COPYRIGHT Wachovia CONFIDENTIAL Surviving the Credit Crunch October 22 nd 2008.

12

COPYRIGHT Wachovia CONFIDENTIAL Surviving the Credit Crunch October 22 nd 2008

-

Upload

martha-goodman -

Category

Documents

-

view

220 -

download

0

Transcript of COPYRIGHT Wachovia CONFIDENTIAL Surviving the Credit Crunch October 22 nd 2008.

COPYRIGHT Wachovia CONFIDENTIAL

Surviving the Credit CrunchOctober 22nd 2008

How Did We Get Here

1. Social Engineering by Government

2. Wall Street Creativity in Creating Money Supply

3. Mortgage Lending Standards Reduced

4. Consumer Frenzy for Real Estate

5. Accounting Rules Change for Banks (M to M)

Where Are We Today?$700 Billion Rescue Plan Placed in Force

a. $250 Billion in Capital being injected into banks

b. Mark to Market adjusted to change valuing assets in disorderly market away from lowest price paid to discounted cash value, if cash flow exists

c. Bad mortgage pools bought by Government

d. $250,000 guarantee amount on CD’s and interest bearing accounts

e. Unlimited guarantee on NI checking accounts

f. Temporary insurance for Money Market funds

g. Unlimited guarantee of interbank loans

Where are we today?Availability of Capital and Debt Less than Certain

Underwriting and standards for Debt are being tightened

Cost of Capital and Debt is going upWhat is “cost of capital”Why is it going up?

Many industries are challengedResidentialDevelopersRetail and Wholesale to HomeownersDiscretionary Goods and Services

10 year history of Libor

0%

2%

4%

6%

8%

10%

12%

1988 1993 1998 2003 2008

1-Month Libor

Average = 4.76%

Current = 4.36%

Where are we headed?

Certainly, a period of global economic slowdown

A time when many businesses will be severely tested

Poor plans or no plans will be deadly

Need for closer communication with your banker

Companies that make careful decisions can emerge stronger than before

Sources of FinancingPros and Cons

Commercial Finance (Factoring)

SBA7a and 504

Conventional Bank lendingLines and term loans

Private Equity

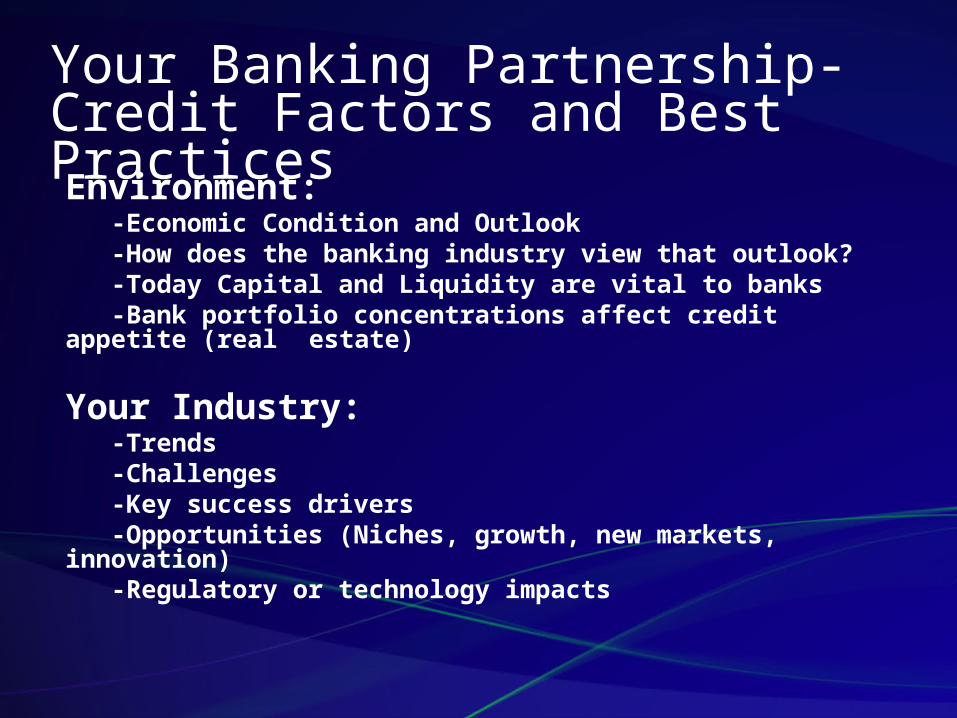

Your Banking Partnership-Credit Factors and Best PracticesEnvironment:

-Economic Condition and Outlook-How does the banking industry view that

outlook?-Today Capital and Liquidity are vital to banks-Bank portfolio concentrations affect credit

appetite (real estate)

Your Industry:-Trends -Challenges-Key success drivers-Opportunities (Niches, growth, new markets,

innovation)-Regulatory or technology impacts

Your Banking Partnership-Credit Factors and Best PracticesYour Company:

-Positioning in competitive landscape-Operating model (Markets, Customers, Suppliers, Fixed

Costs, Inventory, Key Drivers)-Financial condition, profitability-Ownership structure-Succession-Management team

Capital Structure:-Balance Sheet components-Optimize returns-Support existing operating model effectively-Support your strategic and tactical goals-What role can bank play in optimizing structure?

Your Banking Partnership-Credit Factors and Best PracticesManagement Team (Most Important Factor):

-Experience

-Functional strength of org chart in key areas:

finance, marketing, production, technology, human resources

-Clear identification of opportunities and challenges

-Clear, open, timely communication of same

-Strategy and tactics

-Written Business Plan

Your Banking Partnership-Credit Factors and Best PracticesInformation-The Basics:

-Timely, quality financial reporting:-CPA prepared statements/tax returns-A/R Aging-Projections

-Key Ratios (Cash flow/debt service, liquidity, leverage, return percentages)

-Collateral/Guarantees (LTV, Lendable Value, advance rates, guarantor strength, credit enhancement)

Information-Best Practices-Early notice of material change-Shared business plan-Advisory Team Meetings (Banker, CPA, Legal, Insurance)

ConclusionAction plan

-Meet with your banker

-Assemble a quality advisory team

-Communicate often and fully

-Expect value, ideas, and advice

More…

Our panel will stay for a few minutes afterwards to answer more questions. In addition we have a number of Wachovia Bankers here today that are also available.