Convergent Charging and Digital Transformationsolutions.amdocs.com/rs/647-OJR-802/images/IDC...

16

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends An IDC White Paper Sponsored by Amdocs January 2017 Author: Andy Hicks

Transcript of Convergent Charging and Digital Transformationsolutions.amdocs.com/rs/647-OJR-802/images/IDC...

Convergent Charging and Digital Transformation:

A Fundamental Platform Serving New Ends

An IDC White PaperSponsored by Amdocs

January 2017

Author: Andy Hicks

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 2

How Do Service Providers Need Their

Classic Systems to Support Their

Transformation?

Digital transformation: Most people in the telecommunications industry

believe it is essential. The tricky part is that everyone has a different idea of

what it means. Some put the emphasis on upgrading their networks, some on

content and entertainment, some on decommissioning legacy and unifying

platforms, some on automation, and some on customer-facing functions. And

all of these efforts can be transformative, at least potentially.

Digital transformation (DX) spans the whole organization; it can involve

elements specific to the telecommunications business, as well as back-office

functions common to many industries. At IDC, we have an extensive

framework for digital transformation, but underlying all of it is a fundamental

principle: The technology must serve the business. IT transformation — no

matter how expensive — is not digital transformation unless it makes some

aspect of the business better.

The flip side is the real benefit: Since digital transformation is about how

carriers use tools both old and new, they do not need to focus all their energy

on brand-new architectures to realize DX benefits. Upgrading foundational

systems — or even making incremental changes — is every bit as valid an

approach to DX progress.

The only challenge with this approach is a practical one: If there are many

paths to the same goal, how can we tell which ones might be better? What

are the best practices? What are carriers around the world focusing on? How

are DX imperatives affecting core technology? To find out, we surveyed 80

large communications service providers in Europe, North America,

Central/Latin America, and Asia Pacific on their DX plans as they related to the

fundamental convergent charging function.

IT transformation

— no matter how

expensive — is not

digital

transformation

unless it makes

some aspect of the

business better.

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 3

One Key to Revolutionizing Revenue:

Personalization

If you measure DX’s benefit by the effect it has on the top line, then one result

of the survey pops out immediately: Over half of the carriers we surveyed

believe that significantly improving personalization and customization could

boost revenue substantially over the next three years:

FIGURE 1

Carriers Expect Personalization to Substantially Boost Revenue

Q. How much would you expect your revenues to grow cumulatively over the next three years if you could employ significantly more personalized information and more customized offers?

Note: N = 80Source: IDC survey performed for Amdocs, 2016

Keen parsers of survey results will notice something about this graph: The

scale does not go high enough. When we designed the question, we did

anticipate that carriers would expect greater personalization and

customization to boost revenue, but we underestimated how strongly they

believed in it. The next time we ask this question, we will increase the scale. In

any case, it is clear that personalization of offers and services is one of carriers'

central transformative hopes.

Personalization and customization usually mean finer segmentation — down,

eventually, to the promised “segment of one.” Usually, in turn, this finer

4

18

23

53

0 5 10 15 20 25 30 35 40 45 50 55

0-5%

5-10%

10-15%

More than 15%

(%)

Over half of the

carriers believe that

personalization and

customization can

boost revenue

substantially.

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 4

segmentation requires a more robust technical environment. Based on the

carrier’s individual needs, this could include a faster database, a unified

product catalogue, or stronger analytics. It will certainly require a more robust

management capability and stronger assurance, especially as service-level

agreements (SLAs) build in more business-oriented key performance

indicators (KPIs) and quality-of-service levels.

Personalization and customization also require drastically reduced time to

market in order to serve these increased, more finely sliced segments. Greater

segmentation requires the carrier to produce and manage more offers and

products in the same period of time. Each individual offering, therefore, must

come to market more rapidly to support this increased volume, and all parts

of the chain must enable this speed. Increasingly, this will require real-time

functionality as adjustments are made on the fly. Convergent charging

systems can also provide a timely, rich set of usage data for segmentation and

analytics. As the real-time monetization engine, convergent charging will

become an essential part of this environment.

Carriers Expect More than Personalization

from Convergent Charging

Digital transformation has many aspects, and carriers expect convergent

charging to support many of them. When we asked carriers to choose the

capabilities of convergent charging that supported a digital strategy, not a

single choice ranked below 50%.

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 5

FIGURE 2

No Shortage of DX Requirements for Charging Systems

Q. What key capabilities of a charging system are required to support a digital strategy?

Note: N = 80Source: IDC survey performed for Amdocs, 2016

This broad set of high scores reflects the diversity of approaches to digital

transformation. Starting with the lowest score — which still rates a solid 59%

— real-time re-rating suggests that the mix of agility and personalization that

we saw in previous questions may be enough to trump the need for this

capability. These include the ability to create targeted offers and products for

every finely differentiated segment the marketing department may choose to

address. In other words, if you can target everyone separately, applying

immediate discounts may be a lower priority.

Moving up the scale, the more highly ranked choices attest to the priority that

carriers place on flexibility and speed in DX. Predefined widgets, adjustable

plan parameters, and flexible, open application programming interfaces (APIs)

all enable carriers to develop offers quickly, using an agile, fast-fail approach

to constructing new offers. At its core, agility depends on dramatically

reducing the time and cost — and thus the opportunity cost — of every

service, campaign, and tariff that the carrier produces.

59

68

73

81

83

84

85

0 10 20 30 40 50 60 70 80 90

Re-rating of events in real time

A set of predefined widgets for billing- andcharging-related functions

A flexible plan and offer definition withadjustable parameters

An open and rich API

Real-time plan updates

An easily integrated API

Support for the selling of virtual andphysical goods

(%)

The broad set of high

scores reflects the

diversity of

approaches to digital

transformation.

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 6

The top-ranked choice provides another perspective. Support for the selling of

virtual and physical goods indicates that carriers would like to become more of

a retailer, not only for their traditional services and devices, but also acting as

the portal for partners. The importance placed on easy-to-use APIs could point

to convergent charging as the center of a largely self-service platform

capability, where the carrier acts as an economic enabler. This model is more

prevalent in some largely self-contained developing markets such as China;

nevertheless, even in more mature markets, selling virtual and physical goods

still has room to run.

Carriers Are Becoming More Open to

Alternate Delivery Models

Traditionally, billing and charging have lagged behind the network and other

parts of telecom infrastructure in outsourcing, but it looks like that may be

changing. We asked carriers how they would acquire their billing and charging,

and see a shift on the horizon:

FIGURE 3

Increased Flexibility in BSS Delivery Models

Q. Three years from now, which of the following delivery models will you probably use to supply your billing and charging capabilities?

Note: N = 80Source: IDC survey performed for Amdocs, 2016

40

55

75

89

0 10 20 30 40 50 60 70 80 90

Operated on our premises on dedicatedhardware

Provided as a cloud service

Provided in a managed-servicesrelationship

Operated in a private cloud that weadminister

(%)

Moving to private

cloud allows carriers

to realize benefits of

cloudification

without surrendering

the control that

comes from

operating their own

environment.

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 7

There are two stories here. The first is the move to private cloud from

dedicated hardware, which allows carriers to realize the benefits of

cloudification without surrendering the control that comes from operating

their own environment. The second, more recent story is that the majority of

carriers are increasingly embracing multitenancy. In our conversations on

business support systems (BSS) over the years, we have consistently heard

that even carriers that outsource other parts of their infrastructure want to

retain internal control of their billing and charging. At IDC, we generally hear

two main reasons for this: First, many carriers want to retain control because

they see billing and charging as a source of competitive differentiation.

Second, an equal number have BSS environments so confusing that they do

not want to outsource them until they understand how they work and what

systems they tie into.

As the chart below shows, both of those objections seem to be diminishing as

carriers come to believe that engaging a partner can solve some of these

problems, or at least that the cost and agility benefits outweigh whatever

reservations they may have.

FIGURE 4

Strong Benefits for New Delivery Models

Q. How much do you expect to benefit from cloud-based or managed deployment of charging in each of the following areas?

Note: n = 71Source: IDC survey performed for Amdocs, 2016

38

56

62

66

83

45

27

28

3

9

17

17

10

31

9

0 10 20 30 40 50 60 70 80 90 100

Modernization and adherence tocorporate policy

CAPEX reduction through the move to avirtualized environment

Increased flexible scalability

Greater agility leading to lower time-to-market for new offers

OPEX reduction by simplifying operations

(%)

High and Maximum Benefit Moderate Benefit No or Low Benefit

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 8

As usual, the top benefit of managed or as-a-service delivery is OPEX

reduction, but CAPEX reduction also scores well in this question. In between

are the DX benefits: agility, time to market, and scalability. Moving away from

an in-house model can be a major disruption, which may be why managed

delivery outranks as-a-service delivery in the previous graph: Carriers need

help with implementing and administering the change. Managed service

delivery can bring with it more business transformation assistance than pure

cloud delivery.

Consumer and Enterprise Priorities for

Convergent Charging

We asked carriers who had or were planning to implement convergent

charging to tell us what capabilities they expected to enjoy. It turned out that

they expected a lot.

FIGURE 5

Much Expected from Converged Charging in the Consumer Market

Q. For what new offers or capabilities are you planning to use your converged charging?

Note: N = 80Source: IDC survey performed for Amdocs, 2016

39

53

75

78

79

80

0 10 20 30 40 50 60 70 80 90

To launch quality-of-service-basedofferings

To launch sub-branded offerings fortargeted customer segments

To provide billing and charging capabilitiesto partners

To create better bundled offers

To create single-bill relationships withcustomers

To personalize offers to a greater extent

(%)

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 9

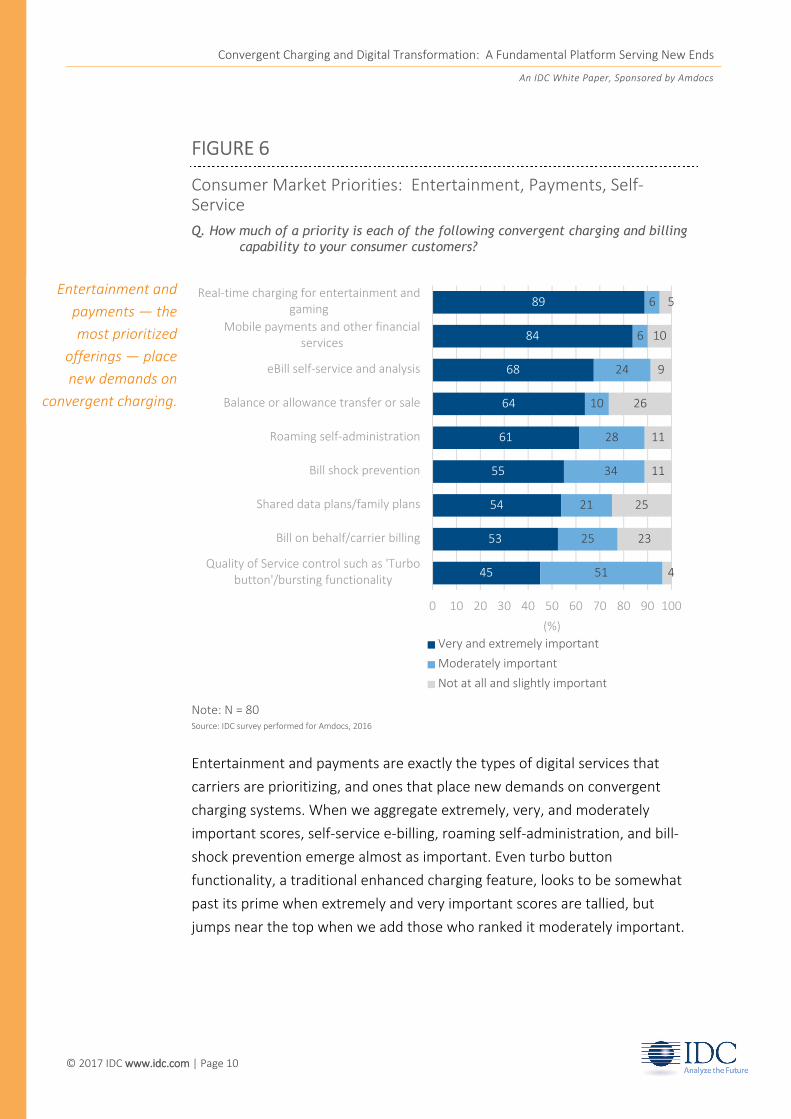

Aside from personalization, three other goals have scores of 75% or more.

These are very strong scores for features in the consumer and business

markets: Single-bill relationships are typically demanded by enterprises, which

require transparency and ease of administration for their communications

services, but also have applications for family plans and multiplay bundles.

Bundling and partner billing have broad applications for both markets,

especially with the rise of hyperscale-style platforms that enable a whole

ecosystem of partners to collaborate to provide value to a given customer

base.

Given these high-level results, we drilled down further into consumer and

enterprise market preferences.

Consumer Market Preferences for

Convergent Charging

That consumer offerings are shifting can be seen from the top two priorities

among telcos that serve that market: Entertainment and mobile payments are

essential, high growth areas for telcos. Not coincidentally, neither priority is a

traditional telecom function.

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 10

FIGURE 6

Consumer Market Priorities: Entertainment, Payments, Self-Service

Q. How much of a priority is each of the following convergent charging and billing capability to your consumer customers?

Note: N = 80Source: IDC survey performed for Amdocs, 2016

Entertainment and payments are exactly the types of digital services that

carriers are prioritizing, and ones that place new demands on convergent

charging systems. When we aggregate extremely, very, and moderately

important scores, self-service e-billing, roaming self-administration, and bill-

shock prevention emerge almost as important. Even turbo button

functionality, a traditional enhanced charging feature, looks to be somewhat

past its prime when extremely and very important scores are tallied, but

jumps near the top when we add those who ranked it moderately important.

45

53

54

55

61

64

68

84

89

51

25

21

34

28

10

24

6

6

4

23

25

11

11

26

9

10

5

0 10 20 30 40 50 60 70 80 90 100

Quality of Service control such as 'Turbobutton'/bursting functionality

Bill on behalf/carrier billing

Shared data plans/family plans

Bill shock prevention

Roaming self-administration

Balance or allowance transfer or sale

eBill self-service and analysis

Mobile payments and other financialservices

Real-time charging for entertainment andgaming

(%)

Very and extremely important

Moderately important

Not at all and slightly important

Entertainment and

payments — the

most prioritized

offerings — place

new demands on

convergent charging.

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 11

Enterprise Market Preferences for

Convergent Charging

Though fragmented, the enterprise market presents more potential for

expansion into a market of converged ICT services than the consumer market,

where many of the high-value services have been captured by over-the-top

providers. We asked carriers what offerings were priorities in their enterprise

market strategy, and then what capabilities needed to improve in order to

best serve them.

FIGURE 7

The Enterprise Market Also Expects Much

Q. How much of a priority is each of the following offerings to your enterprise customers?

Note: N = 80Source: IDC survey performed for Amdocs, 2016

36

41

50

59

65

66

68

74

40

39

21

16

26

10

19

10

24

20

29

25

9

24

14

16

0 10 20 30 40 50 60 70 80 90 100

Multiuser data plans

Multi-provider bundling where partner servicesare being sold to customers along with your

own services

Bill on behalf/carrier billing

Integration with enterprise mobilitymanagement platforms

White-labelled or pass-through services fromthird parties, for example Microsoft Office 365

or SAP

On-demand videoconferencing, collaboration,etc.

Media and content offerings

Bring your own device support where theenterprise would split usage and payments

with its employees

(%)

Very and extremely important

Moderately important

Not at all and slightly important

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 12

The top scorer — split billing that would support personal and enterprise

usage on a single device — addresses a traditional enterprise mobility

management market that is receptive to carrier partners, as does the choice

for integration with enterprise mobility management platforms. The other top

offerings lie more outside the traditional telco realm: As with the consumer

market, media and content offerings are highly desired, followed immediately

by enterprise collaboration. The options for pass-through services and carrier

billing point to the need for the enterprise services telco to manage a much

more complex partner and customer ecosystem than it has to date, with

enablement of multi-provider service bundling, as well as revenue recognition,

for each partner in the ecosystem.

These and related requirements suggest that carriers will need to substantially

upgrade their charging environments for the enterprise market. In fact, we

see that the need for enterprise-related charging improvements is substantial:

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 13

FIGURE 8

Enterprise Systems: Much-Needed Improvement

Q. How much does each of the following systems need to improve in order to serve enterprise markets better?

Note: N = 80Source: IDC survey performed for Amdocs, 2016

This graph shows a flat distribution of high priority responses — in other

words, every improvement is a priority. From self-service, real-time, and

single-bill capabilities, to capabilities that are essential to enabling ecosystem

models such as integration with application provisioning and microservice

exposure, it is clear that billing and charging environments need to

substantially change in order to support the enterprise market. This

environment of strong need argues for a large-scale transformation of the BSS

environment: If not rip-and-replace, then a concerted technical

transformation must be a priority, so that the technology can serve the goals

of digital transformation.

51

59

60

65

69

73

74

74

76

76

35

28

21

23

20

14

10

19

9

13

14

14

19

13

11

14

16

8

15

11

0 10 20 30 40 50 60 70 80 90 100

Support for flexible and complex accounthierarchies

Support variable/peak pricing

Enabling per-user control of quality of service

The ability to handle billing settlements forecosystem partners

Offering split billing to differentiate personal andbusiness payments

Real-time visibility into charges and usage

Exposing capabilities and microservices tocustomers and third parties via APIs or SDKs

Single bill/unified visibility for all services

eBill self-service and analysis

Integrating with enterprise-specific applicationprovisioning

(%)

Quite a lot and significantly

Fairly

Not at all and very little

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 14

Conclusion: Convergent Charging as

Support for Digital Transformation

Our group of 80 carriers has spoken: personalization requires speed, and

speed requires real-time capabilities. A robust charging environment with the

right capabilities can not only save on OPEX and CAPEX, but can enable

significant increases in revenue as well. Convergent charging can serve the

consumer market by adding capabilities to accommodate new services, but

likely needs a dramatic refit to support services for the enterprise market. The

need for change is substantial.

That need cannot be met by technology alone. As we noted at the beginning

of this paper, digital transformation requires not only technology, but also that

the technology be made to serve the business. In order to do that, carriers will

need help with the business as well: They will need help on process reform,

retraining or reducing staff, decomposing KPIs to make business change more

meaningful to all levels of the organization, assistance in managing a vastly

more complicated partner ecosystem, and more besides. Technology

selections are no longer only that, but also partner selections in an effort to

improve the whole business.

About Amdocs

Amdocs provides customer experience software solutions and services to

communications, entertainment, and media service providers. For more than

30 years, Amdocs has delivered its solutions, which include business support

systems, operations support systems, network control and optimization,

coupled with professional and managed services aimed at streamlining

complex operating environments, reducing costs, and expediting time to

market for new products and services.

Amdocs considers its experience in successfully delivering complex software

projects in the communications environment as its key capability. In

comparison to general IT vendors, Amdocs emphasizes its service-provider-

oriented mindset — the company has been focused exclusively on serving the

service provider industry throughout its existence, supporting that industry's

significant transformational processes.

The need for change

is substantial and

cannot be met by

technology alone;

digital transformation

requires technology

be made to serve the

business.

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC www.idc.com | Page 15

In its approach to charging, Amdocs leverages its knowledge of the service

provider business environment, processes, and operational constraints, as

well as telecommunications industry regulatory issues. Amdocs views these

core capabilities as necessary to ensure a successful transition to a digital,

software-led telecom business, while at the same time maintaining existing

SLAs and customer satisfaction levels.

The Amdocs Convergent Charging and Billing solution:

» Supports digital transformation with a single, convergent charging

system for all lines of business, customer segments and payment types

» Utilizes a single real-time, 3GPP Rel-13 compliant OCS for online and

offline charging and integrated PCC solution with a single set of

integrated products

» Reduces total cost of ownership using NoSQL technology in event

processing while maintaining high benchmarked performance levels

» Is deployed in fully virtualized environments and private cloud,

enabling dynamic allocation of OCS resources and 24x7 charging

availability

» Increases revenues through innovative business and monetization

models with rapid time to market of new customer offerings.

» Network agnostic, supporting 3G, 4G and 5G networks as well as new

network services such as VoLTE and ViLTE

» Delivers real-time charging performance and scalability in a single

carrier-grade solution

Amdocs and its 25,000 employees serve customers in over 90 countries. Listed

on the NASDAQ Global Select Market, Amdocs had revenue of $3.7 billion in

fiscal 2016.

Convergent Charging and Digital Transformation: A Fundamental Platform Serving New Ends

An IDC White Paper, Sponsored by Amdocs

© 2017 IDC. www.idc.com | Page 16

About IDC

International Data Corporation (IDC) is the premier global provider of market

intelligence, advisory services, and events for the information technology,

telecommunications, and consumer technology markets. IDC helps IT

professionals, business executives, and the investment community make fact-

based decisions on technology purchases and business strategy. More than

1,100 IDC analysts provide global, regional, and local expertise on technology

and industry opportunities and trends in over 110 countries worldwide. For 50

years, IDC has provided strategic insights to help our clients achieve their key

business objectives. IDC is a subsidiary of IDG, the world's leading technology

media, research, and events company.

IDC CEMA

Male namesti 13

110 00 Praha 1

Czech Republic

+420 221 423 140

Twitter: @IDC

https://idc-community.com/

www.idc.com

Copyright Notice: External Publication of IDC Information and Data — Any IDC information that is to be used in advertising, press

releases, or promotional materials requires prior written approval from the appropriate IDC vice president or country manager. A draft

of the proposed document should accompany any such request. IDC reserves the right to deny approval of external usage for any

reason. Copyright 2017 IDC. Reproduction without written permission is completely forbidden.