CYH Pitchbook

32

1 Community Health Systems, Inc. Strategic Discussion Materials | April 17, 2015

-

Upload

richard-cao -

Category

Business

-

view

71 -

download

4

Transcript of CYH Pitchbook

1

Community Health Systems, Inc.

Strategic Discussion Materials | April 17, 2015

2

Keith Radzik is Co-Global Head of Healthcare Investment Banking at Rightview

Partners. Before joining Rightview, Keith majored in Finance and Entrepreneurship at

Indiana University – Kelley School of Business. Prior work experience includes an internship at Granite Creek Partners, LLP in

Chicago, IL. Keith plans to study abroad at the London School of Economics

while enrolling in two banking and valuation classes.

Clayton Stoker is Co-Global Head of Healthcare Investment Banking at Rightview

Partners. Before joining Rightview, Clayton majored in Finance and Accounting at Indiana

University – Kelley School of Business. Prior work experiences include internships at, Smith Moore, The Audit Group and

Tobin & Company Investment Banking Group. This summer he will be joining

Janes Capital Partners in Irvine, California doing Aerospace and Defense M&A.

Rightview Partners

Richard Cao is a Managing Director in Healthcare Investment Banking at

Rightview Partners. Before joining Rightview, Richard majored in Finance and Accounting at Indiana

University – Kelley School of Business. Prior work experience includes an internship at Systemax, Inc. in Port

Washington, NY. Richard plans to return to work at Systemax this summer in

their Industrials group.

Nathan Upchurch is a Managing Director in Mergers and Acquisitions at

Rightview Partners. Before joining Rightview, Nathan majored in Finance and Entrepreneurship at

Indiana University – Kelley School of Business. Prior work experience includes Project Manager at MEU Holding, LLC in Appleton,

WI. Nathan will be joining Trilliant Solutions this summer as an intern.

3

Table of Contents

I. Executive Summary

4

II. Overview of the Hospital Industry

6

III. Community Health Systems Overview

9

IV. Valuation Summary 12

V. Strategic Recommendation

15

VI. Merger Model

19

VII. Appendix 24

4

I. Executive Summary

5

Executive Summary

Because of high M&A multiples being achieved in the hospital sector, Rightview Partners believe selling CYH to UHS is the best strategic alternative.

If management desires their company and seeks an acquisition, Lifepoint Hospitals provides the best target to achieve cost synergies while maintaining a sufficient D/E level.

Overview Community Health Systems, Inc. (CYH) is a leading operator of non-urban acute care hospitals in midsize

markets in the United States. The company currently owns, leases or operates 206 hospitals in 29

different states making it the most diversified operator among competitors. Community Health has used acquisitions as their primary method of growth. The successful integration of

31 hospitals since 2010, including Health Management Associates, Inc. in 2014, has made it the largest

publicly traded acute care hospital operator in the nation. The company’s subsidiary, Quorum Health Resources, LLC, provides management and consulting services

to 150 independent hospital clients. This industry is mature with stable operations.

Current Positioning Community Health recently acquired Health Management Associates, Inc. at $7.5B with $3.7B in debt The hospital operator has a net debt to EDITDA ratio of 6.4x ranking the second highest among

competitors due to the acquisition and integration of HMA in 2014. CYH is currently trading at a P/E of 60. ACA reform and Medicaid expansion is expected to enhance future EBITDA not only through a decrease in

bad debt expense, but through significant synergies due to the HMA acquisition. Because CYH is highly leveraged, Rightview Partners believe that acquiring a company must be through

an all equity deal, or sale to a potential acquirer.

Strategic Alternatives Assessment Given Community Health Systems established presence as the leading acute health care operator, we

believe future growth from increased Emergency Room visits will be key to attract potential buyers and

mergers as a result of expansion of Medicaid, increase in managed care, and the notable correlation of

reduction in unemployment rate with ER volumes. Medicaid expansion in 13 states, including PA which accounts for 12% of LTM revenue, will continue to

foster consistent growth, further attracting potential acquirers. Recommendations

Rightview Partners believe that CYH sell to Universal Health Services due to the combination of high

multiples that hospital companies are achieving in the M&A market and its highly levered capital

structure. If prompted to make an acquisition, Rightview Partners sees Lifepoint as the most logical potential target

due to similar business plans and a favorable accretion and dilution model.

6

II. Hospital Services Industry

7

Macroeconomic Landscape

Macroeconomic trends point to a higher population of insured individuals, but are subject to hazy government reimbursement levels

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

-

10

20

30

40

50

60

US Age 65+ Population (in millions)

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

$11,000

$12,000

$13,000

$14,000

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%US Unemployment Rate vs. Disposable

Income

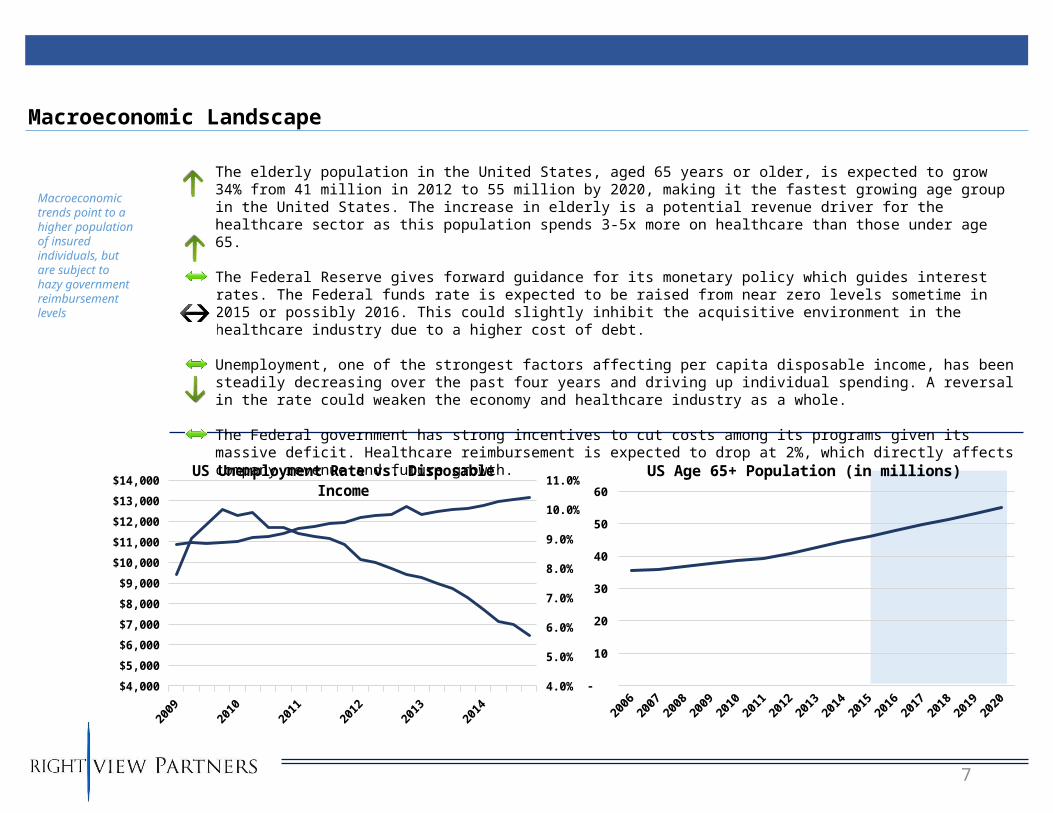

The elderly population in the United States, aged 65 years or older, is expected to grow 34% from 41 million in 2012 to 55 million by 2020, making it the fastest growing age group in the United States. The increase in elderly is a potential revenue driver for the healthcare sector as this population spends 3-5x more on healthcare than those under age 65.

The Federal Reserve gives forward guidance for its monetary policy which guides interest rates. The Federal funds rate is expected to be raised from near zero levels sometime in 2015 or possibly 2016. This could slightly inhibit the acquisitive environment in the healthcare industry due to a higher cost of debt.

Unemployment, one of the strongest factors affecting per capita disposable income, has been steadily decreasing over the past four years and driving up individual spending. A reversal in the rate could weaken the economy and healthcare industry as a whole.

The Federal government has strong incentives to cut costs among its programs given its massive deficit. Healthcare reimbursement is expected to drop at 2%, which directly affects company revenue and future growth.

8

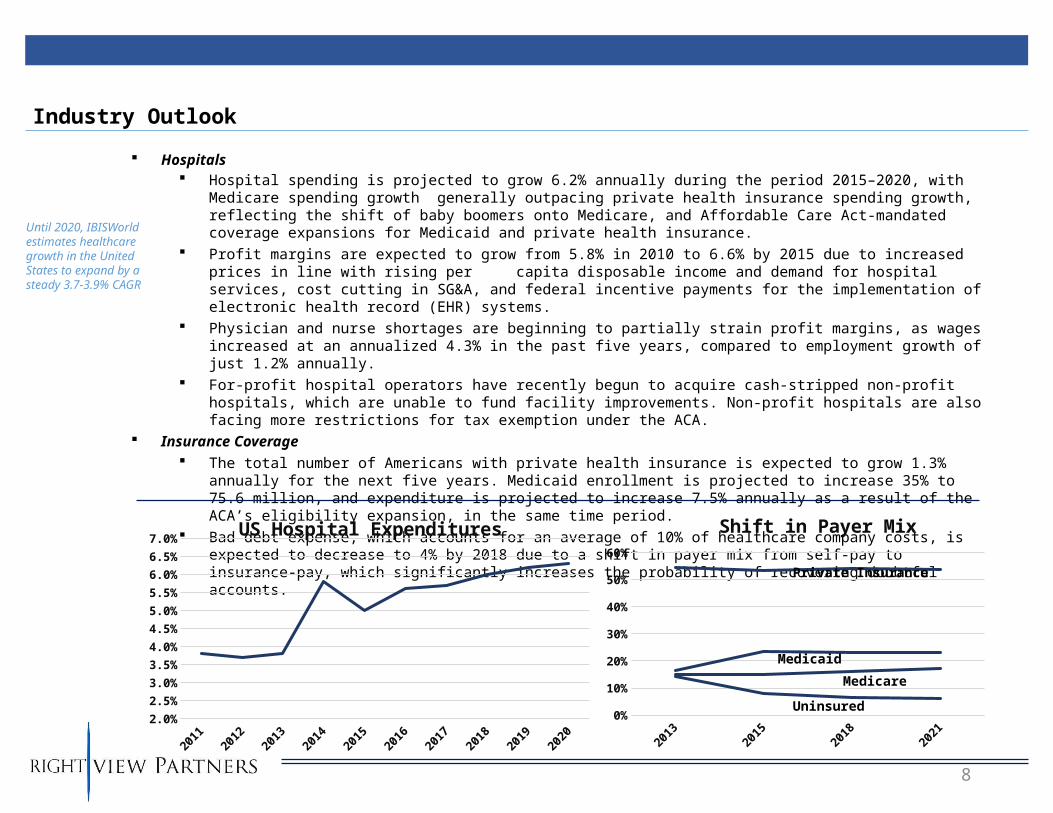

Hospitals Hospital spending is projected to grow 6.2% annually during the period 2015–2020, with Medicare

spending growth generally outpacing private health insurance spending growth, reflecting the shift of baby boomers onto Medicare, and Affordable Care Act-mandated coverage expansions for Medicaid and private health insurance.

Profit margins are expected to grow from 5.8% in 2010 to 6.6% by 2015 due to increased prices in line with rising per capita disposable income and demand for hospital services, cost cutting in SG&A, and federal incentive payments for the implementation of electronic health record (EHR) systems.

Physician and nurse shortages are beginning to partially strain profit margins, as wages increased at an annualized 4.3% in the past five years, compared to employment growth of just 1.2% annually.

For-profit hospital operators have recently begun to acquire cash-stripped non-profit hospitals, which are unable to fund facility improvements. Non-profit hospitals are also facing more restrictions for tax exemption under the ACA.

Insurance Coverage The total number of Americans with private health insurance is expected to grow 1.3% annually for the

next five years. Medicaid enrollment is projected to increase 35% to 75.6 million, and expenditure is projected to increase 7.5% annually as a result of the ACA’s eligibility expansion, in the same time period.

Bad debt expense, which accounts for an average of 10% of healthcare company costs, is expected to decrease to 4% by 2018 due to a shift in payer mix from self-pay to insurance-pay, which significantly increases the probability of recovering doubtful accounts.

Until 2020, IBISWorld estimates healthcare growth in the United States to expand by a steady 3.7-3.9% CAGR

Industry Outlook

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%US Hospital Expenditures

2013

2015

2018

2021

0%

10%

20%

30%

40%

50%

60%

Shift in Payer Mix

Private Insurance

Medicaid

Medicare

Uninsured

9

III. Community Health Systems Overview

10

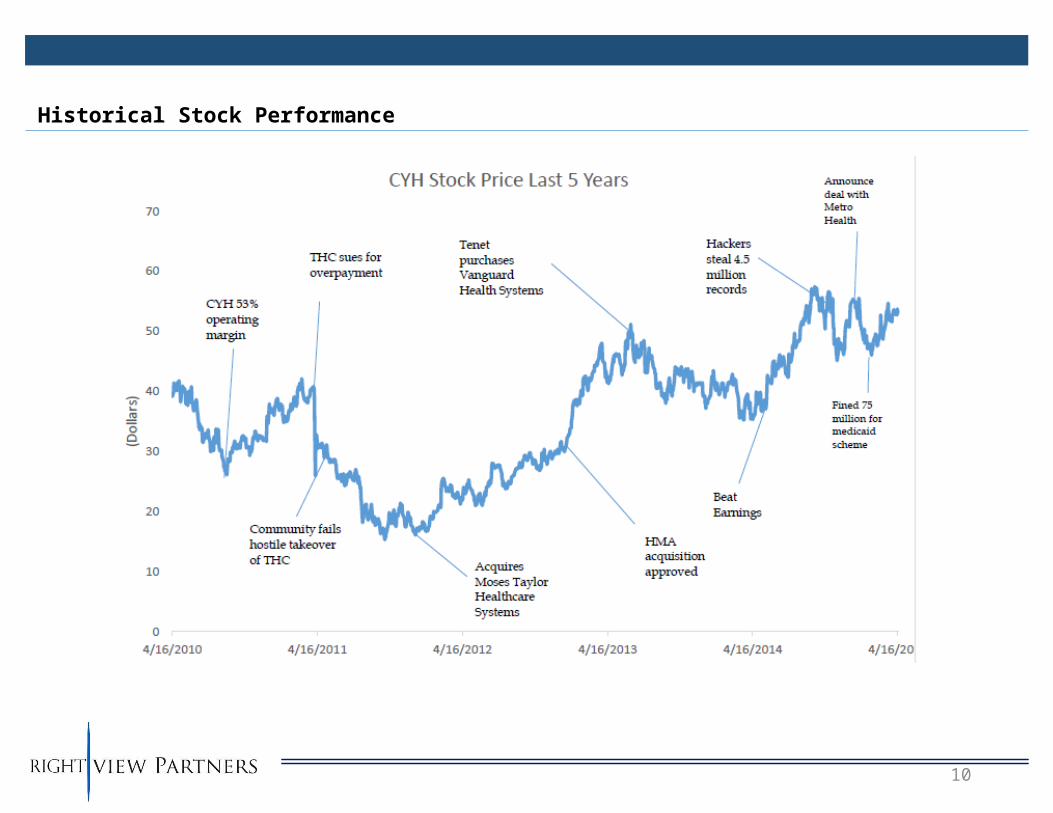

Historical Stock Performance

11

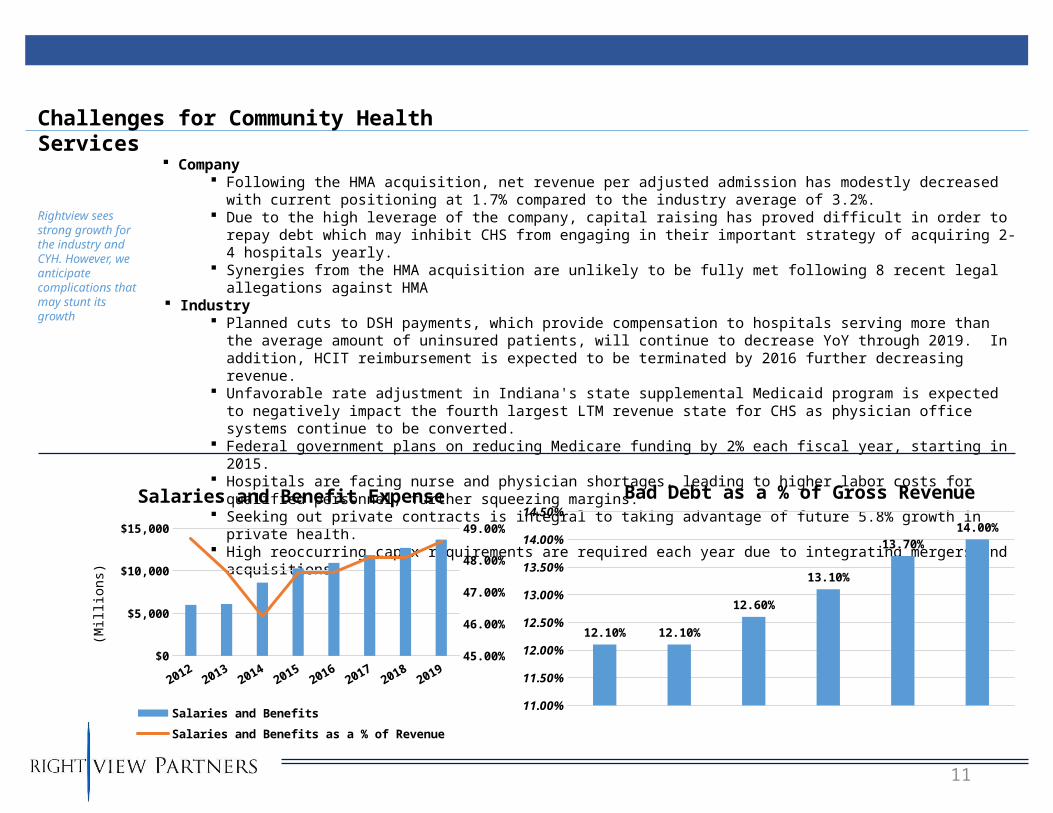

Rightview sees strong growth for the industry and CYH. However, we anticipate complications that may stunt its growth

Company Following the HMA acquisition, net revenue per adjusted admission has modestly decreased with current

positioning at 1.7% compared to the industry average of 3.2%. Due to the high leverage of the company, capital raising has proved difficult in order to repay debt which

may inhibit CHS from engaging in their important strategy of acquiring 2-4 hospitals yearly. Synergies from the HMA acquisition are unlikely to be fully met following 8 recent legal allegations against

HMA Industry

Planned cuts to DSH payments, which provide compensation to hospitals serving more than the average amount of uninsured patients, will continue to decrease YoY through 2019. In addition, HCIT reimbursement is expected to be terminated by 2016 further decreasing revenue.

Unfavorable rate adjustment in Indiana's state supplemental Medicaid program is expected to negatively impact the fourth largest LTM revenue state for CHS as physician office systems continue to be converted.

Federal government plans on reducing Medicare funding by 2% each fiscal year, starting in 2015. Hospitals are facing nurse and physician shortages, leading to higher labor costs for qualified personnel,

further squeezing margins. Seeking out private contracts is integral to taking advantage of future 5.8% growth in private health. High reoccurring capex requirements are required each year due to integrating mergers and acquisitions.

Challenges for Community Health Services

11.00%

11.50%

12.00%

12.50%

13.00%

13.50%

14.00%

14.50%

12.10% 12.10%

12.60%

13.10%

13.70%14.00%

Bad Debt as a % of Gross Revenue

20122013

20142015

20162017

20182019

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

45.00%

45.50%

46.00%

46.50%

47.00%

47.50%

48.00%

48.50%49.00%

Salaries and Benefit Expense

Salaries and Benefits

Salaries and Benefits as a % of Revenue

(Millions)

12

IV. Valuation Summary

13

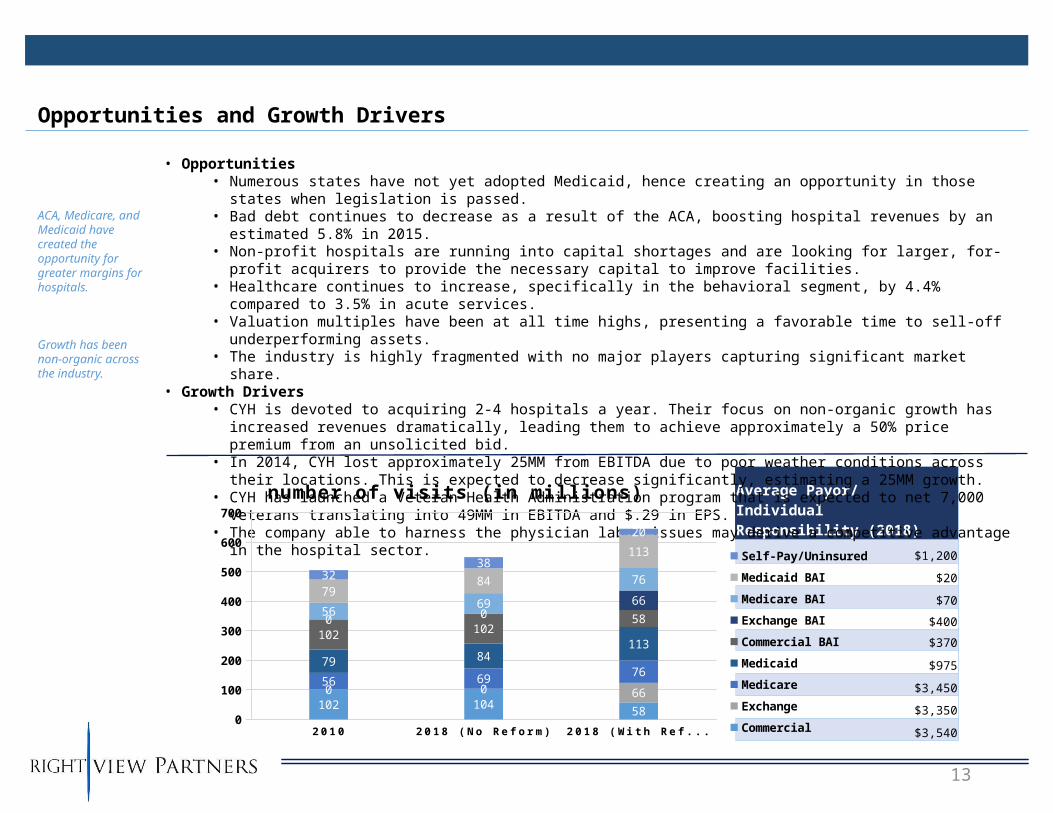

Average Payor/Individual Responsibility (2018)

$1,200

$20

$70

$400

$370

$975

$3,450

$3,350

$3,540

• Opportunities• Numerous states have not yet adopted Medicaid, hence creating an opportunity in those states when

legislation is passed.• Bad debt continues to decrease as a result of the ACA, boosting hospital revenues by an estimated 5.8% in

2015.• Non-profit hospitals are running into capital shortages and are looking for larger, for-profit acquirers to

provide the necessary capital to improve facilities.• Healthcare continues to increase, specifically in the behavioral segment, by 4.4% compared to 3.5% in

acute services.• Valuation multiples have been at all time highs, presenting a favorable time to sell-off underperforming

assets.• The industry is highly fragmented with no major players capturing significant market share.

• Growth Drivers• CYH is devoted to acquiring 2-4 hospitals a year. Their focus on non-organic growth has increased

revenues dramatically, leading them to achieve approximately a 50% price premium from an unsolicited bid.

• In 2014, CYH lost approximately 25MM from EBITDA due to poor weather conditions across their locations. This is expected to decrease significantly, estimating a 25MM growth.

• CYH has launched a Veteran Health Administration program that is expected to net 7,000 veterans translating into 49MM in EBITDA and $.29 in EPS.

• The company able to harness the physician labor issues may derive a competitive advantage in the hospital sector.

ACA, Medicare, and Medicaid have created the opportunity for greater margins for hospitals.

Growth has been non-organic across the industry.

Opportunities and Growth Drivers

2 0 1 0 2 0 1 8 (No Ref o rm) 2 0 1 8 (W i th Ref o rm)

0

100

200

300

400

500

600

700

102 104 58

0 0 6656 69 7679 84

113102 102

580 066

5669

7679

84

113

3238

20

number of visits (in mill ions)

Self-Pay/Uninsured

Medicaid BAI

Medicare BAI

Exchange BAI

Commercial BAI

Medicaid

Medicare

Exchange

Commercial

14

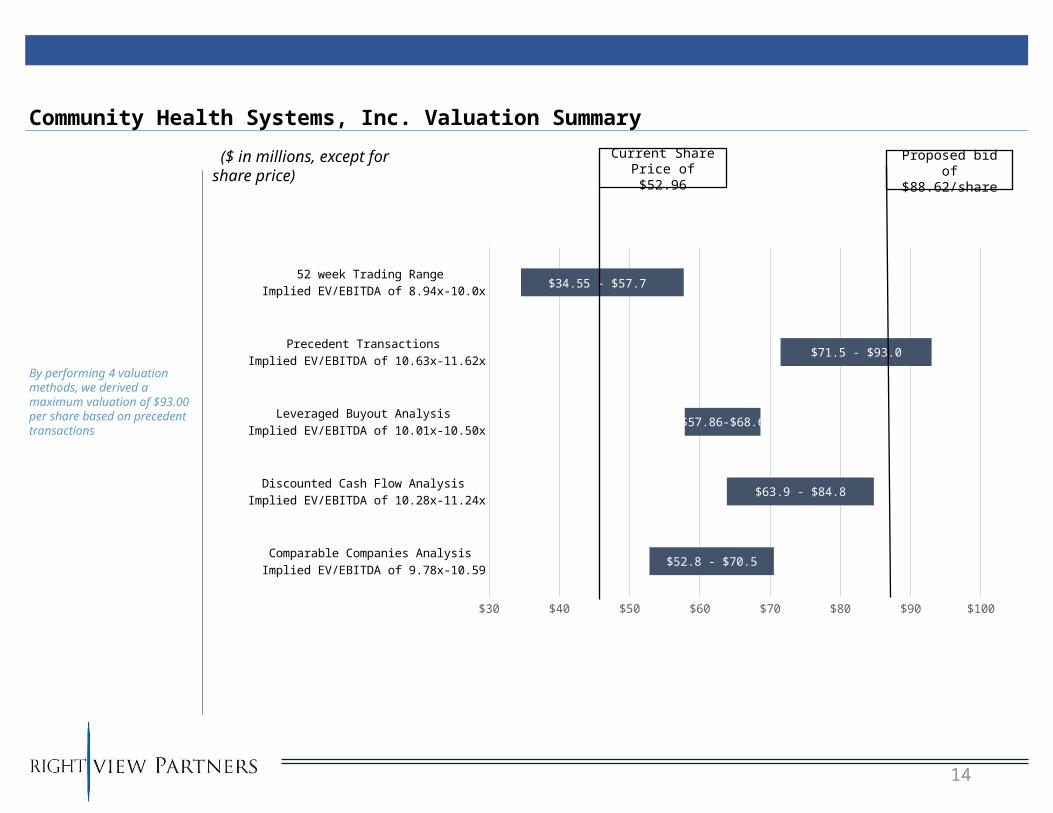

Community Health Systems, Inc. Valuation Summary

By performing 4 valuation methods, we derived a maximum valuation of $93.00 per share based on precedent transactions

($ in millions, except for share price)

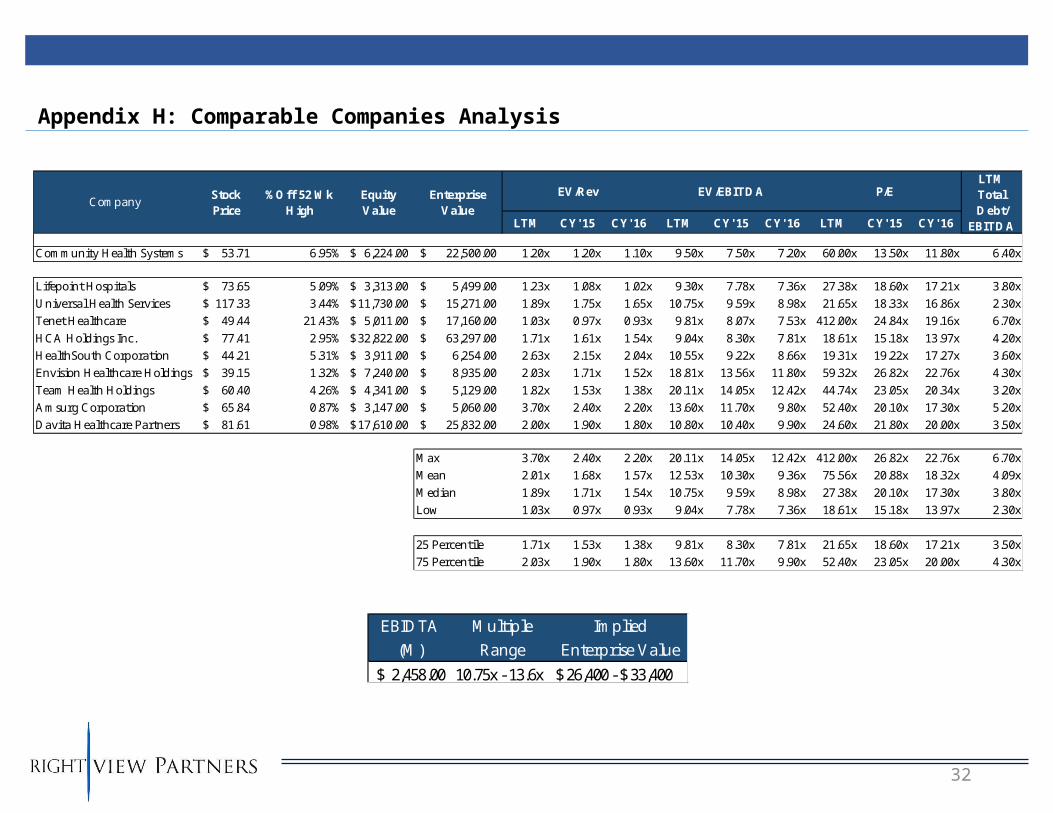

Comparable Companies Analysis Implied EV/EBITDA of 9.78x-10.59

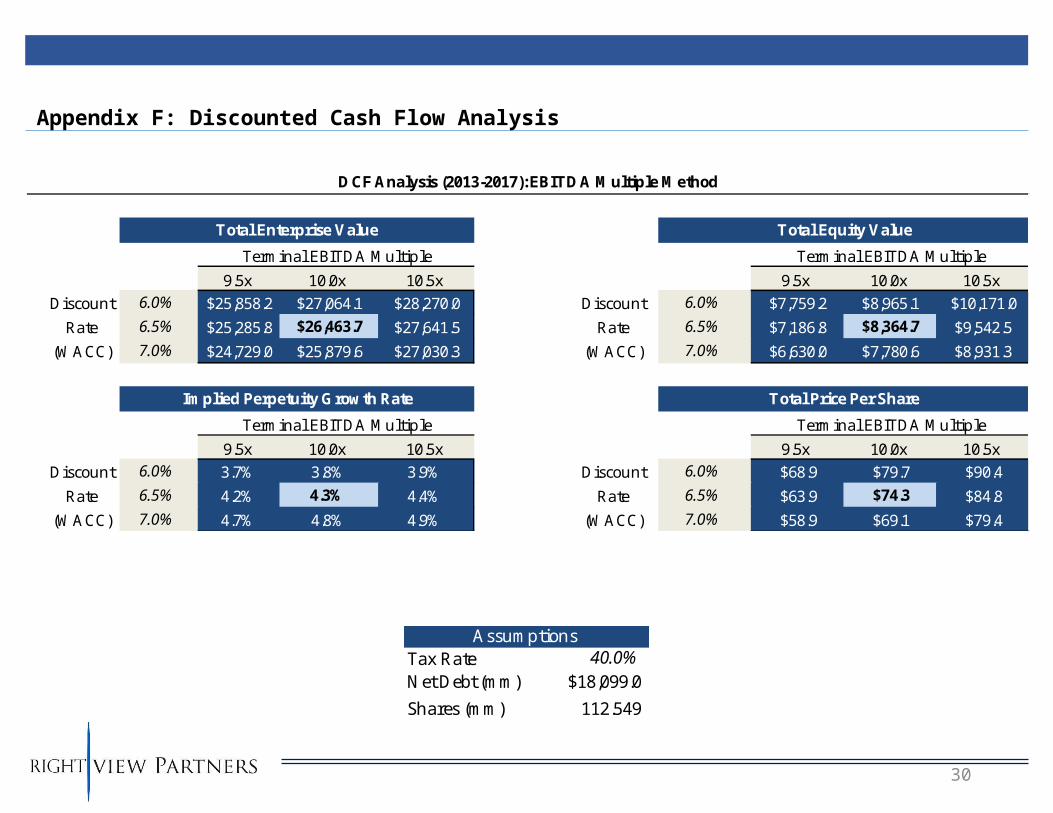

Discounted Cash Flow Analysis Implied EV/EBITDA of 10.28x-11.24x

Leveraged Buyout Analysis Implied EV/EBITDA of 10.01x-10.50x

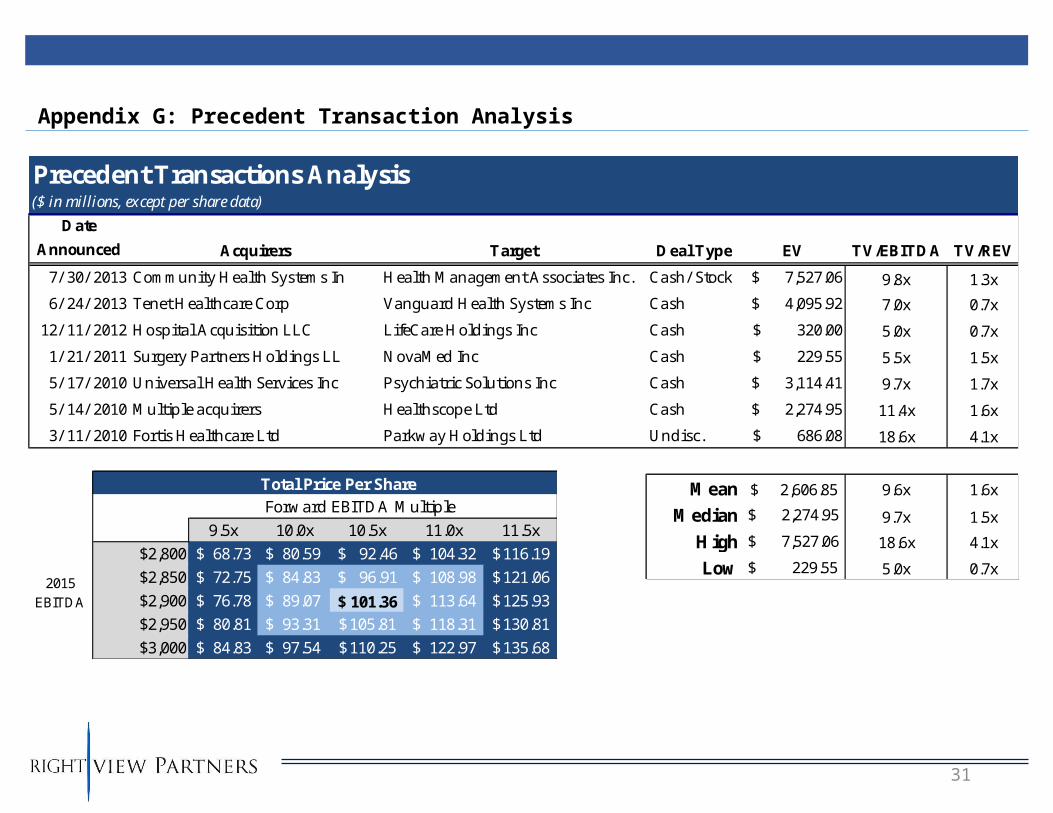

Precedent Transactions Implied EV/EBITDA of 10.63x-11.62x

52 week Trading Range Implied EV/EBITDA of 8.94x-10.0x

$30 $40 $50 $60 $70 $80 $90 $100

$52.8 - $70.5

$63.9 - $84.8

$57.86-$68.6

$71.5 - $93.0

$34.55 - $57.7

Current Share Price of $52.96

Proposed bid of $88.62/share

15

V. Strategic Recommendation

1616

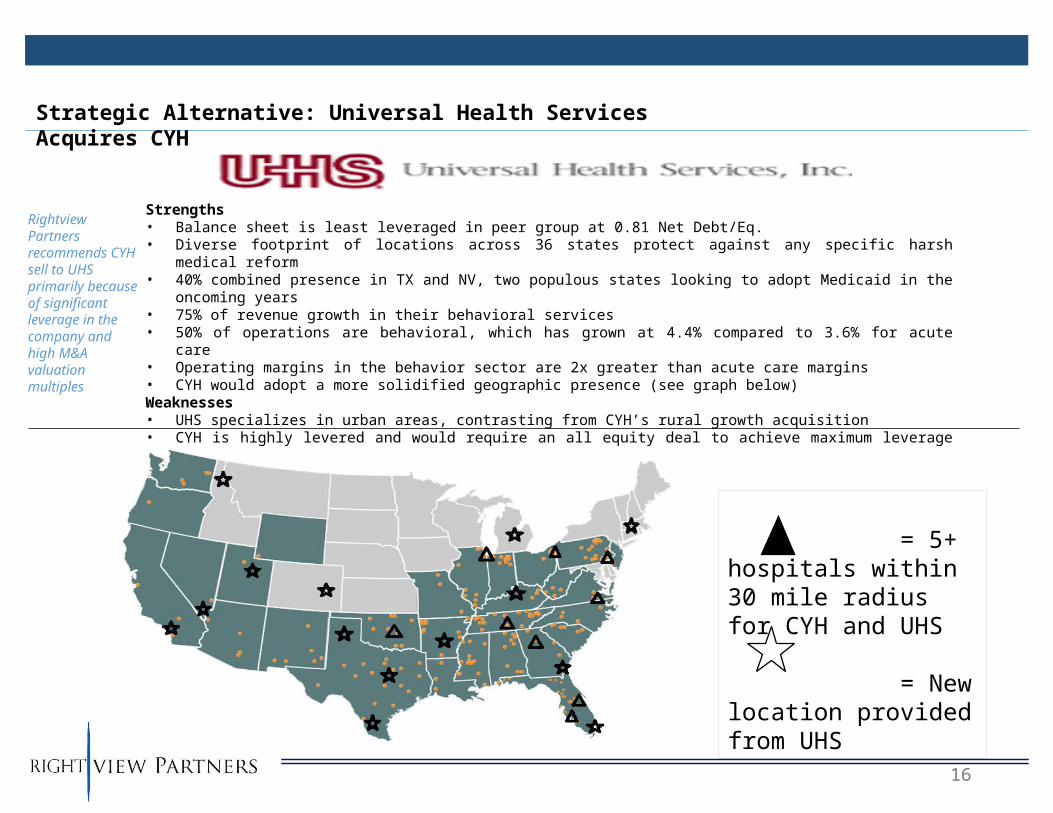

Strengths• Balance sheet is least leveraged in peer group at 0.81 Net Debt/Eq.• Diverse footprint of locations across 36 states protect against any specific harsh medical reform• 40% combined presence in TX and NV, two populous states looking to adopt Medicaid in the oncoming

years• 75% of revenue growth in their behavioral services• 50% of operations are behavioral, which has grown at 4.4% compared to 3.6% for acute care• Operating margins in the behavior sector are 2x greater than acute care margins• CYH would adopt a more solidified geographic presence (see graph below)Weaknesses• UHS specializes in urban areas, contrasting from CYH’s rural growth acquisition • CYH is highly levered and would require an all equity deal to achieve maximum leverage at 6.5x from the

current 6.41x

Strategic Alternative: Universal Health Services Acquires CYH

= 5+ hospitals within 30 mile radius for CYH and UHS

= New location provided from UHS

Rightview Partners recommends CYH sell to UHS primarily because of significant leverage in the company and high M&A valuation multiples

1717

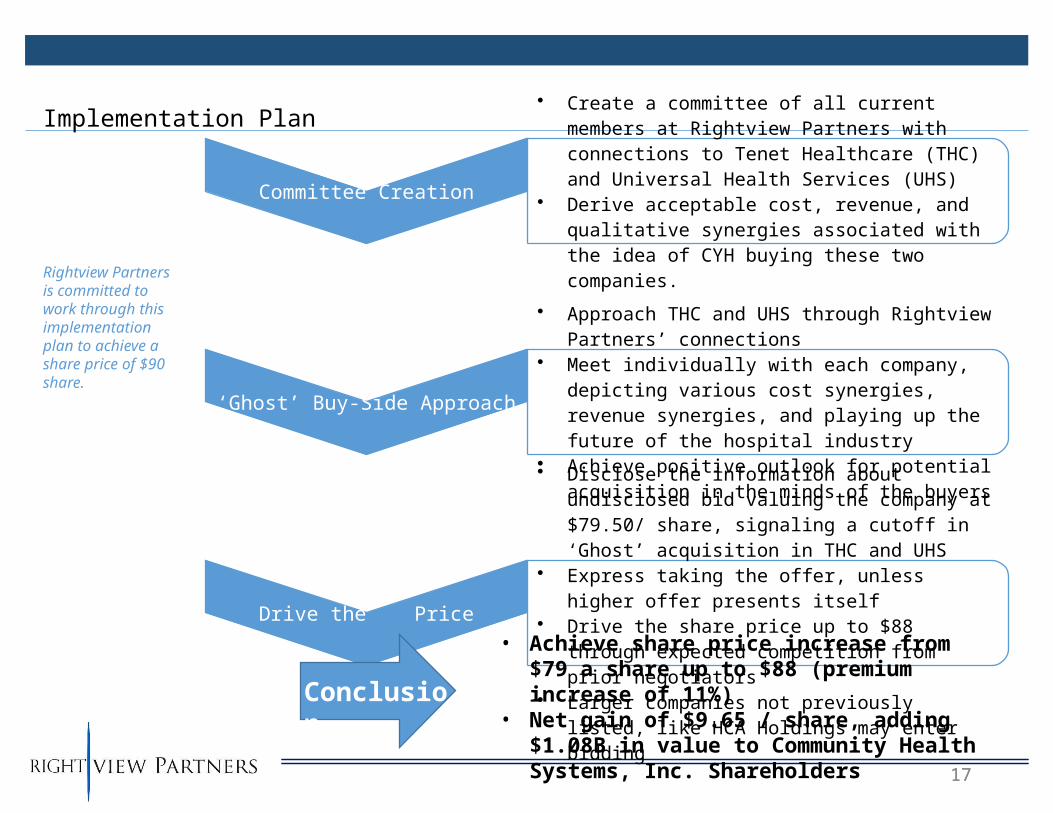

Implementation Plan

Committee Creation

• Create a committee of all current members at Rightview Partners with connections to Tenet Healthcare (THC) and Universal Health Services (UHS)

• Derive acceptable cost, revenue, and qualitative synergies associated with the idea of CYH buying these two companies.

‘Ghost’ Buy-Side Approach

• Approach THC and UHS through Rightview Partners’ connections

• Meet individually with each company, depicting various cost synergies, revenue synergies, and playing up the future of the hospital industry

• Achieve positive outlook for potential acquisition in the minds of the buyers

Drive the Price

• Disclose the information about undisclosed bid valuing the company at $79.50/ share, signaling a cutoff in ‘Ghost’ acquisition in THC and UHS

• Express taking the offer, unless higher offer presents itself

• Drive the share price up to $88 through expected competition from prior negotiators

• Larger companies not previously listed, like HCA Holdings may enter bidding

Rightview Partners is committed to work through this implementation plan to achieve a share price of $90 share.

Conclusion

• Achieve share price increase from $79 a share up to $88 (premium increase of 11%)

• Net gain of $9.65 / share, adding $1.08B in value to Community Health Systems, Inc. Shareholders

18

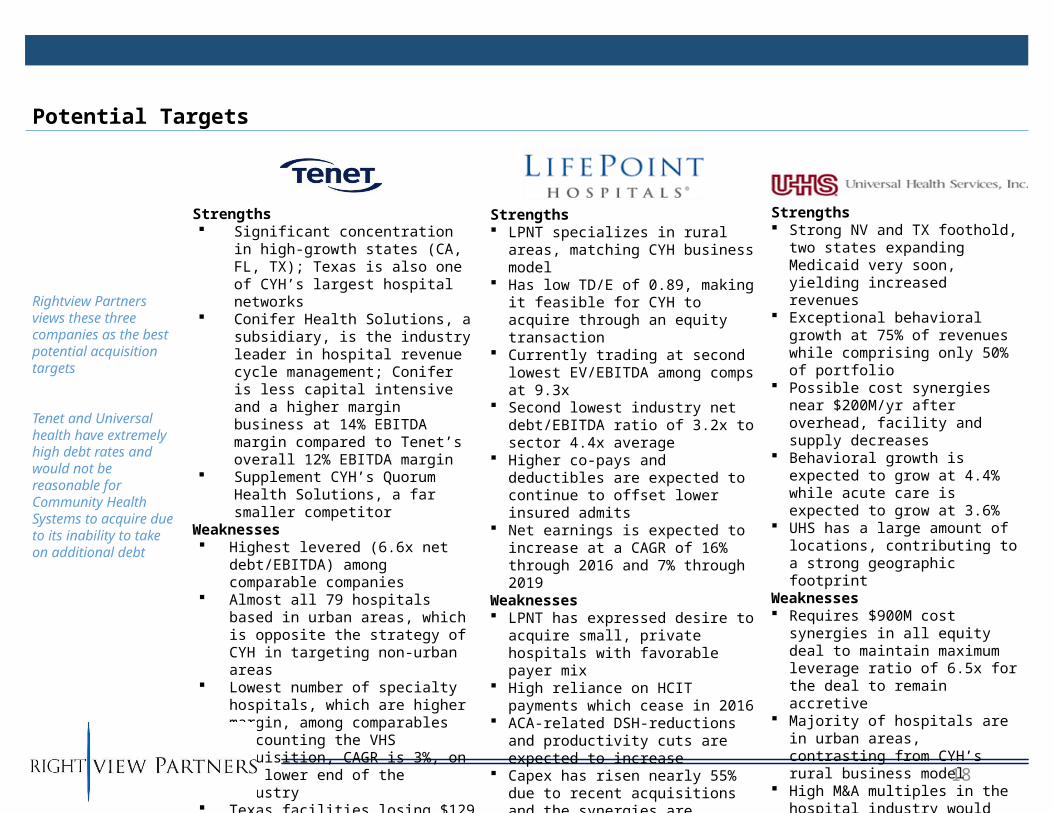

Strengths Significant concentration in

high-growth states (CA, FL, TX); Texas is also one of CYH’s largest hospital networks

Conifer Health Solutions, a subsidiary, is the industry leader in hospital revenue cycle management; Conifer is less capital intensive and a higher margin business at 14% EBITDA margin compared to Tenet’s overall 12% EBITDA margin

Supplement CYH’s Quorum Health Solutions, a far smaller competitor

Weaknesses Highest levered (6.6x net

debt/EBITDA) among comparable companies

Almost all 79 hospitals based in urban areas, which is opposite the strategy of CYH in targeting non-urban areas

Lowest number of specialty hospitals, which are higher margin, among comparables

Discounting the VHS acquisition, CAGR is 3%, on the lower end of the industry

Texas facilities losing $129 million a year since 2013

Rightview Partners views these three companies as the best potential acquisition targets

Tenet and Universal health have extremely high debt rates and would not be reasonable for Community Health Systems to acquire due to its inability to take on additional debt

Potential Targets

Strengths LPNT specializes in rural areas,

matching CYH business model Has low TD/E of 0.89, making it

feasible for CYH to acquire through an equity transaction

Currently trading at second lowest EV/EBITDA among comps at 9.3x

Second lowest industry net debt/EBITDA ratio of 3.2x to sector 4.4x average

Higher co-pays and deductibles are expected to continue to offset lower insured admits

Net earnings is expected to increase at a CAGR of 16% through 2016 and 7% through 2019

Weaknesses LPNT has expressed desire to

acquire small, private hospitals with favorable payer mix

High reliance on HCIT payments which cease in 2016

ACA-related DSH-reductions and productivity cuts are expected to increase

Capex has risen nearly 55% due to recent acquisitions and the synergies are expected to be realized later than anticipated

Strengths Strong NV and TX foothold,

two states expanding Medicaid very soon, yielding increased revenues

Exceptional behavioral growth at 75% of revenues while comprising only 50% of portfolio

Possible cost synergies near $200M/yr after overhead, facility and supply decreases

Behavioral growth is expected to grow at 4.4% while acute care is expected to grow at 3.6%

UHS has a large amount of locations, contributing to a strong geographic footprint

Weaknesses Requires $900M cost synergies

in all equity deal to maintain maximum leverage ratio of 6.5x for the deal to remain accretive

Majority of hospitals are in urban areas, contrasting from CYH’s rural business model

High M&A multiples in the hospital industry would require an expensive multiple

19

VI. Merger Model

20

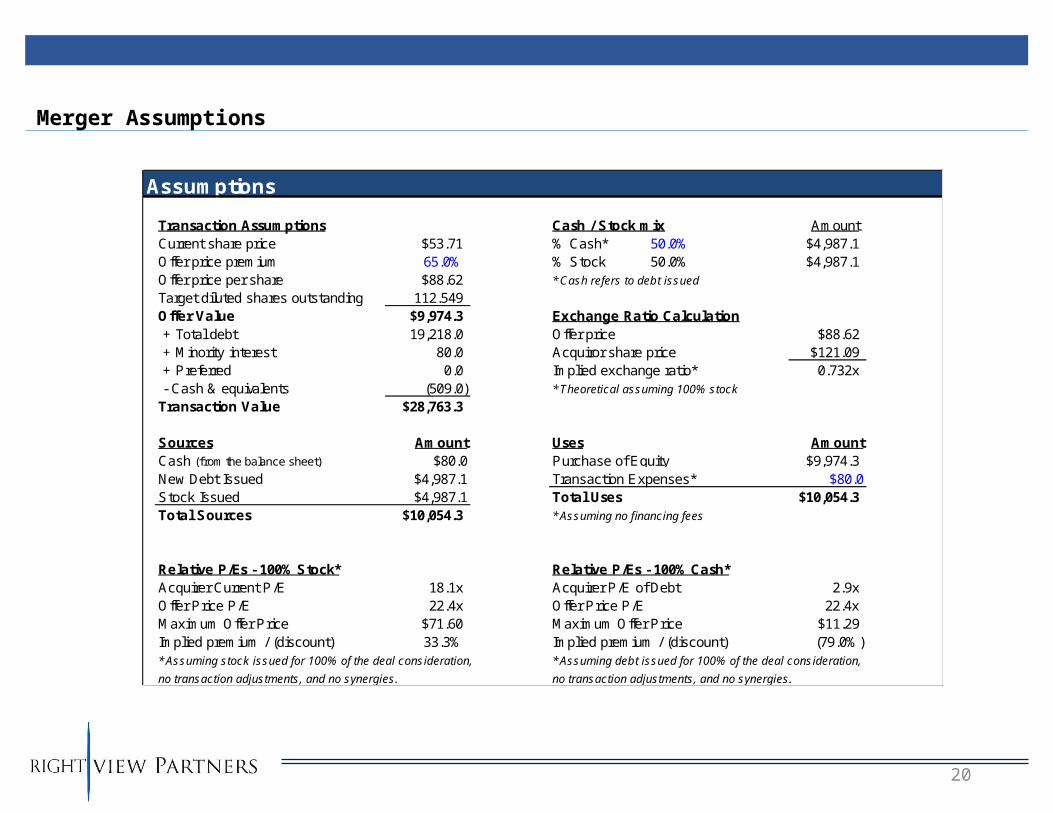

Merger Assumptions

Assumptions

Transaction Assumptions Cash / Stock mix AmountCurrent share price $53.71 % Cash* 50.0% $4,987.1Offer price premium 65.0% % Stock 50.0% $4,987.1Offer price per share $88.62 * Cash refers to debt issued

Target diluted shares outstanding 112.549Offer Value $9,974.3 Exchange Ratio Calculation + Total debt 19,218.0 Offer price $88.62 + Minority interest 80.0 Acquiror share price $121.09 + Preferred 0.0 Implied exchange ratio* 0.732x - Cash & equivalents (509.0) * Theoretical assuming 100% stock

Transaction Value $28,763.3

Sources Amount Uses AmountCash (from the balance sheet) $80.0 Purchase of Equity $9,974.3New Debt Issued $4,987.1 Transaction Expenses* $80.0Stock Issued $4,987.1 Total Uses $10,054.3Total Sources $10,054.3 * Assuming no financing fees

Relative P/Es - 100% Stock* Relative P/Es - 100% Cash*Acquirer Current P/E 18.1x Acquirer P/E of Debt 2.9xOffer Price P/E 22.4x Offer Price P/E 22.4xMaximum Offer Price $71.60 Maximum Offer Price $11.29Implied premium / (discount) 33.3% Implied premium / (discount) (79.0%)* Assuming stock issued for 100% of the deal consideration, * Assuming debt issued for 100% of the deal consideration,

no transaction adjustments, and no synergies. no transaction adjustments, and no synergies.

21

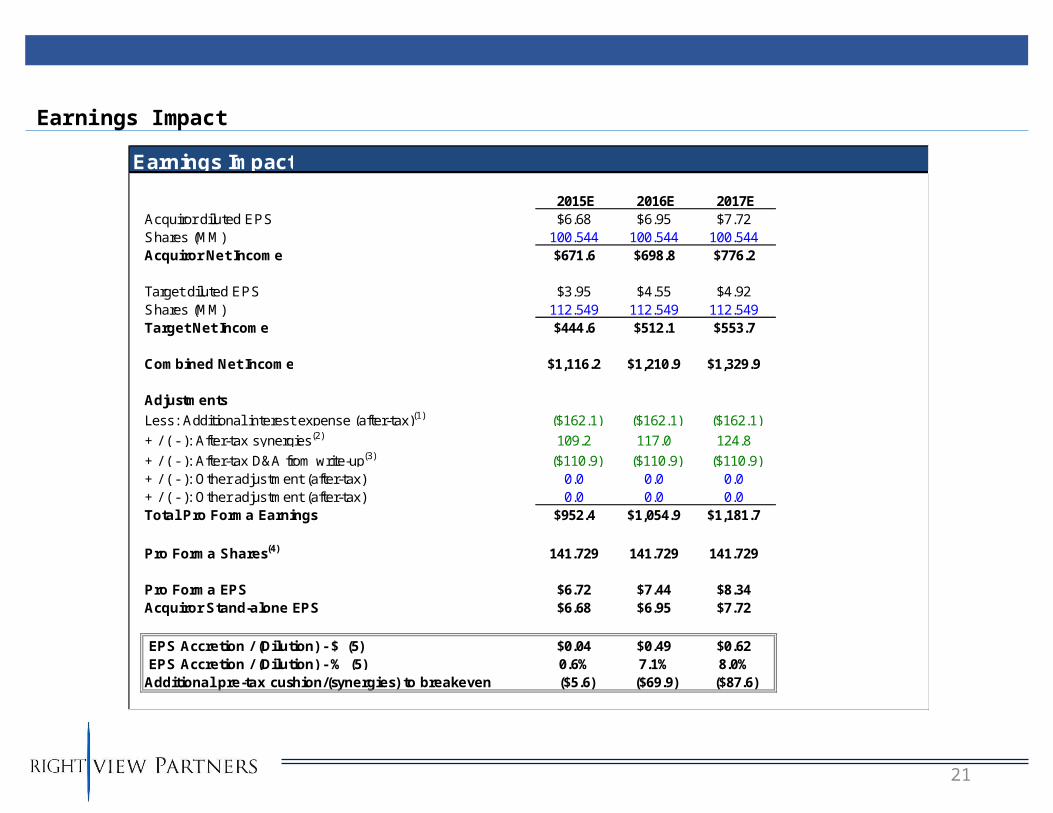

Earnings Impact

Earnings Impact

2015E 2016E 2017EAcquiror diluted EPS $6.68 $6.95 $7.72Shares (MM) 100.544 100.544 100.544Acquiror Net Income $671.6 $698.8 $776.2

Target diluted EPS $3.95 $4.55 $4.92Shares (MM) 112.549 112.549 112.549Target Net Income $444.6 $512.1 $553.7

Combined Net Income $1,116.2 $1,210.9 $1,329.9

Adjustments

Less: Additional interest expense (after-tax)(1) ($162.1) ($162.1) ($162.1)

+ / ( - ): After-tax synergies(2) 109.2 117.0 124.8

+ / ( - ): After-tax D&A from write-up(3) ($110.9) ($110.9) ($110.9)+ / ( - ): Other adjustment (after-tax) 0.0 0.0 0.0+ / ( - ): Other adjustment (after-tax) 0.0 0.0 0.0Total Pro Forma Earnings $952.4 $1,054.9 $1,181.7

Pro Forma Shares(4) 141.729 141.729 141.729

Pro Forma EPS $6.72 $7.44 $8.34Acquiror Stand-alone EPS $6.68 $6.95 $7.72

EPS Accretion / (Dilution) - $ (5) $0.04 $0.49 $0.62EPS Accretion / (Dilution) - % (5) 0.6% 7.1% 8.0%

Additional pre-tax cushion/(synergies) to breakeven ($5.6) ($69.9) ($87.6)

22

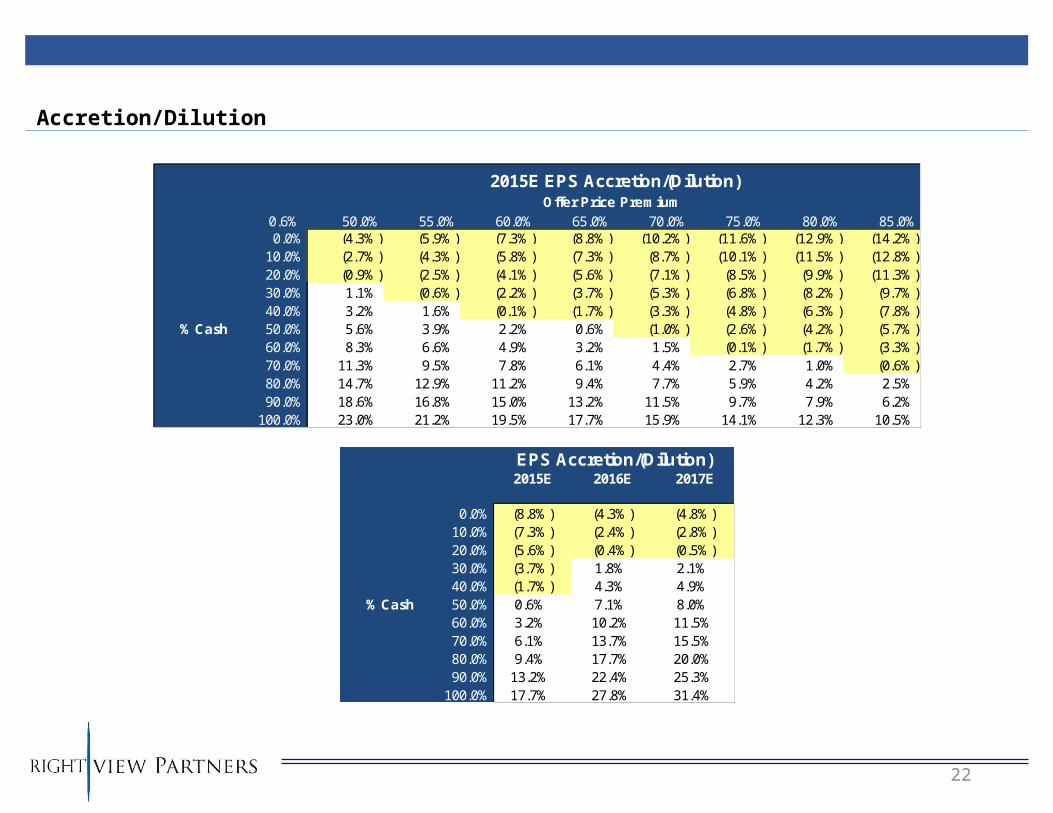

Accretion/Dilution

2015E EPS Accretion/(Dilution)Offer Price Premium

0.6% 50.0% 55.0% 60.0% 65.0% 70.0% 75.0% 80.0% 85.0%0.0% (4.3%) (5.9%) (7.3%) (8.8%) (10.2%) (11.6%) (12.9%) (14.2%)

10.0% (2.7%) (4.3%) (5.8%) (7.3%) (8.7%) (10.1%) (11.5%) (12.8%)20.0% (0.9%) (2.5%) (4.1%) (5.6%) (7.1%) (8.5%) (9.9%) (11.3%)30.0% 1.1% (0.6%) (2.2%) (3.7%) (5.3%) (6.8%) (8.2%) (9.7%)40.0% 3.2% 1.6% (0.1%) (1.7%) (3.3%) (4.8%) (6.3%) (7.8%)

% Cash 50.0% 5.6% 3.9% 2.2% 0.6% (1.0%) (2.6%) (4.2%) (5.7%)60.0% 8.3% 6.6% 4.9% 3.2% 1.5% (0.1%) (1.7%) (3.3%)70.0% 11.3% 9.5% 7.8% 6.1% 4.4% 2.7% 1.0% (0.6%)80.0% 14.7% 12.9% 11.2% 9.4% 7.7% 5.9% 4.2% 2.5%90.0% 18.6% 16.8% 15.0% 13.2% 11.5% 9.7% 7.9% 6.2%

100.0% 23.0% 21.2% 19.5% 17.7% 15.9% 14.1% 12.3% 10.5%

EPS Accretion/(Dilution) Offer Price Premium 2015E 2016E 2017E

0.6% 7.1% 8.0%0.0% (8.8%) (4.3%) (4.8%)

10.0% (7.3%) (2.4%) (2.8%)20.0% (5.6%) (0.4%) (0.5%)30.0% (3.7%) 1.8% 2.1%40.0% (1.7%) 4.3% 4.9%

% Cash 50.0% 0.6% 7.1% 8.0%60.0% 3.2% 10.2% 11.5%70.0% 6.1% 13.7% 15.5%80.0% 9.4% 17.7% 20.0%90.0% 13.2% 22.4% 25.3%

100.0% 17.7% 27.8% 31.4%

23

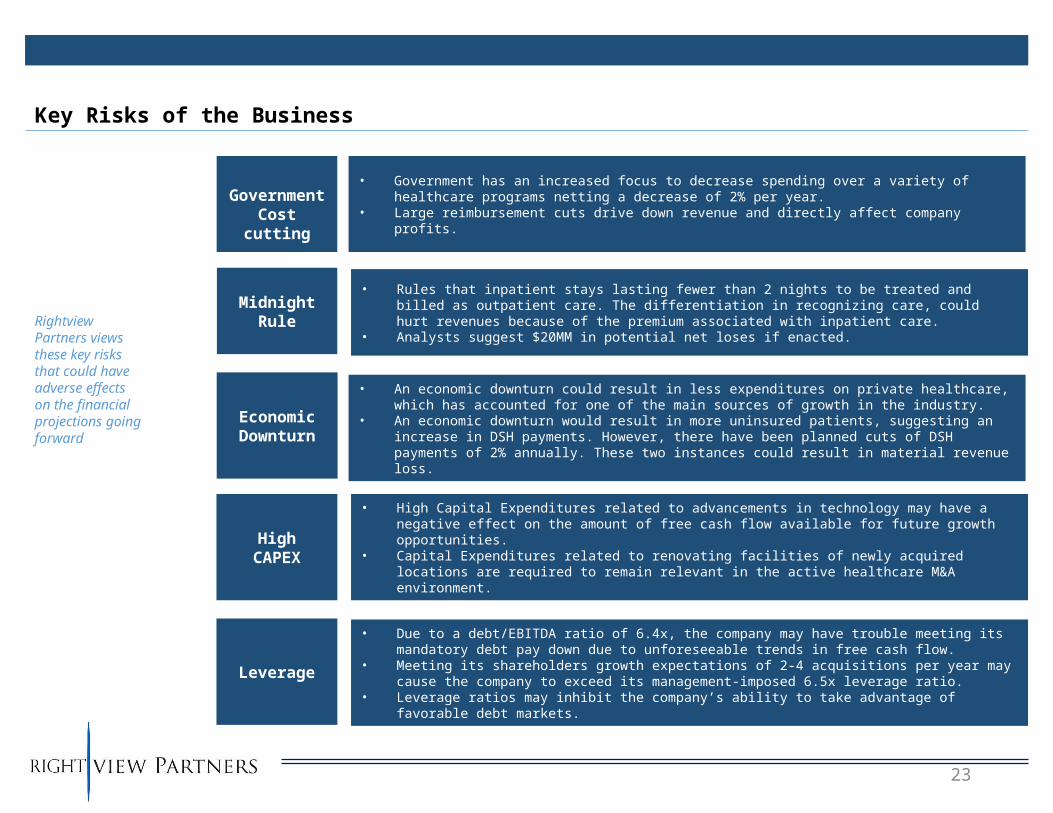

Governme

nt Cost cutting

Midnight Rule

Economic Downturn

• Government has an increased focus to decrease spending over a variety of healthcare programs netting a decrease of 2% per year.

• Large reimbursement cuts drive down revenue and directly affect company profits.

• Rules that inpatient stays lasting fewer than 2 nights to be treated and billed as outpatient care. The differentiation in recognizing care, could hurt revenues because of the premium associated with inpatient care.

• Analysts suggest $20MM in potential net loses if enacted.

• An economic downturn could result in less expenditures on private healthcare, which has accounted for one of the main sources of growth in the industry.

• An economic downturn would result in more uninsured patients, suggesting an increase in DSH payments. However, there have been planned cuts of DSH payments of 2% annually. These two instances could result in material revenue loss.

Key Risks of the Business

Rightview Partners views these key risks that could have adverse effects on the financial projections going forward

HighCAPEX

• High Capital Expenditures related to advancements in technology may have a negative effect on the amount of free cash flow available for future growth opportunities.

• Capital Expenditures related to renovating facilities of newly acquired locations are required to remain relevant in the active healthcare M&A environment.

Leverage

• Due to a debt/EBITDA ratio of 6.4x, the company may have trouble meeting its mandatory debt pay down due to unforeseeable trends in free cash flow.

• Meeting its shareholders growth expectations of 2-4 acquisitions per year may cause the company to exceed its management-imposed 6.5x leverage ratio.

• Leverage ratios may inhibit the company’s ability to take advantage of favorable debt markets.

24

VII. Appendix

25

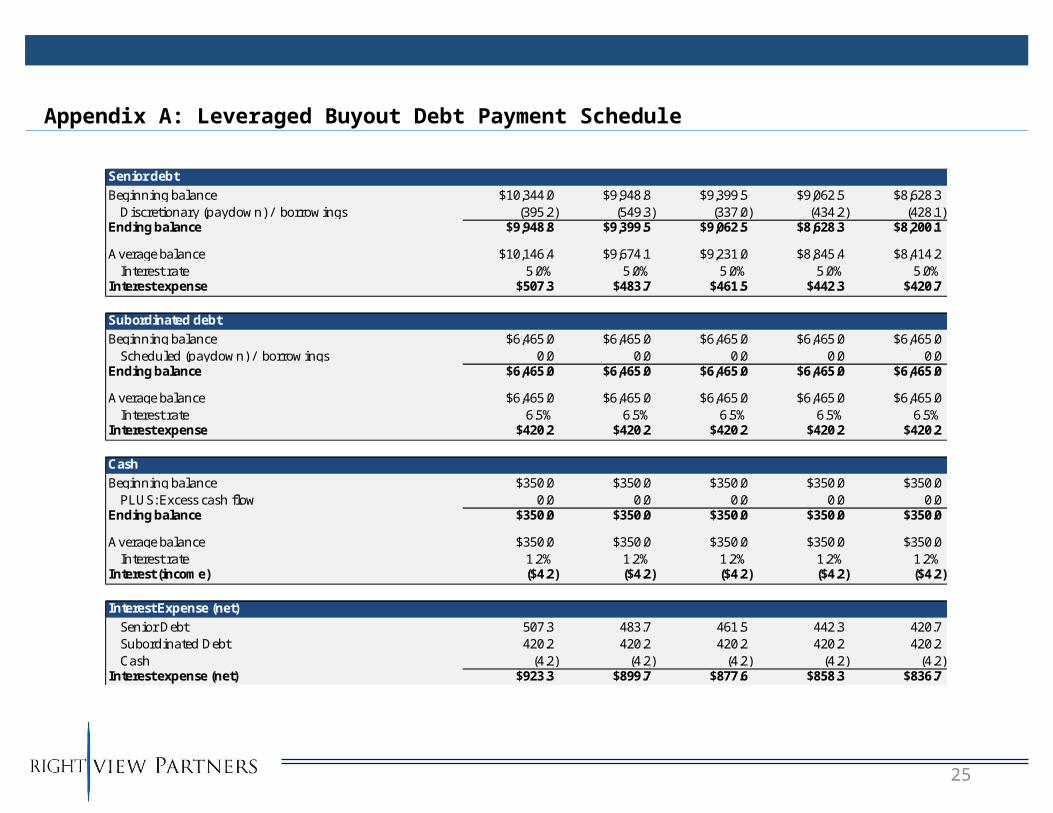

Appendix A: Leveraged Buyout Debt Payment Schedule

Senior debt

Beginning balance $10,344.0 $9,948.8 $9,399.5 $9,062.5 $8,628.3Discretionary (paydown) / borrowings (395.2) (549.3) (337.0) (434.2) (428.1)

Ending balance $9,948.8 $9,399.5 $9,062.5 $8,628.3 $8,200.1

Average balance $10,146.4 $9,674.1 $9,231.0 $8,845.4 $8,414.2Interest rate 5.0% 5.0% 5.0% 5.0% 5.0%

Interest expense $507.3 $483.7 $461.5 $442.3 $420.7

Subordinated debt

Beginning balance $6,465.0 $6,465.0 $6,465.0 $6,465.0 $6,465.0Scheduled (paydown) / borrowings 0.0 0.0 0.0 0.0 0.0

Ending balance $6,465.0 $6,465.0 $6,465.0 $6,465.0 $6,465.0

Average balance $6,465.0 $6,465.0 $6,465.0 $6,465.0 $6,465.0Interest rate 6.5% 6.5% 6.5% 6.5% 6.5%

Interest expense $420.2 $420.2 $420.2 $420.2 $420.2

Cash

Beginning balance $350.0 $350.0 $350.0 $350.0 $350.0PLUS: Excess cash flow 0.0 0.0 0.0 0.0 0.0

Ending balance $350.0 $350.0 $350.0 $350.0 $350.0

Average balance $350.0 $350.0 $350.0 $350.0 $350.0Interest rate 1.2% 1.2% 1.2% 1.2% 1.2%

Interest (income) ($4.2) ($4.2) ($4.2) ($4.2) ($4.2)

Interest Expense (net)

Senior Debt 507.3 483.7 461.5 442.3 420.7Subordinated Debt 420.2 420.2 420.2 420.2 420.2Cash (4.2) (4.2) (4.2) (4.2) (4.2)

Interest expense (net) $923.3 $899.7 $877.6 $858.3 $836.7

26

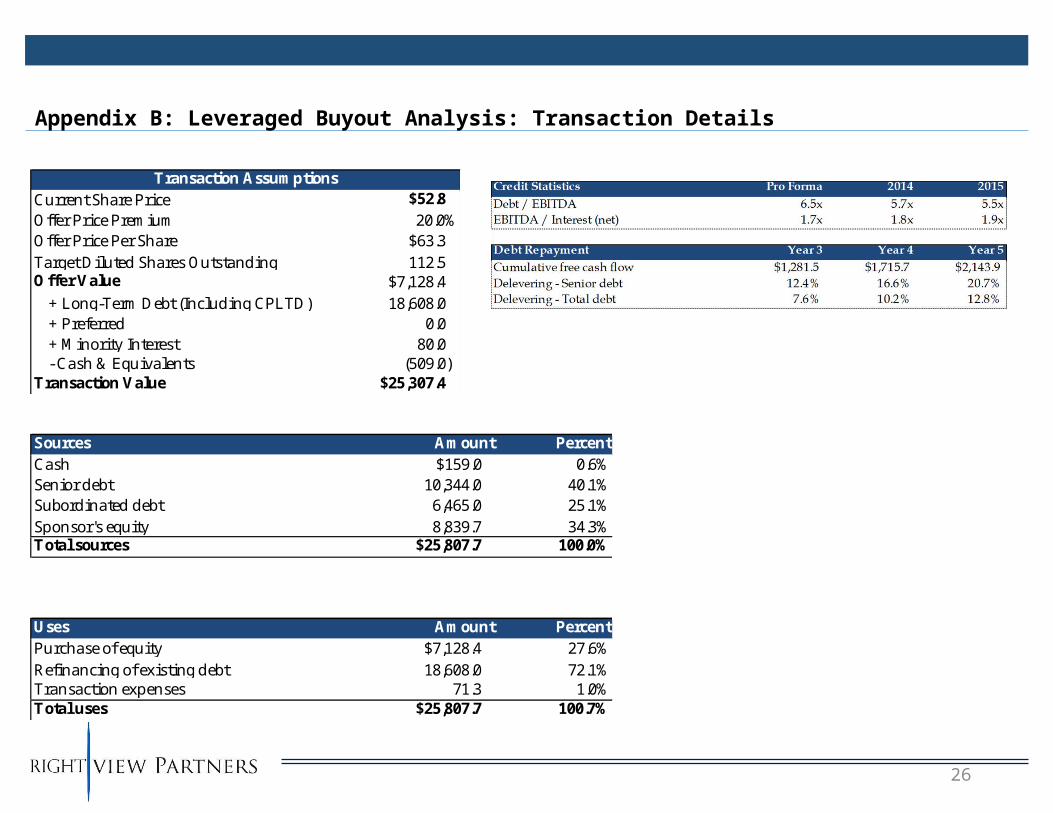

Appendix B: Leveraged Buyout Analysis: Transaction Details

Sources Amount PercentCash $159.0 0.6%Senior debt 10,344.0 40.1%Subordinated debt 6,465.0 25.1%Sponsor's equity 8,839.7 34.3%Total sources $25,807.7 100.0%

Uses Amount PercentPurchase of equity $7,128.4 27.6%Refinancing of existing debt 18,608.0 72.1%Transaction expenses 71.3 1.0%Total uses $25,807.7 100.7%

Transaction AssumptionsCurrent Share Price $52.8 Offer Price Premium 20.0%Offer Price Per Share $63.3 Target Diluted Shares Outstanding 112.5 Offer Value $7,128.4

+ Long-Term Debt (Including CPLTD) 18,608.0 + Preferred 0.0 + Minority Interest 80.0 - Cash & Equivalents (509.0)

Transaction Value $25,307.4

27

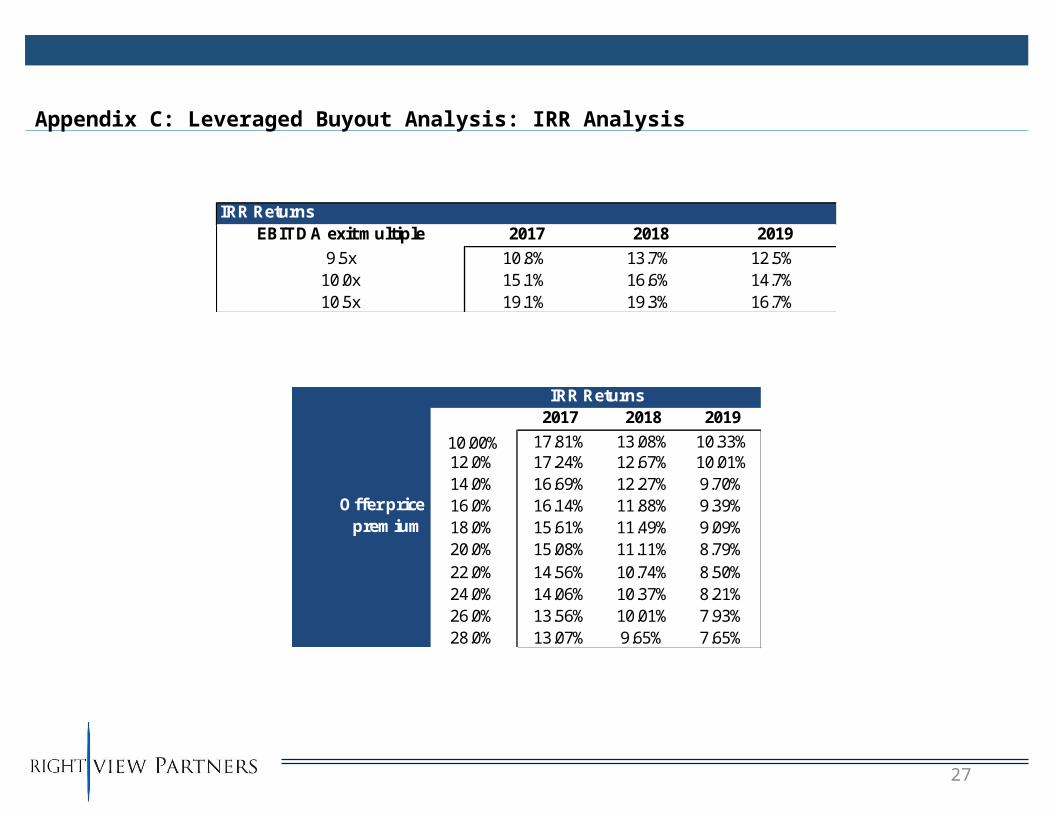

Appendix C: Leveraged Buyout Analysis: IRR Analysis

IRR Returns15.1% 2017 2018 2019

10.00% 17.81% 13.08% 10.33%12.0% 17.24% 12.67% 10.01%14.0% 16.69% 12.27% 9.70%

Offer price 16.0% 16.14% 11.88% 9.39%premium 18.0% 15.61% 11.49% 9.09%

20.0% 15.08% 11.11% 8.79%22.0% 14.56% 10.74% 8.50%24.0% 14.06% 10.37% 8.21%26.0% 13.56% 10.01% 7.93%28.0% 13.07% 9.65% 7.65%

IRR ReturnsEBITDA exit multiple 2017 2018 2019

9.5x 10.8% 13.7% 12.5%10.0x 15.1% 16.6% 14.7%10.5x 19.1% 19.3% 16.7%

28

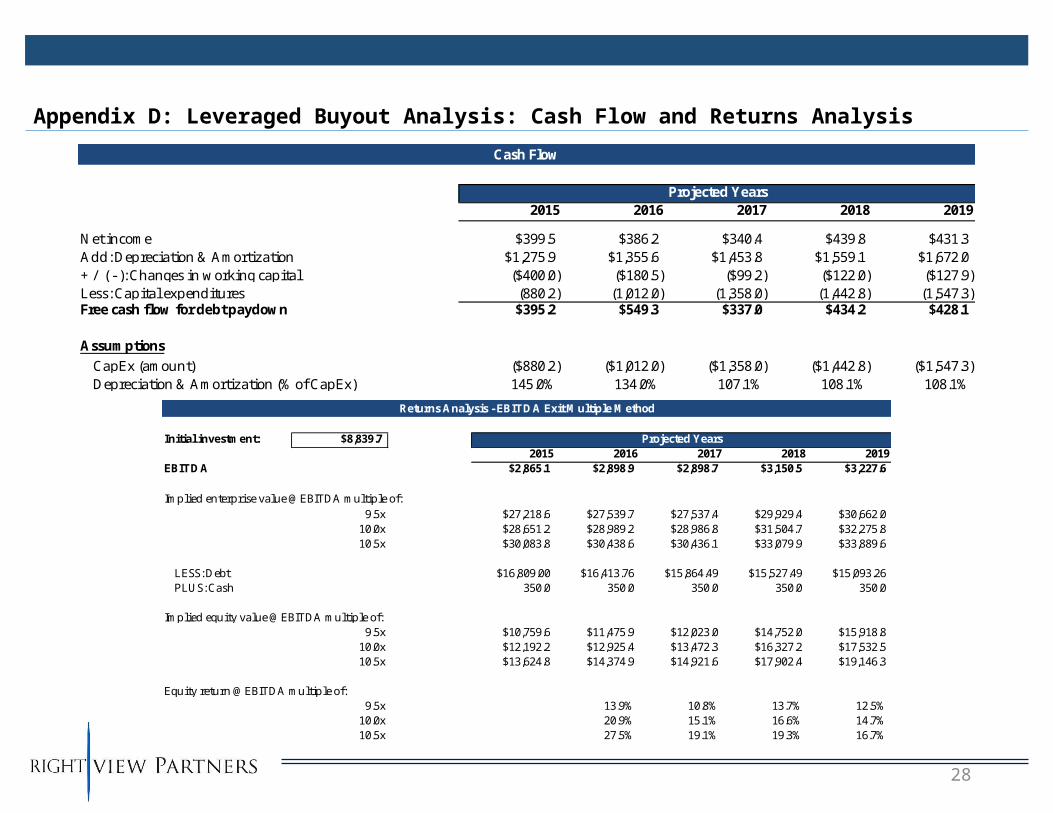

Appendix D: Leveraged Buyout Analysis: Cash Flow and Returns Analysis

Cash Flow

Projected Years2015 2016 2017 2018 2019

Net income $399.5 $386.2 $340.4 $439.8 $431.3Add: Depreciation & Amortization $1,275.9 $1,355.6 $1,453.8 $1,559.1 $1,672.0+ / ( - ): Changes in working capital ($400.0) ($180.5) ($99.2) ($122.0) ($127.9)Less: Capital expenditures (880.2) (1,012.0) (1,358.0) (1,442.8) (1,547.3)Free cash flow for debt paydown $395.2 $549.3 $337.0 $434.2 $428.1

AssumptionsCapEx (amount) ($880.2) ($1,012.0) ($1,358.0) ($1,442.8) ($1,547.3)Depreciation & Amortization (% of CapEx) 145.0% 134.0% 107.1% 108.1% 108.1%

Returns Analysis - EBITDA Exit Multiple Method

Initial investment: $8,839.7 Projected Years2015 2016 2017 2018 2019

EBITDA $2,865.1 $2,898.9 $2,898.7 $3,150.5 $3,227.6

Implied enterprise value @ EBITDA multiple of:9.5x $27,218.6 $27,539.7 $27,537.4 $29,929.4 $30,662.0

10.0x $28,651.2 $28,989.2 $28,986.8 $31,504.7 $32,275.810.5x $30,083.8 $30,438.6 $30,436.1 $33,079.9 $33,889.6

LESS: Debt $16,809.00 $16,413.76 $15,864.49 $15,527.49 $15,093.26PLUS: Cash 350.0 350.0 350.0 350.0 350.0

Implied equity value @ EBITDA multiple of:9.5x $10,759.6 $11,475.9 $12,023.0 $14,752.0 $15,918.8

10.0x $12,192.2 $12,925.4 $13,472.3 $16,327.2 $17,532.510.5x $13,624.8 $14,374.9 $14,921.6 $17,902.4 $19,146.3

Equity return @ EBITDA multiple of:9.5x 13.9% 10.8% 13.7% 12.5%

10.0x 20.9% 15.1% 16.6% 14.7%10.5x 27.5% 19.1% 19.3% 16.7%

29

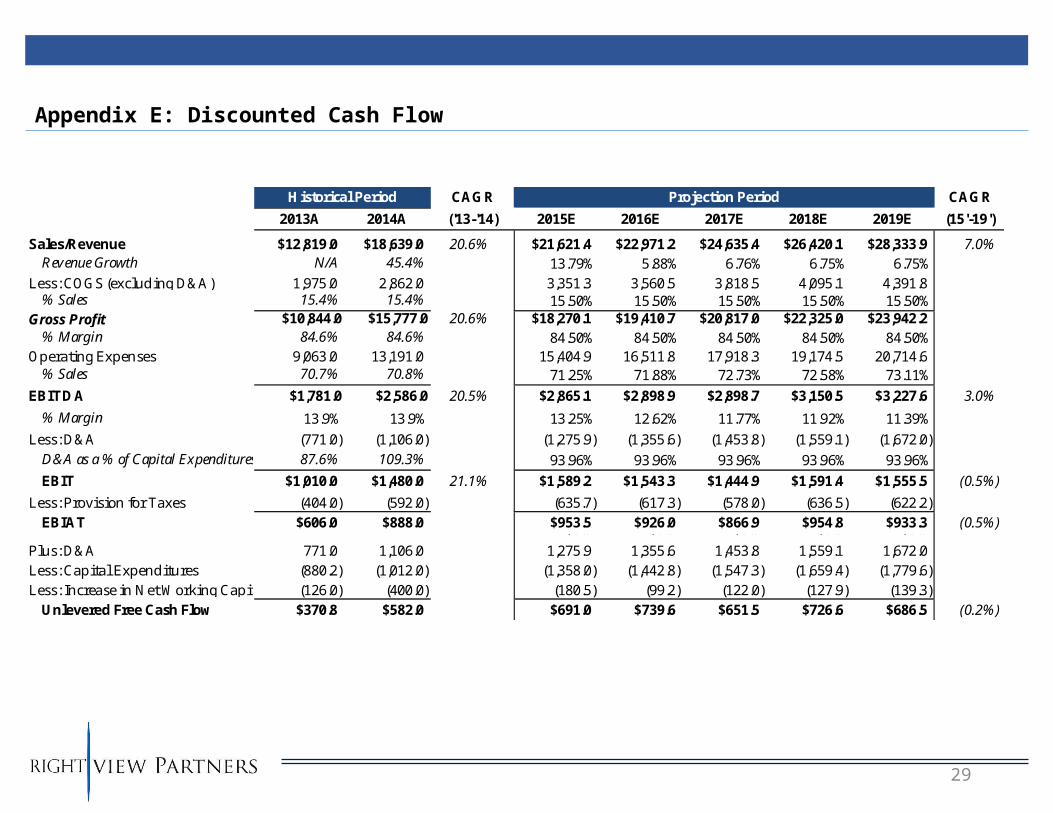

Appendix E: Discounted Cash Flow

Historical Period CAGR Projection Period CAGR

2013A 2014A ('13-'14) 2015E 2016E 2017E 2018E 2019E (15'-19')

Sales/Revenue $12,819.0 $18,639.0 20.6% $21,621.4 $22,971.2 $24,635.4 $26,420.1 $28,333.9 7.0%Revenue Growth N/A 45.4% 13.79% 5.88% 6.76% 6.75% 6.75%

Less: COGS (excluding D&A) 1,975.0 2,862.0 3,351.3 3,560.5 3,818.5 4,095.1 4,391.8% Sales 15.4% 15.4% 15.50% 15.50% 15.50% 15.50% 15.50%

Gross Profit $10,844.0 $15,777.0 20.6% $18,270.1 $19,410.7 $20,817.0 $22,325.0 $23,942.2% Margin 84.6% 84.6% 84.50% 84.50% 84.50% 84.50% 84.50%

Operating Expenses 9,063.0 13,191.0 15,404.9 16,511.8 17,918.3 19,174.5 20,714.6% Sales 70.7% 70.8% 71.25% 71.88% 72.73% 72.58% 73.11%

EBITDA $1,781.0 $2,586.0 20.5% $2,865.1 $2,898.9 $2,898.7 $3,150.5 $3,227.6 3.0%

% Margin 13.9% 13.9% 13.25% 12.62% 11.77% 11.92% 11.39%

Less: D&A (771.0) (1,106.0) (1,275.9) (1,355.6) (1,453.8) (1,559.1) (1,672.0)D&A as a % of Capital Expenditures 87.6% 109.3% 93.96% 93.96% 93.96% 93.96% 93.96%

EBIT $1,010.0 $1,480.0 21.1% $1,589.2 $1,543.3 $1,444.9 $1,591.4 $1,555.5 (0.5%)

Less: Provision for Taxes (404.0) (592.0) (635.7) (617.3) (578.0) (636.5) (622.2)EBIAT $606.0 $888.0 $953.5 $926.0 $866.9 $954.8 $933.3 (0.5%)$0.0 $0.0 $0.0 $0.0 $0.0

Plus: D&A 771.0 1,106.0 1,275.9 1,355.6 1,453.8 1,559.1 1,672.0Less: Capital Expenditures (880.2) (1,012.0) (1,358.0) (1,442.8) (1,547.3) (1,659.4) (1,779.6)Less: Increase in Net Working Capital (126.0) (400.0) (180.5) (99.2) (122.0) (127.9) (139.3)

Unlevered Free Cash Flow $370.8 $582.0 $691.0 $739.6 $651.5 $726.6 $686.5 (0.2%)

30

Appendix F: Discounted Cash Flow Analysis

DCF Analysis (2013-2017): EBITDA Multiple Method

Total Enterprise Value Total Equity Value

Terminal EBITDA Multiple Terminal EBITDA Multiple

9.5x 10.0x 10.5x 9.5x 10.0x 10.5x

Discount 6.0% $25,858.2 $27,064.1 $28,270.0 Discount 6.0% $7,759.2 $8,965.1 $10,171.0

Rate 6.5% $25,285.8 $26,463.7 $27,641.5 Rate 6.5% $7,186.8 $8,364.7 $9,542.5

(WACC) 7.0% $24,729.0 $25,879.6 $27,030.3 (WACC) 7.0% $6,630.0 $7,780.6 $8,931.3

Implied Perpetuity Growth Rate Total Price Per Share

Terminal EBITDA Multiple Terminal EBITDA Multiple

9.5x 10.0x 10.5x 9.5x 10.0x 10.5x

Discount 6.0% 3.7% 3.8% 3.9% Discount 6.0% $68.9 $79.7 $90.4

Rate 6.5% 4.2% 4.3% 4.4% Rate 6.5% $63.9 $74.3 $84.8

(WACC) 7.0% 4.7% 4.8% 4.9% (WACC) 7.0% $58.9 $69.1 $79.4

AssumptionsTax Rate 40.0%Net Debt (mm) $18,099.0

Shares (mm) 112.549

31

Appendix G: Precedent Transaction Analysis

Precedent Transactions Analysis($ in millions, except per share data)

Date

Announced Acquirers Target Deal Type EV TV/EBITDA TV/REV

7/ 30/ 2013 Community Health Systems In Health Management Associates Inc. Cash/ Stock $ 7,527.06 9.8x 1.3x

6/ 24/ 2013 Tenet Healthcare Corp Vanguard Health Systems Inc Cash $ 4,095.92 7.0x 0.7x

12/ 11/ 2012 Hospital Acquisition LLC LifeCare Holdings Inc Cash $ 320.00 5.0x 0.7x

1/ 21/ 2011 Surgery Partners Holdings LL NovaMed Inc Cash $ 229.55 5.5x 1.5x

5/ 17/ 2010 Universal Health Services Inc Psychiatric Solutions Inc Cash $ 3,114.41 9.7x 1.7x

5/ 14/ 2010 Multiple acquirers Healthscope Ltd Cash $ 2,274.95 11.4x 1.6x

3/ 11/ 2010 Fortis Healthcare Ltd Parkway Holdings Ltd Undisc. $ 686.08 18.6x 4.1x

Mean 2,606.85$ 9.6x 1.6x

Median $ 2,274.95 9.7x 1.5x

High $ 7,527.06 18.6x 4.1x

Low $ 229.55 5.0x 0.7x

Total Price Per Share Forward EBITDA Multiple

68.0779661 9.5x 10.0x 10.5x 11.0x 11.5x

$2,800 $ 68.73 $ 80.59 $ 92.46 104.32$ 116.19$

$2,850 $ 72.75 $ 84.83 $ 96.91 108.98$ 121.06$

$2,900 $ 76.78 $ 89.07 $ 101.36 113.64$ 125.93$

$2,950 $ 80.81 $ 93.31 105.81$ 118.31$ 130.81$

$3,000 $ 84.83 $ 97.54 110.25$ 122.97$ 135.68$

2015 EBITDA

32

Appendix H: Comparable Companies Analysis

EBIDTA

(M)

Multiple

Range

Implied

Enterprise Value2,458.00$ 10.75x - 13.6x $ 26,400 - $ 33,400

EV/EBITDA

LTM CY' 15 CY' 16 LTM CY' 15 CY' 16 LTM CY' 15 CY' 16

Community Health Systems 53.71$ 6.95% 6,224.00$ 22,500.00$ 1.20x 1.20x 1.10x 9.50x 7.50x 7.20x 60.00x 13.50x 11.80x 6.40x

Lifepoint Hospitals 73.65$ 5.09% 3,313.00$ 5,499.00$ 1.23x 1.08x 1.02x 9.30x 7.78x 7.36x 27.38x 18.60x 17.21x 3.80x

Universal Health Services 117.33$ 3.44% 11,730.00$ 15,271.00$ 1.89x 1.75x 1.65x 10.75x 9.59x 8.98x 21.65x 18.33x 16.86x 2.30x

Tenet Healthcare 49.44$ 21.43% 5,011.00$ 17,160.00$ 1.03x 0.97x 0.93x 9.81x 8.07x 7.53x 412.00x 24.84x 19.16x 6.70x

HCA Holdings Inc. 77.41$ 2.95% 32,822.00$ 63,297.00$ 1.71x 1.61x 1.54x 9.04x 8.30x 7.81x 18.61x 15.18x 13.97x 4.20x

HealthSouth Corporation 44.21$ 5.31% 3,911.00$ 6,254.00$ 2.63x 2.15x 2.04x 10.55x 9.22x 8.66x 19.31x 19.22x 17.27x 3.60x

Envision Healthcare Holdings 39.15$ 1.32% 7,240.00$ 8,935.00$ 2.03x 1.71x 1.52x 18.81x 13.56x 11.80x 59.32x 26.82x 22.76x 4.30x

Team Health Holdings 60.40$ 4.26% 4,341.00$ 5,129.00$ 1.82x 1.53x 1.38x 20.11x 14.05x 12.42x 44.74x 23.05x 20.34x 3.20x

Amsurg Corporation 65.84$ 0.87% 3,147.00$ 5,060.00$ 3.70x 2.40x 2.20x 13.60x 11.70x 9.80x 52.40x 20.10x 17.30x 5.20x

Davita Healthcare Partners 81.61$ 0.98% 17,610.00$ 25,832.00$ 2.00x 1.90x 1.80x 10.80x 10.40x 9.90x 24.60x 21.80x 20.00x 3.50x

Max 3.70x 2.40x 2.20x 20.11x 14.05x 12.42x 412.00x 26.82x 22.76x 6.70x

Mean 2.01x 1.68x 1.57x 12.53x 10.30x 9.36x 75.56x 20.88x 18.32x 4.09x

Median 1.89x 1.71x 1.54x 10.75x 9.59x 8.98x 27.38x 20.10x 17.30x 3.80x

Low 1.03x 0.97x 0.93x 9.04x 7.78x 7.36x 18.61x 15.18x 13.97x 2.30x

25 Percentile 1.71x 1.53x 1.38x 9.81x 8.30x 7.81x 21.65x 18.60x 17.21x 3.50x

75 Percentile 2.03x 1.90x 1.80x 13.60x 11.70x 9.90x 52.40x 23.05x 20.00x 4.30x

CompanyStock Price

%Off 52 Wk High

Equity Value

Enterprise Value

P/EEV/RevLTM Total Debt/

EBITDA