COA Annual Audit Report (2011) on the City of Iligan

182

Republic of the Philippines COMMISSION ON AUDIT Commonwealth Avenue, Quezon City ANNUAL AUDIT REPORT ON THE CITY OF ILIGAN For the Year Ended December 31, 2011

-

Upload

jess-villarin-quijano -

Category

Documents

-

view

265 -

download

16

description

The audit covered the accounts and operations of the city government of Iligan for the period January 1 to December 31, 2011. The audit was undertaken to ascertain the fairness in the presentation of the financial statements and adherence to prescribe laws,rules and regulations, and whether programs, activities and projects were carried out in an economical, effective and efficient manner.

Transcript of COA Annual Audit Report (2011) on the City of Iligan

Republic of the Philippines

COMMISSION ON AUDIT

Commonwealth Avenue, Quezon City

ANNUAL AUDIT REPORT

ON THE

CITY OF ILIGAN

For the Year Ended December 31, 2011

Republic of the Philippines

COMMISSION ON AUDIT

OFFICE OF THE REGIONAL DIRECTOR

Regional Office No. X

Cagayan de Oro City

April30, 2012

Honorable Lawrence Ll. Cruz

City Mayor

IliganCity

Sir:

We are pleased to transmit the Annual Audit Report (AAR) on the audit of the

accounts and operations of the City of Iligan for the year ended December 31, 2011, in

compliance with Article IX-D of the Philippine Constitution and pertinent provisions of

Section 43 of Presidential Decree No. 1445.

The AAR contains results of the audit, which was primarily conducted to

ascertain the propriety of financial transactions and compliance of the city with laws and

regulations. The financial and compliance audit, which was conducted on a test basis,

was primarily focused on the validity and propriety of transactions as well as the fairness

in the presentation of the financial statements. The details of these results, which included

positive and negative audit observations, as well as, the corresponding recommendations,

are discussed in the report.

We request that the recommendations be implemented and we would appreciate

being informed of the action taken hereon within one month from receipt hereof.

We acknowledge the cooperation extended to our Auditors by the officials and

employees of the City Government of Iligan.

Very truly yours,

By authority of the Chairman:

DONELO A. SESCON

Director III

Officer-in-Charge

Republic of the Philippines

COMMISSION ON AUDIT

Regional Office X

Audit Group J IliganCity

Office of the Supervising Auditor

April 24, 2012

DONELO A. SESCON Director III

Officer-in-Charge

COA Regional Office No.X

Cagayan de Oro City

Sir:

In compliance with Section 2, Article IX-D of the Philippine Constitution and

Section 43 of the Government Auditing Code of the Philippines (PD) 1445, we have

audited the Annual Audit Report (AAR) on the City of Iligan for the year ended

December 31, 2011.

The audit was conducted to ascertain the propriety of financial transactions and

the extent of compliance by the city with laws and regulations. It was also made to

ascertain the accuracy of financial records and reports, as well as the fairness in the

presentation of accounts in the financial statements.

Our attached report consists of four parts, Part I contains Audited Financial

Statements, Part II - Detailed Findings and Recommendations, Part III - the Status of

Prior Year’s Audit Recommendations, and Part IV – Annexes. The audit findings and

recommendations were discussed with concerned managementofficials and staffs in an

exit conference held on February 29, 2012.

As discussed in Part II of the attached report, the Cash Disbursing Officers

account of which the amount of P3,981,625.62pertains to the cash accountability of

Special Disbursing Officer who are already dead may no longer be liquidated and

considered loss of government funds. The balances of Property, Plant and Equipment

Accounts was understated by P350,101,622.53 due to non-recording of the Power Plant

acquired pursuant to Section 263 of the Local Government Code of 1991.

In our opinion, except for the effect of any adjustments, as might have been

required on the matter as discussed in the preceding paragraph, the financial statements

referred to above present fairly, in all material respects, the financial position of the City

of Iligan as of December 31, 2011 and the results of its operations and its cash flows for

the year then ended in accordance with applicable laws, rules and regulations and in

conformity with generally accepted accounting principles.

Our audit was conducted in accordance with the generally accepted state auditing

standards and we believe that it provides reasonable basis for the results of the audit. The

audit observations noted contained all the elements of an audit observation. The status of

implementation of prior years recommendations are likewise updated and validated.

We acknowledge the cooperation extended to us by the Officials and Staff of the

City Government of Iligan.

EXECUTIVE SUMMARY

A. Introduction

Iligan was created on June 16, 1950 under Republic Act 525. In November 22,

1983, it was declared Highly Urbanized City, in compliance with Memorandum Circular

No. 83-49 and Sections 166 and 168 of the Local Government Code. It is a Gateway to

Christian and Muslim Mindanao, and site of Mindanao’s electric power source. The city

is composed of 44 barangays with a total land area of81,337 hectares.

The city is considered stable and low-risk compared tomany surrounding areas of

Mindanao and its geographic positioning is advantageous as a commercial center. It has

high hopes for the development of its tourism and business related to its role as a

commercial center for Central Mindanao. Natural resources, such as waterfalls, coastline

and forest create favorable conditions for the development of tourism.

The administration in Iligan has staked on its ability to deliver law and order,

improving the accessibility and quality of the public water supply, house building

programs, improving garbage collection and public healthcare.

The City Government of Iligan is headed by City Mayor Lawrence Ll. Cruz. As

of December 31, 2011, the City Government has 4,564 employees consisting of 1,308

permanent; 11 co-terminus; 3,229 job orders; 14 elected and 2 ex-officio officials.

For the year under review, the City Treasurer is estimated to collect income of

P1,372,196,291.00 of which 62.21% or P853,673,770.00 came from its share in Internal

Revenue Allotment and 37.79% or P518,822,521.00 from tax revenue and other service

income to finance its program of expenditures classified into general public services,

social services and economic services in the total amount of P1,503,786,178.75. To fill

the variance between the estimated collectible income and proposed current operating

expenditures of P131,589,887.75, the City resorted to secure domestic loan of P75M;

reversion/realignment of some of prior years (continuing) and current year

appropriations, 20% Development Fund, of P 50,487,057.65, un-appropriated beginning

balance of P4,715,952.90 and reversion of certified obligations of P1,386,877.20 all

these are contained in the Supplemental Budget Nos. 1, 2, and 3 duly approved by the

Sanggunian Panlunsod of Iligan. In addition thereto, the city has a continuing

appropriation amounting to P716,025,316.52, accounted as P149,723,825.52 for 20%

Development Fund and General Fund Proper P566,301,491.00.

During the year the City government have collected the sum of

P1,298,226,495.19 from all sources, total current operating expenditures of

P1,008,009,788.97 inclusive of the amount of P256,847,636.41 utilized from continuing

appropriations, and net income of P290,216,706.22.

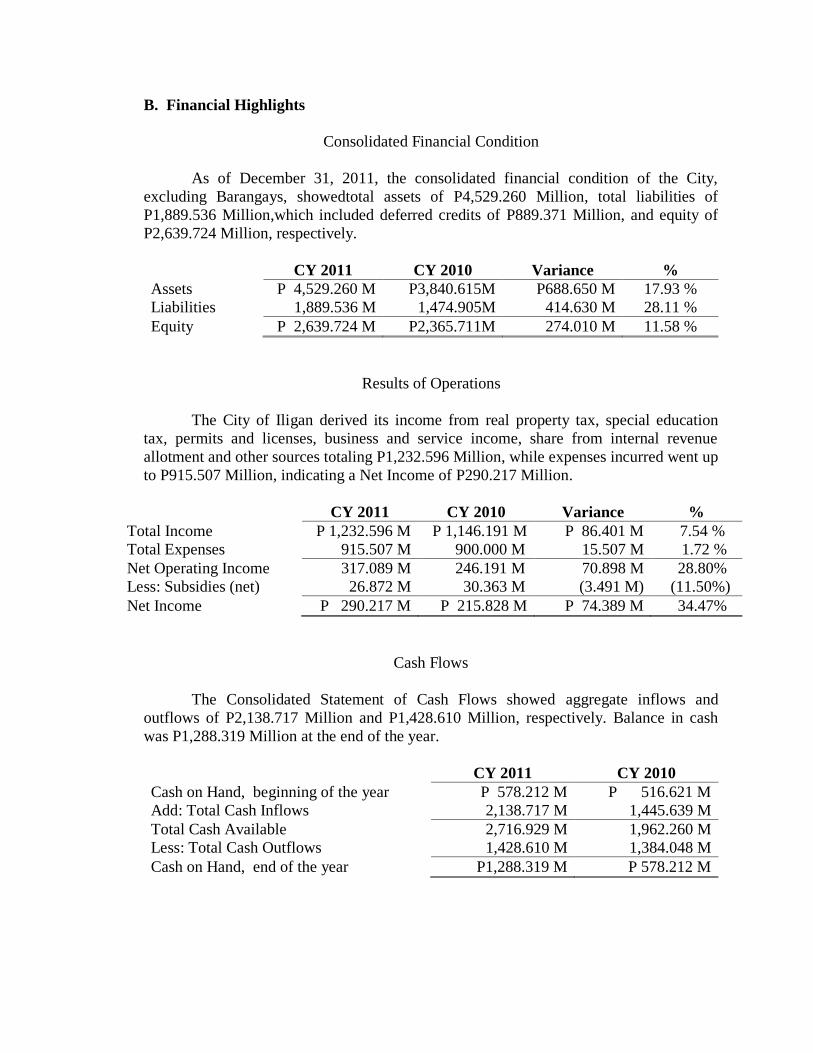

B. Financial Highlights

Consolidated Financial Condition

As of December 31, 2011, the consolidated financial condition of the City,

excluding Barangays, showedtotal assets of P4,529.260 Million, total liabilities of

P1,889.536 Million,which included deferred credits of P889.371 Million, and equity of

P2,639.724 Million, respectively.

CY 2011 CY 2010 Variance %

Assets P 4,529.260 M P3,840.615M P688.650 M 17.93 %

Liabilities 1,889.536 M 1,474.905M 414.630 M 28.11 %

Equity P 2,639.724 M P2,365.711M 274.010 M 11.58 %

Results of Operations

The City of Iligan derived its income from real property tax, special education

tax, permits and licenses, business and service income, share from internal revenue

allotment and other sources totaling P1,232.596 Million, while expenses incurred went up

to P915.507 Million, indicating a Net Income of P290.217 Million.

CY 2011 CY 2010 Variance %

Total Income P 1,232.596 M P 1,146.191 M P 86.401 M 7.54 %

Total Expenses 915.507 M 900.000 M 15.507 M 1.72 %

Net Operating Income 317.089 M 246.191 M 70.898 M 28.80%

Less: Subsidies (net) 26.872 M 30.363 M (3.491 M) (11.50%)

Net Income P 290.217 M P 215.828 M P 74.389 M 34.47%

Cash Flows

The Consolidated Statement of Cash Flows showed aggregate inflows and

outflows of P2,138.717 Million and P1,428.610 Million, respectively. Balance in cash

was P1,288.319 Million at the end of the year.

CY 2011 CY 2010

Cash on Hand, beginning of the year P 578.212 M P 516.621 M

Add: Total Cash Inflows 2,138.717 M 1,445.639 M

Total Cash Available 2,716.929 M 1,962.260 M

Less: Total Cash Outflows 1,428.610 M 1,384.048 M

Cash on Hand, end of the year P1,288.319 M P 578.212 M

C. Scope of Audit

The audit covered the accounts and operations of the city government of Iligan for

the period January 1 to December 31, 2011. The audit was undertaken to ascertain the

fairness in the presentation of the financial statements and adherence to prescribe laws,

rules and regulations, and whether programs, activities and projects were carried out in an

economical, effective and efficient manner.

D. Audit Opinion on the Financial Statements

The Auditor rendered a qualified opinion on the financial statements based on the

examination conducted which is in accordance with the applicable laws, rules and

regulations and the generally accepted auditing standards.

E. Significant Audit Findings and Recommendations

The following are some of the significant findings and recommendations in the audit of the

City Government of Iligan for the year 2011:

A. Value-for-Money Audit

The city government had wasted government funds in the amount of P3,126,800.00

as an interest for one on one loan secured with the DBP in the amount of P47.0M at

6% per annum for the non-implementation of the projects funded out of the

proceeds of the loan. Likewise, the amortization of the loan amounting to P75.0M

was not included in the annual budget for Calendar Year 2011.

We recommended that: a) the proponent(s) of project(s) sourced from the

proceeds of loan should adequately plan and program the proposal project

before negotiating loan with any Government Financial Institution (GFI’s).

The proposed project should be included in the three (3), five (5) or ten (10)

years development plan of the City Government; b) the SP shall invite the

proponent of the project , the City Planning & Development Officer, and the

local finance committee (LFC) for an executive session to friendly discuss

the viability of the project before a SP Resolution is pass authorizing the City

Mayor to negotiate a loan; c) as soon as the GFI’s approved the loan, the

proponent shall coordinate with City Engineer, the CGS officer, the LFC and

the BAC for the conduct of pre-procurement process to ensure timely

implementation of the propose project and d) upon release of the loan, the

BAC shall award the project to the lowest calculated & responsive bid

(LCRB).

Financial assistance received in checks and cash in the total amount of

P363,541,553.22for the flood victims of “Typhoon Sendong” have remained intact

and deposited with the LBP and DBP for the accounts of the City Government of

Iligan.Likewise, as of January 31,2012 no disbursements was recorded.

We recommendedthat: a) the City Treasurer to open an account either with

the LBP and/or LBP specifically for calamity fund for Typhoon Sendong to

ensure transparency and accountability; b) the City Treasurer is required to

deposit future financial assistance received and caused the transfer of said

fund deposited to the LBP and DBP, as validated by the respective head of

the bank, to said newly opened account to fast track monitoring, facilitate

verification of the account balances and ensures that account

debited/credited to this account is exclusively for the account of “Typhoon

Sendong “; c)the Sangguniang Panlunsod shall pass and approve the Special

Budget for the utilization of the calamity fund in order the City Mayor can

zero in or focus in the implementation of identified infrastructure projects

focus on the welfare of the flood victims; d) to fast track the implementation

of the calamity projects/programs, the Budget Office shall immediately

release the fund appropriated for the calamity fund projects/programs; The

BAC Chairman shall give utmost priority in the time schedule of the conduct

of public bidding for the infrastructure projects, and the City Accountant’s

Office shall designate accounting personnel to expedite the processing of

disbursement vouchers related to calamity funds; e) the City Accountant

shall render financial report copy furnished the City Auditor and submit all

financial records, such as disbursement vouchers, payrolls, if any, monthly

bank reconciliation statements together with the checks encashed or paid by

the bank for post audit and final custody; f) the implementer office shall see

to it that the utilizations and disbursements of the calamity fund must comply

to appropriate law, auditing rules and regulations. Strictly comply the

DSWD shelter assistance guidelines and render progress and terminal report

to the City Mayor, City Vice Mayor and City Councilors copy furnished the

City Auditor and the concern offices; g) related government expenditures

incurred by the personnel of the implementing office in connection with the

implementation of the calamity fund projects shall be proper charged to the

regular budget appropriated for thier office; h) the City Mayor and upon

request by higher authority or by the Department Secretary concern shall

render final report, copy furnished the Vice Mayor and SP members and the

City Auditor; i) in case the negotiation on the acquisition of the 15.9 has.

failed, seek assistance/intervention from the national government.

B. Financial and Compliance Audit:

Cash Disbursing Officers account has increased by 9,678,814 or 131%,

liquidations/refunds of prior years accounts was 652,945 or measly 8.12% and

probable loss of in the amount of P3,981,625.62 or 53.89%, thus, resulting also in

the overstatement of Government Equity by P7,388,823.

We recommended that the City Accountant to: a) sent notice of

liquidation/refund to the Special Disbursing Officer (SDO) still employee in

the city government including those who havealready retired, resigned and

separated from the service but are still livingfor the immediate settlement of

his/her cash advance. Copy furnished the City Legal Office and the

Commission on Audit. After six (6) months, the notice was received, yet no

action taken by the concern SDO/employee, request the City Legal Office to

institute administrative charge; b) identify and document those former SDO

but already dead and submit to the Sangguniang Panlungsod for the

adoption of a resolution to request the Commission for the write-off of their

unliquidated cash advance. In this case, the City Accountant shall properly

coordinate with the City Auditor for his comments, evaluation, review and

submission of additional documents if needed in the request; andc) institute

measures to limit the number of SDO to be granted with cash advance and

see to it that the requirement on the bonding of the SDO shall be strictly

adhered to and no cash advance shall be granted unless it is for public

purpose and availability of sufficient appropriation is provided and cash

advance request to circumvent the procurement law must not be allowed.

The Power Plant (IDPP 1 & IDPP 2) which was finally turnover by PSALM/NPC to

the City Government on December 16, 2010 was not recorded/booked in the latter’s

book of accounts, thus, the PPE and Government Equity was understated by

P350,101,622.53, the amount which the former owed to the latter for unpaid Real

Property Tax, as of March 2007.

We recommendedthat the City Accountant to: a) book/ record the Power

Plant at a book value equal or equivalent of the unpaid RPT from

NPC/PSALM as advertised on April 2, 2007 in the amount of

P350,101,622.53 and b) adjust the contra accounts under the General Fund

and Special Education Fund for the respective portion of the amount as

recorded.

The City Government had appropriated funds for Security, General and Janitorial

Services,averaging monthly of 3,229 Job Orders (JOs) Personnel, in the amount of

P59.2M and spent P 82,421,798.34 for undefined local projects, contradicts Section

77, RA 7160 and the number of JOs hired is excessive runs counter to COA Circular

Nos. 85-55A and 2002-003.

We recommendedthat: a) the City Mayor may employee emergency or casual

employees or laborers paid on a daily wage or piece of work basis and hired

through job orders for local projects authorized by the Sanggunian

Panglunsod pursuant to section 77, RA 7160 (LGC) and see to it that these

local projects are consistent with Section 16 and within those identified in

Section 17 of the LGC; b) limit the number of personnel hired on job orders

by evaluating the mission and thrust whether the services needed is

supportive to the implementation of their objectives; c) limit the expenditures

on General Services, Janitorial Services and Security Services and re-visit

COA Circular No. 2002-003 as amended, as to what particular object of

expenditures may be properly charged to these accounts d) Concern

department/office head to submit the PAPs and justify the hiring of personnel

thru job orders; e) Salary of hired JO’s personnel shall be charged to

personal services; and f) in case the city government needs personnel to

maintain the orderliness, sanitation and hygiene, cleanliness, beautification

and good ambiance in the various offices, hire the services of agency

specializing for janitorial services.

Overtime pay in the amount of P 1,867,085.29, out of it, P382,494.45 pertains to

Buhanginan (city government) Voice, paid to some city government employees for

services rendered beyond regular office hours and during weekends and holidays

for works or activities, some of which are not allowable pursuant to National Budget

Circular No. 410 dated April 28, 1990.

We recommended that: a) the head of the agency and/ or the local chief

executive shall determine among the offices of the city government who will

be granted to render overtime base on the IRR of Memorandum Circular

N0. 228 (NBC No. 410 dated April 28, 1990). For this purpose, an executive

order should be issued; b) the department/office head of the

department/office determined or identified by the LCE shall identify the

specific activities cover by the IRR related to the functions of their

department/office: c) the department/office head of the concern

department/office shall state the purpose, duration, list of employees,

justification and the source of fund in their request for authority to render

overtime with compensation; and d) the concerns department/office head

shall strictly follow the funding source and cost limitation provided in the

IRR (NBC No. 410).

Honoraria of the personnel involved in the procurement processes was sourced from

the General Fund appropriation of P 2.0M instead of P 330,663 collections source

from the specific procurement activities provided in DBM Budget Circular 2007-3,

thus payment of honoraria in excess from the actual proceeds may be considered

irregular, unnecessary and excessive.

We recommendedthat: a) require the Head, BAC Secretariat to prepare

report on the number of projects bidded, project completed procurement

or procurement contracts awarded to support claimed for honoraria; b)

limit the payment of honoraria to the source identified in Budget Circular

No. 2007-3 dated November 29, 2007 and to the savings from the local

budget approved by the Sangguniang Panlungsod; c) limit the number of

person involved in TWG to at least three (3) per procurement project. The

person with technical expertise on a particular procurement project shall

be designated as chair; and d) provide BAC Secretariat to at least three

(3) including the Head to each procurement project.

Programs, Activities, Projects (PAPs) approved by the Sangguniang Panlungsod

funded from the LDRRM Fund amounting to P 67,485,600 to mitigate disaster was

not implemented while P28,922,000 for Quick Response Fund (QRF) of which

P7,529,213.37was disbursed for the relief and rehabilitation operationsaftermath of

“Typhoon Sendong”.

We recommended that: a) the City Government shall fully establish and

organize the LDDRM office with able, responsible and full time head and

staff which shall perform inherent functions in the disaster preparedness

as stated in Section 12 (c) of RA No. 10121 and its IRR; b) see to it that

during the declaration of the State of Calamity, Local officials shall make

mandatory undertaking remedial measures as provided in Section 17 (a,

b, c,& d) of RA No. 10121 and its IRR; c) ensure that all related PAPs to

be funded from the LDRRMF will support the disaster risk reduction and

management activities during the pre disaster preparedness programs and

post disaster activities; and d) after post disaster activities, the DRRM

officer shall prepare and submit terminal report on the utilization of

LDRRMF to the City Auditor.

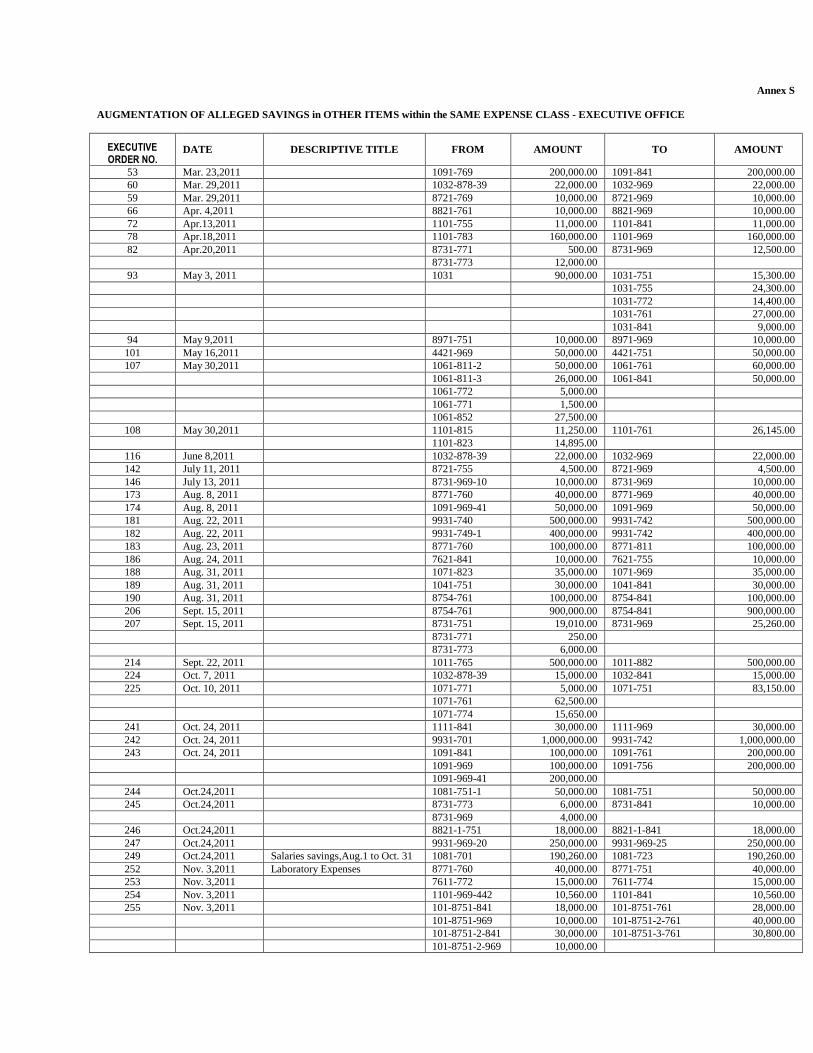

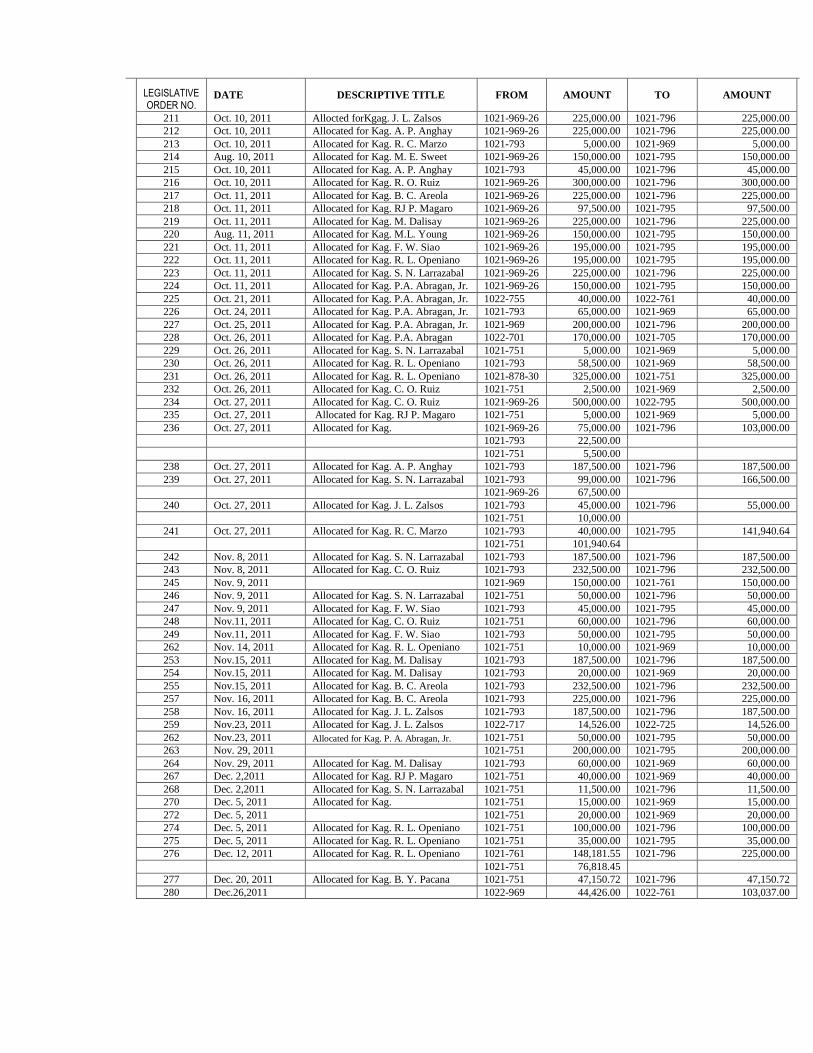

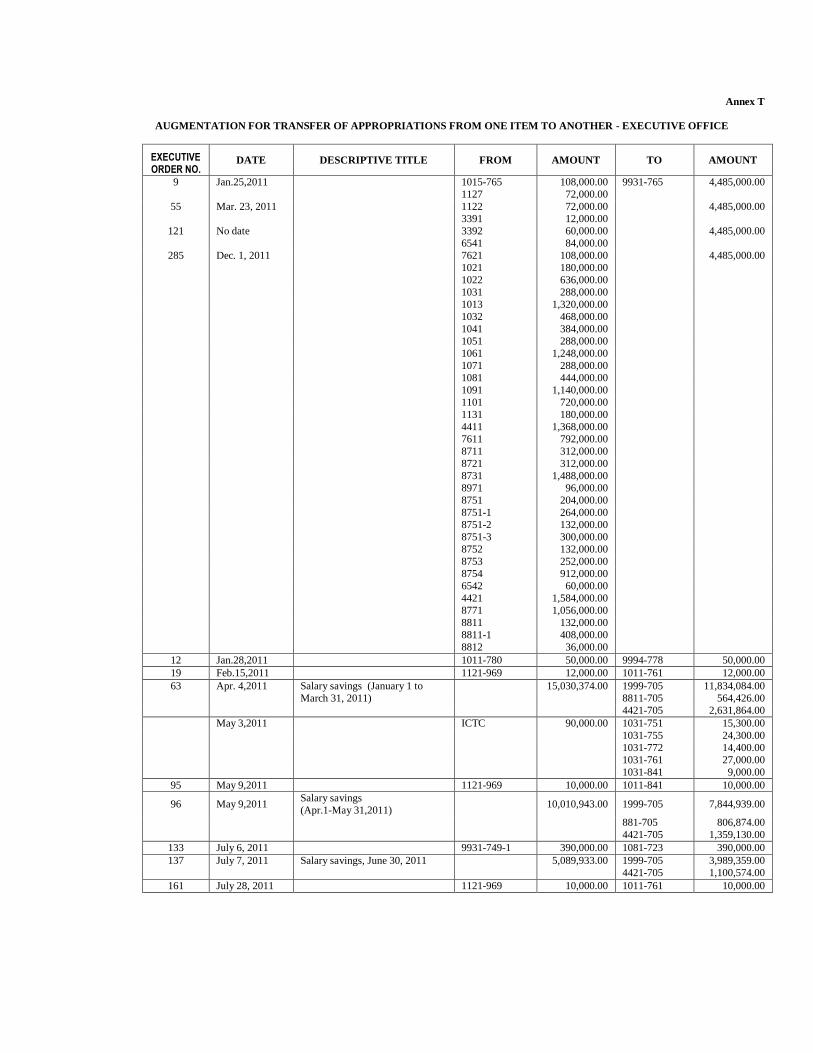

The preparation, authorization and execution of the annual budget for General

Fund and Special Accounts Fund are inefficient due to often declaration of alleged

savings for augmentationin the amount of P 159,030,310.80pursuant to Section 336,

the local Code in some instances, the exercise of the authority, contradicts Section

322 of the same Code.

We recommendedthat the City Mayor shall: a) direct all department/office

to submit their budget proposals to the local chief executive (LCE) thru the

local financing committee (LFC) on or before the 15th

of July of each year.

Said budget proposals shall be prepared in accordance with the AIP, and

guidelines and spending ceilings contained in the Budget Call and the

other general requirements prescribed under Section 317 of RA 7160 ( the

Local Code); b) re-visit the provision of Section 336 of the Code as well as

the provision of City Ordinance No. 2060, series of 1992 by restating this

authority as a general provision of the Annual Budget of each year to

ensure that unexpended balances of appropriations will not be included as

source of fund for augmentation; and c) department/office head shall

observe prudence in the proper allocation of their respective

appropriations to ensure attaining the objectives of their programs,

projects, activities (PPAs).

F. Favorable Observations

Five (5) out of Five (5) Audit Observations and Memorandum (AOMs) issued in

Calendar Year 2011 were implemented at the year end and at the beginning of

Calendar Year 2012.

G. Status of Implementation of Prior Year’s Audit Recommendations

Of the thirty-two (32) prior years’ audit recommendations, 28% or 9 were fully

implemented, 28% or 9 were partially implemented and 44% or 14 were not

implemented.

TABLE OF CONTENTS

Page

PART I – FINANCIAL STATEMENTS

Independent Audit Report’s

Statement of Management Responsibility

Financial Statements:

Consolidated Balance Sheet.

Consolidated Statement of Income and Expenses

Consolidated Statement of Cash Flows

Notes to Financial Statements

PART II – DETAILED FINDINGS & RECOMMENDATIONS

Value for Money Audit

Financial and Compliance Audit

PART III – STATUS OF IMPLEMENTATION OF PRIOR YEAR’S

RECOMMENDATIONS

PART IV – ANNEXES

1

2

3

5

6

8

23

28

36

68

78

Part I – Audited Financial Statements

Republic of the Philippines

COMMISSION ON AUDIT

Office of the Regional Director

Regional Office No. 10 Cagayan de Oro City

INDEPENDENT AUDIT REPORT’S

We have audited the accompanying Consolidated Balance Sheet of the City of

Iligan as of December 31, 2011 and the related Statements of Income and Expenses and

Cash Flows for the year then ended. These financial statements are the responsibility of

the City Government of Iligan’s Management. Our responsibility is to express an opinion on these financial statements based on our audit.

We conducted our audit in accordance with laws, COA and INTOSAI standards,

and applicable generally accepted auditing standards. Those standards require that we

plan and perform the audit to obtain reasonable assurance about whether the financial

statements are free of material misstatement/s. The audit includes examining, on a test

basis, evidence supporting the accounts and disclosures in the financial statements. It also

includes assessing the accounting principles used and review of significant estimates

made by the management as well as evaluating the over-all financial statements

presentation. We believe that our audit provides a reasonable basis for our opinion.

As discussed in Part II of the attached report, the Cash Disbursing Officers

account of which the amount of P3,981,625.62pertains to the cash accountability of

Special Disbursing Officer who have already separated from the service may no longer

be liquidated and considered loss of government funds. The balances of Property, Plant

and Equipment Accounts was understated by P350,101,622.53 due to non-recording of

the Power Plant acquired pursuant to Section 263 of the Local Government Code of

1991.

In our opinion, except for the effect of any adjustments, as might have been

required on the matter as discussed in the preceding paragraph, the financial statements

referred to above present fairly, in all material respects, the financial position of the City

of Iligan as of December 31, 2011 and the results of its operations and its cash flows for

the year then ended in accordance with applicable laws, rules and regulations and in

conformity with generally accepted accounting principles.

By: COMMISSION ON AUDIT

February 28, 2012

Republic of the Philippines

CITY OF ILIGAN

OFFICE OF THE CITY MAYOR

STATEMENT OF MANAGEMENT RESPONSIBILITY

FOR FINANCIAL STATEMENTS

The Management of the CITY GOVERNMENT OF ILIGANis responsible for all information and representation contained in the Consolidated Balance sheet as of

December 31, 2011 and the related Consolidated Statement of Income and Expenses and

Statement of Cash Flows for the period ended. The financial statements have been

prepared in conformity with generally accepted accounting principles and reflect amounts

that are based on best estimates and informed judgment of management with an

appropriate consideration of materiality.

In this regard, management maintains a system of accounting and reporting which

provides for the necessary internal controls to ensure that transactions are properly

authorized and recorded, assets are safeguarded against unauthorized use or disposition

and liabilities recognized.

3

Republic of the Philippines

CITY GOVERNMENT OF ILIGAN

CONSOLIDATED BALANCE SHEET

As of December 31, 2011

(With Comparative Figures for 2010)

2011 2010

ASSETS

Current Assets:

Cash, (Note 3) 1,288,318,945.11 578,211,600.47

Receivables, (Note 4) 1,001,635,179.76 1,096,562,671.97

Inventories, (Note 5) 4,706,104.00 4,676,160.00

Prepayments, (Note 6) 33,738,887.97 36,758,785.58

Other Current Assets 80,000.00 80,000.00

Total Current Assets 2,328,479,116.84 1,716,289,218.02

Investments:

Investments in Securities, (Note 7) 6,000,000.00 6,000,000.00

Total Investments 6,000,000.00 6,000,000.00

Property, Plant & Equipment (Net of Depreciation)

Land and Land Improvements 326,428,216.33 311,612,895.52

Buildings 494,274,491.27 485,898,821.50

Leasehold Improvements 2,486,484.71 2,486,484.71

Office Equipment, Furniture and Fixtures 123,795,673.43 126,317,788.52

Machineries and Equipment 134,533,534.45 135,079,492.08

Transportation Equipment 93,009,220.21 101,403,551.16

Other Property, Plant and Equipment 264,446,255.12 264,872,759.77

Public Infrastructures 170,264,101.70 170,538,000.69

Reforestation Projects 49,500.00 49,500.00

Construction in Progress 553,298,024.49 488,211,760.38

Total Property, Plant and

Equipment, (Note 8) 2,162,585,501.71 2,086,471,054.33

Other Assets, (Note 9) 32,195,520.49 31,855,020.49

TOTAL ASSETS 4,529,260,139.04 3,840,615,292.84

4

LIABILITIES AND EQUITY

LIABILITIES

Current Liabilities, (Note 10) 662,995,470.11 197,659,482.80

Long-Term Liabilities,( Note 11) 337,168,765.41 262,603,167.14

Deferred Credits, (Note 12) 889,371,435.96 1,014,641,897.06

Total Liabilities 1,889,535,761.48 1,474,904,547.00

EQUITY

Government Equity, Beg. 2,365,710,745.84 2,280,089,049.94

Add/Deduct:

Retained Operating Surplus 290,216,706.22 215,827,917.60

Prior Year's Adjustments 3,071,726.47 (99,898,118.81)

Transfers to Registry (19,274,710.97) (30,308,102.89)

Government Equity, End (Note 13) 2,639,724,467.56 2,365,710,745.84

TOTAL LIABILITIES AND EQUITY 4,529,260,139.04 3,840,615,292.84

See Accompanying Notes to Financial Statements

5

Republic of the Philippines

CITY GOVERNMENT OF ILIGAN

CONSOLIDATED STATEMENT OF INCOME AND EXPENSES

For the year December 31, 2011

(With Comparative Figures for CY 2010)

2011 2010

INCOME, (Note 14)

Local Taxes 231,642,149.73 211,248,590.78

Internal Revenue Allotment 853,673,770.00 793,816,617.00

Permits and Licenses 8,167,651.62 7,632,177.78

Service Income 16,985,799.03 15,824,028.65

Business Income 90,174,625.70 82,765,110.23

Other Income 31,951,729.05 34,904,802.85

Total Income 1,232,595,725.13 1,146,191,327.29

Less: EXPENSES, (Note 15)

Personal Services 490,794,856.47 471,484,032.03

Maintenance and Other Operating

Expenses 394,069,044.29 399,336,004.35

Financial Expenses 30,643,124.10 29,180,311.67

Total Expenses 915,507,024.86 900,000,348.05

NET OPERATING INCOME 317,088,700.27 246,190,979.24

Add: Subsidies to Other Funds 65,630,770.06 58,666,401.85

Total 382,719,470.33 304,857,381.09

Less: Subsidies to Other LGUs 6,483,816.00 5,700,000.00

Subsidies to NGO's/PO's 7,711,993.42 10,557,329.44

Subsidies to Other Funds 66,830,770.06 63,311,969.85

Subsidies to NGA's

Donations 11,476,184.63 9,460,164.20

Total 95,502,764.11 89,029,463.49

NET INCOME 290,216,706.22 215,827,917.60

See Accompanying Notes to Financial Statements

6

Republic of the Philippines

CITY GOVERNMENT OF ILIGAN

CONSOLIDATED STATEMENT OF CASH FLOWS

For the year ended December 31, 2011

(With Comparative Figures for 2010)

2011 2010

Cash Flows from Operating Activities

Cash Inflows:

Share from Internal Revenue Collections 853,673,770.00 793,816,617.00

Collection from Taxpayers 360,483,134.93 331,421,186.52

Receipts from Sale of Good and Services 13,099,014.23 11,567,583.34

Interest Income 5,443,666.31 8,059,411.50

Other Receipts 718,814,417.97 224,515,081.67

Total Cash Inflows 1,951,514,003.44 1,369,379,880.03

Cash Outflows:

Payments:

To Suppliers/Creditors 364,095,613.65 448,883,240.16

To Employees 663,395,528.18 642,794,731.00

Interest Expense 30,309,341.82 27,899,780.39

Other Disbursements 235,985,012.53 170,293,456.37

Total Cash Outflows 1,293,785,496.18 1,289,871,207.92

Net Cash Operating Activities 657,728,507.26 79,508,672.11

Cash Flows from Investing Activities:

Cash Inflows:

Sale of Property, Plant and Equipment 0.00 0.00

Sale of Debt Securities of Other Entities 0.00 0.00

Collection of Principal on Loans to Other

Entities 0.00 0.00

Total Cash Inflows 0.00 0.00

Cash Outflows:

Purchase Property, Plant & Equipment

and

Public Infrastructures 22,186,760.89 39,379,074.44

Purchase Debt Securities of Other Entities 0.00

Grant/Loans to Other Entities 0.00

Total Cash Outflows 22,186,760.89 39,379,074.44

Net Cash from Investing Activities (22,186,760.89) (39,379,074.44)

7

Cash Flows from Financing Activities

Cash Inflows:

Issuance of Debt Securities 0.00

Acquisition of Loan 187,203,218.73 76,258,691.50

Total Cash Inflows 187,203,218.73 76,258,691.50

Cash Outflows:

Retirement/Redemption of Debt

Securities 0.00 0.00

Payment of Loan Amortization 112,637,620.46 54,797,699.13

Total Cash Outflows 112,637,620.46 54,797,699.13

Net Cash from Financing Activities 74,565,598.27 21,460,992.37

Net Increase in Cash 710,107,344.64 61,590,590.04

Cash at Beginning of the Year 578,211,600.47 516,621,010.43

Cash at the End of the Period 1,288,318,945.11 578,211,600.47

See Accompanying Notes to Financial Statements

8

Notes to Consolidated Financial Statements

(With Comparative Figures for 2010)

Note 1: General Profile of the City Government of Iligan

1.1 Iligan became a chartered city through RA 525 on June 16, 1950 and on 19

September 2001 the city was transferred from Region 12 to Region 10 by

virtue of EO No. 36. Based on national and regional development plans,

IliganCity is envisioned to be the industrial center in the Northern Mindanao

Growth Area and a sub-regional growth center for education, service and

recreation, among others. The city plays a key role in the development of the

region as it supplies most of the area’s electrical power. In addition, it has

great eco-tourism potential with the presence of a number of waterfalls and

water features. The influx of immigrants due to the city’s industrial boom in

the 1950s through the 1980s, coupled with its natural population growth,

created a strain, not only in urban space, but also on the capacity of the local

government to deliver services and provide employment and livelihood

opportunities. To address urban social ills, the city aims to implement a

comprehensive human resource development approach that focuses on

education and training; health, nutrition and socialized housing; and poverty

alleviation.

1.2 IliganCity has a land use plan and an area development framework, which aim

to locate public and community services strategically, to properly allocate

land towards sustainable development, and to rezone excess lands to allow

new developments for socioeconomic ends. Iligan has a relatively adequate

transport system and is accessible from major Philippine cities through air,

water, and land.

Note 2: Summary of Significant Accounting Policies

2.1 Basis of Financial Statements Presentation.

2.1.1 The statements have been prepared in accordance with generally

accepted state accounting principles and standards.

2.1.2 The consolidated financial statements consist of transactions from the

General Fund, Special Education Fund and Trust Fund.

2.2 Accounting Policies Observed for Each Account

2.2.1 The city uses accrual basis of accounting. All expenses are recognized

when incurred and reported in the financial statements in the period to

which they relate. Income is on accrual basis except for transactions

where accrual basis is impractical or when law requires other methods.

9

2.2.2 Allowance for doubtful accounts are maintained at a level adequate to provide

for potential uncollectibility of receivables. A review of the

receivables, designed to identify accounts to be provided with

allowance is made on a regular basis.

2.2.3 The Modified Obligation System is used to record allotments received

and obligations incurred. Separate registries are maintained to control

allotments and obligations for each class of allotment.

2.2.4 The costs of ending inventory of office supplies and materials and

other inventory items are computed using the Moving Average

Method.

2.2.5 Supplies and materials purchased for the inventory purposes are

recorded using the Perpetual Inventory System.

2.2.6 Petty Cash Fund (PCF) account is maintained under the Imprest

System. All replenishments are directly charged in the expense

account. The PCF is not used to purchase regular inventory items for

stock.

2.2.7 Property Plant and Equipment are carried at cost less accumulated

depreciation.

2.2.8 Bonus paid to contractors for early completion of the work was added

to the total cost of the project while liquidated damages paid for by the

contractor for delayed completion of the project was deducted from the

project cost.

2.2.9 For assets under construction, all related expenses incurred during the

construction of the project are capitalized and those incurred after the

construction are charged against the operating cost.

2.2.10 The construction period theory shall also apply for expenditures on

infrastructure projects of the Trust Funds. For other projects,

expenditures shall be debited to the appropriate expenditure account.

Expenditures shall be closed to Project Equity account at year-end or

upon project completion, whichever comes first.

2.2.11 Properties of the government, which are used by the general public,

are accounted for under the Public Infrastructures/Reforestation

Projects. These are dropped from Property, Plant & Equipment

account and recorded in the Registry of Public

Infrastructure/Reforestation Projects.

10

2.2.12 Public Infrastructures/Reforestation Projects and serviceable assets not

used in operation are not subject to depreciation.

2.2.13The Straight Line Method of depreciation is used in depreciating the

Property, Plant & Equipment with estimated useful lives ranging from

five to fifty years. A residual value, computed at ten percent of the cost

of asset is set and depreciation starts on the second month after

purchase.

2.2.14 Payable accounts are recognized and recorded in the books of accounts

only upon acceptance of the goods/inventory/other assets and rendition

of services to the agency.

2.2.15Accounts were again reclassified in conformity with the revised new

Chart of Accounts prescribed under COA Circular No. 2003-002 dated

August 1, 2003.

2.2.16 Financial expenses such as bank charges are separately classified from

MOOE.

2.2.17Transactions in foreign currencies are recorded in Philippine Peso based

on the BSP rate of exchange prevailing at the date of transactions.

2.2.18Foreign currency denominated monetary assets and liabilities at balance

sheet date is restated based on BSP exchange rate at the date. Foreign

exchange gains/losses are recognized in the books of accounts.

2.2.19Fundamental errors of prior years are corrected by using the Prior

Year’s Adjustment account. Errors affecting current year’s operation

are charged to the current year’s accounts.

Note 3: Cash and Cash in Banks P 1,288,318,945.11

Compositions of cash and cash in banks are as follows:

Account Title GF SEF TF CY 2011 PY 2010

Cash in Vault - - - - 590.80

Cash-Disbursing Officers

13,267,502.57 991,332.54 2,808,802.03 17,067,637.14 8,041,768.06

Petty Cash Fund 133,243.40 - - 133,243.40 137,021.65

Cash in Bank-LC,

Current Acct. 595,003,916.10 33,922,276.02 419,164,346.85 1,048,090,538.97 350,878,203.43

Cash-Bank-LC, Time Deposit

184,866,957.55 22,535,368.64 15,625,199.41 223,027,525.60 219,154,016.53

Total 793,271,619.62 57,448,977.20 437,598,348.29 1,288,318,945.11 578,211,600.47

11

• Total cash balances as of December 31, 2011 for all

funds amounted to P 1,288,318,945.11, comprising the

General Fund, Special Education Fund and the Trust Fund,

with an amount of P793,271,619.62 , P57,448,977.20

and P437,598,348.29 , respectively. A portion of the General Fund ,

included Cash in Bank - Current Accounts representing deposits held in

trust . Transactions submitted after February 11, 2012 were not included .

• Cash balances per books differ from bank due to outstanding checks, deposit-

in-transit and other reconciling items which are shown in detailed per Bank

Reconciliation Reports.

• In connection with the city's approved term loan with Land Bank of the

Philippines-Iligan Branch with principal amount of P 445.50M and P 50M

equity on the development and expansion of Iligan City Water System

Project, additional releases in the following amount are as follows : P

14,476,166.24; P 17,272,705.25 ; P 69,574,896.52 ; and P 85,879,450.72 ,

representing second, third, fourth and fifth releases, respectively. Amount

directly debited by the bank as payment in favor of the Contractor and

suppliers, representing cost of billing of the said project were not recorded

due to insufficient documents needed for proper recording.

• Hold out deposit under Development Bank of the Philippines-Time Deposits,

are as follows :

ACCOUNT EFFECTIVITY DATE

NUMBER NAME Dec. 15, 2010* Feb. 01, 2011** April 5, 2011** Sept. 9, 2011***

0820-016198-160 ILIGAN CITY

GOVERNMENT 40,650,000.00 70,650,000.00 23,650,000.00 13,650,000.00

0820-017665-160 NATIONAL

WEALTH 30,000,000.00

Total Amount Held 70,650,000.00 70,650,000.00 23,650,000.00 13,650,000.00

* Effectivity date of LGU 's request for the transfer of hold-out on

deposit amounting to P 30M from SSD No. 0820-017665-160 to SSD

No. 0820-016198-160.

** Release of P 47M hold -out amount due to full payment of loan.

*** Release of P10M hold-out amount due to payment of IBJT Loan.

12

Note 4: Receivables P 1,001,635,179.76

This account includes the following:

Account Title GF SEF TF CY 2011 PY 2010

Account Receivable - - - - -

Due from Officers & Employees

7,552,683.02 311,905.95 232,945.70 8,097,534.67

9,577,909.72

Loans Receivable,

Others 7,110,507.04 1,580,341.16 8,690,848.20

10,065,390.14

Real Property Tax Receivable

471,856,200.59 471,856,200.59

537,333,419.93

Special Edu. Tax

Receivable 408,755,365.54 408,755,365.54

468,606,443.55

Due from NGAs 6,397,110.19 6,397,110.19 1,207,000.00

Due from GOCC’s 1,285,000.00 1,285,000.00 1,285,000.00

Due from LGUs 81,888,862.75 81,888,862.75 51,325,833.46

Due from NGOs/POs 6,995,809.51 2,000,000.00 8,995,809.51 8,874,258.55

Due from other Funds 2,243,371.51 79,586.60 2,322,958.11 4,829,966.15

Receivables-

Dis./Charges 3,156,660.16 41,763.18 3,198,423.34

3,254,823.34

Other Receivables 146,966.66 100.20 147,066.86 202,627.13

Total 588,633,171.43 411,109,034.67 1,892,973.66 1,001,635,179.76 1,096,562,671.97

• Total Receivables as of December 31, 2011 , P 1,001,635,179.76 shows

a rapid decrease of P 94,927,492.21 against December 31, 2010 balance

of P 1,096,562,671.97 . Material amount of reductions from Due to Officers

and Employees, RPT and SEF receivables, Due from NGAs and Due from

GOCCs and Due from Other Funds.

• Due from Officers and Employees , as of December 31,

2011 reduces by P 1,480,375.05 for all funds. Under the

General Fund, total reduction amounted to P 1,315,447.57, as a

result of liquidations submitted .

• RPT and SEF Receivables of P 471,856,200.59 and P 408,755,365.54,

respectively represents the uncollected amounts due from taxpayers for basic

real property taxes and additional levy on real property taxes accruing to

General Fund and Special Education Fund for the year 2011. Subject for

adjustments and reconciliation , due to some delinquent taxpayers which can

no longer be located, availment of tax amnesties, company's

bankrupcy/disclosure, etc. pending submission of the complete records from

the City Treasurer's Office .

• Due from LGU’s of P 81,888,862.75 represents barangay projects funded

from their barangay share on the 20% development fund of the city. Full

settlement/liquidatiions of all fully implemented and completed projects

were required. Increased in amount resulted from some projects not yet fully

13

completed when another fund transfer was made in less than a year. LGUs

with no outstanding balances transferredfunds from the city to there respective

barangay funds and failure of some LGUs to submitted proper documents of

completed projects to the office of the city accountant for recording in the

books of accounts.

Note 5: Inventories P 4,706,104.00

This account consist of :

Account Title GF SEF TF CY 2011 PY 2010

Office Supplies Inventory 102,089.50 1,700.00 103,789.50 52,209.50

Accountable Forms Inventory 141,076.19 141,076.19 162,712.19

Drugs and Medicine Inventory 791,211.90 791,211.90 788,711.90

Medical, Dental and Laboratory 488,305.00 488,305.00 490,805.00

Gasoline, Oil and Lubricants Inventory 822,073.41 822,073.41 822,073.41

Other Supplies Inventory 293,148.00 293,148.00 293,148.00

Spare Parts Inventory 2,066,500.00 2,066,500.00 2,066,500.00

Total 4,704,404.00 - 1,700.00 4,706,104.00 4,676,160.00

• Total inventory items amounted to P 4,706,104.00 , comprises P 4,704,404.00

under the General Fund and only P 1,700.00 was under Trust Fund .

• Supplies and materials, gasoline, lubricant and oil were coursed thru

inventories upon acquisition and recorded directly the issuances as it is

directly delivered to end user. While those not directly delivered / distributed

to end user were coursed to inventory account.

Note 6: Prepayments P 33,738,887.97

This account consists of:

Account Title GF SEF TF CY 2011 PY 2010

Prepaid Insurance 1,146,581.79 1,146,581.79 1,146,581.79

Advances to Contractors 31,006,859.68 103,401.70 1,482,044.80 32,592,306.18 35,612,203.79

Total 32,153,441.47 103,401.70 1,482,044.80 33,738,887.97 36,758,785.58

• Under the General Fund and Special Education Fund , total

prepayments st year 2010 , while the total amount of all

prepayments as of December 31, 2011 amounted to P

36,758,785.58 resulting from the decrease in the Advances to

Contractors in the amount of P 3,019,897.61 under the General Fund.

14

Note 7: Long Term Investment P 6,000,000.00

• This represents Iligan City Government’s equity in the joint assistance

program of Landbank and Iligan City Government known as ”Share Financing

Program for Cooperatives in Iligan City”. The objective of the program is to

make available to cooperatives in the City of Iligan financial assistance for

income generating projects.

• The fund is deposited in a trust account with Landbank, subject for verification

, pending status from Landbank.

• The status of the city's investment and the balance of city government equity,

still for further verification on Landbank of the Philippines.

Note 8: Property, Plant and Equipment ( net ) P 2,162,585,501.71

This account consists of: (see attached table)

• Property, Plant and Equipment (net) in the total amount of P

2,162,585,501.71 comprises the General Fund, Special

Education Fund and Trust Fund amounting to P

1,963,355,939.58 , P 146,543,751.19 and P 52,685,810.94 , respectively.

• Another set of depreciable properties, set-up in the lump-sum appropriations

during the installation of the e-ngas program, were partially itemized,

including its estimated useful life. Depreciation was computed using the

straight-line method , after deducting its residual value of ten percent (10%) of

the acquisition cost. Prior - year's depreciation were recorded as prior-year's

adjustments while depreciation for the year were recorded as expense.

• A good number of completed public infrastructure projects and agency assets

were transferred to Registry on Public Infrastructure at year end per list of

completed projects as of December 31, 2011 submitted by the City

Engineer's Office. These included completed projects of different

barangays funded from the 20% Development Fund Equal Sharing.

Under the General Fund, the Electrification, Power & energy Structures

balance is subject for review. The process of itemizing and reconciling

the records against the lumpsum appropriation are still on progress.

• Disposal/Dropping of Unserviceable Properties of Property, Plant and

Equipment duly recommended/considered dropped by COA were already

dropped, as submitted by the City General Services Officer. Purchases of

heavy equipment, IT equipments, and other properties resulted to the increase

in amount.

15

Property, Plant and Equipment

ACCOUNT TITLE

General Fund Special Education Fund Trust Fund CY 2011 PY 2010

Cost Accum. Dep. Net Cost Accum. Dep. Net Cost Accum.

Dep. Net Cost Accum. Dep. Net Cost Accum. Dep. Net

Land 307,183,026.68

307,183,026.68 8,946,883.05

8,946,883.05 3,608,600.00

3,608,600.00 319,738,509.73 0.00 319,738,509.73 303,764,571.71 0.00 303,764,571.71

Land Improvements 5,907,979.61

5,907,979.61 354,853.90

354,853.90

0.00 6,262,833.51 0.00 6,262,833.51 6,262,833.51 0.00 6,262,833.51

Electrification, Power

& Energy Structures 1,540,583.75 1,561,131.31 (20,547.56) 807,914.15 360,493.50 447,420.65

0.00 2,348,497.90 1,921,624.81 426,873.09 1,945,983.80 360,493.50 1,585,490.30

Office Buildings 176,248,124.19 2,030,115.45 174,218,008.74 110,268,050.05 16,540,207.50 93,727,842.55

0.00 286,516,174.24 18,570,322.95 267,945,851.29 286,516,174.24 16,540,207.50 269,975,966.74

School Buildings 26,099,335.15

26,099,335.15 5,485,070.13 541,070.76 4,943,999.37

0.00 31,584,405.28 541,070.76 31,043,334.52 30,764,788.20 517,637.54 30,247,150.66

Hospitals & Health Centers

5,819,160.00 3,748.83 5,815,411.17

0.00 2,640,664.48 4,826.98 2,635,837.50 8,459,824.48 8,575.81 8,451,248.67 8,421,660.79 2,413.49 8,419,247.30

Markets &

Slaughterhouses 115,931,136.23 3,598,837.76 112,332,298.47

0.00

0.00 115,931,136.23 3,598,837.76 112,332,298.47 115,931,136.23 0.00 115,931,136.23

Other Structures 61,784,416.21 2,190,891.33 59,593,524.88 132,367.28 18,447.31 113,919.97 14,831,391.95 37,078.48 14,794,313.47 76,748,175.44 2,246,417.12 74,501,758.32 61,619,896.61 294,576.04 61,325,320.57

Leasehold Improvements, Land

2,486,484.71

2,486,484.71

0.00

0.00 2,486,484.71 0.00 2,486,484.71 2,486,484.71 0.00 2,486,484.71

Leasehold Improvements,

Buildings

0.00

0.00

0.00 0.00 0.00 0.00 0.00 0.00 0.00

Office Equipment 34,880,283.09 3,729,958.58 31,150,324.51 1,842,667.55 1,477,781.75 364,885.80 1,762,022.30 33,895.51 1,728,126.79 38,484,972.94 5,241,635.84 33,243,337.10 38,557,870.13 4,087,005.37 34,470,864.76

Furniture & Fixtures 20,979,204.42 670,930.61 20,308,273.81 15,755,274.24 7,182,174.82 8,573,099.42 291,483.00 3,438.81 288,044.19 37,025,961.66 7,856,544.24 29,169,417.42 36,452,013.91 7,311,164.74 29,140,849.17

IT Equipment & Software

63,545,152.40 16,938,444.90 46,606,707.50 656,090.00 382,938.98 273,151.02 616,850.50 14,024.88 602,825.62 64,818,092.90 17,335,408.76 47,482,684.14 61,426,785.41 12,829,259.58 48,597,525.83

Library Books 10,717,311.67 8,246,787.63 2,470,524.04 20,451,138.10 9,406,868.16 11,044,269.94 385,440.79

385,440.79 31,553,890.56 17,653,655.79 13,900,234.77 31,553,890.56 17,445,341.80 14,108,548.76

Machineries 254,321.00 114,444.45 139,876.55 344,016.09 154,807.25 189,208.84

0.00 598,337.09 269,251.70 329,085.39 598,337.09 269,251.70 329,085.39

Agricultural, Fishery & Forestry Equipment

1,189,835.00 594,552.31 595,282.69

0.00 33,000.00

33,000.00 1,222,835.00 594,552.31 628,282.69 1,222,835.00 468,905.25 753,929.75

Communication Equipment

12,107,554.90 5,271,389.12 6,836,165.78 47,013.29 21,156.00 25,857.29

0.00 12,154,568.19 5,292,545.12 6,862,023.07 11,859,060.19 4,937,996.26 6,921,063.93

Construction & Heavy

Equipment 120,357,954.89 16,761,848.53 103,596,106.36

0.00

0.00 120,357,954.89 16,761,848.53 103,596,106.36 120,317,954.89 15,971,624.57 104,346,330.32

Firefighting Equipment & Accessories

1,373,751.74 761,806.92 611,944.82 28,890.00 18,572.15 10,317.85

0.00 1,402,641.74 780,379.07 622,262.67 1,316,241.74 755,171.25 561,070.49

Hospital Equipment 7,786,609.75 2,250,796.61 5,535,813.14

0.00 55,000.00 825.00 54,175.00 7,841,609.75 2,251,621.61 5,589,988.14 7,078,424.75 1,635,591.51 5,442,833.24

Medical, Dental & Laboratory Equipment

7,737,361.60 1,315,309.15 6,422,052.45

0.00 65,000.00 975.00 64,025.00 7,802,361.60 1,316,284.15 6,486,077.45 7,735,761.60 869,693.07 6,866,068.53

Military & Police

Equipment 1,404,563.53 470,605.59 933,957.94

0.00

0.00 1,404,563.53 470,605.59 933,957.94 1,027,303.53 459,532.59 567,770.94

Sport Equipment 1,902,792.00 836,098.89 1,066,693.11 349,100.00 113,457.50 235,642.50

0.00 2,251,892.00 949,556.39 1,302,335.61 2,251,892.00 872,808.60 1,379,083.40

Technical & Scientific Equipment

12,105,662.47 5,267,244.04 6,838,418.43 545,996.57 245,698.45 300,298.12

0.00 12,651,659.04 5,512,942.49 7,138,716.55 12,329,259.04 5,469,207.05 6,860,051.99

Other Machineries & Equipment

1,847,157.00 802,458.42 1,044,698.58

0.00

0.00 1,847,157.00 802,458.42 1,044,698.58 1,847,157.00 794,952.90 1,052,204.10

Motor Vehicles 105,224,146.63 18,628,714.12 86,595,432.51 3,104,650.00 1,997,988.24 1,106,661.76 4,876,500.00 78,230.31 4,798,269.69 113,205,296.63 20,704,932.67 92,500,363.96 117,424,313.77 16,259,512.61 101,164,801.16

Watercrafts 197,500.00 51,843.75 145,656.25

0.00

0.00 197,500.00 51,843.75 145,656.25 197,500.00 35,550.00 161,950.00

Other Transportation Equipment

374,000.00 10,800.00 363,200.00

0.00

0.00 374,000.00 10,800.00 363,200.00 84,000.00 7,200.00 76,800.00

16

Other Property, Plant & Equipment

264,914,814.14 1,111,907.35 263,802,906.79 3,410,002.53 3,069,002.30 341,000.23 306,123.00 3,774.90 302,348.10 268,630,939.67 4,184,684.55 264,446,255.12 268,102,797.22 3,230,037.45 264,872,759.77

Roads, Highways and Bridges

0.00

0.00

0.00 0.00 0.00 0.00

Parks, Plazas & Monuments

2,427,223.00

2,427,223.00

0.00

0.00 2,427,223.00 0.00 2,427,223.00 2,427,223.00 0.00 2,427,223.00

Docks and Wharves including Passageway

0.00

0.00

0.00 0.00 0.00 0.00 0.00

Water Supply, Head Control, Reservoir and

Conduits

0.00

0.00

0.00 0.00 0.00 0.00 0.00

Artesian Wells, Reservoir, Pumping

Stations & Conduits

62,874.97

62,874.97 384,335.11

384,335.11

0.00 447,210.08 0.00 447,210.08 721,109.07 0.00 721,109.07

Irrigation, Canals &

Laterals 42,901,095.17

42,901,095.17

0.00

0.00 42,901,095.17 0.00 42,901,095.17 43,112,295.17 0.00 43,112,295.17

Harbor, Riverwall,

Seawalls and Improvements

0.00

0.00

0.00 0.00 0.00 0.00 0.00

Other Public

Infrastructures 124,488,393.45

124,488,393.45 180.00

180.00

0.00 124,488,573.45 0.00 124,488,573.45 124,277,373.45 0.00 124,277,373.45

Reforestation - Upland 49,500.00

49,500.00

0.00

0.00 49,500.00 0.00 49,500.00 49,500.00 0.00 49,500.00

Construction in Progress - Agency Assets

241,139,143.22

241,139,143.22 14,923,236.92

14,923,236.92 17,715,140.79

17,715,140.79 273,777,520.93 0.00 273,777,520.93 243,783,265.16 0.00 243,783,265.16

Construction in Progress - Roads, Highways & Bridges

87,427,024.56

87,427,024.56

0.00 3,462,119.00

3,462,119.00 90,889,143.56 0.00 90,889,143.56 78,393,874.95 0.00 78,393,874.95

Construction in Progress - Parks, Plazas & Monuments

2,058,473.40

2,058,473.40

0.00

0.00 2,058,473.40 0.00 2,058,473.40 2,058,473.40 0.00 2,058,473.40

Construction in Progress - Artesian

Wells, Reservoirs, Pumping Station & Conduits

104,723,349.21

104,723,349.21

0.00 7,135.00

7,135.00 104,730,484.21 0.00 104,730,484.21 100,877,095.56 0.00 100,877,095.56

Construction in Progress - Irrigation,

Canals and Laterals

19,101,803.79

19,101,803.79

0.00

0.00 19,101,803.79 0.00 19,101,803.79 17,613,994.98 0.00 17,613,994.98

Construction in Progress - Flood

Controls

3,280,873.82

3,280,873.82

0.00

0.00 3,280,873.82 0.00 3,280,873.82 2,220,860.62 0.00 2,220,860.62

Construction in

Progress - Waterways, Aquaducts, Seawalls, River Walls and Others

4,353,352.73

4,353,352.73

0.00

0.00 4,353,352.73 0.00 4,353,352.73 3,536,717.73 0.00 3,536,717.73

Construction in Progress - Other Public

Infrastructures

52,656,078.07

52,656,078.07 236,686.90

236,686.90 2,206,410.00

2,206,410.00 55,099,174.97 0.00 55,099,174.97 39,720,280.90 0.00 39,720,280.90

Construction in

Progress - Reforestation - Marshland/Swampland

7,197.08

7,197.08

0.00

0.00 7,197.08 0.00 7,197.08 7,197.08 0.00 7,197.08

TOTAL 2,056,576,605.23 93,220,665.65 1,963,355,939.58 188,074,415.86 41,530,664.67 146,543,751.19 52,862,880.81 177,069.87 52,685,810.94 2,297,513,901.90 134,928,400.19 2,162,585,501.71 2,197,896,188.70 111,425,134.37 2,086,471,054.33

17

Note 9: Other Assets P 32,195,520.49

This account consists of:

Account Title GF SEF TF CY 2011 PY 2010

Work/Other Animals 1,322,924.00 233,000.00 1,555,924.00 1,255,924.00

Breeding Stocks 28,090,731.28 28,090,731.28 28,090,731.28

Other Assets 353,092.00 2,195,773.21 2,548,865.21 2,508,365.21

Total 29,766,747.28 2,195,773.21 233,000.00 32,195,520.49 31,855,020.49

• Total Other Assets amounted to P 32,195,520.49 for all

funds, General Fund, Special Education Fund and Trust

Fund, broken down into P 28,443,823.28 ; P 2,195,773.21

and P 233,000 , respectively, as caused by an increase from

General Fund Work / Other Animals and Breeding stocks, in

the amount of P 300,000.00 and P 40,500.00, respectively.

Note 10: Current Liabilities P 662,995,470.11

This account consist of:

Account Title GF SEF TF CY 2011 PY 2010

Payables:

Accounts Payable 60,325,841.14 4,059,216.23 - 64,385,057.37 78,229,298.63

Due to Officers &

Employees 6,568,183.00 2,611.11 - 6,570,794.11 6,614,387.07

Sub-Total 66,894,024.14 4,061,827.34 - 70,955,851.48 84,843,685.70

Inter-Agency Payables:

Due to BIR 10,863,339.11 1,120,763.68 1,215,391.56 13,199,494.35 8,094,563.04

Due to GSIS (1,187,610.49) 294,615.49 - (892,995.00) (763,665.82)

Due to PAG-IBIG 2,545,176.17 126,678.95 - 2,671,855.12 2,658,644.12

Due to PHILHEALTH 812,902.52 1,431,459.37 - 2,244,361.89 2,632,962.34

Due to Other NGAs 10,993,528.18 - 51,461,610.20 62,455,138.38 44,722,140.00

Due to Other GOCCs 189,810.00 - 14,448,074.34 14,637,884.34 11,185,222.75

Due to LGUs 166,496.29 - 1,720,235.66 1,886,731.95 2,710,091.96

Sub-Total 24,383,641.78 2,973,517.49 68,845,311.76 96,202,471.03 71,239,958.39

Intra-Agency Payables:

Due to Other Funds 103,917,127.00 170,415.45 26,735.86 104,114,278.31 639,924.01

Sub-Total 103,917,127.00 170,415.45 26,735.86 104,114,278.31 639,924.01

Other Liability Accounts:

Guaranty Deposits Payable 8,825,441.82 215,863.33 609,204.36 9,650,509.51 6,982,473.76

Performance/Bidders/Bail

Bonds Payable 666,575.65 - 64,583,945.28 65,250,520.93 4,351,842.09

18

Other Payables 13,887,524.95 234,690.33 302,699,623.57 316,821,838.85 29,601,598.85

Sub-Total 23,379,542.42 450,553.66 367,892,773.21 391,722,869.29 40,935,914.70

Grand-Total 218,574,335.34 7,656,313.94 436,764,820.83 662,995,470.11 197,659,482.80

• Under the General Fund , Accounts Payable due to GSIS

incurred a debit balance P 892,995.00 , broken down from Special

Education Fund balance of P 294,615.49 and a debit balance of P

1,187,610.49 under the General Fund. A debit balance under General Fund,

as a result from the city’s partial settlement of premiums, penalties and

surcharges in arrear, subject for review and verification pending submission

of GSIS detailed listing.

• Due to Other Funds , as of December 31, 2011 and as of December 31,

2010 amounting to P104,114,278.31 and P639,924.01, respectively, with a

difference of more or less P103M , included among others , PDAF

and Calamity Fund for Typhoon Sendong in the total amount of

P 103,909,661.54 , which was transferred Jan 2012.

• Performance/Bidders/Bail Bonds Payable increase by more or less P 60M due

to the receipt of Performance / Bidders' Bond of Conal Holding Incorporated.

Note 11: Long Term Liabilities P 337,168,765.41

This account consists of :

ACCOUNT TITLE CY 2011 PY 2010

National Government Agencies

MDFO- PRMDP 24,525,239.78 28,911,071.42

Total

24,525,239.78 28,911,071.42

Government Owned and/or Controlled Corporation

DBP- IBJT 45,589,285.62

DBP-Miscellaneous Health Services 47M 47,000,000.00

DBP-WATER WORKS PROJECT 50M

Total 92,589,285.62

Solid Waste Management Project & Heavy Equipment

DBP-SOLID WASTE MANAGEMENT PROJECT

(DBP funds) - 1st drawdown ( 7,538,000.00)

1,413,375.00

DBP-SOLID WASTE MANAGEMENT PROJECT

(kfw funds) - 1st drawdown (62,440.000.00)

42,147,000.00

48,391,000.00

DBP-Solid Waste Management Project (kfw funds)

- 2nd drawdown (78,050.000.00)

54,034,615.40

62,039,743.60

Total

96,181,615.40 111,844,118.60

19

IliganCity Water Supply System Development Project

LBP - WATER SYSTEM EXPANSION PROJECT (445.5M)

-1st Released

29,258,691.50

29,258,691.50

LBP - WATER SYSTEM EXPANSION PROJECT

(14,476,166.24)-2nd Released

14,476,166.24

LBP - WATER SYSTEM EXPANSION PROJECT

(17,272,705.25)-3rd Released

17,272,705.25

LBP - WATER SYSTEM EXPANSION PROJECT

(69,574,896.52)-4th Released

69,574,896.52

LBP - WATER EXPANSION PROJECT (96,931,035.49)-5th

Released

85,879,450.72

Total 216,461,910.23 29,258,691.50

Grand Total 337,168,765.41 262,603,167.14

• The city government of Iligan had fully paid three DBP loans,

namely : Various Priority Projects - Miscellaneous Health Services P

47M , the Solid Waste Management Project P 7.538M (with

unreleased balance of P 15.610M) and the Integrated Bus & Jeepney

Terminal (IBJT), Market & Drainage P 111M , last March 25, 2011 , August

9, 2011 and August 31 , 2011, respectively.

• Under the General Fund , the outstanding principal balances of the

existing loans as of December 31, 2011, totalled P 337,168,765.41, consist

of MDFO-PRMDP , DBP - Solid Waste Management Project and the LBP -

Water System Expansion Project (445.5M), with corresponding loan amount

of P 24,525,239.78 , P 96,181,615.40 and P 216,461,910.23 , respectively.

• Total balance as of December 31, 2011 showed an increased of P

74,565,598.27 due to full payment of loans and new releases of approved

loans of the city.

• Necessary adjustments will be made to reconcile loan records as soon as

debit / credit memos from the bank with sufficient data be furnished.

Note 12 : Deferred Credits P 889,371,435.96

This account consist of :

Account Title GF SEF TF CY 2011 PY 2010

Deferred Real Property

Tax Income 480,095,775.09 - - 480,095,775.09 545,572,994.43

Deferred Special

Education Tax Income - 408,754,935.44 - 408,754,935.44 468,606,013.45

Other Deferred Credits 264,839.17 7,614.00 248,272.26 520,725.43 462,889.18

Total 480,360,614.26 408,762,549.44 248,272.26 889,371,435.96 1,014,641,897.06

20

• Total amount of P 889,371,435.96 representing Total Deferred

Credits under the General Fund Account, Special Education

Fund and Trust Fund with an amount of P 480,360,614.26,

P 408,762,549.44 and P 248, 272.26 , respectively .

• Other Deferred Credits in the amount of P 520,725.43 included Real

Property Tax advance payments, as well as Real Property tax credits.

Note 13: Government Equity Composition :

Account Title GF SEF TF CY 2011 PY 2010

Government Equity, Beg. 2,143,790,906.15 184,750,867.67 37,168,972.02 2,365,710,745.84 2,280,089,049.94

Add:

Retained Operating

Surplus 277,285,671.62 12,931,034.60 - 290,216,706.22 215,827,917.60

Prior Year's Adjustments (8,805,747.22) 3,300,172.32 19,711,812.58 14,206,237.68 (99,898,118.81)

Deduct:

Public Infrastructures (19,274,710.97)

(19,274,710.97) (30,308,102.89)

Prior Year's Adjustments (11,134,511.21)

(11,134,511.21)

Government Equity, End 2,381,861,608.37 200,982,074.59 56,880,784.60 2,639,724,467.56 2,365,710,745.84

• Total amount of government equity as of December 31, 2011

and December 31, 2010, P 2,700,542,911.92 and P 2,365,710,745.84 ,

respectively, a difference of P 334,832,166.08.

• A good number of completed public infrastructure projects and agency assets

as of December 31, 2011 had been transferred to Registry of Public Infra

in the amount of P 19,274,710.97. Itemizing some Property, Plant and

Equipment including public infrastructures from the lumpsum amount are still

on progress.

• Equity set aside to finance capital projects with appropriations provided in the

current year and previous years.

• Prior-Year adjustments included those transactions affecting the nominal

accounts and other adjustments which increase or decrease the Retained

Operating Surplus account, such as adjustments of excess revenue recorded in

prior years; payments of unrecorded expenses of prior years such as

depreciation, liquidations of prior year expenses, etc.

Note 14: Income P1,232,575,725.13

Account Title GF SEF TF CY 2011 PY 2010

Local Taxes 163,172,740.15 68,469,409.58

231,642,149.73 211,248,590.78

Internal Revenue Allotment 853,673,770.00

853,673,770.00 793,816,617.00

Permits and Licenses 8,167,651.62

8,167,651.62 7,632,177.78

21

Service Income 16,985,799.03

16,985,799.03 15,824,028.65

Business Income 90,174,625.70

90,174,625.70 82,765,110.23

Other Income 31,124,465.50 827,263.55

31,951,729.05 34,904,802.85

Total 1,163,299,052.00 69,296,673.13 - 1,232,595,725.13 1,146,191,327.29

• Total Operating Income as of December 31, 2011 and as of December

31, 2010 amounted to P 1,232,595,725.13 and P 1,146,191,327.29 ,

under General Fund and Special Education Fund, respectively.

• Under the General Fund Account, total Share from National Wealth as of

December 31, 2011 amounted to P 19,576,757.34 . Included in this year's

share was the P 5,394,978.39 uncollected portion of year 2010, while the

Fourth Quarter, 2011 share was not yet collected.

• Share from IRA, for the year 2011, amounted to P 853,673,770.00

as compared to year 2010, which was only P 793,816,617.00 , with

an increased of P 59,857,153.00.

• Share from Economic Zone as of December 31, 2011, amounted to

P5,298,121.09, a portion of which included the fourth quarter, 2010 share of

P 1,714,255.00 . While the fourth quarter, 2011 share, was not yet collected .

• Total Interest Income for the year ended December 31, 2011 and as

of December 31, 2010 , for both GF and SEF amounted to

P5,443,666.31 and P 7,352,635.32 , respectively.

Note 15: Expenses P915,507,024.86

Account Title GF SEF TF CY 2011 PY 2010

Personal Expenses 441,818,436.67 48,976,419.80 - 490,794,856.47 471,484,032.03

Maintenance & Other Operating Expenses

386,679,825.56 7,389,218.73 - 394,069,044.29 399,336,004.35

Financial Charges 30,643,124.10 - - 30,643,124.10 29,180,311.67

Total 859,141,386.33 56,365,638.53 - 915,507,024.86 900,000,348.05

• Total Expenditure as of December 31, 2011 and December 31,

2010, amounted to P 915,507,024.86 and P 900,000,348.05,

respectively, showing a net addition of P 15,506,676.81 for

both the General Fund and Special Education Fund.

22

Part II – Detailed Findings and Recommendations

23

Part II - FINDINGS AND RECOMMENDATIONS

The city government in Iligan has two main sources of funds, Internal Revenue

Allotment (IRA) and locally generated revenues. It controls a range of economic

enterprises, the operations of which are consolidated in its financial statements. Almost

all of these enterprises are self-liquidating, though for all of them, the bulk of their

operating costs are still being subsidized by the city and fully consolidated in its financial

statements.

The city is considered stable and low-risk compared to many surrounding areas of

Mindanao and its geographic positioning is advantageous as a commercial center. It has

high hopes for the development of its tourism and business related to its role as a

commercial center for Central Mindanao. Natural resources, such as waterfalls, coastline

and forest create favorable conditions for the development of tourism.

MARIA CRISTINA FALLS

The city was struck by “Typhoon Sendong” (the strongest typhoon to hit this place) and

devastated 36 out of 44 barangays of this City, last December 17, 2011. Final report

received from the City Social Welfare & Development (CSWD) showed that: a) 29,265

families with total dependents of 117,303 have been affected; b) rendered homeless to

6,701 families, while 22,564 families whose houses were partially damaged; c) 1,775

families with total dependents of 8,839 stayed in 19 evacuation centers and 4,926

families with 108,464 dependents prepared to stay in their respective homes; d) 805 dead

bodies have been recovered of which 269 are unidentified bodies, 758 are missing

persons and 4,511 are injured (citywide); and e)estimated damages to property ( personal)

amounting to P 2,118,809,237.

24

Sources of Revenue, Application of Funds and Results of Operations

For the year under review, the City Treasurer is estimated to collect income of

P1,372,196,291.00 of which 62.21% or P853,673,770.00 came from its share in Internal

Revenue Allotment and 37.79% or P518,822,521.00 from tax revenue and other service

income to finance its program of expenditures classified into general public services,

social services and economic services in the total amount of P1,503,786,178.75. To fill

the variance between the estimated collectible income and proposed current operating

expenditures of P131,589,887.75, the City resorted to secure domestic loan of P75M;

reversion/realignment of some of prior years (continuing) and current year

appropriations, 20% Development Fund, of P 50,487,057.65, un-appropriated beginning

balance of P4,715,952.90 and reversion of certified obligations of P1,386,877.20 all

these are contained in the Supplemental Budget Nos. 1, 2, and 3 duly approved by the

Sanggunian Panlunsod of Iligan. In addition thereto, the city has a continuing

appropriation amounting to P716,025,316.52, accounted as P149,723,825.52 for 20%

Development Fund and General Fund Proper P566,301,491.00

During the year the City government have collected the sum of

P1,298,226,495.19 from all sources, total current operating expenditures of

P1,008,009,788.97 inclusive of the amount of P256,847,636.41 utilized from continuing

appropriations, and net income of P290,216,706.22.

The following pie and bar charts showed the distributions of estimated income,

against actual collections; appropriations & allotments, obligations, and net income vis a

vis actual current operating expenses by fund. The details are presented in the

Consolidated Statement of Income and Expenses and annexes of the report.

A. Sources of Revenue

Figure 1- Estimated Income

Variance

Figure 2 – Actual Income

GF 1,087,173,866.00

SAGF 213,278,442.00

SEF 71,743,983.00

Total 1,372,196,291.00

GF 1,073,642,204.11 GF (13,531,661.59)

SAGF 155,287,617.65 SAGF (57,990,824.35)

SEF 69,296,673.13 SEF (2,447,309.87)

Total 1,298,226,495.19 Total (73,969,795.81)

25

GF 1,040,039,111.00

SAGF 385,900,254.65

SEF 77,846,813.10

Total 1,503,786,178.75

CA 716,025,316.52

Total Available for Expenditures 2,219,811,495.27

Note: CA -Continuing Appropriations

Figure 3 – Appropriations

& Allotments

B. Application of Funds (Obligations)Unexpended Allotment

Figure 4 - Obligations

Allocation by class of expenditures by Funds

General Fund (GF)

Figure 4.1 Details of Obligations

Special Accounts in the General Fund (SAGF)- Economic Enterprises & 20%

Development Fund

Personal Services 78,877,941.71

MOOE 57,141,852.47

Financial Expenses 17,658,406.95

Capital Outlay 78,688,740.20

Total 232,461,941.33

Figure 4.2 Details of Obligations

GF 892,930,715.03 147,108,395.07

SAGF 232,461,941.33 153,438,313.32

SEF 57,161,441.02 20,685,372.08

Subtotal 1,182,554,097.38 321,232,091.37

CA 256,847,636.14 459,177,680.38

Total Obligations 1,439,401,733.52 780,409,761.75

Personal Services 354,994,993.78

MOOE 403,731,028.06

Financial Expenses 128,563,593.77

Capital Outlay 5,641,099.42

TOTAL 892,930,715.03

26

Special Education Fund (SEF)

Figure 4.3 Details of Obligations

C. Results of Operations

Figure 5-Actual Income

Figure 6- Actual Current Operating

Expenses

BREAKDOWN OF CURRENT OPERATING EXPENSES (COE):

General Fund

Personal Services 362,940,494.96

MOOE 422,040,737.20

Financial Expenses 12,984,717.15

Total 797,965,949.31

Figure 6.1 Details of COE

Special Accounts in the General Fund (SAGF)

Personal Services 78,877,941.71

MOOE 57,141,852.47

Personal Services 48,798,967.18

MOOE 8,178,278.01

Capital Outlay 184,195.83

Total 57,161,441.02

GF 1,073,642,204.41

SAGF 155,287,617.65

SEF 69,296,673.13

TOTAL 1,298,226,495.19

COE Excess of Income

over Expenses

GF 797,965,949.31 274,676,255.10

SAGF 153,678,201.13 1,609,416.52

SEF 56,365,638.53 12,931,034.60

TOTAL 1,008,009,788.97 290,216,706.22

27

Financial Expenses 17,658,406.95

Total 153,678,201.13

Figure 6.2 Details of COE

Special Education Fund (SEF)

Figure 6.3 Details of COE

Personal Services 48,976,419.80

MOOE 7,389,218.73

Total 56,365,638.53

28

Detailed Findings and Recommendations