CLERK, BOARD OF SUPERVISORS - ACGOV.org · Clerk, Board of Supervisors ... Collection Advisory Team...

66

Agenda __ January 24, 2017 CLERK, BOARD OF SUPERVISORS Board of Supervisors County of Alameda 1221 Oak Street Oakland CA 94612 Dear Board Members: January 4, 2017 SUBJECT: Claims for Excess Proceeds -2014 Tax Defaulted Property Sales RECOMMENDATIONS: Pursuant to the applicable provisions of the Revenue and Taxation Code, it is recommended that your Board approve the Hearing Officer's decisions regarding the Excess Proceeds Claims from tax defaulted property sales of 2014, included in Attachment A and authorize the Auditor- Controller to distribute the excess proceeds to the affected claimants pursuant to the Hearing Officer's decision detailed in Attachment B: Claimants A. Global Discoveries, Ltd B. Global Discoveries, Ltd C. Global Discoveries, Ltd D. Global Discoveries, Ltd E. Global Discoveries, Ltd F. Harry Bernstein DISCUSSION/SUMMARY Parcel No.(s) 99A-2310-4-7 48H-7704-120 48H-7704-121 48H-7704-122 48G-7449-34 48G-7449-27 The Tax Collector conducted sales of tax defaulted properties in 2014. Any excess in the proceeds of these sales, over and above the amounts collected to satisfy the tax delinquencies, were deposited by the Tax Collector in a delinquent tax sale trust fund. The excess proceeds were subject to claims made by parties of interest in accordance with applicable provisions of the California Revenue and Taxation Code. All claimants were given the opportunity for a hearing before the Assessment Hearing Officer to establish the priority and extent of their claims. SUSAN S. MURANISHI, County Administrator ANIKA CAMPBELL-BELTON, Clerk of the Board 1221 Oak Street, Room 536, Oakland, California 94612, (510) 272-3854, Fax: (510) 208-9660

Transcript of CLERK, BOARD OF SUPERVISORS - ACGOV.org · Clerk, Board of Supervisors ... Collection Advisory Team...

Agenda __ January 24, 2017

CLERK, BOARD OF SUPERVISORS

Board of Supervisors County of Alameda 1221 Oak Street Oakland CA 94612

Dear Board Members:

January 4, 2017

SUBJECT: Claims for Excess Proceeds -2014 Tax Defaulted Property Sales

RECOMMENDATIONS:

Pursuant to the applicable provisions of the Revenue and Taxation Code, it is recommended that your Board approve the Hearing Officer's decisions regarding the Excess Proceeds Claims from tax defaulted property sales of 2014, included in Attachment A and authorize the AuditorController to distribute the excess proceeds to the affected claimants pursuant to the Hearing Officer's decision detailed in Attachment B:

Claimants

A. Global Discoveries, Ltd B. Global Discoveries, Ltd C. Global Discoveries, Ltd D. Global Discoveries, Ltd E. Global Discoveries, Ltd F. Harry Bernstein

DISCUSSION/SUMMARY

Parcel No.(s)

99A-2310-4-7 48H-7704-120 48H-7704-121 48H-7704-122 48G-7449-34 48G-7449-27

The Tax Collector conducted sales of tax defaulted properties in 2014. Any excess in the proceeds of these sales, over and above the amounts collected to satisfy the tax delinquencies, were deposited by the Tax Collector in a delinquent tax sale trust fund.

The excess proceeds were subject to claims made by parties of interest in accordance with applicable provisions of the California Revenue and Taxation Code. All claimants were given the opportunity for a hearing before the Assessment Hearing Officer to establish the priority and extent of their claims.

SUSAN S. MURANISHI, County Administrator ANIKA CAMPBELL-BELTON, Clerk of the Board 1221 Oak Street, Room 536, Oakland, California 94612, (510) 272-3854, Fax: (510) 208-9660

Honorable Board of Supervisors January 4, 2017

The Hearing Officer has rendered his written decisions on these claims, which is now being submitted to your Board for approval. Approval of the decisions listed in Attachment B will result in the Auditor-Controller distributing the excess proceeds.

FINANCING:

There is no impact on the General Fund. Excess proceed claims are paid from funds held in trust.

ACB:db P:\LegalHO\bdltr_01_24_17

Attachments

cc: Auditor-Controller File

Sincerely,

/ / . ?/; /!"---- I/_ ./r: ·- £ {1:_

Anika Campbell-Belton Clerk, Board of Supervisors

SUSAN S. MURANISHI, County Administrator ANIKA CAMPBELL-BELTON, Clerk of the Board 1221 Oak Street, Room 536, Oakland, California 94612, (510) 272-3854, Fax: (510) 208-9660

Honorable Board of Supervisors January 4, 2017

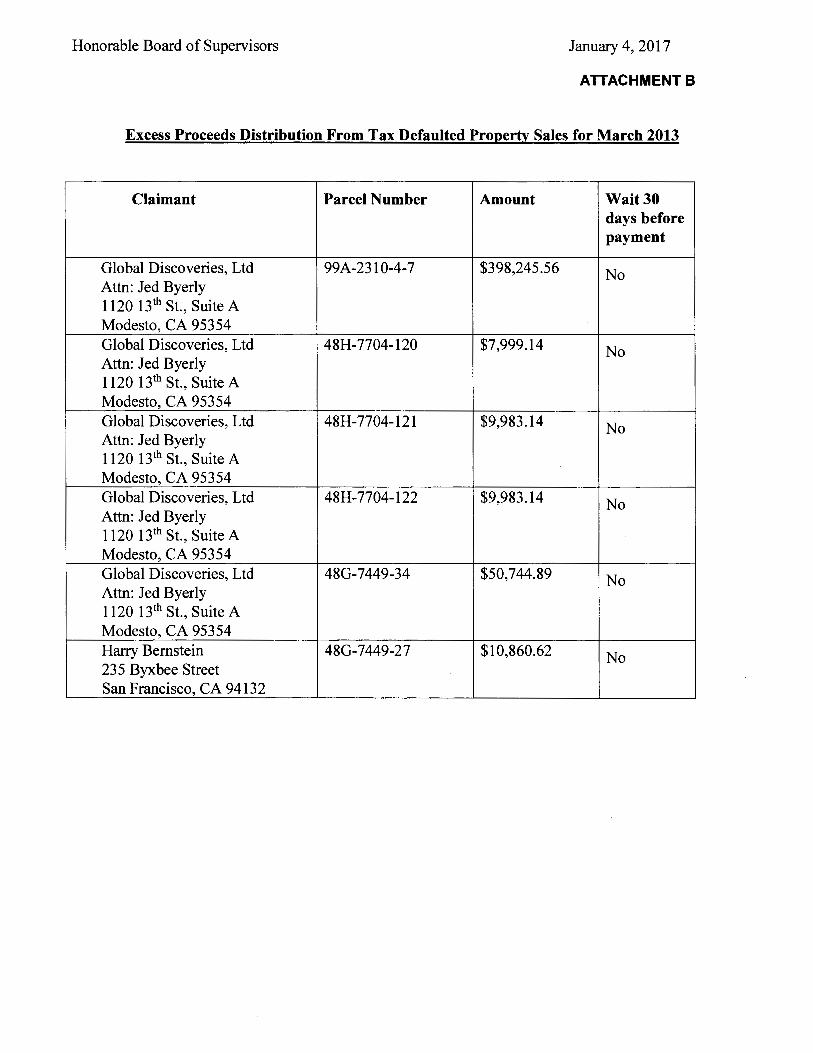

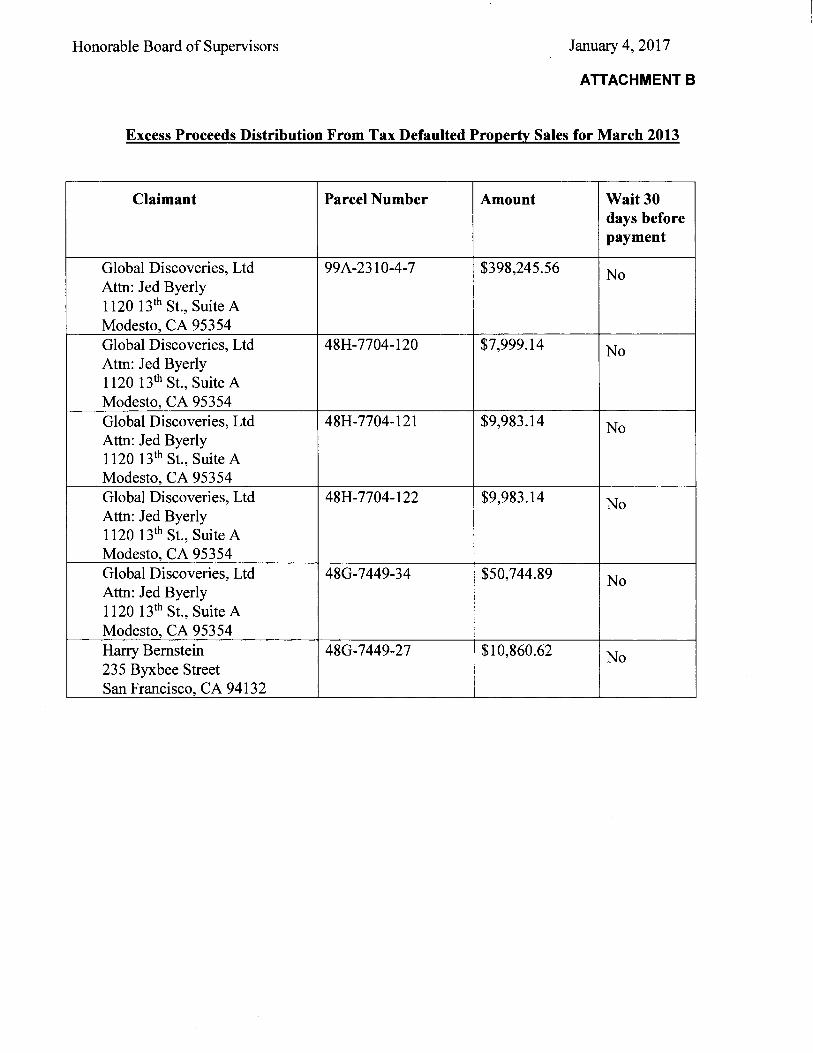

ATTACHMENT B

Excess Proceeds Distribution From Tax Defaulted Property Sales for March 2013

Claimant Parcel Number Amount Wait 30 days before payment

Global Discoveries, Ltd 99A-2310-4-7 $398,245.56 No Attn: Jed Byerly 1120 13th St., Suite A Modesto, CA 95354 Global Discoveries, Ltd 48H-7704-120 $7,999.14 No Attn: Jed Byerly 1120 13th St., Suite A Modesto, CA 95354 Global Discoveries, Ltd 48H-7704-121 $9,983.14 No Attn: Jed Byerly 1120 13th St., Suite A Modesto, CA 95354 Global Discoveries, Ltd 48H-7704-122 $9,983.14 No Attn: Jed Byerly 1120 13th St., Suite A Modesto, CA 95354 Global Discoveries, Ltd 48G-7449-34 $50,744.89 No Attn: Jed Byerly 1120 13th St., Suite A Modesto, CA 95354 Harry Bernstein 48G-7449-27 $10,860.62 No 235 Byxbee Street San Francisco, CA 94132

Attachment A

DECISION OF LEGAL HEARING OFFICER COUNTY OF ALAMEDA

CLAIMANTS:

PARCEL: FILE NOS:

HEARING DATE: AGENDA NUMBERS:

HEARING OFFICER:

FACTS

WELLS FARGO EQUIPMENT FINANCE, INC., FRANCHISE TAX BOARD, ALAMEDA COUNTY TAX COLLECTOR, AAA WONG FAMILY LIMITED PARTNERSHIP, GLOBAL DISCOVERIES on assignment from TIMOTHY SHAON, US FOOD SERVICE 99A-2610-4-7 2014-94002, 2014-94007, 2014-94030, 2014-94031, 2014-94052 NOVEMBER 3, 2016 FORTY-NINE, FIFTY, FIFTY-ONE, FIFTY-TWO, FIFTY-THREE, FIFTY-FOUR JED SOMIT, Esq.

Six Claims for Excess Proceeds were filed hoping to obtain all or part of

the almost $400,000 in excess proceeds remaining after the March, 2014,

online auction sale of the tax defaulted parcel.

Claims

A. Wells Fargo Equipment Finance, Inc. 2014-94002. Rachel Owens,

Loan Adjuster for Wells Fargo Equipment Finance, Inc., filed a Claim for

Excess Proceeds on May 2, 2014, seeking $27,282.48 for Wells Fargo

Equipment Finance, Inc., including interest through April 28, 2014 (about 6

weeks after the sale).

The Claim is supported by a Judgment entered May 13, 2010, in Wells

Fargo Equipment Finance, Inc. vs. Marino Sandoval, et al, Superior Court of

HEARING OFFICER DECISION Page 1

California for Contra Costa County No. C09-01111.

No recorded Abstract of Judgment, nor any deed showing the

defendant had an interest in the parcel, was provided with the Claim.

B. California Franchise Tax Board. 2014-94007. Deborah Barret,

Supervisor, Collection Advisory Team for the Franchise Tax Board filed a

Claim for Excess Proceeds in the amount of $40,985.20 as of March 14,

2014, based upon Certificates of Tax Due and Delinquency against Nicole S.

Sandoval, recorded November 30, 2011 ($5,490.13) and July 18, 2013

($35,595.07). These Certificates create a lien on all property of the

taxpayer, under Revenue & Taxation Code section 19221.

Additionally, an Order to Withhold Personal Income Tax was served

upon the County of Alameda, demanding that from any share allocated to

Nicole S. Sandoval, the amount of $72,441.39 be withheld and paid to the

Franchise Tax Board, with specific remitting instructions.

C. Alameda County Tax Collector. 2014-94030. Donald R. White,

Alameda County Tax Collector, attn: Theody Virrey, seeks a total of

$9,504.83 in unsecured property taxes. This Claim is supported by a

number of Unsecured Property Tax Statements on two locations in Alameda

County for various tax years.

No showing that the obligations were recorded, or became liens in the

absence of recordation, was provided with the Claim.

D. AAA Wong Family Limited Partnership. 2014-94031. AAA Wong

HEARING OFFICER DECISION Page2

Family Limited Partnership, through General Wong, LLC, its General Partner,

by Alexanda Hoi To Wong, claims an amount, not stated, by virtue of a Deed

of Trust recorded September 17, 2010, which names as a beneficiary the

AAA Wong Family Ltd. Partnership as to a 35°/o interest as tenant in common

on the Deed of Trust, which identifies a parcel with the same APN as the tax

defaulted parcel. The recited principal sum is $260,000. The underlying

Installment Note also has Claimant as the Holder of a 35°/o ownership

interest; the Note is non-interest bearing, calling for payments starting

September 2010, with a full maturity on September 1, 2019.

The Preliminary Report for title insurance for this loan and Deed of

Trust notes that as of July 23, 2010, title was vested in "Marino Sandoval

and Nicole Sandoval, husband and wife, as joint tenants". It notes unpaid

real property taxes for fiscal year 2009-10, a lien under a Deed of Trust

recorded January 11, 2001 in the principal amount of $343,000, two liens for

unsecured property taxes, and two abstracts of judgment (neither of which

is the Judgment underlying Claim A).

Both General Wong LLC and the AAA Wong Family Limited Partnership

were listed as active in an online search on the California Secretary of State

website on October 13, 2016.

Aside from the mention in the title reports, no showing of the

Sandovals' title of record of the parcel was submitted with the Claim.

E. Global Discoveries-Shaon. 2014-94037. Global Discoveries, Ltd.,

HEARING OFFICER DECISION Page3

seeks 100°/o of the excess proceeds based upon an assignment from Timothy

Shaon, in ·a Claim filed March 9, 2015. This Claim arises from the $343,000

Deed of Trust noted in the discussion of Claim D.

The Claim is supported on the merits by the recorded Deed of Trust,

naming beneficiaries Timothy and Jennifer Shaon, covering the subject and

other parcels, and by a Promissory Note in the principal amount of

$343,000, providing for monthly payments commencing February 1, 2001, a

maturity date of February 1, 2010, and a 6°/o late charge.

Also submitted is a Judgment of Dissolution of the Jennifer Shaon and

Timothy Shaon marriage from a Contra Costa County proceeding, which

Judgment awards to Timothy the "Promissory Note to Marino Sandoval".

A Statement of Amount Due and Owing asserts that no payments were

made, and that the amount due, through the date of sale, is $826,459.14,

which includes $42,575.51 late fees.

F. US Food Service. 2014-94052. David J. Cook, Esq., of Cook

Collection Attorneys, PLC, filed a Claim for Excess Proceeds on April 17,

2015, in his own name, but stating "attorney for US Foodservice, Inc." That

corporation is listed as "active" and as a dba in California for US Foods, Inc.,

as of October 13, 2016, in the California Secretary of State's online service.

This Claim is supported by an Abstract of Judgment in US Foodservice, Inc.,

v. Marino Sandoval, Superior Court of the State of California for Alameda

County, recorded May 12, 2009, in the amount of $75,421.96.

HEARING OFFICER DECISION Page4

A Cash Flow Data sheet lists several payments on the Judgment, and

adds interest, to arrive at an amount due on March 14, 2015, of

$115,509.40.

Hearing on November 3, 2016

Appearing at the hearing on November 3, 2016, were: Jed Byerly for

Global Discoveries, Ltd.; Ryan Dobb for US Food Service; Alex Wong for

AAA Wong Family Ltd Partnership; Matthew Androtti for the Franchise Tax

Board; Deo Devarie for the Alameda County Tax Collector; and, Rachelle

Owens (by telephone), an employee of Wells Fargo Bank.

Mr. Kan noted his Office represents the County Tax Collector, creating

a potential conflict, but the Tax Collector's representative decided to proceed

without separate representation.

Alex Wong noted that the Claim for Excess Proceeds filed for the AAA

Wong Family Limited Partnership had intended to be for the entire interest

under the Deed of Trust for both of the beneficiaries, not just the AAA Wong

Family Limited Partnership's interest.

Ryan Dobb agreed that the date of sale could be used as the latest

date for accrual of interest on the US Food Service Claim.

Matthew Androtti noted that the Franchise Tax Board submission at the

hearing was a reduction in the amount of the lien and an increase in the

amount to withhold, if money is granted to Nicole Sandoval.

Each party stated it had no objection to the Claim of the other parties.

HEARING OFFICER DECISION Page5

All parties agreed that priorities for the first priority Claims are

determined by the date of recording of the lien instruments.

Several additional documents were received at the hearing {some

duplicating prior filings):

For AAA Wong Family Limited Partnership

• Exhibit 1. Deed of Trust dated August 19, 2010, with Trustor Marino

Sandoval and Nicole Sandoval, and beneficiary "AAA Wong Family Ltd.

Partnership as to an undivided 35°/o interest. AWK Family Ltd.

Partnership, as to an undivided 65°/o interest", securing an obligation

of $260,000. The Deed of Trust does not show recording data. Also

included in this Exhibit was a Request for Notice dated September 14,

2010, referring to a Deed of Trust recorded January 11, 2011

{2001012039).

• Exhibit 2. Installment Note, dated August 19, 2010, in the principal

amount of $260,000, with no interest "until the principal sum is paid in

full", with monthly payments and a final maturity date of September 1,

2019.

• Exhibit 3. Letter of October 27, 2016, from Alexanda Hoi To Wong,

Authorized Signatory for AAA Wong Family Limited Partnership, LP, by

General Wong, LLC, its General Partner. This letter explains that the

$260,000 debt was a consolidation of past-due rent for two locations,

one owned by AAA Wong Family Limited Partnership and the other by

HEARING OFFICER DECISION Page6

AWK Family Limited Partnership. The letter states that no payments

on the Installment Note were made, and the amount due remains

$260,000. Various other papers are included in this packet, including

the first pages of the Agreement of Limited Partnership for AWK Family

Limited Partnership and AAA Wong Family Limited Partnership; the first

pages indicate that the General Partner and the Limited Partners of

each entity are identical.

For Wells Fargo Equipment Finance

• Exhibit 1. Accounting on Judgment entered May 13, 2010, showing a

balance due (with interest) on April 28, 2014, and October 25, 2016.

• Exhibit 2. Corporate Summary Report

• Exhibit 3. Recorded (6/4/2010) Abstract of Judgment cover sheet.

• Exhibit 4. Abstract of Judgment in favor of Wells Fargo Equipment

Finance, Inc., and debtor Marino Sandoval, in the original amount of

$19,502.10, entered May 13, 2010.

• Exhibit 5. Minnesota Secretary of State Certificate of Good Standing

for Weis Fargo Equipment Finance, Inc.

• Exhibit 6. Certificate of Authority for Rachel Owens.

For Alameda Tax Collector

• Six Unsecured Property Tax Statements for various fiscal years on two

accounts with taxpayers Marino & Nicole Sandoval.

• Four Certificates of Lien for Unsecured Property Taxes, with recording

HEARING OFFICER DECISION Page?

data.

• Grant Deed recorded in 1998 of the parcel to "Marino Sandoval and

Nicole Sandoval, husband and wife, as joint tenants".

• Tape showing total amount due as $8,399.81, plus $92.00.

For Franchise Tax Board

• Two recorded Notices of State Tax Lien against Nicole S Sandoval.

• Certificate of Tax Due and Delinquency against Nicole S Sandoval,

stating total liened amount of $39,985.20 through the date of the tax

default sale, and total un-liened additional amount of $93,941.34 as of

November 2, 2016, with daily interest thereafter of $7.67.

• Order to Alameda Office of the Treasurer to Withhold Personal Income

Tax from any "value ... belonging to Nicole S. Sandoval."

• Claim for Excess Proceeds claiming $40,985.20 as of March 14, 2014

(later Certificate of Tax Due, Etc., has the amount reduced by an

additional $1,000 in payments).

The matter was submitted.

DECISION

The Claim for Excess Proceeds of Global Discoveries, Ltd., as assignee

of Timothy Shaon, is granted. All of the excess proceeds of $398,245.56

shall be paid to "Global Discoveries, Ltd.".

The Claim for Excess Proceeds of Wells Fargo Equipment Finance, Inc.,

HEARING OFFICER DECISION Page8

is denied, as there are no remaining excess proceeds after the award to

Global Discoveries, Ltd.

The Claim for Excess Proceeds of the State of California Franchise Tax

Board is denied, as there are no remaining excess proceeds after the award

to Global Discoveries, Ltd.

The Claim for Excess Proceeds of Donald White, Alameda County Tax

Collector, is denied, as there are no remaining excess proceeds after the

award to Global Discoveries, Ltd.

The Claim for Excess Proceeds of AAA Wong Family Limited Partnership

is denied, as there are no remaining excess proceeds after the award to

Global Discoveries, Ltd.

The Claim for Excess Proceeds of US Food Service, through Donald

Cook, Esq., is denied, as there are no remaining excess proceeds after the

award to Global Discoveries, Ltd.

RATIONALE

Revenue & Taxation Code §4674 directs that excess proceeds may be

claimed by parties of interest in the property as provided in Section 4675.

Unclaimed excess proceeds may be transferred to the county general fund.

Revenue & Taxation Code §4675(a) provides that any party of interest

in the property may file with the county a claim for the excess proceeds, in

proportion to his or her interest held with others of equal priority in the

HEARING OFFICER DECISION Page9

property at the time of sale, at any time prior to the expiration of one year

following the recordation of the tax collector's deed to the purchaser. Each

of the six Claims here was filed timely.

Section 4675(b) continues: "After the property has been sold, a party

of interest in the property at the time of the sale may assign his or her right

to claim the excess proceeds only by a dated, written instrument that

explicitly states that the right to claim the excess proceeds is being assigned,

and only after each party to the proposed assignment has disclosed to each

other party to the proposed assignment all facts of which he or she is aware

relating to the value of the right that is being assigned. Any attempted

assignment that does not comply with these requirements shall have no

effect .... " The assignment papers for Timothy Shaon to Global Discoveries,

Ltd., satisfy the statutory requirements.

Section 4675( c) adds further requirements for assignment: "Any

person or entity who in any way acts on behalf of, or in place of, any party of

interest with respect to filing a claim for any excess proceeds shall submit

proof with the claim that the amount of excess proceeds has been disclosed

to the party of interest and that the party of interest has been advised of his

or her right to file a claim for the excess proceeds on his or her own behalf

directly with the county at no cost." The assignment papers for Timothy

Shaon to Global Discoveries, ltd., satisfy the statutory requirements.

Section 4675(e)(l) defines the parties of interest who may make a

HEARING OFFICER DECISION Page 10

claim:

[T]he excess proceeds shall be distributed on order of the board of supervisors to the parties of interest who have claimed the excess proceeds in the order of priority set forth in subdivisions (a) and (b). For the purposes of this article, parties of interest and their order of priority are:

{A) First, lienholders of record prior to the recordation of the tax deed to the purchaser in the order of their priority.

(B) Second, any person with title of record to all or any portion of the property prior to the recordation of the tax deed to the purchaser.

There were no claims filed based on the second priority of ownership.

All Claims were by lienholders of record.

Each of the Claimants adequately established status a lienholder of

record prior to the recordation of the tax deed to the purchaser. The next

step is to determine the order of priority. All of the Claimants agreed that

the proper order of priority among them is determined by the date that their

lien instrument was recorded.

The Claim with the earliest recorded lien is that of Global Discoveries,

based upon the assignment from Timothy Shaon; the relevant Deed of Trust

was recorded January 11, 2001 (this is the Deed of Trust for which the AAA

Wong Family Limited Partnership recorded a Request for Notice of Default).

The other claimants have nine liens recorded after that date.

Further examination of the Global Discoveries Claims uncovers no

problems. The Promissory Note was awarded to Global's assignor in the

dissolution of marriage proceeding of the original lenders/beneficiaries; that

HEARING OFFICER DECISION Page 11

award also transfers the Deed of Trust. Civil Code section 2936. That award

was confirmed by Jennifer Shaon. No maturity date appears on the face of

the recorded Deed of Trust, so there is no problem with an "ancient

mortgage" (even if the 2010 maturity date were on the Deed of Trust, the

Deed of Trust would still have been valid in 2014).

There is a sworn statement that no payments were made on the

Promissory Note underlying the Deed of Trust. Simple interest at the 9. 75°/o

per annum rate stated in the Note on the principal balance of $343,000 is

$33,442.50/year; the total amount due, without considering late charges,

exceeds the amount of excess proceeds available in less than two years.

The excess proceeds statute requires payment in order of priority,

rather than in any pro rata manner. The Global Discoveries Claim of highest

priority exhausts the excess proceeds. There is no need to consider the

other Claims further, notwithstanding the several interesting issues which

might arise.

Dated: December 13, 2016

HEARING OFFICER DECISION

= Jed Somit, Attorney at Law Legal Hearing Officer

Page 12

CLAIMANTS:

PARCEL:

DECISION OF LEGAL HEARING OFFICER COUNTY OF ALAMEDA

0(1..)C\.l .... s HOLSCLAW, JR., GLOBAL DISCOVERIES, LTD by assignment from MARTHA HUTSON SAXTON 48H-7704-120

FILE NOS: HEARING DATE:

EXCESS PROCEEDS 2014-94032, 2014-94056 NOVEMBER 3, 2016

AGENDA NUMBERS: TWENTY-EIGHT, TWENTY-NINE HEARING OFFICER: JED SOMIT, Esq.

FACTS

Almost $16,000 is at issue for the two claimants for the excess

proceeds generated by the March, 2014, tax default auction sale of this

parcel.

Claims

A. Da-"'t,l..,...f.Holsclaw, Jr. 2014-94056. Mr. Holsclaw filed a Claim for

Excess Proceeds on April 22, 2015, Mr. Holsclaw claims all of the proceeds as

an owner. No grant documents supported the Claim, although he is listed

as one of the last assessees prior to the tax default sale. (Documents

submitted on behalf of the other Claim will be considered for this Claimant,

however.)

B. Global Discoveries, Ltd. 2014-940532. In a Claim for Excess

Proceeds filed March 10, 2015, Global Discoveries claims $8,455.50

(apparently an estimate of 50°/o of the excess proceeds). Apart from the

assignment papers, which will be reviewed later, the Claim is substantively

HEARING OFFICER DECISION Page 1

supported by:

• Grant Deed recorded in 1966 of certain property, without an APN, with

grantees Douglas Holsclaw, Jr., and Martha Holsclaw, his wife, as joint

tenants.

• Interlocutory Judgment of Dissolution of Marriage in In re Marriage of

Holsclaw, Alameda County Superior Court, recorded in 1974, which

confirms ownership of this property as 50°/o in each former spouse.

• Final Judgment of Dissolution of Marriage recorded in 1974,

incorporating the Interlocutory Judgment, also awarding 50°/o of

several lots to Martha Holsclaw.

County Counsel Memorandum

Farand C. Kan, Deputy County Counsel, and Paige N. Pembrook,

Graduate Law Clerk, provided a Memorandum for the Office of the County

Counsel dated September 22, 2016, reviewing the Claims for Excess

Proceeds and supporting documentation.

The Memorandum concludes the Holsclaw Claim was not filed timely,

as the tax deed to the purchaser was recorded on April 21, 2014; the

Memorandum therefore recommends denial of this Claim. Other,

substantive, problems with the Claim are discussed.

The Memorandum concludes that the Global Discoveries Claim is

adequately supported, and was filed timely. It finds the assignment to

Global Discoveries met the statutory requirements. The underling deed, it

HEARING OFFICER DECISION Page2

states, must be established to be for the same parcel.

Hearing November 3, 2016

At the hearing on November 3, 2016, Jed Byerly appeared for Claimant

Global Discoveries, Ltd. Douglas Holsclaw appeared by telephone (he lives

in Pennsylvania). He stated he was 82 years old. He testified that he was

contacted by many people seeking to assist with his claim, and (mis-)

informed by them that he could not file a Claim for Excess Proceeds prior to

a year from the recordation of the tax deed. He did not suggest that any

employee of the County told him that. He testified that with that

understanding, he tried to make sure his Claim was the first received and

tried to file early on the day following one year. He mailed his Claim for this

parcel and three others together, though the US Postal Service. He started

to read from his receipt. He was given permission to file a copy of his

mailing receipt and any other papers concerning his mailing of the Claim.

Mr. Holsclaw stated he had no objections to wife's Claim.

The matter was submitted, except for the leave given Claimant

Holsclaw to provide copies of his mailing receipt, etc.

His mailing receipt was received. It shows a mailing in Pennsylvania

on April 22, 2015, at 11:58 a.m. It evidences delivery to the Clerk of the

Board in Oakland on April 23, 2015.

DECISION

HEARING OFFICER DECISION Page3

Douglas Holsclaw's Claim for Excess Proceeds was not filed timely, and

is denied.

The Claim for Excess Proceeds of Global Discoveries, Ltd., on

assignment from Martha Hutson Saxton, is granted as to 50°/o of the excess

proceeds, or $7,999.14. The check should be made payable to "Global

Discoveries, Ltd."

RATIONALE

Douglas Holsclaw Claim

Revenue & Taxation Code §4675(a) provides that any party of interest

in the property may file with the county a claim for the excess proceeds, in

proportion to his or her interest held with others of equal priority in the

property at the time of sale, "at any time prior to the expiration of one year

following the recordation of the tax collector's deed to the purchaser."

This is exactly our problem. The recordation of the tax deed resulting

from the tax default auction sale occurred on April 21, 2014. The Claim for

Excess Proceeds was received on April 23, 2015, although stamped "April

22, 2015", possibly because it was received prior to the start of business on

April 23rd.

In normal parlance, "prior to the expiration of one year" would mean

the Claim had to be filed before April 21, 2015. However, most California

government agencies follow the time computation approach stated in Civil

Code section 10:

HEARING OFFICER DECISION Page4

The time in which any act provided by law is to be done is computed by excluding the first day and including the last, unless the last day is a holiday, and then it is also excluded.

Applying this makes the "one year" end on April 21, 2015, unless extended.

April 21, 2015 was a weekday (Tuesday), and, although there were several

holidays, including Easter, in April, 2015, April 21st was not a holiday.

Therefore, April 21st was the last day on which a Claim for Excess Proceeds

for this parcel could be filed timely. Here, the Claim was received either on

April 22nd or April 23rd.

However, the date of receipt by the County is not always the date of

filing. Revenue & Taxation Code section 166 provides:

(a) Whenever a taxpayer is required to file any statement, affidavit, application, or any other paper or document with a taxing agency by a specified time on a specified date, such filing shall be deemed to be within the specified period if it is sent by United States mail, properly addressed with postage prepaid, and bears a post office cancellation mark of the specified date, or earlier within the specified period, stamped on the envelope, or on itself, or if proof satisfactory to the agency establishes that the mailing occurred on the specified date, or earlier within the specified period. (b) The provisions of this section shall supersede any contrary special provision of this division unless such special provision specifically provides that this section shall not be applicable. ( c) The provisions of this section are applicable to any filing required to be made by ordinance, rule, or regulation of a taxing agency. (d) Any statement or affidavit made by a taxpayer asserting such a timely filing must be made within one year of the deadline applicable to the original filing; provided, however, that this subsection shall not apply to any statement or affidavit asserting the timely filing of a property statement or to any statement made by the taxpayer in connection with an escape assessment imposed pursuant to Section 531. (e) It is the intent of the Legislature that this section be liberally

HEARING OFFICER DECISION Pages

construed in favor of the taxpayer and be applicable to all filings relating to property taxation which are required to be made by a taxpayer by a specified time on a specified date.

Unfortunately, the mailing receipt does not save Claimant, even under

a liberal construction. It shows a mailing on April 22nd, at 11:58 a.m. Even

taking into account the different time zones, it is clear the mailing occurred

on April 22nd, whether the date is determined in Oakland or in Pennsylvania.

The Hearing Officer cannot conclude, simply to validate this Claim, that the

mailing receipt incorrectly stated a date a day later than the actual mailing

and delivery in Oakland; there is insufficient evidence on which to assume

two separate mistakes were made.

The next issue is whether the Hearing Officer can overlook one day of

lateness, given Claimant's misinformation about when to file. No source for

such discretion can be found. The statute is unambiguous concerning the

filing period, and suggests that unclaimed excess proceeds could be

immediately distributed to the public entities on expiration of the one year.

No general discretion to relieve taxpayers from error is given.

In fact, case law holds that Revenue & Taxation Code time filing

requirements are given preclusive effect, even when a taxpayer loses an

otherwise viable claim as a result. Sea World, Inc. v. County of San Diego

(1994) 27 Cal.App.4th 1390.

For these reasons, without reaching the merits of the Claim, Douglas

Holsclaw's Claim must be denied.

HEARING OFFICER DECISION Page6

Global Discoveries-Martha Hutson Saxton Claim

This Claim was timely filed.

Section 4675(b) continues: "After the property has been sold, a party

of interest in the property at the time of the sale may assign his or her right

to claim the excess proceeds only by a dated, written instrument that

explicitly states that the right to claim the excess proceeds is being assigned,

and only after each party to the proposed assignment has disclosed to each

other party to the proposed assignment all facts of which he or she is aware

relating to the value of the right that is being assigned. Any attempted

assignment that does not comply with these requirements shall have no

effect .... " The Hearing Officer has reviewed Global Discoveries' assignment

papers; they satisfy the statutory requirements. Indicating only 50°/o of the

total excess proceeds are available for this Claim adds some support to the

rote declaration that all facts relating to the value of the Claim were mutually

disclosed.

Section 4675(c) adds further requirements for assignment: "Any

person or entity who in any way acts on behalf of, or in place of, any party of

interest with respect to filing a claim for any excess proceeds shall submit

proof with the claim that the amount of excess proceeds has been disclosed

to the party of interest and that the party of interest has been advised of his

or her right to file a claim for the excess proceeds on his or her own behalf

directly with the county at no cost." The Global Discoveries papers indicate

HEARING OFFICER DECISION Page?

an estimate of the excess proceeds for this Claim and contain the required

advisements.

claim:

Section 4675(e)(l) defines the parties of interest who may make a

[T]he excess proceeds shall be distributed on order of the board of supervisors to the parties of interest who have claimed the excess proceeds in the order of priority set forth in subdivisions (a) and (b). For the purposes of this article, parties of interest and their order of priority are:

(A) First, lienholders of record prior to the recordation of the tax deed to the purchaser in the order of their priority.

(B) Second, any person with title of record to all or any portion of the property prior to the recordation of the tax deed to the purchaser.

The Global Discoveries Claim is of the second priority. There were no

claims of the first priority.

There is adequate evidence to find that Global Discoveries' assignor

was a person with title of record to 50°/o of the fee interest prior to the tax

auction sale. Claimant supplied a recorded Grant Deed by which Martha and

Douglas Holsclaw acquired certain property jointly, as well as the Judgment

of Dissolution of Marriage confirming the assignor's continued ownership of a

50°/o interest in several lots. Claimant showed that "Martha Holsclaw" on the

Grant Deed is the same person as "Martha Saxton", Global's assignor.

The Hearing Officer, using the Assessor's online maps for Map 48H-

7704, ascertained that the legal description on the Grant Deed is consistent

with the APN for this parcel.

HEARING OFFICER DECISION Page8

Claimant established its right to 50°/o of the excess proceeds. Even

though Mr. Holsclaw's Claim is denied, only 50°/o of the excess proceeds can

be awarded to Claimant. A claimant is entitled to only the share of the

excess proceeds corresponding to the claimant's ownership interest

(assuming no claims of a higher priority), even when the other owner fails to

file a claim for the excess proceeds. First Corporation, Inc. v. County of

Santa Clara (1983) 146 CA3d 841.

For these reasons, one-half of the excess proceeds are awarded to

Global Discoveries, Ltd.

Dated: December 13, 2016

HEARING OFFICER DECISION

~~-.-"--Jed Somit, Attorney at Law Legal Hearing Officer

Page 9

CLAIMANTS:

PARCEL:

DECISION OF LEGAL HEARING OFFICER COUNTY OF ALAMEDA

DOUGLAS HOLSCLAW, JR., GLOBAL DISCOVERIES, LTD by assignment from MARTHA HUTSON SAXTON 48H-7704-121

FILE NOS: HEARING DATE:

EXCESS PROCEEDS 2014-94033, 2014-94057 NOVEMBER 3, 2016

AGENDA NUMBERS: THIRTY, THIRTY-ONE HEARING OFFICER: JED SOMIT, Esq.

FACTS

Over $18,500 is at issue for the two claimants for the excess proceeds

generated by the March, 2014, tax default auction sale of this parcel.

Claims

A. Douglas Holsclaw, Jr. 2014-94057. Mr. Holsclaw filed a Claim for

Excess Proceeds on April 22, 2015, Mr. Holsclaw claims all of the proceeds as

an owner. No grant documents supported the Claim, although he is listed as

one of the last assessees prior to the tax default sale. (Documents submitted

on behalf of the other Claim will be considered for this Claimant,

however.)

B. Global Discoveries, Ltd. 2014-94033. By a Claim for Excess

Proceeds filed March 10, 2015, Global Discoveries claims $9,749.50

(apparently an estimate of 50°/o of the excess proceeds). Apart from the

assignment papers, which will be reviewed later, the Claim is substantively

HEARING OFFICER DECISION Page 1

papers, which will be reviewed later, the Claim is substantively supported

by:

• Grant Deed recorded in 1966 of certain property, without an APN, with

grantees Douglas Holsclaw, Jr., and Martha Holsclaw, his wife, as joint

tenants.

• Interlocutory Judgment of Dissolution of Marriage in In re Marriage of

Holsclaw, Alameda County Superior Court, recorded in 1974, which

confirms ownership of this property as 50°/o in each former spouse.

• Final Judgment of Dissolution of Marriage recorded in 1974,

incorporating the Interlocutory Judgment, also awarding 50°/o of

several lots to Martha Holsclaw.

County Counsel Memorandum

Farand C. Kan, Deputy County Counsel, and Paige N. Pembrook,

Graduate Law Clerk, provided a Memorandum for the Office of the County

Counsel dated September 22, 2016, reviewing the Claims for Excess

Proceeds and supporting documentation.

The Memorandum concludes the Holsclaw Claim was not filed timely,

as the tax deed to the purchaser was recorded on April 21, 2014. The

Memorandum therefore recommends denial of the Holsclaw Claim. Other,

substantive, problems with this Claim are also discussed.

The Memorandum concludes that the Global Discoveries Claim is

adequately supported, and was filed timely. It finds the assignment to

HEARING OFFICER DECISION Page2

Global Discoveries met the statutory requirements. The underling deed

must be established to be for the same parcel.

Hearing November 3, 2016

At the hearing on November 3, 2016, Jed Byerly appeared for Claimant

Global Discoveries, Ltd. Douglas Holsclaw appeared by telephone (he lives

in Pennsylvania). He stated he was 82 years old. He testified that he was

contacted by many people seeking to assist with his claim, and (mis-)

informed by them that he could not file a Claim for Excess Proceeds prior to

a year from the recordation of the tax deed. He did not suggest that any

employee of the County told him that. He testified that with that

understanding, he tried to make sure his Claim was the first received and

tried to file early on the day following one year. He mailed his Claim for this

parcel and three others together, though the US Postal Service. He started

to read from his receipt. He was given permission to file a copy of his

mailing receipt and any other papers concerning his mailing of the Claim.

Mr. Holsclaw stated he had no objections to wife's Claim.

The matter was submitted, except for the leave given Claimant

Holsclaw to provide copies of his mailing receipt, etc.

His mailing receipt was received. It shows a mailing in Pennsylvania

on April 22, 2015, at 11:58 a.m. It evidences delivery to the Clerk of the

Board in Oakland on April 23, 2015.

DECISION

HEARING OFFICER DECISION Page3

Douglas Holsclaw's Claim for Excess Proceeds was not filed timely, and

is denied.

The Claim for Excess Proceeds of Global Discoveries, Ltd., on

assignment from Martha Hutson Saxton, is granted as to 50°/o of the excess

proceeds, or $9,983.14. The check should be made payable to "Global

Discoveries, Ltd."

RATIONALE

Douglas Holsclaw Claim

Revenue & Taxation Code §4675(a) provides that any party of interest

in the property may file with the county a claim for the excess proceeds, in

proportion to his or her interest held with others of equal priority in the

property at the time of sale, "at any time prior to the expiration of one year

following the recordation of the tax collector's deed to the purchaser."

This is exactly our problem. The recordation of the tax deed resulting

from the tax default auction sale occurred on April 21, 2014. The Claim for

Excess Proceeds was received on April 23, 2015, although stamped "April

22, 2015", possibly because it was received prior to the start of business on

April 23rd.

In normal parlance, "prior to the expiration of one year" would mean

the Claim had to be filed before April 21, 2015. However, most California

government agencies follow the time computation approach stated in Civil

Code section 10:

HEARING OFFICER DECISION Page4

The time in which any act provided by law is to be done is computed by excluding the first day and including the last, unless the last day is a holiday, and then it is also excluded.

Applying this makes the "one year" end on April 21, 2015, unless extended.

April 21, 2015 was a weekday (Tuesday), and, although there were several

holidays, including Easter, in April, 2015, April 21st was not a holiday.

Therefore, April 21st was the last day on which a Claim for Excess Proceeds

for this parcel could be filed timely. Here, the Claim was received either on

April 22nd or April 23rd.

However, the date of receipt by the County is not always the date of

filing. Revenue & Taxation Code section 166 provides:

(a) Whenever a taxpayer is required to file any statement, affidavit, application, or any other paper or document with a taxing agency by a specified time on a specified date, such filing shall be deemed to be within the specified period if it is sent by United States mail, properly addressed with postage prepaid, and bears a post office cancellation mark of the specified date, or earlier within the specified period, stamped on the envelope, or on itself, or if proof satisfactory to the agency establishes that the mailing occurred on the specified date, or earlier within the specified period. (b) The provisions of this section shall supersede any contrary special provision of this division unless such special provision specifically provides that this section shall not be applicable. ( c) The provisions of this section are applicable to any filing required to be made by ordinance, rule, or regulation of a taxing agency. (d) Any statement or affidavit made by a taxpayer asserting such a timely filing must be made within one year of the deadline applicable to the original filing; provided, however, that this subsection shall not apply to any statement or affidavit asserting the timely filing of a property statement or to any statement made by the taxpayer in connection with an escape assessment imposed pursuant to Section 531. (e) It is the intent of the Legislature that this section be liberally

HEARING OFFICER DECISION Pages

construed in favor of the taxpayer and be applicable to all filings relating to property taxation which are required to be made by a taxpayer by a specified time on a specified date.

Unfortunately, the mailing receipt does not save Claimant, even under

a liberal construction. It shows a mailing on April 22nd, at 11:58 a.m. Even

taking into account the different time zones, it is clear the mailing occurred

on April 22nd, whether the date is determined in Oakland or in Pennsylvania.

The Hearing Officer cannot conclude, simply to validate this Claim, that the

mailing receipt incorrectly stated a date a day later than the actual mailing

and delivery in Oakland; there is insufficient evidence on which to assume

two separate mistakes were made.

The next issue is whether the Hearing Officer can overlook one day of

lateness, given Claimant's misinformation about when to file. No source for

such discretion can be found. The statute is unambiguous concerning the

filing period, and suggests that unclaimed excess proceeds could be

immediately distributed to the public entities on expiration of the one year.

No general discretion to relieve taxpayers from error is given.

In fact, case law holds that Revenue & Taxation Code time filing

requirements are given preclusive effect, even when a taxpayer loses an

otherwise viable claim as a result. Sea World, Inc. v. County of San Diego

(1994) 27 Cal.App.4th 1390.

For these reasons, without reaching the merits of the Claim, Douglas

Holsclaw's Claim must be denied.

HEARING OFFICER DECISION Page6

Global Discoveries-Martha Hutson Saxton Claim

This Claim was timely filed.

Section 4675(b) continues: "After the property has been sold, a party

of interest in the property at the time of the sale may assign his or her right

to claim the excess proceeds only by a dated, written instrument that

explicitly states that the right to claim the excess proceeds is being assigned,

and only after each party to the proposed assignment has disclosed to each

other party to the proposed assignment all facts of which he or she is aware

relating to the value of the right that is being assigned. Any attempted

assignment that does not comply with these requirements shall have no

effect .... " The Hearing Officer has reviewed Global Discoveries' assignment

papers; they satisfy the statutory requirements. Indicating only 50°/o of the

total excess proceeds are available for this Claim adds some support to the

rote declaration that all facts relating to the value of the Claim were mutually

disclosed.

Section 4675(c) adds further requirements for assignment: "Any

person or entity who in any way acts on behalf of, or in place of, any party of

interest with respect to filing a claim for any excess proceeds shall submit

proof with the claim that the amount of excess proceeds has been disclosed

to the party of interest and that the party of interest has been advised of his

or her right to file a claim for the excess proceeds on his or her own behalf

directly with the county at no cost." The Global Discoveries papers indicate

HEARING OFFICER DECISION Page?

an estimate of the excess proceeds for this Claim and contain the required

advisements.

claim:

Section 4675(e)(l) defines the parties of interest who may make a

[T]he excess proceeds shaU be distributed on order of the board of supervisors to the parties of interest who have claimed the excess proceeds in the order of priority set forth in subdivisions (a) and (b). For the purposes of this article, parties of interest and their order of priority are:

(A) First, lienholders of record prior to the recordation of the tax deed to the purchaser in the order of their priority.

(B) Second, any person with title of record to all or any portion of the property prior to the recordation of the tax deed to the purchaser.

The Global Discoveries Claim is of the second priority. There were no

claims of the first priority.

There is adequate evidence to find that Global Discoveries' assignor

was a person with title of record to 50°/o of the fee interest prior to the tax

auction sale. Claimant supplied a recorded Grant Deed by which Martha and

Douglas Holsclaw acquired certain property jointly, as well as the Judgment

of Dissolution of Marriage confirming the assignor's continued ownership of a

50°/o interest in several lots. Claimant showed that "Martha Holsclaw" on the

Grant Deed is the same person as "Martha Saxton", Global's assignor.

The Hearing Officer, using the Assessor's online maps for Map 48H-

7704, ascertained that the legal description on the Grant Deed is consistent

with the APN for this parcel.

HEARING OFFICER DECISION Page 8

Claimant established its right to 50°/o of the excess proceeds. Even

though Mr. Holsclaw's Claim is denied, only 50°/o of the excess proceeds can

be awarded to Claimant. A claimant is entitled to only the share of the

excess proceeds corresponding to the claimant's ownership interest

(assuming no claims of a higher priority), even when the other owner fails to

file a claim for the excess proceeds. First Corporation, Inc. v. County of

Santa Clara (1983) 146 CA3d 841.

For these reasons, one-half of the excess proceeds are awarded to

Global Discoveries, Ltd.

Dated: December 13, 2016

HEARING OFFICER DECISION

~-,-f ____ __

Jed Somit, Attorney at Law Legal Hearing Officer

Page9

CLAIMANTS:

PARCEL:

DECISION OF LEGAL HEARING OFFICER COUNTY OF ALAMEDA

DENNIS HOLSCLAW, JR., GLOBAL DISCOVERIES, LTD by assignment from MARTHA HUTSON SAXTON ASH-7704-122

FILE NOS: HEARING DATE:

EXCESS PROCEEDS 2014-94034, 2014-94058 NOVEMBER 3, 2016

AGENDA NUMBERS: THIRTY-TWO, THIRTY-THREE HEARING OFFICER: JED SOMIT, Esq.

FACTS

Almost $20,000 is at issue for the two claimants for the excess

proceeds generated by the March, 2014, tax default auction sale of this

parcel.

Claims

A. Dennis Holsclaw, Jr. 2014-94058. Mr. Holsclaw filed a Claim for

Excess Proceeds on April 22, 2015, Mr. Holsclaw claims all of the proceeds as

an owner. No grant documents supported the Claim, although he is listed as

one of the last assessees prior to the tax default sale. (Documents

submitted on behalf of the other Claim will be considered for this Claimant,

however.)

B. Global Discoveries, Ltd. 2014-94034. By Claim for Excess Proceeds

filed March 10, 2015, Global Discoveries claims $10,439.50 (apparently an

estimate of 50°/o of the excess proceeds). Apart from the assignment

HEARING OFFICER DECISION Page 1

papers, which will be reviewed later, the Claim is substantively supported

by:

• Grant Deed recorded in 1966 of certain property, without an APN, with

grantees Douglas Holsclaw, Jr., and Martha Holsclaw, his wife, as joint

tenants.

• Interlocutory Judgment of Dissolution of Marriage in In re Marriage of

Holsclaw, Alameda County Superior Court, recorded in 1974, which

confirms ownership of this property as 50% in each former spouse.

• Final Judgment of Dissolution of Marriage recorded in 1974,

incorporating the Interlocutory Judgment, also awarding 50°/o of

several lots to Martha Holsclaw.

County Counsel Memorandum

Farand C. Kan, Deputy County Counsel, and Paige N. Pembrook,

Graduate Law Clerk, provided a Memorandum for the Office of the County

Counsel dated September 22, 2016, reviewing the Claims for Excess

Proceeds and supporting documentation.

The Memorandum concludes the Holsclaw Claim was not filed timely,

as the tax deed to the purchaser was recorded on April 21, 2014. The

Memorandum therefore recommends denial of the Holsclaw Claim. Other,

substantive, problems with this Claim are also discussed.

The Memorandum concludes that the Global Discoveries Claim is

adequately supported, and was filed timely. It finds the assignment to

HEARING OFFICER DECISION Page 2

Global Discoveries met the statutory requirements. The underling deed

must be established to be for the same parcel.

Hearing November 3, 2016

At the hearing on November 3, 2016, Jed Byerly appeared for Claimant

Global Discoveries, Ltd. Douglas Holsclaw appeared by telephone (he lives

in Pennsylvania). He stated he was 82 years old. He testified that he was

contacted by many people seeking to assist with his claim, and (mis-)

informed by them that he could not file a Claim for Excess Proceeds prior to

a year from the recordation of the tax deed. He did not suggest that any

employee of the County told him that. He testified that with that

understanding, he tried to make sure his Claim was the first received and

tried to file early on the day following one year. He mailed his Claim for this

parcel and three others together, though the US Postal Service. He started

to read from his receipt. He was given permission to file a copy of his

mailing receipt and any other papers concerning his mailing of the Claim.

Mr. Holsclaw stated he had no objections to wife's Claim.

The matter was submitted, except for the leave given Claimant

Holsclaw to provide copies of his mailing receipt, etc.

His mailing receipt was received. It shows a mailing in Pennsylvania

on April 22, 2015, at 11: 58 a.m. It evidences delivery to the Clerk of the

Board in Oakland on April 23, 2015.

DECISION

HEARING OFFICER DECISION Page3

Douglas Holsclaw's Claim for Excess Proceeds was not filed timely, and

is denied.

The Claim for Excess Proceeds of Global Discoveries, Ltd., on

assignment from Martha Hutson Saxton, is granted as to 50°/o of the excess

proceeds, or $9,983.14. The check should be made payable to "Global

Discoveries, Ltd."

RATIONALE

Douglas Holsclaw Claim

Revenue & Taxation Code §4675(a) provides that any party of interest

in the property may file with the county a claim for the excess proceeds, in

proportion to his or her interest held with others of equal priority in the

property at the time of sale, "at any time prior to the expiration of one year

following the recordation of the tax collector's deed to the purchaser."

This is exactly our problem. The recordation of the tax deed resulting

from the tax default auction sale occurred on April 21, 2014. The Claim for

Excess Proceeds was received on April 23, 2015, although stamped "April

22, 2015", possibly because it was received prior to the start of business on

April 23rd.

In normal parlance, "prior to the expiration of one year" would mean

the Claim had to be filed before April 21, 2015. However, most California

government agencies follow the time computation approach stated in Civil

Code section 10:

HEARING OFFICER DECISION Page4

The time in which any act provided by law is to be done is computed by excluding the first day and including the last, unless the last day is a holiday, and then it is also excluded.

Applying this makes the "one year" end on April 21, 2015, unless extended.

April 21, 2015 was a weekday (Tuesday), and, although there were several

holidays, including Easter, in April, 2015, April 21st was not a holiday.

Therefore, April 21st was the last day on which a Claim for Excess Proceeds

for this parcel could be filed timely. Here, the Claim was received either on

April 22nd or April 23rd.

However, the date of receipt by the County is not always the date of

filing. Revenue & Taxation Code section 166 provides:

(a) Whenever a taxpayer is required to file any statement, affidavit, application, or any other paper or document with a taxing agency by a specified time on a specified date, such filing shall be deemed to be within the specified period if it is sent by United States mail, properly addressed with postage prepaid, and bears a post office cancellation mark of the specified date, or earlier within the specified period, stamped on the envelope, or on itself, or if proof satisfactory to the agency establishes that the mailing occurred on the specified date, or earlier within the specified period. (b) The provisions of this section shall supersede any contrary special provision of this division unless such special provision specifically provides that this section shall not be applicable. ( c) The provisions of this section are applicable to any filing required to be made by ordinance, rule, or regulation of a taxing agency. (d) Any statement or affidavit made by a taxpayer asserting such a timely filing must be made within one year of the deadline applicable to the original filing; provided, however, that this subsection shall not apply to any statement or affidavit asserting the timely filing of a property statement or to any statement made by the taxpayer in connection with an escape assessment imposed pursuant to Section 531. ( e) It is the intent of the Legislature that this section be liberally

HEARING OFFICER DECISION Page 5

construed in favor of the taxpayer and be applicable to all filings relating to property taxation which are required to be made by a taxpayer by a specified time on a specified date.

Unfortunately, the mailing receipt does not save Claimant, even under

a liberal construction. It shows a mailing on April 22nd, at 11:58 a.m. Even

taking into account the different time zones, it is clear the mailing occurred

on April 22nd, whether the date is determined in Oakland or in Pennsylvania.

The Hearing Officer cannot conclude, simply to validate this Claim, that the

mailing receipt incorrectly stated a date a day later than the actual mailing

and delivery in Oakland; there is insufficient evidence on which to assume

two separate mistakes were made.

The next issue is whether the Hearing Officer can overlook one day of

lateness, given Claimant's misinformation about when to file. No source for

such discretion can be found. The statute is unambiguous concerning the

filing period, and suggests that unclaimed excess proceeds could be

immediately distributed to the public entities on expiration of the one year.

No general discretion to relieve taxpayers from error is given.

In fact, case law holds that Revenue & Taxation Code time filing

requirements are given preclusive effect, even when a taxpayer loses an

otherwise viable claim as a result. Sea World, Inc. v. County of San Diego

(1994) 27 Cal.App.4th 1390.

For these reasons, without reaching the merits of the Claim, Douglas

Holsclaw's Claim must be denied.

HEARING OFFICER DECISION Page 6

Global Discoveries-Martha Hutson Saxton Claim

This Claim was timely filed.

Section 4675(b) continues: "After the property has been sold, a party

of interest in the property at the time of the sale may assign his or her right

to claim the excess proceeds only by a dated, written instrument that

explicitly states that the right to claim the excess proceeds is being assigned,

and only after each party to the proposed assignment has disclosed to each

other party to the proposed assignment all facts of which he or she is aware

relating to the value of the right that is being assigned. Any attempted

assignment that does not comply with these requirements shall have no

effect .... " The Hearing Officer has reviewed Global Discoveries' assignment

papers; they satisfy the statutory requirements. Indicating only 50°/o of the

total excess proceeds are available for this Claim adds some support to the

rote declaration that all facts relating to the value of the Claim were mutually

disclosed.

Section 4675(c) adds further requirements for assignment: "Any

person or entity who in any way acts on behalf of, or in place of, any party of

interest with respect to filing a claim for any excess proceeds shall submit

proof with the claim that the amount of excess proceeds has been disclosed

to the party of interest and that the party of interest has been advised of his

or her right to file a claim for the excess proceeds on his or her own behalf

directly with the county at no cost." The Global Discoveries papers indicate

HEARING OFFICER DECISION Page 7

an estimate of the excess proceeds for this Claim and contain the required

advisements.

claim:

Section 4675(e)(1) defines the parties of interest who may make a

[T]he excess proceeds shall be distributed on order of the board of supervisors to the parties of interest who have claimed the excess proceeds in the order of priority set forth in subdivisions (a) and (b). For the purposes of this article, parties of interest and their order of priority are:

(A) First, lienholders of record prior to the recordation of the tax deed to the purchaser in the order of their priority.

(B) Second, any person with title of record to all or any portion of the property prior to the recordation of the tax deed to the purchaser.

The Global Discoveries Claim is of the second priority. There were no

claims of the first priority.

There is adequate evidence to find that Global Discoveries' assignor

was a person with title of record to 50% of the fee interest prior to the tax

auction sale. Claimant supplied a recorded Grant Deed by which Martha and

Douglas Holsclaw acquired certain property jointly, as well as the Judgment

of Dissolution of Marriage confirming the assignor's continued ownership of a

50°/o interest in several lots. Claimant showed that "Martha Holsclaw" on the

Grant Deed is the same person as "Martha Saxton", Global's assignor.

The Hearing Officer, using the Assessor's online maps for Map 48H-

7704, ascertained that the legal description on the Grant Deed is consistent

with the APN for this parcel.

HEARING OFFICER DECISION Page 8

Claimant established its right to 50% of the excess proceeds. Even

though Mr. Holsclaw's Claim is denied, only 50% of the excess proceeds can

be awarded to Claimant. A claimant is entitled to only the share of the

excess proceeds corresponding to the claimant's ownership interest

(assuming no claims of a higher priority), even when the other owner fails to

file a claim for the excess proceeds. First Corporation, Inc. v. County of

Santa Clara (1983) 146 CA3d 841.

For these reasons, one-half of the excess proceeds are awarded to

Global Discoveries, Ltd.

Dated: December 30, 2016

HEARING OFFICER DECISION

Jed Somit, Attorney at Law Legal Hearing Officer

Page 9

DECISION OF LEGAL HEARING OFFICER COUNTY OF ALAMEDA

CLAIMANTS:

PARCEL: FILE NOS:

HEARING DATE: AGENDA NUMBERS:

HEARING OFFICER:

FACTS

GLOBAL DISCOVERIES, LTD., as assignee of FRANCIS TOM; GLOBAL DISCOVERIES, LTD., as assignee of KEITH WILSON; FOUND EXTRA MONEY, LLC as assignee of KEITH WILSON; KEITH WILSON 48G-7449-34 EXCESS PROCEEDS MARCH 2014; 2014-94010, 2014-94017, 2014-94021(A), (B) NOVEMBER 3, 2016 THIRTY-FOUR, THIRTY-FIVE, THIRTY-SIX THIRTY-SEVEN JED SOMIT, Esq.

Several Claims for Excess Proceeds were filed after the March, 2014,

auction sale of this tax defaulted parcel.

Claims

A. Global Discoveries: Francis Tom. 2014-94010. This Claim, filed

June 24, 2014, is on an assignment dated April 26, 2014, from Francis Tom,

subsequent beneficiary of a Deed of Trust recorded as a lien on the parcel in

1987, in which the truster is Keith R. Wilson. The recited principal amount of

the secured obligation is $40,000 as of May 6, 1987. The assignment of

interest to Francis Tom was recorded next in sequence after the Deed of

Trust. The Promissory Note reveals the obligation as a loan due in full on

January 1, 1988, supposedly with 14°/o interest payable "monthly", and a

HEARING OFFICER DECISION Page 1

late charge of 6°/o. A Substitution of Trustee recorded in 1988 suggests a

default at that time. A Statement of Amount Due and Owing avers that no

payments were made, and the amount due with interest as of March 14,

2014, is $190,391.11 (no amount included for late payments).

The assignment to Global Discoveries is 100°/o of the assignor's claim.

B. Global Discoveries: Keith Wilson. 2014-94010. This Claim for all

of the excess proceeds was filed August 18, 2014, based upon a 100°/o

assignment from Keith Wilson dated June 26, 2014. There is no mention of

the existence or possible effect of the Deed of Trust, beyond the rote

recitation that there was a mutual disclosure of all facts concerning the value

of the rights assigned.

Substantively, the Claim is supported by a Grant Deed of the parcel

recorded in 1987 to grantee "Keith R. Wilson".

C. Keith Wilson. 2014-94021(A). By a Claim for Excess Proceeds

dated October 11, 2014, filed October 20, 2014, prepared by Found Extra

Money, Keith Wilson claims 75°/o of the excess proceeds, assigning (by

documents dated October 11, 2014) 25°/o to Found Extra Money.

Substantively, the Claim is supported by a Grant Deed of the parcel

recorded in 1987 to grantee "Keith R. Wilson".

D. Found Extra Money. 2014-94021(B). This is a Claim for the 25°/o

assigned by Keith Wilson to FEM in October, 2014, supported by the same

documentation as the Claim described in "C". There is no mention, beyond

HEARING OFFICER DECISION Page2

the rote, of a disclosure of the existence and/or possible effect of the Deed

of Trust.

County Counsel Memorandum

The various Claims and supporting documentation were reviewed in a

Memorandum for the Office of the County Counsel dated September 27,

2016, by Farand C. Kan, Deputy County Counsel, and Paige N. Pembrook,

Graduate Law Clerk. The Memorandum reveals that $50,744.89 is available

for distribution.

On the Global-Tom Claim, the Memorandum notes that 14°/o interest is

usurious, unless an exception to the 10°/o limit of California Constitution

Article XV §1 is established.

On the Global-Wilson Claim and the Keith Wilson/Fem Claims, the

Memorandum points out that the two Keith Wilsons - of the Global

assignment and the FEM Claims - are two different individuals, and the

proper one must be identified.

The Memorandum conditionally recommends granting the Global-Tom

Claim for $40,000, and then settling the Keith Wilson identity issue to

determine who receives the remainder of the excess proceeds.

Brief Submitted by Global Discoveries

A brief dated October 27, 2016, was submitted by C. Daniel Carroll,

Esq., of Mccann & Carroll, on behalf of Global Discoveries.

The brief contends first that interest should be allowed on the usurious

HEARING OFFICER DECISION Page3

promissory note. The brief does not dispute that pre-maturity interest is lost

due to usury. However, it contends that once the maturity date of a

usurious obligation is reached, "a debtor who wrongfully withholds payment

is obligated to pay pre-judgment interest at the legal rate from the date of

maturity until the date of judgment." Green v. Future Two (1986) 179 CA3d

738, 744, and Epstein v. Frank (1981) 125 CA3d 111, 123 are cited.

Epstein says that "[b]y analogy, therefore, the payee of a note with a

usurious interest provision would be entitled to damages in the nature of

interest at the legal rate for that period of time which the obliger on the note

withheld the principal beyond the date of maturity." Denial of interest

through maturity "is a sufficient deterrent" to usury. Green notes that a

usurious note is treated as having no interest; a "non-interest bearing note

is entitled to interest at the legal rate from the date of maturity to the date

of judgment." (179 CA3rd at 744). Since the obligation is not a judgment

and does not specify an interest rate, "the constitutional rate of 7 percent

per annum applies." (Id.)

The brief's second subject is that there are two Keith R. Wilson

assignors. The brief argues that the issue is moot since the award on the

Tom assigned claim, with 7°/o interest, will exhaust the excess proceeds.

Reaching the moot issue, the brief asserts that the signature of Global's

assignor is more similar to the signatures on the original Note and Deed of

Trust, an assertion the Hearing Officer finds questionable. It further asserts

HEARING OFFICER DECISION Page4

that the California Drivers' License of Global's assignor-Wilson matches the

CDR of the Keith R. Wilson identified in an Abstract of Judgment recorded as

a lien against the property as document No. 2008-291665.

Since the Abstract was not provided, the Hearing Officer could not

ascertain whether it was a non-form, singular Abstract - one that attached

to the particular parcel - rather than the Judicial Council form, which creates

a lien against all real property within the county held in the judgment

debtor's name. A Judicial Council's Abstract of Judgment's having a

concurring CDR to a claimant provides no evidence of identity of the owner

of a particular parcel, only of the judgment debtor.

Hearing on November 3, 2016

Jed Byerly appeared for Global Discoveries, Ltd., and for its assignors

Francis Tom and one Keith Wilson. There were no appearances for Found

Extra Money, LLC, or for its assignor and separate Claimant the other Keith

Wilson.

Farand Kan, Deputy County Counsel, also participated in the hearing.

Mr. Byerly stated he had the original Promissory Note with him; the

Hearing Officer declined to take the original as an exhibit.

Mr. Byerly was unaware of whether the Abstract of Judgment referred

to in Mr. Carroll's brief was in an unusual form; he agreed that normally an

Abstract of Judgment does not attach to a particular property, and that

consequently a matching of driver's license number would not assist in

HEARING OFFICER DECISION Pages

determining which "Keith Wilson" was the former owner of the parcel.

The matter was submitted.

DECISION

The Claim for Excess Proceeds of Global Discoveries, Ltd., on

assignment from Francis Tom, is granted as to all of the $50,744.89 excess

proceeds. The check should be payable to "Global Discoveries, Ltd."

The Claim for Excess Proceeds of Global Discoveries, Ltd., on

assignment from Keith Wilson, is denied.

The Claim for Excess Proceeds of Keith Wilson is denied.

The Claim for Excess Proceeds of Found Extra Money, LLC., on

assignment from Keith Wilson, is denied.

RATIONALE

Procedural Issues

Revenue & Taxation Code §4674 directs that excess proceeds may be

claimed by parties of interest in the property as provided in Section 4675.

Unclaimed excess proceeds may be transferred to the county general fund.

Revenue & Taxation Code §4675(a) provides that any party of interest

in the property may file with the county a claim for the excess proceeds, in

proportion to his or her interest held with others of equal priority in the

property at the time of sale, at any time prior to the expiration of one year

following the recordation of the tax collector's deed to the purchaser. All of

HEARING OFFICER DECISION Page6

the Claims for Excess Proceeds were submitted within that period.

Section 4675(b) continues: "After the property has been sold, a party

of interest in the property at the time of the sale may assign his or her right

to claim the excess proceeds only by a dated, written instrument that

explicitly states that the right to claim the excess proceeds is being assigned,

and only after each party to the proposed assignment has disclosed to each

other party to the proposed assignment all facts of which he or she is aware

relating to the value of the right that is being assigned. Any attempted

assignment that does not comply with these requirements shall have no

effect .... "

The Hearing Officer has reviewed the assignment from Francis Tom to

Global Discoveries, Ltd. It is a dated, written instrument that explicitly

states that the right to claim the excess proceeds is being assigned. It

contains a rote declaration that each party has disclosed to each other party

all facts each is aware of regarding the value of the rights being assigned.

This statement will be deemed sufficient in this matter; that conclusion,

however is based significantly on the ultimate outcome here of an award of

the entire excess proceeds on this Claim.

Were the analysis to be on the other Global Claim for Excess Proceeds,

for example, the decision might be to reject the assignment. There is no

showing that (disregarding the identity issue) Keith Wilson or Global

Discoveries disclosed the existence of the Frankfurt Deed of Trust, and its

HEARING OFFICER DECISION Page?

possible effect on a second priority claim. A rote recitation of compliance will

not always suffice.

Section 4675(c) adds further requirements for assignment: "Any ·

person or entity who in any way acts on behalf of, or in place of, any party of

interest with respect to filing a claim for any excess proceeds shall submit

proof with the claim that the amount of excess proceeds has been disclosed

to the party of interest and that the party of interest has been advised of his

or her right to file a claim for the excess proceeds on his or her own behalf

directly with the county at no cost." This is accomplished in Global's

Assignment of Rights for the Tom assignment.

In light of the eventual result, no analysis will be made of the Found

Extra Money assignment.

Substantive Issues

claim:

Section 4675(e)(l) defines the parties of interest who may make a

[T]he excess proceeds shall be distributed on order of the board of supervisors to the parties of interest who have claimed the excess proceeds in the order of priority set forth in subdivisions (a) and (b). For the purposes of this article, parties of interest and their order of priority are:

(A) First, lienholders of record prior to the recordation of the tax deed to the purchaser in the order of their priority.

(B) Second, any person with title of record to all or any portion of the property prior to the recordation of the tax deed to the purchaser.

HEARING OFFICER DECISION Page8

Global Discoveries' Claim on assignment from Francis Tom is of the

first priority; all other Claims are of the second priority. The first priority

Claim should be analyzed first.

Adequate proof that Global's assignor was a lienholder of record prior

to the recordation of the tax deed to the purchaser was presented through

the combination of: the Grant Deed to Keith R. Wilson, recorded May 8,

1987; the Deed of Trust recorded July 8, 1987, with truster Keith R. Wilson

and beneficiary Robert L. Frankfurt; and, the Assignment of Deed of Trust

recorded the same date, next in sequence, assigning the Deed of Trust to

Global's assignor, Francis Tom. That the obligation was also assigned is

adequately established by Mr. Byerly's possession of the original Promissory

Note.

Although the age of the Deed of Trust might suggest a problem of an

ancient mortgage, the Marketable Record Title Act (MRTA, Civil Code section

882.02 et seq.) requires that the maturity date of the underlying obligation

be contained in the recorded lien for the ten years after maturity invalidation

to apply. The Hearing Officer has reviewed the Deed of Trust and

Assignment, and finds no maturity date other than the "due on sale" notice

in the Assignment. Therefore, a sixty-year period after recordation of the

Deed of Trust applies, and the tax auction sale date was comfortably within

that period.

On the usury/interest issue, the Hearing Officer has reviewed the

HEARING OFFICER DECISION Page9

cases cited in Daniel Carroll's brief and determined that they represent

current California law. Interest at 7°10 is appropriate after maturity.

The Promissory Note has a principal obligation of $40,000; no

payments were made thereon, according to the Statement of Amount Due

and Owing. The maturity date was January 1, 1988. At 7°10 simple interest,

the amount of interest exceeds $11,000 within four years. No detailed

accounting is necessary to establish that all of the excess proceeds will be

exhausted well before interest to the date of sale is computed.

All of the excess proceeds are to be distributed to Global Discoveries

on the Tom assignment. The other Claims, of the second priority, must be

denied for lack of excess proceeds to distribute after that award, without

reaching the merits of the other Claims.

Dated: December 13, 2016

HEARING OFFICER DECISION

::::r~c:_~~~~~~---Jed Samit, Attorney at Law Legal Hearing Officer

Page 10

DECISION OF LEGAL HEARING OFFICER _ COUNTY OF ALAMEDA

CLAIMANTS:

PARCEL: FILE NOS:

HEARING DATE:

AGENDA NUMBERS: HEARING OFFICER:

FACTS

Claims

ANNE FLEXER, FOUND EXTRA MONEY, LLC, by assignment from Anne Flexer, HARRY BERNSTEIN 48G-7449-27 2014-94005; 2014-94020; 2014-94035 EXCESS PROCEEDS SALE OF MARCH, 2014 NOVEMBER 3, 2016, after submission on JULY 21, 2016, and subsequent request for hearing by ANNE FLEXER TWENTY-ONE, TWENTY-TWO, TWENTY-THREE JED SOMIT, Esq.