Cpsp competitive analysis

41

Creating and Presenting Strategic Plans Competitive Analysis and Strategies (B.2.4.)

-

Upload

prof-patrick-mcnamee -

Category

Business

-

view

248 -

download

0

Transcript of Cpsp competitive analysis

Creating and Presenting Strategic Plans

Competitive Analysis and Strategies (B.2.4.)

Competition at 3 Levels

B.2.3. Competitive Analysis

B.2.3.1.Industry Forces

B.2.3.2.Firm Position

B.2.3.3. Actual Competitors

Profit Levels for Pharmaceutical Manufacturers in 2014 Fortune 500 List

Company Codes: JNJ: Johnson and Johnson, PFE: Pfizer, MRK: Merch, LLY: Eli Lilly and Company, ABBV: AbbVie,

AMBN: Amgen, BMY: Bristonl-Myers Squibb Company, GILD: Gilead Sciences, BIIB: Biogen Idec, MYL: Mylan,

CELG: Celgene, AGN: Allergen

Source: http://www.drugchannels.net/2014/06/profits-in-2014-fortune-500.html

0

30

60

90

120

JNJPFE

MRKLLY ABBV

AMGNBMY GILD

BIIB MYL CELGAGN

92.7

5

0.8

18.8

6.8

11.4

26.3 22.5

5.9

31.2

11.634.6

26.326.9

7.3 5.0

34.8

68.5

104.5

91.0

58.1

115.3

21.3

Annualized Return To Investors (2003 - 2013) (%) Total Return to Investors 2013 (%)

(%)

Coincidence?

Luck?

Supply and demand?

No

Underlying structure

Not just competitors, other forces

Degree of Competition in Any Industry

Porter’s 5 Competitive Forces Model

Power of BuyersPower of Suppliers

Threat of New Entrants

Threat of Substitutes

Degree

of

Rivalry

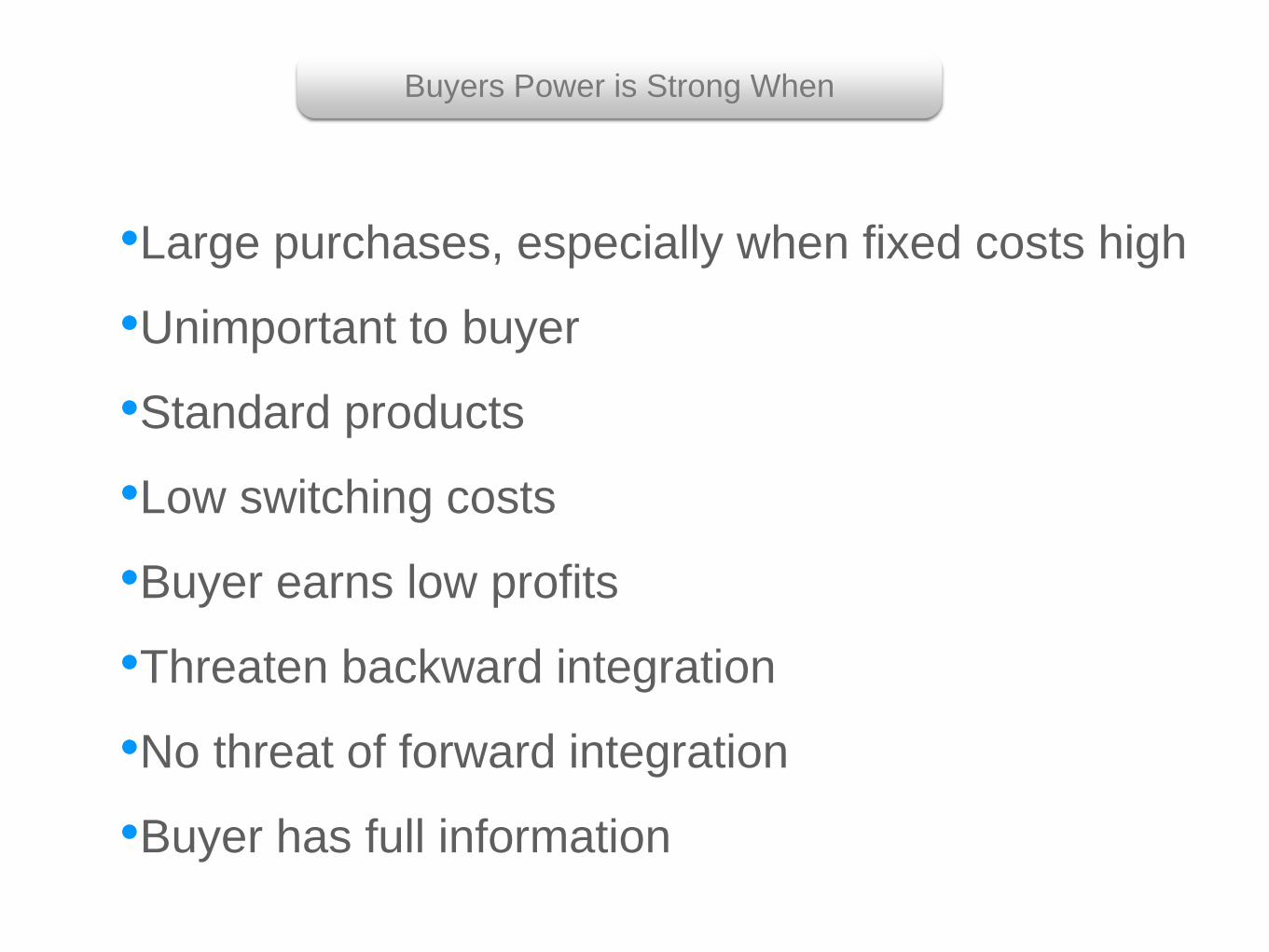

•Large purchases, especially when fixed costs high

•Unimportant to buyer

•Standard products

•Low switching costs

•Buyer earns low profits

•Threaten backward integration

•No threat of forward integration

•Buyer has full information

Buyers Power is Strong When

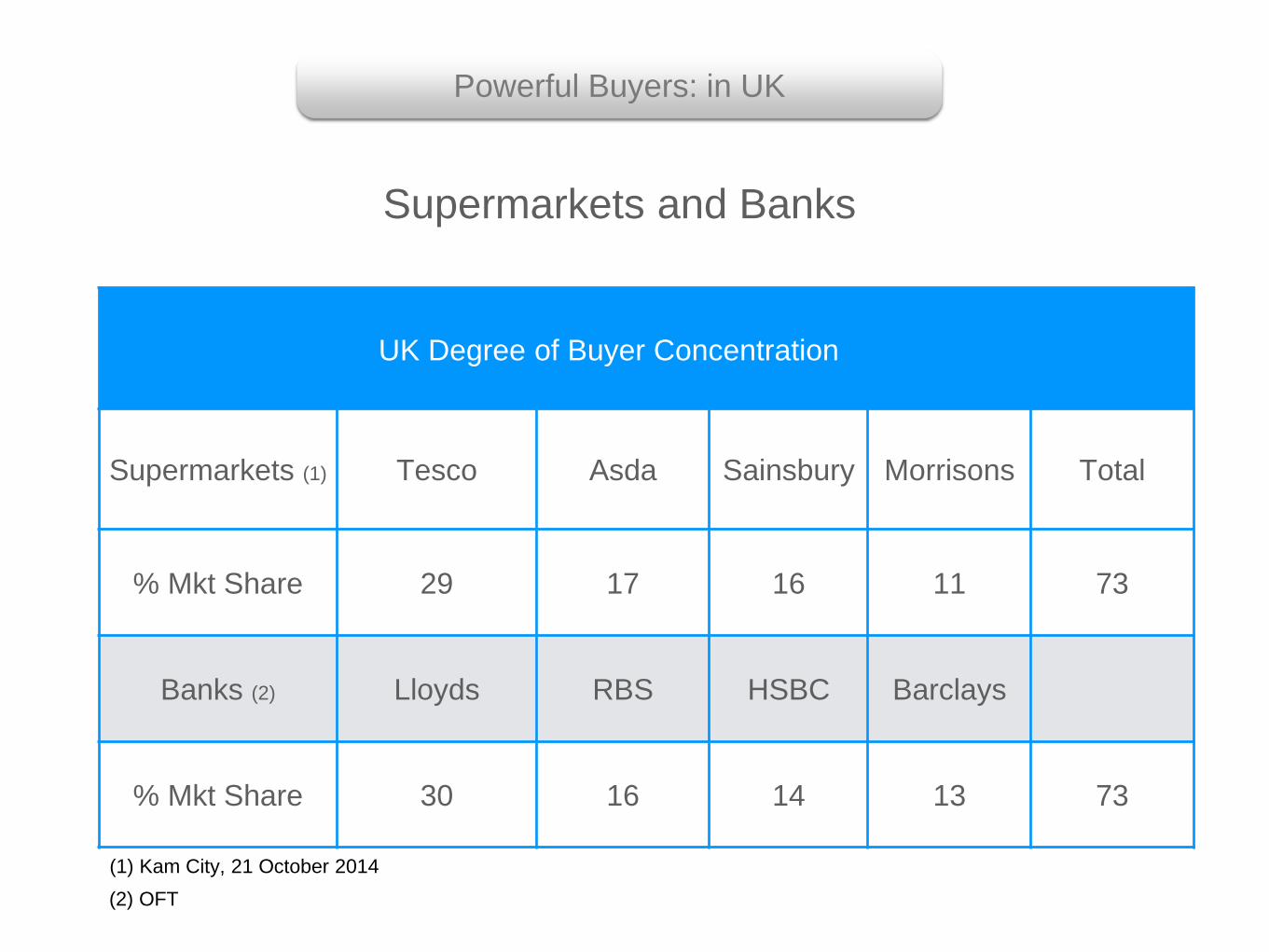

Powerful Buyers: in UK

UK Degree of Buyer Concentration

Supermarkets (1) Tesco Asda Sainsbury Morrisons Total

% Mkt Share 29 17 16 11 73

Banks (2) Lloyds RBS HSBC Barclays

% Mkt Share 30 16 14 13 73

(1) Kam City, 21 October 2014

(2) OFT

Supermarkets and Banks

•Suppliers highly concentrated

•Government is a supplier

•No substitutes

•Buyer has high switching costs

•Threatens forward integration

•Not an important customer of supplier

•Supplier product important

•Supplier’s products differentiated

Supplier Power (Mirror of Buyer) is Strong

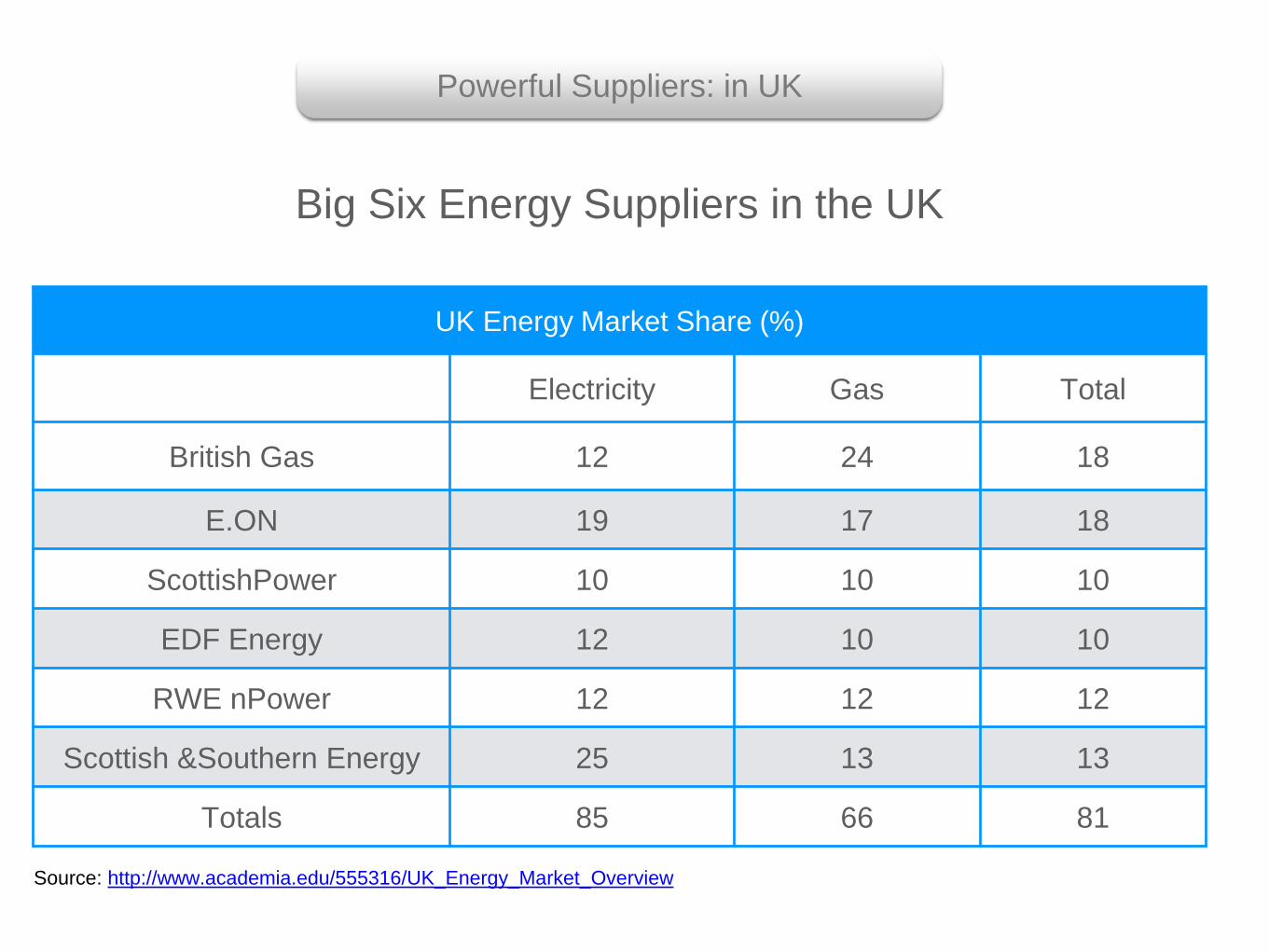

Powerful Suppliers: in UK

UK Energy Market Share (%)

Electricity Gas Total

British Gas 12 24 18

E.ON 19 17 18

ScottishPower 10 10 10

EDF Energy 12 10 10

RWE nPower 12 12 12

Scottish &Southern Energy 25 13 13

Totals 85 66 81

Source: http://www.academia.edu/555316/UK_Energy_Market_Overview

Big Six Energy Suppliers in the UK

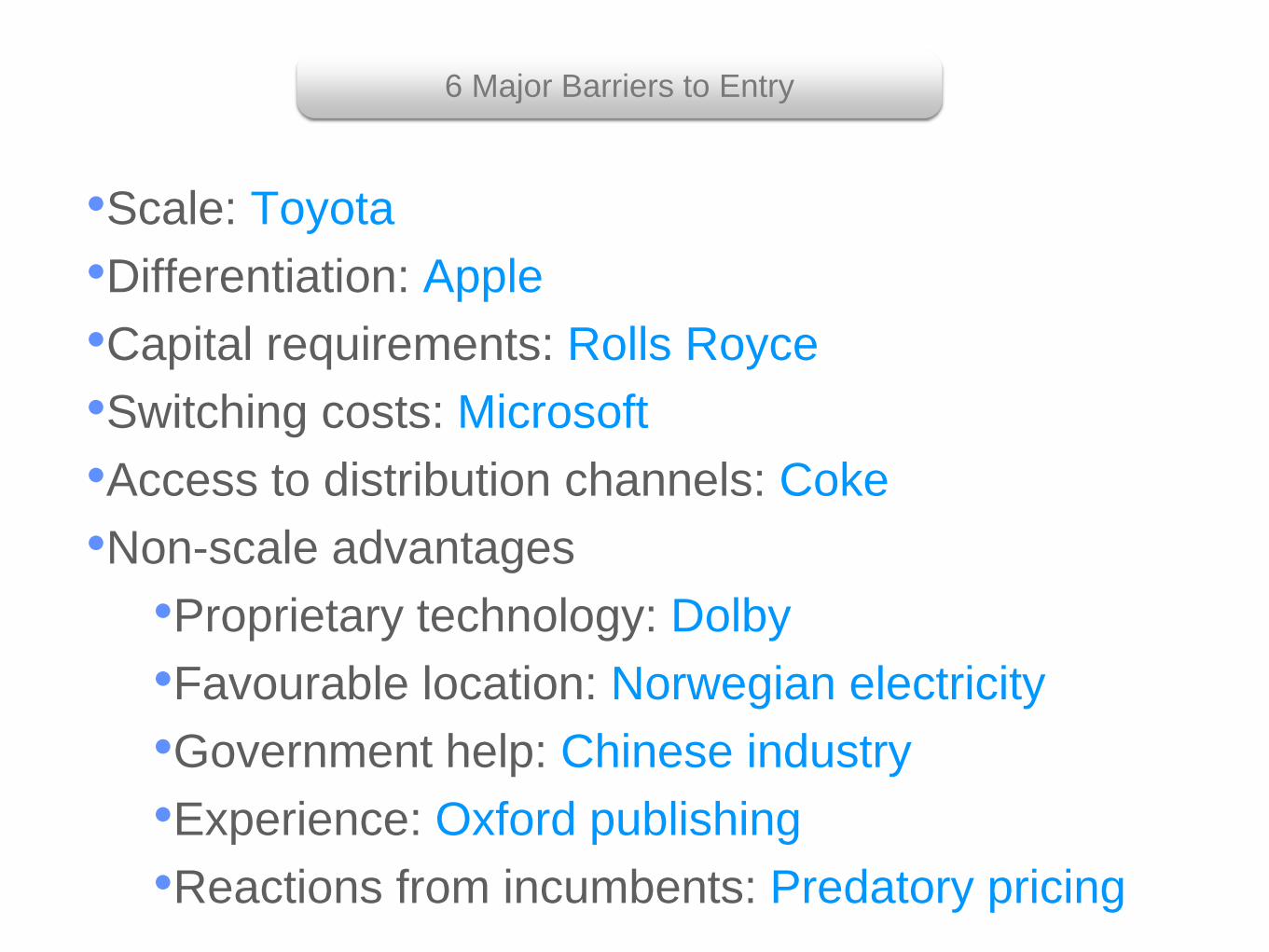

•Scale: Toyota

•Differentiation: Apple

•Capital requirements: Rolls Royce

•Switching costs: Microsoft

•Access to distribution channels: Coke

•Non-scale advantages

•Proprietary technology: Dolby

•Favourable location: Norwegian electricity

•Government help: Chinese industry

•Experience: Oxford publishing

•Reactions from incumbents: Predatory pricing

6 Major Barriers to Entry

•Other products/services which

perform the same function

•Place a ceiling on the price

Product/Service Substitutes

Movie Television, DVD, stage play

Telephone call Letter, fax, email

CD bought from retailer Download, Stream

Ferry journeyAeroplane, tunnel plus car, rail

tunnel

Product catalogue CD, download from web

Substitutes

•Slow industry growth: House Building

Intensity of Rivalry

•Numerous equally balanced competitors: Web Page Designers

•High fixed costs: Rolls Royce

•Lack of differentiation: Office Stationery

•Large increments in capacity: Oil Refining

•Diverse competitors: Recorded Music

•High strategic stakes: Military

•High exit barriers: Shipyards

•Actual market rivals

Competition: All Five Forces

•Potential entrants

•Buyers

•Suppliers

•Substitutes

How?

Appraise each force

Then

Compete using a generic strategy

Find a position in the industry where you can

best defend yourself

Goal of Competitive Strategy

•High volume low cost (HVLC)

•Differentiation

•Focus

The Generic Strategies

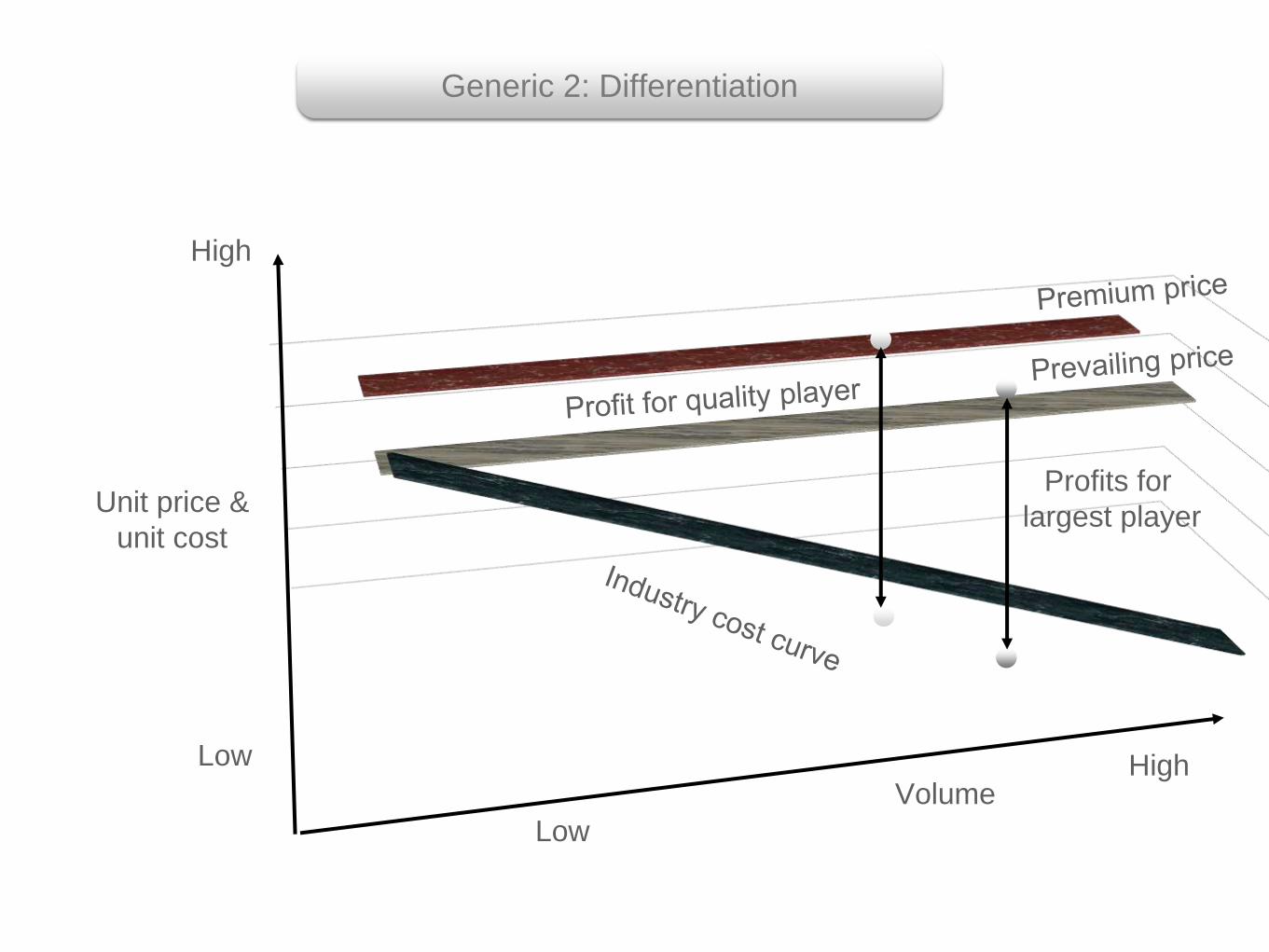

Loss for small player

High

LowVolume

Unit price &

unit cost

Low

High

Profits for

largest player

Generic 1: High Volume Low Cost (HVLC)

High

Low

Volume

Unit price &

unit cost

Low

High

Profits for

largest player

Generic 2: Differentiation

Lever Effects Difficulty

Price

Lower profits,

Disloyal buyers,

No skill

Retaliation

Easy

PromotionExpand overall

marketDifficult

Distribution Maintain margins Difficult

InnovationHigher and more

sustained profitsDifficult

ServicePrice and cost

advantageDifficult

QualityPrice and cost

advantageDifficult

Sources of Differentiation: The Marketing Levers

Or why low price is a terrible weapon

Differentiation

Marketing/Promotion

Innovation

Major Global Advertising Spend : A Paradox?

Samsung: World’s biggest advertising spend 2014Yet its Phone profits declined 78% in Q4

Apple: Lowest % advertising spendYet its profits soar

Microsoft spend 8.0% of sales

Apple spend 0.7% of sales

8.0%

0.7%

x 11 timesWhy?

The Reason

One is selling a product

The other is marketing a brand

Product Brand

Product

Price

Advertising

Product + Associated Services

Promotion

Design

Warranty

Quality

Customer service

Innovation

Distribution

Uniqueness

The World’s Top Brands 2014

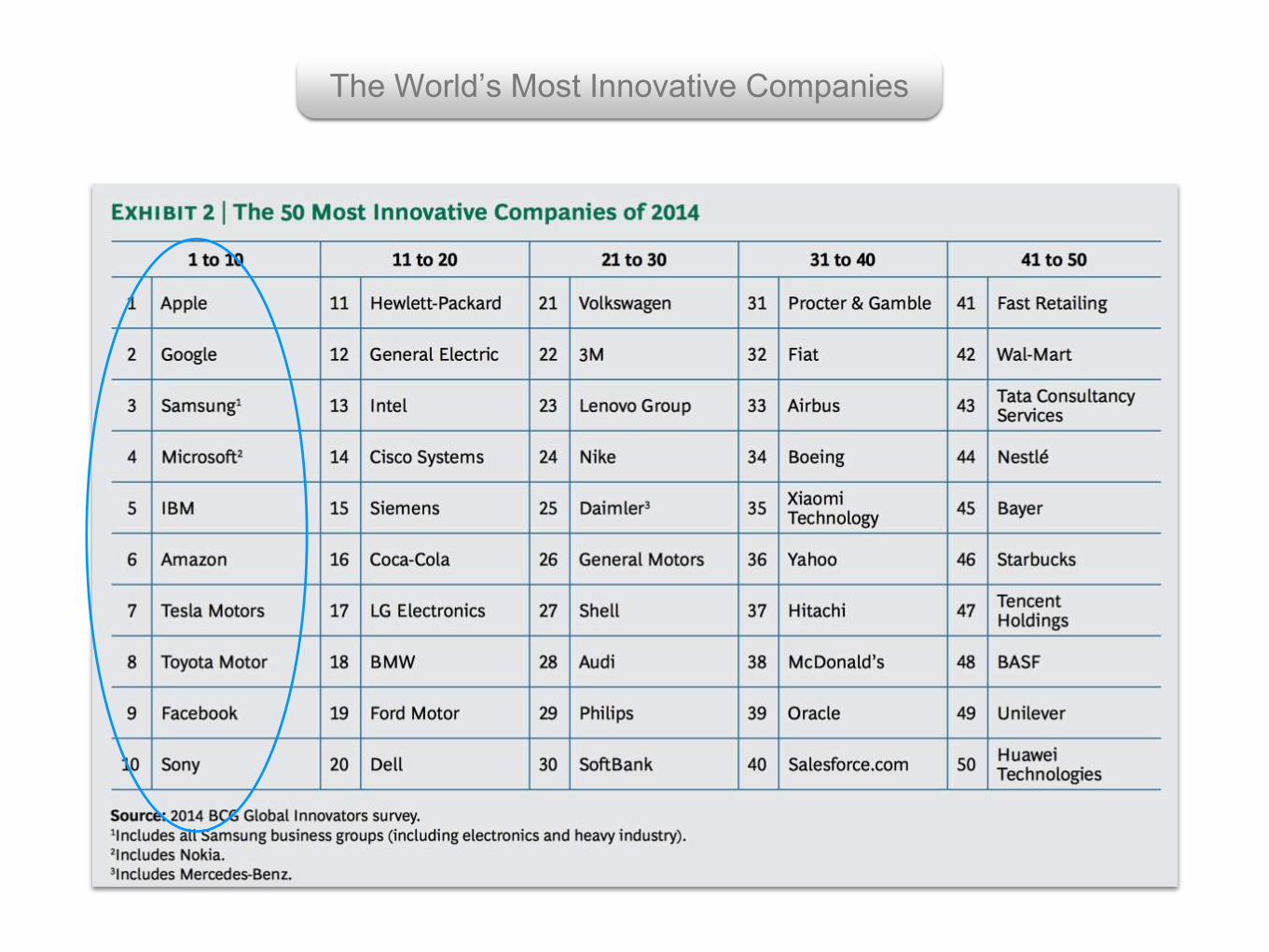

The World’s Most Innovative Companies

Cultures which Promote Innovation

Source: Forbes

0

20

40

60

80

Revenue GrowthEBITDA Grth

Mkt Cap Growth

Top 10 Innovators Top 10 Spenders

Top 10 innovators outperform their peers in 3 key

financial metrics (5 years CAGR)

Real Innovation Pays

Lever Effects Difficulty

Price

Lower profits,

Disloyal buyers,

No skill

Retaliation

Easy

PromotionExpand overall

marketDifficult

Distribution Maintain margins Difficult

InnovationHigher and more

sustained profitsDifficult

ServicePrice and cost

advantageDifficult

QualityPrice and cost

advantageDifficult

The Marketing Levers

Reminder

•Buyer power reduced – alternatives denied

Differentiation

•Price premiums + loyal buyers give

margins to deal with supplier power

•Brand loyalty protects

•Differentiated focus

•HVLC focus

Focus

You really must pick one

•Structures etc.

•Resources

•Styles,

Each generic requires different

Which Generic?

ROCE

RMS HighLow

High

LowHVLCDifferentiated Stuck in the middle

The U-Shaped Curve

•More important than ever

•Generic strategies vital – the basis of

much successful e-business

The big changes:

•Switching costs reduced

•Fantastic opportunities to resolutely

pursue a generic

Competitive Forces in the Internet Ear

Force Threats Our strategy

Power of Buyers

Power of Suppliers

Threat of New Entrants

Threat of substitutes

Degree of rivalry

Our generic strategy:

Practical Application

Creating and Presenting Strategic Plans

Competitive Analysis and Strategies (B.2.4.)

Firm Competitive Position

Characteristic Comment

Sales (£) The larger the better

Market share (%) The larger the better

RMS The larger the better

RPQ The larger the better

Price rel to comp (%) The larger the better

New prod/sales (%) *The larger the better

R&D/Sales (%) The larger the better

Degree of Competition The more benign the better

Determinants of Firm Competitive Position

* Assuming firm is already No. 1 in RPQ

Which is

best?

Firm Competitive Position: Discussion

• Political

• Economic

• Social

• Technological

• Environmental

• Other influences

• Legal

• Barons

• Insurgent

s

• Serfs

Product Sales ($)Mkt Sh.

(%)RMS RPQ RP NP/Sales

R&D/Sal

esCompetition

Comments

Current Competitive Position Template

Creating and Presenting Strategic Plans

Competitive Analysis and Strategies (B.2.4.)

Actual Competitors

Know the Gossip

•Predictions

Actual Competitors: Wide discussion

•History:

•Leader/Follower

•Growth

•Focus on Leaders - past behaviours

•Focus on Insurgents and Barons

•HVLC versus Diff. versus Focus

•Organic versus Acquisition

Existing

•New diverse entrants or threatsNew

Competitor

nameMain person Growth rate

Leader/Follo

wer

Strategy:

HVLC/Diff/F

ocus

Strategy:

Org/AcqOur strategy

1

2

3

4

5

6

Comments

Actual Competitor Analysis

The End