Competitiveness for job creation -Afghanistan … Development model –chain and doughnut Inputs...

100

Competitiveness for job creation - Afghanistan agricultural value chains - Stakeholders’ Meeting MoLSAMD , Kabul, 25 February 2015 Hideki Kagohashi , Senior Coordinator, ILO Office for Afghanistan Khairul Islam, Research Coordinator

Transcript of Competitiveness for job creation -Afghanistan … Development model –chain and doughnut Inputs...

Competitiveness for job creation

- Afghanistan agricultural value chains -

Stakeholders’ Meeting

MoLSAMD, Kabul, 25 February 2015

Hideki Kagohashi, Senior Coordinator, ILO Office for Afghanistan

Khairul Islam, Research Coordinator

Objective of the workshop

• To share key findings, preliminary

conclusions and recommendations with the

national stakeholders (concerned ministries

and representatives of employers and

workers) in order to receive feedback prior

to the finalization of the technical report of

the cross-country agriculture value chain

study.

• After the workshop, some information, conclusions

and recommendations may be modified/added in the

final report.

Why work on value chains?

Improve the overall efficiency of the value chain

by addressing a bottleneck

VC Development model – chain and doughnut

Inputs Production & post-harvest

Transport & delivery

Rules

Support functions

Interventions

Interventions

Why we are concerned?

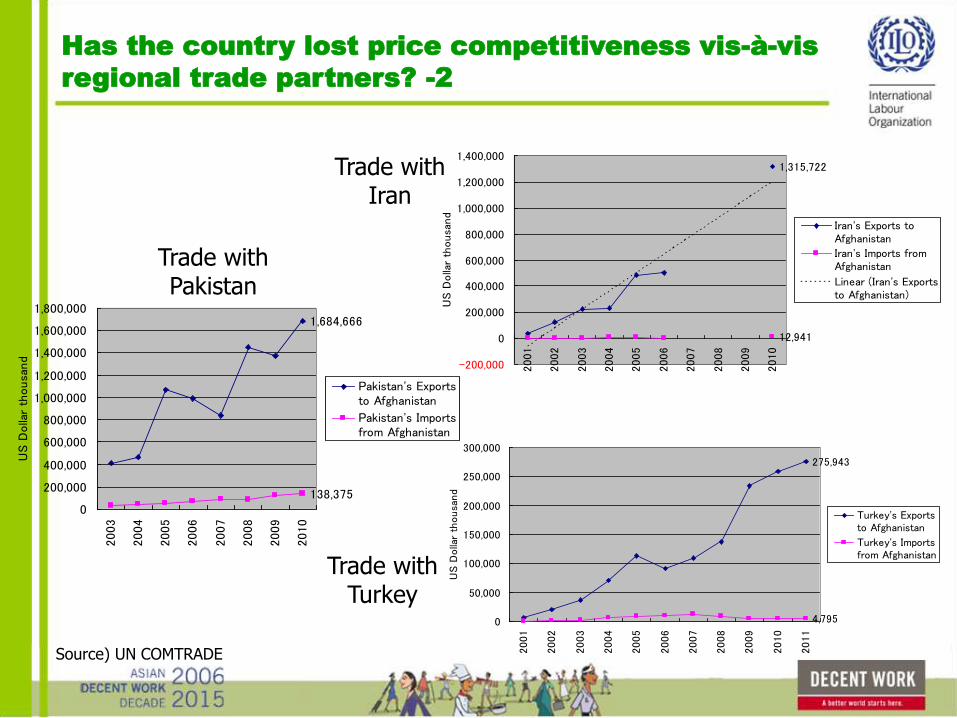

Has the country lost price competitiveness vis-à-vis

regional trade partners? -1

0

1

2

3

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Compared to 2003, the currencies depreicated against USD by

Pakistan India Iran (official) Iran (market) Afghanistan Bangladesh China

IRR - 218%

PKR - 75%

BDT - 33%INR - 31%

Afs – 18%

CHY - (26%)

Has the country lost price competitiveness vis-à-vis

regional trade partners? -2

Source) UN COMTRADE

1,315,722

12,941

-200,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

US D

olla

r th

ousa

nd

Iran's Exports toAfghanistan

Iran's Imports fromAfghanistan

Linear (Iran's Exportsto Afghanistan)

275,943

4,7950

50,000

100,000

150,000

200,000

250,000

300,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

US D

olla

r th

ousa

nd

Turkey's Exportsto Afghanistan

Turkey's Importsfrom Afghanistan

Trade withIran

Trade withPakistan

Trade withTurkey

1,684,666

138,3750

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2003

2004

2005

2006

2007

2008

2009

2010

US D

olla

r th

ousa

nd

Pakistan's Exportsto Afghanistan

Pakistan's Importsfrom Afghanistan

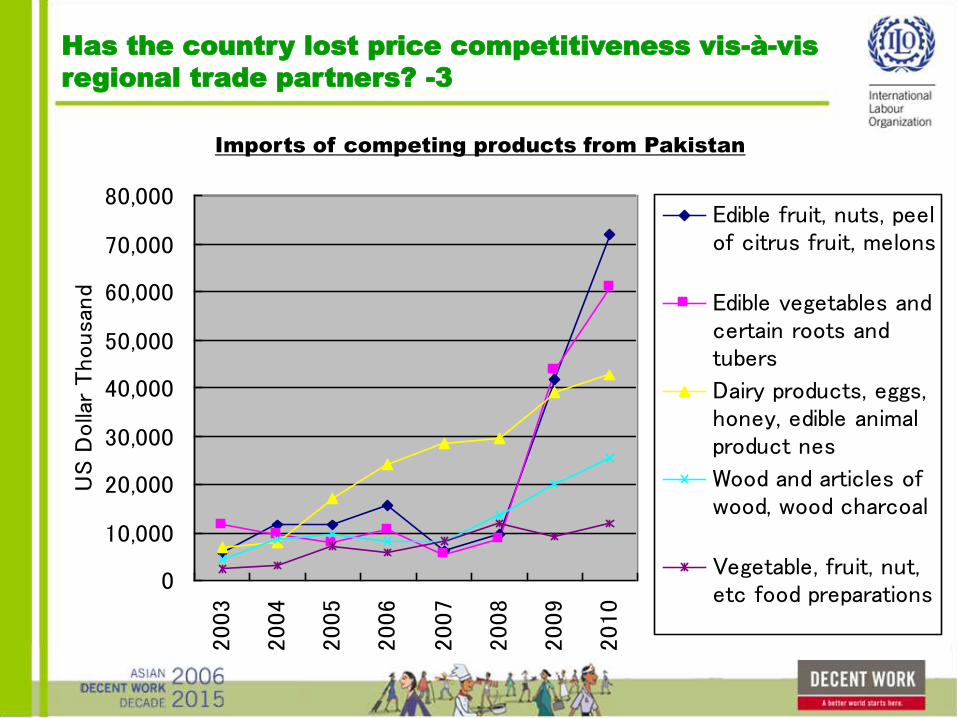

Has the country lost price competitiveness vis-à-vis

regional trade partners? -3

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,0002003

2004

2005

2006

2007

2008

2009

2010

US D

olla

r Thousa

nd

Edible fruit, nuts, peelof citrus fruit, melons

Edible vegetables andcertain roots andtubers

Dairy products, eggs,honey, edible animalproduct nes

Wood and articles ofwood, wood charcoal

Vegetable, fruit, nut,etc food preparations

Imports of competing products from Pakistan

Has the country lost price competitiveness vis-à-vis

regional trade partners? -4

-50,000

0

50,000

100,000

150,000

200,000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

US

Dol

lar

Thou

sand

Carpets and other textile floorcoverings

Salt, sulphur, earth, stone,plaster, lime and cement

Animal,vegetable fats and oils,cleavage products, etc

Edible fruit, nuts, peel of citrusfruit, melons

Wool, animal hair, horsehairyarn and fabric thereof

Stone, plaster, cement,asbestos, mica, etc articles

Edible vegetables and certainroots and tubers

Poly. (Carpets and othertextile floor coverings)

Poly. (Salt, sulphur, earth,stone, plaster, lime andcement)Poly. (Animal,vegetable fatsand oils, cleavage products,etc)Poly. (Edible fruit, nuts, peel ofcitrus fruit, melons)

Poly. (Stone, plaster, cement,asbestos, mica, etc articles)

Poly. (Edible vegetables andcertain roots and tubers)

Imports of competing products from Iran

Key questions

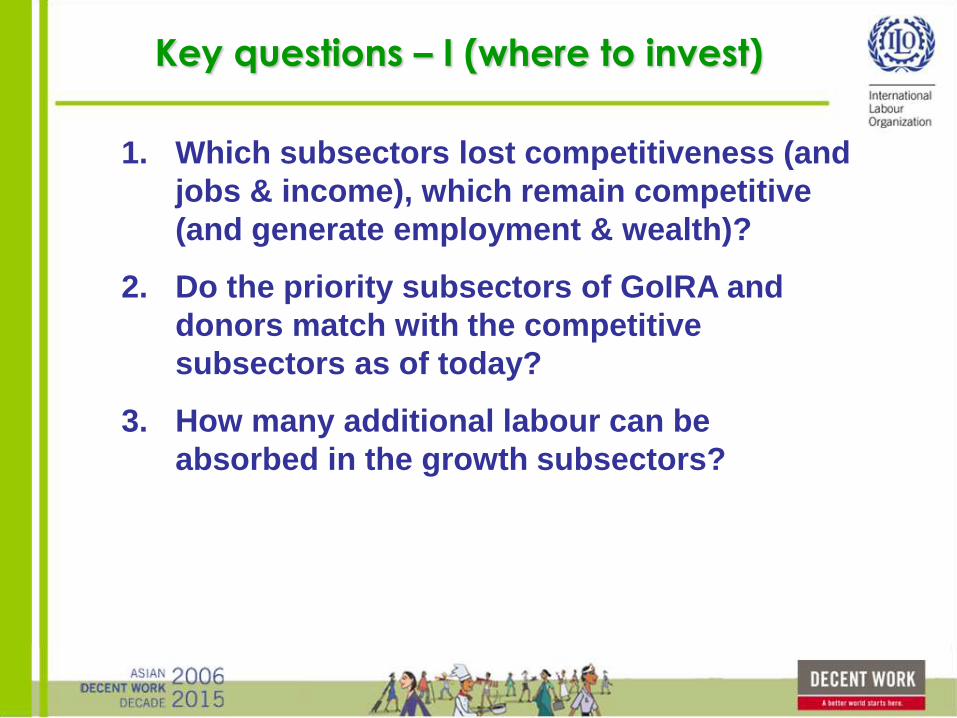

Key questions – I (where to invest)

1. Which subsectors lost competitiveness (and

jobs & income), which remain competitive

(and generate employment & wealth)?

2. Do the priority subsectors of GoIRA and

donors match with the competitive

subsectors as of today?

3. How many additional labour can be

absorbed in the growth subsectors?

Key questions – II (on what to invest)

4. Which factors explain the competitiveness

and employment situation better?

5. Can the competitiveness and employment

situation of the struggling subsectors be

turned around by addressing the key

factors?

6. Do the policies and programmes of GoIRA

and donors address the key factors?

Key questions – III (HHs’ response)

7. Do ag works provide decent income for

HHs’ survival?

8. Where do youth from ag HHs find jobs?

9. Are ag HHs in the growth spiral or in the

poverty trap?

Scope of the research

Benchmark years2007 and 2012

3 countries

Afghanistan, Pakistan and Iran

5 VCsGrapes, wheat, rice,

tomatoes and potatoes

3 major production

clusters in each country

Allmajor cities in

each country

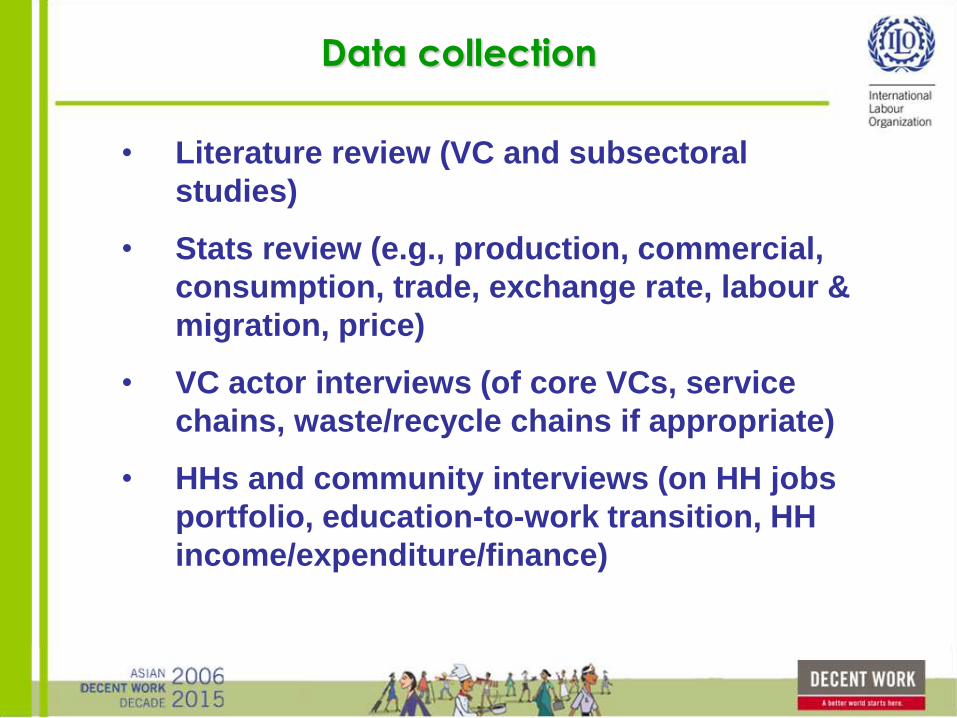

Data collection

• Literature review (VC and subsectoral

studies)

• Stats review (e.g., production, commercial,

consumption, trade, exchange rate, labour &

migration, price)

• VC actor interviews (of core VCs, service

chains, waste/recycle chains if appropriate)

• HHs and community interviews (on HH jobs

portfolio, education-to-work transition, HH

income/expenditure/finance)

Research findings

Major production factors

How is the price change for major factors

of production

•Energy

•Fertilizer

•Labour

Pakistan is gaining P advantage in energy

Changes in price between 2007 and 2012

Country Change in local

currency

Change in USD

Afghanistan App. + 100% App. + 96%

Pakistan App. + 121% App.+ 43%

Iran App. > +400% App. +120%

Pakistan is gaining P advantage in fertilizer

Country Change in local

currency

Change in USD

Afghanistan App. + 100% App. + 96%

Pakistan App. + 109% App. +35%

Iran App. +>500% App. +160%

Changes in price between 2007 and 2012

Pakistan P leader on labour cost

Farm wage rate in 2007 and 2012

Afghanistan (per

day)

Pakistan (per day) Iran (per day)

Year 2007 2012 2007 2012 2007 2012

Local

currency

200 Afs 350 Afs 185 PKR 310 PKR 120.00

IRR

270,000

IRR

USD 4.00 6.87 3.05 3.32 12.82 12.86

Grape

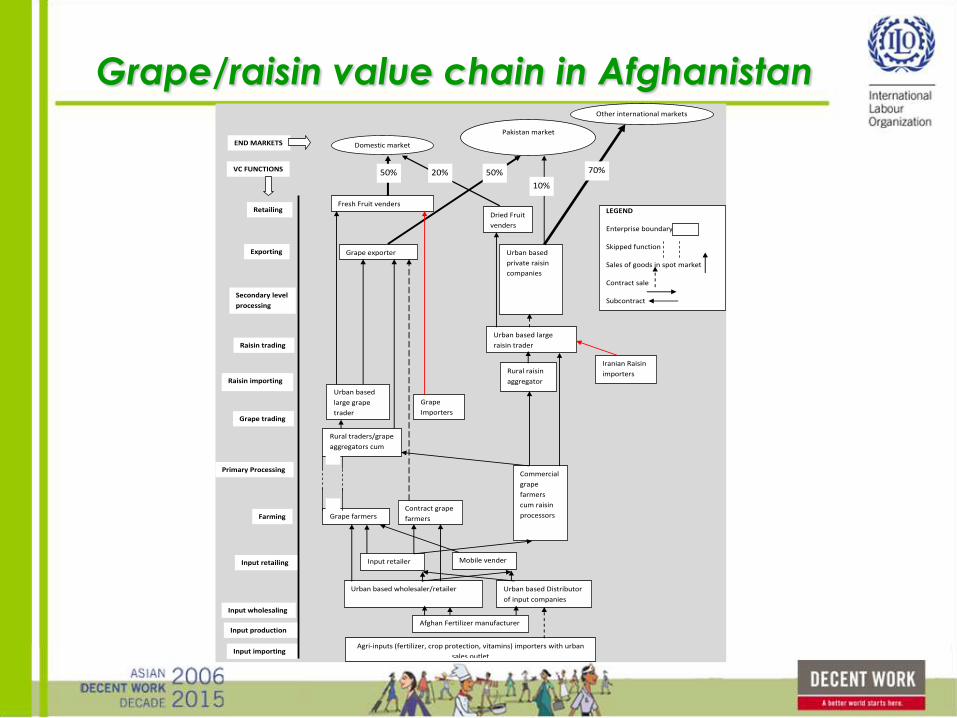

Grape/raisin value chain in Afghanistan

Other international markets

LEGEND Enterprise boundary Skipped function Sales of goods in spot market Contract sale Subcontract

Input importing

Input wholesaling

Input retailing

Farming

Primary Processing

Grape trading

Raisin trading

Secondary level

processing

Retailing

Exporting

Agri-inputs (fertilizer, crop protection, vitamins) importers with urban

sales outlet

Urban based wholesaler/retailer Urban based Distributor

of input companies

Mobile vender

Grape farmers

Commercial

grape

farmers

cum raisin

processors

Rural traders/grape

aggregators cum

Urban based

large grape

trader

Rural raisin

aggregator

Urban based

private raisin

companies

Fresh Fruit venders

Domestic market

Pakistan market

Urban based large

raisin trader

Grape exporter

Contract grape

farmers

Dried Fruit

venders

Raisin importing

Iranian Raisin

importers

Afghan Fertilizer manufacturer Input production

VC FUNCTIONS

END MARKETS

Input retailer

Grape

Importers

50% 50% 20%

10%

70%

Enterprise and jobs

Export

Retail

Wholesale

Import

Production

Inputs Inputs importers cum wholesaler N=100, E=2700, F= 0%

Fertilizer manufacturer N=1, E= 1500, F=10%

Inputs retailer N=750, E=750, F=0%

Grapes farmer

N=67350; E=740850; F = 18% (for processing 50+%)

Grapes importer N=10, E=500, F=0%

Raisin importer N=5, E=50, F=0%

Urban based grape wholesaler N=200, E=4000, F=0%

Rural grape aggregator N=500, E=5000, F=0%

Rural raisin aggregator N= 200, E=2000, F=0%

Urban based raisin wholesaler N=40, E=800, F=0%

Grape retailer N=3,000, E=3000, F=0%

Raisin retailer N=1,200, E=1200, F=0%

Grape exporter N=65, E=3250, F=0%

Raisin exporter N=135, E=11,750, F = 0% (Kandahar) 50+% (Kabul & Mazaar)

N= enterprise

E=employment

F= female

involvement

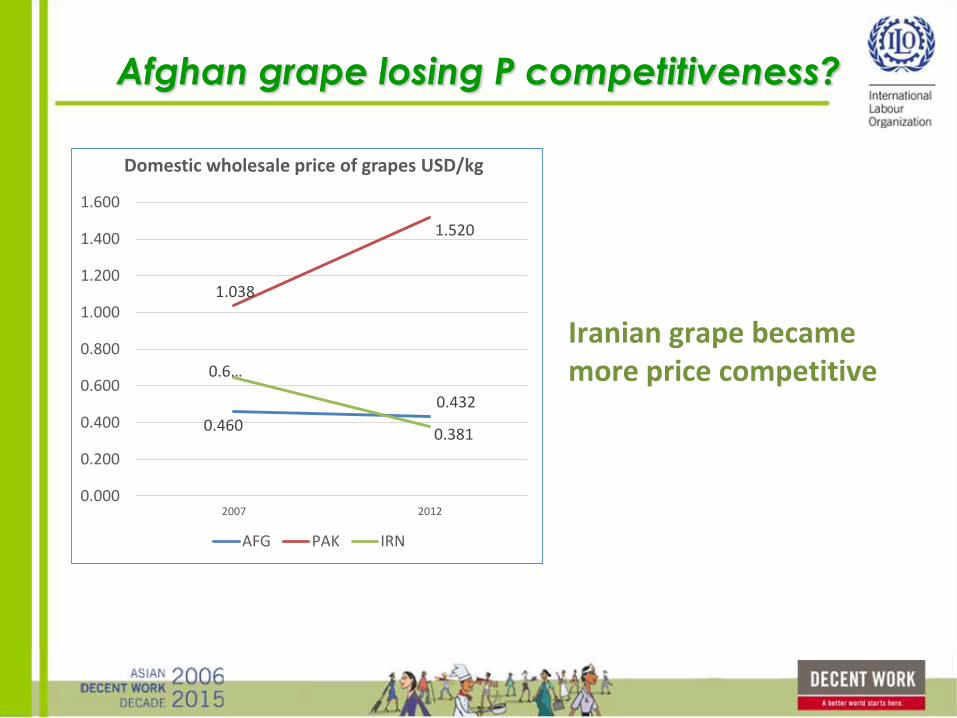

Afghan grape losing P competitiveness?

0.460

0.432

1.038

1.520

0.6…

0.381

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

1.600

2007 2012

Domestic wholesale price of grapes USD/kg

AFG PAK IRN

Iranian grape became more price competitive

Lost in Pakistan but remain competitive in Afghanistan

Afghanistan stagnant, Iran grows fast

Chile 853,000 tons

USA 416,000 tons

Turkey 240 ,000 tonsChina 217,000 tons

Uzbekistan 112 ,000 tons

Iran 10,000 tons

Afghanistan 20,000tons

Pakistan 172 tons-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

-$500 $0 $500 $1,000 $1,500 $2,000 $2,500 $3,000

Global annual growth rate in value 2001-11:

10 %

Global average price in 2011per ton $1,788.44

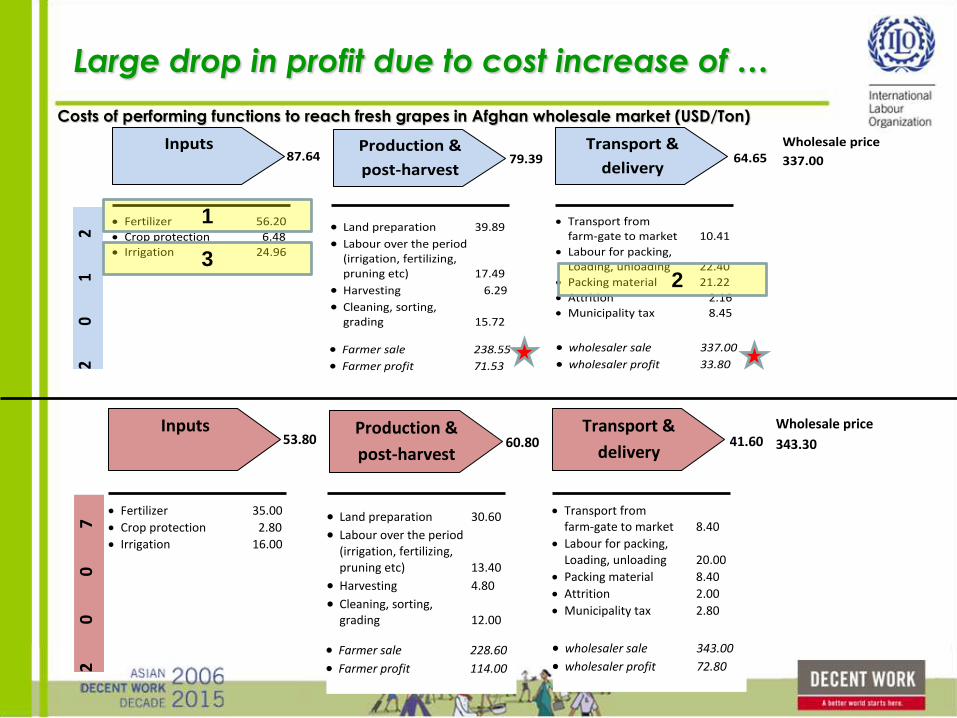

Costs of performing functions to reach fresh grapes in Afghan wholesale market (USD/Ton)

Farmer sale 238.55 Farmer profit 71.53

2 0

1 2

Fertilizer 56.20

Crop protection 6.48

Irrigation 24.96

Land preparation 39.89 Labour over the period

(irrigation, fertilizing, pruning etc) 17.49

Harvesting 6.29 Cleaning, sorting,

grading 15.72

Transport from farm-gate to market 10.41

Labour for packing, Loading, unloading 22.40

Packing material 21.22

Attrition 2.16

Municipality tax 8.45

87.64 79.39 64.65 Inputs Production &

post-harvest

Transport &

delivery

wholesaler sale 337.00

wholesaler profit 33.80

Wholesale price

337.00

2

0

0

7 Fertilizer 35.00

Crop protection 2.80

Irrigation 16.00

Land preparation 30.60 Labour over the period

(irrigation, fertilizing, pruning etc) 13.40

Harvesting 4.80

Cleaning, sorting, grading 12.00

Transport from farm-gate to market 8.40

Labour for packing, Loading, unloading 20.00

Packing material 8.40

Attrition 2.00

Municipality tax 2.80

53.80 60.80 41.60 Inputs Production &

post-harvest

Transport &

delivery

Farmer sale 228.60

Farmer profit 114.00

wholesaler sale 343.00 wholesaler profit 72.80

Wholesale price

343.30

1

23

Large drop in profit due to cost increase of …

Conclusions – fresh grapes

•Losing price competitiveness but surviving in domestic market

•Increased fertilizer cost, packaging and irrigation cost

•Low farm-gate price

•Shrinking profit margin for wholesalers/ exporters

•Limited export market

•Poor business enabling environment

Recommendations – fresh grapes

R1- Reduce unit cost of production by

adopting trellis method

Inputs Production & post-harvest

Transport & delivery

Rules

Support functions

• Promote trellis

method in Shamali

plain land in the

short-run

• Establishing trellis

system and thereby

increased supply in

the VC can create 1.1

million new labour

days (= 4000+ full

time employment)

R2 - Educate farmers on financial management to better manage their farms

Inputs Production & post-harvest

Transport & delivery

Rules

Support functions

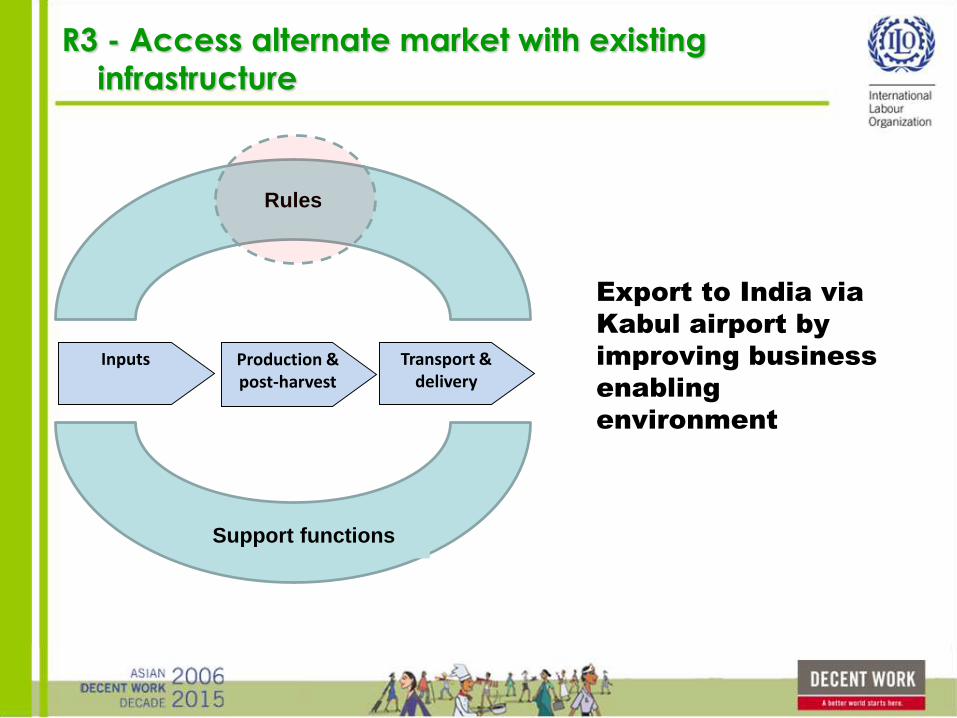

R3 - Access alternate market with existing

infrastructure

Inputs Production & post-harvest

Transport & delivery

Rules

Support functions

Export to India via

Kabul airport by

improving business

enabling

environment

Raisins

Afghan raisin losing P competitiveness

5.800

7.466

2.6363.212

1.… 1.238

0.000

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

2007 2012

Domestic wholesale price of raisin USD/kg

AFG PAK IRN

Afghan raisin keeps losing

its price competitiveness

Pakistani raisin maintains

its position in between

Iranian raisin still maintains

its price competitiveness

Lost P competitiveness in all market but….

Still showing a high growth in parallel to Iran

Uzbakistan 26,000 tons

USA 148,000 tons

China 48 ,000 tons Turkey 214,000 tons

Chile 70 ,000 tons

Iran 112,000 tonsAfghanistan 28,000tons

Pakistan 47 tons

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

$0 $500 $1,000 $1,500 $2,000 $2,500 $3,000 $3,500

Global annual growth rate in value 2001-11:

12 %

Global average price in 2011per ton $1,788.44

Large drop in profit due to cost increase of…

Farmer sale 828.84 Farmer profit 94.32

2

0

1

2 Fertilizer 168.57

Crop protection 19.45

Irrigation 74.85

Land preparation 119.67 Labour over the period

(irrigation, fertilizing, pruning etc) 52.47

Harvesting 18.86 Cleaning, drying,

Collection 280.60

Factory level cleaning, processing 90.00

Machine processing 33.00

Packing material 71.00

Attrition 124.00

Transport from factory gate to border 30.00

Custom clearance 12.00

262.87 471.60 330.00 Inputs Production & post-

harvest

Processing, transport

& delivery

exporter sale 1300.00 exporter profit 141.21

FoB price 1300.00

Farmer sale 660.00 Farmer profit 138.00

2

0

0

7 Fertilizer 105.00

Crop protection 8.40

Irrigation 48.00

Land preparation 91.80 Labour over the period

(irrigation, fertilizing, pruning etc) 40.20

Harvesting 14.40 Cleaning, drying,

Collection 214.20

Factory level cleaning, processing 82.00

Machine processing 29.00

Packing material 73.00

Attrition 107.12

Transport from factory gate to border 25.60

Custom clearance 10.00

161.40 360.60 326.72 Inputs Production & post-

harvest

Processing, transport

& delivery

exporter sale 1150.00 exporter profit 163.28

FoB price 1150.00

1

2

3

Costs of performing functions to reach raisins in Afghan border for export (USD/Ton)

Conclusions

• Eroded price competitiveness

• Shrinking profit and market in traditional market against competitors

• Stands out by quality for high-end market

• Only few exporters currently reach high-end market

• More raisins, more jobs

Recommendations – raisins

R1- Assist current high end exporters to

penetrate further

Inputs Production & post-harvest

Processing, Transport &

delivery

Rules

Support functions

50% increase in export volume of 5 such exporters can create 0.8 million new labour days where around 50% for women

R2 - Enable raisin exporters to reach high end

markets

Inputs Production & post-harvest

Processing Transport &

delivery

Rules

Support functions

220% increase in export volume of 35 such exporters can create 3.1 million new labour days where around 50% for women

R3 - Support certification agencies to get access

to Afghan market

Inputs Production & post-harvest

Processing, Transport &

delivery

Rules

Support functions

Wheat

Wheat value chain in Afghanistan

Input importing

Input wholesaling

Input retailing

Farming

Wheat trading

Processing

Wheat flour

importing

Wheat flour

trading

Bread making

Wholesaling

Agri-inputs (fertilizer, crop protection, vitamins) importers with urban

sales outlet

Urban based

large wholesaler

Urban based Distributor

of input companies

Rural retailers

Rural/localized market National market

Flour mills

Semi

commer

cial

wheat

farmer

Rural wheat trader

Wheat retailer

Commercial/large wheat farmer

Urban large wheat trader

Millers’ urban based distributor

Rural wheat flour trader

Urban based imported wheat flour trader

Rural imported wheat flour trader

Input production

Seed producing farms supported by FAO/GIZ

Grocery shops Retailing

Bakery

Wheat bran

Livestock farms

Wheat bran trader

Wheat bran retailer

Local millers

Contract seed growers

Mobile vender

Wheat bran importer

Wheat

importing

Afghan Fertilizer manufacturer

FAO

VC FUNCTIONS

END MARKETS

Threshing Threshers

Wheat and wheat flour importers

24%

6%

70%

Enterprise and jobs

Processing

Retail

Wholesale

Import

Production

Inputs Inputs importers cum wholesaler N=100, E=2700, F= 0%

Fertilizer manufacturer N=1, E= 1500, F=10%

Inputs retailer N=750, E=750, F=0%

Wheat farmer N=480,011; E=2,400,055; F = 5%

Wheat importer N=20, E=680, F=0%

Wheat flour importer N=450, E=9,900; F=0%

Rural wheat aggregator N=360, E=360, F=0%

Urban based wheat flour wholesaler N=500, E=10,000, F=0%

wheat retailer N=300, E=300, F=0%

Wheat flour retailer N=5,000; E=5,000, F=0%

Flour mills N=35, E=3500, F=10%

Zirandas N=30,000; E=30,000, F = 0%

N= enterprise

E=employment

F= female

involvement

Seed processor N=100, E=2600, F=0%

Wheat bran importer N=8, E=40; F=0%

Threshers N=3,600; E=3,600,; F = 5%

Bakery N=3,600; E=7,200; F = 0%

Afghan wheat lost P competitiveness further

while Pakistan gained

0.260

0.363

0.214

0.1890.199

0.212

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

0.400

2007 2012

Domestic wholesale price of wheat USD/kg

AFG PAK IRN

Afghan wheat price lost its

price competitiveness

further

Pakistani wheat gains

further price

competitiveness

Iranian wheat slightly lost

its price competitiveness

but still competitive against

Afghani wheat

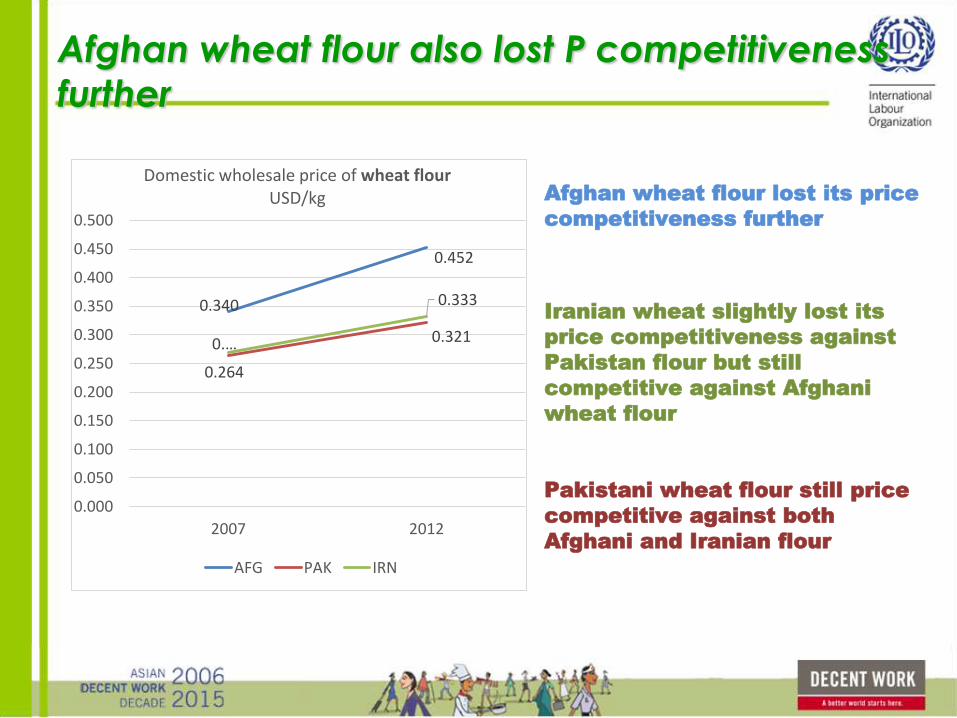

Afghan wheat flour also lost P competitiveness

further

0.340

0.452

0.264

0.3210.…

0.333

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

0.400

0.450

0.500

2007 2012

Domestic wholesale price of wheat flourUSD/kg

AFG PAK IRN

Afghan wheat flour lost its price

competitiveness further

Iranian wheat slightly lost its

price competitiveness against

Pakistan flour but still

competitive against Afghani

wheat flour

Pakistani wheat flour still price

competitive against both

Afghani and Iranian flour

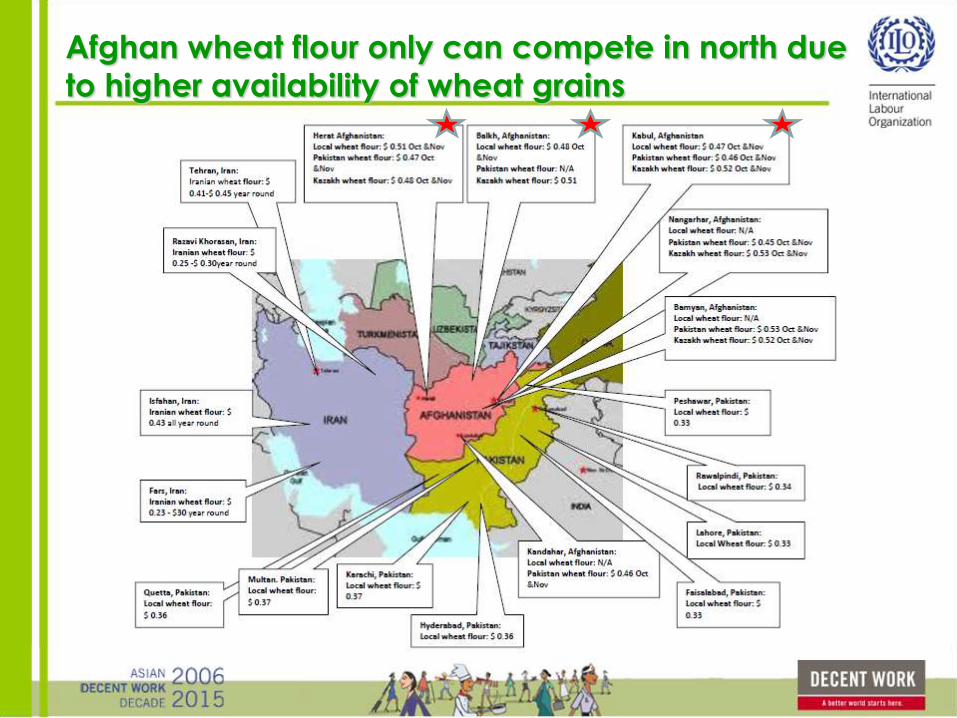

Afghan wheat flour only can compete in north due

to higher availability of wheat grains

In wheat, Iran has higher growth though little in

volume compared to Pakistan

China 40,000 tons

USA 33 million tons

Kazakhstan 3 million tons

Pakistan 2 million tons

Iran 45,000 tons

Uzbekistan 130,000 tons

India 500,000 tons-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

160.00%

$0 $100 $200 $300 $400 $500 $600

Global annual growth rate in value 2001-11:

11 %

Global average price in 2011per ton $316

In wheat flour, Pakistan is regional large player second to

Kazakhstan though the latter shows higher growth

China 300,000 tons

USA 300,000 tons

Kazakhstan 2 million tons

Pakistan 1.2 million tons

India 70,000 tons

Uzbekistan 2,000 tons

Iran 70,000 tons

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

$0 $100 $200 $300 $400 $500 $600 $700

Global annual growth rate in value 2001-11:

12 %

Global average price in 2011per ton $434

High flour price due to high production cost

Farmer sale 345.25 Farmer profit 92.94

Aggregator sale 359.20 Aggregator profit 7.66

2 0

1 2

Seeds 28.30

Fertilizer 99.04

Crop protection 3.14

Irrigation 6.09

Land preparation 34.78

Labour over the period (sowing, planting, weeding etc) 19.06

Harvesting 29.48 Threshing 32.42

Aggregation cost 6.29

Transport from Aggregation to mill 9.83

Labour for packing, Loading, unloading 1.57

Milling cost 56.99

Packing material 15.72

136.57 122.02 84.10 Inputs Production, post-

harvest & aggregation

Processing, transport

& delivery

miller sale 451.95 miller profit 8.65

Miller price

451.95

Farmer sale 262.00 Farmer profit 90.80 Aggregator sale 270.00 Aggregator profit 3.80

2 0

0 7

Seeds 22.60

Fertilizer 43.40

Crop protection 1.60

Irrigation 5.00

Land preparation 27.20

Labour over the period (sowing, planting, weeding etc) 14.40

Harvesting 24.40 Threshing 32.60

Aggregation cost 4.20

Transport from Aggregation to mill 8.00

Labour for packing, Loading, unloading 1.20

Milling cost 43.00

Packing material 12.00

72.6 102.08 64.20 Inputs Production, post-

harvest & aggregation

Processing, transport

& delivery

miller sale 343.00 miller profit 8.80

Miller price

343.00

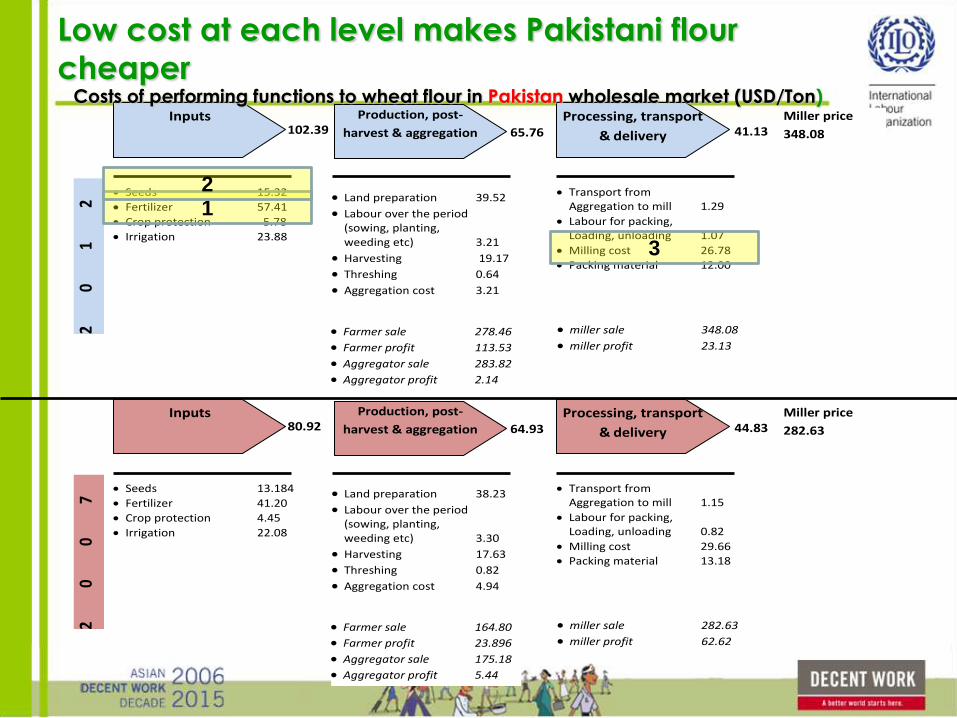

Costs of performing functions to wheat flour in Afghan wholesale market (USD/Ton)

21

3

Low cost at each level makes Pakistani flour

cheaper

Farmer sale 278.46 Farmer profit 113.53

Aggregator sale 283.82 Aggregator profit 2.14

2 0

1 2

Seeds 15.32

Fertilizer 57.41

Crop protection 5.78

Irrigation 23.88

Land preparation 39.52

Labour over the period (sowing, planting, weeding etc) 3.21

Harvesting 19.17 Threshing 0.64

Aggregation cost 3.21

Transport from Aggregation to mill 1.29

Labour for packing, Loading, unloading 1.07

Milling cost 26.78

Packing material 12.00

102.39 65.76 41.13 Inputs Production, post-

harvest & aggregation

Processing, transport

& delivery

miller sale 348.08

miller profit 23.13

Miller price

348.08

Farmer sale 164.80 Farmer profit 23.896

Aggregator sale 175.18 Aggregator profit 5.44

2 0

0 7

Seeds 13.184

Fertilizer 41.20

Crop protection 4.45

Irrigation 22.08

Land preparation 38.23

Labour over the period (sowing, planting, weeding etc) 3.30

Harvesting 17.63 Threshing 0.82

Aggregation cost 4.94

Transport from Aggregation to mill 1.15

Labour for packing, Loading, unloading 0.82

Milling cost 29.66

Packing material 13.18

80.92 64.93 44.83 Inputs Production, post-

harvest & aggregation

Processing, transport

& delivery

miller sale 282.63 miller profit 62.62

Miller price

282.63

Costs of performing functions to wheat flour in Pakistan wholesale market (USD/Ton)

12

3

Conclusions

• Increased cost of production due to high

input cost

• Low yield

• Competitiveness is lost further

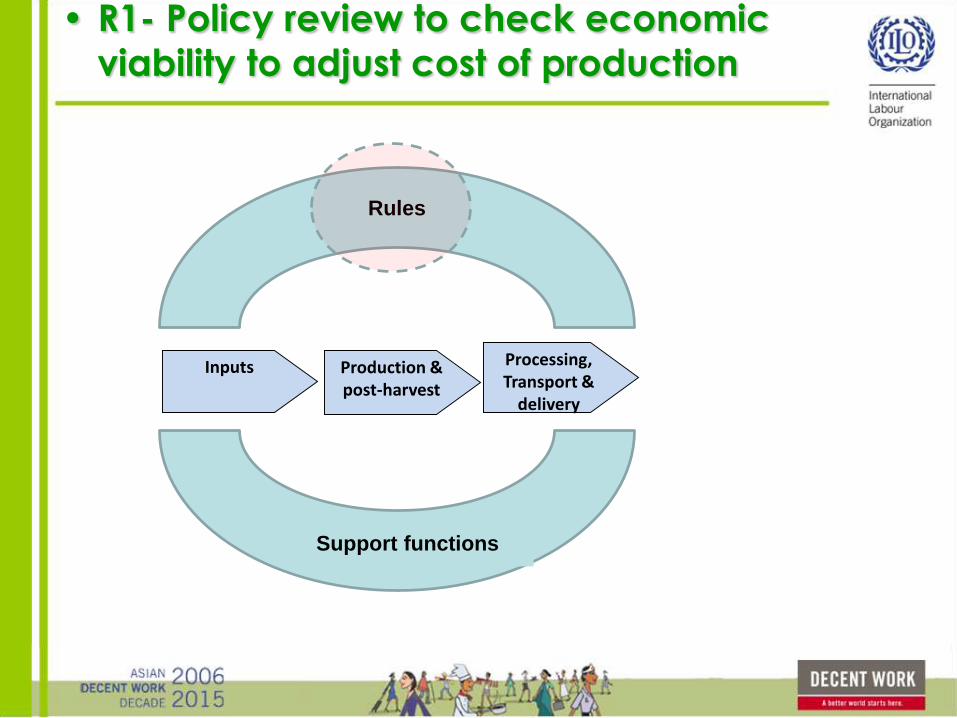

Recommendations – wheat

• R1- Policy review to check economic

viability to adjust cost of production

Inputs Production & post-harvest

Processing, Transport &

delivery

Rules

Support functions

R2 – Increase the availability of improve wheat seeds through private sector channel

Inputs Production & post-harvest

Transport & delivery

Rules

Support functions

Rice

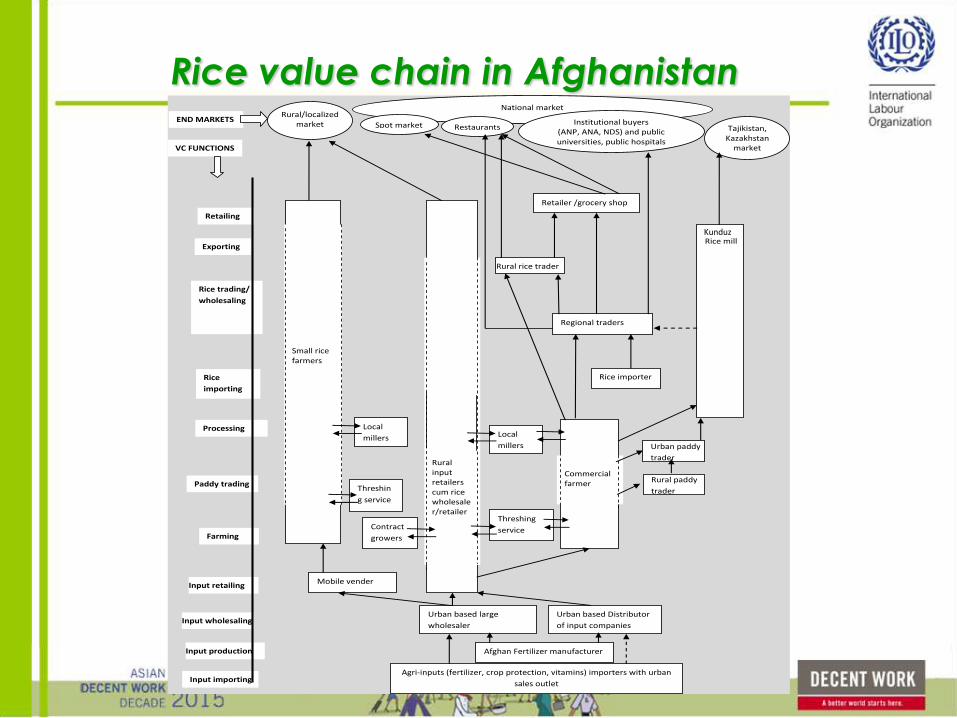

Rice value chain in Afghanistan

Input importing

Input wholesaling

Input retailing

Farming

Paddy trading

Processing

Rice

importing

Rice trading/

wholesaling

Agri-inputs (fertilizer, crop protection, vitamins) importers with urban

sales outlet

Urban based large

wholesaler

Urban based Distributor

of input companies

Rural/localized market

National market

Retailing

Contract

growers

Rural input retailers cum rice wholesaler/retailer

Rice importer

Commercial farmer

Retailer /grocery shop

Rural rice trader

Regional traders

Small rice farmers

Mobile vender

Farming

Input production Afghan Fertilizer manufacturer

Spot market Restaurants Institutional buyers

(ANP, ANA, NDS) and public universities, public hospitals

Local

millers

Local

millers

Threshing

service

Threshin

g service

Tajikistan, Kazakhstan

market

Rural paddy

trader

Urban paddy

trader

Mazaar

Rice mill Exporting

VC FUNCTIONS

END MARKETS

Kunduz

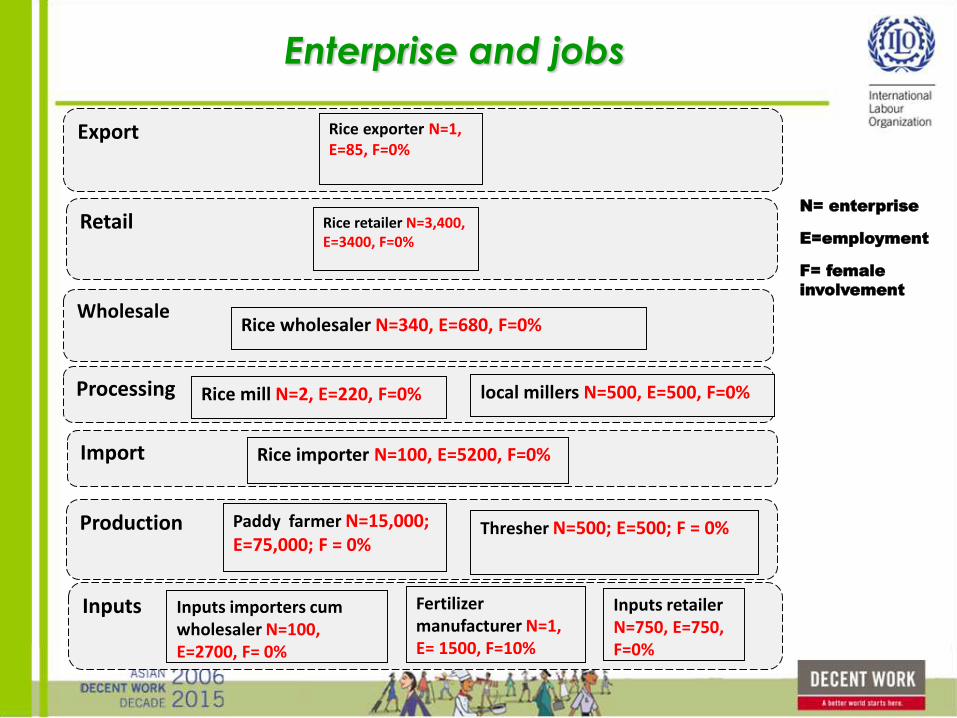

Enterprise and jobs

Export

Retail

Wholesale

Import

Production

Inputs Inputs importers cum wholesaler N=100, E=2700, F= 0%

Fertilizer manufacturer N=1, E= 1500, F=10%

Inputs retailer N=750, E=750, F=0%

Paddy farmer N=15,000; E=75,000; F = 0%

Rice retailer N=3,400, E=3400, F=0%

Rice exporter N=1, E=85, F=0%

N= enterprise

E=employment

F= female

involvement

Thresher N=500; E=500; F = 0%

Processing

Rice importer N=100, E=5200, F=0%

local millers N=500, E=500, F=0%Rice mill N=2, E=220, F=0%

Rice wholesaler N=340, E=680, F=0%

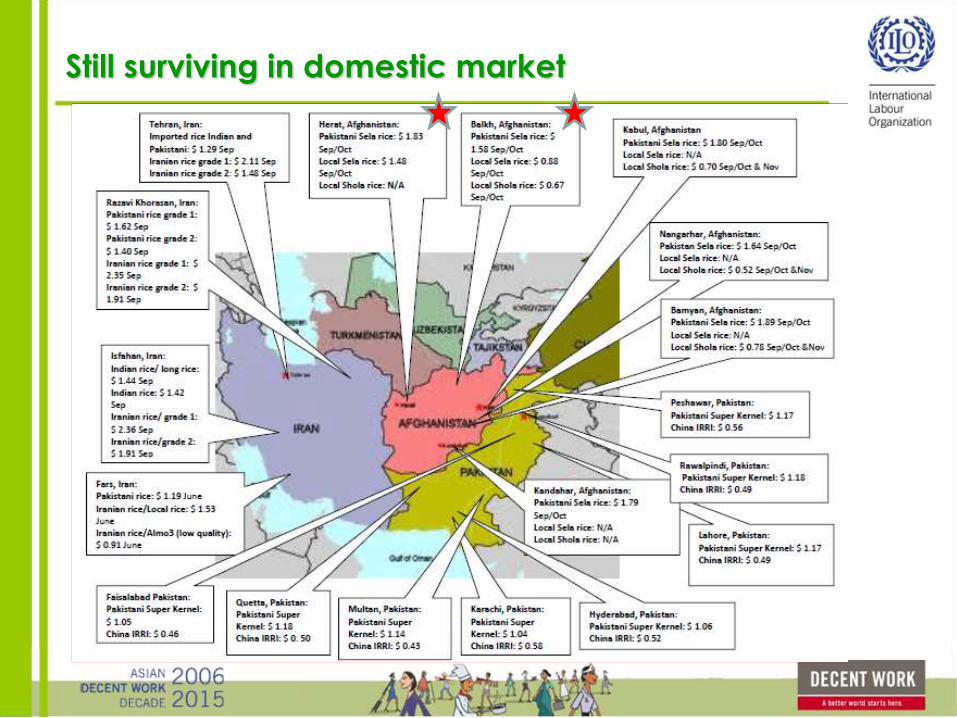

Pakistani rice reaches at price parity with

Afghan rice

0.8200.923

0.988 0.942

2.…

1.571

0.000

0.500

1.000

1.500

2.000

2.500

2007 2012

Domestic wholesale price of rice USD/kg

AFG PAK IRN

Pakistani rice is gaining

further price

competitiveness

Once most competitive,

Afghan rice is losing its

price competitiveness

against Pakistani rice

Still surviving in domestic market

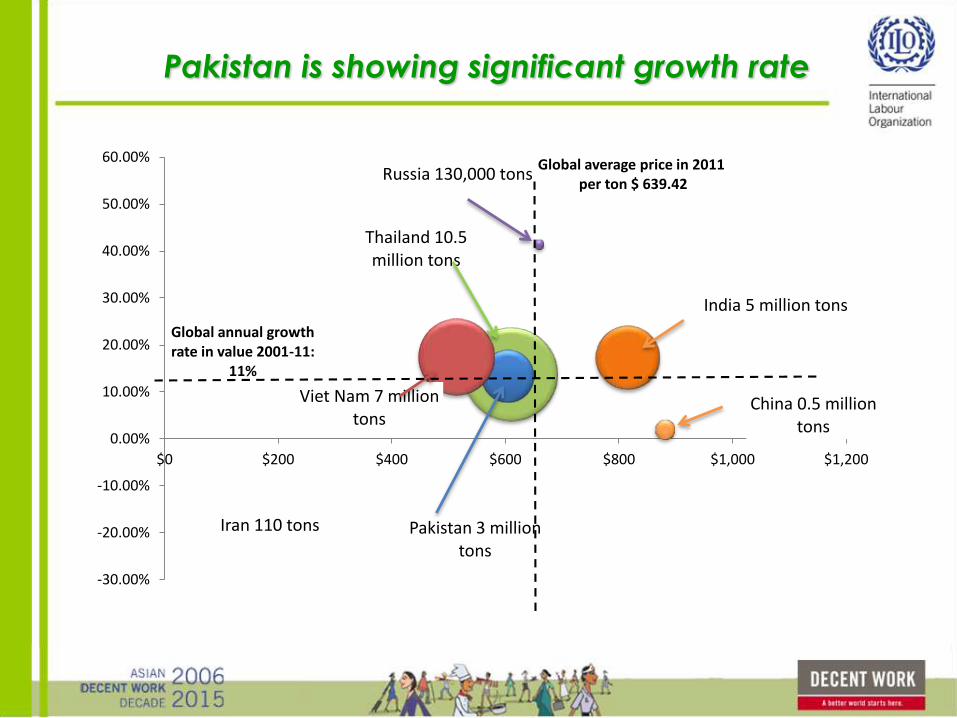

Pakistan is showing significant growth rate

Russia 130,000 tons

India 5 million tons

Iran 110 tons Pakistan 3 million tons

Thailand 10.5 million tons

China 0.5 million tons

Viet Nam 7 million tons

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

$0 $200 $400 $600 $800 $1,000 $1,200

Global annual growth rate in value 2001-11:

11%

Global average price in 2011per ton $ 639.42

Still rice is giving good profit to VC actors though

increased production cost

Farmer sale 491.25 Farmer profit 242.48

2

0

1

2 Seeds 14.34

Fertilizer 76.05

Irrigation 0.79

Land preparation 37.53 Labour over the period

(sowing, planting, weeding etc) 47.16

Harvesting 45.00 Threshing 27.90

Transport from farmgate to mill 13.95

Milling cost 82.14

Packing material 2.75

Distribution cost 9.83

91.18 157.59 108.66 Inputs Production & post-

harvest

Processing, transport

& delivery

miller sale 925.52

miller profit 325.60

Miller price

925.52

Farmer sale 428.40 Farmer profit 261.60

2

0

0

7 Seeds 10.08

Fertilizer 42.20

Irrigation 0.8

Land preparation 26.4

Labour over the period (sowing, planting, weeding etc) 27.00

Harvesting 33.80 Threshing 25.80

Transport from farmgate to mill 12.00

Milling cost 69.60

Packing material 6.00

Distribution cost 6.00

53.80 113.00 93.60 Inputs Production & post-

harvest

Processing, transport

& delivery

miller sale 820.00 miller profit 298.00

Miller price

820.00

Costs of performing functions to reach milled rice in Afghan wholesale market (USD/Ton)

1

2 1

Conclusions

• Like wheat, increased cost of production

due to high input cost

• Low yield

• Price competitiveness is at parity

Recommendations – rice

• R1- Policy review to check economic

viability to adjust cost of production

Inputs Production & post-harvest

Processing, Transport &

delivery

Rules

Support functions

• R2- Trade policy review to check the viability of protecting

domestic rice production and thereby jobs in the sector

Inputs Production & post-harvest

Processing, Transport &

delivery

Rules

Support functions

Tomato

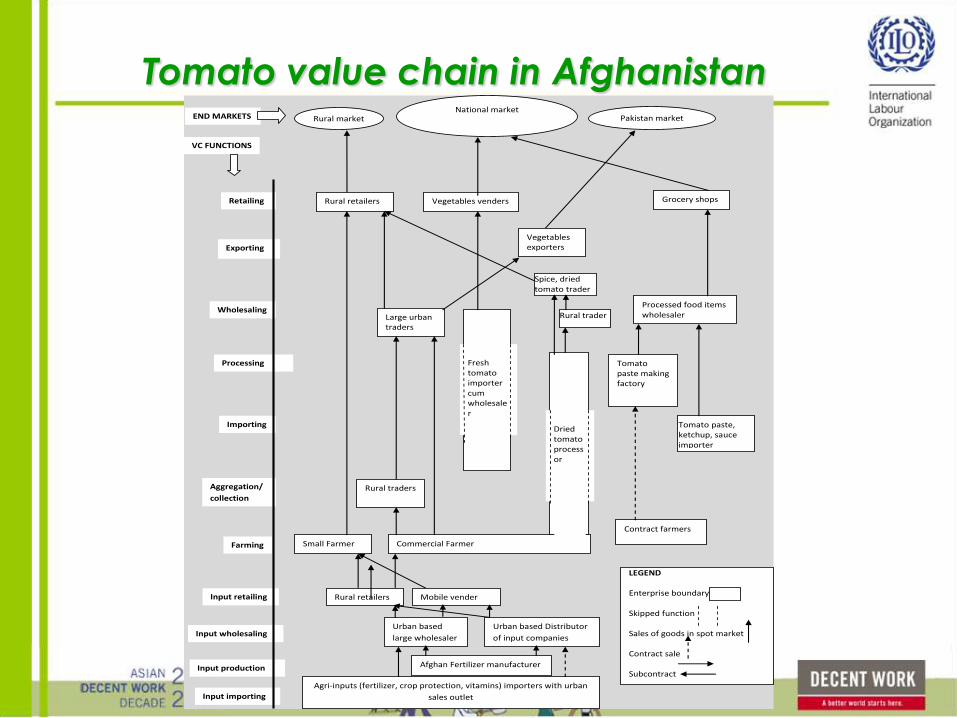

Tomato value chain in Afghanistan

Input importing

Input wholesaling

Input retailing

Farming

Processing

Importing

Aggregation/

collection

Exporting

Retailing

Wholesaling

Agri-inputs (fertilizer, crop protection, vitamins) importers with urban

sales outlet

Urban based

large wholesaler

Urban based Distributor

of input companies

Rural retailers

Rural market Pakistan market

Small Farmer

Rural retailers

Input production

Commercial Farmer

Vegetables exporters

Fresh tomato importer cum wholesaler

Rural traders

Large urban traders

National market

Vegetables venders

Tomato paste making factory

Contract farmers

Processed food items wholesaler

Grocery shops

Afghan Fertilizer manufacturer

Mobile vender

Dried tomato processor

Spice, dried tomato trader

Tomato paste, ketchup, sauce importer

VC FUNCTIONS

END MARKETS

Rural trader

LEGEND Enterprise boundary Skipped function Sales of goods in spot market Contract sale Subcontract

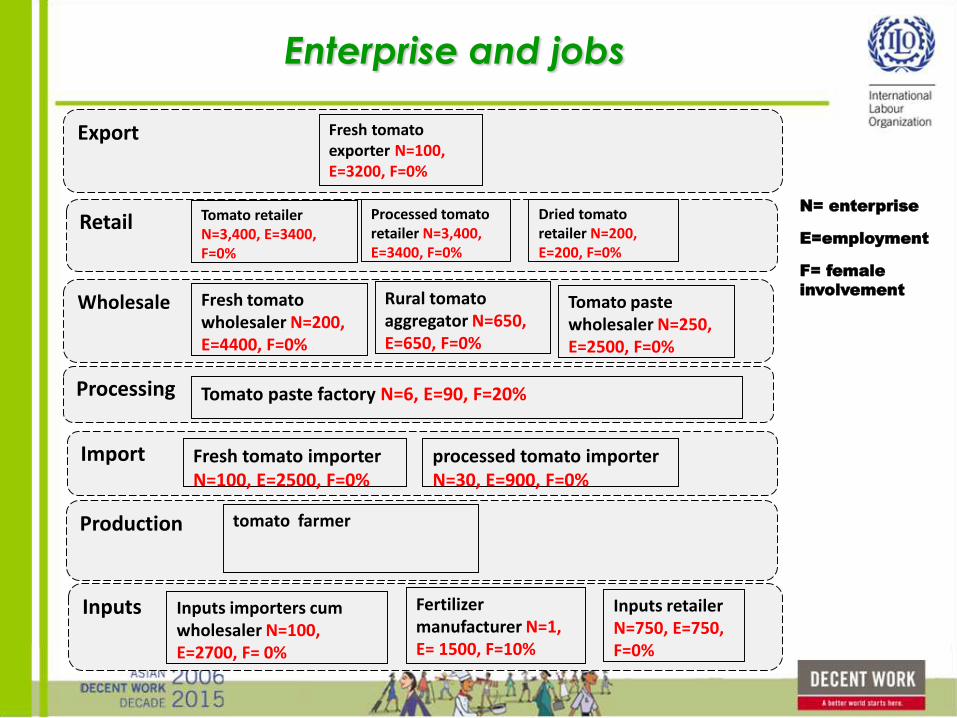

Enterprise and jobs

N= enterprise

E=employment

F= female

involvement

Export

Retail

Wholesale

Import

Production

Inputs Inputs importers cum wholesaler N=100, E=2700, F= 0%

Fertilizer manufacturer N=1, E= 1500, F=10%

Inputs retailer N=750, E=750, F=0%

tomato farmer

Tomato retailer N=3,400, E=3400, F=0%

Fresh tomato exporter N=100, E=3200, F=0%

Processing Tomato paste factory N=6, E=90, F=20%

Fresh tomato importer N=100, E=2500, F=0%

processed tomato importer N=30, E=900, F=0%

Fresh tomato wholesaler N=200, E=4400, F=0%

Rural tomato aggregator N=650, E=650, F=0%

Tomato paste wholesaler N=250, E=2500, F=0%

Processed tomato retailer N=3,400, E=3400, F=0%

Dried tomato retailer N=200, E=200, F=0%

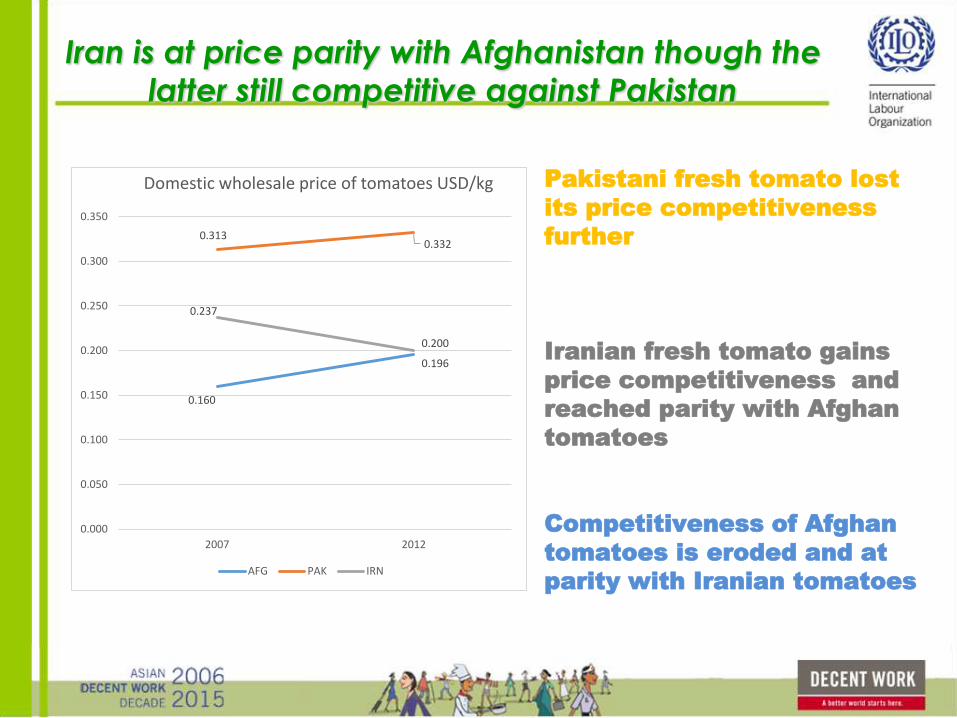

Iran is at price parity with Afghanistan though the

latter still competitive against Pakistan

0.160

0.196

0.3130.332

0.237

0.200

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

2007 2012

Domestic wholesale price of tomatoes USD/kg

AFG PAK IRN

Pakistani fresh tomato lost

its price competitiveness

further

Iranian fresh tomato gains

price competitiveness and

reached parity with Afghan

tomatoes

Competitiveness of Afghan

tomatoes is eroded and at

parity with Iranian tomatoes

Iranian tomato paste also reached at price parity

with Afghani

0.740

0.845

1.…

0.857

0.000

0.200

0.400

0.600

0.800

1.000

1.200

2007 2012

Domestic wholesale price of tomato pasteUSD/kg

AFG IRN

Iranian tomato paste gained

price competitiveness and

at parity with Afghan tomato

paste

Afghan tomato paste lost

competitiveness against

Iranian tomato paste

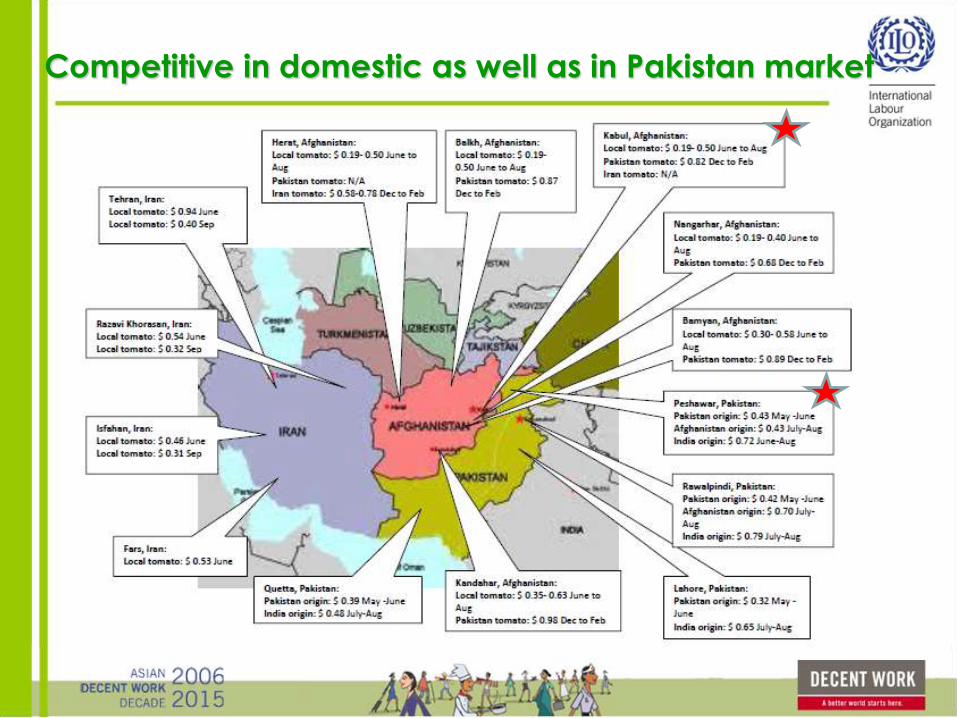

Competitive in domestic as well as in Pakistan market

Afghan tomato paste is still P competitive in

domestic market

Iran is growing in fresh tomato

Tajikistan 12,000 tons

India 230,000 tons

Turkey 550,000 tons

China 130,000 tons

Uzbekistan 52,000 tons

Iran 140,000 tonnsUSA 200,000 tons

Pakistan 45,000 tons

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

120.00%

140.00%

160.00%

180.00%

$0 $200 $400 $600 $800 $1,000 $1,200 $1,400 $1,600 $1,800 $2,000

Global annual growth rate in value 2001-11:

10 %

Global average price in 2011per ton $1,141

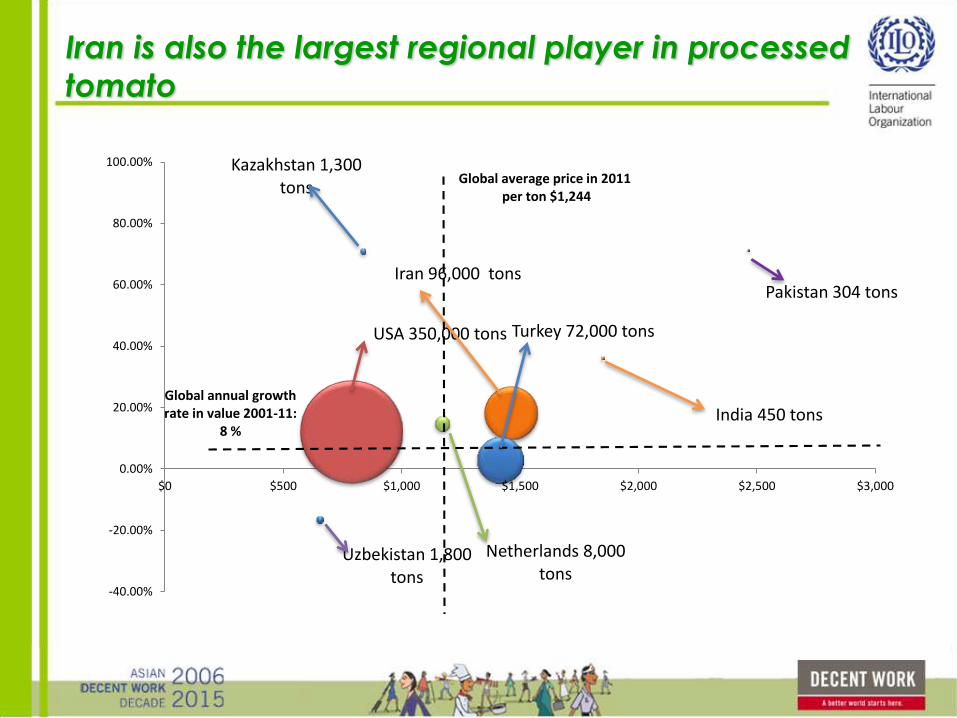

Iran is also the largest regional player in processed

tomato

Netherlands 8,000 tons

Kazakhstan 1,300 tons

Iran 96,000 tons

Turkey 72,000 tons

Pakistan 304 tons

USA 350,000 tons

India 450 tons

Uzbekistan 1,800 tons

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

$0 $500 $1,000 $1,500 $2,000 $2,500 $3,000

Global annual growth rate in value 2001-11:

8 %

Global average price in 2011per ton $1,244

Processor profit is shrinking due to high raw material cost

Farmer sale 352.52 Farmer profit 173.55

*2.3 kg makes 800 gm canned tomatoes

2 0

1 2

Seeds 2.71

Fertilizer 52.43

Crop protection 5.42

Irrigation 50.62

Land preparation 14.46 Labour over the period

(sowing, planting, weeding etc) 13.11

Cleaning, sorting packing 8.14

Transport to processing plant 32.09

Processing cost 50.01

Packing material 358.61

Distribution cost 6.29

111.18 67.79 414.91 Inputs Production & post-

harvest

Processing, transport

& delivery

processor sale 844.95 processor profit 77.52

Processor price

844.96

Farmer sale 276.00 Farmer profit 166.98

*2.3 kg makes 800 gm canned tomatoes

2 0

0 7

Seeds 1.84

Fertilizer 25.76

Crop protection 3.68

Irrigation 30.36

Land preparation 8.74 Labour over the period

(sowing, planting, weeding etc) 6.44

Cleaning, sorting packing 6.90

Transport to processing plant 25.30

Processing cost 40.00

Packing material 322.50

Distribution cost 4.40

61.64 47.38 366.90 Inputs Production & post-

harvest

Processing, transport

& delivery

processor sale 780.00 processor profit 137.10

Processor price

780.00

Costs of performing functions to reach tomato paste in Afghan wholesale market (USD/Ton)

1

2

1

Conclusions

• Eroded competitiveness brought at price

parity with Iran

• Still competitive for fresh produce at

domestic and Pakistan market

Recommendations – tomato

• R1- Policy review to check economic

viability to adjust cost of production

Inputs Production & post-harvest

Processing, Transport &

delivery

Rules

Support functions

• R2- Devise appropriate sourcing

mechanism to procure at low price

Inputs Production & post-harvest

Processing, Transport &

delivery

Rules

Support functions

Potato

Potato value chain in Afghanistan

LEGEND Enterprise boundary Skipped function Sales of goods in spot market Contract sale Subcontract

Input importing

Input wholesaling

Input retailing

Farming

Storing

Trading

Wholesaling

Processing

Retailing

Exporting

Agri-inputs (fertilizer, crop protection, vitamins) importers with urban

sales outlet

Urban based wholesaler/retailer Urban based Distributor

of input companies

Small Potato farmers

Potato

traders

cum

seed

seller

Rural vegetables retailers

National market International market

Urban based large trader

Potato chips

manufactur

er

Large commercial farmers

Processed items distributer

Importing

French fries processors

Afghan Fertilizer manufacturer Input production

VC FUNCTIONS

END MARKETS

Input retailer

Large

farmer

cum

trader

Regional trader

Potato Importers

General stores

Potato chips

importers

Distribution

Localized market

Vegetables/fruits vendors/ grocery shops

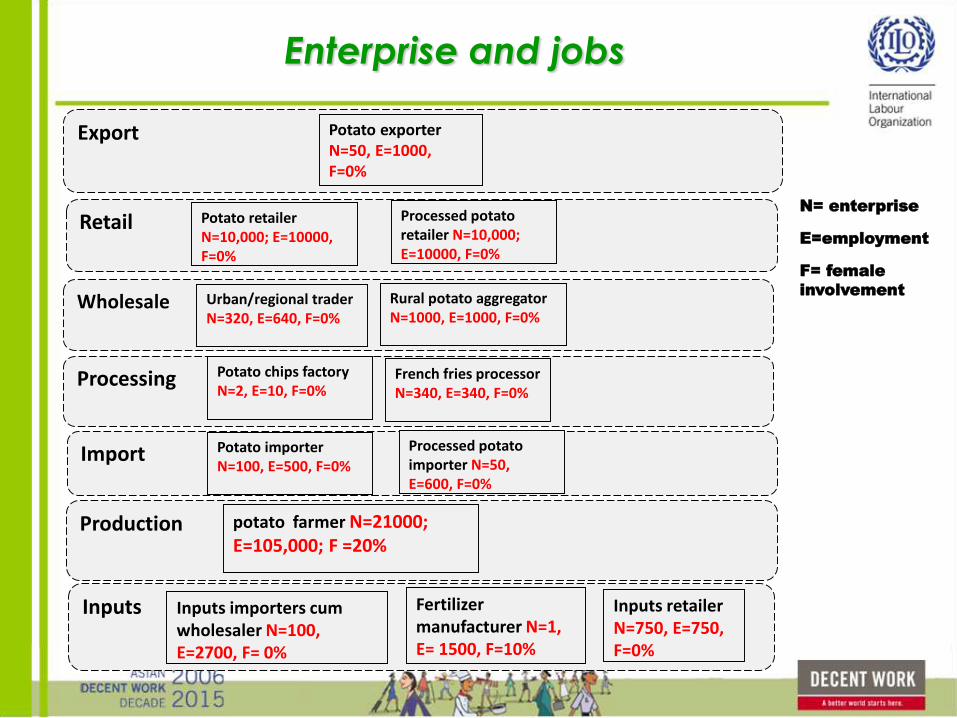

Enterprise and jobs

N= enterprise

E=employment

F= female

involvement

Export

Retail

Wholesale

Import

Production

Inputs Inputs importers cum wholesaler N=100, E=2700, F= 0%

Fertilizer manufacturer N=1, E= 1500, F=10%

Inputs retailer N=750, E=750, F=0%

potato farmer N=21000; E=105,000; F =20%

Potato retailer N=10,000; E=10000, F=0%

Potato exporter N=50, E=1000, F=0%

Processing

Potato importer N=100, E=500, F=0%

Processed potato importer N=50, E=600, F=0%

Potato chips factory N=2, E=10, F=0%

French fries processor N=340, E=340, F=0%

Urban/regional trader N=320, E=640, F=0%

Rural potato aggregator N=1000, E=1000, F=0%

Processed potato retailer N=10,000; E=10000, F=0%

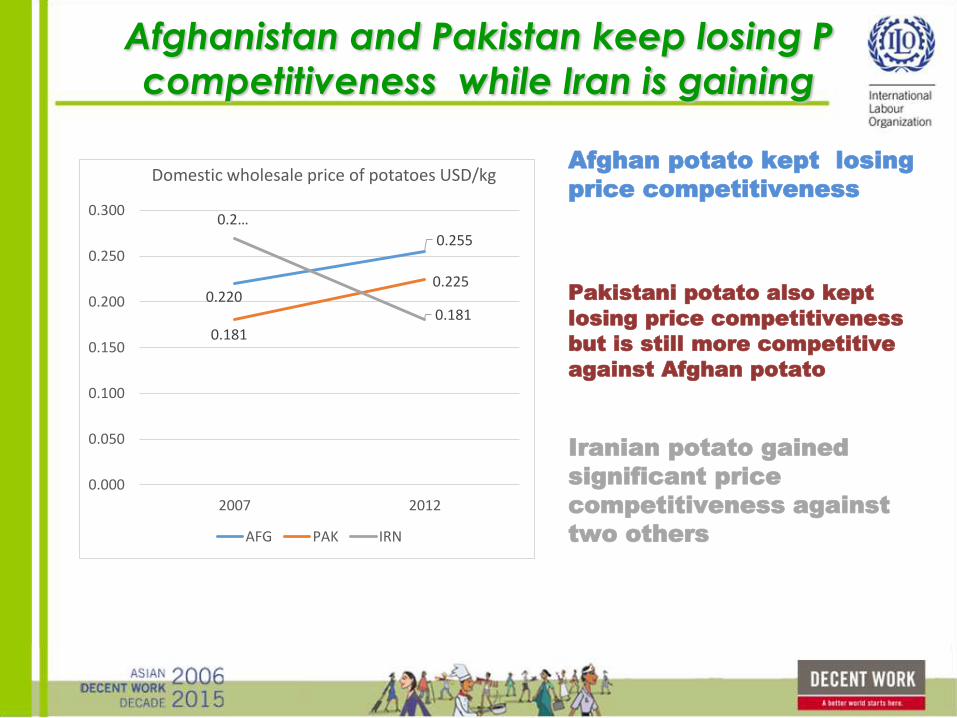

Afghanistan and Pakistan keep losing P

competitiveness while Iran is gaining

Afghan potato kept losing

price competitiveness

Pakistani potato also kept

losing price competitiveness

but is still more competitive

against Afghan potato

Iranian potato gained

significant price

competitiveness against

two others

0.220

0.255

0.181

0.225

0.2…

0.181

0.000

0.050

0.100

0.150

0.200

0.250

0.300

2007 2012

Domestic wholesale price of potatoes USD/kg

AFG PAK IRN

Afghan potato Still P competitive in domestic market

and nearby Pakistan areas

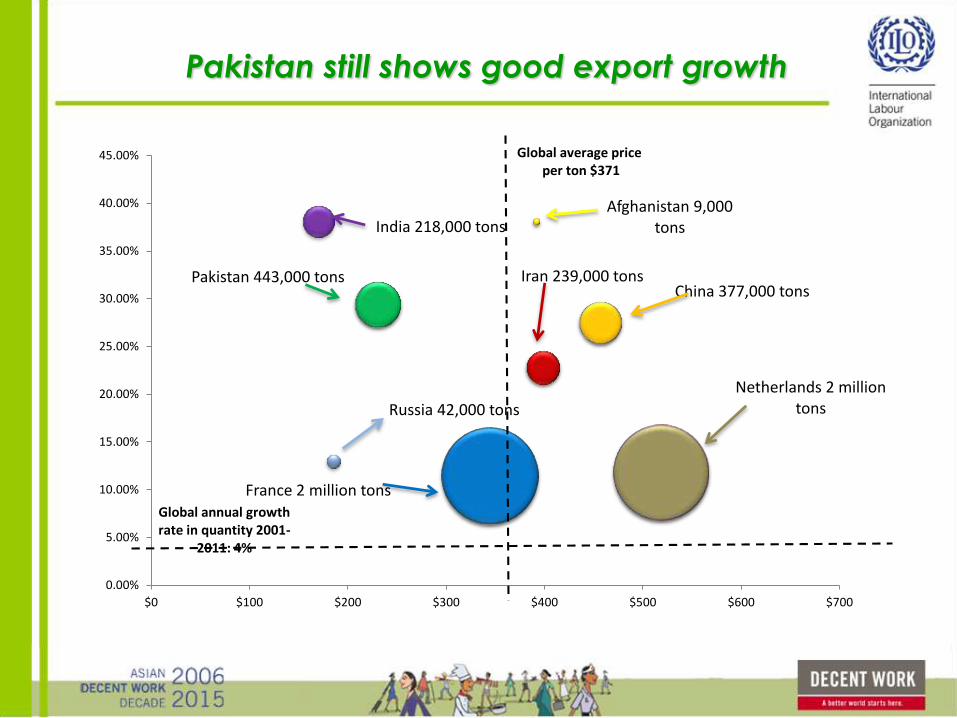

Pakistan still shows good export growth

France 2 million tons

Netherlands 2 million tons

Pakistan 443,000 tons Iran 239,000 tonsChina 377,000 tons

Afghanistan 9,000 tonsIndia 218,000 tons

Russia 42,000 tons

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

$0 $100 $200 $300 $400 $500 $600 $700

Global annual growth rate in quantity 2001-

2011: 4%

Global average priceper ton $371

Conclusions

• Lost price competitiveness

• Increased production cost due to high

fertilizer cost

Households’ response to

changing environment

Varying levels of income – by occupation

-50000

0

50000

100000

150000

200000

250000

300000

Sub

sist

ence

Bam

yan

Po

tato

Far

mer

Sub

sist

ence

Kab

ul G

rap

e Fa

rmer

Sub

sist

ence

Bag

hla

n W

hea

t Fa

rmer

Sem

i-C

om

mer

cial

Kab

ul G

rap

e fa

rme

r

Lab

ou

r (c

on

stru

ctio

n)

Co

mm

erci

al B

amya

n P

ota

to F

arm

er

Lab

ou

r (o

ther

far

ms)

Co

mm

erci

al B

agh

lan

To

mat

o F

arm

er

Sem

i-C

om

mer

cial

Kab

ul W

hea

t Fa

rmer

Cle

aner

Teac

her

Lab

ou

r (o

ther

far

ms)

Co

ntr

acti

ng

Maz

ar T

om

ato

Far

mer

Go

vern

men

t (D

AIL

)

Ow

n t

ruck

Co

mm

erci

al K

abu

l Gra

pe

Farm

er

Taxi

Dri

ver,

par

t ti

me

Lab

ou

r (o

ther

far

ms

+ co

nst

ruct

ion

)

Car

pen

ter

Gu

ard

NG

O

Po

lice

Lab

ou

r (o

ther

far

ms)

Teac

her

Taxi

Dri

ver

Co

mm

erci

al B

agh

lan

Ric

e fa

rmer

Secu

rity

Co

mp

any

Mili

tary

Ow

n S

ho

p

Go

vern

men

t (D

ail)

Co

ntr

acti

ng

Wh

eat

Ku

nd

uz

Farm

er

NG

O D

rive

r

Teac

her

Ve

teri

nar

y Sh

op

Teac

her

Mili

tary

agri income per person; daily labourers; formal public jobs; formal private jobs, own activity

Subsistence farms rely on non-ag income

Grand

pa/ma

Parents

Young

adults

Kids

• Agriculture work by head of HH

and family labour

[underemployment]

• Total agri income negative due

to self consumption

• Daily labour by head of HH

[underemployment]

• Female jobs?

• Multiple loans & debt shuffling

• Sell animals/other assets to

compensate insufficient income

Struggling subsistence farm HH (sell less than 20% of harvest)

w/o sufficient income earners

Semi-commercial still rely on non-ag income

Grand

pa/ma

Parents

Young

adults

Kids

• Agriculture work by adult males

and family labour

[underemployment]

• Total agri income could be

negative or positive

• Daily labour by adult males

[underemployment]

• Educated youth in low-rank

formal jobs [fully employed]

• Female jobs?

• Vary from debt shufflers to

savers at home

Semi-commercial farm HH (sell 20-60% of harvest)

w/o sufficient income earners

Commercial farming – more ag promises

Grand

pa/ma

Parents

Young

adults

Kids

• Agri work by adult males and

family labour [underemployment

to near full emp]

• Total agri income could cover

50% or more of HH expense

• Daily labour by adult males if

needed

• Educated youth in low-rank

formal jobs [fully employed]

• Female jobs for highly educated?

• Vary from loan takers to loan

givers, but savings at home

Commercial farm HH (sell 60% or more of harvest)

w/o sufficient income earners

To where labour moves?

Estalif district (Kabul) Yakawlang (Bamyan)

School-to-work transition

• The level of education of those under 18 is significantly higher than that of their parents and grandparents

• Children in 70% HHs combine light agricultural field work with school

• 28% of HHs had to stop children’s school before 18 years mainly due to economic hardship (while for girls, religious reason

• Students seem to access formal jobs after high school (e,g,. teachers, army, police), but a significant portion still gets wage, agriculture or skills-based jobs even after completing high school. Higher studies after high school usually lead to government or NGO jobs.

Poverty trap or upward mobility

• 75% of HHs borrowing but mainly for HHs expense.

• Average outstanding amount is 27% of annual income but the borrowing pattern is in constant or increasing trend

• Significant percent of HHs repay loans by taking another loans

• Only 17% HHs actually save money

Just for farm19%

Farm + HH42%

Just for HH39%

Reasons for borrowing

Never45%

Often 2%

Sometimes

49%

Very often 4%

Borrow to repay?

Summary outputs – macro picture:

Afghanistan-Pakistan

Which is the situation of your VC?

a) expanding domestic production with expansion of exports to

neighboring countries; grapes, raisins, fresh tomatoes

b) expanding domestic production with expansion of imports

from neighboring countries; wheat, wheat flour, rice, processed

tomatoes.

c) declining domestic production with expansion/flat level of

exports to neighboring countries;

d) declining domestic production with expansion of imports

from neighboring countries; potatoes

e) or somewhere in-between.

Summary outputs – macro picture

Labour & migration trends with each VC?

Due to the lack of longitudinal data on labour migration, the

questions below remain as future research questions.

a) expanding production with increase of Afghan labour & incoming foreign

labour;

b) expanding production with increase of Afghan labour & flat/declining foreign

labour;

c) Expanding production with flat/declining Afghan labour & increase in

incoming foreign labour;

d) declining production with increase of Afghan labour & incoming foreign

labour;

e) declining production with declining Afghan labour & incoming foreign

labour;

f) Declining production with flat/declining Afghan labour & increase of incoming

foreign labour;

… and more scenarios.

Overarching Recommendations

• Establish an Observatory of Competitiveness and Jobs

which will continuously monitor critical indicators and report

to the top level policymakers and the private sector

stakeholders.

• Establish a National Commission on Competitiveness and Jobs

as an inter-ministerial body chaired by an executive member

of the Government with the participation of the employers

and workers representatives

to review the reports of the Observatory and coordinate

policies in order to guide sectoral strategies on the basis of

the dynamic competitiveness and to ensure optimal

employment outcomes.

Thank you

Questions & Discussion