Consulting Services for Technical Assistance on Study for ... for Rural Communications in... ·...

64

REPUBLIC OF MOZAMBIQUE MINISTRYOF TRANSPORTS AND COMMUNICATIONS MOZAMBIQUE’S COMMUNICATIONS NATIONAL INSTITUTE FINAL REPORT Written by: Luís Rego and Hermínia Fernandes-Samuel MAPUTO, OCTOBER 2017 Consulting Services for Technical Assistance on Study for Rural Communications Viability in Mozambique

-

Upload

duongduong -

Category

Documents

-

view

213 -

download

0

Transcript of Consulting Services for Technical Assistance on Study for ... for Rural Communications in... ·...

REPUBLIC OF MOZAMBIQUE

MINISTRYOF TRANSPORTS AND COMMUNICATIONS

MOZAMBIQUE’S COMMUNICATIONS NATIONAL INSTITUTE

FINAL REPORT

Written by: Luís Rego and Hermínia Fernandes-Samuel

MAPUTO, OCTOBER 2017

Consulting Services for Technical Assistance on Study for Rural Communications Viability in

Mozambique

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 0

Table of Contents List of Abbreviations and Acronyms .......................................................................................... 3

1. Executive Summary ........................................................................................................... 5

2. Methodology .................................................................................................................... 8

3. Political and Economic Environment ................................................................................ 10

3.1. Political Environment ............................................................................................... 10

3.2. Economic Environment ............................................................................................ 11

3.3. Demographics.......................................................................................................... 13

3.4. Government Programs and Projects ........................................................................ 14

3.4.1. Five-YearGovernmentProgram 2015-2019 ....................................................... 14

3.4.2. GovernmentProjects in ICTs ............................................................................. 15

3.4.3. Electronic Government Network (GovNet) ....................................................... 15

3.4.4. Government Portal .......................................................................................... 17

3.4.5. System of Financial Administration of the State (e-SISTAFE) ............................. 17

3.4.6. Programs of Community Multimedia Centers (CMCs) ....................................... 17

3.4.7. Internet in Schools ........................................................................................... 17

3.4.8. Electronic Currency Platform............................................................................ 18

3.4.9. Project of National Network of Higher Education and Research (MoRENet) ..... 18

4. Doing Business in Mozambique ....................................................................................... 19

4.1. Investment Guarantee and Tax Incentives ....................................................... …….20

4.1.1. Registration Process ......................................................................................... 20

4.2. Paying Taxes ............................................................................................................ 21

4.2.1 Types of Taxes …………………………………………………………………………………………………22

4.3. Guarantees to Investment ....................................................................................... 23

4.3.1. Investment Guarantees .................................................................................... 23

4.3.2. Investment Incentives ...................................................................................... 24

4.3.3. National and Foreign Direct Investment ........................................................... 25

4.4. Access to Land ......................................................................................................... 25

4.5. Enforcing Contracts ................................................................................................. 25

5. Telecommunication Sector Analysis ................................................................................ 27

5.1. Policy and Regulatory Framework ............................................................................ 27

5.1.1. Telecommunications Market Regulator ............................................................ 27

5.1.2. Licensing .......................................................................................................... 28

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 1

5.1.3. Network sharing .............................................................................................. 28

5.1.4. Interconnectivity .............................................................................................. 30

5.1.5. Fair Competition .............................................................................................. 30

5.1.6. Quality of Service ............................................................................................. 31

5.1.7. Spectrum Management ................................................................................... 31

5.1.8. Telecommunications Taxes and Fees ................................................................ 32

5.1.9. Spectrum Charges ............................................................................................ 32

5.1.10. Universal Service Access Fund (USAF) .............................................................. 32

5.1.11. Consumer protection ....................................................................................... 34

5.1.12. Remove Market Barriers .................................................................................. 35

6. Market Structure ............................................................................................................. 36

6.1. Voice Market ........................................................................................................... 36

6.1.1. Fixed Market .................................................................................................... 36

6.1.2. Mobile Market ................................................................................................. 37

6.2. Broadband and Internet Market .............................................................................. 39

6.2.1. Fixed Market .................................................................................................... 39

6.2.2. Mobile Market ................................................................................................. 40

6.3. Market Revenue and Investment ............................................................................. 40

6.3.1. Revenue of Mobile Market............................................................................... 40

6.3.2. Revenue of Fixed Market ................................................................................. 40

6.3.3. Investment of Mobile Market .......................................................................... 41

6.3.4. Investment of Fixed Market ............................................................................. 41

6.4. Market Players ........................................................................................................ 42

6.5. Backbone Infrastructure .......................................................................................... 43

6.6. International Connectivity ....................................................................................... 45

6.7. Middle-Mile (Backhaul) Infrastructure ..................................................................... 47

6.8. Access Networks ...................................................................................................... 47

6.9. International Services .............................................................................................. 47

7. Merging State-Owned Operating Companies ................................................................... 48

8. Reforming the Market ..................................................................................................... 49

9. Business Opportunity ...................................................................................................... 49

9.1. Rural Area................................................................................................................ 49

9.2. Urban Area .............................................................................................................. 50

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 2

9.3. Potential Financing and Funding Partners for Rural Telecommunications Infrastructure ...................................................................................................................... 50

10. Barriers to Investment..................................................................................................... 51

11. Conclusion and Recommendation ................................................................................... 53

11.1. Conclusion ........................................................................................................... 53

11.2. Recommendation ................................................................................................ 53

12. References ...................................................................................................................... 54

13. Annexures ....................................................................................................................... 56

13.1. Annexure I: Bureaucratic and Legal Steps to Incorporate and Register a New Firm .......... 56

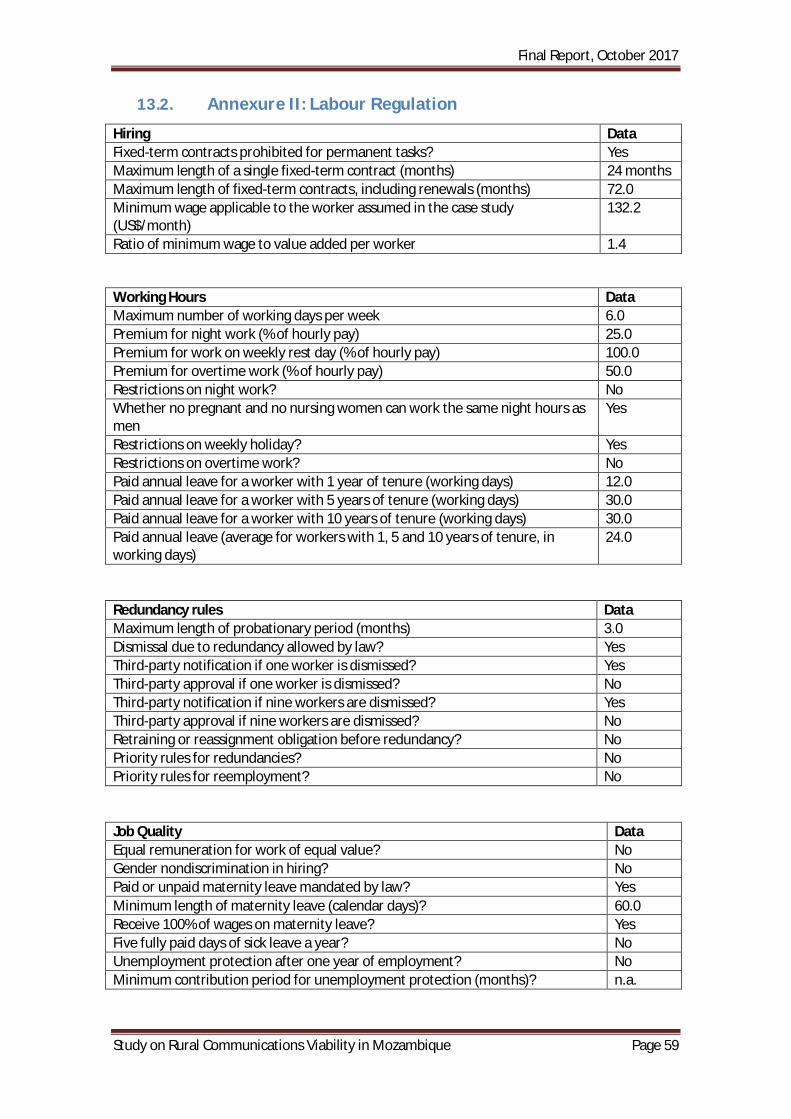

13.2. Annexure II: Labour Regulation ............................................................................ 59

13.3. Annexure III: Licensing and Numbering Fees ....................................................... 60

13.4. Annexure IV: Spectrum Charges and Fee Formula ................................................ 60

13.5. Annexure V: Example of Invitation for Bids .......................................................... 61

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 3

List of Abbreviations and Acronyms

CAGR Compound Annual Growth Rate

CMC CommunityMultimediaCenters

CPI Centro de Promoção de Investimentos

EASSy Eastern Africa Submarine Cable System

e-SISTAFE Electronic System of Financial Administration of the State

FRELIMO Frente de Libertação de Moçambique

FTTP Fiber to thePremises GAZEDA Gabinete das Zonas Económicas de Desenvolvimento

GDP Gross Domestic Product

GNI Gross National Income

GovNet Electronic Government Network

HSPA High Speed Packet Access

ICC International Chamber of Commerce

ICE Imposto de ConsumoEspecífico

ICT Information and Communication Technology

ICSID International Centre for Settlement of Investment Disputes

INCM Instituto Nacional das Comunicações de Moçambique

INE Instituto Nacional de Estatística

INTIC Instituto Nacional de Tecnologias de Informação e Comunicação

IMF International Monetary Fund

ISP Internet Service Provider

IRPC Imposto sobre Rendimento de Pessoas Colectivas

IRPS Imposto sobre o Rendimento de Pessoas Singulares

IVA Imposto de Valor Acrescentado

LTE Long TermEvolution

Mcel Moçambique Celular

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 4

MCT Ministério de Ciência e Tecnologia (MinistryofScienceandTechnology)

MIGA Multilateral Investment Guarantee Agency

MoRENet Mozambique Research and Education Network

MOTRACO Mozambique Transmission Company

MZN Mozambique’s Metical

OPIC Overseas Private Investment Corporation

PPP Public-private partnerships QoS Quality of Service

RENAMO Resistência Nacional de Moçambique

SADC Southern Africa DevelopmentCommunity

SAFE/SAT-3 South Atlantic and Far Eastern SEACOM Submarine Cable System

2G Second Generation

SISA Imposto Aplicável a Transacções de Propriedades Imobiliárias

SME Small and Medium Sized-Enterprises

STM SynchronousTransferMode TDM Telecomunicações de Moçambique

3G Third Generation

TV Television

UNICEF United Nations Children's Fund

USAF Universal Service Access Fund

VAT Value Added Tax

VSAT Very Small Aperture Terminal

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 5

1. Executive Summary

The purpose of this study is to access the Implementation of Rural Communications in

Mozambique.The natural and historical saying on the topic is that the return on the

investment in such areas is length if any, despite the huge and visible opportunities.

The reality is that investors might be faced with unexpected challenges, lack of adequate roads,

lack of government support just to name few that, if not accounted and considered in

projection phase can lead any investment into failure.

Considering Mozambique’s landscape in terms of the demographic distribution of the near 27

million inhabitants, 70% in rural areas and 30% in urban areas, one actually questions why is

the level of investment still so low in rural areas considering the reasons for investing so strong?

Studies confirm that Mozambique is one of the 20 Markets of the future that will offer the

most opportunities for consumer goods companies globally. The country is one of the fastest

growing and most promising economies in sub-Saharan Africa.

The facts are that, Mozambique has both comparative and competitive advantages, which are

supplemented with good governance, as well:

Mozambique as a strategic Location (as a gateway to SADC): Providing infrastructures

that give access to land-locked SADC Countries (Ports, Railways, Pipeline and Roads);

Rich and diverse natural resources: Vast land reserves, mineral resources, water and

diverse cultural and historical heritage;

Abundant labor force: availability of competitive, educated and easily trainable labor

force;

Increased investment into infrastructures: infrastructure development is one of the

country’s top priorities and public/private partnerships are encouraged;

Protection of investments: Investment adequately regulated by relevant laws;

membership of ICSID, MIGA and ICC; and a signatory to the bilateral investment

promotion and protection agreements with many countries around the globe including

South Africa, Germany, Algeria, Belgium, Botswana, China, Cuba, Denmark, Egypt, USA,

USA (OPIC), Finland, France, Indonesia, Italy, Mauritius, Netherlands, Portugal, Sweden,

United Kingdom, Vietnam, Zimbabwe, India, Spain, Switzerland, and Japan;

Competitive Incentives: Fiscal and non-fiscal incentives, agreements to prevent double

taxation and fiscal evasion with Portugal, Mauritius, UAE, the Administrative Region of

Macau, Italy, South Africa, Botswana, India and Vietnam;

Good Life Environment: Sincerity, hospitality, friendliness, delicious food, beautiful

beaches;

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 6

Telecommunications infrastructure is largely confined to urban areas, and its service is

predominantly mobile. The telecommunications sector in Mozambique is dominated by the

three mobile operators Vodacom, Movitel and Mcel and the incumbent fixed operator, TDM

(Telecomunicações de Moçambique). Mobile broadband penetration (3G HSPA) is currently

estimated at approximately 30%, mainly in urban areas of Mozambique. Mobile broadband

coverage is largely confined to urban areas. This is because most of Mozambique’s inhabitants

(up to 70%) live in rural areas where high costs and low returns make it commercially

unattractive for mobile operators to roll out mobile broadband services across the rest of

country (rural areas). New entrant Movitel has been rolling out its network aggressively in

rural areas and it offers to some extend3G-based voice services and broadband.

Most urban areas of Mozambique are likely to benefit from investment in fiber networks by

commercial players, but this will be limited to very dense urban areas in the large cities.

Significant investment has been made in backbone networks over the last few years, but this

has been at the expense of rural expansion.

Mobile operators Vodacom and Movitel, along with incumbent fixed operator TDM operate

their own backbone networks, and so there is a significant amount of duplication in backbone

network infrastructure. However, this has been at the expense of investment in access and

backhaul networks in rural areas, which remain largely undeveloped and in need of

investment.

On the other hand, Mozambique is well served by international connectivity from EASSy and

SEACOM. In general, there do not appear to be any concerns regarding the pricing of or

availability of international connectivity. However, it can be expensive to access international

connectivity through backhaul service providers such as TDM and Movitel.

Factors such aspoor network quality, a lack of standardized network specifications, high

backbone network pricing, unbalanced spectrum charging mechanisms and a wide range of

economic factors have resulted in a lack of infrastructure sharing, duplication of backbone

networks and a lack of investment in telecommunications networks in rural areas to provide

voice and broadband services.

Further, there are a number of steps that the Government had taken to reform the legal and

regulatory framework to increase competition, strengthen sector governance, reorganize

state-owned operating companies, and extend services to all.

The World Bank Study indicates that a 10 percentage point increase in fixed broadband

penetration could increase GDP growth by 1.21% in developed economies and 1.38% in

developing ones.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 7

Throughout this document our intention is to demonstrate that with the adequate tool and

market knowledge it is possible to invest in communications in semi-urban and rural areas, and

by doing so contribute to increase network accessibility to all Mozambicans irrespective of

class and economic status.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 8

2. Methodology

In order to allow easy understanding of the topic, we have divided the scope of the document

in 3 (three) parts:

We found that updated market intelligence for Mozambique was extremely limited and

difficult to find, therefore all data and material results of a combination of in-depth local and

international organizations available studies, analytical reports and research and interviews

with key market players of either public or private sector.

In some sectors of the report, it is possible to have comparison of Mozambique economies and

other in the region and of the world.

In order to allow an adequate, current and easy to understand to read content we have

decided to focus our analysis in 3 (three) main areas: (i) political and economic context, (ii)

general management business rules, (iii) telecommunications sector rules and environment.

The study methods comprised the extensive analysis of available literature available in

different encyclopedias (on- line and hard copy).

Understanding the Mozambican political and economic context is crucial for every potential

investor, the sources for the information gathered were the Government Five-Year

Part I – Political and Economic Context for Mozambique:

The intent is to provide adequate context on political and economical Mozambique's outlook.

Part II – General Management Business Rules:

With the aim at sheds light on how easy or difficult for a local or foreigner company to open and run business when complying with relevant regulations;

Part III – The Telecommunication Sector Rules and Environment:

Detailed overview of the sector, its stage , challenges and potencial opportunities

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 9

Development Program, World Bank, IMF, Central Bank of Mozambique, National Institute of

Statistics documentation.

The generic management business rules that allows the readers to perceive what is required to

set up a company in Mozambique, timelines and cost is an effective insight for those that wish

to open a business in a specific country . The information was collected in several sources i.e.,

Centro de Promoção do Investment (CPI), Gazeda, Comercial Code, Investment Law,

Regulations for Investment Law, Code of Fiscal Benefits , etc.

Regarding the Telecommunications sector the main source were Telecommunications

Regulatory Authority (INCM), international survey institutions and the telecommunications

operators’ companies reports. With collected data, graphics were developed and compared

with main telecommunications players for easy analyses and understanding of the information

provided in this report.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 10

3. Political and Economic Environment

3.1. Political Environment

Mozambique is a tropical country located in Southern Africa, surrounded by warm waters and

exotic beaches. It is a culturally rich country with Portuguese and Arab influences, where racial

integration happens naturally despite its strong colonial past.

The government is strongly involved in the reduction of absolute poverty trough the

establishment of economic reforms and attainment of the Millennium Goals. The districts are

seen as the source of development thus they are a priority in the government’s agenda.

The Mozambique Liberation Front (FRELIMO) party, headed since 2015 by President Filipe

Nyusi, has been in power since independence from Portugal in 1975. Following independence,

there was a 16-year civil war between FRELIMO and the rebel Mozambican National

Resistance (RENAMO) movement that ended with the Rome Peace Accords in 1992. In October

2013, after several armed clashes with FRELIMO troops, RENAMO announced that it was

pulling out of the peace accord. Despite a new peace deal in September 2014, violence has

continued, and thousands have fled to Malawi. Since December 2016, the situation is again

stabilized, due to continuous efforts for the establishment of peace taken by FRELIMO and

REMANO Leaders, Filipe Nyusi and Afonso Dhlakama.

Previously undisclosed debts of about $1.4 billion amassed by the former government came to

light in 2016, prompting donors to suspend budgetary support.

Mozambique is a Member of the SADC and favors from regional integration. It also favors from

an attractive business environment offering numerous business opportunities due to its

potential agro, tourism and energy sectors. It has 5 harbors from which agricultural products

flow to neighboring countries. The most important exports are aluminum, prawns, cashews,

cotton, sugar, citrus, timber and bulk electricity; the most important imports are machinery

and equipment, vehicles, fuel, chemicals and metal products.

Mozambique has undertaken reforms to encourage economic development, although progress

has been very gradual. Private-sector involvement in the economy is substantial, but

privatization of state-owned enterprises has slowed. Foreign capital is treated the same as

domestic capital in most cases, and trade liberalization has progressed.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 11

3.2. Economic Environment

Despite Mozambique’s tumultuous past, the massive task of reconstructing the country and

tackling social issues has begun to show.

The business environment in Mozambique has improved and still remains one of the

government’s top priorities. The government is strongly implementing policy reforms in order

to simplify the process of opening and operating enterprises and to facilitate cross-border

trade. This is reflected in the latest scoring of Mozambique in the World Bank report "Doing

Business 2017" where the country is making a remarkable improvement.

Government has reviewed tax incentives in order to minimize donor dependency while

promoting direct foreign investment. Legislation supports the creation of export processing

zones. Free zone concessions can be granted for a renewable 50 years period.

With regards to the economic crisis, the financial forecasts for Mozambique were encouraging

but companies are beginning to suffer the effects of the recession. The international economic

crisis forced the reduction of exports in Mozambique thus exacerbating the trade deficit. The

volume of business fell by 36% over a period of 1 year. Despite these developments, the

economic scenario remains positive.

South Africa is the country’s main trading partner but it also trades with the USA, Portugal,

France, Italy and others. Currently, Mozambique's exports include aluminum, electricity, and

gas.

The national financial system is visibly improving. Financing of the private sector through the

national banking system has doubled in the last year. The banking system is steadily increasing,

but still a challenge for the SMEs due to high interest rate.

There are operating under the central bank's supervision and offering a diversity of currently

15 banks products. The number of desks increased, and the Central Bank established a policy

of disclosing information on commissions and other fees in order to promote competition and

transparency in the sector.

The SADC free trade protocol is aimed at making the Southern African region more

competitive by eliminating tariffs and other trade barriers.

The World Bank in 2007 talked of Mozambique's blistering pace of economic growth. A joint

donor-government study in early 2007 said Mozambique is generally considered an aid success

story.

The IMF in early 2007 said 'Mozambique is a success story in Sub-Saharan Africa. Yet, despite

this apparent success, both the World Bank and UNICEF used the word 'paradox' to describe

rising chronic child malnutrition in the face of GDP growth.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 12

Mozambique is classified as an underdeveloped country and has a GNI per capita of USD600,

compared with the Sub-Saharan average of USD1638 1 . Following the global financial

difficulties, Mozambique’s economy has shown strong growth and low inflation rates (see

Figure 3.1). Real GDP has increased by approximately 7% per annum since 2011, largely due to

growth in financial services, agriculture and extractive industries. Inflation rates have also

been stable in recent years.

However, economic growth slowed down in 2015 and 2016, due to lower exports and foreign

direct investments as well as a rise in import costs. Foreign exchange rate deterioration led to

a depreciation of the Metical and a spike in inflation rates, which has exposed the country to

economic and political volatility, contributing to an uncertain outlook (see Figure 3.2).

1. Source World Bank, based on 2014 data.

Figure 3.1: Real GDP growth rate vs. inflation, [Source: EIU, Euromonitor, 2016]

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 13

There have been reports that Mozambique’s economy has grown increasingly unstable in the

last year, due to the discovery of undisclosed liabilities. This has led to the suspension of IMF

aid and limited Mozambique’s access to financing for infrastructure programs.

3.3. Demographics

Mozambique has a population of approximately 27 million, dispersed over a large surface of

approximately 800 000km2. Most of Mozambique’s inhabitants live in rural areas, with around

30% living in urban areas. Mozambique has experienced increasing urbanization in recent

decades: the rate of urbanization has slowed since 1992, but is still growing steadily.

The north-central provinces of Zambézia and Nampula are the most populous, with about 45%

of the population. Maputo is the largest city, with around 1.2 million inhabitants, followed by

Matola (both in Maputo Province). Approximately 56% of the population lives below the

poverty line, and rural areas have a higher number of people living in poverty.

Mozambique has one of the largest and fastest growing populations in sub-Saharan Africa (see

Figure 3.3). The population is anticipated to reach 30 million by 2020 due to improving life

expectancy and high fertility rates.

2Source: INE, 2016/African Outlook 2008; The World Fact Book 2011; UN Human Development Report 2014, CIA Fact book

Figure 3.2: Exchange rate MZN/USD, [Source: EIU, 2016]

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 14

Despite high economic growth, Gross National Income per capita remains half the average for

sub-Saharan Africa. The majority of the rural population remains poor, whilethe middle class

emerges in Maputo and other major cities, driven by fast economic growth.

Figure 3.3: Population and Age Profile in Mozambique, [Source: INE et all]

3.4. Government Programs and Projects

3.4.1. Five-YearGovernmentProgram 2015-2019

As a result of the growing globalization of the economy and the emergence of new production

centers, there has been increasing mobility of people and goods, integrated logistics,

transportation and communications services.

In this perspective, the Government continues to direct its efforts in the construction and

reconstruction of communications infrastructures for access to Information and

Communication Technologies.

The Strategic Actions in the communications sub-sector are:

Expand telecommunication services to cover all administrative posts and half of the

country's locations;

To license new operators that provide telephony and data transmission services;

Expand 3rd or 4th generation services to district headquarters;

Expand the broadband transmission infrastructure including the installation of Fiber

Optic Rings in the Provincial Capitals.

Life expectancy at birth Total population: 54.1 yearsMale: 52.0 yearsFemale: 56. 2 years (2016 est.)

Affordability/price

sensitivity

54% below poverty line

Literacy rates. 51%

Mobile Penetration Below 40%

Population Coverage 60%Less than 20% of the population is online on mobile

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 15

3.4.2. GovernmentProjects in ICTs

The Government is developing a number of information and communication technology

projects and initiatives at national level in the areas of public administration and education (e-

Government Network (GovNet), Government Portal, State Financial Administration System (e-

SISTAFE), Programs of Community Multimedia Centers, Mobile Money Platform, National

Network of Higher Education and Research (MoRENet), Internet in Schools, among others.

3.4.3. Electronic Government Network (GovNet)

The e-Government network project started in 2004 initially as a pilot phase and was intended

to provide the necessary support in defining the technical requirements, communication

protocols and definition of network security rules. During the initial phase the project was

based only on the capital of the country but due to its success, it was extended to other

provinces and then to the district level. However, not all districts are properly connected to the

Government network.

Today, GovNet is a physical data communication platform, aimed at connecting public sector

bodies to each other, at national level, in order to ensure the safe circulation of information

and access to shared documents in a secure, reliable and cost effective manner. It is therefore

an optimized solution, in all respects, without duplication of actions and expenditure.

Therefore, GovNet is a communication platform that connects the local networks of public

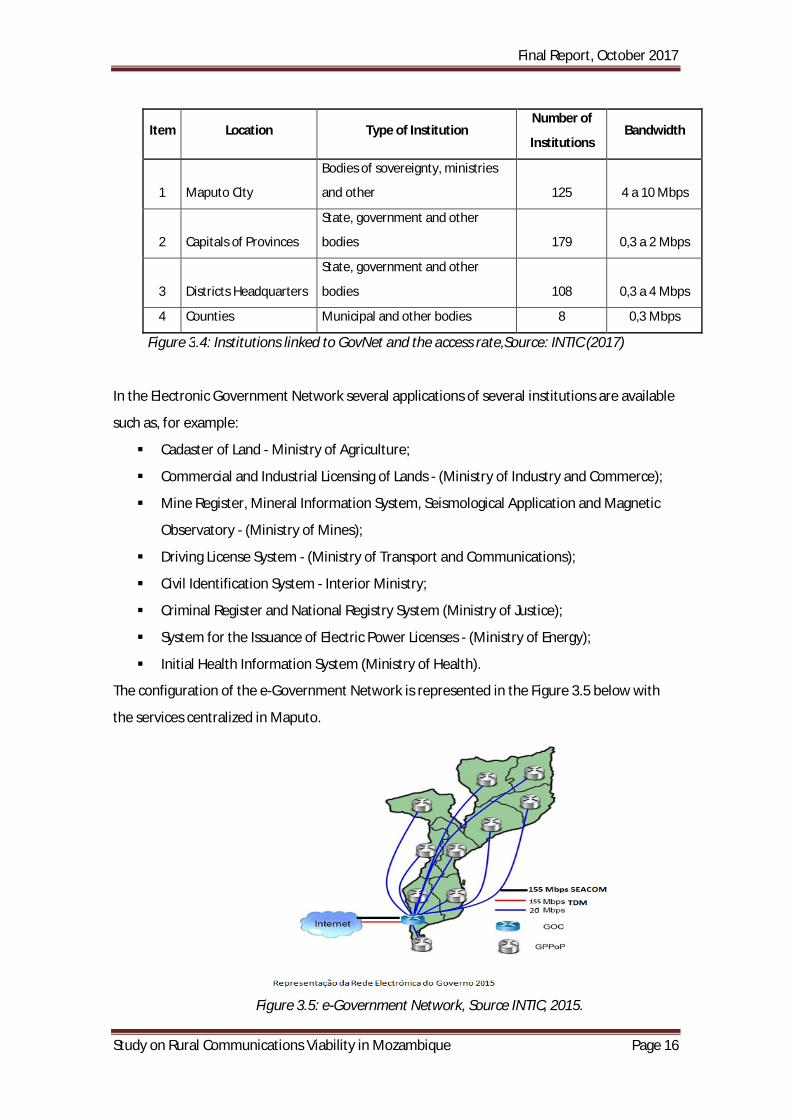

institutions and government (see Figure 3.4), through the national telecommunications

infrastructure, allowing, among other benefits, that:

1. Government and civil servants are permanently connected online;

2. Public services are closer to the citizen;

3. The Government and the civil service become more efficient; and,

4. Public services yield more at lower costs.

With GovNet, you move from individual access to the Internet, to global, centralized, fast and

secure access, allowing:

The exchange of messages and documents through electronic mail; and,

Shared access to document files.

GovNet is a network based on the infrastructure of the Mozambican National

Telecommunications Company (TDM), which offers connectivity services through leased lines

(broadband leased lines).

The table below shows the number of institutions in the state, their scope and the bandwidth

used to access the various facilities available on the GovNet platform.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 16

Item Location Type of Institution

Number of

Institutions Bandwidth

1 Maputo City

Bodies of sovereignty, ministries

and other 125 4 a 10 Mbps

2 Capitals of Provinces

State, government and other

bodies 179 0,3 a 2 Mbps

3 Districts Headquarters

State, government and other

bodies 108 0,3 a 4 Mbps

4 Counties Municipal and other bodies 8 0,3 Mbps

Figure 3.4: Institutions linked to GovNet and the access rate,Source: INTIC (2017)

In the Electronic Government Network several applications of several institutions are available

such as, for example:

Cadaster of Land - Ministry of Agriculture;

Commercial and Industrial Licensing of Lands - (Ministry of Industry and Commerce);

Mine Register, Mineral Information System, Seismological Application and Magnetic

Observatory - (Ministry of Mines);

Driving License System - (Ministry of Transport and Communications);

Civil Identification System - Interior Ministry;

Criminal Register and National Registry System (Ministry of Justice);

System for the Issuance of Electric Power Licenses - (Ministry of Energy);

Initial Health Information System (Ministry of Health).

The configuration of the e-Government Network is represented in the Figure 3.5 below with

the services centralized in Maputo.

Figure 3.5: e-Government Network, Source INTIC, 2015.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 17

3.4.4. Government Portal

The initiative of the Government Portal aims to provide a single point of entry for government

services and information that are organized according to the interests and needs of citizens,

allowing online access. The Government Portal was launched in 2006. Following this initiative,

several provincial government portals were developed and, at this stage, citizens can access

State services provided through the Government portal. Therefore, the Government portal

consists of providing services in which citizens can interact with the government through a

single point, and are able to find what they need quickly and have easy access to information.

3.4.5. System of Financial Administration of the State (e-SISTAFE)

The State Financial Administration System (e-SISTAFE) has been implemented to provide

financial administration services over the Internet, using a single bank account for all

government and public expenditure institutions.

Through this system, the institutional budgets of the Public Administration are allocated in this

way and the monthly reports are also presented, allowing the Ministry of Economy and

Finance to present the annual State Financial Report in a timely manner, as well as quarterly

reports on the implementation of the budget.

With this project it has been demonstrated that government transactions, for example G2G

(government-to-government), G2B (government-to-business) and G2C (government-to-citizen),

can be effected effectively and efficiently.

3.4.6. Programs of Community Multimedia Centers (CMCs)

This program aims to provide a means by which communities can access information using a

wide range of information and communication technologies through a single point. It also

serves to bridge the digital divide by enabling people in communities to address the

development challenges they face and to strengthen their ability to use and learn in the use of

information and communication technologies.

3.4.7. Internet in Schools

"Internet in Schools" is a national network of professional educators and schools working to

make Mozambican education system competitive by preparing young people in schools for

Internet connectivity and technology. The network aims to increase learning opportunities for

students, teachers and the surrounding community through the Internet. "Internet in schools"

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 18

is also seen as a way to prepare Mozambican students for work in the global information

society.

3.4.8. Electronic Currency Platform

As a way of expanding financial services, especially in rural areas where traditional banking is

not physically present, mobile money service (mobile money) was introduced in the country

through the mobile telephone network. The service has been an added value by allowing

citizens residing in places without banking institutions to use this service to make purchases,

send and receive monetary values, as well as receive salaries through this platform.

3.4.9. Project of National Network of Higher Education and Research (MoRENet)

The national network of Higher Education and Research interconnects the Public and Private

Institutions of Higher Education and Professional Technical Education with broadband

connections at national level. The main objective of the network is to integrate higher

education and research institutions in a high-speed network national, providing quality

services and economic, technological and institutional sustainability to be a fundamental

partner in the development of the Mozambican academic community.

MoRENet is part of the Network of Higher Education and Research (NREN) families, which in

various parts of the world provide solutions dedicated to the needs of the academic sector and

is a platform for the scientific development and sharing of information among students,

academics and researchers.

The expectation is to help reduce distances, facilitate access to virtual bookstores in

Mozambique, Africa, Europe or America, through the interconnection of MoRENet with the

world academic networks.

This measure is in line with the objectives of the Information Technology Policy, the

Implementation Strategy of the Information Technology Policy and the Science, Technology

and Innovation Strategy of Mozambique.

In lieu of the above, it is clear that the acceleration of communication in the rural areas of Mozambiquewill enhance mobile data speeds, contributes to the acceleration of these Government initiatives and subsequently by increasing broadband penetration the contribution to the economic and social growth is expected to be immediate.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 19

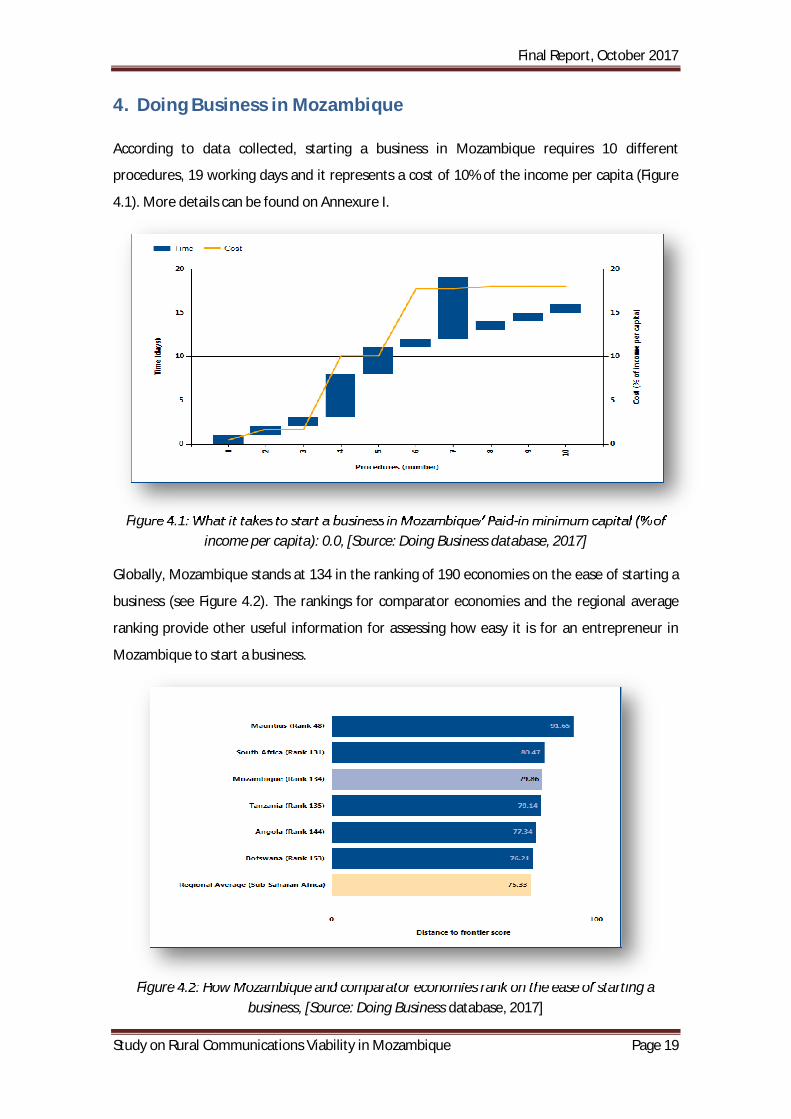

4. Doing Business in Mozambique

According to data collected, starting a business in Mozambique requires 10 different

procedures, 19 working days and it represents a cost of 10% of the income per capita (Figure

4.1). More details can be found on Annexure I.

Figure 4.1: What it takes to start a business in Mozambique/ Paid-in minimum capital (% of income per capita): 0.0, [Source: Doing Business database, 2017]

Globally, Mozambique stands at 134 in the ranking of 190 economies on the ease of starting a

business (see Figure 4.2). The rankings for comparator economies and the regional average

ranking provide other useful information for assessing how easy it is for an entrepreneur in

Mozambique to start a business.

Figure 4.2: How Mozambique and comparator economies rank on the ease of starting a business, [Source: Doing Business database, 2017]

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 20

4.1. Investment Guarantee and Tax Incentives

In light of the Investment Law (Law 3/93, of 24th June) and complementary legislation, in

order to obtain the Guarantees and incentives offered by the Government the investors should

submit the application form with the details of their business plan to CPI or GAZEDA, for

approval. Procedures for Approval of Investment Projects are represented in the Figure 4.3

below:

Figure 4.3: Procedures for approval of investment projects

4.1.1. Registration Process

The registration process comprises the following steps:

1. Company name reservation at the Conservatory of Legal Entities' Registration Office;

2. Company registration at the Conservatory of Legal Entities' Registration Office.

Documents to be submitted:

a) Copy of the company’s name reservation certificate,

b) Company’s Articles of Association,

c) Certified copies of the shareholders' identification documents or passports.

More detailed information can be found in AnnexureII of the report.

The investor submits CPI three

copies of a Business Plan

as well as the filled application form

CPI coordinates with the Sector

Authority and the Environment Authority at

local and central levels for

approval, assesses the Business

Proposals and

negotiates the Terms of

Authorization with investors

Upon agreement on the Terms of

Authorization CPI submits the Project

for

approval by the relevant authority

(Provincial Governor, Minister

of Economy

and Finance or the Council of Ministers)

1 2 3

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 21

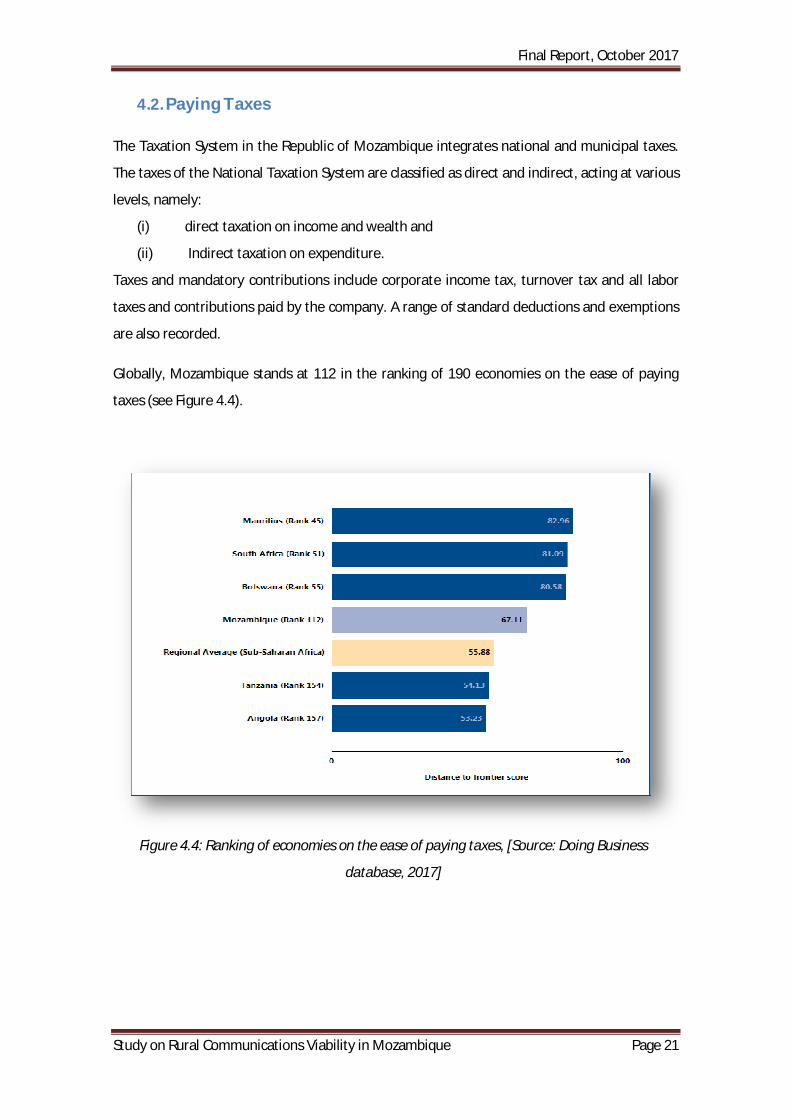

4.2. Paying Taxes

The Taxation System in the Republic of Mozambique integrates national and municipal taxes.

The taxes of the National Taxation System are classified as direct and indirect, acting at various

levels, namely:

(i) direct taxation on income and wealth and

(ii) Indirect taxation on expenditure.

Taxes and mandatory contributions include corporate income tax, turnover tax and all labor

taxes and contributions paid by the company. A range of standard deductions and exemptions

are also recorded.

Globally, Mozambique stands at 112 in the ranking of 190 economies on the ease of paying

taxes (see Figure 4.4).

Figure 4.4: Ranking of economies on the ease of paying taxes, [Source: Doing Business

database, 2017]

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 22

4.2.1 Types of Taxes

DIRECT TAXATION on income is made through Corporate Income Tax (IRPC) and

Personal Income Tax (IRPS).

Corporate Income Tax (IRPC) is taxable on gained income, during the taxation period,

from tax payers, namely commercial or civil companies, cooperatives, public companies

and other corporate, both public and private, entities with no legal existence whose

incomes are not subject to taxation in the form of IRPS or IRPC.

General 32%

Agriculture & cattle breeding activities (until 31 Dec 2015): 10%.

Personal Income Tax (IRPS) is imposed on the global annual value of income and is

paid by singular persons residing in the Mozambican territory and by those not

residing in the country but gaining income from it.

Minimum 10%

Maximum 32%.

INDIRECT TAXATION, which comprises taxes on expenditure, integrates Value Added

Tax (VAT), Specific Consumption Tax (ICE) and Customs Duties.

Value Added Tax (VAT) is imposed on the sale of goods and provision of services in the

national territory by a tax payer acting as such, as well as on the importation of goods:

17%.

Specific Consumption Tax (ICE) is imposed on the consumption of certain specified

goods, produced or imported:20%.

Customs Duties are imposed on imported and exported goods. The rates vary as

follows:

Raw materials: 2.5%

Capital goods (class K): 5%

Intermediary goods: 7.5%

Consumption goods: 20%

Withholding tax: 20%

Labor Market Regulation – the registration of workers and their respective employers

with the National Social Security System is mandatory. The fee for social security is 7%,

namely:

- 4% paid by the employer; and

- 3% paid by the employee.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 23

Under the SADC trade protocol implementation framework, various products from SADC

region countries benefit from exemptions from payment of customs duties.

The Taxation System is augmented by other taxes, namely the Stamp Duty, Tax on

Successions and Donations, SISA, Special Tax on Gambling, National Reconstruction Tax,

Vehicle Tax and other, Legally established taxes and specific charges (see Figure 4.5).

Figure 4.5: Legal Obligations

4.3. Guarantees to Investment

The guarantees envisaged in the legislation in force comprise:

1. Legal protection on property and rights, including industrial property rights;

2. No restriction of borrowing and payment of interest abroad;

3. Transfer of dividends abroad;

4. Arbitration according to ICSID or ICC rules for the resolutions of disputes on

investments;

5. MIGA and OPIC services on issues related to investment risk insurance.

4.3.1. Investment Guarantees

Mozambique is signatory to agreements and has signed investment promotion and reciprocal

protection agreements with countries across Africa, America, Asia and Europe

Tax or mandatory

contribution

Payments

(number)

Time

(hours)

Statutory tax

rate

Tax base Total tax

rate (% of

profit)

Notes on

total tax rate

Social security

contributions

12 30 4% gross salaries 4.51

Corporate income

tax

7 50 32% taxable profit 30.80

Municipal property

tax

2 0.1% to 1% building value 0.54

Tax on interest 0 20% interest

income

0.51 not included

Municipal tax on

economical activity

1 MZN 4,500 fixed fee 0.15

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 24

4.3.2. Investment Incentives

The Investment Law grants certain tax and customs benefits depending on the amount,

location and sector of investment activity. The current incentive schemes are:

Generic Fiscal and Customs Benefits: Investments carried out under the Investment

Law are exempt from payment of customs duties and VAT on capital goods and their

accompanying parts and accessories classified as Class K of the Customs Tariff.

Tax Credit per Investment: Investments carried out in Maputo City benefit, for a period

of five tax years, from a deduction (not to exceed the tax payable in respect of the

investment project activity) from Corporate Income Tax (IRPC) that is equal to 5% of

the total investment actually realized. The percentage is 10% in all other remaining

provinces.

In addition there are specific regimes for:

Agriculture and Fisheries;

Trade and Industry in Rural Areas;

Transforming and Assembly Industry;

Creation of Basic Infrastructures;

Industrial Free Zones;

Tourism and Hotels;

Large Scale Projects.

Rapid Development Zones;

Investments under the Mining Law;

Investments under the Petroleum Law

Special Economic Zones

Science and Technology Parks

The country has signed investment promotion and reciprocal protection agreements with the

following countries: South Africa, Germany, Algeria, Belgium, China, Cuba, Denmark, Egypt,

USA, USA (OPIC), Finland, France, Indonesia, Italy, Mauritius, Netherlands, Portugal, Sweden,

United Kingdom, Vietnam, Zimbabwe, India, Spain, Republic of Korea, Botswana and the

Autonomous Special Administrative Region of Macau

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 25

4.3.3. National and Foreign Direct Investment

The minimum value of foreign direct investment resulting from the inflow of own capital from

foreign investors, is set at the equivalent of 2.5 million MT for the specific purposes of transfer

of profits abroad and the re-exportable invested capital.

The real value of foreign direct investment, for registration and eligibility for guarantees and

incentives established for this purpose shall consist of the sum of the values of equity,

shareholders' loans without interest and/or supplementary capital provided by investors

themselves , as well as exportable profits that might have been reinvested in the country.

4.4. Access to Land

Under the Constitution of the Republic of Mozambique all land is the property of the State and

can be used on a lease basis, and the right to land use is regulated by the Land Law (Law Nº

19/97, 1 of October) and the Land Law Regulation (Decree Nº 66/98, 8 of December). The

maximum period of a land lease is 50 years, renewable for a further 50-year period.

Land title is transferable for buildings and real property assets upon presentation of a public

deed. Following conditions will apply to become holders of land-use rights:

Foreign individuals or collective persons with adequately approved investment

projects and applicable to either

Single individuals who have been residing in Mozambique for at least five years;

or Collective entities who are incorporated and registered in Mozambique

The entity responsible for registration and information on land use is:

MINISTRY OF LAND, ENVIRONMENT AND RURAL DEVELOPMENT

Rua Kassuende 167, Maputo

Tel: + 258 21492403

4.5. Enforcing Contracts

Globally, Mozambique stands at 185 in the ranking of 190 economies on the ease of enforcing

contracts. The rankings for comparator economies and the regional average provide other

useful benchmarks for assessing the efficiency of contract enforcement in Mozambique.

According to data collected by Doing Business, contract enforcement takes 950.0 days and

costs 119.0% of the value of the claim

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 26

The quality of judicial processes index measures whether each economy has adopted a series

of good practices in its court system in four areas: court structure and proceedings, case

management, court automation and alternative dispute resolution.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 27

5. Telecommunication Sector Analysis

5.1. Policy and Regulatory Framework

Since 2002 Mozambique has moved decisively towards an open and competitive

telecommunications market. In particular, competition in mobile services has led to

spectacular growth of voice and now increasingly of broadband services. The government is

encouraging and facilitating increased competition especially in infrastructure networks,

access networks, and international calls. Therefore, all segments of the telecommunications

market are open to new entrants and competition. In practice, however, competition has built

up faster in some market segments than in others.

The government is also encouraging more operators to come to the market, offer their

services, and compete in domestic networks. The infrastructure market is subject to the rules

that apply to the provision of network services generally, including interconnection,

infrastructure sharing, and use of public rights of way, and to rules on fair competition.

Therefore, in 2016, the Telecommunications Law has been revised and further licensing

regulations modernized and strengthenedto accommodate the normative framework for fair

competition and the new developments in the sector.The Regulatory Body is only intervening

if necessary to promote and enforce these rules.

5.1.1. Telecommunications Market Regulator

The telecommunications market’s Regulatory Body is the Instituto Nacional das Comunicações

de Moçambique 3 (INCM), (Mozambique’s Communications National Institute). INCM is

responsible for licensing and registration of telecommunications networks and services for

public use, and the frequency assignment and management. INCM is the public entity, with

administrative and financial autonomy for regulation, supervision and government’s

representation in the telecommunications sector4.

The INCM is viewed as a largely effective and independent organization by the key

telecommunications market stakeholders in Mozambique. Even new players, who are

considering entering the market, also consider the INCM to be independent of the

government and see the INCM as a generally supportive institution.

3Telecommunications Law (Law n.º 4/2016, of 3 June) 4Decree n.º 32/2001, of 6 November, which defines the Organization and Functioning of the INCM.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 28

5.1.2. Licensing

Mozambique adopted a combination of unified and class operating licenses5. Unified licenses

are now available on demand to individual operators willing and able to develop a wide range

of services and networks countrywide.

Class licenses are made available without individual authorization to operators with narrower

functional or geographical scope. The number of licenses of each type is not limited, and the

choice of type of license is left to each operator. Both types of license are subject to the rights

and obligations applicable to all providers of telecommunications services and networks.

All operators must apply separately for authorizations to use scarce resources (e.g. radio

spectrum, rights of way) and numbering blocks, if needed.

The new licensing regime is enable existing and new operating companies to respond more

effectively to the growing opportunities and challenges posed by convergence among services,

technologies, and business models. The new licensing regime is also in line with global trends

towards general authorization. Operating licenses in Mozambique at pastwere narrowly

segmented by types of service and associated technologies. In general, both type, unified and

class, operating licenses for the provision of telecommunications services and networks are

issued within 30 days after individual application.

5.1.3. Network sharing

The Telecommunications Law gives telecommunications license holders guaranteed rights to

request access to take ownership of land or to request the right to use land.

Telecommunications license holders also have the right to access public land to install and

maintain their network infrastructure6.

Infrastructure sharing and open access are important for the development of national

telecommunications networks and specifically in underserved areas, where economic and

commercial bottlenecks prevent the deployment of infrastructure.

5Decree n.º 26/2017, of 30 June, which approves the Regulation for the Licensing and Registration Regime, and Scarce Resources 6Decree nº 62/2010, of 27 December, which states the conditions of sharing of such infrastructures

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 29

Figure 5.1: Regulation indicates the conditions of sharing of such infrastructures

Regulated open access in Mozambique is limited to passive infrastructure sharing, whereby

all operators have to share their infrastructure if requested by the counterparty. Operators

are free to negotiate individual sharing agreements. However, prices need to be fair and

reasonable, guided by costing principles. If no consensus is reached, the INCM has the power

to determine the conditions of the agreement. Through conditions on QoS and capacity, the

regulation mandates nondiscrimination and equal treatment to all operators wishing to have

access to the passive infrastructure of another operator. The regulation also requires that

operators take into account the needs of new entrants by ensuring new entrants have

enough capacity if requested to share their infrastructure.

Although the regulation on passive infrastructure sharing adheres to the general principles of

openness, non-discrimination and transparency, in practice there is limited infrastructure

sharing on the market. Therefore, infrastructure for the telecommunications networks need

to be built with sharing principles in mindi.e. ensuring operators have enough capacity if

requested to share their infrastructure.

The INCM is currently working on introducing new regulation that aims to standardize

infrastructure roll-outand includes mandatory infrastructure sharing as well as specific

guidelines on pricing.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 30

5.1.4. Interconnectivity

The Telecommunications Law states that operators have the right to enter into private

interconnection agreements, acting in good faith. The Interconnection Regulation7 gives more

detailed provisions to ensure that these agreements are concluded.

The main objectives of the interconnectivity are to:

Establish a transparent operators’ networks interconnection to promote a fair

concurrency;

Assure the services interoperability and basic relationship rules in adopting cost model,

which facilitates negotiations for the interconnection’s contract between operators;

Adopt and apply the interconnection principles based on World Trade Organization’s

Reference Document on Basics Telecommunications Agreement.

INCM may intervene only when no consensus between operators is reached during the

interconnection process.

5.1.5. Fair Competition

The revised Telecommunications Law reaffirm that all market segments are open to new entry

and competition, establish rules of fair competition and safeguards against anti-competitive

behavior, and identify unacceptable practices. Unacceptable practices will include engaging in

anti-competitive cross-subsidization, using information obtained from competitors with anti-

competitive results, and not making available to other service suppliers technical and

commercial information necessary for them to provide services.

Under the new Telecommunications Law, the INCMis designated as the competition authority

for the telecommunications sector. INCMis developing regulations to implement the law's

provisions on fair competition. Once a general competition law and authority are in place,

INCMwill work together with this new authority to strengthen monitoring and enforcement of

fair competition and gradually transfer some responsibilities.

Accounting separation for regulatory purposes is mandatory for any operator with market

power that provides both wholesale and retail services.

7Decree n.º 34/2001, of 6 November, which approves the Interconnection Regulation as amended by

Decree 43/2004, of 29 September

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 31

5.1.6. Quality of Service

The government relies primarily on the market to set and meet standards for quality of service.

INCM defines indicators for service quality and publish (and from time to time update)

benchmarks for these indicators, reflecting good practice in Southern Africa Region and

selected other countries8. Operators must commit levels of performance they intend to

achieve for these indicators and must publish their results periodically.

INCM will also verify that the quality of service results are consistent with each operator's

license obligations and prevailing regulations, and take any corrective measures that may be

necessary. These measures will help improve the quality of telecommunications services.

Published results will help businesses and households make informed choices among

alternative telecommunications service providers.

Further, the Telecommunications Lawprovides for mandatory mobile number portability at a

date to be determined. The INCM, in consultation with the operating companies, will establish

a timetable for implementation.

Mobile number portability will make it easier for users to change service provider in response

to differences in service quality, price, and other aspects. The subscriber number is a valuable

business asset for independent workers and small entrepreneurs as well as for professionals,

companies, and government agencies dealing with the public.

5.1.7. Spectrum Management

Revised radio communication regulations9is now consistent with the Telecommunications Law,

by reducing administrative costs and delays, avoiding lost market opportunities for spectrum

users, facilitating innovation, and preventing potential tensions among spectrum rights holders.

Spectrum assignment and licensing has been simplified, expedited, and made more

transparent and equitable. Technological and service neutrality of spectrum authorization is

enhanced. Spectrum pricing and taxation has been revised to better reflect spectrum value

and regulatory cost. A provision for the transition to digital television is firmed up, including

future allocation and assignment of the frequency bands to be vacated.

8Decree n.º 6/2011, of 3 May, which approves the Regulation of Public Telecommunications Services

Quality

9Decree n.º 64/2004, of 29 December, which approves the Telecommunications rates regulation

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 32

Mobile and fixed wireless technologies will continue to figure prominently in extending

affordable basic services throughout the population as well as rolling out broadband beyond

the main markets.

5.1.8. Telecommunications Taxes and Fees

The regulation on telecommunications taxes and fees sets out the terms and conditions for

the collection of charges from telecommunications operators as well as determining the size of

these charges and prescribing sanctions in case of non-compliance (see Annexure III). Taxes

include an annual telecommunications tax and fees for acquiring a license and registration.

The annual telecommunications license fee is set at 3% of the gross revenue of operators. In

addition, mobile operators pay spectrum charges, which are levied per site (see the section

below).

The regulation on telecommunications taxes and fees points out that the purpose of the

levied fees is to cover the costs of the INCM’s regulatory functions. Further, these fees are

deemed as a key income stream for the INCM to cover costs incurred in carrying out its

regulatory functions.

5.1.9. Spectrum Charges

As per the regulation10, the fees levied for spectrum charges are aimed at covering the costs of

managing and monitoring the use of spectrum. The spectrum fee formula is set taking into

account types, number of channels spacing, spectrum type, type of users, etc. The regulation

also stipulates penalties levied in case of failure of fee payments.

The regulation implies that the larger the network of a given operator, the more fees it needs

to pay, as these fees are based on the number of sites an operator has. The INCM has

introduced a new regulation related to spectrum charges (see Annexure IV).

5.1.10. Universal Service Access Fund (USAF)

The Universal Service Access Fund (USAF) is established by theTelecommunicationsLaw. Terms

and conditions for the operations of the fund are laid out in the USAF regulation11 recently

revised by the government to accommodate the new Telecommunications Law. The

government's objective is extending services throughout the population and will be achieved 10Decree n.º 64/2004, of 29 December, which approves the Telecommunications rates regulation

11Decree n.° 69/2006 of 26 December, which approves Universal Service Access Fund regulation

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 33

primarily by operating companies on a business basis in a competitive market. The benefits of

modern telecommunications should reach all inhabitants, irrespective of where they live, their

ability to pay, and their physical capabilities.

Today only about 20 percent of the population is connected to basic voice and text services,

and as much as 50 percent lives in places where service is not available12. Fiscal resources are

used as necessary to narrow any remaining gaps between what service providers are prepared

to do on a business basis alone and the country's broader development needs. In 2006, the

government created the USAF, the main instrument to provide fiscal support. The government

is also encouraging development of applications, content, and user skills to enhance the value

of advanced services to the population at large.

USAFsupports extending voice, data, and Internet service to rural areas that lack the necessary

infrastructure and where services are not commercially viable on their own. USAFis funded

mainly by a mandatory 1 percent levy on operators' gross revenues. USAFallocates subsidies

though competitive tender to the responsive bidder that requires the lowest one-time subsidy

for a project.

Building up USAFoperations is supporting the government's objectives as well as removing

development obligations from state-owned operators (TDM and Mcel) so they can perform

well in a competitive environment.

In 2008 started the enforcement of the USAF regulation and the collection of the contribution

fee on the telecommunications operators from 2009 to 2016 amountsto 919,887,928.77 MZN

(USD 16.725,22 million, exchange rate of 55 MZN to 1 USD), see Figure 5.1 below.

Figure 5.2: Operators’ contribution to USAF from 2009 to 2016

12Report on Mozambique’s broadband strategy.

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 34

The total amount of funds invested in USAF-related projects between 2008 and 2016 amounts

to MZN405 million (USD8 million)13, see Figure 5.2.

Figure 5.3: Number of sites and total amount of funds invested in USAF-related projects

between 2008 and 2016.

The costs covered by the USAF mobile voice projects include backhaul, site and active

equipment. Operators are obliged to share the infrastructure with other operators; however

there are no price guidelines for sharing infrastructure.

Since 2007, fiveprojects related to mobile coverage, broadcast, television and six community

multimedia centers have been funded under USAF. Costs covered under the community

multimedia center projects include set-up costs, computer equipment and furnishings.

The tenders are defined by the government which is responsible to set criteria for establishing

a project that are sent out(see Annexure V). Private can propose projects to be funded by

USAF.

However, operators have pointed out that the funds awarded for projects under the USAF are

insufficient to build infrastructure which meets international deployment standards, and so

they have decided not to take part in the tenders. Operators are concerned that operational

expenditure (opex) – which can be significant in remote areas – is not covered under the USAF.

5.1.11. Consumer protection

The principles and rules on consumer protection have been established in the revised

Telecommunications Law and protecting consumers will remain INCM's responsibility. INCM is 13USAF Report 2017 and internal presentation, Source INCM

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 35

developing an institutional program to improve customer protection and will consider

outsourcing routine work to contractors or industry or consumer associations.

In emerging markets, telecommunications consumer protection tends to be mainly or entirely

the regulator's responsibility, but often receives rather low priority and more technical matters

dominate. As markets mature, responsibility for different aspect of consumer protection is

often divided among different agencies. In highly competitive markets, industry self-regulation

is fairly common. Mozambique is in the early stages of this trajectory, with INCM bearing the

main responsibility for telecommunications consumer protection and there is no law or

authority on general consumer protection.14

5.1.12. Remove Market Barriers

INCM is identifying and addressing any remaining legal, regulatory, tax, or other restrictions to

the commercial viability of service for rural and remote communities, low-income areas of

towns and cities, and people with disabilities.

But even in a well-working market, important gaps are likely to remain between what

operators are willing to do on a business basis and broader development objectives. Not all

parts of Mozambique are commercially viable for all services. And where service is

commercially viable, it may not be affordable to all potential users.

When services needed for development are not commercially viable on their own,

Government is using fiscal resources under USAF to turn them into attractive businesses as

described above. In most cases, support will subsidize investment and start-up costs, expecting

that once service is established the recurrent expenses can be met from operating revenues. In

some situations, however, it may be necessary and justified to also subsidize use for some time.

In particular, could be that for the Internet to be extensively adopted and become sustainable

in rural areas may require making it available free of charge, and also training and helping

people to use the devices and content. Important initiatives are already in place to narrow

these gaps, including the FSAU managed by INCM, ICT connectivity programs managed by the

MCT (Ministry of Science and Technology), and voluntary social programs of the operating

companies.

14There is a consumer protection association, and work is underway to establish an Institutode Defesa dosConsumidores(Institute for Consumer Protection).

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 36

6. Market Structure

6.1. Voice Market

6.1.1. Fixed Market

The fixed telephony market has been liberalized since 2007. However, no new players have

been granted a fixed license, and TDM (the incumbent operator) remain the only significant

player in the fixed market. Due to poor infrastructure, TDM has been struggling to provide an

alternative to the services offered by Mozambique’s mobile operators using CDMA technology

to offer services with limited mobility.

Mozambique has one of the lowest levels of fixed telephony penetration in the region, at just

under 2% of households in 2014 (see Figure6.1). At present, and according to INCM, the fixed

subscribers dropped drastically to approximately 59,000.

Mozambique’s fixed penetration rates lags far behind those of South Africa (29%) and

Botswana (28%), which are the leaders in the region (see Figure6.2).

Figure 6.1: Fixed subscribers and household penetration in Mozambique, 2006 to 2014 [Source: TDM Report, 2016]

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 37

6.1.2. Mobile Market

The mobile market in Mozambique grew significantly between 2006 and 2014, at a compound

annual growth rate (CAGR) of 26%15. Key drivers of this growth were the lack of a fixed

alternative, due to the poor services provided by TDM, and the relative ease of mobile

network expansion. Competition in the mobile market increased following the launch of a

third player, Movitel, in 2011. Movitel has been rolling out its network aggressively, focusing

on rural areas and unconnected consumers.

Figure6.3 shows the mobile market subscribers in Mozambique by technology implemented

along past years, which lead to anactual market share as shown in the Figure 6.4.

15 INCM Annual Report 2016

Figure 6.2: Benchmark of fixed telecoms penetration, 2014 [Source: TeleGeography]

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 38

Figure6.3: Mobile market subscribers in Mozambique by technology, 2006 to 2014 [Source:

TeleGeography, 2016]

Figure6.4: Mobile market share in Mozambique, 2017 [Source: INCM, 2017]

The mobile network coverage is mainly in the cities, villages, along the main roads and

corridors, and touristic centers in the coastal line of the country (see Figure6.5).

27%

26%

47%

Mobile market share

Mcel

Vodacom

Movitel

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 39

Figure6.5: Mcel, Vodacom and Movitel country’s coverage, [Source: INCM, 2017]

6.2. Broadband and Internet Market

6.2.1. Fixed Market

Low commercial returns, poor network quality and inconsistent standards, high pricing,

unbalanced spectrum charging mechanisms and a wide range of economic conditions have

resulted in a lack of infrastructure sharing, duplication of backbone networks and a lack of

investment in broadband networks in rural areas. Fixed broadband penetration is very low in

Mozambique, just 0.9% of households at the end of 2016 (see Figure6.6), well below the

average for the region of 4.5%16. Digital Subscriber Line (DSL), rolled out by the incumbent, is

the dominant technology, followed by cable and WiMax rolled out by TVCaboandTeledata,

both which are subsidiaries of TDM.

16Analysys Mason Report 2016, on Mozambique’s broadband strategy

Figure 6.6: Fixed broadband subscribers and penetration, 2006 to 2016 [Source: TDM Report, 2016]

Final Report, October 2017

Study on Rural Communications Viability in Mozambique Page 40

6.2.2. Mobile Market

In Mozambique, mobile broadband has become essential for development and has provided a

real alternative to fixed. Mobile broadband subscriptions per 100 inhabitants have increased in

recent years, whereas fixed broadband subscribers have been declining over the recent years

(see Figure6.7). Mobile broadband networks can be deployed quickly and cost-effectively to

provide access to the Internet, web browsing, email, video and music downloads, mobile

banking, delivery of social services, and other applications that require high data transmission

speed.

6.3. Market Revenue and Investment

6.3.1. Revenue of Mobile Market

Mozambique’s telecoms sector is dominated by the mobile segment. Mobile revenue reached

approximately USD689 million in 2014, which represented 86% of total telecoms revenue.

6.3.2. Revenue of Fixed Market

Compared to USD109 million for the fixed segment (see Figure 6.8)17 and is believed to be