Completing the Accounting Cycle -...

66

C H A P T E R ELECTRONIC ARTS I N C. 4 Completing the Accounting Cycle M ost of us have had to file a personal tax return. At the beginning of the year, you estimate your up- coming income and decide whether you need to increase your payroll tax withholdings or perhaps pay estimated taxes. During the year, you earn income and enter into tax- related transactions, such as making charitable contribu- tions. At the end of the year, your employer sends you a tax withholding information form (W-2) form, and you col- lect the tax records needed for completing your yearly tax forms. As the next year begins, you start the cycle all over again. Businesses also go through a cycle of activities. For ex- ample, Electronic Arts Inc., the world’s largest developer and marketer of electronic game software, begins its cycle by developing new or revised game titles, such as Madden NFL Football ® , Need for Speed ® , Tiger Woods PGA Tour ® , The Sims ® , and The Lord of the Rings ® . These games are marketed and sold throughout the year. During the year, operating transactions of the business are recorded. For Electronic Arts, such transactions include the salaries for game developers, advertising expenditures, costs for pro- ducing and packaging games, and game revenues. At the end of the year, financial statements are prepared that sum- marize the operating activities for the year. Electronic Arts publishes these statements on its Web site at http:// investor.ea.com. Finally, before the start of the next year, the accounts are readied for recording the operations of the next year. As we saw in Chapter 1, the initial cycle for NetSolutions began with Chris Clark’s investment in the business on November 1, 2009. The cycle continued with recording NetSolutions’ transactions for November and December, as we discussed and illustrated in Chapters 1 and 2. In Chapter 3, the cycle continued when the adjust- ing entries for the two months ending December 31, 2009, were recorded. In this chapter, we complete the cycle for NetSolutions by preparing financial statements and getting the accounts ready for recording transactions of the next period. © AP Photo/Gregory Bull

Transcript of Completing the Accounting Cycle -...

C H A P T E R

E L E C T R O N I C A R T S I N C.

4

Completing the Accounting Cycle

Most of us have had to file a personal tax return. At

the beginning of the year, you estimate your up-

coming income and decide whether you need to increase

your payroll tax withholdings or perhaps pay estimated

taxes. During the year, you earn income and enter into tax-

related transactions, such as making charitable contribu-

tions. At the end of the year, your employer sends you a

tax withholding information form (W-2) form, and you col-

lect the tax records needed for completing your yearly tax

forms. As the next year begins, you start the cycle all over

again.

Businesses also go through a cycle of activities. For ex-

ample, Electronic Arts Inc., the world’s largest developer

and marketer of electronic game software, begins its cycle

by developing new or revised game titles, such as Madden

NFL Football®, Need for Speed®, Tiger Woods PGA Tour®,

The Sims®, and The Lord of the Rings®. These games are

marketed and sold throughout the year. During the year,

operating transactions of the business are recorded. For

Electronic Arts, such transactions include the salaries for

game developers, advertising expenditures, costs for pro-

ducing and packaging games, and game revenues. At the

end of the year, financial statements are prepared that sum-

marize the operating activities for the year. Electronic Arts

publishes these statements on its Web site at http:// investor.ea.com. Finally, before the start of the next year,

the accounts are readied for recording the operations of the

next year.

As we saw in Chapter 1, the initial cycle for NetSolutions

began with Chris Clark’s investment in the business on

November 1, 2009. The cycle continued with recording

NetSolutions’ transactions for November and December, as

we discussed and illustrated in Chapters 1 and 2. In Chapter

3, the cycle continued when the adjust-

ing entries for the two months ending

December 31, 2009, were recorded. In

this chapter, we complete the cycle for

NetSolutions by preparing financial

statements and getting the accounts

ready for recording transactions of the

next period.

© A

P Ph

oto

/Gre

go

ry B

ull

144 Chapter 4 Completing the Accounting Cycle

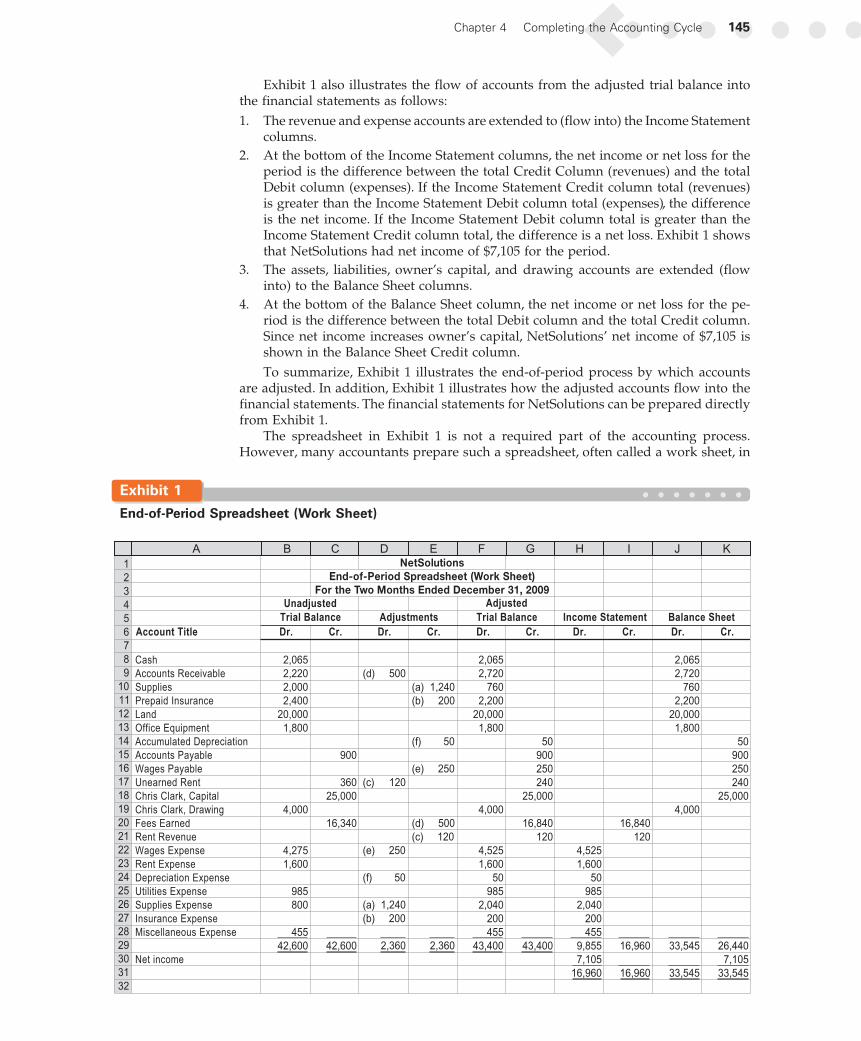

Flow of Accounting InformationThe end-of-period process by which accounts are adjusted and the financial statementsare prepared is one of the most important in accounting. Using our illustration ofNetSolutions from Chapters 1–3, this process is summarized in spreadsheet form inExhibit 1.

Exhibit 1 begins with the unadjusted trial balance as of the end of the period. Theunadjusted trial balance verifies that the total of the debit balances equals the total ofthe credit balances. If the trial balance totals are unequal, an error has occurred. Anyerror must be found and corrected before the end-of-period process can continue.

The adjustments for NetSolutions from Chapter 3 are shown in the Adjustmentscolumns of Exhibit 1. Cross-referencing (by letters) the debit and credit of each adjustmentis useful in reviewing the impact of the adjustments on the unadjusted account balances.The adjustments are normally entered in the order in which the data are assembled. If thetitles of the accounts to be adjusted do not appear in the unadjusted trial balance, the ac-counts are inserted in their proper order in the Account Title column. The total of theAdjustments columns verifies that the debits equals the credits for the adjustment data andadjusting entries. The total of the Debit column must equal the total of the Credit column.

The adjustment data are added to or subtracted from the amounts in the UnadjustedTrial Balance columns to arrive at the Adjusted Trial Balance columns. In this way, theAdjusted Trial Balance columns of Exhibit 1 illustrate the impact of the adjusting entrieson the unadjusted accounts. The totals of the Adjusted Trial Balance columns verifythe equality of the totals of the debit and credit balances after adjustment.

Describe the flow of accountinginformation from the unadjusted trialbalance into theadjusted trial balance and financial statements.

Explain what is meant by the fiscal year and thenatural business year.

Fiscal Year

Prepare financialstatements from adjusted account balances.

IncomeStatement

Statement ofOwner’s Equity

Balance Sheet

FinancialStatements

Closing Entries

Journalizing and PostingClosing Entries

Prepare closing entries.

Post-Closing TrialBalance

Describe the accounting cycle.

Accounting Cycle Illustration of theAccounting Cycle

Illustrate the accounting cycle for one period.

After studying this chapter, you should be able to:1

At a Glance Menu Turn to pg 170

2 3 4 5 6

Describe

the flow of

accounting informa-

tion from the unad-

justed trial balance

into the adjusted trial

balance and financial

statements.

1

Flow ofAccountingInformation

EE 4-1(page 146)

EE 4-2(page 146)

EE 4-3(page 148)

EE 4-5(page 153)

EE 4-6(page 156)

EE 4-4(page 149)

Many companies useMicrosoft’s Excel® softwareto prepare end-of-periodspreadsheets (work sheets).

Chapter 4 Completing the Accounting Cycle 145

Exhibit 1 also illustrates the flow of accounts from the adjusted trial balance intothe financial statements as follows:

1. The revenue and expense accounts are extended to (flow into) the Income Statementcolumns.

2. At the bottom of the Income Statement columns, the net income or net loss for theperiod is the difference between the total Credit Column (revenues) and the totalDebit column (expenses). If the Income Statement Credit column total (revenues)is greater than the Income Statement Debit column total (expenses), the differenceis the net income. If the Income Statement Debit column total is greater than theIncome Statement Credit column total, the difference is a net loss. Exhibit 1 showsthat NetSolutions had net income of $7,105 for the period.

3. The assets, liabilities, owner’s capital, and drawing accounts are extended (flowinto) to the Balance Sheet columns.

4. At the bottom of the Balance Sheet column, the net income or net loss for the pe-riod is the difference between the total Debit column and the total Credit column.Since net income increases owner’s capital, NetSolutions’ net income of $7,105 isshown in the Balance Sheet Credit column.

To summarize, Exhibit 1 illustrates the end-of-period process by which accountsare adjusted. In addition, Exhibit 1 illustrates how the adjusted accounts flow into thefinancial statements. The financial statements for NetSolutions can be prepared directlyfrom Exhibit 1.

The spreadsheet in Exhibit 1 is not a required part of the accounting process.However, many accountants prepare such a spreadsheet, often called a work sheet, in

Cash

Accounts Receivable

Supplies

Prepaid Insurance

Land

Office Equipment

Accumulated Depreciation

Accounts Payable

Wages Payable

Unearned Rent

Chris Clark, Capital

Chris Clark, Drawing

Fees Earned

Rent Revenue

Wages Expense

Rent Expense

Depreciation Expense

Utilities Expense

Supplies Expense

Insurance Expense

Miscellaneous Expense

Net income

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

NetSolutionsEnd-of-Period Spreadsheet (Work Sheet)

For the Two Months Ended December 31, 2009Unadjusted

Income Statement Adjustments Trial Balance Trial Balance

Account Title Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.

Balance Sheet

Adjusted

2,065

2,220

2,000

2,400

20,000

1,800

4,000

4,275

1,600

985

800

455

42,600

900

360

25,000

16,340

42,600

(d) 500

(c) 120

(e) 250

(f) 50

(a) 1,240

(b) 200

2,360

(a) 1,240

(b) 200

(f) 50

(e) 250

(d) 500

(c) 120

2,360

2,065

2,720

760

2,200

20,000

1,800

4,000

4,525

1,600

50

985

2,040

200

455

43,400

50

900

250

240

25,000

16,840

120

43,400

4,525

1,600

50

985

2,040

200

455

9,855

7,105

16,960

16,840

120

16,960

16,960

2,065

2,720

760

2,200

20,000

1,800

4,000

33,545

33,545

50

900

250

240

25,000

26,440

7,105

33,545

B C D E F G H I J K A

Exhibit 1

End-of-Period Spreadsheet (Work Sheet)

146 Chapter 4 Completing the Accounting Cycle

manual or electronic form, as part of their normal end-of-period process. The primaryadvantage in doing so is that it allows managers and accountants to see the impact ofthe adjustments on the financial statements. This is especially useful for adjustmentsthat depend upon estimates. We discuss such estimates and their impact on the finan-cial statements in later chapters.1

Example Exercise 4-1 Flow of Accounts into Financial Statements

The balances for the accounts listed below appear in the Adjusted Trial Balance columns of the end-of-period spreadsheet (work sheet). Indicate whether each balance should be extended to (a) an IncomeStatement column or (b) a Balance Sheet column.

1. Amber Bablock, Drawing 5. Fees Earned2. Utilities Expense 6. Accounts Payable3. Accumulated Depreciation—Equipment 7. Rent Revenue4. Unearned Rent 8. Supplies

1

Follow My Example 4-1

1. Balance Sheet column 5. Income Statement column2. Income Statement column 6. Balance Sheet column3. Balance Sheet column 7. Income Statement column4. Balance Sheet column 8. Balance Sheet column

For Practice: PE 4-1A, PE 4-1B

Example Exercise 4-2 Determining Net Income from End-of-Period Spreadsheet

In the Balance Sheet columns of the end-of-period spreadsheet (work sheet) for Dimple Consulting Co.for the current year, the Debit column total is $678,450, and the Credit column total is $599,750 beforethe amount for net income or net loss has been included. In preparing the income statement from theend-of-period spreadsheet (work sheet), what is the amount of net income or net loss?

2

Follow My Example 4-2

A net income of $78,700 ($678,450 � $599,750) would be reported. When the Debit column of theBalance Sheet columns is more than the Credit column, net income is reported. If the Credit column exceeds the Debit column, a net loss is reported.

For Practice: PE 4-2A, PE 4-2B

Financial StatementsUsing Exhibit 1, the financial statements for NetSolutions can be prepared. The incomestatement, the statement of owner’s equity, and the balance sheet are shown in Exhibit 2.

Income StatementThe income statement is prepared directly from the Income Statement or Adjusted TrialBalance columns of Exhibit 1 beginning with fees earned of $16,840. The expenses inthe income statement in Exhibit 2 are listed in order of size, beginning with the largeritems. Miscellaneous expense is the last item, regardless of its amount.

Prepare

financial

statements from

adjusted account

balances.

2

1 The appendix to this chapter describes and illustrates how to prepare the end-of-period spreadsheet (work sheet)shown in Exhibit 1.

Chapter 4 Completing the Accounting Cycle 147

Fees earned

Rent revenue

Total revenues

Expenses:

Wages expense

Supplies expense

Rent expense

Utilities expense

Insurance expense

Depreciation expense

Miscellaneous expense

Total expenses

Net income

$16,840

120

$4,525

2,040

1,600

985

200

50

455

$16,960

9,855

$ 7,105

$ 0

28,105

$28,105

$25,000

7 ,105

$32,105

4,000

Chris Clark, capital, November 1, 2009

Investment on November 1, 2009

Net income for November and December

Less withdrawals

Increase in owner’s equity

Chris Clark, capital, December 31, 2009

Current assets:

Cash

Accounts receivable

Supplies

Prepaid insurance

Total current assets

Property, plant, and equipment:

Land

Office equipment

Less accum. depreciation

Total property, plant,

and equipment

Total assets

$ 7,745

21,750

$29,495

$ 2,065

2,720

760

2,200

$20,000

1,750

Current liabilities:

Accounts payable

Wages payable

Unearned rent

Total liabilities

$900

250

240

Chris Clark, capital

Total liabilities and

owner’s equity

Liabilities

Owner’s Equity

Assets

$ 1,390

28,105

$29,495

NetSolutionsIncome Statement

For the Two Months Ended December 31, 2009

NetSolutionsStatement of Owner’s Equity

For the Two Months Ended December 31, 2009

NetSolutionsBalance Sheet

December 31, 2009

$1,800

50

Exhibit 2

Financial Statements Prepared from Work Sheet

148 Chapter 4 Completing the Accounting Cycle

Statement of Owner’s EquityThe first item presented on the statement of owner’s equity is the balance of the owner’scapital account at the beginning of the period. The amount listed as owner’s capital inthe spreadsheet, however, is not always the account balance at the beginning of the pe-riod. The owner may have invested additional assets in the business during the period.Thus, for the beginning balance and any additional investments, it is necessary to re-fer to the owner’s capital account in the ledger. These amounts, along with the net in-come (or net loss) and the drawing account balance, are used to determine the endingowner’s capital account balance.

The basic form of the statement of owner’s equity is shown in Exhibit 2. ForNetSolutions, the amount of drawings by the owner was less than the net income. If theowner’s withdrawals had exceeded the net income, the order of the net income and thewithdrawals would have been reversed. The difference between the two items would thenbe deducted from the beginning capital account balance. Other factors, such as additionalinvestments or a net loss, also require some change in the form, as shown below.

Allan Johnson, capital, January 1, 2009 $39,000Additional investment during the year 6,000__________

Total $45,000Net loss for the year $ 5,600Withdrawals 9,500__________

Decrease in owner’s equity 15,100__________

Allan Johnson, capital, December 31, 2009 $29,900____________________

THE ROUND TRIP

A common type of fraud involves artificially inflating revenue. One fraudulent method of inflating revenue iscalled “round tripping.” Under this scheme, a sellingcompany (S) “lends” money to a customer company (C).The money is then used by C to purchase a product

from S. Thus, S sells product to C and is paid with themoney just loaned to C! This looks like a sale in the ac-counting records, but in reality, S is shipping free prod-uct. The fraud is exposed when it is determined thatthere was no intent to repay the original loan.

Example Exercise 4-3 Statement of Owner’s EquityZack Gaddis owns and operates Gaddis Employment Services. On January 1, 2009, Zack Gaddis, Capitalhad a balance of $186,000. During the year, Zack invested an additional $40,000 and withdrew $25,000. Forthe year ended December 31, 2009, Gaddis Employment Services reported a net income of $18,750.Prepare a statement of owner’s equity for the year ended December 31, 2009.

Follow My Example 4-3

GADDIS EMPLOYMENT SERVICESSTATEMENT OF OWNER’S EQUITY

For the Year Ended December 31, 2009

Zack Gaddis, capital, January 1, 2009 . . . . . . $186,000Additional investment during 2009 . . . . . . . . 40,000__________

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . $226,000Withdrawals . . . . . . . . . . . . . . . . . . . . . . . . $ 25,000Less net income . . . . . . . . . . . . . . . . . . . . . 18,750__________

Decrease in owner’s equity . . . . . . . . . . . . . 6,250___________

Zack Gaddis, capital, December 31, 2009 . . . $219,750______________________

For Practice: PE 4-3A, PE 4-3B

2

Chapter 4 Completing the Accounting Cycle 149

Balance SheetThe balance sheet is prepared directly from the Balance Sheet or Adjusted Trial Balancecolumns of Exhibit 1 beginning with Cash of $2,065.

The balance sheet in Exhibit 2 shows subsections for assets and liabilities. Such abalance sheet is a classified balance sheet. We describe these subsections next.

Assets Assets are commonly divided into two sections on the bal-ance sheet: (1) current assets and (2) property, plant, and equipment.

Current Assets Cash and other assets that are expected to be con-verted to cash or sold or used up usually within one year or less,through the normal operations of the business, are called currentassets. In addition to cash, the current assets may include notes re-ceivable, accounts receivable, supplies, and other prepaid expenses.

Notes receivable are amounts that customers owe. They are written promises topay the amount of the note and interest. Accounts receivable are also amounts cus-tomers owe, but they are less formal than notes. Accounts receivable normally resultfrom providing services or selling merchandise on account. Notes receivable and ac-counts receivable are current assets because they are usually converted to cash withinone year or less.

Property, Plant, and Equipment The property, plant, and equipment section may also bedescribed as fixed assets or plant assets.These assets include equipment,machinery,build-ings, and land. With the exception of land, as we discussed in Chapter 3, fixed assetsdepreciate over a period of time. The cost, accumulated depreciation, and book value ofeach major type of fixed asset are normally reported on the balance sheet or in the notesto the financial statements.

Liabilities Liabilities are the amounts the business owes to credi-tors. Liabilities are commonly divided into two sections on thebalance sheet: (1) current liabilities and (2) long-term liabilities.

Current Liabilities Liabilities that will be due within a short time(usually one year or less) and that are to be paid out of currentassets are called current liabilities. The most common liabilities in

this group are notes payable and accounts payable. Other current liabilities may in-clude Wages Payable, Interest Payable, Taxes Payable, and Unearned Fees.

Long-Term Liabilities Liabilities that will not be due for a long time (usually more thanone year) are called long-term liabilities. If NetSolutions had long-term liabilities, theywould be reported below the current liabilities. As long-term liabilities come due andare to be paid within one year, they are reported as current liabilities. If they are to berenewed rather than paid, they would continue to be reported as long term. When anasset is pledged as security for a liability, the obligation may be called a mortgage notepayable or a mortgage payable.

Owner’s Equity The owner’s right to the assets of the business is presented on thebalance sheet below the liabilities section. The owner’s equity is added to the total lia-bilities, and this total must be equal to the total assets.

Example Exercise 4-4 Classified Balance Sheet The following accounts appear in an adjusted trial balance of Hindsight Consulting. Indicate whethereach account would be reported in the (a) current asset; (b) property, plant, and equipment; (c) currentliability; (d) long-term liability; or (e) owner’s equity section of the December 31, 2009, balance sheet ofHindsight Consulting.

1. Jason Corbin, Capital 5. Cash2. Notes Receivable (due in 6 months) 6. Unearned Rent (3 months)3. Notes Payable (due in 2011) 7. Accumulated Depreciation—Equipment4. Land 8. Accounts Payable

2

(continued)

Two common classes of assets arecurrent assets and property, plant,and equipment.

Two common classes of liabilitiesare current liabilities and long-termliabilities.

150 Chapter 4 Completing the Accounting Cycle

Closing EntriesAs discussed in Chapter 3, the adjusting entries are recorded in the journal at the endof the accounting period. For NetSolutions, the adjusting entries are shown in Exhibit 7of Chapter 3.

After the adjusting entries are posted to NetSolutions’ ledger, shown in Exhibit 6(on pages 154–155), the ledger agrees with the data reported on the financial statements.

The balances of the accounts reported on the balance sheet are carried forward fromyear to year. Because they are relatively permanent, these accounts are called permanent ac-counts or real accounts. For example, Cash, Accounts Receivable, Equipment, AccumulatedDepreciation, Accounts Payable, and Owner’s Capital are all permanent accounts.

The balances of the accounts reported on the income statement are not carried for-ward from year to year. Also, the balance of the owner’s drawing account, which is re-ported on the statement of owner’s equity, is not carried forward. Because these ac-counts report amounts for only one period, they are called temporary accounts ornominal accounts. Temporary accounts are not carried forward because they relateonly to one period. For example, the Fees Earned of $16,840 and Wages Expense of$4,525 for NetSolutions shown in Exhibit 2 are for the two months ending December

31, 2009, and should not be carried forward to 2010.At the beginning of the next period, temporary accounts should

have zero balances. To achieve this, temporary account balances are transferred to permanent accounts at the end of the accountingperiod. The entries that transfer these balances are called closingentries. The transfer process is called the closing process and issometimes referred to as closing the books.

Follow My Example 4-41. Owner’s equity 5. Current asset2. Current asset 6. Current liability3. Long-term liability 7. Property, plant, and equipment4. Property, plant, and equipment 8. Current liability

For Practice: PE 4-4A, PE 4-4B

INTERNATIONAL DIFFERENCES

Financial statements prepared under accounting practicesin other countries often differ from those prepared undergenerally accepted accounting principles in the UnitedStates. This is to be expected, since cultures and marketstructures differ from country to country.

To illustrate, BMW Group prepares its financial state-ments under International Financial Reporting Standards asadopted by the European Union. In doing so, BMW’s bal-ance sheet reports fixed assets first, followed by current as-sets. It also reports owner’s equity before the liabilities. Incontrast, balance sheets prepared under U.S. accountingprinciples report current assets followed by fixed assets and

current liabilities followed by long-term liabilities and owner’sequity. The U.S. form of balance sheet is organized to em-phasize creditor interpretation and analysis. For example,current assets and current liabilities are presented first tofacilitate their interpretation and analysis by creditors.Likewise, to emphasize their importance, liabilities are re-ported before owner’s equity.

Regardless of these differences, the basic principlesunderlying the accounting equation and the double-entryaccounting system are the same in Germany and theUnited States. Even though differences in recording andreporting exist, the accounting equation holds true: thetotal assets still equal the total liabilities and owner’sequity.

Prepare clos-

ing entries.

3

Closing entries transfer the bal-ances of temporary accounts to the owner’s capital account.

Chapter 4 Completing the Accounting Cycle 151

The closing process involves the following four steps:

1. Revenue account balances are transferred to an account called Income Summary.

2. Expense account balances are transferred to an account called Income Summary.

3. The balance of Income Summary (net income or net loss) is transferred to theowner’s capital account.

4. The balance of the owner’s drawing account is transferred to the owner’s capitalaccount.

Exhibit 3 diagrams the closing process.

Revenuesare transferred toIncome Summary

SUMMARY INCOME

Net Income or Net Loss is transferred to Owner’s Capital

Drawings are transferred to Owner’s Capital

Owner's Capital

...........

......

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ......

..........................

Expenses are transferred

to Income Summary

Exhibit 3

The ClosingProcess

Income Summary is a temporary account that is only used dur-ing the closing process. At the beginning of the closing process,Income Summary has no balance. During the closing process,Income Summary will be debited and credited for variousamounts. At the end of the closing process, Income Summary willagain have no balance. Because Income Summary has the effect ofclearing the revenue and expense accounts of their balances, it is

sometimes called a clearing account. Other titles used for this account include Revenueand Expense Summary, Profit and Loss Summary, and Income and Expense Summary.

The four closing entries required in the closing process are as follows:

1. Debit each revenue account for its balance and credit Income Summary for the totalrevenue.

2. Credit each expense account for its balance and debit Income Summary for the totalexpenses.

3. Debit Income Summary for its balance and credit the owner’s capital account.

4. Debit the owner’s capital account for the balance of the drawing account and creditthe drawing account.

In the case of a net loss, Income Summary will have a debit balance after the firsttwo closing entries. In this case, credit Income Summary for the amount of its balanceand debit the owner’s capital account for the amount of the net loss.

Closing entries are recorded in the journal and are dated as of the last day of theaccounting period. In the journal, closing entries are recorded immediately followingthe adjusting entries. The caption, Closing Entries, is often inserted above the closing en-tries to separate them from the adjusting entries.

The income summary account does not appear on the financialstatements.

152 Chapter 4 Completing the Accounting Cycle

It is possible to close the temporary revenue and expense accounts without usinga clearing account such as Income Summary. In this case, the balances of the revenueand expense accounts are closed directly to the owner’s capital account. This processmay be used in a computerized accounting system. In a manual system, the use of anincome summary account aids in detecting and correcting errors.

Journalizing and Posting Closing EntriesA flowchart of the four closing entries for NetSolutions is shown in Exhibit 4. The bal-ances in the accounts are those shown in the Adjusted Trial Balance columns of theend-of-period spreadsheet shown in Exhibit 1.

Owner’s Equity

Wages Expense

Bal. 4,525 4,525

Rent Expense

Bal. 1,600 1,600

Depreciation Expense

Bal. 50 50

Utilities Expense

Bal. 985 985

Supplies Expense

Bal. 2,040 2,040

Insurance Expense

Bal. 200 200

Miscellaneous Expense

Bal. 455 455

Chris Clark, Capital

Bal. 4,000 25,000 7,105

Chris Clark, Drawing

Bal. 4,000 4,000

Income Summary

9,855 7,105

16,960

Fees Earned

Bal. 16,840 16,840

Rent Revenue

Bal. 120 120

1. Debit each revenue account for its balance, and credit Income Summary for the total revenue.2. Debit Income Summary for the total expenses, and credit each expense account for its balance.3. Debit Income Summary for the amount of its balance (net income), and credit the capital account. (The accounts debited and credited are reversed if there is a net loss.)4. Debit the capital account for the balance of the drawing account, and credit the drawing account.

①②

③

④

Exhibit 4

Flowchart of Closing Entries for NetSolutions

The closing entries for NetSolutions are shown in Exhibit 5. The account titles andbalances for the these entries may be obtained from the end-of-period spreadsheet, theadjusted trial balance, the income statement, the statement of owner’s equity,or the ledger.

The closing entries are posted to NetSolutions ledger as shown in Exhibit 6 (pages154–155). Income Summary has been added to NetSolutions’ ledger in Exhibit 6 asaccount number 33. After the closing entries are posted, NetSolutions’ ledger has thefollowing characteristics:

1. The balance of Chris Clark, Capital of $28,105 agrees with the amount reportedon the statement of owner’s equity and the balance sheet.

2. The revenue, expense, and drawing accounts will have zero balances.

As shown in Exhibit 6, the closing entries are normally identified in the ledger as“Closing.” In addition, a line is often inserted in both balance columns after a closingentry is posted. This separates next period’s revenue, expense, and withdrawal trans-actions from those of the current period. Next period’s transactions will be posted di-rectly below the closing entry.

Chapter 4 Completing the Accounting Cycle 153

Journal Page 6

Date DescriptionPost.Ref. Debit Credit

Dec.2009

31

31

31

31

Closing Entries

Fees Earned

Rent Revenue

Income Summary

Income Summary

Wages Expense

Rent Expense

Depreciation Expense

Utilities Expense

Supplies Expense

Insurance Expense

Miscellaneous Expense

Income Summary

Chris Clark, Capital

Chris Clark, Capital

Chris Clark, Drawing

41

42

33

33

51

52

53

54

55

56

59

33

31

31

32

16,960

4,525

1,600

50

985

2,040

200

455

7,105

4,000

16,840

120

9,855

7,105

4,000

Exhibit 5

ClosingEntries forNetSolutions

3Example Exercise 4-5 Closing Entries After the accounts have been adjusted at July 31, the end of the fiscal year, the following balances aretaken from the ledger of Cabriolet Services Co.:

Terry Lambert, Capital $615,850Terry Lambert, Drawing 25,000Fees Earned 380,450Wages Expense 250,000Rent Expense 65,000Supplies Expense 18,250Miscellaneous Expense 6,200

Journalize the four entries required to close the accounts.

Follow My Example 4-5July 31 Fees Earned 380,450

Income Summary 380,450

31 Income Summary 339,450Wages Expense 250,000Rent Expense 65,000Supplies Expense 18,250Miscellaneous Expense 6,200

31 Income Summary 41,000 Terry Lambert, Capital 41,000

31 Terry Lambert, Capital 25,000Terry Lambert, Drawing 25,000

For Practice: PE 4-5A, PE 4-5B

Exhibit 6

Ledger for NetSolutions

1

1

1

1

1

2

2

2

2

2

2

3

3

3

3

3

3

3

4

4

4

25,000

7,500

360

3,100

650

2,870

Account Cash Account No. 11

Date ItemPost.Ref. Debit Credit

Nov. 1

5

18

30

30

30

Dec. 1

1

1

6

11

13

16

20

21

23

27

31

31

31

31

2009

20,000

3,650

950

2,000

2,400

800

180

400

950

900

1,450

1,200

310

225

2,000

25,000

5,000

12,500

8,850

7,900

5,900

3,500

2,700

3,060

2,880

2,480

1,530

4,630

3,730

4,380

2,930

1,730

1,420

1,195

4,065

2,065

Debit Credit

Balance

Ledger

3

3

4

5

1,750

1,120

500

Date ItemPost.Ref. Debit Credit

Dec. 16

21

31

31

2009

650

1,750

1,100

2,220

2,720

Debit Credit

Balance

Account No. 12Account Accounts Receivable

1

1

3

5

1,350

1,450

Date ItemPost.Ref. Debit Credit

Nov. 10

30

23

Dec. 31

2009

800

1,240Adjusting

Adjusting

Adjusting

1,350

550

2,000

760

Debit Credit

Balance

Account No. 14Account Supplies

2

5

2,400

200

Date ItemPost.Ref. Debit Credit

Dec. 1

31

2009

2,400

2,200

Debit Credit

Balance

Account No. 15Account Prepaid Insurance

1 20,000

Date ItemPost.Ref. Debit Credit

Nov. 52009

20,000

Debit Credit

Balance

Account No. 17Account Land

2 1,800

Date ItemPost.Ref. Debit Credit

Dec. 42009

1,800

Debit Credit

Balance

Account No. 18Account Office Equipment

5 50 50

Date ItemPost.Ref. Debit Credit

Dec. 312009

Debit Credit

Balance

Account No. 19

1

1

2

2

3

950

400

900

Date ItemPost.Ref. Debit Credit

Nov. 10

30

Dec. 4

11

20

2009

1,350

1,800

Debit Credit

Balance

1,350

400

2,200

1,800

900

Account No. 21Account Accounts Payable

2

5

360

120

Date ItemPost.Ref. Debit Credit

Dec. 1

31

2009

360

240

Debit Credit

Balance

Account No. 23Account Unearned Rent

5 250

Date ItemPost.Ref. Debit Credit

Dec. 312009

250

Debit Credit

Balance

Account No. 22Account Wages Payable

1

6

6

25,000

7,105

4,000

Date ItemPost.Ref. Debit Credit

Nov. 1

Dec. 31

31

2009

25,000

32,105

28,105

Debit Credit

Balance

Account No. 31Account Chris Clark, Capital

2

4

6

Date ItemPost.Ref. Debit Credit

Nov. 30Dec. 31

31

2009

Debit Credit

Balance

Account No. 32Account Chris Clark, Drawing

2,000

2,000

2,000

4,000

Account Accumulated Depreciation

Adjusting

Adjusting

Adjusting

Closing 4,000

Closing

Closing

— —

154

Chapter 4 Completing the Accounting Cycle 155

Exhibit 6

(continued)

1

5

6

Date ItemPost.Ref. Debit Credit

2009

800

2,040

Debit Credit

Balance

Account No. 55Account Supplies Expense

1

3

4

6

Date ItemPost.Ref. Debit Credit

Nov. 30

Dec. 31

31

31

Nov. 30

Dec. 31

31

2009

Debit Credit

Balance

Account No. 54Account Utilities Expense

450

310

225

450

760

985

1

2

6

Date ItemPost.Ref. Debit Credit

Nov. 30

Dec. 1

31

2009

Debit Credit

Balance

Account No. 52Account Rent Expense

800

800

1,600

800

1,600

5

6

Date ItemPost.Ref. Debit Credit

Dec. 31

31

2009

Debit Credit

Balance

Account No. 42Account Rent Revenue

120

120 120

6

6

6

Date ItemPost.Ref. Debit Credit

Dec. 31

31

31

2009

Debit Credit

Balance

Account No. 33Account Income Summary

9,855

7,105

16,960

7,105

16,960

5

6

Date ItemPost.Ref. Debit Credit

Dec. 31

31

2009

Debit Credit

Balance

Account No. 56Account Insurance Expense

200 200

200

5

6

Date ItemPost.Ref. Debit Credit

Dec. 31

31

2009

Debit Credit

Balance

Account No. 53Account Depreciation Expense

1

3

3

5

6

Date ItemPost.Ref. Debit Credit

Nov. 30

Dec. 13

27

31

31

2009

Debit Credit

Balance

Account No. 51Account Wages Expense

2,125

950

1,200

250

2,125

3,075

4,275

4,525

—

Date ItemPost.Ref. Debit Credit

Nov. 18

Dec. 16

16

31

31

31

31

2009

Debit Credit

Balance

Account No. 41Account Fees Earned

16,840

—

— —

— —

— —

— —

—

Closing

Closing

Closing

—

—

—

—

—

— —

1

3

3

4

4

5

6

7,500

10,600

12,350

15,220

16,340

16,840

7,500

3,100

1,750

2,870

1,120

500Adjusting

Closing

Adjusting

Closing

Adjusting

Closing 4,525

Closing

1

2

6

Date ItemPost.Ref. Debit Credit

Nov. 30

Dec. 6

31

2009

Debit Credit

Balance

Account No. 59Account Miscellaneous Expense

275

180

455

275

455

— —Closing

50 50

50

Adjusting

Closing

985Closing

2,040

800

1,240Adjusting

Closing

Adjusting

Closing

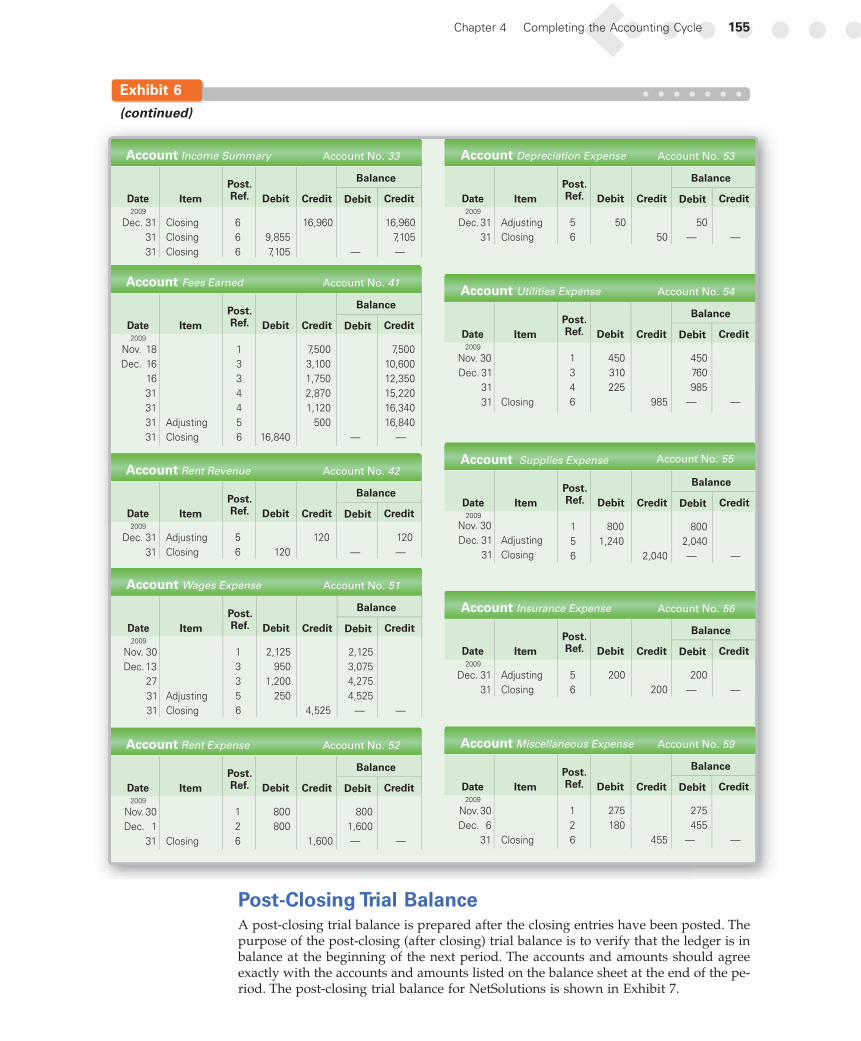

Post-Closing Trial BalanceA post-closing trial balance is prepared after the closing entries have been posted. Thepurpose of the post-closing (after closing) trial balance is to verify that the ledger is inbalance at the beginning of the next period. The accounts and amounts should agreeexactly with the accounts and amounts listed on the balance sheet at the end of the pe-riod. The post-closing trial balance for NetSolutions is shown in Exhibit 7.

156 Chapter 4 Completing the Accounting Cycle

4Example Exercise 4-6 Accounting CycleFrom the following list of steps in the accounting cycle, identify what two steps are missing.

a. Transactions are analyzed and recorded in the journal.

b. Transactions are posted to the ledger.

c. Adjustment data are assembled and analyzed.

d. An optional end-of-period spreadsheet (work sheet) is prepared.

e. Adjusting entries are journalized and posted to the ledger.

f. Financial statements are prepared.

g. Closing entries are journalized and posted to the ledger.

h. A post-closing trial balance is prepared.

50

900

250

240

28,105

29,545

2,065

2,720

760

2,200

20,000

1,800

29,545

Cash

Accounts Receivable

Supplies

Prepaid Insurance

Land

Office Equipment

Accumulated Depreciation

Accounts Payable

Wages Payable

Unearned Rent

Chris Clark, Capital

NetSolutionsPost-Closing Trial Balance

December 31, 2009

DebitBalances

CreditBalances

Exhibit 7

Post-ClosingTrial Balance

Accounting CycleThe accounting process that begins with analyzing and journalizing transactions andends with the post-closing trial balance is called the accounting cycle. The steps in theaccounting cycle are as follows:

1. Transactions are analyzed and recorded in the journal.

2. Transactions are posted to the ledger.

3. An unadjusted trial balance is prepared.

4. Adjustment data are assembled and analyzed.

5. An optional end-of-period spreadsheet (work sheet) is prepared.

6. Adjusting entries are journalized and posted to the ledger.

7. An adjusted trial balance is prepared.

8. Financial statements are prepared.

9. Closing entries are journalized and posted to the ledger.

10. A post-closing trial balance is prepared.2

Exhibit 8 illustrates the accounting cycle in graphic form. It also illustrates how theaccounting cycle begins with the source documents for a transaction and flows throughthe accounting system and into the financial statements.

Describe the

accounting

cycle.

4

2 Some accountants include the journalizing and posting of “reversing entries” as the last step in the accounting cycle.Because reversing entries are not required, we describe and illustrate them in Appendix B at the end of the book.

(continued)

Chapter 4 Completing the Accounting Cycle 157

Exhibit 8

Accounting Cycle

Follow My Example 4-6The following two steps are missing: (1) the preparation of an unadjusted trial balance and (2) the prepa-ration of the adjusted trial balance. The unadjusted trial balance should be prepared after step (b). Theadjusted trial balance should be prepared after step (e).

For Practice: PE 4-6A, PE 4-6B

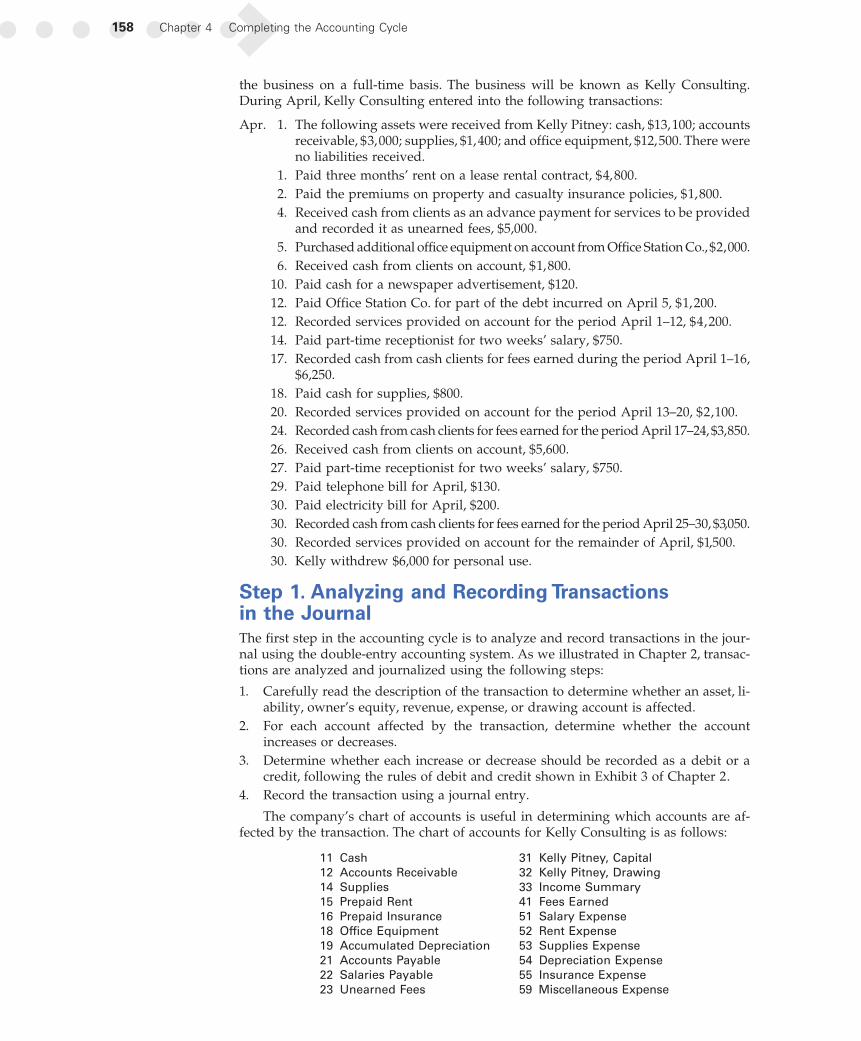

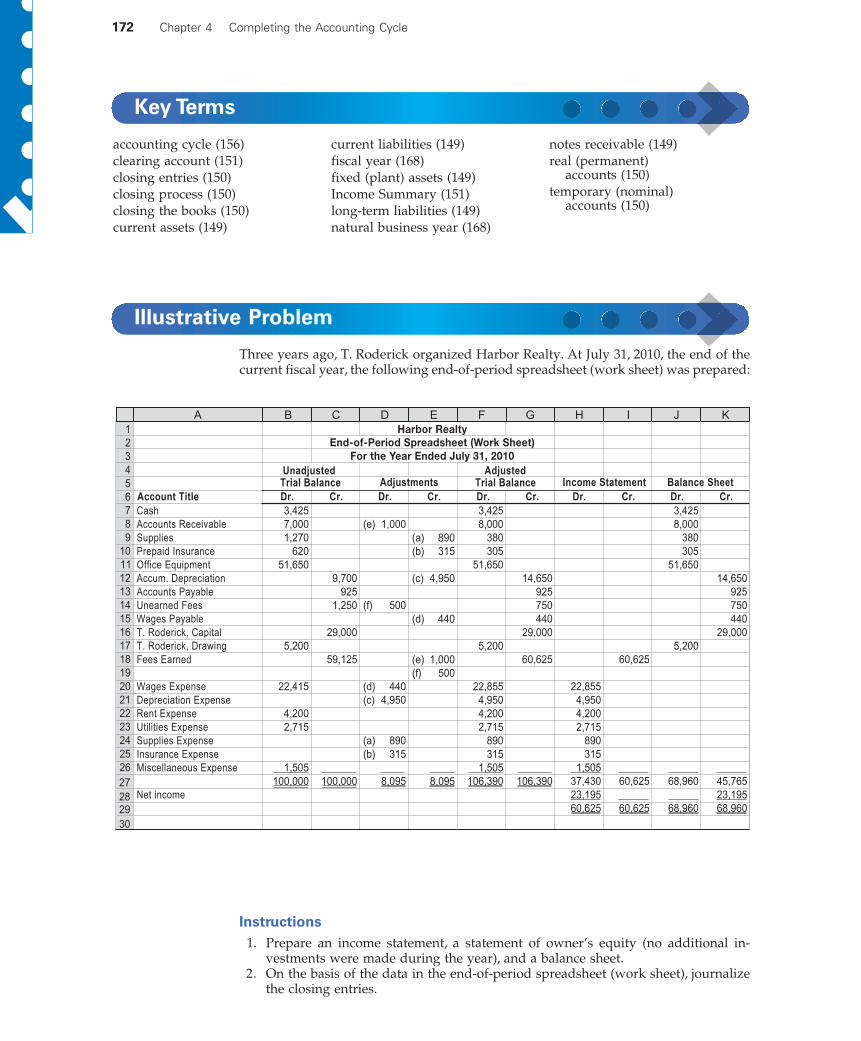

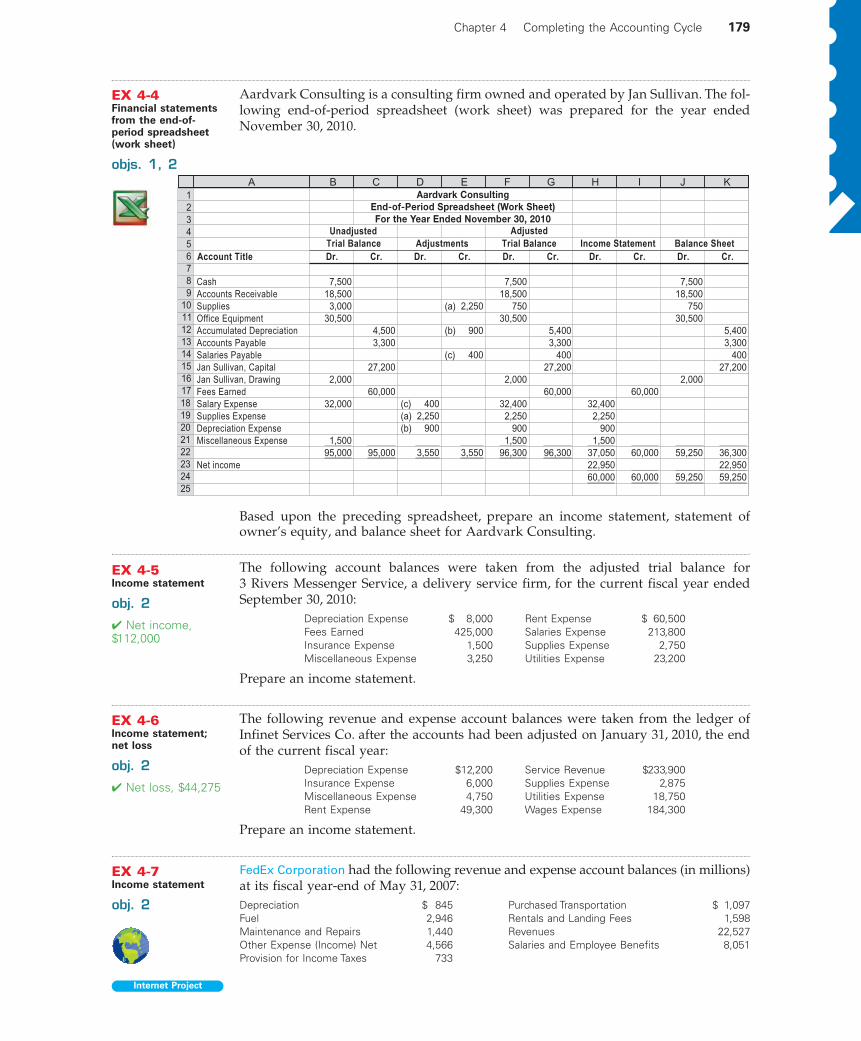

Illustration of the Accounting CycleIn this section, we will illustate the complete accounting cycle for one period. We assumethat for several years Kelly Pitney has operated a part-time consulting business fromher home. As of April 1, 2010, Kelly decided to move to rented quarters and to operate

Illustrate the

accounting

cycle for one period.

5

158 Chapter 4 Completing the Accounting Cycle

the business on a full-time basis. The business will be known as Kelly Consulting.During April, Kelly Consulting entered into the following transactions:

Apr. 1. The following assets were received from Kelly Pitney: cash, $13,100; accountsreceivable, $3,000; supplies, $1,400; and office equipment, $12,500. There wereno liabilities received.

1. Paid three months’ rent on a lease rental contract, $4,800.

2. Paid the premiums on property and casualty insurance policies, $1,800.

4. Received cash from clients as an advance payment for services to be providedand recorded it as unearned fees, $5,000.

5. Purchased additional office equipment on account from Office Station Co.,$2,000.

6. Received cash from clients on account, $1,800.

10. Paid cash for a newspaper advertisement, $120.

12. Paid Office Station Co. for part of the debt incurred on April 5, $1,200.

12. Recorded services provided on account for the period April 1–12, $4,200.

14. Paid part-time receptionist for two weeks’ salary, $750.

17. Recorded cash from cash clients for fees earned during the period April 1–16,$6,250.

18. Paid cash for supplies, $800.

20. Recorded services provided on account for the period April 13–20, $2,100.

24. Recorded cash from cash clients for fees earned for the period April 17–24,$3,850.

26. Received cash from clients on account, $5,600.

27. Paid part-time receptionist for two weeks’ salary, $750.

29. Paid telephone bill for April, $130.

30. Paid electricity bill for April, $200.

30. Recorded cash from cash clients for fees earned for the period April 25–30, $3,050.

30. Recorded services provided on account for the remainder of April, $1,500.

30. Kelly withdrew $6,000 for personal use.

Step 1. Analyzing and Recording Transactions in the JournalThe first step in the accounting cycle is to analyze and record transactions in the jour-nal using the double-entry accounting system. As we illustrated in Chapter 2, transac-tions are analyzed and journalized using the following steps:

1. Carefully read the description of the transaction to determine whether an asset, li-ability, owner’s equity, revenue, expense, or drawing account is affected.

2. For each account affected by the transaction, determine whether the accountincreases or decreases.

3. Determine whether each increase or decrease should be recorded as a debit or acredit, following the rules of debit and credit shown in Exhibit 3 of Chapter 2.

4. Record the transaction using a journal entry.

The company’s chart of accounts is useful in determining which accounts are af-fected by the transaction. The chart of accounts for Kelly Consulting is as follows:

11 Cash 31 Kelly Pitney, Capital12 Accounts Receivable 32 Kelly Pitney, Drawing14 Supplies 33 Income Summary15 Prepaid Rent 41 Fees Earned16 Prepaid Insurance 51 Salary Expense18 Office Equipment 52 Rent Expense19 Accumulated Depreciation 53 Supplies Expense21 Accounts Payable 54 Depreciation Expense22 Salaries Payable 55 Insurance Expense23 Unearned Fees 59 Miscellaneous Expense

Chapter 4 Completing the Accounting Cycle 159

After analyzing each of Kelly Consulting’s transactions for April, the journal en-tries are recorded as shown in Exhibit 9.

Step 2. Posting Transactions to the LedgerPeriodically, the transactions recorded in the journal are posted to the accounts in theledger. The debits and credits for each journal entry are posted to the accounts in theorder in which they occur in the journal. As we illustrated in Chapters 2 and 3, jour-nal entries are posted to the accounts using the following four steps.

1. The date is entered in the Date column of the account.

2. The amount is entered into the Debit or Credit column of the account.

3. The journal page number is entered in the Posting Reference column.

4. The account number is entered in the Posting Reference (Post. Ref.) column in thejournal.

The journal entries for Kelly Consulting have been posted to the ledger shown inExhibit 17 on pages 166–168.

Page 1

Date DescriptionPost.Ref. Debit Credit

Apr.2010

Journal

30,000

4,800

1,800

5,000

2,000

1,800

120

1,200

4,200

750

13,100

3,000

1,400

12,500

4,800

1,800

5,000

2,000

1,800

120

1,200

4,200

750

Cash

Accounts Receivable

Supplies

Office Equipment

Kelly Pitney, Capital

Prepaid Rent

Cash

Prepaid Insurance

Cash

Cash

Unearned Fees

Office Equipment

Accounts Payable

Cash

Accounts Receivable

Miscellaneous Expense

Cash

Accounts Payable

Cash

Accounts Receivable

Fees Earned

Salary Expense

Cash

1

1

2

4

5

6

10

12

12

14

11

12

14

18

31

15

11

16

11

11

23

18

21

11

12

59

11

21

11

12

41

51

11

Exhibit 9

Journal Entriesfor April, KellyConsulting

(continued)

160 Chapter 4 Completing the Accounting Cycle

Step 3. Preparing an Unadjusted Trial BalanceAn unadjusted trial balance is prepared to determine whether any errors have beenmade in posting the debits and credits to the ledger. The unadjusted trial balance doesnot provide complete proof of the accuracy of the ledger. It indicates only that the deb-its and the credits are equal. This proof is of value, however, because errors often af-fect the equality of debits and credits. If the two totals of a trial balance are not equal,an error has occurred that must be discovered and corrected.

The unadjusted trial balance for Kelly Consulting is shown in Exhibit 10. Theunadjusted account balances shown in Exhibit 10 were taken from Kelly Consulting’sledger shown in Exhibit 17, on pages 166–168, before any adjusting entries were recorded.

Step 4. Assembling and Analyzing Adjustment DataBefore the financial statements can be prepared, the accounts must be updated. Thefour types of accounts that normally require adjustment include prepaid expenses, un-earned revenue, accrued revenue, and accrued expenses. In addition, depreciation

Page 2

Date DescriptionPost.Ref. Debit Credit

Apr.2010

Journal

6,250

800

2,100

3,850

5,600

750

130

200

3,050

1,500

6,000

6,250

800

2,100

3,850

5,600

750

130

200

3,050

1,500

6,000

Cash

Fees Earned

Supplies

Cash

Accounts Receivable

Fees Earned

Cash

Fees Earned

Cash

Accounts Receivable

Salary Expense

Cash

Miscellaneous Expense

Cash

Miscellaneous Expense

Cash

Cash

Fees Earned

Accounts Receivable

Fees Earned

Kelly Pitney, Drawing

Cash

17

18

20

24

26

27

29

30

30

30

30

11

41

14

11

12

41

11

41

11

12

51

11

59

11

59

11

11

41

12

41

32

11

Exhibit 9

Journal Entriesfor April, KellyConsulting(continued)

Chapter 4 Completing the Accounting Cycle 161

expense must be recorded for fixed assets other than land. The following data have beenassembled on April 30, 2010, for analysis of possible adjustments for Kelly Consulting:

a. Insurance expired during April is $300.

b. Supplies on hand on April 30 are $1,350.

c. Depreciation of office equipment for April is $330.

d. Accrued receptionist salary on April 30 is $120.

e. Rent expired during April is $1,600.

f. Unearned fees on April 30 are $2,500.

Step 5. Preparing an Optional End-of-PeriodSpreadsheet (Work Sheet)Although an end-of-period spreadsheet (work sheet) is not required, it is useful in show-ing the flow of accounting information from the unadjusted trial balance to the ad-justed trial balance and financial statements. In addition, an end-of-period spreadsheetis useful in analyzing the impact of proposed adjustments on the financial statements.The end-of-period spreadsheet for Kelly Consulting is shown in Exhibit 11.

Step 6. Journalizing and Posting Adjusting EntriesBased on the adjustment data shown in step 4, adjusting entries for Kelly Consultingare prepared as shown in Exhibit 12. Each adjusting entry affects at least one incomestatement account and one balance sheet account. Explanations for each adjustmentincluding any computations are normally included with each adjusting entry.

Kelly ConsultingUnadjusted Trial Balance

April 30, 2010

0

800

0

5,000

30,000

20,950

56,750

22,100

3,400

2,200

4,800

1,800

14,500

6,000

1,500

0

0

0

0

450

56,750

Cash

Accounts Receivable

Supplies

Prepaid Rent

Prepaid Insurance

Office Equipment

Accumulated Depreciation

Accounts Payable

Salaries Payable

Unearned Fees

Kelly Pitney, Capital

Kelly Pitney, Drawing

Fees Earned

Salary Expense

Rent Expense

Supplies Expense

Depreciation Expense

Insurance Expense

Miscellaneous Expense

DebitBalances

CreditBalances

Exhibit 10

Unadjusted TrialBalance, KellyConsulting

162 Chapter 4 Completing the Accounting Cycle

CashAccounts ReceivableSuppliesPrepaid RentPrepaid InsuranceOffice EquipmentAccum. DepreciationAccounts PayableSalaries PayableUnearned FeesKelly Pitney, CapitalKelly Pitney, DrawingFees EarnedSalary ExpenseRent ExpenseSupplies ExpenseDepreciation ExpenseInsurance ExpenseMiscellaneous Expense

Net income

123456789

1011121314151617181920212223242526272829

Kelly ConsultingEnd-of-Period Spreadsheet (Work Sheet)

For the Month Ended April 30, 2010Unadjusted

Income StatementAdjustmentsTrial Balance Trial BalanceAccount Title Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.

Balance SheetAdjusted

22,1003,4002,2004,8001,800

14,500

6,000

1,500

45056,750

800

5,00030,000

20,950

56,750

(f) 2,500

(d) 120(e) 1,600(b) 850(c) 330(a) 300

5,700

(b) 850(e) 1,600(a) 300

(c) 330

(d) 120

(f) 2,500

5,700

22,1003,4001,3503,2001,500

14,500

6,000

1,6201,600

850330300450

57,200

330800120

2,50030,000

23,450

57,200

1,6201,600

850330300450

5,15018,30023,450

23,450

23,450

23,450

22,1003,4001,3503,2001,500

14,500

6,000

52,050

52,050

330800120

2,50030,000

33,75018,30052,050

A B C D E F G H I J K

Exhibit 11

End-of-Period Spreadsheet (Work Sheet)

Page 3

Date

Adjusting Entries

Post.Ref. Debit Credit

Apr.2010

30

30

30

30

30

30

300

850

330

120

1,600

2,500

300

850

330

120

1,600

2,500

Insurance Expense

Prepaid Insurance

Expired Insurance.

Supplies Expense

Supplies

Supplies used ($2,200 – $1,350).

Depreciation Expense

Accumulated Depreciation

Depreciation of office equipment.

Salary Expense

Salaries Payable

Accrued salary.

Rent Expense

Prepaid Rent

Rent expired during April.

Unearned Fees

Fees Earned

Fees earned ($5,000 – $2,500).

55

16

53

14

54

19

51

22

52

15

23

41

Journal

Exhibit 12

AdjustingEntries, KellyConsulting

Chapter 4 Completing the Accounting Cycle 163

Each of the adjusting entries shown in Exhibit 12 is posted to Kelly Consulting’sledger shown in Exhibit 17 on pages 166–168. The adjusting entries are identified in theledger as “Adjusting.”

Step 7. Preparing an Adjusted Trial BalanceAfter the adjustments have been journalized and posted, an adjusted trial balance isprepared to verify the equality of the total of the debit and credit balances. This is thelast step before preparing the financial statements. If the adjusted trial balance does notbalance, an error has occurred and must be found and corrected. The adjusted trial bal-ance for Kelly Consulting as of April 30, 2010, is shown in Exhibit 13.

Step 8. Preparing the Financial StatementsThe most important outcome of the accounting cycle is the financial statements. Theincome statement is prepared first, followed by the statement of owner’s equity andthen the balance sheet. The statements can be prepared directly from the adjusted trialbalance, the end-of-period spreadsheet, or the ledger. The net income or net loss shownon the income statement is reported on the statement of owner’s equity along with anyadditional investments by the owner and any withdrawals. The ending owner’s capital is reported on the balance sheet and is added with total liabilities to equal totalassets.

The financial statements for Kelly Consulting are shown in Exhibit 14. KellyConsulting earned net income of $18,300 for April. As of April 30, 2010, KellyConsulting has total assets of $45,720, total liabilities of $3,420, and total owner’s equityof $42,300.

Kelly ConsultingAdjusted Trial Balance

April 30, 2010

Cash

Accounts Receivable

Supplies

Prepaid Rent

Prepaid Insurance

Office Equipment

Accumulated Depreciation

Accounts Payable

Salaries Payable

Unearned Fees

Kelly Pitney, Capital

Kelly Pitney, Drawing

Fees Earned

Salary Expense

Rent Expense

Supplies Expense

Depreciation Expense

Insurance Expense

Miscellaneous Expense

22,100

3,400

1,350

3,200

1,500

14,500

6,000

1,620

1,600

850

330

300

450

57,200

330

800

120

2,500

30,000

23,450

57,200

CreditBalances

DebitBalances

Exhibit 13

Adjusted TrialBalance, KellyConsulting

164 Chapter 4 Completing the Accounting Cycle

Fees earned

Expenses:

Salary expense

Rent expense

Supplies expense

Depreciation expense

Insurance expense

Miscellaneous expense

Total expenses

Net income

$1,620

1,600

850

330

300

450

$23,450

5,150

$18,300

Kelly ConsultingIncome Statement

For the Month Ended April 30, 2010

Kelly ConsultingStatement of Owner’s Equity

For the Month Ended April 30, 2010

$ 0

42,300

$42,300

$30,000

18,300

$48,300

6,000

Kelly Pitney, capital, April 1, 2010

Investment during the month

Net income for the month

Less withdrawals

Increase in owner’s equity

Kelly Pitney, capital, April 30, 2010

Kelly ConsultingBalance SheetApril 30, 2010

Current assets:

Cash

Accounts receivable

Supplies

Prepaid rent

Prepaid insurance

Total current assets

Property, plant, and equipment:

Office equipment

Less accumulated depreciation

Total property, plant,

and equipment

Total assets

$31,550

14,170

$45,720

$22,100

3,400

1,350

3,200

1,500

$14,500

330

Current liabilities:

Accounts payable

Salaries payable

Unearned fees

Total liabilities

$ 800

120

2,500

Kelly Pitney, capital

Total liabilities and

owner’s equity

Liabilities

Owner’s Equity

Assets

$ 3,420

42,300

$45,720

Exhibit 14

FinancialStatements,Kelly Consulting

Chapter 4 Completing the Accounting Cycle 165

Step 9. Journalizing and Posting Closing EntriesAs described earlier in this chapter, four closing entries are required at the end of anaccounting period. These four closing entries are as follows:

1. Debit each revenue account for its balance and credit Income Summary for the totalrevenue.

2. Credit each expense account for its balance and debit Income Summary for the totalexpenses.

3. Debit Income Summary for its balance and credit the owner’s capital account.

4. Debit the owner’s capital account for the balance of the drawing account and creditthe drawing account.

The four closing entries for Kelly Consulting are shown in Exhibit 15. The closingentries are posted to Kelly Consulting’s ledger as shown in Exhibit 17 (pages 166–168).After the closing entries are posted, Kelly Consulting’s ledger has the followingcharacteristics:

1. The balance of Kelly Pitney, Capital of $42,300 agrees with the amount reportedon the statement of owner’s equity and the balance sheet.

2. The revenue, expense, and drawing account will have zero balances.

The closing entries are normally identified in the ledger as “Closing.” In addition,a line is often inserted in both balance columns after a closing entry is posted. This sep-arates next period’s revenue, expense, and withdrawal transactions from those of thecurrent period.

Step 10. Preparing a Post-Closing Trial BalanceA post-closing trial balance is prepared after the closing entries have been posted. Thepurpose of the post-closing trial balance is to verify that the ledger is in balance at thebeginning of the next period. The accounts and amounts in the post-closing trial balance

Page 4

Date Description

Closing Entries

Post.Ref. Debit Credit

Apr.2010

Journal

23,450

1,620

1,600

850

330

300

450

18,300

6,000

23,450

5,150

18,300

6,000

Fees Earned

Income Summary

Income Summary

Salary Expense

Rent Expense

Supplies Expense

Depreciation Expense

Insurance Expense

Miscellaneous Expense

Income Summary

Kelly Pitney, Capital

Kelly Pitney, Capital

Kelly Pitney, Drawing

30

30

30

30

41

33

33

51

52

53

54

55

59

33

31

31

32

Exhibit 15

ClosingEntries, KellyConsulting

166 Chapter 4 Completing the Accounting Cycle

Kelly ConsultingPost-Closing Trial Balance

April 30, 2010

330

800

120

2,500

42,300

46,050

22,100

3,400

1,350

3,200

1,500

14,500

46,050

Cash

Accounts Receivable

Supplies

Prepaid Rent

Prepaid Insurance

Office Equipment

Accumulated Depreciation

Accounts Payable

Salaries Payable

Unearned Fees

Kelly Pitney, Capital

DebitBalances

CreditBalances

Exhibit 16

Post-ClosingTrial Balance,Kelly Consulting

Exhibit 17

Ledger, Kelly Consulting

1

1

1

1

1

1

1

1

2

2

2

2

2

2

2

2

2

Account Cash Account No. 11

Date ItemPost.Ref. Debit Credit

Apr. 1

1

2

4

6

10

12

14

17

18

24

26

27

29

30

30

30

2010

Debit Credit

Balance

Ledger

Date ItemPost.Ref. Debit Credit

Apr. 1

6

12

20

26

30

2010

Debit Credit

Balance

Account No. 12Account Accounts Receivable

1

2

3

Date ItemPost.Ref. Debit Credit

Apr. 1

18

30

2010

Adjusting

Debit Credit

Balance

Account No. 14Account Supplies

1

1

1

2

2

2

3,000

1,200

5,400

7,500

1,900

3,400

1,800

5,600

3,000

4,200

2,100

1,500

1,400

2,200

1,350850

1,400

800

13,100

8,300

6,500

11,500

13,300

13,180

11,980

11,230

17,480

16,680

20,530

26,130

25,380

25,250

25,050

28,100

22,100

4,800

1,800

120

1,200

750

800

750

130

200

6,000

13,100

5,000

1,800

6,250

3,850

5,600

3,050

should agree exactly with the accounts and amounts listed on the balance sheet at theend of the period.

The post-closing trial balance for Kelly Consulting is shown in Exhibit 16. The bal-ances shown in the post-closing trial balance are taken from the ending balances in theledger shown in Exhibit 17. These balances agree with the amounts shown on KellyConsulting’s balance sheet in Exhibit 14.

Chapter 4 Completing the Accounting Cycle 167

Exhibit 17

Ledger, Kelly Consulting (continued)

Adjusting1

3

4,800

1,600

Date ItemPost.Ref. Debit Credit

Apr. 1

30

2010

Debit Credit

Balance

Account No. 15Account Prepaid Rent

4,800

3,200

1

3

5,000

2,500

Date ItemPost.Ref. Debit Credit

Apr. 4

30

2010

Debit Credit

Balance

Account No. 23Account Unearned Fees

Adjusting

5,000

2,500

1

4

4

30,000

18,300

6,000

Date ItemPost.Ref. Debit Credit

Apr. 1

30

30

2010

Debit Credit

Balance

Account No. 31Account Kelly Pitney, Capital

2

4

Date ItemPost.Ref. Debit Credit

Apr. 3030

2010

Debit Credit

Balance

Account No. 32Account Kelly Pitney, Drawing

Closing 6,000

Closing

Closing

— —

30,000

48,300

42,300

6,0006,000

3 330 330

Date ItemPost.Ref. Debit Credit

Apr. 302010

Debit Credit

Balance

Account No. 19Account Accumulated Depreciation

Adjusting

1

1

Date ItemPost.Ref. Debit Credit

Apr. 1

5

2010

Debit Credit

Balance

Account No. 18Account Office Equipment

12,500

14,500

12,500

2,000

1

1

Date ItemPost.Ref. Debit Credit

Apr. 5

12

2010

Debit Credit

Balance

Account No. 21Account Accounts Payable

2,000

800

2,000

1,200

3 120

Date ItemPost.Ref. Debit Credit

Apr. 302010

120

Debit Credit

Balance

Account No. 22Account Salaries Payable

Adjusting

Adjusting1

3

1,800

300

Date ItemPost.Ref. Debit Credit

Apr. 2

30

2010

Debit Credit

Balance

Account No. 16Account Prepaid Insurance

1,800

1,500

4

4

4

Date ItemPost.Ref. Debit Credit

Apr. 30

30

30

2010

Debit Credit

Balance

Account No. 33Account Income Summary

23,450

Date ItemPost.Ref. Debit Credit

Apr. 14

27

30

30

2010

Debit Credit

Balance

Account No. 51Account Salary Expense

Date ItemPost.Ref. Debit Credit

Apr. 12

17

20

24

30

30

30

30

2010

Debit Credit

Balance

Account No. 41Account Fees Earned

—

Closing

Closing

Closing

—

—

Adjusting

Closing

Adjusting

Closing 1,620

Date ItemPost.Ref. Debit Credit

Apr. 30

30

2010

Debit Credit

Balance

Account No. 52Account Rent Expense

1,600 — —

Adjusting

Closing

3

4

1,600 1,600

23,450

18,300

—

5,150

18,300

1

2

2

2

2

2

3

4

4,200

10,450

12,550

16,400

19,450

20,950

23,450

— 23,450

4,200

6,250

2,100

3,850

3,050

1,500

2,500

1

2

3

4

750

1,500

1,620

—

750

750

120

(continued)

168 Chapter 4 Completing the Accounting Cycle

Because companies with fiscal years often have highly seasonaloperations, investors and others should be careful in interpretingpartial-year reports for such companies. That is, you should expectthe results of operations for these companies to vary significantlythroughout the fiscal year.

The financial history of a business may be shown by a seriesof balance sheets and income statements for several fiscal years. Ifthe life of a business is expressed by a line moving from left toright, the series of balance sheets and income statements may begraphed as follows:

Source: Accounting Trends & Techniques, 61st edition,2007 (New York: American Institute of Certified PublicAccountants).

Percentage of Companies with Fiscal Years Ending in:

January 5% July 2%February 1 August 2March 3 September 7April 2 October 3May 3 November 2June 7 December 63

Income Statement

for the year ended

Dec. 31, 2008

Balance SheetDec. 31, 2008

Balance SheetDec. 31, 2009

Balance SheetDec. 31, 2010

Income Statement

for the year ended

Dec. 31, 2009

Income Statement

for the year ended

Dec. 31, 20102008Dec.

31

2009Dec.

31

2010Dec.

31

Financial History of a Business

3

4

Date ItemPost.Ref. Debit Credit

Apr. 30

30

2010

Debit Credit

Balance

Account No. 53Account Supplies Expense

— —

850 850

850

Adjusting

Closing

3

4

Date ItemPost.Ref. Debit Credit

Apr. 30

30

2010

Debit Credit

Balance

Account No. 54Account Depreciation Expense

— —

330 330

330

Adjusting

Closing

Date ItemPost.Ref. Debit Credit

Apr. 10

29

30

30

2010

Debit Credit

Balance

Account No. 59Account Miscellaneous Expense

450 —Closing

3

4

Date ItemPost.Ref. Debit Credit

Apr. 30

30

2010

Debit Credit

Balance

Account No. 55Account Insurance Expense

— —

300 300

300

Adjusting

Closing

1

2

2

4

120

250

450

—

120

130

200

Fiscal YearThe annual accounting period adopted by a business is known as its fiscal year. Fiscalyears begin with the first day of the month selected and end on the last day of thefollowing twelfth month. The period most commonly used is the calendar year. Otherperiods are not unusual, especially for businesses organized as corporations. For ex-ample, a corporation may adopt a fiscal year that ends when business activities havereached the lowest point in its annual operating cycle. Such a fiscal year is called thenatural business year. At the low point in its operating cycle, a business has more timeto analyze the results of operations and to prepare financial statements.

Explain what

is meant by

the fiscal year and the

natural business year.

6

Exhibit 17

Ledger, Kelly Consulting (concluded)

Chapter 4 Completing the Accounting Cycle 168A

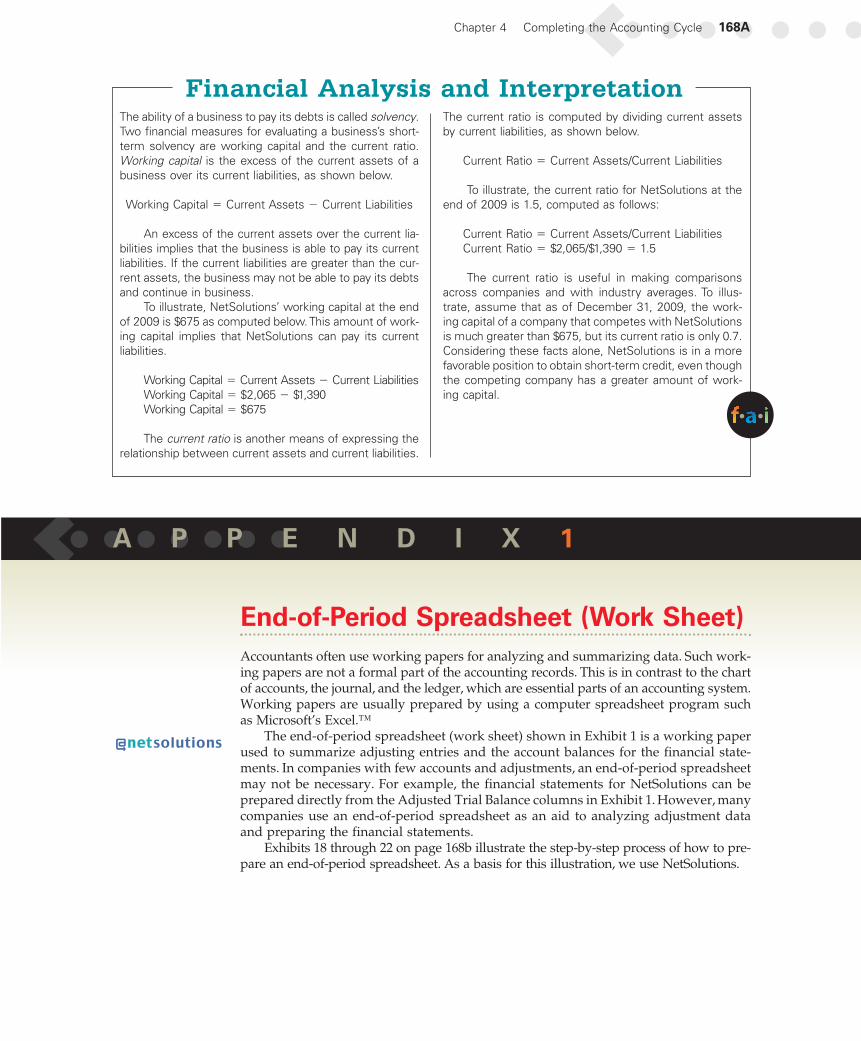

A P P E N D I X 1

End-of-Period Spreadsheet (Work Sheet)Accountants often use working papers for analyzing and summarizing data. Such work-ing papers are not a formal part of the accounting records. This is in contrast to the chartof accounts, the journal, and the ledger, which are essential parts of an accounting system.Working papers are usually prepared by using a computer spreadsheet program suchas Microsoft’s Excel.™

The end-of-period spreadsheet (work sheet) shown in Exhibit 1 is a working paperused to summarize adjusting entries and the account balances for the financial state-ments. In companies with few accounts and adjustments, an end-of-period spreadsheetmay not be necessary. For example, the financial statements for NetSolutions can beprepared directly from the Adjusted Trial Balance columns in Exhibit 1. However, manycompanies use an end-of-period spreadsheet as an aid to analyzing adjustment dataand preparing the financial statements.

Exhibits 18 through 22 on page 168b illustrate the step-by-step process of how to pre-pare an end-of-period spreadsheet. As a basis for this illustration, we use NetSolutions.

The ability of a business to pay its debts is called solvency.Two financial measures for evaluating a business’s short-term solvency are working capital and the current ratio.Working capital is the excess of the current assets of abusiness over its current liabilities, as shown below.

Working Capital � Current Assets � Current Liabilities

An excess of the current assets over the current lia-bilities implies that the business is able to pay its currentliabilities. If the current liabilities are greater than the cur-rent assets, the business may not be able to pay its debtsand continue in business.

To illustrate, NetSolutions’ working capital at the endof 2009 is $675 as computed below. This amount of work-ing capital implies that NetSolutions can pay its currentliabilities.

Working Capital � Current Assets � Current LiabilitiesWorking Capital � $2,065 � $1,390Working Capital � $675

The current ratio is another means of expressing therelationship between current assets and current liabilities.

The current ratio is computed by dividing current assetsby current liabilities, as shown below.

Current Ratio � Current Assets/Current Liabilities

To illustrate, the current ratio for NetSolutions at theend of 2009 is 1.5, computed as follows:

Current Ratio � Current Assets/Current LiabilitiesCurrent Ratio � $2,065/$1,390 � 1.5

The current ratio is useful in making comparisonsacross companies and with industry averages. To illus-trate, assume that as of December 31, 2009, the work-ing capital of a company that competes with NetSolutionsis much greater than $675, but its current ratio is only 0.7.Considering these facts alone, NetSolutions is in a morefavorable position to obtain short-term credit, even thoughthe competing company has a greater amount of work-ing capital.

Financial Analysis and Interpretation

168B Chapter 4 Completing the Accounting Cycle

Cash

Accounts Receivable

Supplies

Prepaid Insurance

Land

Office Equipment

Accumulated Depreciation

Accounts Payable

Wages Payable

Unearned Rent

Chris Clark, Capital

Chris Clark, Drawing

Fees Earned

Rent Revenue

Wages Expense

Rent Expense

Depreciation Expense

Utilities Expense

Supplies Expense

Insurance Expense

Miscellaneous Expense

Insurance Expense

Rent Revenue

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

NetSolutionsEnd-of-Period Spreadsheet (Work Sheet)

For the Two Months Ended December 31, 2009Unadjusted

Income StatementAdjustmentsTrial Balance Trial Balance

Account Title Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr. Dr. Cr.

Balance Sheet

Adjusted

2,065

2,220

2,000

2,400

20,000

1,800

4,000

4,275

1,600

985

800

455

42,600

900

360

25,000

16,340

42,600

B C D E F G H I J KA

26

27

28

29

30

31

32

Exhibit 18

Spreadsheet (Work Sheet) with Unadjusted Trial Balance Entered

The spreadsheet (work sheet)

is used for summarizing the

effects of adjusting entries. It

also aids in preparing financial

statements.

Exhibit 19

Spreadsheet (Work Sheet) with Unadjusted Trial Balance and Adjustments

The adjustments on the spreadsheet

(work sheet) are used in preparing

the adjusting journal entries.

Office EquipmentAccumulated DepreciationAccounts PayableWages PayableUnearned RentChris Clark, CapitalChris Clark, DrawingFees EarnedRent RevenueWages ExpenseRent ExpenseDepreciation ExpenseUtilities ExpenseSupplies ExpenseInsurance Expense

(d) 500

(c) 120

(e) 250

(f) 50

(a) 1,240(b) 200

2,360

(a) 1,240(b) 200

(f) 50

(e) 250

(d) 500(c) 120

2,360

Exhibit 20

Spreadsheet (Work Sheet) with Unadjusted Trial Balance, Adjustments, and Adjusted TrialBalance Entered

The adjusted trial balance amounts are

determined by adding the adjustments to or

subtracting the adjustments from the trial

balance amounts. For example, the Wages

Expense debit of $4,525 is the trial balance