The Role of teacher training in technical and vocational education ...

1

AGBOH, CALLISTUS IK

PG/Ph.D/06/42140

UTILIZATION OF CAPITAL BUDGETING AS AN OPTIMAL TOOL FOR INVESTMENT ANALYSIS IN MANUFACTURING COMPANIES IN ENUGU AND ANAMBRA STATES

FACULTY OF EDUCATION

DEPARTMENT OF VOCATIONAL TEACHER EDUCATION (BUSINESS EDUCATION),

Paul Okeke

Digitally Signed by: Content manager’s Name DN : CN = Webmaster’s name O= University of Nigeria, Nsukka OU = Innovation Centre

2

UTILIZATION OF CAPITAL BUDGETING AS AN OPTIMAL TOOL FOR INVESTMENT ANALYSIS IN MANUFACTURING COMPANIES IN E NUGU

AND ANAMBRA STATES

BY

AGBOH, CALLISTUS IK PG/Ph.D/06/42140

A THESIS SUBMITTED TO THE FACULTY OF EDUCATION, UNIVERSITY OF NIGERIA, NSUKKA

IN PARTIAL FULFILLMENT FOR THE AWARD OF THE DEGREE OF DOCTOR OF PHILOSOPHY (Ph.D) IN BUSINESS EDUCATION

SUPERVISOR: PROF. E.C. OSUALA

MARCH, 2011

APPROVAL PAGE

3

This Thesis has been approved for the Department of Vocational Teacher

Education (Business Education), University of Nigeria, Nsukka.

By

_____________________ __________________ Prof. E.C. Osuala Internal Examiner Thesis Supervisor

_____________________ __________________ External Examiner Prof. C. A. Obi Thesis Supervisor Head of Department

___________________ Prof. I. Ifelunni

Dean, Faculty of Education

4

CERTIFICATION

Agboh, Callistus Ik., a Postgraduate student in the Department of Vocational

Teacher Education, with Registration Number PG/Ph.D/06/42140, has satisfactorily

completed the requirements for the award of the Degree of Doctor of Philosophy

(Ph.D) in Business Education.

The work embodied in this thesis is original and has not been submitted in part

or full for any other diploma or degree of this or any other University.

_______________________ _______________________ Agboh, Callistus Ik Prof. E. C. Osuala Student Supervisor

5

DEDICATION

This research work is dedicated to my late mother, Mrs. Virginia A. Agboh,

for offering her life for my education.

6

ACKNOWLEDGMENT

I am particularly grateful to my thesis supervisor, Professor E. C. Osuala,

whom under his guidance this study was inspired, organized and completed. His

kindness, care, understanding, constructive criticisms and advice throughout the

various stages of this work were indispensable. I am highly elated by his fatherly role.

My heartfelt appreciation also goes to Prof. (Mrs) C. A. Obi, Prof. (Mrs) Igbo,

Prof. N. O. Ogbonnaya, Prof. (Mrs) U. N. V. Agwagah, Dr E. A. C. Etonyeaku, and

Dr (Mrs) T. C. Ogbuanya for their invaluable corrections, guidance and stimulating

academic offers which led to the successful completion of this work. The

contributions and assistance of Prof. E. E. Agomuo, Prof. A. U. Nweze, Dr R. O.

Ugwoke, Dr. (Mrs) Regina Okafor and Mr J. K. Edeh were immeasurable especially

in reading through my work and in validating the instrument for this work. Their

comments, advice and suggestions gave this work a facelift.

I am highly indebted to the management and staff of the manufacturing

companies in Enugu and Anambra States, especially those that responded to my

instrument. I am particularly grateful to Engr. C. G. Nzewi, Chairman, Anambra,

Enugu and Ebonyi States branch of Manufacturing Association of Nigeria for availing

me the necessary information for this study.

The kindness and assistance meted to me by Prof. Ben Mba, Provost, Federal

College of Education, Eha-Amufu, and my colleagues in the Department of Business

Education is also highly appreciated. I also wish to appreciate my wife, Chidimma,

my siblings, Chijioke, Fr. Denis, Ibe, Sunday and Kenechukwu; and my children,

Ebubechukwu, Nnadozie, Adaeze and Chijiekwu for their prayers and understanding

during the writing of this work. Finally, I thank Mrs Angela Eze, for typesetting this

work.

Agboh, Callistus IK Department of Vocational Teacher Education

University of Nigeria, Nsukka

7

TABLE OF CONTENTS

Page

TITLE PAGE … … i

APPROVAL PAGE … … ii

CERTIFICATION … … iii

DEDICATION … … iv

ACKNOWLEDGMENT … … v

TABLE OF CONTENTS … … vi

LIST OF TABLES … … ix

LIST OF FIGURES … … xi

ABSTRACT … … xii

CHAPTER ONE: INTRODUCTION … 1

Background of the Study … … 1

Statement of the Problem … … 8

Purpose of the Study … … 9

Research Questions … … 10

Hypotheses … … 11

Significance of the Study … … 12

Delimitation of the Study … … 14

CHAPTER TWO: REVIEW OF RELATED LITERATURE 15

Conceptual Framework … … 16

• Company … … 16

• Manufacturing … … 17

• Manufacturing Company … 18

• Capital … … 21

• Investment … … 22

• Budget … … 23

• Investment Analysis … … 26

• Capital Budgeting … … 27

8

• Utilization of Capital Budgeting for Investment Analysis 32

• The Need for Capital Budgeting Decision Processes in corporate planning … … 35

• Management Compliance in the use of Capital Budgeting Techniques 47

• Utilization of Capital Budgeting by Manufacturing Companies for Investment Analysis … … 72

• Outsourcing of Capital Expenditure Decisions and the Prospect of Manufacturing Companies … 77

• The Effect of Utilization of Capital Budgeting on companies earnings 81

• Constraints to Effective use of Capital Budgeting for Investment Analysis … … 99

• Strategies for Improving on the use of Effective Capital Budgeting 102

Theoretical Framework … … 111

• Quantity Theory of Money … 111

• Liquidity Premium Theory … 111

• Arbitrage Theory of Capital Assets Pricing … 112

• Utility Theory … … 113

• Portfolio Investment Theory … 115

• Dominant Theory of Budgeting … 116

Related Empirical Studies … … 119

Summary of Related Literature … … 125

CHAPTER THREE: METHODOLOGY … 128

Design of the Study … … 128

Area of the Study … … 128

Population for the Study … … 129

Sampling Technique … … 129

Instrument for Data Collection … … 130

Validation of the Instrument … … 132

Reliability of the Instrument … … 132

Method of Data Collection … … 133

Data Analysis Technique … … 134

9

CHAPTER FOUR: DATA PRESENTATION AND ANALYSIS 136

Major Findings of the Study … … 153

Discussion of Major Findings … … 157

CHAPTER FIVE: SUMMARY, CONCLUSIONS AND RECOMMENDATIONS … 168

Restatement of the Problem … … 168

Summary of the Procedures Used … … 169

Summary of Findings … … 170

Conclusions … … 172

Implications for Accounting Education … 174

Recommendations … … 175

Suggestion for Further Research … … 176 REFERENCES … … 177

APPENDIX A: LETTER OF INTRODUCTION … 187

APPENDIX B: EVIDIENCE OF INSTRUMENT VALIDATION 188

APPENDIX C: QUESTIONNAIRE … 189

APPENDIX D: LIST OF URBAN AND RURAL; SMALL, MEDIUM AND LARGE SCALE MANUFACTURING COMPANIES IN ENUGU AND ANAMBRA STATES 196

APPENDIX E: POPULATION AND SAMPLE DISTRIBUTION 205

APPENDIX F: RESULT FOR RESEARCH QUESTIONS 206

APPENDIX G: RESPONSE FREQUENCIES AND PERCENTAGES 210

APPENDIX H: RESULTS OF HYPOTHESES TESTING 210

APPENDIX I: CRONBACH ALPHA RELIABILITY RESULTS FOR RESEARCH QUESTIONS 1 – 7 241

10

LIST OF TABLES

Table Page

1. Mean Ratings and Standard Deviations of Respondents on the Extent the Use of Capital Budgeting Decision

Processes Aid Corporate Planning for Long Term Survival of Manufacturing Companies … … … 137

2. A t-test of the Differences between the Means of Urban and Rural Manufacturing Companies on the Extent Capital Budgeting Processes aid Corporate Planning for Long Term Survival of Manufacturing Companies … … 138

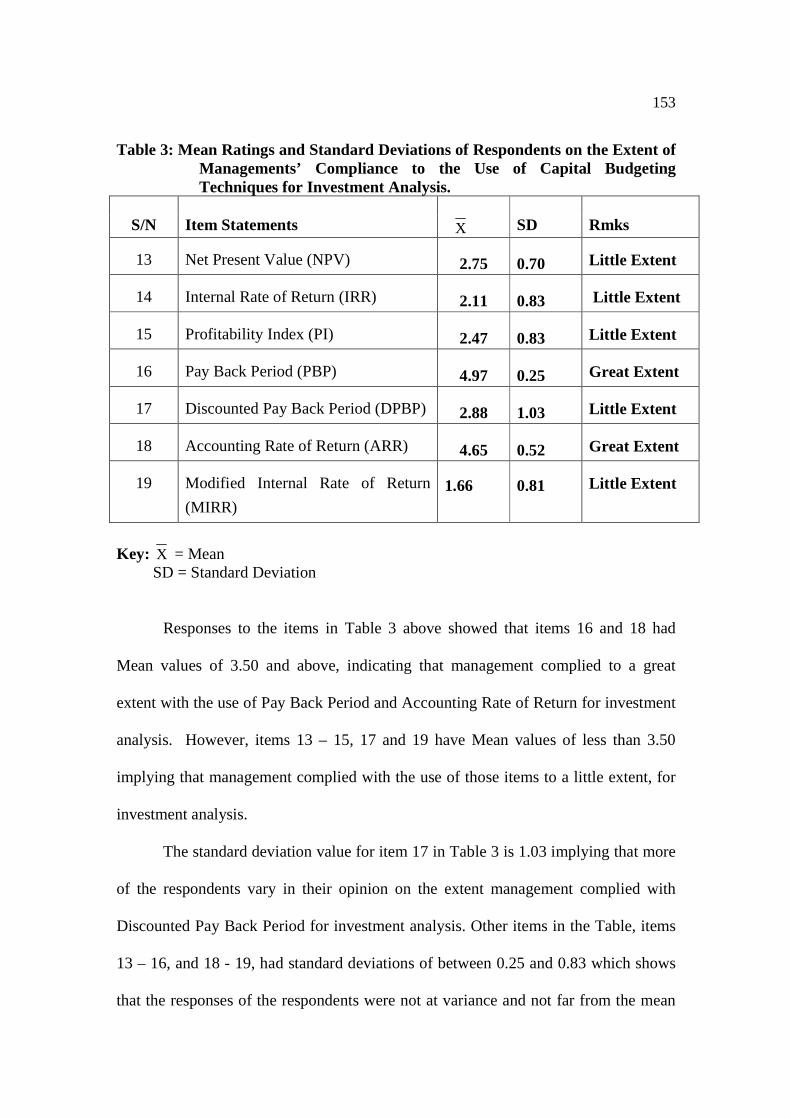

3. Mean Ratings and Standard Deviations of Respondents on the

Extent of Management Compliance to the Use of Capital Budgeting Techniques for Investment Analysis … 140

4. Analysis of Variance (ANOVA) of the Means of Managing Directors, Accountants and Purchasing Managers on Management’s Compliance with the use of Capital Budgeting Techniques for Investment Analysis … … 141

5. Mean Ratings and Standard Deviations of Respondents on the

Extent Manufacturing Companies Utilize Capital Budgeting Investment Evaluation Criteria for Investment Decisions … … … 142

6. Mean Ratings and Standard Deviations of Respondents on the

Extent Manufacturing Companies Utilize Outsourcing for Capital Expenditure Decisions … … 144

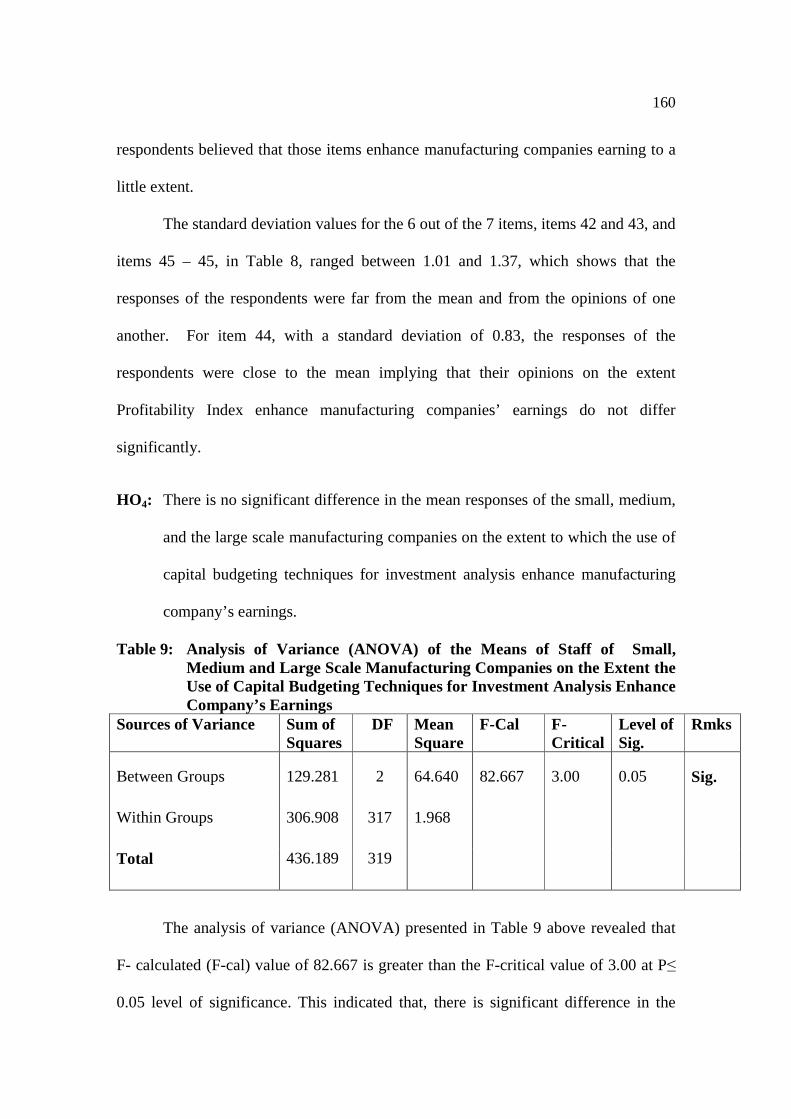

7. Analysis of Variance (ANOVA) of the Means of the Staff of Small, Medium and Large Scale Manufacturers on the Extent Outsourcing is Utilized for Capital Expenditure Decisions 145

8. Mean Ratings and Standard Deviations of Respondents on the

Extent the Use of Capital Budgeting Techniques for Investment Analysis Enhance the Earnings of Manufacturing Companies … … … 146

9. Analysis of Variance (ANOVA) of the Means of Staff of Small, Medium and Large Scale Manufacturing Companies on the Extent the Use of Capital Budgeting Techniques for

11

Investment Analysis Enhance Company’s Earnings … 147

10. Mean Ratings and Standard Deviations of Respondents on the

Constraints to Effective Use of Capital Budgeting for Investment Analysis … … … 149

11. A t-test of the Differences between the Means of Urban and Rural Manufacturing Companies on the Factors that Constrain Effective Use of Capital Budgeting for Investment Analysis … 150

12. Mean Ratings and Standard Deviations of Respondents on

Strategies for Improving on Effective Use of Capital Budgeting for Investment Analysis … … … 152

12

LIST OF FIGURES

Figure Page

1. A Decision Making Process for Capital Investment Decision 43 2. Graphical Representation of Internal Rate of Return (IRR) Estimate 61

3. Organisation of Finance Functions in a Typical Nigerian Manufacturing Company … … … … 73

4. Schematic Representation of Conceptual Framework 109

13

ABSTRACT

The major purpose of the study was to determine the extent to which capital budgeting is being utilized as a tool for optimum investment analysis in manufacturing companies in Enugu and Anambra States. The study adopted a survey research design. Seven specific purposes were developed in line with the major purpose of the study. The study answered seven research questions and tested five hypotheses at 0.05 level of significance. The population for the study consisted of 552 management staff of the 138 registered manufacturing companies operating in Enugu and Anambra Sates. Stratified random sampling technique was used to select a total of 336 management staff of 84 manufacturing companies which therefore constituted the sample. The questionnaire was structured on a 5-point rating scale and was validated by five experts; two from the Department of Vocational Teacher Education, University of Nigeria, Nsukka; two from Accountancy Department of University of Nigeria, Enugu Campus and one professional Accountant from Bursary Department of the University of Nigeria, Nsukka. Their suggestions were incorporated to improve the final draft of the instrument used for the study. Cronbach Alpha reliability coefficient of 0.95 was obtained for the entire items in the instrument. While the 7 clusters had Cronbach Alpha coefficients of 0.959, 0.953, 0.967, 0.932, 0.972, 0.940 and 0.984 respectively. A total of 320 of the 336 copies of the questionnaire administered were retrieved representing about 95% retrieval. The data collected were analyzed using frequency, percentage and mean for answering the seven research questions while t-test statistic and analysis of variance (ANOVA) were used in testing the five null hypotheses at 0.05 level of significance and 318 degree of freedom (df) for the t-test statistic. The major findings of the study were: 1) capital budgeting decision processes were used to a little extent to aid corporate planning; 2) management complied to a little extent with the use of capital budgeting techniques for investment analysis; 3) balancing strategic management consideration with capital budgeting evaluative techniques will improve on effective use of capital budgeting for investment analysis. It was concluded that manufacturing companies utilized non discounted investment evaluation techniques to a great extent for investment decisions. Based on the findings and conclusion, it was recommended that management should ensure the use of discounted capital budgeting techniques for investment analysis, and allow financial managers free hand in project evaluation and selection.

14

CHAPTER ONE

INTRODUCTION

Background of the Study

A company is a form of business organization, a corporate body or a

corporation, generally registered under the company’s Act or similar legislations. It is

a legal entity, created under an enabling law of the government, having unlimited life

span and limited liability. Igben (2007) defines a company as a body corporate,

having a distinct legal personality created by or under an enabling statute of the

government. A company is a form of business organization, whose characteristics

include; limited liability, corporate body, right to sue or be sued, enter into contracts,

owe debts, pay debts, pay taxes, pay dividend from earnings, and neither the death nor

the bankruptcy of any of its members can force it to liquidate (Chartered Institute of

Management Accountants (CIMA), 2004).

Manufacturing companies are companies that convert raw materials and

component parts into consumer, and or industrial goods (Garner, 2001).

Manufacturing companies are companies that engage in production (i.e. business

organizations which creates utility). The manufacturing sub-sector can be classified

based on two major sub-division; either in accordance with area of coverage, or in

relation to its capital base. Based on area of coverage, four distinct groups are

identified, namely: the multi-nationals, the nationals, the regional and the local

manufacturing companies. Based on size of capital, four companies can be identified,

namely: the micro cottage, the small scale, the medium scale, and the large scale

manufacturing companies. However, manufacturing companies as is used in this

15

work refers essentially to companies that engage in productive activities and whose

liability is limited, irrespective of size or area of coverage.

Micro-Cottage companies are those which have a total capital employed of not

more than N1.5 million excluding cost of land and, or a workforce of not more than

10 persons. Small Scale companies have over N1.5 million but not more than N50

million excluding cost of land and, or 11 – 100 workers. The medium scale has over

N50 million but not more than N200 million, excluding cost of land and, or 101 – 300

workers. Any company that has a capital of more than N200 million, excluding cost

of land and, or more than 300 workers in its employ is classified large scale (National

Council on Industry (NCI) 2004, in Eneh, 2005).

According to Eneh (2005) the large sums of capital involved in siting

companies in the Urban areas had often made the growing manufacturing companies

to be located in the suburb and rural areas. Urban areas Eneh referred to as places

with many huge concrete buildings, shops, places of work, entertainment, worship

centers, and with large concentration of people industries and social amenities. While

rural areas are countryside which lack in some of these amenities and are under-

developed. Other reasons for siting manufacturing companies in the rural areas which

may affect capital budget include: government tax benefits, cheaper land, cheaper

manpower, and nearness to raw material deposits.

The manufacturing sector has grown much in size that its level of intensity has

become an acceptable index for measuring the economic prosperity of any nation

(Okafor, 1983). High level of productive activities gives rise to abundance of

consumer goods and services, thus facilitating improvement in the productive

efficiency of the factor inputs. The factor inputs comprises of the primary factors

16

(land, labour and other natural resources); and secondary or produced factor inputs of

money, machine and other man-made resources. These produced factor inputs

according to Sadler (2003), are otherwise referred to as capital.

Capital consists of assets, monetary and non monetary, contributed by owners

of a corporate organization to keep a business afloat. Association of Certified

Chartered Accountants (ACCA) (1998) defined capital as the monetary and non

monetary assets contributed by the owners of an enterprise (equity capital) and by the

creditors (loan capital) to get the organization going. It refers to the right of a

company to utilize the services of produced factor inputs. This right can be exercised

either in the ownership and control of real assets or in that of the financial assets.

Real assets are tangible assets, while financial assets are claims on income to be

generated by real assets. The total value of real and financial assets available to an

economic unit at any point in time constitutes its stock of capital (Gordon, 2004).

Capital is a discrete variable. It is not measured over a given period, rather at a given

or discrete time. As such, the design to increase, improve or maintain capital (i.e.

investment) has to be planned and returns predetermined. The predetermination of

investment returns before venturing into it keeps manufacturing companies on track,

in the choice of investment.

Investment refers to assets acquisition by company for the purposes of capital

appreciation and income generation (Nweze, 2004). It encompasses all economic

activities designed to increase, improve or maintain the productive quality of existing

stock of capital. When the stock of available capital falls below the quantity required

to achieve the desired levels of output, the need for additional investment arises

(Williams, 2008). Consequently, the desired stock of capital depends basically on

17

two factors; viz: (i) the volume of output, and (ii) the amount of capital stock required

per unit of the output. It is the determination of this desired stock level of capital

coupled with its relative rates of return (cashflow) that makes budget an inevitable

tool for corporate existence.

A budget is a formal statement of a company’s future plans which is usually

expressed in monetary terms. It is an investment analytical tool which aids financial

managers to make an informed managerial decision. The Chartered Institute of

Management Accountants (CIMA), 2004) defined budget as a plan quantified in

monetary terms, prepared and approved prior to a defined period of time, usually

showing a planned income to be generated, and or expenditure to be incurred during

that period, and the capital to be employed to attain a given objective. In essence, the

budget of a company cannot be prepared in isolation of the firm’s financial status –

stock of capital.

Capital budgeting is the process of planning expenditure on assets whose

returns are expected to extend beyond one year. Institute of Chartered Accountants of

Nigeria (ICAN) (2006) described capital budgeting as a firm’s decision to invest its

current funds most efficiently in long term assets in anticipation of an expected flow

of benefits over a series of years. The ability to take capital budgeting decisions

satisfactorily is dependent on the evaluation for proper use of capital budgeting

techniques employed for investment analysis. The reason is that, every investment

environment is usually surrounded by investment risks. Such risks include the ‘alpha’

or non market imposed risks, and ‘beta’ or the market imposed risks.

In other words, the effectiveness of capital budgeting as an investment tool for

optimal investment decision is dependent on the management’s ability to functionally

18

utilize the capital budgeting evaluation criteria to obviate or minimize investment

risks. Capital budgeting evaluation criteria is a combination of capital budgeting

techniques and the risk adjusted techniques. The capital budgeting techniques include

the discounted and the non discounted investment evaluation criteria, while the risk

adjusted techniques are management strategies adopted by companies to avert or

minimize investment risks. They include, the risk adjusted statistical techniques; the

conventional techniques of risk analysis; the scenario analysis; and the sensitivity

analysis.

In most companies, the finance unit constitutes a department, headed by the

finance director. In the capital budgeting section, the management staff that usually

constitute members are; the managing director, the finance manager, the internal

auditor and the purchasing manager. The managing director is often the president of

the firm and is responsible for all top level decisions including the introduction of

change into the organization. The finance manager who is usually the head of the

budgeting unit is responsible for obtaining and managing the company’s fund. The

internal auditor monitors, evaluates and reports to management on the internal control

system of the company. While the purchasing manager takes charge of stock control

and management, both of goods and property (Surridge and Gillespie, 2008).

However, most small and medium scale companies, due to capital constraints

and cost implications of establishing a budget unit, utilize the services of an external

provider. In essence, manufacturing companies that were not viable enough to

establish a budget unit would require to outsource its capital budgeting decisions in

order to achieve efficiency. Outsourcing refers to the utilization of external resources,

the commission of the execution of tasks, function and processes as cannot be

19

efficiently handled in-house to an external provider specializing in a given area

(Koszewska, 2004).

Effective capital budgeting presupposes adequate timing of assets acquisition

and rate of returns forecast. A manufacturing company which foresees the need to

procure capital assets in time has the opportunity to install the assets before its sales

are at capacity (Elijelly, 2004). Wrong forecast of capital assets’ requirement

plunders companies into adverse business consequences that may be very difficult to

reverse. It can result in loss of company’s market share to rivals, capacity

underutilization, poor earnings and losses.

To achieve effective capital budgeting, management has to be guided by the

company’s corporate plan. Corporate planning entails establishing goals and suitable

courses of action for achieving such goals. Management in order to achieve effective

capital budgeting shall comply with the procedure established for such goal

attainment. Nwude (2001) elaborated on the typical procedure en-route effective

capital budgeting to include, establishing selection criteria; investigating proposals to

determine their value and feasibility; comparing alternative projects; determining the

financial needs, costs and resources; deciding on the projects to be implemented;

allocating funds to their development; and controlling and reviewing results. This

procedure otherwise referred to as capital budgeting decision process, is, according to

Pandy (2006), termed capital investment analysis.

Investment Analysis entails adequate knowledge of cost of sales, estimate of

yield, and formulation of optimal mix of securities to obtain higher yielding

portfolios. It involves the evaluation of an investment through the establishment of

cash flow, estimation of the required rate of return (the opportunity cost of capital)

20

and the application of a decision rule for making the choice (Leloup, 1998). The

implication is that, the most accurate investment analysis and subsequent decision can

only be achieved in a predictable investment environment.

Nigerian investment environment is full of uncertainties that are often

responsible for investment failure. These uncertainties Eneh (2005) elaborated,

include: the uncertainty in the occurrence of future expectations caused by political

factors; the uncertainty of economic climate caused by interest rate fluctuations,

inflationary pressure, monetary and fiscal policy inconsistencies; uncertain social and

cultural factors caused by the mood and belief inconsistencies of the citizenry; and the

ever growing technological factors which affect the utilitarian purposes of capital

asset’s procurement. These uncertainties pose threat and are danger signals to the

Nigerian manufacturers; hence they are potentials for their incessant failure.

Examples of moribund manufacturing companies in Enugu and Anambra states

include, Niger-Delta Floor Mill, Umunya; Anambra Machine Tools and Foundry,

Onitisha; Premier Breweries, Onitsha; Science Equipment Manufacturing Company,

Akwuke; Brick Manufacturing Company, Akegbe Ugwu; Anambra Vegetable Oil,

Nachi; Aluminum Product (ALPUM), Ohebe-Dim; to mention but a few.

In the South Eastern states, the Bureau for Public Enterprises noted that, most

manufacturing companies disappeared in the last two decades due to unpredictable

government policies, lack of basic raw materials (most of which are imported), high

interest rates, non implementation of protective existing policies, lack of effective

regulatory agencies, infrastructural inadequacies, unfair tariff and low patronage

(BPE, 2004). Despite these risk factors noted above, and uncertain investment

environment, Nzelibe (2000) contends that the prospects of Nigeria manufacturers are

21

bright. According to him, giving the nation’s nascent democracy, a market size of

140 million people, rich mineral and other resources, size of the West African market,

as well as cheap and abundant labour; the prospects of manufacturing in Nigeria are

bright.

Statement of the Problem

The manufacturing sub-sector in every economy serves as an engine for

economic development, yet the manufacturing sub-sector in Nigeria, and Enugu and

Anambra States in particular, has continued to decline in growth. This slow pace in

growth can be traced to the ‘risk averse’ economic environment which has

discouraged diversification and expansion of local industries. The situation is further

complicated by the political, economic and socio-cultural inconsistencies (Eneh,

2000).

A recent survey conducted by Eneh (2005) showed that 97.6% of Nigeria’s

industrial and manufacturing sub-sectors are made up of Micro Cottage, Small and

Medium Scale Enterprises (MSMSE’s), and that three out of four of these firms fail

every year; while nine out of the ten prospective entrepreneurs did not venture into

the business. Similarly, Nzewi (2007) classified the state of the Nigerian

Manufacturing Companies as follows: 30% closed down; 60% ailing and 10%

operating at sustainable level. Nzewi furthered maintained that one of the major

constraints identified is the business environment – the enabling conditions in terms

of government policies, institutions, physical infrastructure, human resources and

administrative services, are lacking. Nigeria’s manufacturing sub-sector witnessed a

12% growth in 1976, and its contribution to Gross Domestic Product rose from 4% in

22

1973 to 13% in 1983; but turned a negative value of – 0.9% in 1999, from – 2.6% in

1994 (CBN Statistical Bulletin, 2001).

These rates of failures though may be partly blamed on the socio-political and

economic inconsistencies of Nigeria investment environment, the adequacy, extent of

use, and the efficiency of capital budgeting need to be ascertained. This is necessary

because of the materiality of capital budgeting decisions, which its efficient

application or otherwise, could determine the future prospect of the company. The

problems of predicting events with certainty in an uncertain economic environment;

the complex nature of capital budgeting application and method of computation; the

sophistication of the capital budgeting evaluation techniques and risk measurement

devices; and inadequate infrastructure and manpower, affect manufacturing

companies’ effective operations. These problems also militate against efficient

utilization of capital budgeting for investment analysis in most manufacturing

companies. The mass failure of industries in the manufacturing sub-sector which is

presumed to have resulted from the improper use of capital budgeting for optimal

investment analysis by manufacturers in Enugu and Anambra States necessitated this

study.

Purpose of the Study

The major purpose of this study was to determine the extent to which capital

budgeting is being utilized as a tool for optimal investment analysis in manufacturing

companies in Enugu and Anambra states. Specifically, the study sought to:

1. ascertain the extent to which capital budgeting processes aided corporate

planning for long term survival of manufacturing companies,

23

2. determine the extent of management’s compliance to the use of capital

budgeting techniques for investment decisions,

3. determine the extent to which manufacturing companies utilize capital

budgeting investment evaluation criteria for investment decisions,

4. ascertain the extent to which outsourcing is utilized by manufacturing

companies in taking capital expenditure decisions,

5. determine the extent the use of capital budgeting techniques for investment

analysis enhance the earnings of manufacturing companies,

6. find out the constraints to effective use of capital budgeting for investment

analysis’ and

7. determine the strategies for improving on the effective use of capital budgeting

for investment analysis in manufacturing companies.

Research Questions

The following research questions guided the study:

1. To what extent does the use of capital budgeting decision processes aid

corporate planning for long term survival of manufacturing companies?

2. What is the extent of management compliance to the use of capital budgeting

techniques for investment analysis?

3. To what extent does manufacturing companies utilize capital budgeting

investment evaluation criteria for investment decisions?

4. To what extent does manufacturing companies utilize outsourcing for capital

expenditure decisions?

24

5. To what extent does the use of capital budgeting techniques for investment

analysis enhance the earnings of manufacturing companies?

6. What are the constraints to the effective use of capital budgeting for

investment analysis?

7. What are the strategies for improving on effective use of capital budgeting for

investment analysis?

Hypotheses

The study tested the following five null hypotheses at 0.05 level of

significance.

HO1: There is no significant difference between the mean responses of the

management staff from urban manufacturing companies and those from rural

manufacturing companies on the extent to which capital budgeting is utilized

for investment decisions in Enugu and Anambra states of Nigeria.

HO2: There is no significant difference among the mean responses of the managing

directors, the accountants, and the purchasing managers on management’s

compliance in the use of capital budgeting techniques in manufacturing

companies.

HO3: There is no significant difference among the mean responses of the small,

medium, and the large scale manufacturing companies on the extent to which

outsourcing is utilized by manufacturing companies in taking capital

expenditure decisions.

HO4: There is no significant difference among the mean responses of the small,

medium, and the large scale manufacturing companies on the extent to which

25

the use of capital budgeting techniques for investment analysis enhance

manufacturing company’s earnings.

HO5: There is no significant difference between the mean responses of the

management staff from urban manufacturing companies and those from rural

manufacturing companies on the factors that constrain effective use of capital

budgeting for investment analysis.

Significance of the Study

The findings of this study would be of immense benefit to many people and

institutions in Enugu and Anambra states. Manufacturers would be made to

understand that investment decisions are long-term decisions where consumptions

and investment alternatives are balanced over time, in the hope that new investment

would generate extra returns in the future. They would also understand that capital

budgeting aid organizational efficiency and survival, irrespective of the risk factors

inherent in the business environment. Equally, they would appreciate that effective

use of capital budgeting strengthens corporate plan through timely and optimum

employment of capital for maximum returns. Management would be made to

understand that corporate planning enhance the predictive possibility of embarking on

a specific course of action with relative certainty of the outcome.

The findings of this study would assist the manufacturers, managers and

investors alike, in taking realistic investment decisions. Analysis of the investment

evaluation criteria, especially with regards to environmental risks, would enable

investors and managers minimize the errors of investing wrongly on capital assets.

The findings would sensitize manufacturers that wrong procurement of capital assets

26

might lead to capital underutilization which could plunder a firm into adverse

business consequences. Specifically, both the management, and the financial

managers would be made to understand that investment decisions are more realistic

when taken based on strategic management information and capital budgeting

evaluation techniques.

The findings of this study would assist management and investors with

information on how to avert the dangers of adverse environmental variables through

the prediction of the present value of future investment and its relative rate of returns

overtime. Risks may not be fully adjusted using only capital budgeting techniques.

The findings of this study would enable manufacturers understand that, though the

difficulty in using risk adjusted techniques to compliment capital budgeting

techniques when evaluating investment decisions, expenditure decisions so reached

are usually stable and realistic.

The findings would assist management in choosing and allocating resources

to capital assets that would boost the profit base of the company. Efficient use of

outsourcing in execution of tasks and functions which cannot be effectively handled

in-house would reduce cost and boost manufacturing company’s earning. The study

would highlight the strengths and weaknesses of outsourcing to facilitate

manufacturing companies’ choice of when, how, what, and who to outsource.

The findings of this study would significantly be beneficial to researchers,

teachers and students of Accountancy and Accounting education in tertiary

institutions in Nigeria. It would aid researchers generate base information for their

research work, as well as aid further investigation on ways of improving on capital

budgeting to obviate the mass winding-up of manufacturing companies in Nigeria.

27

The knowledge of the extent capital budgeting is utilized by manufacturing

companies for investment analysis would assist accounting educators improve on

their course content, curriculum and method of teaching. It would equally aid them

guide prospective investors and manufacturers on when and where to invest.

Curriculum planners of accounting education would use the facts of the findings in

curriculum planning and review. Students would be placed in the right frame of mind

to actualize their dreams of investing wisely, also being successfully employed as

financial analysts or in the least being self employed after graduation.

Finally, the knowledge that would be embodied in this study will aid policy

makers and public authorities responsible for the formulation of investment policies

and regulatory measures, make formidable policies and rules that would protect and

promote manufacturing companies to foster the economic development it is meant to

achieve.

Delimitation of the Study

This study was conducted in Enugu and Anambra states of Nigeria. It

covered the extent manufacturing companies’ utilize capital budgeting for optimal

investment analysis. No attempt was made to include other manufacturing companies

in other states of the federation.

28

CHAPTER TWO

REVIEW OF RELATED LITERATURE

The literature related to this study was discussed under the following headings:

Conceptual Framework

• Company • Manufacturing • Manufacturing Company • Capital • Investment • Budget • Capital Budgeting • Investment Analysis • Utilization of Capital Budgeting for Investment Analysis • The need for capital budgeting decision processes in corporate planning

• Management compliance in the use of capital budgeting techniques

• Utilization of capital budgeting by manufacturing companies for investment analysis

• Outsourcing of capital expenditure decisions and the prospect of

manufacturing companies • The effect of utilization of capital budgeting on companies earnings

• Constraints to effective use of capital budgeting for investment analysis

• Strategies for improving on the use of effective capital budgeting

Theoretical Framework

• Quantity Theory of Money

29

• Liquidity Premium Theory

• Arbitrage Theory of Capital Assets Pricing

• Utility Theory

• Portfolio Investment Theory

• Dominant Theory of Budgeting Related Empirical Studies

Summary of Related Literature

Conceptual Framework

Company

A company is a form of business organization, a corporate body or a

corporation, generally registered under the company’s Act or similar legislation.

Chartered Institute of Management Accountants (2004) defined a company as a legal

entity, an artificial person, that has rights and responsibilities of a real person, hence

very independent of its owners, and whose formation is either through the acts of

parliament or by the nations company’s acts. It is a form of business organization

incorporated according to the relevant laws of the country in which it operate, having

unlimited life span and limited liability, which can sue or be sued, enter into contracts

and pay dividend.

In English law, and therefore in Commonwealth realms, a company is a form

of body corporate or corporation, generally registered under the companies Acts or

similar legislations. It does not include a partnership or any other unincorporated

group of persons; hence they are not formed by the Act of parliament or by legislation

under company law, referred to as a limited liability or joint stock company. In the

30

United Kingdom, the main regulating laws are the Company’s Act of 1985 and the

Company’s Act of 2006. In Nigeria, references are made to the Company’s

Ordinance of 1912, 1917, 1922 and 1948; which later metamorphosised to the

Company and Allied Matter Decree of 1968; now revised, and known as company

and Allied Matter Act of 1990.

Companies may be classified into two major groups, namely: the private

company, and the public company. Private company according to Anyaele (2003), is

a form of limited liability organization formed and owned by between two and fifty

shareholders, whose shares cannot be traded on publicly nor transferred without the

consent of other shareholders, and is not quoted or listed in the stock exchange

market. Section 2 of the Company and Allied Matters Act of 1990 classified as

public, a company which has limitless number of shareholders, whose shares are

traded publicly and quoted in the stock exchange, and which members transfer shares

at will. Public companies are companies whose shares can be publicly traded, often

(although not always) on a regulated stock exchange; while private companies do not

have publicly traded shares, and often contain restrictions on transfer of shares

(Garner,2001).

Manufacturing

Manufacturing refers to a range of human activities, from handicraft to high-

tech, but is most commonly applied to industrial production, in which raw materials

are transformed into finished goods on a large scale (Zhou, 1995). The term

manufacturing is coined out from the Latin word “manu-factura”, meaning ‘making

by hand’. It is the use of tools and labour to make things which are utility bound, for

31

use or sale. Zhou further stated that modern manufacturing includes all intermediate

processes required for the production and integration of a product’s components.

This presupposes that manufacturing goes farther than transforming raw materials to

finished goods to include, processing of raw materials to semi finished (industrial)

goods for a second company’s further processing. This later class of manufacturing is

according to Zhou referred to as “toll manufacturing”.

Manufacturing Company

Manufacturing company on the other hand are companies that converts raw

materials and component parts into consumer or industrial goods. They are

companies that engage in fabrication of semi finished goods and, or the direct

processing of raw materials to finished goods (Afolabi, 1999).

The manufacturing sub sector can be classified based on two major sub-

divisions; either in accordance with area of coverage, or in relation to its capital base.

Based on area of coverage, four distinct groups are identified, namely; the

multinationals, the nationals, the regional and the local manufacturing companies.

The multinational companies encompass all companies with international spread.

That is, company with branches in many countries of the world. The nationals are

classified as those that are based within a country; while regional and locally based

are those that have their branches, if any, located within a region and those which

may concentrate in the rural areas of a state (Graham and Harvey, 2001).

Based on size of capital, four distinct classes of manufacturing companies are

also identified and they include; the micro cottage, the small scale, the medium scale,

and the large scale manufacturing companies. The definition of each of these class of

32

company varies from nation to nation and even authors, according to the number of

persons employed and the size of company’s capital base.

In Nigeria, single skilled artisans carried out the earliest form of

manufacturing with assistants, and training was through apprenticeship (Eneh, 2000).

Though remarkable change may be assumed to have taken place following Nigerian

independence, the wrongly held views and misconceptions about Vocational and

Technical Education made for a minimal progress in entrenching work habits in the

beneficiaries. In fact, Vocational Technical Education beneficiaries who could have

created work (become manufacturers) seek employment.

Vocational Technical Education according to Osuala (2000) is that type of

education which promotes the dignity of labour by entrenching work as a goal of

education. One of the goals of Vocational Technical Education according to NPE

(2004) is, to give training and impact the necessary skills to individuals who shall be

self reliant economically. If manufacturing as is earlier defined entails range of

human activities (work), ranging from handicraft to high-tech, and VTE was fully

entrenched in the Nigeria school system since the 1980’s, it may be presumed that

Nigeria has embraced early, a class of education that could have aid meaningful

progress in their manufacturing sub sector.

Nzelibe in Eneh (2005) posit that for most part of the last decade, the Nigeria

industrial and manufacturing sectors account for less than 10% of the nations Gross

Domestic Product (GDP), with manufacturing capacity utilization remaining below

30%. This contrasts what obtains in the developed economies whose manufacturing

sub sector according to Eneh accounts for over 70% of its gross national earnings.

33

Wehmeier (2001) defined apprenticeship as a system where someone is

contracted out to serve a skilled person for a period of time, and often for low

payment, in order to learn that person’s (master’s) skill. It is the process of educating

the child on the skills of the master. In essence, the first known Nigeria

manufacturers are the porters, weavers, the blacksmith, painters, sculptors, carvers,

and even farmers; and skills were owned by families, hence are highly valued and

zealously protected (Banjo, 1974). Even with the introduction of Vocational

Technical Education during the post independence era, the uncheering image which

followed suit made people believe that only the less privileged should be given the

knowledge of trading, cooking, gardening, carpentry (vocational education), while

academically bright students should go into literal education to get acquainted with

how to administer and govern (gain knowledge for white collar job).

Fafunwa (1974:195) in support of the above view opined, “the voluntary

agencies who pioneered western education in Nigeria were unable to popularize

Vocational Technical Education because of cost of training the staff and equipping of

such schools”. Apart from the cost Fafunwa further stated, evidence abound that the

colonial lords were mainly concerned with offering the natives little liberal education

which will enable them become interpreters, hence aid them achieve their economic

and religious aim. As such, Vocational Education and Manufacturing in Nigeria

suffer till date.

The manufacturing sector in developed countries has grown in size that its

level of intensity has become an acceptable index for measuring the economic

prosperity of any nation (Okafor, 1983). High level of production activities give rise

to abundance of consumer goods and services, thus facilitates improvement in the

34

production efficiency of the factor inputs, namely: the primary inputs (land, labour

and other resources); and the man made or produced factors. This produced factor

inputs are otherwise referred to as capital (Sadler, 2003).

Capital

Capital consists of assets, monetary and non monetary, contributed by owners

of a corporate organization to keep a business afloat. Association of Certificated and

Chartered Accountants (1998) defined capital as the monetary and non-monetary

assets contributed by owners of an enterprise (equity capital), and by the creditors

(loan capital) to get the organization going. It refers to the right of an enterprise to

utilize the services of produced factor inputs. In other words, capital (money) is held

because transactions take place at discrete time intervals.

However, the right of a company to utilize the services of produced factor

inputs (capital) is a function of the total value of real and financial assets available to

it (Govidarajan and Anthony, 2004). This right can be exercised either in the

ownership and control of real assets, or in that of financial assets. According to Pandy

(2006), real assets are tangible assets, while financial assets are claims on income to

be generated by real assets. Pandy further stated that, the total value of real and

financial assets available to an economic unit at any point in time constitutes its stock

of capital, otherwise referred to as, the wealth of that economic unit.

The objective for setting up manufacturing companies is wealth creation (Hirst

and Baxter, 1996), otherwise referred to as creation of utility (Samuelson, 1978).

Samuelson refer to utility as the ability of a product or service to satisfy human wants.

35

Hirst and Baxter defined utility as, that added value which makes a product or service

to be more esteemed than it initially was. This Hanson (1976) sees as production.

Wealth on the other hand, refers to the totality of a company’s earning

resulting from its investment (Lucy, 2003). As such, the design to increase, improve

or maintain capital (i.e. investment) has to be planned and returns predetermined,

hence every manufacturing company aims at wealth maximization. The wealth

maximization principle implies that the fundamental objective of a company is to

maximize the value of its shares (Pandy, 2006). The value of the company’s shares is

represented by their market price, which in turn is a reflection of shareholders

perception about quality of the firm’s financial position. Pandy maintained that, the

market price of shares serves as the company’s performance indicator.

Investment

Nweze (2004) defined investment as assets acquisition by an enterprise for the

purposes of capital appreciation and income generation. It encompasses all economic

activities designed to increase, improve or maintain the productive quality of existing

stock of capital. When the stock of available capital is less than the stock of capital

required to achieve the desired level of output, the need for additional investment

arises (Arnold and Turley, 1996). Consequently, the desired stock of capital

according to Okafor (1983) depends basically on two factors, viz: (i) the volume of

output, and (ii) amount of capital stock required per unit of the output. Similarly,

Hampton (1986) opined, optimum level of investment is reached when a company’s

capital stock available could maintain maximally, the volume of output demanded of

the company to meet its market share. This implies that, optimum investment reflects

36

the production point at which a company meets its desired capital stock level to

achieve the best rate of returns, more so when compared with that of competitors. It

is the determination of this desired stock level of capital coupled with its relative rates

of return that makes budget an inevitable tool for company’s corporate existence.

Budgeting

Budget is defined as the quantitative analysis made prior to a defined period of

time of a policy to be pursued for the period, to attain a given objective (Hanson,

1987). Similarly, Bodernhorn (2002) defines budget as, financial plans that provide

the basis for directing and evaluating the performances of individuals and segments of

the organizations. According to CIMA (2004), a budget is a plan quantified in

monetary terms, prepared and approved prior to a defined period of time, usually

showing a planned income to be generated, and or expenditure to be incurred during

that period, and the capital to be employed to attain a given objective. A budget could

be deduced to mean, a quantitative statement of plan of action for a defined period of

time, which may include planned revenues, expenses, assets, liabilities, and cash

flows which provides a focus for an organization; hence aids co-ordination of

activities, allocation of resources, and direction of activities for control purposes.

It may be pertinent at this juncture to note that different classes of budget exist

though may be subsumed into what is referred to as the master budget. The master

budget is the total budget package for an organization (Nweze, 2004). It combines all

the individual budgets for each part of the organization and aggregates it into one

overall budget for the entire organization. It may be subdivided into two major types

of budget, namely; i) the operating budget and, ii) the financial budget. The operating

budget consists of two parts, the programme budget and the responsibility budget.

37

The programme budget sets plan for estimated revenues and costs of the major

programmes that a company plans to undertake during the year (Hartmann and

Vassen 2003). It helps to determine, whether so much could be spent on a particular

item; whether adequate funds are available; whether the future benefits are

commensurate to the fund being committed; and so forth. The responses to these

opinions enable management take formidable decision that will stand the taste of

time.

The responsibility budget on the other hand, sets forth plans for persons

responsible for carrying out a specific task, work or activity. It is an excellent control

device since it is a statement of the performance that is expected of each

responsibility centre manager, against which his actual performance can later be

compared (Nweze, 2004). Nweze further contended that, if the total cost in a

responsibility centre is expected to vary with changes in volume as is the case with

most production responsibility centres, the responsibility budget may be in the form

of a variable or flexible budget, and as such will show the planned behaviour of costs

at various value levels.

The financial budget focuses more on plans for sources and application of fund

of the company. The major classes of financial budget include, the proforma

statement, the cash budget, the sales budget, the purchases budget, the production

budget and the capital expenditure budget. The proforma budget statement may be

further classified into, the budget income statement and the balance sheet budget.

The budget income statement is an estimated income statement, which indicates the

company’s planned profit and loss activities; while the balance sheet budget statement

is an estimated balance sheet, which gives the company an indication as to what its

38

balance sheet will look like in the future. It enables the company to make a judgment

in advance whether or not, its financial position will be suitable to meet its need;

particularly in the eyes of creditors (Nweze, 2004). The proforma statement budget

are generally less useful than other types of budgets because they do not have periodic

comparisons for variance analysis (Nweze, 2004; and Nolon, 2005).

Cash budget according to Nolon (2005) is an operating budget detailing the

planned cash receipts and payments. It represents the cash requirements of the

business during the budget period, hence makes certain that the business has

sufficient cash to meet its needs as and when they arise. Cash budget may be seen to

replicate receipt and payment account except that, while cash budget is futuristic,

receipt and payment account is historical. Cash budget are routinely prepared, while

receipt and payment accounts are conventionally prepared annually (Dam, 2005).

Sadler (2003) opined, the corner stone of successful marketing plan in a firm is

the measurement and forecasting of market demand. The key figure needed by every

company for successful operation is the sales forecast. Pike and Zanibbi (1996)

expressed the view that, effectiveness of budgetary control depends on the accuracy

of sales estimate. As such, sales budget is usually the starting point for budgeting

purposes, and is defined as an estimate of the revenue to be generated by the company

from its operations, as well as the focus of the much that is done within the company.

It is the sales value computed for individual products in units, in naria and in total for

the whole organization.

The purchase of direct materials is dependent on the levels of the beginning

inventory and the ending inventory. Hence, the units of materials to be purchased are

determined thus; budget usage plus desired ending inventory, less beginning

39

inventory. The result will equal purchases in units for the year, and the responsibility

area of the purchasing manager. It is the determination of the physical units of

material inventory, as well as the monetary value from the raw material usage budget

and from the stockholding policy that is referred to as purchases budget (Dam, 2005).

The production budget on the other hand according to Osisioma (1997), is a

statement of output expressed in tones, units or standard hours. He stated further that

production budget determines what is to be produced, when it is to be produced, and

how many are to be produced. It is generally prepared after the sales budget and the

total units to be produced, which is dependant on the planned sales and the expected

changes in inventory levels.

Investment Analysis

Manufacturing companies in order to serve Nigerian economic climate need to

develop and implement a well-conceived strategic plan for analyzing its capital

investment. Investment analysis entails adequate knowledge of cost of sales, estimate

of yield, and formulation of optimal mix of securities to obtain higher yielding

portfolios. According to Brounen and Kosdijk (2004), investment analysis involves

the evaluation of an investment through the establishment of cash flow, estimation of

the required rate of return (the opportunity cost of capital) and the application of a

decision rule for making choice. It is an appraisal technique whereby the need for the

decision is outlined and set in the context of the organization’s strategy. All realistic

options are identified and the relative merits and drawbacks of each option are

analyzed, culminating in the identification of a preferred course of action. In essence,

every investment is x-rayed in terms of its objectives, set in accordance with the

40

identified need, and clearly defined to produce criteria against which options can be

judged and against which the success of the project can be evaluated.

Similarly, Pandy (1999) posit that, it is important that the objectives of

investment are not so narrowly defined more so when such investment is strategic to

the company’s survival, as to prevent consideration of inappropriate range of options,

as loose as to generate unnecessary work. A plan is strategic when it is very detailed

for achieving success in situations as complex as war, politics, business, industry or

sports (Procter, 1996).

Capital Budgeting

Capital budgeting which is the main concentrate of this work is defined

according to ICAN (2006) as, the firm’s decision to invest its current funds most

efficiently in long term activities in anticipation of an expected flow of the future

benefits over a series of years. It is the process of planning expenditure on assets

whose returns are expected to extend beyond one year. Pandy (2006) pointed out that

investment decisions of the firm on capital assets are commonly referred to as capital

budgeting, capital expenditure management, capital expenditure decisions, capital or

long term investment decision, or management of fixed assets. It is the planning,

evaluation, and selection of investment in fixed asset proposals, which involves a

huge current outlay of cash resources in return for an anticipated flow of future

benefits. Investment in fixed assets have a long gestation period, from conceptual and

procurement stage, to when it starts to yield some stream of cashflows. Such

investment should be capable of yielding a reasonable rate of return so that the

business could meet its financial obligations to providers of capital (financiers) and

41

pay dividend to shareholders, or in a nutshell, maximize the wealth base of the

company.

According to Hilton (2004:186) capital budgeting is, “the decision making

process by which firms evaluate the purchase of major fixed assets, including

budilings, machinery and equipment. It also covers decisions to acquire other firms

common stock or groups of assets that can be used to conduct an on going business”.

Capital budgeting as described here involves the formal planning process to invest the

company’s capital in the procurement of fixed assets, or otherwise in the buying-up of

an existing business (company) or its fixed assets, purposefully to enhance the

viability of the investing company through enhanced business activities.

Warren and Fess (1996:76) defined capital budgeting as, ‘the process by which

management plans, evaluates and control capital expenditure decisions’. They stated

further that it maximizes the profit base of a company when handled proficiently and

may lead to liquidation when neglected. The implication is that, the management and

control of capital budgeting to a very large extent determines the company’s viability

and survival or otherwise, its failure.

According to Philippalys (2003), capital budgeting is concerned with the

allocation of firm’s scarce financial resources among the available market

opportunities. The consideration of investment opportunities involves comparison of

expected future streams of earnings from a project with immediate and subsequent

streams of expenditure on it. This assertion presupposes that capital budgeting

consists of the planning and development of available capital for the purposes of

maximizing the long-term profitability of the company. In other words, the system of

capital budgeting is employed to evaluate expenditure decisions which involve

42

current outlays, but likely to produce benefits over a period of time longer than one

year. The benefits referred to, may be either in the form of increased revenue or

reduction in costs. In essence, capital expenditure decision includes in addition,

disposition, modification and replacement of fixed assets.

The basic features of capital budgeting according to Pandy (2006) include,

potentially large anticipated benefits; a relatively high degree of risk; and a relatively

long time period between initial outlay and anticipated returns. These features Pandy

further stated are of paramount importance in financial decision-making and as such,

care should be taken in making such decisions on account that,

• Such decisions affect the profitability of the firm and also have much bearing on the competitive position of the enterprise;

• The future destiny of the company lies on capital budgeting decisions;

• It has its effect over a long time span and inevitably affects the company’s future cost structure;

• Capital investment decisions once made are not easily reversible without much financial loss to the firm;

• Capital investment involves huge cost and the majority of the firms have scarce capital resources;

• Over or under capacity should be in constant check as both results to waste; and

• Investment decision though taken by individual concerns is one of national importance because it determines employment, economic activities and economic growth.

The point worthy of note in these features and care as is elaborated is that a

company which carefully plan the allocation of its resources to capital assets,

evaluates available alternatives, ranks properly the alternatives; and then decides on

which best alternative to undertake using the available capital investment techniques,

43

will always stand competitive through increased sales, profit and dividend, and

ultimately increase the value of its share price.

Capital budgeting refers to the total processes of generating, evaluating,

selecting and following-up on capital expenditure alternatives. The company allocates

and budgets financial resources to new investment proposal. It is unlike investing in

stocks and bonds, where one is required to approach the securities market and based

on established forecast, invest. A company has to be proactive while investing in

capital assets since it has to take the very first step of planning for such asset

acquisition (Brigham and Weston, 1992). The authors further stated that, because the

company has to take the initial action (has to be proactive) in allocating or budgeting

financial resources to new investment proposal, it might be confronted with three

types of capital decisions. They include;

1. Accept or Reject Decision: The fundamental decision in capital budgeting is

to accept or reject a project proposal. This decision is often based on,

accepting proposals which yield a rate of return which is greater than a certain

required rate of return or cost of capital. By this application, all independent

projects are accepted. Independent projects are projects that do not compete

with one another in such a way that acceptance of one precludes the possibility

of the acceptance of another. This entails that all the independent projects that

satisfy the minimum investment criteria are implemented.

2. Mutually Exclusive Project Decision: Mutually exclusive projects are that

which compete with other projects in such a way that the acceptance of one

will exclude the acceptance of the other projects. Alternative projects are

mutually exclusive when each project is a perfect substitute of the other. It

44

may be noted that the mutually exclusive projects’ decision are not

independent of accept/reject decision. Mutually exclusive project decisions

acquire significance when more than one proposal is acceptable under the

accept/reject decision. As such, it then implies that some techniques (capital

budgeting techniques) have to be used to determine the best one. The

acceptance of the best alternative automatically eliminates the other

alternatives.

3. Capital Rationing Decision: Capital rationing refers to a situation where the

firm is constrained for external, or self imposed reasons, to obtain necessary

funds to invest in all investment projects with positive Net Present Value

(NPV). In a situation where a company has unlimited funds, capital budgeting

becomes a very simple process since independent investment proposals

yielding a return greater than some predetermined levels are accepted. (P.283).

However, this is not the situation prevailing in most of the business firms of

the real world. Though a company may have fixed capital budget, a large number of

investment proposals always compete in these limited funds. The company allocates

funds to projects in a manner that maximizes its long run returns. In that sense,

capital rationing refers to a situation where the company has more acceptable

investments requiring a greater amount of finance than is available with the firm. It is

concerned with the selection of group of investment proposals acceptable under the

accept/reject decision; hence ranking of the investment project is required. In capital

rationing, projects can be ranked on the basis of some predetermined criterion such as

the rate of return. The project with the highest return is ranked first and other

45

acceptable projects are ranked thereafter based on projected returns (Van Horne,

1998).

Utilization of Capital Budgeting for Investment Analysis

From the foregoing discussions on capital budgeting and investment analysis,

one may invariably argue that before a company can start the production of goods and

services, it must make adequate arrangement for all the necessary facilitates. The

acquisition of such facilities involves an enormous outlay of the company’s capital

funds and must be carefully selected. Capital budgeting decisions shall be rooted in

efficient and effective use of the company’s fund in the acquisition of the required

fixed assets. Effective and efficient utilization of capital budgeting provides a buffer

that will allow any company make good her sales, control its market share, maximize

its wealth base, and thus remain competitive (Hartmann and Vassen, 2003).

Utilization means to put into effective use (Wehmeier, 2001), while effectiveness and

efficiency go together in the literature of organization (Ile, 1999). Ile (1999) asserts

that effectiveness refers to the extent to which output is in line with organizational

objectives, while efficiency discusses the relationship between resources consumed in

the process of generating effective output and the output so produced.

Similarly, the foregoing discussion infers that efficient and effective utilization

of capital budgeting will result to the production of the desired output level at

minimal cost. Predicated upon this assertion is that any company that utilizes capital

budgeting effectively and efficiently will minimize cost, thus maximize the wealth

base of the company and as such cannot get liquidated.

46

The history of industrial development and manufacturing in Nigeria according

to Nzelibe in Eneh (2005), is a classic illustration of how a nation could neglect a

vital sector through policy inconsistencies and distractions, attributable to the

discovery of oil. Eneh affirms that manufacturing companies in Nigeria have suffered

tremendous set back since the late 1970’s due to the discovery of oil. The near total

neglect of agriculture has denied many manufacturers and industries their primary

source of raw materials. The Nigerian populace today seek non-existing white-collar

jobs and political positions, ‘cheap means of making it’, rather than embracing

agriculture which in the past was the mainstay of Nigerian economy. This has

resulted to mass unemployment and continued winding up of the manufacturing

companies in Nigeria. In line with this view, the Bureau for Public Enterprise have

noted that, with the exception of the multinational operators in the manufacturing sub-

sector, that other manufacturing companies have disappeared in the last two decades

due to unpredictable government polices, lack of basic raw materials (most of which

are imported), high interest rates, non implementation of protective existing policies,

lack of effective regulatory agencies, infrastructural inadequacies, unfair tariff and

low patronage (BPE, 2004).

According to Adams (2003), the Nigeria manufacturing companies are facing

lots of challenges as they struggle with economic depression and high inflation,

resulting from the international monetary fund (IMF) and World Bank credit policies

which have ushered in such programmes as Structural Adjustment Programme (SAP)

of the past, and the recent privatization and commercialization policies and

programmes. These programmes were initiated to promote the liberalization of the

Nigerian domestic economy, operations efficiency and productivity; promote private

47

owned enterprises growth and development, promote economic growth, trade and

investment.

Ocampe (2003) defined liberalization as the act of providing maximum

opportunity for a world free market economy, an open political system in which all

nations would participate to operate a long set of order and conventions. Though it

may have been the contention of the Nigerian government that its economic

liberalization policies would nurture an open economy and minimize the hurdles the

manufacturing companies need to clear in order to obtain raw materials and inputs,

and other resources for productive activities, Adams (2003) opined, it has created an

unprecedented change in their business environment through increased competition

both in the domestic market and from imports into the country.

Globalization constitutes another major challenge to Nigerian manufacturer.

Kwanashie (1998) defined globalization as the systematic integration of autonomous

economies into a global system of production and distribution. Globalization

encompasses global financial market; growth inter-connectedness of the media,

information systems, telecommunications and labour market; and global and regional

trade agreement. It is the common use and management of all nation’s resources, and

as such, involve intensified competition, increased focus on product quality and more

attention on research and development.

Since globalization involve intensified competition, increased focus on

product quality and demands more attention to research and development, one may

conclude that it poses even a greater threat to Nigerian manufacturers’ prospect;

moreso as Nigerian investment environment is full of uncertainties. These

uncertainties Eneh (2000) elaborated to include, the uncertainty in the occurrence of

48

future expectations caused by political factors; the uncertainty of economic climate

caused by interest rate fluctuations, inflationary pressure, monetary and fiscal policy

inconsistencies; uncertain social and cultural factors caused by the mood and belief

inconsistencies of the citizenry; and the ever growing technological factors which

affect the utilitarian purpose of capital assets procurement. These economic and

environmental uncertainties as elaborated above, pose great threat and are danger

signals to the Nigerian manufacturers, hence are potential for their incessant failure.

According to Eneh (2005), the Nigerian industrial and manufacturing sector

which accounts for over 50% of Nigeria’s GDP in the past, account for less than 10%

with manufacturing capacity utilization remaining below 35% for most part of the last

decade. Eneh further observed that 97.6% of Nigeria’s industrial and manufacturing

sub-sector is made up of Micro-cottage, Small and Medium Scale Enterprises

(MSMSE’s) and 3 out of 4 of these companies fails every year, while 9 out of the 10

persons who wished to go into business in Nigeria failed to do so. Nigerian

manufacturing sub-sector witnessed 12% growth in 1976, and its contribution to

Gross Domestic Product (GDP) rose from 4% in 1973 to 13% in 1983, but turned a

negative value of -0.9% in 1999, from -2.6% in 1994 (CBN Statistical Bulletin,

2001).

The Need for Capital Budgeting Decision Process in Corporate Planning

Businesses have limited resources, which serve their basis for operation.

These limited resources impose limits on the number, extent, and range of end results

each business sometimes sets out to achieve. Limitedness of resources has made

planning an inevitable tool for corporate existence in any company, and one of the

49

most essential tools of management (Koontz, and O’Donnel, 1972). Koontz and

O’Donnel further stated that, though other management functions are important,

planning is all embracing since the future survival or otherwise of every corporate

organization revolves around it.

Corporate planning entails the perception of immediate and past position of

the organization to enhance estimation of the future capabilities and reduction of

perceived uncertainties (Lee, 1991). It equips management with adequate information

about a company’s position to enable them estimate the possibility of embarking on a

specific course of action and achieve the desired result. According to Trewartha and

Newport (1992), corporate planning is a process of establishing goals and suitable

courses of action for achieving these goals. Similarly, Akpala (1990) defined it as

that plan made by a corporate organization to decide, what is to be done and to what

end; who will do what at certain time; and how it will be accomplished. Corporate

planning encompasses courses of action (plans) made by a corporate organization to

select in advance for its functional areas, future possible courses of action from

among alternatives that will lead to the realization of the organization’s set objectives.

Corporate Planning reorganizes decision making; envisages problems;

evaluates a range of information hence make use of relevant ones to develop a

suitable line of action which when adhered to, will lead to the attainment of the

organizational goal. Trewartha and Newport (1992:90) defined corporate planning as