Daimler Chrysler

10

POST MERGER INTEGRATION CHALLENGES

-

Upload

rebeca-osuna -

Category

Documents

-

view

213 -

download

1

description

Post-merger integration challenges

Transcript of Daimler Chrysler

POST MERGER INTEGRATION CHALLENGES

1. EXECUTIVE SUMMARY

2. DAIMLER CHRYSLER SWOT ANALYSIS

3. INNOVATION CHALLENGES

4. STRATEGIC INITIATIVES & ROADMAP

During the last few years, production and innovation strategies have revolutionized worldwide the automobile industry. Globalization in the supply chain, changing demand, and increasing competition are some of the main elements changing the face of the industry. It’s evident that the size of the organization is no longer a guarantee of success. Only those companies that find innovative ways to create value may prosper in the future. Development departments are not just overburdened by the complexity of new technologies, but also by the shortening of product lifecycles. Another aspect is the increasing number of parallel development projects since companies develop more and more niche models for special target groups and the opening up and growth of several emerging markets. Under this scenario, Daimler Benz and Chrysler Corporation are facing new and pressing challenges in the development of a well executed merger. The purpose of this paper is to present a short overview of the sources of competitive advantage and strategic cost efficiency opportunities that must be analyzed during the merging of both companies. Based on this perspective, a strategic roadmap will be presented at the end to help DaimlerChrysler become a highly competitive business venture.

EXECUTIVE SUMMARY

2. SWOT ANALYSIS

Trustworthiness and brand recognition , the consolidation of Chrysler and Mercedes represents becoming the fifth largest automobile manufacturer in vehicles sales and third largest in revenues.

Chryslers experience in supplier cost reduction and leading edge technologies of Mercedes can help both companies achieve strategic excellence in coming years.

Significantly greater geographic scope , this gives Daimler Chrysler a chance to expand to new emerging markets, but also increases the threat of new entrants or increased competition in

traditional markets.

Sour

ces

of C

ompe

titiv

e

Adv

anta

ge

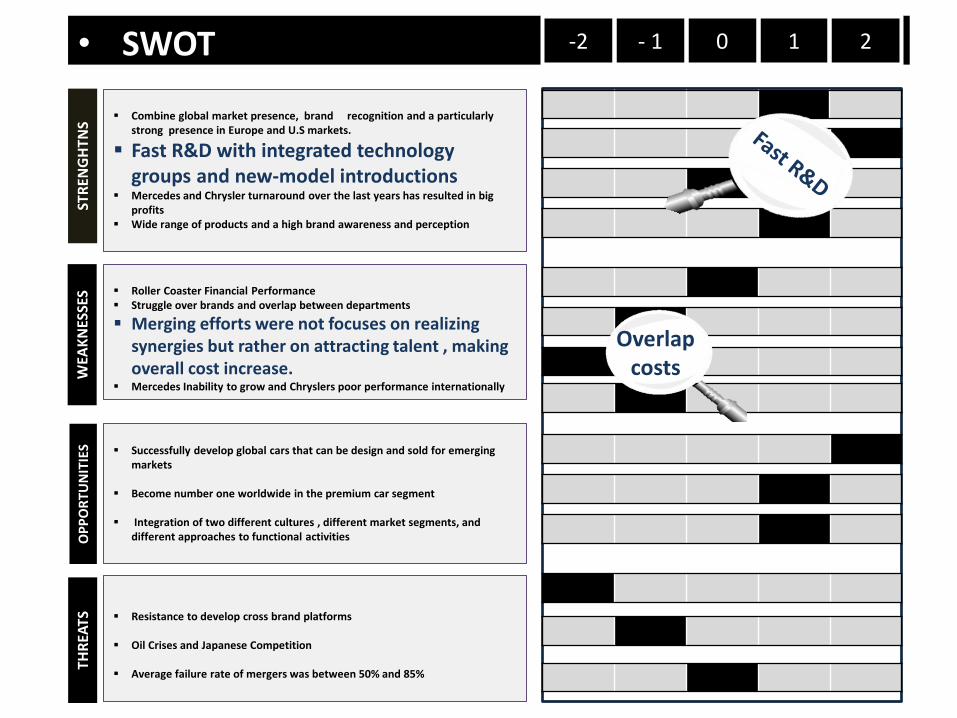

• SWOT

Global market presence, brand recognition and a particularly strong presence in Europe.

Poor Profitability: Ford still loses money on many automobile lines, particularly within the United States

Economic slowdown in the US and Eurozone And intense competition.

Bankruptcy of Visteon or other parts supplier could cause severe disruption of supply chain. While Ford has too many dealers at this time, it should remain wary of too many closures. In addition, because Ford Credit provides financing for most dealers it must be careful to avoid holding the bag when dealerships close. While Ford is readjusting production, truck sales are falling rapidly and Ford may not be able to shift production quickly enough to meet changing demand

Increased demand for fuel dual free vehicles, It is expected to reach 4.5 million units in 2013 The ‘One Ford’ vision has the chance to generate significant margin increases for Ford’s smaller line of vehicles. Of particular importance is the Ford Fiesta, which has achieved brilliant results in Emerging markets such as India and China. The ‘One Ford’ vision appears to be a coherent strategy for Ford to adopt given its changed role within the industry. GM and Chrysler flexibility is limited by government involvement in their debt situation, putting Ford as a competitive advantage

THR

EATS

O

PP

OR

TUN

ITIE

S W

EAK

NES

SES

STR

ENG

HT

NS

Combine global market presence, brand recognition and a particularly

strong presence in Europe and U.S markets.

Fast R&D with integrated technology groups and new-model introductions

Mercedes and Chrysler turnaround over the last years has resulted in big profits

Wide range of products and a high brand awareness and perception

Roller Coaster Financial Performance Struggle over brands and overlap between departments

Merging efforts were not focuses on realizing synergies but rather on attracting talent , making overall cost increase.

Mercedes Inability to grow and Chryslers poor performance internationally

Successfully develop global cars that can be design and sold for emerging

markets Become number one worldwide in the premium car segment Integration of two different cultures , different market segments, and

different approaches to functional activities

Resistance to develop cross brand platforms Oil Crises and Japanese Competition Average failure rate of mergers was between 50% and 85%

-2 - 1 0 1 2

Poor Profitability: Ford still loses money on many automobile lines, particularly within the United States

Overlap costs

3. INNOVATION CHALLENGES

The market is developing new segments and facing

the reintroduction of some old top brands

The vision of the global car had been evolving for most manufacturers, in

which one common design, manufactured with components

built through the world, would be sold in all markets.

Global competition in emerging markets with a

stronger focus on price and not on brand loyalty.

SUPPLY CHAIN GLOBALIZATION

CHANGING DEMAND

FIERCE COMPETITION

ALIGNMENT OF INNOVATION STRATEGY

COMPETITOR INNOVATION ARCHETYPE

INNOVATION PROPOSITION

FOCUS AND COLLABORATION

BUSINESS CASE

BMW Brand Builder Brand oriented product innovations Mid size

volumes high end customers

Specialized focus strong supplier coops and R&D

outsourcing

Low cost, Fairly weak IP protection

Daewoo Hyundai

Fast Follower Improves innovations and brings them to the mass-

market

Medium focus selective coops , extensive R&D

outsourcing

Low costs , Weak IP protection, brand image

Ford / GM Mass-market adapter Adapts and improves existing product

innovations

Broad focus R&D outsourcing of whole

systems limited network

Cost-oriented innovations fairly strong IP protection

Toyota / VW Architectural revolutionizer

Focuses largely on process innovation shifts from mass to niche markets

Network builder modularization limited

R&D outsourcing

Innovations Strong IP Protection Brand image

Porshe / Hummer

High-end optimizer Premium product innovation by systems and components enhancement

Specialized focus very limited R&D outsourcing

Innovations , strong IP protection brand image

Kia / Dacia Cost and process specialist

Innovations based on new manufacturing process customer orientation

Broad focus Medium R&D outsourcing formal

partners

Low cost product , fairly strong IP protection

1

In order to achieve a competitive position and a long-term profitability DaimlerChrysler needs to analyze the overall innovation strategy of its competitors. The below chart can serve as a benchmark analysis to understand, check and improve the different aspects of innovation around the automobile industry.

2

3 4

5

6

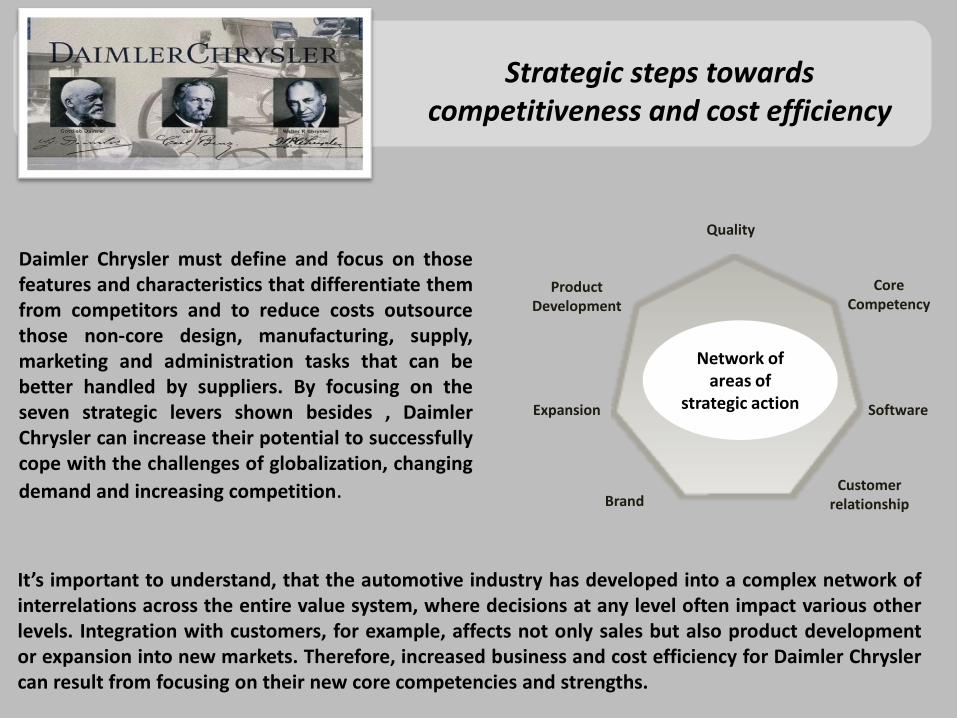

Strategic steps towards competitiveness and cost efficiency

Network of areas of

strategic action

Quality

Core Competency

Software

Customer relationship

Product Development

Expansion

Brand

Daimler Chrysler must define and focus on those features and characteristics that differentiate them from competitors and to reduce costs outsource those non-core design, manufacturing, supply, marketing and administration tasks that can be better handled by suppliers. By focusing on the seven strategic levers shown besides , Daimler Chrysler can increase their potential to successfully cope with the challenges of globalization, changing

demand and increasing competition.

It’s important to understand, that the automotive industry has developed into a complex network of interrelations across the entire value system, where decisions at any level often impact various other levels. Integration with customers, for example, affects not only sales but also product development or expansion into new markets. Therefore, increased business and cost efficiency for Daimler Chrysler can result from focusing on their new core competencies and strengths.

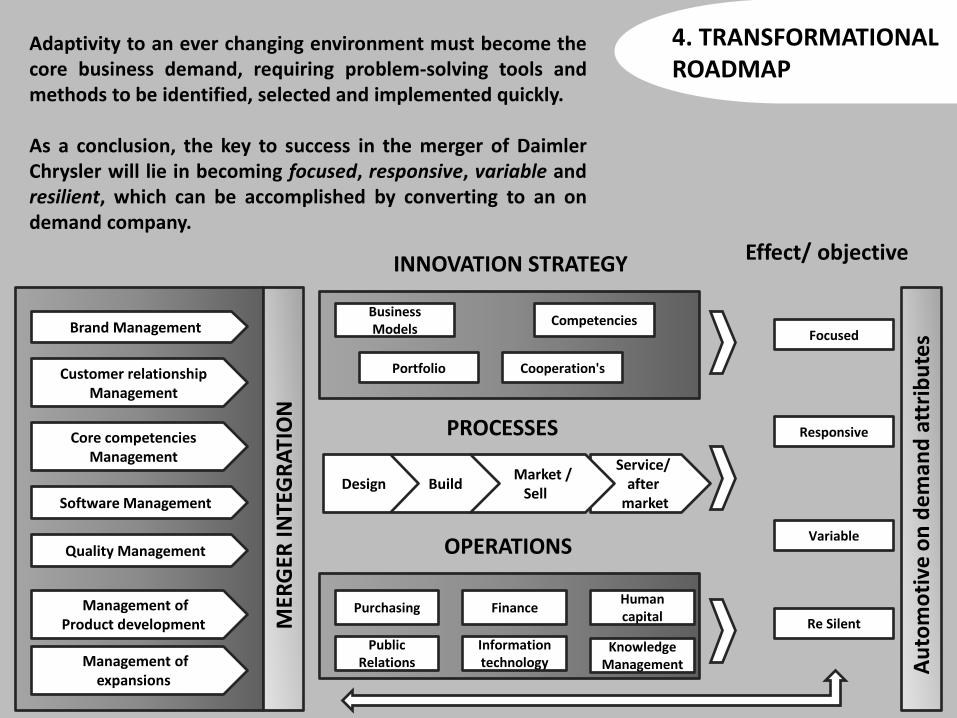

4. TRANSFORMATIONAL ROADMAP

Brand Management

Customer relationship Management

Core competencies Management

Software Management

Quality Management

Management of Product development

Management of expansions

MER

GER

INTE

GR

ATI

ON

INNOVATION STRATEGY Effect/ objective

Business Models

Portfolio

Competencies

Cooperation's

PROCESSES

OPERATIONS

Public Relations

Purchasing Finance Human capital

Information technology

Knowledge Management

Service/ after

market

Market / Sell

Build Design

Focused

Responsive

Variable

Re Silent

Au

tom

oti

ve o

n d

em

and

att

rib

ute

s

Adaptivity to an ever changing environment must become the core business demand, requiring problem-solving tools and methods to be identified, selected and implemented quickly. As a conclusion, the key to success in the merger of Daimler Chrysler will lie in becoming focused, responsive, variable and resilient, which can be accomplished by converting to an on demand company.

How to Identify and Build Disruptive New Businesses, MIT Sloan Management Review Spring 2002

Christensen, Clayton M. (1997), The innovator's dilemma: when new technologies cause great firms to fail, Boston, Massachusetts, USA: Harvard Business School Press, ISBN978-0-87584-585-2

Mercer Management Consulting/Marco Ehmer, 2002: Automobiltechnologie 2010. http://www.vectorinformatik.com/ongress/VeCo_Vortrag04_Ehmer.pdf

Christensen, Clayton M. (2003). The innovator's solution : creating and sustaining

successful growth. Harvard Business Pres

Sources :

The information and opinions presented in this paper are based on a series of publications written by

automotive industry experts, who gave the benefit of their extensive knowledge.

![State ex rel. Daimler Chrysler Corp. v. Indus. Comm.Cite as State ex rel. Daimler Chrysler Corp. v. Indus. Comm., 2014-Ohio-2072.] IN THE COURT OF APPEALS OF OHIO TENTH APPELLATE DISTRICT](https://static.fdocuments.in/doc/165x107/5add1d427f8b9a9a768c6a39/state-ex-rel-daimler-chrysler-corp-v-indus-comm-cite-as-state-ex-rel-daimler.jpg)