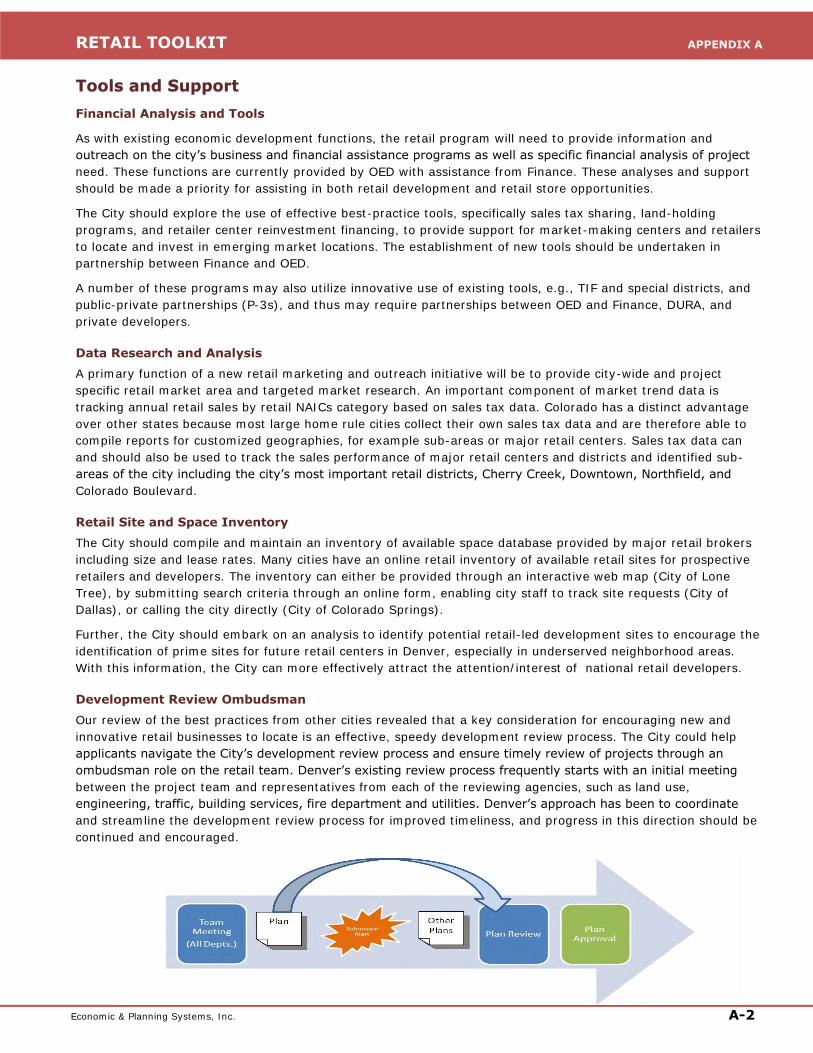

Denver - Economic & Planning Systems · County of Denver (City) to improve retail shopping...

44

Denver Retail Conditions and Opportunities Study June 2013 Prepared for: City and County of Denver Prepared by: Economic & Planning Systems with David, Hicks & Lampert Brokerage

Transcript of Denver - Economic & Planning Systems · County of Denver (City) to improve retail shopping...

Denver Retail Conditions and

Opportunities Study

June 2013

Prepared for: City and County of Denver

Prepared by: Economic & Planning Systems

with David, Hicks & Lampert Brokerage

ACKNOWLEDGEMENTS

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY

City and County of Denver

Michael B. Hancock, Mayor

Denver City Council

Mary Beth Susman, District 5, DRSAC Member

City Departments

Office of Economic Development

Department of Finance

Community Planning and Development

Denver Retail Strategic Advisory Council (DRSAC)

Marc Feder, Feder Commercial Realty Advisors

MC Genova, VISIT DENVER

Nick LeMasters, Cherry Creek Mall

Pat McHenry, Larimer Associates

Brian Phetteplace, Downtown Denver Partnership

Richard Sapkin, Edgemark Commercial Real Estate Services

Mark Sidell, Gart Properties

Julie Underdahl, Cherry Creek North BID

Joe Vostrejs, Larimer Associates

Consultants

Daniel Guimond, Economic & Planning Systems, Inc.

Chris Leutzinger, Economic & Planning Systems, Inc.

Matt Prosser, Economic & Planning Systems, Inc.

Steve Markey, David, Hicks & Lampert Brokerage, LLC

Scott Kaplan, CBRE

Erik Westedt, CBRE

Section 1:

Introduction

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY INTRODUCTION

Economic & Planning Systems, Inc. 1

This study was completed to provide information and insight to guide program development by the City and

County of Denver (City) to improve retail shopping opportunities within Denver. The need for both the study and

an enhanced retail development program is called for in the vision and strategies of Mayor Hancock’s

administration, and has been reinforced through the work of the City’s Structural Financial Task Force (SFTF).

The report of the SFTF emphasized that a strong and growing retail employment base is at the core of Denver’s

financial health and recommended that the City develop a more comprehensive and robust program to deliver

retail growth. The Denver Retail Conditions and Opportunities Study delivers proposed elements of that program,

providing analysis to understand the opportunities and challenges of enhancing Denver as a competitive market

for retailers and shoppers, while continuing to serve residents and neighborhoods.

In cooperation between the Mayor’s Office, the Office of Economic Development (OED), the Department of

Finance (DOF) and the Community Planning and Development Department (CPD), the City retained Economic &

Planning Systems (EPS), with David, Hicks & Lampert Brokerage to complete an analysis and study of the retail

conditions and opportunities affecting the Denver market. The study report is provided as recommendations to

these primary City clients for their shared efforts to develop strategies to meet the opportunities in Denver. The

OED formed the Denver Retail Strategic Advisory Council (DRSAC) in 2012 to provide advice and assistance in

promoting retail development and success. DRSAC has been a valued voice in the discussions and review of the

analysis underlying this study, along with vetting some of the ideas and recommendations within the report. In

the coming months, DRSAC will be a critical sounding board as the City’s retail program partners explore the

best methods for encouraging Denver’s retail market.

The EPS Team assignment, which is one part of a larger program initiative, was to:

Examine the existing retail conditions and activity to provide information about the changing resident and

visitor (customer) needs and demands in the marketplace, and the market capture of current retail centers

and stores (by retail category);

Review the immediate market strength and conditions of existing retail centers/areas, by category type;

Identify existing gaps in the Denver market, both by retail category and by center type;

Review and highlight best practices for retail development – program design, implementation strategies,

and appropriate tools (available currently and missing) for the City’s toolkit; and

Recommend potential retail program approaches for consideration by the appropriate Denver retail

partner–city department, quasi-public agency, and private sector developers, brokers or other key

stakeholder.

This report is intended to be a starting resource for the next stage in the City’s retail initiative and strategic

program development. With the advice and insights from the DRSAC, private sector partners, public and quasi-

public stakeholders, the Mayor along with the City’s leadership will work in the coming months to design a

successful, impactful retail program.

Study Goals

Improve the existing retail mix, increase retail sales tax revenue and attract new retailers to

the City and County of Denver without compromising existing retail.

Fully recognize and capitalize on existing consumer opportunities and identify retail gaps.

Add retail as a placemaking element consistent with citywide and small area plans especially

in identified mixed-use areas.

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY INTRODUCTION

Economic & Planning Systems, Inc. 2

Retail Aspirations As a bustling metropolis set against the backdrop of the Rocky Mountains, Denver is nationally recognized for its

exceptional balance of outdoor lifestyle and urban amenity. With the continued implementation of FasTracks and

rapidly expanding transportation options, Denver is also quickly becoming one of the country’s most livable

cities. This unique combination of assets has attracted an ever-growing population base and increasingly diverse

economy as employees and employers alike chose to locate in the region. Over the last decade, new restaurants

and retailers have also taken notice, and Denver’s downtown and urban neighborhoods are benefiting from an

increasingly vibrant mix of shops and eating and drinking options. Thus, Denver has all of the ingredients that

make a city a great place for retail. Yet in certain retail segments, Denver lags behind many cities throughout the

West as a nationally-recognized shopping destination. In order for Denver to reach the next step in its aspiration

of becoming a world class shopping destination, Denver needs to become a great retail city. The fundamental

components of any great retail city include having a vibrant downtown shopping environment, strong regional

retail destinations, and unique neighborhood business districts.

Vibrant Downtown Shopping

As the front door to visitors and the focal point of activity for residents and

employees, a vibrant downtown shopping district featuring a mix of strong

retail anchors, unique retail boutiques, and exciting entertainment, eating,

and drinking destinations is essential to any great retail city. Vibrant

downtowns successfully balance more traditional street-level storefronts

with new infill retail formats and centers that meet the needs and

requirements of the full range of store types and retailers. Vibrant

downtown retail districts generally have an identifiable retail core,

supporting a critical mass of activity, and provide strong connections to

adjacent retail streets. Challenged with negative perceptions of public

safety, successful downtown retail districts provide an identifiable and

functional public realm that softens the urban environment, creates visual

coherency, and offers a unique and interactive experience to the shopper.

In addition, the most successful downtown shopping districts are

supported by a strong downtown residential base. Combined with a unique

sense of authenticity, these distinctive attributes allow great downtown

retail districts to better compete with more traditional regional mall

destinations and provide both residents and visitors with a memorable and enduring experience.

Denver’s successful revitalization projects, including the 16th Street

Mall, Larimer Square, Denver Pavilions, Coors Field, Central Platte

Valley/Riverfront Park, and the soon to be completed Union Station,

have created vital pedestrian activity and elevated downtown’s status

as the region’s premier destination for eating, drinking, and

entertainment. However, downtown still lacks the diverse set of retail

stores found in cities with a core of downtown departments stores. In

addition, downtown’s flagship retail destination (REI) is located in an

isolated setting at the edge of downtown, limiting the ability to draw

customers to other downtown establishments. The linear pattern of

downtown established by the 16th Street Mall does not allow for a

sufficient critical mass of activity at any one segment, limiting its

ability to support new downtown retail. As a result, the quality and

mix of downtown retail is often cited as needing improvement by both

residents and visitors.

Strong Regional Anchors and Destinations

All great retail cities benefit from strong regional retail destinations throughout the city. This includes traditional

shopping malls, lifestyle centers, neighborhood business districts, and distinct retail corridors. While few

traditional shopping malls have been constructed nationally in the last decade, urban malls continue to perform

Pacific Place, Seattle, WA

Neiman Marcus, Union Square San Francisco, CA

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY INTRODUCTION

Economic & Planning Systems, Inc. 3

at peak levels and serve as home to many cities’ top retail attractions. These

retail centers not only provide critical format and demographic requirements

for some of the most desirable “one in the market,” specialty, and/or luxury

retailers. They often have some of the highest real estate values in the city

and anchor activity for a host of other uses, including residential and

employment. The best examples of strong regional retail destinations have a

defined sense of place, support enhanced densities, and frequently feature

the highest levels of vertical mixed-use development outside of downtown.

Similarly, regional retail corridors provide the necessary traffic counts to

attract and support a critical set of retailers. In great retail cities, these

corridors have undergone significant infrastructure (and often transit)

investment and have been reinvented from simple high-volume, automobile-

oriented thoroughfares to highly-functional economic places that support the

full-range of transportation modes, land use mixes, and modern urban retail

formats.

The Cherry Creek Shopping District, including Cherry Creek Mall and Cherry

Creek North, represents Denver’s strongest regional retail asset. Cherry

Creek Mall is home to Denver’s most diverse and highest quality retailers. Cherry Creek North is also host to a

strong collection of specialty and lifestyle-oriented retailers. Cherry Creek North has a strong mix of specialty

stores, contains the most progressive mixed use projects in Denver and landlords continually update outdated

space and users. Both locations within the shopping district could support the density and magnitude of vertical

mixed-use development found at world-class shopping destinations.

Unique Neighborhood Business Districts

Particularly critical to any great retail city are unique neighborhood

business districts (NBDs). These districts contain a strong mix of unique

and local businesses, balance locally-serving and destination retailers,

and serve as the setting for some of a community’s highest quality eating

and drinking options. Great NBDs have a strong sense of place and

defined identity and/or brand. As they are generally embedded within

existing residential neighborhoods, these districts have a strong

attachment with the local community; however, some of the best

neighborhood business districts also provide for the opportunity to mix in

retailers that serve a broader, citywide role. All great neighborhood

business districts feature strong multi-modal connections to allow for

greater neighborhood access, utilize the public realm for retailing

opportunities (sidewalk dining, farmers markets, etc.), and work together

to create parking solutions that do not conflict with local residents. In the

best retail cities, NBDs are also supported by a strong business district program with active city and community

leadership and with programs in place to encourage new and unique small business entrepreneurship.

Denver is home to a strong collection of urban NBDs. Denver’s districts are located throughout the city, along

large arterials or small neighborhood streets. The majority of retailers in Denver’s district contain a mix of eating

and drinking establishments and professional services. While some “soft” good retail (clothing, gifts, books/

music, etc.) exists, the City could do more to encourage local entrepreneurs (and some national stores) to open

new retail shops and boutiques.

The Challenge

The quality and diversity of retail in Denver has made great strides over the last 25 years. Retail in Downtown

has grown and increased in quality. Cherry Creek has emerged as a destination for fashion and specialty

retailers. New neighborhood business districts continue to emerge and thrive as the city grows. The assets

needed for a great retail city are present in Denver, but steps still need to be taken to reach this aspiration. This

study outlines the challenges and opportunities facing Denver.

Nordstrom at Horton Plaza, San Diego, CA

West Village, Dallas, TX

Section 2:

Retail Conditions

Economic & Planning Systems, Inc. 4

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL CONDITIONS

Retail Trends

Changing Demographics

Denver continues to grow, reaching a population of over

620,000 in 2011. Within this growth, there are five

major demographic shifts that are affecting retail

spending patterns.

The Denver metro area has become a major

destination for the Gen Y population in the past five

years. From 2008 to 2010, the Denver metro area had

the highest in-migration of 25 to 34 year olds in the

country. Gen Y has a higher preference for urban,

walkable neighborhoods and enhanced retail and

entertainment environments which is increasing the

market for neighborhood business districts in the city.

At the same time, Colorado is also a destination

for the Baby Boomer population. Colorado has

the fourth highest growth rate of people over age 65.

Many of these residents are choosing to downsize

their homes, which is changing their buying habits

and reducing demand for items to keep up their

homes. Although baby boomer spending patterns are

changing, they have the time and income for more

discretionary spending on natural and organic groceries,

dining, entertainment and travel.

The city has become more ethnically diverse, which is generating demand for a wider variety of products and

retail formats, such as supermarkets and other specialty stores oriented to Hispanic and Asian shoppers.

Many of Denver’s older, historic neighborhoods are attracting new residents and new development,

which is creating demand for new retail options. However there is a limited amount of existing, quality retail

space or areas to expand in these historic business districts.

Lastly, Denver has been experiencing an infill housing boom in the past five years. Multifamily units have

accounted for half of new residential building permits in recent years. In the downtown area alone, 6,700 new

multifamily units will be built between 2012 and 2014. The retail needs and preferences are different for these

smaller households and new retail space will be needed to meet the demand of new residents.

Denver MSA Residential Building Permits

(2003 - 2012)

City of Denver Capture of MSA Residential Building

Permits (2003 - 2012)

Net Migration of Population Age 25 to 34

American Community Survey Data BROOKINGS

Economic & Planning Systems, Inc. 5

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL CONDITIONS

Growth in E-Commerce

Online retail purchases grew at a 20 percent annual

rate over the previous 10 years compared to just 2.7

percent for total retail stores. However, e-commerce

sales (non-automotive) still comprise only 6.1 percent

of total retail spending. Online shopping is

changing the demand for traditional brick and

mortar retail which is pushing retailers to alter their

store formats and incorporate internet sales and

marketing into their business concepts. The line

between traditional and e-commerce retailers

continues to blur; 12 of the top online retail

businesses are actually major retailers including

Walmart, LL Bean, JCPenney, Macy’s, Staples, Best

Buy, and Bed Bath & Beyond.

Retail Evolution

The retail industry is and will continue to evolve and become more specialized. The growth in retail stores is

becoming bifurcated due to growth of sales at discount and luxury ends of the spectrum as shoppers look for

either lower prices or greater quality. The sales and profitability of mid-market stores are being squeezed; this

applies to general merchandise and department stores as well as to grocery and supermarkets. Retailers are

downsizing stores sizes and becoming more selective. Store size reductions (e.g., Best Buy, Office Depot,

Target, Walmart) reflect the need for less showroom space as well as lower sales per square foot. The number of

retail chains has been decreasing, due to reduced demand. At the same time, retailers are using larger trade

areas resulting in less total stores. Retailers are also developing new store formats or going to alternative

or smaller store formats to fit into underserved areas, primarily urban infill sites. Lastly, shoppers prefer retail

to be a fun and entertaining experience which is leading to new shopping center formats and retail as a

placemaking element.

US Total Retail Inventory, 1979 to 2013

US E-Commerce Retail Sales 2001 to 2010

Economic & Planning Systems, Inc. 6

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL CONDITIONS

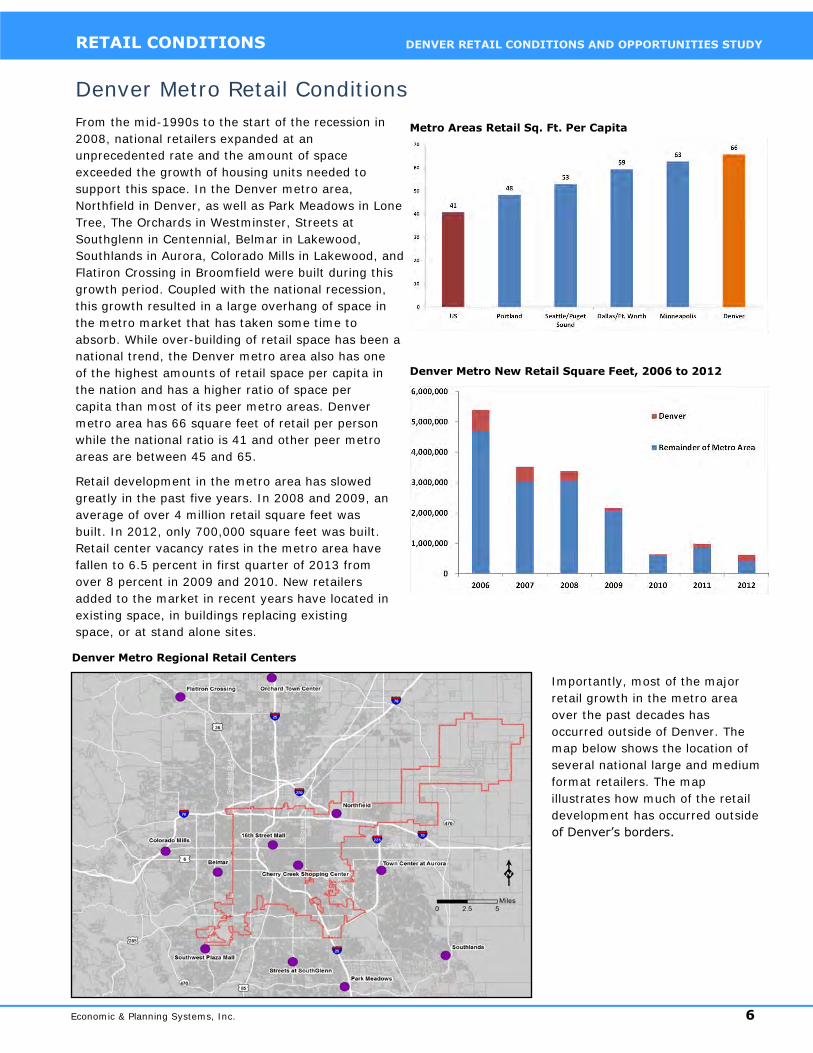

Denver Metro Retail Conditions

From the mid-1990s to the start of the recession in

2008, national retailers expanded at an

unprecedented rate and the amount of space

exceeded the growth of housing units needed to

support this space. In the Denver metro area,

Northfield in Denver, as well as Park Meadows in Lone

Tree, The Orchards in Westminster, Streets at

Southglenn in Centennial, Belmar in Lakewood,

Southlands in Aurora, Colorado Mills in Lakewood, and

Flatiron Crossing in Broomfield were built during this

growth period. Coupled with the national recession,

this growth resulted in a large overhang of space in

the metro market that has taken some time to

absorb. While over-building of retail space has been a

national trend, the Denver metro area also has one

of the highest amounts of retail space per capita in

the nation and has a higher ratio of space per

capita than most of its peer metro areas. Denver

metro area has 66 square feet of retail per person

while the national ratio is 41 and other peer metro

areas are between 45 and 65.

Retail development in the metro area has slowed

greatly in the past five years. In 2008 and 2009, an

average of over 4 million retail square feet was

built. In 2012, only 700,000 square feet was built.

Retail center vacancy rates in the metro area have

fallen to 6.5 percent in first quarter of 2013 from

over 8 percent in 2009 and 2010. New retailers

added to the market in recent years have located in

existing space, in buildings replacing existing

space, or at stand alone sites.

Importantly, most of the major

retail growth in the metro area

over the past decades has

occurred outside of Denver. The

map below shows the location of

several national large and medium

format retailers. The map

illustrates how much of the retail

development has occurred outside

of Denver’s borders.

Denver Metro Regional Retail Centers

Metro Areas Retail Sq. Ft. Per Capita

Denver Metro New Retail Square Feet, 2006 to 2012

Economic & Planning Systems, Inc. 7

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL CONDITIONS

Denver Retail Conditions

Retail Space There is approximately 34 million square feet of retail

space in Denver, which is 55 square feet of retail

space per capita and is less than the metro ratio of 66

square feet. This means that Denver is closer to the

national average and considering the city’s higher

incomes and spending power, Denver is therefore not

significantly overbuilt. The retail vacancy rate in

Denver was 5.6 percent in first quarter 2013, which is lower than the metro average of 6.5 percent. The average

rental rate is $16.97 per square foot which is higher than the metro area average of $14.65. While neighboring

cities continue to struggle to address their retail box vacancies, Denver has relatively few vacant boxes. The

vacant retail space that does exist is typically of poor quality and in less than prime locations. Thus, Denver is

better positioned to be more strategic in targeting sites for retail development.

The four major regional retail areas in the city are Downtown, Cherry Creek, Stapleton and Colorado Boulevard.

The city retail space is a mixture of space types with far less suburban style shopping centers than the

surrounding cities. Major recent retail additions include Northfield at Stapleton anchored by Macy’s, JCPenney

and Bass Pro Shops, and the Quebec Square power center anchored by Walmart, Sam’s Club, and Home Depot.

These two centers total over 1.8 million square feet of retail space.

There are few traditional shopping centers in the northern and central portions of the city. Much of the retail

space in these neighborhoods are in smaller buildings on shallow lots along major arterial corridors, such as

Colfax Avenue and Federal Boulevard, or in commercial blocks embedded within residential areas. These types of

retail spaces and buildings in the older portions of the city create both advantages and disadvantages. The

historic commercial building fabric in older neighborhoods is ideal for neighborhood business districts that serve

the surrounding neighborhoods. These districts have flourished in the past decade and can become vibrant

entertainment nodes with a mix of eating establishments and specialty retail. The development pattern has left

very few parcels that can accommodate larger, more modern retail development projects. Areas along I-25,

which runs through the entire city would be ideal for regionally oriented retail centers, but there is a lack of sites

suitable for retail development.

Major Denver Shopping Centers

Retail Market Denver (City) Denver (Metro)

Retail Square Feet 34,000,000 190,000,000

Square Feet per Capita 55 66

Average Rental Rates $16.97 $14.65

Vacancy Rate 5.6% 6.5%

Source: CoStar

Economic & Planning Systems, Inc. 8

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL CONDITIONS

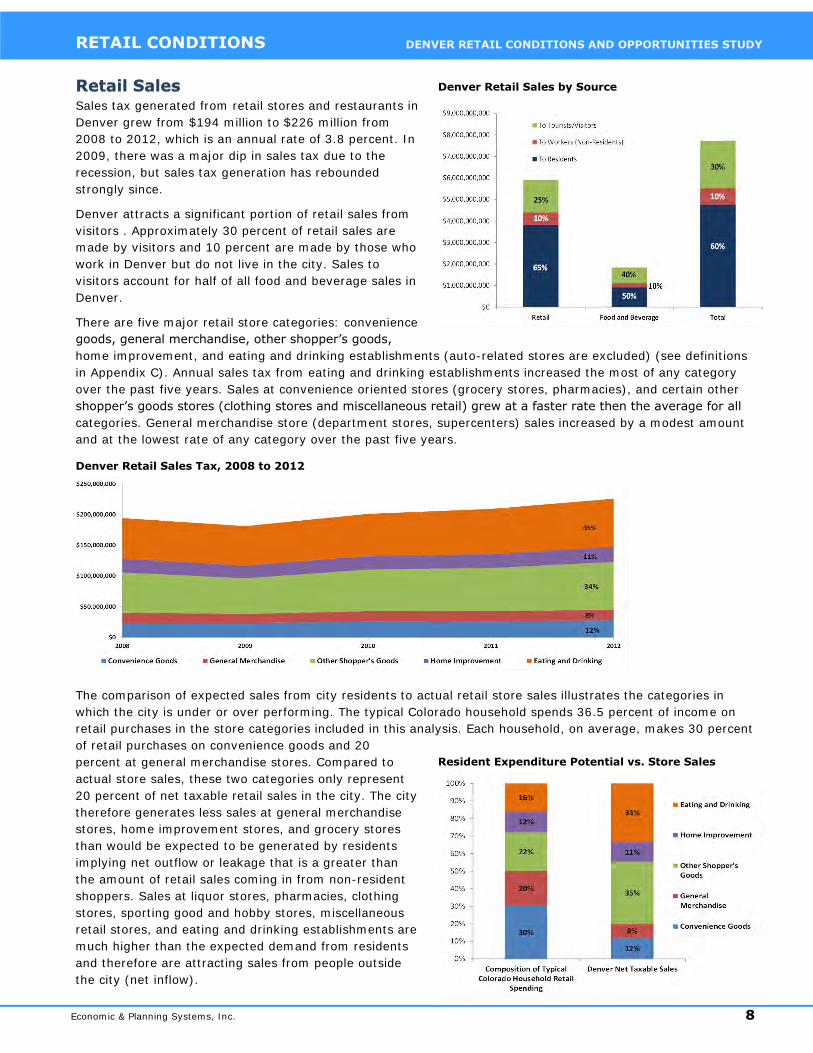

Retail Sales Sales tax generated from retail stores and restaurants in

Denver grew from $194 million to $226 million from

2008 to 2012, which is an annual rate of 3.8 percent. In

2009, there was a major dip in sales tax due to the

recession, but sales tax generation has rebounded

strongly since.

Denver attracts a significant portion of retail sales from

visitors . Approximately 30 percent of retail sales are

made by visitors and 10 percent are made by those who

work in Denver but do not live in the city. Sales to

visitors account for half of all food and beverage sales in

Denver.

There are five major retail store categories: convenience

goods, general merchandise, other shopper’s goods,

home improvement, and eating and drinking establishments (auto-related stores are excluded) (see definitions

in Appendix C). Annual sales tax from eating and drinking establishments increased the most of any category

over the past five years. Sales at convenience oriented stores (grocery stores, pharmacies), and certain other

shopper’s goods stores (clothing stores and miscellaneous retail) grew at a faster rate then the average for all

categories. General merchandise store (department stores, supercenters) sales increased by a modest amount

and at the lowest rate of any category over the past five years.

The comparison of expected sales from city residents to actual retail store sales illustrates the categories in

which the city is under or over performing. The typical Colorado household spends 36.5 percent of income on

retail purchases in the store categories included in this analysis. Each household, on average, makes 30 percent

of retail purchases on convenience goods and 20

percent at general merchandise stores. Compared to

actual store sales, these two categories only represent

20 percent of net taxable retail sales in the city. The city

therefore generates less sales at general merchandise

stores, home improvement stores, and grocery stores

than would be expected to be generated by residents

implying net outflow or leakage that is a greater than

the amount of retail sales coming in from non-resident

shoppers. Sales at liquor stores, pharmacies, clothing

stores, sporting good and hobby stores, miscellaneous

retail stores, and eating and drinking establishments are

much higher than the expected demand from residents

and therefore are attracting sales from people outside

the city (net inflow).

Denver Retail Sales by Source

Resident Expenditure Potential vs. Store Sales

Denver Retail Sales Tax, 2008 to 2012

Economic & Planning Systems, Inc. 9

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL CONDITIONS

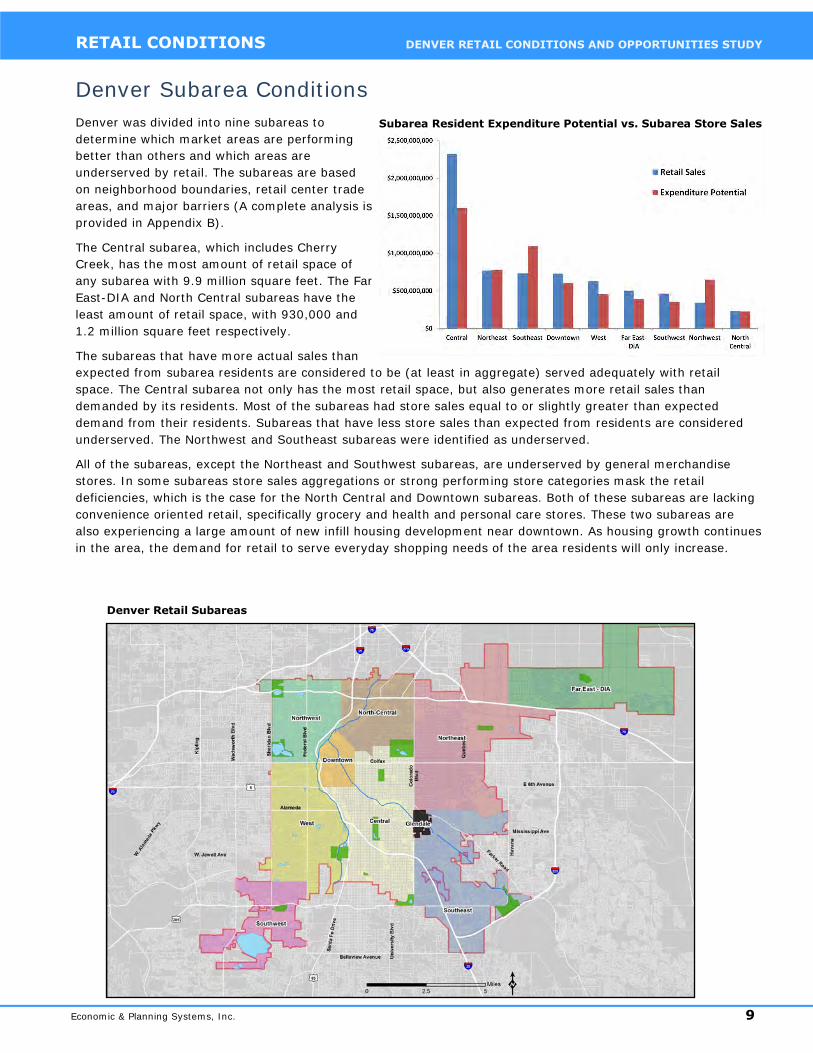

Denver Subarea Conditions

Denver was divided into nine subareas to

determine which market areas are performing

better than others and which areas are

underserved by retail. The subareas are based

on neighborhood boundaries, retail center trade

areas, and major barriers (A complete analysis is

provided in Appendix B).

The Central subarea, which includes Cherry

Creek, has the most amount of retail space of

any subarea with 9.9 million square feet. The Far

East-DIA and North Central subareas have the

least amount of retail space, with 930,000 and

1.2 million square feet respectively.

The subareas that have more actual sales than

expected from subarea residents are considered to be (at least in aggregate) served adequately with retail

space. The Central subarea not only has the most retail space, but also generates more retail sales than

demanded by its residents. Most of the subareas had store sales equal to or slightly greater than expected

demand from their residents. Subareas that have less store sales than expected from residents are considered

underserved. The Northwest and Southeast subareas were identified as underserved.

All of the subareas, except the Northeast and Southwest subareas, are underserved by general merchandise

stores. In some subareas store sales aggregations or strong performing store categories mask the retail

deficiencies, which is the case for the North Central and Downtown subareas. Both of these subareas are lacking

convenience oriented retail, specifically grocery and health and personal care stores. These two subareas are

also experiencing a large amount of new infill housing development near downtown. As housing growth continues

in the area, the demand for retail to serve everyday shopping needs of the area residents will only increase.

Denver Retail Subareas

Subarea Resident Expenditure Potential vs. Subarea Store Sales

Economic & Planning Systems, Inc. 10

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL CONDITIONS

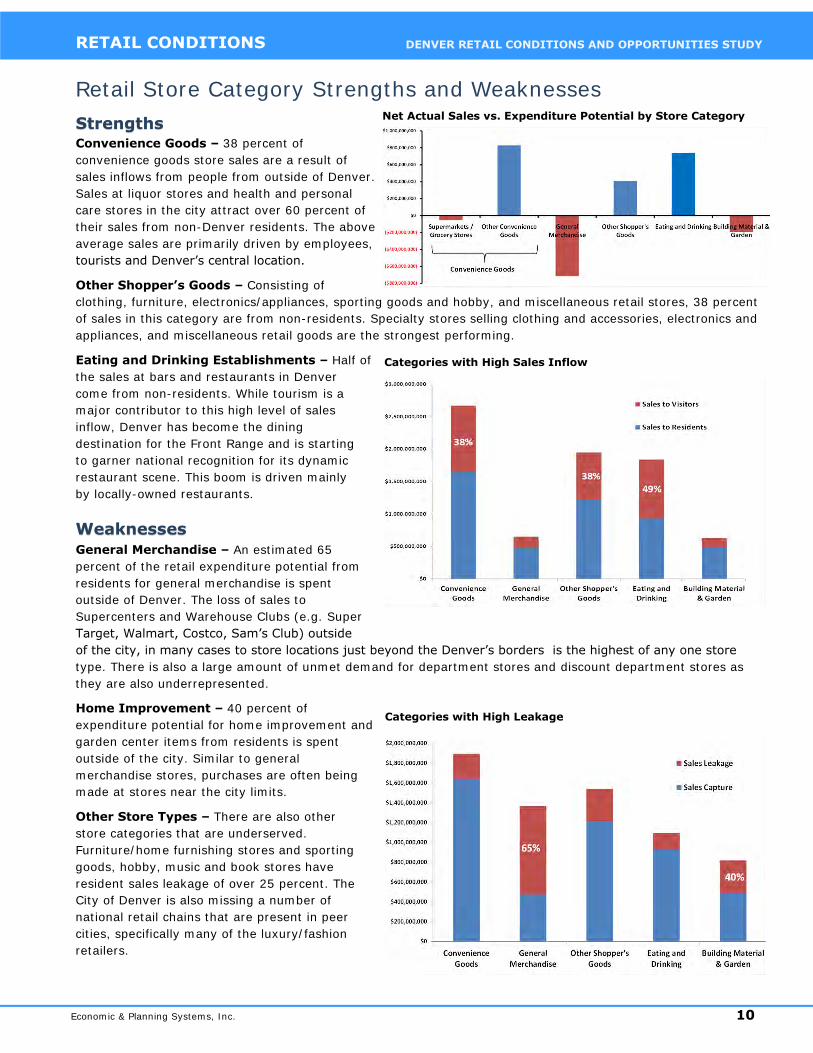

Retail Store Category Strengths and Weaknesses

Strengths Convenience Goods – 38 percent of

convenience goods store sales are a result of

sales inflows from people from outside of Denver.

Sales at liquor stores and health and personal

care stores in the city attract over 60 percent of

their sales from non-Denver residents. The above

average sales are primarily driven by employees,

tourists and Denver’s central location.

Other Shopper’s Goods – Consisting of

clothing, furniture, electronics/appliances, sporting goods and hobby, and miscellaneous retail stores, 38 percent

of sales in this category are from non-residents. Specialty stores selling clothing and accessories, electronics and

appliances, and miscellaneous retail goods are the strongest performing.

Eating and Drinking Establishments – Half of

the sales at bars and restaurants in Denver

come from non-residents. While tourism is a

major contributor to this high level of sales

inflow, Denver has become the dining

destination for the Front Range and is starting

to garner national recognition for its dynamic

restaurant scene. This boom is driven mainly

by locally-owned restaurants.

Weaknesses General Merchandise – An estimated 65

percent of the retail expenditure potential from

residents for general merchandise is spent

outside of Denver. The loss of sales to

Supercenters and Warehouse Clubs (e.g. Super

Target, Walmart, Costco, Sam’s Club) outside

of the city, in many cases to store locations just beyond the Denver’s borders is the highest of any one store

type. There is also a large amount of unmet demand for department stores and discount department stores as

they are also underrepresented.

Home Improvement – 40 percent of

expenditure potential for home improvement and

garden center items from residents is spent

outside of the city. Similar to general

merchandise stores, purchases are often being

made at stores near the city limits.

Other Store Types – There are also other

store categories that are underserved.

Furniture/home furnishing stores and sporting

goods, hobby, music and book stores have

resident sales leakage of over 25 percent. The

City of Denver is also missing a number of

national retail chains that are present in peer

cities, specifically many of the luxury/fashion

retailers.

Categories with High Sales Inflow

Categories with High Leakage

Net Actual Sales vs. Expenditure Potential by Store Category

Economic & Planning Systems, Inc. 11

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL CONDITIONS

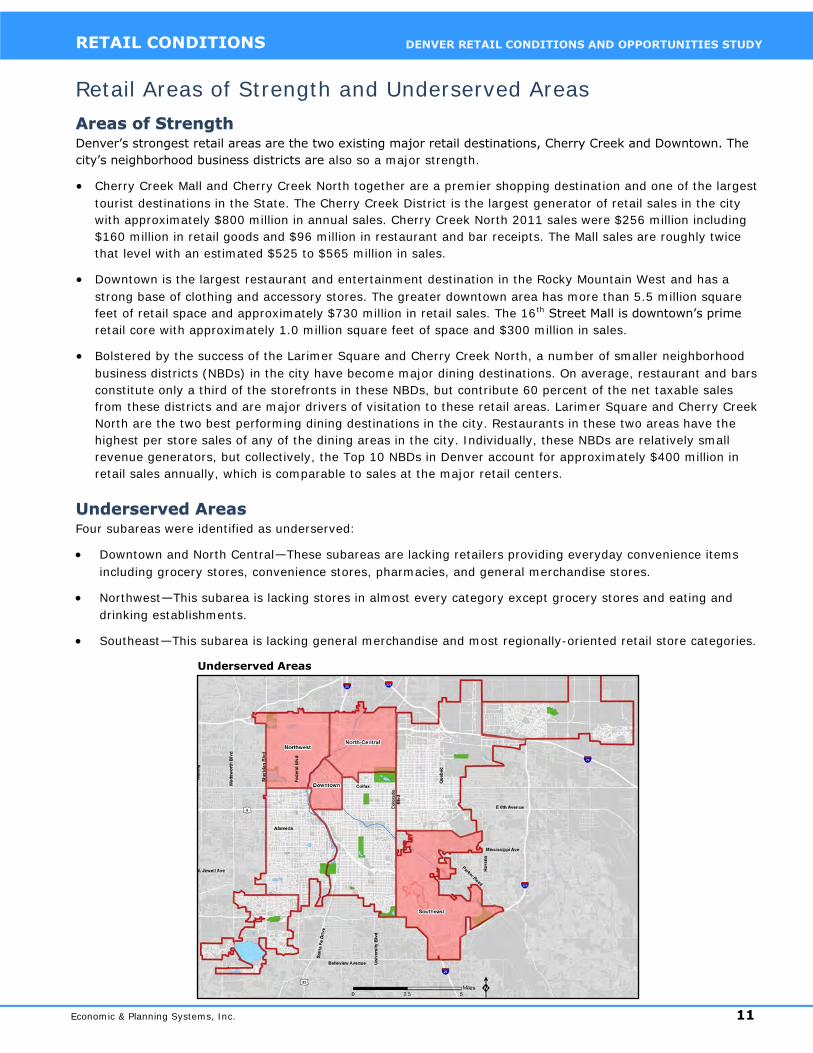

Retail Areas of Strength and Underserved Areas

Areas of Strength Denver’s strongest retail areas are the two existing major retail destinations, Cherry Creek and Downtown. The

city’s neighborhood business districts are also so a major strength.

Cherry Creek Mall and Cherry Creek North together are a premier shopping destination and one of the largest

tourist destinations in the State. The Cherry Creek District is the largest generator of retail sales in the city

with approximately $800 million in annual sales. Cherry Creek North 2011 sales were $256 million including

$160 million in retail goods and $96 million in restaurant and bar receipts. The Mall sales are roughly twice

that level with an estimated $525 to $565 million in sales.

Downtown is the largest restaurant and entertainment destination in the Rocky Mountain West and has a

strong base of clothing and accessory stores. The greater downtown area has more than 5.5 million square

feet of retail space and approximately $730 million in retail sales. The 16th Street Mall is downtown’s prime

retail core with approximately 1.0 million square feet of space and $300 million in sales.

Bolstered by the success of the Larimer Square and Cherry Creek North, a number of smaller neighborhood

business districts (NBDs) in the city have become major dining destinations. On average, restaurant and bars

constitute only a third of the storefronts in these NBDs, but contribute 60 percent of the net taxable sales

from these districts and are major drivers of visitation to these retail areas. Larimer Square and Cherry Creek

North are the two best performing dining destinations in the city. Restaurants in these two areas have the

highest per store sales of any of the dining areas in the city. Individually, these NBDs are relatively small

revenue generators, but collectively, the Top 10 NBDs in Denver account for approximately $400 million in

retail sales annually, which is comparable to sales at the major retail centers.

Underserved Areas Four subareas were identified as underserved:

Downtown and North Central—These subareas are lacking retailers providing everyday convenience items

including grocery stores, convenience stores, pharmacies, and general merchandise stores.

Northwest—This subarea is lacking stores in almost every category except grocery stores and eating and

drinking establishments.

Southeast—This subarea is lacking general merchandise and most regionally-oriented retail store categories.

Underserved Areas

Economic & Planning Systems, Inc. 12

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL CONDITIONS

Other Retail Observations

The successful retail areas and strong store categories in Denver are the result of several factors that are retail

strengths. Denver has strong retail leaders, especially in entertainment. The urban form and aesthetic of the

embedded neighborhood districts has proved to be the ideal fit for creating destination retail areas. The recent

surge of housing development in the city has driven up demand for retail growth and change. The workforce in

Denver generates 10 percent of retail sales. Lastly, 30 percent of total retail sales and 40 percent of food and

beverage sales are from visitors to Denver, both tourist, business visitors and residents of surrounding

communities.

However, there are underlying factors that have lead to obstacles to successful retail in Denver. The city lacks

development ready sites for new regional retail centers, particularly in northern subareas. There is a lack of

available Class A retail space and development sites. Large format retailers have located in the communities

surrounding Denver due to more attractive sites as well as the strong retail development programs in these

cities/towns. Denver has few local retail development companies in the market focused on projects in Denver as

compared to other cities. The city has not had an established retail development and recruitment program, which

has caused it to miss out on a number of major store location searches and decisions.

Surrounding Competition

(Example of General Merchandiser Locations)

Competing Trade Areas

Section 3:

Retail Opportunities

Economic & Planning Systems, Inc. 13

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL OPPORTUNITIES

Denver Retail Opportunity Areas

Denver’s opportunities for retail growth are reviewed in four locational categories, Regional Expansion Sites,

Potential Regional Retail Sites, Emerging Business Districts, and Refill/Redevelopment Sites.

Regional Expansion Sites The greatest opportunities for increasing retail sales activity are at the strongest existing regional nodes. Retail is

constantly evolving; centers and districts that do not reinvest and regenerate quickly become tired and

outmoded, and then lose sales to new competition. Therefore, identifying the opportunities for continued growth

and improvement in the city’s strongest retail districts should be a top priority.

1. Downtown/16th Street Mall

Much of downtown’s pedestrian traffic is funneled through the 16th Street supported by the Free Mall Shuttle

and pedestrian mall. As a result, 16th Street Mall has been most successful for restaurants and bars serving

this population for up to 18 hours a day. The Mall has been less successful developing a diverse mix of retail

shopping. Since downtown’s four remaining department stores closed in the early 1990s, the retail mix has

favored discount retail, oriented to a moderate income population and gift shops oriented to visitors. The

700,000 square foot Pavilions, built in 1998, provided an infusion of lifestyle and entertainment retail, but to

date has not generated as much spinoff development as anticipated. The remaining pockets of specialty retail

are dispersed throughout LoDo and the Central Platte Valley (CPV). Downtown, therefore has a solid retail

core but there are additional opportunities that can be pursued to achieve its potential full potential, such as:

Economic & Planning Systems, Inc. 14

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL OPPORTUNITIES

Continue to pursue department and other general merchandise anchor stores along or in close proximity to

the 16th Street prime retail core.

Redevelop key underutilized buildings and sites for retail and mixed use development including the

underutilized Gart’s building on California, Cottrell’s on Glenarm, and the Shames Makovsky site at 15th and

California.

Develop key cross streets between 16th Street and the Convention Center and Denver Center for the

Performing Arts on 14th Street including Champa and California.

Capitalize on the growing concentration of outdoor sporting good and apparel businesses in Lodo and Central

Platte Valley. Downtown has evolved into a young, hip residential and retail hub. Tenants such as Patagonia

and REI, along with chef driven restaurants and entertainment, reflect these demographics and psycho-

graphics. In order to capitalize on this trend, Downtown should continue to differentiate itself from the luxury/

adult image of Cherry Creek.

2. Cherry Creek

The Cherry Creek District has been extraordinarily

successful in the nearly 25 years since the Mall opened in

1989 and the Cherry Creek North District organized and

created the BID and implemented the first streetscape

program. Cherry Creek North has continued to evolve with

updated streetscape improvements completed in 2011

and the addition of a number of high quality infill and

redevelopment projects including Clayton Lane (2006),

300 Clayton (2007), Steele Creek (2009), North Creek

(2011), and Fillmore Plaza (2012). The immediate

changes anticipated are the implementation of the Cherry

Creek North Neighborhood Plan 2012 and a number of

additional redevelopment projects including 200

Columbine and the First and Steele mixed use projects.

Cherry Creek is a luxury destination, as well as a center for the adult/empty nester population groups. It is

important to continue to promote a separate and distinct brand for Cherry Creek. Both the Downtown and

Cherry Creek trade areas will benefit from a distinct, separate marketing approach.

Cherry Creek Mall faces the immediate challenge to reposition the vacant Saks Fifth Avenue Building, which is

expected to be developed as additional Mall retail space with improved access to First Avenue. Longer term

expansion opportunities include redevelopment of the Safeway/Rite Aid property on the east side of the Mall

and additional infill development on the original Mall property on the University Boulevard frontage.

3. South Colorado Boulevard

Colorado Boulevard is an important arterial retail corridor with a number of high performing community and

power centers serving the eastern portion of Denver. Extending from Alameda on the north to Yale on the

south, South Colorado Boulevard is one of the top suburban style retail corridors in the metro area supported

by a combination of high density population, high incomes, and office/daytime commuter activity. There has

been redevelopment of existing centers and sites on the corridor including the former supermarket at Evans.

More redevelopment, however, has occurred in Glendale than in Denver. The corridor suffers from shallow

retail parcels that do not fit the modern retail formats and relatively high land prices. The City should find

solutions to these challenges that are an impediment to further retail growth. The Colorado Boulevard corridor

continues to be a strong retail location with additional opportunities for infill and redevelopment including:

University Hospital Redevelopment – This 30-acre redevelopment site north on Colorado between 8th and 9th

Avenues is planned as a higher density mixed use development. It has the potential to include a significant

retail component to serve the adjacent Congress Park and Mayfair neighborhoods.

University Hills North Shopping Center – Immediately north of University Hills Plaza, this former community

shopping center maintains a strong mix of tenants in spite of being a dated property from the 1960s.

Cherry Creek North

Economic & Planning Systems, Inc. 15

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL OPPORTUNITIES

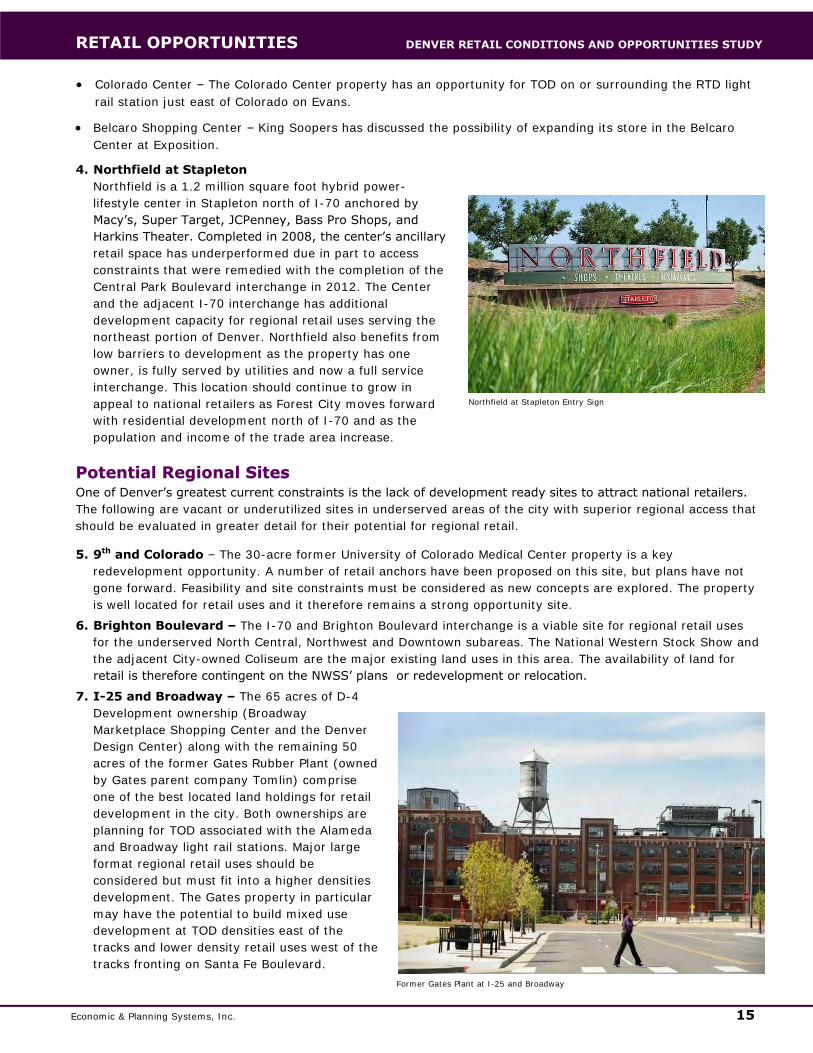

Colorado Center – The Colorado Center property has an opportunity for TOD on or surrounding the RTD light

rail station just east of Colorado on Evans.

Belcaro Shopping Center – King Soopers has discussed the possibility of expanding its store in the Belcaro

Center at Exposition.

4. Northfield at Stapleton

Northfield is a 1.2 million square foot hybrid power-

lifestyle center in Stapleton north of I-70 anchored by

Macy’s, Super Target, JCPenney, Bass Pro Shops, and

Harkins Theater. Completed in 2008, the center’s ancillary

retail space has underperformed due in part to access

constraints that were remedied with the completion of the

Central Park Boulevard interchange in 2012. The Center

and the adjacent I-70 interchange has additional

development capacity for regional retail uses serving the

northeast portion of Denver. Northfield also benefits from

low barriers to development as the property has one

owner, is fully served by utilities and now a full service

interchange. This location should continue to grow in

appeal to national retailers as Forest City moves forward

with residential development north of I-70 and as the

population and income of the trade area increase.

Potential Regional Sites One of Denver’s greatest current constraints is the lack of development ready sites to attract national retailers.

The following are vacant or underutilized sites in underserved areas of the city with superior regional access that

should be evaluated in greater detail for their potential for regional retail.

5. 9th and Colorado – The 30-acre former University of Colorado Medical Center property is a key

redevelopment opportunity. A number of retail anchors have been proposed on this site, but plans have not

gone forward. Feasibility and site constraints must be considered as new concepts are explored. The property

is well located for retail uses and it therefore remains a strong opportunity site.

6. Brighton Boulevard – The I-70 and Brighton Boulevard interchange is a viable site for regional retail uses

for the underserved North Central, Northwest and Downtown subareas. The National Western Stock Show and

the adjacent City-owned Coliseum are the major existing land uses in this area. The availability of land for

retail is therefore contingent on the NWSS’ plans or redevelopment or relocation.

7. I-25 and Broadway – The 65 acres of D-4

Development ownership (Broadway

Marketplace Shopping Center and the Denver

Design Center) along with the remaining 50

acres of the former Gates Rubber Plant (owned

by Gates parent company Tomlin) comprise

one of the best located land holdings for retail

development in the city. Both ownerships are

planning for TOD associated with the Alameda

and Broadway light rail stations. Major large

format regional retail uses should be

considered but must fit into a higher densities

development. The Gates property in particular

may have the potential to build mixed use

development at TOD densities east of the

tracks and lower density retail uses west of the

tracks fronting on Santa Fe Boulevard.

Northfield at Stapleton Entry Sign

Former Gates Plant at I-25 and Broadway

Economic & Planning Systems, Inc. 16

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL OPPORTUNITIES

8. I-70 and I-25 – The 35-acre former printing plant south of I-

70 between Pecos and I-25 is at the intersection of Colorado’s

two major national interstates with the greatest traffic volumes

in the state. This location has appeal for unique “one in the

market” uses. However, the site has major infrastructure

constraints including local access and utilities that would need

to be addressed before it is development ready.

9. Lowry Vista – This 72-acre site is located on Alameda

Boulevard in the Lowry Redevelopment. International Risk

Group (IRG) remediated the former landfill in 2004 and

completed a general development plan (GDP) in 2010 for

mixed use development including retail. The site would have

marketability for community and regional retail uses including general merchandise, home improvement, and

other shoppers goods stores. The site is also a great opportunity for conventional retail design that is

otherwise in short supply in Denver.

10. Belleview Station – This TOD is a 42-acre master planned development located north of Belleview and

west of I-25 at the Belleview light rail station. The project is at the Denver’s border with Greenwood Village.

It is planned for 2 million square feet of office, 1,800 housing units, two hotels, and 250,000 square feet of

retail. It is one of the city’s best opportunity for lifestyle and specialty retail at a transit station outside of

downtown.

11. Sun Valley – The parking lots surrounding Sports Authority Field at Mile High as well as land near the new

light rail station comprise a significant amount of land with I-25 frontage just to the west of downtown that

would have great appeal for retail. This area has a heavy demand for parking on only a limited number of

days per year. However, their ownership and competing uses make their availability for retail a challenge, in

the near term.

Emerging Neighborhood Business Districts High quality neighborhood business districts (NBDs) are an important amenity to desirable urban neighborhoods.

Most of Denver’s most desirable neighborhoods can claim a NBD. For both livability and revenue reasons, the

City should continue to promote and nurture the revitalization of older commercial areas into more specialized

retail and entertainment districts. Emerging NBDs have stores and restaurants that respond to the changing

demographics of the adjacent neighborhoods, but also contain unique local businesses and restaurants that

appeal to a larger citywide population.

12. East Colfax – East Colfax from York to Monaco

has become a more specialized district with newer

generation stores and restaurants serving the

nearby revitalizing neighborhoods including

Congress Park, City Park West, Mayfair, and Park

Hill. Businesses along the portion of Colfax from

York to Colorado recently formed the Bluebird

BID. A number of major new businesses have

been established including Marczyk’s Fine Foods,

Ace Hardware and Sprouts. There remain plenty

of sites for new stores to locate in existing retail

buildings or for new infill retail or mixed use

projects. However, similar to Colorado Boulevard,

Colfax is challenged by shallow, small parcels

prohibiting many larger users from finding a

location and providing services to residents.

13. Federal Boulevard – This segment of Federal (Alameda on the north to Mississippi on the south) has

developed a critical mass of Asian (mostly Vietnamese) shops and restaurants. This specialized retail cluster

has citywide appeal, but could benefit from the addition of an additional retail anchor, more specialty stores,

streetscape improvements and district identity improvements.

I-25/I-70 Opportunity Site

East Colfax Avenue

Economic & Planning Systems, Inc. 17

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL OPPORTUNITIES

14. River North (RiNo) – The developing area north of downtown

extending to I-25 is an emerging commercial and residential mixed

use district. Brighton Boulevard and Larimer Street have attracted

several new retail business, art galleries and a large amount of new

infill housing development. The area has potential for a cluster of

retail, restaurant and arts related businesses.

15. South Broadway – The City has supported South Broadway as a

revitalization district as early as the 1980s. The area from 6th

Avenue south to Alameda is finally gaining momentum as a hip

location for edgy local entrepreneurs to open boutiques, restaurants

and entertainment venues. This NBD is the most successful district

in the city in terms of the portion of sales from retail stores (not

restaurants) with 74 percent of the total activity. The intersection of

1st and Broadway is the epicenter of new activity supported by the

Mayan Theater and the new Punch Bowl Social (a nationally

recognized concept).

16. Central Platte Valley – The CPV is an area that is lacking a

defined NBD retail street or node. There are pockets of both

neighborhood serving and more regionally oriented specialty stores

including Platte Street, but a more comprehensive retail

development plan and image for the neighborhood should be

developed.

17. Welton Street – This historic NBD is in the heart of the largely African-American Five Points neighborhood

north of downtown. The City has invested an extensive amount of effort and funds into stimulating its

revitalization including the Wellington Webb Library and The Point housing development. It retains a mix of

other neighborhood oriented business and newer business start-ups. The high level of investment in new

infill housing and renovation of older homes in the neighborhood is both increasing area incomes and the

prospects for new neighborhood oriented business and restaurants.

Refill/Redevelop There are a limited number of vacant large format retail stores and vacant or outmoded shopping center sites in

Denver. These stores and centers create the potential for neighborhood or community infill retail/commercial

development to better serve the residents of these neighborhoods.

18. Chambers Place Shopping Center – This Safeway anchored neighborhood shopping center at 48th Avenue

just east of Montbello has a vacant junior anchor building with 25,000 square feet. The Safeway is an older

property with only 40,000 of leasable space, making the entire center is also a redevelopment possibility.

19. Southwest Commons – This shopping center is located in Denver immediately north of Southwest Plaza

Mall in Jefferson County and contains a number of mass merchandisers commonly found near malls including

Jo-Ann’s Fabrics and Cost Plus.

20. Alameda Square – The 100,000 square foot former home improvement store in the Alameda Square

Shopping Center at Alameda and Tejon is vacant and available for re-tenanting.

21. Federal and Evans (former K-Mart) - This 90,000 square foot vacant site has approximately 9.5 acres

and could be redeveloped for a range of neighborhood or community serving retail uses including potentially

an Hispanic superstore like Pro’s Ranch or a large format, general merchandiser.

22. Evans and Monaco (former K-Mart) – A K-Mart Holding Company (part of the Sears Company) owns this

vacant K-Mart store and property at 2150 South Monaco. This site is a good location for neighborhood or

community oriented retail. The vacant King Soopers west of Monaco is being redeveloped for a Walmart

Neighborhood Center.

The Hornet restaurant on South Broadway

Economic & Planning Systems, Inc. 18

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL OPPORTUNITIES

Denver’s Retailer Targets

The list of national retailers looking to expand is lengthy, but also fluid. Many retailers’ plans change year to year

based on overall corporate performance and shifting business plans. Denver’s retail tenant recruitment strategy

should focus on:

Building on existing strengths – Target and recruit additional retailers in the store categories and locations

of retail strength including fashion/luxury goods and home furnishings in Cherry Creek; general merchandise

and outdoor/ active lifestyle in downtown and Cherry Creek; and general merchandisers and mass

merchandisers on Colorado Boulevard and at the regional retail opportunity sites.

Address market gaps – Target and recruit retailers in the store categories that are underrepresented in the

city and for which there is leakage to the surrounding cities including general merchandise and home

improvement.

Capitalize on specialty/niche market opportunities— Denver’s ethnically diverse population creates

buyer demand for retail stores focusing on a specific consumer clusters. A recruitment strategy should identify

and pursue these market opportunities.

Target profitable and expanding retailers – The greatest retail expansion is currently taking place in the

store categories, such as luxury fashion and specialized food stores, that have responded to demographic

shifts and preferences, and area less impacted by online sales .

A number of major retailer opportunities are highlighted in the following list due to their absence or under

representation and/or their interest in the Denver market. A full list of tenants can be found in the Technical

Appendix of this report.

From Left to Right and Top to Bottom: Target store, downtown Minneapolis, MN; Dillard’s department store at the Atlantic Station development, Atlanta, GA;

Van Maur department store, Beavercreek, OH; Costco storefront

Economic & Planning Systems, Inc. 19

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY RETAIL OPPORTUNITIES

Specialty and Apparel

Areosoles

Build A Bear

C Wonder

CB2

Club Monaco

dELia's

Disney

Fuego

Hanna Andersson

Intermix

Lego

Original Penguin

Pottery Barn

Sperry Topsider

Splendid

TopShop

UniQlo

ZARA

Outdoor/Active Lifestyle

Adidas Sport

Billabong

Burton

Columbia Sportswear

ecco

Helly Hanson

mont-bell

Moosejaw

Mountain Hardwear

Marmot

Merrell

New Balance

Convenience Goods

The grocery store market is growing due to changing demographics and consumer preferences. There are

additional store opportunities for ethnic grocers and natural food markets including:

Pro’s Ranch—Hispanic Superstore

H-Mart—Asian Supermarket

Trader Joe’s—Natural Foods Grocer

General Merchandise

Denver is underserved in general merchandise stores with considerable leakage to the suburbs. The following

successful chains are opportunities to open their first store in Denver or expand to underserved neighborhoods:

Von Maur—Department Store

Dillard’s—Department Store

Kohl’s—Department Store

City Target and Super Target—Super Center

Costco—Warehouse Club

Mass Merchandisers

The following mass merchandisers also represent opportunities due to leakage and interest by these retailers in

the Denver market:

Conn’s—Electronics

Dicks Sporting Goods—Sporting Goods

Lowe’s—Home Improvement

Menard’s—Home Improvement

Scheels—Sporting Goods

Specialty Stores

Based on a survey of specialty retailers found in Denver’s peer cities including Seattle and Dallas, there are

several candidate apparel, home furnishings, and jewelry/accessory stores not present in the Denver. Below is a

list of potential retailers that may be attracted to Denver. In addition, a list of over 40 additional luxury retailers

present in other cities is provided in the Technical Appendix .

Section 4:

Retail Blueprint

RETAIL BLUEPRINT

Economic & Planning Systems, Inc. 20

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY

Program Development Observations

Great retail cities take a variety of approaches to support the retail sector, ranging from relatively hands off to

very intentional. They require strategic planning, leadership, adaptability, and careful coordination among a

variety of public and private partners. There is no one right program or organizational structure. The optimum

city staffing for implementing a retail program should be based on identified city needs and the strengths of

existing public and private entities with a role in retail development and recruitment.

Denver has no strategic program or policy for growing the retail sector to date. The City’s economic development

initiatives have focused primarily on recruitment of new office and industrial based firms, as well as retention and

expansion of existing businesses. The retail sector has been secondary, particularly because of the lower wage

rates associated with most retail jobs. However, the importance of the retail sector has grown for a number of

reasons:

Denver has become a regional draw in a number of specialized retail sectors, including fashion, outdoor

lifestyle apparel and sporting goods, and restaurants and entertainment uses. The collective impact of these

attractions generates significant inflow of retail spending and sales tax revenues for the City.

There is greater recognition of the importance of having retail goods and services conveniently located near

and within the city’s neighborhoods to add to the quality of the neighborhood . The most desirable areas of

the city have close-by grocery and other convenience goods stores and restaurants and specialty merchants

in walkable neighborhood business districts.

A significant portion of Denver households do not have retail stores close by, resulting in retail sales leakage

and the loss of associated sales tax revenues. This is particularly true in the northern subareas of the city.

The City is increasingly dependent on sales tax revenues for fiscal viability. Retail store sales taxes account

for approximately 25 percent of general fund revenues and will continue to are a grow as other sources,

including employment and property taxes, have been increasing at a slower rate.

For these multiple reasons, EPS recommends the City take a more proactive stance toward growing and

attracting new retail business. EPS outlined its recommendations for an overall vision, specific objectives and

specific strategies based on a review of programs and policies of other cities’ programs and the opportunities

identified in the analysis.

Larimer Square

RETAIL BLUEPRINT

Economic & Planning Systems, Inc. 21

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY

Conceptual Vision

The City and County of Denver seeks to attract new retail businesses

and investments in existing and new retail centers and districts to serve

the needs and desires of residents and visitors, increase city retail sales

tax revenues, and improve the quality and livability of its neighborhoods,

transit oriented developments, and neighborhood, community, and

regional centers.

Objectives to Achieve the Vision EPS recommends six retail development and marketing objectives designed to help the City achieve the above

vision and its goals for retail expansion and enhancement. For each objective, a series of high priority strategies

are recommended.

Ensure that all Denver residents have the opportunity to buy

the full range of retail goods and services within the city 1

Support the expansion of Denver’s existing regional retail

destinations 2

Attract additional regional retail stores and centers 3

Cultivate and expand Denver’s neighborhood business

districts 4

Promote Denver’s brand as the premier destination for

outdoor/active lifestyle retailers 5

Maintain and grow Denver as the entertainment destination

of the Rocky Mountain West 6

RETAIL BLUEPRINT

Economic & Planning Systems, Inc. 22

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY

In addition to being underserved in large-format retailers, several subareas are lacking in the full range of

convenience-oriented goods that are necessary for everyday living including grocer and drug stores. Without the

addition of new retail in these areas, existing and future residents will be increasingly forced to leave their

neighborhood, as well as the city, to acquire retail goods. To prevent this growth in retail leakage, the City

should actively recruit new retailers in convenience-oriented store categories to these subareas, as well as

revitalize existing outmoded neighborhood retail space to accommodate new tenants.

Create a recruitment strategy for convenience-

oriented store categories in underserved areas. The

City should actively market underserved retail areas to

convenience-oriented store categories, including grocery,

health and beauty (pharmacies), as well as smaller-scale

home improvement and/or eating and drinking

establishments that serve neighborhood needs. The

subareas with the most need include Downtown and North

Central. Opportunity to attract new quality national

Hispanic-oriented supermarkets offering discount and

specialty food items also exists in the West subarea.

Create tools and policies for retailers in underserved

store categories. In addition to marketing, the City

should investigate using financial tools to target

underserved store categories. This includes structuring

criteria specific to convenience-oriented retailers, as well

as evaluating the use of the recently established Colorado

Fresh Food Financing Fund to target new grocery and

supermarket stores.

Provide support for the renovation of outmoded

retail centers and stores and technical assistance in

underserved neighborhoods. Many of the underserved

subareas possess existing neighborhood retail centers that

feature a significant amount of deferred maintenance and

are outmoded for today’s retailers. The City should create

financial tools that promote the reinvestment of these

centers in order to fit the needs of new tenants. In addition, the City should expand its technical assistance

services to encourage local entrepreneurs to open new retail establishments to meet the needs in the community

where national retailers are unwilling to locate.

Ensure that all Denver residents have the opportunity to buy the full

range of retail goods and services within the city 1

Ross and Slyderman food chart, 16th Street Mall

South Federal Blvd retail

RETAIL BLUEPRINT

Economic & Planning Systems, Inc. 23

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY

Support the expansion of Denver’s existing regional retail destinations 2 The City should take every measure to help support and promote its existing regional destinations. These assets

are often the most desirable locations for new retailers to locate, and thus, should be given considerable

attention in communications with brokers, developers, and national retailers for high priority tenants and

developments. As many of these regional assets have existing points of contact, the City should clearly define

the roles of communication between OED and public and private partners.

Determine the roles and staffing for OED to serve as the primary point of contact for retail

development. As existing regional destinations, Downtown (Downtown Denver Partnership), Cherry Creek Mall

(Taubman), Cherry Creek North (Cherry Creek North BID), and Northfield (Forest City) already have their own

retail promotion and marketing efforts in place. Thus, establishing definitive roles with external partners will be

particularly critical in order to avoid the duplication of efforts and miscommunication with potential retail targets.

For areas outside of these large private-ownership or special districts, OED should be the primary point of

contact for retail development, including new store recruitment, retail center development, local public and

private improvements, and ongoing support of existing retailers.

Develop information marketing materials for retail recruitment and promotion. OED should develop

trade area profiles and customized market studies for tenant recruitment, and all regional retail assets should be

highlighted as major shopping destinations in tourism outreach efforts. OED should also compile a

comprehensive inventory of key retail sites and buildings in each of the regional retail nodes to track ongoing

performance and identify tenant opportunities in support of recruitment efforts.

Provide appropriate development assistance and incentives for identified retail stores and/or

categories. Specifically, sales tax sharing is an effective tool for assisting in attracting key retailers to a specific

location. OED should have pre-established criteria for the use of any tools in order to provide transparency and

consistency to public and private partners. OED should support the expansion of all regional assets, providing

development assistance incentives and polices where appropriate. This is particularly true for identified targeted

retailers and/or retail store categories.

16th Street Mall Clayton Lane, Cherry Creek North

RETAIL BLUEPRINT

Economic & Planning Systems, Inc. 24

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY

Despite strong regional assets, Denver is currently

underserved by regional retail uses and should encourage the

development of new regional stores and centers. This includes

the addition of general merchandise, furniture, home

improvement, and other large-format retailers with significant

sales tax generation potential. Attracting these types of

retailers requires the identification and creation of regionally-

accessible sites, as well as establishing a “business-friendly”

reputation to the national retail and brokerage community.

Identify potential sites for regional retail uses and one

in the market retailers. An evaluation of potential new

regional retail sites that could serve identified underserved

areas and also possess the qualities (acreage, regional access,

demographics, etc.) desired by new retailers yielded two

potential locations; a northern location along I-25 between 6th

Avenue and I-70 and a midtown location along I-25 near the

intersection with Broadway. The City should factor the

potential for new regional retail uses in its future planning

efforts in these areas, including the evaluation of necessary

property assemblage, remediation, and regional infrastructure improvements.

Actively recruit additional general merchandise retailers and major retail sales tax generators. As

noted, the city is underserved in general merchandise, furniture, and home improvement retailers and has

limited large retail sales tax generators. In order to attract these types of retailers, the City should be proactive

in its marketing efforts and incentive policy, and identify specific criteria and tools focused on large sales tax

generators.

Market Denver as a business-friendly retail destination to the retail development and brokerage

community. In order to establish its vision and commit to creating great places; the City should clearly

communicate to the brokerage and retail community that it is willing and able to think creatively to

accommodate new large-format retailers, including working to meet financial and physical needs of priority

stores and categories. This involves meeting regularly with the local retail brokerage and development

community, as well as attending national showcases such as the ICSC RECon Marketplace.

Attract additional regional retail stores and centers 3

H&M, Denver Pavilions

City Target, Seattle, WA

RETAIL BLUEPRINT

Economic & Planning Systems, Inc. 25

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY

While more traditional retail formats are important for providing necessary goods and services to residents and

generating sales tax dollars to the city, neighborhood business districts are critical to supporting local

entrepreneurship, as well as providing unique shopping, entertainment, and dining destinations to residents and

visitors throughout the city. In aggregate, the city’s strong collection of established and emerging neighborhood

business districts also generate a substantial sales tax revenue to the city and should continue to be cultivated

and expanded as critical retail assets.

Create a coordinated citywide marketing program to promote local businesses and neighborhood

retail districts. The city currently has a mix of programs used to market its neighborhood business districts,

including neighborhood profile brochures, as well as various business district profiles on Visit Denver’s tourism

website. In order to successfully market its neighborhood retail districts, the City needs a coordinated effort that

includes a consistent set of marketing materials and separate business district website that effectively

communicates the unique identity of each district, as well as highlights shops, restaurants, and local

entrepreneurs.

Establish a citywide neighborhood business district program eligible to all neighborhood business

districts. The city currently has two primary financial tools targeted to assist neighborhood business districts, as

well as more traditional national programs including Enterprise Zones and CDBG funds. While these are

important, the City should evaluate the potential to expand some form of eligibility to all neighborhood business

districts through a qualifying process in order to support local entrepreneurship throughout the city. In addition

to expanding assistance to neighborhoods of all economic status, the City should continue to expand the amount

of available tools and technical assistance.

Cultivate and expand Denver’s neighborhood business districts 4

Little Man Ice Cream and Linger Restaurant, LoHi

Fancy Tiger Clothing, South Broadway Talulah Jones, East 17th Avenue

Platte Street, Central Platte Valley

RETAIL BLUEPRINT

Economic & Planning Systems, Inc. 26

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY

As Colorado’s front door, Denver’s nationally known as a premier outdoor

activity destination, and this reputation should continue to be promoted.

This includes developing a strong cluster of outdoor lifestyle retailers and

advertising the Denver brand to national retailers and visitors.

Develop a list of desirable targeted outdoor/active lifestyle

retailers not present in Denver, including fashion, apparel, and

sporting goods retailers, and market Denver to these retailers in

recruitment efforts. Denver’s outdoor lifestyle brand should span several

retail categories, including fashion and apparel, sporting goods, and even

health food retailers. The City should develop a list of the most desirable

retailers not currently present in Denver, and target these retailers in its

recruitment efforts.

Designate a retail node as the regional hub for outdoor/active

lifestyle attractions, including identified development sites and/or

store locations. In order to attract a cluster of similar retailers, the City

should designate a retail node, or nodes, that serve as the regional

destination for outdoor lifestyle shopping. This includes identifying existing

buildings, sites, streets, and store locations. The co-tenancy requirements

of these retailers is strong and will require a critical mass to be successful.

Hold fashion and retail showcase events during outdoor lifestyle conventions and sporting events

including the SIA Snow Show, International Sportsman Expo, USA Pro Challenge, and Colorado

Crossroads Volleyball Tournament. The City of Denver should leverage the national visitation of its large

outdoor lifestyle events to include the promotion of its outdoor lifestyle retailers. This includes holding fashion

shows at targeted sporting events and industry conventions. It also includes elevating the status of the city’s

existing fashion industry by holding premier fashion events that integrate traditional fashion and apparel with

outdoor lifestyle retailers, as well as the growing “fashion truck” scene.

Promote Denver’s brand as the premier destination for outdoor/active

lifestyle retailers 5

REI Flagship store, Central Platte Valley

Patagonia, 15th Street, LoDo

RETAIL BLUEPRINT

Economic & Planning Systems, Inc. 27

DENVER RETAIL CONDITIONS AND OPPORTUNITIES STUDY

With the magnitude of sports teams, cultural amenities, music venues, and growing collection of world-class

eating and drinking establishments, Denver has established itself as the premier entertainment destination of

the Rocky Mountains West, attracting 11 million visitors per year from the length of the Front Range and

frequent visitors from states such as California, Arizona, and Texas. As the city’s primary retail strength, the City

should continue to grow and develop this desirable market niche.

Market available financial tools to local eating and drinking restaurateurs. Eating and drinking

businesses have experienced the most significant growth of any retail category over the last five years. Local

chefs are beginning to receive national acclaim and a growing group of world-class chefs are beginning to

migrate to Denver, attracted by its increasing urban sophistication and laid-back attitude. Yet, few restaurants

have utilized small business assistance programs. To maintain the city’s momentum and elevate its stature as a

world-class dining destination, the City should actively market available tools to and support local and national

restaurateurs.

Continue to support restaurant promotion programs such as EatDrinkDenver.com and Denver

Restaurant Week. Denver Restaurant Week has successfully expanded into a renowned eating and drinking

event, promoting dining options throughout the city to local and regional residents. In addition, VisitDenver

recently launched an independent eating and drinking website that successfully highlights Denver’s strengths,

such the local brewing industry, growing street food scene, and strong neighborhood dining destinations. The

City should closely evaluate how this effort should be incorporated into its own promotion of retail and

neighborhood business districts.

Build on Create Denver program and art events such as First Friday. The City has recently recognized the

importance of its local arts and culture destinations and has two art districts, Sante Fe Arts District (certified)

and RiNo Arts District (prospective) qualified with the Colorado Creative Industries program. The City should

continue to support these districts, as well as include additional growing districts such as the Golden Triangle

and Tennyson Street. The City has also established its own program, Create Denver, which promotes the city’s