Consolidations Week 2 TEXT CHAP 15 TEXT CHAP 15. Carrying amount of assets @ acquisition nSo far it...

30

Consolidations Week 2 Consolidations Week 2 TEXT CHAP 15

-

Upload

dean-thorley -

Category

Documents

-

view

231 -

download

0

Transcript of Consolidations Week 2 TEXT CHAP 15 TEXT CHAP 15. Carrying amount of assets @ acquisition nSo far it...

Consolidations Week 2Consolidations Week 2

TEXT CHAP 15

TEXT CHAP 15

Carrying amount of assets Carrying amount of assets @ acquisition@ acquisition

So far it has been assumed that the subsidiary’s net So far it has been assumed that the subsidiary’s net assets are recorded at fair valuesassets are recorded at fair values

When the carrying amount of the subsidiary's When the carrying amount of the subsidiary's assets are different from fair values AASB 1024 assets are different from fair values AASB 1024 sets out two (2) approaches to recognising the sets out two (2) approaches to recognising the necessary adjustmentsnecessary adjustments

(1) to recognise the necessary adjustment on (1) to recognise the necessary adjustment on consolidationconsolidation

(2) to revalue the assets in the accounting records (2) to revalue the assets in the accounting records of the subsidiaryof the subsidiary

Adjustment on Adjustment on ConsolidationConsolidation

The non-current assets of the subsidiary are The non-current assets of the subsidiary are adjusted to the fair values on consolidationadjusted to the fair values on consolidation

The differences being recorded in the assets The differences being recorded in the assets revaluation reserverevaluation reserve

The asset revaluation reserve is then part of the The asset revaluation reserve is then part of the equity acquired equity acquired

Inventory has to carried at the lower of cost or net Inventory has to carried at the lower of cost or net realisable value, they cannot be adjusted to assets realisable value, they cannot be adjusted to assets revaluation reserve but adjusted directly in pre-revaluation reserve but adjusted directly in pre-acquisition entryacquisition entry

Example - LandExample - Land

Green Ltd purchased all of the shares of Frog Ltd on 1 Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date July 19x5 for $117,000. The equity of Frog Ltd at that date was :-was :-

CAPITAL $80,000CAPITAL $80,000

RETAINED PROFITS 30,000RETAINED PROFITS 30,000

All the identified net assets of Frog Ltd were recorded at fair All the identified net assets of Frog Ltd were recorded at fair value value

Except for land which had a carrying amount of $26000, $10 Except for land which had a carrying amount of $26000, $10 000 less than its fair value of $36,000.000 less than its fair value of $36,000.

Example - LandExample - Land

Green Ltd purchased all of the shares of Frog Ltd on 1 Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date July 19x5 for $117,000. The equity of Frog Ltd at that date was :-was :-

CAPITAL $80,000CAPITAL $80,000

RETAINED PROFITS 30,000RETAINED PROFITS 30,000

All the identified net assets of Frog Ltd were recorded at fair All the identified net assets of Frog Ltd were recorded at fair value value

Except for land which had a carrying amount of $26000, $10 Except for land which had a carrying amount of $26000, $10 000 less than its fair value of $36,000.000 less than its fair value of $36,000.

FV of INA= 80+30+.7(10) =117Cost =117

FV of INA= 80+30+.7(10) =117Cost =117

Example - LandExample - Land

Green Ltd purchased all of the shares of Frog Ltd on 1 Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date July 19x5 for $117,000. The equity of Frog Ltd at that date was :-was :-

CAPITAL $80,000CAPITAL $80,000

RETAINED PROFITS 30,000RETAINED PROFITS 30,000

All the identified net assets of Frog Ltd were recorded at fair All the identified net assets of Frog Ltd were recorded at fair value value

Except for land which had a carrying amount of $26000, $10 Except for land which had a carrying amount of $26000, $10 000 less than its fair value of $36,000.000 less than its fair value of $36,000.

FIRST CONS ENTRY::

DR LAND 10,000 CR Deferred Tax Liab 3 000 CR ASSET REVALN RESERVE 7,000

FIRST CONS ENTRY::

DR LAND 10,000 CR Deferred Tax Liab 3 000 CR ASSET REVALN RESERVE 7,000

Example - LandExample - Land

Green Ltd purchased all of the shares of Frog Ltd on 1 Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date July 19x5 for $117,000. The equity of Frog Ltd at that date was :-was :-

CAPITAL $80,000CAPITAL $80,000

RETAINED PROFITS 30,000RETAINED PROFITS 30,000

All the identified net assets of Frog Ltd were recorded at fair All the identified net assets of Frog Ltd were recorded at fair value value

Except for land which had a carrying amount of $26000, $10 Except for land which had a carrying amount of $26000, $10 000 less than its fair value of $36,000.000 less than its fair value of $36,000.

DR CAPITAL 80,000DR RETAINED PROFITS 30,000DR A.R.R. 7,000 CR SHARES IN FROG LTD 117,000

DR CAPITAL 80,000DR RETAINED PROFITS 30,000DR A.R.R. 7,000 CR SHARES IN FROG LTD 117,000

FV of INA= 80+30+.7(10) =117Cost =117

FV of INA= 80+30+.7(10) =117Cost =117

Example - Depreciable Example - Depreciable AssetAsset

Green Ltd purchased all of the shares of Frog Ltd on 1 July Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date was :-19x5 for $117,000. The equity of Frog Ltd at that date was :-

Capital $80,000Capital $80,000

Retained profits 30,000Retained profits 30,000

All the identified net assets of Frog ltd were recorded at fair value All the identified net assets of Frog ltd were recorded at fair value

Except for a depreciable asset Plant which has a fair value Except for a depreciable asset Plant which has a fair value $10,000 greater than its carrying amount (Frog Ltd has it $10,000 greater than its carrying amount (Frog Ltd has it recorded at $45,000 with accumulated depreciation $5,000)recorded at $45,000 with accumulated depreciation $5,000)

Example - Depreciable Example - Depreciable AssetAsset

Green Ltd purchased all of the shares of Frog Ltd on 1 July Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date was :-19x5 for $117,000. The equity of Frog Ltd at that date was :-

Capital $80,000Capital $80,000

Retained profits 30,000Retained profits 30,000

All the identified net assets of Frog ltd were recorded at fair value All the identified net assets of Frog ltd were recorded at fair value

Except for a depreciable asset Plant which has a fair value Except for a depreciable asset Plant which has a fair value $10,000 greater than its carrying amount (Frog Ltd has it $10,000 greater than its carrying amount (Frog Ltd has it recorded at $45,000 with accumulated depreciation $5,000)recorded at $45,000 with accumulated depreciation $5,000)

F.V. Assets acquired = (Capital $80 000 + RP $30 000 + 70 %ARR $10 000) = 117 000Cost of Acquisition = 117 000

F.V. Assets acquired = (Capital $80 000 + RP $30 000 + 70 %ARR $10 000) = 117 000Cost of Acquisition = 117 000

Example - Depreciable Example - Depreciable AssetAsset

Green Ltd purchased all of the shares of Frog Ltd on 1 July Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date was :-19x5 for $117,000. The equity of Frog Ltd at that date was :-

Capital $80,000Capital $80,000

Retained profits 30,000Retained profits 30,000

All the identified net assets of Frog ltd were recorded at fair value All the identified net assets of Frog ltd were recorded at fair value

Except for a depreciable asset Plant which has a fair value Except for a depreciable asset Plant which has a fair value $10,000 greater than its carrying amount (Frog Ltd has it $10,000 greater than its carrying amount (Frog Ltd has it recorded at $45,000 with accumulated depreciation $5,000)recorded at $45,000 with accumulated depreciation $5,000)

second cons entry::DR PLANT 10,000 Cr Deferred Tax Lia 3,000 CR A.R.R. 7,000

second cons entry::DR PLANT 10,000 Cr Deferred Tax Lia 3,000 CR A.R.R. 7,000

Write off accum depn::DR Accumulated Depn 5,000 CR Plant 5,000

Write off accum depn::DR Accumulated Depn 5,000 CR Plant 5,000

Example - Depreciable Example - Depreciable AssetAsset

Green Ltd purchased all of the shares of Frog Ltd on 1 July Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date was :-19x5 for $117,000. The equity of Frog Ltd at that date was :-

Capital $80,000Capital $80,000

Retained profits 30,000Retained profits 30,000

All the identified net assets of Frog ltd were recorded at fair value All the identified net assets of Frog ltd were recorded at fair value

Except for a depreciable asset Plant which has a fair value Except for a depreciable asset Plant which has a fair value $10,000 greater than its carrying amount (Frog Ltd has it $10,000 greater than its carrying amount (Frog Ltd has it recorded at $45,000 with accumulated depreciation $5,000)recorded at $45,000 with accumulated depreciation $5,000)

DR CAPITAL 80,000DR R.P. 30,000DR A.R.R. 7,000 CR SHARES IN FROG 117,000

DR CAPITAL 80,000DR R.P. 30,000DR A.R.R. 7,000 CR SHARES IN FROG 117,000

F.V. Assets acquired = (Capital $80 000 + RP $30 000 + 70 %ARR $10 000) = 117 000Cost of Acquisition = 117 000

F.V. Assets acquired = (Capital $80 000 + RP $30 000 + 70 %ARR $10 000) = 117 000Cost of Acquisition = 117 000

Example - Depreciable Example - Depreciable AssetAsset

Green Ltd purchased all of the shares of Frog Ltd on 1 July Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date was :-19x5 for $117,000. The equity of Frog Ltd at that date was :-

Capital $80,000Capital $80,000

Retained profits 30,000Retained profits 30,000

All the identified net assets of Frog ltd were recorded at fair value All the identified net assets of Frog ltd were recorded at fair value

Except for a depreciable asset Plant which has a fair value Except for a depreciable asset Plant which has a fair value $10,000 greater than its carrying amount (Frog Ltd has it $10,000 greater than its carrying amount (Frog Ltd has it recorded at $45,000 with accumulated depreciation $5,000)recorded at $45,000 with accumulated depreciation $5,000)

cons entry::DR PLANT 10,000 Cr DTL 3,000 CR A.R.R. 7,000DR DEPN 2,500 CR ACC DEPN 2,500DR DTL 750 CR Income tax Exp 750

cons entry::DR PLANT 10,000 Cr DTL 3,000 CR A.R.R. 7,000DR DEPN 2,500 CR ACC DEPN 2,500DR DTL 750 CR Income tax Exp 750

ENTRY AFTER 1 YEARS ASSUMINGPLANT HAS LIFEOF 4 YEARS

Example - Depreciable Example - Depreciable AssetAsset

Green Ltd purchased all of the shares of Frog Ltd on 1 July Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date was :-19x5 for $117,000. The equity of Frog Ltd at that date was :-

Capital $80,000Capital $80,000

Retained profits 30,000Retained profits 30,000

All the identified net assets of Frog ltd were recorded at fair value All the identified net assets of Frog ltd were recorded at fair value

Except for a depreciable asset Plant which has a fair value Except for a depreciable asset Plant which has a fair value $10,000 greater than its carrying amount (Frog Ltd has it $10,000 greater than its carrying amount (Frog Ltd has it recorded at $45,000 with accumulated depreciation $5,000)recorded at $45,000 with accumulated depreciation $5,000)

second cons entry::DR PLANT 10,000 Cr DTL 3,000 CR A.R.R. 7,000DR DEPN 2,500DR RP 2,500 CR ACC DEPN 5,000DR DTL 1,500 CR Income tax Exp 750 Cr RP 750

second cons entry::DR PLANT 10,000 Cr DTL 3,000 CR A.R.R. 7,000DR DEPN 2,500DR RP 2,500 CR ACC DEPN 5,000DR DTL 1,500 CR Income tax Exp 750 Cr RP 750

ENTRY AFTER 2 YEARS ASSUMINGPLANT HAS LIFEOF 4 YEARS

Example - InventoriesExample - Inventories

Green Ltd purchased all of the shares of Frog Ltd on 1 July Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date was :-19x5 for $117,000. The equity of Frog Ltd at that date was :-

Capital $80,000Capital $80,000

Retained profits 30,000Retained profits 30,000

All the identified net assets of Frog Ltd were recorded at fair All the identified net assets of Frog Ltd were recorded at fair value value

Except for inventory which had a carrying amount of $10 000 Except for inventory which had a carrying amount of $10 000 greater than its book value.greater than its book value.

Example - InventoriesExample - Inventories

Green Ltd purchased all of the shares of Frog Ltd on 1 July Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date was :-19x5 for $117,000. The equity of Frog Ltd at that date was :-

Capital $80,000Capital $80,000

Retained profits 30,000Retained profits 30,000

All the identified net assets of Frog Ltd were recorded at fair All the identified net assets of Frog Ltd were recorded at fair value except for inventory which had a carrying amount of value except for inventory which had a carrying amount of $10 000 greater than its book value.$10 000 greater than its book value.

F.V. Assets acquired = (Capital $80 000 + RP $30 000 + 70 % Invent $10 000) = 117 000Cost of Acquisition = 117 000

F.V. Assets acquired = (Capital $80 000 + RP $30 000 + 70 % Invent $10 000) = 117 000Cost of Acquisition = 117 000

Example - InventoriesExample - Inventories

Green Ltd purchased all of the shares of Frog Ltd on 1 July Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date was :-19x5 for $117,000. The equity of Frog Ltd at that date was :-

Capital $80,000Capital $80,000

Retained profits 30,000Retained profits 30,000

All the identified net assets of Frog Ltd were recorded at fair All the identified net assets of Frog Ltd were recorded at fair value value

Except for inventory which had a carrying amount of $10 000 Except for inventory which had a carrying amount of $10 000 greater than its book value.greater than its book value.

CONS ENTRY:: DR CAPITAL 80,000DR R.P. 30,000DR INVENTORY 10,000 CR Deferred Tax Liab 3,000 CR SHARES IN FROG 117,000

CONS ENTRY:: DR CAPITAL 80,000DR R.P. 30,000DR INVENTORY 10,000 CR Deferred Tax Liab 3,000 CR SHARES IN FROG 117,000

F.V. Assets acquired = (Capital $80 000 + RP $30 000 + 70 % Invent $10 000) = 117 000Cost of Acquisition = 117 000

F.V. Assets acquired = (Capital $80 000 + RP $30 000 + 70 % Invent $10 000) = 117 000Cost of Acquisition = 117 000

Example - InventoriesExample - Inventories

Green Ltd purchased all of the shares of Frog Ltd on 1 July Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date was :-19x5 for $117,000. The equity of Frog Ltd at that date was :-

Capital $80,000Capital $80,000

Retained profits 30,000Retained profits 30,000

All the identified net assets of Frog Ltd were recorded at fair All the identified net assets of Frog Ltd were recorded at fair value value

Except for inventory which had a carrying amount of $10 000 Except for inventory which had a carrying amount of $10 000 greater than its book value.greater than its book value.

CONS ENTRY:: YEAR INVENTORY SOLDDR CAPITAL 80,000DR R.P. 30,000DR COST OF SALES 10,000 CR TAX EXPENSE 3,000 CR SHARES IN FROG 117,000

CONS ENTRY:: YEAR INVENTORY SOLDDR CAPITAL 80,000DR R.P. 30,000DR COST OF SALES 10,000 CR TAX EXPENSE 3,000 CR SHARES IN FROG 117,000

Example - InventoriesExample - Inventories

Green Ltd purchased all of the shares of Frog Ltd on 1 July Green Ltd purchased all of the shares of Frog Ltd on 1 July 19x5 for $117,000. The equity of Frog Ltd at that date was :-19x5 for $117,000. The equity of Frog Ltd at that date was :-

Capital $80,000Capital $80,000

Retained profits 30,000Retained profits 30,000

All the identified net assets of Frog Ltd were recorded at fair All the identified net assets of Frog Ltd were recorded at fair value value

Except for inventory which had a carrying amount of $10 000 Except for inventory which had a carrying amount of $10 000 greater than its book value.greater than its book value.

CONS ENTRY:: FOLLOWING YEARSDR CAPITAL 80,000DR R.P. 37,000 (30,000+10,000-3,000) CR SHARES IN FROG 117000

CONS ENTRY:: FOLLOWING YEARSDR CAPITAL 80,000DR R.P. 37,000 (30,000+10,000-3,000) CR SHARES IN FROG 117000

Revaluation of assets in Revaluation of assets in Subsidiary’s booksSubsidiary’s books

As per AASB 1010 subsidiary can revalue non current As per AASB 1010 subsidiary can revalue non current assets in its books ie assets in its books ie

DR Non current assetDR Non current asset

CR Deferred Tax LiabilityCR Deferred Tax Liability

CR Asset revaluation reserveCR Asset revaluation reserve If depreciable assets accumulated depreciation must be If depreciable assets accumulated depreciation must be

written off as beforewritten off as before If revalue in books no need to adjust depreciationIf revalue in books no need to adjust depreciation

as this will be adjusted in the booksas this will be adjusted in the books Inventory as per AASB 1019 cannot be written up and Inventory as per AASB 1019 cannot be written up and

therefore still adjusted on consolidationtherefore still adjusted on consolidation

Revaln in Subsidiary’s Revaln in Subsidiary’s books - goodwillbooks - goodwill

On 1 January 19x7, Buddy Ltd acquired all the issued shares of On 1 January 19x7, Buddy Ltd acquired all the issued shares of Holly Ltd for $52,000. At this date the financial position of Holly Ltd for $52,000. At this date the financial position of Holly Ltd was as followsHolly Ltd was as follows:-:-

CAPITAL 22,000CAPITAL 22,000

RETAINED PROFITS 18,000RETAINED PROFITS 18,000

F. V.F. V.

PLANT (COST $20,000) 15,000 18,000PLANT (COST $20,000) 15,000 18,000

LAND 5,000 7,000LAND 5,000 7,000

INVENTORY 20,000 25,000INVENTORY 20,000 25,000

Holly revalues to fair values (except inventory)Holly revalues to fair values (except inventory)

Revaln in Subsidiary’s Revaln in Subsidiary’s books - goodwillbooks - goodwill

On 1 January 19x7, Buddy Ltd acquired all the issued shares of On 1 January 19x7, Buddy Ltd acquired all the issued shares of Holly Ltd for $52,000. At this date the financial position of Holly Ltd for $52,000. At this date the financial position of Holly Ltd was as followsHolly Ltd was as follows:-:-

CAPITAL 22,000CAPITAL 22,000

RETAINED PROFITS 18,000RETAINED PROFITS 18,000

F. V.F. V.

PLANT (COST $20,000) 15,000 18,000PLANT (COST $20,000) 15,000 18,000

LAND 5,000 7,000LAND 5,000 7,000

INVENTORY 20,000 25,000INVENTORY 20,000 25,000

Holly revalues to fair values (except inventory)Holly revalues to fair values (except inventory)

FV of Assets Acq= 22000+18000+.7(3000+2000+5000)=47 000Cost 52 000Goodwill 5 000

FV of Assets Acq= 22000+18000+.7(3000+2000+5000)=47 000Cost 52 000Goodwill 5 000

Revaln in Subsidiary’s Revaln in Subsidiary’s books - goodwillbooks - goodwill

On 1 January 19x7, Buddy Ltd acquired all the issued shares of On 1 January 19x7, Buddy Ltd acquired all the issued shares of Holly Ltd for $52,000. At this date the financial position of Holly Ltd for $52,000. At this date the financial position of Holly Ltd was as followsHolly Ltd was as follows:-:-

CAPITAL 22,000CAPITAL 22,000

RETAINED PROFITS 18,000RETAINED PROFITS 18,000

F. V.F. V.

PLANT (COST $20,000) 15,000 18,000PLANT (COST $20,000) 15,000 18,000

LAND 5,000 7,000LAND 5,000 7,000

INVENTORY 20,000 25,000INVENTORY 20,000 25,000

Holly revalues to fair values (except inventory)Holly revalues to fair values (except inventory)

entries in BOOKS OF SUBDr Land 2,000 Cr Deferred Tax Lia 600 Cr ARR 1,400DR ACC DEPN 5,000 CR PLANT 5,000Dr Plant 3,000 Cr DTL 900 Cr ARR 2,100

entries in BOOKS OF SUBDr Land 2,000 Cr Deferred Tax Lia 600 Cr ARR 1,400DR ACC DEPN 5,000 CR PLANT 5,000Dr Plant 3,000 Cr DTL 900 Cr ARR 2,100

Revaln in Subsidiary’s Revaln in Subsidiary’s books - goodwillbooks - goodwill

On 1 January 19x7, Buddy Ltd acquired all the issued shares of On 1 January 19x7, Buddy Ltd acquired all the issued shares of Holly Ltd for $52,000. At this date the financial position of Holly Ltd for $52,000. At this date the financial position of Holly Ltd was as followsHolly Ltd was as follows:-:-

CAPITAL 22,000CAPITAL 22,000

RETAINED PROFITS 18,000RETAINED PROFITS 18,000

F. V.F. V.

PLANT (COST $20,000) 15,000 18,000PLANT (COST $20,000) 15,000 18,000

LAND 5,000 7,000LAND 5,000 7,000

INVENTORY 20,000 25,000INVENTORY 20,000 25,000

Holly revalues to fair values (except inventory)Holly revalues to fair values (except inventory)

CONS entries::DR CAPITAL 22,000DR R.P. 18,000DR A.R.R. 3,500DR G’WILL 5,000DR INVENT. 5,000 CR Deferred Tax Liab 1,500 CR SHARES S 52,000

CONS entries::DR CAPITAL 22,000DR R.P. 18,000DR A.R.R. 3,500DR G’WILL 5,000DR INVENT. 5,000 CR Deferred Tax Liab 1,500 CR SHARES S 52,000

FV of Assets Acq= 22000+18000+.7(3000+2000+5000)=47 000Cost 52 000Goodwill 5 000

FV of Assets Acq= 22000+18000+.7(3000+2000+5000)=47 000Cost 52 000Goodwill 5 000

Revaln in Subsidiary’s Revaln in Subsidiary’s books - goodwillbooks - goodwill

On 1 January 19x7, Buddy Ltd acquired all the issued shares of On 1 January 19x7, Buddy Ltd acquired all the issued shares of Holly Ltd for $52,000. At this date the financial position of Holly Ltd for $52,000. At this date the financial position of Holly Ltd was as followsHolly Ltd was as follows:-:-

CAPITAL 22,000CAPITAL 22,000

RETAINED PROFITS 18,000RETAINED PROFITS 18,000

F. V.F. V.

PLANT (COST $20,000) 15,000 18,000PLANT (COST $20,000) 15,000 18,000

LAND 5,000 7,000LAND 5,000 7,000

INVENTORY 20,000 25,000INVENTORY 20,000 25,000

Holly revalues to fair values (except inventory)Holly revalues to fair values (except inventory)

entries (after 1 year)::Dr Goodwill Exp 500DR CAPITAL 22,000DR R.P. 18,000DR A.R.R. 3,500DR G’WILL 5,000 CR Acc Amort 500DR Cost of Sales 5,000 CR Tax Expense 1,500 CR SHARES S 52,000

entries (after 1 year)::Dr Goodwill Exp 500DR CAPITAL 22,000DR R.P. 18,000DR A.R.R. 3,500DR G’WILL 5,000 CR Acc Amort 500DR Cost of Sales 5,000 CR Tax Expense 1,500 CR SHARES S 52,000

CONS entries::DR CAPITAL 22,000DR R.P. 18,000DR A.R.R. 3,500DR G’WILL 5,000DR INVENT. 5,000 CR Deferred Tax Liab 1,500 CR SHARES S 52,000

CONS entries::DR CAPITAL 22,000DR R.P. 18,000DR A.R.R. 3,500DR G’WILL 5,000DR INVENT. 5,000 CR Deferred Tax Liab 1,500 CR SHARES S 52,000

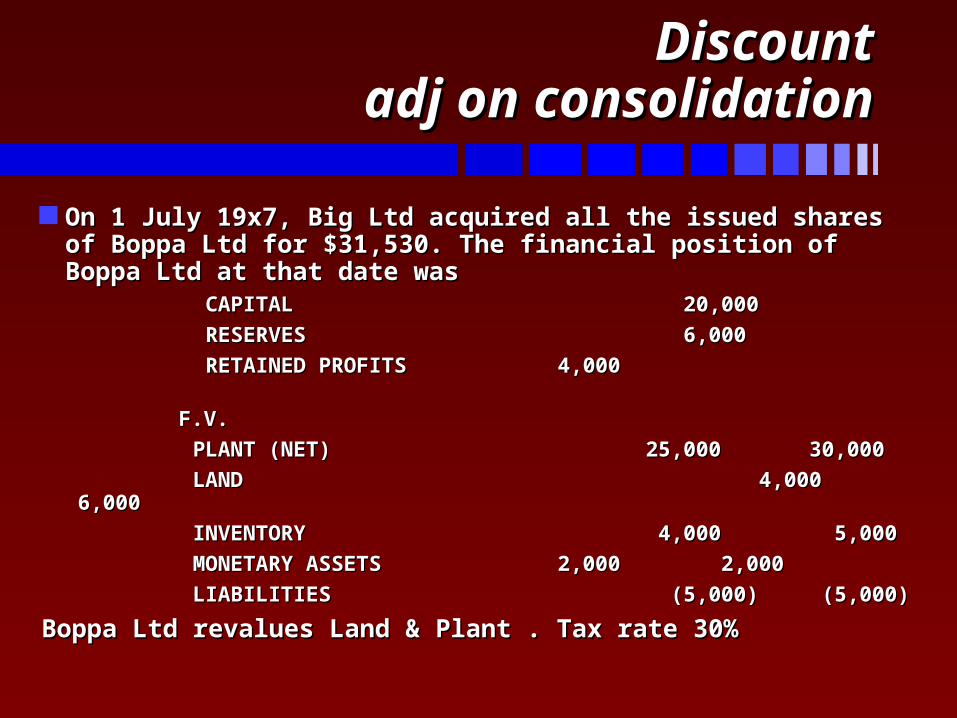

DiscountDiscountadj on consolidationadj on consolidation

On 1 July 19x7, Big Ltd acquired all the issued shares of Boppa Ltd On 1 July 19x7, Big Ltd acquired all the issued shares of Boppa Ltd for $31,530. The financial position of Boppa Ltd at that date wasfor $31,530. The financial position of Boppa Ltd at that date was

CAPITAL 20,000CAPITAL 20,000

RESERVES 6,000RESERVES 6,000

RETAINED PROFITS 4,000RETAINED PROFITS 4,000

F.V.F.V.

PLANT (NET) 25,000 30,000PLANT (NET) 25,000 30,000

LAND 4,000 6,000LAND 4,000 6,000

INVENTORY 4,000 5,000INVENTORY 4,000 5,000

MONETARY ASSETS 2,000 2,000MONETARY ASSETS 2,000 2,000

LIABILITIES (5,000) (5,000)LIABILITIES (5,000) (5,000)

Boppa Ltd revalues Land & Plant . Tax rate 30% Boppa Ltd revalues Land & Plant . Tax rate 30%

DiscountDiscount

On 1 July 19x7, Big Ltd acquired all the issued shares of Boppa Ltd On 1 July 19x7, Big Ltd acquired all the issued shares of Boppa Ltd for $31,530. The financial position of Boppa Ltd at that date wasfor $31,530. The financial position of Boppa Ltd at that date was

CAPITAL 20,000CAPITAL 20,000

RESERVES 6,000RESERVES 6,000

RETAINED PROFITS 4,000RETAINED PROFITS 4,000

F.V.F.V.

PLANT (NET) 25,000 30,000PLANT (NET) 25,000 30,000

LAND 4,000 6,000LAND 4,000 6,000

INVENTORY 4,000 5,000INVENTORY 4,000 5,000

MONETARY ASSETS 2,000 2,000MONETARY ASSETS 2,000 2,000

LIABILITIES (5,000) (5,000)LIABILITIES (5,000) (5,000)

Boppa Ltd revalues Land & Plant . Tax rate 30%Boppa Ltd revalues Land & Plant . Tax rate 30%

F,V, OF ASSETS ACQ(20,000+6,000+4,000+ .7 (A.R.R. 7,000+INV 1,000) = $35,600COST = 31,530

DISCOUNT $ 4,070

F,V, OF ASSETS ACQ(20,000+6,000+4,000+ .7 (A.R.R. 7,000+INV 1,000) = $35,600COST = 31,530

DISCOUNT $ 4,070

DiscountDiscount

On 1 July 19x7, Big Ltd acquired all the issued shares of Boppa Ltd On 1 July 19x7, Big Ltd acquired all the issued shares of Boppa Ltd for $31,530. The financial position of Boppa Ltd at that date wasfor $31,530. The financial position of Boppa Ltd at that date was

CAPITAL 20,000CAPITAL 20,000

RESERVES 6,000RESERVES 6,000

RETAINED PROFITS 4,000RETAINED PROFITS 4,000

F.V.F.V.

PLANT (NET) 25,000 30,000PLANT (NET) 25,000 30,000

LAND 4,000 6,000LAND 4,000 6,000

INVENTORY 4,000 5,000INVENTORY 4,000 5,000

MONETARY ASSETS 2,000 2,000MONETARY ASSETS 2,000 2,000

LIABILITIES (5,000) (5,000)LIABILITIES (5,000) (5,000)

Boppa Ltd revalues Land & Plant . Tax rate 30%Boppa Ltd revalues Land & Plant . Tax rate 30%

Revaluation:Dr Land 2 000 Cr DTL 600 Cr ARR 1 400

Dr Plant 5 000 Cr DTL 1 500 Cr ARR 3 500

Revaluation:Dr Land 2 000 Cr DTL 600 Cr ARR 1 400

Dr Plant 5 000 Cr DTL 1 500 Cr ARR 3 500

DiscountDiscount

On 1 July 19x7, Big Ltd acquired all the issued shares of Boppa Ltd On 1 July 19x7, Big Ltd acquired all the issued shares of Boppa Ltd for $31,530. The financial position of Boppa Ltd at that date wasfor $31,530. The financial position of Boppa Ltd at that date was

CAPITAL 20,000CAPITAL 20,000

RESERVES 6,000RESERVES 6,000

RETAINED PROFITS 4,000RETAINED PROFITS 4,000

F.V.F.V.

PLANT (NET) 25,000 30,000PLANT (NET) 25,000 30,000

LAND 4,000 6,000LAND 4,000 6,000

INVENTORY 4,000 5,000INVENTORY 4,000 5,000

MONETARY ASSETS 2,000 2,000MONETARY ASSETS 2,000 2,000

LIABILITIES (5,000) (5,000)LIABILITIES (5,000) (5,000)

Boppa Ltd revalues Land & Plant . Tax rate 30%Boppa Ltd revalues Land & Plant . Tax rate 30%

ALLOCATION OF DISCOUNT: N-M ASSETS F.V. DISCOUNT Grossed Tax Effect Cost upPLANT 30,000 3,000 4286 1286 25714LAND 6,000 600 857 257 5143INVENTORY Net of tax 4,700 470 4230 40,700 $4070Carry Amount of Inventory $4000 Gross up $230 /.7Carrying Amt Plant & Land now fair values

ALLOCATION OF DISCOUNT: N-M ASSETS F.V. DISCOUNT Grossed Tax Effect Cost upPLANT 30,000 3,000 4286 1286 25714LAND 6,000 600 857 257 5143INVENTORY Net of tax 4,700 470 4230 40,700 $4070Carry Amount of Inventory $4000 Gross up $230 /.7Carrying Amt Plant & Land now fair values

DiscountDiscount

On 1 July 19x7, Big Ltd acquired all the issued shares of Boppa Ltd On 1 July 19x7, Big Ltd acquired all the issued shares of Boppa Ltd for $31,530. The financial position of Boppa Ltd at that date wasfor $31,530. The financial position of Boppa Ltd at that date was

CAPITAL 20,000CAPITAL 20,000

RESERVES 6,000RESERVES 6,000

RETAINED PROFITS 4,000RETAINED PROFITS 4,000

F.V.F.V.

PLANT (NET) 25,000 30,000PLANT (NET) 25,000 30,000

LAND 4,000 6,000LAND 4,000 6,000

INVENTORY 4,000 5,000INVENTORY 4,000 5,000

MONETARY ASSETS 2,000 2,000MONETARY ASSETS 2,000 2,000

LIABILITIES (5,000) (5,000)LIABILITIES (5,000) (5,000)

Boppa Ltd revalues Land & Plant . Tax rate 30%Boppa Ltd revalues Land & Plant . Tax rate 30%

F,V, OF ASSETS ACQ(20,000+6,000+4,000+ .7 (A.R.R. 7,000+INV 1,000) = $35,600COST = 31,530

DISCOUNT $ 4,070

F,V, OF ASSETS ACQ(20,000+6,000+4,000+ .7 (A.R.R. 7,000+INV 1,000) = $35,600COST = 31,530

DISCOUNT $ 4,070

ALLOCATION OF DISCOUNT: N-M ASSETS F.V. DISCOUNT Grossed Tax Effect Cost upPLANT 30,000 3,000 4286 1286 25714LAND 6,000 600 857 257 5143INVENTORY Net of tax 4,700 470 4230 40,700 $4070NET GROSS UP /.7230/.7=329

ALLOCATION OF DISCOUNT: N-M ASSETS F.V. DISCOUNT Grossed Tax Effect Cost upPLANT 30,000 3,000 4286 1286 25714LAND 6,000 600 857 257 5143INVENTORY Net of tax 4,700 470 4230 40,700 $4070NET GROSS UP /.7230/.7=329

CONS ENTRY ::

DR CAPITAL 20,000DR G.R. 6,000DR R.P. 4,000DR A.R.R. 4,900 CR PLANT 4,286Dr Deferred Tax Liab 1,286 CR LAND 857DR Deferred Tax Liab 257DR INVENT 329 CR DTL 99 CR SHARES IN B 31,530

CONS ENTRY ::

DR CAPITAL 20,000DR G.R. 6,000DR R.P. 4,000DR A.R.R. 4,900 CR PLANT 4,286Dr Deferred Tax Liab 1,286 CR LAND 857DR Deferred Tax Liab 257DR INVENT 329 CR DTL 99 CR SHARES IN B 31,530

Tutorial QuestionsTutorial Questions

Problem 15.1Problem 15.1 Problem 15.2Problem 15.2 Problem 15.3Problem 15.3 Problem 15.4Problem 15.4 Problem 15.5Problem 15.5