Digital Experience: Are Brands Meeting Consumer Expectations?

CONSUMER TRENDS SHAKE BRANDS!

AND THE CASE FOR ‘SHOPPER FIRST’

Peter Kirby

Director of Consulting, Kantar Retail

Incorporating TNS Retail & Shopper

INTRODUCTION

There can be little doubt that the industry we work in is being

reshaped by an unprecedented period of turbulence

Shifts in the global economy, demographics, technology,

shopper trends and retailer strategy are impacting the way

in which Brands are able reach the end consumer

While there is clearly a great deal of inter-connectivity, we

have attempted to isolate the 12 most pertinent shifts

For each trend, we have highlighted the impact on retail

customers, together with implications for suppliers

The precise impact might vary by category, but we believe that

most of these trends will impact most suppliers in some way

2

Incorporating TNS Retail & Shopper

THE 12 MOST PERTINENT SHIFTS

HAVE & HAVE

NOTS

EUROPE'S

AGING

POPULATION

RELIGIOUS

POLARISATION IMMIGRATION URBANISATION ECOMMERCE

MOBILE PROMOTIONAL

RELIANCE

CUSTOMER

GROWTH

DIVERGENCE

BIG BOX VS

SMALL BOX AMAZON

RISE OF THE

DISCOUNTERS

3

Incorporating TNS Retail & Shopper

Why do we think

‘Shopper’ is the

most important

perspective?

4

Incorporating TNS Retail & Shopper

1. SHOPPERS ARE INEXTRICABLY LINKED WITH CONSUMERS

Consumers become shoppers at the point of decision

‘ Shoppers only shop to fulfil the

needs of a consumer’

5

Incorporating TNS Retail & Shopper

2. SHOPPERS PROVIDE THE FOCUS, COMMON AIM & PURPOSE FOR SUPPLIER / RETAILER COLLABORATION

6

Incorporating TNS Retail & Shopper

BECAUSE WE KNOW...

75 % of all decisions are made

AT THE SHELF

AT THE MOMENT

OF TRUTH

60-80% of shoppers are ‘Decided’

BEFORE THE SHELF

7

Incorporating TNS Retail & Shopper

3. SHOPPER INSIGHT MUST MIGRATE ‘UPSTREAM’ FROM MERELY ‘SHELF MARKETING’ INTO THE FULL (& DYNAMIC) PATH TO PURCHASE

Brand marketing

Customer or Shopper marketing

8

Incorporating TNS Retail & Shopper

THE 5 MOST PERTINENT SHIFTS

EUROPE'S

AGING

POPULATION URBANISATION ECOMMERCE PROMOTIONAL

RELIANCE

HAVE & HAVE

NOTS

9

Incorporating TNS Retail & Shopper

HAVES / NOTS WHAT SUPPLIERS & RETAILERS ARE DOING ABOUT THIS

HAVES

Innovating in

premium brands

Provide Time / Convenience

driving solutions to shoppers

Explore super-premium

channels

HAVE NOTS

Entry level price points – new

O/L value ranges

Economy variants / sub

brands

Consider the Discount

channel opportunity

10

Incorporating TNS Retail & Shopper

AGEING POPULATION WHAT SUPPLIERS & RETAILERS ARE DOING ABOUT THIS

Prioritize neighbourhood, pharmacies /

drugstores and online

Develop lifestage-specific products

Legible printing and easy-to-open

packaging

Enhance & improve shopping

experience for older shoppers

Font size up by 20%;

colour contrast enhanced

to account

for ageing shopper base

11

Incorporating TNS Retail & Shopper

URBANISATION: WHAT SUPPLIERS & RETAILERS ARE DOING ABOUT THIS

Sharpen ranging strategies to win on the smaller

shelves in the convenience channel

Target new purchase and consumption occasions –

such as commuting, in-office and vending

Tailor pack size and format to better serve immediate

consumption and portability

Making products easier to identify, find and purchase

in the smaller, busier store environment

12

Incorporating TNS Retail & Shopper

PROMOTIONAL RELIANCE WHAT ARE SUPPLIERS & RETAILERS DOING ABOUT THIS

“There is nothing proprietary in price promotions.

We believe promotions win quarters but true innovation

wins decades” - P&G

Collaborative (retailer/category captain) promotional

planning in line with agreed Category Vision

In-house data tools and capability o drive efficiency

and effectiveness of trade spend

Offering retailers npd exclusivity, differentiation via

contests or engagement with CSR objectives

Value added consumer mechanics to drive

engagement e.g. Limited edition SKUs, contests,

social media and direct-to-consumer

loyalty schemes

13

Incorporating TNS Retail & Shopper

ECOMMERCE WHAT ARE SUPPLIERS & RETAILER DOING ABOUT THIS

Optimising current digital presence to create ‘one

click away’ conversion

Building & integrating ecommerce excellence into existing Customer teams

Defining & Understanding what Amazon can do for you

Building links between e commerce (Sales) and Equity commerce (Brand building)

Building a collaborative, learning e commerce

agenda with bricks & mortar customers

14

Incorporating TNS Retail & Shopper

SUMMARY MESSAGES

– ‘Change will never be this slow again’. Intel founder , Gordon

Moore, 1965

– Putting Shopper at the heart of your strategies embraces

both upstream (Consumer) and downstream (Customer)

interests

– With increasing ‘Points of Decision’ along the Path to

Purchase there will be ever greater need for insight

– Why (not) here, Why (not) Now?!

– What are the implications of these dynamics for your own

brands, business, customers and channels?

15

Incorporating TNS Retail & Shopper

Contact:

Peter Kirby

Director of Consulting

Kantar Retail

M:+44 7795 013816

www.kantarretail.com

www.kantarretailiQ.eu

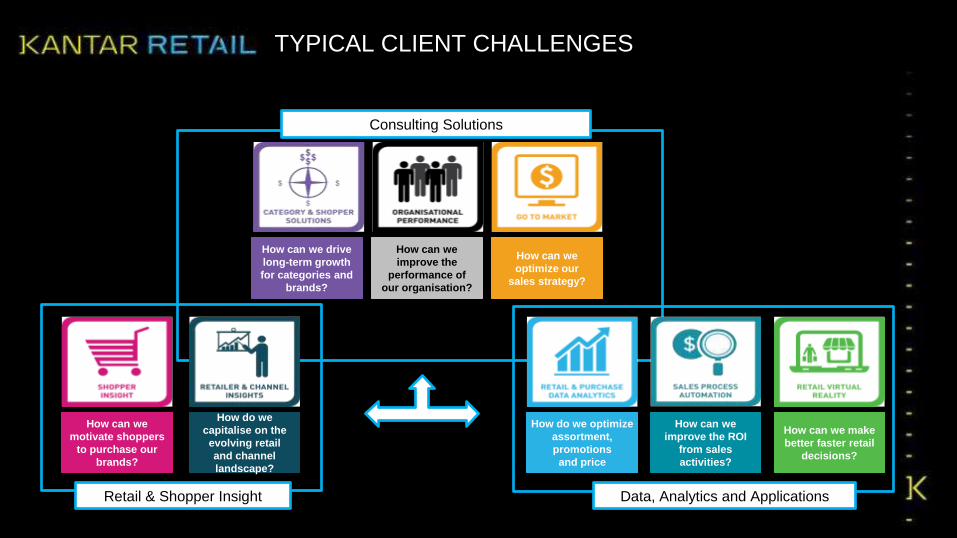

How can we

motivate shoppers

to purchase our

brands?

How do we

capitalise on the

evolving retail

and channel

landscape?

Retail & Shopper Insight

How do we optimize

assortment,

promotions

and price

How can we

improve the ROI

from sales

activities?

How can we make

better faster retail

decisions?

Data, Analytics and Applications

How can we drive

long-term growth

for categories and

brands?

How can we

improve the

performance of

our organisation?

How can we

optimize our

sales strategy?

Consulting Solutions

TYPICAL CLIENT CHALLENGES