Deloitte Shared Services, GBS & BPO Conferences3-eu-west-1.amazonaws.com/deloitte-conf-2015/... ·...

16

14-15 September 2016 Lisbon, Portugal Deloitte Shared Services, GBS & BPO Conference Plenary 3A: AstraZeneca – The case for functional shared services Tony Glynn, AstraZeneca

Transcript of Deloitte Shared Services, GBS & BPO Conferences3-eu-west-1.amazonaws.com/deloitte-conf-2015/... ·...

14-15 September 2016

Lisbon, Portugal

Deloitte Shared Services, GBS & BPO Conference

Plenary 3A: AstraZeneca – The case for functional shared servicesTony Glynn, AstraZeneca

The case for Functional Shared Services…

…or is it?

Tony Glynn

Deloitte Shared Services, Business Services and BPO Conference

September 2016

0

10

20

30

40

50

60

70

80

90

1 2 3 4 5 6 7

Popularity Index

Introduction

Share

mistakes

Brexit

Poll

Coffee Break

Tony Glynn

• Ernst & Young

• AstraZeneca 1994-2016

o Currently UK CFO

o Previously VP Global

Finance Services

• Shared Service advisory /

Non-Executive work

• Enjoys…Cycling, Running

and Lake District

4

$24.7bn total

revenue

$23.6bn product

sales

$1.1bn externalisation

revenue

As at 31 December 2015

5

61,500 employees

Over 500collaborations and

partnerships globally

Manufacturing in 17countries

$5.6bn invested in

R&D with research

across 5 countries

15 new medical

entities in late-stage

development

Global dimensions

We push the boundaries of science to deliver

life-changing medicines.

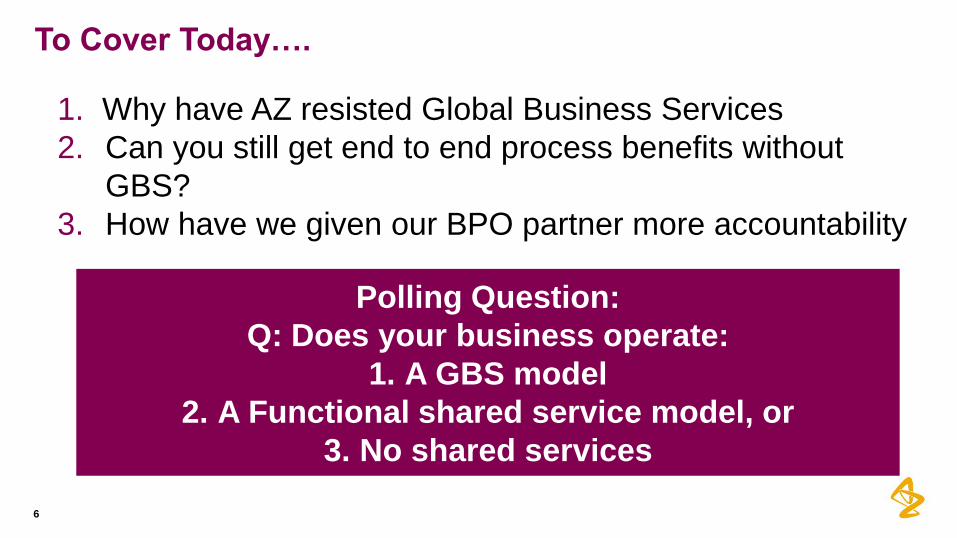

To Cover Today….

6

1. Why have AZ resisted Global Business Services

2. Can you still get end to end process benefits without

GBS?

3. How have we given our BPO partner more accountability

Polling Question:

Q: Does your business operate:

1. A GBS model

2. A Functional shared service model, or

3. No shared services

1. Why have AZ resisted Global Business Services?

7

2014• Business rationale compelling….but

• No burning platform, and

• Our functional track record was mixed…

2016• Business shape necessitates change

• Improving service and confidence

• Executive sponsorship

• GBS Council set up to explore

Yeah….but

no….but

yeah….but no

8

A Functional Strategy does bring its own problems…..

2. …But, a lack

of GBS has not

been all bad.

Finance

IT – 2016 plan

Procurement

HR

Commercial

Regulatory

Affairs

1. Independent

strategies are

creating a

complex Shared

Service Centre

landscape

GFS KL

GFS EMEA

GFS America

Genpact

Lublin

Genpact Cluj

Genpact Delhi

Genpact

Guatemala

Genpact Sao Paolo

GTC Chennai:

Computacenter

Barcelona

Genpact Hyderabad

FTE: 41

Infosys Bangalore

AZ Americas

AZ EMEA

AZ APAC

NGA, Buenos Aires

NGA, Grenada

NGA, Katowice

NGA, Manila

NGA, Dalian

Genpact Hyderabad

FTE: 41

Genpact Delhi

Accenture, Mumbai

Cognizant, Delhi

Accenture, Warsaw

Accenture, Hyderabad

Indigene, Bangalore

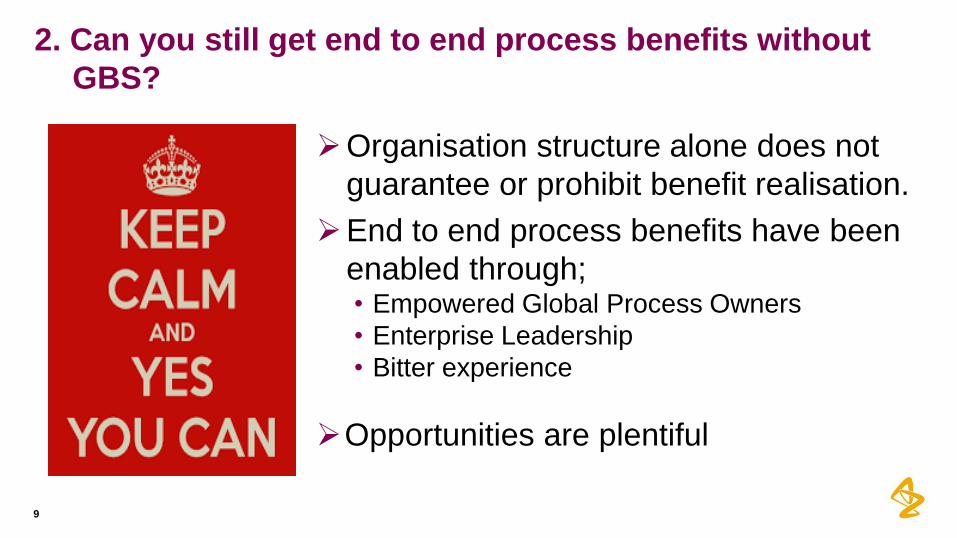

Organisation structure alone does not

guarantee or prohibit benefit realisation.

End to end process benefits have been

enabled through;• Empowered Global Process Owners

• Enterprise Leadership

• Bitter experience

Opportunities are plentiful

9

2. Can you still get end to end process benefits without

GBS?

10

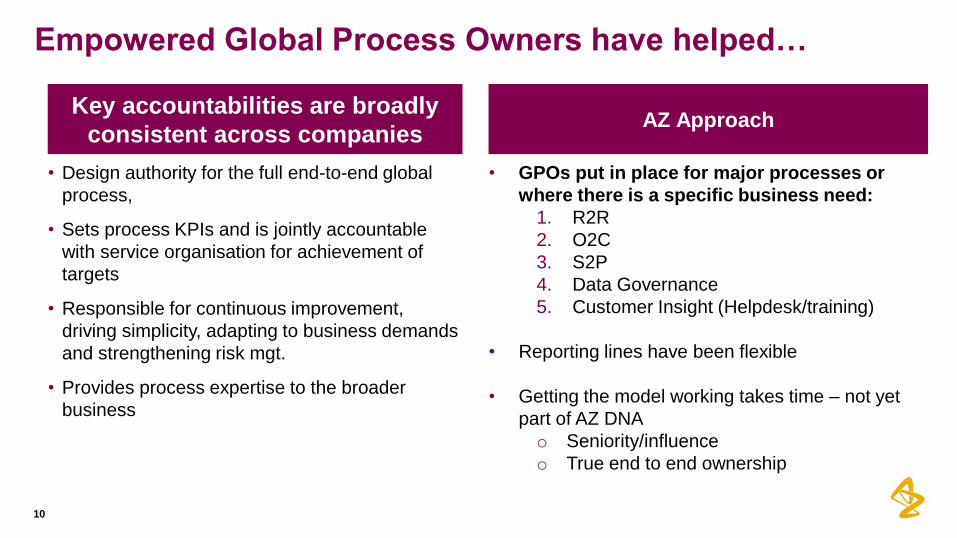

Empowered Global Process Owners have helped…

Key accountabilities are broadly

consistent across companies

• Design authority for the full end-to-end global

process,

• Sets process KPIs and is jointly accountable

with service organisation for achievement of

targets

• Responsible for continuous improvement,

driving simplicity, adapting to business demands

and strengthening risk mgt.

• Provides process expertise to the broader

business

AZ Approach

• GPOs put in place for major processes or

where there is a specific business need:

1. R2R

2. O2C

3. S2P

4. Data Governance

5. Customer Insight (Helpdesk/training)

• Reporting lines have been flexible

• Getting the model working takes time – not yet

part of AZ DNA

o Seniority/influence

o True end to end ownership

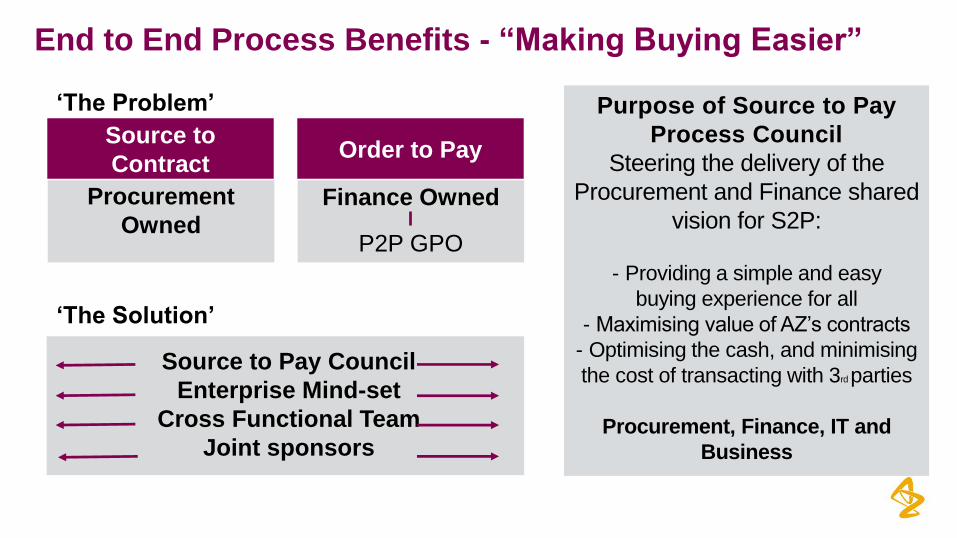

Source to

ContractOrder to Pay

Procurement

OwnedFinance Owned

P2P GPO

‘The Problem’

‘The Solution’

Source to Pay Council

Enterprise Mind-set

Cross Functional Team

Joint sponsors

Purpose of Source to Pay

Process Council

Steering the delivery of the

Procurement and Finance shared

vision for S2P:

- Providing a simple and easy

buying experience for all

- Maximising value of AZ’s contracts

- Optimising the cash, and minimising

the cost of transacting with 3rd parties

Procurement, Finance, IT and

Business

End to End Process Benefits - “Making Buying Easier”

12

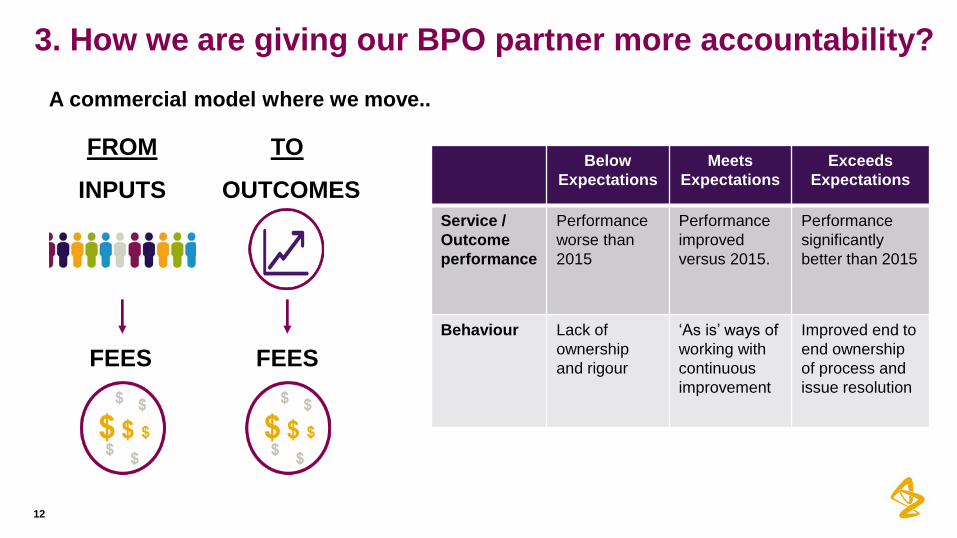

A commercial model where we move..

FROM

INPUTS

FEES

OUTCOMES

TO

FEES

Below

Expectations

Meets

Expectations

Exceeds

Expectations

Service /

Outcome

performance

Performance

worse than

2015

Performance

improved

versus 2015.

Performance

significantly

better than 2015

Behaviour Lack of

ownership

and rigour

‘As is’ ways of

working with

continuous

improvement

Improved end to

end ownership

of process and

issue resolution

3. How we are giving our BPO partner more accountability?

13

• Relatively few outcome measures to drive focus on key areas;– Balance Sheet Quality, Cash, Payment Process, Helpdesk, Engagement

Desired Outcome Outcome

Charge

Outcome Measure Base Charge Base Measure

Improve Helpdesk

quality

50% Customer

Satisfaction score• Below 50%

• Meets 100%

• Exceeds 125%

50% Queries resolved in SLA, First

Time Resolution

• This is a journey….– Two major change management exercises

– Are outcomes and measures the right ones

– Suppliers are aware of the trend to paying for outcomes

3. How we are giving our BPO partner more accountability?

• Service Desk

NOTE: FIGURES ARE ILLUSTRATIVE

Conclusions

The journey to GBS is not straightforward – there are pre-requisites• Executive Support, consistent service delivery etc…

End to End process improvements can still be achieved• GPOs and enterprise leadership key

BPO partners are becoming increasingly aware that customers are

prepared to pay for outcomes rather than inputs

Confidentiality Notice

This file is private and may contain confidential and proprietary information. If you have received this file in error, please notify us and remove

it from your system and note that you must not copy, distribute or take any action in reliance on it. Any unauthorized use or disclosure of the

contents of this file is not permitted and may be unlawful. AstraZeneca PLC, 1 Francis Crick Avenue, Cambridge Biomedical Campus,

Cambridge, CB2 0AA, UK, T: +44(0)203 749 5000, www.astrazeneca.com

15

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte MCS Limited is a subsidiary of Deloitte LLP, the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte MCS Limited would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte MCS Limited accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

© 2016 Deloitte MCS Limited. All rights reserved.

Registered office: Hill House, 1 Little New Street, London EC4A 3TR, United Kingdom. Registered in England No 3311052.