Ovum Decision Matrix: Selecting a Middleware-as-a-Service Suite, 2017–18

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Publication Date: 20 Jul 2016 | Product code: IT0012-000172

Chantel Cary

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Summary

CatalystService capabilities and customer needs have evolved at a rate that has outpaced the capabilities of

telcos' legacy BSS systems. In order to support and monetize the new technologies emerging in the

telecoms industry and serve changing customer needs, telcos are investing in upgrading their

revenue management systems. Central to the improvement of the state of revenue management in

the telco organization is the upgrading of billing and charging systems. In Ovum's 2016 ICT Enterprise

Insights survey of more than 500 telco CIOs, 80% of telcos stated that they plan to make some type of

upgrade to their billing and charging systems in the next 12–18 months, with nearly 45% undertaking

major transformation projects or completely replacing these systems.

In light of these facts, Ovum has produced this Ovum Decision Matrix to identify how the market's top

billing and charging vendors compare against one another across technical capabilities, execution of

strategy, and market impact.

Ovum viewAs telcos aim to compete in an increasingly online and digital market, meet customer expectations,

and improve revenue growth, it is growing more evident that they must first upgrade their revenue

management systems. Legacy and multiple revenue management systems have created a bottleneck

for telcos as they attempt to evolve operations. According to Ovum's most recent ICT Enterprise

Insights survey of more than 500 telco CIOs, 60% of telcos stated that they had 50 or more revenue

management systems supporting the business. Hosting this many systems is not only costly, but also

hinders the telcos' ability to execute large-scale changes efficiently. In response, the industry is

undergoing a wide-scale transformation, with a large number of telcos focusing on billing and charging

transformation projects.

As telcos award new billing and charging contracts, they are seeking out vendors that can improve

business agility, have configurable systems that can be quickly deployed, and also support them as

the telcos develop new business models to compete in the market.

The telecoms vendor space has become quite competitive over the last decade. As telcos' financial

situations have worsened, telcos have changed their criteria for awarding new contracts. As a result,

telcos have moved away from awarding to "best of breed" vendors for a single system component

(such as just rating engines) and have increasingly begun to award contracts to vendors with a

comprehensive or "best of suite" product and service portfolio.

Key findings More than 80% of telcos plan to upgrade their revenue management systems over the next

18 months, according to Ovum's ICT Enterprise Insights survey.

Telcos are upgrading billing and charging systems in order to improve operational agility and

support new and digital business models.

Improving pricing tariffs, adding convergence, and improving real-time capabilities are among

the top priorities for telcos that are upgrading billing and charging systems.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 2

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Network equipment providers (NEPs) and vendors with an end-to-end BSS portfolio, are the

vendors of choice for telcos upgrading their billing and charging systems.

A vendor with a strong billing and charging solution will offer several pre-integrated

components, have a complete BSS portfolio, strong services revenues and capabilities, and a

fully virtualized solution with low latency.

The market leaders in this Ovum Decision Matrix – Amdocs, Ericsson, Huawei, Netcracker,

and Oracle – have technically strong solutions, have demonstrated innovation in the

development of the product, and have varied global footprints.

AsiaInfo, CSG International, Comarch, Redknee, and ZTESoft are the market challengers and

all offer unique and differentiating capabilities, but fall short of the market leader category

because their capabilities are not as deep.

Vendor solution selection

Inclusion criteriaOvum defines billing and charging as a subset of processes occurring within telco revenue

management systems. While typically delivered as two separate products, the two systems and

processes are closely linked and are evolving as a result of recent changes in the telecoms market.

In order to be included in this Decision Matrix, vendors had to meet the following criteria:

The vendor must offer both billing and charging solutions, and those must be convergent. For

the purpose of this report, Ovum defines convergent as being capable of supporting prepaid

and postpaid subscribers, multiple service types, online and offline charging, multiple service

provider types (i.e. consumer, wholesale, and enterprise), and network types (e.g. LTE, IMS).

The vendor's solution must be in commercial use, and have at least one operational telco

customer using both the convergent charging and convergent billing solutions.

Vendors included in the Decision Matrix were evaluated not only on their technical strengths and the

execution of their solutions, but also their market impact, which includes the opinions of their

customers. Ovum's Decision Matrix diagram, vendor assessment, and overall positioning are based

on information and data shared by the vendors through the completion of a technical worksheet,

demo, and briefing discussions. Ovum does not make any assumptions regarding information not

disclosed by participants (such as specific revenue breakdowns), therefore the final positioning is a

representation solely of the information provided by the vendor to Ovum. To understand the

competitive dynamics in the billing and charging market, Ovum evaluated and profiled the following

ten providers:

Amdocs

AsiaInfo

Comarch

CSG International

Ericsson

Huawei

Netcracker

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 3

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Oracle

Redknee

ZTESoft

Exclusion criteriaOvum excluded vendors' solutions if the vendor

did not meet the deadline to return all required information.

could not provide customer references or case studies.

does not actively sell a component of its core solution (i.e. charging or billing).

MethodologyTechnology/service assessment

Ovum analysts assign vendors a score from 1 to 10 for each of the assessment criteria, and the

scores are averaged to determine each vendor's overall technology assessment rating. The four

technology assessment criteria used for the real-time convergent billing and charging ODM include:

Product development: Assesses how and to what extent the vendor invests in developing

and evolving its solution, and how well aligned it is with industry frameworks.

Platform capabilities: Assesses the features and functionalities included in the standard

solution.

Usability: Assesses the ease of use of the solution for business users.

Completeness of solution: Assesses the extent to which the solutions are fully functional,

and capable of supporting next-generation business models and challenges, while also

evaluating the degree to which the vendor brings new ideas, features, and services to the

market.

Execution

In this dimension, Ovum analysts review the vendor's ability to deliver the solution for an array of telco

types, focusing specifically on the following six areas:

Maturity: The stage that the product is currently at in the maturity lifecycle is assessed here,

relating to the maturity of the product relative to the market.

Interoperability: In this element we assess how easily the solution can be integrated into the

organization's operations, relative to the demand for integration for the project.

Innovation: Innovation can be a key differentiator in the value that a telco achieves from a

software or services implementation, and this is assessed in this criteria.

Deployment: Referring to a combination of assessed criteria and points of information, Ovum

provides detail on various deployment issues, including time needed for deployment,

industries covered, services offered, and support.

Scalability: Points of information are provided to show the scalability of the solution across

different scenarios.

Enterprise fit: The alignment of the solution is assessed in this dimension, and the potential

ROI period identified.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 4

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Market impact

The global market impact of a solution is assessed in this dimension. Market impact is measured

across four categories, each of which has a maximum score of 10.

Revenue and growth: Each solution's global billing and charging revenues are calculated as

a percentage of the market leader's. This percentage is then multiplied by a market maturity

value and rounded to the nearest integer. Overall global revenue carries the highest weighting

in the market impact dimension.

Telecoms reach: Ovum determines each vendor's revenues in four regions: North America;

Latin America and the Caribbean; Europe, the Middle East, and Africa (EMEA); and

Asia-Pacific. These revenues are calculated as a percentage of the market-leading solution's

revenues in each region, multiplied by 10, and then rounded to the nearest integer. The

solution's overall geographical reach score is the average of these three values.

Vertical penetration: Ovum determines each vendor's revenues in the following verticals:

energy and utilities; financial services; healthcare; life sciences; manufacturing; media and

entertainment; professional services; public sector; retail; wholesale and distribution;

telecommunications; and travel, transportation, logistics, and hospitality. These revenues are

calculated as a percentage of the market leader's revenues in each vertical, multiplied by 10,

and then rounded to the nearest integer. The solution's overall vertical penetration score is the

average of these three values.

Customer sentiment: Vendors were asked to provide no fewer than three customer

references to participate in a survey. References were surveyed and asked to evaluate the

vendor's billing and charging solution's capabilities, including ease of use, pricing, and

innovation. Participants also ranked the top three perceived market leaders, preferred vendor

type, and buying preference. Customer sentiment is captured in four categories: vendor's

charging solution, vendor's billing solution, vendor-type preference (e.g. telecoms-specific

vendor, large software vendor, or NEP), and vendor portfolio preference (e.g. best of breed,

BSS only, or best of suite). Each section within the customer sentiment category has a

maximum score of 2.5, with the maximum score for overall customer sentiment being 10.

Ovum ratings Market leader: This category represents the leading solutions that we believe are worthy of a

place on most technology selection shortlists. The vendor has established a commanding

market position with a product that is widely accepted as best-of-breed.

Market challenger: The solutions in this category have a good market positioning and the

vendors are selling and marketing the products well. The products offer competitive

functionality and a good price-performance proposition, and should be considered as part of

the technology selection.

Market follower: Solutions in this category are typically aimed at meeting the requirements of

a particular kind of customer. As a tier-one offering, they should be explored as part of the

technology selection. (In this Decision Matrix, no vendors fell into this category.)

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 5

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Market and solution analysisThe telecoms industry is undergoing a unique period of change. New business models, technologies,

and customer expectations are forcing telcos to invest in improving systems across the business;

revenue management, particularly in improving billing and charging systems, is one of the first areas

of investment.

Billing and charging systems are central to telcos' ability to operate and generate revenue. However,

over the years, billing operations have become neglected. Through mergers and acquisitions, and in

support of new product launches, telcos have accumulated dozens of billing and charging systems,

which have in turn greatly hindered their ability to evolve. According to Ovum's 2016 ICT Enterprise

Insights survey of more than 500 telco CIOs, 60% of telcos stated that they had 50 or more revenue

management systems supporting their operations, with 12% stating they had more than 1,000.

Housing this many legacy, siloed, and rigid systems is not only expensive, but also stifles telcos'

ability to innovate and keep up with fast-changing expectations. As a result, telcos are increasingly

opting to transform and, in many cases, completely replace their billing and charging systems.

In the same Ovum survey, 80% of telcos stated that they plan to upgrade their billing and charging

systems over the next 18 months. Among the top priorities were improving pricing tariffs to gain more

agility in charging parameters, introducing convergence in the billing and charging processes, and

improving real-time capabilities. These features are crucial for telcos as their business environment

becomes more digitally driven; they are required to operate in near-real time, charge for (and

monetize) new services as new technologies emerge, and charge and bill for multiple services on a

single bill. Additionally, telcos are facing pressure to provide a more personalized customer

experience and so require close integration of billing and charging with systems such as CRM and

policy. Having these capabilities is at the top of the minds of telcos as they seek new billing and

charging solutions and vendor partners.

Our analysis shows that vendors with comprehensive "best of suite" offerings are favored over those

with niche, "best of breed" solutions. Moreover, network equipment providers (NEPs) and

telecoms-specific vendors are seen as more favorable providers than large software vendors,

according to an Ovum survey of 30 vendor customer references. This shift in preference from "best of

breed" solutions to "best of suite" is attributed mostly to the need to lower capex and opex, but is

reinforced by the need to also closely integrate billing and charging systems with other systems such

as product catalogs, service activation and provisioning systems, CRM, and policy control.

Ovum Decision Matrix: Real-time Convergent Billing and Charging, 2016–17The billing and charging space has fully matured and competition among vendors has become

extremely competitive, as Figures 1 and 2 show. As a result of the technology being mature, vendors

must differentiate their offerings by developing new and innovative features and use cases. They must

differentiate themselves through pricing and deployment time and by offering an array of products

beyond just billing and charging. Additionally, to be considered strong, a vendor's solution must be

capable of supporting existing telco business models with enough agility and use cases to support

next-generation and digital business models. Key capabilities and features that a vendor's solution

should possess include:

real-time charging

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 6

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

convergence across customer types (i.e. prepaid, postpaid), service type (e.g. fixed, mobile),

and network type (e.g. 2G, 3G, LTE)

ability to charge for any instance or thing

ability to issue bills in multiple formats including HTML and apps

real-time analytics engine

reporting system with insight into revenue performance, billing process status, etc.

billing operations management portal to enable users to bill on-demand, roll back to the

previous step in the billing process, and generate alerts for issues in the billing process.

In addition, a strong billing and charging vendor will offer an array of additional products across a BSS

and OSS portfolio. According to an Ovum survey of telcos planning to upgrade their billing and

charging solutions, CRM, analytics, and policy were the products that telcos prefer to have

pre-integrated into their billing and charging systems.

Finally, a strong vendor will have an array of services and support capabilities that spans from

professional services (e.g. consulting) to varying SLA options, systems integrations, and SaaS.

Figure 1: Ovum Decision Matrix: Real-time Convergent Billing and Charging, 2016–17

Source: Ovum

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 7

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

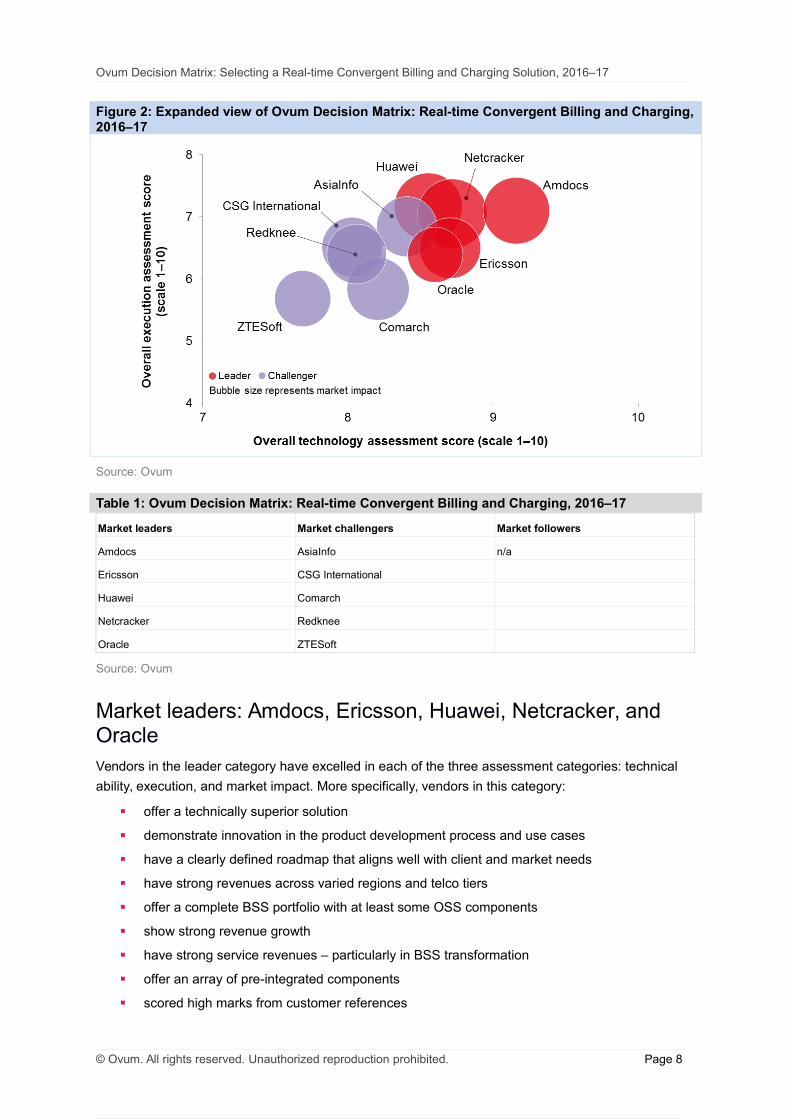

Figure 2: Expanded view of Ovum Decision Matrix: Real-time Convergent Billing and Charging,2016–17

Source: Ovum

Table 1: Ovum Decision Matrix: Real-time Convergent Billing and Charging, 2016–17

Market leaders Market challengers Market followers

Amdocs AsiaInfo n/a

Ericsson CSG International

Huawei Comarch

Netcracker Redknee

Oracle ZTESoft

Source: Ovum

Market leaders: Amdocs, Ericsson, Huawei, Netcracker, and OracleVendors in the leader category have excelled in each of the three assessment categories: technical

ability, execution, and market impact. More specifically, vendors in this category:

offer a technically superior solution

demonstrate innovation in the product development process and use cases

have a clearly defined roadmap that aligns well with client and market needs

have strong revenues across varied regions and telco tiers

offer a complete BSS portfolio with at least some OSS components

show strong revenue growth

have strong service revenues – particularly in BSS transformation

offer an array of pre-integrated components

scored high marks from customer references

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 8

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

scored high marks in the perceived market leader section of the customer reference survey

have live use cases, proof of concepts, or both that prove their solution's ability to support

next-generation technologies.

To be clear, Ovum does not make any assumptions regarding information not disclosed by

participants (such as specific revenue breakdowns), therefore the final positioning is a representation

solely of the information provided by the vendor to Ovum (see the earlier "Inclusion criteria" section for

more detail).

Amdocs is a telecoms software vendor, and its solution is technically strong. The vendor has

developed a wide array of use cases to address telco needs and market challenges specifically. The

vendor also performed well among all customer references, with telcos identifying Amdocs as the

clear market leader in the billing space and as one of the top two vendors in the charging space. This,

in addition to the vendor's strong service revenues, overall revenue growth, and commitment to

continuous innovation for telecoms specifically, makes Amdocs a leader in the market.

Ericsson is a network equipment provider (NEP) with an extensive portfolio spanning both BSS and

OSS. In addition to its comprehensive product portfolio, the vendor's understanding of and ability to

provide telco networks bolster its position as a market leader. According to two recent Ovum surveys

with telcos executives, NEPs are seen as the most desirable group of providers for billing and

charging solutions due to their ability to evolve the products to support network capabilities.

Additionally, Ericsson's strong revenues, large number of BSS transformation project wins, and focus

on aligning its product roadmap with the market and its customers' immediate needs help it stand as a

market leader.

Huawei is also an NEP with a portfolio that includes a full suite of products across BSS and OSS. The

vendor's numerous BSS transformation project wins, along with early investments into offering a

next-generation, digital-ready BSS solution in its BES product, has cemented the vendor's positioning

as a market leader.

Netcracker is a telecoms software vendor but, as a subsidiary of NEC, also possesses the ability to

partner with its parent company to provide network equipment. The vendor has a technically

advanced solution that includes pre-integrated products across BSS and OSS. Netcracker's strong

revenues, increasing number of BSS wins, and 20+ BSS transformation project wins over the last 12

months are just some examples of how the vendor has been able to emerge as a market leader.

Oracle is a large software vendor with a strong presence across multiple industries. While the vendor

has a technically competent solution with a wide portfolio of BSS and OSS that can be pre-integrated

or included as add-ons, the vendor must improve on telecoms-specific product innovation in order to

improve its overall market position.

Market challengers: AsiaInfo, CSG International, Comarch, Redknee, and ZTESoftVendors in the challenger category have excelled in two of the three assessment categories. Market

challengers have a solution that is technically competent. They also show some product innovation

and have a product roadmap that is aligned with the industry. Vendors in this category may be lacking

in minor areas. For example, they might have minimal footprint among telco types or regions; the

majority of their total revenues or investments may be in an area outside of BSS or telecoms; and

they might have limited industry use cases and a less established record of innovation (compared to

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 9

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

the market, other vendors, and/or as indicated by customer references). Vendors in this category can

become a market leader by improving in one key area.

AsiaInfo is a software vendor operating mainly in the Asia-Pacific region with a technically strong

solution that includes an end-to-end BSS offering. The vendor has invested significantly in developing

a billing and charging solution that is well aligned with telco needs and ahead of its competitors in

terms of technical capabilities. Investments into developing a quickly deployable BSS-lite solution and

a public cloud-enabled BSS solution have allowed AsiaInfo to differentiate itself in the market. To

move into the leader category, however, the vendor will need to expand its global footprint and claim a

larger market share and brand presence in more regions outside Asia.

CSG International is a telecoms software vendor with a strong presence in the enterprise space. The

vendor has made great strides to align its product with its customer's needs and offer flexible pricing

options for telcos. Growing the consumer business will allow CSG to improving its overall position.

Comarch is primarily a telecoms software vendor with BSS and OSS products and capabilities in

additional industries. While the vendor offers a solution that meets telcos' technical needs, the vendor

must further develop its product roadmap, introduce innovative industry use cases, and expand its

global footprint in order to improve its overall positioning.

Redknee is primarily a telecoms software vendor with a strong, though incomplete, BSS portfolio. The

vendor has made significant investments into enhancing its solution both through mergers and

acquisitions, and organic R&D. The vendor has made significant strides to improve its overall market

position but will need to show steady revenue growth before it can be considered a market leader.

ZTESoft is a telecoms software vendor and subsidiary of network equipment provider ZTE. The

vendor offers an array of products that span BSS and OSS, in addition to providing network

equipment through its parent company. While the vendor has a product roadmap aligned with industry

trends, the vendor must develop more innovative use cases and expand its global footprint, and

emerge as a leader in at least one region to improve its overall positioning.

Market followersMarket followers, of which there were none in this Decision Matrix, have excelled in one of the three

assessment categories. Market followers have a product that meets the standard technical

requirements for telcos, but have demonstrated minimal product innovation or do not have a product

roadmap that aligns well with industry trends. Vendors in this category also have not yet developed a

strong presence in a particular market or penetrated a telco subset.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 10

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Market leaders

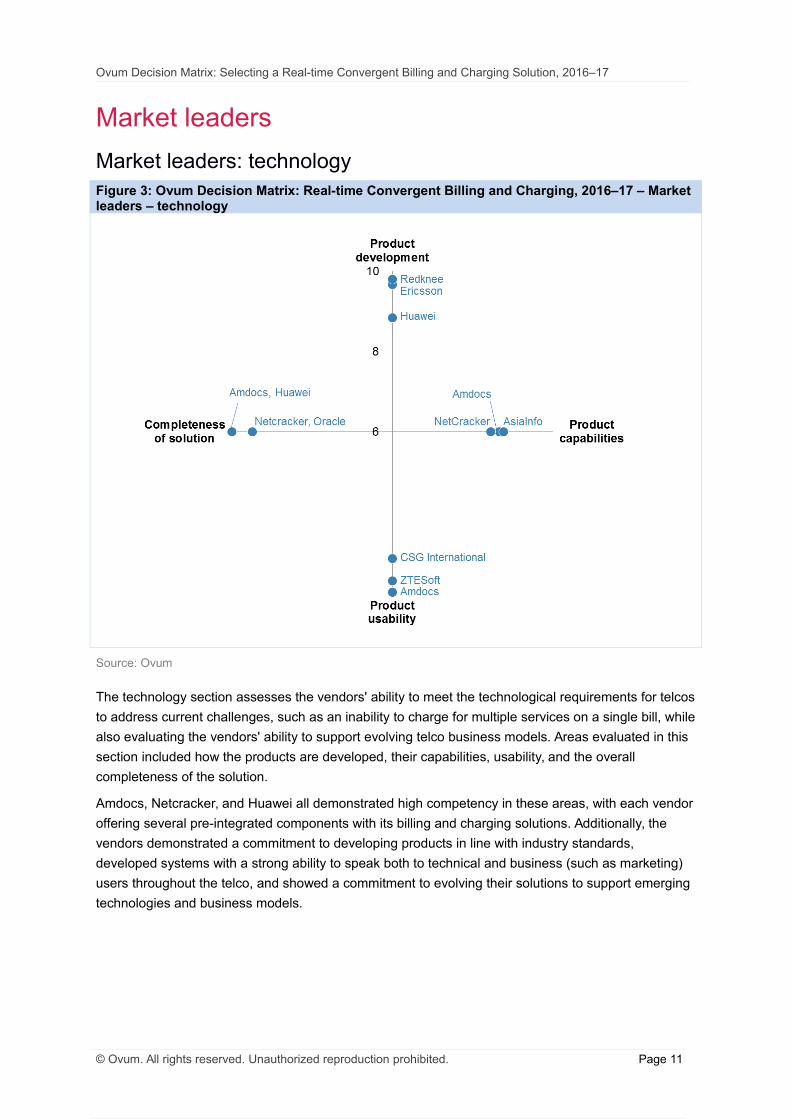

Market leaders: technologyFigure 3: Ovum Decision Matrix: Real-time Convergent Billing and Charging, 2016–17 – Market leaders – technology

Source: Ovum

The technology section assesses the vendors' ability to meet the technological requirements for telcos

to address current challenges, such as an inability to charge for multiple services on a single bill, while

also evaluating the vendors' ability to support evolving telco business models. Areas evaluated in this

section included how the products are developed, their capabilities, usability, and the overall

completeness of the solution.

Amdocs, Netcracker, and Huawei all demonstrated high competency in these areas, with each vendor

offering several pre-integrated components with its billing and charging solutions. Additionally, the

vendors demonstrated a commitment to developing products in line with industry standards,

developed systems with a strong ability to speak both to technical and business (such as marketing)

users throughout the telco, and showed a commitment to evolving their solutions to support emerging

technologies and business models.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 11

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Market leaders: executionFigure 4: Ovum Decision Matrix: Real-time Convergent Billing and Charging, 2016–17 – Market leaders – execution

Source: Ovum

The execution section evaluates how effectively a vendor's solution can be deployed within a telco,

regardless of telco type. Areas assessed in the execution section include: the maturity of the solution,

how well aligned the solution is with market needs (from an architectural and capabilities standpoint),

the scalability of the solution, and how effectively the solution can be deployed.

Amdocs, Huawei, and Netcracker separated themselves as leaders in this category. Each of the

vendors have developed mature solutions that are well aligned with the needs of the telecoms

industry and have invested in developing product roadmaps that include innovative and differentiating

features or capabilities.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 12

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

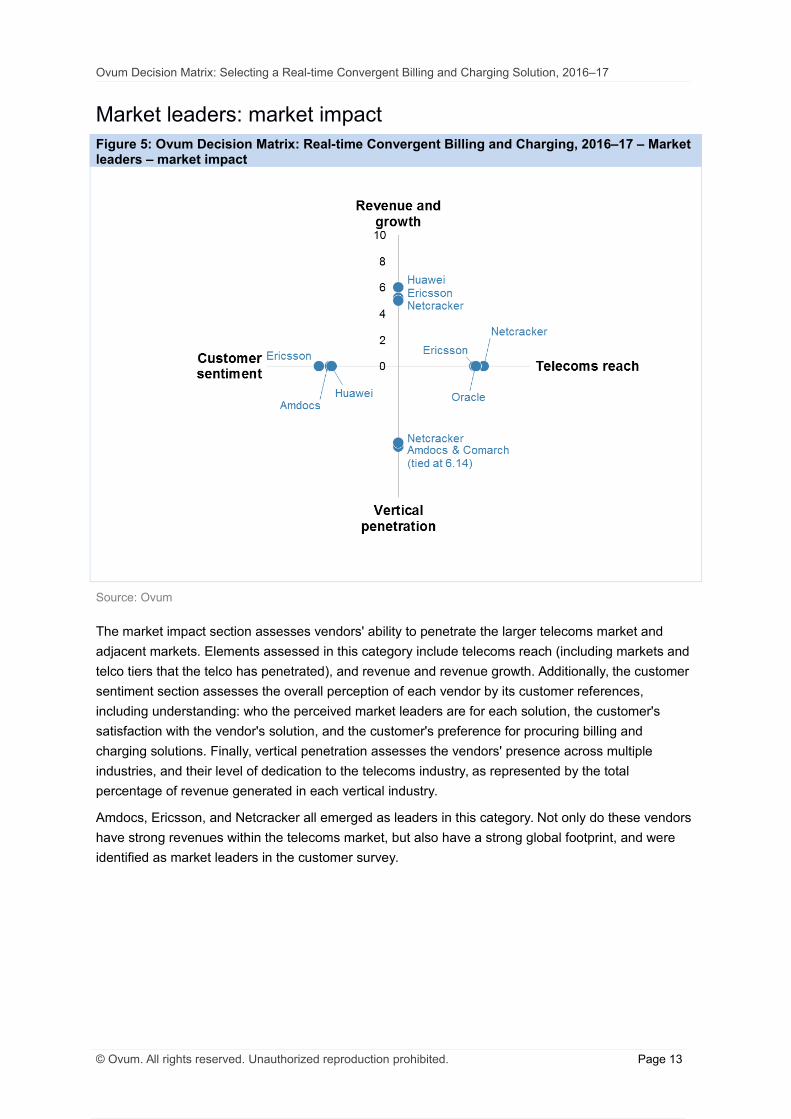

Market leaders: market impactFigure 5: Ovum Decision Matrix: Real-time Convergent Billing and Charging, 2016–17 – Market leaders – market impact

Source: Ovum

The market impact section assesses vendors' ability to penetrate the larger telecoms market and

adjacent markets. Elements assessed in this category include telecoms reach (including markets and

telco tiers that the telco has penetrated), and revenue and revenue growth. Additionally, the customer

sentiment section assesses the overall perception of each vendor by its customer references,

including understanding: who the perceived market leaders are for each solution, the customer's

satisfaction with the vendor's solution, and the customer's preference for procuring billing and

charging solutions. Finally, vertical penetration assesses the vendors' presence across multiple

industries, and their level of dedication to the telecoms industry, as represented by the total

percentage of revenue generated in each vertical industry.

Amdocs, Ericsson, and Netcracker all emerged as leaders in this category. Not only do these vendors

have strong revenues within the telecoms market, but also have a strong global footprint, and were

identified as market leaders in the customer survey.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 13

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Vendor analysis

Amdocs (Ovum recommendation: Leader)Figure 6: Amdocs radars

Source: Ovum

Ovum SWOT assessment

Strengths

Strong solution with aggressive focus on supporting next-gen: Amdocs is a clear market leader

within the billing and charging space. Its product is widely recognized and regarded as an all-round

leader in the industry by both telcos and competing vendors. Amdocs' market positioning has been

solidified not only by large contract wins, but likewise by the vendor's commitment to proactively

address the market challenges (both existing and future) to telcos' revenue management systems in

the development of its product roadmap, including a clearly defined roadmap for a fully virtualized

BSS stack. Over the years, Amdocs has enhanced its billing and charging solution to incorporate

features such as pre-integrated analytics, mediation, and partner management, and has increased its

focus on the networks domain in order to incorporate additional components such as network quality

of experience (QoE) and other elements of the OSS. Additionally, the vendor supports the delivery of

its billing and charging systems in a virtualized environment (with low latency and high availability),

complete with the support of its extensive services offerings, which are bundled into the software

contracts. The vendor has also done a superb job at following market technology trends and

anticipating their impact and challenges on telcos' billing and charging systems, and building

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 14

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

out-of-the-box solutions built off its core billing and charging offering, such as its recently launched IoT

monetization and digital platforms.

Strong global footprint: As a result of differentiating its products in the market, Amdocs has been

able to capture a significant portion of market share in the telecoms market. The vendor has more

than 250 telco clients spread across 80 countries. Additionally, several recent BSS transformation

project wins have allowed Amdocs to strengthen its geographical footprint and overall market impact.

Weaknesses

Limited footprint among smaller telcos: Although Amdocs has strong relationships with tier-1 telcos

and has demonstrated an ongoing dedication to supporting the next-generation telco, the vendor has

a limited footprint within the tier-2 and smaller telco space, which has left a large addressable market

on the table. Specifically, 55% of the vendor's revenue came from North America in 2015, with AT&T

accounting for approximately 33% of the revenue in North America. While the vendor offers Amdocs

Compact Convergence – a solution targeted at the small telco and MVNO space – its core focus

remains on building out the capabilities of its Amdocs CES solution, which has performed better in the

tier-1 telco market. Furthermore, as the vendor invests in developing new capabilities such as a fully

virtualized billing system, it will find that larger vendors will be more hesitant to adopt these

technologies, while the smaller players will be more willing. Gaining these smaller wins and

developing market use cases, albeit with smaller telcos, will allow Amdocs to not only increase its

market footprint, but also provide practical market use cases, which it can use to grow the business

further.

Opportunities

Grow emerging markets presence to capture new opportunities: According to Ovum's most

recent Telecoms IT spend forecast, global IT spend in emerging markets in Latin America, Central and

Southern Asia, and Africa is expected to grow at a CAGR of 2.9%, 6.4%, and 5.0%, respectively, over

the next five years. Telcos in these regions are urgently undertaking substantial transformation

projects to keep up with – and in many cases, leapfrog – the competition. While Amdocs has a strong

market presence in mature markets such as Europe and North America, only 25% of its total revenue

comes from the Asia-Pacific and Latin American markets. Focusing on securing deals with smaller

telcos in these regions will enable the vendor to better penetrate the emerging markets and capture

the increasing IT spend from these regions.

Threats

NEPs seen as the favored provider: According to a recent Ovum survey of telco executives, 45% of

telcos stated that NEPs (network equipment providers) were the vendor type of choice when selecting

a new billing and charging solution. As the industry moves closer to rolling out 5G networks and live

deployments of NFV and SDN, telcos will need to also invest in upgrading their billing and charging

systems to support and monetize these new technologies. It is also likely, as we have seen in the

past, that the NEPs will bundle in billing and charging software to support these rollouts, thus cutting

out non-network vendors such as Amdocs. As a result, Amdocs will see the competition for billing and

charging contracts become fiercer and will need to have several clear, innovative use cases available

in order to justify telcos seeking out a "best of breed" option for billing and charging over a bundled

deal with a NEP.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 15

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

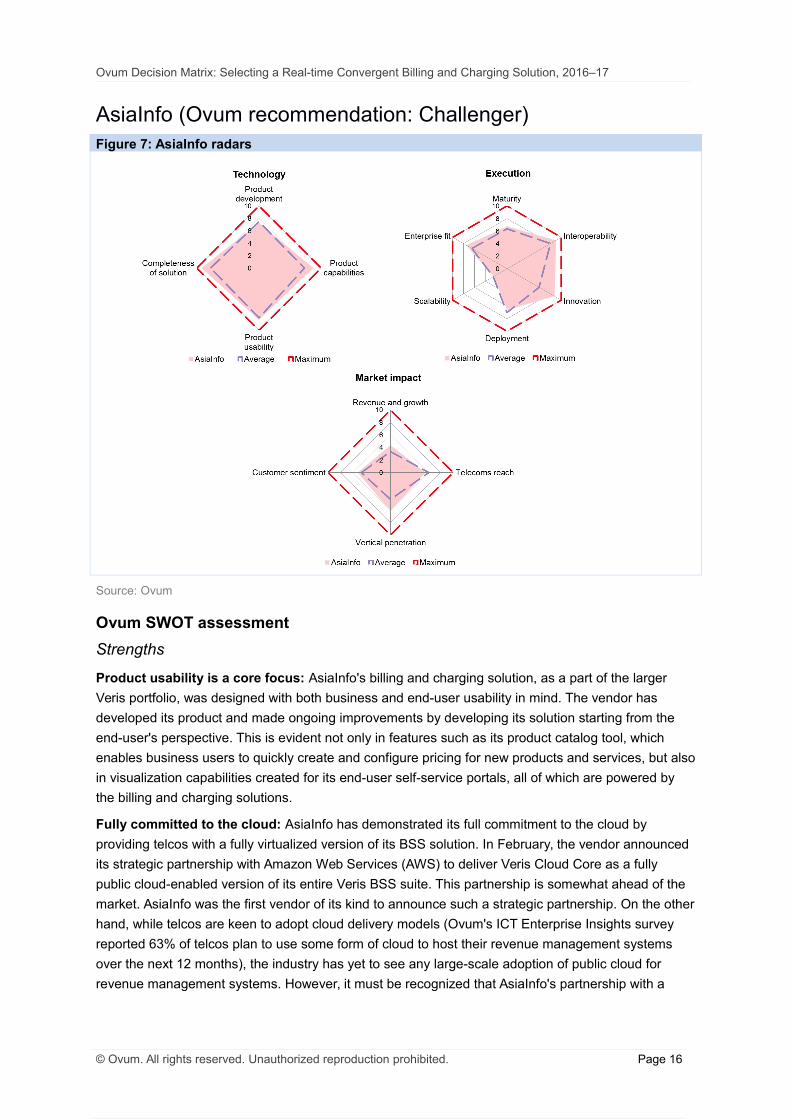

AsiaInfo (Ovum recommendation: Challenger)Figure 7: AsiaInfo radars

Source: Ovum

Ovum SWOT assessment

Strengths

Product usability is a core focus: AsiaInfo's billing and charging solution, as a part of the larger

Veris portfolio, was designed with both business and end-user usability in mind. The vendor has

developed its product and made ongoing improvements by developing its solution starting from the

end-user's perspective. This is evident not only in features such as its product catalog tool, which

enables business users to quickly create and configure pricing for new products and services, but also

in visualization capabilities created for its end-user self-service portals, all of which are powered by

the billing and charging solutions.

Fully committed to the cloud: AsiaInfo has demonstrated its full commitment to the cloud by

providing telcos with a fully virtualized version of its BSS solution. In February, the vendor announced

its strategic partnership with Amazon Web Services (AWS) to deliver Veris Cloud Core as a fully

public cloud-enabled version of its entire Veris BSS suite. This partnership is somewhat ahead of the

market. AsiaInfo was the first vendor of its kind to announce such a strategic partnership. On the other

hand, while telcos are keen to adopt cloud delivery models (Ovum's ICT Enterprise Insights survey

reported 63% of telcos plan to use some form of cloud to host their revenue management systems

over the next 12 months), the industry has yet to see any large-scale adoption of public cloud for

revenue management systems. However, it must be recognized that AsiaInfo's partnership with a

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 16

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

proven, secure, and trusted public cloud provider such as AWS puts it in a favorable position to win

business down the line as telcos begin to adopt public cloud for BSS.

Weaknesses

Limited global footprint: Although AsiaInfo offers an end-to-end BSS solution that is technically

strong with high usability, the vendor falls short in its ability to capture global market share and expand

its footprint. Ninety-nine percent of AsiaInfo's billing and charging revenue comes from Asia-Pacific,

while only 1% of its revenue comes from the EMEA region. Though the vendor began expanding into

EMEA three years ago, this lack of global penetration limits its ability to be seen as a global market

leader and severely limits the vendor's revenue potential. Though it has proven itself as a leading

vendor within the Asia-Pacific market, AsiaInfo will need to secure more deals and distribute its

revenue across more regions to improve its positioning and be seen as a leading billing and charging

vendor in the overall telecoms market.

Opportunities

Address digital pain points to win big: As telcos undertake BSS transformation projects they must

find a balance between appreciating that true IT transformation is a long-term, multiyear commitment

while also finding the means to support digital services today. AsiaInfo's Real Time Charging solution

allows the vendor to go after this segment by providing a BSS "lite" solution, which includes online

charging, policy, and product catalog. The solution can be quickly deployed to enable functions such

as e-commerce and other capabilities to support digital business models. This approach will allow

AsiaInfo to:

secure revenue from those telcos that have already committed to long-term transformation

projects but that are looking for immediate solutions

penetrate smaller to medium-sized telcos who have not yet committed to full transformation

projects

position itself favorably to win larger transformation projects and expand its footprint.

Threats

Recent security breaches call cloud security into question: AsiaInfo has placed a big bet on

telcos buying into public cloud for BSS. While this is a bold, forward-looking move, telcos are still

hesitant to adopt public delivery models for fear of security breaches. Moreover, the showdown

between Apple and the US government calls into question more concerns around cloud security. After

the US government was able to successfully hack into the iPhones of two terror suspects, the

question has become, "Just how safe is cloud security?" Although AsiaInfo has the backing from a

trusted cloud provider in AWS, this development is likely to make telcos more hesitant to invest in

putting business-critical systems like billing and charging into the public cloud.

Competitors are strengthening their positioning in AsiaInfo's key market: The competition in

AsiaInfo's key Asia-Pacific markets is becoming more intense. Huawei and Ericsson have both

announced their own strategic partnerships with cloud providers to offer public cloud versions of their

respective solutions. These vendors, because of their ability to supply the network, services, and

cloud capabilities, in addition to offering both BSS and OSS, will have a competitive advantage when

going up against AsiaInfo. The increased competition in this market reinforces the fact that AsiaInfo

needs to continue to expand its footprint to secure and improve its market impact and overall

positioning.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 17

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Comarch (Ovum recommendation: Challenger)Figure 8: Comarch radars

Source: Ovum

Ovum SWOT assessment

Strengths

Simplified BSS solution: Comarch is a homegrown European vendor with a strong presence in

Eastern Europe and competent technical credentials. Its Comarch BSS solution is a pre-integrated

platform that combines billing, charging, CRM, product catalog, and service activation. The solution,

which is available out of the box, is also supported by Comarch's extensive services offering, which

includes managed services and BSS transformations, among others.

Cross-industry expertise: Comarch's reach extends across 12 industries, including banking, utilities,

education, retail, and others. This multi-industry experience provides Comarch with a competitive

edge as more telcos search for ways to expand into new industries. Despite this multi-industry

presence, Comarch's focus and core revenue driver remains within the telecoms space. Owing to its

expertise in multiple industries, Comarch is also well positioned to win deals with telcos looking to

support IoT and cloud services, or expand into new industries.

Weaknesses

Little market differentiation: Although Comarch offers a solid billing and charging solution with

multiple industry use cases, the vendor has not yet developed any differentiating elements to

competitively separate its solution from other competitors in the market. The billing and charging

market has already matured and it is important for vendors to develop differentiating capabilities and

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 18

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

unique use cases to win new telco business, especially as telcos set out to innovate and compete

against new market players such as OTT providers. Furthermore, because Comarch operates in

industries other than telecoms, the vendor is well positioned to develop new products or features

aimed at addressing the challenges of telcos trying to open revenue streams in new industries.

Limited footprint: The majority of Comarch's market share (85%) comes from the EMEA region. It

has a limited footprint across the Americas and Africa, and no market share in Asia-Pacific. Its market

share comes mostly from smaller tier-2 and tier-3 telcos. It is important for Comarch to expand its

footprint more evenly across multiple regions, and secure deals with larger telcos to improve its

market impact and overall market positioning. The vendor has begun focusing on expanding into new

regions, however, and has recently established local business development centers throughout the

world, including in Benelux, Brazil, Chile, Dubai, Italy, Malaysia, Spain, and the UK. By opening offices

in these countries, Comarch intends to ramp up sales and support activities in these regions and

improve its global footprint.

Opportunities

Expand footprint by going after telcos expanding into new industries: As a vendor with expertise

in 12 industries, Comarch is well positioned to become the vendor of choice for those telcos seeking

revenue opportunities in new industries. It is important for Comarch to develop relevant solutions

based on its experience in other industries, yet it must also make sure these solutions translate to the

telecoms industry. Experiences with the challenges of the retail industry, which accounts for 17% of

Comarch's revenue, can be used develop relevant solutions for telcos planning to expand into this

area. Securing wins from telcos expanding into new industries will allow Comarch to improve its

market impact and overall positioning.

Threats

Product innovation from competitors is threatening market share: The telecoms vendor space

has become highly competitive over the last several years. Even more so is the BSS and revenue

management space, as this is an area that has seen very little change over the years. As a result of

changing market conditions and telco needs, vendors are investing significantly in incorporating

differentiating capabilities and developing unique use cases for their billing and charging solutions.

Additionally, small, niche digital billing vendors are emerging in the market, attempting to disrupt the

vendor space and provide telcos with low-cost, quick-deployment, digital solutions that center on

online charging. As these small vendors begin to win business from telcos looking for a quick,

short-term solution for digital, and as the larger vendors win bigger multiyear contracts and

transformation projects, Comarch will need to find new ways to differentiate itself in the market or risk

its positioning.

Services revenue has remained flat: Globally, we have observed a gradual shift in BSS revenue

away from software revenue and toward services revenue. This is the result of large transformation

projects being attributed toward managed services revenue, as well as an increase in cloud services

for BSS. During this same timeframe we have also observed vendor services revenue increase

throughout the market. Although services revenue accounts for 44% of Comarch's total revenue, this

number has remained flat over the last couple of years. The vendor must find a way to show growth in

its services revenue to improve its overall market positioning.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 19

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

CSG International (Ovum recommendation: Challenger)Figure 9: CSG International radars

Source: Ovum

Ovum SWOT assessment

Strengths

Highly pre-integrated solution: CSG's Singleview platform is a pre-integrated solution that includes

billing, charging, and customer management. The vendor also offers mediation (Intermediate),

interconnect billing (WBMS), and digital commerce (Ascendon) solutions, which are typically

purchased as add-ons by many of its customers. Singleview was designed to allow telcos to run both

their enterprise and consumer operations on a single platform. The solution is deployable out of the

box, with major updates released every 12–18 months. As new releases and minor updates are made

available, customers have the option to upgrade the entire platform or choose to upgrade individual

modules that best suit their needs.

Weaknesses

Small share of consumer market: While CSG has more than 200 customers, the consumer market

only makes up 30% of its overall contract wins. This suggests that the vendor has not gained the

confidence of the larger consumer market where conditions are sparking unprecedented needs and

buying habits that are driven by motivations that differ from those in the past. The lack of consumer

business also shows that the vendor's solution may not be as strong or have as much of a market

impact as expected.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 20

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Opportunities

Leverage positioning to win IoT business: As a result of the majority of CSG's revenue coming

from the enterprise space and its thought-leadership on IoT, the vendor is well positioned to become a

leading vendor for IoT monetization solutions for telcos. CSG not only has a strong understanding of

the challenges telcos will face with monetizing IoT, but is working on developing relevant use cases

for how its billing and charging systems can help telcos open up more revenue streams for IoT. This

forward-thinking approach to IoT puts the vendor in position to secure early wins from telcos entering

the IoT space, which should improve CSG's market share and overall market positioning. Many of

CSG's competitors have a limited view of IoT and thus are not improving their billing and charging

solutions or developing relevant use cases for IoT. Thus, CSG is in a favorable position to capitalize

on this weakness in the industry.

Expand enterprise success into consumer market: Telco interest in improving enterprise

operations is increasing; however, the consumer space is facing unprecedented challenges and is in

dire need of transformation. CSG states that its Singleview platform is capable of supporting both

enterprises and consumers on a single platform; this is a strength that it must play up to further

penetrate its existing client base and secure more wins on the consumer side of the business.

Improving its market share on the consumer side of the business will help CSG to improve its overall

market positioning.

Threats

Competitors have the consumer business and the networks: CSG sees its biggest competitors as

being large telecoms vendors and NEPs such as Amdocs, Netcracker, Huawei, and Ericsson. While

the vendor has many strengths in its platform capabilities and overall portfolio, telcos are tending to

award contracts to vendors that can offer more of a "best of suite" solution with pre-integrated

components of the BSS and OSS stacks. Furthermore, in an Ovum survey of telcos' preferred

vendors, 45% of telcos stated that NEPs were the vendor type of choice when selecting a new billing

and charging provider. This poses the biggest threat to CSG's market position.

Growing presence in the consumer market is challenging without use cases: Another threat to

CSG's market positioning is the lack of consumer telco clients. This is unfortunately a vicious cycle

that will be a challenge for the vendor to break. As the industry approaches a breaking point where

telcos move beyond conjecturing about digital transformation and start to award contracts to vendors

to complete these transformations, CSG will face a double-edged sword as a result of a limited

number of consumer telco clients. Telcos will be awarding contracts to trusted vendors with proven

industry use cases for the consumer sector and CSG will struggle to win new contracts due to its lack

of use cases in this area – potentially compromising its current market position. The vendor must find

a way to leverage its existing enterprise customer base to secure small wins on the consumer side of

the business. This will allow the vendor to develop use cases so that it can begin to improve its

consumer and overall market position, with the eventual goal of winning larger deals on the consumer

side.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 21

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Ericsson (Ovum recommendation: Leader)Figure 10: Ericsson radars

Source: Ovum

Ovum SWOT assessment

Strengths

Strong next-gen-ready solution: Ericsson has three versions of its core billing and charging

solution. The first, CBIO (Charging & Billing in One), was developed from the Charging System and

BSCS iX Billing products created over more than 16 years through a combination of organic R&D –

with the support of the vendor's 14 global R&D centers – and M&A activity. The second is its

Enterprise and Cloud Billing solution, which was developed for enterprise customers and incorporated

into Ericsson's portfolio after acquiring MetraTech in 2014, and the final one is its Revenue Manager,

which was recently launched as a new solution and was developed in-house to support the

next-generation digital telco. As the industry trends towards new business models and needs,

Ericsson will continue enhancing its Revenue Manager solution to meet the evolving requirements of

the industry, including planning a future release to enable enterprise support on the platform. Though

the vendor plans to evolve its solution and make it more efficient (in terms of offering a single solution

for both enterprise and consumer customers), Ericsson has also guaranteed its customers that it will

continue to support its Enterprise and CBIO solutions until at least 2022. The key factor that makes

the Revenue Manager platform a strong solution is its end-to-end approach at BSS. The solution

includes a combination of billing, charging, partner and customer management, and analytics.

Revenue Manager also allows business users to create new business logic for potential products and

set up and test new rating and charging scenarios before launching them in the market. Furthermore,

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 22

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

the platform has high usability for business users, and enables telcos as well as enterprise partners

(such as OTTs) to have visibility into unbilled revenue. The solution also allows users to gain insight

into the revenue generated from partners, marketing campaigns, and promotions, as well as see

customer conversion rates.

Closed-loop feedback system aligns products with customer needs: Customer feedback is

central to Ericsson's ability to develop its billing and charging solutions. The vendor has developed a

closed-loop feedback system which assesses the larger trends and needs in the market, while also

incorporating and prioritizing customer feedback. The vendor holds customer events and strategy

sessions to gain an understanding of telcos' challenges – both overall and with Ericsson's solution.

Additionally, the vendor takes in feedback on which features and capabilities the telcos would like

added to the solutions. Once feedback has been gathered, the vendor sends out a list of the recurring

features and capabilities mentioned by telcos, at which point telcos have an opportunity to rate the

most important features. After the feedback is gathered, the vendor creates a prioritized list of features

and capabilities that its customers need. Using this information, Ericsson then incorporates this

feedback into its product roadmap, adding more complex capabilities as future product roadmap items

and easily addressable features as system updates. This thorough feedback process allows Ericsson

to not only ensure that it spends its R&D dollars wisely, but also ensures the vendor's solution remains

relevant and aligned with its customers' needs. This closed-loop feedback system has become a

differentiator for Ericsson, with its clients listing its well-aligned and clearly defined product roadmap

as one of the top benefits of working with the vendor.

Weaknesses

Limited footprint in Latin America: Although Ericsson has a strong global footprint overall, its

presence in Latin America has been somewhat limited, with only 9% of its revenue being generated in

the region. This is despite the fact that the region is experiencing a significant amount of growth;

Ovum predicts Latin America will generate $6bn in IT spend in 2020, growing at a CAGR rate of 3.9%.

Although Ericsson recently announced a transformation deal with Entel Chile and Peru, overall a lack

of penetration in this region means that the vendor is missing out on an opportunity to diversify its

footprint and capitalize on an increasing number of transformation projects being awarded in the

region. An increasing presence in Latin America is especially important as the competition in more

mature markets is reaching a saturation point.

Opportunities

Offer out-of-the-box digital solutions: Ericsson engages well with its client base and understands

the challenges and immediate needs of the telco. This enables it to align its products with market

trends and challenges. The vendor also states that a great deal of education and consulting is

required to provide customers with an understanding of the market and best practices. There is still a

huge learning curve for telcos trying to compete in the digital space and many will look to leading

vendors like Ericsson to provide them with guidance for what to do next. Ericsson has an opportunity

to leverage the insights gained from these client interactions, and offer prepackaged solutions based

on its billing and charging systems that also speak to specific use cases for the digital telco.

Threats

Competitive Asia-Pacific market biggest threat to Ericsson's market share: While Ericsson is

considered a leading vendor in many markets, its efforts to break into the Asia-Pacific market mean

that the vendor will be going up against Huawei, who has secured a large market share in the region.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 23

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

While Ericsson can be a real contender to Huawei in this region, it should also focus on strengthening

its position in markets such as the Americas, where Huawei has little to no market presence.

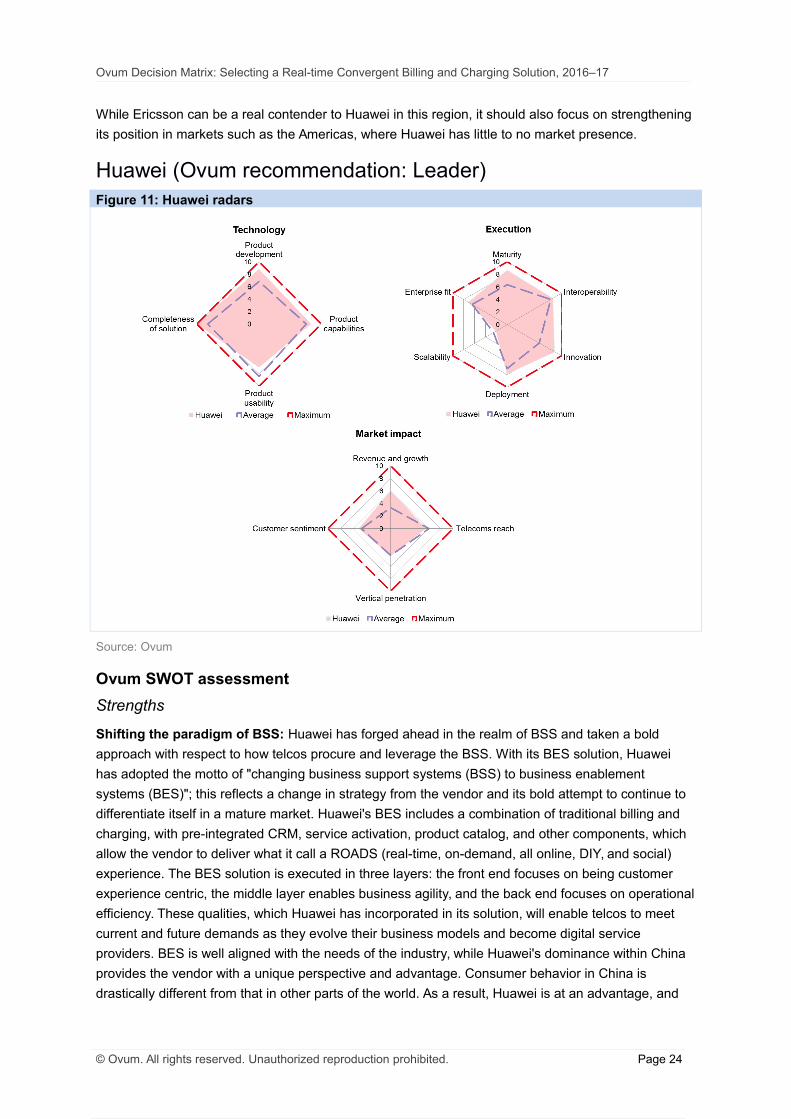

Huawei (Ovum recommendation: Leader)Figure 11: Huawei radars

Source: Ovum

Ovum SWOT assessment

Strengths

Shifting the paradigm of BSS: Huawei has forged ahead in the realm of BSS and taken a bold

approach with respect to how telcos procure and leverage the BSS. With its BES solution, Huawei

has adopted the motto of "changing business support systems (BSS) to business enablement

systems (BES)"; this reflects a change in strategy from the vendor and its bold attempt to continue to

differentiate itself in a mature market. Huawei's BES includes a combination of traditional billing and

charging, with pre-integrated CRM, service activation, product catalog, and other components, which

allow the vendor to deliver what it call a ROADS (real-time, on-demand, all online, DIY, and social)

experience. The BES solution is executed in three layers: the front end focuses on being customer

experience centric, the middle layer enables business agility, and the back end focuses on operational

efficiency. These qualities, which Huawei has incorporated in its solution, will enable telcos to meet

current and future demands as they evolve their business models and become digital service

providers. BES is well aligned with the needs of the industry, while Huawei's dominance within China

provides the vendor with a unique perspective and advantage. Consumer behavior in China is

drastically different from that in other parts of the world. As a result, Huawei is at an advantage, and

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 24

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

has been able to incorporate an array of features into its solution that its competitors have yet to

develop. Capabilities incorporated into the solution, such as supporting C2C business models, speak

specifically to the Chinese market. These capabilities also hold relevance in other markets and yet are

clearly ahead of the competition. The vendor has done an excellent job at leveraging its position as a

leader in the Chinese market, to develop capabilities and use cases that are relevant and

thought-leading throughout the industry.

Growing revenues suggests telco confidence: Huawei reported revenues of $60bn in 2015, with

$1bn estimated to be attributed directly to billing and charging. This boost in revenue and market

share suggests that telcos have growing confidence in Huawei's solution and its ability to support their

businesses as they make strategic upgrades to the BSS. Specifically, the vendor has been able to

secure a large number of new transformation projects and other large wins in the billing and charging

space over the last 12 months.

Weaknesses

Little emphasis on the impact of next-gen technologies on billing and charging systems:

Huawei has committed itself to becoming an enabler of next-generation technologies such as 5G,

NFV, SDN, cloud, IoT, as well as in other areas. However, the vendor's focus on next-generation

capabilities remains mainly on the network and connectivity aspects of these technologies. Its

roadmap currently lacks a plan to develop its billing and charging solutions to support and monetize

these next-gen capabilities, leaving the vendor in a vulnerable position as other vendors begin to act

on evolving their solutions.

Government restrictions in North America hinder global market share: Though Huawei's 2015

revenues were impressive, government restrictions in the Americas region, particularly in North

America, dilute the vendor's overall market impact.

Opportunities

Prepare billing and charging to support next-gen technologies: As Huawei continues to work

toward enabling next-generation technologies such as IoT and NFV and collaborating with telcos to

develop PoCs (proof of concepts), the vendor is in a strong position to concurrently invest in evolving

its billing and charging solutions and test them alongside its existing PoCs.

Develop use cases for BES: Although BES is a very strong technical solution, Huawei admits that it

requires telcos to undergo a paradigm shift. After launching BES in 2015, Huawei has been able to

deploy the solution with four telcos, with more contracts in the works. However, because of the

relative newness of the solution, Huawei will need to develop its customer use cases to prove the

effectiveness of the solution on the market. By building on its existing client base and recruiting

customers undergoing transformation projects, Huawei can easily win new contracts for BES.

Developing multiple use cases with compelling data will also allow the vendor to validate the success

of the solution.

Threats

Competitors are evolving the BSS: While Huawei offers a technically strong billing and charging

solution, its closest competitors are working on evolving their billing and charging solutions and

preparing proof of concepts to ensure that its systems can support the demands of emerging

technologies. Unless Huawei commits to a product roadmap for billing and charging that aligns with its

roadmap for its other business areas (such as in the networks and in IoT), the vendor will lose its

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 25

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

market share and will be adversely impacted in terms of its positioning as a billing and charging leader

in the coming years.

Netcracker (Ovum recommendation: Leader)Figure 12: Netcracker radars

Source: Ovum

Ovum SWOT assessment

Strengths

Strong end-to-end offering: Netcracker has developed a strong end-to-end solution for telcos. The

vendor's history as an NEP and OSS provider, as well as the backing it has from parent company

NEC, have all worked in Netcracker's favor and aided in its ability to provide a full suite solution

across BSS and OSS. Netcracker's billing and charging solution is incredibly fit for market. The

vendor has incorporated standard features such as real-time analytics, a unified product catalog, and

customer management into the solution. Capabilities such as dynamic pricing and quote bidding –

which allows end users to bid on the price they want to be charged for consuming data or minutes –

allow Netcracker to differentiate its solution in the market. Netcracker has continued to grow its BSS

footprint, winning a large number of new BSS contracts over the last 12 months, including 30 BSS

transformation projects.

Thought-leader on the next-gen telco: Netcracker's ongoing focus on being a thought-leader for

telcos puts it in a strong position to not only forge new relationships with telcos, but also allows the

vendor to focus on improving its billing and charging systems to support new requirements as they

emerge in the industry. The vendor has taken the lead on topics such as billing in the cloud, billing for

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 26

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

NFV, and other areas. This focus on looking ahead to next-generation capabilities provides the vendor

with foresight to make early improvements to its billing and charging solution and secure key wins

very early on as the market shifts towards new trends.

Weaknesses

Still establishing itself as a major player in the BSS domain: Netcracker's history and deep roots

within the OSS sector, as well as its backing from parent company NEC, have naturally put OSS and

networks at the forefront of the vendor's business. However, over the last eight years, the vendor has

begun increasing its focus on developing its BSS solution. The vendor entered the charging space in

2008 when it was acquired by NEC, and began offering its billing solution in 2012 after it acquired the

Convergys billing solution. As a result of entering the billing and charging space relatively late

compared to its competitors, Netcracker has had to work at establishing itself as a competitor in the

market. However, recent billing wins and BSS transformation project wins are helping Netcracker to

improve its overall standing as a billing and charging vendor.

Opportunities

Leverage PoCs to improve solution: Netcracker is doing extensive work with telcos to develop

PoCs around NFV and SDN. The vendor is in an excellent position to develop relevant solutions and

use cases with its billing and charging solutions for NFV and SDN. Netcracker can leverage the PoCs

it is running for NFV and SDN to test new billing and charging enhancements and capabilities at the

same time.

Threats

Competitors are focusing more on BSS: Netcracker's biggest competitors, such as Amdocs and

Huawei, are focusing more on evolving the billing and charging solutions to support next-generation

technologies such as IoT and payments, and new business models. To ensure it can remain

competitive in the market, Netcracker will need to continue to develop new and innovative use cases

for its billing and charging solution. The vendor is well positioned to provide relevant use cases of its

billing and charging solution to support its NFV and SDN efforts, and can easily leverage these

capabilities and become a market leader.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 27

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

Oracle (Ovum recommendation: Leader)Figure 13: Oracle radars

Source: Ovum

Ovum SWOT assessment

Strengths

"Smart" features allow telcos to fully monetize data: Oracle Communications Billing and Revenue

Management (BRM) is the vendor's pre-integrated billing and charging product. BRM includes billing

and charging along with settlement, partner management, interconnect, and data management, and is

also available as a fully virtualized product. Within BRM, Oracle has evolved its solution and Pricing

Design Center (i.e. product catalog) to include "Smart" features known as "Smart Add-ons." The

Smart Add-ons feature allows telcos to create relevant customer offers in real time to fully monetize

customer data. The Smart Add-ons feature includes an array of use cases such as speed boosters,

data sharing, roaming packs, and social media packs, among others. Specifically, the feature

addresses a challenge that many telcos are facing with low ARPU rates, and provides a single

platform for them to monetize data by creating contextual pricing and offers in real time.

Weaknesses

Limited product differentiation: While Oracle has developed a series of "smart add-ons" to help

telcos monetize data, this feature has become a common and standard offering among billing and

charging vendors. Additionally, while BRM can complete as many as 3 billion charges per hour, the

product itself has few other differentiating capabilities. As a large software vendor with market share

across several industries, Oracle has the cross-industry insight that should afford it both the foresight

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 28

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

and ability to make more innovative improvements to its billing and charging products. Oracle states

that its approach is to develop products from a horizontal perspective so that they can be used in any

industry; however, this type of development goes against the preferences of many telcos. Telcos are

showing preference to telco-centric solutions, which are developed with the telco industry's specific

pain points in mind. Furthermore, in a recent Ovum survey, only 11% of telcos stated that large

software providers were likely to be their vendor of choice when selecting a new billing and charging

solution. Thus it is imperative for Oracle to incorporate differentiating capabilities in its solution to

continue to win telco business.

Opportunities

Leverage cross-industry expertise to enhance telco offering: As a large software vendor serving

more than 20 industries, Oracle has an opportunity to leverage its cross-industry expertise to

strengthen its positioning in the telecoms space. While the vendor has an extensive partner

ecosystem, it also relies heavily on these partners to leverage BRM and offer industry-specific

solutions to telcos. As telcos explore new opportunities in other industries and seek out new vendors

to award contracts to, Oracle will need to demonstrate its ability to provide off-the-shelf and

prepackaged options that telcos can quickly leverage to address a business challenge. Oracle's

competitors are creating off-the-shelf products to specifically address telcos' pain points, such as IoT

monetization platforms, digital BSS platforms, and other solutions. By leveraging its cross-industry

experience and offering prepackaged, off-the-shelf solutions for telcos, Oracle can fight off the

preconceived notions about large software vendors competing in the telecoms space and improve its

overall market positioning.

Threats

Telcos prefer telco-centric vendors: According to an Ovum survey of telco vendor preferences and

a customer feedback survey, nearly 90% of telcos prefer to award contracts to vendors whose core

focus is within the telecoms industry. For Oracle, whose roots are not inherently within the telecoms

industry, this poses the biggest threat to the vendor's overall positioning. As such, it is important for

the vendor to continuously invest in evolving its solution and develop innovative use cases to maintain

its position as a market leader.

Competitors are experiencing revenue growth: While Oracle boasts a solid billing and charging

solution, its declining revenue poses a large threat to the vendor's positioning. While Oracle does not

break down its reported revenues by industry or by product, the vendor's overall revenues were down

5% year on year in 2015. This casts an unfavorable light on the vendor, particularly as vendors within

the telecoms space are reporting significant growth. Regardless of what the vendor's actual telecoms

revenues are, the perception that Oracle's revenues are declining suggests that the vendor's market

impact is waning. Telcos will look to partner with trusted vendors when awarding new contracts,

particularly those for long-term BSS transformation projects.

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 29

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

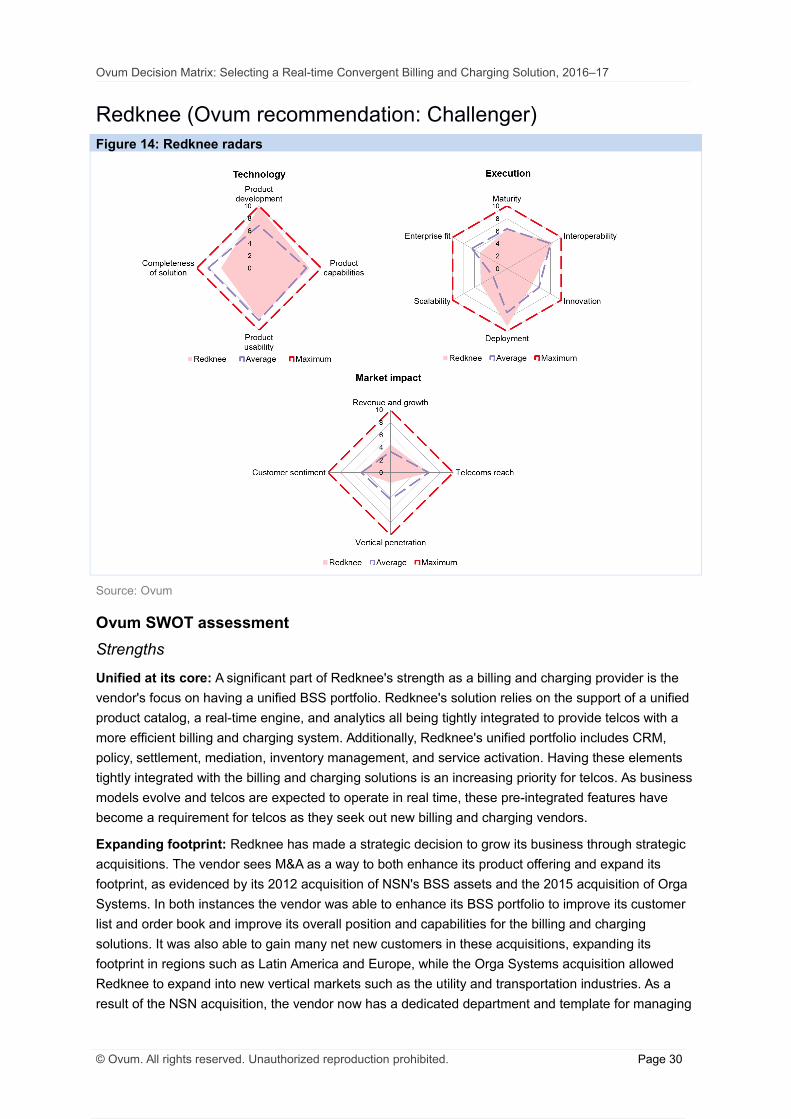

Redknee (Ovum recommendation: Challenger)Figure 14: Redknee radars

Source: Ovum

Ovum SWOT assessment

Strengths

Unified at its core: A significant part of Redknee's strength as a billing and charging provider is the

vendor's focus on having a unified BSS portfolio. Redknee's solution relies on the support of a unified

product catalog, a real-time engine, and analytics all being tightly integrated to provide telcos with a

more efficient billing and charging system. Additionally, Redknee's unified portfolio includes CRM,

policy, settlement, mediation, inventory management, and service activation. Having these elements

tightly integrated with the billing and charging solutions is an increasing priority for telcos. As business

models evolve and telcos are expected to operate in real time, these pre-integrated features have

become a requirement for telcos as they seek out new billing and charging vendors.

Expanding footprint: Redknee has made a strategic decision to grow its business through strategic

acquisitions. The vendor sees M&A as a way to both enhance its product offering and expand its

footprint, as evidenced by its 2012 acquisition of NSN's BSS assets and the 2015 acquisition of Orga

Systems. In both instances the vendor was able to enhance its BSS portfolio to improve its customer

list and order book and improve its overall position and capabilities for the billing and charging

solutions. It was also able to gain many net new customers in these acquisitions, expanding its

footprint in regions such as Latin America and Europe, while the Orga Systems acquisition allowed

Redknee to expand into new vertical markets such as the utility and transportation industries. As a

result of the NSN acquisition, the vendor now has a dedicated department and template for managing

© Ovum. All rights reserved. Unauthorized reproduction prohibited. Page 30

Ovum Decision Matrix: Selecting a Real-time Convergent Billing and Charging Solution, 2016–17

future M&As. This reiterates that Redknee is committed to using M&As to maintain its positioning and

make strategic improvements to its offering.

Weaknesses

Limited overall growth: Redknee's overall revenue is down year on year at $223m in 2015, down

from $258m in 2014. This decline could be a cause for concern as telco IT spend and vendor

revenues are trending upward. It is also important to note that this initial decline in revenue can likely

be attributed to the vendor's acquisition of Orga Systems at the beginning of 2015; a similar dip in

revenue occurred after the acquisition of NSN in 2012 and the vendor was able to recover. While this

acquisition may have adversely impacted the vendor's revenues for the year, the acquisition was seen

as a strategic move made to enhance the vendor's overall BSS offering and market positioning. The

vendor will need to recover its revenue and show organic growth during the 2016 fiscal year in order

to improve its market positioning.

Opportunities

Develop use cases for Smart Pricing: Redknee's Smart Pricing feature, which incorporates big

data, customer behavior, and other factors to provide personalized pricing on the fly, is a

differentiating feature to its charging system and has the potential to give the vendor a competitive

edge. While the solution is innovative, Redknee has yet to secure a contract to launch the capability

within a telco. Securing wins for this feature and developing use cases will allow Redknee to

differentiate itself more within the billing and charging space.

Threats

Holes in BSS portfolio make it vulnerable against larger players: As telcos award new contracts