Curacao Economic Outlook 2011

138

-

Upload

hubcuracao -

Category

Economy & Finance

-

view

1.859 -

download

0

Transcript of Curacao Economic Outlook 2011

Curaçao Economic Outlook 2011En route towards the strengthening of the economic structure of new country Curaçao

Contents

PREFACE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

EXECUTIVE SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

CHAPTER 1: MACROECONOMIC DEVELOPMENTS . . . . 10

1.1 International and Regional Developments

and their Consequences for Curaçao . . . . . . . . . . . . . . . . . . . . . 10

1.2 Macro Economic Indicators for Curaçao . . . . . . . . . . . . . . . . . . . 26

1.3 Labor Market Developments . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

1.4 Public Finances . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

1.5 Monetary Developments in Curaçao . . . . . . . . . . . . . . . . . . . . . . 45

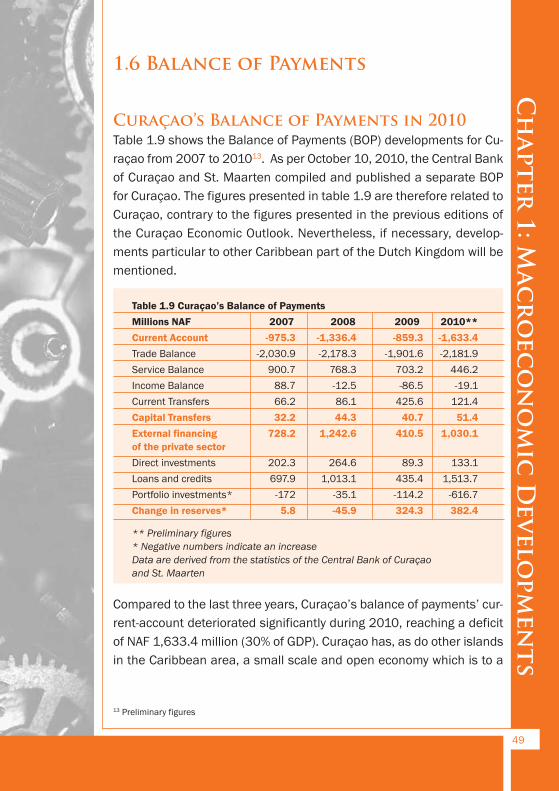

1.6 Balance of Payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

1.7 SEI Program . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

CHAPTER 2: SECTORAL DEVELOPMENTS . . . . . . . . . . . . 58

2.1 Production Sectors: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

2.1.1 Agriculture, Livestock and Fisheries . . . . . . . . . . . . . . . . . . . . . . 58

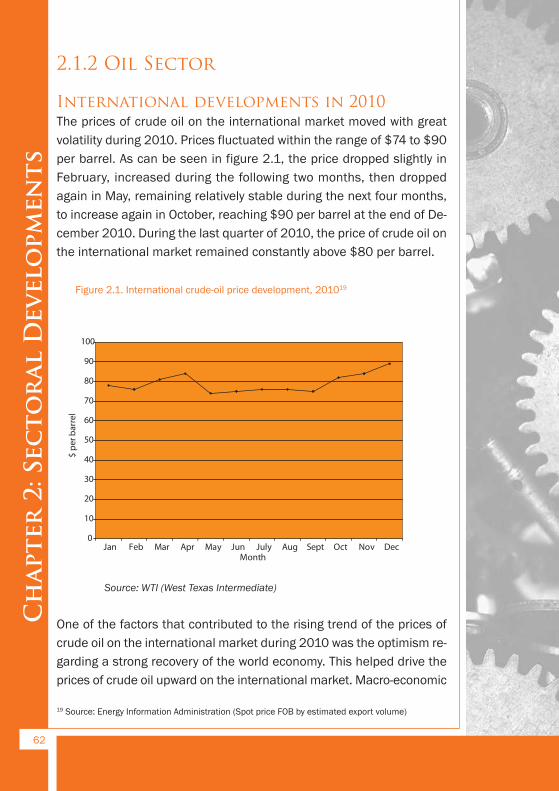

2.1.2 Oil Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

2.1.3 Utilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

2.1.4 Manufacturing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

2.2 Construction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

2.3 Trade Sectors: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

2.3.1 Wholesale and Retail Trade . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

2.3.2 Economic Zones and E-commerce . . . . . . . . . . . . . . . . . . . . . . . 83

2.4 Transportation Sector: . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

2.4.1 Air Transport . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

2.4.2 Harbor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

2.5 Tourism . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .101

2.6 Financial and Business Services: . . . . . . . . . . . . . . . . . . . . . . . .106

2.6.1 Commercial Banks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .106

2.6.2 International Financial and Business Services . . . . . . . . . . . . .109

2.6.3 Insurance Companies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .113

2.7 Healthcare . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .117

CHAPTER 3: ENHANCING BUSINESS CLIMATE . . . . . . .123

APPENDICES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .129

Appendix I: Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .129

Appendix II: List of Tables and Figures . . . . . . . . . . . . . . . . . . . . . . . . . .131

Appendix III: List of Abbreviations . . . . . . . . . . . . . . . . . . . . . . . . . . . . .133

2

Conte

nts

Preface

The Ministry of Economic Development, on behalf of the Government

of Curaçao, is proud to present the Curaçao Economic Outlook 2011.

This publication provides an overview of Curaçao’s macroeconomic and

sectoral performance in 2010 and 2011, the latter based on the devel-

opments up to the first nine months of the year, and in addition dis-

cusses the prospects for the whole economy in 2012, underlining some

key policy intentions for the near future to strengthen Curaçao’s eco-

nomic structure.

The Curaçao Economic Outlook 2011 was prepared by a team of policy

advisors at the Ministry of Economic Development, with contributions

from several government institutions, the private sector and sector-spe-

cific associations, which shared their latest data and knowledge with

the Ministry.

Through these words, the Ministry would like to thank all who, in one

way or the other, contributed to the realization of this publication.

Ing. Luelo Girigorie, CPC, MSc.

Head of the Directorate of Economic Policy

3

Prefac

e

Executive Summary

Macroeconomic developmentsThe world economy continued to recover in 2010. As fears of global re-

cession receded in 2009, businesses regained confidence and indus-

trial production and trade boomed. The extent of growth differs per

region: in the major advanced economies growth was modest while

many emerging and developing countries saw robust growth rates. Un-

employment remained high, particularly in advanced economies, while

commodity prices increased sharply in 2010.

The global economy is anticipated to continue growing, and again, ad-

vanced economies are projected to grow at a slower rate in 2011 than

emerging and developing economies.

Commodity prices continued increasing at the beginning of 2011 but

energy prices have receded. Food prices, however, have fallen to a

much lesser extent. As a consequence inflationary pressure is lower in

advanced economies than in emerging and developing economies.

According to preliminary macroeconomic indicators, Curaçao’s econ-

omy grew by a mere 0.1 percent in 2010. Growth was led by a moderate

increase in public and private consumption but was mitigated by shrin -

king public investments and exports. The consumer price index re-

mained moderate at 2.8 percent in 2010.

For 2011, an expansion of 0.3 percent of the real economy is expected.

Growth is led, mainly, by foreign demand, which stimulates local de-

mand. Inflation is estimated at approximately 2.4 percent in 2011.

Traditionally, the CBS provides the relevant labor-market statistics

through their Labor Force Survey. However, as the CBS was preparing

intensely for the Census that took place in March and April of 2011,

the Labor Force Survey was not conducted in 2010. Hence, the usual

overview on participation, employment and unemployment is not avai l-

able in this edition. Some other indicators are used to describe the

latest developments.

4

Exec

utive Su

mmar

y

Preliminary figures on public finances up to October 10, 2010 indicate

a surplus of NAF 32.3 million for the treasury of the Island Territory of

Curaçao.

The revenue and expenditure projections were based on a forecasted

economic growth rate higher than the rate registered in 2010. Never-

theless, the actual revenues turned out to be slightly higher than bud-

geted, at NAF 911.4 million, while total expenditures turned out lower

than budgeted, at NAF 879.1 million.

Despite the extra liquidity in the domestic money market, the Central

Bank conducted a passive monetary policy in 2010, owing to a slo w-

down in economic activities. The aggregate money supply of the Nether-

lands Antilles decreased by NAF 241.7 million in 2010, while the net

foreign assets improved by NAF 582.6 million. The official lending rate

of the Central Bank remained unchanged at 1.00 percent in 2010.

As per October 10, 2010, Curaçao and St. Maarten form a monetary

union with a common currency, which at the moment is still the Nether-

lands Antilles guilder, and a common Central Bank, the Central Bank

of Curaçao and St. Maarten. The Central Bank’s monetary policy has

remained directed at the promotion of a stable external value of the

Netherlands Antilles guilder in 2011 and has been a common policy

supported by both countries.

The current account of Curaçao’s balance of payments deteriorated

during 2010, reaching a deficit of NAF 1,633.4 million, mainly because

of the worsening of the trade and the service balance and lower current

transfers received from abroad. Capital transfers increased by NAF 10.7

million, linked to increased capital inflows from Dutch development-aid

funds. The deterioration of the current account in 2010 as compared

to the year before resulted in a drop in the net foreign wealth of the

private sector.

For 2011, the current account deficit is anticipated to stay at approxi-

mately the same level as in 2010.

The execution of the SEI program reached its peak during the last quar-

ter of 2010, as the last day of the year was set as deadline to commit

5

Exec

utiv

e Summar

y

the projects’ budget. By January 1, 2011, 97 percent of the budget was

committed to 85 projects. The rest of the projects’ funds should have

been committed by September 30, 2011 at the latest, to avoid under-

spending of the SEI budget. At the moment of writing, negotiations are

being prepared for a new deadline, because some projects have not

been committed yet.

The USONA approved a total of 110 projects for an amount of approxi-

mately NAF 121 million, 33 of which are economic projects. Up to the

end of 2010, not much of the budget for the economic projects had

been touched. In 2011, however, the pace of these economic projects

increased considerably, putting the execution of the projects in full

swing.

Sectoral developmentsAn abnormally high level of rainfall brought the agriculture sector to its

knees during the last months of 2010 and first months of 2011, result-

ing in the import of fruits and vegetables that are otherwise grown lo-

cally. Greenhouse initiatives are being tested to increase the local

supply of fruits and vegetables.

The livestock sector did not show remarkable developments.

The growing lionfish population is threatening the fisheries industry.

Policies to prevent overfishing are being prepared, while actions to com-

bat the lionfish population have already started.

Equipment malfunctions at the BOO plant resulted in a shutdown of the

oil refinery for several months in 2010. The refinery started operating

again in December 2010, but environmental groups are putting pres-

sure on the refinery to reduce pollution, which leads to uncertainties

with regard to its future.

The distribution market was also affected by the shutdown of the refin-

ery: traffic in the harbor diminished and, as a consequence, bunkering

activities for the distributor decreased. Prospects are positive, however,

and there are plans to expand the bunkering and aviation market.

6

Exec

utive Su

mmar

y

During 2010, the international energy-price developments were not -

incorporated into local energy prices. In 2011, two additional players

have been allowed to enter the production market in the utilities sector.

Furthermore, policies are being prepared to reduce utility prices and

dependence on oil supply.

Besides the oil refinery and the shipyard company, business by other

players in the manufacturing sector remained the same or decreased

slightly in 2010 as compared to 2009, owing to increased competition

from imported products and high utility costs. The sector is positive

about the future due to the planned policy measures, such as a reform

of the tax structure and energy production.

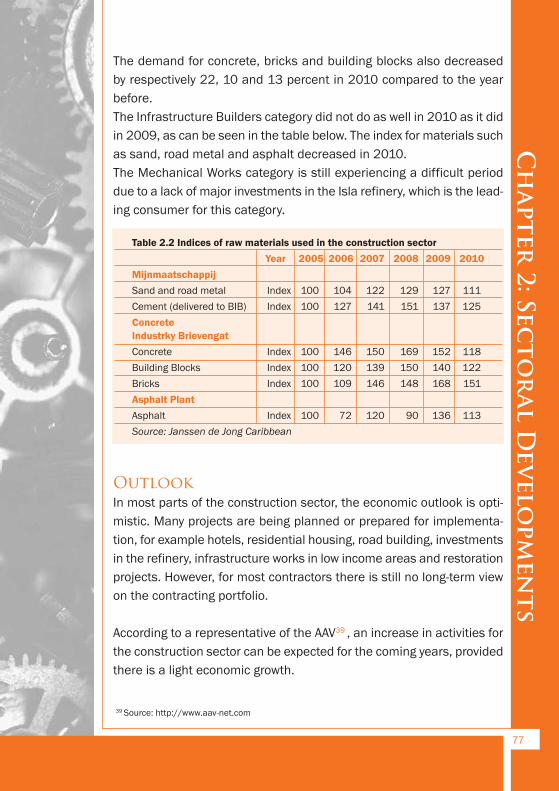

Sale of important raw materials for the construction sector decreased

by between 8 and 22 percent in 2010 compared to 2009, since several

major projects were completed in the course of 2010. The number of

buildings completed in 2010 was slightly higher compared to 2009.

The number of building permits issued in 2010 decreased, however,

compared to the previous year.

There are, nevertheless, many projects being planned and prepared,

but the contracting portfolios are not known yet.

Sales in the wholesale sector remained the same or decreased slightly,

while sales in the retail sector increased slightly in 2010 compared to

the year before. Challenges for the sector lie in remaining competitive

and increasing the quality of the products supplied.

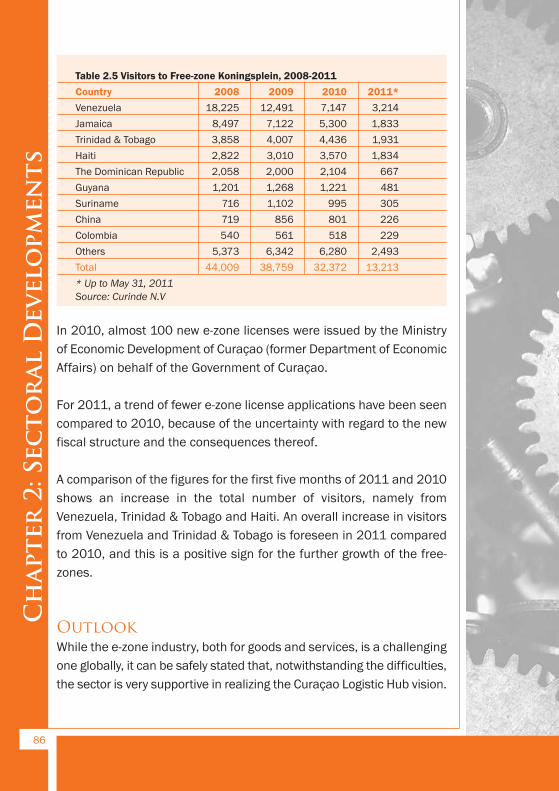

There are 10 service e-zones in operation on Curaçao and 2 free-zones

for international trading of goods. The total number of visitors to the

free-zones decreased by approximately 16 percent in 2010 compared

to 2009.

It is expected that at least two additional service e-zones will be insti-

tuted soon, but fewer e-zone license applications have been seen in

2011. The number of free-zone visitors is expected to increase.

7

Exec

utiv

e Summar

y

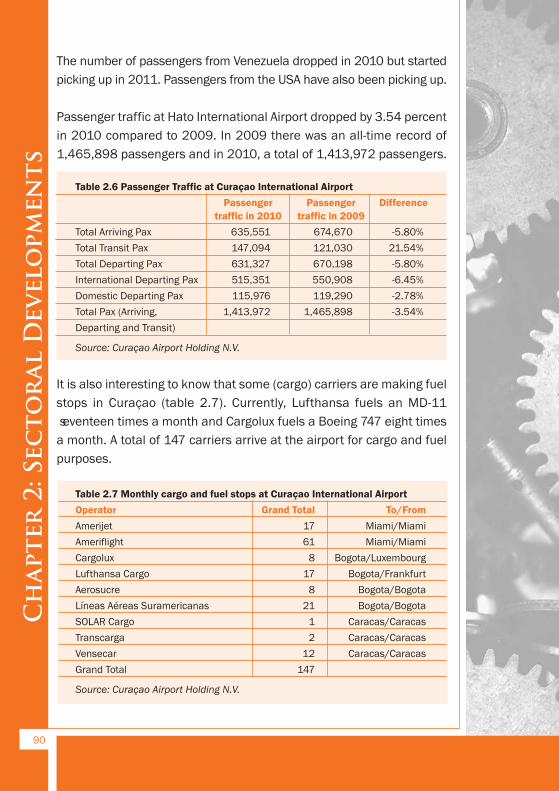

Passenger traffic at the Hato International Airport dropped by 3.54 per-

cent in 2010 compared to 2009. The economic crisis was largely to

blame for this drop. Moreover, some airlines deleted routes to lower

costs. Passenger traffic is predicted to increase slightly in 2011 be-

cause the number of flights connected to Curaçao has increased.

Harbor activities in terms of mooring ships (freighters, tankers and

cruise ships) declined by almost 14 percent in 2010 compared to the

year before. The volume of freight also decreased accordingly, from

97,913 TEUs in 2009 to 93,603 TEUs in 2010.

Preliminary figures indicate that cruise-ship calls have increased to 249

in 2011, but will decline to 219 in 2012. The number of cruise visitors

is expected to have increased in both years, despite the decline in calls

in 2012, as bigger ships are expected to anchor.

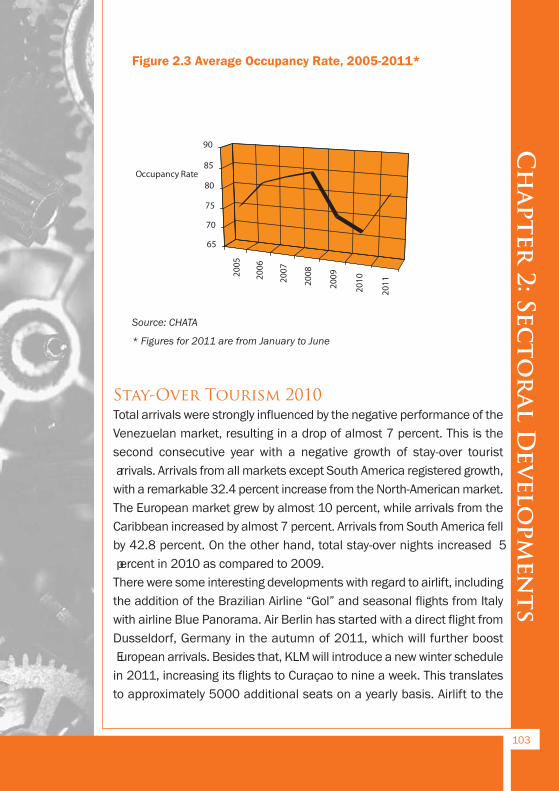

Tourism arrivals dropped by almost 7 percent in 2010 compared to

2009. Together with the increase in the room stock during recent years,

this resulted in a 3 percentage point decline of the hotel occupancy

rate.

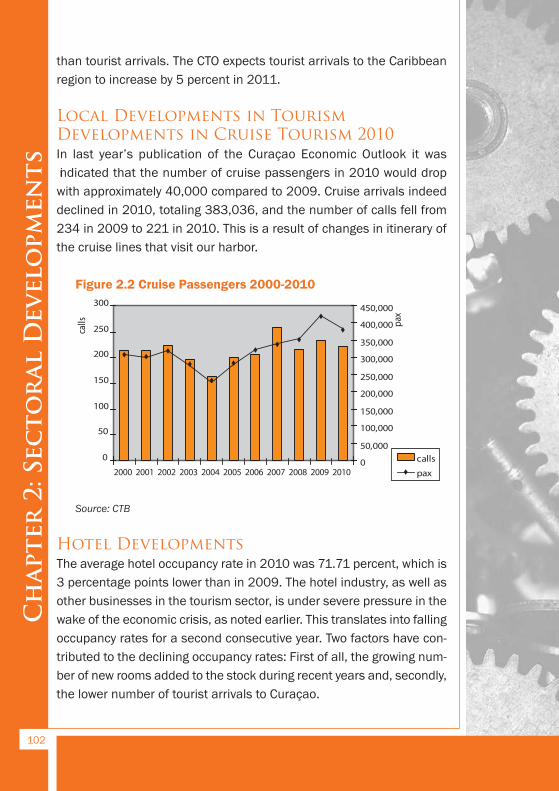

The number of cruise arrivals decreased to almost 390,000 in 2010,

while the number of calls fell from 234 in 2009 to 221 in 2010.

The decline in tourist arrivals is mainly caused by the substantial drop

in arrivals from Venezuela. Arrivals from other South-American countries

increased but were not enough to offset the decrease from Venezuela.

In the first eight months of 2011, arrivals from Venezuela increased

compared to the same period in 2010. Arrivals from North-America in-

creased in 2010 and continue to be extremely positive in 2011. Arrivals

from other Caribbean islands increased in 2010 and continued to in-

crease in the first eight months of 2011. The Netherlands continue to

be the largest market and contributed to the strong growth in arrivals

from Europe in 2010. Growth has declined, however, in 2011.

Lending rates at commercial banks were reduced to approximately

3 to 5 percent and saving rates were reduced to approximately 0.75 to

2 percent in 2010. Most banks experienced an increase in net income

and loan portfolios expanded, stimulated by the lower lending rates.

8

Exec

utive Su

mmar

y

Increased competition on the local market will continue increasing the

volatility of interest rates while depreciation of the Euro will decrease

investments and higher imported inflation will mitigate consumer

spending.

The international financial and business services sector is considered

important for the local economy. It is perceived that this sector con-

tributed mostly to the slight economic expansion in 2010. Therefore,

concrete actions are being taken to maintain the country’s position on

the OECD white list, to take Curaçao off Brazil’s black list, sign tax

treaties with Brazil very soon and with other countries in the near future.

Local insurance companies faced increased operational costs in 2010

because of the aftermath of tropical storm Tomas, but this had a mini-

mum effect on their results.

However, falling interest rates, the new constitutional status of the BES

Islands and the anticipated introduction of a general healthcare insur-

ance are threats to insurance companies.

A number of healthcare coverage measures were proposed in 2009

which should have led to structural savings on healthcare spending.

Some have been put on hold for further analysis while others will be in-

troduced shortly. The definite location of the new hospital has been

stipulated and the construction is planned to start in the second quarter

of 2012.

9

Exec

utiv

e Summar

y

1.1 International and Regional Developments and Their Consequences for Curaçao

Global DevelopmentsThe world economy continued to recover in 2010. World economic

growth was estimated by the IMF at 5.1 percent in 2010 after the con-

traction of 0.7 percent in 2009. As fears of global recession receded in

2009, businesses regained confidence and industrial production and

trade boomed in the first half of 2010, accelerating in the second half.

The reduced excess capacity, accommodative policies and further im-

provement in confidence and financial conditions encouraged invest-

ments and sharply reduced the rate of job destruction.

The extent of growth experienced differs per region. In the major ad-

vanced economies, growth was modest, reaching an average of 3.1 per-

cent in 2010. Many emerging and developing countries, on the other

hand, saw robust growth rates, averaging 7.3 percent in 2010.

Despite these growth rates, unemployment remained high, since the

increase in unemployment in advanced economies was very severe du -

r ing the crisis years. Youth unemployment is a particular concern in

emerging and developing countries, despite the low national overall un-

employment rates.

Following the collapse during the crisis, global capital flows rebounded

sharply in 2010, but are still below pre-crisis averages of 2006/2007

in many countries. Strong growth prospects and relatively high yields

are attracting capital flows into emerging markets, while sluggish ac-

tivity and damaged financial systems continue hampering flows be-

tween advanced economies. As a consequence, stock markets and

credit have rebounded from the falls during the crisis, particularly fast

in emerging markets, reaching or surpassing average pre-crisis levels

in some of the larger markets.

The robust capital flow to emerging markets may continue, even though

10

Chapter 1: M

acroec

onomic Developm

ents

questions about macroeconomic policies and geopolitical uncertainties

could slow flows on the short run. The difference between advanced and

emerging economies is not expected to diminish significantly, however.

Furthermore, advanced economies face the challenge of preserving or

regaining fiscal credibility owing to high public deficits and debts. Most

of the advanced countries are planning to tighten fiscal policy. Most

G20 advanced economies have made it their target to halve deficits by

2013 compared to the levels in 2010. However, well-specified medium-

term measures to reduce debt remain absent in many advanced coun-

tries, putting upward pressure on interest rates and lowering potential

output and slowing economic recovery as a consequence. The eventual

increase in interest rates would affect emerging economies also by

destabilizing global bond markets, which would slow investments in

general and thus in the developing economies in particular.

Commodity prices increased sharply in 2010, especially in the second

half of the year, owing to a combination of strong increase in demand

(oil and food) and supply shocks (food), e.g. lower agricultural produc-

tion because of unfavorable weather conditions. Commodity prices con-

tinued increasing at the beginning of 2011 because of lower oil

production, owing to unrest in the Middle-East and North-Africa, which

resulted in increased overall marginal costs and thus higher costs of

production in the agricultural sector. Nevertheless, in the last months

of 2011, energy prices have receded to levels far below their peaks in

that same year. Food prices, however, have fallen to a much lesser ex-

tent. As a consequence inflationary pressure is lower in advanced

economies than in emerging and developing economies, because food

and fuel account for a higher share of consumption in the latter.

In advanced economies, inflation is projected to be approximately 2.5

percent in 2011 and then recede to approximately 1.5 percent in 2012,

while in emerging and developing countries inflation is likely to be

around 7.5 and 6 percent in 2011 and 2012 respectively. The high ex-

pected inflation in the emerging and developing economies is led by

demand pressures (core inflation)1.

11

Chapter

1: Mac

roec

onomic Develo

pmen

ts

1 Excluding food and energy prices

The global economy is expected to continue growing. For 2011, the

world economy is expected to grow by 4.0 percent and this same growth

rate is expected in 2012. However, in advanced economies, again

growth is expected to be lower in 2011–at 1.6 percent– than in emer g-

ing and developing economies–at 6.4 percent. Output in advanced

economies remains below potential, resulting in persistent high unem-

ployment, and the situation is expected to remain so considering the

low growth rate owing to pre-crisis excesses and crisis wounds. Further-

more, consumer and business confidence has deteriorated and

stronger activities are expected to be delayed. This makes the outlook

point to low growth in 2012 also–at 1.9 percent.

In emerging economies the crisis left no lasting wounds. Hence exports

have recovered and shortfalls in external demand are compensated by

domestic demand. Capital outflows turned into capital inflows because

of better growth prospects and higher interest rates than in advanced

economies. Growth in emerging and developing economies is estimated

to decline from an average of 6.4 percent in 2011 to 6.1 percent in

2012, as capacity constraints, policy tightening and slowing foreign de-

mand are expected to dampen growth.

Latin America and the CaribbeanAccording to estimates of the Economic Commission for Latin America

and the Caribbean (ECLAC), the economy of the Latin American and

Caribbean region grew by an estimated 6 percent in 2010. The upturn,

however, has been uneven among the sub regions.

Growth in 2010 firmed up the recovery that began in most of the re-

gion’s economies in the second half of 2009, thanks to actions to coun-

terbalance the impacts implemented by many of the countries in the

region combined with improving conditions in the global economy. The

stronger economic growth boosted demand for labor, thanks to which

the region’s unemployment rate eased back to around 7.6 percent and

the quality of new jobs improved. Economic growth was coupled with a

slight rise in inflation, from 4.7 percent in 2009 to around 6.2 percent

in 2010, basically reflecting the behavior of prices for a number of in-

ternational commodity prices including food and fuel. Labor market per-

12

Chapter 1: M

acroec

onomic Developm

ents

formance, more readily available credit and brightening expectations

boosted private consumption which, along with a significant increase

in investment in machinery and equipment, became the engine of de-

mand in 2010.

Commodity exporting countries (agricultural, mineral and petroleum

goods) benefited from terms-of-trade gains and higher export values.

However, most of the Central American and Caribbean countries, once

more, sustained net losses in terms of trade owing to higher import

values, which worsened the current-account position. These adverse

effects were partially offset by a slight upturn in tourism and in remit-

tances sent home from developed countries by migrant workers.

ECLAC projects a slight fall in the region’s growth rate to 4.2 percent in

2011 owing to the slightly dampened global economic outlook and the

easing off of public spending as a stimulus in many countries because

excess idle capacity has been used up.

According to the IMF, the pace of expansion in Latin America and the

Caribbean has begun to moderate because many economies have fully

recovered from the global crisis and macroeconomic policies are being

tightened. Growth remains above potential, at 4.5 percent in 2011 and

4.0 percent in 2012, with indicators suggesting that mainly exporting

economies (in South America) may be overheating. Economic growth is

projected to slow as domestic demand growth moderates, in response

to less accommodative macroeconomic policies, and external demand

weakens.

The outlook for commodity exporting countries (e.g. Argentina, Chile,

Paraguay, Peru and Uruguay) is positive with growth rates of approxi-

mately 6 percent in 2011. Growth in South America is projected average

4.9 and 4.1 percent in 2011 and 2012 respectively.

In Central America and the Caribbean, economic activity remains

subdued, reflecting stronger trade linkages with the U.S. and other

advanced economies and, in some cases, high levels of public debt.

Growth will continue to be constrained by slow recovery of remittances

and tourism at between 3.3 and 3.9 percent in 2011 and increase to

between 4.0 and 4.3 percent in 2012.

13

Chapter

1: Mac

roec

onomic Develo

pmen

ts

Inflation is projected to increase from 6 percent in 2010 to 6.7 percent

in 2011, because of the overheating and as commodity prices in-

creased in 2011, but to recede to 6 percent in 2012 as activity moder-

ates and commodity prices stabilize.

The region faces some downside risks, however: sharper slowdown in

advanced economies would dampen growth, especially in economies

dependent on trade, tourism spending and remittances. Moreover, the

strong presence of Spanish banks in the region could raise some risks

while potential spillovers from China could show up through trade

dampening the outlook for the commodity exporting countries. However,

domestic demand growth could exceed expectations if global risks un-

wind quickly, resuming the strong wave of capital flows to the region,

which is an upside risk. The risk pattern is reinforced by the region’s in-

ternal and external integration. An eventual slowdown in global growth

would cause a drop in the region’s commodity export.

Furthermore, many neighboring countries are profiting from strong

growth in Brazil. Consequently, an abrupt slowdown in activities in Brazil

would adversely affect the region. The challenge that lies ahead is to

maintain the region’s resilience to potential problems.

North AmericaAccording to the IMF, the US economy grew in 2010 by almost 3 percent

in real terms, after contracting by 2.6 percent in 2009. This recovery

was mainly supported by private demand. By the last quarter of 2010,

consumer demand was rising at its fastest pace in five years. Low cor-

porate borrowing rates and the easing tightness of lending conditions

reflected improved financial conditions resulting in a pickup of eco-

nomic activities. This has helped to rebuild consumer confidence

despite poor performing labor and housing markets.

After shredding more than 8.5 million jobs during crisis years, the labor

market has managed to add 1.5 million jobs, which was barely suffi-

cient to keep up with growth of the work-age population. A large part of

the decline in the unemployment rate is attributable to a decline in par-

ticipation. The unemployment rate reached 9.6 percent in 2010.

14

Chapter 1: M

acroec

onomic Developm

ents

According to forecasts of the IMF, the real GDP of the US will increase

by 1.5 percent in 2011 and in 2012 by 1.8 percent with a large number

of unsold properties and high mortgages repressing consumption.

House prices in the US have been declining, with harmful effects on

household and financial balance sheets, deteriorating household and

business confidence. Unemployment is high at approximately 9.1 per-

cent in 2011 and is expected to remain so in 2012, holding back wages.

The fiscal deficit and debt have resulted in a decreased solvency rating

for the US, and financial turmoil in the Euro area has tightened financial

conditions and weakened global demand with consequences for the

US also.

Inflation is moderate at 3 percent in 2011, but up from 1.6 percent in

2010. In 2012, the inflation rate is predicted to drop back to 1.3 per-

cent, in line with the pullback of commodity prices.

There are, however, some downside risks to the projected economic

growth in the US: growth will suffer if the temporary payroll tax cuts and

increased unemployment insurance are discontinued in 2012 and if

political consensus on the design of debt reduction is not reached soon.

Furthermore, prolonged delay in recovery of house prices, sustained

losses in equity markets and upside risks on commodity prices would

further repress consumer spending.

Sooner-than-expected restored financial stability and consumer and

business confidence could strengthen growth on the short run.

The main challenge for the US lies in reducing the structural deficit and

public debt in an environment of weak growth and high unemployment.

Economic developments in Canada in 2010 mirrored developments in

the U.S.A. The deceleration reflected the drag on Canadian export from

weak US activity, strong import growth from investment spending and

cooling of domestic activities.

Canada’s GDP is estimated to have increased by 3.3 percent in 2010

and is projected to expand by 2.1 percent in 2011 and by 1.9 percent

in 2012, with domestic demand being the force behind the growth. Job

creation has rebounded at a faster pace compared to the U.S.A., but a

slower pace of recovery over the near term is expected to keep unem-

15

Chapter

1: Mac

roec

onomic Develo

pmen

ts

ployment at approximately 7.5 percent in 2011 and 2012.

US risks are expected to shape Canada’s outlook through real and

financial spillovers.

EuropeThe IMF estimates that GDP in Europe grew by 2.2 percent in 2010,

despite financial turbulence in peripheral countries of the Euro area

during the last quarter of 2010. Concerns about banking sector losses

and fiscal sustainability caused sovereign spreads to widen in the Euro

area. The situation was controlled by strong policy responses at national

and EU level with measures to improve fiscal balances and to push for-

ward with structural reforms in the affected areas, liquidity support and

security purchases by the ECB. Therefore, the damage to economic

activity was limited to affected areas only and did not spread to the rest

of Europe.

Nevertheless, the ongoing fiscal tightening and the effect of the crisis

on consumer and business confidence are repressing growth this year,

especially after the first quarter. The year 2011 is predicted to show a

real expansion of 2.0 percent in Europe while for 2012 a 1.5 percent

growth is estimated.

Growth in emerging countries was higher in 2010 at 4.5 percent, com-

pared to 1.8 percent in the advanced economies, and is predicted to

be higher at 4.3 percent in 2011. In 2012, however, growth in emerging

countries is expected to decline to 2.7 percent as domestic and external

demand moderates. In advanced countries, GDP growth of 1.6 and 1.1

percent in 2011 and 2012 respectively is expected. Prospects across

regions are likewise divergent, reflecting differences in the state of

public and private balance sheets and the stance of macroeconomic

policies.

Germany for instance, which has been the continent’s growth locomo-

tive, grew by 3.6 percent in 2010, but growth is expected to slow down

to 2.7 percent in 2011 and to 1.3 percent in 2012. The expected slow-

down is due to the withdrawal of fiscal support and an expected slow-

down in external demand growth.

16

Chapter 1: M

acroec

onomic Developm

ents

Retrenchment of fiscal stimulus, which is expected to reduce consump-

tion growth and weaken export growth as consequence of slower exter-

nal demand, will cause France’s growth rate in 2011 and 2012 to be

in line with the 1.5-percent growth rate of 2010.

In advanced economies outside the Euro area, activity growth is like-

wise differentiated. The UK’s economy, for instance, grew by 1.4 per-

cent in 2010 and is projected to grow by 1.1 percent in 2011 and 1.6

percent in 2012 as fiscal consolidation dampens domestic demand.

In Sweden, real activity grew by 5.7 percent in 2010, but the growth

rate is expected to decelerate to 4.4 and 3.8 percent in 2011 and 2012

respectively amid improving financial conditions and signs of over-

heating in the real-estate sector.

In emerging Europe, recovery is expected to continue, boosted by inter-

nal demand, owing to credit growth accompanied by accommodative

macroeconomic policies. Growth is expected to remain more subdued

in countries that experienced unsustainable domestic booms.

In general, countries that avoided major imbalances and have benefit-

ted from the strong rebound in global manufacturing are close to pre-

crisis growth rates in 2011. Some others are below pre-crisis rates

because of sharp economic adjustments as consequence of the finan-

cial crises while others are recuperating from recent crises while ad-

dressing a number of challenges, such as weak banking systems and

high unemployment. The rest of the European countries are likely to

grow at less than pre-crisis averages as some are shaken by contagion

from the Euro area periphery while others are less affected.

Inflation has remained subdued in advanced Europe at 1.9 and at 2.5

percent in 2010 and 2011 respectively, and is expected to remain low

at 1.5 percent in 2012 in the absence of inflation expectations and be-

cause there is still excess capacity. In emerging Europe, inflation has

been higher at 5.3 percent in 2010 and 2011 but is expected to decline

to 4.5 percent in 2012.

17

Chapter

1: Mac

roec

onomic Develo

pmen

ts

The uncertain environment dominated by tension from the euro area

debt crisis imply downside risks to growth in Europe, as well as negative

spillovers from slower US growth. Securing debt sustainability and

strengthening the financial systems remain a priority for most European

countries. The largest economies are already implementing measures

to reduce their deficits.

Commonwealth and Independent StatesRecovery in CIS has been proceeding at a steady pace, supported by

higher commodity prices that have been boosting production and em-

ployment in the region’s exporting countries. The rebound in real activity

in Russia is also benefiting other countries through trade, remittances

and investment. On the other hand, dependence on external financing

and lingering banking sector vulnerabilities are holding back growth in

several CIS economies.

Real activity in CIS increased by 4.6 percent in 2010 and is projected

to expand by 4.6 percent in 2011 and by 4.4 percent in 2012, but

growth prospects differ within the region.

In Russia and other energy exporters, growth is estimated to pick up

modestly with growth rates at approximately 4.5 percent in 2011 and

2012. Growth is expected to slow down slightly in 2012 compared to

2011 as energy prices decline somewhat. Energy importers are ex-

pected to benefit from the rebound in remittances from Russia and oth-

ers from the return of financial stability.

Inflation in the region has been on the rise, led by higher commodity

prices, especially in the first half of 2011, the high share of food in the

consumption basket and demand pressure.

For most countries in the region, prospects depend highly on the economic

development in Russia, the rest of the world and commodity prices. Higher

commodity prices represent an upside risk to commodity exporting coun-

tries. But global slowdown would reduce commodity prices, dampening

the prospects for the region. Furthermore, lower external demand from

advanced economies represents a downside risk.

The key challenge is to abort crisis-related macroeconomic and financial

18

Chapter 1: M

acroec

onomic Developm

ents

policies in a way that provides sufficient support to the incomplete re-

covery without jeopardizing price stability, reduce external vulnerability

and raise potential growth through a more diversified pattern of eco-

nomic development.

AsiaReal GDP growth in Asia is moderating after a sharp rebound from the

global crisis, with a GDP growth of 8.2 percent in 2010 and a projected

growth of 6.2 and 6.6 percent in 2011 and 2012 respectively. The strong

rebound is supported by a strong export performance, private domestic

demand and in some cases rapid credit growth. Asia continues to outpace

other regions but external demand in emerging Asia has dampened

recently because of slowdown in the US and the Euro area.

Inflation in Asia averaged 4.1 percent in 2010 and is projected to ave rage

5.3 and 4.0 in 2011 and 2012 respectively. Inflation was higher in

developing Asia than in advanced Asia in 2010, and the difference is

likely to remain. Inflation pressures are higher in economies with

sustained credit growth, positive output gaps, and/or relatively accom-

modative policies.

China, today the world’s second largest economy and its leading ex-

porter and manufacturer, will remain a powerful source of external de-

mand for Asian producers in the foreseeable future. Growth in China is

projected to remain robust at 9.5 percent in 2011 and 9.0 percent in

2012 after growing by 10.3 percent in 2010, driven by private demand

caused by rapid investment growth, favorable labor market conditions

and continued policies to increase disposable income of households.

Inflation pressure in China remains, but efforts to withdraw credit stimu-

lus and to restrain property price inflation have been gaining ground.

India’s economic growth slowed down in the last quarter of 2010 as the

manufacturing sector was held back in the wake of multiple interest-rate

increases by the central bank amid rising prices. The Reserve Bank of India

raised its benchmark lending rates in seven equal installments of 0.25

percentage points since the beginning of 2010 to control rising prices.

19

Chapter

1: Mac

roec

onomic Develo

pmen

ts

The Indian economy grew by 10.1 percent in 2010, led by infrastructural

investments, and is forecasted to grow by 7.8 and 7.5 percent in 2011

and 2012 respectively, driven by private consumption.

After a rapid growth at 8.4 percent in 2010, growth in the newly indus-

trialized Asian economies is projected to moderate at 4.7 percent in

2011 and 4.5 percent in 2012 as activity moderates to close positive

output gaps. Both the internal and external private demand remain

important drivers behind growth.

ASEAN economies grew by 6.9 percent in 2010 and are projected to

grow by 5.3 and 5.6 percent in 2011 and 2012 respectively, driven by

domestic demand. ASEAN economies are led by Indonesia, where

strong consumption and recovery in investments are projected to raise

growth to 6.4 percent in 2011 and 6.3 percent in 2012.

Japan, the third largest economy in the world after the US and China,

grew by 3.9 percent in 2010 and was one of the highest among the

advanced economies. Japan’s growth was driven by significant fiscal

stimulus and a rebound in exports. Forecasts for 2011 are somewhat

pessimistic, because of damages caused by the Tohuku earthquake.

Japan’s economy is projected to contract by 0.5 percent in 2011, de-

spite an expected vigorous expansion in the second half of 2011.

Growth is projected to increase to 2.3 percent in 2012, with activity

sharply rebounding on reconstruction investment. Japan experienced

deflation of 0.7 percent in 2010 and further deflation is projected of

approximately 0.5 percent in 2011 and 2012.

In Australia, flooding in key mining and agricultural regions subtracted

from growth in 2010. The economy grew by 2.7 percent in 2010 and

for 2011 and 2012 the economy is projected to grow by 1.8 and

percent respectively.

In New Zealand, despite the recent earthquakes, growth is projected to

pick up. In 2011 a 2.0-percent growth rate is projected after already

increased economic activities of 1.7 percent in 2010. In 2012 growth

is expected to rise to 3.8 percent supported by strong terms of trade

and positive trade spillovers from the region.

20

Chapter 1: M

acroec

onomic Developm

ents

The financial turbulence in the Euro area and the US pose downside

risks for the region, since these would affect export in Asia through

trade linkages. Despite increase in intraregional trade in Asia, two-third

of the final demand comes from outside the region.

The Middle East and North Africa According to the Economist Intelligence Unit (EIU), economic growth in

the Middle East and North Africa (MENA) picked up in 2010, boosted

by the increase in oil prices, a stronger global economy and loose do-

mestic policy conditions. According to estimates of the IMF, GDP in

MENA grew by 4.4 percent in 2010.

Production in many countries in the region has been boosted by higher

commodity prices and external demand. In addition, government spen d-

ing programs have been fostering recovery in many oil-exporting coun-

tries.

In contrast, political discontent and high unemployment are causing

social unrest in a number of countries, which might dampen short-term

economic growth as these factors weigh heavily on tourism receipts,

capital flows and investment. Based on the above mentioned factors,

the IMF forecasts that economic activities in the region will increase by

4 percent in 2011 and by 3.6 percent in 2012.

Growth in oil-exporting countries is projected to pick up to almost 5 per-

cent in 2011, slightly higher than the 4.4 percent in 2010. In Qatar, for

instance, economic activity is projected to increase by 18.7 percent

boosted by continued expansion in natural gas production and large in-

vestment expenditures. In Saudi Arabia, growth is forecasted to be 6.5

percent, supported by public infrastructural investments. In the Repu b-

lic of Iran, growth is anticipated to stall temporarily as subsidies for en-

ergy and other products are phased out. This reform is expected to yield

benefits on the longer run. Disruptions of oil production in Libya in-

creased oil supply by other OPEC suppliers.

In oil-importing countries, growth in economic activity is more subdued,

down to 1.4 percent in 2011 compared to 2010 (4.5 percent).

21

Chapter

1: Mac

roec

onomic Develo

pmen

ts

Activity in some countries will be constrained by domestic social unrest

and an associated slow recovery in tourism receipts and remittances.

Growth in oil-importing countries is projected at 2.6 percent in 2012,

harmed by a slow recovery in investment.

Inflation is high in the MENA region, reaching almost 10 percent in 2011,

but is expected to decline somewhat in 2012, reflecting receding

commodity prices. For oil-exporters, inflation is forecasted to fall from 10.8

percent in 2011 to 7.6 percent in 2012 while for oil-importing countries,

inflation is anticipated to stay below 8 percent during 2011 and 2012.

Downside risks are the domestic effects of political and social unrest

that could be larger than expected, especially if unrest spills over to

additional countries in the region. In addition, financial markets have

not stayed immune, and as these developments on the financial market

continue, higher funding costs for governments and firms could be the

result. Moreover, weak performance of advanced economies, mainly

the US and Europe, could adversely affect the region’s export earnings,

fiscal and external imbalances and growth.

The MENA region is challenged to raise growth and tackle high unem-

ployment, mainly among young people. Oil exporters should strengthen

or develop financial systems and promote economic diversification.

Sub-Saharan AfricaSub-Saharan Africa has recovered well from the financial crisis. The

region grew rapidly in 2010 by 5.4 percent. Growth in domestic demand

remained robust, trade and commodity prices rebounded and macro-

economic policies remained accommodative.

Terms of trade gains are supporting the region’s external balances and

gradual reorientation of export towards fast-growing regions such as

Asia is being sustained. As a consequence, according to the IMF, real

activity in Sub-Saharan Africa is projected to expand by 5.2 and 5.8

percent in 2011 and 2012 respectively.

22

Chapter 1: M

acroec

onomic Developm

ents

However, prospects differ considerably within the region. Growth is

being led by the low-income countries which are projected to grow by

approximately 6 percent in 2011 and by 6.5 percent in 2012, stimu-

lated by launching of oil production (Ghana) and infrastructural invest-

ment and improved agricultural production (Kenya and Ethiopia).

The prospect of oil-exporting countries is likewise positive, with a fore-

casted growth rate of almost 6 percent in 2011 and over 7 percent in

2012, sustained by continued strength in domestic public investment

spending and strong rebound in oil production in Angola following the

disruption in 2011.

Middle-income countries are more vulnerable to the crisis as they are

more integrated with the global market, hence recovery is delayed. In

South Africa, the region’s largest economy, recovery is projected to remain

relatively modest at approximately 3.5 percent in 2011 and 2012,

because of an increase in unemployment, high household debt, low

capacity utilization, the slow down in advanced countries and substantial

real exchange rate appreciation. Growth is driven by private consumption

and investment supported by a low interest rate environment.

The region is vulnerable to some external forces, however. Europe is

the main trading partner for the region’s non-oil exporting countries.

Consequently a slowdown in Europe hurts manufacturing exporters in

the region.

Implications for CuraçaoAfter contracting by 0.5 percent in 2009, activities in Curaçao increased

by 0.1 percent in 2010, lagging far behind the Latin American and

Caribbean region in general and the Caribbean in particular. The slight

increase in economic activities is attributable to increased public

consumption of goods and services with regards to the dismantling

activities and the SEI program and increased private consumption.

These increases were offset by decreased public and private invest-

ments and export.

23

Chapter

1: Mac

roec

onomic Develo

pmen

ts

Curaçao is largely dependent on the import of goods from its main

tra ding partners, Venezuela, the U.S.A. and the Netherlands. Hence,

inflationary pressure in these regions leads to increased inflation in

Curaçao. Inflation remained subdued in the main trading countries and

as a consequence inflation in Curaçao remained moderate at 2.8

percent.

For 2011, the economy is expected to expand by 0.3 percent and inflation

to be slightly lower than the year before.

However, since Curaçao’s export of principally (tourism) services is largely

to the main trading countries, the risks of decreased growth in these coun-

tries pose risks to the island’s medium-term macroeconomic perfor -

mance. Any slowdown in growth in these countries would negatively affect

demand for the island’s tourism services.

Curaçao has achieved a sustainable level of public debt and this poses

prospects for stable long-term economic growth in general where

investments in infrastructure and socio-economic projects can be

improved. A compulsory balanced budget rule has been set, aimed at

avoiding the unrestrained buildup of public debt in the future.

On the downside, development aid from the Netherlands is planned to

stop by 2013, threatening the infrastructural and socioeconomic invest-

ments.

Sources:

Deloitte: 4th Quarter 2010: Global Economic Outlook. Multi Speed Recovery.

Economist Intelligence Unit, (The Economist) May 2011

International Monetary Fund: World Economic Outlook, April 2011

International Monetary Fund: World Economic Outlook Update, June 2011

International Monetary Fund: World Economic Outlook, September 2011

United Nations: Economic Development in Africa 2010 south – south Coopera-

tion: Africa and the new forms of Development Partnership

World Bank: East Asia and Pacific Economic Update 2011, Vol.1

World Bank: Global Economic Prospects; Crisis, Finance and Growth 2010.

24

Chapter 1: M

acroec

onomic Developm

ents

Websites:

http://www.unctad.org

http://www.nytimes.com

http://www.blogjaviervega.blogspot.com

http://www.cfr.org/refugees-and-the-displaced/eu-concerns-over-mideast-mi-

grants/p24672

http://www.eclac.org/cgi-

bin/getProd.asp?xml=/publicaciones/xml/4/41974/P41974.xml&xsl=/de/tpl-

i/p9f.xsl&base=/tpl-i/top-bottom.xslt

25

Chapter

1: Mac

roec

onomic Develo

pmen

ts

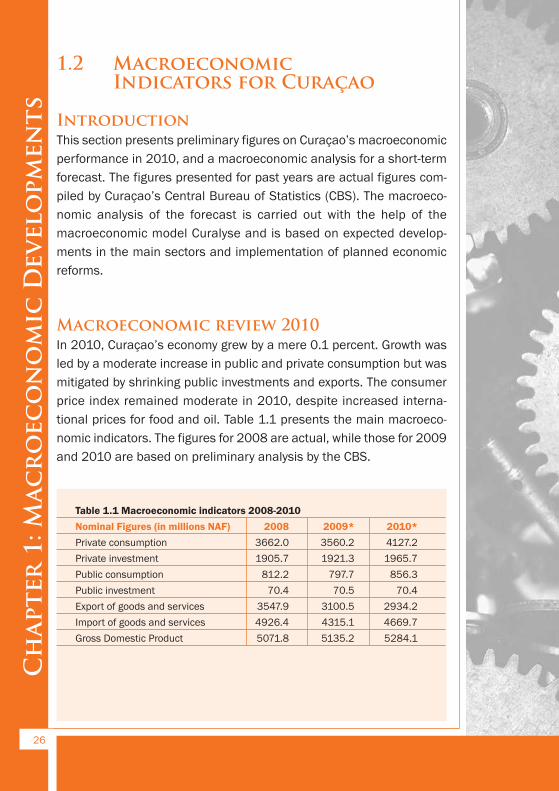

1.2 Macroeconomic Indicators for Curaçao

IntroductionThis section presents preliminary figures on Curaçao’s macroeconomic

performance in 2010, and a macroeconomic analysis for a short-term

forecast. The figures presented for past years are actual figures com-

piled by Curaçao’s Central Bureau of Statistics (CBS). The macroeco-

nomic analysis of the forecast is carried out with the help of the

macroeconomic model Curalyse and is based on expected develop-

ments in the main sectors and implementation of planned economic

reforms.

Macroeconomic review 2010In 2010, Curaçao’s economy grew by a mere 0.1 percent. Growth was

led by a moderate increase in public and private consumption but was

mitigated by shrinking public investments and exports. The consumer

price index remained moderate in 2010, despite increased interna-

tional prices for food and oil. Table 1.1 presents the main macroeco-

nomic indicators. The figures for 2008 are actual, while those for 2009

and 2010 are based on preliminary analysis by the CBS.

Table 1.1 Macroeconomic indicators 2008-2010

Nominal Figures (in millions NAF) 2008 2009* 2010*

Private consumption 3662.0 3560.2 4127.2

Private investment 1905.7 1921.3 1965.7

Public consumption 812.2 797.7 856.3

Public investment 70.4 70.5 70.4

Export of goods and services 3547.9 3100.5 2934.2

Import of goods and services 4926.4 4315.1 4669.7

Gross Domestic Product 5071.8 5135.2 5284.1

26

Chapter 1: M

acroec

onomic Developm

ents

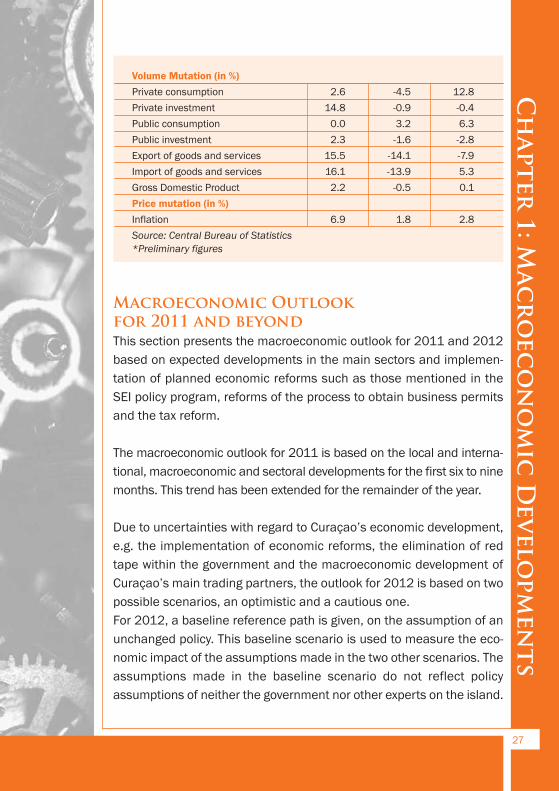

Volume Mutation (in %)

Private consumption 2.6 -4.5 12.8

Private investment 14.8 -0.9 -0.4

Public consumption 0.0 3.2 6.3

Public investment 2.3 -1.6 -2.8

Export of goods and services 15.5 -14.1 -7.9

Import of goods and services 16.1 -13.9 5.3

Gross Domestic Product 2.2 -0.5 0.1

Price mutation (in %)

Inflation 6.9 1.8 2.8

Source: Central Bureau of Statistics

*Preliminary figures

Macroeconomic Outlook for 2011 and beyondThis section presents the macroeconomic outlook for 2011 and 2012

based on expected developments in the main sectors and implemen-

tation of planned economic reforms such as those mentioned in the

SEI policy program, reforms of the process to obtain business permits

and the tax reform.

The macroeconomic outlook for 2011 is based on the local and interna-

tional, macroeconomic and sectoral developments for the first six to nine

months. This trend has been extended for the remainder of the year.

Due to uncertainties with regard to Curaçao’s economic development,

e.g. the implementation of economic reforms, the elimination of red

tape within the government and the macroeconomic development of

Curaçao’s main trading partners, the outlook for 2012 is based on two

possible scenarios, an optimistic and a cautious one.

For 2012, a baseline reference path is given, on the assumption of an

unchanged policy. This baseline scenario is used to measure the eco-

nomic impact of the assumptions made in the two other scenarios. The

assumptions made in the baseline scenario do not reflect policy

assumptions of neither the government nor other experts on the island.

27

Chapter

1: Mac

roec

onomic Develo

pmen

ts

Outlook 2011This section presents the assumptions which are used to forecast the

macroeconomic developments in 2011. The assumptions mentioned

below occur autonomously and, as mentioned previously, are based on

indications of the developments in the first six to nine months of 2011:

· An increase in the number of stay-over arrivals, especially from the

North-American and South-American market, mitigated by a slow-

down of arrivals from the European market. This is reflected by a

7-percent increase in stay-over nights in 2011 compared to 2010;

· A 1-percent decline in private investments. The incentives to invest

remain withheld owing to, among other factors, the lower occupancy

rate of hotels in the past years and international economic and

financial turmoil. The previous decline in occupancy rates resulted

in postponement of planned investments in room inventory to 2012;

· NAF 20 million in total investments related to SEI projects;

· Public finances show no deficit, in accordance with the agreements

with College financieel toezicht (Cft). Real public consumption

declines by approximately 10 percent, as it picks up in the third and

the fourth quarter of 2011. Public investments increase by 20

percent in 2011 compared to 2010 as they slow down in the second

half; and

· Non-tourism exports show no real growth in 2011 compared to

2010.

The results based on the abovementioned assumptions are presented

in table 1.2. The increase in exports in the form of tourism services

results in a higher demand for local products and services. No invest-

ments to handle the increased demand are shown, because there

already is sufficient inventory to deal with the increased demand of the

tourism sector. As business production increases to accommodate the

higher local demand, employment by enterprises grows. However, this

growth in employment is not sufficient to stimulate a decrease in the

number of unemployed. The increased employment of businesses,

combined with the increased wage rate, results in an increased con-

sumption of 0.2 percent. This increased consumption can be derived

28

Chapter 1: M

acroec

onomic Developm

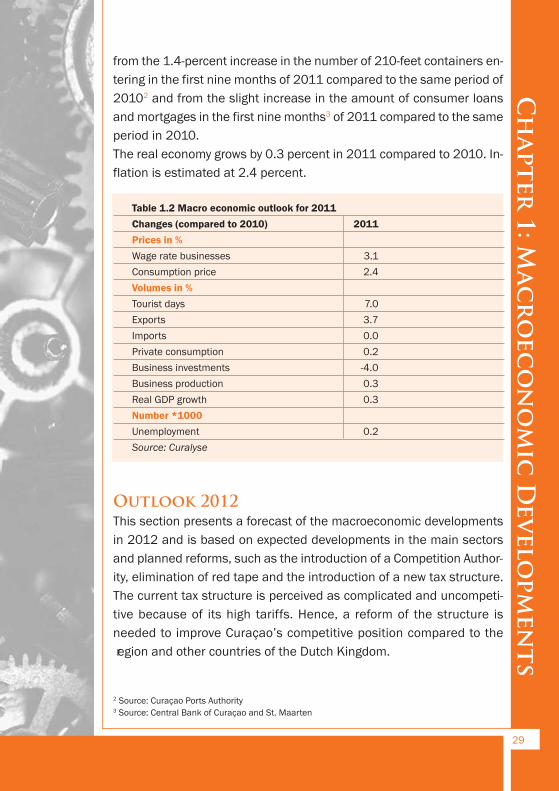

ents

from the 1.4-percent increase in the number of 210-feet containers en-

tering in the first nine months of 2011 compared to the same period of

20102 and from the slight increase in the amount of consumer loans

and mortgages in the first nine months3 of 2011 compared to the same

period in 2010.

The real economy grows by 0.3 percent in 2011 compared to 2010. In-

flation is estimated at 2.4 percent.

Table 1.2 Macro economic outlook for 2011

Changes (compared to 2010) 2011

Prices in %

Wage rate businesses 3.1

Consumption price 2.4

Volumes in %

Tourist days 7.0

Exports 3.7

Imports 0.0

Private consumption 0.2

Business investments -4.0

Business production 0.3

Real GDP growth 0.3

Number *1000

Unemployment 0.2

Source: Curalyse

Outlook 2012This section presents a forecast of the macroeconomic developments

in 2012 and is based on expected developments in the main sectors

and planned reforms, such as the introduction of a Competition Author-

ity, elimination of red tape and the introduction of a new tax structure.

The current tax structure is perceived as complicated and uncompeti-

tive because of its high tariffs. Hence, a reform of the structure is

needed to improve Curaçao’s competitive position compared to the

region and other countries of the Dutch Kingdom.

29

Chapter

1: Mac

roec

onomic Develo

pmen

ts

2 Source: Curaçao Ports Authority3 Source: Central Bank of Curaçao and St. Maarten

Baseline scenarioFor the purpose of measuring the impact of the possible scenarios, first

the baseline scenario is given. The assumptions of the baseline

scenario are:

· A 2-percent increase in stay-over nights, which is the average over

the past 15 years;

· The amount of private and public consumption and investment will

remain at the same level in 2012 as in 2011;

· The investments and reforms within the framework of the SEI will

be neglected; and

· Exports in the non-tourism sectors show zero growth in 2012

compared to 2011.

The macroeconomic effect of the baseline scenario is presented in

table 1.3. In this scenario, growth in 2012 is led by the increase in

tourism arrivals which manifests itself in a 2-percent increase in the

number of stay-over nights. This slight increase in tourism demand

encourages a slight (0.1%) increase in business production and, as a

consequence, in real GDP also of 0.1 percent. The increased demand

is not enough to increase the number of jobs available and accommo-

date citizens that are entering the labor market. Hence, the number of

unemployed persons increases by 300.

Inflation is estimated to follow the trend in 2011 at 2.3 percent.

Optimistic scenarioFor the optimistic scenario, the following assumptions are made:

· Stay-over nights will increase by 10 percent in 2012 compared to

2011 owing to intensified marketing efforts in existing markets and

the tapping of new markets such as Canada and Germany;

· The new fiscal structure is introduced as of January 1, 2012 and

includes:

o a decrease in profit tax, from 34.5 percent to 27.5 percent;

o a reform of the structure of wage and income taxation;

o an increase of turnover tax from 5 to 6 percent; and

o a decrease of the excise duty on gasoline of NAF 15.75 per

100 liter and on Low Sulfur Diesel of NAF 8.50 per 100 liter.

30

Chapter 1: M

acroec

onomic Developm

ents

· Private investments increase by NAF 38 million as investments in

room inventory are continued. The hotel occupancy rate reaches

the level of 75 percent, which will encourage new investments in

the tourism sector;

· Investments within the framework of the SEI amount to

NAF 40 million in 2012; and

· The Competition Authority and Red Carpet instead of Red Tape are

fully introduced implying an increase of labor productivity of

0.25 percent.

· Other assumptions remain the same as in the baseline scenario.

The macroeconomic impact of the optimistic scenario is given in table

1.3. In the optimistic scenario, growth in 2012 is led by an increase in

the number of stay-over nights, increased private investments and

increased labor productivity. Stay-over nights increase by 10 percent in

2012 owing to, among other factors, increased marketing efforts in the

North-American market, especially in the North-Eastern part of North

America and the new air connection established with Air Berlin in the

last quarter of 2011.

The higher number of tourists in 2011 and the first months of 2012

gives a boost to private investments in 2012 with a NAF 38-million

expansion of the room inventory as planned, according to the Curaçao

Tourist Board (CTB).

Most of the remaining SEI budget is used. Hence, SEI investments are

for an amount of NAF 40 million. The SEI investments accelerate public

consumption and investment as several SEI projects are co-financed

by the government.

The higher tourism demand, public consumption and public and private

investments boost economic growth by increasing business production,

which on its turn boosts job creation. Unemployment is reduced by 200

persons, contributing to an increased real private consumption of 0.2

percent. The growth of private consumption is mitigated by the higher

turnover tax, which causes an increase in prices. The interaction

between increased local demand and supply results in an increased

real GDP of 0.9 percent.

The wage rate is increased because of the increase in productivity.

31

Chapter

1: Mac

roec

onomic Develo

pmen

ts

The increase in turnover tax and wages results in an inflation of 3.4

percent in 2012.

Cautious scenarioThe cautious scenario is based on the following assumptions:

· The marketing efforts are less intense compared to the optimistic

scenario, resulting in a 6-percent increase in stay-over nights in

2012 compared to 2011;

· The new fiscal structure is introduced per January 1, 2012 as men-

tioned in the optimistic scenario;

· Private investments increase by NAF 20 million compared to 2011;

· Investments within the framework of the SEI are for NAF 20 million;

and

· The introduction of the Competition Authority and Red Carpet in-

stead of Red Tape is delayed, implying an increase in labor produc-

tivity of only 0.1 percent.

· Other assumptions remain the same as in the baseline scenario.

For the cautious scenario, a 6-percent increase in stay-over nights is

considered in 2012. The increase in tourism demand of the previous

and current year induces investments in room inventory by NAF 20 mil-

lion. SEI investments are for another NAF 20 million, boosting public

consumption and investments.

The higher tourism demand, public consumption and private and public

investments give a boost to economic growth through an increase in

demand for local products and services. However, due to increased

labor productivity, the demand for labor remains idle. The lack of job

creation has a negative impact on consumption as the purchasing

power of households decrease because of the increased consumption

prices and is not compensated by an increase in wages.

Business production and real GDP increase by 0.3 percent each, lack-

ing force to increase employment. Unemployment increases by 200 per-

sons due to migration and demographic developments. Inflation is at

3.3 percent, as the turnover tax is raised and wage rates are increased.

32

Chapter 1: M

acroec

onomic Developm

ents

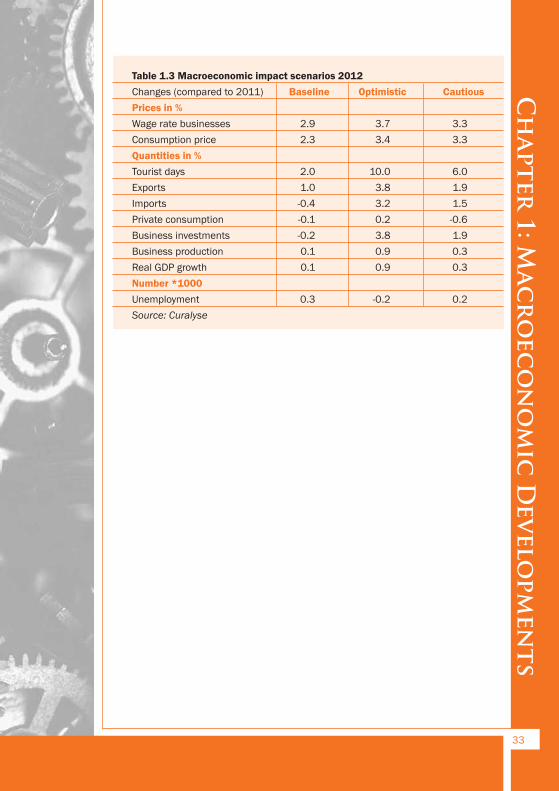

Table 1.3 Macroeconomic impact scenarios 2012

Changes (compared to 2011) Baseline Optimistic Cautious

Prices in %

Wage rate businesses 2.9 3.7 3.3

Consumption price 2.3 3.4 3.3

Quantities in %

Tourist days 2.0 10.0 6.0

Exports 1.0 3.8 1.9

Imports -0.4 3.2 1.5

Private consumption -0.1 0.2 -0.6

Business investments -0.2 3.8 1.9

Business production 0.1 0.9 0.3

Real GDP growth 0.1 0.9 0.3

Number *1000

Unemployment 0.3 -0.2 0.2

Source: Curalyse

33

Chapter

1: Mac

roec

onomic Develo

pmen

ts

1.3 Labor-Market Developments

IntroductionThis section will give a summary of important developments regarding

the labor market in Curaçao. Unfortunately, the labor market statistics4

for 2010 are not available because the CBS did not conduct the Labor

Force Survey. As a consequence, a different approach is used this time.

Based on some other useful indicators, an approximation of the

develop ments is discussed. These indicators are:

o the number of requests for dismissal;

o the number of new registrations for assistance in finding a job; and

o the number of vacancies and placements into these vacancies.

The statistics were collected from the Ministry of Social Affairs, Labor

and Welfare (the former DirAZ and DWI).

An overview from 2006 on is given for the purpose of comparing the

developments in 2010 to those of previous years.

Local Developments

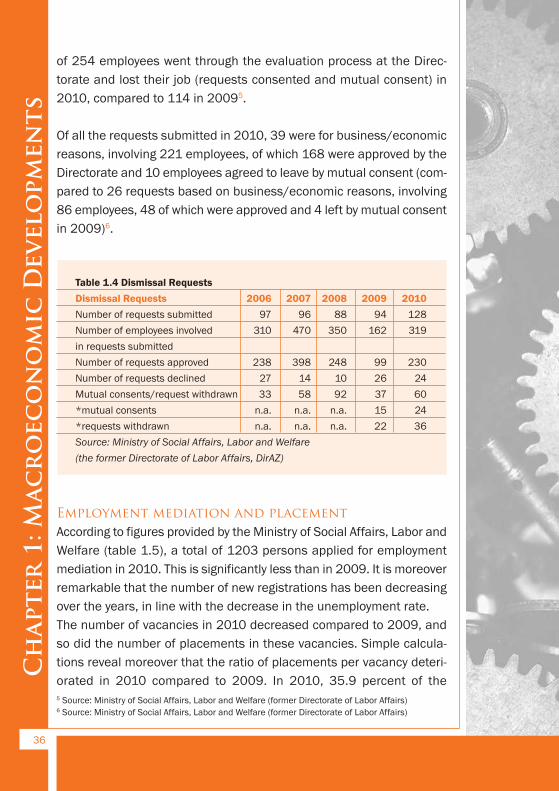

Dismissal RequestsTable 1.4 provides an overview of different developments related to dis-

missals in Curaçao.

In certain cases, when an employer wants to terminate a contract with

an employee, the approval of the former Directorate of Labor Affairs

(DirAZ, now a section of the Ministry of Social Affairs, Labor and Wel-

fare) is needed. The dismissal legislation is primarily meant to protect

the weaker party of the labor market, the employee, from unreasonable

and arbitrary dismissal, but also keeps the interests of the employer in

mind. Since proper functioning of the business comes first to the

employer, the possibility should exist to discharge employees within a

relatively short period of time depending on the business results.

34

Chapter 1: M

acroec

onomic Developm

ents

4 Traditionally, the Central Bureau of Statistics (CBS) provides the relevant statistics through their

Labor Force Survey. However, CBS was preparing intensely for the Census that took place in March

and April 2011.

A dysfunctional employee may also hamper the company’s operation,

so in such cases too it should be possible for the employer to terminate

the work relation with such an employee.

The dismissal ordinance is not applicable to:

· employees of public corporations (civil servants, as well as laborers

and employees working for the government on labor contracts);

· educational personnel and teachers;

· clergymen (priests and ministers, for example);

· employees that perform domestic labor in private households (do-

mestic personnel);

· directors’ labor contracts;

· fixed-term labor contracts, except fixed-term contracts that are di-

rectly or indirectly preceded by a contract without a fixed term or

contracts in which the same worker has successively worked for dif-

ferent employers, who can reasonably be considered to be each

other’s successors with regard to the work performed; and

· in cases of bankruptcy.

In some other cases approval from the Directorate is not required, e.g.

dismissal “on the spot” (in case of theft, gross neglect of duties, drunk-

enness or debauchery during work by the employee), dismissal by mu-

tual consent, the expiring of a fixed-term labor contract, dismissal within

the trial period or dissolution of the labor contract by court.

As can be seen in table 1.4, a total of 128 collective requests for dis-

missal were made in 2010 involving a total of 319 employees. The Di-

rectorate approved 230 of these individual dismissal requests. These

employees lost their jobs. An additional 24 employees also lost their

jobs when they agreed to terminate the labor agreement without going

through the dismissal evaluation process (mutual consent). A total of

24 individual requests were declined by the Directorate.

The number of submitted requests for dismissal was higher in 2010

compared to the previous years. The number of employees involved in

the requests almost doubled compared to 2009 and the number of re-

quests consented was more than double the number in 2009. A total

35

Chapter

1: Mac

roec

onomic Develo

pmen

ts

of 254 employees went through the evaluation process at the Direc-

torate and lost their job (requests consented and mutual consent) in

2010, compared to 114 in 20095.

Of all the requests submitted in 2010, 39 were for business/economic

reasons, involving 221 employees, of which 168 were approved by the

Directorate and 10 employees agreed to leave by mutual consent (com-

pared to 26 requests based on business/economic reasons, involving

86 employees, 48 of which were approved and 4 left by mutual consent

in 2009)6.

Table 1.4 Dismissal Requests

Dismissal Requests 2006 2007 2008 2009 2010

Number of requests submitted 97 96 88 94 128

Number of employees involved 310 470 350 162 319

in requests submitted

Number of requests approved 238 398 248 99 230

Number of requests declined 27 14 10 26 24

Mutual consents/request withdrawn 33 58 92 37 60

*mutual consents n.a. n.a. n.a. 15 24

*requests withdrawn n.a. n.a. n.a. 22 36

Source: Ministry of Social Affairs, Labor and Welfare

(the former Directorate of Labor Affairs, DirAZ)

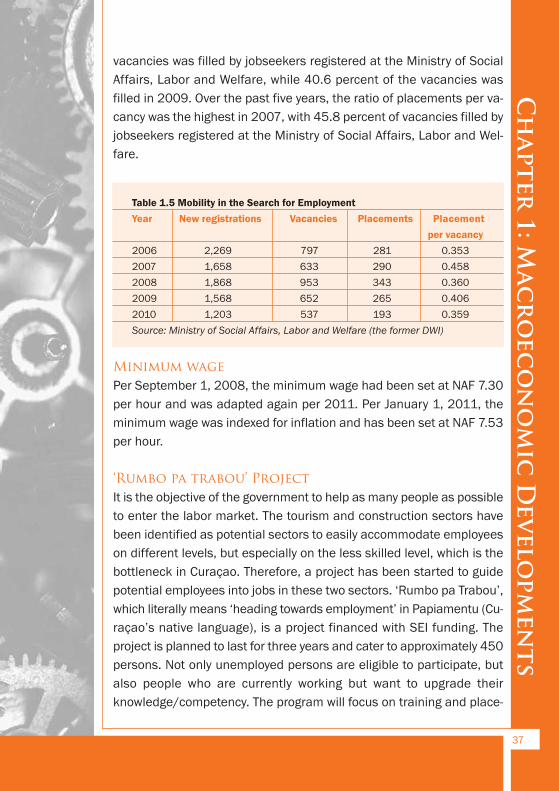

Employment mediation and placementAccording to figures provided by the Ministry of Social Affairs, Labor and

Welfare (table 1.5), a total of 1203 persons applied for employment

mediation in 2010. This is significantly less than in 2009. It is moreover

remarkable that the number of new registrations has been decreasing

over the years, in line with the decrease in the unemployment rate.

The number of vacancies in 2010 decreased compared to 2009, and

so did the number of placements in these vacancies. Simple calcula-

tions reveal moreover that the ratio of placements per vacancy deteri-

orated in 2010 compared to 2009. In 2010, 35.9 percent of the

36

Chapter 1: M

acroec

onomic Developm

ents

5 Source: Ministry of Social Affairs, Labor and Welfare (former Directorate of Labor Affairs)6 Source: Ministry of Social Affairs, Labor and Welfare (former Directorate of Labor Affairs)

vacancies was filled by jobseekers registered at the Ministry of Social

Affairs, Labor and Welfare, while 40.6 percent of the vacancies was

filled in 2009. Over the past five years, the ratio of placements per va-

cancy was the highest in 2007, with 45.8 percent of vacancies filled by

jobseekers registered at the Ministry of Social Affairs, Labor and Wel-

fare.

Table 1.5 Mobility in the Search for Employment

Year New registrations Vacancies Placements Placement

per vacancy

2006 2,269 797 281 0.353

2007 1,658 633 290 0.458

2008 1,868 953 343 0.360

2009 1,568 652 265 0.406

2010 1,203 537 193 0.359

Source: Ministry of Social Affairs, Labor and Welfare (the former DWI)

Minimum wagePer September 1, 2008, the minimum wage had been set at NAF 7.30

per hour and was adapted again per 2011. Per January 1, 2011, the

minimum wage was indexed for inflation and has been set at NAF 7.53

per hour.

‘Rumbo pa trabou’ ProjectIt is the objective of the government to help as many people as possible

to enter the labor market. The tourism and construction sectors have

been identified as potential sectors to easily accommodate employees

on different levels, but especially on the less skilled level, which is the

bottleneck in Curaçao. Therefore, a project has been started to guide

potential employees into jobs in these two sectors. ‘Rumbo pa Trabou’,

which literally means ‘heading towards employment’ in Papiamentu (Cu-

raçao’s native language), is a project financed with SEI funding. The

project is planned to last for three years and cater to approximately 450

persons. Not only unemployed persons are eligible to participate, but

also people who are currently working but want to upgrade their

knowledge/competency. The program will focus on training and place-

37

Chapter

1: Mac

roec

onomic Develo

pmen

ts

ment of people on the local labor market. Participants are guaranteed

a job after finishing the program and will be assisted during the first six

months of their new job.

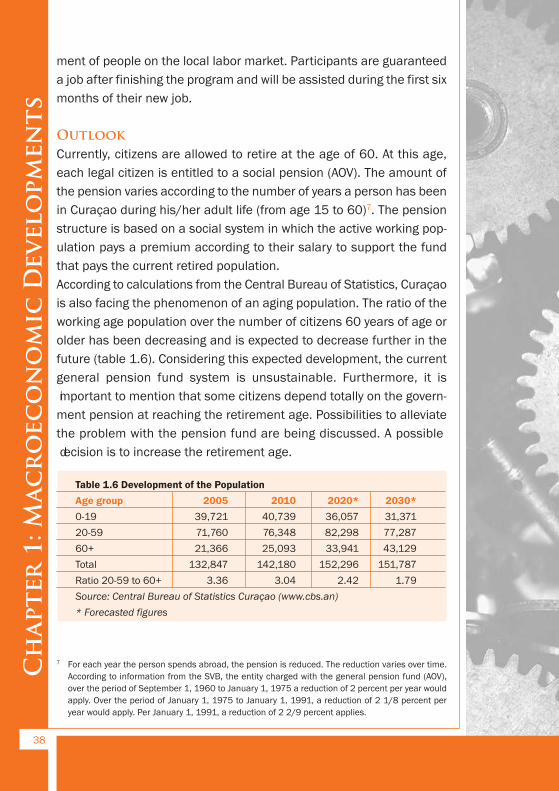

OutlookCurrently, citizens are allowed to retire at the age of 60. At this age,

each legal citizen is entitled to a social pension (AOV). The amount of

the pension varies according to the number of years a person has been

in Curaçao during his/her adult life (from age 15 to 60)7. The pension

structure is based on a social system in which the active working pop-

ulation pays a premium according to their salary to support the fund

that pays the current retired population.

According to calculations from the Central Bureau of Statistics, Curaçao

is also facing the phenomenon of an aging population. The ratio of the

working age population over the number of citizens 60 years of age or

older has been decreasing and is expected to decrease further in the

future (table 1.6). Considering this expected development, the current

general pension fund system is unsustainable. Furthermore, it is

important to mention that some citizens depend totally on the govern-

ment pension at reaching the retirement age. Possibilities to alleviate

the problem with the pension fund are being discussed. A possible

decision is to increase the retirement age.

Table 1.6 Development of the Population

Age group 2005 2010 2020* 2030*

0-19 39,721 40,739 36,057 31,371

20-59 71,760 76,348 82,298 77,287

60+ 21,366 25,093 33,941 43,129

Total 132,847 142,180 152,296 151,787

Ratio 20-59 to 60+ 3.36 3.04 2.42 1.79

Source: Central Bureau of Statistics Curaçao (www.cbs.an)

* Forecasted figures

38

Chapter 1: M

acroec

onomic Developm

ents

7 For each year the person spends abroad, the pension is reduced. The reduction varies over time.

According to information from the SVB, the entity charged with the general pension fund (AOV),

over the period of September 1, 1960 to January 1, 1975 a reduction of 2 percent per year would

apply. Over the period of January 1, 1975 to January 1, 1991, a reduction of 2 1/8 percent per

year would apply. Per January 1, 1991, a reduction of 2 2/9 percent applies.

Considering the pool of unemployed and in an effort to stimulate

among locals, a new act has been proposed to the Executive Council.

This proposal sets a quota on the number of foreigners working in the

firms in Curaçao. A ratio of 1 foreigner per 5 locals (20% foreigners and

80% locals) in each firm has been proposed. In the proposal, locals are

defined as persons born in Curaçao or whose mother or father, with

Dutch citizenship, was born in Curaçao, or persons born on one of the

other islands of the former Netherlands Antilles and living in Curaçao

by October 10, 2010.

The proposal has been approved by the Council and is awaiting legisla-

tion. It can be expected that some businesses will have difficulty to with

this act.

39

Chapter

1: Mac

roec

onomic Develo

pmen

ts

1.4 Public Finances

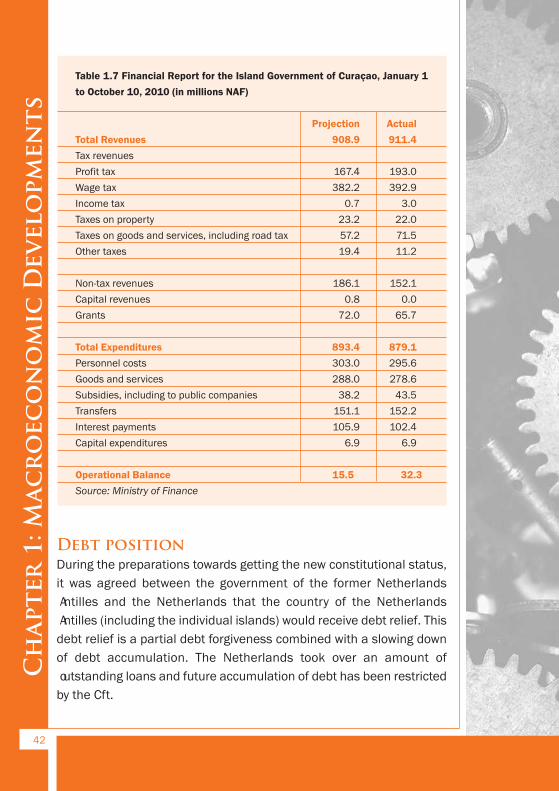

IntroductionThe year 2010 marked a transition year for Curaçao and the public

finances of Curaçao. On October 10, 2010, Curaçao became an

autonomous country within the Dutch Kingdom and the two govern-