IAS 37 - Provisions, Contingent Liabilities and Contingent Assets

CONTINGENT BUSINESS INTERRUPTION IN THE MANUFACTURING INDUSTRY

INS001

SPEAKERS:

• Andrew Bourne, Partner, BDO Canada LLP

• Paul McGuire, Treasury Manager, Martinrea International Inc.

1

Introduction of Speakers

Paul McGuire

• Treasury Manager of Martinrea International Inc.

• Joined the company in 2007

• Responsible for global treasury operations, pension committee and a plan trustee and managing the company’s global insurance program

Andrew Bourne

• Partner at BDO Canada LLP Financial Advisory Services, Investigative & Forensic Accounting

• Areas of practice include damage quantification, fraud investigation, loss of profit claims, employee theft and fraud

• Insurance claims experience in business interruption losses, stock loss, extra expense and physical damage

2

1. Understanding CBI Coverage (and the difference between typical Business Interruption coverage and Contingent Business Interruption coverage)

2. Key factors to consider in determining whether CBI Coverage is appropriate for your organization

3. How to determine the key CBI exposures for your business

4. How to quantify these exposures, and sell it to your organization

Overview of Key Learning Objectives

3

Introductory CBI Claims Scenario

4

CBI Claim Scenario

3rd Party

Supplier

Operating

Facility A

Operating

Facility B

Customer

Facility ACustomer

Facility B

50% 50%

50% 50%100%

Note: % represent distribution of product through tiers of production

Scenario: 3rd party supplier experiences a catastrophic fire, shutting down

production for 12 months. 5

Fire

Introduction to CBI

6

Overview of CBI Coverage

Typical Business Interruption Coverage

• Extension of property policy. Losses stemming from damage sustained from a covered peril at a location insured under your policy.

• Subject to all exclusions in policy

Contingent Business Interruption Coverage

• Extension of business interruption coverage, same exclusions apply

• Main difference – loss occurs at a location not insured under your policy.

7

Overview of CBI Coverage (continued)Different ways CBI can be included in the policy

• Named locations vs. unnamed locations

• Direct vs. indirect locations (Tier 1 / Tier 2 locations)

What types of locations/businesses can be covered?

• Suppliers

• Customers

• Leader (or Magnet) Properties

8

Does your company need CBI Insurance?

9

Supply ChainCustomer Base

Vertical

Integration

Reliant on

3rd Party

Suppliers

Sales to

Openly

Traded

Commodity

Market

Reliant Upon

3rd Party

Customer for

Sales/

Distribution

Examining Different Claims Scenarios – Does CBI Coverage Apply?

10

Scenario A

Plant A

Supplier

Location

Port

Scenario A: There is an explosion at a supplier location that supplies raw

materials to your company’s manufacturing facilities. Does CBI coverage

apply?

Plant B

How would this situation change if the supply disruption was a result of a

strike at the port, impacting the transport of goods?11

Strike

Explosion

Scenario B

Plant

Customer

Location

3rd Party

Location

Scenario: A landslide at an adjacent 3rd party location causes temporary

loss of access to your plant, which impacts sales temporarily. This 3rd party

location is not affiliated with your operations. Does CBI coverage apply?12

Landslide

Scenario C

Plant

Customer

Civil Authority

Declaration

Scenario: A Civil Authority Declaration temporarily impacts access to your

company’s manufacturing facility, which reduces sales to customers. Does

CBI coverage apply?

13

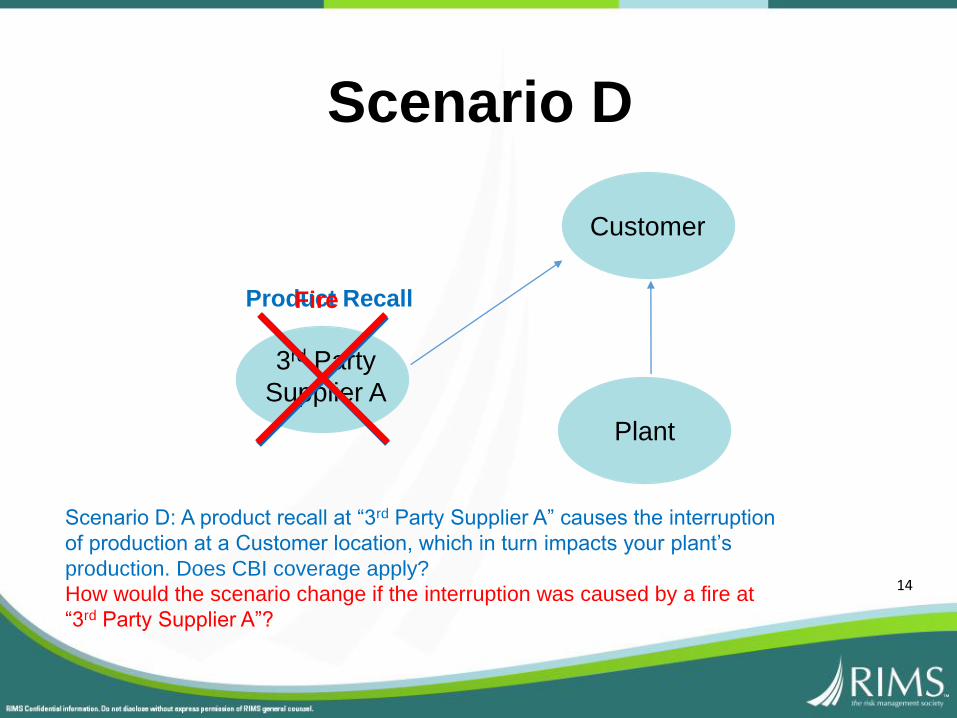

Scenario D

Plant

Customer

Scenario D: A product recall at “3rd Party Supplier A” causes the interruption

of production at a Customer location, which in turn impacts your plant’s

production. Does CBI coverage apply?

3rd Party

Supplier A

How would the scenario change if the interruption was caused by a fire at

“3rd Party Supplier A”?

14

Product RecallFire

Approach to CBI Exposure Study

15

Five Risk Management Process Steps - CBI1. Identify the Risk

• Is my organization exposed as a result of 3rd party suppliers/customers?

2. Analyze the Risk• Detailed supplier/customer mapping

3. Evaluate the Risk• Quantify potential exposure

4. Treat the Risk• Determine, as an organization, how best to approach the risk

• Insurance

• Disaster Recovery Plan

5. Monitor the Risk• Continue to evaluate and monitor 16

Determining CBI Exposure –Supplier Analysis

Raw Material A

Manufacturing

Facility

Raw Material B Raw Material C

1 location

source for raw

materials

Sourcing materials

from 10 locations

Sourcing materials

from 100 locations17

Determining CBI Exposure –Customer AnalysisTwo ends of the spectrum – where does your company fit in?

1) Heavily reliant upon customer 2) No reliance upon customer

Plant A Plant B

One Single

Customer

Location

Plant A

Plant B

Plant C

Open Market

Trading

18

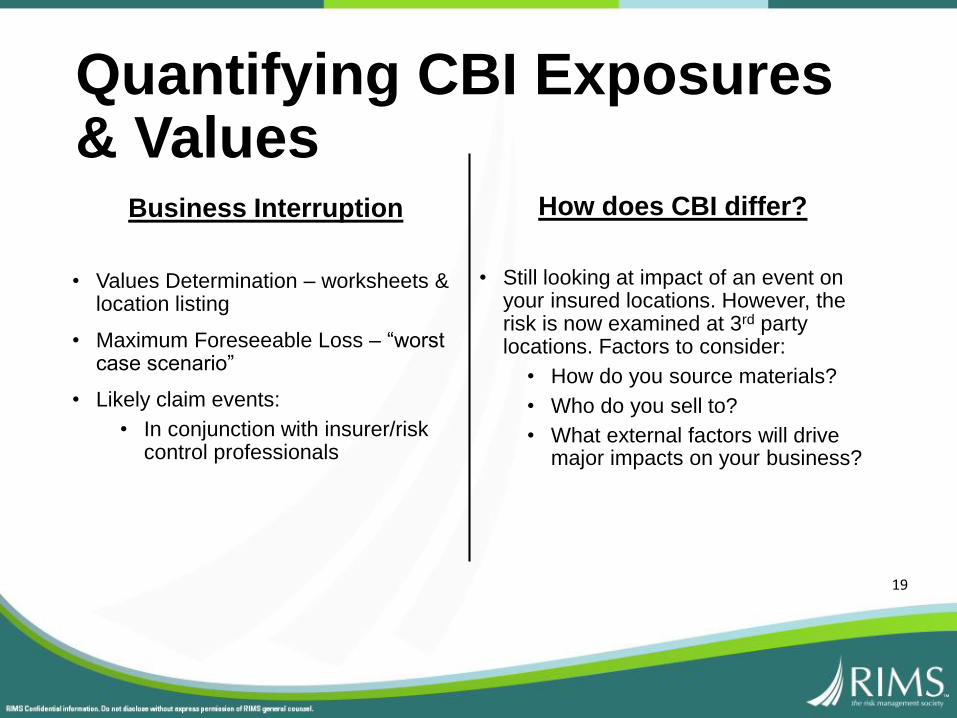

Quantifying CBI Exposures & Values

Business Interruption

• Values Determination – worksheets & location listing

• Maximum Foreseeable Loss – “worst case scenario”

• Likely claim events:

• In conjunction with insurer/risk control professionals

How does CBI differ?

• Still looking at impact of an event on your insured locations. However, the risk is now examined at 3rd party locations. Factors to consider:

• How do you source materials?

• Who do you sell to?

• What external factors will drive major impacts on your business?

19

Quantify the Risk –Sample Case Study

20

CBI Exposure Case Study

$100 Million

BI Exposure

1 Customer Location

75% of Margin

Multiple Customers

25% of Margin

1 Supplier Location

Feeding Essential Raw

Material

Multiple Suppliers

Feeding Remaining Raw

Materials

21

What is your CBI exposure?

Potential CBI Exposure QuantificationWhat is the maximum foreseeable loss based on a 12-month downtime at the supplier location?

Loss From Supplier Downtime:

• 1st month: use of inventory: $0 Million

• Months 2 to 3: 100% down: $17 Million

• Months 4 through 12: use of new

supplier at extra cost: $10 Million

Total Loss: $27 Million22

Potential CBI Exposure QuantificationWhat is the maximum foreseeable loss based on a 12-month downtime at the customer location?

Loss From Customer Downtime

• ½ of volume to be sold on intermediate

market at 50% lower margin: $18.8 Million

• ½ of profit to main customer lost: $37.5 Million

Total Loss: $56.3 Million

23

Main Considerations in Quantification

• What is your company’s maximum foreseeable loss?

• What proportion of your business will be impacted?

• What mitigation steps can be undertaken, and how will these steps impact raw material costs or customer margins?

• A detailed supplier and customer analysis is required.

24

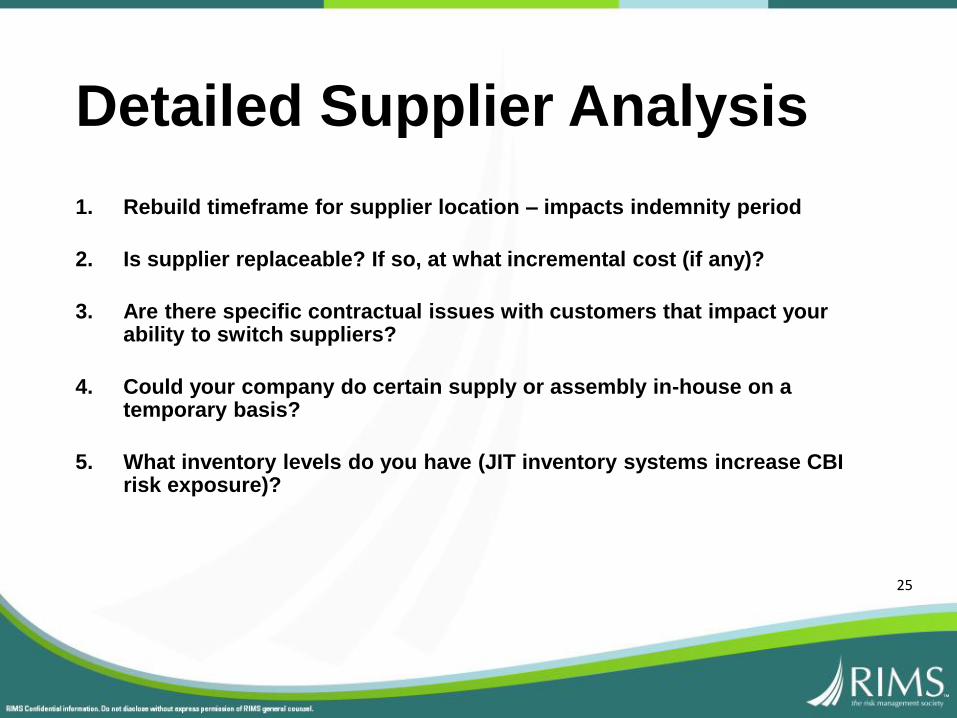

Detailed Supplier Analysis

1. Rebuild timeframe for supplier location – impacts indemnity period

2. Is supplier replaceable? If so, at what incremental cost (if any)?

3. Are there specific contractual issues with customers that impact your ability to switch suppliers?

4. Could your company do certain supply or assembly in-house on a temporary basis?

5. What inventory levels do you have (JIT inventory systems increase CBI risk exposure)?

25

Detailed Customer Analysis

1. Rebuild timeframe for customer location – impacts indemnity period

2. Does customer have other locations?

3. Is your product essential in the marketplace? Will other customers try to fill the void?

4. Mitigation potential – can sales be made on the intermediate market at a reduced price/margin?

26

CBI Values & Exposure Analysis – From a Risk Manager’s Perspective

27

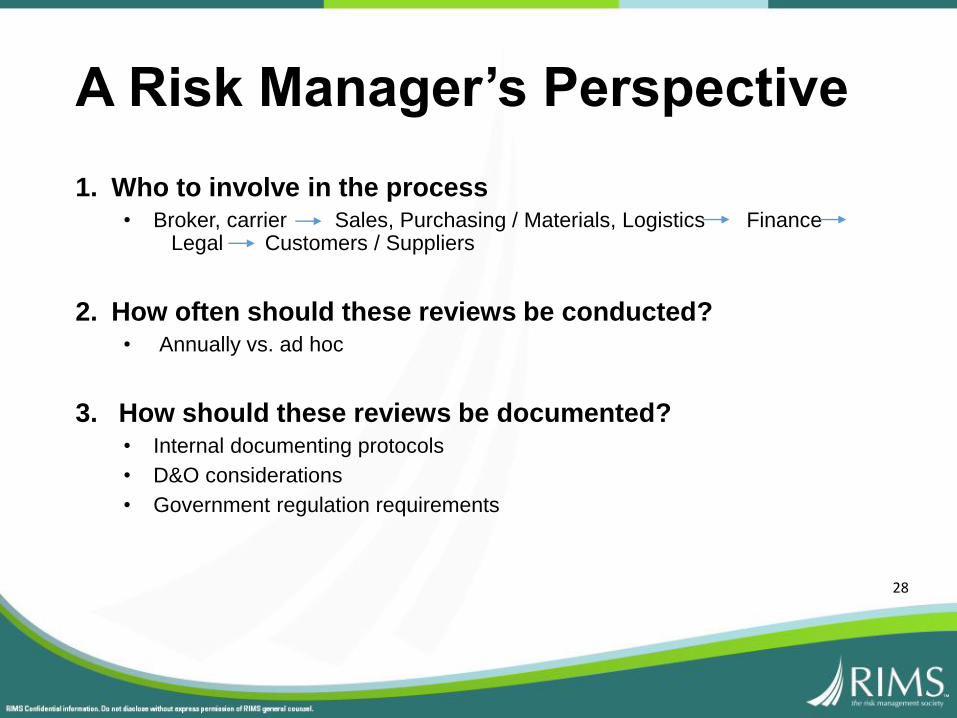

1. Who to involve in the process• Broker, carrier Sales, Purchasing / Materials, Logistics Finance

Legal Customers / Suppliers

2. How often should these reviews be conducted?• Annually vs. ad hoc

3. How should these reviews be documented?• Internal documenting protocols

• D&O considerations

• Government regulation requirements

A Risk Manager’s Perspective

28

4. Once the exposure study is done, what are the next steps?• Underwriting Considerations

• Inclusions / exclusions considerations (Endorsements)

5. How to sell coverage to your internal team/Cost Benefit Considerations

• What is management’s view of the trade off between premium and the underlying exposure?

• How would a CBI event impact the organization's financial strength?

• How are your competitors, customers, suppliers managing the risk?

A Risk Manager’s Perspective (continued)

29

1. Understanding CBI Coverage (and the difference between typical Business Interruption coverage and Contingent Business Interruption coverage)

2. Key factors to consider in determining whether CBI Coverage is appropriate for your organization

3. How to determine the key CBI exposures for your business

4. How to quantify these exposures, and sell it to your organization

Overview of Key Learning Objectives

30

Question Period

31