Construction Sector - EMIS Insight - Turkey... · The list of future projects ... Turkish...

42

- 1 - Any redistribution of this information is strictly prohibited. Copyright © 2014 EMIS, all rights reserved. Produced by: Any redistribution of this information is strictly prohibited. Copyright © 2014 EMIS, all rights reserved. Construction Sector Turkey July 2014

-

Upload

truongkhue -

Category

Documents

-

view

222 -

download

5

Transcript of Construction Sector - EMIS Insight - Turkey... · The list of future projects ... Turkish...

- 1 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Produced by:

Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Construction Sector Turkey

July 2014

- 2 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Table of Contents

I. Sector Overview

1. Sector Highlights

2. Economic Importance

3. Construction Sector Indicators

4. Construction Sector Forecast

5. Main Sector Indices

6. Employment

7. Employment and Salary Indices

8. International Operation of Turkish Contractors in 2010-2013

9. International Operations of Turkish Contractors to Date

10.M&A

II. Construction and Occupancy Permits

1. Construction Permits by Number of Buildings

2. Floor Area of Construction Permits

3. Construction Permits Value

4. Occupancy Permits by Number of Buildings

5. Floor Area of Occupancy Permits

6. Occupancy Permits Value

III.Homes and Commercial Centers

1. Home Prices and Sales

2. New House Price Index

3. Housing Loans

4. Housing Lending by Quarters

5. Shopping Centers

IV.Related Industries

1. Cement & Clinker Industry

2. Steel Industry

V. Latest Developments

1. Latest Developments Part I

2. Latest Developments Part II

VI. Main Players

1. Tekfen Holding

2. Tekfen Holding (cont’d)

3. Enka Insaat

4. Enka Insaat (cont’d)

5. Nurol Insaat

6. Nurol REIT

7. Cimsa

8. Cimsa (cont’d)

- 3 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

I. Sector Overview

- 4 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Sector Highlights

The Turkish construction sector grew by 7.1% in 2013, up from 0.6% in the previous year, becoming one of the main drivers of the local economy. The construction permits statistics point to a sustained growth of the sector in 2014. Despite the weaker performance in the last quarter of 2013 and the first three months of 2014, the industry's growth rate remains higher than that of the entire economy. The medium and long-term outlook for the sector remains optimistic due to growing population and the rapid urban development as well as the rising incomes in the country.

Performance

In 2013, the government introduced an Urban Transformation project, which envisages the replacement of risky buildings with new earthquake-resistant ones. Some 6.5 million buildings should be demolished and reconstructed over 15 to 20 years, with some 400,000 units planned to be destructed in 2014. The project will provide an additional impetus to the demand in the construction and related industries, such as cement manufacturing.

The government has launched a number of large-scale infrastructure projects, including a third bridge over the Bosphorus strait and a third airport

in Istanbul, which will further underpin the industry's growth. The list of future projects includes two nuclear power plants in Mersin and Sinop,

pipelines construction and an artificial waterway called Canal Istanbul.

The Turkish construction industry is highly competitive. The leading companies, including Enka, Gama, Tekfen, TAV, STFA, Dogus,

Yuksel, Mak-Yol and Nurol, boast a long track record of successfully implemented projects both at home and abroad. Turkish construction companies won contracts for a total of 374 projects worth USD 31.3bn, highest figure ever, in 45 countries in 2013. The Turkish contractors are mainly active in the CIS and MENA regions.

The number of people employed in the construction sector stood at 1.9 million at the end of April 2014, or 7.3% of the total workforce in Turkey. The

number of construction workers peaked to a record high 1.926 million people in October 2013, representing 7.9% of the country's total labour force.

Urban Transformation

Infrastructure projects

Main players

Employment

- 5 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Economic Importance

Turkey construction sector in figures

Turkstat, Ministry of Economy, Turkish Treasury

Indicator 2008 2009 2010 2011 2012 2013

Household consumption (TRY mn) 695,620 714,245 819,224 965,772 1,044,049 1,165,985

Share of housing and rent in household consumption (%) 29.1 28.2 27.1 25.8 25.8 n/a

Consumer price inflation (%) 10.1 6.5 6.4 10.5 6.2 7.4

Construction in public sector gross fixed capital formation (TRY mn) 30,071 29,113 36,751 41,728 45,000 61,254

Public sector gross fixed capital formation (TRY mn) 36,725 35,335 43,407 49,075 54,424 73,151

Construction in private sector gross fixed capital formation (TRY mn) 60,222 44,960 55,731 76,240 82,108 80,445

Private sector gross fixed capital formation (TRY mn) 152,369 125,383 164,409 234,088 231,695 244,295

Gross fixed capital formation (TRY mn) 189,094 160,718 207,816 283,163 287,121 317,446

Foreign capital inflow in construction industry (USD mn) 337 209 310 301 1,428 206

Turkey’s total net foreign direct investment, USD mn 19,762 8,629 9,058 16,171 13,224 12,868

Construction value (TRY mn) 44,658 36,578 45,670 57,751 62,157 68,930

Share in GDP (%) 4.7 3.8 4.2 4.5 4.4 4.4

Construction industry real growth (%) -8.1 -16.1 18.3 11.5 0.6 7.1

GDP real growth (%) 0.7 -4.8 9.2 8.8 2.1 4.0

GDP, TRY mn 950,534 952,559 1,098,799 1,297,713 1,416,798 1,561,510

GDP, USD mn 742,094 616,703 731,608 773,980 786,283 820,012

GDP per capita, USD 10,444 8,561 10,003 10,428 10,459 10,782

- 6 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

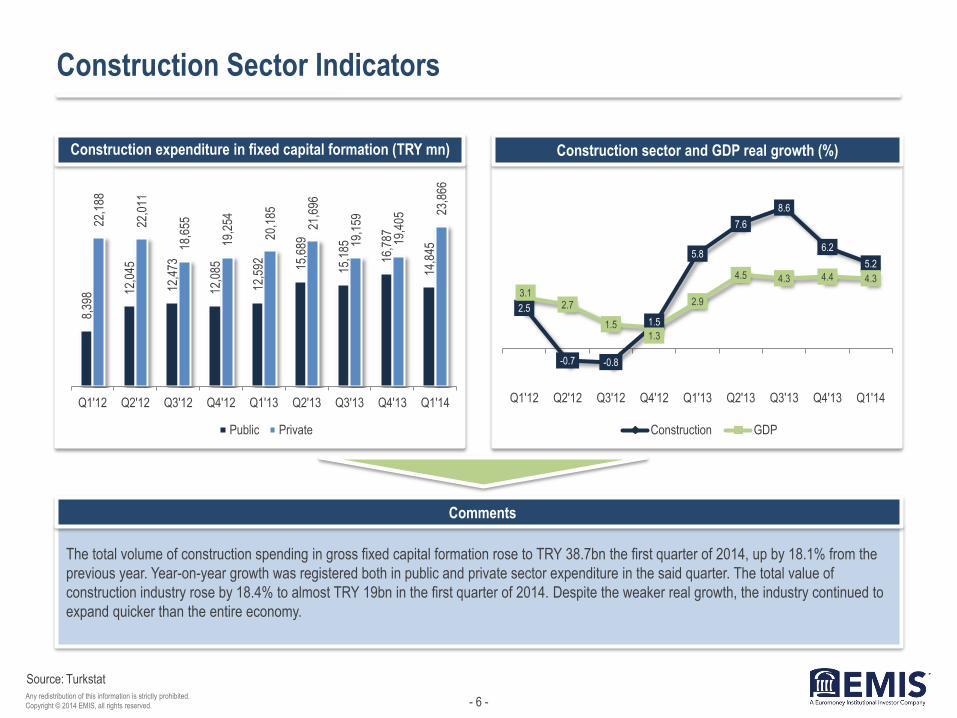

Construction Sector Indicators

The total volume of construction spending in gross fixed capital formation rose to TRY 38.7bn the first quarter of 2014, up by 18.1% from the

previous year. Year-on-year growth was registered both in public and private sector expenditure in the said quarter. The total value of

construction industry rose by 18.4% to almost TRY 19bn in the first quarter of 2014. Despite the weaker real growth, the industry continued to

expand quicker than the entire economy.

Construction expenditure in fixed capital formation (TRY mn) Construction sector and GDP real growth (%)

Turkstat

8,3

98 12,

045

12,

473

12,

085

12,

592

15,

689

15,

185

16,

787

14,

845

22,

188

22,

011

18,

655

19,

254

20,

185

21,

696

19,

159

19,

405

23,

866

Q1'12 Q2'12 Q3'12 Q4'12 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14

Public Private

2.5

-0.7 -0.8

1.5

5.8

7.6

8.6

6.2

5.2

3.1 2.7

1.5 1.3

2.9

4.5 4.3 4.4 4.3

Q1'12 Q2'12 Q3'12 Q4'12 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14

Construction GDP

- 7 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Construction Sector Forecast

Turkey construction sector forecast

BMI

Indicator 2013 2014 2015 2016 2016

Construction value (TRY bn) 70.46 78.91 88.11 98.24 109.34

Construction industry real growth (%) 6.50 5.35 5.78 5.63 5.30

Construction industry of GDP (%) 4.5 4.6 4.7 4.8 4.8

Gross fixed capital formation (TRY bn) 315.30 338.79 367.16 401.58 443.35

Construction industry employment (‘000) 1,616.3 1,710.2 1,817.1 1,927.3 2,036.9

Construction industry employees as % of total

labour force 3.22 3.36 3.52 3.68 3.85

Infrastructure industry value (TRY bn) 33.47 38.08 43.19 48.77 54.86

Infrastructure Industry Value As % of Total

Construction 47.5 48.3 49.0 49.6 50.2

Infrastructure Industry Value Real Growth (%) 6.1 7.1 7.5 7.0 6.5

Infrastructure Industry Value as % of GDP 2.1 2.2 2.3 2.4 2.4

Residential and Non-residential Building

Industry Value (TRY bn) 36.99 40.84 44.92 49.47 54.48

Residential and Non-residential Building

Industry Value As % of Total Construction 52.49 51.75 50.98 50.36 49.82

Residential and Non-residential Building

Industry Value Real Growth (%) 6.86 3.76 4.12 4.26 4.12

Residential and Non-residential Building

Industry Value as % of GDP 2.36 2.38 2.39 2.40 2.40

- 8 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Main Sector Indices

Construction production and turnover indices Construction cost index

Turkstat

0

20

40

60

80

100

120

140

160

180

200

Production index Turnover index

150

155

160

165

170

175

180

185

190

195

200

205

Residential buildings

Commercial, office, medical and school

- 9 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Comments

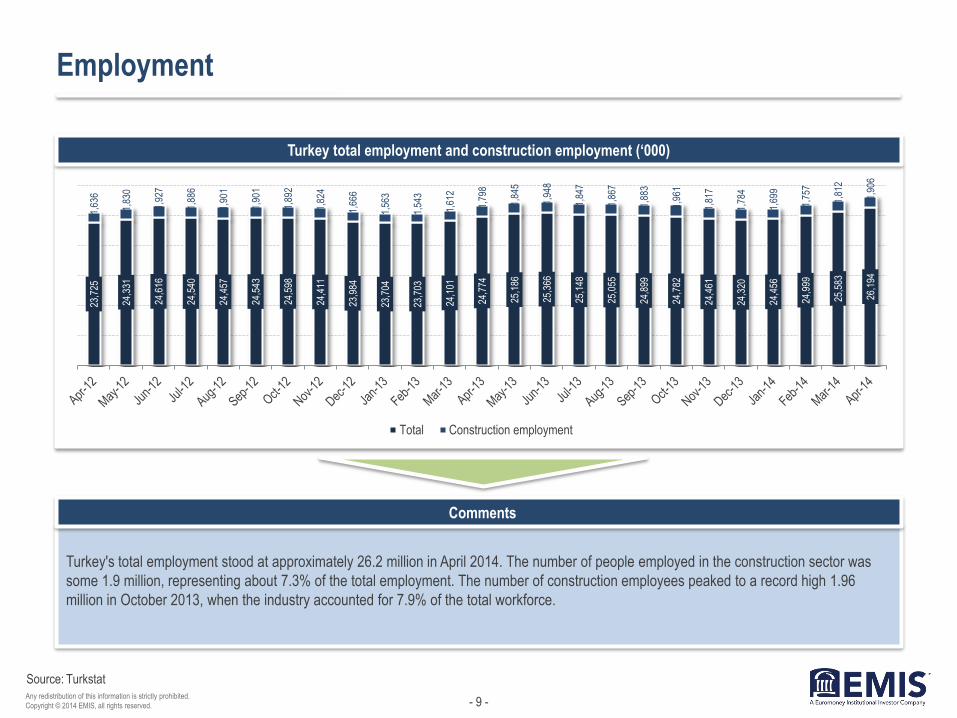

Employment

Turkey's total employment stood at approximately 26.2 million in April 2014. The number of people employed in the construction sector was

some 1.9 million, representing about 7.3% of the total employment. The number of construction employees peaked to a record high 1.96

million in October 2013, when the industry accounted for 7.9% of the total workforce.

Turkey total employment and construction employment (‘000)

Turkstat

23,7

25

24,3

31

24,6

16

24,5

40

24,4

57

24,5

43

24,5

98

24,4

11

23,9

84

23,7

04

23,7

03

24,1

01

24,7

74

25,1

86

25,3

66

25,1

48

25,0

55

24,8

99

24,7

82

24,4

61

24,3

20

24,4

56

24,9

99

25,5

83

26,1

94

1,63

6

1,83

0

1,92

7

1,88

6

1,90

1

1,90

1

1,89

2

1,82

4

1,66

6

1,56

3

1,54

3

1,61

2

1,79

8

1,84

5

1,94

8

1,84

7

1,86

7

1,88

3

1,96

1

1,81

7

1,78

4

1,69

9

1,75

7

1,81

2

1,90

6

Total Construction employment

- 10 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Employment and Salary Indices

Employment and salary indices Labour construction cost index

Turkstat

0

20

40

60

80

100

120

140

160

Employment index Gross wage & salary index

Hourly labour cost index Hours worked index

160

170

180

190

200

210

220

230

for residential buildings

for commercial, office, medicalbuildings

- 11 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

International Operations of Turkish Contractors in 2010-2013

Turkish contractors have signed international projects worth USD 31.3bn in 2013, up by 35.5%, compared with 2010. The biggest share of the

projects in terms of value are in Turkmenistan with a 23% share, followed by Russia and Iraq with shares of 16.9% and 11.6%, respectively.

Most of the projects, about 14% of the total, were for the construction of roads, tunnels and bridges, followed by residential projects.

International projects by country International projects by type

TMB

Turkmenistan 23.0%

Russia 16.9%

Iraq 11.6%

Saudi Arabia 5.2%

Azerbaijan 4.9%

Kazakhstan 4.5% Libya 3.6%

Iran 2.9% Qatar 2.5%

Other 24.9%

Road-Tunnel-Bridge 14.0%

Residential 12.6%

Airport 8.0%

Sports Facilities 7.0%

Business Center 7.0%

Power plant 5.6%

Tourist Facility 5.2%

Petrochemical 4.5%

Industrial 3.2% Railway 2.9%

Other 30.0%

- 12 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

International Operations of Turkish Contractors to Date

The total value of the international business of Turkish contractors amounted to USD 274.2bn between 1972 and 2013. The Turkish

companies were most active in Russia, Turkmenistan and Libya. Most of the projects implemented by the Turkish contractors over this period

were residential, road/bridge/tunnel and airport developments.

Intl business of Turkish contractors (USD bn) Distribution by country (1972-2013)

TMB

4.5

11.4 12.4

24.1 25.2 24.6

21.7 23.1

20.5

29.4 31.3

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013Russia 18.0%

Turkmenistan 14.6%

Libya 10.2%

Iraq 7.1%

Kazakhstan 6.4%

Saudi Arabia 4.8%

Qatar 4.5% UAE 3.2%

Azerbaijan 3.2%

Algeria 3.0%

Other 25.0%

- 13 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

M&A

Mergers and acquisitions in construction and related industries (2011–July 2014)

DealWatch

Date Target Company Deal Type Stake % Buyer Country of

Buyer Deal Industries

Deal Value

(USDmn)

Feb-11 Italicementi Set Group Acquisition 100 Limak

Holding Turkey

Cement and Concrete Product

Manufacturing 400

Jun-12 Kumas Kutahya Manyezit

Isletmeleri Privatization 100

Gozde

Girisim Turkey Nonmetallic Mineral Products 286

Jul-14 Sancim Bilecik Cimento Acquisition 100 Cimsa

Cimento Turkey

Cement and Concrete Product

Manufacturing 221

Mar-12 AE Arma Elektropanc Acquisition 80 Imtech Netherlands Construction 187

Apr-12 Ozisik Insaat Acquisition 93

Cemas

Dokum

Sanayi

Turkey Construction 116

Nov-12 Yesil Insaat Acquisition 100 Borova Yapi Turkey Construction 106

Nov-13 Cemre Insaat Minority stake purchase 37 Jadwa

Investment Saudi Arabia

Residential Building

Construction 100

May-11 Afyon Cimento Minority stake purchase 26

Institutional

and private

investors

Turkey Cement Manufacturing 82

Jan-12 Graniser Granit Seramik

Sanayi Acquisition 75

Bancroft

Private Equity

United

Kingdom

Ceramic Wall and Floor Tile

Manufacturing 75

Feb-13 Akfil Holding ; Garanti Koza

Akis Adi Ortakligi Minority stake purchase

Garanti-Koza

Insaat Turkey

Land Subdivision and Land

Development 62

- 14 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

II. Construction and Occupancy Permits

- 15 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Construction Permits by Number of Buildings

Local municipalities granted construction permits for 117,663 buildings in 2013, the highest number in three years. Most of the permits

are for residential buildings, followed by the wholesale and retail segment. A total 2,563 permits for the construction of office buildings were

issued during the year, registering the highest rise of over 34%.

Number of buildings (‘000) Distribution by buildings type (2013)

Turkstat

75.5

114.3 114.2 106.7

95.2 92.3

139.6

101.9 104.8

117.7

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Residential building with

two and more dwellings 66%

Single dwelling building 19%

Wholesale & retail trade 3%

Industrial & Warehouses

3%

Other 9%

- 16 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Floor Area of Construction Permits

The total floor area of buildings with newly-issued construction permits rose by almost 10% to 168.9 million m2 in 2013. Residential buildings with two and

more dwellings accounted for the biggest share of permits in terms of floor area, followed by public entertainment, education, hospital or institutional care

buildings and industrial buildings.

The highest increase of 26.5% was registered in the floor area of permits issued for hotels and other accommodation buildings, followed by industrial

buildings and warehouses with an 18.7% growth. A decrease of 22.6% was registered in the floor area of permits issued for the construction of buildings

used in wholesale and retail trade.

Floor area of issued construction permits (million m2) Floor area by building type 2013

Turkstat

69.7

106.4

122.9 125.1

103.8 100.7

176.4

123.6

153.7

168.9

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Residential building with two and more dwellings 72%

Public entertainment,

education, hospital 6%

Industrial & warehouses

5% Wholesale &

retail 4%

Office 4%

Other 9%

- 17 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Construction Permits Value

The total value of buildings with newly-issued construction permits rose by 15.5% to an all time high of TRY 121.8bn in 2013. Residential

buildings with two and more dwellings represented nearly 73% of the value of the newly-issued construction permits. The highest growth of

36.9% was registered in the value of permits issued for hotels and other accommodation buildings, which totalled TRY 3.3bn. Industrial

buildings and warehouses segment followed with a 24.8% increase to TR 5.5bn. The only shrinking segment was that of wholesale and retail

trade buildings, with a drop of 19.6% to TRY 4.8bn in the value of issued construction permits.

Value of issued construction permits (TRY bn) Value by building type (2013)

Turkstat

24.1

40.5

56.2 61.3 59.0

54.4

101.9

80.8

105.5

121.8

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Residential building with

two and more dwellings 73%

Public entertainment

6% Industrial &

Warehouses 5%

Office 4%

Wholesale & retail 4%

Other 9%

- 18 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Occupancy Permits by Number of Buildings

The total number of buildings with newly-issued occupancy permits rose by 23.9% to 118,036 in 2013. Residential buildings with two

and more dwellings accounted for 63 of the newly-issued occupancy permits. The highest annual increase of was registered in the occupancy

permits issued to hotels & accommodation buildings and traffic & communication buildings, which more than doubled to 1,661 and 153,

respectively.

Number of buildings (‘000) Distribution by buildings type (2013)

Turkstat

40.8

64.1 73.4

68.1 76.1

94.8

82.1

98.3 95.2

118.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Residential building with

two and more dwellings 63%

Single dwelling

building 22%

Wholesale & retail trade 6%

Industrial & Warehouses

3%

Other 6%

- 19 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Floor Area of Occupancy Permits

The total floor area of buildings with newly-issued occupancy permits rose by 28.3 to 134.1 million m2 in 2012. Most of the permits were

issued to residential buildings, followed by buildings for wholesale and retail trade. The highest annual increase was registered in the floor

area of permits issued for traffic and communication buildings as well as for hotels and accommodation buildings.

Floor area of issued occupancy permits (million m2) Floor area by building type (2013)

Turkstat

31.0

50.3 57.2

63.4 71.0

94.6 85.3

105.7 104.5

134.1

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Residential building with

two and more dwellings

71.5%

Wholesale & retail 6.3%

Industrial & warehousing

5.8%

Public entertainment,

education, hospital 3.8%

Other 12.5%

- 20 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Occupancy Permits Value

The total value of buildings with newly-issued occupancy permits surged by 36.5% to record high TRY 94.9bn in 2013. Significant growth was

seen in all segments with the highest increases registered in the value of permits issued for traffic and communication buildings with 85.5% as

well as for hotels and accommodation buildings with 74.2%.

Value of issued occupancy permits (TRY bn) Value by building type (2013)

Turkstat

10.3

18.4 25.1

30.4

39.0

49.4 47.4

67.0 69.5

94.9

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Residential building with two and more

dwellings 72.5%

Wholesale & retail 6.1%

Industrial & Warehouses

5.5% Public

entertainment, education,

hospital 3.8%

Single dwelling building 3.4%

Other 9%

- 21 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

III. Homes and Commercial Centers

- 22 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Home Prices and Sales

House price index

Dwellings sales in units

Central Bank, Turkstat

020406080

100120140160180

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb

-12

Mar

-12

Apr

-12

May

-12

Jun-

12

Jul-1

2

Aug

-12

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb

-14

Mar

-14

Apr

-14

173,

949

194,

888

162,

648

176,

790

144,

845

173,

515

170,

333

212,

928 27

3,82

6

295,

010

293,

318

282,

835

257,

853

266,

923

Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12 Q3'12 Q2'12 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14

- 23 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

New House Price Index

New house prices rose by 0.34% month-on-month and by 12.05% year-on-year in June 2014, according to New House Price Index calculated

by REIDIN.com and GYODER. The prices increased by 13.62% in 2013 and by 44.3% since January 2010 when the index was introduced.

New house price index Monthly growth of new house prices (%)

Central Bank, REIDIN-GYODER

0

20

40

60

80

100

120

140

160

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep

-11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep

-12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep

-13

Nov

-13

Jan-

14

Mar

-14

0.55

0.23

1.02

0.31

0.54

1.84 1.88

2.66

1.51

1.06 0.98

0.28 0.49

0.34 0.41

1.03

0.47 0.34

Jan-

13

Feb

-13

Mar

-13

Apr

-13

May

-13

Jun-

13

Jul-1

3

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14

Feb

-14

Mar

-14

Apr

-14

May

-14

Jun-

14

- 24 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Housing Loans

The volume of housing loans increased by 284% to over TRY 110bn in 2013. Housing loans accounted for over 45% of consumer loans and

10.5% of total loans at the end of 2013.

Most of the housing loans are extended for 5 to 10 years and the size of an average housing loan is some TRY 84,000 (USD 38,000).

Housing loans and average interest rate Housing loans outstanding (TRY bn)

Central Bank, GYODER

0.81

0.92

1.04

1.20

1.10 1.05

0.98 0.83

0.76 0.69

0.91 0.89

0.65 0.71 0.73 0.75 0.75 0.78 0.78 0.81

0.85 0.92

1.06 1.10

Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12 Q3'12 Q2'12 Q1'13 Q2'13 Q3'13 Q4'13

Monthly interest rate (%) Extended loans (100 mn TRY)

12.79

23.20

32.23 38.78

44.69

60.69

74.51

85.95

110.43

2005 2006 2007 2008 2009 2010 2011 2012 2013

- 25 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Housing Lending by Quarters

The number and volume on newly-extended housing loans peaked in the second quarter of 2013 with the decline in interest rates. Over

198,000 borrowers received housing loans worth more than TRY 16.8bn in the second quarter of 2013.

Volume of newly issued housing loans (TRY bn) Number of borrowers of new housing loans (‘000)

Banks Association of Turkey

9.8 9.4

5.3 5.3 4.8

6.8 6.5

10.3

12.3

16.9

11.2

9.9

7.2

Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12 Q3'12 Q4'12 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14

135.2 124.6

75.1 79.2 66.6

87.8 85.4

133.0

152.5

198.0

130.4 114.9

85.6

Q1'11 Q2'11 Q3'11 Q4'11 Q1'12 Q2'12 Q3'12 Q4'12 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14

- 26 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Shopping Centers

Total number and leasable space of shopping centers

In 2013, 30 new Turkish shopping centers opened

doors adding over 1.0 million m2 to the total leasable

area across the country.

At the end of 2013, the country had 326 shopping

centres with combined leasable area of 9.25 million

m2. Local investors account for around 66% of the

operating shopping centres in terms of leasable area.

The share of foreign investors is 27% and the

remaining ownership is mixed.

By the end of 2016, the total number of shopping

centres in Turkey is expected to increase to some

450. Their total leasable area is seen at around 13.6

million m2.

Leasable area per capita (m2)

GYODER

3.1 4.1 5.1 5.8 6.5 7.6 8.2 9.2 11.2

12.8 13.6 117 145

189 207 232

264 296

326

389 431 449

0

100

200

300

400

500

0

2

4

6

8

10

12

14

16

2006 2007 2008 2009 2010 2011 2012 2013 2014(e)

2015(e)

2016(e)

Leasable area ('000 m2) Number of shopping centres

57.6

71.2 79.9

88.6

101.9 108.8

122.5

2007 2008 2009 2010 2011 2012 2013

- 27 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

IV. Related Industries

- 28 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Cement & Clinker Industry

Cement and clinker production (million tons)

Turkey is the largest European and world's fourth

biggest cement producer after China, India and the

United States.

The Turkish cement producers increased their output

by 11.7% % to 71.3 million tons in 2013, according to

data of Turkish Cement Manufacturers Association

(TCMB).

The total output figure does not include production of

manufacturers, which are not TCMB members.

Domestic sales of TCMB members rose by 13% to

53.9 million tons in 2013. They had a combined an

annual capacity of 107.7 million tons of cement and

68.5 million tons of clinker at the end of 2013.

The annual turnover of the Turkish cement sector is

estimated at some USD 4bn.

Domestic cement sales (million tons)

TCMB

49.3 51.4 54.0 62.7 63.4 63.9

71.3

41.6 44.7 46.2 52.8 54.3 54.8

60.2

2007 2008 2009 2010 2011 2012 2013

Cement Clinker

42.5 40.6 40

47.7 52.3 53.9

60.9

2007 2008 2009 2010 2011 2012 2013

- 29 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Comments

Source:

Steel Industry

Turkey's crude steel production decreased by 3.4% to 34.6 million tons in 2013 but kept its place as the eighth biggest steel manufacturer in

the world despite the decline. The country's production reached a record high 35.9 million tons in 2012.

Turkish steel exports declined 7.9% in value terms to USD 15.78bn in 2013, while imports rose by 14.1% to USD 12.81bn.

Crude steel production and consumption (million tons) Steel & iron foreign trade (million tons)

DCUD

25.8 26.8 25.3

29.1

34.1 35.9 34.7

23.8 21.5

18.0

23.6

26.9 28.5

31.3

2007 2008 2009 2010 2011 2012 2013

Production Consumption

16.7

20.0 18.7

17.6 18.5

20.3 19

13.9 13.6

10.5 11.1 10.7 11.6

14.9

2007 2008 2009 2010 2011 2012 2013

Exports Imports

- 30 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

V. Latest Developments

- 31 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Latest Developments Part I

Infrastructure

investment Turkey will need to invest some USD 700bn in infrastructure projects until 2023, Deputy Prime Minister Ali Babacan

said in late June 2014. Of these, about USD 200bn are to be spent through public-private-partnerships (PPP).

Enka

In July 2014, Turkish energy-to-construction firm Enka Insaat and Bechtel, the largest U.S. engineering company,

were selected by the government of Kosovo to build a new 60-kilometer motorway linking the capital Pristina with

neighboring Macedonia. The project will cost EUR 600mn. This is the second motorway contract awarded to the

consortium in Kosovo.

Gas Storage

Construction

In July 2014, World Bank approved an additional financing of USD 400mn to the already existing Gas Sector

Development Project in Turkey. The additional loan would finance the cost overrun in the Tuz Golu gas storage

facility. The original USD 325mn project, approved in 2005, consists of two component and the gas storage facility

and a network expansion.

Bosphorus

Bridges

In May 2014, Turkish construction firm IC Ictas and Italy's Astaldi announced the financial close of a USD 2.3bn

loan extended by a group of local lenders for the construction of a third Bosphorus bridge. The overall value of the

project is about USD 2.9bn. The concession has a 10-year duration with 30 months allocated for construction.

Tekfen

In May 2014, Tekfen Holding said its contracting subsidiary Tekfen Insaat's 40% subsidiary Azfen JV and Italian oil

services company Saipem have won a USD 735mn contract to build a natural gas pipeline in Shah Deniz Phase II

natural gas project in Azerbaijan.

- 32 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Latest Developments Part II

Ronesans

Insaat In May 2014, Turkish builder Ronesans Insaat started the construction of a USD 450mn St. Petersburg Kola

Industrial Park in Russia. The development will include industrial buildings, warehouses and office buildings.

Third

Istanbul

Airport

The government will not provide state guarantee for the construction of the third airport project in Istanbul, Treasury

Undersecretary, Ibrahim Canakci, said in May 2014. The EUR 22.15bn project was won by the Cengiz-Kolin-Limak-

Mapa-Kalyon consortium, which will operate the airport for 25 years. The airport will have six runways and service

150 million passengers annually.

Elitas, Kur

and Intas

A consortium made up of Turkish construction companies Elitas, Kur and Intas won a USD 415mn tender to build

the 60 Metre Street in Sulaymaniyah, in Iraq's Kurdistan region. The project is scheduled to be completed in three

years.

TANAP The construction of Trans-Anatolian Natural Gas Pipeline (TANAP) will start in April 2015, the project's general

manager, Saltuk Duzyol, said in April 2014. The USD 20bn pipeline will transport natural gas from the Shah Deniz II

field in Azerbaijan to Europe starting from 2018 or 2019. The construction was initially planned to start in 2013.

Akkuyu

nuclear plant

In February 2014, Russia's Atomstroyexport said it will may start the construction Turkey's first nuclear plant in

Akkuyu on the Mediterranean coast as soon as it receives environmental impact report approval in April or May this

year. The total cost of the 4,800 MW plant is estimated at USD 20bn.

- 33 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

VI. Main Players

- 34 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Highlights

Source:

Tekfen Holding

Financial performance (TRY mn)

Contracting group performance (TRY mn)

Tekfen Holding was established in 1956 as an

engineering and consultancy firm. Currently the group

comprises contracting, agri industry, real estate and

other divisions.

Tekfen continued operations in eight countries in

2013. It had a backlog of USD 3bn at the end of 2013.

Backlog abroad constitutes 84% of the total.

This portfolio, concentrating mainly on three

geographical regions, namely the Caspian Region,

Middle East and North Africa, includes, besides

Turkey, Azerbaijan, Turkmenistan, Iraq, Saudi Arabia,

Qatar, Morocco and Libya.

The group has three manufacturing plants in Derince,

Ceyhan in Turkey and in Baku, Azerbaijan.

Tekfen Holding had total assets of TRY 4.7bn and

workforce of over 15,500 people at the end of 2013.

Company data

3,949 3,846 3,991

300

-64

151 281 10 272

2012 2013 2014 (projected)

Revenues Net profit EBIDTA

2,395 2,327 2,445

24

-217

37 142

-100

167

2012 2013 2014 (projected)

Revenues Net profit EBIDTA

- 35 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Tekfen Holding (cont’d)

Revenue breakdown (2013)

Investment (TRY mn)

Backlog by countries (end-2013)

Workforce (2013)

Company data

Contracting 60.5%

Agri industry 37.0%

Real estate 0.8%

Other 1.7%

Contracting 87.8%

Agri-industry 6.7%

Real estate 2.2%

Other 3.3%

78.4

142.6

24.7

11.4

49.9

158.4 6.7

0.8 1.0

96.5 193.3 184.1

0

50

100

150

200

250

2011 2012 2013

Contracting Agri Industry

Other (incl. real estate) Total

Turkey 15.8% Turkmenistan 1.1%

Azerbaijan 55.3%

Saudi Arabia 3.5% Marocco 1.4%

Qatar 18.4%

Libya 3.3%

Iraq 1.2%

- 36 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Highlights

Source:

Enka Insaat

Financial performance (USD mn)

Construction operations performance

Enka was founded in 1957. It active in construction, power

generation, real estate investment and management,

trading and manufacturing.

The company undertakes projects in Turkey, Russia and

the CIS region, the MENA region and Europe, usually with

international contractors and often with its long-standing

partner U.S.-based Bechtel.

Enka Insaat had a project backlog of USD 3.17bn in the

construction segment at the end of 2013. The group

employs over 25,300.

Company data

5,037 5,746

6,547

509 628 656 857 708 1,032

2011 2012 2013

Revenues Net profit EBIDTA

993

1,384

2,550

259 125

357

2011 2012 2013

Revenues EBIDTA

- 37 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Enka Insaat (cont’d)

Real estate performance (USD mn)

Revenue distribution (2013)

Backlog by countries (end-2013)

Ownership

Company data

407 442

478

306 308 346

2011 2012 2013

Revenues EBIDTA

Construction 37.7%

Power generation

48.6%

Real estate 7.1%

Trade & manufacturing

6.6%

Iraq 37.1%

US Embassy Projects 14.3%

Russia 10.4%

Oman 9.8%

Gabon 6.9%

Turkey 6.7%

USA 6.1%

Libya 3.1%

Kazakhstan 1.9%

Other 3.7%

Tara family 50.1%

Gulcelik family 31.6%

Enka Foundation

6.0%

Free float 12.3%

- 38 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Highlights

Source:

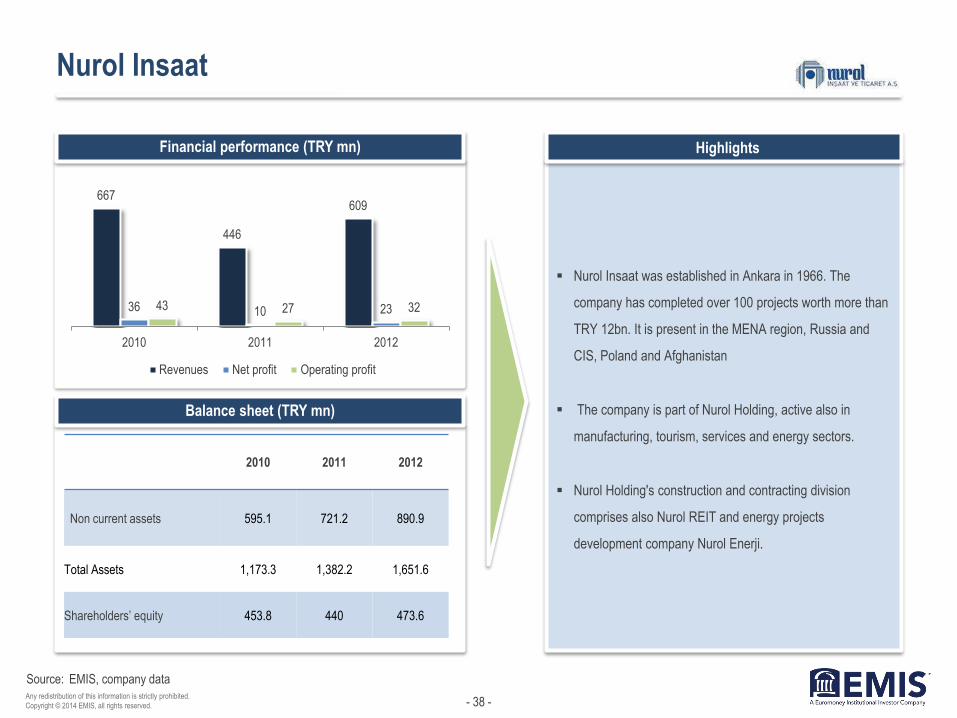

Nurol Insaat

Financial performance (TRY mn)

Balance sheet (TRY mn)

Nurol Insaat was established in Ankara in 1966. The

company has completed over 100 projects worth more than

TRY 12bn. It is present in the MENA region, Russia and

CIS, Poland and Afghanistan

The company is part of Nurol Holding, active also in

manufacturing, tourism, services and energy sectors.

Nurol Holding's construction and contracting division

comprises also Nurol REIT and energy projects

development company Nurol Enerji.

EMIS, company data

2010 2011 2012

Non current assets 595.1 721.2 890.9

Total Assets 1,173.3 1,382.2 1,651.6

Shareholders’ equity 453.8 440 473.6

667

446

609

36 10 23 43 27 32

2010 2011 2012

Revenues Net profit Operating profit

- 39 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Highlights

Source:

Nurol REIT

Financial performance (TRY mn)

Ownership

Nurol REIT, part of Nurol Group, was established in

September 1997. It was listed on the Istanbul Stock

Exchange in December 1999.

The company’s current portfolio includes Nurol Plaza

office building and Nurol Zekeriyakoy Houses in

Istanbul, Nurol Residence and Karum Business and

Shopping Center in Ankara and shopping, culture and

entertainment center Oasis in seaside resort Bodrum.

The company has another three mix-use

developments - Nurol Tower, Nurol Park and

Seyrantepe projects, all in Istanbul.

Nurol REIT plans to invest USD 340mn in Nurol Park

project, which it will develop on the land of former

Hurriyet Medya Tower, acquired from Dogan Group for

USD 127.5mn.

Company data

Nurol Insaat 31.97%

Nurol Yatirim Bankasi 15.97%

Free float 52.03%

Other 0.04%

2011 2012 2013

Net sales 4.6 4.3 8.4

Net profit/loss 1 7.1 -17.3

Total assets 178.6 508.1 840.5

- 40 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Highlights

Source:

Cimsa

Financial performance (TRY mn)

Owenership

Cement producer Cimsa, established in 1972, is part

of industrial conglomerate Sabanci Holding and is

listed on Borsa Istanbul.

The company operates five integrated factories,

located in Mersin, Kayseri, Eskisehir, Nigde and

Afyon. It has a grinding facility in Ankara, s terminal in

Marmara region and a cement packing plant in

Malatya. The company has 35 ready-mix concreate

plants across Turkey.

In 2012, Cimsa acquired 51% of cement manufacturer

Afyon Cimento from Italy's ItalCementi Group for USD

32.4mn and in July 2014 it agreed to purchase rival

Sancim for USD 220.7mn.

Cimsa is the third largest white cement manufacturer

worldwide. It is present in 46 countries through

subsidiaries and terminals, including in Spain,

Germany, Romania and Russia.

Company data

801 857

954

123 111

302 201 192 234

2011 2012 2013

Revenues Net profit EBITDA

Sabanci Holding 49.42%

Aberdeen Asset Management 13.79%

Adana Cimento 5.11%

Akcansa Cimento 8.98%

Sabanci Foundation 0.11%

Other 22.59%

- 41 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Source:

Cimsa (cont’d)

Cement production (million tons)

Clinker production (million tons)

Cement products by type (2013)

Clinker products by type (2013)

Company data

5.6

6.1

6.3

2011 2012 2013

4.9

5.2

5.5

2011 2012 2013

Grey cement 84%

White cement 16%

Other products 1%

Grey clinker 81%

White clinker 19%

Other products 1%

- 42 - Any redistribution of this information is strictly prohibited.

Copyright © 2014 EMIS, all rights reserved.

Contact:

Corporate Headquarters

Nestor House

Playhouse Yard

London EC4V 5EX

UK

Voice: +44 207 779 8471

Fax: +44 207 779 8224

Americas Headquarters

225 Park Avenue South

New York, New York 10003

US

Voice: +1 212 610 2900

Fax: +1 212 610 2950

Asia Headquarters

Eucharistic Congress Bldg. No.

III

4th Floor, 5 Convent Street

Mumbai 400 001

India

Voice: +91 22 22881123

Fax: +91 22 22881137

Disclaimer:

The material is based on sources which we believe are reliable, but no warranty, either expressed or implied, is provided in relation to the accuracy or completeness

of the information. The views expressed are our best judgment as of the date of issue and are subject to change without notice. EMIS and Euromoney Institutional

Investor PLC take no responsibility for decisions made on the basis of these opinions.

Any redistribution of this information is strictly prohibited. Copyright © 2014 EMIS, all rights reserved. A Euromoney Institutional Investor company.

About EMIS Insight

EMIS Insight is a unit of EMIS that produces proprietary strategic research and analysis. The service features market overviews, industry trend analysis, legislation

and profiles of the leading sector companies provided by locally-based analysts.

About EMIS

Founded in 1994, EMIS (formerly known as ISI Emerging Markets) was acquired by Euromoney Institutional Investor PLC in 1999. EMIS works from over 15 offices

around the world to deliver electronic information products, by subscription, to institutional customers globally. EMIS provides hard-to-get information covering more

than 100 emerging markets. Its flagship products are EMIS Intelligence and EMIS Professional.

EMIS clients include top investment banks, corporations, law firms, consultants, investment and insurance companies, universities and libraries, multilateral

organizations, and others.