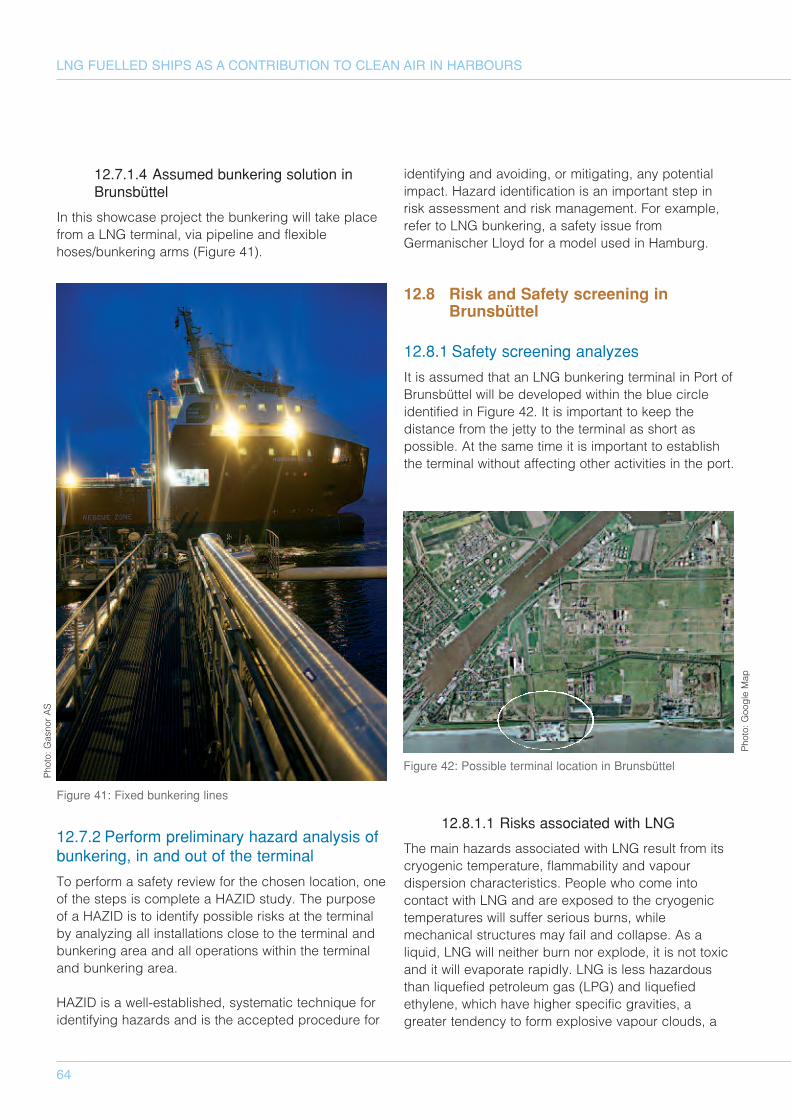

CNSS Work package 4, Showcase LNG LNG fuelled ships as...

80

CNSS Work package 4, Showcase LNG LNG fuelled ships as a contribution to clean air in harbours CNSS May 2013

Transcript of CNSS Work package 4, Showcase LNG LNG fuelled ships as...

CNSS Work package 4, Showcase LNG

LNG fuelled ships as a contribution to clean air in harbours

CNSS

May 2013

2

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

1 Introduction 41.1 Clean North Sea Shipping 41.2 LNG showcase 41.3 Main contributors 41.4 Report structure 41.5 Limitations 41.6 Abbreviations and definitions 5

2 Summary 73 LNG supply chain 8

3.1 Introduction 83.2 LNG Source 103.3 Intermediate terminal 113.4 Bunker vessel 123.5 Feeder vessel 123.6 LNG Truck 133.7 LNG Pipeline 133.8 Receiving vessels 13

4 LNG stakeholders demands 154.1 Introduction 154.2 Ship owners/operators 154.3 Policy makers 154.4 Authorities 164.5 Ports 164.6 Terminal operators 164.7 LNG suppliers 164.8 Others 17

5 Existing and future regulations, standards and legislations 185.1 Regulations for marine activities 185.2 Ship-to-shore and ship-to-ship transfer standards 195.3 Global initiatives by involved parties 205.4 Regulations for onshore activities 215.5 Regulations for transporting LNG via inland ship-based activities 225.6 Conclusion 23

6 Bunkering procedures 246.1 Present status 246.2 On-going international developments 246.3 National initiatives and solutions 246.4 Conclusion 25

7 Bunkering and navigational safety evaluation 267.1 Introduction 267.2 HAZID 267.3 Traffic analysis 307.4 Quantitative risk assessment 317.5 Collision rates for a realistic scenario 327.6 Conclusion 33

8 Health and environmental aspects 348.1 Definition of LNG 348.2 Impact on the operation of machinery onboard ships 348.3 Health effects and risk potential 348.4 Comparison of alternative fuels 358.5 Global effects 378.6 A local emission scenario for the city of Hamburg based on the replacement

of oil-based fuels by LNG 378.7 Summary 39

Table of Contents

3

9 LNG Market overview 409.1 The history of LNG 409.2 Increase in availability 409.3 Regional pricing imbalance 429.4 Price development in the future 439.5 Conclusion 43

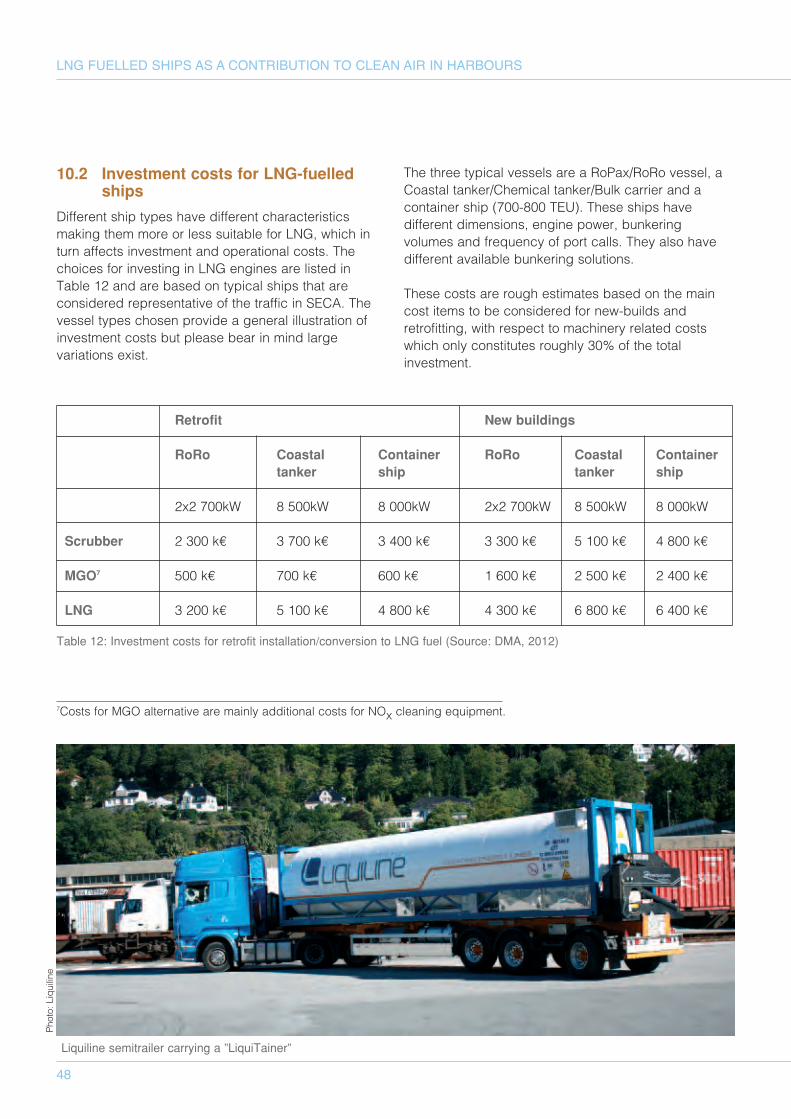

10 Cost-benefit analysis 4410.1 Introduction 4410.2 Investment costs for LNG-fuelled ships 4810.3 LNG fuel supply infrastructure 49

11 Knowledge, training and certification 5111.1 Crew on IGF vessels 5111.2 Bunker vessels crew 5211.3 Inland water way shipping 5311.4 Shore based LNG supply professionals 5411.5 Directly related professionals 5411.6 Authorities 55

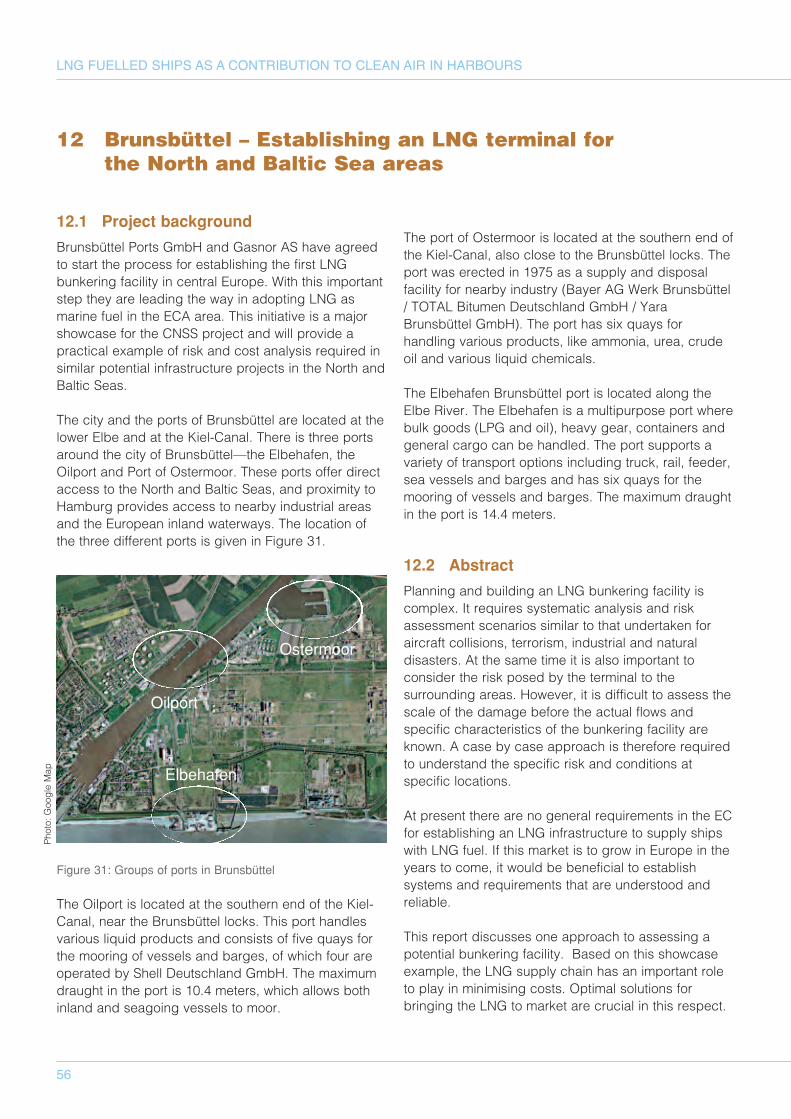

12 Brunsbüttel – Establishing an LNG terminal for the North and Baltic Sea areas 5612.1 Project background 5612.2 Abstract 5612.3 LNG supply chain 5712.4 Alternative terminal concepts 5912.5 Potential market for LNG as fuel in the showcase 6012.6 Preparations for the application 6212.7 Evaluation of bunkering procedures 6312.8 Risk and Safety screening in Brunsbüttel 6412.9 Pilot study 6812.10 Bunkering in Brunsbüttel 70

13 Findings 7413.1 Regulatory 7413.2 Commercial 7413.3 Environmental 7513.4 Education, training and certification 75

References 76Appendices 79

Appendix A LNG Bunkering from Bunker vessel in port of HamburgAppendix B Navigational Safety Study on LNG-Tanker and LNG-Bunker Supply Vessel

operation at Port of HamburgAppendix C Rules and regulations of the report modalities for the provisioning of LNG as

shipping fuel in Flemish ports

Photo: Deen Shipping

4

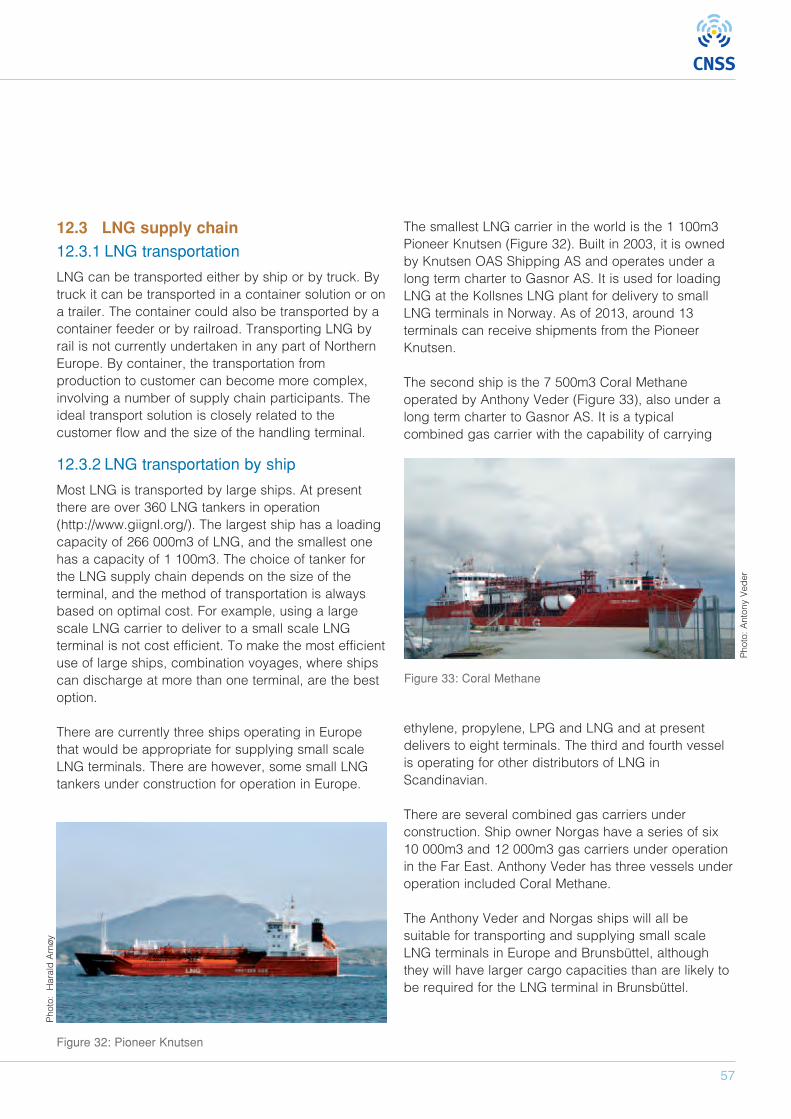

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

1 Introduction

1.1 Clean North Sea Shipping

The Clean North Sea Shipping (CNSS) project,involving 18 partners from six countries, seeks toaddress the problems caused by air pollution andgreenhouse gases produced by ships operating alongthe North Sea coast and within North Sea ports andharbours. A reduction in exhaust gas emissions fromships will improve the general environmental situationin the North Sea Region.The CNSS project aims to create awareness, shareknowledge and convince influential stakeholders,including regional and European politicians, ports,shipping companies and cargo owners, to take action.

1.2 LNG showcase

This report is the result of one of the activities of theWP4 Clean Shipping Technology work package calledthe LNG (Liquefied Natural Gas) showcase. The mainpurpose of the showcase is to increase awareness andunderstanding among policy makers and otherstakeholders of gas-fuelled ships as a potential CleanShipping Technology. The showcase report will provide an introduction toLNG or biogas as an alternative fuel for ships andanswer most of the questions that the stakeholdersmight have relating to this technology.

1.3 Main contributors

The main contributors to this report are as follows:

Chapter Main contributor

1 White Smoke Consulting on behalf ofHordaland County Council

2 White Smoke Consulting on behalf ofHordaland County Council

3 Swedish Marine Technology Forum

4 Swedish Marine Technology Forum

5 Port of Antwerp

6 Germanischer Lloyd

7 Germanischer Lloyd

8 BSU Hamburg together with Helmholtz-Zentrum Geesthacht

9 White Smoke Consulting on behalf ofHordaland County Council

10 White Smoke Consulting on behalf ofHordaland County Council

11 White Smoke Consulting on behalf ofHordaland County Council

12 GASNOR

13 White Smoke Consulting on behalf ofHordaland County Council

Groningen Seaports and the Port of Harlingen areacknowledged for their contribution at different stagesof the report compilation. The Port of Gothenburg andMaritime Kompetenzzentrum in Leer (MARIKO) arealso acknowledged for their contribution andparticipation in the early stages of the WP4 workpackage of the CNSS project.

1.4 Report structure

The report is structured as follows:• Chapter 1 and 2 provide an introduction to, and a

summary of, the main issues.• Chapters 3 to 11 highlight specific aspects of the

introduction of LNG as marine fuel and provide anoverview of each topic. For those interested infinding out more about some of the topicsdiscussed, references to further sources ofinformation are provided throughout the report. Forchapter 5 and 7, supplementary information isavailable in the appendices.

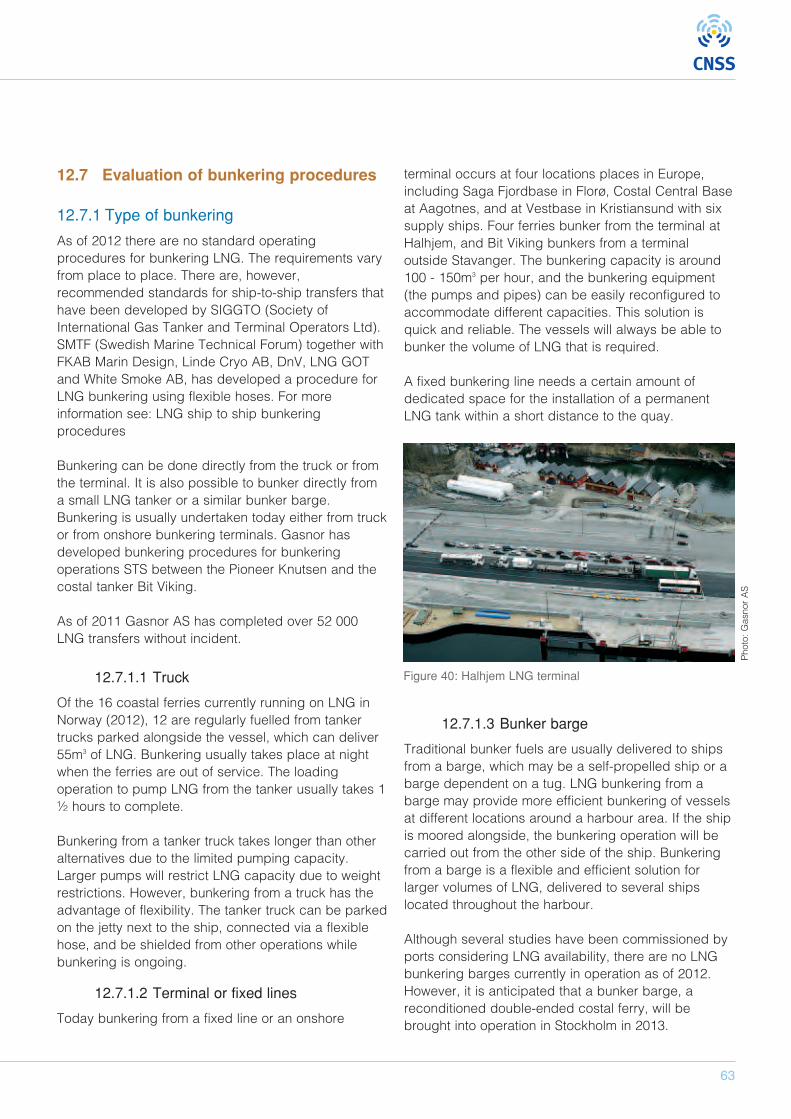

• Chapter 12 illustrates many of the topicsdiscussed in the preceding chapters with aspecific reference case—the Gasnor LNGbunkering facility establishment in the port ofBrunsbüttel, close to the North Sea entrance of theKiel Canal and the main entrance to the Port ofHamburg.

• Chapter 13 concludes the report withrecommendation for different stakeholdersprovided by the participants in the LNG showcasework.

1.5 Limitations

The purpose of this showcase report is to provide aninsight into most, if not all, of the topics to beaddressed when considering LNG bunkering and toprovide additional references for further information.This report will not contain detailed information, nor willit provide complete guidelines on establishing andoperating LNG bunkering.

5

1.6 Abbreviations and definitions

AND International Carriage of Dangerous

Goods by Inland Waterways

ADR International Carriage of Dangerous

Goods by Road

AIS Automatic Identification System

API American Petroleum Institute

BLG International Maritime Organisation (IMO)

sub-committee dealing with Bulk Liquids

and Gases

BOE Barrel of oil equivalent

CCNR Central Commission for the Navigation of

the Rhine

CEN European Committee for Standardization

CFR Code of Federal Regulations

CNG Compressed natural gas

CH4 Methane

CO2 Carbon dioxide

DMA Danish Maritime Authority

ECA Emission Control Area

EGR Exhaust gas recirculation

EIA Environmental Impact Assessment

EMSA European Maritime Safety Agency

ESD Emergency Shut Down

ESPO European Sea Ports Organization

EU European Union

Flemish

Study Solutions for the provision of LNG as

shipping fuel in Flemish ports

Fracking A method to extract shale natural gas

(NG) from flaky shale rock

FOB Free On Board (as defined in the

Incoterms 2010 by the International

Chamber of Commerce)

GHG Greenhouse Gas. Emissions of gaseous

substances that trap heat in the

atmosphere and contribute to the Green

House effect and climate change.

GJ Giga Joule

GL Germanischer Lloyd

HA Hazardous Area. An area in which an

explosive gas atmosphere is present, or

may be expected to be present, in

quantities such as to require special

precautions for the construction,

installation and use of apparatus. [ISO

18132-2:2008, 3.3]

HAZID Hazard Identification

HFO Heavy Fuel Oil

IAPH International Association of Ports and

Harbours

IEA International Energy Agency

IGC International Code For The Construction

And Equipment Of Ships Carrying

Liquefied Gases In Bulk

IGF Code International Code of Safety for Ships

Using Gases or other Low Flashpoint

Fuels (draft)

IGF vessel A vessel using LNG as main fuel designed

and operated for international trade in line

with the IMO regulations

IGO Intergovernmental organization

IMDG International Maritime Dangerous Goods

Code

IMO International Maritime Organisation

ISGINTT International Safety Guide for Inland

Navigation Tank-barges and Terminals

ISGOTT International Safety Guide for Oil Tankers

and Terminals

ISO International Organization for

Standardization

6

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

IWS Inland waterway shipping

Liquefied A tanker that transport liquefied gases

gas such as LNG, LPG, Ethylene, Carbon

tankers Dioxide and so on.

LNG Liquefied Natural Gas

LPG Liquefied Petroleum Gas

MGO Marine Gas Oil

MARPOL International Convention for the Prevention

of Pollution from Ships

MGO Marine Gas Oil

MOW Mobiliteit en Openbare Werken (Flemish

Department of Mobility and Public Work)

NaOH Sodium hydroxide (also known as lye or

caustic soda)

Natural gasA hydrocarbon gas mixture consisting

mainly of methane. The composition of the

gas may also include varying amounts of

nitrogen, carbon dioxide and so on.

NFPA National Fire Protection Association

NG Natural gas

NGO Non-governmental organization

NOx Nitrogen oxides

OCIMF Oil Companies International Marine Forum

PM Particulate matter

PSV Platform supply vessel

QCDC Quick Connect Disconnect

RPT Rapid phase transition

RVIR Rhine Vessel Inspection Regulations

SAR Search and rescue

SCR Selective Catalytic Reduction

SECA Sulphur Emission Control Area

SIGTTO Society of International Gas Tanker &

Terminal Operators

SO2 Sulphur dioxide

SOLAS International Convention for the Safety of

Life at Sea

SOx Sulphur oxides

STCW International Convention on Standards of

Training, Certification, and Watchkeeping

for Seafarers

STW IMO sub-committee dealing with

Standards of Training and Watchkeeping

UN United Nations

UNECE United Nations Economic Commission for

Europe

WPCI World Port Climate Initiative

7

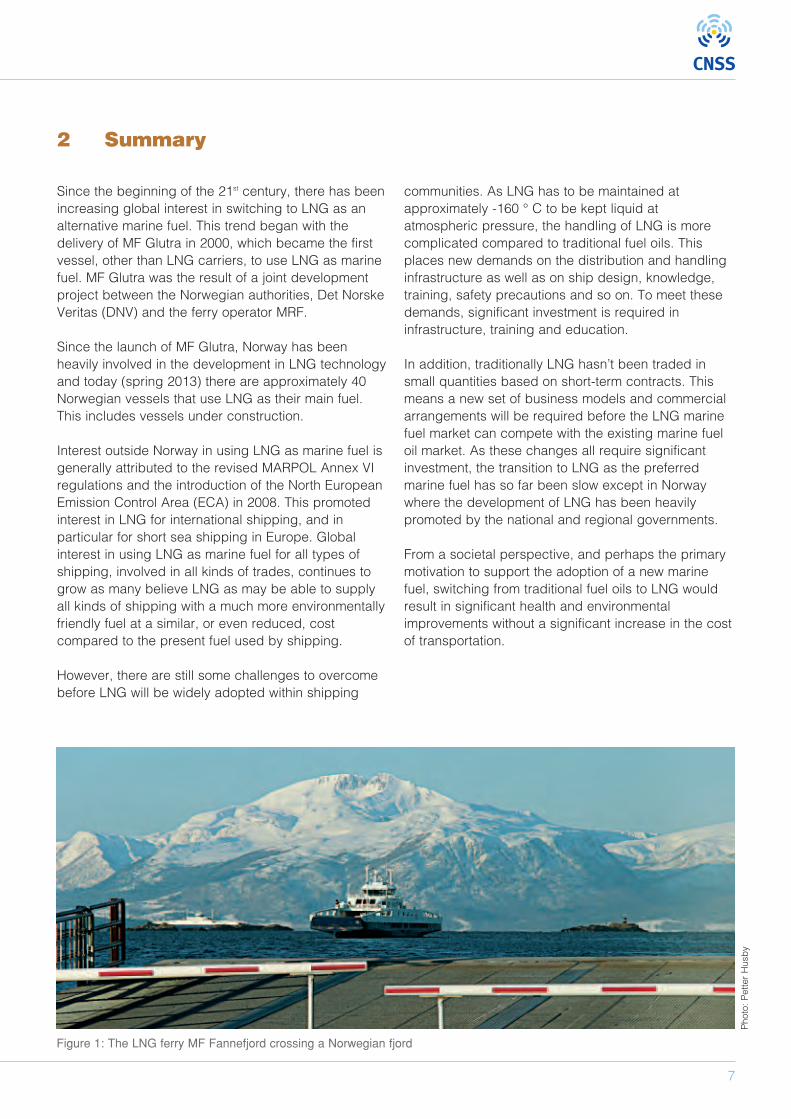

2 Summary

Since the beginning of the 21st century, there has beenincreasing global interest in switching to LNG as analternative marine fuel. This trend began with thedelivery of MF Glutra in 2000, which became the firstvessel, other than LNG carriers, to use LNG as marinefuel. MF Glutra was the result of a joint developmentproject between the Norwegian authorities, Det NorskeVeritas (DNV) and the ferry operator MRF.

Since the launch of MF Glutra, Norway has beenheavily involved in the development in LNG technologyand today (spring 2013) there are approximately 40Norwegian vessels that use LNG as their main fuel.This includes vessels under construction.

Interest outside Norway in using LNG as marine fuel isgenerally attributed to the revised MARPOL Annex VIregulations and the introduction of the North EuropeanEmission Control Area (ECA) in 2008. This promotedinterest in LNG for international shipping, and inparticular for short sea shipping in Europe. Globalinterest in using LNG as marine fuel for all types ofshipping, involved in all kinds of trades, continues togrow as many believe LNG as may be able to supplyall kinds of shipping with a much more environmentallyfriendly fuel at a similar, or even reduced, costcompared to the present fuel used by shipping.

However, there are still some challenges to overcomebefore LNG will be widely adopted within shipping

communities. As LNG has to be maintained atapproximately -160 ° C to be kept liquid atatmospheric pressure, the handling of LNG is morecomplicated compared to traditional fuel oils. Thisplaces new demands on the distribution and handlinginfrastructure as well as on ship design, knowledge,training, safety precautions and so on. To meet thesedemands, significant investment is required ininfrastructure, training and education.

In addition, traditionally LNG hasn’t been traded insmall quantities based on short-term contracts. Thismeans a new set of business models and commercialarrangements will be required before the LNG marinefuel market can compete with the existing marine fueloil market. As these changes all require significantinvestment, the transition to LNG as the preferredmarine fuel has so far been slow except in Norwaywhere the development of LNG has been heavilypromoted by the national and regional governments.

From a societal perspective, and perhaps the primarymotivation to support the adoption of a new marinefuel, switching from traditional fuel oils to LNG wouldresult in significant health and environmentalimprovements without a significant increase in the costof transportation.

Figure 1: The LNG ferry MF Fannefjord crossing a Norwegian fjord

Photo: Petter Husby

8

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

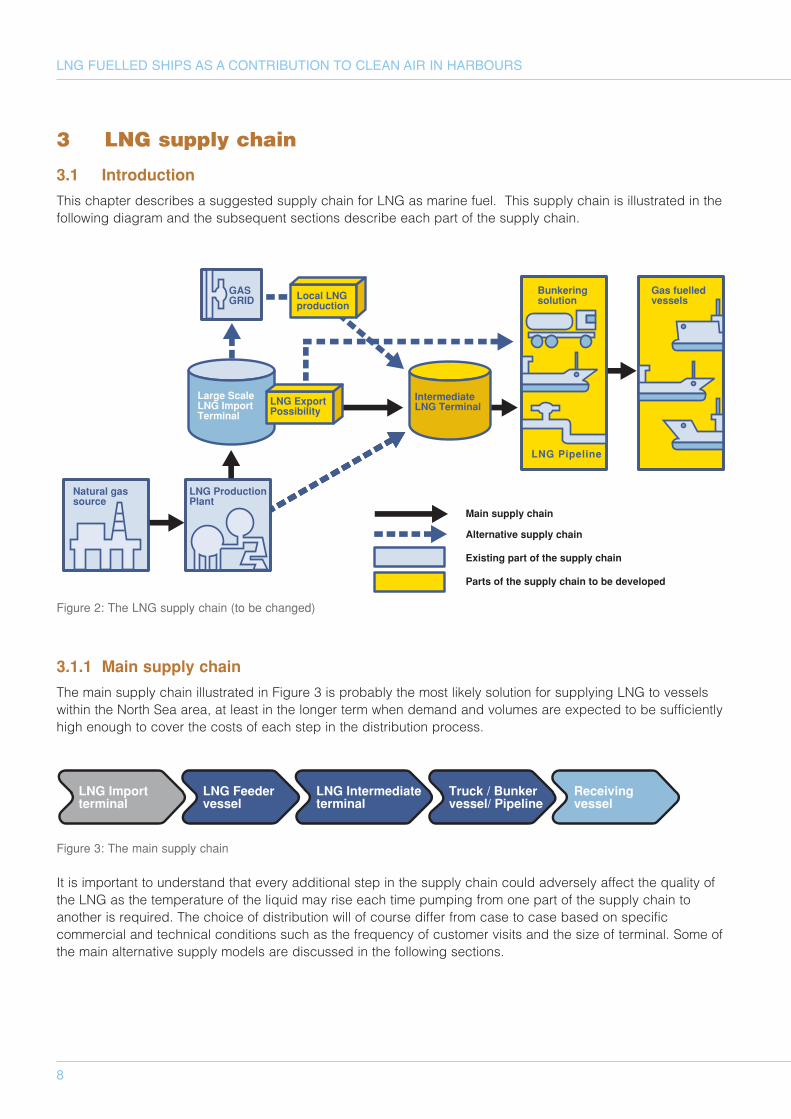

3.1 Introduction

This chapter describes a suggested supply chain for LNG as marine fuel. This supply chain is illustrated in thefollowing diagram and the subsequent sections describe each part of the supply chain.

3.1.1 Main supply chain

The main supply chain illustrated in Figure 3 is probably the most likely solution for supplying LNG to vesselswithin the North Sea area, at least in the longer term when demand and volumes are expected to be sufficientlyhigh enough to cover the costs of each step in the distribution process.

Figure 3: The main supply chain

It is important to understand that every additional step in the supply chain could adversely affect the quality ofthe LNG as the temperature of the liquid may rise each time pumping from one part of the supply chain toanother is required. The choice of distribution will of course differ from case to case based on specificcommercial and technical conditions such as the frequency of customer visits and the size of terminal. Some ofthe main alternative supply models are discussed in the following sections.

3 LNG supply chain

Large ScaleLNG ImportTerminal

LNG ExportPossibility

GASGRID

IntermediateLNG Terminal

Gas fuelledvessels

Natural gassource

LNG ProductionPlant

Bunkeringsolution

LNG Pipeline

Main supply chain

Alternative supply chain

Existing part of the supply chain

Parts of the supply chain to be developed

Local LNGproduction

Figure 2: The LNG supply chain (to be changed)

LNG Importterminal

LNG Feedervessel

LNG Intermediateterminal

Truck / Bunkervessel/ Pipeline

Receivingvessel

9

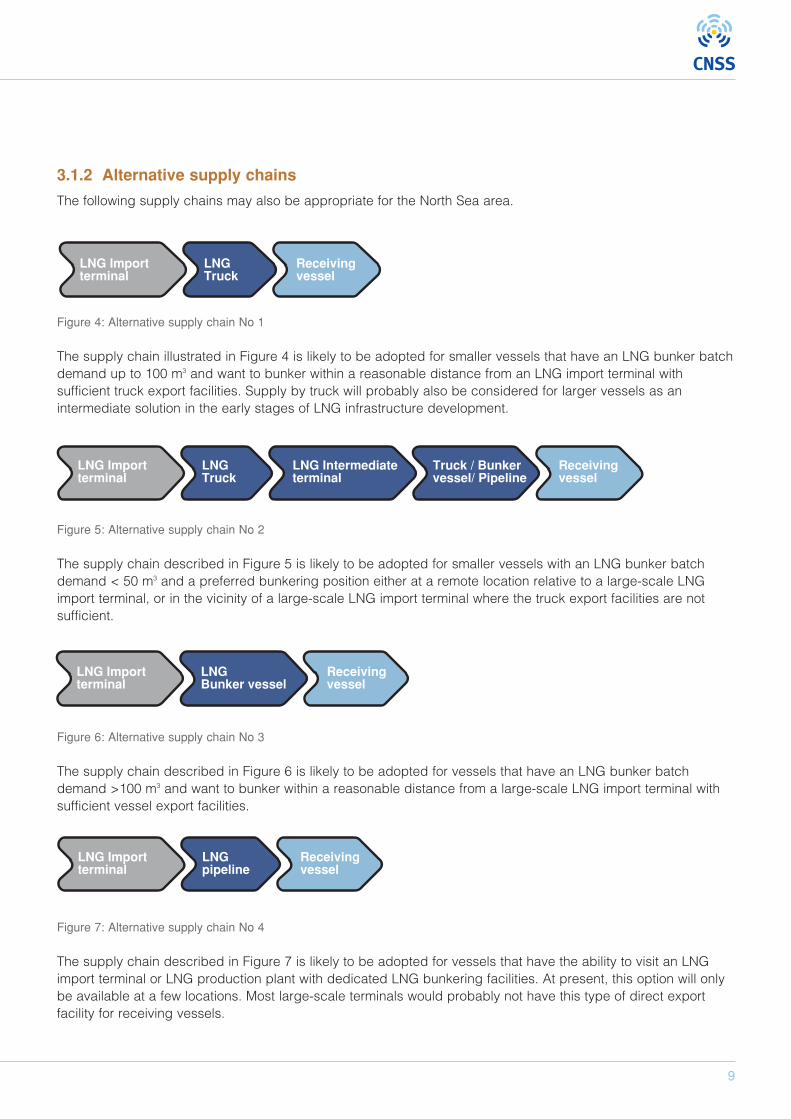

3.1.2 Alternative supply chains

The following supply chains may also be appropriate for the North Sea area.

Figure 4: Alternative supply chain No 1

The supply chain illustrated in Figure 4 is likely to be adopted for smaller vessels that have an LNG bunker batchdemand up to 100 m3 and want to bunker within a reasonable distance from an LNG import terminal withsufficient truck export facilities. Supply by truck will probably also be considered for larger vessels as anintermediate solution in the early stages of LNG infrastructure development.

Figure 5: Alternative supply chain No 2

The supply chain described in Figure 5 is likely to be adopted for smaller vessels with an LNG bunker batchdemand < 50 m3 and a preferred bunkering position either at a remote location relative to a large-scale LNGimport terminal, or in the vicinity of a large-scale LNG import terminal where the truck export facilities are notsufficient.

Figure 6: Alternative supply chain No 3

The supply chain described in Figure 6 is likely to be adopted for vessels that have an LNG bunker batchdemand >100 m3 and want to bunker within a reasonable distance from a large-scale LNG import terminal withsufficient vessel export facilities.

Figure 7: Alternative supply chain No 4

The supply chain described in Figure 7 is likely to be adopted for vessels that have the ability to visit an LNGimport terminal or LNG production plant with dedicated LNG bunkering facilities. At present, this option will onlybe available at a few locations. Most large-scale terminals would probably not have this type of direct exportfacility for receiving vessels.

LNG Importterminal

LNGTruck

Receivingvessel

LNG Importterminal

Receivingvessel

LNG Intermediateterminal

Truck / Bunkervessel/ Pipeline

LNGTruck

LNG Importterminal

Receivingvessel

LNGBunker vessel

LNG Importterminal

Receivingvessel

LNGpipeline

10

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

In addition to the supply chain alternatives describehere, the following technologies could also becomepotential supply solutions for gas-fuelled vessels incertain situations:

• LNG by local liquefaction from NG-pipeline• Container/trailer tank distribution—For example

RoRo (Roll-on, Roll-off) vessels• Compressed natural gas (CNG)—For example

smaller vessels such as commuter ferries

3.2 LNG Source

From a North Sea perspective, the LNG source isdefined as either existing and planned LNG receivingterminals or small-scale LNG production plantsavailable within the North Sea area.Receiving terminals import LNG but store andredistribute the fuel as a gas, primarily to gas grids viapipelines. To use LNG as a fuel for shipping, LNGmust be redistributed in its liquid state. This meansthere is a requirement to establish loading facilities andexport terminals for both trucks and ships. LNG truckloading facilities will have to be designed and built totransport LNG via trucks to end users.

Figure 8: Map of LNG terminals

11

LNG vessel loading and export terminals will also berequired. It is vital that the new export facilities do notinterfere with the operations of the import terminal, andthat both import and export terminals can operateindependently.

The size of ships that will load LNG at an exportterminal may vary. There will probably be both LNGBunker and Feeder vessels loading at the exportfacility. Ideally other types of LNG fuelled vesselscould also be using the facilities to bunker LNG.The design of export terminals for both trucks andvessels should also take possible future expansion intoconsideration.

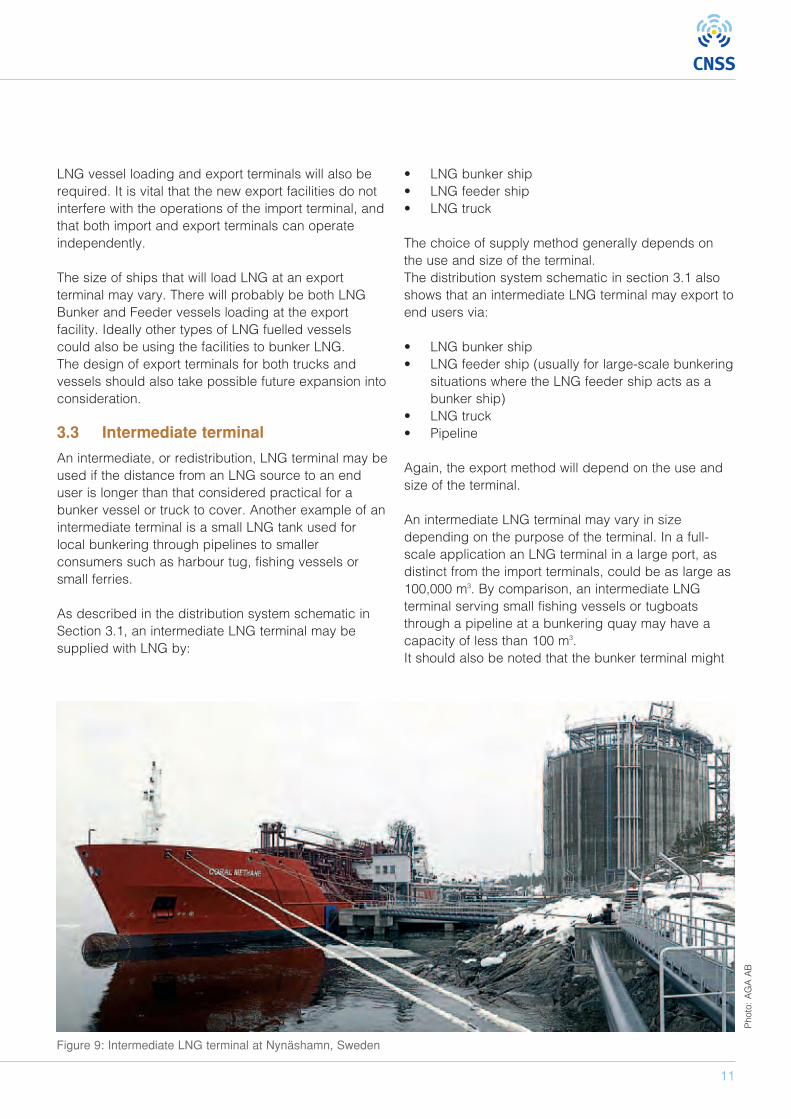

3.3 Intermediate terminal

An intermediate, or redistribution, LNG terminal may beused if the distance from an LNG source to an enduser is longer than that considered practical for abunker vessel or truck to cover. Another example of anintermediate terminal is a small LNG tank used forlocal bunkering through pipelines to smallerconsumers such as harbour tug, fishing vessels orsmall ferries.

As described in the distribution system schematic inSection 3.1, an intermediate LNG terminal may besupplied with LNG by:

• LNG bunker ship• LNG feeder ship• LNG truck

The choice of supply method generally depends onthe use and size of the terminal.The distribution system schematic in section 3.1 alsoshows that an intermediate LNG terminal may export toend users via:

• LNG bunker ship• LNG feeder ship (usually for large-scale bunkering

situations where the LNG feeder ship acts as abunker ship)

• LNG truck• Pipeline

Again, the export method will depend on the use andsize of the terminal.

An intermediate LNG terminal may vary in sizedepending on the purpose of the terminal. In a full-scale application an LNG terminal in a large port, asdistinct from the import terminals, could be as large as100,000 m3. By comparison, an intermediate LNGterminal serving small fishing vessels or tugboatsthrough a pipeline at a bunkering quay may have acapacity of less than 100 m3.It should also be noted that the bunker terminal might

Figure 9: Intermediate LNG terminal at Nynäshamn, Sweden

Photo: AGA AB

be a barge or ship serving as an intermediate terminal.In this case, a bunker vessel as well as an LNG-fuelledship will be able to moor alongside and bunker LNG.

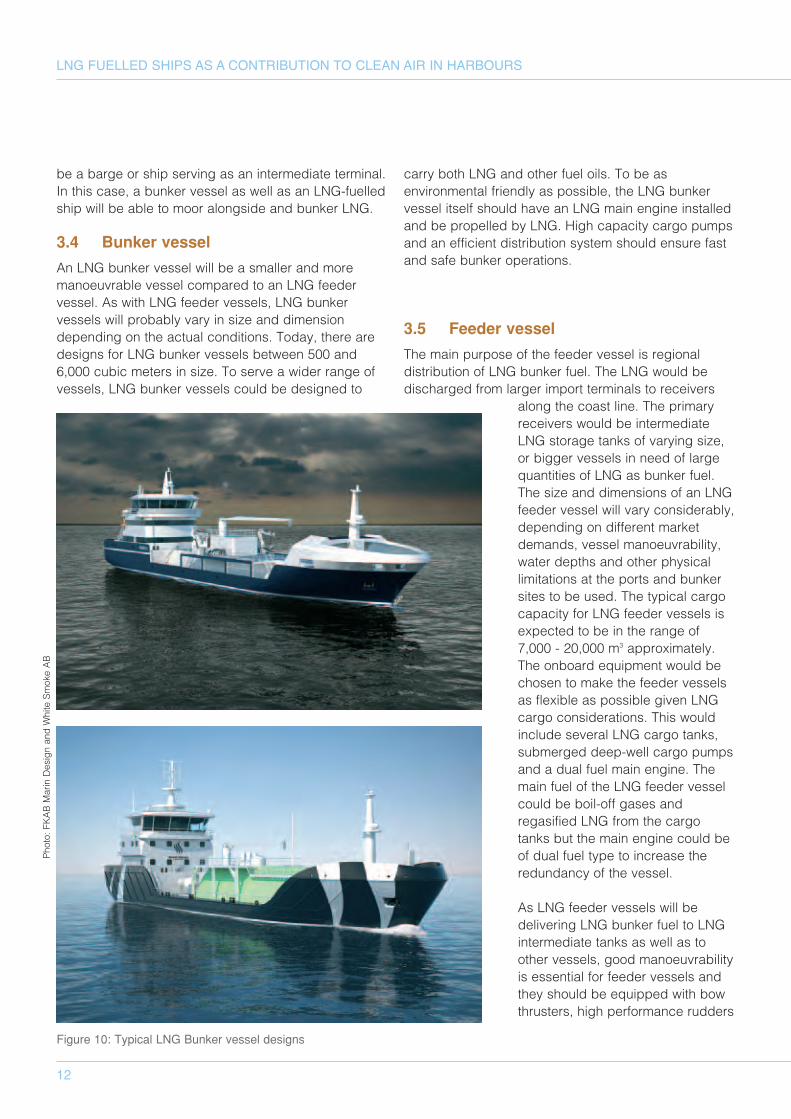

3.4 Bunker vessel

An LNG bunker vessel will be a smaller and moremanoeuvrable vessel compared to an LNG feedervessel. As with LNG feeder vessels, LNG bunkervessels will probably vary in size and dimensiondepending on the actual conditions. Today, there aredesigns for LNG bunker vessels between 500 and6,000 cubic meters in size. To serve a wider range ofvessels, LNG bunker vessels could be designed to

carry both LNG and other fuel oils. To be asenvironmental friendly as possible, the LNG bunkervessel itself should have an LNG main engine installedand be propelled by LNG. High capacity cargo pumpsand an efficient distribution system should ensure fastand safe bunker operations.

3.5 Feeder vessel

The main purpose of the feeder vessel is regionaldistribution of LNG bunker fuel. The LNG would bedischarged from larger import terminals to receivers

along the coast line. The primaryreceivers would be intermediateLNG storage tanks of varying size,or bigger vessels in need of largequantities of LNG as bunker fuel.The size and dimensions of an LNGfeeder vessel will vary considerably,depending on different marketdemands, vessel manoeuvrability,water depths and other physicallimitations at the ports and bunkersites to be used. The typical cargocapacity for LNG feeder vessels isexpected to be in the range of7,000 - 20,000 m3 approximately.The onboard equipment would bechosen to make the feeder vesselsas flexible as possible given LNGcargo considerations. This wouldinclude several LNG cargo tanks,submerged deep-well cargo pumpsand a dual fuel main engine. Themain fuel of the LNG feeder vesselcould be boil-off gases andregasified LNG from the cargotanks but the main engine could beof dual fuel type to increase theredundancy of the vessel.

As LNG feeder vessels will bedelivering LNG bunker fuel to LNGintermediate tanks as well as toother vessels, good manoeuvrabilityis essential for feeder vessels andthey should be equipped with bowthrusters, high performance rudders

12

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURSPhoto: FKAB Marin Design and White Smoke AB

Figure 10: Typical LNG Bunker vessel designs

13

and so on. LNG feeder vessels should beeasy to operate during coastal navigation andmooring operations to minimise the use ofharbour tugs to perform bunker operations.

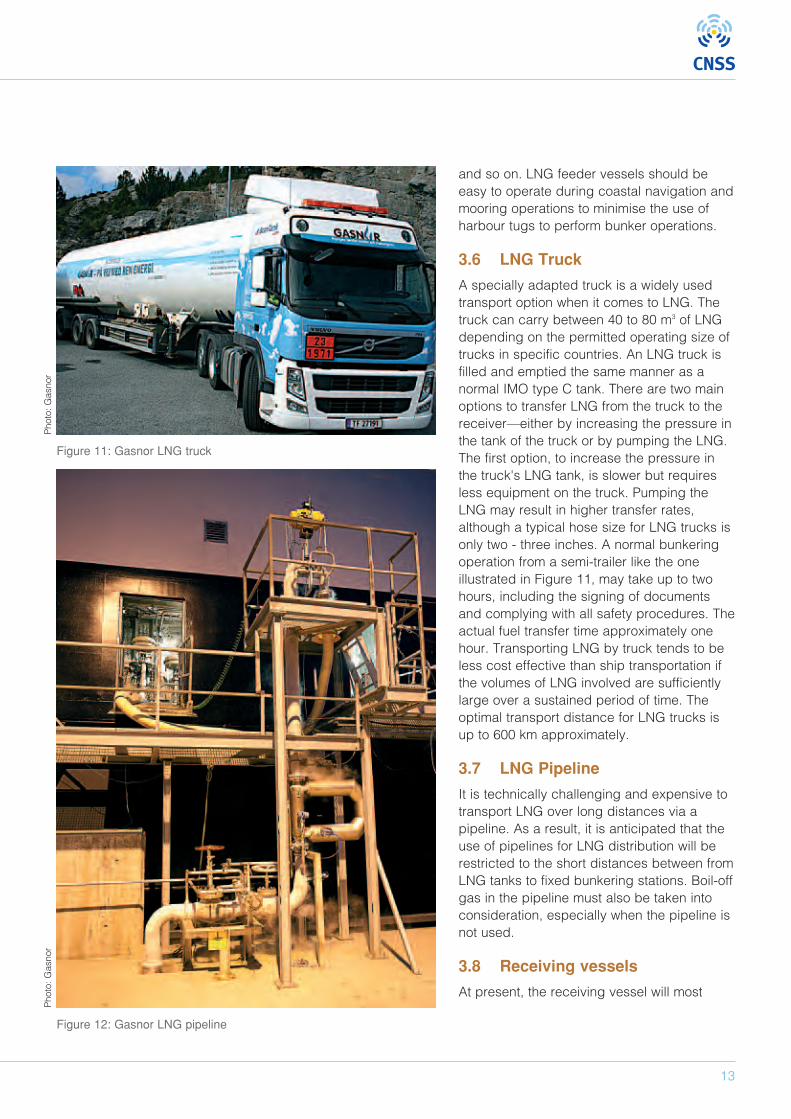

3.6 LNG Truck

A specially adapted truck is a widely usedtransport option when it comes to LNG. Thetruck can carry between 40 to 80 m3 of LNGdepending on the permitted operating size oftrucks in specific countries. An LNG truck isfilled and emptied the same manner as anormal IMO type C tank. There are two mainoptions to transfer LNG from the truck to thereceiver—either by increasing the pressure inthe tank of the truck or by pumping the LNG.The first option, to increase the pressure inthe truck's LNG tank, is slower but requiresless equipment on the truck. Pumping theLNG may result in higher transfer rates,although a typical hose size for LNG trucks isonly two - three inches. A normal bunkeringoperation from a semi-trailer like the oneillustrated in Figure 11, may take up to twohours, including the signing of documentsand complying with all safety procedures. Theactual fuel transfer time approximately onehour. Transporting LNG by truck tends to beless cost effective than ship transportation ifthe volumes of LNG involved are sufficientlylarge over a sustained period of time. Theoptimal transport distance for LNG trucks isup to 600 km approximately.

3.7 LNG Pipeline

It is technically challenging and expensive totransport LNG over long distances via apipeline. As a result, it is anticipated that theuse of pipelines for LNG distribution will berestricted to the short distances between fromLNG tanks to fixed bunkering stations. Boil-offgas in the pipeline must also be taken intoconsideration, especially when the pipeline isnot used.

3.8 Receiving vessels

At present, the receiving vessel will most

Photo: G

asnor

Photo: G

asnor

Figure 11: Gasnor LNG truck

Figure 12: Gasnor LNG pipeline

14

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

likely be using a pressurized IMO type C tank,depending on the size of the vessel. The pressurizedtank will be able to accommodate the increasedpressure that arises during bunkering operations.

From safety perspective, LNG is very different tonormal fuel oils in many respects. During bunkeringoperations, two properties of LNG are particularlyimportant:

• LNG is a very cold (cryogenic) liquid • LNG in gaseous form has a very low flash point

These two properties mean additional requirements forhandling, storage, ventilation and ancillary equipmenton both the receiving vessel as well as the supplysystems. The requirement to ensure the bunkeringarea on the receiving vessel is an all EX-classified andrestricted area during bunkering operations is stillunder discussion. Inside the HA, all electricalequipment is subject to additional safety requirementsand electric energy should be low to avoid ignition ofLNG vapour. The extent of the HA and restricted areais also still under debate and remains to be clarified. Itis not yet clear if it will be possible to use a general HAor if the restricted zone has to be adapted for eachspecific bunkering occasion.

A bunkering station should be located on each side ofthe receiving vessel, preferably on a lower deck andalong the flat section, especially if ship to shipbunkering is to be considered. Although bunkering

options on both sides of the vessel may be a moreexpensive to install, this is the normal configuration ofvessels bunkering fuel oils today. The location of thebunker stations should facilitate hose handling andcommunication for the bunker operator, and ensure thesafety of the bunkering operators on both the receivingship as well as on the supplying source.

Each manifold in the bunker station should beequipped with Break-Away couplings to ensuremaximum safety and minimal leakage. Different driptrays should also be located under the manifolds,optimized for the kind of liquids that will be transferred.For LNG manifolds, the drip tray must feed directly outto sea, to ensure all leakage is drained overboard. Forfuel oil and other liquids, any leakage should be haltedand kept onboard.

The location and design of the bunkering stationsshould also take into consideration the naturalventilation requirements for bunkering operations.

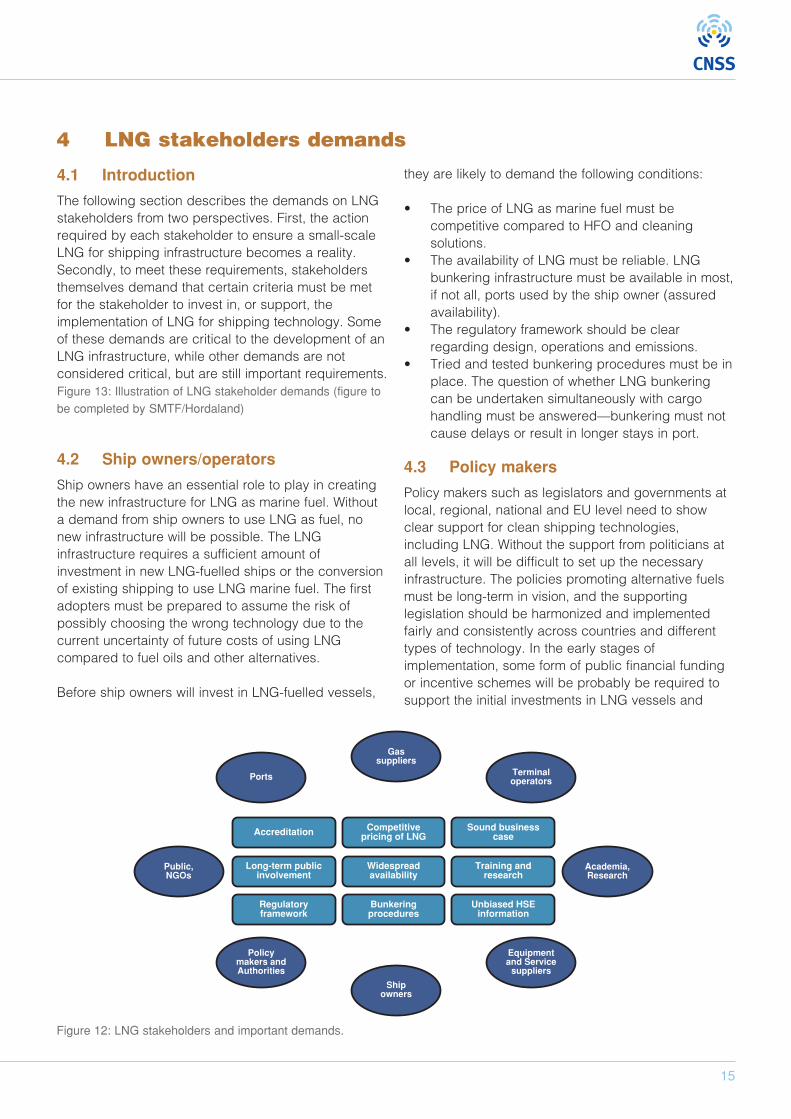

4.1 Introduction

The following section describes the demands on LNGstakeholders from two perspectives. First, the actionrequired by each stakeholder to ensure a small-scaleLNG for shipping infrastructure becomes a reality.Secondly, to meet these requirements, stakeholdersthemselves demand that certain criteria must be metfor the stakeholder to invest in, or support, theimplementation of LNG for shipping technology. Someof these demands are critical to the development of anLNG infrastructure, while other demands are notconsidered critical, but are still important requirements.Figure 13: Illustration of LNG stakeholder demands (figure tobe completed by SMTF/Hordaland)

4.2 Ship owners/operators

Ship owners have an essential role to play in creatingthe new infrastructure for LNG as marine fuel. Withouta demand from ship owners to use LNG as fuel, nonew infrastructure will be possible. The LNGinfrastructure requires a sufficient amount ofinvestment in new LNG-fuelled ships or the conversionof existing shipping to use LNG marine fuel. The firstadopters must be prepared to assume the risk ofpossibly choosing the wrong technology due to thecurrent uncertainty of future costs of using LNGcompared to fuel oils and other alternatives.

Before ship owners will invest in LNG-fuelled vessels,

they are likely to demand the following conditions:

• The price of LNG as marine fuel must becompetitive compared to HFO and cleaningsolutions.

• The availability of LNG must be reliable. LNGbunkering infrastructure must be available in most,if not all, ports used by the ship owner (assuredavailability).

• The regulatory framework should be clearregarding design, operations and emissions.

• Tried and tested bunkering procedures must be inplace. The question of whether LNG bunkeringcan be undertaken simultaneously with cargohandling must be answered—bunkering must notcause delays or result in longer stays in port.

4.3 Policy makers

Policy makers such as legislators and governments atlocal, regional, national and EU level need to showclear support for clean shipping technologies,including LNG. Without the support from politicians atall levels, it will be difficult to set up the necessaryinfrastructure. The policies promoting alternative fuelsmust be long-term in vision, and the supportinglegislation should be harmonized and implementedfairly and consistently across countries and differenttypes of technology. In the early stages ofimplementation, some form of public financial fundingor incentive schemes will be probably be required tosupport the initial investments in LNG vessels and

Ports

Gassuppliers

Terminaloperators

Policymakers andAuthorities

Shipowners

Equipmentand Service

suppliers

Public,NGOs

Academia,Research

Accreditation Competitivepricing of LNG

Sound businesscase

Long-term publicinvolvement

Widespreadavailability

Training andresearch

Regulatoryframework

Bunkeringprocedures

Unbiased HSEinformation

15

4 LNG stakeholders demands

Figure 12: LNG stakeholders and important demands.

16

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

bunkering infrastructure as well as the work required toestablish the necessary regulatory framework.

On the other hand, for policy makers to take astandpoint and make important decisions that will berequired, they will need credible and unbiasedinformation on LNG as a potential clean marine fuel,addressing both the risks and benefits regardinghealth, safety and environment. Any input to theprocess must be of high quality to support policymaking decisions. The political decision makers musthave a realistic view of the technical and financialchallenges posed by LNG and possible implicationsfor the other stakeholders.

4.4 Authorities

Authorities such as transport, safety, environment andsimilar bodies are of crucial importance forimplementing the LNG for shipping infrastructure. Thesupport of these authorities will be essential forimplementing and enforcing the necessary regulatoryframework. The regulations should be set at anappropriate level to ensure safety, but be flexibleenough to accommodate shipping businessoperations. The authorities must communicate theirrequirements to other stakeholders and acquiresufficient knowledge of the LNG infrastructure througheither their own or third party studies. These authoritiesmay be required by politicians to provide many of theexpert statements that will inform the decision makingprocess.

The authorities will require clear directives andfinancial support from the policy makers to completethe research and detailed investigation into what willbe required to set up the appropriate regulatoryframework. Authorities will also require detailedinformation from various stakeholders, researchorganisations, and so on to support their decisions.

4.5 Ports

The ports are a crucial part of the LNG supply chain.From a sustainable LNG infrastructure perspective, asufficient number of ports must make locationsavailable for small-scale LNG terminals and bunkerfacilities. The port authority needs to establish localregulations and port by-laws, approved by otherrelevant authorities. In addition, the ports may be apossible source of funding for investment support. Forexample, the Port of Antwerp is planning to develop an

LNG bunker vessel to support the growing interest inusing LNG as marine fuel. Another example is the Portof Gothenburg, which has decided to invest threebillion SEK in the necessary logistics to offer ships thepossibility to bunker LNG (Henriksson, 2012).

The following points describe some of the generalrequirements that should be met before port authoritieswill support the establishment of an LNG infrastructure.

• Available space both onshore and offshore• A sound business case for the port with sufficient

LNG fuel demand from the users• Support from the owner(s) of the port• Possible internal or external funding• An established regulatory framework • Accreditation of bunker companies

4.6 Terminal operators

The terminal operators are independent companiesbuilding and operating the LNG terminal on the portpremises, where the LNG will be stored and distributedto different customers. If this step is not managed bythe port or the gas supplier, the LNG infrastructuredemands the support of a competent terminal operatorwho can establish and run the terminal and also offer arealistic contract model for gas suppliers regardingquantities and contract length (short-term versus long-term).

Terminal operators will require sufficient user demandwith the potential economies of scale offered bydifferent types of gas users such as the energy sector,manufacturing industries, shipping, and landtransportation (car, trucks, and so on.). Moreover, theregulatory framework should be in place, and externalfunding may also be necessary to persuade potentialoperators to commit to investing in a new terminal.

4.7 LNG suppliers

Gas as fuel for ships is a potentially new market forgas suppliers, although by comparison to the total gasconsumption market, the LNG marine fuel market willbe relatively small.

If LNG as marine fuel is going to be an attractivealternative for shipping, the gas suppliers must be ableto offer stable gas deliveries and competitive pricescompared to other options for fuel and cleaningtechnologies. Contracts with ship and terminal

17

operators should be reasonable in terms of price,quantities and length of contract. It is also importantthat gas suppliers, together with terminal operators,define and adhere to a minimum quality range of LNG.

If a gas supplier is going to deliver LNG to ships, theremust be sufficient user demand. The shipping industrywill probably take a relatively small share of the totalgas deliveries, but with the right location of terminalsthere are bunkering opportunities for a large number ofships of different categories and the possibleeconomies of scale advantages from other types ofusers. The small-scale LNG supply chain is still underdevelopment, as is the regulatory framework for usingLNG as marine fuel. When the supply chain andregulatory framework are established, shipping is likelyto be a growing market for many gas suppliers.

4.8 Others

4.8.1 Equipment and service suppliers

The various marine technology suppliers are importantplayers in the development of a successfulinfrastructure for LNG as marine fuel. Enginemanufacturers and other equipment and servicesuppliers must have the appropriate technologyavailable and the capacity to deliver the necessaryequipment to meet the demand. Most of thetechnology solutions regarding using LNG as fuel areavailable today, but further improvements are stillrequired. The technology suppliers will continue todevelop their equipment if they can expect enoughpotential demand from ship owners who are ready toupgrade their fleet.

4.8.2 Research and education

As with many new technologies, there is also a needfor research and training. Independent studies byresearch institutions and similar organisations areimportant to establish a scientific basis for the real costand benefits of using LNG as marine fuel bycomparison to the alternatives. Universities and othereducational organisations are also important indeveloping the necessary training courses andeducational programs for onboard and offshore crew,authorities and related organisations as to the correctprocedures for using LNG as fuel for ships. For these institutions to consider this matter a priority, itmay be necessary to issue policy directives and offerfinancial support to set up research and educationalprograms. Chapter 11 will provide further informationon LNG education and training.

4.8.3 General public

The general public may not be regarded as a directstakeholder in the development of the LNG forshipping infrastructure, but their indirect support andacceptance of using this technology is still important.People require safe and environmentally friendlytransport at a reasonable price. It may be necessaryfor the other stakeholders to inform and educate thegeneral public about using gas and LNG for shipping.In particular, it seems that safety issues should beaddressed and explained, but also the possibleenvironment and health benefits that comes with acleaner fuel alternative. In the end, it is often thewishes of the general public that direct future policies.

4.8.4 Non-governmental organisations

As with the general public, non-governmentalorganisations such as environmental groups might notbe considered as direct stakeholders in developingLNG for shipping infrastructure. However, their indirect,and occasionally direct, support and acceptance ofthis technology may prove to be very important. TheNGOs will be in favour of safe, clean andenvironmentally friendly transport.

Figur 14: Liquiline semitrailer discharging to ferry

Photo: Liquiline

18

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

This chapter gives a brief overview of the presentregulations, standards and legislation regarding LNG.The initiatives that are currently being undertaken bygovernmental and private bodies are also discussed.Further information can be found in the Flemish Study.

5.1 Regulations for marine activities

The regulatory framework for seagoing vessels isoverseen by the International Maritime Organization(IMO). A brief overview of the most relevant parts ofthe framework is provided in the following sections.

5.1.1 Emission Control Area

Stricter emission controls than those required at aglobal level are enforced in specifically designatedgeographical areas. An Emission Control Area (ECA)can be designated for SOX, NOX or both. An ECA(NOX and SOX) comes in effect in 2012 in NorthAmerica, which includes most of the US and Canadiancoasts. The Baltic Sea, the North Sea and the EnglishChannel have been designated as an ECA for SOXemission reduction, also referred to as a SulphurEmission Control Area (SECA). This restriction meansthat the maximum allowable sulphur content of bunkerfuel is 1% (from July 1, 2010) and 0,1% from January1, 2015 (MOW, 2012).

5.1.2 SOLAS

The International Convention for the Safety of Life atSea (SOLAS) is an international maritime safety treaty.SOLAS requires member states to ensure that theirships comply with minimum safety standards withrespect to construction, equipment and operation.Chapter VII of this treaty requires the carriage of alldangerous goods to be in compliance with theInternational Maritime Dangerous Goods Code (IMDG)but it contains no specific reference to the use of LNG.The construction and equipment of ships carryingliquefied gasses in bulk and gas carriers is determinedin SOLAS to comply with the International Gas CarrierCode (IGC code) (MOW, 2012).

5.1.3 MARPOL

The International Convention for the Prevention ofPollution from Ships (MARPOL) is the maininternational convention covering prevention ofpollution by ships, from operational or accidentalcauses, of the marine environment. The Conventionincludes regulations aimed at preventing andminimizing pollution from ships and currently includessix technical Annexes. Annex VI covers the Preventionof Air Pollution from Ships and it establishes limits onsulphur oxide and nitrogen oxide emissions from shipexhausts, prohibiting deliberate emissions of ozone

5 Existing and future regulations, standards and legislations

Figure 15: Viking Grace and MS Stavangerfjord

Photo: Viking Line

Photo: Fjordline

19

depleting substances. It also sets designated emissioncontrol areas with more stringent standards for SOx,NOx and particulate matter (ECAs) (IMO, 2013).

5.1.4 International Gas Carrier Code (IGCcode)

The IGC-code applies to gas carriers constructed onor after 1/7/1986. The code provides an internationalstandard for safe transportation by prescribing designand construction standards. Older carriers either haveto comply with the Code for the Construction andEquipment of Ships Carrying Liquefied Gases in Bulk(GC Code) or the Code for Existing Ships CarryingLiquefied Gases in Bulk (if the carrier was constructedbefore 31/12/1976) (MOW, 2012).

5.1.5 International Code for the Constructionof Gas Fuelled Ships (IGF code)

There are no formal IMO rules concerning LNG fueledvessels other than the IGC code that permits LNGcarriers to use their boil-off gas as a fuel. Thepublication of an international code for the constructionof gas fueled ships is expected to be published noearlier than 2013-14. As vessels are not permitted touse an oil fuel with a flashpoint of less than 60°(SOLAS, II-2, part B – prevention of fire and explosion),an interim guideline was published by the IMO,formally known as Resolution MSC.285(86). The IGFcode will not include the bunkering of LNG (MOW,2012).

5.1.6 Class rules

Seagoing vessels are all built according to class rulesset by a classification society. With the introduction ofthe first LNG carrier, the classification societiesdeveloped specific rules for the construction and safeoperation of LNG carriers. To ensure the safety andtechnical integrity of propulsion systems fueled byLNG, additional rules are being developed.

The International Association of Classification Societiesis a supra-structure that publishes the UnifiedRequirements, from which requirement M59 is ofparticular relevance: the Control and Safety Systemsfor Dual Fuel Diesel Engines (MOW, 2012).

5.1.7 European Maritime Safety Agency

The European Maritime Safety agency (EMSA) aims toprovide a consolidated version of possible commonEU-wide checklists, guidelines or standards for LNGbunkering. In May 2013 EMSA published a tender for astudy on standards and rules for bunkering of gas-fuelled ships. The first results are expected inDecember 2012. The tender contains 4 tasks (EMSA,2012):1. Provide a detailed description of the standards,

regulations and guidelines related to LNGbunkering

2. Provide a gap analysis on the requirements ofcurrent and on-going LNG related rules

3. Provide a consolidated version of a proposed forcommon EU-wide guidelines or standards for LNGbunkering

4. Present preliminary results of tasks 1-3 tostakeholders and member states

Two working groups have been created—a group ofEU pioneer ports and bunker operators and a group ofship and ferry operators. These groups will act asreference groups for study and potential new LNGrelated initiatives by EMSA.

5.2 Ship-to-shore and ship-to-shiptransfer standards

The regulatory framework for seagoing vessels doesnot include the transfer of materials. Advice andsupport for these operations are captured in currentoperating standards and best practices. These areprepared by societies such as the Society ofInternational Gas Tanker & Terminal Operators(SIGTTO) and the Oil Companies International MarineForum (OCIMF).

An important document for LNG is the Ship-to-ShipTransfer Guide (Liquefied Gases) by OCIMF/SIGTTO,which was originally written for the transfer of LPG atsea. Another important reference is the LNG ship-to-ship transfer guidelines. This covers the transfer ofLNG from carriers at anchor, alongside a shore jetty orunderway (MOW, 2012).

20

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

Several publications that cover ship-to-shore bunkeringare available, for example:

• Safety in Liquefied Gas Marine Transportation anTerminal operators

• Ship-Shore Interface–Safe Working Practices forLPG & Liquefied Chemical Gas Cargoes

• LNG operations in Port Areas, ESD arrangementsand Linker Ship-to-Shore Systems for LiquefiedGas Carriers

Another applicable OCIMF regulation is theInternational Safety Guide for Oil Tankers & Terminals(ISGOTT).

A procedural description on LNG ship-to ship-bunkering has been carried out by the Swedish MarineTechnology Forum1. The document's scope is LNGship-to-ship bunkering procedures in a portenvironment with concurrent cargo and passengerhandling in progress.

5.2.1 International organization forstandardization (ISO)

ISO produces International Standards, TechnicalReports, Technical Specifications, Publicly availableSpecifications, Technical Corrigenda and Guides. Twopublications, “ISO 28460:2010 – LNG ship to shoreinterface and Port Operations” and “ISO13709:2003 –Centrifugal pumps for Petroleum, Petrochemical andNatural Gas Industries” relate to the use of LNG. Aworking group (ISO TC67/WG10) is developingguidelines (in the form of a technical report) forsystems and installations that will use and supply ofLNG as fuel to ships. Results are expected in March2013 (MOW, 2012).

5.3 Global initiatives by involved parties

From a diverse group of companies and institutions,initiatives are currently underway to take the lead in theimplementation of LNG as marine fuel.

5.3.1 World Ports Climate Initiative

The International Association of Ports and Harbours(IAPH) organizes various international workgroups

within the World Ports Climate Initiative (WPCI, 2012),each focusing on a specific aspect of the environmentin the port sector. WPCI is supported by the EuropeanSea Ports Organization (ESPO) and EMSA. Themembers of these workgroups are mainly portauthorities. The WPCI LNG workgroup endeavors to bethe forum for the early standardisation processesbetween ports and to develop guidelines and/orassess the possible impact at ports with regard toinfrastructure, safety requirements for bunkering andthe legal aspects on the use of LNG. WPCI has coversfour main areas:

1. Bunker checklists and guidelines for theaccreditation of LNG bunkering companies

2. Give guidance to harmonize the approach of riskperimeters

3. Provide clear and unbiased information for thepublic

4. Create an information share point between ports

5.3.2 SIGTTO

SIGTTO is concerned that many people who maypotentially be involved in the LNG infrastructure, suchas bunkering suppliers and crew on LNG-fueledvessels, could lack relevant knowledge about theproperties and hazards of LNG. SIGTTO states that anincident on an LNG-fueled vessel will affect the widerLNG industry, which has an almost zero incident trackrecord at the present. Particular areas of concern aretraining of crew and bunker suppliers, simultaneousoperations and ship design. SIGTTO is involved withthe Ship-to-Ship Transfer Guide (Liquefied Gases). TheLNG Ship Fuel Safety Advisory Group promotes theuse of natural gas with an equivalent level of safety forthe large scale LNG transport industry. The AdvisoryGroup supports stakeholders in the marine gas fuelindustry, identifies issues and provides guidance andinformation based on the experience of groupmembers (MOW, 2012). At present, SIGTTO is:

• Participating in IMO work and correspondinggroups of the IGF code

• Part of the ISO TC67 working group 10• Reviewing of IGC Code

1Also: FKAB Marine Design, Linde Cryo AB, Det Norske Veritas AS (DNV), LNG GOT and White Smoke AB

21

5.3.3 North European LNG InfrastructureProject

In 2012, the EU founded a study on the feasibility foran LNG filling station infrastructure in North Europe2. Abrief overview of the permit processes andconsultation with authorities and the general public isprovided. An important part of this study containsrecommendations made on several aspects of theLNG, three of which focused on the permit process(MOW, 2012).

5.3.4 Methods for provision of LNG asshipping fuel in Flemish ports

The Flemish Department of Mobility and Public Work(MOW) commissioned a report on the methods for theproviding LNG as marine fuel in Flemish ports,subsequently referred to as the Flemish Study. Thisstudy also made some recommendations for thenecessary regulatory framework. Theserecommendations have been adopted by the recentlyfounded Flemish LNG expert group, chaired by MOW.

5.4 Regulations for onshore activities

5.4.1 International standards and bestpractices

5.4.1.1 European Committee forStandardization (CEN)

Most of the standards for land-based constructions inEurope are determined by the European Committee forStandardization. Some standards are voluntary, othersmay be mandatory under EU law. A list of standardsthat apply to LNG can be found in the Flemish Study(MOW, 2012).

5.4.1.2 The Code of Federal Regulations(CFR)

CFR standards are produced by different AmericanSocieties, such as the US Department ofTransportation Pipeline and Hazardous MaterialsSafety Administration and others. An overview of LNGapplicable regulations can be found in the FlemishStudy (MOW, 2012).

5.4.1.3 The National Fire ProtectionAssociation (NFPA)

The following NFPA standards apply to LNG facilities:

• NFPA 59A—Production and Storage of LNG • NFPA 30—Flammable and Combustible Liquids

Code

5.4.1.4 The American Petroleum Institute(API)

Most of the standards and recommended practicesfrom the API are dedicated to a single type ofequipment. The Flemish Study (MOW, 2012) providesan overview of the relevant documents.

5.4.2 European legislation

5.4.2.1 Provision of Public Consultation

The national regulations concerning the publicconsultation process and making information availableto the public are governed by the EnvironmentalImpact Assessment (EIA) Directive (85/337/EEC).According to this Directive each Member State candetermine if an Environmental Impact Assessment iscompulsory. The guidelines define minimumrequirements for public consultation. The provisions forpublic participation in the EIA Directive werestrengthened by the introduction of Directive2003/35/EC, which included early public consultationin the decision-making procedure (DMA, 2012).

5.4.2.2 The Seveso Directive

The Seveso Directive (96/82/EC) is the main piece ofEU legislation dealing specifically with the control ofonshore major accidents involving dangeroussubstances. The Directive implements two tiers ofcontrol:

• Lower tier (Seveso I)—Covers establishmentswhich hold more than 50 tonnes of LNG

• Upper tier (Seveso II)—Covers establishmentsabove 200 tonnes (DMA, 2012)

2 The main partner in the study was the Danish Maritime Authority, other partners were Bureau Veritas, Energigas Sverige,Fluxys LNG, Gasnor, Gazprom, GL, Gasunie, Gazprom, Lauritzen Kosan, MAN, Flemish department of Mobility and PublicWorks, Norwegian Ministry of Trade and Industry, Hirtshals Havn, Port of Rotterdam, Port Szczecin-swinoujscie, Port ofZeebrugge, Finnish Transport Safety agency, Den Danske Maritime Fond.

22

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

The Directive also obliges competent authorities to forexample, examine the Safety Report, to communicatewith the operator and the public, and to identify anypossible domino effects following a major incident.

5.4.2.3 International Carriage of DangerousGoods by Road (ADR)

The European agreement concerning the internationalcarriage of dangerous goods by road (ADR) has beenadopted by most of the 56 members of the UnitedNations Economic Commission for Europe (UNECE orECE) and incorporated into the various nationallegislations. The transportation of LNG is subject to theconditions outlined in Annexes A (construction andlabelling) and B (construction of the truck) (MOW,2012).

5.5 Regulations for transporting LNG viainland ship-based activities

The following section provides a brief overview of thetwo main governing bodies, the regulatory frameworkand standards governing the transportation of LNG viainland vessels.

5.5.1 The Rhine Vessel InspectionRegulations (RVIR)

The Central Commission for the Navigation on theRhine (CCNR) publishes its technical rules in the RVIR,which has become Europe's main technical referenceon the subject. The regulations have been partlytransposed into other national regulations by UNECEand the European Community (2006/87/EC). As aresult, the CCNR recognizes the validity of Communitycertificates on the Rhine, while Rhine certificates arealso been recognized on all EU waterways. Futuredevelopment of Rhine and EU regulations areexpected to evolve in tandem so as to remainidentical.

RVIR regulation is stringent but also flexible, with arange of implementation options including:

• Transitory provisions—Takes into account of thevested rights of older vessels

• Temporary 3-year provisions—CCNR may test anew rule for a period 3 years after which the rulewill be either abandoned or adopted

• Waivers—Vessel operators may use alternativetechnology not covered by the regulations other ifcomparable guarantees can be provided (MOW,2012)

5.5.2 The international carriage of dangerousgoods by inland waterways (ADN)

In 2000, the United Nations Economic Commission forEurope (UNECE) produced a European agreementconcerning the International Carriage of DangerousGoods by Inland Waterways (ADN). The regulationsoutlined in the annexes of the ADN contain provisionsconcerning the carriage of dangerous substancesincluding the requirements and procedures forinspections, issuing certificates of approval,recognition of classification societies, monitoring,training and the examination of experts.

Inland shipping legislation—ADN, RVIR and EuropeanDirective—contain specific information about the use offuel in a shipping engine. As the legislation states thatthe use of fuel with a flashpoint below 55°C is notpermitted, propulsion by LNG is prohibited in inlandwaterways. The transportation of LNG as cargo is alsoprohibited. ADN legislation only applies to inland shipsthat are certified for the transportation of dangerousgoods by inland waterways. Ferries and other shipsthat do not transport dangerous goods do not have tocomply with ADN legislation. Despite the fact that thecurrent European legislation prohibits the use of LNGas a fuel, there are already inland ships inside theEuropean Union that are using LNG as marine fuel. Toallow LNG-fuelled ships on national waters, the Dutchauthorities introduced a temporary exemption throughUNECE / CCNR, which implies that the vesselobtaining the exemption can operate in all EUcountries. This temporary exemption is possiblebecause of the waiver arrangements available in theRVIR that provides ship owners and builders theopportunity to implement alternate, equivalentarrangements. Any proposed exemptions mustdemonstrate that the alternative arrangement is at leastas safe as the original arrangements governed by theRVIR. One disadvantage of the waiver principle is twosister ships cannot use the same waiver as they arenot considered unique (MOW, 2012).

23

5.5.3 International Safety Guide for InlandTank-barges and Terminals (ISGINTT)

The OCIMF, together with other stakeholders for inlandwaterways (such as the CCNR), developed theInternational Safety Guide for Inland Tank-barges andTerminals (ISGINTT). The ISGINTT is not intended toreplace or amend current legislation as ADN and RVIR,but to provide additional recommendations. The CCNRsupports the ISGINTT as the principal industryreference manual for the safe operation of tankers andthe terminals that serve them (MOW, 2012).

5.6 Conclusion

As the permitted sulphur emissions inside an ECA willbe further restricted by 2015, an enormous amount ofinfrastructure redevelopment and associated activities

will be required to facilitate the use of LNG as marinefuel. The main parties involved in the shipping industryare urging the adaption of existing legislation andstandards to support the required changes. A majorconsideration is the desire to maintain the good safetyrecord that LNG has acquired over the years. Althoughthis much needed, safety-focused development isvulnerable on two fronts. First-adopter organisationscould be hampered if legislative bodies are notsufficiently involved with currently developing projects.Conversely, too many single-party initiatives could leadto a proliferation of rules and standards that may notbe in line with the eventual legislation. Open andconstructive communication between all stakeholdersis viewed as crucial to avoiding both of these potentialoutcomes.

Photo: Shell

Shell’s LNG powered barge Greenstream

6.1 Present status

As described in Chapter 5 there are no currentinternational standards or guidelines for bunkeringLNG as fuel. A number of LNG transfer guidelines areavailable, for example from the SIGTTO, but theseguidelines are limited to LNG cargo transfer and arenot applicable for bunkering LNG due to the followingtransfer arrangements:

• LNG transfer takes place in dedicated separatedareas such as special harbours for tanker

• Trained crews and personnel handle the LNG• No simultaneous cargo handling operation• No requirement to consider the effect on third

parties such as passengers

Additionally the existing transfer guidelines are limitedto the ship-to-ship transfer of LNG and do not take intoaccount the range of possible bunkering processesincluding:

• Shore-to-ship• Truck-to-ship• Connection and disconnection of mobile fuel tanks

6.2 On-going international developments

The most important international developments withrespect to LNG rules at present are the developmentof the IGF Code by the IMO sub-committee BLG andthe development of Guidelines for bunkering LNG bythe ISO Technical Committee 67 Working Group 10. Asthe IGF code will only include requirements for thebunker station, all other aspects related to the LNGbunkering process were addressed by the ISO TC 67WG 10, which was established to develop the"Guidelines for systems and installations for supply ofLNG as fuel to Ships". The working group will producethe final set of guidelines by 2014, with a high-leveldraft version of the guidelines available during the firsthalf of 2013.

The objectives of the ISO guidelines are to standardizethe interface between ship and bunkering facilities,

connection and disconnection, the emergencyshutdown procedures and the LNG bunkering processcontrol, to ensure that an LNG-fuelled ship can refuelsafely and reliably regardless of the type of bunkeringfacility. The LNG bunkering interface comprises thearea of LNG transfer and includes manifold, valves,safety and security systems, and the personnelinvolved in the LNG bunkering operations.

The structure of the ISO guidelines is as follows:1. Scope2. Normative references3. Terms and definitions4. General principles5. Properties and behaviour of LNG as fuel6. Safety7. Functional requirements for LNG bunkering

system8. Requirements to components and systems9. Training10. Requirements for documentation

6.3 National initiatives and solutions

In addition to the on-going international developmentof rules within different European countries, bunkeringprocedures have been developed and are allowedsubject to special permission:

• Many of the existing LNG-fuelled vessels currentlyoperate in Norwegian waters. They are bunkeredvia truck or local bunkering stations. Under normalconditions general permission is given in the lawand is based on risk analysis. Under specialconditions permission is given from NorwegianDirectorate for Civil Protection and the local firebrigade.

• During the LESAS project the current framework ofregulation, codes and standards for theestablishment of a small scale LNG supply chain,and using LNG as fuel for shipping and vehicles inthe Netherlands has been investigated for variousbunkering operations.

24

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

6 Bunkering procedures

25

• Germanischer Lloyd (GL) undertook a study onbehalf of the Federal Ministry of Transport,Building and Urban development ( ”Feasibilitystudy for bunkering liquefied gas within Germanports”) to investigate the current regulatoryframework and safety requirements for a safebunkering of LNG within German ports. One of theresults of the study is a draft report on safetyoperations for LNG bunkering within ports.

• In March 2013 the European Maritime SafetyAgency (EMSA) published the “study onstandards and rules for bunkering of gas-fuelledships” carried out by GL. The objective of theinvestigation is to provide an overview of theexisting rule framework, the current developmentof rules regarding bunkering gas-fuelled vessels,and to identify a possible requirement for aEuropean edict for regulating LNG bunkering.

6.4 Conclusion

At present the development of the ISO TC 67 WG10PT1 LNG bunkering guidelines seems to be the mostimportant step towards the international regulation ofbunkering LNG as fuel for shipping, taking intoaccount a common risk assessment approach as wellas functional and safety requirements for the transfersystem. A first draft of the guidelines will be availablein March 2013. It remains to be seen if theseguidelines will provide the necessary guidance toensure safe LNG bunkering within normal port limitsand during normal harbour operation of vesselsincluding:

• At each harbour within the port• During cargo loading and unloading• During passenger embarkation and

disembarkation

26

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

7.1 Introduction

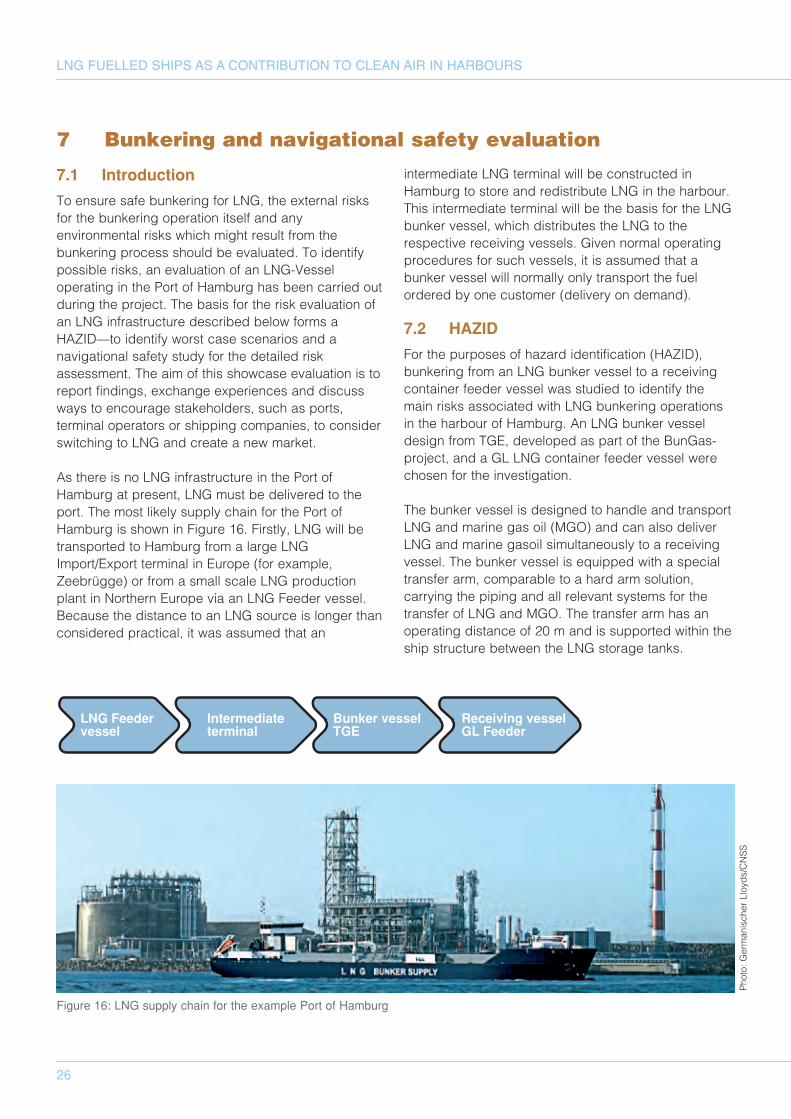

To ensure safe bunkering for LNG, the external risksfor the bunkering operation itself and anyenvironmental risks which might result from thebunkering process should be evaluated. To identifypossible risks, an evaluation of an LNG-Vesseloperating in the Port of Hamburg has been carried outduring the project. The basis for the risk evaluation ofan LNG infrastructure described below forms aHAZID—to identify worst case scenarios and anavigational safety study for the detailed riskassessment. The aim of this showcase evaluation is toreport findings, exchange experiences and discussways to encourage stakeholders, such as ports,terminal operators or shipping companies, to considerswitching to LNG and create a new market.

As there is no LNG infrastructure in the Port ofHamburg at present, LNG must be delivered to theport. The most likely supply chain for the Port ofHamburg is shown in Figure 16. Firstly, LNG will betransported to Hamburg from a large LNGImport/Export terminal in Europe (for example,Zeebrügge) or from a small scale LNG productionplant in Northern Europe via an LNG Feeder vessel.Because the distance to an LNG source is longer thanconsidered practical, it was assumed that an

intermediate LNG terminal will be constructed inHamburg to store and redistribute LNG in the harbour.This intermediate terminal will be the basis for the LNGbunker vessel, which distributes the LNG to therespective receiving vessels. Given normal operatingprocedures for such vessels, it is assumed that abunker vessel will normally only transport the fuelordered by one customer (delivery on demand).

7.2 HAZID

For the purposes of hazard identification (HAZID),bunkering from an LNG bunker vessel to a receivingcontainer feeder vessel was studied to identify themain risks associated with LNG bunkering operationsin the harbour of Hamburg. An LNG bunker vesseldesign from TGE, developed as part of the BunGas-project, and a GL LNG container feeder vessel werechosen for the investigation.

The bunker vessel is designed to handle and transportLNG and marine gas oil (MGO) and can also deliverLNG and marine gasoil simultaneously to a receivingvessel. The bunker vessel is equipped with a specialtransfer arm, comparable to a hard arm solution,carrying the piping and all relevant systems for thetransfer of LNG and MGO. The transfer arm has anoperating distance of 20 m and is supported within theship structure between the LNG storage tanks.

7 Bunkering and navigational safety evaluation

LNG Feedervessel

Intermediateterminal

Bunker vesselTGE

Receiving vesselGL Feeder

Figure 16: LNG supply chain for the example Port of Hamburg

Photo: G

ermanischer Lloyds/CNSS

27

Movements of both ships during fuel transfer can becontrolled by an automatic adjustment control systemthat equalizes all relative movements.

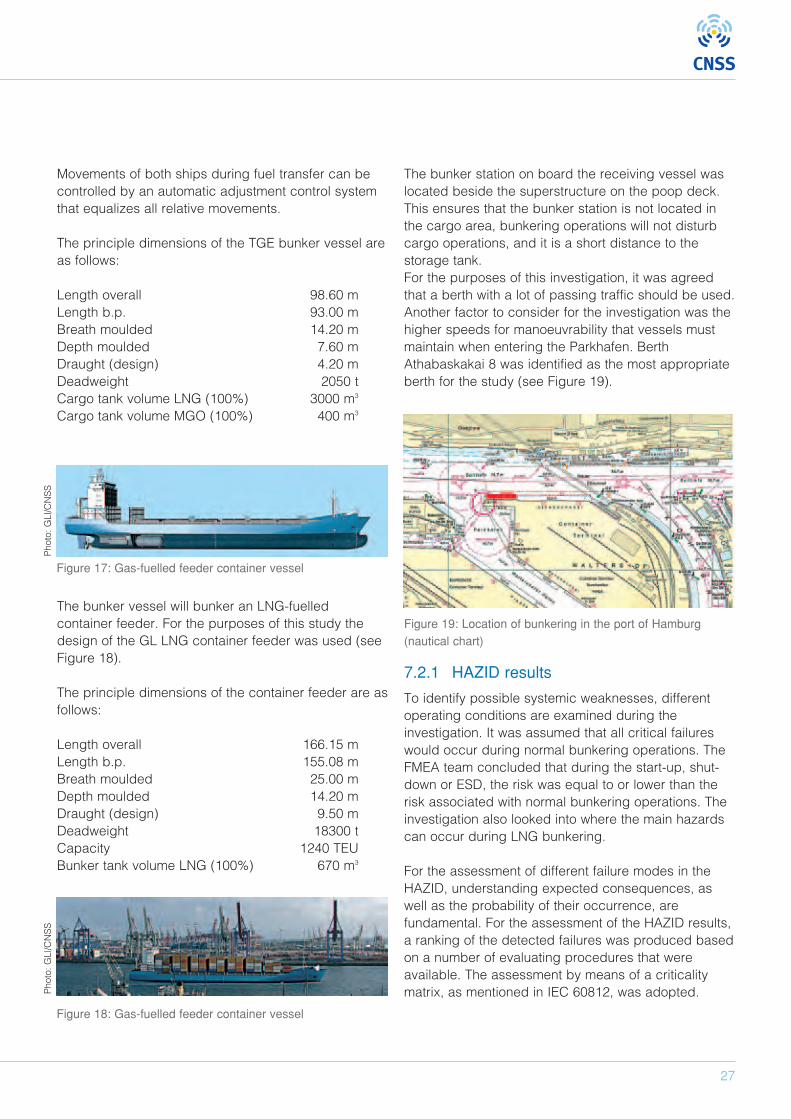

The principle dimensions of the TGE bunker vessel areas follows:

Length overall 98.60 mLength b.p. 93.00 mBreath moulded 14.20 mDepth moulded 7.60 mDraught (design) 4.20 mDeadweight 2050 tCargo tank volume LNG (100%) 3000 m3

Cargo tank volume MGO (100%) 400 m3

The bunker vessel will bunker an LNG-fuelledcontainer feeder. For the purposes of this study thedesign of the GL LNG container feeder was used (seeFigure 18).

The principle dimensions of the container feeder are asfollows:

Length overall 166.15 mLength b.p. 155.08 mBreath moulded 25.00 mDepth moulded 14.20 mDraught (design) 9.50 mDeadweight 18300 tCapacity 1240 TEUBunker tank volume LNG (100%) 670 m3

The bunker station on board the receiving vessel waslocated beside the superstructure on the poop deck.This ensures that the bunker station is not located inthe cargo area, bunkering operations will not disturbcargo operations, and it is a short distance to thestorage tank.For the purposes of this investigation, it was agreedthat a berth with a lot of passing traffic should be used.Another factor to consider for the investigation was thehigher speeds for manoeuvrability that vessels mustmaintain when entering the Parkhafen. BerthAthabaskakai 8 was identified as the most appropriateberth for the study (see Figure 19).

Figure 19: Location of bunkering in the port of Hamburg(nautical chart)

7.2.1 HAZID results

To identify possible systemic weaknesses, differentoperating conditions are examined during theinvestigation. It was assumed that all critical failureswould occur during normal bunkering operations. TheFMEA team concluded that during the start-up, shut-down or ESD, the risk was equal to or lower than therisk associated with normal bunkering operations. Theinvestigation also looked into where the main hazardscan occur during LNG bunkering.

For the assessment of different failure modes in theHAZID, understanding expected consequences, aswell as the probability of their occurrence, arefundamental. For the assessment of the HAZID results,a ranking of the detected failures was produced basedon a number of evaluating procedures that wereavailable. The assessment by means of a criticalitymatrix, as mentioned in IEC 60812, was adopted.

Figure 17: Gas-fuelled feeder container vessel

Figure 18: Gas-fuelled feeder container vessel

Photo: G

Ll/CNSS

Photo: G

Ll/CNSS

28

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

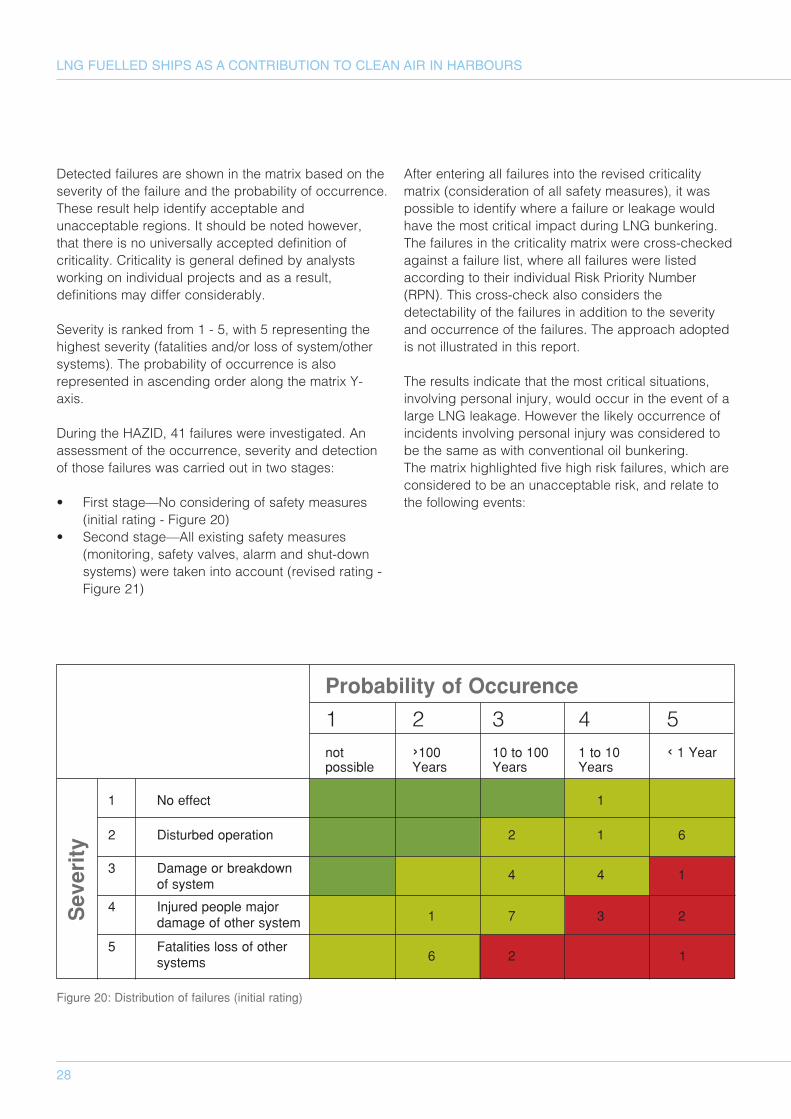

Detected failures are shown in the matrix based on theseverity of the failure and the probability of occurrence.These result help identify acceptable andunacceptable regions. It should be noted however,that there is no universally accepted definition ofcriticality. Criticality is general defined by analystsworking on individual projects and as a result,definitions may differ considerably.

Severity is ranked from 1 - 5, with 5 representing thehighest severity (fatalities and/or loss of system/othersystems). The probability of occurrence is alsorepresented in ascending order along the matrix Y-axis.

During the HAZID, 41 failures were investigated. Anassessment of the occurrence, severity and detectionof those failures was carried out in two stages:

• First stage—No considering of safety measures(initial rating - Figure 20)

• Second stage—All existing safety measures(monitoring, safety valves, alarm and shut-downsystems) were taken into account (revised rating -Figure 21)

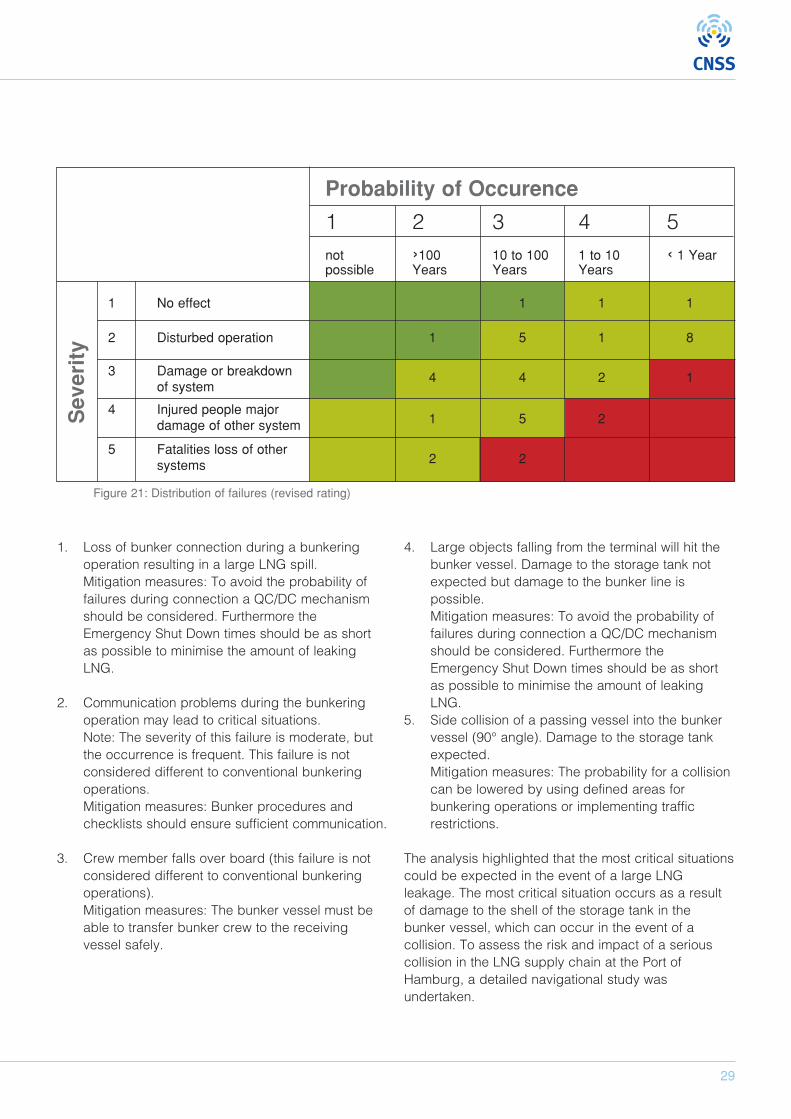

After entering all failures into the revised criticalitymatrix (consideration of all safety measures), it waspossible to identify where a failure or leakage wouldhave the most critical impact during LNG bunkering.The failures in the criticality matrix were cross-checkedagainst a failure list, where all failures were listedaccording to their individual Risk Priority Number(RPN). This cross-check also considers thedetectability of the failures in addition to the severityand occurrence of the failures. The approach adoptedis not illustrated in this report.

The results indicate that the most critical situations,involving personal injury, would occur in the event of alarge LNG leakage. However the likely occurrence ofincidents involving personal injury was considered tobe the same as with conventional oil bunkering.The matrix highlighted five high risk failures, which areconsidered to be an unacceptable risk, and relate tothe following events:

Figure 20: Distribution of failures (initial rating)

Probability of Occurence

1 2 3 4 5not ›100 10 to 100 1 to 10 ‹ 1 Yearpossible Years Years Years

1 No effect 1

2 Disturbed operation 2 1 6

3 Damage or breakdown 4 4 1of system

4 Injured people majordamage of other system 1 7 3 2

5 Fatalities loss of other systems 6 2 1

Severity

29

1. Loss of bunker connection during a bunkeringoperation resulting in a large LNG spill.Mitigation measures: To avoid the probability offailures during connection a QC/DC mechanismshould be considered. Furthermore theEmergency Shut Down times should be as shortas possible to minimise the amount of leakingLNG.

2. Communication problems during the bunkeringoperation may lead to critical situations. Note: The severity of this failure is moderate, butthe occurrence is frequent. This failure is notconsidered different to conventional bunkeringoperations.Mitigation measures: Bunker procedures andchecklists should ensure sufficient communication.

3. Crew member falls over board (this failure is notconsidered different to conventional bunkeringoperations).Mitigation measures: The bunker vessel must beable to transfer bunker crew to the receivingvessel safely.

4. Large objects falling from the terminal will hit thebunker vessel. Damage to the storage tank notexpected but damage to the bunker line ispossible.Mitigation measures: To avoid the probability offailures during connection a QC/DC mechanismshould be considered. Furthermore theEmergency Shut Down times should be as shortas possible to minimise the amount of leakingLNG.

5. Side collision of a passing vessel into the bunkervessel (90° angle). Damage to the storage tankexpected. Mitigation measures: The probability for a collisioncan be lowered by using defined areas forbunkering operations or implementing trafficrestrictions.

The analysis highlighted that the most critical situationscould be expected in the event of a large LNGleakage. The most critical situation occurs as a resultof damage to the shell of the storage tank in thebunker vessel, which can occur in the event of acollision. To assess the risk and impact of a seriouscollision in the LNG supply chain at the Port ofHamburg, a detailed navigational study wasundertaken.

Figure 21: Distribution of failures (revised rating)

Probability of Occurence

1 2 3 4 5not ›100 10 to 100 1 to 10 ‹ 1 Yearpossible Years Years Years

1 No effect 1 1 1

2 Disturbed operation 1 5 1 8

3 Damage or breakdown 4 4 2 1of system

4 Injured people majordamage of other system 1 5 2

5 Fatalities loss of other systems 2 2

Severity

30

LNG FUELLED SHIPS AS A CONTRIBUTION TO CLEAN AIR IN HARBOURS

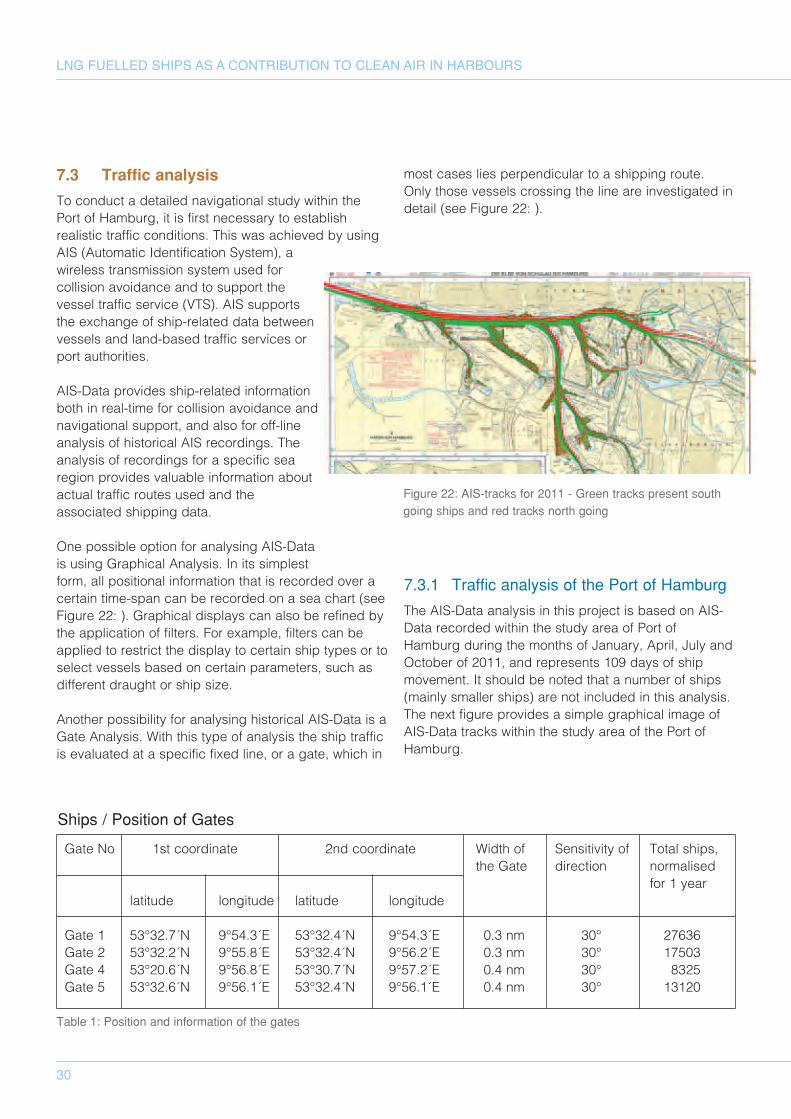

7.3 Traffic analysis

To conduct a detailed navigational study within thePort of Hamburg, it is first necessary to establishrealistic traffic conditions. This was achieved by usingAIS (Automatic Identification System), awireless transmission system used forcollision avoidance and to support thevessel traffic service (VTS). AIS supportsthe exchange of ship-related data betweenvessels and land-based traffic services orport authorities.

AIS-Data provides ship-related informationboth in real-time for collision avoidance andnavigational support, and also for off-lineanalysis of historical AIS recordings. Theanalysis of recordings for a specific searegion provides valuable information aboutactual traffic routes used and theassociated shipping data.

One possible option for analysing AIS-Datais using Graphical Analysis. In its simplestform, all positional information that is recorded over acertain time-span can be recorded on a sea chart (seeFigure 22: ). Graphical displays can also be refined bythe application of filters. For example, filters can beapplied to restrict the display to certain ship types or toselect vessels based on certain parameters, such asdifferent draught or ship size.

Another possibility for analysing historical AIS-Data is aGate Analysis. With this type of analysis the ship trafficis evaluated at a specific fixed line, or a gate, which in

most cases lies perpendicular to a shipping route.Only those vessels crossing the line are investigated indetail (see Figure 22: ).

7.3.1 Traffic analysis of the Port of Hamburg

The AIS-Data analysis in this project is based on AIS-Data recorded within the study area of Port ofHamburg during the months of January, April, July andOctober of 2011, and represents 109 days of shipmovement. It should be noted that a number of ships(mainly smaller ships) are not included in this analysis.The next figure provides a simple graphical image ofAIS-Data tracks within the study area of the Port ofHamburg.

Figure 22: AIS-tracks for 2011 - Green tracks present southgoing ships and red tracks north going

Gate No 1st coordinate 2nd coordinate Width of Sensitivity of Total ships,the Gate direction normalised

for 1 yearlatitude longitude latitude longitude

Gate 1 53°32.7´N 9°54.3´E 53°32.4´N 9°54.3´E 0.3 nm 30° 27636Gate 2 53°32.2´N 9°55.8´E 53°32.4´N 9°56.2´E 0.3 nm 30° 17503Gate 4 53°20.6´N 9°56.8´E 53°30.7´N 9°57.2´E 0.4 nm 30° 8325Gate 5 53°32.6´N 9°56.1´E 53°32.4´N 9°56.1´E 0.4 nm 30° 13120

Table 1: Position and information of the gates

Ships / Position of Gates

31

Gate analyses have been performed at five locations inthe Port of Hamburg. Gate 1 is close to the jetty ofAthabaskakai. Gate 2 detects the passing traffic fromand to Köhlbrand. Gate 3 detects the shipping trafficgoing in and out of the Waltershofer Hafen (results atGate 3 have not been considered within this analysis),Gate 4 detects the traffic passing the Rethe from andto the Kattwykhafen, and Gate 5 detects the trafficpassing the Ferry Terminal Altona. These data areused as input parameters for the quantitative riskassessment.

7.4 Quantitative risk assessment

The applied model for calculating the frequency ofcollision accidents in the Port of Hamburg involves theuse of a so-called causation probability that ismultiplied by a theoretically obtained number ofcollision candidates.

The causation factor models the probability that theofficer on the watch has not reacted in time given thathis vessel is on a collision course with another vessel.The numerical value of the causation probability is nota single value but often varies in different geographicallocations.

Due to a causation factor (probability that last-minuterecovery action will be unsuccessful) of 2.7 (Karlssonet al, 1998), a value of 10-5 seems to be adequate andis used for the following calculations of head-oncollisions.

7.4.1 Considered situations for the LNG-Tanker

The following two scenarios have been evaluated foran LNG-Tanker (LNG-T) operating within the Port ofHamburg:

• Collision on transit within the Port of Hamburg:

• For an LNG-Tanker the head-on collision isanalysed for its route within Port of Hamburg.For the analysis the speed of the LNG-Tankeron its transit within Port of Hamburg was setto 8 kn, the average ship speed in this area.

• Overtaking collisions, collisions at junctionsas well as grounding are indirectlyconsidered due to calibration with actualCollision Rates of the Port of Hamburg.

• Collision at berthing position:

• The probability of being involved in a collisionwhile off-loading at Kattwykhafen has alsobeen analysed. The probable berth atKattwykhafen provides some protectionagainst such collisions, and this has beentaken into consideration by reducing thevulnerable length to half the ship length.

7.4.2 Considered situations for the LNG-Bunker Vessel

The following scenarios for an LNG-Bunker Vessel(LNG-BSV) operating within the Port of Hamburg havebeen evaluated:• Collision on transit within the Port of Hamburg.

• For the LNG-Bunker Vessel a head-oncollision along its route within the Port ofHamburg has been analysed. For theanalysis the speed of the LNG-Bunker Vesselon its transit within Port of Hamburg was setto 8 kn, the average ship speed in this area.

• Overtaking collisions, collisions at Junctionsas well as grounding are indirectlyconsidered due to calibration with actualCollision Rates of the Port of Hamburg.