CONSTRUCTION CONTRACT & MANAGEMENT ISSUESentrusty.com/articles/MBJ-Vol-4-2010.pdf · On overheads,...

9

60 Master Builders 4 th Quarter 2010 Articles CONSTRUCTION CONTRACT & MANAGEMENT ISSUES In this 4 th quarter 2010 issue of Master Builders Journal for 2011, BK Burns & Ong Sdn Bhd, a subsidiary of BK Asia Pacific, a regional group providing project, commercial and contractual management services joins with Entrusty Group, a multi-disciplinary group, collectively named as BK Entrusty, presents a new series of contract and management articles in construction related areas of project, commercial, contracts, risks, quality and value, on “What is head office overheads?” INTRODUCTION e calculation of head office overheads or “extended home office overheads” have been puzzling many in the construction industry for a number of years. As we could see later in this article, case laws continue to refine and define head office overheads until today. Simplistically, Clark and Lorenzni (1997) cited “ese fixed (overhead) costs include items, such as office rental, utilities, janitorial services and corporate management.” e RICS (2000) defined it as “..expenditure on support services and general running costs, Overheads refer to the contractor’s general running of business as distinct from site costs of any particular contract. Overheads include, the rental of the contractor’s building and general support staff, and if they are proved to have been increased by the contract’s delay, there is no doubt, in principle, that they can be claimed (Finnegan and Sheffield City Council 1998).” is article discusses claims for head office overheads and the relevant case laws to elaborate the background which defined the methods of calculating before briefly moving into contractual definitions and formulas, and proceeding to, illustrating the application of the additional overheads methods discussed in a real project. CONTRACTUAL DEFINITION e term “head office overheads” is often not included in both local and international contracts but is usually included as one of the heads of claims under the clauses of Loss and/or Expense. For examples of Head Office overheads, please refer to the tabulated head offices items in the following section on Application. In Clause 24.1 of PAM 2006, the claim for head office overheads is implied in “...by matters expressed in Clause 24.3, and the Contractor has incurred or is likely to incur loss and/or expense which could not be reimbursed by a payment made under any other provision in the Contract, the Contractor may claim for such loss and/or expense provided...” Again, in PWD203 (2007), the same is elaborated under Clause 44 which states “If at any time during the regular progress of the Works or any part thereof has been materially affected by reason of delays as stated under clause 43.1 (c), (d), (e), (f) and (h), and the Contractor has incurred direct loss and/or expense beyond that reasonably contemplated and for which the Contractor would not be reimbursed by a payment made under any other provision in this Contract,...”. In CIDB (2000), the head office overheads claim is embedded within the expressed term of Clause 31, “e Contractor shall be entitled to recover Loss and Expense sustained or incurred by him and for which he would not be reimbursed by any other provision of the Contract, however arising as a result of the regular progress and/or completion of the Works or any section of the Works having been disrupted, prolonged or otherwise materially affected by any of the following events:...” e term “Loss and Expense” is defined under Clause 1 (b) as “costs of an overhead nature actually and necessarily incurred on the Site..”. CASE LAWS Generally, claims for head office overheads are supported and defined in many case laws, the following are a few of them, which are commonly cited; In Tate & Lyle Food & Distribution and Another v GLC and Another (1982), the Court of Appeal held: “the expenditure of managerial time in remedying an actionable wrong can properly form the subject matter of a special head of damages. e onus was on the plaintiffs to prove the actual loss incurred, percentage figure being unacceptable. As they had not produced evidence as to actual loss they could claim nothing under this head.” In Euro Pools v Clydesdale Fabrication (2003), the Scottish Court held: “It may not leave the company out of pocket, in the sense of having to pay more to the managing director; nevertheless, the company will inevitably be deprived of part of the services that it would normally expect

Transcript of CONSTRUCTION CONTRACT & MANAGEMENT ISSUESentrusty.com/articles/MBJ-Vol-4-2010.pdf · On overheads,...

60Master builders 4 t h Q u a r t e r 2 0 1 0

Articles

CONSTRUCTION CONTRACT& MANAGEMENT ISSUESIn this 4th quarter 2010 issue of Master Builders Journal for 2011, BK Burns & Ong Sdn Bhd, a subsidiary of Bk Asia Pacific, a regional group providing project, commercial and contractual management services joins with Entrusty Group, a multi-disciplinary group, collectively named as Bk Entrusty, presents a new series of contract and management articles in construction related areas of project, commercial, contracts, risks, quality and value, on “What is head office overheads?”

INTRODUCTIONThe calculation of head office overheads or “extended home office overheads” have been puzzling many in the construction industry for a number of years. As we could see later in this article, case laws continue to refine and define head office overheads until today. Simplistically, Clark and Lorenzni (1997) cited “These fixed (overhead) costs include items, such as office rental, utilities, janitorial services and corporate management.” The RICS (2000) defined it as “..expenditure on support services and general running costs, Overheads refer to the contractor’s general running of business as distinct from site costs of any particular contract. Overheads include, the rental of the contractor’s building and general support staff, and if they are proved to have been increased by the contract’s delay, there is no doubt, in principle, that they can be claimed (Finnegan and Sheffield City Council 1998).”

This article discusses claims for head office overheads and the relevant case laws to elaborate the background which defined the methods of calculating before briefly moving into contractual definitions and formulas, and proceeding to, illustrating the application of the additional overheads methods discussed in a real project.

CONTRACTUAL DEfINITIONThe term “head office overheads” is often not included in both local and international contracts but is usually included as one of the heads of claims under the clauses of Loss and/or Expense.

For examples of Head Office overheads, please refer to the tabulated head offices items in the following section on Application.

In Clause 24.1 of PAM 2006, the claim for head office overheads is implied in “...by matters expressed in Clause 24.3, and the Contractor has incurred or is likely to incur loss

and/or expense which could not be reimbursed by a payment made under any other provision in the Contract, the Contractor may claim for such loss and/or expense provided...”

Again, in PWD203 (2007), the same is elaborated under Clause 44 which states “If at any time during the regular progress of the Works or any part thereof has been materially affected by reason of delays as stated under clause 43.1 (c), (d), (e), (f ) and (h), and the Contractor has incurred direct loss and/or expense beyond that reasonably contemplated and for which the Contractor would not be reimbursed by a payment made under any other provision in this Contract,...”.

In CIDB (2000), the head office overheads claim is embedded within the expressed term of Clause 31, “The Contractor shall be entitled to recover Loss and Expense sustained or incurred by him and for which he would not be reimbursed by any other provision of the Contract, however arising as a result of the regular progress and/or completion of the Works or any section of the Works having been disrupted, prolonged or otherwise materially affected by any of the following events:...” The term “Loss and Expense” is defined under Clause 1 (b) as “costs of an overhead nature actually and necessarily incurred on the Site..”.

CASE LAWSGenerally, claims for head office overheads are supported and defined in many case laws, the following are a few of them, which are commonly cited;

In Tate & Lyle food & Distribution and Another v GLC and Another (1982), the Court of Appeal held:

“the expenditure of managerial time in remedying an actionable wrong can properly form the subject matter of a special head of damages. The onus was on the plaintiffs to prove the actual loss incurred, percentage figure being unacceptable. As they had not produced evidence as to actual loss they could claim nothing under this head.”

In Euro Pools v Clydesdale fabrication (2003), the Scottish Court held:

“It may not leave the company out of pocket, in the sense of having to pay more to the managing director; nevertheless, the company will inevitably be deprived of part of the services that it would normally expect

61 4 t h Q u a r t e r 2 0 1 0Master builders

ArticlesArticles

from the managing director. That might mean, for example, that the managing director was unable to devote as much time as would otherwise have been possible to the planning of an important marketing initiative, or the development of a new product, or to general administration of the company’s affairs and the supervision of its employees. In any of these cases, the loss of time inevitably represents a loss of services provided by the managing director to the company. Thus in any case the existence of a loss is established.”

The calculation of head office overheads was assisted by a few precedence, which clarified the application of two approaches; a) formula in the opportunity costs approach and b) the actual costs approach.

On overheads, it is worth noting Keating on Construction Contracts (8th edition), states that;

“If a particular head office costs are proved to have been increased by a contract’s delay, they are recoverable. Examples would be the cost of extra telephone calls and postage in the period of delay...A contractor’s overhead are commonly taken to be recovered out of income from his business as a whole and ordinarily where completion of one contract is delayed the contractor claims to have suffered a loss arising from the diminution of his income from the job and hence the turnover of his business. But he continues to incur expenditure on overhead which he cannot materially reduce or, in respect of the site, can only reduce, if at all, to a limited extent. But for the delay, the workforce would have had the opportunity of being employed on another contract which would have had the effect of contributing to the overheads during the overrun period. There is some authority that a claim on this basis is sustainable. But it is suggested that, in order to succeed, a contractor has in principle to prove that there was other work available which, but for the delay, he would have secured but which in fact because of the delay he did not secure.”

Keating suggested that in order to succeed in the overheads claim, the contractor has to prove that due to the delay, the contractor was unable to secure another project as his workforce was tied up with the delayed project.

In Whittal Builders and Chester-le-Street District Council (1987), “Whittal”, the deputy official referee, Mr Recorder Percival QC in a sub trial said:

“What has to be calculated here is the contribution to off-site overheads and profit which the contractor might reasonably have expected to earn with these resources if not deprived of them. The percentage to be taken for overhead and profit for this purpose is not therefore the percentage allowed by the contractor in compiling price for this particular contract, which may have been larger or smaller than his usual percentage and may or may not have been realised. It is not that percentage that one has to take for this purpose, but the average percentage earned by the contractor on his turnover as shown by the contractor’s account.”

“Whittal” limits the calculation of overheads and profit to the contractor’s average percentage contribution to his head office overhead during the period of delay, based on the contractor’s annual audited account rather than the allowance made for the same by the contractor at the time of tendering.

In J.f. finnegan Ltd v Sheffield City Council (1988), the Court held:

“It is generally accepted that, on principle, a contractor who has delayed in completing a contract due to the default of his employer may properly have a claim for head office or off-site overheads during the period of delay in the basis that the work force, but for the delay, might have the opportunity of being employed on another contract, which would have had the effect of funding the overheads during the overrun period.”

This case encourages the claimant to accept the concept that the claim of head office overheads should be worked on the basis that the contribution to the head office overheads during the time of delay, could have been substituted by contribution for the same from another project had the same head office resources, equipment, etc been deployed in another project, and had the project in question not been delayed.

In Alfred McAlpine homes North v Property and Land Contractors (1995), the court held:

“There was no objection in principle to a claim for head office overheads made on the opportunity costs approach, and further that there was no objection in principle to such a claim being calculated by reference to a formula. It should be noted however that in this case the court in fact refused to adopt such an approach principally because it was the contractor’s working arrangement that they only ever undertook one construction project at a time and did not undertake another until the project was complete. It was therefore inappropriate to use opportunity costs as the basis of calculation.”

62Master builders 4 t h Q u a r t e r 2 0 1 0

Articles

The development of the above case defines another boundary as to when opportunity costs approach should be applied, and vice versa. The opportunity approach which is formulas dependent is permitted by the courts, primarily, during the time of high construction activity, and where business practise in the construction industry such as in Malaysia and Asia in general, which does not permit idling but is likely to continue to undertake new projects despite current delay in existing project(s). In the above case and in the case of Amec Building Ltd v Cadmus Investment Co Ltd (June 1996), the actual costs approach (additional overheads approach) is permitted by using a formula to arrive at the additional overheads.

fORMULA METhODSFrom the cases above described, it could be noted that apart from the actual costs approach in calculating both the “unabsorbed” and “additional” head office overheads, and amongst many other formulas, the loss of opportunity costs approach could be calculated based on the following three commonly used formulas namely, Hudson, Emden and Eichleay.

Hudson which was introduced during the boom of the 1970s simply derived the percentage of overheads and profit of the Contract Sum, proportioned the said to the period in delay over the contract period in weeks. This method is not preferred mainly due to the formula’s dependency on the adequacy of the tender and there is possibility of double counting as overheads and profit are already included in the tender sum.

On the other hand, the pre-condition for the application of Emden and Eichleay is the availability of other projects during the time of the delay. Eichleay, introduced in the 1960s, based the amount claimed on the delayed contractor’s total invoices in the contract period over total of all invoices of the organisation during the contract period, and multiplying the afore mentioned, with the ratio of delayed period of which overheads contribution are required over the contract period in weeks.

Emden uses actual percentage of head office overhead and profit multiplied by the contract sum over the contract period in weeks followed by multiplication of days in delay.

The following tabulations are the realigned formulas of the three commonly used methods.

hudson Emden Eichleay

(H.O/P%) x CS x PD 100 CP

H x CS x PD100 CP

1. (DCI in CP) x (TFOO in CP) = (RO in CP) (AIO in CP)2. DCROC = PWO CP3. PWO x PD = Amount Claimed

hudsonHO/P% = Head Office Overheads and/or Profit PercentageCS = Contract SumCP = Contract Period (in weeks)PD = Period of Delay (in weeks)

EmdenH = Head Office Percentage – arrived at by dividing the total overhead cost and profit of the contractor’s

organisation as a whole by the total turnover, all extracted from the contractor’s year end accounts.

CS = Contract SumCP = Contract Period (in weeks)PD = Period of Delay (in weeks)

63 4 t h Q u a r t e r 2 0 1 0Master builders

Articles Articles

EichleayDCI in CP = Delayed Contract’s Invoices in Contract PeriodAIO in CP = All Invoices of Organisation in Contract PeriodTFOO in CP = Total Fixed Overheads of Organisation in Contract PeriodRO in CP = Required Overhead contribution from delayed contract in Contract PeriodDCROC = Delayed Contract’s Required Overhead ContributionCP = Contract Period ( in weeks)PWO = Potential Weekly Overhead contribution from delayed contract organisation

Eichleay is more sophisticated and perhaps more precise for the calculation as compared to Emden’s and Hudson’s. The distinction between Emden’s and Hudson’s is the calculation of percentage of overheads and profit. In Emden’s, as defined in Whittal, the said percentage is the average percentage the contractor in delay is to incur for overheads and profit for all his projects. Unlike Hudson’s, where the same percentage is the allowance made by the contractor in delay, for his tender for the specific project. The said percentage in Hudson’s, due to the circumstances in the project in delay, may deviate from the contractor’s norm in pricing his overheads and profit, hence, the inaccuracy. Emden’s has improved on this aspect. Eichleay has relatively higher accuracy because not only the calculation is based on the actual invoices for both the total contract sum and all the contract running in tandem in the organisation during the time of the delay, but also, the percentage of overheads and profit is derived from the average of at least three years’ of the organisation’s audited account.

ThE APPLICATIONThis section illustrates the application for claim of the contribution to head office overheads in a real life project, the delayed Project X. This head of claim was based on the actual costs (additional head office overheads) approach.

Project X’s original commencement and completion were 15 Sep 1996 and 15 Jan 1998, respectively. Interestingly, Project X experienced two stop work orders; on 5 Mar 1997 and again on 14 May 1999. In the first stop work order, the contractor was told to be on standby but nevertheless, was told to demobilise on 14 Dec 1997 and subsequently, told to remobilise on the 23 Feb 1998. The latter stop work order was the result of a determination letter from the client dated 2 days earlier, 12 May 1999.

To add to the complication, the Construction Management and Builder’s Works were subcontracted from a Main Contractor, Contractor A to a Subcontractor, Contractor B and was consented by the Client, at the outset, leaving specialists and design works to remain with Contractor A; meaning two sets of head office overheads were to be determined.

Due to the double stop start nature of the delay, the following options were considered:a) loss of opportunity approach as a consequent from the first stop work order coupled with additional costs approach

consequent from the second stop work order;b) combining both delays in one approach, additional costs approach; andc) combining both delays in one approach, loss of opportunity approach

The period of 1996 to 1999 were a period of construction downturn, work was scarce and therefore the consideration of applying Option (a) and (c) which involved proof of loss of opportunity did not arise. The reasonable approach was to apply Option (b). If the scenario were to be lifted into a period of construction boom, Option (c) as opposed to Option (a) would have been selected as the “standby” requested by the client in the first stop work order would have affected site preliminaries more than head office overheads. However, should it be proven that during the boom, the particular contractor was still deprived of work, hence the head office overheads would have been under utilised and the first stop work order would have impacted on head office overheads, hence Option (b) would have been the choice forward.

CONTRACTOR A’S hEAD OffICE OvERhEADS CONTRIBUTIONIn the first set of actual head office overheads, the Main Contractor, Contractor A’s overheads were as calculated:

The overheads items were extracted from Contractor A’s Overheads Expenditure in year 1996, 1997 and 1998.

64Master builders 4 t h Q u a r t e r 2 0 1 0

Articles

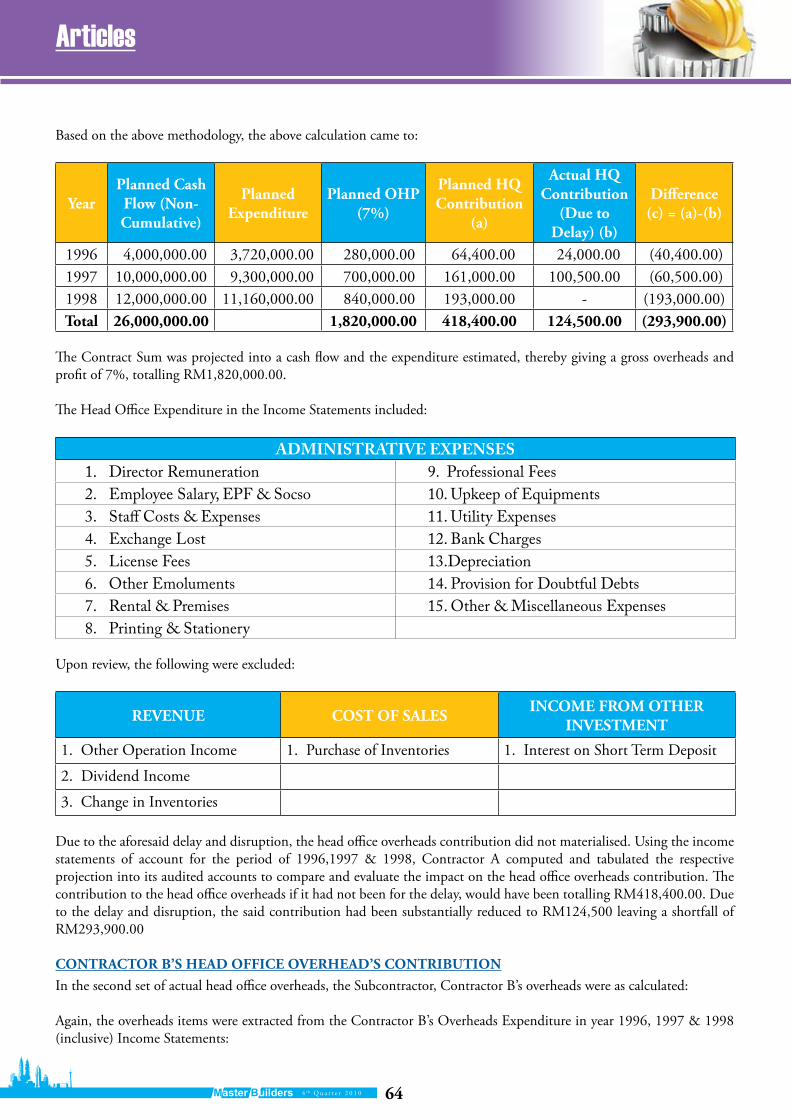

Based on the above methodology, the above calculation came to:

YearPlanned Cash flow (Non-Cumulative)

Planned Expenditure

Planned OhP (7%)

Planned hQ Contribution

(a)

Actual hQ Contribution

(Due to Delay) (b)

Difference (c) = (a)-(b)

1996 4,000,000.00 3,720,000.00 280,000.00 64,400.00 24,000.00 (40,400.00)1997 10,000,000.00 9,300,000.00 700,000.00 161,000.00 100,500.00 (60,500.00)1998 12,000,000.00 11,160,000.00 840,000.00 193,000.00 - (193,000.00)Total 26,000,000.00 1,820,000.00 418,400.00 124,500.00 (293,900.00)

The Contract Sum was projected into a cash flow and the expenditure estimated, thereby giving a gross overheads and profit of 7%, totalling RM1,820,000.00.

The Head Office Expenditure in the Income Statements included:

ADMINISTRATIVE EXPENSES1. Director Remuneration 9. Professional Fees2. Employee Salary, EPF & Socso 10. Upkeep of Equipments3. Staff Costs & Expenses 11. Utility Expenses4. Exchange Lost 12. Bank Charges5. License Fees 13.Depreciation6. Other Emoluments 14. Provision for Doubtful Debts7. Rental & Premises 15. Other & Miscellaneous Expenses8. Printing & Stationery

Upon review, the following were excluded:

REvENUE COST Of SALES INCOME fROM OThER INvESTMENT

1. Other Operation Income 1. Purchase of Inventories 1. Interest on Short Term Deposit

2. Dividend Income

3. Change in Inventories

Due to the aforesaid delay and disruption, the head office overheads contribution did not materialised. Using the income statements of account for the period of 1996,1997 & 1998, Contractor A computed and tabulated the respective projection into its audited accounts to compare and evaluate the impact on the head office overheads contribution. The contribution to the head office overheads if it had not been for the delay, would have been totalling RM418,400.00. Due to the delay and disruption, the said contribution had been substantially reduced to RM124,500 leaving a shortfall of RM293,900.00

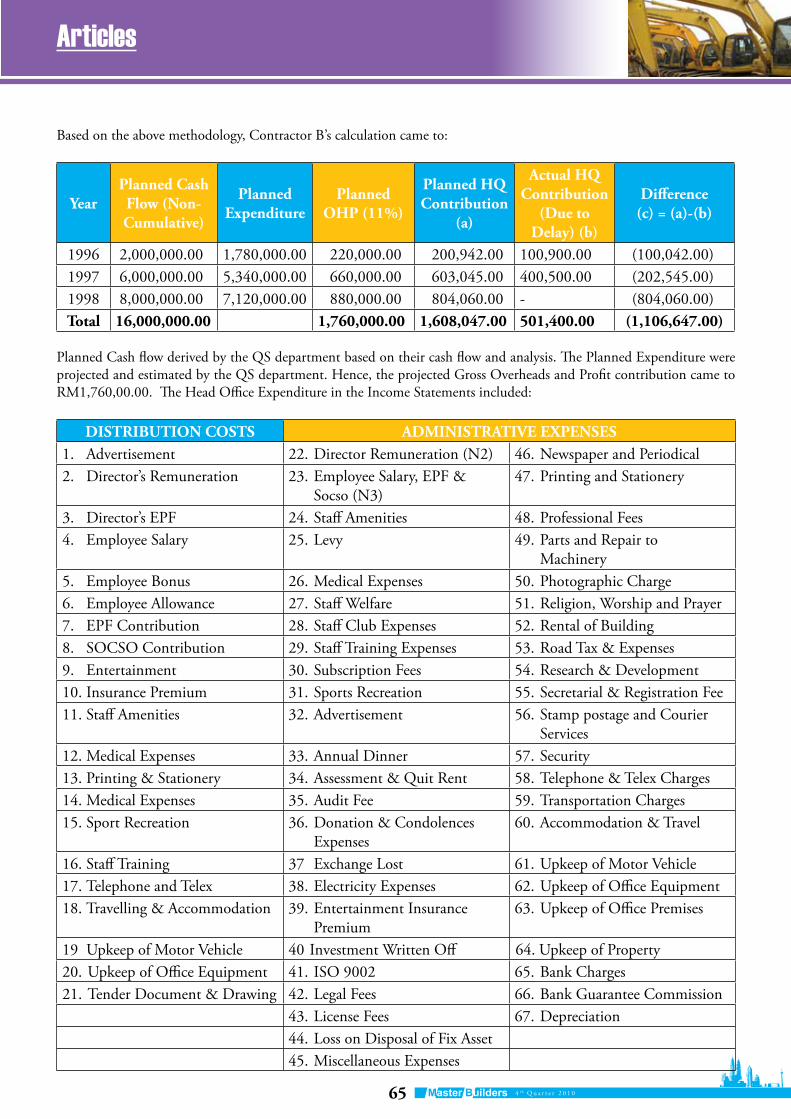

CONTRACTOR B’S hEAD OffICE OvERhEAD’S CONTRIBUTIONIn the second set of actual head office overheads, the Subcontractor, Contractor B’s overheads were as calculated:

Again, the overheads items were extracted from the Contractor B’s Overheads Expenditure in year 1996, 1997 & 1998 (inclusive) Income Statements:

65 4 t h Q u a r t e r 2 0 1 0Master builders

ArticlesArticles

Based on the above methodology, Contractor B’s calculation came to:

YearPlanned Cash flow (Non-Cumulative)

Planned Expenditure

Planned OhP (11%)

Planned hQ Contribution

(a)

Actual hQ Contribution

(Due to Delay) (b)

Difference (c) = (a)-(b)

1996 2,000,000.00 1,780,000.00 220,000.00 200,942.00 100,900.00 (100,042.00)1997 6,000,000.00 5,340,000.00 660,000.00 603,045.00 400,500.00 (202,545.00)1998 8,000,000.00 7,120,000.00 880,000.00 804,060.00 - (804,060.00)Total 16,000,000.00 1,760,000.00 1,608,047.00 501,400.00 (1,106,647.00)

Planned Cash flow derived by the QS department based on their cash flow and analysis. The Planned Expenditure were projected and estimated by the QS department. Hence, the projected Gross Overheads and Profit contribution came to RM1,760,00.00. The Head Office Expenditure in the Income Statements included:

DISTRIBUTION COSTS ADMINISTRATIvE EXPENSES1. Advertisement 22. Director Remuneration (N2) 46. Newspaper and Periodical2. Director’s Remuneration 23. Employee Salary, EPF &

Socso (N3)47. Printing and Stationery

3. Director’s EPF 24. Staff Amenities 48. Professional Fees4. Employee Salary 25. Levy 49. Parts and Repair to

Machinery5. Employee Bonus 26. Medical Expenses 50. Photographic Charge6. Employee Allowance 27. Staff Welfare 51. Religion, Worship and Prayer7. EPF Contribution 28. Staff Club Expenses 52. Rental of Building8. SOCSO Contribution 29. Staff Training Expenses 53. Road Tax & Expenses9. Entertainment 30. Subscription Fees 54. Research & Development10. Insurance Premium 31. Sports Recreation 55. Secretarial & Registration Fee11. Staff Amenities 32. Advertisement 56. Stamp postage and Courier

Services12. Medical Expenses 33. Annual Dinner 57. Security13. Printing & Stationery 34. Assessment & Quit Rent 58. Telephone & Telex Charges14. Medical Expenses 35. Audit Fee 59. Transportation Charges15. Sport Recreation 36. Donation & Condolences

Expenses60. Accommodation & Travel

16. Staff Training 37 Exchange Lost 61. Upkeep of Motor Vehicle17. Telephone and Telex 38. Electricity Expenses 62. Upkeep of Office Equipment18. Travelling & Accommodation 39. Entertainment Insurance

Premium63. Upkeep of Office Premises

19 Upkeep of Motor Vehicle 40 Investment Written Off 64. Upkeep of Property20. Upkeep of Office Equipment 41. ISO 9002 65. Bank Charges21. Tender Document & Drawing 42. Legal Fees 66. Bank Guarantee Commission

43. License Fees 67. Depreciation44. Loss on Disposal of Fix Asset45. Miscellaneous Expenses

66Master builders 4 t h Q u a r t e r 2 0 1 0

Articles

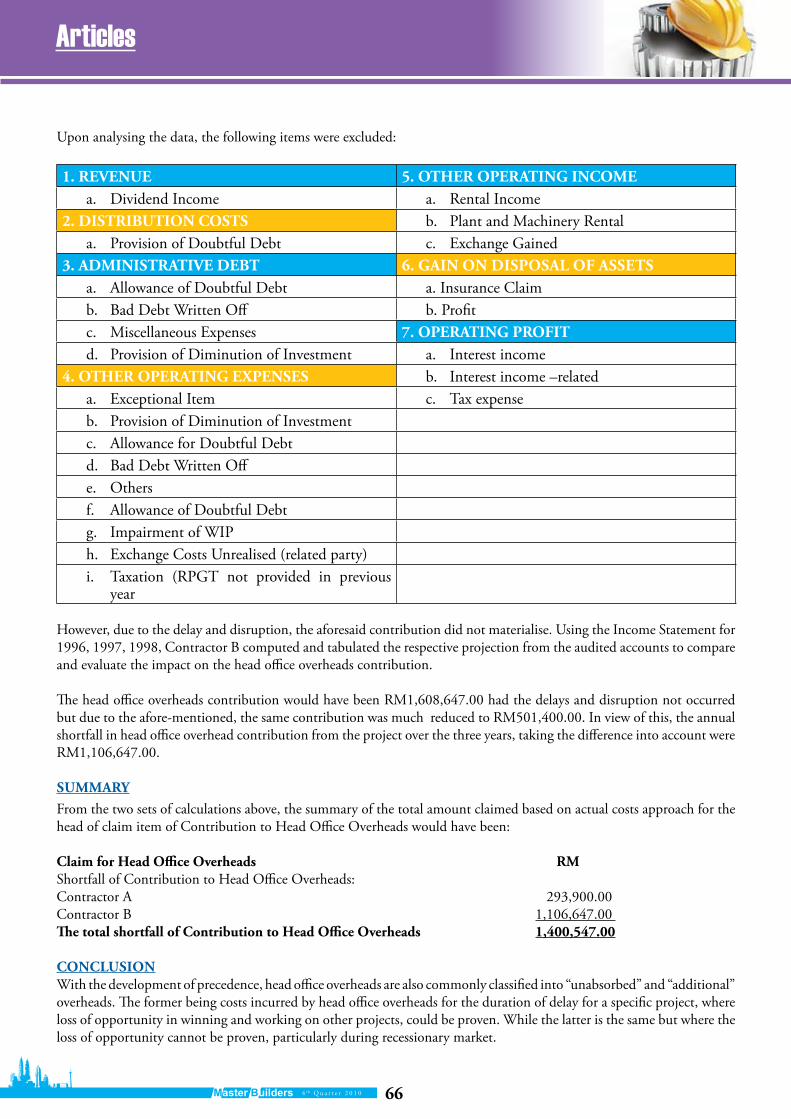

Upon analysing the data, the following items were excluded:

1. REvENUE 5. OThER OPERATING INCOMEa. Dividend Income a. Rental Income

2. DISTRIBUTION COSTS b. Plant and Machinery Rentala. Provision of Doubtful Debt c. Exchange Gained

3. ADMINISTRATIvE DEBT 6. GAIN ON DISPOSAL Of ASSETSa. Allowance of Doubtful Debt a. Insurance Claimb. Bad Debt Written Off b. Profitc. Miscellaneous Expenses 7. OPERATING PROfITd. Provision of Diminution of Investment a. Interest income

4. OThER OPERATING EXPENSES b. Interest income –relateda. Exceptional Item c. Tax expenseb. Provision of Diminution of Investmentc. Allowance for Doubtful Debtd. Bad Debt Written Offe. Othersf. Allowance of Doubtful Debtg. Impairment of WIPh. Exchange Costs Unrealised (related party)i. Taxation (RPGT not provided in previous

year

However, due to the delay and disruption, the aforesaid contribution did not materialise. Using the Income Statement for 1996, 1997, 1998, Contractor B computed and tabulated the respective projection from the audited accounts to compare and evaluate the impact on the head office overheads contribution.

The head office overheads contribution would have been RM1,608,647.00 had the delays and disruption not occurred but due to the afore-mentioned, the same contribution was much reduced to RM501,400.00. In view of this, the annual shortfall in head office overhead contribution from the project over the three years, taking the difference into account were RM1,106,647.00.

SUMMARYFrom the two sets of calculations above, the summary of the total amount claimed based on actual costs approach for the head of claim item of Contribution to Head Office Overheads would have been:

Claim for head Office Overheads RM Shortfall of Contribution to Head Office Overheads: Contractor A 293,900.00Contractor B 1,106,647.00 The total shortfall of Contribution to head Office Overheads 1,400,547.00

CONCLUSIONWith the development of precedence, head office overheads are also commonly classified into “unabsorbed” and “additional” overheads. The former being costs incurred by head office overheads for the duration of delay for a specific project, where loss of opportunity in winning and working on other projects, could be proven. While the latter is the same but where the loss of opportunity cannot be proven, particularly during recessionary market.

67 4 t h Q u a r t e r 2 0 1 0Master builders

Articles Articles

On the formulas front, despite evolving from Eichleay to Hudson through the refinement of various case laws over the years, and the eventual proposal of Actual costs approach to additional overheads, one could not help but notice that the past formula methods applied are still with many shortcomings. For instance the application poses problems such as when considering admissible payment into the calculation, considerations have to be made as to admit the claimed amount, the amount in the application for payment or the certified amount. Furthermore, when considering the percentage of interest to be admissible, the source of fund for each payment is often not clearly segregated. Not only various payments may come from various sources of funds, but each payment may have been paid from multiple sources of fund.

Furthermore, there are issues in determining the cut off date to determine the loss, for example, should the calculation be based on the cut off date of paid date, certified payment date or delayed certified payment date. The calculation of the shortfall in Contribution to Head Office Overheads demonstrated in this Article is not a precise science but probably the best estimate on the financial loss suffered and/or costs incurred. In essence, overheads calculation could be based on formula method but when actual costs are available, it is preferable to use the actual costs, not unless the overheads calculation is for prolongation beyond the practical /substantial completion date. Whichever it may be, there are more rooms for improvement in this area of law and practice in the construction industry.

In the next issue of the MBAM journal, BK Entrusty article will deal with a common contractual issue on “Expediting, Accelerating or Mitigating : meaning and implications in construction contracts ”

REfERENCES/ BIBLIOGRAPhY:1. Brewer, G (1998) “Overhead Claims”, Brewer

Consulting, www.brewerconsulting.co.uk/ cases/CJ9828CL.htm, 12 August 1998.

2. Clark, et al (1997) “Applied Cost Engineering”, Dekker, Third Edition, page 199, para. 2, line 1-2.

3. Jayalath, Chandana Dr. (2009) “Recovery of Unabsorbed Head Office Overheads in a Contract Prolongation” http://www.articlesbase.com/print/1378166, 25 October 2009.

4. Knowles, R (2000) “One Hundred Contractual Problems and their Solutions”, Blackwell Science, page 136.

5. Molloy, J.B. (1998) “The calculation of Head Office Overheads”, HKIS Newsletter 7(9) September 1998 issue.

6. RICS (2000) “RICS Scotland, Inform 2000”, RICS paper, page 2, para. 1,line 1-7.

7. THS Ramsey, V and Furst, S (2008) “Keating on Construction Contracts”, Sweet & Maxwell, Eighth Edition.

8. Wallace, I.N. Duncan (1994) “Hudsons Building and Engineering Contract”, Sweet and Maxwell, Eleventh Edition, Volume 1.

9. Winter, J (2001) “Head Office Overhead and Profit”, www.bakernet.com, December 2001.

68Master builders 4 t h Q u a r t e r 2 0 1 0

Articles

Bk Asia Pacific is group of companies incorporated in the Asia Pacific Region providing a comprehensive network of project management, commercial and contract management services to the international construction industry, with offices in Cambodia, China (Hong Kong, Shanghai), Malaysia, Philippines, Singapore, Thailand, Vietnam, United Kingdom and United Arab Emirates. For further details, visit www.bkasiapacific.com.

Entrusty Group is a multidisciplinary group of companies which comprises Entrusty Consultancy Sdn Bhd (formerly known as J.D. Kingsfield (M) Sdn Bhd), BK Burns & Ong Sdn Bhd (a member of BK Asia Pacific Ltd, Hong Kong), Pro-Value Management Sdn Bhd (in association with Applied Facilitation & Training, Australia), International Master Trainers Sdn Bhd (in association with Master Trainer of New York), Agensi Pekerjaan Proforce Sdn Bhd, Alpha-Omega Matrix and Entrusty International Pte Ltd. The Group provides comprehensive consultancy, advisory and management services in project, commercial, contracts, construction, facilities, risks, quality and value management, cost management, executive search / personnel recruitment and corporate training / seminars / workshops to various industries particularly in construction, petrochemical, manufacturing and IT, both locally and internationally. For further details, visi2

Bk Entrusty provides 30 minutes of free consultancy (with prior appointment) to MBAM members in the areas of project, commercial, contracts, risks, quality and value management, For enquiries, please contact HT Ong at BK Entrusty, 22-1& 2 Jalan 2/109E, Desa Business Park, Taman Desa, 58100 Kuala Lumpur, Malaysia. Tel: 6(03)-7982 2123 Fax: 6(03)-7982 3122 Email: [email protected] or [email protected] PUBLIC SEMINARS

1. Claims Preparation and Management 2. Certifications and Payments3. Time and Monetary Claims 4. Common Contractual Issues/Problems in

Malaysia5. Pertinent Contractual Provisions in

Construction Contracts6. Recent Construction Contract case law in

Malaysia

PUBLIC / IN-hOUSE TRAINING PROGRAMMES

1. Effective Project or Contract Administration / Management.2. One Day or Two Days Intensive Seminar (with workshop) on Practical

Construction Claims in Malaysia.3. 10 Half Day or 5 Full Day Modules on Practical Construction Contract

Administration / Management.4. One Day or Two Days Intensive Training (with workshop) on Value

Engineering / Management.5. International/Accredited Value Management Programmes.6. ISO 9001:2008 Training.7. One Day Seminar on “Doing The Right Things Right”.8. Motivation, Train-The-Trainer and NLP programmes.

68Master builders 4 t h Q u a r t e r 2 0 1 0

![chapter 3 overheads - John D. Cresslercressler.ece.gatech.edu/courses/COE_3002/overheads/F19/chapter 3... · Title: Microsoft PowerPoint - chapter 3 overheads [Compatibility Mode]](https://static.fdocuments.in/doc/165x107/5fb70f40766c616ca64667e8/chapter-3-overheads-john-d-3-title-microsoft-powerpoint-chapter-3-overheads.jpg)