COCA-COLA AMATIL...31 COCA-COLA AMATIL CAbout Coca-Cola Amatil oca-Cola Amatil (CCA) is one of the...

19

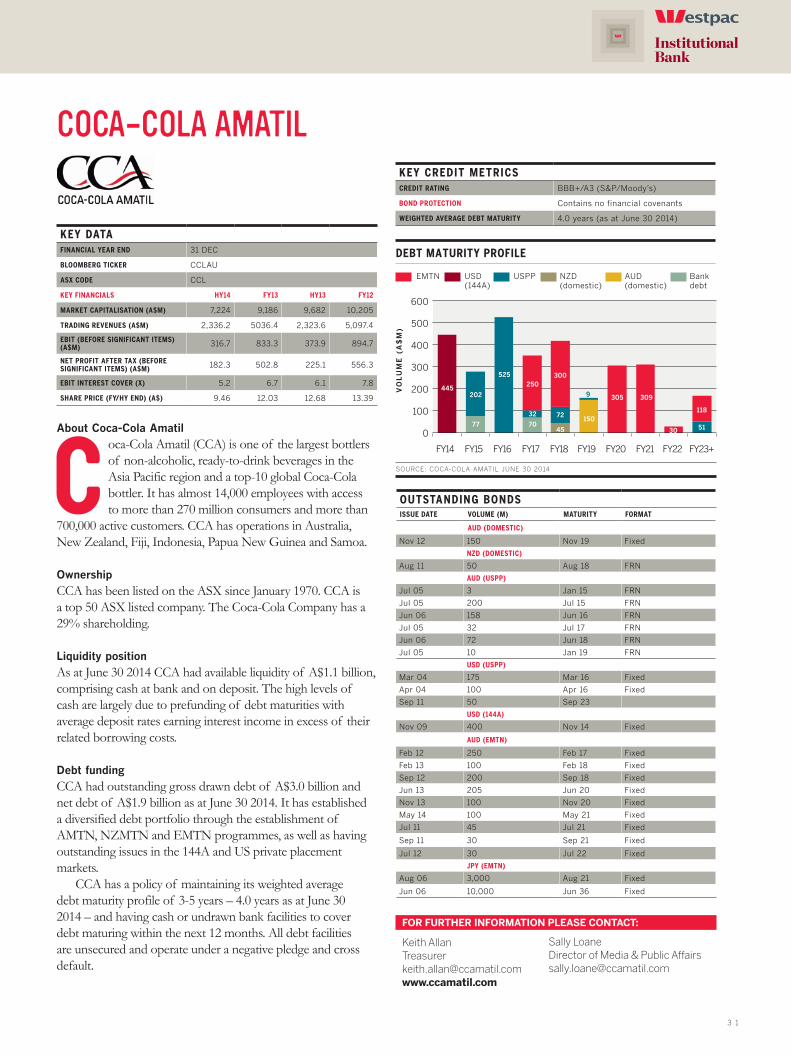

31 COCA-COLA AMATIL About Coca-Cola Amatil C oca-Cola Amatil (CCA) is one of the largest bottlers of non-alcoholic, ready-to-drink beverages in the Asia Pacific region and a top-10 global Coca-Cola bottler. It has almost 14,000 employees with access to more than 270 million consumers and more than 700,000 active customers. CCA has operations in Australia, New Zealand, Fiji, Indonesia, Papua New Guinea and Samoa. Ownership CCA has been listed on the ASX since January 1970. CCA is a top 50 ASX listed company. The Coca-Cola Company has a 29% shareholding. Liquidity position As at June 30 2014 CCA had available liquidity of A$1.1 billion, comprising cash at bank and on deposit. The high levels of cash are largely due to prefunding of debt maturities with average deposit rates earning interest income in excess of their related borrowing costs. Debt funding CCA had outstanding gross drawn debt of A$3.0 billion and net debt of A$1.9 billion as at June 30 2014. It has established a diversified debt portfolio through the establishment of AMTN, NZMTN and EMTN programmes, as well as having outstanding issues in the 144A and US private placement markets. CCA has a policy of maintaining its weighted average debt maturity profile of 3-5 years – 4.0 years as at June 30 2014 – and having cash or undrawn bank facilities to cover debt maturing within the next 12 months. All debt facilities are unsecured and operate under a negative pledge and cross default. FOR FURTHER INFORMATION PLEASE CONTACT: Keith Allan Treasurer [email protected] www.ccamatil.com KEY CREDIT METRICS CREDIT RATING BBB+/A3 (S&P/Moody’s) BOND PROTECTION Contains no financial covenants WEIGHTED AVERAGE DEBT MATURITY 4.0 years (as at June 30 2014) KEY DATA FINANCIAL YEAR END 31 DEC BLOOMBERG TICKER CCLAU ASX CODE CCL KEY FINANCIALS HY14 FY13 HY13 FY12 MARKET CAPITALISATION (A$M) 7,224 9,186 9,682 10,205 TRADING REVENUES (A$M) 2,336.2 5036.4 2,323.6 5,097.4 EBIT (BEFORE SIGNIFICANT ITEMS) (A$M) 316.7 833.3 373.9 894.7 NET PROFIT AFTER TAX (BEFORE SIGNIFICANT ITEMS) (A$M) 182.3 502.8 225.1 556.3 EBIT INTEREST COVER (X) 5.2 6.7 6.1 7.8 SHARE PRICE (FY/HY END) (A$) 9.46 12.03 12.68 13.39 OUTSTANDING BONDS ISSUE DATE VOLUME (M) MATURITY FORMAT AUD (DOMESTIC) Nov 12 150 Nov 19 Fixed NZD (DOMESTIC) Aug 11 50 Aug 18 FRN AUD (USPP) Jul 05 3 Jan 15 FRN Jul 05 200 Jul 15 FRN Jun 06 158 Jun 16 FRN Jul 05 32 Jul 17 FRN Jun 06 72 Jun 18 FRN Jul 05 10 Jan 19 FRN USD (USPP) Mar 04 175 Mar 16 Fixed Apr 04 100 Apr 16 Fixed Sep 11 50 Sep 23 USD (144A) Nov 09 400 Nov 14 Fixed AUD (EMTN) Feb 12 250 Feb 17 Fixed Feb 13 100 Feb 18 Fixed Sep 12 200 Sep 18 Fixed Jun 13 205 Jun 20 Fixed Nov 13 100 Nov 20 Fixed May 14 100 May 21 Fixed Jul 11 45 Jul 21 Fixed Sep 11 30 Sep 21 Fixed Jul 12 30 Jul 22 Fixed JPY (EMTN) Aug 06 3,000 Aug 21 Fixed Jun 06 10,000 Jun 36 Fixed SOURCE: COCA-COLA AMATIL JUNE 30 2014 Sally Loane Director of Media & Public Affairs [email protected] DEBT MATURITY PROFILE USPP EMTN USD (144A) NZD (domestic) AUD (domestic) Bank debt VOLUME (A$M) 600 500 400 300 200 100 0 FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23+ 150 445 202 525 250 32 300 72 9 305 309 118 51 77 70 45 30

Transcript of COCA-COLA AMATIL...31 COCA-COLA AMATIL CAbout Coca-Cola Amatil oca-Cola Amatil (CCA) is one of the...

3 1

COCA-COLA AMATIL

About Coca-Cola Amatil

C oca-Cola Amatil (CCA) is one of the largest bottlers of non-alcoholic, ready-to-drink beverages in the Asia Pacific region and a top-10 global Coca-Cola bottler. It has almost 14,000 employees with access to more than 270 million consumers and more than

700,000 active customers. CCA has operations in Australia, New Zealand, Fiji, Indonesia, Papua New Guinea and Samoa.

OwnershipCCA has been listed on the ASX since January 1970. CCA is a top 50 ASX listed company. The Coca-Cola Company has a 29% shareholding. Liquidity positionAs at June 30 2014 CCA had available liquidity of A$1.1 billion, comprising cash at bank and on deposit. The high levels of cash are largely due to prefunding of debt maturities with average deposit rates earning interest income in excess of their related borrowing costs.

Debt fundingCCA had outstanding gross drawn debt of A$3.0 billion and net debt of A$1.9 billion as at June 30 2014. It has established a diversified debt portfolio through the establishment of AMTN, NZMTN and EMTN programmes, as well as having outstanding issues in the 144A and US private placement markets.

CCA has a policy of maintaining its weighted average debt maturity profile of 3-5 years – 4.0 years as at June 30 2014 – and having cash or undrawn bank facilities to cover debt maturing within the next 12 months. All debt facilities are unsecured and operate under a negative pledge and cross default.

FOR FURTHER INFORMATION PLEASE CONTACT:

Keith AllanTreasurer [email protected]

KEY CREDIT METRICSCREDIT RATING BBB+/A3 (S&P/Moody’s)

BOND PROTECTION Contains no financial covenants

WEIGHTED AVERAGE DEBT MATURITY 4.0 years (as at June 30 2014)

KEY DATAFINANCIAL YEAR END 31 DEC

BLOOMBERG TICKER CCLAU

ASX CODE CCL

KEY FINANCIALS HY14 FY13 HY13 FY12

MARKET CAPITALISATION (A$M) 7,224 9,186 9,682 10,205

TRADING REVENUES (A$M) 2,336.2 5036.4 2,323.6 5,097.4

EBIT (BEFORE SIGNIFICANT ITEMS)(A$M) 316.7 833.3 373.9 894.7

NET PROFIT AFTER TAX (BEFORE SIGNIFICANT ITEMS) (A$M) 182.3 502.8 225.1 556.3

EBIT INTEREST COVER (X) 5.2 6.7 6.1 7.8

SHARE PRICE (FY/HY END) (A$) 9.46 12.03 12.68 13.39

OUTSTANDING BONDSISSUE DATE VOLUME (M) MATURITY FORMAT

AUD (DOMESTIC)

Nov 12 150 Nov 19 Fixed

NZD (DOMESTIC)

Aug 11 50 Aug 18 FRN

AUD (USPP)

Jul 05 3 Jan 15 FRN

Jul 05 200 Jul 15 FRN

Jun 06 158 Jun 16 FRN

Jul 05 32 Jul 17 FRN

Jun 06 72 Jun 18 FRN

Jul 05 10 Jan 19 FRN

USD (USPP)

Mar 04 175 Mar 16 Fixed

Apr 04 100 Apr 16 Fixed

Sep 11 50 Sep 23

USD (144A)

Nov 09 400 Nov 14 Fixed

AUD (EMTN)

Feb 12 250 Feb 17 Fixed

Feb 13 100 Feb 18 Fixed

Sep 12 200 Sep 18 Fixed

Jun 13 205 Jun 20 Fixed

Nov 13 100 Nov 20 Fixed

May 14 100 May 21 Fixed

Jul 11 45 Jul 21 Fixed

Sep 11 30 Sep 21 Fixed

Jul 12 30 Jul 22 Fixed

JPY (EMTN)

Aug 06 3,000 Aug 21 Fixed

Jun 06 10,000 Jun 36 Fixed

SOURCE: COCA-COLA AMATIL JUNE 30 2014

Sally LoaneDirector of Media & Public [email protected]

DEBT MATURITY PROFILE

USPPEMTN USD (144A)

NZD(domestic)

AUD(domestic)

Bankdebt

VO

LU

ME

(A

$M

)

600

500

400

300

200

100

0

FY14 FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22 FY23+

150

445202

525250

32

300

72

9 305 309

118

5177 7045 30

3 2 | A U S T R A L A S I A N C O R P O R A T E Y E A R B O O K : B R O U G H T T O Y O U B Y W E S T P A C I N S T I T U T I O N A L B A N K A N D K A N G A N E W S N O V E M B E R 2 0 1 4

ISSUERPROFILES

CONTACT ENERGY

About Contact Energy

C ontact Energy (Contact) is one of New Zealand’s leading electricity generators and energy retailers, providing electricity, natural gas and liquefied petroleum gas (LPG) to customers nationwide. Contact has around 22% of New Zealand’s retail

electricity market. Its diverse mix of power stations generate around a quarter of the country’s electricity from hydro, geothermal, gas and diesel. In addition, Contact has around 43% of the LPG market in New Zealand.

OwnershipContact is a public company, listed on the NZX as CEN since 1999. Contact is one of New Zealand’s largest listed companies. In 2004, Origin Energy (see p58) became Contact’s majority shareholder with a 51% stake. As at June 30 2014, Origin Energy’s stake was 53.1%.

Liquidity positionContact has NZ$600 million of committed bank facilities, of which NZ$377 million were undrawn at June 30 2014.

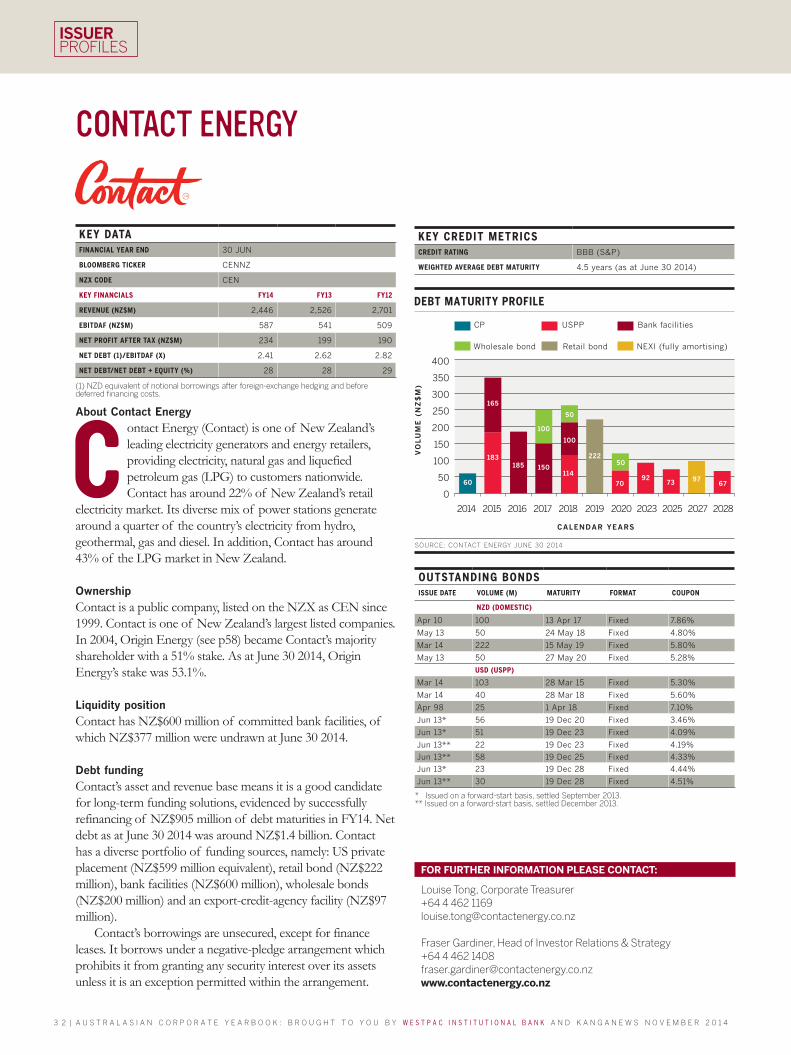

Debt fundingContact’s asset and revenue base means it is a good candidate for long-term funding solutions, evidenced by successfully refinancing of NZ$905 million of debt maturities in FY14. Net debt as at June 30 2014 was around NZ$1.4 billion. Contact has a diverse portfolio of funding sources, namely: US private placement (NZ$599 million equivalent), retail bond (NZ$222 million), bank facilities (NZ$600 million), wholesale bonds (NZ$200 million) and an export-credit-agency facility (NZ$97 million).

Contact’s borrowings are unsecured, except for finance leases. It borrows under a negative-pledge arrangement which prohibits it from granting any security interest over its assets unless it is an exception permitted within the arrangement.

FOR FURTHER INFORMATION PLEASE CONTACT:

Louise Tong, Corporate Treasurer+64 4 462 [email protected]

Fraser Gardiner, Head of Investor Relations & Strategy+64 4 462 [email protected]

KEY CREDIT METRICSCREDIT RATING BBB (S&P)

WEIGHTED AVERAGE DEBT MATURITY 4.5 years (as at June 30 2014)

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER CENNZ

NZX CODE CEN

KEY FINANCIALS FY14 FY13 FY12

REVENUE (NZ$M) 2,446 2,526 2,701

EBITDAF (NZ$M) 587 541 509

NET PROFIT AFTER TAX (NZ$M) 234 199 190

NET DEBT (1)/EBITDAF (X) 2.41 2.62 2.82

NET DEBT/NET DEBT + EQUITY (%) 28 28 29

(1) NZD equivalent of notional borrowings after foreign-exchange hedging and before deferred financing costs.

OUTSTANDING BONDSISSUE DATE VOLUME (M) MATURITY FORMAT COUPON

NZD (DOMESTIC)

Apr 10 100 13 Apr 17 Fixed 7.86%

May 13 50 24 May 18 Fixed 4.80%

Mar 14 222 15 May 19 Fixed 5.80%

May 13 50 27 May 20 Fixed 5.28%

USD (USPP)

Mar 14 103 28 Mar 15 Fixed 5.30%

Mar 14 40 28 Mar 18 Fixed 5.60%

Apr 98 25 1 Apr 18 Fixed 7.10%

Jun 13* 56 19 Dec 20 Fixed 3.46%

Jun 13* 51 19 Dec 23 Fixed 4.09%

Jun 13** 22 19 Dec 23 Fixed 4.19%

Jun 13** 58 19 Dec 25 Fixed 4.33%

Jun 13* 23 19 Dec 28 Fixed 4.44%

Jun 13** 30 19 Dec 28 Fixed 4.51%

* Issued on a forward-start basis, settled September 2013.** Issued on a forward-start basis, settled December 2013.

DEBT MATURITY PROFILE

CP USPP Bank facilities

Retail bondWholesale bond

VO

LU

ME

(N

Z$

M)

400

350

300

250

200

150

100

50

0

2014 2015 2016 2017 20252020 20282018 2019 20272023

SOURCE: CONTACT ENERGY JUNE 30 2014

92

183150

165

100

185114

222

100

50

70

50

73 9767

NEXI (fully amortising)

CALENDAR YEARS

60

3 3

DBP

About DBP

D BP is the trading name of the privately owned group of entities which owns and operates the Dampier to Bunbury Natural Gas Pipeline (DBNGP) – the key gas-transmission pipeline in Western Australia (WA). The 1,530-kilometre mainline connects the extensive

offshore North West Shelf gas fields from Dampier with the population centres and industry in the south-west of the state through to Bunbury.

DBP’s core business is the operation, maintenance and expansion of the pipeline. Most revenue is derived through long-term contracted capacity of the pipeline to various large and dominant industrial and retail end users in WA.

The pipeline was commissioned in 1985 and has an estimated remaining economic life of at least 50 years. The asset has a strong safety and performance track record and the series of expansion projects under the ownership of DBP has ensured that the pipeline’s capacity remains aligned with the gas needs of the state of WA. The owners’ commitment to meeting the needs of customers in WA is ongoing.

DBP is required to operate the pipeline under an access arrangement approved by the Economic Regulatory Authority (ERA) of WA. The ERA is WA’s independent economic regulator. The access arrangement sets out the basis for accessing spare uncontracted capacity on the pipeline, including the terms and conditions of such access. To date, DBP has only expanded capacity on the DBNGP to meet contracted demand. Due to a recontracting with many of the DBNGP shippers announced on August 7 2014, 85% of the DBNGP full-haul capacity will be subject to long-term revenue streams outside of the ERA-determined regulatory tariff (out to December 31 2020).

OwnershipDBP’s shareholders are DUET Group (80%) and Alcoa of Australia (Alcoa) (20%). DUET Group is an ASX-listed owner

FOR FURTHER INFORMATION PLEASE CONTACT:

Michael Allan, Chief Financial Officer+61 8 9223 [email protected]

of energy utility assets in Australia. Alcoa operates the largest integrated bauxite mining and alumina refining operations in the world, comprising two bauxite mines and three alumina refineries in WA. The gas used to support these operations makes Alcoa the biggest single user of pipeline capacity on the DBNGP.

Liquidity positionDBP has stable and predictable operating cash flows that involve long-dated shipper contracts with creditworthy counterparties. As of June 30 2014, DBP had in place a A$20 million working-capital facility, A$28 million in cash at hand and A$35 million undrawn capacity in syndicated-debt facilities.

Debt fundingDBP’s finance arm is DBNGP Finance. In 2010, DBNGP Finance issued A$575 million of five-year domestic MTNs – its first-ever bond to come without a credit wrap, and a landmark domestic transaction for a triple-B minus credit. Subsequently, in November 2012 DBNGP Finance issued A$300 million of seven-year domestic MTNs.

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER DUEAU

ASX CODE NOT LISTED

KEY FINANCIALS FY14 FY13 FY12

REVENUES (A$M) 428.8 449.1 457.2

EBITDA (A$M) 349.2 369.2 365.8

NET PROFIT AFTER TAX (A$M) 33.1 55.6 39.2

DEBT/EBITDA (X) (SENIOR) 7.25 6.84 6.88

NET DEBT/NET DEBT + EQUITY (%) 67.7 68.0 68.1

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPON (% OR BPs)

MARGIN AT ISSUE DATE (BPs)

AUD (DOMESTIC)

22 Sep 10 150 29 Sep 15 Fixed 8.25% 300/swap

22 Sep 10 425 29 Sep 15 FRN 300/BBSW 300/BBSW

12 Apr 05 275 25 Apr 17 FRN* 38/BBSW 38/BBSW

26 Apr 06 325 26 Apr 18 FRN* 26/BBSW 26/BBSW

8 Nov 12 300 11 Oct 19 Fixed 6.00% 270/swap

* Credit-wrapped.

KEY CREDIT METRICSCREDIT RATING BBB-/Baa3 (S&P/Moody’s)

3 4 | A U S T R A L A S I A N C O R P O R A T E Y E A R B O O K : B R O U G H T T O Y O U B Y W E S T P A C I N S T I T U T I O N A L B A N K A N D K A N G A N E W S N O V E M B E R 2 0 1 4

ISSUERPROFILES

DEXUS PROPERTY GROUP

About DEXUS Property Group

D EXUS Property Group (DEXUS) is one of Australia’s leading real-estate groups, investing directly in high-quality Australian office and industrial properties. With over A$17.8 billion of funds under management, DEXUS also actively manages office,

industrial and retail properties located in key Australian markets on behalf of third-party capital partners. With more than 30 years of expertise in property investment, development and asset management, DEXUS has a proven track record in capital and risk management, providing service excellence to tenants and delivering superior risk-adjusted returns for investors.

OwnershipDEXUS is a top-50 entity by market capitalisation (A$6.0 billion as at June 30 2014) listed on the ASX under the stock market trading code DXS. It is supported by more than 32,000 investors from 20 countries.

Liquidity positionDEXUS targets earnings composition of 80-90% from core portfolio income, providing stable cash flows, and is focused on efficient management of working capital and cash. At June 30 2014, DEXUS had surplus liquidity of approximately A$500 million, consisting of undrawn committed facilities and cash. In addition to managing liquidity through a range of debt facilities, DEXUS maintains a distribution payout in line with free cash flow.

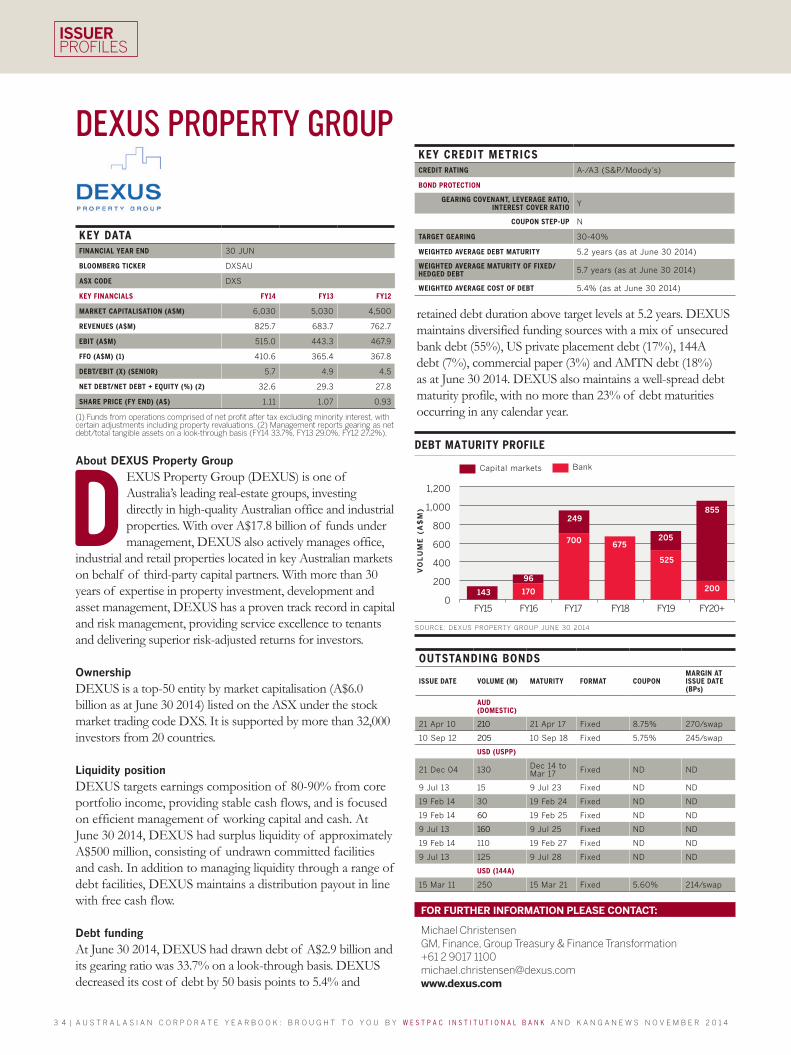

Debt fundingAt June 30 2014, DEXUS had drawn debt of A$2.9 billion and its gearing ratio was 33.7% on a look-through basis. DEXUS decreased its cost of debt by 50 basis points to 5.4% and

FOR FURTHER INFORMATION PLEASE CONTACT:

Michael ChristensenGM, Finance, Group Treasury & Finance Transformation+61 2 9017 [email protected]

KEY CREDIT METRICSCREDIT RATING A-/A3 (S&P/Moody’s)

BOND PROTECTION

GEARING COVENANT, LEVERAGE RATIO, INTEREST COVER RATIO Y

COUPON STEP-UP N

TARGET GEARING 30-40%

WEIGHTED AVERAGE DEBT MATURITY 5.2 years (as at June 30 2014)

WEIGHTED AVERAGE MATURITY OF FIXED/HEDGED DEBT 5.7 years (as at June 30 2014)

WEIGHTED AVERAGE COST OF DEBT 5.4% (as at June 30 2014)

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER DXSAU

ASX CODE DXS

KEY FINANCIALS FY14 FY13 FY12

MARKET CAPITALISATION (A$M) 6,030 5,030 4,500

REVENUES (A$M) 825.7 683.7 762.7

EBIT (A$M) 515.0 443.3 467.9

FFO (A$M) (1) 410.6 365.4 367.8

DEBT/EBIT (X) (SENIOR) 5.7 4.9 4.5

NET DEBT/NET DEBT + EQUITY (%) (2) 32.6 29.3 27.8

SHARE PRICE (FY END) (A$) 1.11 1.07 0.93

(1) Funds from operations comprised of net profit after tax excluding minority interest, with certain adjustments including property revaluations. (2) Management reports gearing as net debt/total tangible assets on a look-through basis (FY14 33.7%, FY13 29.0%, FY12 27.2%).

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPONMARGIN AT ISSUE DATE (BPs)

AUD (DOMESTIC)

21 Apr 10 210 21 Apr 17 Fixed 8.75% 270/swap

10 Sep 12 205 10 Sep 18 Fixed 5.75% 245/swap

USD (USPP)

21 Dec 04 130 Dec 14 to Mar 17 Fixed ND ND

9 Jul 13 15 9 Jul 23 Fixed ND ND

19 Feb 14 30 19 Feb 24 Fixed ND ND

19 Feb 14 60 19 Feb 25 Fixed ND ND

9 Jul 13 160 9 Jul 25 Fixed ND ND

19 Feb 14 110 19 Feb 27 Fixed ND ND

9 Jul 13 125 9 Jul 28 Fixed ND ND

USD (144A)

15 Mar 11 250 15 Mar 21 Fixed 5.60% 214/swap

retained debt duration above target levels at 5.2 years. DEXUS maintains diversified funding sources with a mix of unsecured bank debt (55%), US private placement debt (17%), 144A debt (7%), commercial paper (3%) and AMTN debt (18%) as at June 30 2014. DEXUS also maintains a well-spread debt maturity profile, with no more than 23% of debt maturities occurring in any calendar year.

DEBT MATURITY PROFILE

Capital markets Bank

SOURCE: DEXUS PROPERTY GROUP JUNE 30 2014

VO

LU

ME

(A

$M

)

1,200

1,000

800

600

400

200

0FY15 FY16 FY17 FY18 FY19

170

249855

700

525

200

675

FY20+

205

96

143

3 5

DEXUS WHOLESALE PROPERTY FUND

About DEXUS Wholesale Property Fund

D EXUS Wholesale Property Fund (DWPF) is a A$5 billion, open-ended unlisted property fund which owns interests in a diversified portfolio of office, industrial and retail properties throughout Australia.

The fund’s focus is to drive performance and deliver its investment plan, as well as to improve portfolio quality through strategic acquisitions and the ability to access its development pipeline. DWPF has a strong track record of superior performance through consistent long-term benchmark outperformance.

OwnershipDWPF was established as a wholesale fund in 1995. The responsible entity is DEXUS Wholesale Property Limited, a wholly owned subsidiary of DEXUS Property Group (DEXUS) (see facing page). DEXUS is one of Australia’s leading real-estate groups, with more than A$17.8 billion of funds under management.

Liquidity positionAt June 30 2014, DWPF had surplus liquidity of approximately A$240 million, with a A$100 million MTN settling post balance date and a further A$225 million of forward-start bank facilities to become available over the next 12 months. These facilities and the fund’s distribution reinvestment plan provide a strong liquidity position to fund existing development and fund-through commitments.

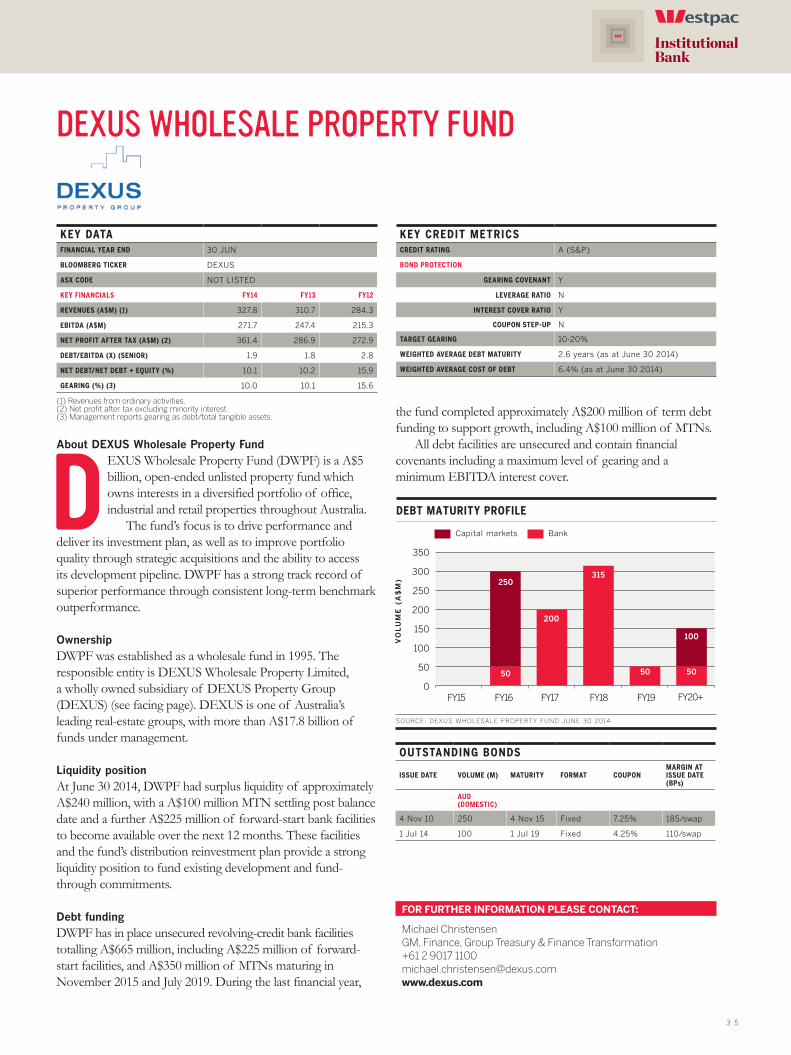

Debt fundingDWPF has in place unsecured revolving-credit bank facilities totalling A$665 million, including A$225 million of forward-start facilities, and A$350 million of MTNs maturing in November 2015 and July 2019. During the last financial year,

FOR FURTHER INFORMATION PLEASE CONTACT:

Michael ChristensenGM, Finance, Group Treasury & Finance Transformation+61 2 9017 [email protected]

the fund completed approximately A$200 million of term debt funding to support growth, including A$100 million of MTNs.

All debt facilities are unsecured and contain financial covenants including a maximum level of gearing and a minimum EBITDA interest cover.

KEY CREDIT METRICSCREDIT RATING A (S&P)

BOND PROTECTION

GEARING COVENANT Y

LEVERAGE RATIO N

INTEREST COVER RATIO Y

COUPON STEP-UP N

TARGET GEARING 10-20%

WEIGHTED AVERAGE DEBT MATURITY 2.6 years (as at June 30 2014)

WEIGHTED AVERAGE COST OF DEBT 6.4% (as at June 30 2014)

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER DEXUS

ASX CODE NOT LISTED

KEY FINANCIALS FY14 FY13 FY12

REVENUES (A$M) (1) 327.8 310.7 284.3

EBITDA (A$M) 271.7 247.4 215.3

NET PROFIT AFTER TAX (A$M) (2) 361.4 286.9 272.9

DEBT/EBITDA (X) (SENIOR) 1.9 1.8 2.8

NET DEBT/NET DEBT + EQUITY (%) 10.1 10.2 15.9

GEARING (%) (3) 10.0 10.1 15.6

(1) Revenues from ordinary activities.(2) Net profit after tax excluding minority interest.(3) Management reports gearing as debt/total tangible assets.

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPONMARGIN AT ISSUE DATE (BPs)

AUD (DOMESTIC)

4 Nov 10 250 4 Nov 15 Fixed 7.25% 185/swap

1 Jul 14 100 1 Jul 19 Fixed 4.25% 110/swap

DEBT MATURITY PROFILE

VO

LU

ME

(A

$M

)

350

300

250

200

150

100

50

0

SOURCE: DEXUS WHOLESALE PROPERTY FUND JUNE 30 2014

FY15 FY16 FY17 FY18 FY19 FY20+

Capital markets Bank

200

50

315

100

50

250

50

3 6 | A U S T R A L A S I A N C O R P O R A T E Y E A R B O O K : B R O U G H T T O Y O U B Y W E S T P A C I N S T I T U T I O N A L B A N K A N D K A N G A N E W S N O V E M B E R 2 0 1 4

ISSUERPROFILES

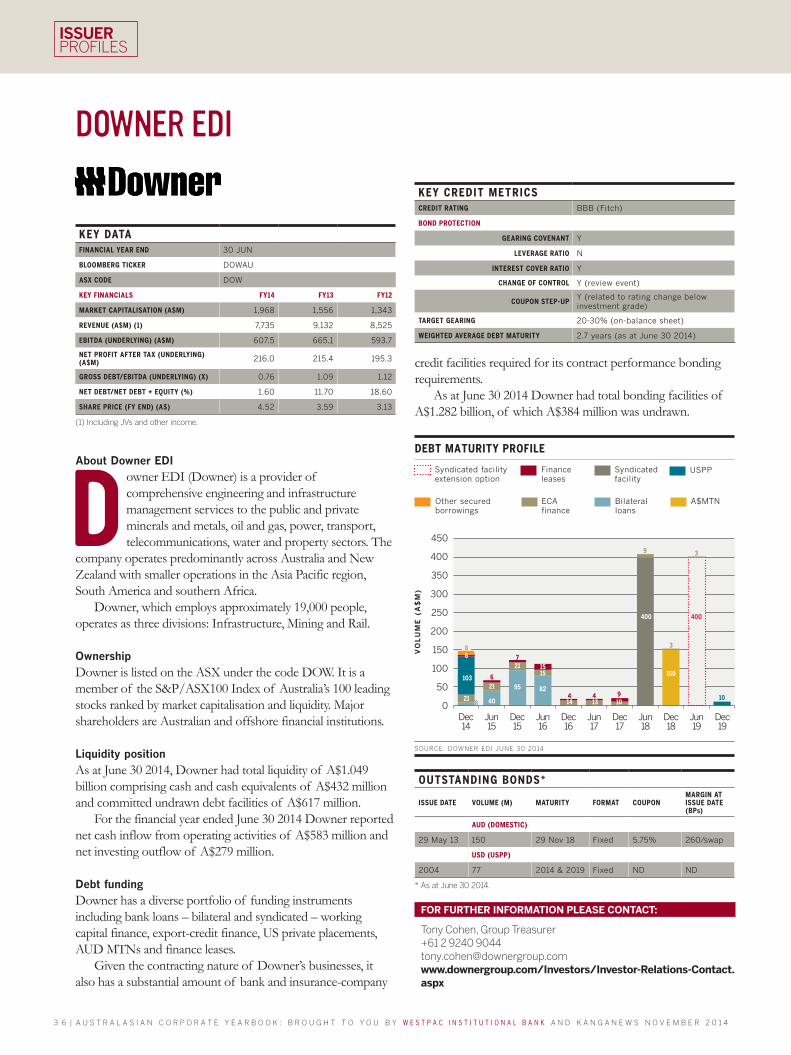

DOWNER EDI

FOR FURTHER INFORMATION PLEASE CONTACT:

Tony Cohen, Group Treasurer +61 2 9240 9044 [email protected]/Investors/Investor-Relations-Contact.aspx

About Downer EDI

D owner EDI (Downer) is a provider of comprehensive engineering and infrastructure management services to the public and private minerals and metals, oil and gas, power, transport, telecommunications, water and property sectors. The

company operates predominantly across Australia and New Zealand with smaller operations in the Asia Pacific region, South America and southern Africa.

Downer, which employs approximately 19,000 people, operates as three divisions: Infrastructure, Mining and Rail.

OwnershipDowner is listed on the ASX under the code DOW. It is a member of the S&P/ASX100 Index of Australia’s 100 leading stocks ranked by market capitalisation and liquidity. Major shareholders are Australian and offshore financial institutions.

Liquidity positionAs at June 30 2014, Downer had total liquidity of A$1.049 billion comprising cash and cash equivalents of A$432 million and committed undrawn debt facilities of A$617 million.

For the financial year ended June 30 2014 Downer reported net cash inflow from operating activities of A$583 million and net investing outflow of A$279 million.

Debt fundingDowner has a diverse portfolio of funding instruments including bank loans – bilateral and syndicated – working capital finance, export-credit finance, US private placements, AUD MTNs and finance leases.

Given the contracting nature of Downer’s businesses, it also has a substantial amount of bank and insurance-company

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER DOWAU

ASX CODE DOW

KEY FINANCIALS FY14 FY13 FY12

MARKET CAPITALISATION (A$M) 1,968 1,556 1,343

REVENUE (A$M) (1) 7,735 9,132 8,525

EBITDA (UNDERLYING) (A$M) 607.5 665.1 593.7

NET PROFIT AFTER TAX (UNDERLYING) (A$M) 216.0 215.4 195.3

GROSS DEBT/EBITDA (UNDERLYING) (X) 0.76 1.09 1.12

NET DEBT/NET DEBT + EQUITY (%) 1.60 11.70 18.60

SHARE PRICE (FY END) (A$) 4.52 3.59 3.13

(1) Including JVs and other income.

OUTSTANDING BONDS*

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPONMARGIN AT ISSUE DATE (BPs)

AUD (DOMESTIC)

29 May 13 150 29 Nov 18 Fixed 5.75% 260/swap

USD (USPP)

2004 77 2014 & 2019 Fixed ND ND

* As at June 30 2014.

KEY CREDIT METRICSCREDIT RATING BBB (Fitch)

BOND PROTECTION

GEARING COVENANT Y

LEVERAGE RATIO N

INTEREST COVER RATIO Y

CHANGE OF CONTROL Y (review event)

COUPON STEP-UPY (related to rating change below investment grade)

TARGET GEARING 20-30% (on-balance sheet)

WEIGHTED AVERAGE DEBT MATURITY 2.7 years (as at June 30 2014)

credit facilities required for its contract performance bonding requirements.

As at June 30 2014 Downer had total bonding facilities of A$1.282 billion, of which A$384 million was undrawn.

DEBT MATURITY PROFILE

Syndicated facility extension option

Finance leases

Syndicated facility

USPP

Other secured borrowings

A$MTN ECA finance

Bilateral loans

VO

LU

ME

(A

$M

)

450

400

350

300

250

200

150

100

50

0Dec 14

Jun 15

Dec 15

Jun 16

Dec 16

Jun 17

Dec 17

Jun 18

Dec 18

Jun 19

Dec 19

SOURCE: DOWNER EDI JUNE 30 2014

86

6

7

4 4 9

103

21 40

21

21

95

1515

82

14 13 10

150

3

10

400 400

3

8

9

3 7

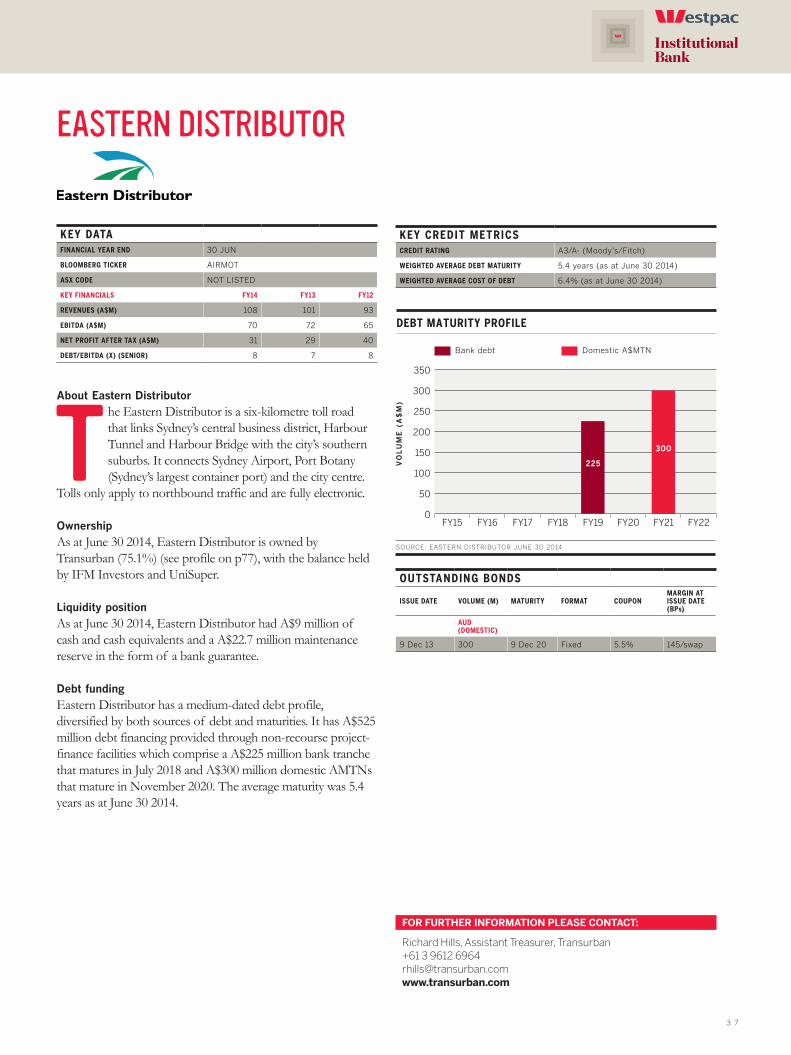

EASTERN DISTRIBUTOR

About Eastern Distributor

T he Eastern Distributor is a six-kilometre toll road that links Sydney’s central business district, Harbour Tunnel and Harbour Bridge with the city’s southern suburbs. It connects Sydney Airport, Port Botany (Sydney’s largest container port) and the city centre.

Tolls only apply to northbound traffic and are fully electronic.

OwnershipAs at June 30 2014, Eastern Distributor is owned by Transurban (75.1%) (see profile on p77), with the balance held by IFM Investors and UniSuper. Liquidity positionAs at June 30 2014, Eastern Distributor had A$9 million of cash and cash equivalents and a A$22.7 million maintenance reserve in the form of a bank guarantee.

Debt fundingEastern Distributor has a medium-dated debt profile, diversified by both sources of debt and maturities. It has A$525 million debt financing provided through non-recourse project-finance facilities which comprise a A$225 million bank tranche that matures in July 2018 and A$300 million domestic AMTNs that mature in November 2020. The average maturity was 5.4 years as at June 30 2014.

FOR FURTHER INFORMATION PLEASE CONTACT:

Richard Hills, Assistant Treasurer, Transurban+61 3 9612 [email protected]

KEY CREDIT METRICSCREDIT RATING A3/A- (Moody’s/Fitch)

WEIGHTED AVERAGE DEBT MATURITY 5.4 years (as at June 30 2014)

WEIGHTED AVERAGE COST OF DEBT 6.4% (as at June 30 2014)

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER AIRMOT

ASX CODE NOT LISTED

KEY FINANCIALS FY14 FY13 FY12

REVENUES (A$M) 108 101 93

EBITDA (A$M) 70 72 65

NET PROFIT AFTER TAX (A$M) 31 29 40

DEBT/EBITDA (X) (SENIOR) 8 7 8

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPONMARGIN AT ISSUE DATE (BPs)

AUD (DOMESTIC)

9 Dec 13 300 9 Dec 20 Fixed 5.5% 145/swap

DEBT MATURITY PROFILE

VO

LU

ME

(A

$M

)

350

300

250

200

150

100

50

0

SOURCE: EASTERN DISTRIBUTOR JUNE 30 2014

FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22

300

225

Bank debt Domestic A$MTN

3 8 | A U S T R A L A S I A N C O R P O R A T E Y E A R B O O K : B R O U G H T T O Y O U B Y W E S T P A C I N S T I T U T I O N A L B A N K A N D K A N G A N E W S N O V E M B E R 2 0 1 4

ISSUERPROFILES

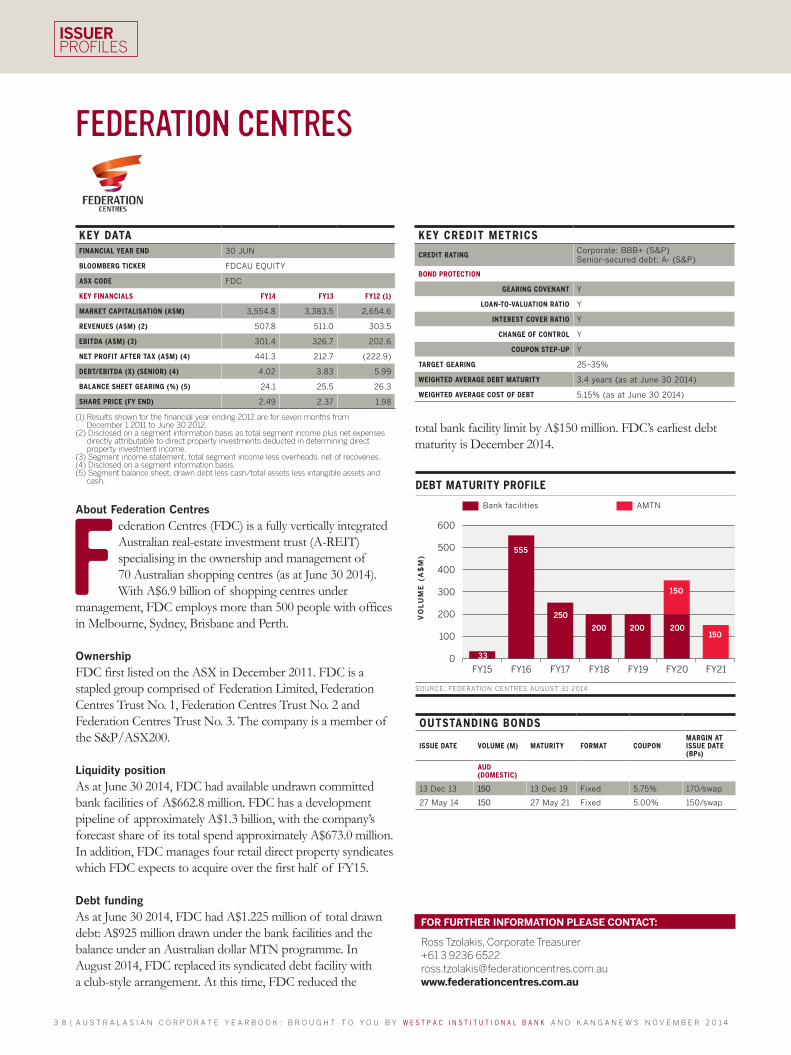

FEDERATION CENTRES

About Federation Centres

F ederation Centres (FDC) is a fully vertically integrated Australian real-estate investment trust (A-REIT) specialising in the ownership and management of 70 Australian shopping centres (as at June 30 2014). With A$6.9 billion of shopping centres under

management, FDC employs more than 500 people with offices in Melbourne, Sydney, Brisbane and Perth.

OwnershipFDC first listed on the ASX in December 2011. FDC is a stapled group comprised of Federation Limited, Federation Centres Trust No. 1, Federation Centres Trust No. 2 and Federation Centres Trust No. 3. The company is a member of the S&P/ASX200.

Liquidity positionAs at June 30 2014, FDC had available undrawn committed bank facilities of A$662.8 million. FDC has a development pipeline of approximately A$1.3 billion, with the company’s forecast share of its total spend approximately A$673.0 million. In addition, FDC manages four retail direct property syndicates which FDC expects to acquire over the first half of FY15.

Debt fundingAs at June 30 2014, FDC had A$1.225 million of total drawn debt: A$925 million drawn under the bank facilities and the balance under an Australian dollar MTN programme. In August 2014, FDC replaced its syndicated debt facility with a club-style arrangement. At this time, FDC reduced the

FOR FURTHER INFORMATION PLEASE CONTACT:

Ross Tzolakis, Corporate Treasurer+61 3 9236 6522ross.tzolakis@federationcentres.com.auwww.federationcentres.com.au

KEY CREDIT METRICS

CREDIT RATINGCorporate: BBB+ (S&P) Senior-secured debt: A- (S&P)

BOND PROTECTION

GEARING COVENANT Y

LOAN-TO-VALUATION RATIO Y

INTEREST COVER RATIO Y

CHANGE OF CONTROL Y

COUPON STEP-UP Y

TARGET GEARING 25–35%

WEIGHTED AVERAGE DEBT MATURITY 3.4 years (as at June 30 2014)

WEIGHTED AVERAGE COST OF DEBT 5.15% (as at June 30 2014)

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER FDCAU EQUITY

ASX CODE FDC

KEY FINANCIALS FY14 FY13 FY12 (1)

MARKET CAPITALISATION (A$M) 3,554.8 3,383.5 2,654.6

REVENUES (A$M) (2) 507.8 511.0 303.5

EBITDA (A$M) (3) 301.4 326.7 202.6

NET PROFIT AFTER TAX (A$M) (4) 441.3 212.7 (222.9)

DEBT/EBITDA (X) (SENIOR) (4) 4.02 3.83 5.99

BALANCE SHEET GEARING (%) (5) 24.1 25.5 26.3

SHARE PRICE (FY END) 2.49 2.37 1.98

(1) Results shown for the financial year ending 2012 are for seven months from December 1 2011 to June 30 2012.

(2) Disclosed on a segment information basis as total segment income plus net expenses directly attributable to direct property investments deducted in determining direct property investment income.

(3) Segment income statement, total segment income less overheads, net of recoveries. (4) Disclosed on a segment information basis.(5) Segment balance sheet, drawn debt less cash/total assets less intangible assets and

cash. DEBT MATURITY PROFILE

VO

LU

ME

(A

$M

)

600

500

400

300

200

100

0

SOURCE: FEDERATION CENTRES AUGUST 31 2014

Bank facilities AMTN

250

555

150

FY15 FY16 FY17 FY18 FY19 FY20 FY21

150200 200 200

33

total bank facility limit by A$150 million. FDC’s earliest debt maturity is December 2014.

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPONMARGIN AT ISSUE DATE (BPs)

AUD (DOMESTIC)

13 Dec 13 150 13 Dec 19 Fixed 5.75% 170/swap

27 May 14 150 27 May 21 Fixed 5.00% 150/swap

3 9

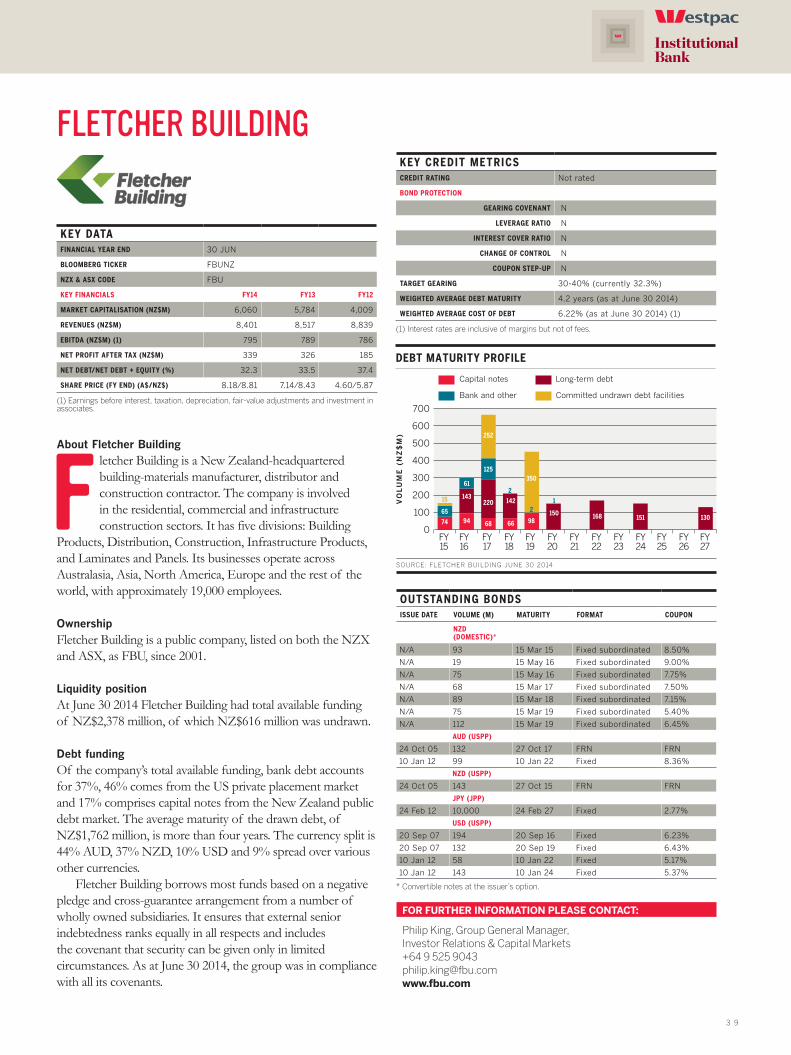

FLETCHER BUILDING

About Fletcher Building

F letcher Building is a New Zealand-headquartered building-materials manufacturer, distributor and construction contractor. The company is involved in the residential, commercial and infrastructure construction sectors. It has five divisions: Building

Products, Distribution, Construction, Infrastructure Products, and Laminates and Panels. Its businesses operate across Australasia, Asia, North America, Europe and the rest of the world, with approximately 19,000 employees.

OwnershipFletcher Building is a public company, listed on both the NZX and ASX, as FBU, since 2001.

Liquidity positionAt June 30 2014 Fletcher Building had total available funding of NZ$2,378 million, of which NZ$616 million was undrawn.

Debt fundingOf the company’s total available funding, bank debt accounts for 37%, 46% comes from the US private placement market and 17% comprises capital notes from the New Zealand public debt market. The average maturity of the drawn debt, of NZ$1,762 million, is more than four years. The currency split is 44% AUD, 37% NZD, 10% USD and 9% spread over various other currencies.

Fletcher Building borrows most funds based on a negative pledge and cross-guarantee arrangement from a number of wholly owned subsidiaries. It ensures that external senior indebtedness ranks equally in all respects and includes the covenant that security can be given only in limited circumstances. As at June 30 2014, the group was in compliance with all its covenants.

FOR FURTHER INFORMATION PLEASE CONTACT:

Philip King, Group General Manager, Investor Relations & Capital Markets+64 9 525 [email protected]

KEY CREDIT METRICSCREDIT RATING Not rated

BOND PROTECTION

GEARING COVENANT N

LEVERAGE RATIO N

INTEREST COVER RATIO N

CHANGE OF CONTROL N

COUPON STEP-UP N

TARGET GEARING 30-40% (currently 32.3%)

WEIGHTED AVERAGE DEBT MATURITY 4.2 years (as at June 30 2014)

WEIGHTED AVERAGE COST OF DEBT 6.22% (as at June 30 2014) (1)

(1) Interest rates are inclusive of margins but not of fees.

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER FBUNZ

NZX & ASX CODE FBU

KEY FINANCIALS FY14 FY13 FY12

MARKET CAPITALISATION (NZ$M) 6,060 5,784 4,009

REVENUES (NZ$M) 8,401 8,517 8,839

EBITDA (NZ$M) (1) 795 789 786

NET PROFIT AFTER TAX (NZ$M) 339 326 185

NET DEBT/NET DEBT + EQUITY (%) 32.3 33.5 37.4

SHARE PRICE (FY END) (A$/NZ$) 8.18/8.81 7.14/8.43 4.60/5.87

(1) Earnings before interest, taxation, depreciation, fair-value adjustments and investment in associates.

OUTSTANDING BONDSISSUE DATE VOLUME (M) MATURITY FORMAT COUPON

NZD (DOMESTIC)*

N/A 93 15 Mar 15 Fixed subordinated 8.50%

N/A 19 15 May 16 Fixed subordinated 9.00%

N/A 75 15 May 16 Fixed subordinated 7.75%

N/A 68 15 Mar 17 Fixed subordinated 7.50%

N/A 89 15 Mar 18 Fixed subordinated 7.15%

N/A 75 15 Mar 19 Fixed subordinated 5.40%

N/A 112 15 Mar 19 Fixed subordinated 6.45%

AUD (USPP)

24 Oct 05 132 27 Oct 17 FRN FRN

10 Jan 12 99 10 Jan 22 Fixed 8.36%

NZD (USPP)

24 Oct 05 143 27 Oct 15 FRN FRN

JPY (JPP)

24 Feb 12 10,000 24 Feb 27 Fixed 2.77%

USD (USPP)

20 Sep 07 194 20 Sep 16 Fixed 6.23%

20 Sep 07 132 20 Sep 19 Fixed 6.43%

10 Jan 12 58 10 Jan 22 Fixed 5.17%

10 Jan 12 143 10 Jan 24 Fixed 5.37%

* Convertible notes at the issuer’s option.

DEBT MATURITY PROFILE

Capital notes Long-term debt

VO

LU

ME

(N

Z$

M)

700

600

500

400

300

200

100

0

SOURCE: FLETCHER BUILDING JUNE 30 2014

Bank and other Committed undrawn debt facilities

65

61

252

6674

15

94

143142

150 168 151 130

220

125350

9868

2

2

FY15

FY16

FY17

FY18

FY19

FY20

FY21

FY22

FY23

FY24

FY25

FY26

FY27

1

4 0 | A U S T R A L A S I A N C O R P O R A T E Y E A R B O O K : B R O U G H T T O Y O U B Y W E S T P A C I N S T I T U T I O N A L B A N K A N D K A N G A N E W S N O V E M B E R 2 0 1 4

ISSUERPROFILES

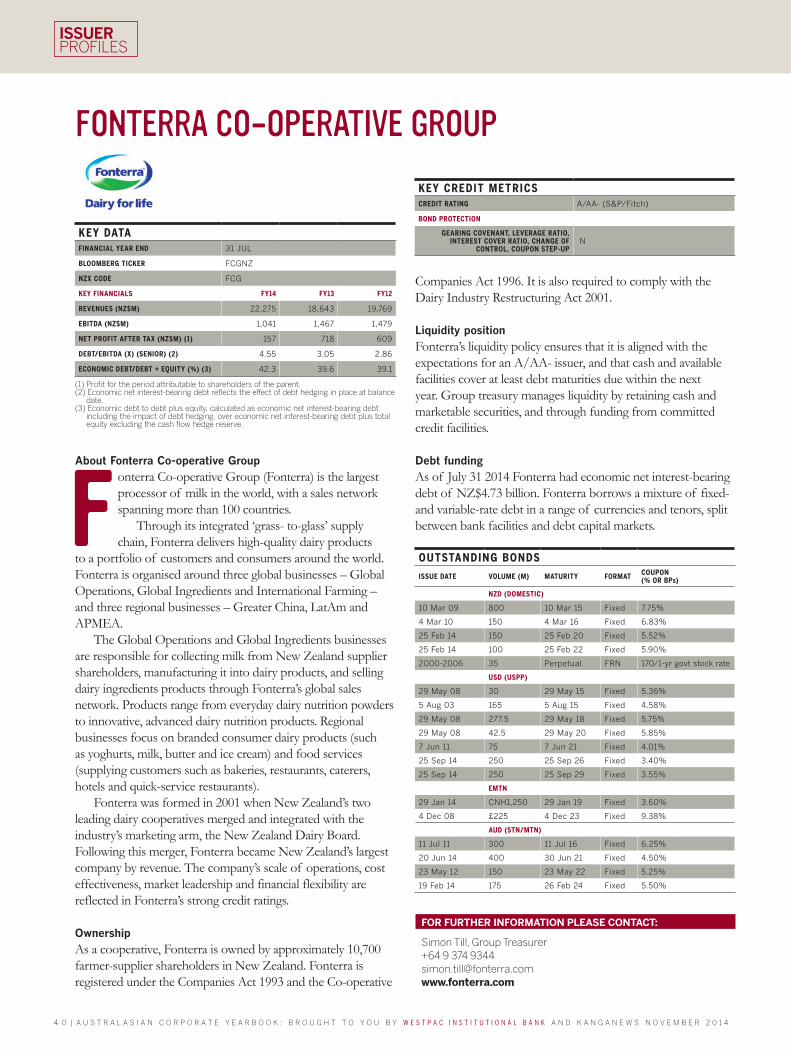

FONTERRA CO-OPERATIVE GROUP

About Fonterra Co-operative Group

F onterra Co-operative Group (Fonterra) is the largest processor of milk in the world, with a sales network spanning more than 100 countries.

Through its integrated ‘grass- to-glass’ supply chain, Fonterra delivers high-quality dairy products

to a portfolio of customers and consumers around the world. Fonterra is organised around three global businesses – Global Operations, Global Ingredients and International Farming – and three regional businesses – Greater China, LatAm and APMEA.

The Global Operations and Global Ingredients businesses are responsible for collecting milk from New Zealand supplier shareholders, manufacturing it into dairy products, and selling dairy ingredients products through Fonterra’s global sales network. Products range from everyday dairy nutrition powders to innovative, advanced dairy nutrition products. Regional businesses focus on branded consumer dairy products (such as yoghurts, milk, butter and ice cream) and food services (supplying customers such as bakeries, restaurants, caterers, hotels and quick-service restaurants).

Fonterra was formed in 2001 when New Zealand’s two leading dairy cooperatives merged and integrated with the industry’s marketing arm, the New Zealand Dairy Board. Following this merger, Fonterra became New Zealand’s largest company by revenue. The company’s scale of operations, cost effectiveness, market leadership and financial flexibility are reflected in Fonterra’s strong credit ratings.

OwnershipAs a cooperative, Fonterra is owned by approximately 10,700 farmer-supplier shareholders in New Zealand. Fonterra is registered under the Companies Act 1993 and the Co-operative

FOR FURTHER INFORMATION PLEASE CONTACT:

Simon Till, Group Treasurer+64 9 374 [email protected]

Companies Act 1996. It is also required to comply with the Dairy Industry Restructuring Act 2001.

Liquidity positionFonterra’s liquidity policy ensures that it is aligned with the expectations for an A/AA- issuer, and that cash and available facilities cover at least debt maturities due within the next year. Group treasury manages liquidity by retaining cash and marketable securities, and through funding from committed credit facilities.

Debt fundingAs of July 31 2014 Fonterra had economic net interest-bearing debt of NZ$4.73 billion. Fonterra borrows a mixture of fixed- and variable-rate debt in a range of currencies and tenors, split between bank facilities and debt capital markets.

KEY CREDIT METRICSCREDIT RATING A/AA- (S&P/Fitch)

BOND PROTECTION

GEARING COVENANT, LEVERAGE RATIO, INTEREST COVER RATIO, CHANGE OF

CONTROL, COUPON STEP-UP N

KEY DATAFINANCIAL YEAR END 31 JUL

BLOOMBERG TICKER FCGNZ

NZX CODE FCG

KEY FINANCIALS FY14 FY13 FY12

REVENUES (NZ$M) 22,275 18,643 19,769

EBITDA (NZ$M) 1,041 1,467 1,479

NET PROFIT AFTER TAX (NZ$M) (1) 157 718 609

DEBT/EBITDA (X) (SENIOR) (2) 4.55 3.05 2.86

ECONOMIC DEBT/DEBT + EQUITY (%) (3) 42.3 39.6 39.1

(1) Profit for the period attributable to shareholders of the parent.(2) Economic net interest-bearing debt reflects the effect of debt hedging in place at balance

date.(3) Economic debt to debt plus equity, calculated as economic net interest-bearing debt

including the impact of debt hedging, over economic net interest-bearing debt plus total equity excluding the cash flow hedge reserve.

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPON (% OR BPs)

NZD (DOMESTIC)

10 Mar 09 800 10 Mar 15 Fixed 7.75%

4 Mar 10 150 4 Mar 16 Fixed 6.83%

25 Feb 14 150 25 Feb 20 Fixed 5.52%

25 Feb 14 100 25 Feb 22 Fixed 5.90%

2000-2006 35 Perpetual FRN 170/1-yr govt stock rate

USD (USPP)

29 May 08 30 29 May 15 Fixed 5.36%

5 Aug 03 165 5 Aug 15 Fixed 4.58%

29 May 08 277.5 29 May 18 Fixed 5.75%

29 May 08 42.5 29 May 20 Fixed 5.85%

7 Jun 11 75 7 Jun 21 Fixed 4.01%

25 Sep 14 250 25 Sep 26 Fixed 3.40%

25 Sep 14 250 25 Sep 29 Fixed 3.55%

EMTN

29 Jan 14 CNH1,250 29 Jan 19 Fixed 3.60%

4 Dec 08 £225 4 Dec 23 Fixed 9.38%

AUD (STN/MTN)

11 Jul 11 300 11 Jul 16 Fixed 6.25%

20 Jun 14 400 30 Jun 21 Fixed 4.50%

23 May 12 150 23 May 22 Fixed 5.25%

19 Feb 14 175 26 Feb 24 Fixed 5.50%

4 1

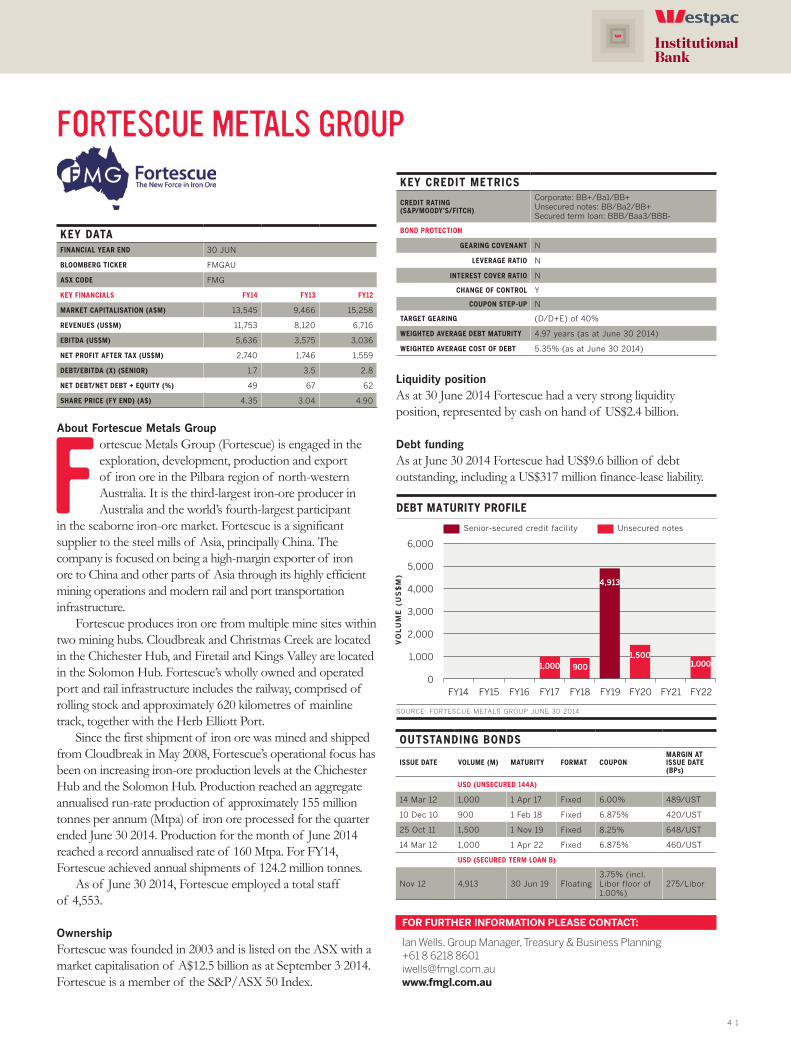

FORTESCUE METALS GROUP

About Fortescue Metals Group

F ortescue Metals Group (Fortescue) is engaged in the exploration, development, production and export of iron ore in the Pilbara region of north-western Australia. It is the third-largest iron-ore producer in Australia and the world’s fourth-largest participant

in the seaborne iron-ore market. Fortescue is a significant supplier to the steel mills of Asia, principally China. The company is focused on being a high-margin exporter of iron ore to China and other parts of Asia through its highly efficient mining operations and modern rail and port transportation infrastructure.

Fortescue produces iron ore from multiple mine sites within two mining hubs. Cloudbreak and Christmas Creek are located in the Chichester Hub, and Firetail and Kings Valley are located in the Solomon Hub. Fortescue’s wholly owned and operated port and rail infrastructure includes the railway, comprised of rolling stock and approximately 620 kilometres of mainline track, together with the Herb Elliott Port.

Since the first shipment of iron ore was mined and shipped from Cloudbreak in May 2008, Fortescue’s operational focus has been on increasing iron-ore production levels at the Chichester Hub and the Solomon Hub. Production reached an aggregate annualised run-rate production of approximately 155 million tonnes per annum (Mtpa) of iron ore processed for the quarter ended June 30 2014. Production for the month of June 2014 reached a record annualised rate of 160 Mtpa. For FY14, Fortescue achieved annual shipments of 124.2 million tonnes.

As of June 30 2014, Fortescue employed a total staff of 4,553.

OwnershipFortescue was founded in 2003 and is listed on the ASX with a market capitalisation of A$12.5 billion as at September 3 2014. Fortescue is a member of the S&P/ASX 50 Index.

FOR FURTHER INFORMATION PLEASE CONTACT:

Ian Wells, Group Manager, Treasury & Business Planning +61 8 6218 8601 [email protected]

Liquidity positionAs at 30 June 2014 Fortescue had a very strong liquidity position, represented by cash on hand of US$2.4 billion.

Debt fundingAs at June 30 2014 Fortescue had US$9.6 billion of debt outstanding, including a US$317 million finance-lease liability.

KEY CREDIT METRICS

CREDIT RATING (S&P/MOODY’S/FITCH)

Corporate: BB+/Ba1/BB+Unsecured notes: BB/Ba2/BB+ Secured term loan: BBB/Baa3/BBB-

BOND PROTECTION

GEARING COVENANT N

LEVERAGE RATIO N

INTEREST COVER RATIO N

CHANGE OF CONTROL Y

COUPON STEP-UP N

TARGET GEARING (D/D+E) of 40%

WEIGHTED AVERAGE DEBT MATURITY 4.97 years (as at June 30 2014)

WEIGHTED AVERAGE COST OF DEBT 5.35% (as at June 30 2014)

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER FMGAU

ASX CODE FMG

KEY FINANCIALS FY14 FY13 FY12

MARKET CAPITALISATION (A$M) 13,545 9,466 15,258

REVENUES (US$M) 11,753 8,120 6,716

EBITDA (US$M) 5,636 3,575 3,036

NET PROFIT AFTER TAX (US$M) 2,740 1,746 1,559

DEBT/EBITDA (X) (SENIOR) 1.7 3.5 2.8

NET DEBT/NET DEBT + EQUITY (%) 49 67 62

SHARE PRICE (FY END) (A$) 4.35 3.04 4.90

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPONMARGIN AT ISSUE DATE (BPs)

USD (UNSECURED 144A)

14 Mar 12 1,000 1 Apr 17 Fixed 6.00% 489/UST

10 Dec 10 900 1 Feb 18 Fixed 6.875% 420/UST

25 Oct 11 1,500 1 Nov 19 Fixed 8.25% 648/UST

14 Mar 12 1,000 1 Apr 22 Fixed 6.875% 460/UST

USD (SECURED TERM LOAN B)

Nov 12 4,913 30 Jun 19 Floating3.75% (incl. Libor floor of 1.00%)

275/Libor

DEBT MATURITY PROFILE

VO

LU

ME

(U

S$

M)

6,000

5,000

4,000

3,000

2,000

1,000

0

SOURCE: FORTESCUE METALS GROUP JUNE 30 2014

Senior-secured credit facility Unsecured notes

1,000

4,913

1,500

FY15 FY16 FY17 FY18 FY19 FY20 FY21 FY22FY14

1,000900

4 2 | A U S T R A L A S I A N C O R P O R A T E Y E A R B O O K : B R O U G H T T O Y O U B Y W E S T P A C I N S T I T U T I O N A L B A N K A N D K A N G A N E W S N O V E M B E R 2 0 1 4

ISSUERPROFILES

GENESIS ENERGY

About Genesis Energy

G enesis Energy is New Zealand’s largest energy retailer. It supplies electricity, gas and LPG to more than 647,000 customers across New Zealand. The company’s ability to bring innovative energy solutions to retail and business customers is supported by a

diverse generation portfolio comprising thermal, wind and hydro generation. This supplied approximately 17% of New Zealand’s electricity in 2013. Genesis Energy also owns 31% of the Kupe oil and gas field.

OwnershipGenesis Energy was listed on the NZX and ASX on April 17 2014, following the company’s partial privatisation by the government of New Zealand.

Liquidity positionA conservative liquidity position and moderate financial flexibility have been provided through headroom in the company’s debt facilities and an appropriately managed near-term liability maturity profile. Genesis Energy’s liquidity risk-management policies are conservative and include committed debt facilities that must be maintained at an amount that is the higher of NZ$50 million or 115% of projected peak over the next two years. The company is operating comfortably above its financial covenants.

Debt fundingGenesis Energy accesses a number of markets to provide debt funding for its business. Of the NZ$1.245 billion of debt facilities in place at June 30 2014, NZ$625 million is through arrangements with individual banks (up NZ$150 million from the previous year). The remaining NZ$620 million is funded through a combination of MTNs, retail and capital bonds. During the most recent financial year, a total of NZ$75 million

FOR FURTHER INFORMATION PLEASE CONTACT:

Dan Dillane, Capital Structure Manager+64 9 951 [email protected]

of capital bonds was repurchased and NZ$120 million of retail bonds matured.

KEY CREDIT METRICSCREDIT RATING BBB+ (S&P)

BOND PROTECTION

GEARING COVENANT, LEVERAGE RATIO, INTEREST COVER RATIO N

CHANGE OF CONTROL Y (capital bonds only) (1)

COUPON STEP-UP Y (capital bonds only) (2)

BANK COVENANTS

GEARING 50%

EBITDAF/INTEREST 2.5x

TARGET GEARING N/A

(1) If a change of control event occurs, Genesis Energy has the right to redeem the capital bonds. If a change of control and an associated ratings downgrade occurs, bondholders may elect to have their capital bond redeemed by Genesis Energy.(2) On July 15 2018 and every five years thereafter, the interest rate will reset to be the sum of the five-year swap on the relevant reset date plus the step-up margin (being the margin set on the minimum rate set date plus the step-up percentage of 0.25%).

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER GENEPO

NZX CODE GNE/GPLFA

KEY FINANCIALS FY14 FY13 FY12

REVENUES (NZ$M) 2,005 2,070 2,265

EBITDA (NZ$M) 307.8 336.6 387.3

NET PROFIT AFTER TAX (NZ$M) 49.2 104.5 86.4

DEBT/EBITDA (X) (SENIOR) (1) 2.9 2.7 1.9

NET DEBT/NET DEBT + EQUITY (%) 31.0 31.1 (1) 26.4 (1)

(1) Treats capital bonds as 100% equity in FY12 and 50% equity in FY13, in line with bank covenants and rating agency treatment.

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPON MARGIN AT ISSUE DATE (BPs)

NZD (DOMESTIC)

Bank debt 125 31 Sep 15 N/A N/A ND

Bank debt 75 12 Nov 16 N/A N/A ND

Bank debt 75 12 Nov 17 N/A N/A ND

Bank debt 350 12 Nov 18 N/A N/A ND

Retail Bonds B 105 15 Mar 16 Fixed 7.65% ND

MTNs 75 15 Sep 16 Fixed 7.19% 48/swap

MTNs 50 20 Feb 17 Fixed/FRN ND 240/BKBM

MTNs 50 1 Nov 19 Fixed 5.21% 175/swap

MTNs 70 23 Jun 20 Fixed 8.25% 255/swap

MTNs 70 8 Mar 23 Fixed 5.81% 175/swap

Capital bonds 200 15 Jul 41 Fixed 6.19% 215/swap

DEBT MATURITY PROFILE

Rolling bank debt Bank debt

VO

LU

ME

(N

Z$

M)

400

350

300

250

200

150

100

50

0FY16

FY17

FY18

FY19

FY20

FY21

FY22

FY41

SOURCE: GENESIS ENERGY JUNE 30 2014

Retail bonds Capital bonds

350

75

50125

7550

105

75

Wholesale domestic bonds

70 70

200

4 3

THE GPT GROUP

About The GPT Group

T he GPT Group (GPT) is a property group with broad access to capital invested in quality assets. The group focuses on active ownership of high-quality Australian real estate in the retail, office, and logistics sectors. Total assets grew from A$6 million in 1971

to A$9.6 billion as at June 30 2014, with retail assets comprising about 51% of the asset base, office at 34%, and logistics at 15%. At June 30 2014 the group had assets under management of A$16.7 billion.

OwnershipGPT listed on the ASX in April 1971. The group has a substantial investor base, with over 38,000 investors, and is one of the top-50 stocks by market capitalisation. GPT is internally managed with the responsible entity (GPT RE) being a subsidiary of GPT Management Holdings.

Liquidity positionAt June 30 2014, GPT had A$209 million of liquidity available in cash and through committed, but undrawn, debt facilities.

Debt fundingGPT manages its gearing within the range of 25-35%. As at June 30 2014, gearing on a net basis was 24.8%. Drawn debt was A$2.4 billion, with the average term to maturity increasing to 6.0 years as a result of a further US$175 million, 15-year US private placement (USPP) issuance in the first half of 2014, swapped back at a margin of 144 basis points over BBSW.

GPT’s debt is sourced from a variety of funding sources – including bank debt facilities from domestic and offshore banks, domestic and foreign MTNs, USPPs and inflation-linked bonds. As at June 30 2014, 40% of drawn debt was sourced through the debt capital markets.

FOR FURTHER INFORMATION PLEASE CONTACT:

Lilly Cheung, Group Treasurer+61 2 8239 [email protected]

KEY CREDIT METRICSCREDIT RATING A-/A3 (S&P/Moody’s)

BOND PROTECTION (2010 PROGRAMME)

GEARING COVENANT Y

LEVERAGE RATIO N

INTEREST COVER RATIO Y

CHANGE OF CONTROL Y

COUPON STEP-UP N

TARGET GEARING 25-35% (mgt. target <=30%)

WEIGHTED AVERAGE DEBT MATURITY 6.0 years (as at June 30 2014)

WEIGHTED AVERAGE COST OF DEBT 4.84% (as at June 30 2014)

KEY DATAFINANCIAL YEAR END 31 DEC

BLOOMBERG TICKER GPTAU

ASX CODE GPT

KEY FINANCIALS HY14 FY13 HY13 FY12

MARKET CAPITALISATION (A$M) 6,472 5,763 6,695 6,502

REVENUES (A$M) 386.3 788.3 400.2 812.9

EBITDA (A$M) 281.7 580.7 291.6 566.8

NET PROFIT AFTER TAX (A$M) 240.6 571.5 257.0 594.5

DEBT/EBITDA (X) (SENIOR) 4.3 4.0 3.5 3.8

NET DEBT/NET DEBT + EQUITY (%) 25.9 23.2 20.3 22.4

SHARE PRICE (FY OR HY END) (A$) 3.84 3.40 3.84 3.68

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPON MARGIN AT ISSUE

DATE (BPs)

AUD (DOMESTIC)

19 Nov 12 30 19 Nov 17 FRN ND ND

24 Jan 12 150 24 Jan 19 Fixed 6.75% 235/swap

2 Aug 12 100 24 Jan 19 Fixed 6.75% 220/swap

11 Sep 14 150 11 Sep 20 Fixed 4.50% 120/swap

16 Aug 12 33 16 Aug 22 Fixed 6.25% 225/swap

31 Aug 12 17 16 Aug 22 Fixed 6.25% 225/swap

10 Dec 99 85 10 Dec 29 CPI-linked 5.90%+CPI ND

USD (USPP)

28 May 13 65 19 Jun 25 Fixed 3.60% 170/UST

19 Jun 13 85 19 Jun 25 Fixed 3.60% 170/UST

19 Jun 13 100 19 Jun 28 Fixed 3.80% 190/UST

6 Jun 14 62.5 8 Jul 29 Fixed 4.33% 162/UST

8 Jul 14 112.5 8 Jul 29 Fixed 4.36% 165/UST

HKD

5-22 Feb 13 800 5 Feb 28 Fixed 3.55% 165/swap

GPT’s aim is to ensure that debt maturity is a maximum of A$1 billion on a rolling 12-month basis and A$500 million in any calendar quarter. Upcoming expiries in the forward 12 months are refinanced well in advance, with existing liquidity headroom and forward-start facilities.

DEBT MATURITY PROFILE

Bank debt Bonds USPP

VO

LU

ME

(A

$M

)

600

500

400

300

200

100

0

SOURCE: THE GPT GROUP JUNE 30 2014

28

9

49

8

38

7 325

250

100

50

97

8514

6

30

188

99

FY15

FY16

FY17

FY18

FY19

FY20

FY21

FY22

FY23

FY24

FY25

FY26

FY27

FY28

FY29

FY14

4 4 | A U S T R A L A S I A N C O R P O R A T E Y E A R B O O K : B R O U G H T T O Y O U B Y W E S T P A C I N S T I T U T I O N A L B A N K A N D K A N G A N E W S N O V E M B E R 2 0 1 4

ISSUERPROFILES

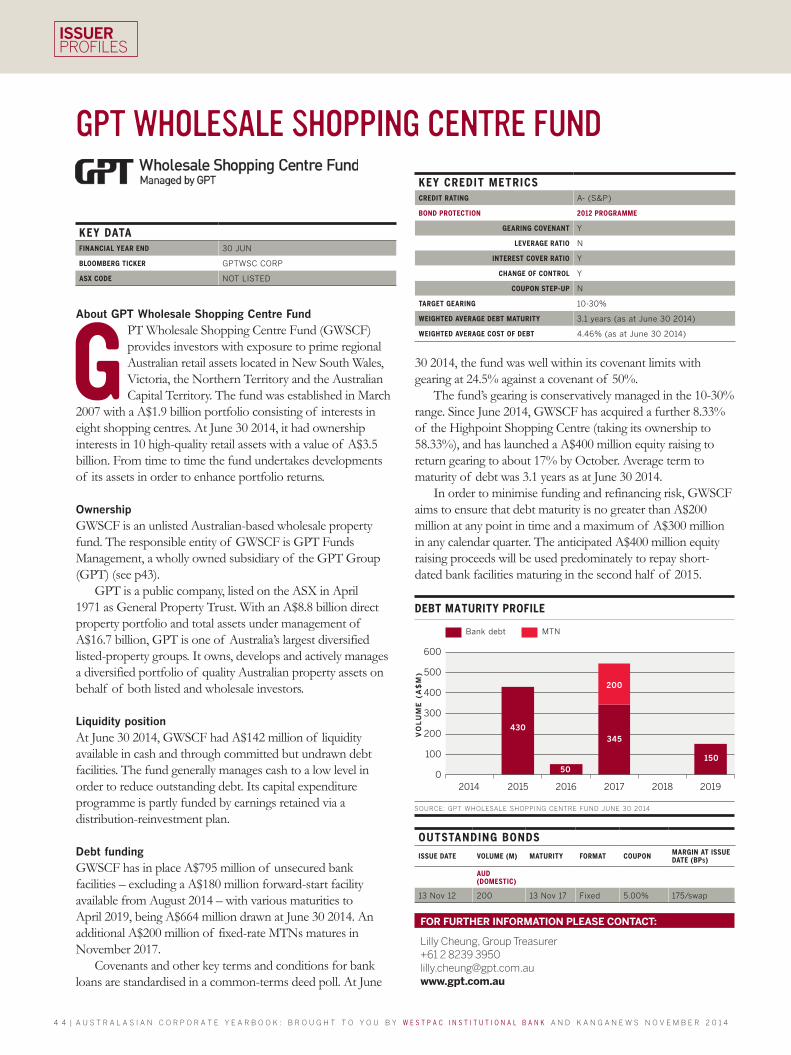

GPT WHOLESALE SHOPPING CENTRE FUND

About GPT Wholesale Shopping Centre Fund

G PT Wholesale Shopping Centre Fund (GWSCF) provides investors with exposure to prime regional Australian retail assets located in New South Wales, Victoria, the Northern Territory and the Australian Capital Territory. The fund was established in March

2007 with a A$1.9 billion portfolio consisting of interests in eight shopping centres. At June 30 2014, it had ownership interests in 10 high-quality retail assets with a value of A$3.5 billion. From time to time the fund undertakes developments of its assets in order to enhance portfolio returns.

OwnershipGWSCF is an unlisted Australian-based wholesale property fund. The responsible entity of GWSCF is GPT Funds Management, a wholly owned subsidiary of the GPT Group (GPT) (see p43).

GPT is a public company, listed on the ASX in April 1971 as General Property Trust. With an A$8.8 billion direct property portfolio and total assets under management of A$16.7 billion, GPT is one of Australia’s largest diversified listed-property groups. It owns, develops and actively manages a diversified portfolio of quality Australian property assets on behalf of both listed and wholesale investors.

Liquidity positionAt June 30 2014, GWSCF had A$142 million of liquidity available in cash and through committed but undrawn debt facilities. The fund generally manages cash to a low level in order to reduce outstanding debt. Its capital expenditure programme is partly funded by earnings retained via a distribution-reinvestment plan.

Debt fundingGWSCF has in place A$795 million of unsecured bank facilities – excluding a A$180 million forward-start facility available from August 2014 – with various maturities to April 2019, being A$664 million drawn at June 30 2014. An additional A$200 million of fixed-rate MTNs matures in November 2017.

Covenants and other key terms and conditions for bank loans are standardised in a common-terms deed poll. At June

FOR FURTHER INFORMATION PLEASE CONTACT:

Lilly Cheung, Group Treasurer+61 2 8239 [email protected]

KEY CREDIT METRICSCREDIT RATING A- (S&P)

BOND PROTECTION 2012 PROGRAMME

GEARING COVENANT Y

LEVERAGE RATIO N

INTEREST COVER RATIO Y

CHANGE OF CONTROL Y

COUPON STEP-UP N

TARGET GEARING 10-30%

WEIGHTED AVERAGE DEBT MATURITY 3.1 years (as at June 30 2014)

WEIGHTED AVERAGE COST OF DEBT 4.46% (as at June 30 2014)

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER GPTWSC CORP

ASX CODE NOT LISTED

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPON MARGIN AT ISSUE DATE (BPs)

AUD (DOMESTIC)

13 Nov 12 200 13 Nov 17 Fixed 5.00% 175/swap

30 2014, the fund was well within its covenant limits with gearing at 24.5% against a covenant of 50%.

The fund’s gearing is conservatively managed in the 10-30% range. Since June 2014, GWSCF has acquired a further 8.33% of the Highpoint Shopping Centre (taking its ownership to 58.33%), and has launched a A$400 million equity raising to return gearing to about 17% by October. Average term to maturity of debt was 3.1 years as at June 30 2014.

In order to minimise funding and refinancing risk, GWSCF aims to ensure that debt maturity is no greater than A$200 million at any point in time and a maximum of A$300 million in any calendar quarter. The anticipated A$400 million equity raising proceeds will be used predominately to repay short-dated bank facilities maturing in the second half of 2015.

VO

LU

ME

(A

$M

)

DEBT MATURITY PROFILE

Bank debt MTN

600

500

400

300

200

100

0

SOURCE: GPT WHOLESALE SHOPPING CENTRE FUND JUNE 30 2014

430

50

200

150

345

2015 2016 2017 2018 20192014

4 5

HOLCIM

About Holcim

F ounded in Switzerland in 1912, Holcim is one of the world’s leading suppliers of cement and aggregates. The group also supplies ready-mix concrete and asphalt, and provides related services. Holcim operates in around 70 countries and employs some 71,000

people. It is more globally spread than any other building materials group, with around 1,750 plants around the world.

Holcim’s business strategy is based on continuous growth in both developed economies and emerging, high-growth markets, where around three-quarters of its operational cement capacity is based. As an economy becomes more mature, vertical integration becomes increasingly important for Holcim.

Holcim took the opportunity to move toward vertical integration in Australia in 2009 through the acquisition of Cemex Australia – now Holcim Australia. Holcim operates around 300 cement, aggregates, ready-mix and grinding plants and employs around 4,500 people in the three companies Holcim Australia, Cement Australia and Holcim New Zealand.

On April 7 2014, Holcim announced that it intends to enter into a merger of equals with Lafarge to create LafargeHolcim. Completion of the merger of equals is expected by the end of the first half of 2015, subject to, among other things, obtaining regulatory approvals.

OwnershipHolcim is listed on the SIX Swiss Exchange. As at December 31 2013, 20.11% of its shares was held by Thomas Schmidheiny, 10.82% by Eurocement Holding AG and 5.11% by Harris Associates L.P.

Liquidity positionAt June 30 2014, Holcim had CHF1.9 billion in cash and marketable securities and CHF3.9 billion in undrawn committed credit lines.

FOR FURTHER INFORMATION PLEASE CONTACT:

Patrick Förg, Corporate Finance & Treasury+41 58 858 8724 [email protected]/bondholders

Debt fundingAs at June 30 2014, Holcim had a net financial debt position of CHF10.6 billion. A total of 77% of its financial liabilities is financed through capital markets and 23% through banks and other lenders.

Holcim has a strong liquidity position of CHF5.9 billion and has decisively strengthened its balance sheet. The company places great importance on maintaining its solid investment-grade credit rating by complying with financial targets – such as funds from operations to net financial debt (target >25%) or net financial debt to EBITDA (target <2.8x).

Outstanding corporate bank lines and bonds at the parent or financial sub-holding level are free from financial covenants, repeating material adverse-change clauses or rating triggers. These debt instruments also feature limited cross-default provisions, which typically exclude operating subsidiaries. This removes the risk that any covenant breach by the group’s operating subsidiaries would contaminate the parent company’s debt.

Holcim Finance (Australia) is used as a finance vehicle for the group and all its long-term transactions are guaranteed by the parent company.

KEY CREDIT METRICSCREDIT RATING BBB/Baa2/BBB (S&P/Moody’s/Fitch)

BOND PROTECTION

GEARING COVENANT N

LEVERAGE RATIO N

INTEREST COVER RATIO N

CHANGE OF CONTROL Y (partial)

COUPON STEP-UP Y (partial)

TARGET GEARING N/A

WEIGHTED AVERAGE DEBT MATURITY 5.0 years (as at June 30 2014)

WEIGHTED AVERAGE COST OF DEBT 4.6% (as at December 31 2013)

KEY DATAFINANCIAL YEAR END 31 DEC

BLOOMBERG TICKER HOLNVX

ASX CODE NOT LISTED IN AUSTRALIA

KEY FINANCIALS HY14 FY13 HY13 FY12

MARKET CAPITALISATION (CHF M) 25,496 21,883 21,539 21,882

REVENUES (CHF M) 9,061 19,719 9,649 21,160

OPERATING EBITDA (CHF M) 1,627 3,896 1,819 3,889

NET PROFIT AFTER TAX (CHF M) 657 1,596 760 1,002

DEBT/EBITDA (X) (SENIOR) ND 2.70 ND 3.09

NET DEBT/NET DEBT + EQUITY (%) 35.94 33.62 36.36 34.93

SHARE PRICE (FY OR HY END) (CHF) 77.95 66.75 65.85 66.9

OUTSTANDING BONDS (HOLCIM FINANCE AUSTRALIA)

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPONMARGIN AT ISSUE DATE (BPs)

AUD (DOMESTIC)

27 Mar 12 250 27 Mar 15 Fixed 7.00% 260/swap

18 Jul 12 250 18 Jul 17 Fixed 6.00% 265/swap

4 Oct 12 200 4 Apr 19 Fixed 5.25% 200/swap

4 6 | A U S T R A L A S I A N C O R P O R A T E Y E A R B O O K : B R O U G H T T O Y O U B Y W E S T P A C I N S T I T U T I O N A L B A N K A N D K A N G A N E W S N O V E M B E R 2 0 1 4

ISSUERPROFILES

INCITEC PIVOT

About Incitec Pivot

I ncitec Pivot is a leading global chemicals company with nitrogen-based manufacturing at its core. The company is the number-one supplier of fertilisers in Australia, a market-leading supplier of explosives products and services in North America – the largest industrial-

explosives market in the world – and number-two supplier of explosives products and services in Australia.

Incitec Pivot has operations throughout the US, Canada, Mexico, Australia, Turkey, Chile, Indonesia and Papua New Guinea, with approximately 5,000 staff worldwide. Its headquarters are in Melbourne.

OwnershipIncitec Pivot was created from the merger between Pivot and Incitec Fertilizers in 2003. It has been listed on the ASX since July 2003, as IPL, and is one of the top-100 listed companies on the exchange.

Liquidity positionIn its 2014 half-year results presentation, Incitec Pivot reported that it has a significant level of funding headroom with undrawn committed funding lines – including cash – of more than A$1.34 billion.

Debt fundingThe consolidated entity has foreign operations with non-AUD functional currencies and so is exposed to translation risk resulting from FX movements. As a result, the consolidated entity has a preference for debt denominated in US dollars.

Incitec Pivot significantly extended the tenor of its debt portfolio with the issue of a US$800 million 144A Reg S bond deal in December 2009 and a US$500 million 144A Reg S bond deal in December 2010. These deals complement

FOR FURTHER INFORMATION PLEASE CONTACT:

Geoff McMurray, General Manager, Treasury+61 3 8695 [email protected]

the company’s A$1.45 billion syndicated facility maturing in October 2016 and September 2018.

In August 2013, the company issued a A$200 million MTN with a maturity date of February 2019.

KEY CREDIT METRICSCREDIT RATING BBB/Baa3/BBB (S&P/Moody’s/Fitch)

BOND PROTECTION

GEARING COVENANT N (USD bonds), Y (AUD bonds)

LEVERAGE RATIO N

INTEREST COVER RATIO N (USD bonds), Y (AUD bonds)

CHANGE OF CONTROLY (only where the company fails to maintain an investment-grade rating)

COUPON STEP-UP N (USD bonds) Y (AUD bonds)

TARGET GEARING <2.5x (debt to EBITDA )

WEIGHTED AVERAGE DEBT MATURITY 4.3 years (as at March 31 2014)

WEIGHTED AVERAGE COST OF DEBT Not disclosed publicly

KEY DATAFINANCIAL YEAR END 30 SEP

BLOOMBERG TICKER IPLAU

ASX CODE IPL

KEY FINANCIALS HY14 FY13 HY13 FY12

MARKET CAPITALISATION (A$M) 4,869.0 4,424.8 5,033.6 4,854.0

REVENUES (A$M) 1,508.4 3,403.7 1,426.9 3,501.0

EBITDA (A$M) 303 650 255 755

NET PROFIT AFTER TAX (A$M) 115.7 372.0 110.2 510.7

DEBT/EBITDA (X) (SENIOR) 2.40 2.00 2.26 1.70

NET DEBT/NET DEBT + EQUITY (%) 30.0 23.2 29.1 24.2

SHARE PRICE (FY OR HY END) (A$) 2.96 2.69 3.09 2.98

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPONMARGIN AT ISSUE DATE (BPs)

AUD (DOMESTIC)

21 Aug 13 200 21 Feb 19 Fixed 5.75% 215/swap

USD (144A)

7 Dec 10 500 7 Dec 15 Fixed 4.00% 275/UST

3 Dec 09 800 10 Dec 19 Fixed 6.00% 270/UST

4 7

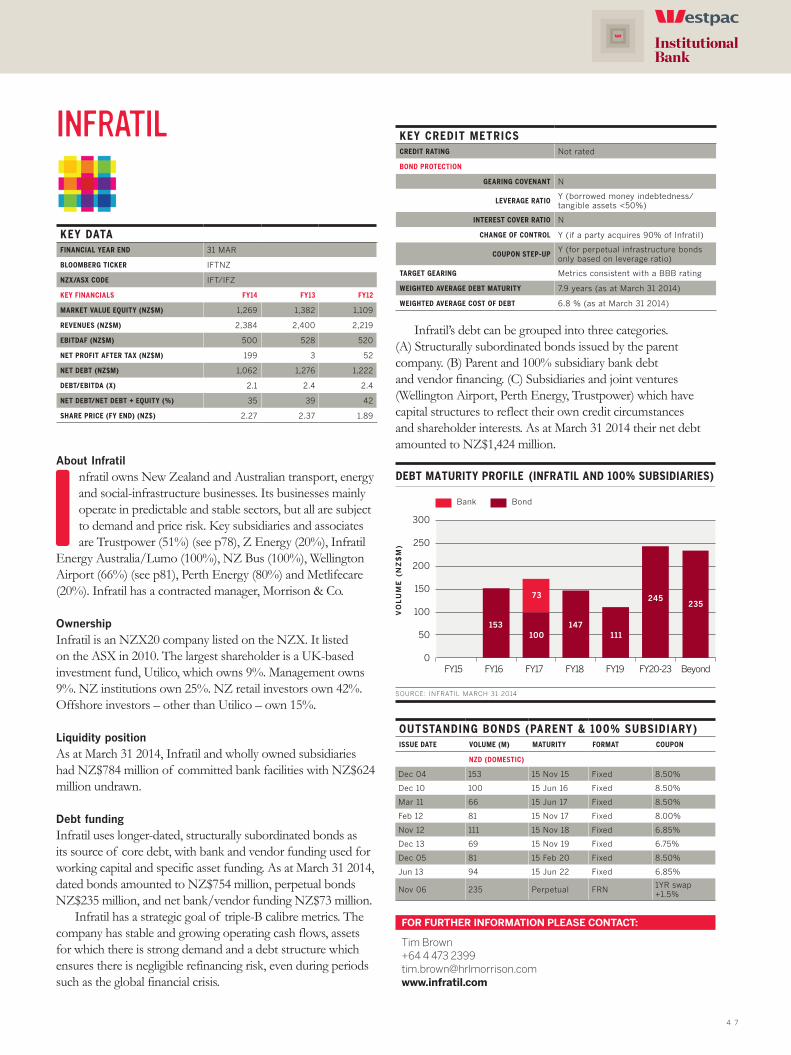

INFRATIL

About Infratil

I nfratil owns New Zealand and Australian transport, energy and social-infrastructure businesses. Its businesses mainly operate in predictable and stable sectors, but all are subject to demand and price risk. Key subsidiaries and associates are Trustpower (51%) (see p78), Z Energy (20%), Infratil

Energy Australia/Lumo (100%), NZ Bus (100%), Wellington Airport (66%) (see p81), Perth Energy (80%) and Metlifecare (20%). Infratil has a contracted manager, Morrison & Co.

OwnershipInfratil is an NZX20 company listed on the NZX. It listed on the ASX in 2010. The largest shareholder is a UK-based investment fund, Utilico, which owns 9%. Management owns 9%. NZ institutions own 25%. NZ retail investors own 42%. Offshore investors – other than Utilico – own 15%.

Liquidity positionAs at March 31 2014, Infratil and wholly owned subsidiaries had NZ$784 million of committed bank facilities with NZ$624 million undrawn.

Debt fundingInfratil uses longer-dated, structurally subordinated bonds as its source of core debt, with bank and vendor funding used for working capital and specific asset funding. As at March 31 2014, dated bonds amounted to NZ$754 million, perpetual bonds NZ$235 million, and net bank/vendor funding NZ$73 million.

Infratil has a strategic goal of triple-B calibre metrics. The company has stable and growing operating cash flows, assets for which there is strong demand and a debt structure which ensures there is negligible refinancing risk, even during periods such as the global financial crisis.

FOR FURTHER INFORMATION PLEASE CONTACT:

Tim Brown+64 4 473 [email protected]

Infratil’s debt can be grouped into three categories. (A) Structurally subordinated bonds issued by the parent company. (B) Parent and 100% subsidiary bank debt and vendor financing. (C) Subsidiaries and joint ventures (Wellington Airport, Perth Energy, Trustpower) which have capital structures to reflect their own credit circumstances and shareholder interests. As at March 31 2014 their net debt amounted to NZ$1,424 million.

KEY CREDIT METRICSCREDIT RATING Not rated

BOND PROTECTION

GEARING COVENANT N

LEVERAGE RATIOY (borrowed money indebtedness/tangible assets <50%)

INTEREST COVER RATIO N

CHANGE OF CONTROL Y (if a party acquires 90% of Infratil)

COUPON STEP-UPY (for perpetual infrastructure bonds only based on leverage ratio)

TARGET GEARING Metrics consistent with a BBB rating

WEIGHTED AVERAGE DEBT MATURITY 7.9 years (as at March 31 2014)

WEIGHTED AVERAGE COST OF DEBT 6.8 % (as at March 31 2014)

KEY DATAFINANCIAL YEAR END 31 MAR

BLOOMBERG TICKER IFTNZ

NZX/ASX CODE IFT/IFZ

KEY FINANCIALS FY14 FY13 FY12

MARKET VALUE EQUITY (NZ$M) 1,269 1,382 1,109

REVENUES (NZ$M) 2,384 2,400 2,219

EBITDAF (NZ$M) 500 528 520

NET PROFIT AFTER TAX (NZ$M) 199 3 52

NET DEBT (NZ$M) 1,062 1,276 1,222

DEBT/EBITDA (X) 2.1 2.4 2.4

NET DEBT/NET DEBT + EQUITY (%) 35 39 42

SHARE PRICE (FY END) (NZ$) 2.27 2.37 1.89

OUTSTANDING BONDS (PARENT & 100% SUBSIDIARY)ISSUE DATE VOLUME (M) MATURITY FORMAT COUPON

NZD (DOMESTIC)

Dec 04 153 15 Nov 15 Fixed 8.50%

Dec 10 100 15 Jun 16 Fixed 8.50%

Mar 11 66 15 Jun 17 Fixed 8.50%

Feb 12 81 15 Nov 17 Fixed 8.00%

Nov 12 111 15 Nov 18 Fixed 6.85%

Dec 13 69 15 Nov 19 Fixed 6.75%

Dec 05 81 15 Feb 20 Fixed 8.50%

Jun 13 94 15 Jun 22 Fixed 6.85%

Nov 06 235 Perpetual FRN1YR swap +1.5%

DEBT MATURITY PROFILE (INFRATIL AND 100% SUBSIDIARIES)

Bank Bond

VO

LU

ME

(N

Z$

M)

300

250

200

150

100

50

0FY15 FY16 FY17 FY18 FY19 FY20-23 Beyond

SOURCE: INFRATIL MARCH 31 2014

153

73

100147

111

245235

4 8 | A U S T R A L A S I A N C O R P O R A T E Y E A R B O O K : B R O U G H T T O Y O U B Y W E S T P A C I N S T I T U T I O N A L B A N K A N D K A N G A N E W S N O V E M B E R 2 0 1 4

ISSUERPROFILES

INVESTA OFFICE FUND

About Investa Office Fund

I nvesta Office Fund (IOF) is a leading owner of investment-grade office buildings, receiving rental income from a tenant register comprised predominately of government and blue-chip tenants. IOF has total assets under management of A$3.1 billion, with 23 investments

located in core CBD markets throughout Australia and one legacy asset in Brussels, Belgium.

The fund’s overarching strategy is to be Australia’s best-performing CBD office fund with a focus on delivering attractive risk-adjusted returns to its unitholders.

OwnershipThe fund was created on January 1 2000, as a result of a merger between Armstrong Jones Office Trust and Prime Credit Property Trust. IOF is a top-100 ASX-listed entity, and major owners include AMP, CBRE Clarion, Morgan Stanley Investment Management and Mitsubishi UFJ Financial Group.

IOF is managed by Investa Office, a specialist owner and manager of high-quality office buildings in core CBD markets across Australia. The Investa Office portfolio incorporates more than a million square metres of quality office space across 47 buildings, worth more than A$8 billion, accommodating some of the world’s leading companies.

Investa Office operates an integrated real-estate platform that incorporates funds management, portfolio and asset-management services, property services, development, sustainability and research.

Liquidity positionIOF maintains a strong balance sheet, with look-through gearing of 31.5% at June 30 2014 and undrawn credit facilities available of A$170 million. Further access to capital will be realised upon the sale of the remaining European asset, valued

FOR FURTHER INFORMATION PLEASE CONTACT:

Ming Long, Finance Director+61 2 8226 [email protected]/iof

at A$78 million. There is a strong focus on cash generation, and IOF targets through-the-cycle distributions no greater than net cash received less maintenance capex.

Debt fundingIn FY14, IOF completed A$727 million of debt refinancing. This resulted in the fund at June 30 2014 having A$648 million of unsecured bank-debt facilities, A$125 million of domestic MTNs, US$325 million US private placements, and A$58 million of nonrecourse property-level debt (for the European asset). Debt expiries are diversified out to FY29, with no single-year maturity greater than A$200 million.

KEY CREDIT METRICSCREDIT RATING BBB+ (S&P)

BOND PROTECTION

GEARING COVENANT Y

LEVERAGE RATIO Y

INTEREST COVER RATIO Y

CHANGE OF CONTROL Y

TARGET GEARING 25-35%

WEIGHTED AVERAGE DEBT MATURITY 5.8 years (as at June 30 2014)

WEIGHTED AVERAGE COST OF DEBT 4.7% (as at June 30 2014)

KEY DATAFINANCIAL YEAR END 30 JUN

BLOOMBERG TICKER IOFAU

ASX CODE IOF

KEY FINANCIALS FY14 FY13 FY12

MARKET CAPITALISATION (A$M) 2,088 1,787 1,660

REVENUES (A$M) 197.9 191.0 202.9

EBIT (A$M) 172.4 171.8 158.5

NET PROFIT AFTER TAX (A$M) 183.6 158.7 101.9

DEBT/EBIT (X) (SENIOR) 5.9 3.9 3.2

DEBT/TOTAL ASSETS (%): LOOK-THROUGH GEARING 31.5 26.3 21.9

SHARE PRICE (FY END) (A$) 3.40 2.91 2.71

DEBT MATURITY PROFILE

USPP (A$)Undrawn bank debt Drawn bank debt

Bastion Tower MTN

VO

LU

ME

(A

$M

)

250

200

150

100

50

0FY15 FY16 FY17 FY18 FY19 FY20 FY25 FY26 FY27 FY28 FY29

SOURCE: INVESTA OFFICE FUND JUNE 30 2014

OUTSTANDING BONDS

ISSUE DATE VOLUME (M) MATURITY FORMAT COUPON MARGIN AT ISSUE DATE (BPs)

AUD (DOMESTIC)

Oct 12 125 Nov 17 Fixed 5.40% 210/swap

USD (USPP)

Jun 13 125 Aug 25 Fixed 3.98% 185/UST

Jan 14 78 Apr 25 Fixed 4.55% 170/UST

Jan 14 64 Apr 27 Fixed 4.69% 175/UST

Jan 14 58 Apr 29 Fixed 4.78% 175/UST

150

50

11689

132

58

No single maturity >A$200m

125

54

146 129

73 66

4 9

KIWI INCOME PROPERTY TRUST

About Kiwi Income Property Trust

K iwi Income Property Trust (KIPT) is New Zealand’s largest internally managed, listed, diversified property trust by total assets, with NZ$2.1 billion invested in a diversified portfolio of prime office and dominant retail assets located throughout New Zealand. KIPT

was founded in 1992 and became the country’s first listed property trust in 1993.

OwnershipKIPT is a unit trust established under the Unit Trusts Act 1960 by a deed of trust dated August 21 1992 (as amended). KIPT is listed on the NZX as KIP.

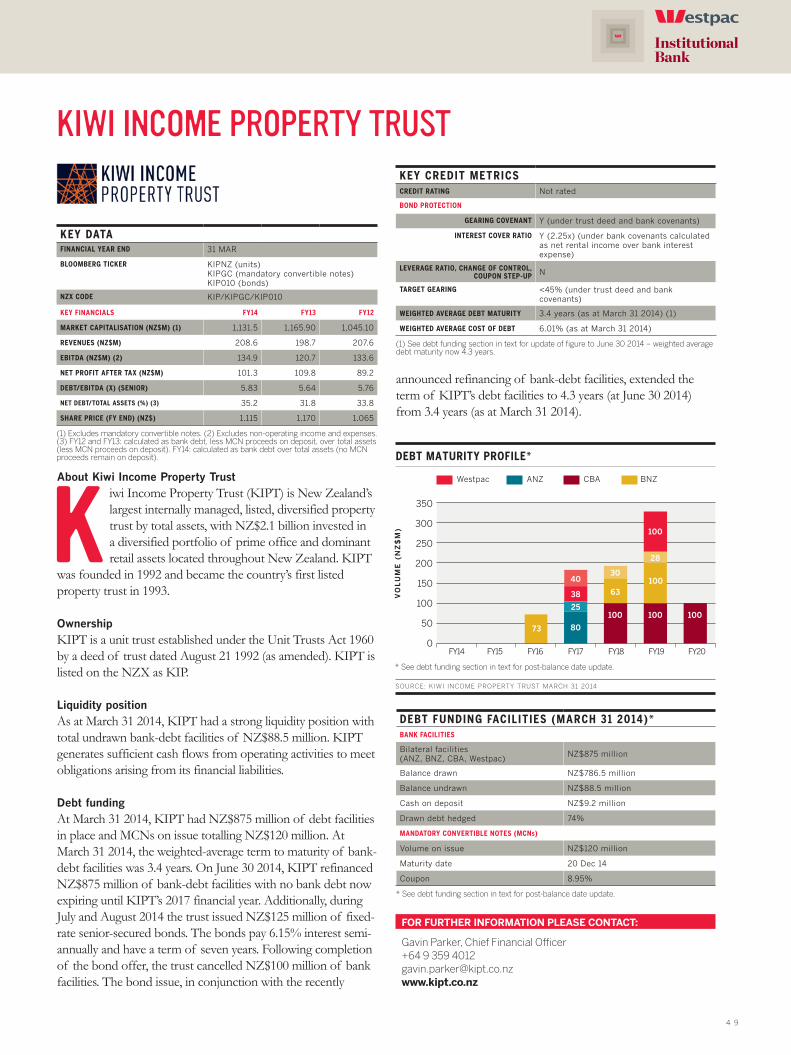

Liquidity positionAs at March 31 2014, KIPT had a strong liquidity position with total undrawn bank-debt facilities of NZ$88.5 million. KIPT generates sufficient cash flows from operating activities to meet obligations arising from its financial liabilities.

Debt fundingAt March 31 2014, KIPT had NZ$875 million of debt facilities in place and MCNs on issue totalling NZ$120 million. At March 31 2014, the weighted-average term to maturity of bank-debt facilities was 3.4 years. On June 30 2014, KIPT refinanced NZ$875 million of bank-debt facilities with no bank debt now expiring until KIPT’s 2017 financial year. Additionally, during July and August 2014 the trust issued NZ$125 million of fixed-rate senior-secured bonds. The bonds pay 6.15% interest semi-annually and have a term of seven years. Following completion of the bond offer, the trust cancelled NZ$100 million of bank facilities. The bond issue, in conjunction with the recently

FOR FURTHER INFORMATION PLEASE CONTACT:

Gavin Parker, Chief Financial Officer+64 9 359 [email protected]

KEY CREDIT METRICSCREDIT RATING Not rated

BOND PROTECTION

GEARING COVENANT Y (under trust deed and bank covenants)

INTEREST COVER RATIO Y (2.25x) (under bank covenants calculated as net rental income over bank interest expense)

LEVERAGE RATIO, CHANGE OF CONTROL, COUPON STEP-UP N

TARGET GEARING <45% (under trust deed and bank covenants)

WEIGHTED AVERAGE DEBT MATURITY 3.4 years (as at March 31 2014) (1)

WEIGHTED AVERAGE COST OF DEBT 6.01% (as at March 31 2014)

(1) See debt funding section in text for update of figure to June 30 2014 – weighted average debt maturity now 4.3 years.

KEY DATAFINANCIAL YEAR END 31 MAR

BLOOMBERG TICKER KIPNZ (units) KIPGC (mandatory convertible notes) KIP010 (bonds)

NZX CODE KIP/KIPGC/KIP010

KEY FINANCIALS FY14 FY13 FY12

MARKET CAPITALISATION (NZ$M) (1) 1,131.5 1,165.90 1,045.10

REVENUES (NZ$M) 208.6 198.7 207.6

EBITDA (NZ$M) (2) 134.9 120.7 133.6

NET PROFIT AFTER TAX (NZ$M) 101.3 109.8 89.2

DEBT/EBITDA (X) (SENIOR) 5.83 5.64 5.76

NET DEBT/TOTAL ASSETS (%) (3) 35.2 31.8 33.8

SHARE PRICE (FY END) (NZ$) 1.115 1.170 1.065

(1) Excludes mandatory convertible notes. (2) Excludes non-operating income and expenses.(3) FY12 and FY13: calculated as bank debt, less MCN proceeds on deposit, over total assets (less MCN proceeds on deposit). FY14: calculated as bank debt over total assets (no MCN proceeds remain on deposit).

DEBT FUNDING FACILITIES (MARCH 31 2014)*BANK FACILITIES

Bilateral facilities (ANZ, BNZ, CBA, Westpac)

NZ$875 million

Balance drawn NZ$786.5 million

Balance undrawn NZ$88.5 million

Cash on deposit NZ$9.2 million

Drawn debt hedged 74%

MANDATORY CONVERTIBLE NOTES (MCNs)

Volume on issue NZ$120 million

Maturity date 20 Dec 14

Coupon 8.95%

* See debt funding section in text for post-balance date update.

announced refinancing of bank-debt facilities, extended the term of KIPT’s debt facilities to 4.3 years (at June 30 2014)from 3.4 years (as at March 31 2014).

DEBT MATURITY PROFILE*

CBAWestpac ANZ BNZ

VO

LU

ME

(N

Z$

M)

350

300

250

200

150

100

50

0

SOURCE: KIWI INCOME PROPERTY TRUST MARCH 31 2014

10040

63

30

100100

28

38

8073

10025

100

FY15 FY16 FY17 FY18 FY19 FY20FY14

* See debt funding section in text for post-balance date update.