Completing the Accounting Cycle for a Merchandising Corporation

Upload

laurel-moralesCategory

view

38download

1description

1

4

Completing the Accounting Cycle

Student Version

21-24-2

1

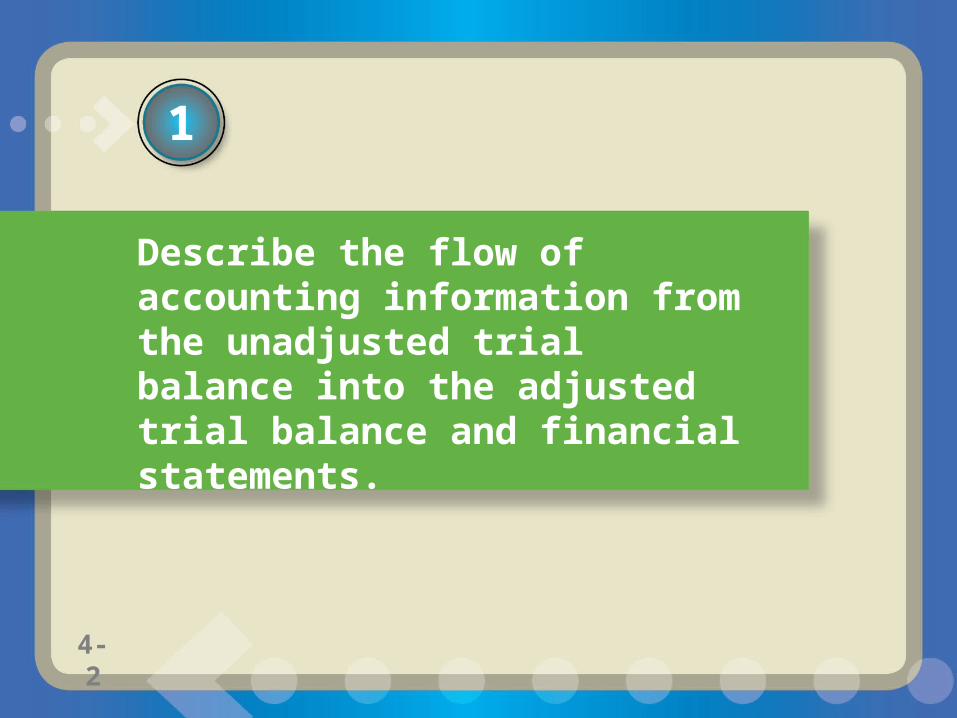

Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance and financial statements.

4-2

31-34-3

1End-of-Period Spreadsheet (Work Sheet)Exhibit 1

41-44-4

Prepare financial statements from adjusted account balances.

2

4-4

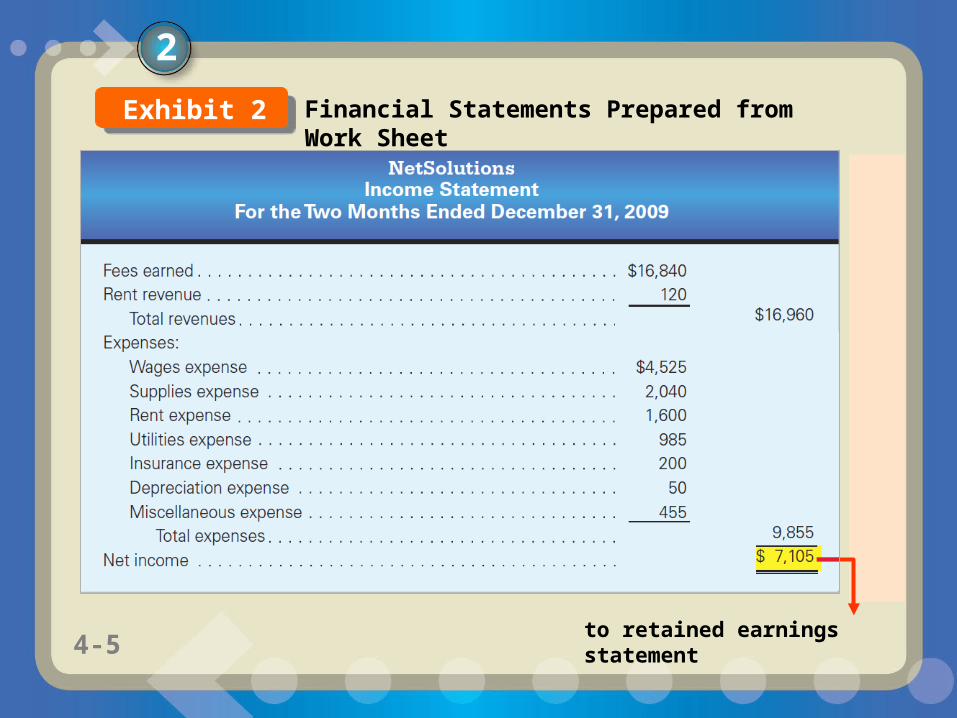

51-54-5

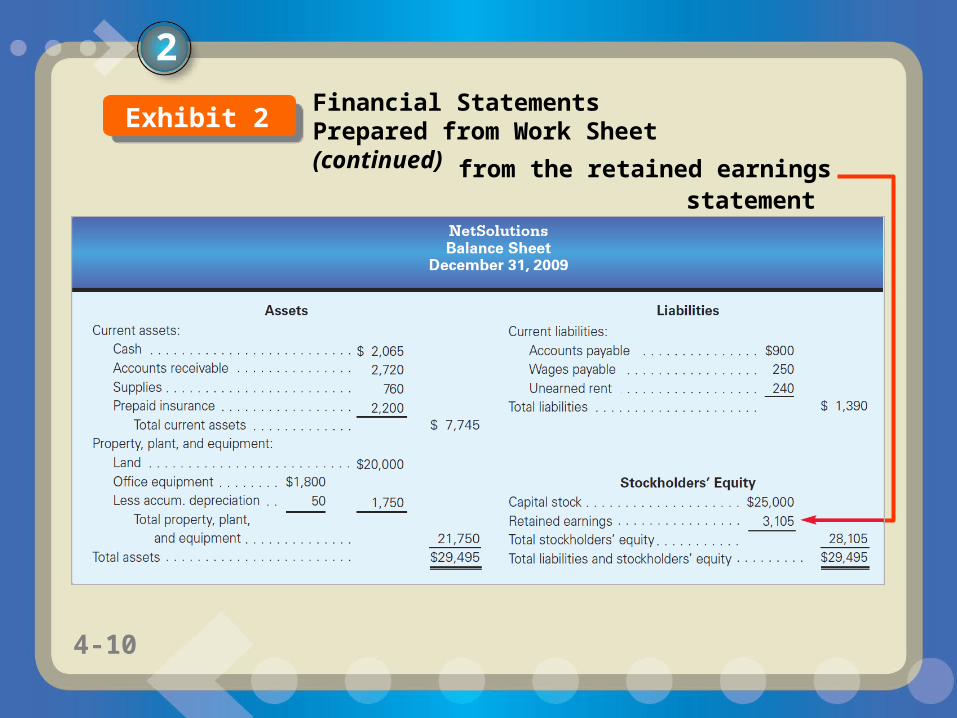

to retained earnings statement

2

Financial Statements Prepared from Work SheetExhibit 2

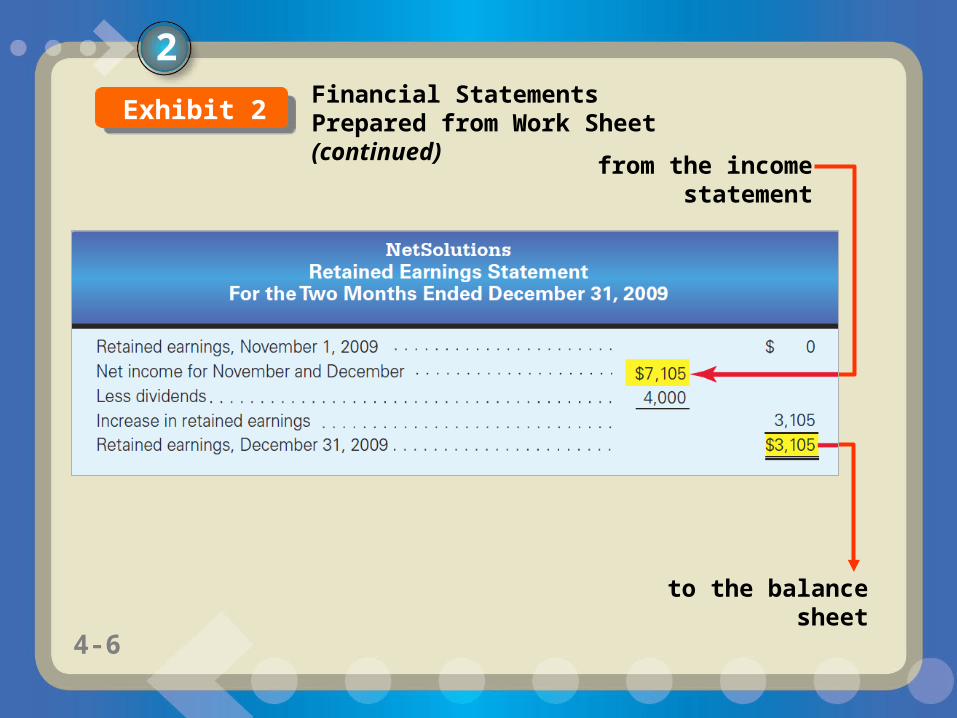

61-64-6

from the income statement

to the balance sheet

2Financial Statements Prepared from Work Sheet (continued)Exhibit 2

71-74-7

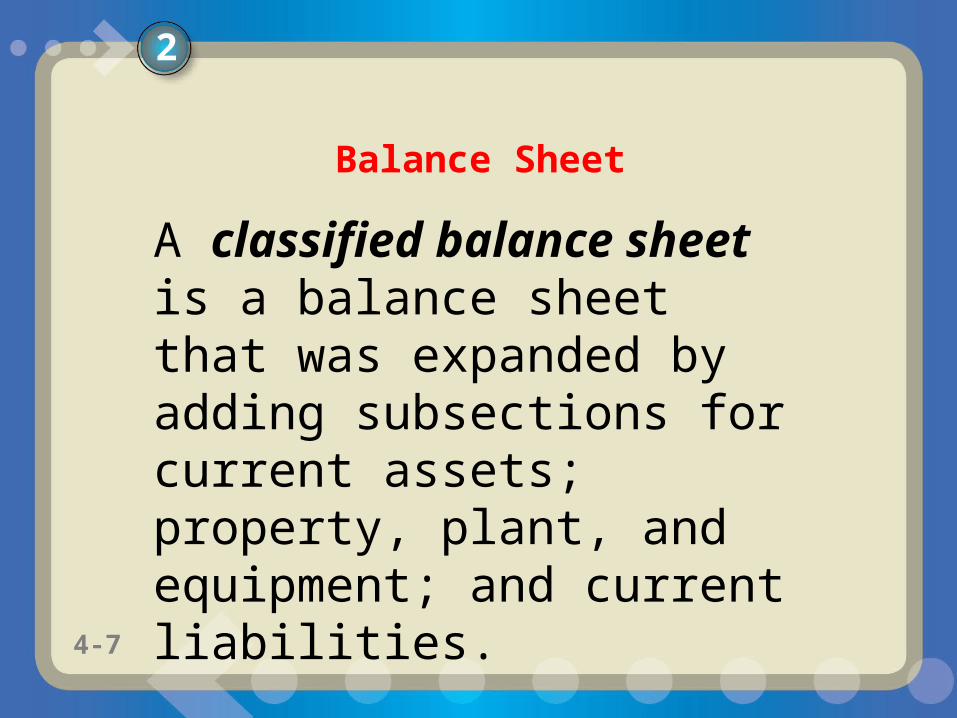

A classified balance sheet is a balance sheet that was expanded by adding subsections for current assets; property, plant, and equipment; and current liabilities.

2

Balance Sheet

81-84-8

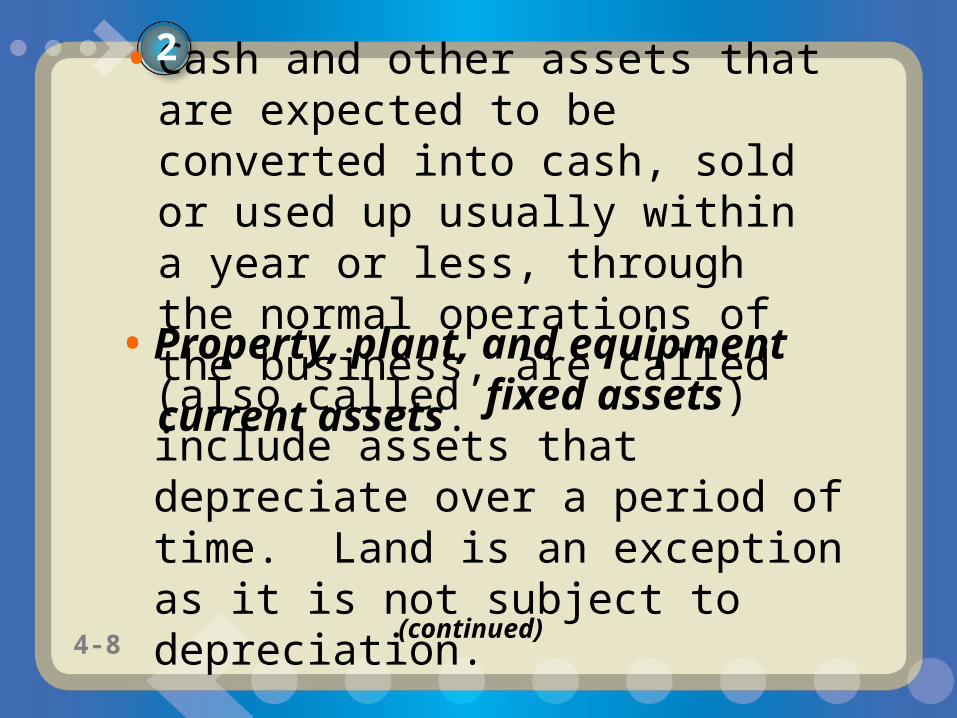

• Cash and other assets that are expected to be converted into cash, sold or used up usually within a year or less, through the normal operations of the business, are called current assets.

2

• Property, plant, and equipment (also called fixed assets) include assets that depreciate over a period of time. Land is an exception as it is not subject to depreciation.

(continued)

91-94-9

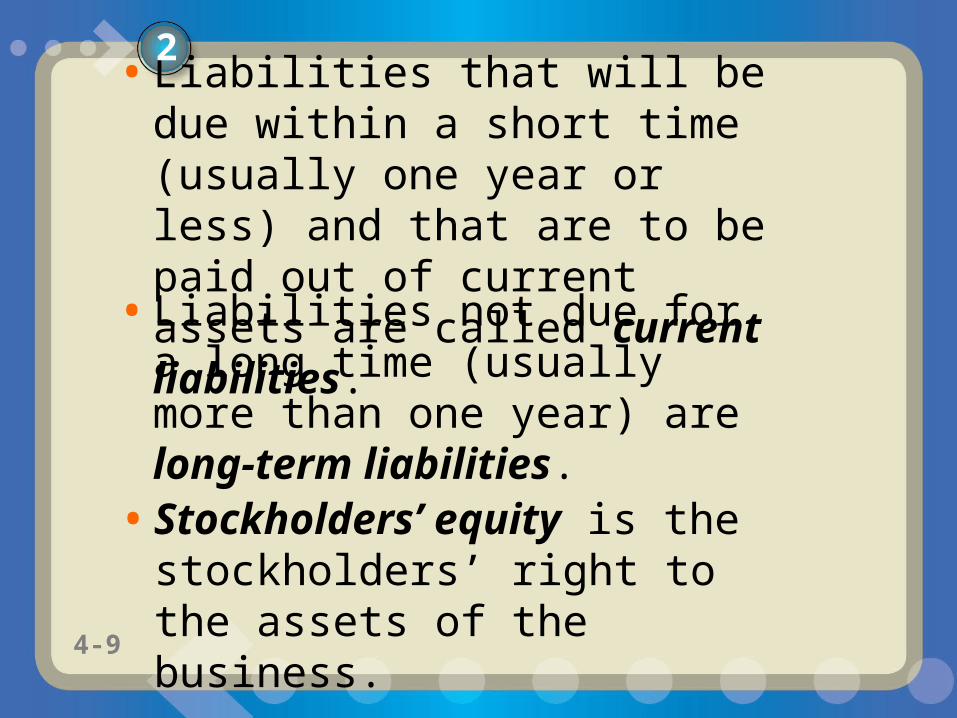

• Liabilities that will be due within a short time (usually one year or less) and that are to be paid out of current assets are called current liabilities.

2

• Liabilities not due for a long time (usually more than one year) are long-term liabilities.

• Stockholders’ equity is the stockholders’ right to the assets of the business.

101-104-10

from the retained earnings statement

2Financial Statements Prepared from Work Sheet (continued)Exhibit 2

111-114-11

Prepare closing entries.

3

4-11

121-124-12

Accounts that are relatively permanent from year to year are called real accounts. Accounts that report amounts for only one period are called temporary accounts or nominal accounts.

3

Closing Entries

131-134-13

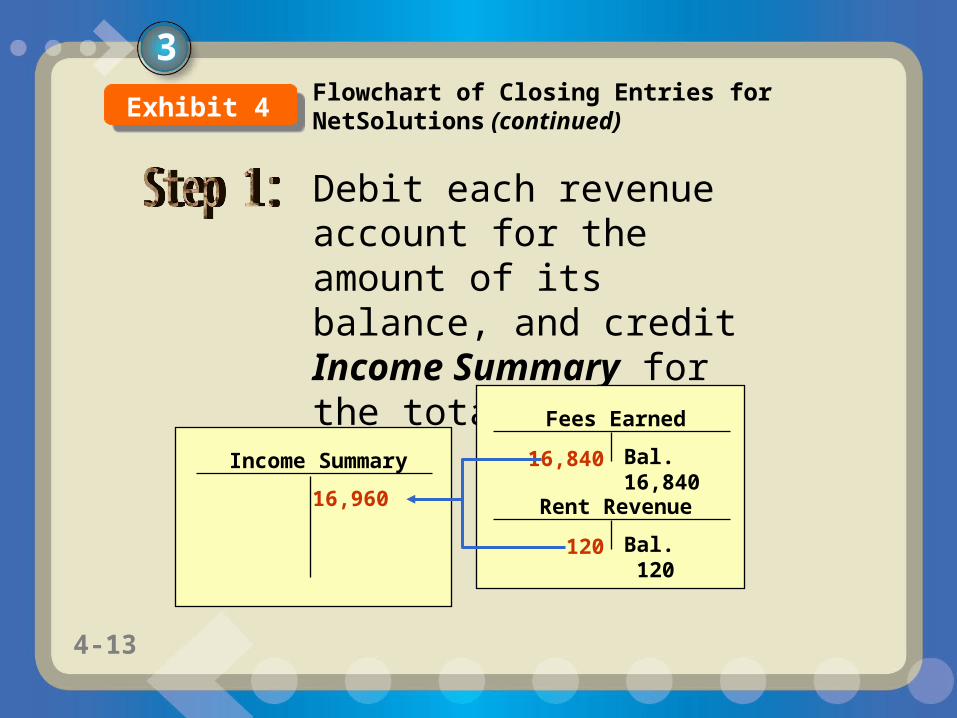

Debit each revenue account for the amount of its balance, and credit Income Summary for the total revenue.

Fees Earned

Bal. 16,840

Rent Revenue

Bal. 120

Income Summary 16,840

120

16,960

3Flowchart of Closing Entries for NetSolutions (continued) Exhibit 4

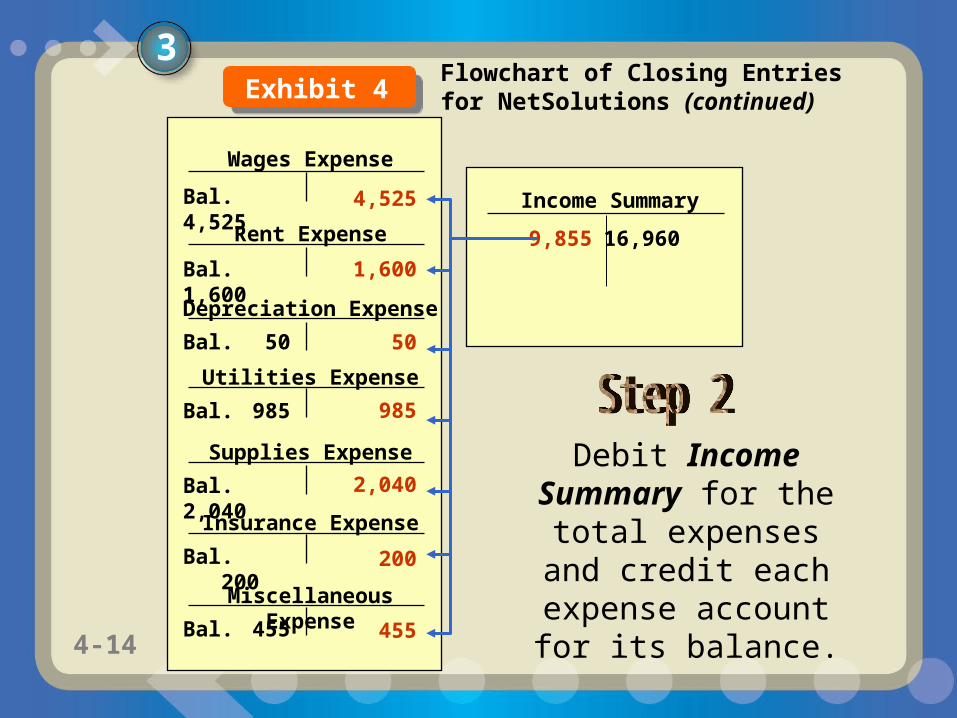

141-144-14

Wages Expense

Rent Expense

Depreciation Expense

Utilities Expense

Supplies Expense

Insurance Expense

Bal. 200

Miscellaneous Expense

Bal. 455

Income Summary

Debit Income Summary for the total expenses and

credit each expense account for its balance.

16,960

Bal. 4,525

Bal. 1,600

Bal. 50

Bal. 985

Bal. 2,040

9,855

455

200

2,040

985

50

1,600

4,525

3Flowchart of Closing Entries for NetSolutions (continued)Exhibit 4

151-154-15

Retained Earnings

Bal. 0

Dividends

Bal. 4,000

Income Summary

16,9609,8557,105

7,105

Debit Income Summary for the

amount of its balance (in this case, the net income) and credit Retained Earnings.

3Flowchart of Closing Entries for NetSolutions (continued)

Exhibit 4

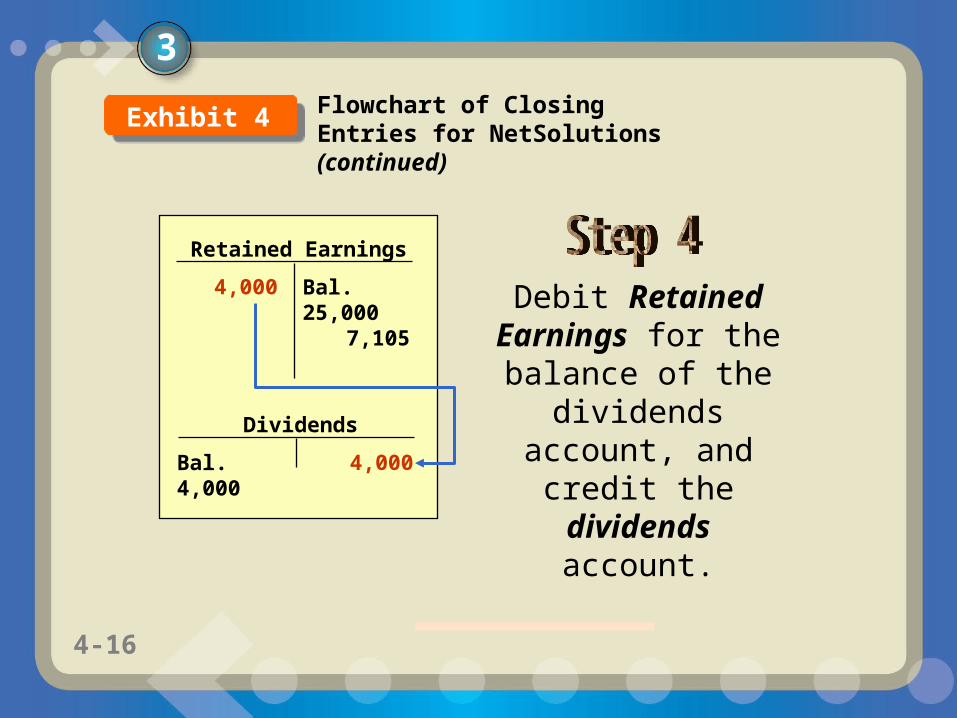

161-164-16

Retained Earnings

Bal. 25,0007,105

Dividends

Bal. 4,000 4,000

4,000 Debit Retained Earnings for the

balance of the dividends account, and

credit the dividends account.

3

Flowchart of Closing Entries for NetSolutions (continued)

Exhibit 4

171-174-17

3

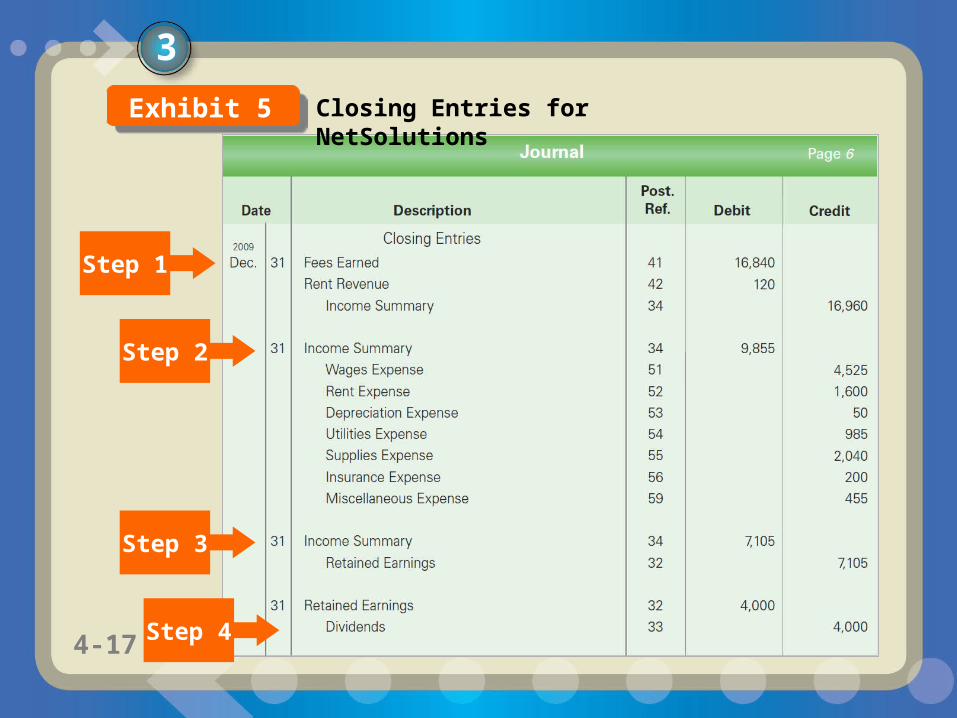

Closing Entries for NetSolutions

Step 2

Step 3

Step 1

Step 4

Exhibit 5

181-184-18

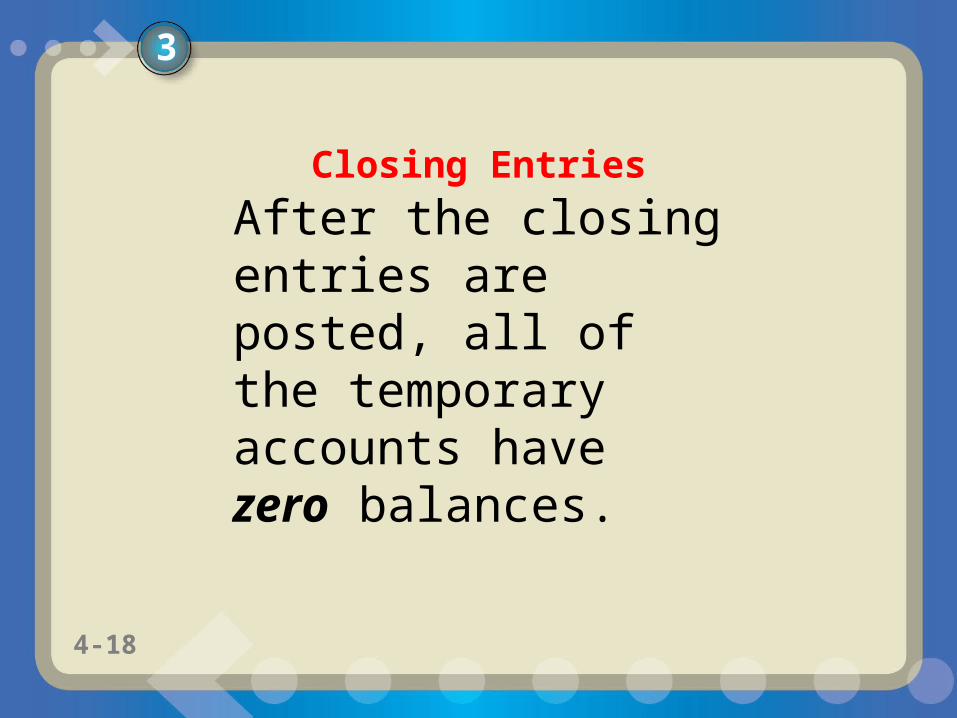

After the closing entries are posted, all of the temporary accounts have zero balances.

3

Closing Entries

191-194-19

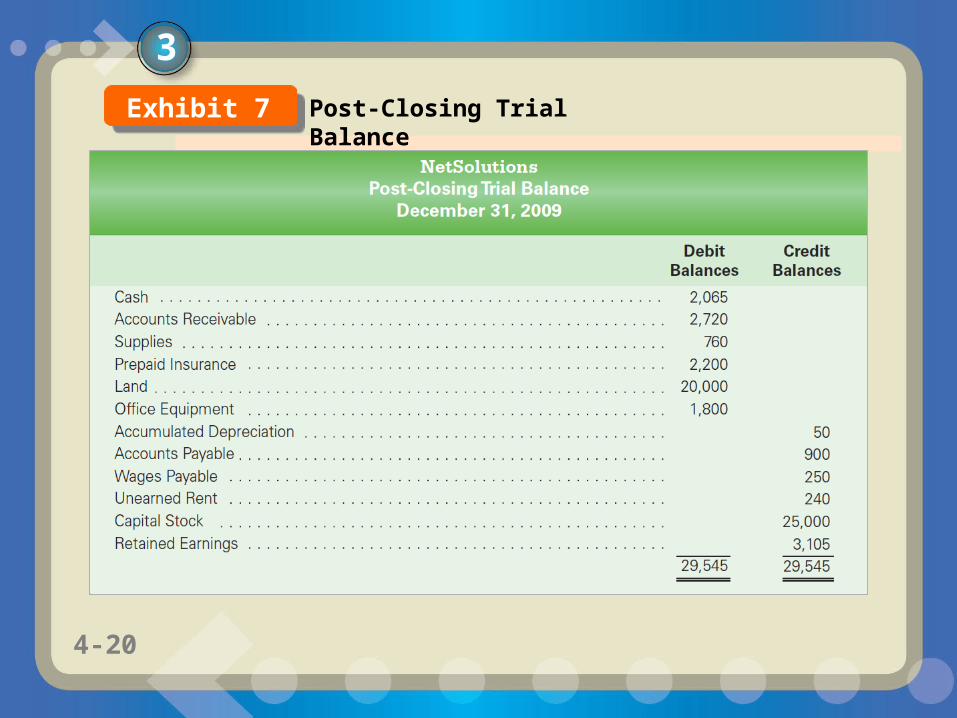

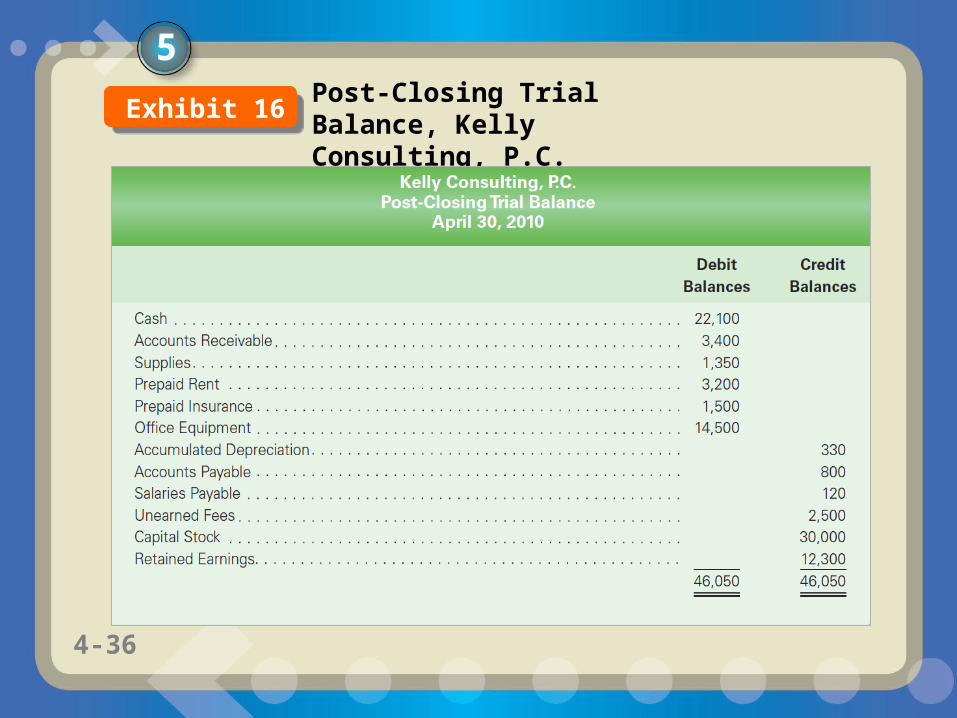

A post-closing trial balance is prepared after the closing entries have been posted. The purpose of the PCTB is to verify that the ledger is in balance at the beginning of the next period.

3

Post-Closing Trial Balance

201-204-20

3

Post-Closing Trial BalanceExhibit 7

211-214-21

Describe the accounting cycle.

4

4-21

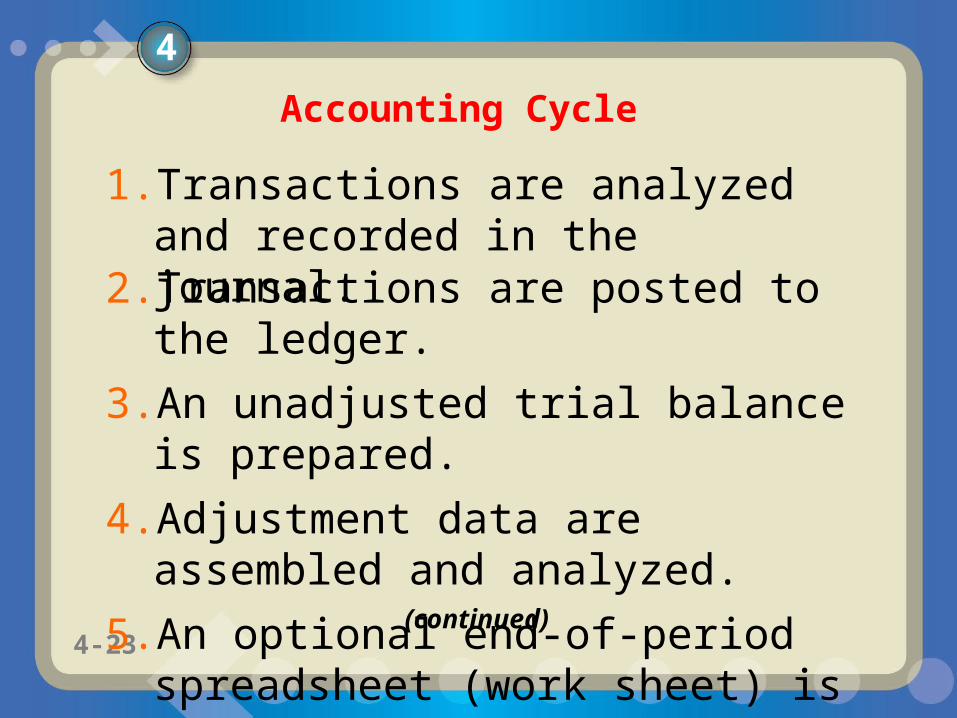

221-224-22

The accounting process that begins with analyzing and journalizing transactions and ends with preparing the accounting records for the next period’s transactions is called the accounting cycle. There are ten steps in the accounting cycle.

4

231-234-23

2. Transactions are posted to the ledger.

3. An unadjusted trial balance is prepared.

4. Adjustment data are assembled and analyzed.

5. An optional end-of-period spreadsheet (work sheet) is prepared.

1. Transactions are analyzed and recorded in the journal.

(continued)

Accounting Cycle

4

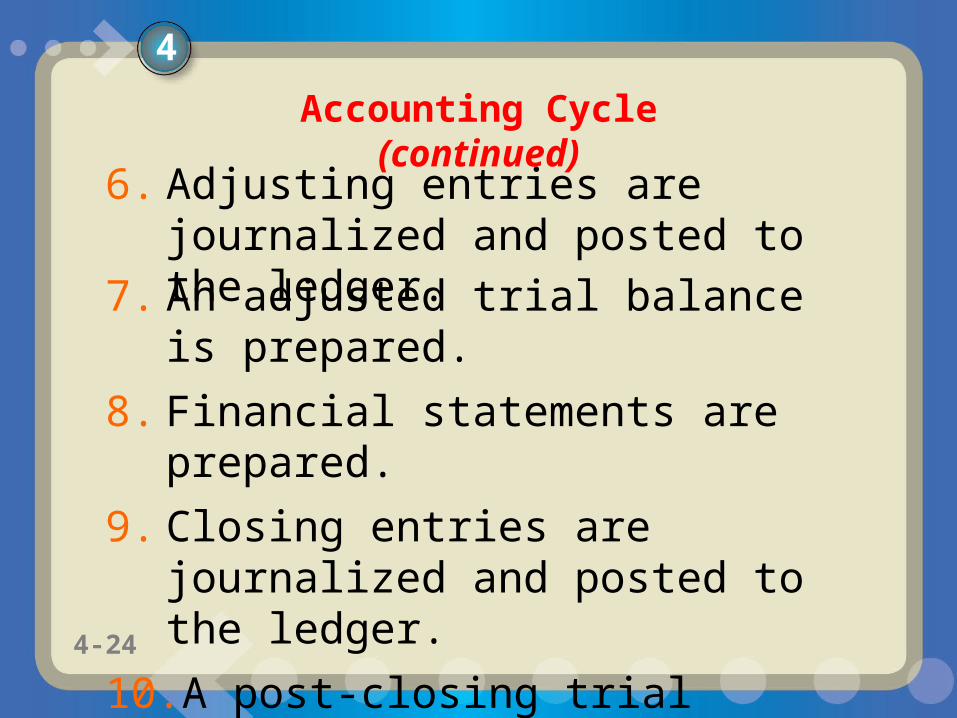

241-244-24

7. An adjusted trial balance is prepared.

8. Financial statements are prepared.

9. Closing entries are journalized and posted to the ledger.

10. A post-closing trial balance is prepared.

6. Adjusting entries are journalized and posted to the ledger.

Accounting Cycle (continued)

4

251-254-25

5

Illustrate the accounting cycle for one period.

4-25

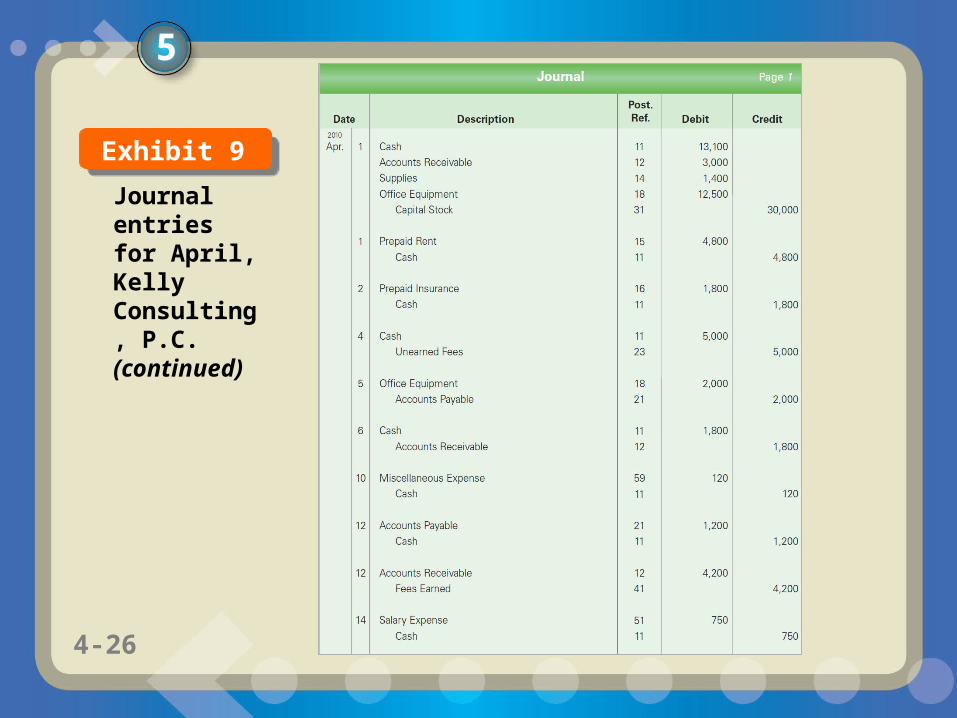

261-264-26

5

Journal entries for April, Kelly Consulting, P.C. (continued)

Exhibit 9

271-274-27

5

Journal entries for April, Kelly Consulting, P.C. (concluded)

Exhibit 9

281-284-28

5Unadjusted Trial Balance, Kelly ConsultingExhibit 10

291-294-29

5

End-of-Period Spreadsheet (Work Sheet)Exhibit 11

4-29

301-304-30

5

Adjusting Entries, Kelly Consulting, P.C.

Exhibit 12

311-314-31

5Adjusted Trial Balance, Kelly Consulting, P.C.

Exhibit 13

321-324-32

5

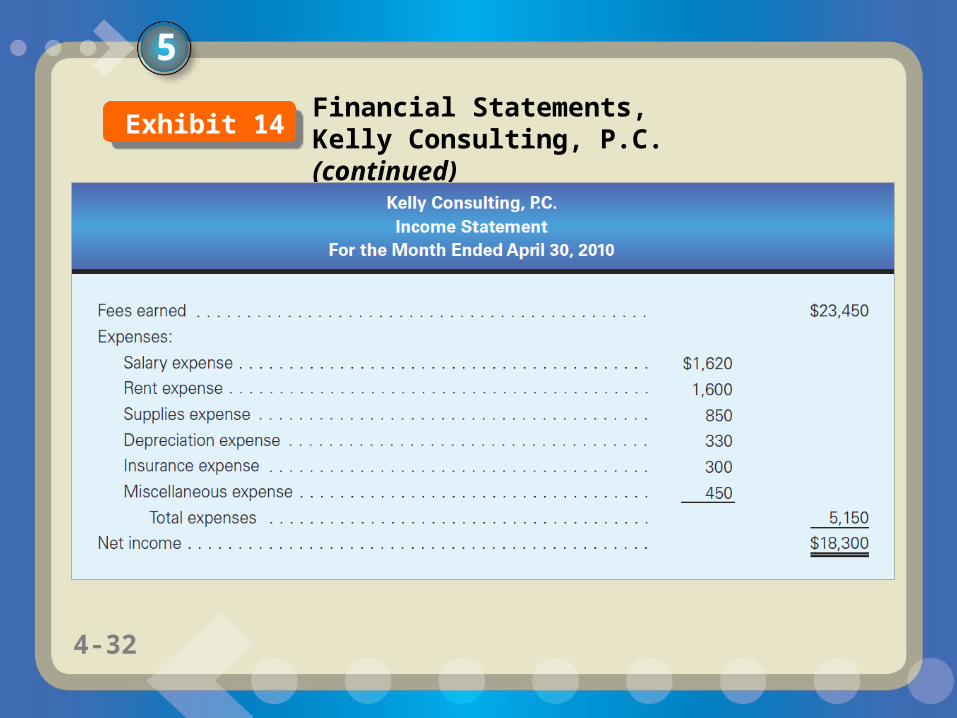

Financial Statements, Kelly Consulting, P.C. (continued)

Exhibit 14

331-334-33

5

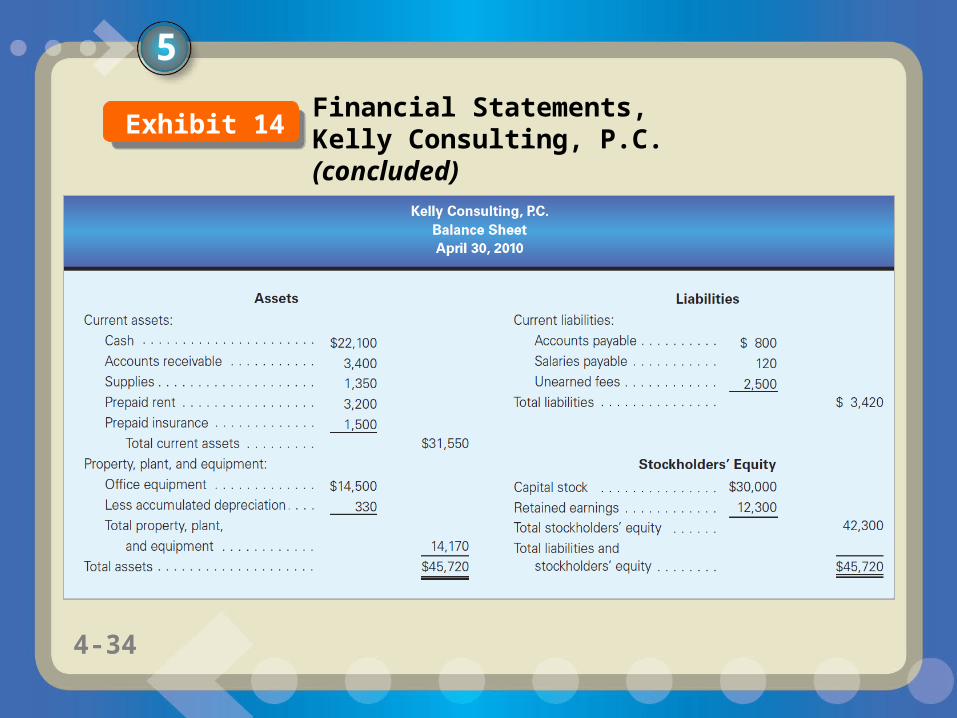

Exhibit 14Financial Statements, Kelly Consulting, P.C. (continued)

341-344-34

Exhibit 14

5

Financial Statements, Kelly Consulting, P.C. (concluded)

351-354-35

5

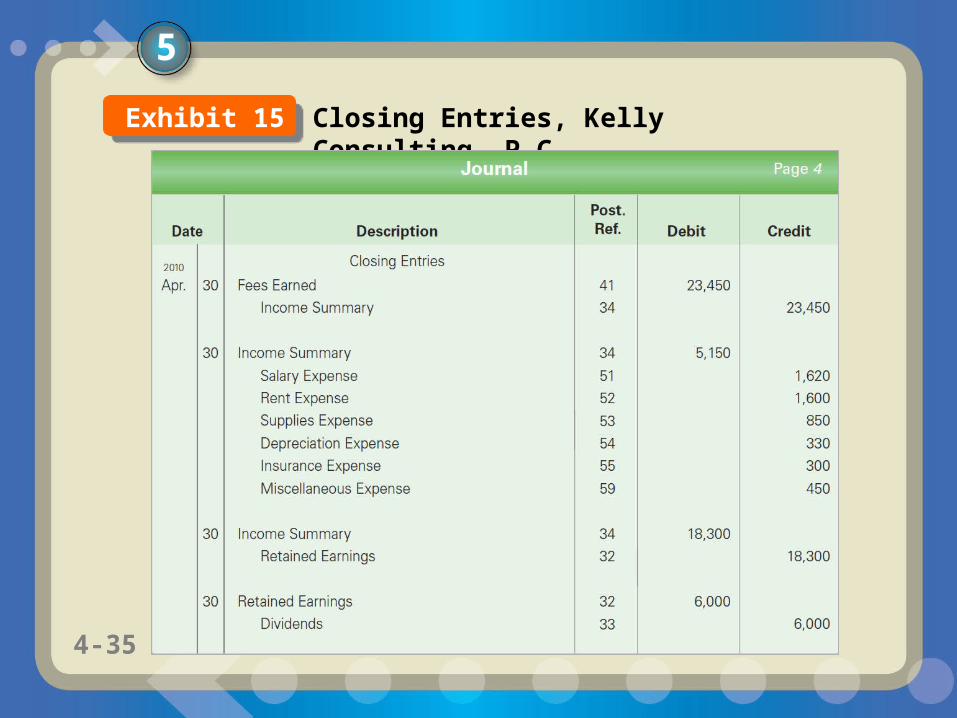

Closing Entries, Kelly Consulting, P.C.Exhibit 15

361-364-36

5Post-Closing Trial Balance, Kelly Consulting, P.C.

Exhibit 16

371-374-37

6

Explain what is meant by the fiscal year and the natural business year.

4-37

381-384-38

The annual accounting period adopted by a business is known as its fiscal year. When a business adopts a fiscal year that ends when business activities have reached the lowest point in its annual operation, such a fiscal year is also called the natural year.

6

Fiscal Year

391-394-39

Financial History of a Business

6

401-404-40

Appendix 1: End-of-Period Spreadsheet (Work Sheet)

4-40

411-414-41

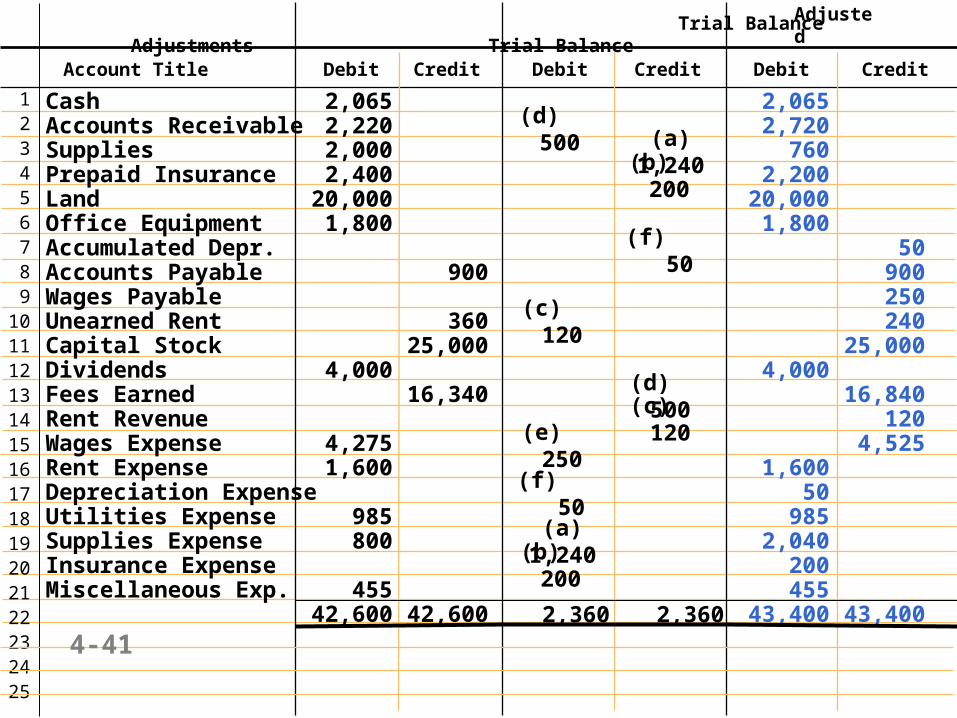

Account Title Debit Credit Debit Credit Debit Credit

Trial Balance Adjustments Trial Balance

123456789

10111213141516171819202122232425

Adjusted

2,360 2,360

(b) 200(a) 1,240

(d) 500

(c) 120

(c) 120(d) 500

(f) 50

(b) 200(a) 1,240

(e) 250

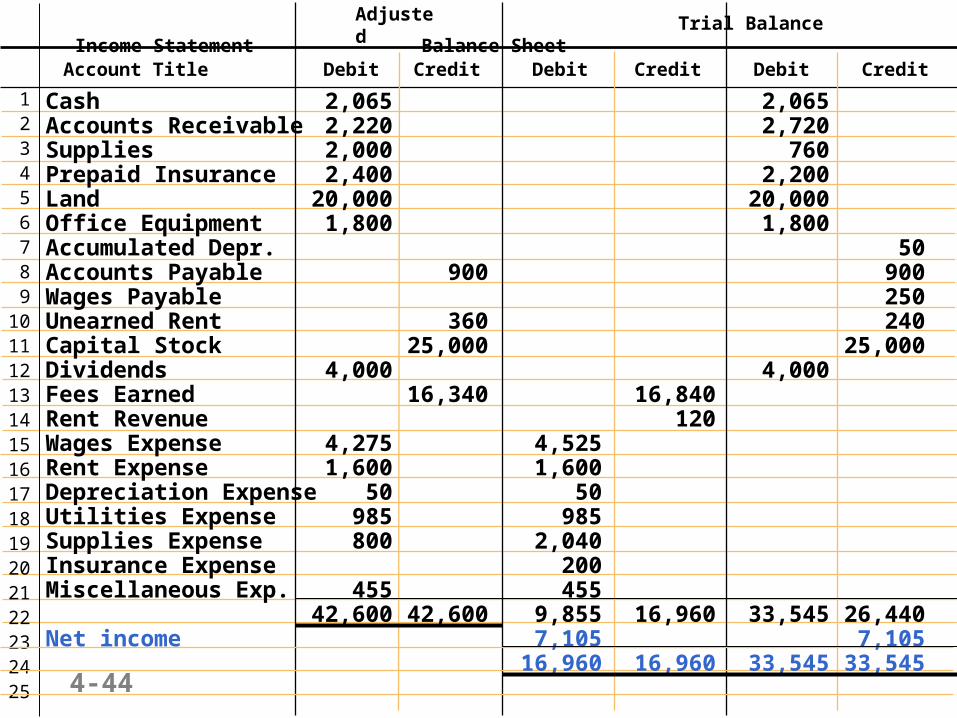

Cash 2,065 2,065Accounts Receivable 2,220 2,720Supplies 2,000 760Prepaid Insurance 2,400 2,200Land 20,000 20,000Office Equipment 1,800 1,800Accumulated Depr. 50Accounts Payable 900 900Wages Payable 250Unearned Rent 360 240Capital Stock 25,000 25,000Dividends 4,000 4,000Fees Earned 16,340 16,840Rent Revenue 120Wages Expense 4,275 4,525Rent Expense 1,600 1,600Depreciation Expense 50Utilities Expense 985 985Supplies Expense 800 2,040Insurance Expense 200Miscellaneous Exp. 455 455

42,600 42,600 43,400 43,400

(f) 50

4-41

421-424-42

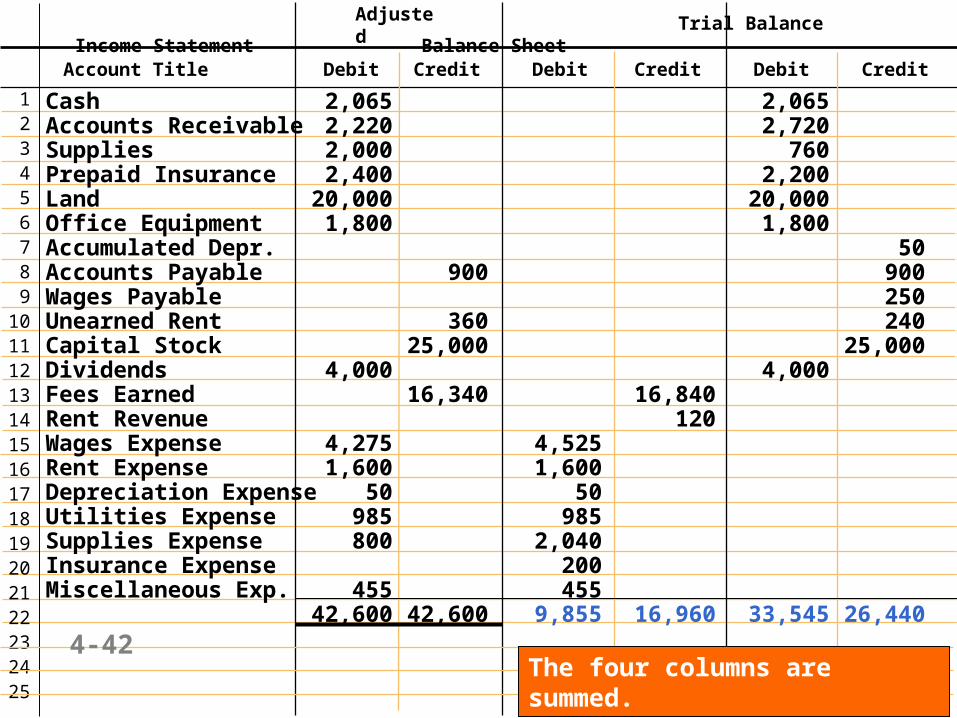

Account Title Debit Credit Debit Credit Debit Credit

Trial Balance Income Statement Balance Sheet

123456789

10111213141516171819202122232425

Adjusted

The four columns are summed.

Cash 2,065 2,065Accounts Receivable 2,220 2,720Supplies 2,000 760Prepaid Insurance 2,400 2,200Land 20,000 20,000Office Equipment 1,800 1,800Accumulated Depr. 50Accounts Payable 900 900Wages Payable 250Unearned Rent 360 240Capital Stock 25,000 25,000Dividends 4,000 4,000Fees Earned 16,340 16,840Rent Revenue 120Wages Expense 4,275 4,525Rent Expense 1,600 1,600Depreciation Expense 50 50Utilities Expense 985 985Supplies Expense 800 2,040Insurance Expense 200Miscellaneous Exp. 455 455

42,600 42,600 9,855 16,960 33,545 26,440

4-42

431-434-43

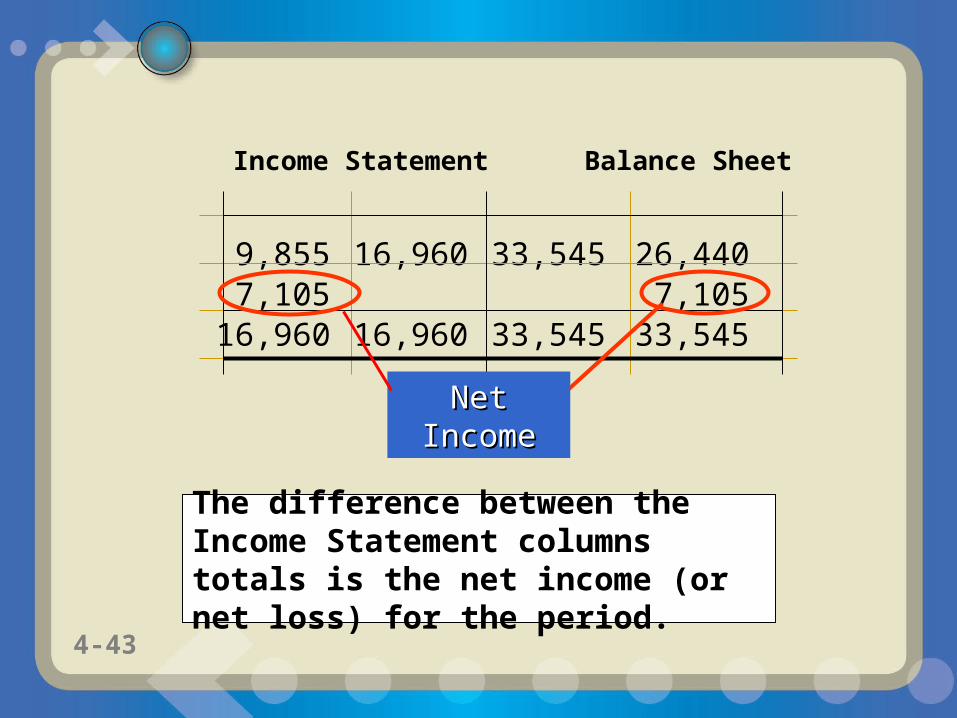

9,855 16,960 33,545 26,4407,105 7,105

16,960 16,960 33,545 33,545

Income Statement Balance Sheet

Net IncomeNet Income

The difference between the Income Statement columns totals is the net income (or net loss) for the period.

441-444-44

Account Title Debit Credit Debit Credit Debit Credit

Trial Balance Income Statement Balance Sheet

123456789

10111213141516171819202122232425

Adjusted

Cash 2,065 2,065Accounts Receivable 2,220 2,720Supplies 2,000 760Prepaid Insurance 2,400 2,200Land 20,000 20,000Office Equipment 1,800 1,800Accumulated Depr. 50Accounts Payable 900 900Wages Payable 250Unearned Rent 360 240Capital Stock 25,000 25,000Dividends 4,000 4,000Fees Earned 16,340 16,840Rent Revenue 120Wages Expense 4,275 4,525Rent Expense 1,600 1,600Depreciation Expense 50 50Utilities Expense 985 985Supplies Expense 800 2,040Insurance Expense 200Miscellaneous Exp. 455 455

42,600 42,600 9,855 16,960 33,545 26,440Net income 7,105 7,105

16,960 16,960 33,545 33,5454-44

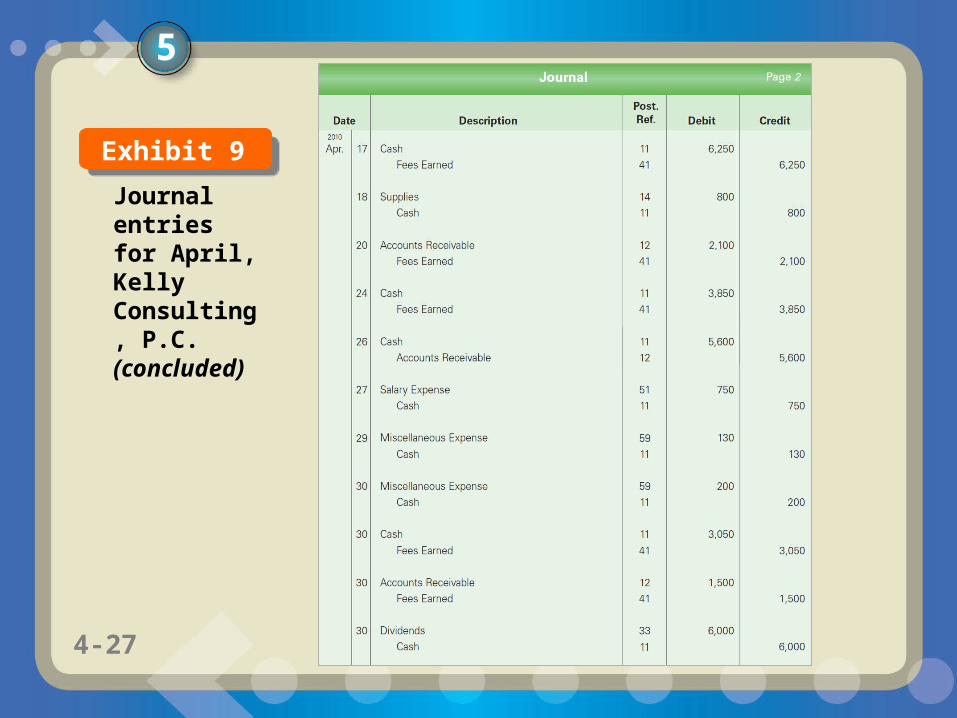

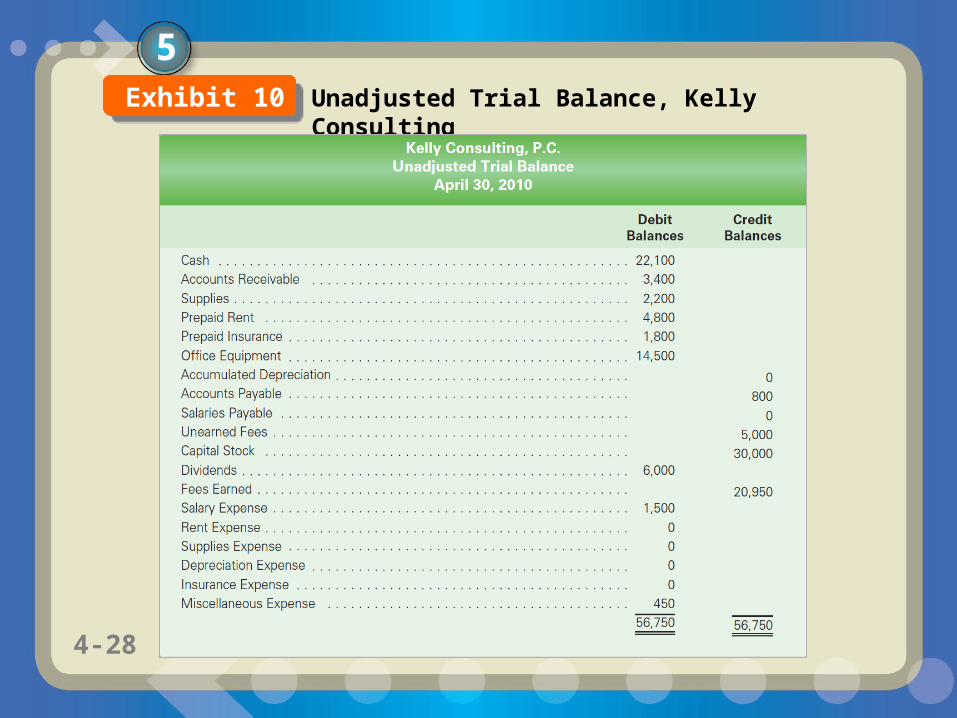

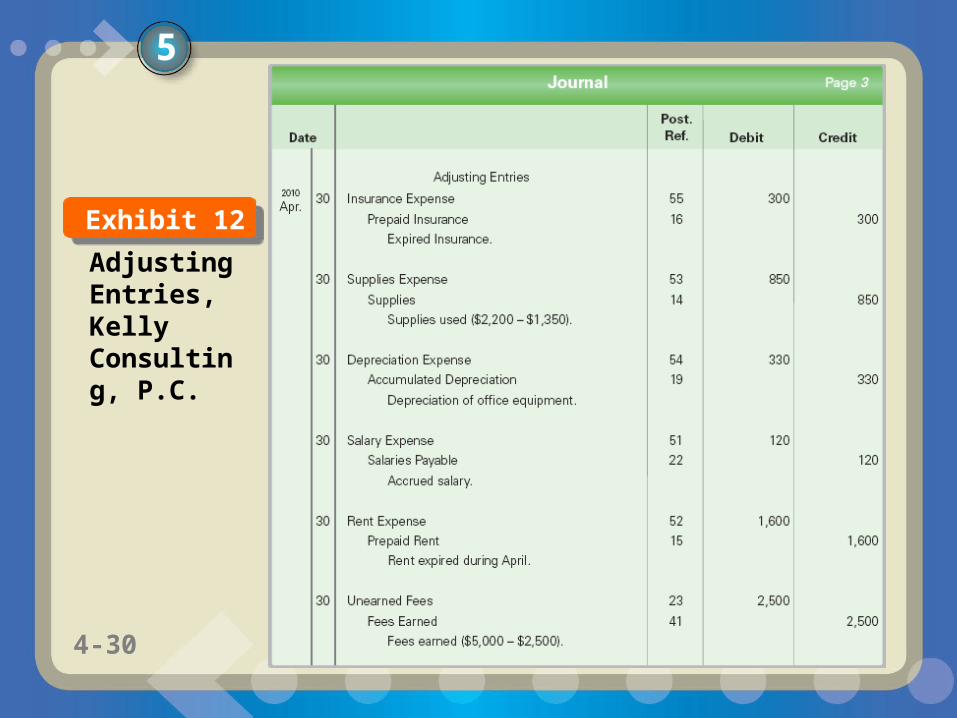

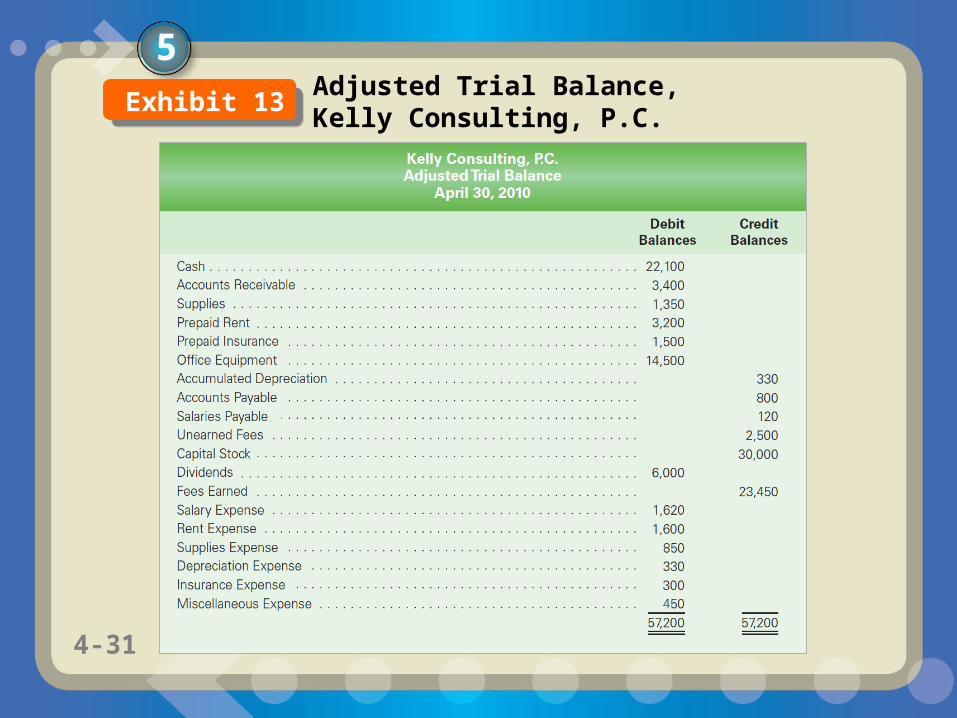

451-454-45