Defining Features. Direct Loan Borrows money from the treasury Gives it directly to borrowers...

52

Defining Features

-

date post

21-Dec-2015 -

Category

Documents

-

view

215 -

download

0

Transcript of Defining Features. Direct Loan Borrows money from the treasury Gives it directly to borrowers...

Defining Features

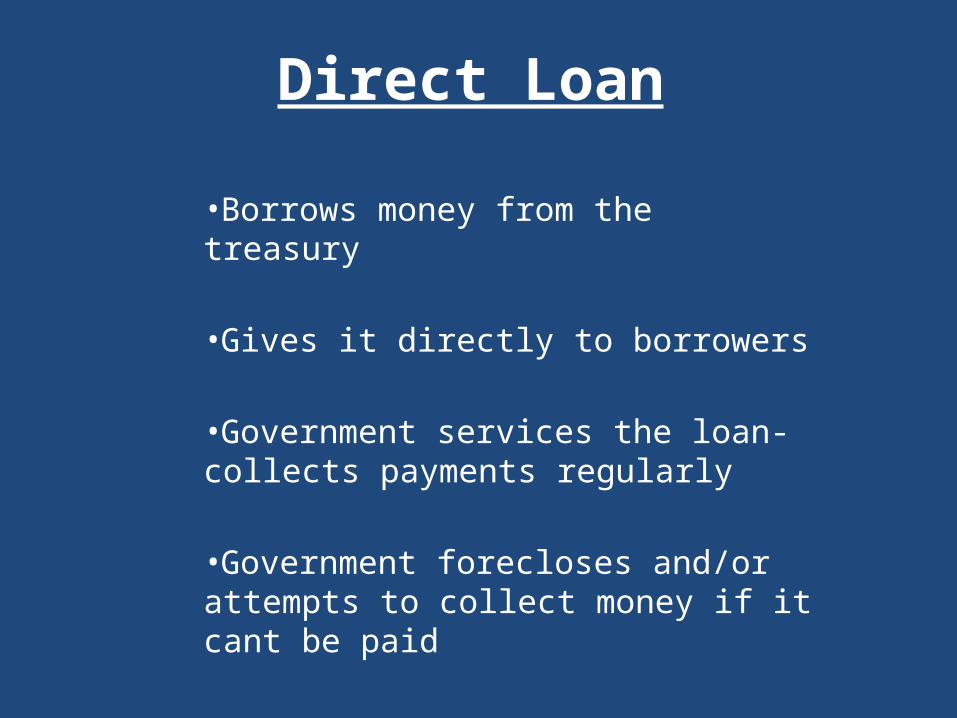

Direct Loan

•Borrows money from the treasury

•Gives it directly to borrowers

•Government services the loan- collects payments regularly

•Government forecloses and/or attempts to collect money if it cant be paid

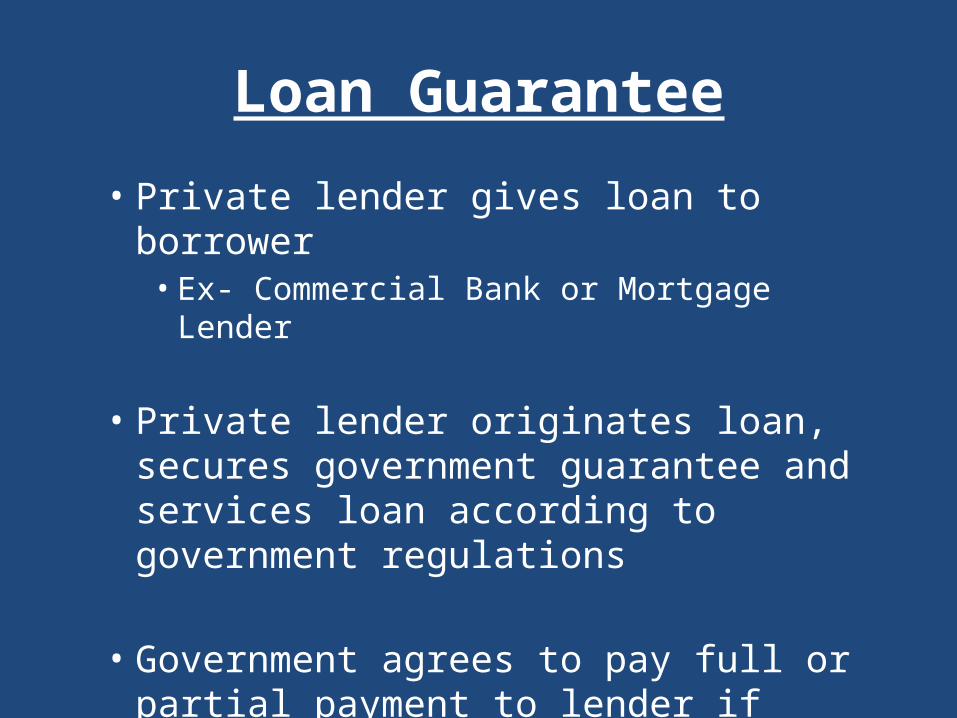

Loan Guarantee

• Private lender gives loan to borrower• Ex- Commercial Bank or Mortgage Lender

• Private lender originates loan, secures government guarantee and services loan according to government regulations

• Government agrees to pay full or partial payment to lender if borrower defaults

Relation to Key Tool Features

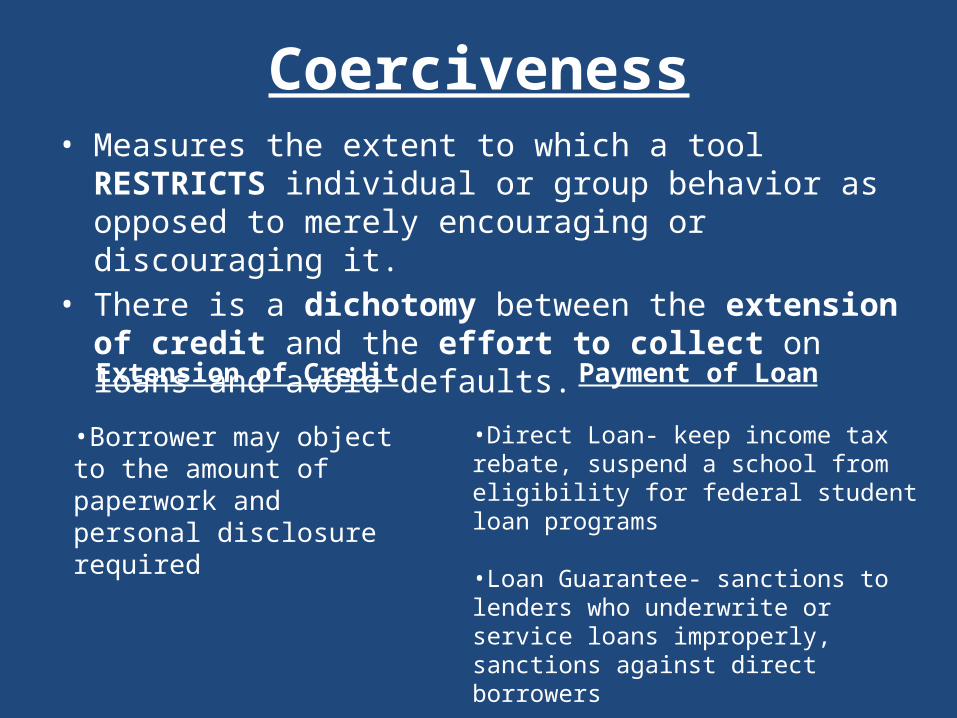

Coerciveness• Measures the extent to which a tool RESTRICTS individual or

group behavior as opposed to merely encouraging or discouraging it.

• There is a dichotomy between the extension of credit and the effort to collect on loans and avoid defaults.

Extension of Credit

•Borrower may object to the amount of paperwork and personal disclosure required

Payment of Loan

•Direct Loan- keep income tax rebate, suspend a school from eligibility for federal student loan programs

•Loan Guarantee- sanctions to lenders who underwrite or service loans improperly, sanctions against direct borrowers

Directness• Measures the extent to which the entity authorizing

or inaugurating a program is involved in executing it.

Direct Loan• Allows government to have more

information about borrowers because it deals directly with them.

Ex- Dept of Agriculture• Servicing center then local office will

attempt to reinstate timely loan payments

• local office will attempt to mitigate loss and may foreclose.

Ex- Dept of Education• Uses schools to originate the loans,

contractors to service loans and mitigate losses

Loan Guarantees•Private lenders have info on borrowers and don’t always give it to government

Ex- U.S. Small Business Administration• Lender originates ,services and forecloses

on the loan • Lender makes a claim to the government

for their fraction of the loss on the defaulted loan.

Autonomy

Direct Loans• Give Loans- Not Direct– have to create a delivery

system to originate and service loans

• Collect Loan- Not Direct

Loan Guarantees• Give Loans- Direct– Uses existing private

financial services system

• Collect Loans- Not Direct

• Measures the extent to which a tool utilizes an existing administrative structure to produce its effects rather than having to create its own administrative apparatus.

Visibility

Direct Loans• Before 1990 Credit Reform Act-

Visible– Year given: Withdrawal of full

loan amount– Years paid back: Deposit of

repayment amount

Loan Guarantees• Before 1990 Credit Reform Act- Not

Visible- Clear Budgetary Advantage– Year given: Not on budget– Year defaulted: Withdrawal when

lender paid

• Measures the extent to which the resources devoted to the tool show up in the normal budget process

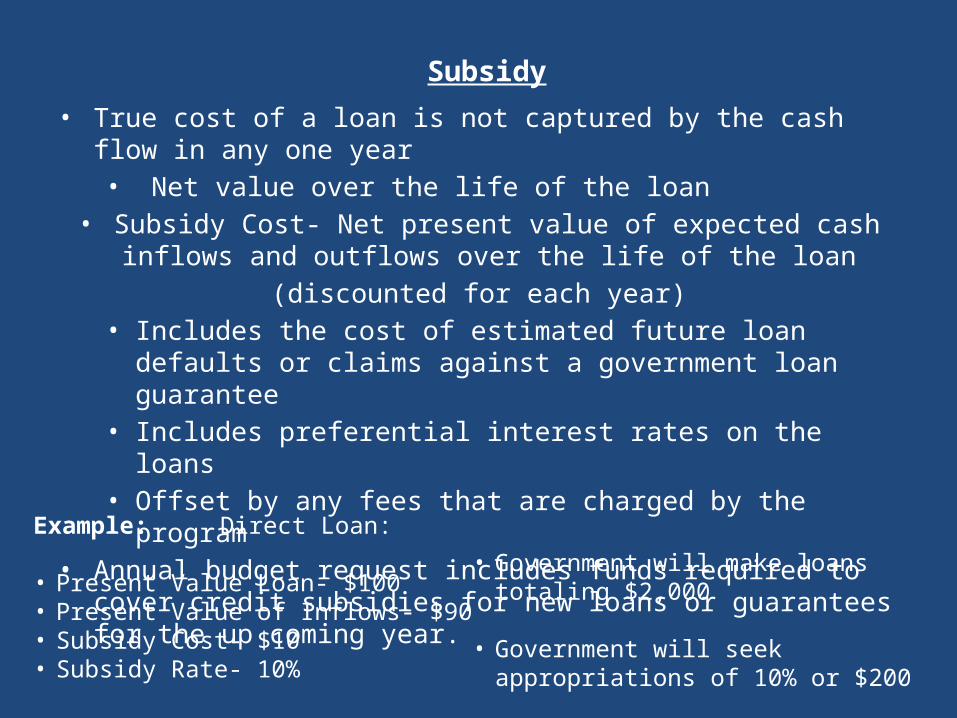

Subsidy• True cost of a loan is not captured by the cash flow in any one year

• Net value over the life of the loan• Subsidy Cost- Net present value of expected cash inflows and outflows

over the life of the loan (discounted for each year)

• Includes the cost of estimated future loan defaults or claims against a government loan guarantee

• Includes preferential interest rates on the loans• Offset by any fees that are charged by the program

• Annual budget request includes funds required to cover credit subsidies for new loans or guarantees for the up coming year.

Example: Direct Loan:

• Present Value Loan- $100• Present Value of Inflows- $90• Subsidy Cost- $10• Subsidy Rate- 10%

• Government will make loans totaling $2,000 • Government will seek appropriations of 10%

or $200

Design Features and Major Variants

A well designed government credit program will balance the tension between

doing good and doing well.

Doing Good• Serving worthy

constituencies

Doing Well• Assuring loans are

rigorously underwritten• Assuring they are

serviced• Assuring they are

foreclosed on if need be.

Defining Eligible Borrowers

• Most beneficial economically if borrowers are those that are not creditworthy enough for private loans, but still creditworthy enough to handle the loan

• FHA-• Was very conservative and didn’t give out much

credit• Then switched and gave lots of financially

unsound people credit• Took years to determine a balance

Determining the Amount of Subsidy to Provide

Forms of Subsidies• Paying some interest• Grace period before borrower

has to start paying interest• Charging lower fees• Tax exemptions of interest

receipts

• If subsidy rate is over 30% then its like giving a grant but its “justified” because the loan will be repaid

• Before the Credit Reform Act of 1990 Congress gave credit to failing companies• Now they would have to figure out a credit subsidy and appropriate

funds in the budget

Deciding Whether Loans Will be Backed by Collateral

Collateral is a way of reducing financial Risk

Secured Loans• For Real Property– Collateral Required

(usually the property itself)

– FHA, Veterans Administration (VA), Rural Housing Service, SBA

– Foreclosing can have unacceptable political costs (ie-a homeowner with a SBA disaster relief loan)

Consumer-Type Loans• Student Loans– Collateral Not Required

Risk Sharing Arrangements• With Lenders or private parties (participating schools)• They gain a stake in managing the origination and servicing of

the loans• With no financial risk the incentives become distorted

• Finding a balance is important– 20 % may not be enough if the return is greater at the

beginning (interest paid first)– BUT, 20 % may deter firms from giving credit to are not as

creditworthy

Direct Loans• Improve alignment of incentives• State may pay servicers a % of what they

collect each month in repayment

Loan GuaranteesEx-Student Loan Programs• Lenders share 5% of financial risk• Any greater and they may not give

disadvantaged students loans

Loan Terms

• Most successful federal programs – FHA- 30 year self-amortizing

mortgage, allows long term funding

– Private mortgage insurance reduces the risks of a level-payment mortgage so private industry has adopted this type of mortgage.

• Replaced “balloon mortgages” that required refinancing every few years

• Include • fees and interest rates• size of loan• Maturities• conditions of default

Addressing Elements of Financial Risk

Borrowers-• Limiting the maximum

loan-to-value requirements assures borrowers have a significant equity stake in homes and will then pay mortgage loans on time.

Government-• The Credit Reform Act

increased the governments financial accountability so they will avoid programs with high default rates

Patterns of Tool Use

U.S. National Government• The largest programs provide credit for housing, education, agriculture and

business purposes– In the last 20-30 years the number of loan guarantees have grown significantly,

direct loans have remained constant.• History

– WWI: War Finance Corporation (WFC) that became a peace time emergency finance corporation- ended in 1929

– 1932: Reconstruction Finance Corporation (RFC)- gave direct loans and stock subscriptions

– Roosevelt Administration- Started FHA, SBA, Export-Import Bank of U.S.• These revived confidence in the markets with the strength of the federal government backing

them.

– 1973-1984: Farmers Home Administration (FmHA)- bailed out lenders hit by the agricultural downturn.

– Reagan Administration- Curtail budget resources. • Push from Direct Loans to Loan Guarantees which continued until the Credit Reform Act

U.S. State and Local Governments• Have less financial capacity than the federal government• Bonds are the most common form of state credit programs• State Bond Banks

– Local governments pool together and receive lower costs and more favorable terms.

• State Revolving Loan Fund– Credit to businesses or localities to help finance long-term economic

development of environmental projects– Begins with a federal grant or long-term loan.– As money is repaid it is put back into the revolving loan fund to be given to

new borrowers.

International Experience• Germany- “Landesbanken”- provide real estate, trade, commercial loans• Japan- Government Housing Loan Corporation (GHLC)

– Provides 40% of the country’s mortgage credit though heavily subsidized loans• France- Used the “Credit Foncier de France”, a quasi-governmental mortgage

bank.– Provides subsidized credit for income-eligible homeowners.– Now use private mortgage credit banks to issue mortgage-backed bonds and fund

mortgages• United Kingdom- Student Loan Company Ltd.- non-profit adjunct of U.K

Dept. of Education.– Provides income contingent repayment of student loans though the tax department

• China- Government has given mass amounts of money to wasteful activities.• Roman Republic- 352 BCE- provided direct loans and loan guarantees to

provide relief to poor debtors. • King George III- Loans for infrastructure improvements and relieve economic

distress• Germany: Post WWII- Reconstruction Finance Corporation (RFC)- provided

support for reconstruction after the war

Basic Mechanics

Start-Up• Develop regulations, contractual agreements, loan

documents that reflect the laws that authorize the program.

• Develop forms and procedures to screen borrowers for eligibility.

• Loan guarantee- procedures to certify/decertify lenders as to edibility to participate in program.

Marketing

• Lenders and institutions need to be persuaded to participate.

• Ex- Student Loans– At first they were 100% guaranteed by the

government, but expensive to service– Large private lenders created specialized student

loan businesses to purchase loans from originating banks to lower the costs of servicing them.

– Then student loans were more widely given.

Origination• The process of actually extending a loan.

– Requires a contractual agreement between lender and borrower stating terms of the loan.

– Requires underwriting- determining if the borrower is capable of repaying the loan.• Federal business loans and home loans require using the business or house

as collateral.

– Federally guaranteed loans require the lender to sign a contract with the government for repayment of a defaulted loan.

• Direct Loans- Government originates the loan.• Loan Guarantee- Private lender originates the loan.• MORAL HAZARD: Government guarantee distorts the usual

economic behavior of the lender.– Enough fees and interest may make the lender indifferent about the

loan defaulting.– Government monitors default rates and lender performance to

combat this.

Disbursement

• Actual Transfer of funds from the government or lender to the borrower.

• Can occur all at once as with a home loan.• Can occur in stages as with a student loan.

Servicing

1. Arranging to receive timely payments from the borrower2. Receiving and accounting for funds as borrowers remit them

– Grace period: when repayment isn't necessary right away as with a student loan. – Delinquent: when the borrowers is late making a scheduled payment.– Default: when the borrower has been delinquent for a previously established

period of time • Requires either restructuring the loan or foreclosure on the loan.

• Direct Loans- serviced by the government Federal agencies are starting to contract with private firms for this

• Loan Guarantees- serviced by the lenders

• MORAL HAZARD:• Loan Guarantees-Private lenders are more carful servicing their own

unguaranteed loans than they are with their government-guaranteed loans.

• Direct Loans- The same can happen if the government contracts out their loans.

Loan Sales and Securitization• It is more economic to bundle up smaller loans and sell them to larger

companies that can service them at a lower cost.Ex- Home Mortgages

• Ginnie Mae- a secondary market institution that helps lenders to secure government-guaranteed home mortgages.– Lenders originate a large number of mortgages– They bundle them together in a trust structure– They allow investors to buy shares in the cash flow from the mortgage to the trust.– Ginnie Mae guarantees that they will receive timely repayments of both the

interest and the principle.

Ex- Student Loans• State Agencies or nonprofit organizations issue tax exempt bonds to fund

pools of student loans that they purchase from the originating lenders.

Government Loan Asset Sales

• The government uses loan asset sales as a way to receive value from loans that it holds.– Both direct loans and defaulted guaranteed loans

• In the 1980s and 90s HUD sold billions of nonperforming loans that they couldn’t collect on.

• SBA used this as a way to reduce its workload burdens when the agency downsized.

• The government can structure incentives so the private sector can collect on nonperforming loans without treating the borrowers unfairly.

Prepayment, Repayment or Collection• Prepayment- when the borrower pays off the loan ahead of

time.• Loan Guarantees- federal government is responsible for some,

others it requires the private lenders to be responsible for.– Either foreclose or forced sale of home/business– Lender then collects the federal guarantee from the government.

• Some federal programs found that borrowers are current with private obligations, but let federally guaranteed loans default.– Credit Alert Interactive Voice Response System- help screen

applicants for federal loans. This finds if they defaulted before and requires that they pay that before getting new credit.

– Federal Tax Income Offset- Allows federal credit agencies to use a borrowers income tax credit to offset some of the loss of a defaulted loan.

Write-Off and Recognition of Losses

• A loan is written-off when there are no further remedies available to mitigate the loss.– Written-off loans have no value

• No incentives for recognizing this financial loss.• Sometimes Disincentives.– Offices may use them as a way to keep more staff – China- Reluctant to close down state-owned enterprises that are

in debt.• They use this as an excuse to make large-scale mistakes that

will cost the economy for years.

Rational For Credit Programs

Market Imperfections Definition: some flaw in the market that deprives creditworthy borrowers

access to credit on appropriate terms.– Credit programs are most effective when they overcome a market imperfection.– Provide credit without risk of high levels of default.

Examples:• Economy is in disarray- Great Depression• Restrictive Legislation- confining banks to geographic locations• Discrimination- FHA: income and race• Student Loans- given even if there isn't a long history of credit

Market Imperfections are hard to find in good times.

Providing A Subsidy• The government may give out preferential terms even when there

isn't a market imperfection.

Example-Export-Import Bank of the United States: Give subsidized loans so foreign governments wont give their own loans and deprive U.S. firms of those markets.

• Government does not always made wise decisions when giving a subsidy.– Creditworthy people may need credit and not subsidies– Non-creditworthy people may need subsidies or grants and not credit.

Government Credit as a Pioneer

• FHA- pioneered the 30 year level payment mortgage that private lenders use today.

• By giving disadvantages borrowers credit they can show private lenders that those borrowers are profitable credit risks.

• The government has to be willing to turn over large numbers of creditworthy borrowers when their program succeeds.

Political Considerations

Developing a Constituency

• Credit programs can be hard to start and hard to end.

• Start- constituencies may not welcome the change and business disrupt.

• End- A successful program will develop a constituency whose well-being will be threatened if the program is terminated.

The Choice between Direct Loans and Loan Guarantees

• Involves political considerations

• Private firms prefer loan guarantees because they keep government participation low.– Lender can earn the fees and interest– Lender develops a relationship with the borrower

which may lead to more loans in the future.– Lenders see direct loans as a competitive threat• Unless they are to the least creditworthy borrowers

Constituencies as a Source of Inertia

• Lenders provide a strong base for the program and inertia to maintain the features of the program.

• Ex- Dept. of Education– Developed formalistic standards of performance to

keep defaults low• Lenders objected- used performance based standards

– Now the Dept. is trying to switch to performance based measures• Lenders objected- don’t want the rules to change again

Program Expansion

• When constituencies emerge Congress may expand the program to include borrowers not originally helped by the program.

Ex-Student Loans– Students that could not show financial need were

permitted to take out loans.

Ex- FHA- was middle-class and suburbs– Included central cities-low income renters and homebuyers

Credit Budget Politics

• Credit Reform Act of 1990- All credit programs are subject to annual budget constraints.

• Congress then reduces the amount of subsidy provides so the amount appropriated can serve more people.

Ex- Student Loans– Students could take out unsubsidized loans regardless of financial

need.– Students make interest payments on these, which the government

only makes payments for the subsidized loans.

Ex- SBA– Increased the amount of risk sharing with private lenders.– Increased the loan-related fees for borrowers.

Management Challenges and Potential Responses

Balancing Risks and Mission• Maintain balance between doing “good” and doing “well”• Extend credit to creditworthy borrowers that need it while ensuring the program does not

incur unacceptable losses.

• Financial problems take years to become apparent which gives them time to accumulate large amount of potential losses.

• Political environmentsEx- congress will give the SBA funds to help business in need, but not money to

cover servicing or foreclosure.

• Wholly government owned organizations do this the best.– They are meant to be self-sustaining

Capacity• Availability of staff and systems to maintain program

– Hiring freezes and mandatory staff reductions

Ex- Ginnie Mae– 1993: 70 staff for hundreds of billions of dollars in mortgage-backed

securities– 1999: 56 staff for $540 Billion in securities

• Policymakers will allocate more money to the programs with the most defaults

• Staff Quality and Training– Less young professionals with new ideas and technology-hiring freezes– More prosperous alternatives in the private market

• “Hollow Government”• Government contracts out, but needs staff to assure relationship between government

and contractors.

Keeping Third Parties Accountable

• Government is devoting increased resources to monitoring performance

Ex- Ginney Mae– 1980s- mortgage backed securities defaulted

• Agency added an information system to tract loan originators.• Monitor default rates and delinquencies so they can act before there is an

unacceptable financial loss.

• Effectiveness depends on legal authority given to agency– Ex- Student Loans- Dept. of Education could take action against schools and the number of

defaulting loans has dropped.

• Accountability- status of defaulted individuals now has to be reported to the credit bureaus.

Adverse Selection• Private lenders want to keep the most profitable loans

and send less profitable ones to the government.

• Many credit programs will only take people that have been turned down by private firms.

• Government credit is at a standard price so private firms want to offer a better price to more creditworthy borrowers.– As they leave government programs the government is left

with a higher proportion of less creditworthy borrowers.– FHA mortgages were 1.9 times more likely to default before

and are not 4.4 times more likely.

Overall Assessment

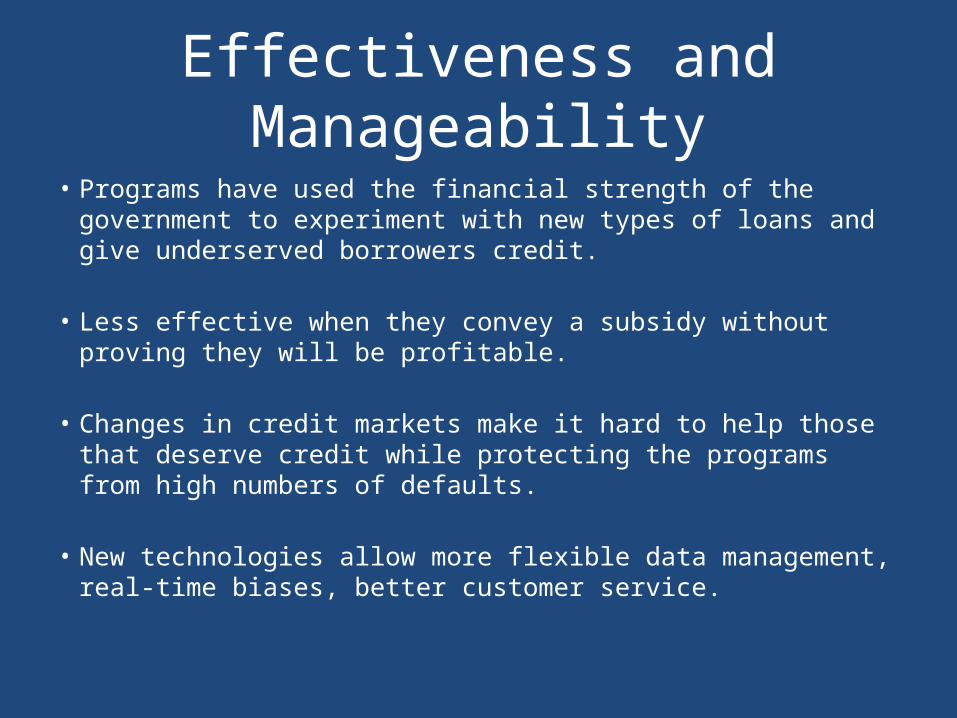

Effectiveness and Manageability• Programs have used the financial strength of the government to

experiment with new types of loans and give underserved borrowers credit.

• Less effective when they convey a subsidy without proving they will be profitable.

• Changes in credit markets make it hard to help those that deserve credit while protecting the programs from high numbers of defaults.

• New technologies allow more flexible data management, real-time biases, better customer service.

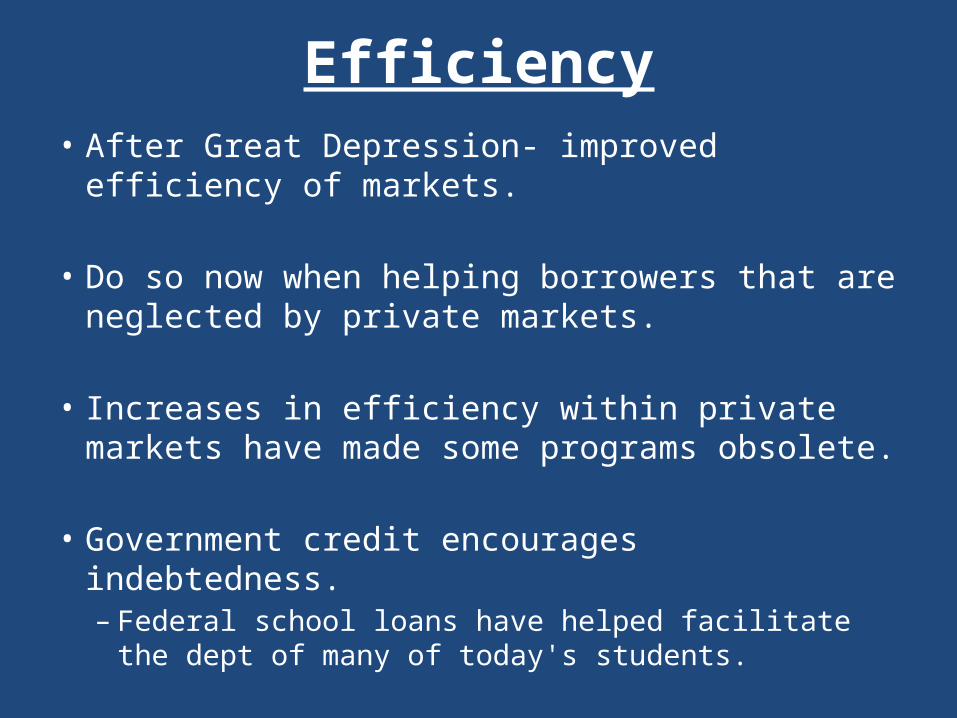

Efficiency• After Great Depression- improved efficiency of

markets.

• Do so now when helping borrowers that are neglected by private markets.

• Increases in efficiency within private markets have made some programs obsolete.

• Government credit encourages indebtedness.– Federal school loans have helped facilitate the dept of

many of today's students.

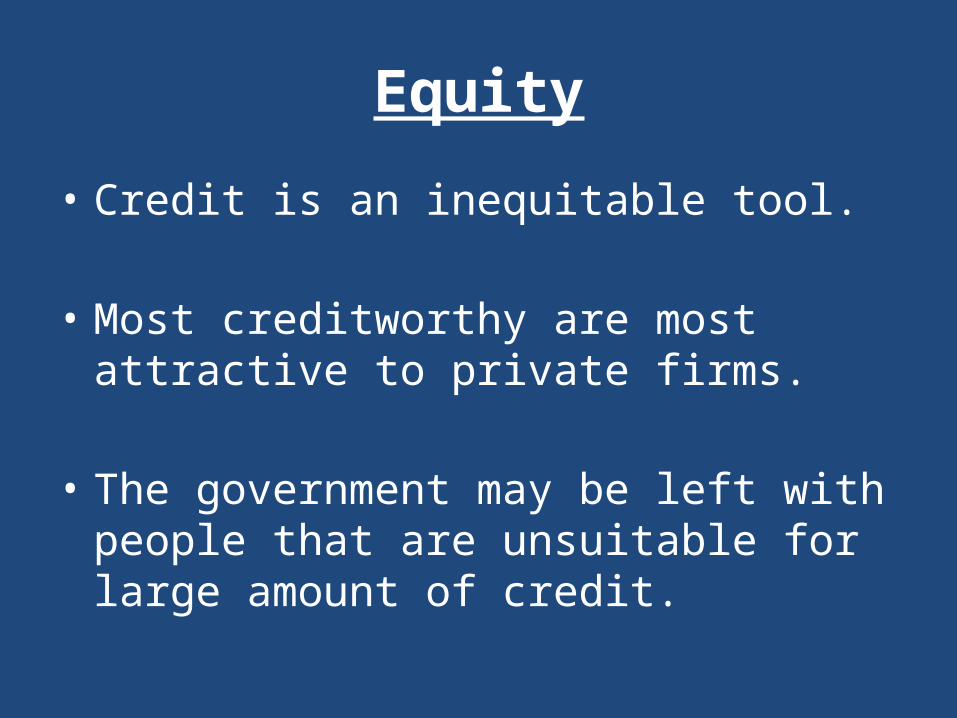

Equity

• Credit is an inequitable tool.

• Most creditworthy are most attractive to private firms.

• The government may be left with people that are unsuitable for large amount of credit.

Legitimacy

• Policymakers favor credit because of the expectation that the money will be paid back.

• Most popular– SBA- helps people that were creditworthy, but have

suddenly come upon a hardship.

• When credit programs fail they hurt borrowers and the tax payers that must pay for them.

Future Direction

• The available tasks for government credit are more diminished than ever before.

• Credit programs require high quality of institution that administers the program, financial soundless of program, and a good exit strategy so the program will end as a success.

• Need to improve design and management of institutions and learn from past experiences.