatory conditions to be agreed

Possibility to exclude a specific piece of pre-existing know-how from the obligation to grant access rights

obligatory agreement of all participants concerned to be agreed before signature of the EC contract should not concern “core” pre-existing know-how

Access rights

2- Annex II - General conditions2.3.9.8- Main issues - IPR

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°58

Access rights topre-existing know-how

Access rights toknowledge resulting from

the project

Yes, if a participant needs them for carrying out his ownwork under the projectFor carrying

out theproject

Royalty-freeunless otherwise agreed

before signing the contractRoyalty-free

Yes, if a participant needs them for using his ownknowledge

For usepurposes

(exploitation+ furtherresearch)

On non-discriminatoryconditions to be agreed

Royalty-freeunless otherwise agreed

before signing the contract

2- Annex II - General conditions2.3.9.9- Main issues - IPR

Access rights

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°59

3- Annex III - Specific provisions

Specific provisions for some instruments Integrated project (IP) Network of excellence (NoE) Integrated infrastructures initiatives (I3) Specific research projects for SMEs (CRAFT/Collective)

Adding complementary provisions to core-contract, Annex I and Annex II

or

Modifying provisions of the core-contract, Annex I and Annex II

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°60

4- Annex IV - Form A4.1- General overview

To be completed by each contractor identified in the core-contract (article 1.2) in order to accede to the contract.

To be signed by each contractor and by the coordinator (One Form A per contractor, except for the coordinator) in three originals:

one for the contractor concerned one for the coordinator one for the Commission

One original to be sent by the coordinator to the Commission at the latest [30][45][60] calendar days after the entry into force of the contract.

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°61

5- Annex V - Form BGeneral overview

To be completed by each new participant willing to become contractor. To be signed by each new participant and by the coordinator (One Form B per new contractor) in three originals:

one for the contractor concerned one for the coordinator one for the Commission

One original to be sent by the coordinator to the Commission at the latest [30][45][60] calendar days after the entry into force of the adhesion to the contract of the new participant. Enclosures:

Contract preparation form duly completed and signed by the new contractor Modified Annex I (technical annex) to the contract describing the work to be performed by the new contractor Competitive call: documents mentioned in Article III.2 (IP) or III.3 (NoE)No competitive call: justification for selection and, where necessary, justification for not having used a competitive call

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°62

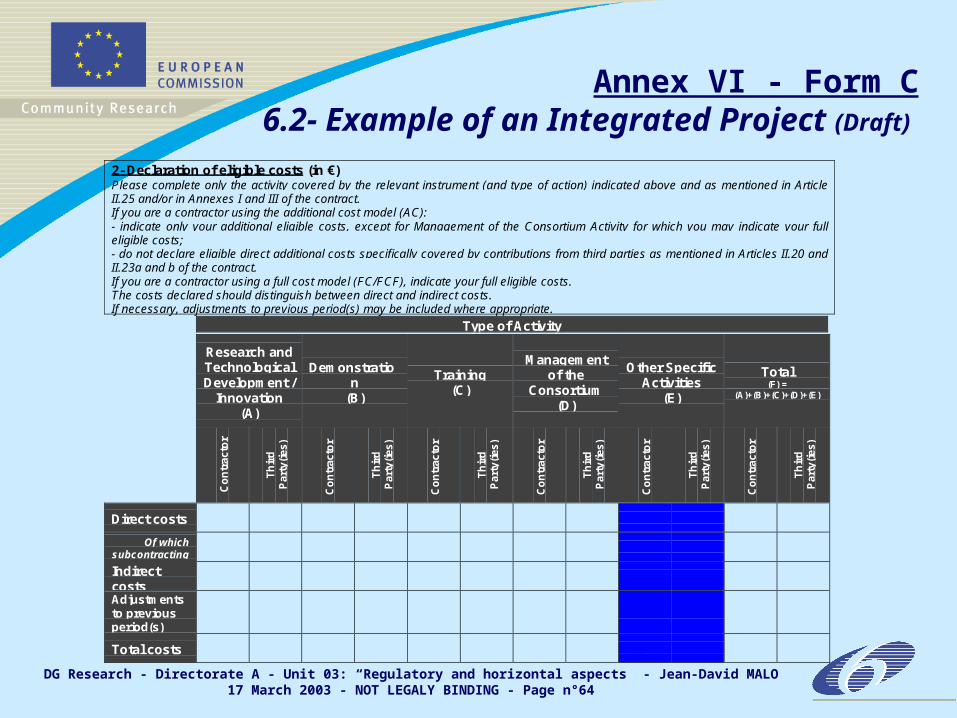

6- Annex VI - Form C6.1- General overview

To be completed by each participant for each period specified in the contract. The structure of a Form C is always the same (content different according to the instrument and type of action concerned)

Resources (third party(ies)) Declaration of eligible costs Declaration of receipts Declaration of interest generated by the pre-financing (coordinator only) Request of FP6 financial contribution Audit certificates Conversion rates Contractor’s certificate

To be signed by the person responsible for the work and the duly authorised financial officer of the contractorTo be sent to the Commission by the coordinator in the delays mentioned in the contract Reminder: a Financial statement per activity (Form C) is not an Audit certificate

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°63

Annex VI - Form C6.2- Example of an Integrated

Project (Draft) Form C - Model of Financial Statement per Activity for an Integrated Project

(to be completed by each contractor)

Type of instrument Integrated Project Type of Action (if necessary) N.A.Project Title (or Acronym) Contract n°

Contractor’s Legal NameLegal TypeContact Person TelephoneTelecopy E-mail

Cost model used(AC//FC or FCF)

Indirect costs (Real or FlatRate of 20% of Direct costs,except subcontracting)

Period from To

1- Resources (Third party(ies))Are there any resources made available on the basis of a prior agreement with third parties identified in Annex I of thecontract? (Yes / No)If Yes, please provide the following informationThird Party 1 (Y1) Legal Name Cost model usedThird Party 2 (Y2) Legal Name Cost model usedThird Party 3 (Y3) Legal Name Cost model usedThird Party 4 (Y4) Legal Name Cost model usedIf necessary add another Form C.

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°64

Annex VI - Form C6.2- Example of an Integrated

Project (Draft) 2- Declaration of eligible costs (in €)Please complete only the activity covered by the relevant instrument (and type of action) indicated above and as mentioned in ArticleII.25 and/or in Annexes I and III of the contract.If you are a contractor using the additional cost model (AC):- indicate only your additional eligible costs, except for Management of the Consortium Activity for which you may indicate your fulleligible costs;- do not declare eligible direct additional costs specifically covered by contributions from third parties as mentioned in Articles II.20 andII.23a and b of the contract.If you are a contractor using a full cost model (FC/FCF), indicate your full eligible costs.The costs declared should distinguish between direct and indirect costs.If necessary, adjustments to previous period(s) may be included where appropriate.

Type of Activity

Research andTechnologicalDevelopment /

Innovation(A)

Demonstration

(B)

Training(C)

Managementof the

Consortium(D)

Other SpecificActivities

(E)

Total(F) =

(A)+(B)+(C)+(D)+(E)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Direct costs

Of whichsubcontracting

IndirectcostsAdjustmentsto previousperiod(s)

Total costs

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°65

Annex VI - Form C6.2- Example of an Integrated

Project (Draft)

3- Declaration of receipts (in €)Please complete only the activity covered by the relevant instrument (and type of action) indicated above and as mentioned inArticle II.25 and/or in Annexes I and III of the contract.If you are a contractor using the additional cost model (AC), indicate only receipts covered by Article II.23.1.c of thecontract.If you are a contractor using a full cost model (FC/FCF), indicate receipts covered by Article II.23.1 of the contract.

Type of Activity

Research andTechnologicalDevelopment /

Innovation(A’)

Demonstration

(B’)

Training(C’)

Managementof the

Consortium(D’)

Other SpecificActivities

(E’)

Total(F’) =

(A)’+(B’)+(C’)+(D’)+(E’)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Co

ntr

acto

r

Th

ird

Par

ty(i

es)

Totalreceipts

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°66

Annex VI - Form C6.2- Example of an Integrated

Project (Draft) 4- Declaration of interest generated by the pre-financing (in €)To be completed only by the coordinator.Did the pre-financing (advance) you received by the Commission for this period earn interest? (Yes / No)If yes, please indicate the amount (in €)

5- Request of FP6 Financial contribution (in €)

For this period, the FP6 Community financial contribution requested is equal to (amount in €)

6- Audit certificates

According to the contract, does this Financial Statement need an audit certificate (or several in case of Thirdparty(ies)) delivered by independent auditor(s)? (Yes / No)If Yes, does this(those) audit certificate(s) cover only this Financial Statement per Activity? (Yes / No)If No, what are the periods covered by this(those) audit certificate(s) ? From – To

What is the total cost of this(those) audit certificate(s) (in €) per independent auditor(s) ?Audit certificate of the contractor (X)

Legal name of the audit firm Cost of the certificate

Audit certificate(s) of the third party(ies) (Ys) (if necessary)Y1 : Legal name of the audit firm Cost of the certificateY2 : Legal name of the audit firm Cost of the certificateY3 : Legal name of the audit firm Cost of the certificateY4 : Legal name of the audit firm Cost of the certificateIf necessary add another Form C. Total (Z) = (X) + (Ys)Reminders:The cost of an audit certificate is included in the costs declared under the activity “Management of the Consortium”.The required audit certificate(s) is(are) attached to this Financial Statement.

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°67

Annex VI - Form C6.2- Example of an Integrated

Project (Draft)

7- Conversion ratesCosts incurred in currencies other than EURO shall be reported in EURO.Please mention the conversion rate used (only one choice is possible) – Please note that the same principle applies forreceipts.

Contractor- Conversion rate of the date of incurred actual costs? (YES / NO)- Conversion rate of the first day of the first month following the period covered by this Financial Statement? (YES/NO)

Third Party(ies) (if necessary)

Third Party 1 (Y1)- Conversion rate of the date of incurred actual costs? (YES / NO)- Conversion rate of the first day of the first month following the period covered by this Financial Statement? (YES/NO)

Third Party 2 (Y2)- Conversion rate of the date of incurred actual costs? (YES / NO)- Conversion rate of the first day of the first month following the period covered by this Financial Statement? (YES/NO)

Third Party 3 (Y3)- Conversion rate of the date of incurred actual costs? (YES / NO)- Conversion rate of the first day of the first month following the period covered by this Financial Statement? (YES/NO)

Third Party 4 (Y4)- Conversion rate of the date of incurred actual costs? (YES / NO)- Conversion rate of the first day of the first month following the period covered by this Financial Statement? (YES/NO)If necessary add another Form C.

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°68

Annex VI - Form C6.2- Example of an Integrated

Project (Draft)

8- Contractor’s Certificate

We certify that:- the costs declared above are directly related to the resources used to reach the objectives of the project ;- the receipts declared above are directly related to the resources used to reach the objectives of the project ;- the costs declared above fall within the definition of eligible costs specified in Articles II.19, II.20, II.21, II.22 and II.25 of the contract,and, if relevant, in Annex III and Article 9 (special clauses) of the contract ;- the receipts declared above fall within the definition of receipts specified in Article II.23.1 of the contract ;- the interest generated by the pre-financing declared above falls within the definition of Article II.27 of the contract ;- the necessary adjustments, especially to costs reported in previous Financial Statement(s) per Activity, have been incorporated in theabove Statement ;- the above information declared is complete and true ;- there is full supporting documentation to justify the information hereby declared. It will be made available at the request of theCommission and in the event of an audit by the Commission and/or by the Court of Auditors and/or their authorised representatives.

Contractor’s Stamp Name of the Person responsiblefor the work

Name of the duly authorisedFinancial Officer

Date Date

Signature Signature

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°69

Annex VI - Form C6.3- 12 different Forms C

Instrument Type of action

Network of excellence N.A. 1

Integrated project N.A. 1

Research and technological development / Innovation 1

Demonstration 1

Combined 1

Integrated infrastructures initiatives N.A. 1

Cooperative research 1

Collective research 1

Classical 1

For infrastructures 1

Classical 1

For transational access to infrastructures 1

12

Specific targeted project

Specific project for SMEs

Coordination action

Specific support action

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°70

Instrument Type of actionAnnex IIGeneral

conditions

Annex IIISpecific

provisions

Annex IVForm A

Annex VForm B

Annex VIForm C

Network of excellence N.A. Yes Yes

Integrated project N.A. Yes Yes

Research and technological development / Innovation No Yes

Demonstration No Yes

Combined No Yes

Integrated infrastructures initiatives N.A. Yes Yes

Cooperative research Yes Yes

Collective research Yes Yes

Classical No Yes

For infrastructures No(special clause)

Yes

Classical No Yes

For transational access to infrastructures No(special clause)

Yes

Yes

Standard text

Yes

Standard text

Yes

Standard text

Specific targeted project

Specific project for SMEs

Coordination action

Specific support action

7- Conclusion7.1- Overview of the Annexes(*) of the core -contract per instrument and type of action

concerned (Draft)

(*) Except Annex I (technical annex - description of the work)

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°71

7-Conclusion7.2- For more information

Information on FP6 model contract are already available on EUROPA web site

http://europa.eu.int/comm/research/fp6/working-groups/model-contract/index_en.html

EC contact points for any question relating to FP6 model contractDG RTD-A3 - “Regulatory and horizontal aspects”Head of Unit: Mrs. Megan Margaret RICHARDSUnit A3 Members:Milagros BAS SANCHEZ - Francisca BRUNET COMPANY(*) - Ernesto CAMPOGRANDEJean-David MALO - Sean O’SULLIVAN(*) - Nicolas SABATIER

For IPR purposes, in addition to the above (*) mentioned people :Denis DAMBOIS - Magali POINOT

and also Legal and Financial Units of other Research DG

DG Research - Directorate A - Unit 03: “Regulatory and horizontal aspects” - Jean-David MALO17 March 2003 - NOT LEGALY BINDING - Page n°72

THANK YOU FOR YOUR ATTENTIONTHANK YOU FOR YOUR ATTENTION

QUESTIONS AND ANSWERSQUESTIONS AND ANSWERS

![Paul et Malo [Social Media Tools]](https://static.fdocuments.in/doc/165x107/568ca6041a28ab186d8f77e4/paul-et-malo-social-media-tools.jpg)