Demographic Fractionalization and the Municipal Bond Market

39

1 Demographic Fractionalization and the Municipal Bond Market Daniel Bergstresser, Randolph Cohen, and Siddharth Shenai* This paper studies the impact of ethnic and religious fractionalization on the U.S. mu- nicipal debt market and finds that issuers from more ethnically and religiously fractional- ized counties pay higher yields on their municipal debt. A two standard deviation increase in religious fractionalization is associated with a six basis point increase in bond yields, and a two standard deviation increase in ethnic fractionalization is associated with a 10 basis point increase. To provide a scale for these results, a four-notch rating change, from AAA to AA–, is associated with an eight basis point increase in yields. Additional analysis suggests that at least some of this effect is not driven by the risk of the bonds but reflects, instead, inefficiency in the underwriting process. A variety of researchers have explored the impact of ethnolinguis- tic diversity on economic outcomes. Easterly and Levine (1997) propose that ethnolinguistic fractionalization can explain the poor growth observed in post-colonial Africa: borders left by the former colo- nial powers have resulted in ethnically divided countries that make for *Daniel Bergstresser is an associate professor of finance at the Brandeis International Business School (IBS). Randolph Cohen is a senior lecturer at the Massachusetts Institute of Technology Sloan School of Management. Both are also active in consulting and other activities in the investment management industry. Siddharth Shenai works at Bracebridge Capital. The authors are grateful for support from Harvard Business School.They are also grateful for comments from Bart Mosley, Alexander Whalley, Andrei Shleifer, and Alberto Alesina, and from seminar participants at the Brandeis University 2012 Municipal Finance Conference, the U.S. Securities and Exchange Commission, Harvard Business School, Boston College, the University of Southern California, and the University of California, Merced. Finally, they are grateful for excellent research assistance from Mei Zuo. This paper was delivered at the Brandeis International Business School’s 2012 Municipal Finance Conference in Boston, Massachusetts, on August 3, 2012. Daniel Bergstresser can be reached by email at [email protected].

Transcript of Demographic Fractionalization and the Municipal Bond Market

1

Demographic Fractionalization and the Municipal Bond Market Daniel Bergstresser, Randolph Cohen, and Siddharth Shenai*

This paper studies the impact of ethnic and religious fractionalization on the U.S. mu-nicipal debt market and fi nds that issuers from more ethnically and religiously fractional-ized counties pay higher yields on their municipal debt. A two standard deviation increase in religious fractionalization is associated with a six basis point increase in bond yields, and a two standard deviation increase in ethnic fractionalization is associated with a 10 basis point increase. To provide a scale for these results, a four-notch rating change, from AAA to AA–, is associated with an eight basis point increase in yields. Additional analysis suggests that at least some of this effect is not driven by the risk of the bonds but refl ects, instead, ineffi ciency in the underwriting process.

A variety of researchers have explored the impact of ethnolinguis- tic diversity on economic outcomes. Easterly and Levine (1997) propose that ethnolinguistic fractionalization can explain the poor

growth observed in post-colonial Africa: borders left by the former colo-nial powers have resulted in ethnically divided countries that make for

*Daniel Bergstresser is an associate professor of fi nance at the Brandeis International Business School (IBS). Randolph Cohen is a senior lecturer at the Massachusetts Institute of Technology Sloan School of Management. Both are also active in consulting and other activities in the investment management industry. Siddharth Shenai works at Bracebridge Capital.

The authors are grateful for support from Harvard Business School. They are also grateful for comments from Bart Mosley, Alexander Whalley, Andrei Shleifer, and Alberto Alesina, and from seminar participants at the Brandeis University 2012 Municipal Finance Conference, the U.S. Securities and Exchange Commission, Harvard Business School, Boston College, the University of Southern California, and the University of California, Merced. Finally, they are grateful for excellent research assistance from Mei Zuo.

This paper was delivered at the Brandeis International Business School’s 2012 Municipal Finance Conference in Boston, Massachusetts, on August 3, 2012. Daniel Bergstresser can be reached by email at [email protected] .

2 MUNICIPAL FINANCE JOURNAL

1 Gettleman (2011): “More than any other continent, Africa is wracked by separatists. There are rebels on the Atlantic and on the Red Sea. There are clearly defi ned liberation movements and rudderless, murderous groups known principally for their cruelty or greed. But these rebels share at least one thing: they direct their fi re against weak states struggling to hold together disparate populations within boundaries drawn by 19th-century white colonialists.”

2 We access these data through the American Religion Data Archive and refer to them throughout the paper as the ARDA data.

challenging governance. 1 In the American context, Glaeser, Scheinkman, and Shleifer (1995) fi nd no effect of racial fragmentation on the growth rates of cities, but Alesina and La Ferrara (2000) fi nd that more ethnically fragmented communities have lower participation in civic associations such as church groups, fraternities, and service groups. These social insti-tutions contribute to social capital and can have positive economic effects, as discussed by Putnam (1993, 1995). Similar research on religious diver-sity, however, is lacking, although McCleary and Barro (2006b) examine the relationship between religious observance and economic growth.

In this paper, we use American counties as a laboratory for studying the impact of fractionalization. This approach has at least two advantages. First, using American counties holds constant a variety of underlying factors that cannot be kept constant in cross-country analysis. Second, because local authorities borrow in credit markets, the yield that they pay on their debt is a natural index for comparing their performance. Higher yields on municipal debt must refl ect either higher risk (if capital markets are working effi ciently) or cross-locality differences in the effi ciency with which the municipal underwriting process works.

We construct fractionalization measures of ethnic diversity using data from the 2000 Census, and of religious diversity using the 2000 Religious Congregations and Membership Study, a survey of the major religious denominations conducted by the Association of Statisticians of American Religious Bodies. 2 In this context, fractionalization represents the probabil-ity that two randomly selected members of a group will share a particular attribute. For example, in a society that is half white and half Hispanic, the ethnic fractionalization measure would be 0.5; there would be a 50% chance that any two randomly selected people would be of the same ethnicity. Fractionalization is the most common measure used to capture the extent to which a particular society is divided across a particular characteristic.

We focus on ethnic and religious fractionalization because these charac-teristics are both salient and relatively fi xed. Wealth, income, and education are not directly observable, and like age they vary mechanically over the life cycle. Ethnic and religious affi liations are generally more static. These mea-sures capture the underlying concept that we focus on, namely the strength of social ties across citizens and between citizens and offi cials in a local area.

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 3

3 The only exception is a handful of counties in south Texas that are homogeneous and Hispanic.

We fi nd evidence that municipal issuers in religiously fractionalized coun-ties pay more to borrow than those in other counties. The point estimates suggest that a one standard deviation increase in fractionalization (0.091) is associated with a three basis point (= 0.3025 * 0.091) increase in the offering yield of debt issued by jurisdictions in the county. A change in religious frac-tionalization from the level observed in highly fractionalized Juneau, Alaska (where our fractionalization index is 0.1746, indicating a 17% chance that two randomly selected people reporting a religion are of the same religion) to highly homogeneous Rich County, Utah (where the fractionalization index is 0.8365) would be associated with a 20 basis point reduction in municipal bond yield at offering. This effect is robust to the inclusion of controls for the overall level of religious observance in a county.

Ethnic fractionalization is also associated with higher bond yields. In contrast to the religion result, the pure effect of ethnic fractionalization is somewhat diffi cult to disentangle from the phenomenon whereby more homogeneously white counties pay less to borrow. While the existence of religiously homogeneous communities of a variety of religious back-grounds allows separate identifi cation of the fractionalization effect, the ethnically homogeneous counties are almost uniformly ethnically white counties. 3 In a specifi cation including just ethnic fractionalization, a one standard deviation increase in ethnic fractionalization is associated with a fi ve basis point increase in bond yields. However, in a specifi cation includ-ing both ethnic fractionalization and the share of the county population that is white, the fractionalization variable is statistically insignifi cant. The result for the white share of population variable suggests that going from 100% white to 100% nonwhite would be associated with a 24 basis point increase in bond yields. Although disentangling an ethnic fractionalization effect from a “share white” effect is diffi cult at the county level, analysis of richer data at the sub-county level suggests that both effects are at work.

Finding a relationship between ethnoreligious fractionalization and municipal bond yields, we investigate potential causes of this relation-ship. By defi nition, one can divide the mechanisms at work into those that refl ect risk and those that are not related to the risk of the municipal bonds. One hypothesis is that more fractionalized localities pay more to borrow because their bonds are riskier; in that sense, higher yields refl ect effi cient operation of municipal capital markets. Alternatively, higher yields could refl ect less effi cient monitoring of the bond underwriting process, meaning that more fractionalized places pay more to borrow but that those higher costs do not refl ect higher risk. We use the shorthand of “risk” versus “monitoring” in describing these two competing hypotheses.

4 MUNICIPAL FINANCE JOURNAL

4 The Herfi ndahl index is the sum of the squares of the different groups’ shares. So, for example, a population that was 80% Hispanic and 20% Asian would have a Herfi ndahl index of (0.8 x 0.8 + 0.2 x 0.2), or 0.68. There would be a 68% chance that two randomly selected individuals were from the same group, and also a 32% chance that they were from different groups. This Herfi ndahl-based measure is not the only measure of diversity that one could choose: Alesina et al. (2003) explore “polarization” measures of diversity. These measures, however, involve explicitly or implicitly specifying a distance between different groups. Although this is natural for measures of diversity in income or wealth, we do not know of any unambiguous one-dimensional measure of religious or ethnic identity and thus use only the fractionalization measure that is more common in the literature.

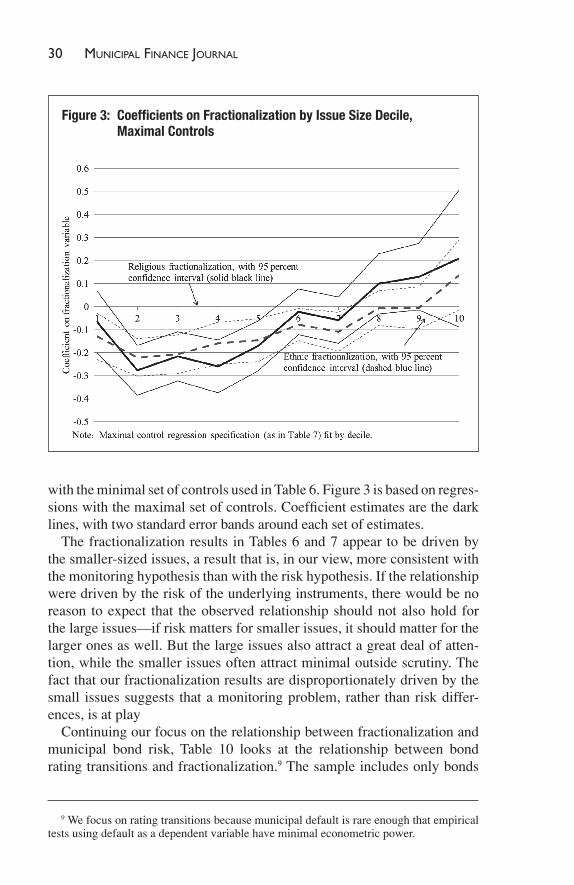

Our analyses suggest that at least part of the fractionalization effect refl ects monitoring rather than risk. When we use credit ratings as a proxy to control for risk, we fi nd that more fractionalized places pay more to borrow, even controlling for the risk of their bonds. We also fi nd some evi-dence that the prices of bonds issued by fractionalized localities increase in the fi rst 120 days post-issuance, suggesting that the yields at issuance are higher (and prices at issuance are lower) than the eventual market equilibrium. We also fi nd that the fractionalization effect is driven by the smaller issues rather than the larger ones. If the fractionalization effect refl ected risk, there is no reason to expect that the effect would be different across issue size. In our view, the fact that the fractionalization effect is strongest for the smallest issues—bonds that are often issued with minimal oversight and attention—is more consistent with the hypothesis that our observed yield differences refl ect differential failures in monitoring than that they refl ect differences in risk. Taken as a whole, our results suggest that religious and ethnic composition have an impact on municipal bor-rowing costs in the United States, and that at least some of this effect is unrelated to the risks of the bonds that localities issue.

The remainder of this paper is organized as follows: The fi rst section presents a brief review of the relevant literature on the economic effects of ethnoreligious fractionalization. The second section describes the empiri-cal tests applied in this paper. The third section describes, in detail, the dataset and econometric methodology that we employ. The fourth section presents and interprets the results of our econometric analysis. A brief fi nal section concludes.

THE EXISTING LITERATURE The index of fractionalization we use in this paper is the ethnolinguistic

fractionalization (ELF) measure developed by Soviet anthropologists in the 1960s and defi ned as one minus the Herfi ndahl index of ethnolinguistic shares. 4 This measure represents the likelihood that two randomly cho-sen individuals in a given population belong to different subgroups. In an empirical paper, Easterly and Levine (1997) show that the high ELFs in

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 5

Sub-Saharan Africa explain characteristics associated with low economic growth, including political instability, underdeveloped fi nancial systems, high government defi cits, and distorted currencies. The authors conclude that ethnolinguistic fractionalization, caused in particular by the ad hoc nature of the national boundaries drawn by colonial powers, explains much of Africa’s post-colonial failure to generate sustained economic growth.

Collier and Gunning (1999) also demonstrate the explanatory power of ELF with respect to economic growth in African nations. Collier (2000) further fi nds that the impact of diversity on economic growth in a sample of countries between 1960 and 1990 was a function of the political context—diverse dictatorships saw slow growth, while diverse democracies did not. La Porta et al. (1999) look at the determinants of the quality of government across countries. Among their fi ndings are that nations that are ethnolinguistically heterogeneous have inferior gov-ernment performance. The dimensions of government performance that they investigate include measures of corruption, bureaucratic delays, tax compliance, and property rights. Alesina et al. (2003) extend this work to include measures of linguistic and religious fractionalization. Their mea-sure of religious diversity is the same as ours, and they point out that, at least in the international context, religious identity is often more reliably measured than linguistic or ethic membership, making the religious frac-tionalization measure particularly useful for empirical research.

Several studies have focused on the economic and fi scal impacts of eth-nolinguistic and racial fractionalization at the city, county, and state levels in the United States. Glaeser, Scheinkman, and Shleifer (1995) investi-gate the socioeconomic determinants of economic growth of U.S. cities between 1960 and 1990. City growth is one reasonable measure of the suc-cess of different areas; if people are free to move across cities, then achiev-ing city growth represents at least relative success. The authors fi nd that the non-white share exerts a minimal impact on subsequent city growth. Among cities with large non-white shares, they fi nd that increased segre-gation is positively related to subsequent growth. One interpretation that they offer is consistent with costs of fractionalization: they suggest that segregation in heavily non-white cities lessens ethnic confl ict. Alesina, Baqir, and Easterly (1999) develop a model connecting heterogeneity of preferences across ethnic groups in a political unit to the amount and type of public goods that the political unit supplies, and they test the model on U.S. cities, urban counties, and states. They fi nd that the provision of pro-ductive public goods (roads, hospitals, schools, etc.) in cities and counties is inversely related to ethnic fragmentation, and they suggest two reasons, which they refl ect in the model: (1) different ethnic groups can have dif-ferent preferences over which public goods should be produced, and (2) different ethnic groups can have their marginal utility of the public

6 MUNICIPAL FINANCE JOURNAL

good reduced by other groups’ consumption. They fi nd some empirical evidence that the fi scal balance before intergovernmental transfers tends to be worse in more ethnically fragmented cities.

A study by Vigdor (2004) looks at response rates to the 2000 Census questionnaire. Responding to the Census refl ects individual provision of a local public good. Because federal grants to local areas are determined by Census counts, an uncounted individual costs his locality as much as $500 per year. Vigdor shows that Census response rates are lower among counties that are more racially, generationally, and socioeconomically het-erogeneous—the provision of this important local public good appears to be lower in more fractionalized localities.

Theoretical work by Alesina and Drazen (1991) explores the relation-ship between fractionalization and the economic outcomes. Both papers present models where sociopolitical fragmentation may lead to confl icts over the allocation of the tax burden and to the consequent delay of defi cit reduction policies. In these models, delayed stabilization is the result of a war of attrition game, where different groups try to force the other to bear the cost of the stabilization. In the context of our research on municipal debt, this effect would make debt issued by fractionalized localities more risky than debt issued by more homogeneous localities because the more fractionalized localities would tend to delay (and possibly fail to enact) budget stabilization packages in the face of persistent defi cits.

McCleary and Barro (2003, 2006a, 2006b) have recently brought ana-lytical rigor to inquiry exploring the relationship between religion and economic outcomes. They present cross-country examination of the two-way interaction between economic growth and religion. With religion as the dependent variable, McCleary and Barro (2006b) fi nd that per capita GDP has a signifi cant negative relationship with all religiosity indicators (e.g., monthly church attendance, belief in hell, etc.). With religion as an independent variable, they fi nd that belief in hell has a strongly positive effect on economic growth, whereas monthly religious service attendance has a strongly negative effect. Hilary and Hui (2009) use one of the same data sources as we use here to investigate the effect of individual religios-ity on the risk-taking behavior of fi rms. Using the rate of religious adher-ence at the county level from the Association of Religion Data Archives (the same ARDA data used in this paper), they fi nd that corporations located in highly religious counties take on less risk, measured by vari-ance in returns on equity and assets, and have higher returns on assets and lower rates of investment.

HYPOTHESES AND EMPIRICAL ANALYSIS We investigate the relationship between religious and ethnic diversity

and municipal bond yields. Municipal bond yields refl ect the costs that

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 7

5 A common assumption in capital markets is that rational arbitrageurs enforce price effi ciency. In the municipal context, an issuer who issued bonds cheap (at high yield) rela-tive to the eventual market equilibrium would cost taxpayers money. In private capital markets, the assumption is that such ineffi cient behavior will rapidly be competed away. In municipal capital markets, the same forces may be at play, but with municipal authorities enjoying (at least in the short run) something like a monopoly, this equilibrating process may take a very long time.

6 See note 4 regarding use of the Herfi ndahl index.

localities face when they borrow. In effi cient credit markets, yields refl ect a time premium, a risk premium, and a premium for the credit quality of the underlying issuer. Our empirical analysis controls for the time pre-mium using fi xed effects for the maturity of the instrument; because the risk-free yield curve fl uctuates over time, we allow these fi xed effects to be time-varying. With the time effect controlled for, and with an addi-tional control for the liquidity of the bond, in an effi cient capital market the resulting coeffi cients will refl ect the combined premium for risk and default charged to the municipal borrowers. Any part of this spread that is uncorrelated with the risk of the instrument will refl ect some ineffi ciency in the underlying issuance process. 5

Our main null hypothesis is that neither religious nor ethnic diversity (fractionalization), as measured by the Herfi ndahl index, has an impact on this premium charged; the alternative hypotheses are that either religious or ethnic diversity could affect the premium. The Herfi ndahl index is just one minus the ELF fractionalization measure, so our results can be thought of interchangeably in terms of concentration or diversity/fractionalization. 6

Establishing a relationship between ethnoreligious fractionalization and bond spreads, we continue by investigating the extent to which the relation-ship refl ects risk. Because our spread measures are based on regressions that have controlled for the yield curve and bond liquidity, we view the part that is orthogonal to risk (however measured) as being consistent with some ineffi ciency in the bond issuance process. As a shorthand, we refer to this as “monitoring,” but this monitoring is a residual that may refl ect many underlying sources. It may refl ect ineffi cient monitoring of the local offi cials—often treasurers—charged with issuing municipal debt. Whal-ley (2011) shows empirically that the background of local treasurers has a signifi cant impact on municipal borrowing costs—in particular, localities in California with appointed treasurers (who are often fi nance profession-als) have lower borrowing costs than localities that elect their treasurers. Any model in which local treasurers trade off effort versus job effective-ness, and where the local offi cials internalize only benefi ts that accrue to constituents of their own type, will deliver a relationship between frac-tionalization and municipal effectiveness—in this case, the spreads that municipalities pay on their bonds.

8 MUNICIPAL FINANCE JOURNAL

7 Splitting the Protestant denominations into Evangelical Protestant groups and Main-line Protestant groups follows general practice in working with the ARDA data. There are very important differences between these groups. For example, the belief in the literal inerrancy of the Bible is much more common among Evangelical Protestants than among Mainline Protestant Christians.

DATA AND ECONOMETRIC METHODOLOGY Data on religious observance and fractionalization come from the 2000

Religious Congregations and Membership Study, a survey conducted by the Association of Statisticians of American Religious bodies (ASARB). These data have also been used in Hilary and Hui (2009) and are available through the Association of Religion Data Archives (ARDA). The survey covered 149 Christian denominations, as well as Jewish and Islamic total adherents, by county. The survey also counted temples for six Eastern reli-gions, but not members. A number of churches, disproportionately his-torically African-American religious bodies, declined to participate in the survey in 2000; estimates of county-level membership counts described in Finke and Sheitle (2005) are used for these congregations.

The fractionalization measure (1—the Herfi ndahl index) is based on a division of religious bodies into eight groups. These groups are Mainline Protestant, Evangelical Protestant, Catholic, Eastern Orthodox, Other par-ticipating Christian groups (predominantly LDS [Mormon] congregations), and Jewish and Muslim congregations. The “Other non-participating” category captures the Finke and Sheitle (2005) county-level estimate of the count of adherents of denominations that did not participate. Table 1 describes the different denomination measures. The table presents results both on a bond-weighted and a county-weighted basis. Based on the sur-vey, religious membership amounts to 63% of the mean county population, with a standard deviation of 21%. The Mainline Protestant denominations have now been eclipsed in membership by the Evangelical Protestant denominations and Catholic churches. 7

Our goal with this eight-category religion division is to capture the strength or weakness of social ties within a locality.

Table 2 describes the adherent and dispersion measures for a hand-ful of counties. The counties presented are the largest counties, the most concentrated and fractionalized counties, and the most concentrated and fractionalized large counties. The most religiously homogeneous large county is Salt Lake County, Utah, where more than half of the popula-tion is in the “Other participating Christian” category, largely LDS con-gregations. El Paso, Texas; Bristol, Massachusetts; and Hidalgo, Texas, are also highly homogeneous in terms of religion and are predominantly Catholic. Highly religiously fractionalized counties include Montgomery

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 9

Table 1: Descriptive Statistics for County Religion Data

Count Mean 25th %ile.

50th %ile.

75th %ile. SD

Total members/1000 population

Bond 1207399 621.2 502.1 619.9 723.3 165

County 2023 628.3 477.3 621.8 772.5 207.2

Mainline ProtestantBond 1207399 112.5 60.8 88.9 136.6 83.8

County 2023 145.1 67.6 109.2 187.9 118.4

Evangelical Protestant

Bond 1207399 151.9 61.8 108.3 204.8 128.8

County 2023 228.6 95.6 175.7 346.2 168.7

CatholicBond 1207399 221.6 102.5 201.1 317.5 147.9

County 2023 138.7 22.6 92.5 205.6 146.6

OrthodoxBond 1207399 2.5 0.0 0.9 3.3 3.8

County 2023 0.7 0.0 0.0 0.0 2.7

Other participating Christiana

Bond 1207399 33.5 7.4 18.2 40.7 58.9

County 2023 20.5 0.1 5.9 14.8 75.2

Jewish Bond 1207399 16.4 0.0 2.9 18.2 32.5

County 2023 2.8 0.0 0.0 0.0 13.2

MuslimBond 1207399 4.3 0.0 1.4 6.2 6.3

County 2023 0.8 0.0 0.0 0.0 3.0

Other non-participating Christianb

Bond 1207399 99.2 59.2 78.2 116.4 64.5

County 2023 94.7 51.5 71.3 100.7 77.5

Religion Herfi ndahl (x 10000)c

Bond 1207399 3304 2650 3133 3685 912

County 2023 3880 3028 3584 4482 1161

Note: Table shows descriptive statistics based on 2000 Religious Congregations and Membership Study by the Association of Statisticians of American Religious Bodies (ASARB). Survey covered 149 religious bodies. Data were accessed from the Association of Religion Data Archives (ARDA) and are described at http://www.thearda.com/Archive/Files/Descriptions/RCMSCY.asp.a Other participating congregations are predominantly LDS (Mormon) congregations.b Other non-participating congregations include religious congregations that did not choose to participate in the 2000 survey. Count based on adjustments described in Finke and Sheitle, 2005 (“Accounting for the Uncounted: Computing Correctives for the 2000 RCMS Data”) to correct for non-participation of religious bodies that did not participate in the 2000 Survey. The bulk of the non-participating bodies (estimated at 25.10 million out of the 29.05 million non-participants are historically African-American congregations. The remainder include the Baptist Bible Fellowship (1.2 million estimated members), the Jehovah’s Witnesses (1.04 million estimated members), and other smaller groups.c Herfi ndahl = 1 – ELF. We use the Herfi ndahl and ELF measures interchangeably; a higher Herfi ndahl = less fractionalization.

10 MUNICIPAL FINANCE JOURNALTa

ble

2: R

elig

ious

Fra

ctio

naliz

atio

n fo

r Par

ticul

ar C

ount

ies

Cong

rega

nts/

1000

Pop

ulat

ion

Popu

la-

tion

Tota

lM

ainl

ine

Prot

es-

tant

Evan

g.

Prot

es-

tant

Cath

olic

Orth

odox

Othe

r (P

artic

i-pa

ting)

Jew

ish

Mus

lim

Othe

r (N

ot

Part

ici-

patin

g)

Herf

. In

dex

(x 1

0000

)

Larg

e cou

nties

Los A

ngele

s, CA

9519

338

771.

535

.661

.839

9.9

3.3

80.3

59.3

9.8

121.

531

90

Cook

, IL

5376

741

852.

253

.450

.239

9.3

9.4

64.0

43.6

17.8

214.

529

91

Harri

s, TX

3400

578

672.

681

.920

4.8

181.

92.

432

.810

.614

.014

4.2

2298

Mar

icopa

, AZ

3072

149

475.

748

.399

.917

2.6

2.3

74.4

19.5

3.3

55.4

2259

Oran

ge, C

A28

4628

954

1.1

38.7

79.6

273.

92.

553

.121

.113

.958

.340

26

Conc

entra

ted co

untie

s

Rich

, UT

1961

932.

90.

00.

00.

00.

084

9.1

0.0

0.0

83.8

8365

Arth

ur, N

E44

479

5.0

723.

00.

00.

00.

00.

00.

00.

072

.083

52

Bann

er, N

E81

913

9.8

127.

00.

00.

00.

00.

00.

00.

012

.883

35

Van

Bure

n, T

N55

0837

6.1

0.0

341.

50.

70.

00.

00.

00.

033

.983

23

Conc

entra

ted co

untie

s > 5

0000

0 po

pulat

ion

Salt

Lake

, UT

8983

8776

0.1

20.6

20.6

59.6

4.1

570.

24.

73.

976

.458

07

Brist

ol, M

A53

4678

696.

040

.425

.850

2.0

2.6

29.1

21.7

3.5

70.9

5381

El P

aso,

TX

6796

2272

8.9

25.6

75.3

514.

81.

317

.37.

40.

986

.352

54

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 11

Hida

lgo,

TX

5694

6356

3.1

28.2

73.4

390.

10.

211

.90.

91.

157

.351

05

Frac

tiona

lized

coun

ties

Mon

tgom

ery,

MD

8733

4177

4.6

100.

878

.821

2.0

6.1

128.

996

.021

.113

0.9

1746

Alex

andr

ia, V

A12

8283

730.

312

7.3

85.4

188.

316

.378

.542

.129

.516

2.9

1773

June

au, A

K30

711

345.

171

.781

.971

.631

.743

.59.

30.

035

.417

81

Was

hten

aw, M

I32

2895

442.

192

.364

.912

9.3

2.7

44.9

21.7

15.1

71.2

1905

Frac

tiona

lized

coun

ties >

500

000

popu

latio

n

Mon

tgom

ery,

MD

8733

4177

4.6

100.

878

.821

2.0

6.1

128.

996

.021

.113

0.9

1746

Pine

llas,

FL92

1482

445.

586

.399

.112

1.6

10.5

34.5

26.3

4.6

62.6

1914

Brow

ard,

FL

1623

018

730.

727

.077

.921

0.6

3.9

139.

113

1.2

4.1

136.

919

94

Palm

Bea

ch, F

L11

3118

483

3.8

47.1

91.5

265.

61.

715

3.3

147.

60.

712

6.3

2048

Note:

Tabl

e sho

ws d

escr

iptiv

e stat

istics

bas

ed o

n 20

00 R

eligi

ous C

ongr

egati

ons a

nd M

embe

rshi

p St

udy.

See n

otes

to Ta

ble 1

for d

escr

iptio

n of

the A

RDA

Relig

ious

Con

greg

ation

s and

Mem

bers

hip

Surv

ey o

n wh

ich th

is tab

le is

base

d.

12 MUNICIPAL FINANCE JOURNAL

County, Maryland, which has a relatively even split across Mainline Protestant, Evangelical Protestant, Catholic, LDS, Jewish, and other non-participating denominations.

Data on ethnicity come from the 2000 Census. Ethnicity and Hispanic identity are overlapping: households can report being Hispanic alongside any ethnicity. For the purposes of our analysis, we create a non-overlapping “Hispanic” category including all households that report Hispanic identity. Other categories, including black, white, American Indian, Asian, and Pacifi c Islander, are based on households that do not also report being Hispanic.

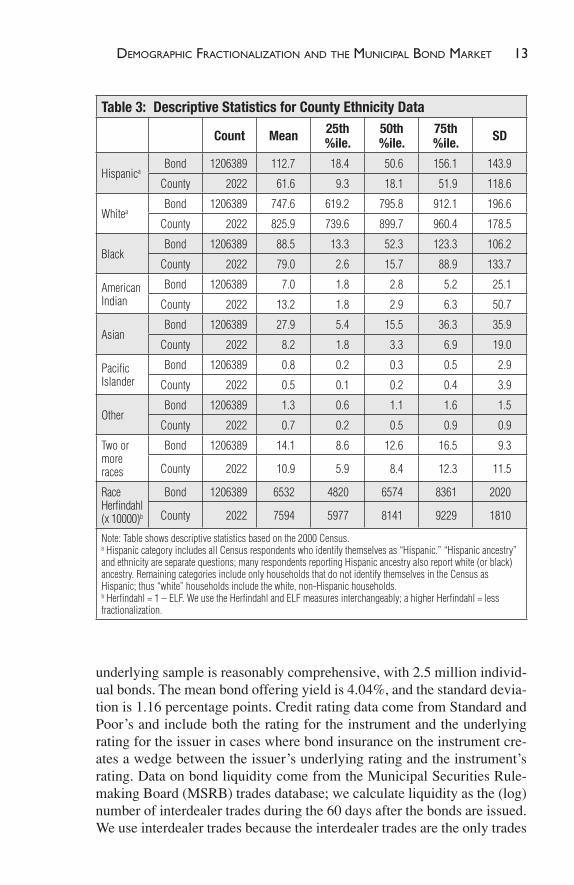

Table 3 presents descriptive statistics for county ethnicity data, again weighted by bond and weighted by county. The difference between the bond-weighted and county-weighted results refl ects the large number of sparsely populated, heavily white counties and the large share of the population that lives in some very large counties with large Hispanic pop-ulations. Table 4 presents ethnicity data and ethnic fractionalization for a handful of counties. The most ethnically fractionalized large counties include Alameda, California; Hudson, New Jersey; and San Francisco, California, which have Herfi ndahl indices below 3,159. This measure refl ects the fact that the odds that any two randomly selected citizens would be of the same ethnicity are less than one-third. There are a num-ber of highly concentrated small counties, in particular very white rural counties in Montana, North Dakota, South Dakota, and West Virginia. The ethnically homogeneous large counties include the heavily white Macomb, Michigan, and Bucks, Pennsylvania. Hidalgo County in Texas is relatively unusual in being a large and highly concentrated county with a predominantly Hispanic population.

We also use additional demographic data from the Census (see Table 5). We control for wealth and income using the median house value and median income in the county. Weighted by bond, the mean of the median county household income measures is $44,000; the mean of the median county home value measures is $123,000. Data on government debt and spend-ing come from the Census of Governments, 1992–2007. The Census of Governments is conducted every fi ve years by the U.S. Census and covers municipal revenues, expenditures, debt, assets, and numbers of employ-ees. These data include annual data on spending and receipts, at the county level, for all subunits within each county. We include total expenditure and total municipal indebtedness taken from the Census of Governments as controls in many of our empirical specifi cations. The average debt per capita is $3,873; the average expenditure per capita is $4,273.

Data on the municipal bond characteristics, issue date, and yield come from Mergent. Our sample includes all municipal bonds listed in Mer-gent that were issued between 1995 and 2010. Mergent also provides data capturing whether the municipal bonds are insured or uninsured. The

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 13

Table 3: Descriptive Statistics for County Ethnicity Data

Count Mean 25th %ile.

50th %ile.

75th %ile. SD

HispanicaBond 1206389 112.7 18.4 50.6 156.1 143.9

County 2022 61.6 9.3 18.1 51.9 118.6

WhiteaBond 1206389 747.6 619.2 795.8 912.1 196.6

County 2022 825.9 739.6 899.7 960.4 178.5

BlackBond 1206389 88.5 13.3 52.3 123.3 106.2

County 2022 79.0 2.6 15.7 88.9 133.7

American Indian

Bond 1206389 7.0 1.8 2.8 5.2 25.1

County 2022 13.2 1.8 2.9 6.3 50.7

AsianBond 1206389 27.9 5.4 15.5 36.3 35.9

County 2022 8.2 1.8 3.3 6.9 19.0

Pacifi c Islander

Bond 1206389 0.8 0.2 0.3 0.5 2.9

County 2022 0.5 0.1 0.2 0.4 3.9

OtherBond 1206389 1.3 0.6 1.1 1.6 1.5

County 2022 0.7 0.2 0.5 0.9 0.9

Two or more races

Bond 1206389 14.1 8.6 12.6 16.5 9.3

County 2022 10.9 5.9 8.4 12.3 11.5

Race Herfi ndahl (x 10000)b

Bond 1206389 6532 4820 6574 8361 2020

County 2022 7594 5977 8141 9229 1810

Note: Table shows descriptive statistics based on the 2000 Census.a Hispanic category includes all Census respondents who identify themselves as “Hispanic.” “Hispanic ancestry” and ethnicity are separate questions; many respondents reporting Hispanic ancestry also report white (or black) ancestry. Remaining categories include only households that do not identify themselves in the Census as Hispanic; thus “white” households include the white, non-Hispanic households.b Herfi ndahl = 1 – ELF. We use the Herfi ndahl and ELF measures interchangeably; a higher Herfi ndahl = less fractionalization.

underlying sample is reasonably comprehensive, with 2.5 million individ-ual bonds. The mean bond offering yield is 4.04%, and the standard devia-tion is 1.16 percentage points. Credit rating data come from Standard and Poor’s and include both the rating for the instrument and the underlying rating for the issuer in cases where bond insurance on the instrument cre-ates a wedge between the issuer’s underlying rating and the instrument’s rating. Data on bond liquidity come from the Municipal Securities Rule-making Board (MSRB) trades database; we calculate liquidity as the (log) number of interdealer trades during the 60 days after the bonds are issued. We use interdealer trades because the interdealer trades are the only trades

14 MUNICIPAL FINANCE JOURNALTa

ble

4: E

thni

city

Mix

for L

arge

Cou

ntie

s

Popu

latio

nHi

span

icW

hite

Blac

kAm

eric

an

Indi

anAs

ian

Paci

fi c

Isla

nder

Othe

rTw

o or

M

ore

Race

s

Herf

. In

dex

(x 1

0000

)

Larg

e cou

nties

Los A

ngele

s, CA

9519

338

445.

631

0.9

94.7

2.7

118.

12.

42.

123

.431

87

Cook

, IL

5376

741

199.

347

5.9

258.

61.

348

.00.

31.

415

.333

56

Harri

s, TX

3400

578

329.

342

1.2

182.

22.

150

.90.

41.

312

.632

18

Mar

icopa

, AZ

3072

149

248.

566

2.2

35.3

14.9

21.0

1.2

1.3

15.5

5025

Conc

entra

ted co

untie

s

Hand

, SD

3741

2.9

991.

40.

31.

30.

80.

00.

03.

298

30

Grig

gs, N

D27

544.

099

0.9

0.0

2.2

1.5

0.0

0.0

1.5

9820

Libe

rty, M

T21

581.

999

0.7

0.0

0.9

3.2

0.0

0.5

2.8

9816

Burk

e, ND

2242

3.6

990.

21.

32.

21.

30.

00.

01.

398

05

Conc

entra

ted co

untie

s > 5

0000

0

Mac

omb,

MI

7881

4915

.891

5.9

26.8

2.9

21.2

0.2

0.9

16.3

8406

Buck

s, PA

5976

3523

.491

1.5

31.7

1.0

22.7

0.1

0.8

8.4

8329

Ocea

n, N

J51

0916

50.0

898.

728

.21.

012

.60.

10.

88.

481

13

Brist

ol, M

A53

4678

36.0

893.

918

.31.

912

.50.

217

.020

.280

15

Hida

lgo,

TX

5694

6388

3.5

104.

33.

40.

85.

60.

00.

32.

079

14

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 15

Frac

tiona

lized

coun

ties

Hawa

ii, H

I14

8677

94.9

297.

44.

03.

225

8.1

105.

51.

823

4.9

2305

Mau

i, HI

1280

9478

.531

9.4

3.8

2.7

302.

910

2.8

1.6

188.

224

60

Kaua

i, HI

5846

382

.227

8.5

2.8

2.4

349.

186

.81.

419

6.8

2525

Alam

eda,

CA14

4374

118

9.7

409.

414

6.2

3.7

202.

75.

93.

239

.126

77

Robe

son,

NC

1233

3948

.630

8.1

249.

937

6.7

3.1

0.4

1.6

11.6

3018

Frac

tiona

lized

coun

ties >

500

000

Alam

eda,

CA14

4374

118

9.7

409.

414

6.2

3.7

202.

75.

93.

239

.126

77

Huds

on, N

J60

8975

397.

635

3.4

121.

61.

592

.60.

36.

027

.030

71

San

Fran

cisco

, CA

7767

3314

1.0

436.

375

.72.

630

6.6

4.6

3.3

29.8

3109

New

York

, NY

1537

195

271.

845

7.9

152.

71.

693

.20.

43.

618

.831

59

Note:

Tabl

e sho

ws d

escr

iptiv

e stat

istics

bas

ed o

n th

e 200

0 Ce

nsus

.

16 MUNICIPAL FINANCE JOURNALTa

ble

5: S

umm

ary

Stat

istic

s, A

ll Va

riabl

es (W

eigh

ted

by b

ond)

Perc

entil

e

Varia

ble

Sour

ceCo

unt

Mea

nSt

anda

rd

Devi

atio

n25

th50

th75

th

Bond

offe

ring

yield

Mer

gent

1902

459

4.04

1.16

3.50

4.15

4.79

Bond

insu

ranc

e dum

my

Mer

gent

1902

459

0.51

0.50

0.00

1.00

1.00

Com

petit

ive b

iddi

ngM

erge

nt19

0245

90.

220.

420.

000.

000.

00

Nego

tiated

offe

rM

erge

nt19

0245

90.

270.

440.

000.

001.

00

Bond

size

($00

0)M

erge

nt18

7197

624

03.3

725

907.

0016

5.00

425.

0012

65.0

0

Issue

size

($00

0)M

erge

nt19

0245

943

385.

0019

0270

.00

3435

.00

8915

.00

2693

0.00

Coun

t of i

nter

deale

r tra

des i

n fi r

st 60

day

sM

SRB

1902

459

2.97

11.9

20.

001.

002.

00

LTCR

S&P

9880

633.

622.

331.

003.

005.

00

SPUR

S&P

8015

644.

252.

233.

004.

006.

00

Relig

ion

Herfi

ndah

lAR

DA12

0739

933

0491

226

5031

3336

85

Relig

ion:

Mem

ber h

ouse

hold

s/10

00AR

DA12

0739

964

218

051

563

475

3

Ethn

icity

Herfi

ndah

lCe

nsus

1206

389

6532

2020

4820

6574

8361

Ethn

icity:

Whi

te ho

useh

olds

/100

0Ce

nsus

1206

389

748

197

619

796

912

Med

. hou

se va

l. ($

000)

Cens

us12

0638

912

265

8210

214

7

Med

ian in

com

e ($0

00)

Cens

us12

0638

944

1137

4349

Log

total

pop

ulati

onCe

nsus

1206

389

12.3

11.

6511

.07

12.3

813

.53

LTD

per c

apita

($00

0)Ce

nsus

of

govts

., Ce

nsus

1206

389

3.90

5.30

1.90

2.90

4.50

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 17

Govt.

exp.

per

capi

ta ($

000)

Cens

us o

f go

vts.,

Cens

us12

0638

94.

304.

403.

003.

704.

50

Butle

r-Fau

ver-M

ortal

Cor

rupt

ion

mea

sure

1a

BFM

(200

9)16

4014

423

.07

24.9

70.

0014

.27

45.8

0

Butle

r-Fau

ver-M

ortal

Cor

rupt

ion

mea

sure

2a

BFM

(200

9)16

4014

421

.29

13.8

89.

0018

.00

33.0

0

Popu

latio

n pe

rcen

t cha

nge (

past

5 ye

ars)

SEER

b12

0278

00.

060.

080.

010.

040.

09

Chan

ge in

whi

te sh

are (

past

5 ye

ars)

SEER

12

0278

0–0

.02

0.02

–0.0

3–0

.02

–0.0

1

Chan

ge in

race

Her

fi nda

hl (p

ast 5

year

s)SE

ER

1202

780

–0.0

30.

02–0

.04

–0.0

2–0

.01

Top

feder

al tax

rate

NBER

c16

4014

435

.79

2.57

33.5

235

.35

38.0

0

Top

state

tax ra

teM

erge

nt16

4014

45.

073.

213.

005.

697.

50

Top

total

tax r

ateM

erge

nt16

4014

440

.87

3.01

38.7

940

.79

42.8

4

Unem

ploy

men

t rate

LA

USd

1206

389

5.55

2.35

4.00

5.10

6.50

Stan

dard

dev

iatio

n of

une

mpl

oym

ent r

ateLA

US12

0638

91.

690.

671.

291.

591.

98

Bond

calla

ble

Mer

gent

1902

459

0.44

0.50

0.00

0.00

1.00

GO B

ond

Mer

gent

1902

459

0.47

0.50

0.00

0.00

1.00

Bond

put

able

Mer

gent

1902

459

0.00

0.04

0.00

0.00

0.00

Bond

subj

ect t

o AM

TM

erge

nt19

0245

90.

030.

160.

000.

000.

00

Taxa

ble b

ond

Mer

gent

1902

459

0.04

0.19

0.00

0.00

0.00

Bond

taxa

ble a

t stat

e lev

elM

erge

nt19

0245

90.

080.

260.

000.

000.

00

Refu

ndin

g bo

ndM

erge

nt19

0245

90.

370.

480.

000.

001.

00a B

FM co

rrupt

ion

mea

sure

1 is

the s

hare

of q

uarte

rs in

whi

ch th

e stat

e is i

n th

e top

qua

rtile

of st

ates i

n ter

ms o

f cor

rupt

ion

conv

ictio

ns p

er ca

pita.

BFM

corru

ptio

n m

easu

re 2

is th

e Bett

er G

over

nmen

t As

socia

tion’s

corru

ptio

n ra

nkin

g fo

r the

state

.b S

EER

is th

e Sur

veill

ance

, Epi

dem

iolo

gy, a

nd E

nd R

esul

ts su

rvey

, a p

rogr

am o

f the

Nati

onal

Canc

er In

stitu

te. S

EER

publ

ishes

annu

al es

timate

s of c

ount

y pop

ulati

on ra

cial b

reak

down

s.c N

BER

is th

e Nati

onal

Bure

au o

f Eco

nom

ic Re

sear

ch. N

BER

publ

ishes

annu

al sta

te-lev

el tax

rates

.d L

AUS

stand

s for

the B

urea

u of

Lab

or S

tatist

ics’ L

ocal

Area

Une

mpl

oym

ent S

tatist

ics d

ataba

se.

18 MUNICIPAL FINANCE JOURNAL

8 As noted in footnote 4, the ethnolinguistic fractionalization (ELF) measure is just 1 – the Herfi ndahl index, so we use the Herfi ndahl measure in our analysis and interpret the coeffi cient estimates as refl ecting the impact of a declining degree of fractionalization.

available in the 1995–1997 subperiod, and we use the fi rst 60 days post-issuance in order to have a consistent window for all of the bonds issued in our sample. In our sample, the mean number of interdealer trades is 1, and the mean is 2.98. In calculating the log, we fi rst add 1 to the count of trades.

We also use data on state-level corruption from Butler, Fauver, and Mortal (2009). We use two corruption measures: the fi rst is the share of calendar quarters in which the state was in the top quartile of states in terms of corruption convictions per capita. The second measure is the Better Government Association’s corruption ranking for the state. We also use time-varying ethnic diversity measures taken from the Surveillance, Epidemiology, and End Results (SEER) survey, which has annual mea-sures back to 1990. Instrumental variables analysis uses 1980 Census data to create instruments for the 2000 fractionalization and white share mea-sures; 1980 is the earliest Census that allows for construction of ethnicity measures including Hispanic origin.

We also construct measures of county population growth from the SEER data, and tax rate measures come from the National Bureau of Economic Research (NBER). Finally, measures of county-level unemployment and unemployment volatility come from the Bureau of Labor Statistics, through their local area unemployment statistics (LAUS) program.

RESULTS OF THE ANALYSIS This section presents the empirical results of our analysis of both ethnic

and religious fractionalization, as measured by the respective Herfi ndahl indices, 8 and their effects on municipal credit markets. The fi rst subsec-tion looks at the relationship between municipal bond yields and mea-sures of fractionalization. The second subsection addresses the question of whether the higher bond yields in more fractionalized counties refl ect risk or monitoring.

Fractionalization and Municipal Bond Yields Our fi rst specifi cation (Table 6) fi ts the bond offering yield on measures

of ethnic and religious fractionalization using a minimal set of controls. These controls include log county size, log issue size, log bond size, and maturity-by-month dummy variables. The maturity-by-month dummy variables allow for a nonparametric time-varying yield curve effect and allow us to interpret the resulting coeffi cients in terms of spreads over a

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 19

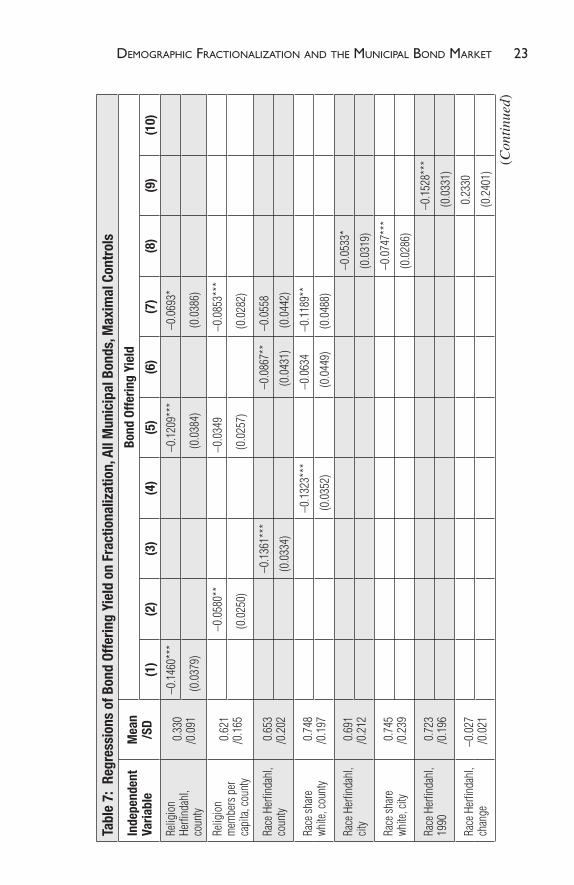

benchmark yield curve. The main independent variable in column (1) is the religion Herfi ndahl index, which has a coeffi cient of –0.3025. This result is highly signifi cant in both statistical and economic terms: a two standard deviation increase in fractionalization would be associated with a six basis point increase in bond spreads. To put this increase into con-text, Figure 1 shows the relationship between credit ratings and spreads during our sample period: moving from an AAA-rated instrument to an AA–instrument, a move of four ratings notches, is associated with an eight basis point increase in yields.

Column (2) controls for total religious observance, using the members per capita variable. The variable is not statistically signifi cant in this speci-fi cation, although it becomes signifi cant with the broader set of controls used in Table 7. Column (3) uses the ethnicity Herfi ndahl index. The coef-fi cient of –0.2435 suggests that a two standard deviation increase in frac-tionalization is associated with a 10 basis point increase in bond yields. Column (4) uses the “share white” and fi nds an effect of similar economic and statistical magnitude.

Column (5) controls for the religious variables together, column (6) for the ethnicity variables together, and column (7) for all four variables in the same regression. The religious Herfi ndahl measure is consistently sig-nifi cant, as is the share of county population that is white. In regressions where ethnic fractionalization is measured at the county level, including

Figure 1: Coeffi cients from Regression of Bond Yield on Rating

20 MUNICIPAL FINANCE JOURNALTa

ble

6: R

egre

ssio

ns o

f Bon

d Of

ferin

g Yi

eld

on F

ract

iona

lizat

ion,

All

Mun

icip

al B

onds

, Min

imal

Con

trol

s

Inde

pend

ent

Varia

ble

Mea

n/S

DBo

nd O

fferin

g Yi

eld

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Relig

ion

Herfi

ndah

l, co

unty

0.33

0/0

.091

–0.3

025*

**–0

.284

4***

–0.3

279*

**

(0.0

713)

(0.0

815)

(0.0

783)

Relig

ion

mem

bers

per

ca

pita,

coun

ty

0.62

1/0

.165

–0.0

687

–0.0

343

–0.0

723

(0.0

561)

(0.0

576)

(0.0

545)

Race

Her

fi nda

hl,

coun

ty0.

653

/0.2

02–0

.243

5***

–0.0

370

0.05

60

(0.0

395)

(0.0

609)

(0.0

626)

Race

shar

e whi

te,

coun

ty0.

748

/0.1

97–0

.266

7***

–0.2

390*

**–0

.337

7***

(0.0

376)

(0.0

575)

(0.0

615)

Race

Her

fi nda

hl,

city

0.69

1/0

.212

–0.1

656*

**

(0.0

442)

Race

shar

e whi

te,

city

0.74

5/0

.239

–0.1

929*

**

(0.0

343)

Race

Her

fi nda

hl,

1990

, cou

nty

0.72

3/0

.196

–0.2

467*

**

(0.0

382)

Race

Her

fi nda

hl,

chan

ge o

ver p

ast

5 ye

ars,

coun

ty

–0.0

27/0

.021

0.47

71*

(0.2

447)

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 21

Race

shar

e whi

te,

1990

, cou

nty

0.80

7/0

.175

–0.2

678*

**

(0.0

408)

Race

shar

e whi

te,

chan

ge p

ast 5

yrs

–0.0

24/0

.018

–0.5

072

(0.4

962)

Addi

tiona

l con

trol v

ariab

les: L

og co

unty

size,

log

issue

size

, log

bon

d siz

e, m

aturit

y-by

-mon

th d

umm

ies

Obse

rvati

ons

1189

975

1189

975

1189

995

1189

995

1189

975

1189

995

1189

975

7038

8311

8496

911

8496

9

R-sq

uare

d0.

8126

0.81

220.

8130

0.81

340.

8126

0.81

340.

8141

0.81

650.

8133

0.81

32

Robu

st sta

ndar

d er

rors

in p

aren

thes

es

Note:

Dep

ende

nt va

riabl

e is b

ond

offer

ing

yield

. Sam

ple i

nclu

des a

ll m

unici

pal d

ebt i

ssue

s tha

t can

be m

appe

d to

coun

ty da

ta. E

xclu

ded

woul

d be

state

and

supr

a-co

unty

bond

s. Ci

ties t

hat c

ross

co

unty

boun

darie

s are

assig

ned

to th

e cou

nty w

ith th

e lar

gest

num

ber o

f zip

code

s. St

anda

rd er

rors

are c

luste

red

by co

unty.

* Sig

nifi c

ant a

t 10%

; ** s

igni

fi can

t at 5

%; *

** si

gnifi

cant

at 1

%.

22 MUNICIPAL FINANCE JOURNAL

both ethnic fractionalization and the share white delivers a signifi cant coeffi cient on the share white variable and an insignifi cant coeffi cient on the fractionalization variable.

Column (8) uses city-level data. This approach leads to a smaller sample but also allows us to control for demographic characteristics at a fi ner level. In particular, although the ethnically homogeneous counties are almost exclusively white, there are ethnically homogeneous cities of each of several races. In the city-level specifi cation, both the fractionalization and share white measures are statistically signifi cant. Columns (9) and (10) use the SEER annual data to calculate measures of ethnic diversity from 1990, fi ve years before the start of the sample. The results suggest that the preexisting fractionalization and share white measures are corre-lated with bond yields. Although predetermination does not automatically imply causation, the fact that the 1990 ethnicity measures are correlated with bond yields does allow us to rule out potential competing stories where bond yields in the 1995–2010 sample are causing the differences in ethnic diversity measures.

Table 7 uses a richer set of control variables, including detailed control for the characteristics of the bond and also the county. While the magnitude of the results is attenuated somewhat with this richer set of controls, the broad picture of the results is not affected. In column (1), which includes the full set of controls but only the religion Herfi ndahl index among the measures of fractionalization, the coeffi cient of –0.1460 implies that a two standard deviation change in religious fractionalization is associated with a three basis point change in bond yields. The coeffi cient on the ethnic Herfi ndahl index in column (3) suggests that a two standard deviation change in fractionalization is associated with a fi ve basis point change in bond yields.

Table 8 shows the coeffi cients on the controls. These coeffi cients are interesting in their own right and also allow us to place the magnitude of the coeffi cients of our diversity measures into context. The coeffi cient of –0.5948 on median county house values suggests that a two standard devi-ation change in house values is associated with a 7.7 basis point change in bond yields. With controls for both county debt and expenditures, an interesting pattern emerges. The coeffi cient on county debt per capita is signifi cant at the 10% confi dence level and has a negative sign, suggesting that a two standard deviation change in debt outstanding is associated with a two basis point change in bond yields. A two standard deviation increase in county expenditures is associated with a nine basis point increase in bond yields. This pattern of results suggests that county borrowing costs are more highly correlated with expenditure levels than with the debt outstanding.

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 23

Tabl

e 7:

Reg

ress

ions

of B

ond

Offe

ring

Yiel

d on

Fra

ctio

naliz

atio

n, A

ll M

unic

ipal

Bon

ds, M

axim

al C

ontr

ols

Inde

pend

ent

Varia

ble

Mea

n/S

DBo

nd O

fferin

g Yi

eld

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Relig

ion

Herfi

ndah

l, co

unty

0.33

0/0

.091

–0.1

460*

**–0

.120

9***

–0.0

693*

(0.0

379)

(0.0

384)

(0.0

386)

Relig

ion

mem

bers

per

ca

pita,

coun

ty

0.62

1/0

.165

–0.0

580*

*–0

.034

9–0

.085

3***

(0.0

250)

(0.0

257)

(0.0

282)

Race

Her

fi nda

hl,

coun

ty0.

653

/0.2

02–0

.136

1***

–0.0

867*

*–0

.055

8

(0.0

334)

(0.0

431)

(0.0

442)

Race

shar

e wh

ite, c

ount

y0.

748

/0.1

97–0

.132

3***

–0.0

634

–0.1

189*

*

(0.0

352)

(0.0

449)

(0.0

488)

Race

Her

fi nda

hl,

city

0.69

1/0

.212

–0.0

533*

(0.0

319)

Race

shar

e wh

ite, c

ity0.

745

/0.2

39–0

.074

7***

(0.0

286)

Race

Her

fi nda

hl,

1990

0.72

3/0

.196

–0.1

528*

**

(0.0

331)

Race

Her

fi nda

hl,

chan

ge–0

.027

/0.0

210.

2330

(0.2

401)

(Con

tinu

ed)

24 MUNICIPAL FINANCE JOURNALTa

ble

7 (C

ontin

ued)

Inde

pend

ent

Varia

ble

Mea

n/S

DBo

nd O

fferin

g Yi

eld

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

Race

shar

e wh

ite, 1

990,

co

unty

0.80

7/0

.175

–0.1

261*

**

(0.0

397)

Race

shar

e wh

ite, c

hang

e pa

st 5

yrs

–0.0

24/0

.018

–0.4

811*

(0.2

895)

Addi

tiona

l con

trol v

ariab

les: C

ount

y size

, iss

ue si

ze, b

ond

size,

bond

trad

e cou

nt in

fi rs

t 60

days

(all

in lo

gs),

coun

ty m

edian

hou

se p

rice,

coun

ty m

edian

inco

me,

coun

ty go

vern

men

t deb

t and

expe

nditu

re p

er ca

p, B

FM co

rrupt

ion

mea

sure

s 1 an

d 2,

com

petit

ive is

sue,

nego

tiated

issu

e, bo

nd in

sura

nce d

umm

y, GO

dum

my,

calla

ble d

umm

y, pu

table

dum

my,

AMT

tax d

umm

y, tax

able

dum

my,

state-

tax d

umm

y, sta

te to

p tax

rate,

state

shar

e of h

ouse

hold

s with

inco

me >

200

k, co

unty

popu

latio

n gr

owth

(5 ye

ar),

coun

ty un

em-

ploy

men

t rate

, cou

nty s

tanda

rd d

eviat

ion

of u

nem

ploy

men

t rate

s, re

fund

ing

bond

dum

my,

matu

rity-

by-m

onth

dum

mies

.

Obse

rvati

ons

1186

441

1186

441

1186

461

1186

461

1186

441

1186

461

1186

441

7021

6711

8496

911

8496

9

R-sq

uare

d

0.87

990.

8799

0.88

000.

8800

0.87

990.

8801

0.88

020.

8851

0.88

010.

8800

Robu

st sta

ndar

d er

rors

in p

aren

thes

es

Note:

Dep

ende

nt va

riabl

e is b

ond

offer

ing

yield

. Sam

ple i

nclu

des a

ll m

unici

pal d

ebt i

ssue

s tha

t can

be m

appe

d to

coun

ty da

ta. E

xclu

ded

woul

d be

state

and

supr

a-co

unty

bond

s. Ci

ties t

hat c

ross

co

unty

boun

darie

s are

assig

ned

to th

e cou

nty w

ith th

e lar

gest

num

ber o

f zip

code

s. St

anda

rd er

rors

are c

luste

red

by co

unty.

* Sig

nifi c

ant a

t 10%

; ** s

igni

fi can

t at 5

%; *

** si

gnifi

cant

at 1

%.

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 25

Tabl

e 8:

Reg

ress

ions

of B

ond

Offe

ring

Yiel

d on

Fra

ctio

naliz

atio

n, A

ll M

unic

ipal

Bon

ds

Ind.

Var

. M

ean

/SD

Coef

.In

d. V

ar.

Mea

n/S

DCo

ef.

Ind.

Var

. M

ean

/SD

Coef

.

Relig

ion

Herfi

ndah

l, co

unty

0.33

0/0

.091

–0.0

693*

Com

petit

ive

issue

0.22

4/0

.417

–0.1

215*

**Re

fund

ing

bond

0.37

0/0

.483

–0.0

085

(0.0

386)

(0.0

090)

(0.0

054)

Relig

ion

mem

bers

per

ca

pita,

coun

ty0.

621

/0.1

65–0

.085

3***

Nego

tiated

issu

e0.

265

/0.4

410.

0598

***

Cons

tant

1.00

0/0

.000

4.

6654

***

(0.0

282)

(0.0

090)

(0.1

420)

Race

Her

fi nda

hl,

coun

ty0.

653

/0.2

02–0

.055

8Bo

nd in

sura

nce

dum

my

0.57

6/0

.494

–0.1

851*

**Ob

serv

ation

s11

8644

1

(0.0

442)

(0.0

124)

R-sq

uare

d0.

8802

Race

shar

e whi

te,

coun

ty0.

748

/0.1

97–0

.118

9**

Calla

ble b

ond

dum

my

0.44

2/0

.497

0.07

05**

*

(0.0

488)

(0.0

108)

Log

coun

ty po

pulat

ion

12.3

06/1

.650

0.00

71GO

bon

d du

mm

y0.

472

/0.4

99–0

.121

3***

(0.0

054)

(0.0

101)

Log

issue

size

16.0

90/1

.724

–0.0

221*

**Pu

table

bond

du

mm

y0.

001

/0.0

38–0

.733

0***

(0.0

028)

(0.1

217)

Log

bond

size

13

.081

/1.6

07–0

.019

6***

AMT

taxab

le 0.

028

/0.1

640.

2560

***

(0.0

039)

(0.0

174)

Log

bond

trad

e cou

nt0.

740

/0.9

22–0

.004

2**

Taxa

ble

0.03

8/0

.192

1.41

28**

*

(0.0

020)

(0.0

170)

(Con

tinu

ed)

26 MUNICIPAL FINANCE JOURNALTa

ble

8 (C

ontin

ued)

Ind.

Var

. M

ean

/SD

Coef

.In

d. V

ar.

Mea

n/S

DCo

ef.

Ind.

Var

. M

ean

/SD

Coef

.

Med

ian co

unty

hous

e va

lue

0.12

2/0

.065

–0.5

948*

**St

ate ta

xabl

e0.

076

/0.2

640.

0119

(0.1

511)

(0.0

104)

Med

ian co

unty

inco

me

0.04

4/0

.011

0.16

08St

ate to

p tax

rate

40.8

68/3

.011

0.00

24

(0.8

247)

(0.0

029)

Coun

ty go

vt. d

ebt/

capi

ta0.

004

/0.0

06

–1.9

207*

State

shar

e of

high

-inco

me

hous

ehol

ds

0.02

3/0

.009

0.57

05

(1.1

102)

(0.9

383)

Coun

ty go

vt. ex

p./

capi

ta0.

004

/0.0

058.

8465

***

Coun

ty po

pula-

tion

chan

ge0.

062

/0.0

800.

2475

***

(1.8

132)

(0.0

693)

BFM

corru

ptio

n m

easu

re 1

23.0

73/2

4.96

5–0

.000

6***

Coun

ty un

em-

ploy

men

t rate

5.55

2/2

.354

0.01

86**

*

(0.0

001)

(0.0

019)

BFM

corru

ptio

n m

easu

re 2

21.2

88/1

3.87

90.

0010

***

Coun

ty un

em-

ploy

men

t S.D

.1.

692

/0.6

66–0

.027

1***

(0.0

004)

(0.0

065)

Note:

Dep

ende

nt va

riabl

e is b

ond

offer

ing

yield

. Sam

ple i

nclu

des a

ll m

unici

pal d

ebt i

ssue

s tha

t can

be m

appe

d to

coun

ty da

ta. E

xclu

ded

woul

d be

state

and

supr

a-co

unty

bond

s. Ci

ties t

hat c

ross

co

unty

boun

darie

s are

assig

ned

to th

e cou

nty w

ith th

e lar

gest

num

ber o

f zip

code

s. St

anda

rd er

rors

are c

luste

red

by co

unty.

Matu

rity-

by-m

onth

dum

my v

ariab

les in

clude

d in

the r

egre

ssio

n.

DEMOGRAPHIC FRACTIONALIZATION AND THE MUNICIPAL BOND MARKET 27

Focusing on the corruption measures from the Butler, Fauver, and Mor-tal (2009) paper, the coeffi cients are statistically signifi cant and have the expected signs. With each coeffi cient, a two standard deviation change in the corruption measure is associated with a three basis point change in bond yields. The fact that our fractionalization measures continue to be signifi cant once the Butler et al. corruption measures are included suggests that the local fractionalization measures are capturing some effect that is orthogonal to those authors’ measures of corruption.

Counties with higher rates of population increase appear to borrow at higher rates, once we have controlled for county-level economic activity. Like our fractionalization measures, the rate of population increase can be viewed as a proxy for the strength of social networks within an area. If social networks take time to build, a population of recent arrivals will have weaker ties than a population that has been more static. County unemploy-ment rates are positively associated with borrowing costs.