Company Update: FPI

8

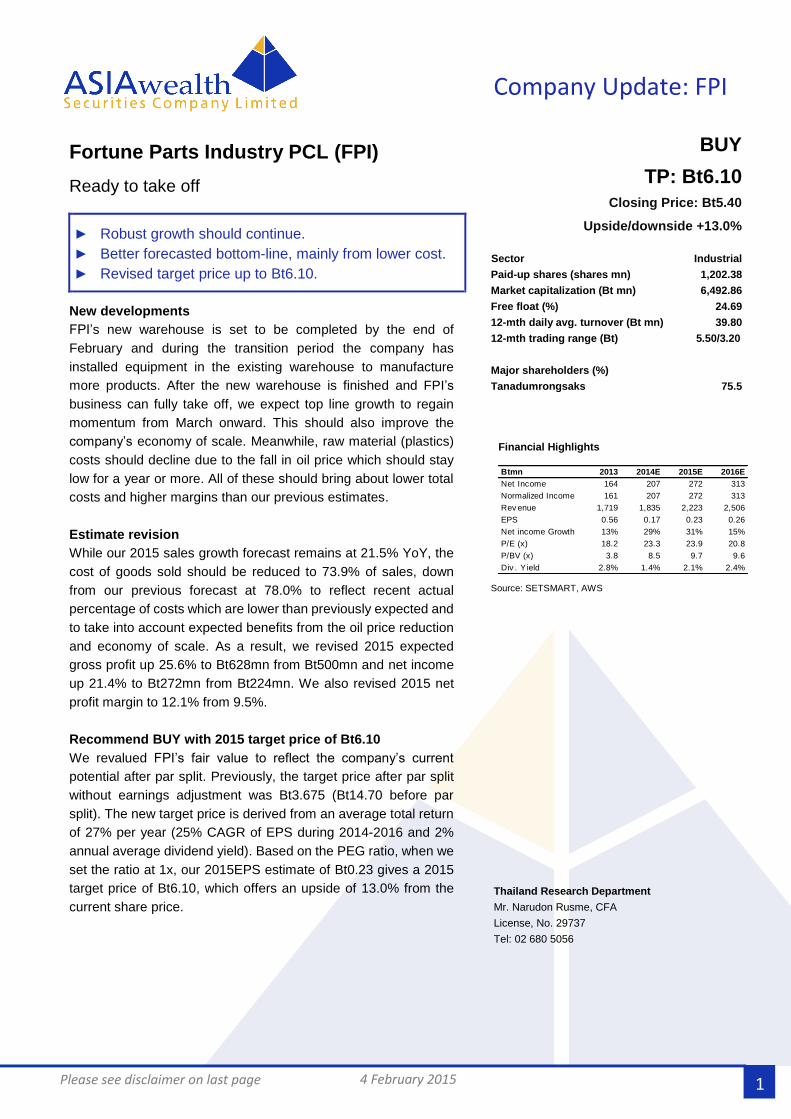

4 February 2015 Company Update: FPI 1 Please see disclaimer on last page Fortune Parts Industry PCL (FPI) Ready to take off ► Robust growth should continue. ► Better forecasted bottom-line, mainly from lower cost. ► Revised target price up to Bt6.10. New developments FPI’s new warehouse is set to be completed by the end of February and during the transition period the company has installed equipment in the existing warehouse to manufacture more products. After the new warehouse is finished and FPI’s business can fully take off, we expect top line growth to regain momentum from March onward. This should also improve the company’s economy of scale. Meanwhile, raw material (plastics) costs should decline due to the fall in oil price which should stay low for a year or more. All of these should bring about lower total costs and higher margins than our previous estimates. Estimate revision While our 2015 sales growth forecast remains at 21.5% YoY, the cost of goods sold should be reduced to 73.9% of sales, down from our previous forecast at 78.0% to reflect recent actual percentage of costs which are lower than previously expected and to take into account expected benefits from the oil price reduction and economy of scale. As a result, we revised 2015 expected gross profit up 25.6% to Bt628mn from Bt500mn and net income up 21.4% to Bt272mn from Bt224mn. We also revised 2015 net profit margin to 12.1% from 9.5%. Recommend BUY with 2015 target price of Bt6.10 We revalued FPI’s fair value to reflect the company’s current potential after par split. Previously, the target price after par split without earnings adjustment was Bt3.675 (Bt14.70 before par split). The new target price is derived from an average total return of 27% per year (25% CAGR of EPS during 2014-2016 and 2% annual average dividend yield). Based on the PEG ratio, when we set the ratio at 1x, our 2015EPS estimate of Bt0.23 gives a 2015 target price of Bt6.10, which offers an upside of 13.0% from the current share price. BUY TP: Bt6.10 Closing Price: Bt5.40 Upside/downside +13.0% Sector Industrial Paid-up shares (shares mn) 1,202.38 Market capitalization (Bt mn) 6,492.86 Free float (%) 24.69 12-mth daily avg. turnover (Bt mn) 39.80 12-mth trading range (Bt) 5.50/3.20 Major shareholders (%) Tanadumrongsaks 75.5 Financial Highlights Source: SETSMART, AWS Thailand Research Department Mr. Narudon Rusme, CFA License, No. 29737 Tel: 02 680 5056 Btmn 2013 2014E 2015E 2016E Net Income 164 207 272 313 Normalized Income 161 207 272 313 Rev enue 1,719 1,835 2,223 2,506 EPS 0.56 0.17 0.23 0.26 Net income Growth 13% 29% 31% 15% P/E (x) 18.2 23.3 23.9 20.8 P/BV (x) 3.8 8.5 9.7 9.6 Div. Yield 2.8% 1.4% 2.1% 2.4%

Transcript of Company Update: FPI

4 February 2015

Company Update: FPI

1

Please see disclaimer on last page

Fortune Parts Industry PCL (FPI)

Ready to take off

► Robust growth should continue.

► Better forecasted bottom-line, mainly from lower cost.

► Revised target price up to Bt6.10.

New developments

FPI’s new warehouse is set to be completed by the end of

February and during the transition period the company has

installed equipment in the existing warehouse to manufacture

more products. After the new warehouse is finished and FPI’s

business can fully take off, we expect top line growth to regain

momentum from March onward. This should also improve the

company’s economy of scale. Meanwhile, raw material (plastics)

costs should decline due to the fall in oil price which should stay

low for a year or more. All of these should bring about lower total

costs and higher margins than our previous estimates.

Estimate revision

While our 2015 sales growth forecast remains at 21.5% YoY, the

cost of goods sold should be reduced to 73.9% of sales, down

from our previous forecast at 78.0% to reflect recent actual

percentage of costs which are lower than previously expected and

to take into account expected benefits from the oil price reduction

and economy of scale. As a result, we revised 2015 expected

gross profit up 25.6% to Bt628mn from Bt500mn and net income

up 21.4% to Bt272mn from Bt224mn. We also revised 2015 net

profit margin to 12.1% from 9.5%.

Recommend BUY with 2015 target price of Bt6.10

We revalued FPI’s fair value to reflect the company’s current

potential after par split. Previously, the target price after par split

without earnings adjustment was Bt3.675 (Bt14.70 before par

split). The new target price is derived from an average total return

of 27% per year (25% CAGR of EPS during 2014-2016 and 2%

annual average dividend yield). Based on the PEG ratio, when we

set the ratio at 1x, our 2015EPS estimate of Bt0.23 gives a 2015

target price of Bt6.10, which offers an upside of 13.0% from the

current share price.

BUY

TP: Bt6.10

Closing Price: Bt5.40 Upside/downside +13.0%

Sector Industrial

Paid-up shares (shares mn) 1,202.38

Market capitalization (Bt mn) 6,492.86

Free float (%) 24.69

12-mth daily avg. turnover (Bt mn) 39.80

12-mth trading range (Bt) 5.50/3.20

Major shareholders (%)

Tanadumrongsaks 75.5

Financial Highlights

Source: SETSMART, AWS

Thailand Research Department

Mr. Narudon Rusme, CFA

License, No. 29737

Tel: 02 680 5056

Btmn 2013 2014E 2015E 2016E

Net Income 164 207 272 313

Normalized Income 161 207 272 313

Rev enue 1,719 1,835 2,223 2,506

EPS 0.56 0.17 0.23 0.26

Net income Growth 13% 29% 31% 15%

P/E (x) 18.2 23.3 23.9 20.8

P/BV (x) 3.8 8.5 9.7 9.6

Div . Y ield 2.8% 1.4% 2.1% 2.4%

4 February 2015

Company Update: FPI

2

Please see disclaimer on last page

Estimate revision

Our 2015 sales growth forecast remains at 21.5% YoY. We anticipate sales of

Bt2.18bn, down slightly from our previous forecast of Bt2.28bn due to a lower sales

forecast for 2014 based on actual 9-month data. What is more important is that the

cost of goods sold should decline to 73.9% of total revenue, which is revised down

from our previous forecast of 78.0% to reflect recent actual percentage of costs,

which have been lower than expected, and to take into account expected benefits

from the fall in oil price and improved economy of scale. FPI’s 2015 COGS would

decrease to Bt1.61bn from Bt1.77bn. As a result, 2015 expected gross profit was

revised up 25.6% to Bt628mn, from Bt500mn, and expected net income was

adjusted up 21.4% to Bt272mn, from Bt224mn. We also revised 2015 net profit

margin to 12.1% from 9.5%.

Robust growth should continue

Warehouse is crucial.

FPI’s new warehouse will be completed by the end of February. This is crucial since

the company’s strength is in the variety of goods available on its shelves and speed

of delivery. Its position as a one-stop service with the fastest delivery will be

supported by the adequate space in its warehouse. Therefore, we expect FPI’s top

line growth to regain momentum from March onward. Its bottom line should show

even more improvement thanks to innovation and branding as well as higher

capacity utilization that will widen its profit margin.

First step in expanding its production base abroad

FPI has diversified its trading portfolio of clients. The company expanded its business

to China, India, Turkey, Italy, Ecuador, Mexico, Brazil, US, North Africa and South

Africa.

Since logistic costs to some areas are quite high, the company is establishing joint

ventures to manufacture products in the destination countries, starting with Ecuador,

where it has a 45% stake in a joint venture. This will have several benefits:

1) Profit from sale of molds

2) Logistic cost savings.

3) Profit margin from sale of goods.

4 February 2015

Company Update: FPI

3

Please see disclaimer on last page

There are clients in other countries that have expressed interest in establishing joint

ventures similar to Ecuador. FPI sees the project in Ecuador as a pilot project since

it has never expanded manufacturing abroad. If it is successful, there will be a

significant number of other projects like it. The company also benefits from the fact

that Ecuador has free trade agreements with Columbia, Peru and Bolivia, so it can

use this Ecuadorian production base for all of these countries. FPI plans to establish

3-5 new production bases in five years.

Benefits from downtrend in fuel prices and recovery in global economy

A consequence of falling oil prices should be an increase in the use of vehicles,

which in turn should result in an increase in car maintenance and repairs leading to

demand for automotive parts, including those produced by FPI. In the longer term,

if the global economy recovers, it will encourage more demand.

Falling oil prices would not only benefit FPI on the demand side, it would also benefit

the company on the supply side. FPI’s raw materials consist of some plastics,

especially ABS (Acrylonitrile Butadiene Styrene) used to produce grilles and

headlight covers which are its key products (30% of total sales for 9M14). The price

of ABS is highly correlated to the price of oil, so the sharp drop in oil price will lead

to a lower cost ratio, meaning higher margin, which will improve the company’s

bottom line. FPI’s other key product, plastic bumpers, should not benefit as much

since the company uses off-grade polypropylene (PP) and it has a fixed price

agreement with its supplier. However, the margin on its bumpers should improve

from an increase in utilization leading to economy of scale.

First mover to niche markets

FPI loves to be the first to produce plastic automotive parts for new car models or

products that other players rarely provide, saying apparent excess demand in those

markets. How can FPI know? There is no need to invest heavily on marketing

research since FPI has key partners and sells its products in 134 countries

worldwide. The partners or clients will tell which type of goods are lacking in each

market and they want to import.

4 February 2015

Company Update: FPI

4

Please see disclaimer on last page

Re-emphasize advantages

A complete one-stop hypermarket for automotive businesses

Unlike traditional manufacturers, FPI not only produces its products, it also sells

trading goods and has 60,000-70,000 goods for customers to choose from. It can

be considered a complete one-stop hypermarket for auto-part downstream

businesses.

FPI has a strong network of suppliers with 500-600 auto-part manufacturer allies

since it has a director seat in the Thai Auto-Parts Manufacturers Association. Its

allies also benefit because they have better distribution channels, especially in the

global market where they have no experience. This connection allows FPI to have

more interesting goods on its shelves for its trading business.

Save on logistic costs and widen margin

Logistic costs are one of the key factors to enhance margin. FPI can save on logistic

costs (freight cost and other transportation-related costs) by operating its trading

business. Its logistic costs are primarily on a per-container basis and some of its

products (e.g. bumpers) are quite bulky, so their value per container is low, saying a

higher logistic cost as a percentage of sales. For example, if the logistic cost to some

countries is US$7,000, for bulky goods, the value of goods can amount to US$15,000

or 47% logistic cost. For other goods that are smaller but more expensive loading in

one container, the value per container can be as much as US$70,000 or down to

10%. Fortunately most foreign importers want a variety of goods rather than just one

product so all the space of a container can be utilized.

Focusing on higher margin business

FPI is positioning itself with brand and design aka “marketing firm”. It trades goods

under the name FPI. As customers believe in FPI’s brand and reputation which has

been built over many years, they feel comfortable in dealing with the company as a

one-stop contact point rather than taking the risk of dealing with each unfamiliar

manufacturer.

Provides one of the fastest deliveries in the world

The company’s lead time to delivery is only about 3 days, one of the fastest in the

world (40 days for China and 21-30 days for Taiwan and Malaysia) because of the

better storage capability from its spacious warehouses. This is why the company is

confident in its claim that it has the fastest average lead time.

4 February 2015

Company Update: FPI

5

Please see disclaimer on last page

Recommend BUY with 2015 target price of Bt6.10

We revalued FPI’s fair value to reflect the company’s current potential after par split.

Previously, the target price after par split without earnings adjustment was Bt3.675

(Bt14.70 before par split). The new target price is derived from an average total

return of 27% per year (25% CAGR of EPS during 2014-2016 and 2% annual

average dividend yield). Based on the PEG ratio, when we set the ratio at 1x, our

2015EPS estimate of Bt0.23 gives a 2015 target price of Bt6.10, which offers an

upside of 13.0% from the current share price.

4 February 2015

Company Update: FPI

6

Please see disclaimer on last page

Financial summary

Key Financial Ratios 2013 2014E 2015E 2016E

Sales Growth (%) 11.9% 7.8% 21.5% 13.0% Net Income Growth (%) 13.0% 28.8% 31.4% 14.9% EBITDA Margin (%) 7.9% 16.3% 19.2% 10.9% Net Profit Margin (%) 9.4% 11.3% 12.1% 12.2% Effective tax rate (%) 19.5% 20.0% 20.0% 20.0% ROA (%) 8.9% 10.3% 11.8% 12.1% ROE (%) 23.4% 24.4% 27.7% 27.4% Net Debt to Equity (x) 1.63 1.38 1.35 1.27 EPS (Bt) 0.55 0.17 0.23 0.26 BVPS (Bt) 0.61 0.73 0.74 0.79 DPS (Bt) 0.28 0.08 0.11 0.13 Net Dividend Payout Ratio 51.4% 45.0% 50.0% 50.0% P/E (x) 16.1 23.3 23.9 20.8 P/BV (x) 3.8 8.5 9.7 9.6 EV/EBITDA (x) 10.4 16.7 14.2 13.0 Div. Yield (%) 2.8% 1.4% 2.1% 2.4%

Income Statement

Unit: Btmn 2013 2014E 2015E 2016E

Sales 1,649 1,777 2,179 2,490 COGS 1,305 1,342 1,609 1,839 Gross Profit 344 435 570 651 SG&A 173 197 243 274 EBITDA 389 453 539 598 Tax 40 52 68 78 Interest Expenses 43 44 45 46 Net Income 164 207 272 313

EPS (Bt) 0.55 0.17 0.23 0.26

Balance Sheet

Unit: Btmn 2013 2014E 2015E 2016E

Cash 48 54 68 79 Account Receivable 528 586 669 756 Inventory 360 460 604 726 Total Current Assets 1,017 1,180 1,438 1,671 Net PP&E 752 783 809 847 Total Non-Current Assets 793 836 873 919 Total Assets 1,810 2,016 2,310 2,591

Short-Term Borrowings 618 622 691 732 Account Payable 258 284 345 390 Total Current Liabilities 1,011 1,058 1,215 1,324 Long-Term Borrowings 107 107 108 122 Total Non-Current Liabilities 111 110 112 127 Total Liabilities 1,122 1,169 1,327 1,451

Paid-up Capital 295 301 301 301 Capital Surplus 151 192 192 192 Retained Earnings 241 355 491 647 Total Equity 687 847 983 1,140

Total Liabilities and Equity 1,810 2,016 2,310 2,591

4 February 2015

CG Report

7

Please see disclaimer on last page

Corporate Governance Report of Thai Listed Companies (CGR). CG Rating by the Thai Institute of Directors Association (IOD) in 2013.

Corporate Governance Report disclaimer

The disclosure of the survey result of the Thai Institute of Directors

Association (“IOD”) regarding corporate governance is made pursuant

to the policy of the Office of the Securities and Exchange Commission.

The survey of the IOD is based on the information of a company listed

on the Stock Exchange of Thailand and the Market for Alternative

Investment disclosed to the public and able to be accessed by a

general public investor. The result, therefore, is from the perspective of

a third party. It is not an evaluation of operation and is not based on

inside information.

The survey result is as of the date appearing in the Corporate

Governance Report of Thai Listed Companies. As a result, the survey

result may be changed after that date, Asia wealth Securities Company

Limited does not conform nor certify the accuracy of such survey result.

Score Range Number of Logo Description

90 – 100

80 – 89

70 – 79

60 – 69

50 – 59

Below 50

No logo given

Excellent

Very Good

Good

Satisfactory

Pass

N/A

BAFS EGCO IRPC KTB PTTEP SAT SIM TOPBCP GRAMMY IVL MINT PTTGC SC SPALIBTS HANA KBANK PSL SAMART SCB TISCOCPN INTUCH KKP PTT SAMTEL SE-ED TMB

AAV BIGC DELTA HMPRO NBC PJW SAMCO SVI TOGACAP BKI DRT ICC NCH PM SCC TCAP TRCADVANC BLA DTAC KCE NINE PPS SINGER TF TRUEANAN BMCL DTC KSL NKI PR SIS THAI TSTEAOT BROOK EASTW LANNA NMG PRANDA SITHAI THANI TSTHASIMAR CENTEL EE LH NSI PS SNC THCOM TTAASK CFRESH ERW LHBANK OCC PT SNP TIP TTWASP CIMBT GBX LOXLEY OFM QH SPI TIPCO TVOBANPU CK GC LPN PAP RATCH SSF TK UACBAY CNT GFPT MACO PE ROBINS SSI TKT VGIBBL CPF GUNKUL MC PG RS SSSC TNITY VNTBECL CSL HEMRAJ MCOT PHOL S&J STA TNL WACOAL

2S BEAUTY CSS IHL MFEC PPM SKR TBSP TSC ZMICOAF BEC DCC INET MJD PPP SMG TEAM TSCAH BFIT DEMCO IRC MODERN PREB SMK TFD TTCLAHC BH DNA IRCP MONO PRG SMPC TFI TUFAIT BJC EA ITD MOONG PRIN SMT THANA TVDAJ BJCHI ESSO KBS MPG PTG SOLAR THIP TWFPAKP BOL FE KGI MTI QLT SPC THREL UMIAKR BTNC FORTH KKC NC QTC SPCG TIC UPAMANAH BWG FPI KTC NTV RCL SPPT TICON UPFAMARIN CCET GENCO L&E NUSA SABINA SST TIW UPOICAMATA CGD GL LRH NWR SALEE STANLY TKS UTAP CGS GLOBAL LST NYT SCBLIF STEC TLUXE UVAPCO CHOW GLOW MAJOR OGC SCCC STPI TMI UWCAPCS CI GOLD MAKRO OISHI SCG SUC TMT VIHAQUA CKP HOTPOT MATCH PACE SEAFCO SWC TNDT WAVEARIP CM HTC MBK PATO SEAOIL SYMC TPC WHAAS CMR HTECH MBKET PB SFP SYNEX TPCORP WINASIA CSC HYDRO MEGA PDI SIAM SYNTEC TRT WINNERAYUD CSP IFS MFC PICO SIRI TASCO TRU YUASA

Source: Thai Institute of Directors (IOD)

4 February 2015

Contact

8

Please see disclaimer on last page

This report has been prepared by Asia Wealth Securities Company Limited (“AWS”). The information herein has been obtained from sources believed to be reliable and accurate, but AWS makes no representation as to the accuracy and completeness of such information. AWS does not accept any liability for any loss or damage of any kind arising out of the use of such information or opinions in this report. Before making your own independent decision to invest or enter into transaction, investors should study this report carefully and should review information relating. All rights are reserved. This report may not be reproduced, distributed or published by any person in any manner for any purpose without permission of AWS. Investment in securities has risks. Investors are advised to consider carefully before making decisions.

Branch Address Phone Fax

Head Office 540 Floor 7,14,17 , Mercury Tower, Ploenchit Road, Lumphini,

Pathumwan Bangkok 10330

02-680-5000 02-680-5111

Silom 191 Silom Complex Building,21st Floor Room 2,3-1 Silom Rd.,

Silom, Bangrak, Bangkok, 10500 Thailand

02-630-3500 02-630-3530-1

Asok 159 Sermmitr Tower, 17th FL. Room No.1703, Sukhumvit 21

Road, Klong Toey Nua, Wattana, Bangkok 10110

02-261-1314-21 02-261-1328

Pinklao

7/3 Central Plaza Pinklao Office Building Tower B, 16th Flr., Room

No.1605-1606 Baromrajachonnanee Road, Arunamarin,

Bangkoknoi, Bangkok 10700

02-884-7333 02-884-7357,

02-884-7367

Chaengwattana

99/99 Moo 2 Central Plaza Chaengwattana Office Tower, 22nd Flr.,

Room 2204 Chaengwattana Road, Bang Talad, Pakkred,

Nonthaburi 11120

02-119-2300 02-8353014

Chaengwattana 2

9/99 Moo 2 Central Plaza Chaengwattana Office Tower, 22nd Flr.,

Room 2203 Chaengwattana Road, Bang Talad, Pakkred,

Nonthaburi 11120

02-119-2388 02-119-2399

Mega Bangna 39 Moo6 Megabangna, 1st Flr., Room 1632/7 Bangna-Trad Road,

Bangkaew Bangplee, Samutprakarn 10540

02-106-7345 02-105-2070

Rayong 356/18 Sukhumvit Road, Nuen-Phra Sub District, Muang District,

Rayong Province 21000

038-808200 038-807200

Khonkaen 26/9 Srijanmai Road, Tamboonnaimuang, Khon Khaen

40000

043-334-700 043-334-799

Chonburi 44 Vachiraprakarn Road, Bangplasoi, Muang Chonburi, Chonburi

20000

038-274-533 038-275-168

Chaseongsao 233-233/2 Moo2 1st Flr., Sukprayoon Road, Na Meung Sub-

District, Meung District, Chachoengsao 24000

038-981-587 038-981-591

![Investor Update [Company Update]](https://static.fdocuments.in/doc/165x107/577c7caa1a28abe0549b8763/investor-update-company-update-578043b3b5bc3.jpg)

![Earnings Update [Company Update]](https://static.fdocuments.in/doc/165x107/577c7f491a28abe054a3eab4/earnings-update-company-update.jpg)

![Performance Update [Company Update]](https://static.fdocuments.in/doc/165x107/577c7c411a28abe05499ee66/performance-update-company-update.jpg)