DELIVERING VALUE - Home - Australian Securities ... VALUE Successful transition to Australia’s...

22

DELIVERING VALUE Successful transition to Australia’s newest coking coal producer Investor Presentation Noosa Mining Conference July 2016 For personal use only

Transcript of DELIVERING VALUE - Home - Australian Securities ... VALUE Successful transition to Australia’s...

DELIVERING VALUESuccessful transition to Australia’snewest coking coal producer

Investor PresentationNoosa Mining ConferenceJuly 2016

For

per

sona

l use

onl

y

IMPORTANTINFORMATION

This document has been prepared by Stanmore CoalLimited (“Stanmore Coal”) for the purpose of providing acompany and technical overview to interestedanalysts/investors. None of Stanmore Coal, nor any of itsrelated bodies corporate, their respective directors,partners, employees or advisers or any other person(“Relevant Parties”) makes any representations orwarranty to, or takes responsibility for, the accuracy,reliability or completeness of the information contained inthis document, to the recipient of this document(“Recipient”), and nothing contained in it is, or may berelied upon as, a promise or representation, whether as tothe past or future.

The information in this document does not purport to becomplete nor does it contain all the information that wouldbe required in a disclosure statement or prospectusprepared in accordance with the Corporations Act 2001(Commonwealth). It should be read in conjunction withStanmore’s other periodic and continuous disclosureannouncements lodged with the Australian SecuritiesExchange, which are available at www.asx.com.au.

This document is not a recommendation to acquireStanmore Coal shares and has been prepared withouttaking into account the objectives, financial situation orneeds of individuals. Before making an investmentdecision prospective investors should consider theappropriateness of the information having regard to theirown objectives, financial situation and needs and seekappropriate advice, including financial, legal and taxationadvice appropriate to their jurisdiction. Except to theextent prohibited by law, the Relevant Parties disclaim allliability that may otherwise arise due to any of thisinformation being inaccurate or incomplete. By obtainingthis document, the Recipient releases the RelevantParties from liability to the Recipient for any loss ordamage that it may suffer or incur arising directly orindirectly out of or in connection with any use of orreliance on any of this information, whether such liabilityarises in contract, tort (including negligence) or otherwise.

This document contains certain “forward-lookingstatements”. The words “forecast”, “estimate”, “like”,“anticipate”, “project”, “opinion”, “should”, “could”, “may”,“target” and other similar expressions are intended toidentify forward looking statements. Indications of, andguidance on, future earnings and financial position andperformance are also forward-looking statements. You arecautioned not to place undue reliance on forward lookingstatements.

Although due care and attention has been used in the

preparation of forward looking statements, suchstatements, opinions and estimates are based onassumptions and contingencies that are subject to changewithout notice, as are statements about market andindustry trends, which are based on interpretations ofcurrent market conditions. Forward looking statementsincluding projections, guidance on future earnings andestimates are provided as a general guide only andshould not be relied upon as an indication or guarantee offuture performance.

Recipients of the document must make their ownindependent investigations, consideration and evaluation.By accepting this document, the Recipient agrees that if itproceeds further with its investigations, consideration orevaluation of investing in the company it will make andrely solely upon its own investigations and inquiries andwill not in any way rely upon this document.

This document is not and should not be considered toform any offer or an invitation to acquire Stanmore Coalshares or any other financial products, and neither thisdocument nor any of its contents will form the basis of anycontract or commitment. In particular, this document doesnot constitute any part of any offer to sell, or thesolicitation of an offer to buy, any securities in the UnitedStates or to, or for the account or benefit of any “USperson” as defined in Regulation S under the USSecurities Act of 1993 (“Securities Act”). Stanmore Coalshares have not been, and will not be, registered underthe Securities Act or the securities laws of any state orother jurisdiction of the United States, and may not beoffered or sold in the United States or to any US personwithout being so registered or pursuant to an exemptionfrom registration.

Marketable Reserves Note – The Range:

The Marketable Coal Reserves of 94Mt is derived from aJORC compliant run of mine (ROM) Probable CoalReserve of 117.5Mt based on a 14.8% ash product andpredicted yield of 80%. The 94Mt marketable reserve isincluded in the 287Mt total JORC Resource (18MtMeasured + 187Mt Indicated + 82Mt Inferred Resource).

Marketable Reserves Note – Isaac Plains:

The Marketable Coal Reserves of 3.7Mt is derived from aJORC compliant run of mine (ROM) Reserve of 5.0Mtbased on a predicted yield of 73%. The 3.7Mt MarketableReserve is included in the 48.2Mt total JORC Resourcefor Isaac Plains(15.2Mt Measured + 23.0Mt Indicated +10.0Mt Inferred Resource).

Marketable Reserves Note – Isaac Plains East:

The Marketable Coal Reserves of 8.3Mt is derived from aJORC compliant run of mine (ROM) Reserve of 10.3Mtbased on a predicted yield of 81%. The 8.3Mt MarketableReserve is included in the 28.7Mt total JORC Resourcefor Isaac Plains East (18.7Mt Indicated + 10.0Mt InferredResource).

Production Target

The production target of 1.1 Mtpa for 10 years (equivalentto 1.5Mtpa run of mine production) is underpinned solelyby total Marketable Reserves of 11.9Mt (10.8 yearsequivalent) within Isaac Plains and Isaac Plains East, asannounced on 6 April 2016, titled “Significant JORCReserves Increase for Isaac Plains Complex”.

The Company confirms that it is not aware of any newinformation or data that materially affects the informationincluded in the announcement made on 6 April 2016 andthat all material assumptions and technical parametersunderpinning the estimates in the announcement made on6 April 2016 continue to apply and have not materiallychanged.

Competent Persons Statement:

The information in this report relating to coal reserves forIsaac Plains and Isaac Plains East was announced on 6April 2016, titled “Significant JORC Reserve Increase forIsaac Plains Complex”, and is based on informationcompiled by Mr Ken Hill who is a full-time employee ofXenith Consulting Pty Ltd. Mr Hill is the ManagingDirector of Xenith Consulting Pty Ltd, is a qualified civilengineer, a member of the Australian Institute of Miningand Metallurgy (AusIMM) and has the relevant experience(30+ years) in relation to the mineralisation being reportedto qualify as a Competent Person as defined in the“Australasian Code for Reporting of Exploration Results,Mineral Resources and Ore Reserves (The JORC Code2012 Edition)”.

The Company confirms that it is not aware of any newinformation or data that materially affects the informationincluded in the announcement made on 6 April 2016 andthat all material assumptions and technical parametersunderpinning the estimates in the announcement made on6 April 2016 continue to apply and have not materiallychanged.

The information in this report relating to coal resources forIsaac Plains and Isaac Plains East was announced on 6April 2016, titled “Significant JORC Resource Increase forIsaac Plains Coking Coal Complex”, and is based oninformation compiled by Mr Troy Turner who is a full-timeemployee of Xenith Consulting Pty Ltd. Mr Turner is aqualified geologist and a member of the AustralianInstitute of Mining and Metallurgy (AusIMM) and hassufficient experience in relation to the style ofmineralisation and type of deposit being reported toqualify as a Competent Person as defined in the“Australasian Code for Reporting of Exploration Results,Mineral Resources and Ore Reserves (The JORC Code2012 Edition)”.

The Company confirms that it is not aware of any newinformation or data that materially affects the informationincluded in the announcement made on 6 April 2016 andthat all material assumptions and technical parametersunderpinning the estimates in the announcement made on6 April 2016 continue to apply and have not materiallychanged.

2

For

per

sona

l use

onl

y

STANMORE COALDELIVERING VALUE AS AUSTRALIA’S NEWEST COKING COAL PRODUCER

ONLY ASX-LISTED MET COAL PURE PLAY

✓Re-commencement of mining achievedIsaac Plains Coal Mine officially re-opened by Queensland State Premier in May 2016.Recommissioning of dragline, washplant and general infrastructure completed – first coal production April 2016

✓Ramp-up of production – first cash receipts in June quarterMilestone June quarter achieving first product coal and cash generation through sales revenue.Fully sold first year of coking coal production to major East Asian steel mills

✓10 years of open cut Reserves - additional 7 years from Isaac Plains East1

Approvals path underway to permit Isaac Plains East for a low cost extension

Note 1: Refer Competent Persons Statement and Marketable Reserves Notes, p23

✓Positive coal market price signalsTwo consecutive quarters of coking coal price increases. Increasing tightness in the met coal market due to improved Asiandemand and Australian supply disruptions.

For

per

sona

l use

onl

y

COKING COALAN ESSENTIAL RESOURCE FOR THE FUTURE

4

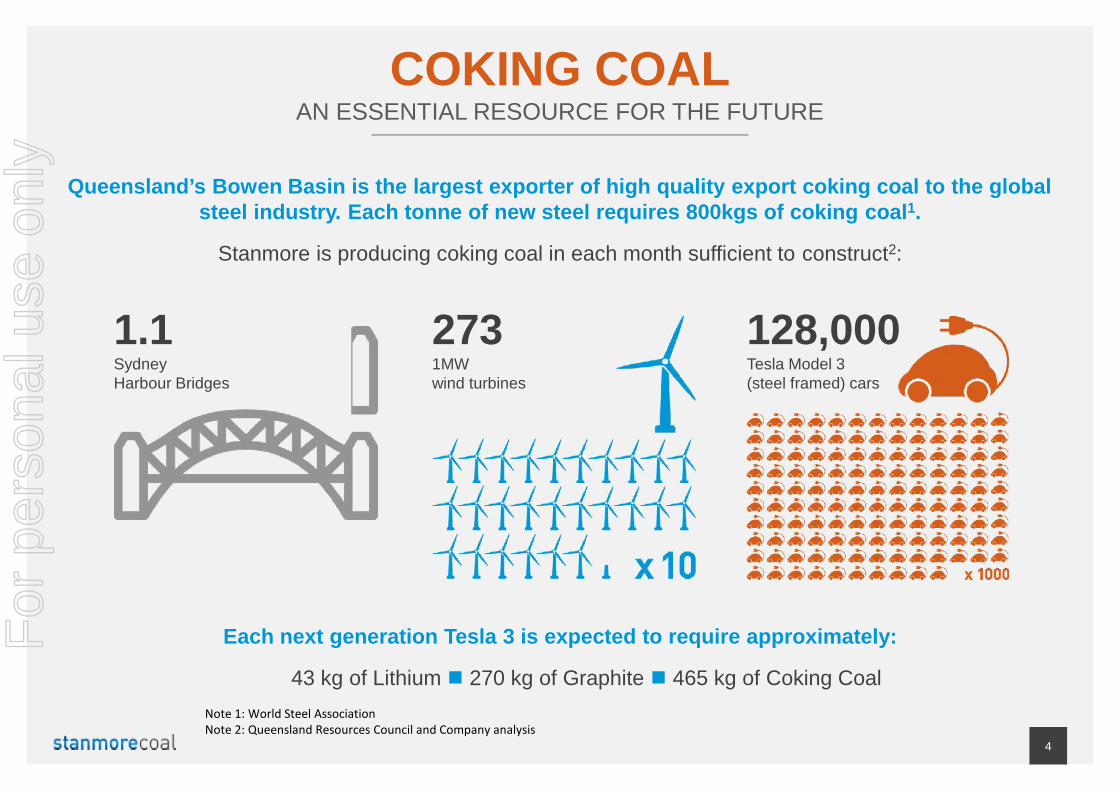

Queensland’s Bowen Basin is the largest exporter of high quality export coking coal to the globalsteel industry. Each tonne of new steel requires 800kgs of coking coal1.

Stanmore is producing coking coal in each month sufficient to construct2:

Each next generation Tesla 3 is expected to require approximately:

43 kg of Lithium 270 kg of Graphite 465 kg of Coking Coal

1.1SydneyHarbour Bridges

2731MWwind turbines

128,000Tesla Model 3(steel framed) cars

Note 1: World Steel AssociationNote 2: Queensland Resources Council and Company analysis

For

per

sona

l use

onl

y

STRONGER PRICING OUTLOOKRECENT STRENGTH IN COKING COAL MARKET

5

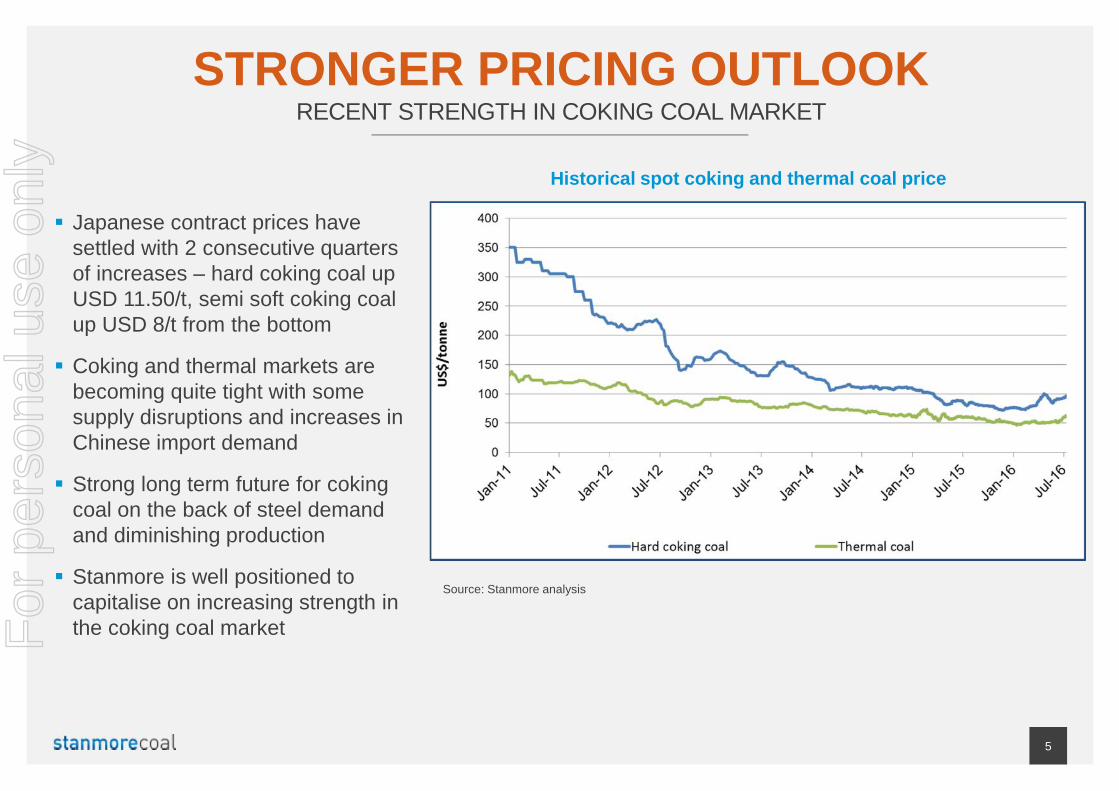

Historical spot coking and thermal coal price

Japanese contract prices havesettled with 2 consecutive quartersof increases – hard coking coal upUSD 11.50/t, semi soft coking coalup USD 8/t from the bottom

Coking and thermal markets arebecoming quite tight with somesupply disruptions and increases inChinese import demand

Strong long term future for cokingcoal on the back of steel demandand diminishing production

Stanmore is well positioned tocapitalise on increasing strength inthe coking coal market

Source: Stanmore analysis

For

per

sona

l use

onl

y

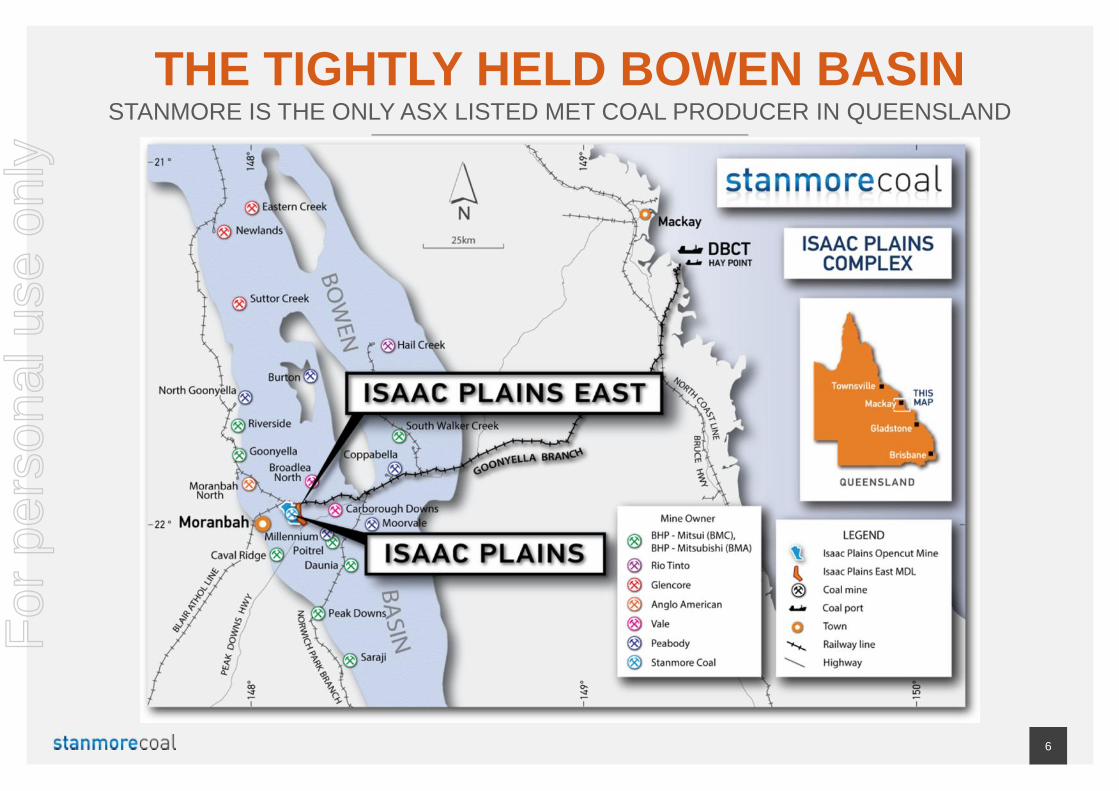

THE TIGHTLY HELD BOWEN BASINSTANMORE IS THE ONLY ASX LISTED MET COAL PRODUCER IN QUEENSLAND

6

For

per

sona

l use

onl

y

ISAAC PLAINS - ATRANSFORMATIONALINVESTMENT

7

For

per

sona

l use

onl

y

Two strategic transactions completed in2015 to present multiple pathways toenhance shareholder value Established coking coal mine with existing

infrastructure Adjacent low strip ratio resource

Delivered without dilution to existingshareholders

TRANSACTION HIGHLIGHTS

8

For

per

sona

l use

onl

y

COAL QUALITY Metallurgical coal – semi-soft,

semi-hard Sold into major steel mills primarily

in Japan and Korea

ISAAC PLAINS COKING COAL MINETRANSACTION OVERVIEW

OVER $350M REPLACMENTVALUE OF AQUIRED ASSETS Dragline - Bucyrus BE1370 500tph Coal Handling and Prep

Plant (wash plant) Product stockpile, conveyors, train

loadout, rail loop Established office setup Several maintenance workshops

ACQUISITION OF ESTABLISHEDMET COAL MINE Existing open-cut operation

commenced production in 2006 Located near Moranbah in

the heart of the Bowen Basin 172 km from DBCT via

Goonyella rail line Placed on care and maintenance

late 2014 by previous owners ValeSA and Sumitomo Corp Rail and port access agreements in

place, exporting through DalrympleBay Coal Terminal (DBCT)

APPROVED MINING LEASE ANDENVIRONMENTAL AUTHORITY Up to 4.0Mtpa run of mine (ROM)

production approval in place

TRANSACTIONCOMPLETEDNovember2015

9

For

per

sona

l use

onl

y

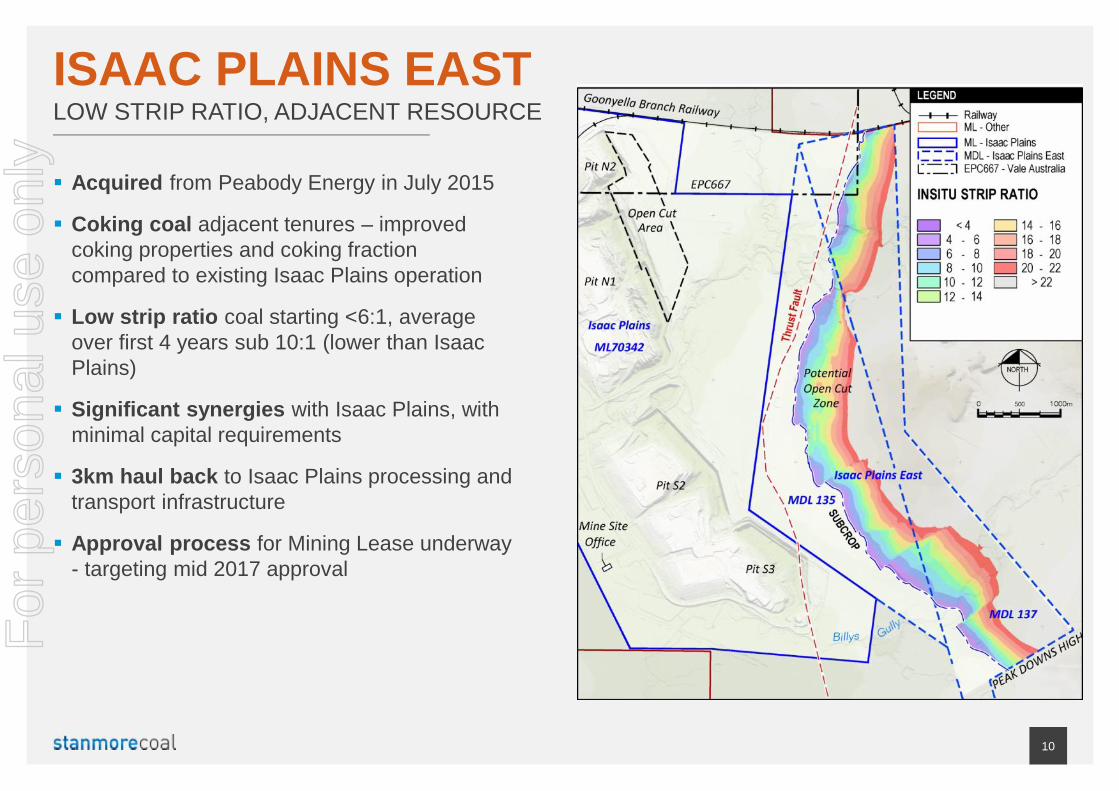

Acquired from Peabody Energy in July 2015

Coking coal adjacent tenures – improvedcoking properties and coking fractioncompared to existing Isaac Plains operation

Low strip ratio coal starting <6:1, averageover first 4 years sub 10:1 (lower than IsaacPlains)

Significant synergies with Isaac Plains, withminimal capital requirements

3km haul back to Isaac Plains processing andtransport infrastructure

Approval process for Mining Lease underway- targeting mid 2017 approval

ISAAC PLAINS EASTLOW STRIP RATIO, ADJACENT RESOURCE

10

For

per

sona

l use

onl

y

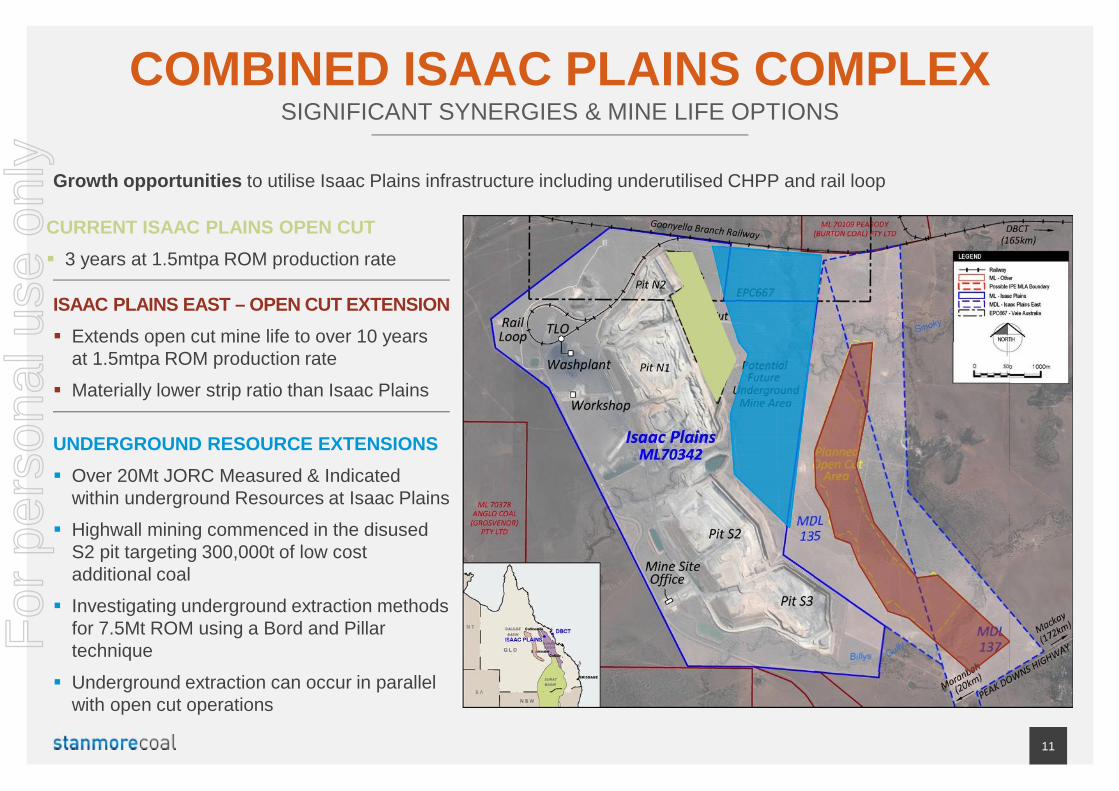

Growth opportunities to utilise Isaac Plains infrastructure including underutilised CHPP and rail loop

UNDERGROUND RESOURCE EXTENSIONS Over 20Mt JORC Measured & Indicated

within underground Resources at Isaac Plains Highwall mining commenced in the disused

S2 pit targeting 300,000t of low costadditional coal

Investigating underground extraction methodsfor 7.5Mt ROM using a Bord and Pillartechnique

Underground extraction can occur in parallelwith open cut operations

ISAAC PLAINS EAST – OPEN CUT EXTENSION Extends open cut mine life to over 10 years

at 1.5mtpa ROM production rate Materially lower strip ratio than Isaac Plains

CURRENT ISAAC PLAINS OPEN CUT 3 years at 1.5mtpa ROM production rate

COMBINED ISAAC PLAINS COMPLEXSIGNIFICANT SYNERGIES & MINE LIFE OPTIONS

11

For

per

sona

l use

onl

y

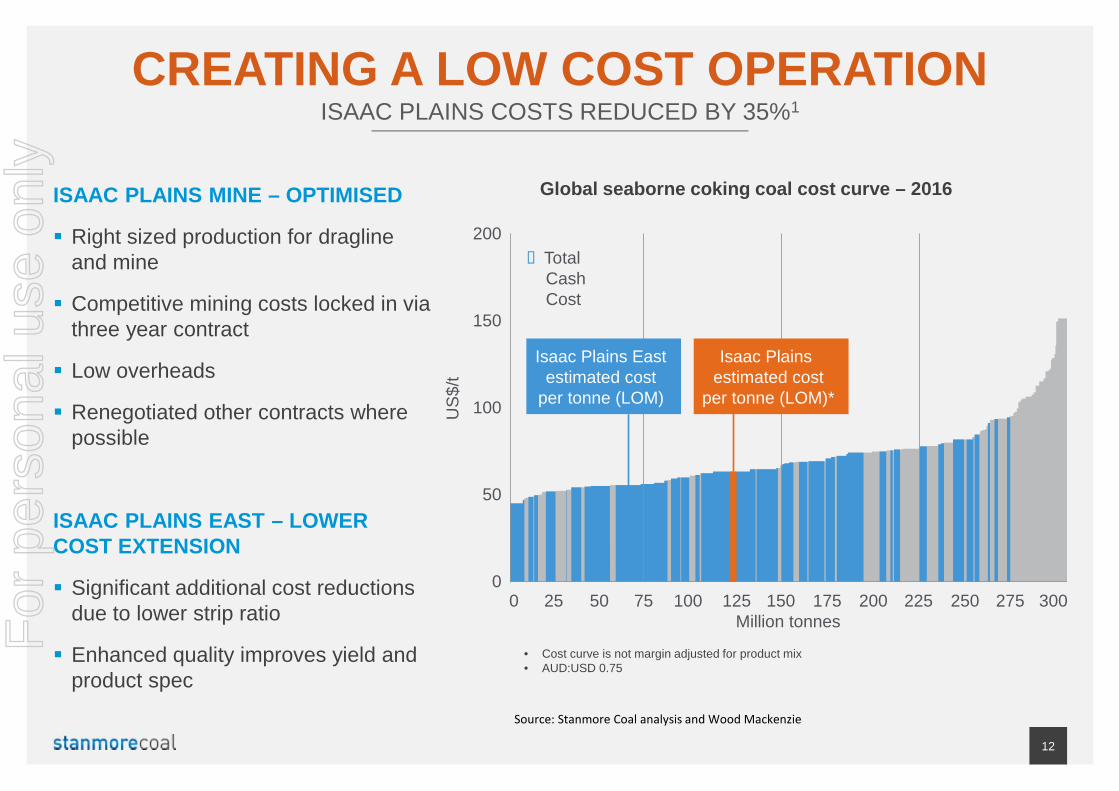

• Cost curve is not margin adjusted for product mix• AUD:USD 0.75

CREATING A LOW COST OPERATIONISAAC PLAINS COSTS REDUCED BY 35%1

Global seaborne coking coal cost curve – 2016

Source: Stanmore Coal analysis and Wood Mackenzie

12

US$

/t

200

0 25 50 75 100 125 150 175 200 225 250 275 300

150

100

50

0

Million tonnes

nTotal Cash Cost

Isaac Plains Eastestimated cost

per tonne (LOM)

Isaac Plainsestimated cost

per tonne (LOM)*

ISAAC PLAINS MINE – OPTIMISED

Right sized production for draglineand mine

Competitive mining costs locked in viathree year contract

Low overheads

Renegotiated other contracts wherepossible

ISAAC PLAINS EAST – LOWERCOST EXTENSION

Significant additional cost reductionsdue to lower strip ratio

Enhanced quality improves yield andproduct spec

For

per

sona

l use

onl

y

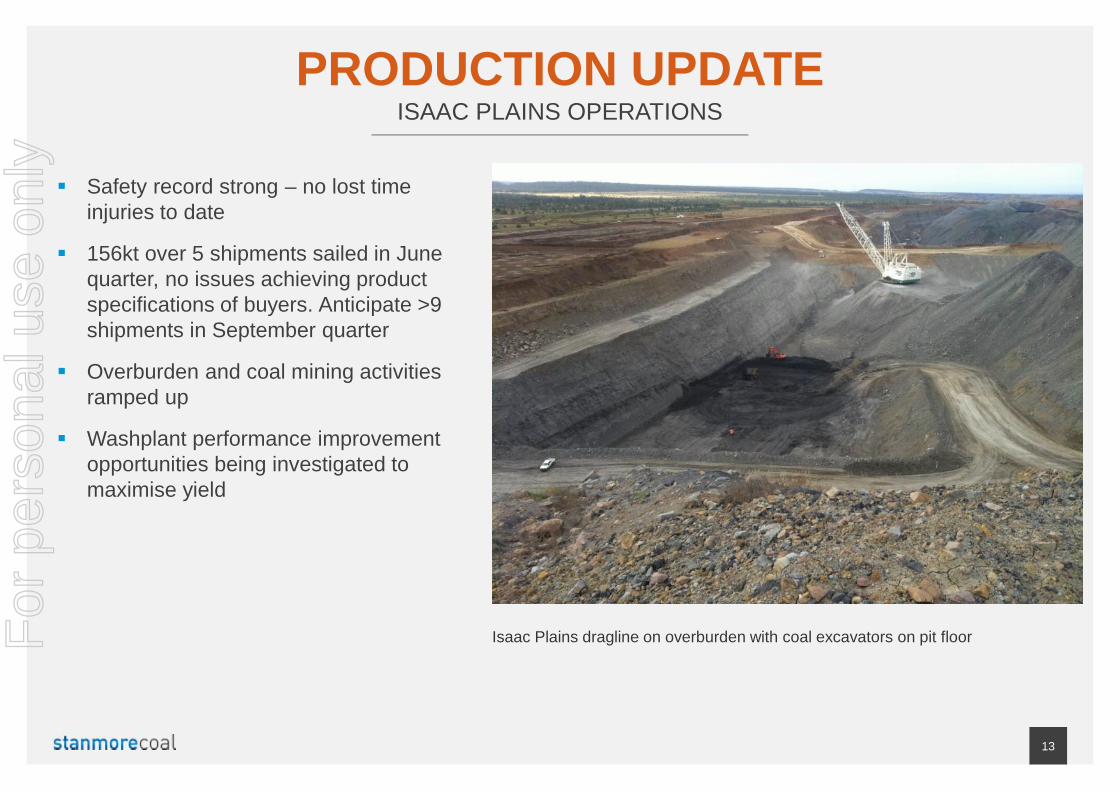

PRODUCTION UPDATEISAAC PLAINS OPERATIONS

Isaac Plains dragline on overburden with coal excavators on pit floor

13

Safety record strong – no lost timeinjuries to date

156kt over 5 shipments sailed in Junequarter, no issues achieving productspecifications of buyers. Anticipate >9shipments in September quarter

Overburden and coal mining activitiesramped up

Washplant performance improvementopportunities being investigated tomaximise yield

For

per

sona

l use

onl

y

JOBS

150 jobs in the Isaac region created by the mine restart

ROYALTIES

Over $7m per year of payments to the State with potential to increase

THE ENVIRONMENT

Fast-tracking rehabilitation

Stanmore is undertaking 84ha of mine site rehabilitation in our firstyear of ownership, more than the total rehab previously completedsince the mine opened in 2006

Substantial bank guarantees provided to the State to back ourongoing environmental commitments

Wash Plant contains belt press filters – no tailings dams required

OUR CONTRIBUTIONStanmore Coal is a Queensland Company that takes its responsibilities seriously

14

Blast Monitor at Moranbahmonitoring compound

Macroinvertebrate sampling inSmoky Creek

For

per

sona

l use

onl

y

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

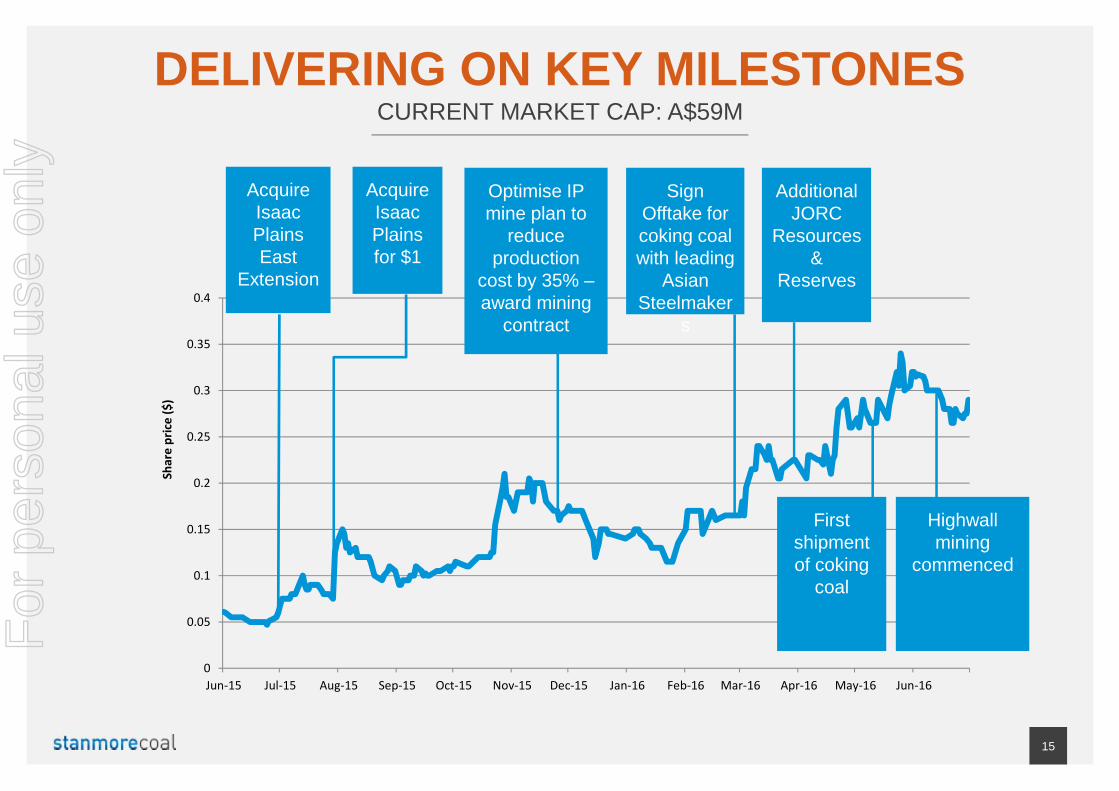

Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

Shar

e pr

ice ($

)

DELIVERING ON KEY MILESTONESCURRENT MARKET CAP: A$59M

15

AcquireIsaacPlainsEast

Extension

Optimise IPmine plan to

reduceproduction

cost by 35% –award mining

contract

SignOfftake forcoking coalwith leading

AsianSteelmaker

s

AdditionalJORC

Resources&

Reserves

AcquireIsaacPlainsfor $1

Firstshipmentof coking

coal

Highwallmining

commenced

For

per

sona

l use

onl

y

VALUE DRIVERSUPCOMING MILESTONES AND OPPORTUNITIES

16

Complete ramp up to steady state productionin September quarter

Finalise submission for low cost Isaac PlainsEast mining lease application, lodgement inDec 2016 quarter

Assess potential underground mining ineastern zone of Mining Lease – over 20MtIndicated and Inferred Resource in this area

Continue to deliver on-spec shipments to termcustomers – assess operational potential ofhigher value coking coal products

Assess acquisition opportunities that leverageexisting significant infrastructure position

Positive coking coal price trends and outlook

First coking coal shipment departing the port of DBCT for Korea

For

per

sona

l use

onl

y

APPENDICES

17

For

per

sona

l use

onl

y

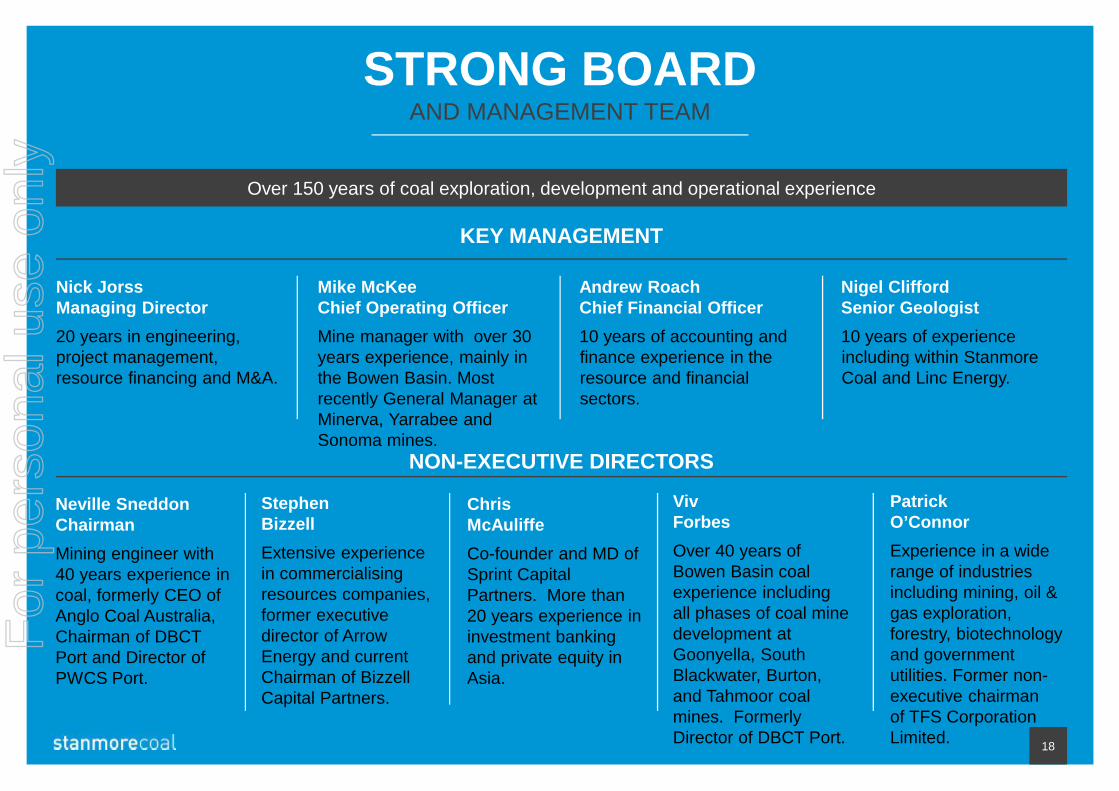

Over 150 years of coal exploration, development and operational experience

Neville SneddonChairmanMining engineer with40 years experience incoal, formerly CEO ofAnglo Coal Australia,Chairman of DBCTPort and Director ofPWCS Port.

StephenBizzellExtensive experiencein commercialisingresources companies,former executivedirector of ArrowEnergy and currentChairman of BizzellCapital Partners.

VivForbesOver 40 years ofBowen Basin coalexperience includingall phases of coal minedevelopment atGoonyella, SouthBlackwater, Burton,and Tahmoor coalmines. FormerlyDirector of DBCT Port.

ChrisMcAuliffeCo-founder and MD ofSprint CapitalPartners. More than20 years experience ininvestment bankingand private equity inAsia.

PatrickO’ConnorExperience in a widerange of industriesincluding mining, oil &gas exploration,forestry, biotechnologyand governmentutilities. Former non-executive chairmanof TFS CorporationLimited.

Nick JorssManaging Director20 years in engineering,project management,resource financing and M&A.

Mike McKeeChief Operating OfficerMine manager with over 30years experience, mainly inthe Bowen Basin. Mostrecently General Manager atMinerva, Yarrabee andSonoma mines.

Andrew RoachChief Financial Officer10 years of accounting andfinance experience in theresource and financialsectors.

NON-EXECUTIVE DIRECTORS

Nigel CliffordSenior Geologist10 years of experienceincluding within StanmoreCoal and Linc Energy.

STRONG BOARDAND MANAGEMENT TEAM

18

KEY MANAGEMENT

For

per

sona

l use

onl

y

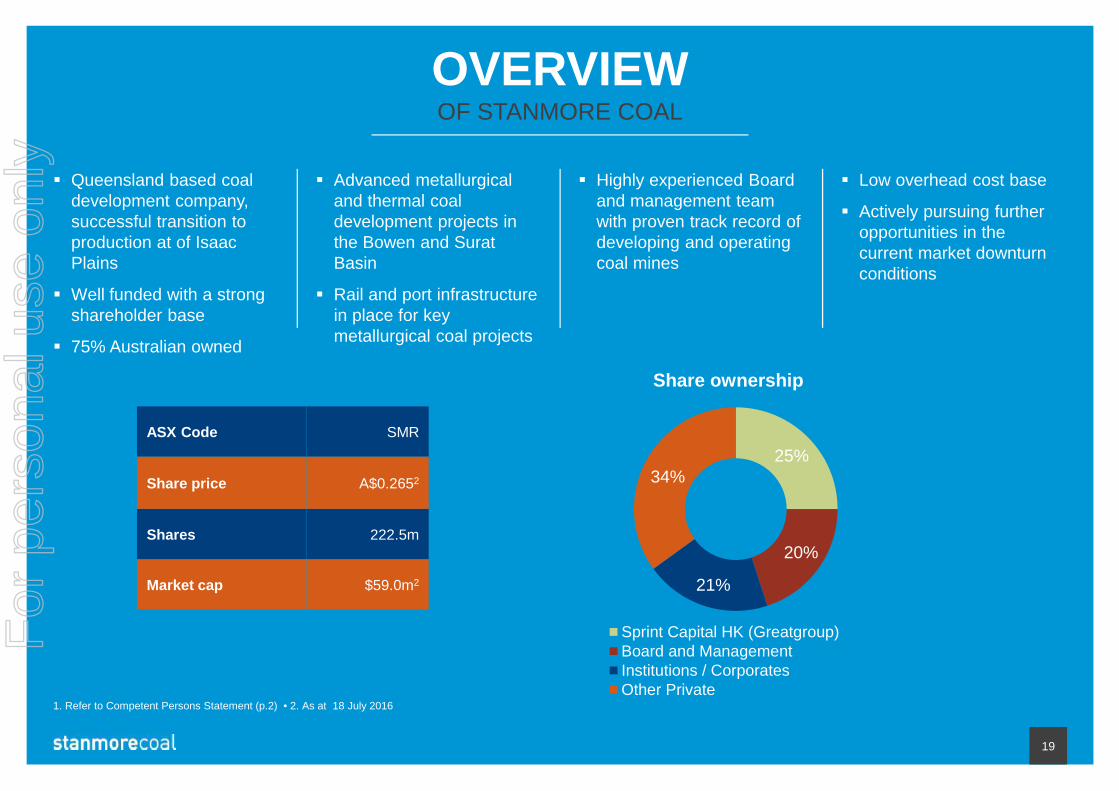

Queensland based coaldevelopment company,successful transition toproduction at of IsaacPlains

Well funded with a strongshareholder base

75% Australian owned

Advanced metallurgicaland thermal coaldevelopment projects inthe Bowen and SuratBasin

Rail and port infrastructurein place for keymetallurgical coal projects

Highly experienced Boardand management teamwith proven track record ofdeveloping and operatingcoal mines

Low overhead cost base

Actively pursuing furtheropportunities in thecurrent market downturnconditions

Share ownership

Sprint Capital HK (Greatgroup)Board and ManagementInstitutions / CorporatesOther Private

ASX Code SMR

Share price A$0.2652

Shares 222.5m

Market cap $59.0m2

1. Refer to Competent Persons Statement (p.2) • 2. As at 18 July 2016

25%

20%

34%

21%

19

OVERVIEWOF STANMORE COAL

For

per

sona

l use

onl

y

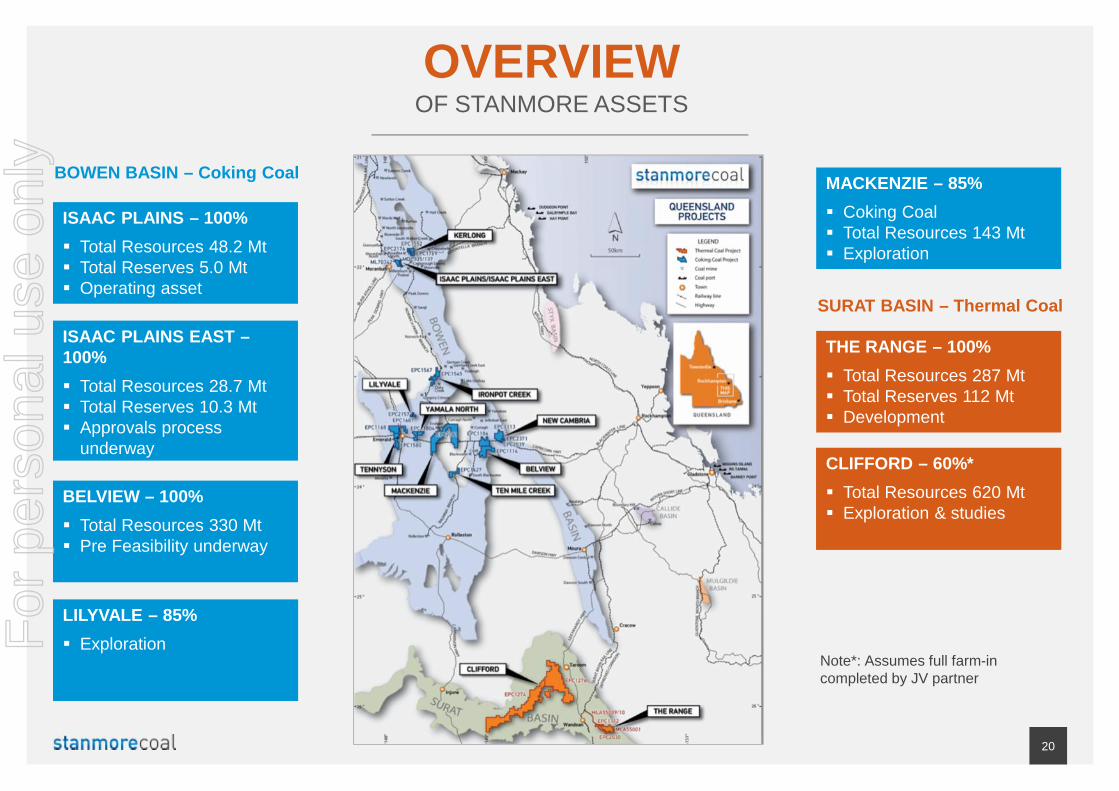

OVERVIEWOF STANMORE ASSETS

ISAAC PLAINS – 100% Total Resources 48.2 Mt Total Reserves 5.0 Mt Operating asset

THE RANGE – 100% Total Resources 287 Mt Total Reserves 112 Mt Development

BELVIEW – 100% Total Resources 330 Mt Pre Feasibility underway

LILYVALE – 85% Exploration

MACKENZIE – 85% Coking Coal Total Resources 143 Mt Exploration

ISAAC PLAINS EAST –100% Total Resources 28.7 Mt Total Reserves 10.3 Mt Approvals process

underway

Note*: Assumes full farm-incompleted by JV partner

20

BOWEN BASIN – Coking Coal

THE RANGE – 100% Total Resources 287 Mt Total Reserves 112 Mt Development

CLIFFORD – 60%* Total Resources 620 Mt Exploration & studies

SURAT BASIN – Thermal Coal

For

per

sona

l use

onl

y

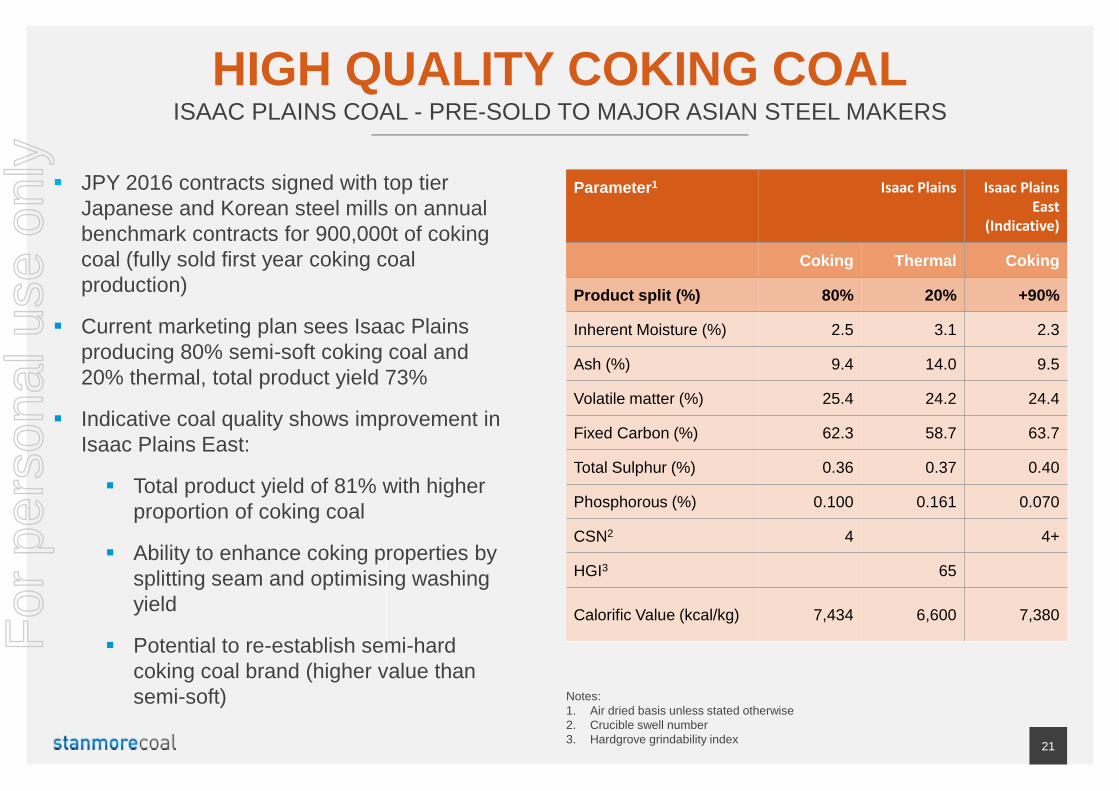

Parameter1 Isaac Plains Isaac PlainsEast

(Indicative)

Coking Thermal Coking

Product split (%) 80% 20% +90%

Inherent Moisture (%) 2.5 3.1 2.3

Ash (%) 9.4 14.0 9.5

Volatile matter (%) 25.4 24.2 24.4

Fixed Carbon (%) 62.3 58.7 63.7

Total Sulphur (%) 0.36 0.37 0.40

Phosphorous (%) 0.100 0.161 0.070

CSN2 4 4+

HGI3 65

Calorific Value (kcal/kg) 7,434 6,600 7,380

HIGH QUALITY COKING COALISAAC PLAINS COAL - PRE-SOLD TO MAJOR ASIAN STEEL MAKERS

JPY 2016 contracts signed with top tierJapanese and Korean steel mills on annualbenchmark contracts for 900,000t of cokingcoal (fully sold first year coking coalproduction)

Current marketing plan sees Isaac Plainsproducing 80% semi-soft coking coal and20% thermal, total product yield 73%

Indicative coal quality shows improvement inIsaac Plains East:

Total product yield of 81% with higherproportion of coking coal

Ability to enhance coking properties bysplitting seam and optimising washingyield

Potential to re-establish semi-hardcoking coal brand (higher value thansemi-soft) Notes:

1. Air dried basis unless stated otherwise2. Crucible swell number3. Hardgrove grindability index 21

For

per

sona

l use

onl

y

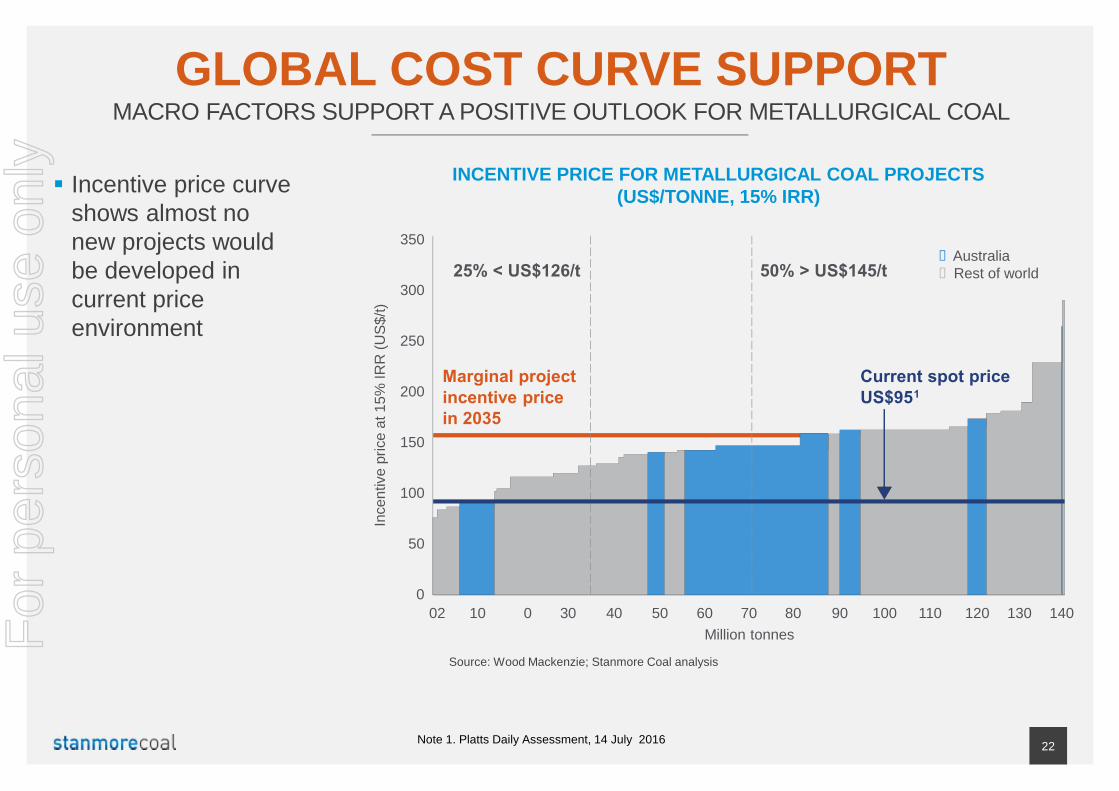

GLOBAL COST CURVE SUPPORTMACRO FACTORS SUPPORT A POSITIVE OUTLOOK FOR METALLURGICAL COAL

Source: Wood Mackenzie; Stanmore Coal analysis

INCENTIVE PRICE FOR METALLURGICAL COAL PROJECTS(US$/TONNE, 15% IRR)

22Note 1. Platts Daily Assessment, 14 July 2016

Incentive price curveshows almost nonew projects wouldbe developed incurrent priceenvironment

I nc e

ntiv

epr

ice

at15

%IR

R(U

S $/t )

350

02 0 30 4010 50 60 70 80 90 100 110 120 130 140

300

250

200

150

100

0

50

Million tonnes

nAustralianRest of world50% > US$145/t25% < US$126/t

Marginal projectincentive pricein 2035

Current spot priceUS$951

For

per

sona

l use

onl

y