CORPORATE PRESENTATION OC OOCTOBER

25

Zircon & Titanium mining and processing Zircon & Titanium mining and processing CORPORATE PRESENTATION OC O 20 CORPORATE PRESENTATION OCTOBER 2011 1 July 2011

Transcript of CORPORATE PRESENTATION OC OOCTOBER

Zircon & Titaniummining and processingZircon & Titanium mining and processing

CORPORATE PRESENTATION OC O 20CORPORATE PRESENTATION OCTOBER 2011

1

July 2011

Mineral Deposits – corporate snapshot

Capitalisation 10 years in Senegal

Li ti ASX (MDL) / TSX (MDM) 2002 St t d l ti G d CôtListings ASX (MDL) / TSX (MDM)

6 mth price range A$7.35 – $3.85

Shares 83.5M

Market cap A$433M / US$440M

2002 Started evaluating Grande Côte

2004 Awarded Sabodala gold project

2007 ‐ 2009 Constructed Sabodala mine

Mar 2009 First gold poured at Sabodalap $ / $

Cash (30/9/2011) US$130M

Investments US$80 (40M Teranga Gold (TGZ) shares)

Debt Nil

g p

2011 ‐ 2013 Construction of Grande Côte

Shareholder Structure (July 2011)

Dec 2010 Sabodala gold assets “demerged” into Teranga Gold

Corporate Transactions

Other Institutions Canada Dec 2010 Corporation (TSX/ASX: TGZ)

Oct 2011 Commencement of JV with Eramet (TiZir) –combining Grande Côte and ilmenite upgrading plant

Australian Institutions

38%

Retail10%

Institutions10%

Canada1%

UK/Europe23%

USA18%

2

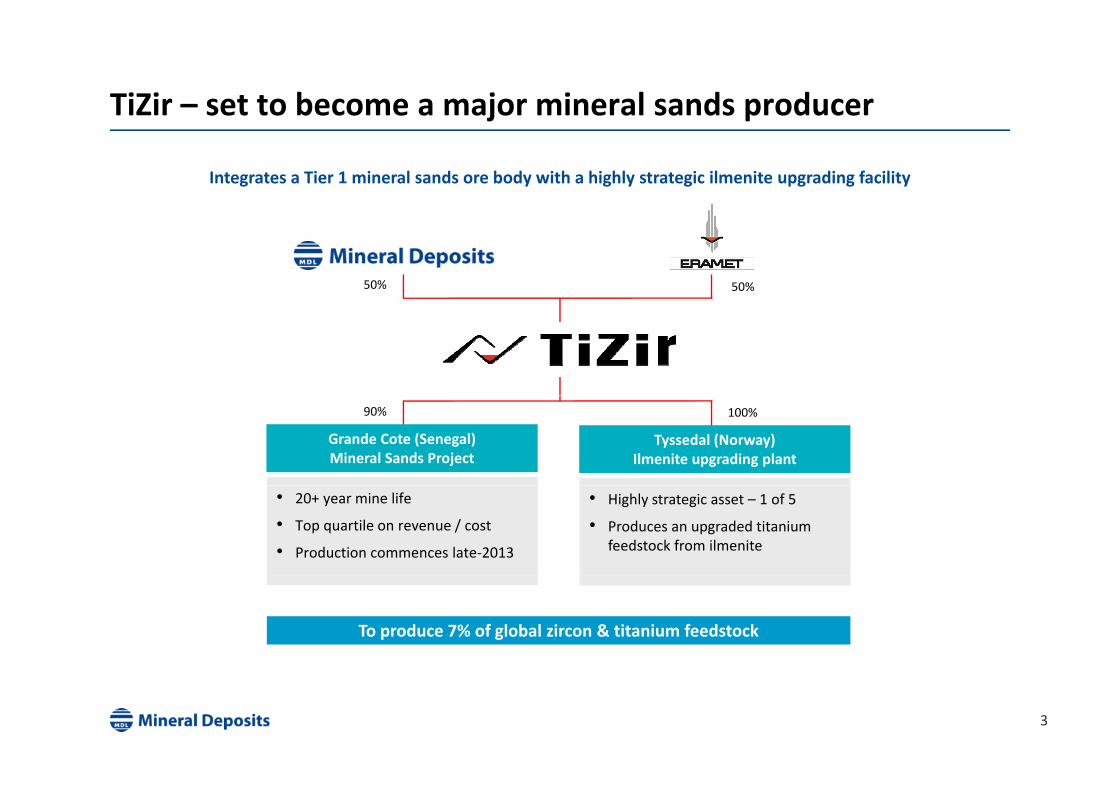

TiZir – set to become a major mineral sands producer

Integrates a Tier 1 mineral sands ore body with a highly strategic ilmenite upgrading facility

50%50%

Grande Cote (Senegal)Mineral Sands Project

Tyssedal (Norway)Ilmenite upgrading plant

100%90%

• Highly strategic asset – 1 of 5

• Produces an upgraded titanium feedstock from ilmenite

• 20+ year mine life

• Top quartile on revenue / cost

• Production commences late‐2013

To produce 7% of global zircon & titanium feedstock

3

Mineral Sands – two distinct product streams

Titanium FeedstockZircon

Market SizeVolume = 6.3m TiO2 units

Value = US$4.5bnVolume = 1.4 MtValue = US$3.5bn

MajorProducers

RIO Tinto 27%Iluka 13%Exxaro 9%

Iluka 31%RIO Tinto 17%Exxaro 15%

Kronos 6%China 9%

SupplyAustralia 21%

South Africa 19%Australia 41%

South Africa 29%pp yby Region China 12%

Canada 11%China 9%USA 7%

China 42% Europe 28%Demandby Region

Europe 24%Asia‐Pac ex China 17%

Americas 13%

Americas 26%China 21%

Asia‐Pac ex China 18%

4

Urbanisation is a key driver of product demand …

Titanium Feedstock consumptionZircon end‐use

Ceramics55%Refractories

14%

Foundrycasting

10%Other3%

Titanium sponge (1)

4%Other (2)

6%

Source: TZMI

Specialty Chemicals & Materials

18% Pigments90%

• Used in ceramics (mainly tiles) as an opacifier (because it is highly refractive) and for its hardness & whiteness

• Used in many applications for its high temperature

• Dominant use is for titanium dioxide (TiO2) pigment –the white pigment of choice – which is used in paints (56%), plastics (25%) and paper (9%)

90%

• Used in many applications for its high temperature resistance and chemical inertness

( ), p ( ) p p ( )

• “Lifestyle” products

• Consumption increases as wealth increases

• Developing nations (mainly China) are the growth engine

• 4% average growth in demand projected to 2020 (TZMI)

51. First stage in the titanium metal sector.2. Includes the manufacture of welding electrode fluxes and other

minor end‐uses – which mainly consume rutile and leucoxene

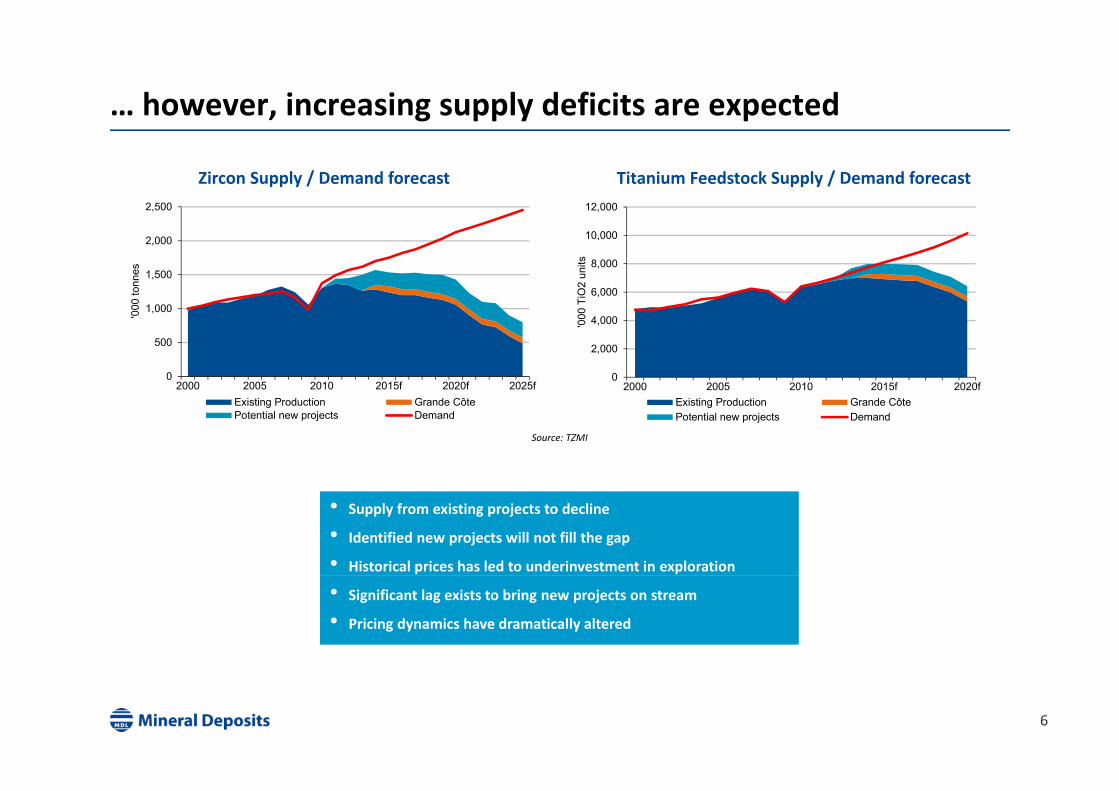

… however, increasing supply deficits are expected

Titanium Feedstock Supply / Demand forecastZircon Supply / Demand forecast12,0002,500

6,000

8,000

10,000

TiO

2 un

its

1 000

1,500

2,000

00 to

nnes

0

2,000

4,000

2000 2005 2010 2015f 2020f

'000

0

500

1,000

2000 2005 2010 2015f 2020f 2025f

'00

Source: TZMI

Existing Production Grande CôtePotential new projects Demand

Existing Production Grande CôtePotential new projects Demand

• Supply from existing projects to decline

• Identified new projects will not fill the gap

• Historical prices has led to underinvestment in exploration

• Significant lag exists to bring new projects on stream

• Pricing dynamics have dramatically altered

6

Grande Côte – a Tier 1 asset in the making

Location Senegal, West Africa

Grande Côt

Ownership 90% (Senegal govt. 10% free carried)

Concession 25 years extendable

Fiscal 5% royalty

e

Fiscal Arrangements

5% royalty10% government production share15 year tax free period

Mine Life 20+ years – potential for significantly y p g ylonger at lower cut‐off grades

Production(projected average p a )

85 ktpa Zircon575 ktpa Ilmenite

average p.a.) 16 ktpa Rutile & Leucoxene

Capex estimate US$516M (revised June 2011)

i $Opex estimate US$84M pa

Timing Construction underwayProduction commencement late‐2013

7

A very large ore body

Resource Estimate (Measured + Indicated)Covering ̴50% of Concession

Grande Côt

Cut‐off (%HM) Tonnes (Bt) HM (%)

0.50 4.14 1.1

0.75 2.90 1.2

1 00 1 72 1 5

e

1.00 1.72 1.5

1.25 1.03 1.7

From a depth 6m below the water table

Mining level Tonnes (mt) HM (%) Years

At water table 1 047 1 5 19

Reserve (Proved + Probable)Covering ̴40% of Concession

At water table 1,047 1.5 19

3m above 863 1.7 16

3‐6m above 751 1.8 14

6m above 684 1.9 13

20+ year mine life

8

A simple ore body

• No overburden

• Minor vegetation

Grande Côtg

• Free flowing sands – no hard lenses

• Minimal (<1.0%) slimes

• Shallow water table

e

• Deep aquifer

9

Conventional dredging and processing

• Dredge sucks sand from front of pond and pumps slurry to

Dredge & Floating Concentrator

Grande Côt• Dredge sucks sand from front of pond and pumps slurry to

floating concentrator

• Sand washed through spirals which using gravity separate heavy mineral concentrate (HMC) from lighter quartz

• Q t d (98%) d t b k f d

e

• Quartz sand (98%) pumped to back of pond

• HMC (2%) transferred to mineral separation plant (MSP)

• Magnetic, electrostatic and gravity processes separate

Mineral Separation Plant

HMC into various minerals – zircon, ilmenite, rutile & leucoxene

• No chemicals

10

Straight forward logisticsGrande Côt

+New 22km rail spur from MSP

Concession for use of existing line

e

Logistics self‐sufficiency

Lease over land at port+

=

11

Uncomplicated marketing

Average annual production Production description / target markets

Grande Côtp

Zircon 85 Kt

• Premium quality – low in key impurities

• Suitable for full spectrum of zircon consumers

• Premium price expected due to:

e

Zircon 85 Kt Premium price expected due to:

– high quality

– container shipments

400 Kt

Ilmenite

400 Kt54% TiO2

• Feedstock for Tyssedal plant

175 Kt59% TiO2

• Feedstock for chloride pigment manufacture

Rutile 6 Kt • Premium grade and fine grain size – ideal for welding sector

Leucoxene 10 Kt • Suitable for welding sector

12

Top quartile revenue / cost

Industry Revenue / Cost curve forecast for 2015(based on individual projects)

Grande Côt

• Valuable zircon stream

• Simple ore body3.50

4.00

Ratio

1st Quartile 2nd Quartile 3rd Quartile 4th Quartile

Why is Grande Côte top quartile?

e

• Large‐scale, low‐cost dredging

2.00

2.50

3.00

Industry Wtd Average 2015fCôt

e

0.50

1.00

1.50Industry Wtd Average 2015f

Gra

nde

C

0.000% 25% 50% 75% 100%

Cumulative TiO2 units produced

Source: TZMI

Note: R/C curve for 2015 based on TZMI’s forecast:1. production volumes for individual operations in 20152. long term real view of product prices

13

2. long term real view of product prices3. operating costs of the individual operations using real 2010 cost rates

Production to commence late‐2013Grande Côte

14

Senegal, West Africa

• Independent from France since 1960

Senegal

Grande CôtIndependent from France since 1960

• French is official language

• Successful, stable democracy

• Location of many foreign embassies and

e

international banks for West African region

• Small population (13M)

• World standard mining laws

• 10 years on the ground

• S b d l fi t j j t f 40

MDL in Senegal

• Sabodala – first major resource project for 40 years

• Strong engagement with local communities

• Excellent government relations

Grande Côte Mineral Sands Project

15

Tyssedal titanium & iron plantTyssedal

16

The drive for high TiO2 feedstocks

Tyssedal Plant Process Why upgrade the TiO2 content of feedstocks?

Tyssedal

• Pigment producers need reduced wasteIlmenite1

44% TiO2(~345 ktpa)

Input

• Pigment producers need reduced waste

• Smelting separates out iron (Fe)

– a valuable co‐product for us

– waste for pigment producers

FurnaceSmelting

p g p

Titanium slag80% TiO2

(~200 ktpa)Outputs

High PurityPig Iron

(~110 ktpa)

PigmentProducers 2

Customers Foundries 3

Notes:1. Mostly sourced from Tellnes mine in Norway2. Mainly European‐based using sulphate process

d f f l d d b

17

3. Used for a variety of purposes, including wind turbine parts

Tyssedal, a highly strategic asset

• Titanium slag accounts for 39% of all titanium feedstock

• Supply is highly concentrated – 3 owners across 5 plants

Split of feedstock supply(2011f = 6.6 m TiO2 units)

Tyssedalpp y g y p

Owner Location ktpa Slag Type

Rio Tinto QIT – Sorel, Canada 1,300 Sulph & Chlor

Rio / BHP RBM – South Africa 1,000 Chloride

Ilmenite41%

Syn Rutile8%

Rutile12%

Exxaro KZN – South Africa 140 Chloride

Exxaro Namakwa – South Africa 140 Chloride

TiZir ETI – Tyssedal, Norway 200 Sulphate

2 780

TitaniumSlag39%

Feedstock demand by pigment process

2,780

• Security of additional Grande Côte feed provides:

Tyssedal growth opportunities

4 0TiO2y p

– Opportunity to build 2nd furnace and double capacity to 400+ ktpa of titanium slag

– Flexibility to produce feedstock for both sulphate and chloride pigment process routes 2.0

3.0

4.0TiO2units(m)

Rutile

Syn Rutile

chloride pigment process routes

• Feasibility study for 2nd furnace underway

0.0

1.0

ChlorideP

SulphateP

TitaniumSlag

Ilmenite

18Sources: TZMI

Process Process

Strategic positioning relative to pigment customersTyssedal

●606

Tyssedal

●1628●17

●606●997

●27●1154

●63●142

●160●170

●55

●151●61

60●170Grande Côte

55

●260●22

●Chloride Pigment capacity (kt)●Sulphate Pigment capacity (kt)TiZir Locations

19Source: TZMI

Indicative financials – based on illustrative pricing

Tyssedal (100%)Grande Côte (100%)

Zircon revenue Zircon: 85Kt x US$2,000/t Slag revenue US$1,000/t

Opex & other

Titaniumfeedstockrevenue

Ilmenite: 575Kt x US$200/t

Costs

Pig ironrevenue €480/t

EBITDA

costs

EBITDA

Costs

MDL participates in earnings from October 2011Production commencement late‐2013

0 20 40 60 80 100 120 140 160 180 200

US$M

0 20 40 60 80 100 120 140 160 180

US$M

p p g

20

Additi l i f tiAdditional information

21

Our titanium feedstocks customers – TiO2 pigment producers Tita

Sulphate Process Chloride Process

Pigment producer market share(2010 capacity = 6.0 mt)

anium feedst

Two distinct processes produce TiO2 pigment

Sulphate Process Chloride Process

48% of capacity 52% of capacity

Sulphuric acid used to dissolve titanium

Chlorine gas used to liberate titanium

tocksDuPont19%

Cristal13%

China22%

Other14%

Ilmenite (low‐TiO2) main feedstock

High‐TiO2 feedstocks (titanium slag, rutile) used

Waste / TiO2 ≈ 4:1 Waste / TiO2 ≈ 1:1

Dominant in China Dominant in the AmericasHuntsman

10%Kronos9%

Tronox6%

Sachtleben4%

ISK3%

22%

37% of capacity in Europenear‐zero in Americas

63% of capacity in Europenear‐zero in China

TiO2 pigment capacity by region(2010 capacity = 6.0 mt)

9%6%

EMEA

Americas

0.0 0.5 1.0 1.5 2.0

Asia-Pacificex China

China

Chloride ProcessSulfate Process

22Sources: TZMI

mt

Grande Côte Financial Estimates

Capital Cost (US$516M)

$

Operating Costs (US$84M pa)

$US$M

Dredge & Services 53.6

Wet Concentrator Plant 95.9

Mineral Separation Plant 63.0

US$M

Power and Fuel 34.2

Employee Costs 9.4

Maintenance 14.4Mineral Separation Plant 63.0

Power Station 49.4

Rail and Rolling Stock 43.6

Port Facilities 21.7

Maintenance 14.4

Transportation / Shipping (FOB) 13.6

Other 12.3

Temporary Construction Facilities 22.4

Indirects – EPCM/ Commissioning /Project Fee 56.7

Owner Costs 61.1

Estimation/Design Allowance/Contingency 49.0

Total 516.4

Total 83.9

23

Statements

Forward Looking Statements• Certain information contained in this presentation including any information on MDL’s plans or future financial or operating performance and other statementsCertain information contained in this presentation, including any information on MDL s plans or future financial or operating performance and other statements

that express management’s expectations or estimates of future performance, constitute forward‐looking statements. Such statements are based on a number of estimates and assumptions that, while considered reasonable by management at the time, are subject to significant business, economic and competitive uncertainties. MDL cautions that such statements involve known and unknown risks, uncertainties and other factors that may cause the actual financial results, performance or achievements of MDL to be materially different from the company’s estimated future results, performance or achievements expressed or implied by those forward‐looking statements. These factors include the inherent risks involved in exploration and development of mineral properties, changes in

d h h ld d f l d h k h l d h f heconomic conditions, changes in the worldwide price of zircon, ilmenite and other key inputs, changes in mine plans and other factors, such as project execution delays, many of which are beyond the control of MDL.

• Nothing in this presentation should be construed as either an offer to sell or a solicitation to buy or sell MDL securities.

24

mineraldeposits.com.au

25